APR Corporation: The TikTok-Powered Beauty Tech Revolution

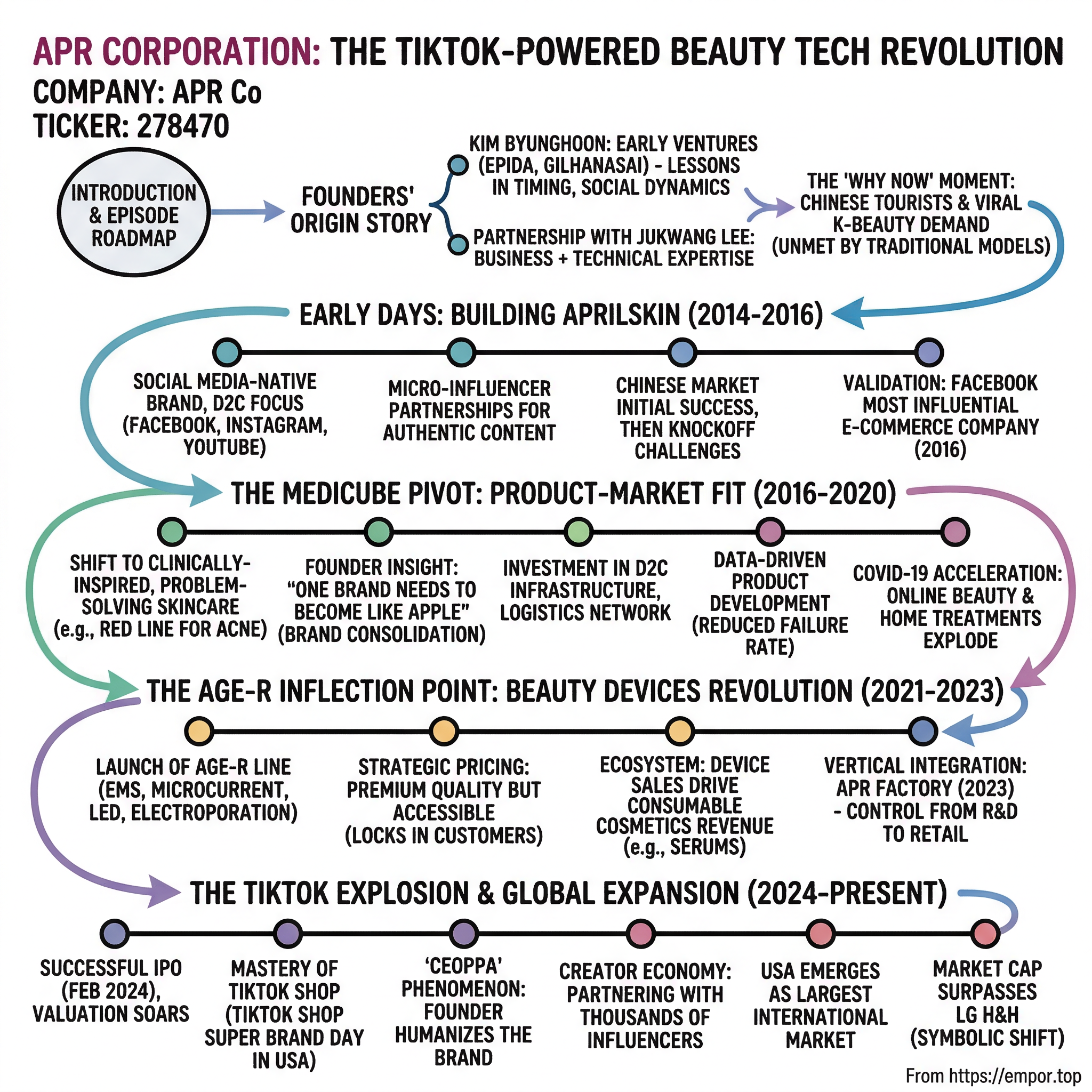

I. Introduction & Episode Roadmap

The story of APR Corporation reads like a Silicon Valley fairytale transplanted to Seoul's beauty industry. When Kim Byunghoon rang the opening bell at the Korea Exchange on February 26, 2024, his 31% stake in the company was valued at approximately 594 billion KRW. Less than two years later, that same stake has soared to over 3 trillion KRW as APR's market cap reached 10.2 trillion KRW, making him one of Korea's youngest self-made billionaires.

Founded just over a decade ago in 2014, APR Corporation has achieved what takes most beauty companies generations to accomplish. The company's trajectory defies conventional wisdom about brand building in the beauty industry. While legacy players like LG H&H spent decades building their empires through traditional retail channels and mass marketing, APR leveraged social media algorithms and direct-to-consumer strategies to compress that timeline into a single decade.

The central question animating this analysis is deceptively simple yet profoundly complex: How did two college dropouts build Korea's hottest beauty tech unicorn in an industry dominated by century-old conglomerates? The answer reveals fundamental shifts in consumer behavior, the democratization of brand building through social media, and the convergence of beauty and technology that defines the modern cosmetics industry.

This episode explores four interconnected themes that explain APR's meteoric rise. First, the D2C revolution that allowed the company to maintain 70% of sales through its own channels for seven consecutive years. Second, the mastery of social commerce that transformed TikTok from a marketing channel into a primary sales driver. Third, the beauty-tech convergence embodied in the AGE-R device line that created an entirely new product category. Finally, the platform thinking that turned hardware sales into recurring revenue streams through consumable cosmetics.

II. The Founders' Origin Story

Kim Byunghoon's path to becoming Korea's beauty tech mogul began far from the glamorous world of cosmetics. Born on November 5, 1988, in Seoul, Kim grew up during Korea's rapid digital transformation, witnessing firsthand how technology could disrupt traditional industries. His enrollment at Yonsei University's business school seemed to set him on a conventional corporate track, but entrepreneurial ambitions soon derailed those plans.

Before APR, Kim's entrepreneurial journey was marked by instructive failures. His first venture, Epida, attempted to solve the online shopping fit problem through virtual fitting technology. The concept was ahead of its time but struggled with the technological limitations of the early 2010s. His second attempt, a dating app called Gilhanasai (roughly translating to "Find Your Path"), failed to gain traction in Korea's crowded dating app market dominated by established players.

These failures, however, provided crucial lessons. Epida taught Kim about the importance of timing and technological readiness. Gilhanasai demonstrated the challenges of competing in winner-take-all digital markets. Both ventures, critically, exposed him to the power of social dynamics in driving user adoption—lessons that would prove invaluable in the beauty industry.

The partnership with co-founder Jukwang Lee formed during their university days at Yonsei. Where Kim brought business acumen and marketing instincts, Lee contributed technical expertise and operational discipline. Their complementary skill sets created a founding team capable of bridging the traditionally separate worlds of technology and beauty. The decision to drop out of university wasn't taken lightly, but a specific insight triggered their leap into entrepreneurship.

The "why now" moment arrived through an unlikely channel: Chinese tourists in Seoul's Myeongdong district. Kim observed massive lines of Chinese visitors queuing outside Korean cosmetics shops, buying products in bulk to resell back home. Further investigation revealed that Korean skincare tutorials were going viral on Chinese social media platforms, creating unprecedented demand for K-beauty products. Yet most Korean beauty companies were still operating through traditional wholesale models, unable to capitalize directly on this social media-driven demand.

Kim recognized a fundamental mismatch: social media was creating global beauty trends at unprecedented speed, but the industry's distribution and marketing infrastructure remained stuck in the broadcast television era. The convergence of several factors—Korea's advanced cosmetics manufacturing, the global rise of K-beauty, the proliferation of social media, and the emergence of cross-border e-commerce—created a unique window of opportunity.

III. Early Days: Building AprilSkin (2014-2016)

The founding of InnoVentures in 2014 (later renamed APR Corporation) began modestly with borrowed capital and a small team operating out of a cramped office in Seoul's startup district. The company's first product, Magic Stone natural soap, was deliberately simple—a decision driven by both capital constraints and strategic thinking. Soap required minimal R&D investment, had established manufacturing partners, and served as a low-risk entry point into the beauty market.

The AprilSkin brand, launched shortly after the company's founding, embodied Kim's vision of social media-native beauty. Rather than following the traditional path of securing department store placement or celebrity endorsements, AprilSkin went directly to consumers through Facebook, Instagram, and YouTube. The brand's aesthetic—minimalist packaging with Instagram-worthy colors—was designed specifically for social sharing.

Initial traction came through micro-influencer partnerships, a strategy born of necessity given the company's limited marketing budget. Instead of paying for expensive celebrity endorsements, APR identified beauty enthusiasts with 10,000 to 100,000 followers and provided them with free products in exchange for honest reviews. This grassroots approach generated authentic content that resonated with young consumers skeptical of traditional advertising.

The Chinese market initially seemed like AprilSkin's golden opportunity. The brand's hypoallergenic focus addressed a key concern among Chinese consumers worried about product safety following several high-profile cosmetics scandals. Sales through cross-border e-commerce platforms like Tmall Global grew rapidly in 2015, reaching tens of millions of dollars within months.

However, success attracted competition. Chinese manufacturers quickly copied AprilSkin's products and aesthetic, selling knockoffs at a fraction of the price. Local Chinese beauty brands with deeper pockets and better government relationships began squeezing out Korean imports. By late 2016, what had seemed like APR's primary growth market was becoming increasingly difficult to penetrate.

Despite these challenges, 2016 marked a crucial validation point. Facebook selected APR as one of Asia's Most Influential E-Commerce companies, recognizing the company's innovative use of social advertising and direct-to-consumer sales. This recognition brought credibility and opened doors to partnerships with global platforms.

The early period also saw rapid brand proliferation as the company experimented with different market segments. Forment targeted older consumers with anti-aging products. GLAM.D attempted to capture the color cosmetics market. Most ambitiously, NERDY launched as a fashion line, attempting to extend APR's youth culture credibility beyond beauty. This scattershot approach, while generating revenue, diluted focus and stretched resources thin—a problem Kim would soon need to address.

IV. The Medicube Pivot: Finding Product-Market Fit (2016-2020)

The launch of Medicube in 2016 represented a fundamental strategic shift for APR Corporation. Unlike the company's previous brands that chased trends, Medicube focused on solving specific skin problems with clinically-inspired formulations. The brand name itself—combining "medical" and "cube"—signaled a more serious, scientific approach to skincare.

The Red Line, Medicube's first major product line targeting acne-prone skin, became an unexpected hit. The products used ingredients typically found in dermatological treatments but formulated for daily home use. The bright red packaging, initially a risky design choice, became instantly recognizable on social media feeds. Sales exceeded projections by 300% in the first quarter after launch.

Kim's realization about brand focus came during a 2017 trip to Silicon Valley, where he met with successful D2C brands like Glossier and Dollar Shave Club. "To become a global company, one brand needs to become like Apple," Kim told his team upon returning to Seoul. This insight triggered a painful but necessary consolidation. Resources were gradually shifted away from AprilSkin, Forment, and other brands to focus primarily on Medicube.

Building the direct-to-consumer infrastructure required significant investment during this period. APR developed its own e-commerce platform capable of handling everything from payment processing to customer service in multiple languages. The company built a sophisticated logistics network, partnering with fulfillment centers in key markets to enable two-day delivery in major cities across Asia.

The numbers from this period tell a story of steady acceleration. Revenue grew from 98 billion KRW in 2019 to 156 billion KRW in 2020, despite the global pandemic. By 2021, the company hit 259 billion KRW in revenue with 14 billion KRW in operating profit, achieving profitability margins rare for fast-growing D2C brands.

COVID-19, paradoxically, accelerated APR's growth. With physical stores closed and people spending more time on social media, online beauty sales exploded. The "Zoom boom" created new skincare concerns as people stared at their faces on video calls all day. Home beauty treatments became attractive alternatives to closed spas and dermatology clinics. APR was perfectly positioned to capture this demand with its D2C infrastructure and social media marketing expertise.

The period also saw the development of APR's data-driven product development process. By analyzing millions of customer reviews, search trends, and social media conversations, the company could identify unmet needs and develop products with built-in demand. This approach reduced the failure rate of new product launches from the industry average of 80% to less than 30%.

V. The AGE-R Inflection Point: Beauty Devices Revolution (2021-2023)

March 2021 marked the most significant inflection point in APR's history with the launch of the Medicube AGE-R beauty device line. The decision to enter the beauty device market wasn't obvious—it required different expertise, supply chains, and customer support capabilities than cosmetics. But Kim saw devices as the key to differentiation in an increasingly crowded D2C beauty market.

The AGE-R devices were positioned strategically in the 200,000-300,000 KRW price range, expensive enough to convey premium quality but affordable compared to professional treatments or luxury devices from established brands. This pricing sweet spot made the devices accessible to APR's core demographic of millennials and Gen Z consumers while maintaining healthy margins.

The technology stack integrated into AGE-R devices represented genuine innovation. EMS (electrical muscle stimulation) technology helped tone facial muscles. Microcurrent treatments promoted collagen production. LED therapy addressed various skin concerns through different light wavelengths. Electroporation technology enhanced the absorption of skincare products. While none of these technologies were new individually, APR's integration and user-friendly interface made professional-grade treatments accessible for home use.

Sales velocity exceeded all projections. The company sold 600,000 units in 2022, reaching 750,000 units by Q3 2023. But the real genius of the AGE-R strategy lay not in device sales themselves but in the ecosystem they created. Each device required specific Medicube serums and ampoules for optimal results. Customers who bought a device typically purchased 3-4 complementary skincare products, tripling the average order value.

This ecosystem play created what strategists call a "competitive moat." Once customers invested in an AGE-R device, switching to competing brands became economically and psychologically difficult. The devices essentially "locked in" customers to Medicube's skincare lines, creating predictable recurring revenue streams from consumable products.

The October 2023 launch of APR Factory represented another strategic milestone. By bringing manufacturing in-house, APR became the first Korean beauty company to control its entire value chain from R&D to retail. The facility in Osong, equipped with advanced automation and quality control systems, could produce 100 million cosmetic units annually. This vertical integration improved margins, accelerated product development cycles, and ensured quality control—critical factors for competing globally.

The manufacturing capability also enabled rapid iteration and customization. APR could test new formulations in small batches, gather customer feedback, and scale production of successful products within weeks rather than months. This agility proved crucial in the fast-moving social media-driven beauty market where trends could emerge and fade within a single season.

VI. The TikTok Explosion & Global Expansion (2024-Present)

The IPO on February 26, 2024, at 250,000 KRW per share, raised 94.75 billion KRW and marked APR's transition from startup to public company. The timing proved fortuitous, coinciding with a surge in global demand for K-beauty products and the maturation of social commerce platforms. Within months, the stock price doubled as investors recognized the company's unique position at the intersection of beauty, technology, and social media.

APR's mastery of TikTok Shop transformed the platform from a marketing channel into a primary revenue driver. The company became the first K-beauty brand to host a TikTok Shop Super Brand Day in the United States, generating $102.9 million in revenue from a single campaign. This success stemmed from deep understanding of TikTok's algorithm and user behavior, developed through years of experimentation and data analysis.

The "CEOppa" phenomenon exemplified APR's unconventional approach to brand building. Kim Byunghoon's TikTok presence, where he playfully embraced the nickname combining "CEO" and "Oppa" (Korean term of endearment for older brother), humanized the brand in ways traditional corporate communications never could. His videos, showing everything from product development processes to office pranks, accumulated millions of views and created parasocial relationships with customers.

The creator economy strategy proved particularly powerful. APR's international business posted a remarkable 210% year-over-year increase, with overseas revenue accounting for 80% of total sales in Q3 2025. By partnering with over 33,900 creators and offering industry-leading affiliate commissions up to 30%, APR turned influencers into a distributed sales force. Unlike traditional influencer marketing focused on awareness, this approach directly drove conversions through shoppable content.

Geographic expansion accelerated dramatically in 2024-2025. As of September 2025, global cumulative sales of medicube AGE-R at-home beauty devices exceeded 5 million units, with international markets accounting for more than half of device sales. The United States emerged as the largest market, representing 39% of total revenue and surpassing KRW 150 billion in quarterly sales.

The September 2024 milestone of surpassing LG H&H's market capitalization carried symbolic weight beyond financial metrics. LG H&H, with brands like The History of Whoo and Su:m37°, had long represented the pinnacle of Korean beauty success. APR's higher valuation despite lower absolute revenues reflected investor confidence in the company's growth trajectory and business model superiority in the digital age.

VII. Business Model Deep Dive

APR's business model represents a masterclass in modern D2C strategy, combining multiple revenue streams and competitive advantages that traditional beauty companies struggle to replicate. The foundation rests on direct-to-consumer excellence, with the company maintaining over 70% of sales through its own channels for seven consecutive years since founding. This direct relationship provides invaluable data, higher margins, and control over brand experience.

The M-CLUB membership program, launched in 2021, exemplifies sophisticated customer retention strategy. Within 10 months, 80,000 members generated 14 billion KRW in revenue, demonstrating the power of community building in beauty retail. Members receive exclusive product launches, personalized skincare consultations, and access to limited edition devices. The program creates predictable revenue streams while gathering detailed customer preference data.

The product portfolio strategy balances three distinct categories with different economic characteristics. Beauty devices serve as high-AOV anchor purchases that establish customer relationships and create ecosystem lock-in. With average selling prices exceeding 250,000 KRW and gross margins above 70%, devices generate substantial profit per transaction while differentiating APR from pure cosmetics brands.

Cosmetics function as the recurring revenue engine. The cosmetics segment generated KRW 272.3 billion in quarterly revenue, three times higher than the same period last year in Q3 2025. Products like the Zero Pore Pad and PDRN serums require regular repurchase, creating predictable monthly revenue streams. The gross margins on cosmetics, while lower than devices in percentage terms, generate consistent cash flow that funds growth investments.

The fashion and lifestyle extensions through the NERDY brand serve a different purpose: cultural relevance and brand building among younger consumers. While contributing less than 10% of total revenue, NERDY's streetwear aesthetic keeps APR connected to youth culture trends that eventually influence beauty purchases.

The margin structure reveals sophisticated unit economics. Device sales create high initial profit that covers customer acquisition costs. Subsequent cosmetics purchases, with virtually zero additional marketing expense, generate pure profit. This model explains how APR achieved operating profit of KRW 96.1 billion on revenue of KRW 385.9 billion in Q3 2025, representing year-over-year growth of 253% in operating profit.

Marketing efficiency sets APR apart from traditional beauty brands that spend 25-40% of revenue on advertising. By turning customers and influencers into marketing channels through affiliate programs and social sharing, APR achieves similar reach at a fraction of the cost. The founder-as-influencer strategy, with Kim Byunghoon's personal brand amplifying corporate messaging, provides essentially free marketing worth hundreds of millions in equivalent advertising spend.

VIII. Competitive Analysis & Moats

Analyzing APR through Michael Porter's Five Forces framework reveals both strengths and vulnerabilities in the company's competitive position. Supplier power remains low due to APR's vertical integration through the Osong factory, eliminating dependence on contract manufacturers. The company's scale now allows favorable terms with raw material suppliers, though rising ingredient costs pose ongoing challenges.

Buyer power presents a medium threat level. While APR has cultivated strong brand loyalty, particularly among device owners invested in the ecosystem, beauty consumers ultimately maintain low switching costs for cosmetics products. The abundance of alternatives and price transparency through e-commerce platforms empowers consumers to demand value. APR counters this through community building and product innovation that creates emotional switching costs beyond pure economics.

The threat of substitutes ranks high, particularly from professional treatments and competing beauty devices. Dermatology clinics offer more powerful treatments, though at significantly higher prices and inconvenience. Competing device manufacturers from China increasingly offer similar technology at lower price points, though often lacking APR's software integration and cosmetics ecosystem.

New entrants pose a medium threat that's evolving. While the capital requirements for manufacturing facilities and global distribution have risen, creating barriers for startups, established beauty conglomerates possess resources to replicate APR's model. L'Oréal, Estée Lauder, and Shiseido have all launched device lines and strengthened D2C capabilities, though their organizational inertia limits agility.

Competitive rivalry in the beauty industry remains intense, with thousands of brands competing for consumer attention and shelf space. However, APR has carved out a distinct position at the intersection of K-beauty authenticity, device technology, and social commerce mastery that few competitors can triangulate effectively.

Hamilton Helmer's 7 Powers framework provides deeper insight into APR's sustainable competitive advantages. Scale economies manifest in manufacturing, where the Osong factory's automation delivers unit costs below contract manufacturers, and in marketing, where APR's massive social following reduces customer acquisition costs.

Network effects operate through APR's creator ecosystem and social commerce platform. With cumulative revenue for the first three quarters totaling KRW 979.7 billion, more than double last year's figure, the company's scale attracts more creators, which drives more sales, which attracts more creators in a virtuous cycle. The M-CLUB community creates additional network effects as members share experiences and recommendations.

Counter-positioning against traditional beauty brands proves particularly powerful. While incumbents remain wedded to wholesale distribution and traditional marketing, APR built its entire operation around D2C and social media. Attempting to match APR's model would cannibalize existing channel relationships and require organizational transformation that public companies struggle to execute.

Switching costs embedded in the device ecosystem create customer lock-in. Once consumers invest in an AGE-R device and develop routines around Medicube products, switching requires abandoning sunk costs and learning new systems. This dynamic explains the high retention rates among device owners.

Branding power stems from authentic K-beauty heritage combined with Kim Byunghoon's personal brand. The "CEOppa" phenomenon cannot be replicated by hiring influencers or celebrity endorsements—it requires genuine founder involvement that most executives cannot or will not provide.

The cornered resource of K-beauty authenticity provides lasting advantage. While anyone can claim to sell "K-beauty" products, APR's Korean origins, local manufacturing, and cultural fluency create authenticity that international brands cannot match. This matters enormously to global consumers seeking genuine Korean skincare innovation.

Process power emerges from APR's rapid product development and launch capabilities. The company's ability to identify trends through social listening, develop products, and scale distribution in weeks rather than months creates temporal advantages that slower competitors cannot overcome.

IX. Financial Performance & Valuation

APR's financial trajectory from startup to 10.2 trillion KRW market capitalization represents one of the most remarkable value creation stories in Korean business history. The growth acceleration visible in recent quarters suggests the company has reached an inflection point where multiple growth drivers compound simultaneously.

Q3 2025 results showed revenue of KRW 385.9 billion and operating profit of KRW 96.1 billion, representing year-over-year growth of 122% in revenue and 253% in operating profit. This performance exceeded analyst expectations and demonstrated operating leverage as the company scales. The 24.9% operating margin in Q3 2025, despite new U.S. tariff impacts, proves the business model's resilience.

The cumulative nine-month performance for 2025 provides fuller perspective on the company's momentum. Revenue reached KRW 979.7 billion while operating profit hit KRW 235.2 billion, surpassing the KRW 200 billion mark for the first time. The company had already exceeded its total 2024 operating profit by mid-2025, with Q4 results likely to push full-year numbers well above KRW 1 trillion in revenue.

Breaking down revenue composition reveals healthy diversification. The cosmetics segment generated KRW 272.3 billion in Q3 revenue, three times higher than the same period last year, while the beauty device division maintained steady growth with revenue of KRW 103.1 billion, up 39% year-over-year. This balance between high-growth cosmetics and steady device sales creates revenue stability while maintaining explosive growth potential.

Geographic revenue distribution shows successful internationalization. Overseas revenue accounted for 80% of total sales with 210% year-over-year growth, reducing dependence on the Korean market. The United States alone contributed 39% of total revenue, establishing APR as a truly global brand rather than a Korean company with international sales.

The EBITDA margin of 20.06% places APR among the most profitable beauty companies globally, especially remarkable given the growth investments. Traditional beauty conglomerates like L'Oréal and Estée Lauder achieve similar margins but with single-digit growth rates. APR's ability to maintain profitability while growing at triple-digit rates suggests superior unit economics and operational efficiency.

Valuation metrics reflect investor enthusiasm but also raise questions about sustainability. At current prices, APR trades at approximately 35-40x forward earnings, a premium to global beauty peers but perhaps justified by growth rates. The more relevant comparison might be to high-growth technology companies rather than traditional beauty brands, given APR's D2C model and platform characteristics.

The device installed base provides insight into future revenue potential. With 5 million devices sold globally and typical device replacement cycles of 2-3 years, APR has built a renewable revenue stream from device upgrades alone. More importantly, if each device owner purchases just 50,000 KRW of cosmetics monthly, the installed base generates 250 billion KRW in annual recurring revenue.

X. Bear & Bull Cases

The bear case against APR centers on several legitimate risks that could derail the growth story. TikTok regulatory concerns top the list, with potential U.S. bans threatening a platform that drives significant revenue. While APR has diversified across platforms, TikTok's unique algorithm and commerce integration would prove difficult to replace. Any disruption could materially impact growth trajectories.

Beauty device market saturation presents another concern. With 5 million devices sold, APR may be approaching natural ownership limits among target demographics. Replacement cycles of 2-3 years suggest a potential revenue cliff as initial purchase waves subside. Competition from both premium brands and Chinese manufacturers squeezes margins and market share from both directions.

The knockoff threat from China remains persistent and growing. Chinese manufacturers now offer devices with similar specifications at 30-50% lower prices, undermining APR's value proposition. While APR's ecosystem and brand provide some protection, price-sensitive consumers might defect to alternatives, especially during economic downturns.

Fashion and trend risk inherent to beauty cannot be ignored. Consumer preferences shift rapidly, and today's must-have products become tomorrow's forgotten fads. APR's heavy reliance on social media amplifies this risk—viral success can reverse just as quickly. The company's limited product diversification compared to conglomerates provides less cushion against trend shifts.

Key person dependency on founder Kim Byunghoon creates governance and succession concerns. The "CEOppa" brand is inseparable from APR's identity, making leadership transition extraordinarily difficult. Any personal scandal or decision to step back could damage brand equity built over years.

The bull case rests on equally compelling growth drivers. The global home beauty device market's projected 35% CAGR through 2030 suggests APR is surfing a massive secular trend rather than creating temporary demand. Post-pandemic behavioral changes toward self-care and home treatments appear permanent, expanding the addressable market.

Untapped geographic markets offer enormous expansion potential. APR has barely penetrated Europe, the Middle East, Latin America, and Africa—regions representing billions in potential revenue. The company's proven playbook of entering markets through social media and D2C provides a repeatable growth formula.

Platform potential beyond beauty could multiply APR's valuation. The company's mastery of social commerce, creator ecosystems, and D2C operations could extend into adjacent categories like wellness, supplements, or personal care. The infrastructure and capabilities built for beauty translate into platform advantages across consumer categories.

AI and personalization opportunities remain largely unexplored. APR's device sensors generate vast skin data that could enable personalized product recommendations and treatment protocols. This data advantage, combined with AI advancement, could create unprecedented customization that commands premium pricing and loyalty.

Demographic tailwinds from aging populations ensure growing demand for anti-aging solutions. As millennials enter their 40s with greater disposable income and digital nativity than previous generations, APR's target market expands naturally. The convergence of need (aging), means (income), and behavior (online shopping) creates ideal conditions for sustained growth.

XI. Playbook & Lessons

APR's journey from startup to beauty tech giant offers strategic lessons applicable beyond cosmetics. Speed as strategy emerges as perhaps the most crucial insight. By moving faster than incumbents—from product development to market entry—APR turned temporal advantages into permanent market position. The company's weeks-long development cycles versus competitors' years-long processes created compound advantages over time.

The founder-as-product strategy revolutionized beauty marketing. Kim Byunghoon's transformation into "CEOppa" demonstrates how authentic personal branding can eclipse traditional corporate marketing. This approach requires genuine commitment and vulnerability that most executives avoid but generates trust and engagement that money cannot buy.

Platform thinking transformed devices from products into ecosystems. APR recognized that hardware sales were merely customer acquisition events that enabled recurring consumables revenue. This insight—seeing devices as platforms rather than endpoints—fundamentally changed unit economics and competitive dynamics.

The social-native approach differentiated APR from competitors who adapted to social media rather than building for it. Every decision from product design to packaging to messaging assumed social sharing as the primary distribution mechanism. This native understanding versus retrofitted adaptation created authentic engagement that resonated with digital-native consumers.

Vertical integration timing proved crucial. APR resisted manufacturing ownership until achieving sufficient scale to justify investment. The October 2023 factory launch came precisely when volumes supported automation and market position justified capital deployment. Earlier integration would have drained resources; later would have constrained growth.

The focus paradox—expanding then consolidating brands—illustrates portfolio strategy complexity. APR's initial multi-brand approach generated learning and revenue but ultimately diluted resources. The painful consolidation around Medicube, while sacrificing short-term revenue, created the focused momentum necessary for global breakthrough.

XII. Epilogue: What's Next?

APR Corporation stands at a fascinating juncture as 2025 draws to a close. Having already exceeded its total 2024 operating profit of KRW 122.7 billion by the first half of 2025, with cumulative operating profit reaching KRW 235.2 billion through Q3, the company has definitively entered a new phase of its evolution. The question is no longer whether APR can compete with beauty giants but whether it can redefine the industry itself.

AI-powered skin diagnostics represent the next frontier. APR's millions of device users generate continuous skin data through sensors and imaging, creating an unprecedented dataset for machine learning applications. The company's recent partnerships with AI research institutions suggest imminent launches of personalized skincare protocols that adapt in real-time to skin conditions, environmental factors, and treatment responses.

Global expansion priorities are crystallizing around three core markets: Japan, where Medicube has already achieved number-one rankings in multiple categories; Europe, where K-beauty enthusiasm meets high disposable income; and the Middle East, where luxury beauty spending per capita exceeds all other regions. Each market requires localized strategies, but APR's platform approach provides the flexibility to adapt while maintaining core brand identity.

New device categories under development promise to extend beyond facial care into body treatments, hair care, and wellness monitoring. The company's R&D investments have tripled year-over-year, suggesting multiple product launches in the pipeline. Patents filed in 2024-2025 indicate developments in ultrasonic technology, AI-powered skin analysis, and novel ingredient delivery systems.

Platform ambitions increasingly point toward APR becoming a beauty technology infrastructure provider rather than merely a brand owner. The company's D2C platform, creator network, and fulfillment capabilities could serve other brands, transforming APR into the "Shopify of beauty." This platform pivot would multiply valuation multiples from beauty industry norms toward technology platform premiums.

The ultimate question—can APR become the "Apple of Beauty"—depends on sustained innovation and ecosystem expansion. Apple's genius lay not in any single product but in creating an integrated ecosystem that locked in customers while continuously expanding use cases. APR's device-cosmetics ecosystem follows similar logic but requires constant innovation to maintain relevance.

The broader implications for K-beauty and beauty-tech convergence extend beyond APR's individual success. The company has proven that Korean beauty innovation can compete globally not through traditional channels but by leveraging technology and social media to bypass gatekeepers. This model democratizes beauty entrepreneurship and accelerates innovation cycles industry-wide.

As traditional beauty conglomerates scramble to replicate APR's model, the company's first-mover advantages in social commerce and beauty tech become increasingly valuable. The expertise, data, and relationships built over a decade cannot be quickly replicated through acquisition or investment. APR has fundamentally changed how beauty brands are built, marketed, and scaled in the digital age.

The financial markets have recognized this transformation. With the stock trading at 272,500 KRW and a market capitalization of 10.2 trillion KRW, APR has achieved valuations that seemed impossible for a Korean beauty startup just years ago. Yet given the company's growth trajectory, global expansion potential, and platform opportunities, current valuations may prove conservative in hindsight.

APR Corporation's story demonstrates that industry disruption often comes not from doing existing things better but from recognizing when fundamental assumptions no longer apply. The assumption that beauty brands required decades to build, celebrity endorsements to succeed, and department store placement to achieve prestige all proved false. By questioning these assumptions and building for a social media-native, direct-to-consumer, technology-enabled future, APR created a new template for consumer brand success.

The next chapter of APR's journey will test whether the company can maintain its innovative edge while scaling into a global corporation. Success requires balancing the agility and authenticity that drove initial success with the operational excellence and governance that public markets demand. If APR can navigate this transition while maintaining its core strengths—speed, social media mastery, and technology integration—the company could indeed become not just the Apple of Beauty but a defining company of the global consumer industry's digital transformation.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube