Delta Electronics: The Power Behind the AI Revolution

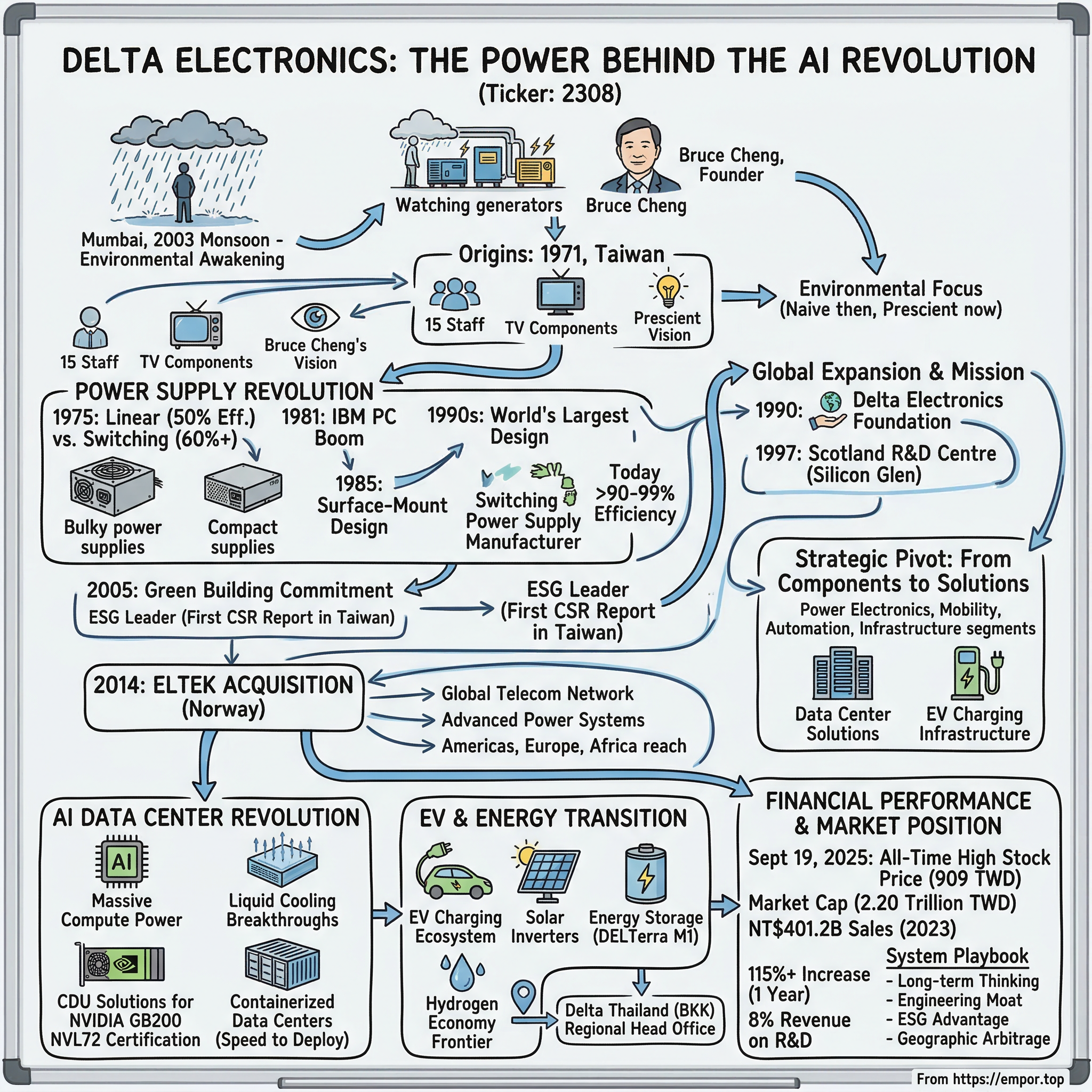

Rainwater cascaded down the streets of Mumbai during the 2003 monsoon season, creating rivers where roads once stood. Through the downpour, Bruce Cheng watched from his car as the urban landscape transformed into a waterlogged maze of vehicles, pedestrians, and the ubiquitous auto-rickshaws that define India's streets. But it wasn't the chaos that caught his attention—it was the resilience. Street vendors continued hawking their wares under makeshift plastic coverings, their portable generators humming away, inefficiently burning through precious fuel just to keep a few light bulbs glowing. The energy waste was staggering.

This moment crystallized something that had been gnawing at Cheng since his days as a young engineer in Tennessee, where he'd witnessed firsthand how American factories meticulously treated their wastewater, a stark contrast to the environmental degradation he'd seen across Asia's industrial boom. Now, watching those generators sputter in the Mumbai rain, the founder of Delta Electronics saw not just inefficiency, but opportunity—the same kind of opportunity that had driven him to build what would become the world's largest switching power supply manufacturer.

Today, as the AI revolution reshapes the global economy, that same company stands at the epicenter of one of technology's most critical challenges: powering and cooling the massive computational infrastructure required for artificial intelligence. Delta reached its all-time high on September 19, 2025, with a price of 909 TWD, pushing its market capitalization to 2.20 trillion TWD. The company that once made TV components now holds certification for in-rack CDU solutions for NVIDIA GB200 NVL72, positioning it as the critical infrastructure provider for the AI age.

How did a Taiwanese component maker founded with 15 employees become the power behind companies like Apple and Tesla? The answer lies in a half-century pursuit of efficiency that seemed quixotic when energy was cheap, prescient when climate change became undeniable, and now essential as AI data centers push the boundaries of power and thermal management. This is the story of how Delta Electronics built an empire on the simple premise that wasting less energy could be both good business and good for the planet—a premise that now makes it indispensable to the artificial intelligence revolution.

Origins: Bruce Cheng's Environmental Awakening

The Tennessee Valley Authority's Wilson Dam stretched before young Bruce Cheng in 1969, its turbines converting the Tennessee River's flow into electricity with remarkable efficiency. But what truly captivated the Taiwanese engineer wasn't the dam itself—it was what happened to the water afterward. Inspired by his first job in the USA, where he witnessed how they collected and treated wastewater, Cheng was determined to do what he could to preserve the environment. The meticulous processes, the careful monitoring, the respect for resources—it all stood in sharp contrast to the industrial practices he'd witnessed across Asia.

Returning to Taiwan in 1971, Cheng saw a different reality. The island nation was riding the wave of its economic miracle, transforming from an agricultural backwater to a manufacturing powerhouse. Factories sprouted like bamboo after rain, churning out electronics for Western consumers. But with this growth came environmental devastation: rivers ran black with industrial waste, the air hung thick with smog, and energy—mostly imported and expensive—was consumed with abandon.

With just 15 staff members, Cheng founded Delta Electronics in 1971 in a modest facility in Taipei's Xinzhuang district. Delta Electronics was founded as a manufacturer of TV deflection coils, electronic components and winding magnetic components. The founding vision seemed almost contradictory for its time: build a profitable electronics business while minimizing environmental impact. In an era when "pollution was the smell of money," as the saying went in Taiwan's industrial zones, Cheng's environmental focus was seen as naive at best, foolish at worst.

The company's early employees remember Cheng as an unusual boss. While other factory owners focused solely on output and margins, Cheng would spend hours on the factory floor, not just checking quality but obsessing over energy consumption. He'd question why certain machines ran continuously when they could be cycled. He'd challenge engineers to find ways to reduce material waste, even when materials were cheap. "Every wasted watt is money thrown away," he would say, though few understood why he cared so much when electricity was subsidized by the government.

Taiwan's broader context made Delta's founding both challenging and opportune. The island had recently lost its United Nations seat to mainland China in 1971, the same year Delta was established. This diplomatic isolation forced Taiwan to become economically indispensable, driving a relentless focus on manufacturing excellence and export competitiveness. The government's industrial policy favored electronics assembly, providing tax incentives and establishing export processing zones. But environmental protection? That was barely an afterthought.

Cheng's environmental consciousness wasn't just philosophical—it was deeply personal. Cheng's fascination with the natural world was kindled at a young age. As a curious child, he gazed up at the night sky, enamoured with the vast array of stars. This childhood wonder at nature's grandeur would later manifest as a determination to protect it, even as he built an industrial empire.

The paradox of Delta's founding mission—environmental protection through electronics manufacturing—would define everything that came after. While competitors chased volume and margins, Delta quietly invested in research that seemed pointless to outsiders: How could they make power supplies that wasted less energy as heat? How could they reduce the materials needed without compromising quality? These questions, born from Cheng's time in Tennessee and his love for the natural world, would prove prophetic as the world awakened to the costs of inefficiency.

The Power Supply Revolution

Inside Delta's cramped Taipei laboratory in 1975, the temperature regularly soared above 35°C, not from Taiwan's subtropical climate but from the heat radiating off traditional linear power supplies. These bulky transformers, made of silicon steel sheets, converted AC power to DC with all the elegance of a sledgehammer—and about 50% efficiency. The other half of the energy? Pure waste heat, enough to cook an egg on the transformer casing.

Bruce Cheng stood before his engineering team with a simple challenge: "If we lose half our energy to heat, we're really selling hot air, not power supplies." The room fell silent. In 1975, nobody cared about efficiency. Electricity was cheap, cooling was someone else's problem, and customers only cared that their TVs and radios worked. But Cheng saw what others missed: every percentage point of efficiency gained was a competitive advantage waiting to be claimed.

Power supplies were the key to Delta's substantial growth in the 1980s. At that time, most transformers were large, heavy and had efficiencies of only 50% (or even lower!). The switching power supplies developed by Delta were not only lightweight but also thin and compact, with a superior efficiency of at least 60% or more. This wasn't just incremental improvement—it was a paradigm shift. Where traditional transformers relied on heavy copper windings and iron cores, Delta's switching power supplies used high-frequency switching circuits that could be miniaturized.

The breakthrough came through obsessive iteration. Delta's engineers, working 80-hour weeks, would build prototypes, test them to failure, analyze the failure modes, and rebuild. They discovered that by switching power on and off thousands of times per second—rather than using continuous transformation—they could dramatically reduce size and heat generation. To enhance product quality, Delta began producing switching power supplies with a surface-mount design in 1985 as the first such manufacturer in the world.

The timing proved perfect. The personal computer revolution was just beginning, with the IBM PC launching in 1981 and compatibles flooding the market shortly after. Each PC needed a reliable, compact power supply, and Delta's switching technology fit perfectly inside the constrained spaces of desktop computers. By focusing on efficiency when nobody else cared, Delta had inadvertently positioned itself for one of technology's greatest booms.

The numbers told the story of transformation: Today, the efficiency of Delta's products all exceed 90%. In particular, the industry-leading efficiency of Delta's telecom power products exceeds 98% and the efficiency of its solar inverters is as high as 99.2%. By the beginning of the 1990s, Delta became the world's largest manufacturer of switching power supplies, a title it still holds today.

But the real genius wasn't just the technology—it was the business model. While competitors fought over slim margins in finished products, Delta focused on components. Every TV, every computer, every piece of electronic equipment needed power conversion. By becoming the critical supplier that brands couldn't do without, Delta embedded itself in the global electronics supply chain. When Compaq, Dell, or HP won, Delta won. When they lost market share to Lenovo or Acer, Delta still won.

The engineering culture Cheng fostered was unlike anything in Taiwan's typically hierarchical corporate structure. Young engineers could challenge senior managers if they had data to back their arguments. Failure was tolerated—even celebrated—if it led to learning. The company partnered with Virginia Tech's power electronics lab, sending engineers to learn from Professor Fred C. Lee, widely considered the father of modern power electronics. Delta built "Delta Power Electronics Laboratory" on campus, and Milan M. Jovanovic was invited to serve as the principal investigator of the lab to lead the development of high-efficiency power supplies with a high-power density.

This investment in R&D seemed excessive to competitors who preferred licensing technology or copying designs. But it created a moat that would prove impossible to cross. By the time competitors realized efficiency mattered, Delta had thousands of patents, deep customer relationships, and manufacturing expertise that couldn't be replicated overnight.

Global Expansion & The Mission Codification

The Scottish mist hung low over East Kilbride on a June morning in 1997 as Delta's advance team surveyed what would become their European beachhead. Delta Electronics established a R&D centre in East Kilbride, Scotland, in June 1997 with the aim of building a global engineering team. This team could support local IT companies like IBM (located in Greenock) and Compaq (located in Erskine) as well as HP who had bases in mainland Europe. Starting with just three engineers, the team steadily grew.

The choice of Scotland wasn't random. The region had become "Silicon Glen," hosting manufacturing operations for major technology companies. But more importantly, it offered Delta something Taiwan couldn't: proximity to European customers who increasingly demanded local support and faster product customization. The East Kilbride facility would become Delta's template for global expansion—not just manufacturing, but deep technical capabilities that could work directly with local customers.

As Delta expanded globally, Cheng recognized the need to formalize what had always been implicit. In board meetings, he would often pause discussions about quarterly targets to ask: "But how does this help the environment?" This wasn't corporate greenwashing—Cheng genuinely struggled to reconcile growth with sustainability. The answer came in the form of a mission statement that would guide every decision: "To provide innovative, clean and energy-efficient solutions for a better tomorrow".

To express his gratitude to Taiwanese society for providing a solid foundation for Delta's growth, Mr. Bruce Cheng, founder of Delta, and Delta jointly established the Delta Electronics Foundation in 1990. The foundation wasn't just about corporate social responsibility checkboxes—it funded serious environmental research, sponsored university programs in power electronics, and promoted green building standards when most people hadn't heard the term.

The green building movement became Cheng's personal obsession. In 2002, founder Mr. Bruce Cheng was impressed by the green buildings mentioned in the book Natural Capitalism. From 2004 to 2005, he led many Delta teams to visit green buildings around the world. The team visited facilities in Germany where buildings generated more energy than they consumed. They studied Japanese factories that recycled every drop of water. They analyzed California offices that used 80% less energy than conventional buildings.

These weren't PR junkets. Cheng took detailed notes, grilled architects and engineers, and often extended trips to understand the minutiae of building systems. Upon returning to Taiwan, In 2005, as Delta was about to set up a plant in the Tainan Science Park, he decided to adopt green building standards for all future Delta plant/buildings. The board initially resisted—green buildings cost 15-20% more upfront. But Cheng insisted, arguing that Delta couldn't credibly sell energy-efficient products from energy-wasting facilities.

The Tainan plant became a living laboratory. Solar panels covered the roof, rainwater collection systems fed the irrigation, and advanced building management systems optimized every watt of consumption. Employees initially complained about motion-sensor lights that turned off when they sat still too long, but energy consumption dropped 45% compared to conventional facilities. The plant became a pilgrimage site for other manufacturers, with Cheng personally leading tours, evangelizing the gospel of green manufacturing.

This period also saw Delta become a pioneer in ESG (Environmental, Social, and Governance) reporting. Among companies based in Taiwan, it was the first to issue a Corporate Social Responsibility (ESG) report in 2005, and publishes a new report annually. It has been listed on the Dow Jones Sustainability Indices for 14 consecutive years and has achieved a top 10% S&P Global CSA score in its most recent 2024 ranking.

The global expansion continued: facilities in Thailand, India, Mexico, and Eastern Europe. Each followed the same playbook—local engineering talent, green building standards, and deep integration with regional customers. But unlike typical multinational expansion driven by labor arbitrage, Delta's was driven by Cheng's vision of creating centers of excellence that could innovate independently while sharing knowledge globally.

The Strategic Pivot: From Components to Solutions

The Lehman Brothers collapse in September 2008 sent shockwaves through Delta's order books. Within weeks, PC manufacturers canceled orders, inventory piled up, and the company faced its first serious crisis in years. In the emergency board meeting, while executives debated cost-cutting measures, Bruce Cheng posed a different question: "What if selling components isn't enough anymore?"

The financial crisis exposed Delta's vulnerability. Despite being the world's largest switching power supply manufacturer, the company was still fundamentally a components supplier, beholden to the fortunes of its customers. If Dell sneezed, Delta caught cold. Cheng had been mulling this dependency for years, but the crisis provided the burning platform for change.

The pivot began with a simple observation: Delta made the best power supplies, thermal management systems, and industrial automation components in the world, but customers had to integrate these pieces themselves. What if Delta provided complete solutions instead? The transformation wasn't just about bundling products—it required a fundamental reimagining of the company's capabilities and market approach.

The company operates through Power Electronics, Mobility, Automation, and Infrastructure segments. This reorganization, completed by 2010, wasn't merely administrative reshuffling. Each segment was given autonomy to develop end-to-end solutions for specific industries. Power Electronics would continue the component business but also develop integrated power systems. Infrastructure would combine power, cooling, and management systems for data centers. Automation would provide complete factory automation solutions, not just motors and drives.

The data center infrastructure business exemplified this transformation. Rather than simply selling power supplies to data center builders, Delta began offering complete power and cooling solutions. They developed modular data center designs that could be deployed rapidly, integrated cooling systems that worked seamlessly with their power supplies, and management software that optimized both. When cloud computing exploded in the 2010s, Delta was ready with solutions, not just components.

The electric vehicle market provided another opportunity. Delta didn't just want to supply DC-DC converters to automotive manufacturers; they wanted to provide complete EV charging infrastructure. They developed charging stations for homes, fast-charging systems for highways, and fleet management solutions for commercial operators. By 2015, Delta charging stations were appearing across Asia and Europe, generating recurring revenue from services, not just one-time product sales.

Renewable energy became another solution area. Delta leveraged its power electronics expertise to develop solar inverters, wind power converters, and energy storage systems. But instead of selling these as individual products, they offered complete renewable energy solutions for commercial buildings, industrial facilities, and utility-scale projects. The approach required Delta to develop capabilities in system design, project management, and long-term service—muscles the company had never needed as a component supplier.

The transformation wasn't without challenges. Solution selling required a different sales force—consultative sellers who could discuss business outcomes, not just technical specifications. It required Delta to take on system integration risk, something component suppliers typically avoided. It also meant competing with some customers who had been integrating Delta components into their own solutions.

But the strategy paid off. Solutions commanded higher margins than components. They created stickier customer relationships—it's easier to switch component suppliers than to rip out an entire integrated system. Most importantly, they positioned Delta to capture more value as industries digitized and required increasingly sophisticated power and automation systems.

The ESG leadership that had seemed quirky in the 1990s now became a competitive advantage. As corporations faced pressure to reduce carbon footprints, Delta's efficient solutions and green credentials opened doors that were closed to competitors. Delta was named 24th in Time Magazine's 2024 ranking of the world's most sustainable companies.

The Eltek Acquisition: Going Global

December 15, 2014, marked a gray Monday morning in Oslo when the news broke that would reshape the global power electronics industry. Delta Electronics Inc., announced the acquisition of Norwegian power solutions provider Eltek ASA. Delta Electronics' 100 percent-owned subsidiary Deltronics (Netherlands) B.V. will acquire the Norwegian company through a public offering at 11.75 Norwegian krone (US$1.57) apiece for up to 100 percent of all outstanding Eltek shares. The transaction, valued at 3.9 billion Norwegian krone (US$530 million), is expected to be complete by mid-2015.

The acquisition represented more than just geographic expansion—it was Delta's boldest move to transform from an Asian component supplier into a global infrastructure player. Eltek was established in 1971 and listed on Oslo Stock Exchange (ELT:Oslo) in 1998. Headquartered in Drammen, Norway, Eltek designs, manufactures, and markets power supplies and has 2,400 employees at 60 offices in almost 40 countries worldwide. Eltek reported revenues of NOK3.7 billion in 2013. The company focuses on power electronics markets and is one of the leaders in telecom power business and a growing force in industrial and datacenter applications.

The strategic logic was compelling. Eltek brought three critical assets Delta lacked: deep relationships with European and American telecom operators including British Telecom Group and AT&T, advanced power system technologies for telecommunications infrastructure, and a global service network that could support mission-critical installations. While Delta dominated in Asia, Eltek opened doors in markets where Asian suppliers were viewed with skepticism.

The integration challenges were substantial. Eltek's Norwegian engineers, accustomed to their autonomous culture, initially bristled at reporting to Taiwan. The company's cost structure—with Norwegian salaries and European regulatory compliance—seemed bloated by Delta's lean standards. Some analysts questioned why Delta would pay a 20% premium for a company with lower margins than its own operations.

But Bruce Cheng and CEO Ping Cheng saw what others missed. The telecommunications industry was undergoing a massive transformation with the rollout of 4G networks and early 5G planning. These networks required unprecedented power reliability and efficiency at cell tower sites, capabilities where Eltek excelled. Moreover, the same technologies that powered remote cell towers could be adapted for edge data centers, a market that would explode with the Internet of Things.

The integration strategy was deliberate and patient. Rather than imposing Delta's manufacturing methods wholesale, the company maintained Eltek's engineering centers in Norway while gradually introducing Delta's efficiency improvements. Eltek's European sales force was retained and strengthened, giving Delta credibility with Western customers who might never have considered an Asian supplier. Manufacturing was selectively moved to lower-cost locations, but critical engineering and customer-facing functions remained in Europe and the Americas.

Through Eltek's network of services, Delta has further strengthened its global business layout and expanded its power supply sales bases and team services in the Americas, Europe, and Africa. The acquisition also brought unexpected benefits. Eltek's expertise in harsh environment power systems—equipment that could operate reliably in Arctic cold or African heat—proved valuable for Delta's expansion into renewable energy projects in extreme locations.

Within three years, the synergies became clear. Delta's manufacturing scale reduced Eltek's product costs by 25%. Eltek's telecom relationships opened doors for Delta's broader portfolio. The combined company could offer end-to-end solutions for telecommunications infrastructure, from power systems to cooling to site management. When 5G rollout accelerated in 2019, Delta-Eltek was positioned as one of the few suppliers capable of meeting the power and thermal challenges of next-generation networks.

The Eltek acquisition proved to be a masterclass in cross-border M&A. Unlike many Asian companies that stumbled trying to integrate Western acquisitions, Delta succeeded by respecting local capabilities while gradually introducing operational improvements. It demonstrated that the company could execute complex strategic moves beyond organic growth, setting the stage for future acquisitions in automation and industrial systems.

The AI Data Center Revolution

March 2020 brought the world to a standstill, but inside data centers from Virginia to Singapore, a different kind of fever was burning. As billions of people shifted to remote work, video calls replaced meetings, and Netflix streaming spiked 16-fold, the world's digital infrastructure groaned under unprecedented load. For Delta Electronics, this wasn't a crisis—it was validation of a bet they'd been making for years.

The COVID pandemic accelerated five years of digital transformation into five months. But the real revolution came 18 months later when OpenAI released ChatGPT in November 2022. Suddenly, every technology company needed AI capabilities, and AI needed something very specific: massive computational power with unprecedented cooling requirements. A single NVIDIA H100 GPU consumed 700 watts—a high-end gaming PC used less power than one chip. The next generation would be even more power-hungry.

Delta's Q2 revenue growth reflects demand for its AI power supply and heat dissipation components, with customers like NVIDIA and hyperscalers adopting its solutions for next-generation servers. But Delta's advantage went deeper than just being a supplier. The company had spent decades perfecting power efficiency and thermal management—exactly the two bottlenecks constraining AI infrastructure growth.

The challenge facing data center operators was stark: traditional air cooling couldn't handle the heat density of AI servers. A conventional data center rack consumed 5-10 kilowatts; an AI rack with eight GPUs could consume 40-60 kilowatts. The industry needed a paradigm shift, and Delta had been preparing for exactly this moment.

The AI Containerized Data Center offers enterprises a ready-to-deploy solution that integrates power, cooling, and IT resources into a single, compact package. Designed to bring AI infrastructure directly to customer facilities, the AI Containerized Data Center simplifies implementation and accelerates adoption without the need for extensive retrofits. This wasn't just incremental innovation—it was a complete reimagining of how AI infrastructure could be deployed.

The liquid cooling breakthrough represented years of R&D investment paying off at exactly the right moment. Delta's newly-launched Power Capacitance Shelves and in-row 1.5MW liquid-to-liquid Coolant Distribution Units (CDU) could handle heat loads that would melt traditional air-cooled systems. The CDUs worked like radiators in reverse, pulling heat from processors through liquid coolant and dissipating it far more efficiently than air ever could.

But the masterstroke came in May 2025. Delta announced new certification for the in-rack CDU solution for NVIDIA GB200 NVL72, delivering more solutions for in-rack cooling for NVIDIA's customers. The GB200 NVL72 wasn't just another server—it was NVIDIA's flagship AI system, a liquid-cooled, rack-scale solution that boasts a 72-GPU NVLink domain that acts as a single massive GPU. Being certified for this system meant Delta had passed the most stringent validation process in the industry.

The numbers told the story of transformation. Delta Electronics emerged as primary supplier of PSUs for the GB200 NVL72 rack, with each rack requiring 36 PSUs providing 5.5kW each, totaling 198kW of power capacity. This wasn't just about selling more units—it was about becoming irreplaceable infrastructure for the AI revolution.

The containerized data center solution addressed another critical challenge: deployment speed. Traditional data centers took 18-24 months to build. This 20-foot container, which integrates power, cooling, and IT equipment, can be deployed within weeks. For companies racing to deploy AI capabilities, this speed advantage was worth millions in competitive advantage.

Delta's approach to the AI market differed from competitors who simply tried to sell bigger versions of existing products. The company developed integrated solutions that addressed the entire power and cooling chain. From chip vertical power supply technology that helps save approximately 5-15% of power losses in AI accelerator systems to complete containerized data centers, Delta offered solutions at every scale.

The shift to liquid cooling also played to Delta's strengths in system integration. Air cooling was relatively simple—blow cold air on hot components. Liquid cooling required sophisticated plumbing, pressure management, leak detection, and coolant chemistry. It was more like building a car's cooling system than a simple fan, requiring exactly the kind of engineering expertise Delta had cultivated over decades.

The EV & Energy Transition Opportunity

The morning of March 23, 2023, brought unusual excitement to the Stock Exchange of Thailand. Delta Electronics (Thailand) surpassed Airports of Thailand to become the most valuable publicly traded company in Thailand, a symbolic moment that captured a larger transformation. The company that had started as a low-cost manufacturing base was now leading Thailand's push into the future economy of electric vehicles and renewable energy.

The electric vehicle revolution presented Delta with an opportunity that mirrored its original power supply business: a massive market transformation requiring fundamental infrastructure changes. But unlike power supplies, which were hidden inside computers, EV charging stations were visible symbols of the energy transition. Every shopping mall, highway rest stop, and corporate parking lot would need them.

Delta's EV strategy went beyond just making charging stations. The company developed a complete ecosystem: home chargers for overnight charging, DC fast chargers for highways, fleet management systems for commercial operators, and bidirectional chargers that could feed power back to the grid. Each product leveraged Delta's core expertise in power conversion, but required new capabilities in outdoor equipment design, payment systems, and grid integration.

The energy storage market represented another massive opportunity. As renewable energy proliferated, the grid needed batteries to store solar power for nighttime use and wind power for calm days. Delta introduces the DELTerra M1, featuring a compact 10-ft battery container design with flexible configurations ranging from 708 kWh to 7.78 MWh. These weren't just batteries in boxes—they were sophisticated systems that managed charging cycles, prevented thermal runaway, and integrated with grid management systems.

Delta's manufacturing footprint in Thailand proved strategically brilliant. Delta Electronics (Thailand) Public Company Limited was founded in 1988. The company is a subsidiary of Delta Electronics, Inc. Delta Thailand has become the regional business head office and manufacturing center in India and Southeast Asia. Thailand's government aggressively promoted EV manufacturing, offering incentives that made it the "Detroit of Asia" for electric vehicles. Being the largest listed company in Thailand gave Delta political influence and access to partnerships that pure foreign companies couldn't achieve.

The renewable energy business showcased Delta's evolution from component supplier to solution provider. The company didn't just sell solar inverters; it provided complete solar power systems for commercial and industrial customers. These included not just hardware but also monitoring software, maintenance services, and financing partnerships. A factory owner could sign a single contract with Delta and have a complete solar installation generating power within months.

Energy management systems represented the convergence of all Delta's capabilities. These systems combined power electronics, automation, software, and services to optimize energy consumption across entire facilities. A Delta energy management system might control HVAC based on occupancy, shift loads to take advantage of time-of-use electricity rates, integrate on-site solar generation, and manage EV charging loads—all while maintaining power quality and reliability.

The hydrogen economy emerged as Delta's next frontier. While batteries worked well for passenger vehicles and short-duration storage, hydrogen offered advantages for long-haul trucking, industrial processes, and seasonal energy storage. Delta began developing power electronics for hydrogen electrolyzers and fuel cells, positioning itself for what many believed would be the next wave of the energy transition.

The business model for energy transition products differed fundamentally from traditional components. Instead of one-time sales to equipment manufacturers, Delta increasingly engaged in long-term service contracts, revenue-sharing agreements, and even ownership models where it retained ownership of equipment and sold energy as a service. This transformation required new financial capabilities, risk management processes, and customer relationship models.

By 2025, Delta's energy transition businesses weren't just growing—they were pulling the entire company forward. EV charging infrastructure deployments led to data center opportunities as companies realized both needed similar power management capabilities. Renewable energy projects introduced Delta to utility customers who then needed grid-scale power quality solutions. Each success created adjacencies that expanded Delta's addressable market.

Financial Performance & Market Position

The numbers on the screen at the Taiwan Stock Exchange on September 19, 2025, seemed almost surreal. Delta's stock hit 909 TWD, an all-time high that valued the company at more than the GDP of several small nations. For long-term shareholders who'd bought in during the 1990s, the returns exceeded 50x. But the real story wasn't the stock price—it was the fundamental transformation underneath.

Over the last year Delta Electronics has showed a 115.23% increase, dramatically outperforming the broader Taiwan market. This wasn't irrational exuberance but recognition of Delta's positioning at the intersection of multiple megatrends: AI infrastructure, energy transition, and industrial automation. The company had evolved from a cyclical component supplier to a structural growth story.

In 2023, Delta totaled NT$401.2bn (approximately US$13B) in sales, representing steady growth even as the global economy faced headwinds from inflation and geopolitical tensions. But revenue only told part of the story. The company's margin structure had transformed as it shifted from components to solutions. Delta Electronics, Inc. EBITDA is 86.30B TWD, and current EBITDA margin is 17.25%, margins that would have seemed impossible in the commodity power supply business of the 1990s.

The geographic diversification strategy proved prescient as US-China tensions escalated. As a result of the US-China trade war, Delta cut its headcount in China by more than half and expanded operations in India and Southeast Asia. This wasn't just moving factories—it was building complete ecosystems. The India operations included R&D centers developing products for global markets, not just low-cost manufacturing. The Thailand operations had become so successful that Delta Electronics (Thailand) surged 12% to a record 930 baht on Tuesday, extending a three-day rally to 32%. That increased its market value to 1.16 trillion baht ($33.8 billion), surpassing Airports of Thailand Pcl and PTT Pcl.

The financial strength enabled aggressive R&D investment that created a virtuous cycle. Delta spent approximately 8% of revenue on R&D, far exceeding the industry average of 3-4%. This investment didn't just improve existing products—it opened entirely new markets. The liquid cooling systems developed for data centers found applications in EV battery management. Power electronics designed for renewable energy proved valuable for industrial automation. Each innovation created options for future growth.

Cash generation remained robust despite heavy investment. The company's asset-light model—focusing on design and final assembly while outsourcing commodity manufacturing—generated consistent free cash flow. This cash funded both organic growth and strategic acquisitions without requiring significant debt. The balance sheet remained fortress-like, with net cash exceeding most competitors' market capitalizations.

The dividend policy reflected confidence in sustained growth. The last dividend per share was 7.00 TWD, providing income to long-term shareholders while retaining sufficient capital for growth investments. The company had increased its dividend for 15 consecutive years, a rare achievement in the volatile technology sector.

Wall Street and Asian analysts had become increasingly bullish. The consensus view was that Delta had transformed from a cyclical hardware company to a secular growth story. The AI infrastructure buildout was expected to last a decade. The energy transition would require trillions in investment. Industrial automation was still in early innings. Delta was positioned to benefit from all three.

But perhaps the most remarkable financial achievement was doing all this while maintaining Cheng's original environmental mission. The company calculated that its products had helped customers save 335 billion kWh of electricity since 2010—equivalent to the annual consumption of Thailand. This wasn't greenwashing; it was measurable impact that also happened to be good business.

The market's recognition of Delta's transformation was evident in its valuation multiples, which had expanded from industrial conglomerate levels to technology platform premiums. Investors weren't just buying a power supply company; they were buying exposure to the infrastructure layer of the digital and energy transitions.

Playbook: The Delta System

Walking through Delta's Taipei headquarters, you notice something unusual: the lights. Or rather, you don't notice them. They adjust imperceptibly as you move through the building, maintaining perfect illumination while minimizing energy use. It's a small detail, but it exemplifies the Delta System—the set of principles that transformed a commodity component maker into a critical infrastructure provider.

Long-term thinking in a short-term world defines Delta's first principle. While competitors optimized for quarterly earnings, Delta invested in efficiency improvements that took years to pay off. Bruce Cheng's 50-year environmental mission seemed quixotic when announced but proved prophetic as sustainability became a business imperative. The company still makes decisions on 10-year horizons while competitors chase quarterly targets. This long-term orientation enabled Delta to invest in liquid cooling technology a decade before AI made it essential.

Engineering excellence as competitive moat runs deeper than just good products. Delta employs more power electronics PhDs than most universities. Engineers can spend entire careers perfecting single aspects of power conversion. One senior engineer spent 15 years improving transformer efficiency by single percentage points—work that seemed obsessive until those improvements saved customers millions in electricity costs. The company's 90%+ efficiency across product lines isn't marketing; it's the result of thousands of engineers making millions of incremental improvements over decades.

Riding technology waves requires patient positioning. Delta didn't try to create the PC revolution, the internet boom, or the AI explosion. Instead, it positioned itself as the critical enabler for each wave. When PCs emerged, Delta had the most efficient power supplies. When telecom networks expanded, Delta provided the power systems. When AI arrived, Delta had spent years preparing liquid cooling solutions. The strategy isn't predicting waves but ensuring readiness when they arrive.

Vertical integration vs. partnerships represents a constant strategic balance. Delta manufactures critical components like transformers and capacitors in-house to ensure quality and protect intellectual property. But it partners for commodity components and distribution. The Eltek acquisition showed Delta could buy capabilities when needed. The NVIDIA certification demonstrated it could partner with technology leaders. The key is controlling what's strategic while remaining flexible on everything else.

The ESG competitive advantage transformed from cost center to profit driver. Customers now pay premiums for energy-efficient products that reduce their carbon footprints. Governments provide incentives for green technology deployment. Investors reward sustainable business models with higher valuations. Delta's decades of environmental investment, once seen as Cheng's expensive hobby, now generate measurable returns. The company's ESG leadership opens doors that remain closed to competitors with weaker environmental credentials.

Geographic arbitrage goes beyond simple labor cost differences. Delta manufactures in Thailand not just for lower costs but for access to Southeast Asian markets and avoiding China risks. It develops products in Taiwan for engineering excellence, in India for frugal innovation, and in Europe for demanding environmental standards. Each location provides unique advantages that Delta orchestrates into global competitive advantage.

The Delta System's power comes from the reinforcement between elements. Long-term thinking enables engineering excellence. Engineering excellence creates products that ride technology waves. Successfully riding waves generates cash for vertical integration or partnerships. ESG leadership opens geographic opportunities. Geographic diversification reduces risks that would derail short-term thinkers. It's a system, not just a collection of strategies.

Competitors have tried copying elements of the Delta System—investing in R&D, expanding geographically, or emphasizing sustainability. But they miss the cultural foundation that Bruce Cheng embedded from day one: the genuine belief that business success and environmental protection aren't just compatible but mutually reinforcing. This belief, seemingly naive in 1971, now seems prescient as the world grapples with climate change while demanding ever more computational power.

The system continues evolving. As quantum computing emerges, Delta is already developing power systems for the extreme cooling requirements. As fusion energy moves toward commercialization, Delta positions itself to handle power conversion. The specific technologies change, but the system—long-term thinking, engineering excellence, riding waves, smart partnerships, ESG leadership, and geographic optimization—remains constant.

Analysis: Bear vs. Bull Case

The conference room at Delta's investor day bristled with tension as an analyst from Morgan Stanley posed the question everyone was thinking: "With the stock up 115% in a year, what could possibly go wrong?" The CFO's response was measured, but the undercurrents were clear—even the best-positioned companies face risks, and Delta's transformation had created new vulnerabilities alongside new opportunities.

Bull Case

The AI infrastructure supercycle represents a generational opportunity that's just beginning. The NVIDIA GB200 NVL72 is a liquid-cooled, rack-scale solution with 72 GPUs acting as a single massive GPU that delivers 30x faster real-time trillion-parameter LLM inference. Each of these systems requires sophisticated power and cooling infrastructure where Delta excels. With AI model complexity doubling every few months, the demand for such infrastructure will only intensify. Delta's first-mover advantage in liquid cooling and high-density power delivery creates switching costs that lock in customers for years.

The unmatched efficiency leadership becomes more valuable as energy constraints tighten. Data centers already consume 2% of global electricity, projected to reach 8% by 2030. Regulators from Brussels to Beijing are implementing strict efficiency standards. Delta's products, with industry-leading 98% efficiency in some categories, don't just meet these standards—they exceed them by margins competitors can't match. In a power-constrained world, Delta's efficiency advantage translates directly to customer capacity and profitability.

First-mover advantage in liquid cooling for AI isn't just about being early—it's about accumulating expertise that compounds. Each deployment teaches Delta about coolant chemistry, flow dynamics, and failure modes. This learning curve advantage accelerates with each installation. Competitors starting now face a multi-year experience gap precisely when customers can't afford cooling failures that could destroy millions in GPU hardware.

The energy transition creating massive new markets represents another leg of growth. Global EV sales are projected to reach 30 million units by 2030, each requiring charging infrastructure. Grid-scale battery deployments are expected to grow 10x by 2030. Renewable energy capacity additions exceed all other power sources combined. Delta plays in all these markets with proven products and established customer relationships. The transition isn't a possibility—it's happening now, and accelerating.

Bear Case

Taiwan geopolitical risk looms as the elephant in every investor presentation. Despite geographic diversification, Delta remains headquartered in Taiwan with critical R&D resources there. Any Taiwan Strait crisis would devastate the stock, regardless of fundamental strength. The company's efforts to build capabilities elsewhere help but can't fully eliminate this existential risk. Insurance exists in the form of geographic diversification, but premiums are paid in reduced efficiency and higher costs.

Competition from Chinese manufacturers intensifies monthly. Companies like Huawei and Vertiv's Chinese operations accept lower margins to gain market share. They receive government support that Delta can't match. While Delta maintains quality advantages, the gap narrows as Chinese competitors hire talent and license technology. In commodity products, Chinese manufacturers already compete effectively. The question isn't if they'll challenge Delta in high-end products, but when.

Cyclical exposure to data center capex creates vulnerability to spending cycles. When hyperscalers pause infrastructure investment, as they did in early 2023, Delta's revenues suffer immediately. AI enthusiasm currently drives spending, but technology cycles are notoriously volatile. If AI applications don't generate expected returns, or if a new architecture reduces power requirements, Delta could face a severe downturn with high fixed costs from its R&D investments.

Technology disruption risk in power electronics could emerge from unexpected directions. Quantum computing might require entirely different power systems. New semiconductor materials like gallium nitride could obsolete silicon-based power supplies. Breakthrough battery technologies could eliminate the need for complex power conversion. Delta's engineering excellence in current technologies could become a liability if the underlying technology shifts fundamentally.

The valuation premium reflects perfect execution expectations. Any stumble—a product recall, integration problems with an acquisition, or margin compression from competition—could trigger multiple compression. The stock's 115% rise has priced in flawless execution of the AI opportunity. Markets that giveth based on future expectations can taketh away even faster when those expectations disappoint.

Epilogue: What Would We Do?

The boardroom on the 15th floor of Delta's Taipei headquarters offers a panoramic view of the city where it all began. Bruce Cheng, now Honorary Chairman, still attends strategic planning sessions, his questions as sharp as ever: "How does this make the world more efficient?" But the questions facing Delta's next generation of leadership are different from those Cheng answered in 1971.

The nuclear option: Should Delta vertically integrate into data centers? The company already provides critical infrastructure—why not own and operate facilities? The margins in colocation and cloud services dwarf equipment sales. Delta understands power and cooling better than most data center operators. But this would mean competing with customers, a line the company has never crossed. The conservative approach would be partnering with data center operators as a technology provider. The aggressive play would be building Delta-operated facilities showcasing the company's technology while generating recurring revenue. The middle path might be joint ventures where Delta provides technology and operations expertise while partners provide capital and customer relationships.

The software play: Power management as a service represents Delta's biggest untapped opportunity. The company generates terabytes of operational data from deployed equipment but monetizes little of it. Imagine AI-driven systems that predict equipment failures, optimize energy consumption across entire portfolios, and automatically adjust to grid conditions and energy prices. This isn't just selling software—it's transforming from a hardware company to a platform company. The challenge is cultural; hardware engineers think in specifications and tolerances, not user experiences and network effects. Success requires hiring software talent that might not appreciate Delta's engineering culture and building cloud capabilities that seem distant from power electronics.

The China question: How to navigate the decoupling becomes more critical monthly. Delta has already reduced China exposure, but complete withdrawal seems impossible and unwise. China remains the world's largest market for electric vehicles, renewable energy, and industrial automation—all Delta strongholds. The strategy requires surgical precision: maintain presence in markets where geopolitics matter less (industrial components) while withdrawing from sensitive areas (AI infrastructure). Building India and Southeast Asia capabilities isn't just about replacing China—it's about creating genuine alternatives that can innovate independently.

Partnership strategy: Deeper integration with hyperscalers could lock in Delta's position but at the cost of independence. Amazon, Microsoft, and Google increasingly design custom infrastructure, sometimes cutting out traditional suppliers. Delta could become a deep partner, co-developing products and sharing intellectual property. This would guarantee volumes but might commoditize Delta's innovations. The alternative—maintaining independence—preserves pricing power but risks being designed out of next-generation architectures.

The next frontier: Quantum computing infrastructure requires decisions today for markets that might emerge in 2035. Quantum computers operate near absolute zero, requiring cooling systems that make current liquid cooling look primitive. Delta could invest now, accepting years of losses for potential leadership in a transformative technology. Or it could wait for market clarity, risking late entry when winners are already established. The company's history suggests patient investment, but public markets might not tolerate another decade-long bet.

The strategic choices facing Delta reflect broader tensions in the global economy. The company must balance efficiency with resilience, globalization with regionalization, sustainability with growth, and hardware heritage with software futures. These aren't problems to solve but tensions to manage.

What's clear is that Delta's next chapter won't be written by following the playbook that brought it here. The company that began making TV components, dominated PC power supplies, and now enables AI infrastructure must reinvent itself again. The constants remain: engineering excellence, environmental responsibility, and long-term thinking. But their expression must evolve.

If Bruce Cheng's generation built Delta into the world's efficiency leader, the next generation must make it indispensable to humanity's digital and energy future. The pieces are in place: unmatched technical capabilities, global presence, customer trust, and financial strength. The question isn't whether Delta can evolve but whether it can evolve fast enough to lead rather than follow the next transformation.

The view from the boardroom stretches to the mountains surrounding Taipei, the same peaks Bruce Cheng gazed at as a child wondering about the stars. The boy who marveled at nature's grandeur built a company to protect it. Now that company stands at the intersection of humanity's greatest challenges: powering artificial intelligence while preserving the planet. It's a position that would have seemed impossible in 1971. It seems inevitable in 2025. The next chapter of Delta's story will determine if it becomes essential in 2050.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube