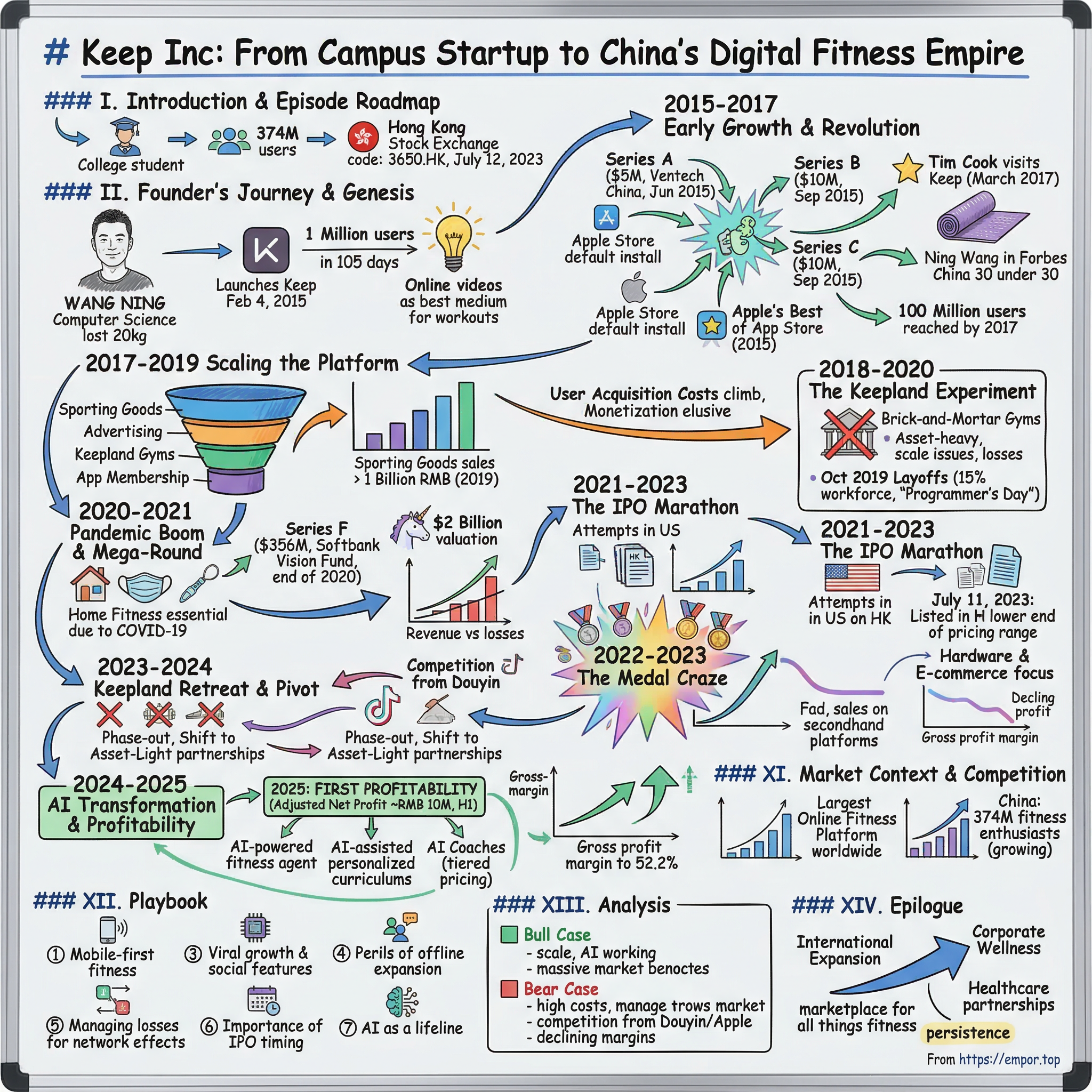

Keep Inc: From Campus Startup to China's Digital Fitness Empire

I. Introduction & Episode Roadmap

Picture this: A chubby college student in Beijing, hunched over his laptop at 2 AM, desperately googling "how to lose weight without a gym." Fast forward a decade, and that same student's fitness app commands 374 million fitness enthusiasts in China—more than the entire population of the United States. This is the improbable journey of Keep Inc., China's First Listed Fitness Company, a story that begins not in a Silicon Valley garage or a Shanghai tech incubator, but in a Beijing dorm room where desperation met determination.

Keep Inc. develops fitness platform providing comprehensive fitness solutions. The Company offers recorded courses and live streaming classes, and sells self-branded fitness devices and products. Listed on the Hong Kong Stock Exchange on July 12, 2023 (stock code: 3650.HK), Keep represents something far more complex than just another fitness app—it's a mirror reflecting China's evolving relationship with health, technology, and the relentless pursuit of profitability in the consumer internet age.

The question that drives our narrative today isn't just "How did a college student's personal weight loss journey become a $2 billion fitness empire?"—though that's certainly part of it. The real question is: How did Keep navigate the treacherous waters of Chinese consumer tech, survive multiple near-death experiences, pivot from physical gyms to virtual medals, and finally, in 2025, achieve what had eluded it for a decade: profitability?

This is a story about Chinese tech entrepreneurship at its most raw—where viral growth masks unit economics challenges, where pandemic windfalls evaporate as quickly as they arrive, where AI transformation becomes not a luxury but a lifeline. It's about the struggle between building a sustainable business and satisfying venture capital appetites, between serving fitness enthusiasts and selling them yoga mats.

II. The Founder's Journey & Keep's Genesis (2014-2015)

The monsoon rains that inspired Ratan Tata's People's Car vision have their parallel in Wang Ning's own moment of clarity—though his came not from witnessing others' struggles, but from confronting his own reflection. Wang Ning graduated from the Beijing Information Science and Technology University in computer science. In his fourth year, he wanted to lose weight but could not afford a personal trainer. After doing research online, he devised a set of strategies for weight loss, enabling him to lose 20kg.

Twenty kilograms. Forty-four pounds. The weight of a large suitcase, shed through sheer determination and late-night research sessions. Subsequently, Wang came up with the idea to create an app which provided the resources to successfully lose weight and lead a healthier lifestyle. But Wang's insight went deeper than personal transformation. In conversations with Tencent Technology in 2018, he articulated a frustration that millions of young Chinese felt: "Traditional gyms can't understand what us simple fatties need to improve our physiques…[and] traditional fitness gave me 10,000 reasons why I couldn't succeed," citing high costs, inconvenient locations, and boredom as the major problems that his company aimed to solve.

The genius wasn't in identifying the problem—everyone knew gyms were expensive and intimidating. The genius was in understanding that online videos were the best medium to enable people to work out anywhere, at any time. This wasn't just about democratizing fitness; it was about reimagining it entirely for a generation that lived their lives through smartphone screens.

Keep was developed by the company Beijing Calories Technology, which was founded by the college student Wang Ning. The name itself was a manifesto: "he believes keeping, or persistence, is the core of losing weight and starting up a company". In the hyper-competitive world of Chinese tech, where companies routinely burn through millions before finding product-market fit, persistence would prove to be more than philosophy—it would be survival strategy.

Wang then led a start-up team of twelve, consisting of his university course mates and colleagues from his internship at the online tutoring platform Yuanfudao. This wasn't a team of seasoned entrepreneurs or fitness gurus—these were young technologists who understood code better than kettlebells, algorithms better than aerobics. Their inexperience in fitness would paradoxically become their greatest asset, allowing them to approach the industry without the baggage of conventional wisdom.

The app was made available for downloading on 4 February 2015. What happened next defied every reasonable expectation. Keep reached one million users downloads by 105 days after its launch—a velocity that would make even seasoned venture capitalists do a double-take. In the context of 2015 China, where hundreds of apps launched daily and most died in obscurity, this wasn't just growth—it was a phenomenon.

III. Early Growth & The Chinese Fitness Revolution (2015-2017)

The year 2015 marked an inflection point in China's relationship with fitness. Keep was founded in 2014 and launched its online fitness platform a year later by offering structured fitness courses. China's fitness market started to generate an outpouring of investor interest that same year. This wasn't coincidence—it was convergence. Rising incomes, health consciousness, and smartphone penetration created a perfect storm that Keep was uniquely positioned to capture.

Keep quickly built up a base of more than 2 million users, which helped it attract $5 million in series-A funding in June 2015 and another $10 million in series-B three months later as its user base soared to 10 million. The math was staggering: from 2 million to 10 million users in three months. In Silicon Valley, this would be called hockey-stick growth. In Beijing, it was called validation.

Ventech China became acquainted with Keep and was immediately impressed by the founder, Ning WANG's profound understanding of the emerging fitness market, his keen grasp of consumer needs, and his unwavering determination. Ventech China promptly invested in Keep's A round one year later than Keep's inception, becoming the leading investor. The early believers saw what others missed—this wasn't just an app, it was a movement.

The platform's integration with Apple's ecosystem proved transformative. Keep was installed by default on devices in Apple Stores in China and earned a spot on Apple's coveted "2015 Best of App Store list." This wasn't just distribution—it was endorsement from the world's most valuable company.

Then came the moment that would cement Keep's place in Chinese tech lore. In March 2017, Apple CEO Tim Cook visited Keep's offices as part of his tour around leading Chinese internet companies. Keep CEO Wang Ning gifted Tim Cook a yoga mat that said "80,000,001", meaning Tim was Keep's 80,000,001st user. In the same year, Ning Wang was featured in Forbes China 30 under 30 list.

The Tim Cook visit was more than a photo opportunity—it was a coronation. When the CEO of Apple visits your office, you've transcended startup status. You've become part of the establishment, even as you're disrupting it. The image of Cook holding that yoga mat would become iconic in Chinese tech circles, a David-and-Goliath moment where David got Goliath's autograph.

By this point, Keep had achieved something remarkable: It was the first fitness app to reach 100 million users in 2017. The velocity was breathtaking—from zero to 100 million in less than three years. For context, it took Facebook four years to reach 100 million users, and Facebook had the entire internet as its playground.

IV. Scaling the Platform & Business Model Evolution (2017-2019)

The funding rounds that followed read like a who's who of global finance. Keep received US$10 million in Series B funding from GGV Capital and US$32 million in Series C funding from Morningside Ventures and GGV Capital, with participation from Bertelsmann Asia Investments. In July 2018, it received $126 million in Series D funding from Goldman Sachs, Tencent, GGV Capital, and Morningside Venture Capital.

But Keep's ambitions extended far beyond being just another fitness app. CB Insights wrote in a 2017 report that "Many fitness mobile apps offer convenience, but Keep has differentiated itself by integrating social media and e-commerce within its app. The app's social media component not only allows fitness enthusiasts to post their own content, but also allows fitness brands to create in-app social campaigns and promotions."

This was the crucial pivot—from fitness app to fitness ecosystem. Keep's four streams of revenue are sporting goods, advertising, its Keepland gyms, and app membership. Each revenue stream told a different story about Keep's evolution and the challenges of monetizing fitness in China.

The sporting goods business was particularly revealing. By 2019, Keep had generated over one billion yuan in sporting goods sales, ranking fourth on Tmall behind established giants like Decathlon and Lululemon. This wasn't just diversification—it was an acknowledgment that in China's fitness market, selling the dream was as important as selling the workout.

By September 2019, Keep had reached 200 million users. The numbers were impressive, but beneath the surface, cracks were beginning to show. User acquisition costs were climbing. Monetization remained elusive. The fundamental question—how do you make money from people who want to get fit for free?—remained unanswered.

A December 2018 report published by Sootoo Institute found that there were 38.8 million downloads of Keep between July and September, making it "the most downloaded fitness app in China". Market leadership, however, didn't translate to profitability. Keep was winning the war for users but losing the battle for sustainable economics.

V. The Keepland Experiment: Physical Meets Digital (2018-2020)

In March 2018, Keep opened a gym in Beijing, its first. China has 11 Keep-owned gyms, called Keepland, with nine located in Beijing and two in Shanghai. The company opened the brick-and-mortar gyms with the goal of nurturing brand loyalty by having online users start in-person relationships.

The logic was seductive: blend online and offline, create a seamless fitness experience, capture more value from your most engaged users. It was the same playbook that had worked for Alibaba with Hema supermarkets and JD.com with retail stores. Surely it would work for fitness?

The reality proved far messier. Running gyms is fundamentally different from running apps. Apps scale with code; gyms scale with real estate. Apps have bugs; gyms have broken treadmills. Apps need developers; gyms need cleaning staff. The unit economics that made sense in a spreadsheet fell apart when confronted with the reality of Beijing rent prices and the fickleness of gym-goers.

By 2019, the strain was showing. Keep had grown from a lean startup to a bloated organization. In 2019, the company had 800 employees. For a company still searching for profitability, this headcount was unsustainable.

Then came the reckoning. As China was experiencing economic deceleration, Keep in October 2019 laid off 15% of its workforce after having increased it by fourfold in 2018. The layoffs were particularly brutal in their timing and execution. "I was notified that I was laid off at 2 a.m. on October 24, had a talk at 3 a.m. and asked to leave at 4 a.m.," said a Maimai user who is a verified Keep employee.

October 24—or "1024"—is celebrated as Programmer's Day in China, making the timing of the layoffs particularly cruel. "The number of Keep colleagues in our working group dropped from 856 to 797, and this is going to continue tomorrow," the same employee noted. The company that had preached "discipline brings freedom" was learning that discipline sometimes means admitting failure.

VI. The Pandemic Boom & Series F Mega-Round (2020-2021)

COVID-19 changed everything. Suddenly, the entire world was locked at home, desperate for ways to stay fit without gyms. Keep, having just endured brutal layoffs and strategic pivots, found itself in the right place at the right time. Softbank's Vision Fund also led its series-F funding at the end of 2020, helping the company raise $356 million and obtain a $2 billion valuation.

The Series F was more than just capital—it was vindication. Keep Inc., China's most popular fitness app backed by SoftBank's Vision Fund and Tencent Holdings, had achieved unicorn status at the perfect moment. The pandemic had done what years of marketing couldn't: convince millions that home fitness wasn't just convenient, it was essential.

Wang Ning, reflecting on this period, understood the opportunity: "The company founded in 2014 by Wang Ning is among the businesses that have benefited from the pandemic as people were forced to work out at home." But he also understood the challenge—pandemic tailwinds wouldn't last forever.

The financial performance during this period was a study in contrasts. Keep logged losses of CNY696 million (USD110.2 million) in the nine months ended Sept. 30, 2021. Revenue, though, jumped 41.3 percent from the same period the year before to CNY1.1 billion (USD183.5 million). Growth was accelerating, but so were losses.

The firm, which had 41.7 million monthly active users in the third quarter last year, was at a crossroads. The pandemic had given Keep a second chance, but it was unclear whether the company could capitalize on it. The fundamental challenge remained: how do you monetize fitness in a market where users expect everything for free?

VII. The IPO Marathon: Multiple Attempts & Reality Check (2021-2023)

The path to public markets was anything but smooth. Initially, Keep harbored ambitions of a US listing, reportedly targeting up to $500 million. But as US-China tensions escalated and Chinese tech stocks cratered on American exchanges, those dreams evaporated.

The pivot to Hong Kong was pragmatic but painful. Investment banks Goldman Sachs and China International Capital Corp. are sponsors of the IPO, operator Beijing Calorie Technology said in the filing on Feb. 25. This first attempt would expire six months later, unrealized.

Keep Inc, backed by SoftBank and Tencent, had filed a listing application in February, but it did not proceed further during the six-month window that ended in August. The company tried again, and again. Each attempt was a Sisyphean effort—pushing the boulder up the regulatory mountain only to watch it roll back down.

Beijing-based Keep, which attempted to list twice in Hong Kong last year, has raised US$40 million from the sale of 10.84 million shares on its third attempt. Third time's the charm, they say, but Keep's charm had worn thin.

The final IPO pricing told the real story. Keep sold 10.8 million shares at HK$28.92 per unit, the lower end of its pricing range—never a good sign. The company was valued at $1.94b, lower than the $2.4b in its last funding round. This wasn't a triumphant public debut; it was a down round disguised as an IPO.

On July 11, 2023, Keep finally went public. The stock opened at HK$30.3, a modest 4.77% premium to the IPO price. For a few hours, it seemed like vindication. But the market's initial enthusiasm quickly faded. The company that had once commanded a $2.4 billion private valuation was now worth significantly less as a public company.

Wang Ning, addressing employees after the IPO, tried to maintain optimism: "This is not the end, but the beginning." In the brutal arithmetic of public markets, however, beginnings that start with disappointment rarely end in triumph.

VIII. The Medal Craze & Product-Market Fit Challenges (2022-2023)

Sometimes salvation comes from the most unexpected places. For Keep, it came in the form of virtual medals—digital badges that users could earn by completing online challenges. When the medal craze took off in May 2022, one user gained over 120,000 "likes" for a post of her collection, with the caption "Showing off the medals my boyfriend ran to get me." There have been over 100,000 posts with related hashtags overall on Xiaohongshu, while videos under the hashtag "Keep medal unboxing" have been viewed over 10 million times on Douyin.

The medals weren't just virtual—Keep shipped physical medals to users who completed challenges. After KEEP and Sanrio's co-brand started and went viral, the company achieved revenue of RMB ¥417 million in the first quarter of 2022, rising 37.6% year-on-year. Hello Kitty medals. Solar term medals. Little Maruko-chan medals. Each limited edition release created a frenzy of activity.

In its Hong Kong listing prospectus, Keep claimed that revenue growth for the first quarter of 2023 was "mainly attributable to…virtual sports events." In other words, the medals paid off. For a brief moment, Keep had cracked the code—turning digital fitness into physical collectibles, transforming sweat into social currency.

But the craze is over. People are selling their medals for discount prices on secondhand ecommerce platforms, while there have only been 556 posts about the medals on the popular social media platform Xiaohongshu in the last 30 days. The medal economy, like all fads, had a half-life measured in months, not years.

The deeper challenge was structural. A full 51% of Keep's revenue in 2022 came from sales of its own products. But its gross profit margins were far lower than other domestic sports brands like Li Ning and Anta—and fell from 21% to under 15% from 2019 to 2022. Keep had become, in essence, a low-margin e-commerce business masquerading as a tech platform.

IX. The Keepland Retreat & Offline Strategy Pivot (2023-2024)

Reality has a way of forcing clarity. Cutthroat competition, high operating costs, and finally the pandemic that forced the temporary closure of most gyms in early 2020, forced it to close all the facilities in Shanghai and maintain just a few in Beijing. By 2024, Keep was actively unwinding its offline gym strategy.

The company's financial statements told the story in stark numbers: "Decreases of RMB7.6 million in outsourcing and other labour cost and RMB7.1 million in employee benefit costs, respectively, relating to the gradual phase-out of the Keepland business in 2024." Each line item was an admission of defeat, a recognition that the offline-online integration dream had become a nightmare.

But Keep wasn't giving up on offline entirely—it was reimagining it. Earlier in 2024, the company announced intentions to increase the number of gyms it collaborates with (rather than owns) from 100 to 150 in Beijing, and from five to 30 in Guangzhou. This was asset-light expansion, the kind that Silicon Valley would approve of. Partner, don't own. Enable, don't operate.

The pivot made sense but came late. Competitors like Douyin had already entered the fitness space, leveraging their massive user bases and sophisticated algorithms to offer fitness content without the burden of physical infrastructure. Liu's cyber gravitation has also ground Keep, a domestically dominant fitness app, to dust. The Shanghai-based app has an accumulated user of 300 million since 2015 and owns 34.4 million monthly active users as of 2021.

Keep's response was to double down on what it did best—content and community. From 2021 to 2022, the number of fitness influencers and third-party content providers contracted to Keep doubled from 321 to 642. Over 35 million people have watched the 10-minute "Beginners' slim stomach" class by Pamela Reif, one of the most popular fitness influencers on the platform.

X. The AI Transformation & Path to Profitability (2024-2025)

The year 2025 marked Keep's most dramatic transformation yet. Wang Ning, Chief Executive Officer commented, "2025 marks a pivotal chapter as we transform from a content-centric platform into an AI-powered, data-driven fitness agent." This wasn't incremental evolution—it was revolution.

The results spoke volumes. Keep reported an adjusted net profit of ~RMB 10 million (non-IFRS) for H1 2025. After a decade of losses, Keep had finally achieved what had seemed impossible: profitability. Wang Ning attributed the milestone to "high-quality business growth" and the elimination of underperforming segments. He described it as "cutting fat and building muscle," emphasizing that profitability is sustainable and not accidental.

The margin improvements were particularly impressive. Gross profit margin reached 52.2% in the first half of 2025, a 6.2 percentage point increase from 46.0% in the first half of 2024. This wasn't just cost-cutting—it was fundamental business model transformation.

Keep's AI strategy went beyond buzzwords. The platform now provides fitness content with AI-assisted personalized curriculums that adjust course content and workout intensity based on users' athletic levels, fitness goals, daily workout patterns, and diet. Looking ahead, Keep's AI coaches will evolve into three tiers: general, personalized IP-based, and specialized (e.g., marathon, boxing). Each will have distinct pricing.

"We're transforming from a content-driven app to a data-driven service platform," Wang said. This was the key insight—Keep wasn't just pivoting to AI, it was reimagining its entire value proposition. No longer would it be a library of workout videos; it would be a personalized fitness companion powered by machine learning.

XI. Market Context & Competition

The market opportunity remains massive, even as competition intensifies. China had the most number of fitness enthusiasts in the world at 374 million last year, according to Keep's prospectus, which cited research from CICC. That number is expected to grow by 24 per cent to 463.5 million by 2027, while per-capita spending on physical fitness in China is only about a sixth of that in the US, implying huge room for growth.

Keep's platform scale is undeniable. The company reached around 30 million monthly active users (MAUs) in 2022–2023. In 2022 alone, Keep recorded approximately 2.1 billion workout sessions on its platform. Today, Keep stands as the largest online fitness platform worldwide, symbolizing health and fitness with its strong brand influence. A staggering 77.5% of the fitness population in China is familiar with the Keep mobile app.

The competitive landscape, however, has evolved dramatically. ByteDance's Douyin has emerged as a formidable competitor, leveraging its massive user base to offer fitness content. Traditional gym chains are digitizing. International players like Peloton and Apple Fitness+ are eyeing the Chinese market. The moat that once seemed insurmountable is now under constant assault.

Ownership structure reveals the stakes involved. Founded in 2015, Keep's largest shareholder is its founder and Chief Executive Wang Ning with an 18.6 percent stake. The US' GGV Capital owns 16.1 percent while Japan's SoftBank has 10.3 percent. This concentration of ownership gives Wang significant control but also significant pressure to deliver returns to blue-chip investors who've been waiting a decade for their exit.

XII. Playbook: Business & Investing Lessons

Mobile-first fitness disruption in emerging markets: Keep proved that in markets where gym penetration is low and smartphone penetration is high, mobile-first fitness can achieve massive scale. The key is understanding that you're not competing with gyms—you're competing with the couch.

The challenges of hardware-software integration: Keep's journey into smart treadmills and physical gyms offers a cautionary tale. Hardware is hard. Retail is harder. The asset-light model exists for a reason, and violating it requires exceptional execution and deep pockets.

Viral growth mechanics and social features: Keep's integration of social features—from friend challenges to medal collecting—demonstrates the power of community in fitness. People don't just want to get fit; they want to be seen getting fit.

The perils of offline expansion for digital companies: Keepland's failure wasn't just about execution—it was about fundamental economics. Digital businesses scale differently than physical ones. Trying to be both often means being neither.

Managing losses while building network effects: Keep burned through over $600 million before achieving profitability. The question for investors: was this investment in growth or subsidization of an unsustainable model? The answer came in 2025—it was both.

The importance of timing in IPO markets: Keep's multiple failed IPO attempts and eventual down-round listing demonstrate that market timing matters more than company readiness. The best time to go public is when investors want to buy, not when you need to sell.

AI as a lifeline for struggling consumer tech companies: Keep's AI transformation wasn't innovation for innovation's sake—it was survival. When your core business model is challenged, radical transformation becomes rational strategy.

XIII. Analysis & Bear vs. Bull Case

Bull Case:

The optimist sees Keep as China's Peloton-meets-MyFitnessPal-meets-Nike, a super-app for fitness that has finally found its path to profitability. With 30 million monthly active users and growing, Keep has achieved the scale necessary for network effects. The AI transformation is working, margins are expanding, and the company is positioned to capture the growth of China's fitness market.

The profitability turnaround in 2025 wasn't a fluke—it was the result of disciplined cost management and strategic focus. As Wang Ning said, this was "cutting fat and building muscle," and the muscle is now showing. The company's evolution from content platform to AI-powered fitness agent positions it at the forefront of the next generation of fitness technology.

Most importantly, the market opportunity remains enormous. With Chinese per-capita fitness spending at just one-sixth of US levels, the runway for growth extends for decades. Keep, as the established market leader with the strongest brand recognition, is best positioned to capture this growth.

Bear Case:

The skeptic sees a company that took a decade and $600 million to achieve bare profitability, and only then by dramatically cutting costs and abandoning core strategies. The Keepland retreat wasn't strategic evolution—it was expensive failure. The medal craze that briefly boosted revenue has faded, revealing the fickleness of Keep's user base.

Competition is intensifying from every direction. ByteDance has unlimited resources and superior algorithms. Apple has hardware integration and premium positioning. Traditional gyms are digitizing rapidly. Keep's moat—if it ever existed—is evaporating.

The company's dependence on product sales (over 50% of revenue) with declining margins (from 21% to 15%) reveals the uncomfortable truth: Keep is more e-commerce than tech platform. The AI pivot, while promising, is unproven and faces the same monetization challenges that have plagued Keep since inception.

Most damning: the stock trades well below its IPO price, itself below the last private valuation. The market has rendered its verdict, and it's not favorable.

XIV. Epilogue & "If We Were CEOs"

If we were running Keep today, the path forward would require brutal focus and strategic clarity. First, double down on AI personalization but with clear monetization—premium AI coaching tiers, corporate wellness programs, insurance partnerships. The technology is only valuable if people pay for it.

Second, abandon any remaining offline ambitions beyond partnerships. Keep is a digital company; trying to be otherwise is a distraction. Let others own the gyms; Keep should own the experience.

Third, international expansion—but carefully. The playbook that worked in China won't necessarily work elsewhere, but the problems Keep solves are universal. Southeast Asia, with its similar demographics and digital adoption, offers the most promise.

Fourth, embrace the platform model fully. Keep should be the iOS of fitness—let thousand flowers bloom, take a cut of everything. The medal craze showed that users want more than workouts; give them a marketplace for all things fitness.

Finally, remember the founding mission. Wang Ning started Keep because traditional fitness failed him. Ten years later, has Keep become what it set out to disrupt? The answer to that question will determine whether Keep's next decade is one of growth or decline.

The China fitness market will continue evolving, with or without Keep. The question is whether Keep can evolve fast enough to remain relevant. The profitability achievement in 2025 suggests it can. The stock price suggests the market isn't convinced.

For other consumer tech companies, Keep offers both inspiration and warning. Inspiration that even the most challenging business models can eventually find profitability. Warning that the path there might cost more—in time, money, and strategic pivots—than anyone imagines at the start.

XV. Recent News

The AI transformation continues to accelerate. In recent earnings calls, management has emphasized that 2025's profitability wasn't a one-time event but the beginning of a sustainable trend. The company is exploring partnerships with healthcare providers and insurance companies, positioning fitness as preventive medicine.

Competition remains fierce. ByteDance's Douyin continues to invest heavily in fitness content, while Apple's expansion in China puts pressure on the premium segment. Keep's response has been to focus on the mass market, where its brand recognition remains strongest.

The macroeconomic environment adds complexity. China's economic slowdown has impacted consumer spending, but paradoxically may benefit Keep as consumers seek affordable fitness alternatives to expensive gym memberships.

XVI. Links & Resources

Primary Sources: - Keep Inc. Hong Kong Stock Exchange Filings (3650.HK) - Annual Reports (2021-2025) - IPO Prospectus (February 2023)

Key Interviews: - Wang Ning interview with Tencent Technology (2018) - Tim Cook China visit coverage (March 2017) - Forbes China 30 Under 30 Profile (2017)

Industry Research: - China Insights Consultancy: China Online Fitness Market Report - CB Insights: Keep Company Profile and Analysis - Sootoo Institute: Chinese Fitness App Market Study

Books on Chinese Tech: - "The Story of Chinese Tech" by Various Authors - "China's Digital Revolution" by Winston Ma - "Billion Dollar Apps" by Michael Tchong

Relevant Analysis: - GGV Capital: The Rise of Digital Fitness in China - SoftBank Vision Fund: Consumer Tech Investment Thesis - Morningside Ventures: China Consumer Trends Report

[End of Article]

This comprehensive analysis of Keep Inc. reveals a company that embodies both the promise and peril of Chinese consumer tech. From a dorm room weight-loss journey to a public company achieving profitability through AI transformation, Keep's story is one of persistence—the very quality embedded in its name. Whether that persistence will be enough to thrive in an increasingly competitive market remains the billion-dollar question.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube