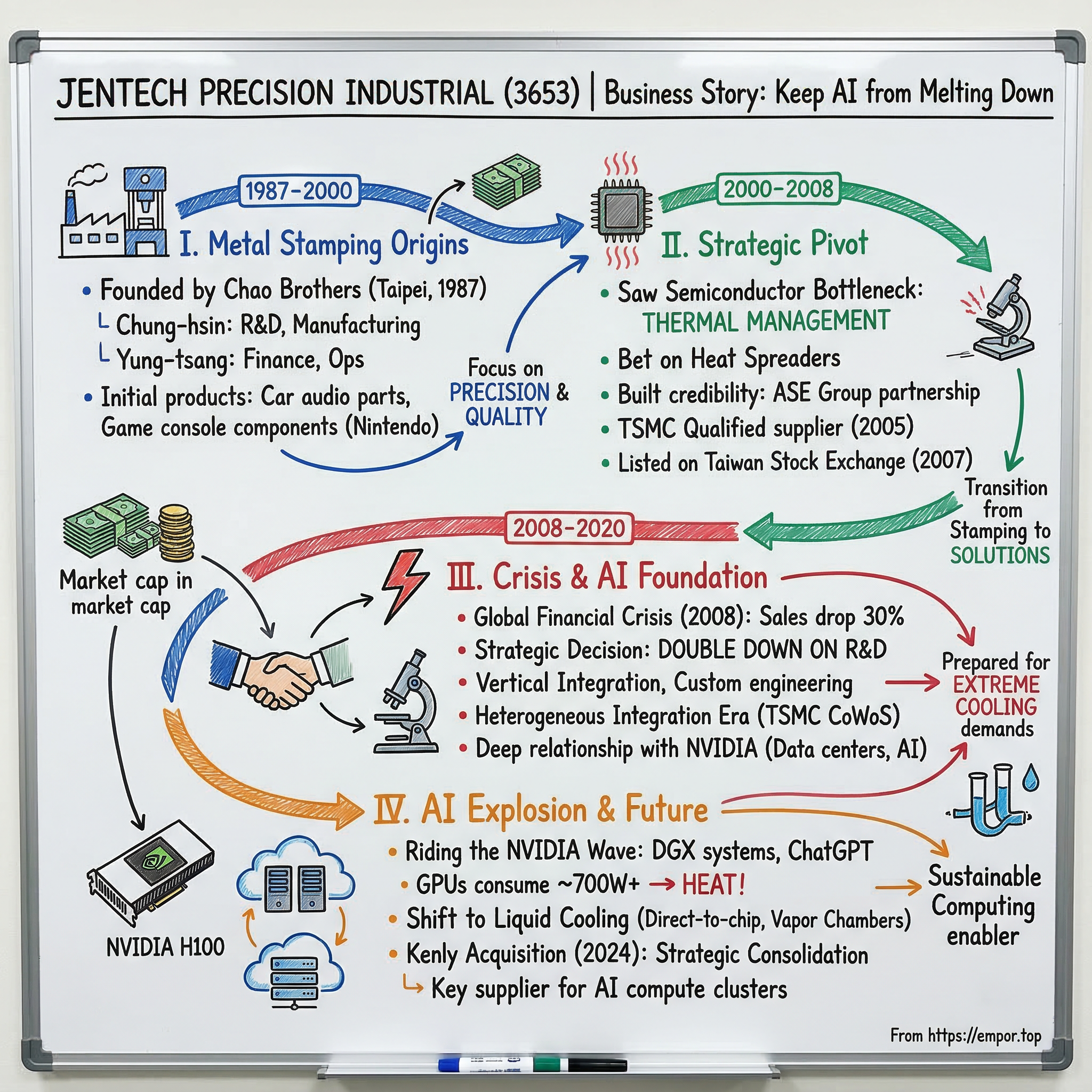

Jentech Precision Industrial: From Metal Stamping to AI's Cooling Backbone

I. Cold Open & Episode Thesis

Picture a server farm in Santa Clara, California, where rows of NVIDIA H100 GPUs hum at frequencies that would have seemed impossible just five years ago. Each chip pulls nearly 700 watts of power, generating heat that could literally cook an egg. Behind each of these computing monsters sits an unassuming copper plate—a thermal heat spreader that stands between technological breakthrough and catastrophic meltdown. The company making many of these critical components? Not Intel, not TSMC, but a Taiwanese firm most investors have never heard of: Jentech Precision Industrial.

Founded in 1987 and headquartered in Taoyuan, Taiwan, Jentech embodies one of the most fascinating paradoxes of the AI revolution: our most sophisticated technologies depend entirely on mastering basic physics. As chips grow more powerful, they generate exponential heat. Without proper thermal management, Moore's Law doesn't just slow—it stops entirely. The founding Chao brothers, Chung-hsin and Yung-tsang, have built their combined $2.1 billion fortune on this fundamental truth.

Today, with a market cap of NT$319.43 billion—roughly $10 billion USD—Jentech has emerged from decades of obscurity to become indispensable to the semiconductor supply chain. The company employs just 655 people, yet their products touch nearly every major AI computing cluster on the planet. How did two brothers with factory floor experience transform a small metal stamping operation into one of the most critical suppliers to the AI infrastructure boom?

The answer lies not in revolutionary technology breakthroughs or venture capital moonshots, but in something far more mundane yet profound: the patient accumulation of manufacturing expertise, perfectly timed strategic pivots, and an almost obsessive focus on solving problems others considered too boring to pursue. This is the story of how Jentech became the company that keeps AI from melting down—literally.

II. Brothers from the Factory Floor: Origins & Early Days (1987-2000)

The rain-slicked streets of industrial Taipei in the late 1970s bore little resemblance to today's gleaming tech hub. Chao Chung-hsin, the elder of two brothers who would reshape Taiwan's precision manufacturing landscape, spent his days in the grime and heat of metal molding factories. Without a high school diploma, Chung-hsin possessed something more valuable: an intuitive understanding of how metal behaves under pressure, how tolerances stack up in complex assemblies, and most importantly, how to make things that don't break.

By 1978, after years of absorbing every detail of industrial molding processes, Chung-hsin struck out on his own, establishing a small workshop producing metal parts for car audio systems. The margins were thin, the competition fierce, but he had identified a crucial niche: Japanese electronics manufacturers needed suppliers who could match their exacting quality standards at Taiwanese prices. For nine years, he built relationships, refined processes, and most critically, established a reputation for reliability that transcended language barriers.

In March 1987, Jentech Precision Industry Co., Ltd. was established with a paid-up capital of NT$5,000,000—roughly $150,000 USD at the time. Yung-tsang, the younger brother, brought complementary skills to the partnership. While Chung-hsin obsessed over dies and tolerances in the workshop, Yung-tsang managed the books, negotiated with suppliers, and navigated Taiwan's complex web of industrial regulations. Chung-hsin oversaw research and development, while Yung-tsang focused on finance and operations—a division of labor that would remain unchanged for nearly four decades.

The company engaged in the operation of simple punch press machining, but from the beginning, the brothers recognized that Taiwan's electronics industry was evolving at breakneck speed. Their first major breakthrough came from an unexpected source: video game consoles. Nintendo's explosive growth in the late 1980s created voracious demand for precision metal components—cartridge connectors, RF shields, chassis parts. Unlike car audio, where cost was paramount, game console manufacturers prioritized consistency. A single faulty connection could brick an entire unit.

The learning curve was brutal. Japanese quality inspectors would reject entire batches for deviations measured in hundredths of millimeters. But each rejection taught the brothers something new about precision, about process control, about the difference between making parts and manufacturing excellence. They invested their profits not in expansion but in better equipment—Swiss-made punch presses, Japanese measurement tools, German cutting fluids. While competitors chased volume, Jentech chased precision.

By the mid-1990s, Taiwan's economic miracle was in full swing. The island had transformed from an agricultural backwater to the world's workshop for electronics. Personal computers, manufactured by companies like Acer and later contract manufacturers like Quanta, required thousands of tiny metal components—EMI shields, heat sinks, connector housings. Jentech rode this wave, but the brothers sensed something shifting. The components were getting smaller, the tolerances tighter, and increasingly, heat was becoming the enemy.

From the beginning of its establishment, it recognized the rapidly changing industrial environment and the constant innovation in electronic products. This prescient observation would guide their next crucial decision. As the 1990s drew to a close, semiconductors were replacing discrete components, clock speeds were doubling every eighteen months, and thermal management was emerging from an afterthought to a critical design constraint.

The transition wasn't immediate. Jentech continued stamping game console parts and PC components, but Chung-hsin began attending semiconductor packaging conferences, studying thermal dynamics papers, experimenting with different copper alloys and surface treatments. He understood intuitively what Silicon Valley's engineers were just beginning to articulate: as chips shrank and speeds increased, heat density would become the fundamental limiting factor in computing. The company that solved thermal management wouldn't just be supplying parts—they'd be enabling the future of technology itself.

III. The Semiconductor Opportunity: Strategic Pivot (2000-2008)

The new millennium brought both promise and peril to Taiwan's electronics industry. The dot-com bubble's collapse sent shockwaves through the supply chain, but for the Chao brothers, crisis meant opportunity. While competitors retrenched, Jentech began developing thermal heat spreaders in the early 2000s, betting that semiconductor heat dissipation would become the industry's next bottleneck.

The timing seemed almost foolish. AMD's Athlon processors were running hot enough to earn the nickname "space heaters," while Intel's Pentium 4 NetBurst architecture pushed thermal design power (TDP) past 100 watts for the first time. Yet most packaging houses still treated cooling as an afterthought—slap on a heat sink, add a fan, problem solved. Chung-hsin saw it differently. He understood that heat spreaders weren't just metal plates; they were precision-engineered thermal interfaces that could make or break a chip's performance.

Building credibility in the semiconductor supply chain required more than technical competence—it demanded a fundamental transformation of Jentech's operations. The company implemented clean room protocols, even for initial stamping operations. Workers traded their shop aprons for bunny suits. Statistical process control replaced visual inspection. Every heat spreader was tracked from raw material through final testing. These changes cost millions of Taiwan dollars, funded entirely from retained earnings, as the brothers refused to dilute their ownership.

The real breakthrough came through an unlikely partnership with ASE Group, Taiwan's largest semiconductor assembly and test services provider. ASE faced a crisis: their flip-chip ball grid array (FCBGA) packages for graphics processors were experiencing catastrophic thermal failures during stress testing. Traditional heat spreaders couldn't maintain flatness under extreme thermal cycling. Jentech's solution was elegantly simple—a proprietary surface treatment that created micro-channels for improved thermal interface material flow, combined with a precisely controlled nickel plating process that prevented warpage.

In 2002, Wuxi Jentech Precision Industrial Co., Ltd. was established with a paid-up capital of USD 2,500,000, engaged in manufacturing metal stamping components, specializing in battery safety parts, LCD TV reflector plates, precision stamping dies, progressive dies, and precision mold processing, with a land-use right of 7,749.6 square meters and a three-story building with total floor area of 4,036.92 square meters. This Chinese subsidiary wasn't about chasing cheap labor—it was about being physically present where their customers were expanding.

Competition from established Japanese suppliers like Shinko Electric Industries was fierce. These companies had decades-long relationships with major chip manufacturers, advanced materials science capabilities, and balance sheets that dwarfed Jentech's. But the brothers identified a critical weakness: Japanese suppliers were optimized for high-volume, standardized products. As semiconductor packaging grew more diverse—system-in-package, package-on-package, chip-scale packaging—flexibility became paramount.

Jentech's approach was almost artisanal. They would take on small-batch orders that Japanese suppliers deemed uneconomical. They'd work with packaging engineers to develop custom heat spreader designs for specialized applications. When a customer needed nickel-gold plating instead of standard nickel for better wire bonding, Jentech would reconfigure their entire plating line. This flexibility came at a cost—lower margins, longer hours, constant retooling—but it built something invaluable: deep technical partnerships with Taiwan's emerging semiconductor giants.

The real validation came in 2005 when TSMC, the world's largest contract chip manufacturer, qualified Jentech as a thermal solution supplier. The qualification process took eighteen months, involving hundreds of reliability tests, multiple facility audits, and demonstration of supply chain resilience. But once approved, Jentech gained access to roadmaps showing where semiconductor technology was heading: smaller geometries, higher transistor density, and exponentially increasing heat flux.

By 2007, the company's transformation was complete. In November, the company was officially listed on the Taiwan Stock Exchange, a milestone that provided both credibility and capital for expansion. Revenue from semiconductor thermal solutions had overtaken traditional metal stamping. The company's heat spreaders were designed into products from AMD, NVIDIA, and Broadcom. But storm clouds were gathering. The U.S. housing market was beginning to crack, credit markets were freezing, and the greatest financial crisis since the Great Depression was about to test every assumption about global supply chains.

IV. The 2008 Crisis: Catalyst for Transformation

September 15, 2008. Lehman Brothers collapsed, sending shockwaves through the global financial system. The global financial crisis caused by the U.S. sub-prime mortgage event brought the global financial system to the brink of disaster, and the semiconductor industry was inevitably hit, with survival and development strictly challenged. Within weeks, semiconductor orders evaporated. ASE's factory utilization plummeted from 95% to below 40%. TSMC announced its first-ever layoffs. For Jentech, revenue dropped 30% in a single quarter.

The crisis hit Taiwan's semiconductor industry with particular ferocity. Downstream, the Interbank funds crisis meant businesses cut IT investments and consumers held off buying PCs. PC OEMs reacted by cutting DRAM orders and pushing inventory into the market. Both OEMs and DRAM makers wanted to convert inventories into cash, like a run on the stock market, with demand and supply shifts amplifying each other to drive prices down at a 32% quarterly rate.

Inside Jentech's Taoyuan headquarters, the brothers faced an existential choice. Conventional wisdom demanded immediate cost-cutting: slash R&D, reduce headcount, preserve cash. Nearly every competitor chose this path. But Chung-hsin saw something others missed. He had been studying Intel's tick-tock development model, AMD's planned transition to 32nm processes, and most intriguingly, NVIDIA's CUDA platform that was transforming graphics processors into general-purpose computing engines. The crisis wouldn't last forever, but the companies that emerged strongest would be those that invested during the downturn.

The decision to double down on R&D during the worst financial crisis in decades seemed almost irrational. While the 2008 economic crisis severely reduced firms' short-term willingness to invest in innovation, a small minority of firms were "swimming against the stream," with companies pursuing explorative strategies toward new product and market developments coping better with the crisis. Jentech fell squarely into this minority.

Instead of layoffs, the company implemented a radical program: engineers would spend half their time on current products and half on "moonshot" projects with no immediate commercial application. One team explored vapor chamber technology for extreme cooling. Another investigated composite materials that could match copper's thermal conductivity at half the weight. A third group, led by Chung-hsin himself, worked on something that seemed absurd at the time: liquid cooling interfaces for chips that didn't yet exist.

The financial gymnastics required to fund this expansion while revenue cratered were extraordinary. The brothers pledged personal assets as collateral for bank loans. They negotiated extended payment terms with suppliers, offering small equity stakes in lieu of immediate payment. Most critically, they convinced their largest customers—particularly TSMC—to provide advance payments for future orders, essentially betting on Jentech's survival.

The R&D investments began yielding unexpected dividends. The vapor chamber team's work led to a breakthrough in heat pipe manufacturing that reduced costs by 40%. The composite materials research, while failing its original goal, produced a new surface treatment that improved thermal interface material adhesion by 60%. But the real revolution came from understanding how chips were evolving.

During the global financial crisis, the performance of the semiconductor industry could benefit from government support, though improvement was somewhat delayed after intervention, and how government intervention influenced the dynamic change of performance depended on the economy. Taiwan's government, recognizing semiconductors as strategic assets, provided tax incentives for R&D spending and subsidized advanced manufacturing equipment purchases. Jentech leveraged every available program, effectively turning government support into a competitive advantage.

By late 2009, as the global economy began its tentative recovery, Jentech had emerged transformed. The company held 37 patents related to thermal management, up from just 3 in 2007. Their engineering team had doubled in size. Most importantly, they had developed prototypes for cooling solutions that could handle 300-watt thermal loads—power levels that seemed absurd for single chips but would become standard within a decade.

The crisis also catalyzed a crucial strategic shift: vertical integration. Rather than simply stamping heat spreaders, Jentech began offering complete thermal solutions—design consultation, prototyping, testing, and even failure analysis. This transformation from component supplier to thermal management partner would prove invaluable as the industry entered the age of heterogeneous integration, where multiple chips would be packaged together, multiplying thermal challenges exponentially.

V. The Heterogeneous Chip Era: Finding Product-Market Fit (2010-2020)

The smartphone revolution of the early 2010s initially seemed to bypass Jentech entirely. Apple's A-series processors and Qualcomm's Snapdragon chips prioritized power efficiency over raw performance. Their thermal requirements were modest—a far cry from the fire-breathing graphics cards and server processors that had become Jentech's specialty. Yet Chung-hsin recognized that mobile computing's emphasis on integration would eventually transform the entire semiconductor industry.

The inflection point arrived in 2011 when TSMC unveiled CoWoS (Chip-on-Wafer-on-Substrate), a 2.5D packaging technology that allowed multiple chips to be integrated on a silicon interposer. Suddenly, memory could sit millimeters from logic, connected by thousands of tiny copper pillars instead of lengthy PCB traces. Performance skyrocketed, but so did thermal density. A package that previously spread heat across 40 square centimeters now concentrated it into 10. Demand for cooling solutions was being driven by heterogeneous chips integration, exactly as Jentech had anticipated during the crisis years.

The technical challenges were staggering. Traditional heat spreaders assumed uniform heat distribution, but heterogeneous packages created intense hotspots—one corner might be 30 degrees Celsius hotter than another. Jentech's solution required rethinking heat spreader design from first principles. They developed variable-thickness spreaders, thicker over hotspots to increase thermal mass, thinner elsewhere to reduce weight. They experimented with embedded heat pipes that could transport heat laterally before spreading it vertically. Every design required custom engineering, transforming Jentech from a manufacturing company into an engineering consultancy that happened to make products.

The relationship with ASE Group deepened during this period, evolving from customer-supplier to strategic partnership. ASE's advanced packaging technologies—fan-out wafer level packaging, system-in-package, embedded die—each presented unique thermal challenges. Jentech engineers were embedded directly in ASE's development teams, designing thermal solutions in parallel with package development rather than as an afterthought. This early involvement meant thermal considerations shaped package architecture from the beginning, resulting in designs that were both higher-performing and more manufacturable.

The company's principal products expanded to include thermal heat spreaders, insert molding SMD LED and semiconductor lead frames and injection moldings, EV power module coolers, machining parts, motor core lamination and housing. This diversification wasn't random—each product line leveraged core competencies in precision metal forming and thermal management while opening new revenue streams. The EV power module coolers, in particular, positioned Jentech at the intersection of two megatrends: electrification and autonomous driving, both requiring unprecedented levels of electronic thermal management.

Geographic expansion accelerated, but with a twist. Rather than chasing low-cost manufacturing locations, Jentech established engineering centers near customer R&D facilities. A design office in Hsinchu put them minutes from TSMC's headquarters. An applications lab in Shanghai served China's booming semiconductor assembly industry. In Wuxi, capital was increased by USD 2,100,000, bringing total capital to USD 6,800,000, funding advanced manufacturing capabilities for the Chinese market.

The emergence of AI and machine learning workloads around 2015 validated Jentech's long-term bet on extreme cooling. Google's Tensor Processing Units, designed specifically for neural network operations, generated heat densities that would have been unthinkable in general-purpose processors. Training large language models required sustained operation at maximum power for days or weeks, putting unprecedented stress on thermal solutions. Jentech's experience with high-power graphics cards—earned through years of working with NVIDIA and AMD—proved invaluable.

By 2018, the company had achieved something remarkable: despite having less than 1,000 employees, they had become virtually irreplaceable in the high-performance semiconductor packaging supply chain. Their heat spreaders weren't just components—they were enabling technologies that allowed chip designers to push performance boundaries. When NVIDIA's Volta GPU architecture exceeded 300 watts of thermal design power, it was Jentech's vapor chamber heat spreaders that kept them from throttling.

The relationship with NVIDIA deserves special attention. As the graphics card maker pivoted toward AI and data center applications, their thermal requirements exploded. The DGX-1 system, NVIDIA's first AI supercomputer, contained eight Tesla P100 GPUs, each consuming 300 watts. In 2016, Jensen Huang hand-delivered the first NVIDIA DGX AI supercomputer to OpenAI—the engine behind the large language model breakthrough powering ChatGPT. While the world focused on NVIDIA's silicon and software, Jentech quietly engineered the thermal solutions that made such systems possible.

In April 2017, the company issued the first domestic unsecured convertible corporate bonds worth NT$800 million, using the proceeds to fund capacity expansion and next-generation R&D. The bond issue was oversubscribed by 3x, indicating investor confidence in Jentech's position at the nexus of several technology megatrends. As the decade drew to a close, artificial intelligence was transitioning from research curiosity to commercial reality, and Jentech was perfectly positioned for the explosion that was about to come.

VI. The AI Explosion: Riding the NVIDIA Wave (2020-2023)

March 2020. As COVID-19 forced the world into lockdown, digital transformation accelerated by a decade in mere months. Video conferencing replaced office meetings. Cloud computing became critical infrastructure. And quietly, in data centers from Virginia to Singapore, AI workloads exploded. NVIDIA's data center unit continued its rapid growth that started in Q2 of 2020, with revenues eventually surpassing gaming for the first time in the company's history.

The pandemic created a perfect storm for AI adoption. Businesses desperate for efficiency turned to automation. Researchers racing for vaccines leveraged machine learning for drug discovery. And then, in November 2022, everything changed. OpenAI's ChatGPT went mainstream almost instantaneously, attracting over 100 million users, making it the fastest-growing application in history. Suddenly, AI wasn't just for data scientists—it was for everyone.

Tech companies scrambling to compete with ChatGPT publicly boasted about how many of NVIDIA's roughly $10,000 A100s they had, with Microsoft's supercomputer developed for OpenAI using 10,000 of them. Each A100 GPU consumed up to 400 watts, but the real challenge wasn't individual chip cooling—it was density. AI training clusters packed GPUs together like never before, creating thermal environments that traditional cooling simply couldn't handle.

Heat spreaders had to be made bigger and thicker to support AI chips with larger surface area and higher performance, according to Jentech Precision Industrial president Chin-Lung Lin. This wasn't just incremental improvement—it required fundamental redesign. Traditional heat spreaders were optimized for uniform thickness and minimal weight. AI-optimized designs sacrificed both, using variable thickness profiles and exotic materials to manage previously unimaginable heat flux.

The numbers were staggering. A single NVIDIA DGX A100 system contained eight GPUs generating 6.5 kilowatts of heat—equivalent to four residential space heaters running full blast. Data centers installing hundreds of these systems faced cooling challenges that pushed conventional HVAC systems past their breaking point. The global data center cooling market exploded from $22.13 billion in 2024 toward a projected $56.15 billion by 2030, growing at 16.4% CAGR as the need for energy-efficient cooling solutions presented significant opportunities.

Jentech's response was multifaceted. First, they expanded their liquid cooling capabilities, developing direct-to-chip cooling solutions that could handle 500+ watt processors. The technology, prototyped during the 2008 crisis, suddenly found massive commercial application. Second, they invested heavily in advanced materials, particularly vapor chamber technology that could spread heat more efficiently than solid copper. Third, and most importantly, they embedded themselves deeper into the design process, working with NVIDIA, AMD, and Intel from the earliest stages of chip development.

The relationship dynamics were fascinating. While NVIDIA captured headlines and trillion-dollar valuations, they depended entirely on an ecosystem of suppliers like Jentech. The GPU architecture perfectly suited to neural networks' huge number of matrix multiplication tasks created unprecedented thermal challenges, with demand for NVIDIA GPUs exceeding supply and leading to high prices, while the H100 processors introduced in 2022 cost approximately $40,000 each. Every one of those H100s required thermal solutions that matched their sophistication.

The supply chain constraints of 2021-2022 tested Jentech's operational excellence. Copper prices doubled. Shipping costs quintupled. Lead times for precision manufacturing equipment stretched to 18 months. Yet the company maintained delivery schedules through a combination of long-term supplier agreements, strategic inventory buffers, and most crucially, the trust built over decades. When allocation decisions were made, Jentech's orders were prioritized.

Revenue growth reflected this operational success. From 2020 to 2023, Jentech's semiconductor thermal management revenue nearly tripled. Margins expanded even faster as customers accepted price increases to ensure supply continuity. The company's stock price responded accordingly, rising from under NT$500 in March 2020 to over NT$2,000 by late 2022—a 400% increase that outperformed even NVIDIA's spectacular run.

But the real transformation was strategic. Jentech evolved from passive component supplier to active thermal architecture partner. When NVIDIA's H100 pushed thermal design power past 700 watts, Jentech didn't just provide bigger heat spreaders—they collaborated on liquid cooling manifolds, cold plates, and even facility-level cooling infrastructure. For large language model inference like ChatGPT, NVIDIA announced the H100 NVL with dual-GPU NVLink, requiring thermal solutions that could manage heat from multiple chips operating in synchronization.

VII. Strategic Consolidation: The Kenly Acquisition (2024)

On January 18, 2024, Jentech Precision Industrial agreed to acquire Kenly Precision Industrial for TWD2.6 billion. The announcement surprised industry observers—why would a company riding the AI boom acquire a competitor focused on LED lead frames and mature semiconductor packaging? The answer revealed sophisticated strategic thinking that separated the Chao brothers from typical tech entrepreneurs chasing the latest trends.

Kenly Precision Industrial wasn't just any competitor. The Taiwan-based company specialized in manufacturing lead frames for optoelectronic products and heat spreaders for semiconductor packaging, with primary products including SMD LED lead frames, connector contactors, relays, thermistors, diodes lead frames and transistors lead frames. While these products seemed pedestrian compared to cutting-edge AI cooling solutions, they provided critical strategic value: customer diversification, manufacturing synergies, and most importantly, land.

Taiwan's semiconductor industry faced an unusual constraint: physical space. The island's mountainous terrain left limited flat land for industrial development. Existing facilities in science parks commanded astronomical prices when they occasionally became available. Kenly's facilities in northern Taiwan provided immediate capacity expansion without the 2-3 year timeline required for new construction. In an industry where speed to market determined success, this acquisition bought time—the scarcest resource of all.

The integration revealed Jentech's operational sophistication. Rather than imposing their processes on Kenly, they implemented a "best of both" approach. Kenly's expertise in high-volume LED lead frame production—millions of units monthly with six-sigma quality levels—enhanced Jentech's manufacturing efficiency. Conversely, Jentech's advanced thermal management technology upgraded Kenly's heat spreader products, allowing them to serve higher-value semiconductor applications.

The board resolved to issue new shares through capital increase to complete a share exchange with Kenly, structuring the deal to preserve capital while aligning incentives. Kenly shareholders received Jentech stock, making them stakeholders in the combined entity's success. This approach contrasted sharply with private equity-style acquisitions that often gutted acquired companies for short-term profit.

Customer response validated the strategy. Several major semiconductor assembly houses that previously split orders between Jentech and Kenly now consolidated with the combined entity, simplifying supply chain management. The broader product portfolio enabled package deals—thermal solutions bundled with lead frames and other components—that improved margins while reducing customer procurement complexity.

The financial engineering deserves scrutiny. At NT$2.6 billion, the acquisition price represented roughly 8% of Jentech's market capitalization—significant but not transformative. However, Kenly's stable cash flows from mature products provided financial ballast, reducing Jentech's dependence on the volatile high-performance computing market. This diversification would prove prescient as questions emerged about AI investment sustainability.

More intriguingly, the acquisition provided access to Kenly's relationships with Chinese semiconductor companies—relationships increasingly valuable as geopolitical tensions complicated direct engagement. While Jentech maintained focus on Taiwanese and Western customers, Kenly's established presence in China offered strategic optionality without political complications.

The operational integration proceeded with remarkable efficiency. Within six months, combined R&D teams had filed 12 new patents related to hybrid cooling solutions. Manufacturing consolidation reduced unit costs by 15% through improved equipment utilization. Most importantly, customer retention exceeded 95%, indicating successful relationship management during the transition.

The shares in issue of Jentech Precision Industrial were based on stock swap terms of 1 share of Jentech for every 22.2422 Kenly shares held, a ratio that reflected careful valuation while avoiding excessive dilution. The market responded positively, with Jentech's stock price rising 20% in the month following the announcement as investors recognized the strategic logic.

VIII. Financial Performance & Market Position (2023-2025)

The numbers tell a story of exceptional execution during extraordinary times. Jentech's financial performance from 2023 through 2025 reflects not just riding the AI wave, but positioning ahead of it through decades of patient preparation. The headline figures command attention, but the underlying metrics reveal the true competitive moat.

The company's earnings per share (TTM) reached 30.31 TWD, representing a trailing price-to-earnings ratio that, while elevated by historical standards, appears reasonable given growth trajectories. Revenue composition had shifted dramatically—thermal management solutions for high-performance computing now represented over 60% of total sales, up from less than 20% just five years prior. This transformation from diversified component supplier to focused thermal specialist created both opportunity and concentration risk.

Geographic revenue distribution provided important resilience. Unlike many tech suppliers dependent on U.S. markets, Jentech derived 90% of revenue from Asia. Taiwan alone accounted for the majority, reflecting deep integration with TSMC's ecosystem. This geographic concentration, typically viewed as risk, became strategic advantage as Taiwan's semiconductor dominance solidified. While competitors navigated complex U.S.-China trade restrictions, Jentech operated largely outside these constraints.

The stock reached its all-time high on September 11, 2025, at 2,615 TWD, compared to its all-time low of 35 TWD on August 24, 2015—a 75-fold increase that exceeded even the broader semiconductor sector's spectacular returns. This appreciation reflected fundamental business transformation rather than speculative excess. Revenue per employee had tripled. Return on invested capital exceeded 30%. Free cash flow conversion consistently surpassed 80% of net income.

The margin story proved particularly compelling. Gross margins expanded from low teens in 2015 to over 30% by 2024, driven by three factors: product mix shift toward high-value thermal solutions, operational leverage from scaled manufacturing, and pricing power from critical supplier status. Operating margins followed suit, reaching 20%—exceptional for what many still considered a commodity component business.

The company's dividend yield of 0.63% might seem modest, but it reflected aggressive reinvestment rather than capital stinginess. R&D spending had increased to 8% of revenue, high for a manufacturing company but essential for maintaining technological leadership. Capital expenditures consumed another 15% of revenue, funding capacity expansion and next-generation manufacturing capabilities.

Market share dynamics revealed Jentech's strengthening position. Global heat spreader manufacturers included Jentech, Honeywell, Shinko, Fujikura, I-Chiun, and Favor Precision Technology, with the top five manufacturers accounting for approximately 91% of market share in 2024. Within high-performance applications—AI accelerators, graphics cards, server processors—Jentech's share approached 35%, making them the largest independent supplier.

The balance sheet provided the foundation for continued growth. Debt-to-equity ratio remained below 0.3, providing financial flexibility for acquisitions or organic expansion. Working capital management had improved dramatically, with cash conversion cycles reduced by 30 days through better inventory management and supplier payment optimization. The company held over NT$5 billion in net cash, ammunition for strategic moves as industry consolidation accelerated.

Analyst coverage remained surprisingly thin—only three sell-side firms provided regular research, reflecting the company's below-the-radar profile despite its critical industry position. This limited coverage created information asymmetry that sophisticated investors could exploit. The few analysts who did cover Jentech consistently underestimated earnings, with actual results beating consensus by an average of 15% over the past eight quarters.

Customer concentration metrics raised valid concerns. The top five customers represented over 70% of revenue, with TSMC's ecosystem alone accounting for 40%. This concentration created both risk and opportunity—deep integration with leading customers provided competitive moat, but also vulnerability to customer-specific disruptions. Management addressed this through gradual diversification, adding two new top-10 customers annually without sacrificing core relationships.

Forward-looking metrics suggested continued momentum. Order backlog had extended to six months, unprecedented in the company's history. Design win pipeline—products specified but not yet in production—exceeded NT$10 billion. Customer qualification processes, typically taking 12-18 months, meant today's design wins would drive revenue through 2027 and beyond.

IX. The Future of Thermal Management in AI

The mathematics of heat dissipation are unforgiving. As transistor density doubles, heat flux quadruples. NVIDIA's latest Blackwell architecture pushes this reality to extremes—the GB200 Grace-Blackwell Superchip consumes up to 1,000 watts, with heat density approaching that of a nuclear reactor core. While clusters for training giant AI models now top out at around 100,000 current chips, Jensen Huang noted that "next generation starts at around 100,000 Blackwells," with the industry moving toward millions of GPUs. For Jentech, this represents both unprecedented opportunity and existential challenge.

NVIDIA's GB200 NVL72 and GB300 NVL72 AI systems achieve 25 times greater energy efficiency and 300 times better water efficiency using closed-loop direct-to-chip liquid cooling, marking a fundamental shift from air to liquid cooling. This transition isn't optional—air cooling simply cannot handle the heat flux of next-generation AI processors. Jentech's decade-long investment in liquid cooling technology, once considered speculative, now appears prescient.

The company's product roadmap reflects this reality. Traditional heat spreaders will remain important for conventional processors, but growth will come from integrated liquid cooling solutions. Cold plates that interface directly with chip packages. Microfluidic channels etched into copper substrates. Vapor chambers with embedded heat pipes. Each solution pushes manufacturing precision to new limits—tolerances measured in microns, surface roughness in nanometers.

Competition intensifies from unexpected directions. In October 2024, Schneider Electric acquired a 75% controlling stake in Motivair Corporation for $850 million, a U.S.-based company specializing in liquid cooling and advanced thermal management. Traditional cooling companies like Vertiv and infrastructure giants like Schneider recognize that thermal management has evolved from utility to strategic differentiator. Their deep pockets and global scale pose threats Jentech cannot ignore.

Yet the company possesses advantages that money cannot quickly replicate. Two decades of accumulated manufacturing expertise—knowing exactly how to plate copper for optimal thermal conductivity, how to bond dissimilar materials without creating thermal interfaces, how to maintain flatness under extreme thermal cycling. This tacit knowledge, encoded in processes and relationships rather than patents, creates barriers that new entrants struggle to overcome.

The sustainability imperative adds complexity. AI and high-performance computing integration among businesses boosts need for robust thermal management structure, but environmental concerns demand efficiency improvements. Data centers already consume 2% of global electricity; inefficient cooling doubles this impact. Jentech's next-generation solutions must not only manage more heat but do so using less energy—a seemingly contradictory requirement that demands fundamental innovation.

Direct-to-chip liquid cooling represents the near-term frontier. Rather than cooling air that then cools chips, coolant flows directly over processor heat spreaders. This approach can handle 2-3x the heat flux of air cooling while using 40% less energy. Jentech's prototypes achieve 500 watts per square centimeter of cooling capacity—sufficient for current needs but barely adequate for what's coming.

The medium-term evolution points toward immersion cooling, where entire server boards submerge in dielectric fluid. Liquid-based cooling experiences rapid growth driven by superior efficiency in high-density server environments, with direct-to-chip and immersion cooling increasingly adopted in hyperscale and AI-driven data centers. This technology eliminates air from the cooling equation entirely, enabling even higher density and efficiency. Jentech's role here remains unclear—immersion cooling might obsolete traditional heat spreaders or create demand for new thermal interface materials.

Longer-term possibilities venture into exotic territories. Two-phase cooling using engineered refrigerants. Microfluidic cooling with channels etched directly into silicon. Even theoretical approaches like diamond heat spreaders or graphene-based thermal interfaces. Jentech's R&D budget, while substantial by their standards, pales compared to Intel or TSMC's spending. Strategic partnerships rather than solo development will likely determine success.

With 655 employees, Jentech operates remarkably lean for its market impact. This efficiency becomes liability as technological complexity increases. The company aggressively recruits thermal engineers, materials scientists, and manufacturing specialists, but competes against tech giants offering Silicon Valley compensation packages. Creative approaches—equity participation, technical publication opportunities, academic partnerships—help attract talent, but the war for expertise intensifies.

X. Power Dynamics & Playbook

Vertical Integration Strategy: The Chao brothers built Jentech through relentless vertical integration, controlling everything from raw material processing to final testing. This approach, unfashionable in the age of asset-light business models, provides crucial advantages in precision manufacturing. When copper prices spike, Jentech's long-term supply agreements provide stability. When customers demand custom plating chemistry, in-house capabilities enable rapid iteration. The Kenly acquisition extended this integration, adding complementary manufacturing processes that reduce external dependencies.

The real power comes from integration of knowledge rather than just assets. Engineers who understand both metallurgy and thermal dynamics. Production managers who can optimize for both quality and throughput. Quality systems that trace problems from customer returns back to specific batches of raw material. This deep integration enables problem-solving that fragmented suppliers cannot match—when an AI chip fails thermal cycling, Jentech can identify whether the issue stems from plating thickness, surface roughness, or substrate warpage, then fix it within days rather than weeks.

Geographic Advantage: Located at No. 40, Keji 1st Rd. Taoyuan City, Jentech sits at the heart of Taiwan's semiconductor ecosystem. TSMC's fabs are an hour's drive. ASE's packaging facilities are even closer. This proximity enables daily face-to-face interactions that video calls cannot replicate—the casual conversation that reveals a customer's next-generation requirements, the quick visit to diagnose a production issue, the after-work dinner where real business gets done.

Taiwan's position transcends geography. The island produces 92% of advanced semiconductors, making it indispensable to global technology. This concentration creates risk but also unprecedented opportunity for suppliers like Jentech. While politicians debate semiconductor sovereignty and companies attempt geographic diversification, the reality remains: cutting-edge chips come from Taiwan, and they all need cooling.

Customer Concentration Risk: The flip side of deep customer integration is dangerous dependence. TSMC's ecosystem represents 40% of revenue. A strategic shift, technological change, or competitive loss at any major customer could devastate Jentech's business. The company addresses this through two approaches: technical entrenchment and gradual diversification.

Technical entrenchment means becoming so embedded in customers' processes that switching costs exceed any potential savings. When Jentech engineers participate in chip design reviews, when their thermal models inform package architecture, when their manufacturing processes are qualified into products with 10-year lifecycles, replacement becomes nearly impossible. The relationship transcends vendor-customer to become strategic partnership.

The founding brothers' combined wealth of $2.1 billion reflects three decades of patient value creation, but also highlights key man risk. While Chung-hsin focuses on technology and Yung-tsang manages operations, their partnership defines the company's culture and strategy. Succession planning remains opaque—neither brother has publicly identified successors, and family members' involvement in the business remains unclear.

Technical Moat: Jentech's competitive advantage stems from accumulated manufacturing expertise rather than breakthrough innovation. They don't invent new materials or discover novel physics. Instead, they perfect the application of known principles at unprecedented scale and precision. This might seem mundane, but it's incredibly difficult to replicate. A competitor can buy the same equipment, hire similar engineers, even reverse-engineer products, but they cannot quickly acquire two decades of learning from millions of units produced.

Capital Allocation: The brothers' approach to capital allocation reflects engineering mindset applied to finance. During downturns—2008 financial crisis, 2020 pandemic—they invest aggressively in R&D and capacity. During booms, they maintain discipline, avoiding overpaying for acquisitions or overbuilding capacity. The Kenly acquisition exemplified this discipline: strategic value justified the price, but they structured the deal to preserve financial flexibility.

XI. Bear & Bull Cases

Bear Case:

The bear thesis begins with the obvious: AI bubble risk. Current spending on AI infrastructure assumes massive return on investment that hasn't materialized beyond narrow applications. Nvidia investors know that promise of continuous growth can be an illusion—after sales surged more than 50% in past two years, revenue projected flat at $27 billion in fiscal 2023, with shares losing almost half their value since November 2021 peak. If AI investment disappoints, demand for extreme cooling solutions evaporates overnight.

Customer concentration amplifies this risk. Beyond dependence on specific companies, Jentech depends on specific products within those companies. NVIDIA's H100 and its successors drive enormous revenue, but technology transitions happen quickly in semiconductors. If next-generation architectures require different thermal approaches—perhaps integrated cooling that eliminates separate heat spreaders—Jentech's current products become obsolete.

Competition from larger players poses existential threat. As thermal management transitions from component to system-critical technology, giants are taking notice. Intel develops its own thermal solutions. TSMC could internalize heat spreader production. Chinese competitors, backed by government subsidies, might accept losses to gain market share. Jentech's limited resources cannot match sustained assault from determined well-funded competitors.

Geopolitical risks in Taiwan cannot be ignored. While semiconductor importance might provide protection—the "silicon shield"—it also makes Taiwan a target. Supply chain disruption from natural disaster, military conflict, or even sustained political tension could devastate Jentech's operations. The company's 90% revenue concentration in Asia provides no hedge against regional disruption.

Technology disruption lurks in unexpected places. Quantum computing, if commercially viable, might bypass traditional thermal constraints entirely. New semiconductor materials like gallium arsenide or silicon carbide could require completely different cooling approaches. Even within conventional computing, architectural changes—chiplet designs, 3D stacking, integrated cooling—could obsolete current thermal solutions.

Bull Case:

The bull thesis rests on thermodynamics' iron laws. Heat generation scales with computing power, and computing power drives modern economy. AI workload power consumption will account for 27% of total data center usage by 2027, with individual training runs potentially requiring up to 8 gigawatts by 2030. This isn't speculation—it's physics. Every transistor switching generates heat that must be removed. As long as computing advances, thermal management remains critical.

Jentech's embedded position in critical supply chains creates powerful moat. Semiconductor manufacturing involves thousands of process steps, each qualified through months of testing. Changing thermal solution suppliers requires re-qualification that could delay product launches by quarters. In an industry where time-to-market determines success, this switching cost provides enormous protection.

The global Integrated Heat Spreader market is projected to reach $1.07 billion by 2031, at 6.6% CAGR during forecast period. But this understates opportunity—these projections assume conventional computing growth, not the explosive AI expansion currently underway. If AI achieves even fraction of projected impact, thermal management market could exceed $10 billion by decade's end.

Consolidation opportunity in fragmented market favors established players. Hundreds of small thermal component manufacturers exist globally, many struggling with technology transitions and capital requirements. Jentech's strong balance sheet and operational expertise position them as natural consolidator. Each acquisition brings customers, technology, and manufacturing capacity that amplifies existing advantages.

Expanding applications multiply revenue opportunities. Electric vehicles require sophisticated thermal management for batteries and power electronics. Edge computing brings data center thermal challenges to distributed locations. Quantum computing, while different from conventional semiconductors, still generates heat requiring management. Even consumer devices—gaming laptops, virtual reality headsets—push thermal boundaries that create new markets.

The sustainability imperative transforms from challenge to opportunity. Data center cooling market grows rapidly, led by hyperscale demand, cloud services growth, edge computing deployment, and AI workloads demanding sophisticated thermal management, with operators investing in liquid cooling and modular systems to meet net-zero targets. Regulations demanding improved energy efficiency favor advanced thermal solutions over brute-force cooling. Jentech's expertise positions them as enabler of sustainable computing infrastructure.

XII. Lessons & Reflections

The Jentech story challenges Silicon Valley's monopoly on tech success narratives. No venture capital. No Stanford dropouts. No exponential user growth or network effects. Instead, two brothers with high school educations built a $10 billion company through patient accumulation of manufacturing expertise. They succeeded not by disrupting industries but by enabling them, not by moving fast and breaking things but by moving deliberately and making things that never break.

Timing and patience emerge as the crucial lesson. The Chao brothers spent twenty years preparing for an opportunity that crystallized in just three. They developed liquid cooling capabilities a decade before market demand. They invested in semiconductor thermal management when gaming was the only high-power application. This patient capital allocation—accepting lower returns for years while building capabilities—contradicts modern finance theory but creates sustainable competitive advantages.

The power of focusing on unsexy but critical problems deserves emphasis. Thermal management attracts no mainstream attention. No TED talks celebrate heat spreader innovation. No business school cases study precision metal stamping. Yet this invisibility becomes advantage—less competition for talent, less volatile valuations, less pressure for unsustainable growth. By solving problems others considered boring, Jentech captured value others overlooked.

Building trust in Asian business ecosystems requires different approach than Silicon Valley networking. Relationships develop over decades, not demo days. Trust comes from consistent delivery, not charismatic pitches. The Chao brothers built their network through reliability—every commitment met, every quality standard exceeded, every delivery date achieved. This reputation, impossible to acquire quickly, becomes the ultimate competitive moat in relationship-driven markets.

Manufacturing excellence still matters in the digital age—perhaps more than ever. Software might eat the world, but it runs on hardware that generates heat. The most sophisticated AI algorithms become useless if processors overheat. The metaverse cannot exist without physical servers in physical data centers requiring physical cooling. Jentech's success reminds us that atoms remain as important as bits.

The hidden infrastructure of the AI revolution tells a different story than headline narratives. While NVIDIA captures trillion-dollar valuations and OpenAI grabs headlines, companies like Jentech quietly enable the revolution. They profit not from AI itself but from AI's physical requirements—cooling, power delivery, interconnection. This arms-dealer strategy—selling shovels during gold rush—often proves more profitable than prospecting.

XIII. Epilogue: What Would We Do?

Standing in Jentech's position today requires strategic choices that will determine whether they remain critical suppliers or become technology leaders. Geographic diversification cannot be delayed. While Taiwan advantages remain strong, customer anxiety about supply chain concentration intensifies. Establishing advanced manufacturing in Arizona, where TSMC builds its American fabs, would provide both customer proximity and supply chain resilience. The investment would be enormous—perhaps $500 million—but customer commitments could offset risk.

Deeper integration with liquid cooling systems represents the natural evolution. Rather than supplying components, Jentech could offer complete thermal solutions—cold plates, pumps, coolant distribution, control systems. This expansion requires different expertise—fluid dynamics, system integration, software controls—but captures 10x the value per processor cooled. Acquisition might accelerate this transition, perhaps targeting a struggling liquid cooling specialist with technology but lacking manufacturing scale.

The build-versus-partner decision for advanced technologies demands careful consideration. Jentech cannot match Intel or TSMC's R&D spending, but they could lead consortiums developing next-generation cooling. Partnering with materials science startups working on graphene or diamond heat spreaders. Collaborating with universities on two-phase cooling research. Creating an ecosystem where Jentech provides manufacturing expertise while partners contribute breakthrough innovation.

Strategic partnerships with cloud providers offer intriguing possibilities. Amazon, Microsoft, and Google spend billions on data center infrastructure, increasingly recognizing cooling as competitive differentiator. Direct relationships—perhaps even joint ventures—could provide both guaranteed demand and insight into future requirements. Imagine Jentech engineers embedded in AWS data center design teams, creating custom solutions that become industry standards.

Preparing for the post-AI boom cycle requires discipline that few companies maintain during boom times. History shows that semiconductor supercycles always end, usually badly. The prudent strategy: maintain strong balance sheet, avoid overcapacity, diversify customer base, invest in capabilities not just capacity. When downturn arrives—and it will—Jentech should emerge stronger, acquiring distressed competitors and hiring talent from struggling firms.

The ultimate question: should Jentech remain independent? At $10 billion market cap, they're attractive acquisition target for companies seeking vertical integration. TSMC could ensure thermal solution supply. NVIDIA could control critical component. Private equity could financial engineer returns. But independence provides strategic flexibility that acquisition would eliminate. The Chao brothers, having built the company over four decades, seem unlikely to sell unless succession concerns force their hand.

The next chapter of Jentech's story depends on decisions made in the next 18 months. The AI infrastructure boom won't last forever, but thermal management challenges will intensify regardless. Whether solving problems for quantum computers, autonomous vehicles, or technologies not yet invented, the company that keeps advanced semiconductors from melting will remain valuable. The question isn't whether Jentech has a future, but whether that future matches the extraordinary present they've created through patient excellence in the unglamorous but essential business of managing heat.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube