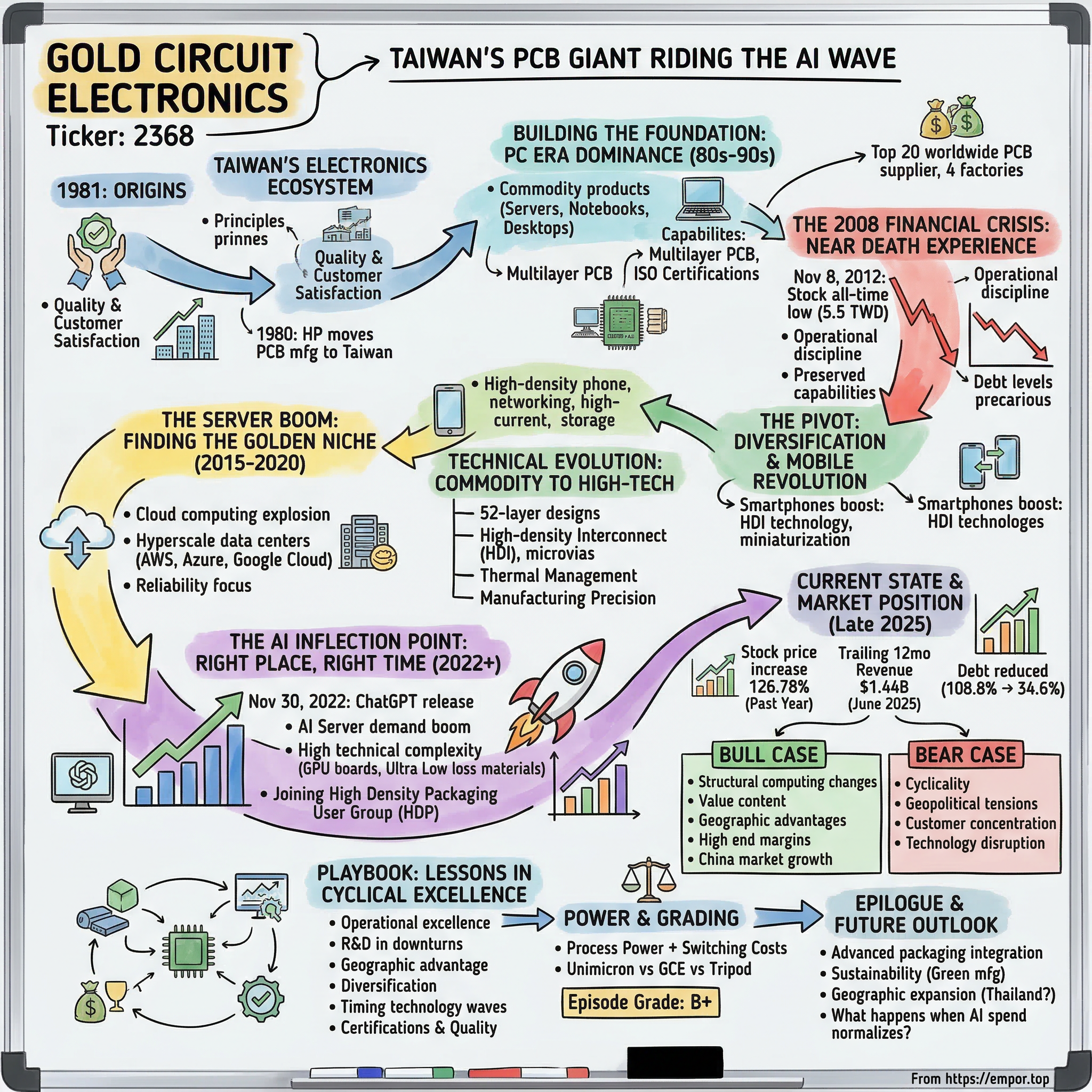

Gold Circuit Electronics: Taiwan's PCB Giant Riding the AI Wave

I. Introduction & Cold Open

Picture Taoyuan City on a humid November morning in 2012. Inside the headquarters of Gold Circuit Electronics, executives stared at computer screens showing a stock price that had just touched 5.5 TWD—the lowest point in the company's three-decade history. The all-time low was reached on November 8, 2012, a painful reminder of how far the company had fallen in the aftermath of the global financial crisis. The electronics industry was in shambles, demand had evaporated, and many wondered if this Taiwanese PCB manufacturer would survive.

Fast forward to August 2025: that same stock trades above 400 TWD, delivering a 126.78% increase over the past year. The transformation is nothing short of remarkable. How did a commodity PCB maker founded in 1981 position itself to become one of the critical enablers of the artificial intelligence revolution?

The answer lies not in a single pivot or lucky break, but in a series of calculated risks, operational discipline during the darkest hours, and an uncanny ability to sense where the technology puck was heading. This is the story of Gold Circuit Electronics (GCE)—a company that survived near-death to emerge as a key supplier in the AI infrastructure gold rush.

II. Origins & Taiwan's Electronics Ecosystem

GCE was established in 1981, born into the heart of Taiwan's electronics manufacturing boom. The early 1980s marked a pivotal moment for the island nation—a transition from agricultural economy to technology powerhouse was underway, and printed circuit boards were the foundation upon which this transformation would be built.

Quality and Customer Satisfaction became the company's key principles from day one—not mere corporate slogans but operational imperatives in an industry where a single defective board could torpedo client relationships. The founders understood that Taiwan's geographic disadvantage—an island far from major markets—could only be overcome through relentless focus on reliability.

Taiwan's PCB industry didn't emerge in isolation. The industry began to take root in 1969 with Ampex establishing a plant, during Taiwan's export expansion period when the government actively promoted policies and incentives attracting foreign investment through stable social environment, low-cost labor, and lenient environmental policies. As foreign investment poured in, a supply chain gradually developed and formed a thriving industry chain.

The real accelerant came in 1980. HP moved its PCB manufacturing to Taiwan and invited Nan Ya Plastics to become a partner, planting the seeds for Taiwan's current position in the tech industry. This partnership model—foreign technology married to local manufacturing excellence—would become the template for Taiwan's rise.

By the time GCE was founded, Taiwan was rapidly evolving into what would become the world's highest market share holder at 31.3%, followed by China at 23% and Japan at 19.1% as the third largest. The company wasn't just riding a wave; it was part of the tsunami that would reshape global electronics manufacturing.

III. Building the Foundation: PC Era Dominance

The personal computer revolution of the 1980s and 1990s provided GCE with its first major growth engine. In the past, the company's focus had been on computer-related products including servers, workstations, notebook personal computers and desktop personal computers. This wasn't glamorous work—manufacturing PCBs for computers was already becoming commoditized—but it taught the company invaluable lessons about scale, efficiency, and the relentless pace of technology evolution.

The company was headquartered in Taoyuan City, Taiwan, strategically positioned in what would become Taiwan's PCB manufacturing hub. Taoyuan wasn't chosen by accident—the region offered proximity to component suppliers, access to skilled labor from nearby technical universities, and critically, direct shipping routes to global markets.

During these formative decades, GCE developed capabilities in multilayer PCB production, mastering the art of creating boards with increasing complexity. The company's facilities are certified to ISO 9001, ISO 14001, ISO 45001, IATF 16949, IECQ QC 080000, ISO 27001, ISO 14064, and ISO 50001—each certification representing not just compliance, but a systematic approach to quality that would prove crucial when the company later pursued higher-margin opportunities.

The relationship building during the PC era laid groundwork that would pay dividends decades later. OEMs learned to trust GCE's consistency. When a Dell or HP needed millions of motherboards manufactured to exact specifications, delivered on time, every time, GCE was there. These weren't sexy products that made headlines, but they generated the cash flow and operational expertise that would enable the company to survive the storms ahead.

By the early 2000s, GCE had established itself as a reliable, if unremarkable, player in the global PCB ecosystem. The company had grown to become a Top 20 worldwide printed circuit board supplier with 4 factories, one in Taiwan, three in China. The geographic expansion into China was both opportunity and necessity—following customers who were themselves chasing lower costs. But this commodity path was about to hit a wall.

IV. The 2008 Financial Crisis: Near Death Experience

The global financial crisis that erupted in 2008 was particularly brutal for electronics manufacturers. Consumer spending collapsed, enterprise IT budgets evaporated, and suddenly the world needed far fewer printed circuit boards. For a company like GCE, operating in a capital-intensive industry with high fixed costs, the downturn was existential.

The numbers tell a story of near-catastrophe. While the crisis peaked in 2008-2009, its aftershocks continued reverberating through the electronics industry for years. GCE's stock reached its all-time low of 5.5 TWD on November 8, 2012—a staggering decline that reflected not just temporary market pessimism but genuine questions about the company's survival.

What happened inside GCE during these dark years reveals the character of the organization. While competitors slashed R&D budgets and shuttered facilities, GCE's management made a counterintuitive decision: maintain technological capabilities at all costs. Engineers who might have been laid off elsewhere were retained. Equipment upgrades that seemed foolish given the market conditions were quietly executed. The betting was simple—when demand returned, and it always did in cyclical industries, GCE would be ready with better technology than competitors who had retreated.

The operational discipline required was extraordinary. Every expense was scrutinized. Non-essential spending vanished. Travel budgets disappeared. But the core—the ability to manufacture increasingly complex boards with high reliability—was protected like a vital organ.

Debt levels during this period painted a precarious picture. Looking at the company's leverage journey, we see that at various points, the burden was crushing. The company's debt to equity ratio has reduced from 108.8% to 34.6% over the past 5 years, but those five years don't capture the full story of the crisis period when leverage was even higher and survival was measured in quarters, not years.

The crisis forced a reckoning. The comfortable position as a commodity PC board supplier was no longer tenable. Margins were disappearing. Chinese competitors with lower cost structures were attacking from below. Japanese competitors with superior technology owned the high end. GCE was caught in the middle—the worst place to be in manufacturing. Something had to change.

V. The Pivot: Diversification & Mobile Revolution

Coming out of the crisis, GCE's leadership recognized that survival required transformation. The company couldn't compete on cost alone against Chinese manufacturers, nor could it match the technological sophistication of Japanese players like Ibiden. The strategy that emerged was pragmatic: diversify within core competencies while gradually moving up the technology curve.

Over the past several years the company diversified into additional markets including telecommunications, networking, cell phones, high-current power supplies, storage, and many other exciting fields. This wasn't random expansion—each new market was carefully chosen based on GCE's existing capabilities and relationships.

The smartphone boom of 2010-2015 provided the first validation of this strategy. As Apple's iPhone and Android devices exploded in popularity, demand for high-density interconnect (HDI) boards surged. These weren't the simple PCBs of the PC era. Smartphone boards required precise miniaturization, multiple layers, and zero tolerance for defects. The R&D investments preserved during the crisis suddenly looked prescient.

The company specialized in notebook/netbook, high density phone/consumer electronics, server, network, telecom, backplane applications, building expertise across multiple demanding sectors. Each market taught different lessons. Telecom equipment required boards that could handle high-frequency signals. Servers demanded thermal management capabilities. Smartphones needed extreme miniaturization.

The mobile revolution also forced GCE to accelerate its technology development. Gold Circuit Electronics was originally a company focusing on consumer electronics such as notebook computers, mobile phones, and displays. In light of the prices getting more and more competitive and the lack of powerful financial support or subsidies from the government, however, the company decided to innovate and change and it helped survive in the red ocean.

By 2015, the transformation was bearing fruit. Revenue was recovering, margins were improving, and most importantly, GCE was no longer purely a commodity player. The company had successfully diversified its customer base and product portfolio. But the real opportunity was yet to come.

VI. Technical Evolution: From Commodity to High-Tech

The technical capabilities GCE developed during its diversification phase deserve deeper examination, as they would prove crucial for capturing the AI opportunity later. The evolution from simple four-layer boards to complex 52-layer designs with HDI technology represented not just incremental improvement but fundamental reimagination of what a PCB could be.

The company's manufacturing facilities are certified to ISO 14001, and will be continuously working on compliance with international standard for environmental management systems. But certifications only tell part of the story. The real transformation happened on the factory floor, where engineers pushed the boundaries of what was possible with copper, fiberglass, and increasingly exotic materials.

High-density interconnect technology became a core competency. Unlike traditional PCBs where connections between layers used mechanical drilling, HDI boards employed laser-drilled microvias—holes so small they were invisible to the naked eye. This technology enabled the component density required for modern electronics where every millimeter mattered.

The company also mastered thermal management—a critical capability as processors became more powerful and generated more heat. Advanced materials like low-loss dielectrics and thermally conductive substrates were incorporated into designs. What seemed like esoteric technical capabilities would later prove essential for AI server applications where GPUs could consume 700 watts of power.

Manufacturing precision reached new levels. Line widths shrank to less than 50 microns. Registration accuracy between layers was measured in tens of microns. Yield rates on complex boards—the percentage that passed final testing—became a key competitive differentiator. Where competitors might achieve 70% yields on 20-layer boards, GCE pushed toward 90% through obsessive process control.

The investment in advanced manufacturing wasn't cheap. New equipment for laser drilling, automated optical inspection, and precision plating ran into millions of dollars. But each capability added became a barrier to competition. By 2020, GCE had quietly transformed from a commodity manufacturer into a sophisticated technology company that happened to make circuit boards.

VII. The Server Boom: Finding the Golden Niche

The period from 2015 to 2020 marked GCE's strategic shift toward enterprise computing, a move that would position the company perfectly for the AI revolution. While consumer electronics grabbed headlines, the unglamorous world of server PCBs offered better margins, longer product cycles, and deeper customer relationships.

Server boards were different beasts entirely. Where a smartphone PCB might be 10 layers and the size of a credit card, server motherboards could span 20+ layers and measure over a foot across. The complexity was orders of magnitude higher. Signal integrity at multi-gigabit speeds, power delivery for processors consuming hundreds of watts, and reliability requirements measured in years of continuous operation—these were the new challenges GCE embraced.

The timing was fortuitous. Cloud computing was exploding, driving hyperscale data center construction worldwide. Amazon Web Services, Microsoft Azure, and Google Cloud Platform were in an arms race, each building massive facilities filled with hundreds of thousands of servers. Every one of those servers needed multiple PCBs—motherboards, backplanes, power distribution boards.

COVID-19, arriving in early 2020, accelerated digital transformation by years. Video conferencing, streaming, e-commerce, remote work—suddenly the entire global economy ran on data centers. Server demand spiked, and GCE was ready with capacity and capabilities honed over the previous decade.

The relationships built during this period would prove invaluable. When hyperscalers needed a supplier who could handle sophisticated designs, maintain quality at massive scale, and actually deliver on aggressive timelines, GCE's name kept coming up. Trust, in the B2B world, is earned in decades and lost in moments. GCE had earned it.

Margins in server boards were structurally better than consumer electronics. Product lifecycles stretched to 3-5 years versus 12-18 months for smartphones. Customers valued reliability over rock-bottom pricing. The competitive landscape was less crowded—not every PCB manufacturer could handle the complexity. GCE had found its niche, though nobody yet realized just how golden it would become.

VIII. The AI Inflection Point: Right Place, Right Time

November 30, 2022: OpenAI releases ChatGPT to the public. Within five days, one million users. Within two months, 100 million. The world suddenly understood what artificial intelligence could do, and more importantly, what infrastructure it would require. For GCE, positioned in the server PCB market with advanced technical capabilities, the timing couldn't have been better.

According to market sources, GCE is expected to see orders for AI servers generate 3-4% of revenue in 2023, with the proportion set to rise to a double-digit figure in 2024. These projections, made in August 2023, would prove conservative. The AI boom wasn't just another technology cycle—it was a fundamental reimagining of computing architecture.

The numbers tell a story of explosive growth. GCE expects its AI server boards' share in overall server board shipments to rise from a low single-digit percentage in the first half of 2023 to a mid-to-high single-digit one in the fourth quarter. But understanding why AI servers transformed GCE's business requires examining the technology itself.

AI servers are fundamentally different from traditional servers. Where a standard server might have one or two CPUs and basic cooling, an AI server like NVIDIA's DGX H100 contains eight GPUs, each consuming up to 700 watts, connected through complex high-speed interconnects. The PCB requirements are staggering: GPU boards, including GPU boards, NV Switch, OAM (OCP Accelerator Module), and UBB (Unit Baseboard), account for around 79% of the total AI server PCB value.

In February 2024, Gold Circuit Electronics became a member of the High Density Packaging User Group (HDP), with the company described as "a top 25 printed circuit board manufacturer with top Fortune 100 OEM customers in the server, AI, data center, cloud, storage, switch, router, base station, telecom, automotive, industrial and medical markets". This wasn't just joining another industry association—HDP membership signaled GCE's arrival in the highest tier of PCB technology.

The technical requirements for AI server PCBs pushed GCE's capabilities to their limits. OAM boards, UBB boards, and CPU motherboards with large value in AI servers are expected to bring a market increase of US$1 billion in 2024. These boards required ultra-low loss materials, 20-30 layer counts, and HDI technology throughout. The AI Server motherboard, GPU OAM accelerator module, and GPU UBB motherboard required for AI Server all require at least Ultra Low loss or Very Low loss grade copper foil substrate materials.

The competitive dynamics in AI server PCBs favored established players with proven capabilities. Since AI servers require multiple card interconnections with more extensive and denser wiring compared to general servers, and AI GPUs have more pins and an increased number of memory chips, GPU board assemblies may reach 20 layers or more. With the increase in the number of layers, the yield rate decreases. This complexity created a moat—new entrants couldn't simply build capacity and compete.

By late 2024, GCE's transformation was complete. In 2024, Gold Circuit Electronics's revenue was 38.95 billion TWD, an increase of 29.65% compared to the previous year's 30.04 billion. Earnings were 5.62 billion TWD, an increase of 59.15%. The margin expansion—earnings growing nearly twice as fast as revenue—revealed the power of the AI server opportunity.

IX. Current State & Market Position

As we sit here in late October 2025, Gold Circuit Electronics has emerged as one of the clear winners in the AI infrastructure boom. The trailing twelve month revenue for Gold Circuit Electronics is $1.44B as of June 2025. Gold Circuit Electronics has 8,831 total employees, each one part of an organization that has successfully navigated one of the most dramatic transformations in electronics manufacturing history.

The stock market has recognized this transformation. The stock price has increased 126.78% over the past year, dramatically outperforming both the broader market and industry peers. The stock has fluctuated within a 52-week range spanning from 142.50 to 514.00 TWD, with the upper bound representing nearly 100x the crisis-era lows.

Looking at the company's operations today reveals a fundamentally different organization than existed even five years ago. GCE operates as a Top 20 worldwide printed circuit board supplier with 4 factories, but these facilities now produce some of the most sophisticated PCBs in the industry. The product mix has shifted dramatically upmarket, with AI server boards, HDI smartphone boards, and advanced automotive PCBs dominating production.

Financial metrics tell a story of operational excellence. The debt to equity ratio has reduced from 108.8% to 34.6% over the past 5 years, representing both deleveraging and equity value creation. The company's debt is well covered by operating cash flow at 81.4%, providing financial flexibility for continued investment.

The customer concentration that might concern some investors actually represents competitive advantage. When hyperscalers like Microsoft, Amazon, and Google need PCBs for their most critical AI infrastructure, they turn to a handful of suppliers who can meet their exacting requirements. GCE has earned its place in that elite group.

Industry dynamics continue to favor GCE's positioning. Looking ahead to 2024, China's PCB industry is expected to grow rapidly to $26.79 billion, with a 16.6% annual growth rate, raising its global market share to 32.8%. The rising demand for AI servers and automotive electronics, driven by AI applications and the EV boom, has become a key growth driver. As one of Taiwan's leading PCB manufacturers, GCE benefits from both regional growth and the "China plus one" strategies of global customers seeking supply chain diversification.

The transformation in margin structure reveals the power of the product mix shift. Where commodity PC motherboards might generate gross margins in the mid-teens, AI server boards command margins north of 30%. The increased complexity, higher material costs, and limited supplier base all contribute to this margin expansion. It's a classic case of value migration—from simple to complex, from commodity to specialty, from low-touch to high-service.

X. Playbook: Lessons in Cyclical Excellence

Lesson 1: Surviving commodity cycles through operational excellence GCE's journey demonstrates that commodity manufacturers can escape the commodity trap, but only through relentless operational discipline. During the good times, the company invested in capabilities. During downturns, it preserved those capabilities even at great cost. This counter-cyclical investment strategy created competitive advantages when markets recovered.

Lesson 2: R&D investment during downturns pays off in technology transitions The decision to maintain R&D spending during the 2008-2012 crisis seemed foolish at the time. But when smartphones needed HDI boards and AI servers required ultra-low loss materials, GCE had the capabilities ready. Technology transitions are discontinuous—you can't catch up after they've started.

Lesson 3: Geographic advantage—being in the right ecosystem matters Taiwan's PCB ecosystem provided advantages no single company could replicate. Component suppliers, equipment vendors, technical talent, customer proximity—these ecosystem benefits compounded over decades. GCE's success is inseparable from Taiwan's broader electronics manufacturing excellence.

Lesson 4: Diversification within core competency GCE didn't try to become a semiconductor company or a systems integrator. It remained a PCB manufacturer but diversified across end markets, technologies, and customer segments. This focused diversification reduced risk while leveraging existing capabilities.

Lesson 5: Timing technology waves The progression from PC to mobile to cloud to AI wasn't luck—it was pattern recognition. Each wave built on the previous one. Companies that survived one transition developed the sensors to detect the next. GCE's leadership learned to spot weak signals and position accordingly.

Lesson 6: The importance of certifications and quality in B2B markets In consumer markets, brand and marketing matter. In B2B manufacturing, certifications and track records are everything. Every ISO certification GCE obtained, every quarter of on-time delivery, every reliability test passed—these accumulated into an unassailable reputation that became the company's greatest asset.

XI. Bear Case vs. Bull Case

Bear Case:

The bear case for GCE starts with the fundamental cyclicality of the electronics industry. AI server demand, while explosive today, won't grow exponentially forever. When hyperscalers eventually overbuild capacity—and they always do—the correction could be severe. GCE's increasing exposure to this segment, while profitable now, concentrates risk.

Geopolitical tensions represent an existential threat. Taiwan's unique position in global electronics manufacturing is both blessing and curse. Any escalation in cross-strait tensions could disrupt operations, freeze customer relationships, or worse. The "China plus one" strategies that benefit GCE today could accelerate if customers perceive Taiwan risk as unacceptable.

Customer concentration is a double-edged sword. When a handful of hyperscalers drive the majority of AI server demand, their purchasing decisions can make or break suppliers. If Microsoft or Google decided to dual-source more aggressively or bring PCB manufacturing in-house (unlikely but not impossible), GCE's growth story would unravel quickly.

Technology disruption looms on the horizon. Advanced packaging technologies like chiplets and 3D integration could reduce PCB complexity. If more functionality moves into the package rather than onto the board, traditional PCB manufacturers could see their value proposition erode. The industry has survived many predicted obsolescence events, but eventually, one might stick.

Bull Case:

The bull case rests on structural changes in computing architecture that favor GCE for years to come. In 2023, AI servers accounted for around 8% of total server shipments, and by 2024, this figure is expected to rise to 12.1%. This penetration has much further to run as AI capabilities become table stakes for all computing applications.

The value content argument is compelling. AI server PCBs command 5-6 times the value of traditional server boards. Even if unit growth moderates, revenue can expand dramatically through mix shift. As AI models become more complex, requiring more powerful hardware, PCB content per server should continue increasing.

GCE's position among Taiwan's PCB manufacturers provides strategic advantages. Taiwan's ecosystem depth, technical talent, and manufacturing expertise create barriers that new entrants—whether in Southeast Asia or elsewhere—will take decades to replicate. The company benefits from both regional strength and company-specific capabilities.

Limited competition at the high end supports margins. The technological barriers of AI servers are rising, leading to a decrease in the number of suppliers. Not every PCB manufacturer can produce 20+ layer boards with ultra-low loss materials and achieve acceptable yields. This capability moat should protect margins even as the market matures.

The China PCB market growth provides additional tailwind. China's PCB industry is expected to grow to $26.79 billion in 2024 with an annual growth rate of 16.6%, driven by both AI servers and electric vehicles. While GCE is Taiwan-based, it benefits from regional growth and serves many of the same end markets.

XII. Power & Grading

What type of power: Process Power + Switching Costs

GCE's power derives from two sources that reinforce each other. Process Power comes from the company's ability to manufacture highly complex PCBs with industry-leading yields. This isn't easily replicable—it requires years of accumulated knowledge, specialized equipment, and trained operators. When yields on 20-layer AI server boards can vary by 20 percentage points between manufacturers, process excellence becomes a sustainable competitive advantage.

Switching Costs compound this advantage. When a hyperscaler qualifies a PCB supplier for AI servers, the process takes months. Design files must be transferred, prototypes validated, reliability testing completed, and production ramped. Once qualified, customers are reluctant to switch for marginal cost savings. The risk of quality issues or supply disruptions far outweighs potential savings.

Market position among Taiwan PCB manufacturers places GCE in the sweet spot—large enough to handle hyperscale volumes but focused enough to provide superior service. Compared to Unimicron (the largest), GCE is more nimble. Compared to smaller players, it has better scale economies. This goldilocks positioning has served the company well.

The comparison to peers is revealing. Unimicron generates higher revenues but spreads across more segments, diluting focus. Tripod has similar capabilities but less AI server exposure. Zhen Ding dominates flexible PCBs but has less presence in rigid server boards. GCE's focused excellence in high-complexity rigid boards for servers creates a defensible niche.

Episode Grade: B+

GCE earns a B+ for exceptional execution in a cyclical industry and successful positioning for the AI wave. The company transformed from near-bankruptcy to AI infrastructure supplier through operational discipline, strategic focus, and fortunate timing. Points are deducted for geographic concentration risk and customer dependency, but overall this is a remarkable business transformation story.

The grade reflects both achievement and remaining challenges. GCE has successfully navigated one of the most difficult transformations in manufacturing—from commodity to specialty, from survival to prosperity. But geographic risks remain unhedged, and the AI boom won't last forever. A truly great business would have more diversification and less cyclical exposure. Still, for a company that nearly died in 2012, today's position is nothing short of extraordinary.

XIII. Epilogue & Future Outlook

The next frontier for Gold Circuit Electronics likely lies in advanced packaging integration. As semiconductors approach physical limits, more innovation is happening at the package and board level. Technologies like embedded components, substrate-like PCBs, and advanced materials represent growth opportunities. GCE's technical capabilities position it well for this evolution.

Sustainability initiatives are becoming table stakes in electronics manufacturing. As a leading global printed circuit board manufacturer, GCE is committed to responsible environmental practices supporting green manufacturing objectives of customers. Environmental compliance, particularly in Europe and North America, will require continued investment but also creates barriers for less sophisticated competitors.

Geographic expansion beyond Taiwan seems inevitable but fraught with challenges. Thailand has emerged as the preferred destination for Taiwanese PCB manufacturers seeking supply chain diversification. Whether GCE follows this path or doubles down on Taiwan excellence remains to be seen. Each strategy has merits and risks.

The critical question is what happens when AI infrastructure spending normalizes. History suggests it will—every technology boom eventually moderates. But AI might be different. If artificial general intelligence emerges, if AI becomes embedded in every device and application, if the intelligence revolution proves as transformative as optimists believe, then we're still in the early innings. GCE is betting its future on this continued growth.

Final thought: Sometimes the best technology companies aren't the sexy consumer brands or cutting-edge semiconductor designers, but the picks-and-shovels suppliers that enable every revolution. Gold Circuit Electronics exemplifies this principle. While OpenAI and NVIDIA capture headlines, companies like GCE quietly manufacture the physical infrastructure that makes the AI revolution possible. In technology investing, boring can be beautiful, especially when boring comes with 126% annual returns.

The story of Gold Circuit Electronics is far from over. The company that survived near-death in 2012 now stands at the forefront of the AI infrastructure boom. Whether it can navigate the next crisis—and there will be one—while positioning for the next technology wave will determine if GCE becomes a truly great company or merely a good one that happened to catch lightning in a bottle. For now, the Taiwanese PCB manufacturer that nobody outside the industry has heard of continues its quiet march upward, one circuit board at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube