SK Hynix: From Korea's "Penny Stock" to AI Memory Champion

I. Cold Open & The HBM Revolution

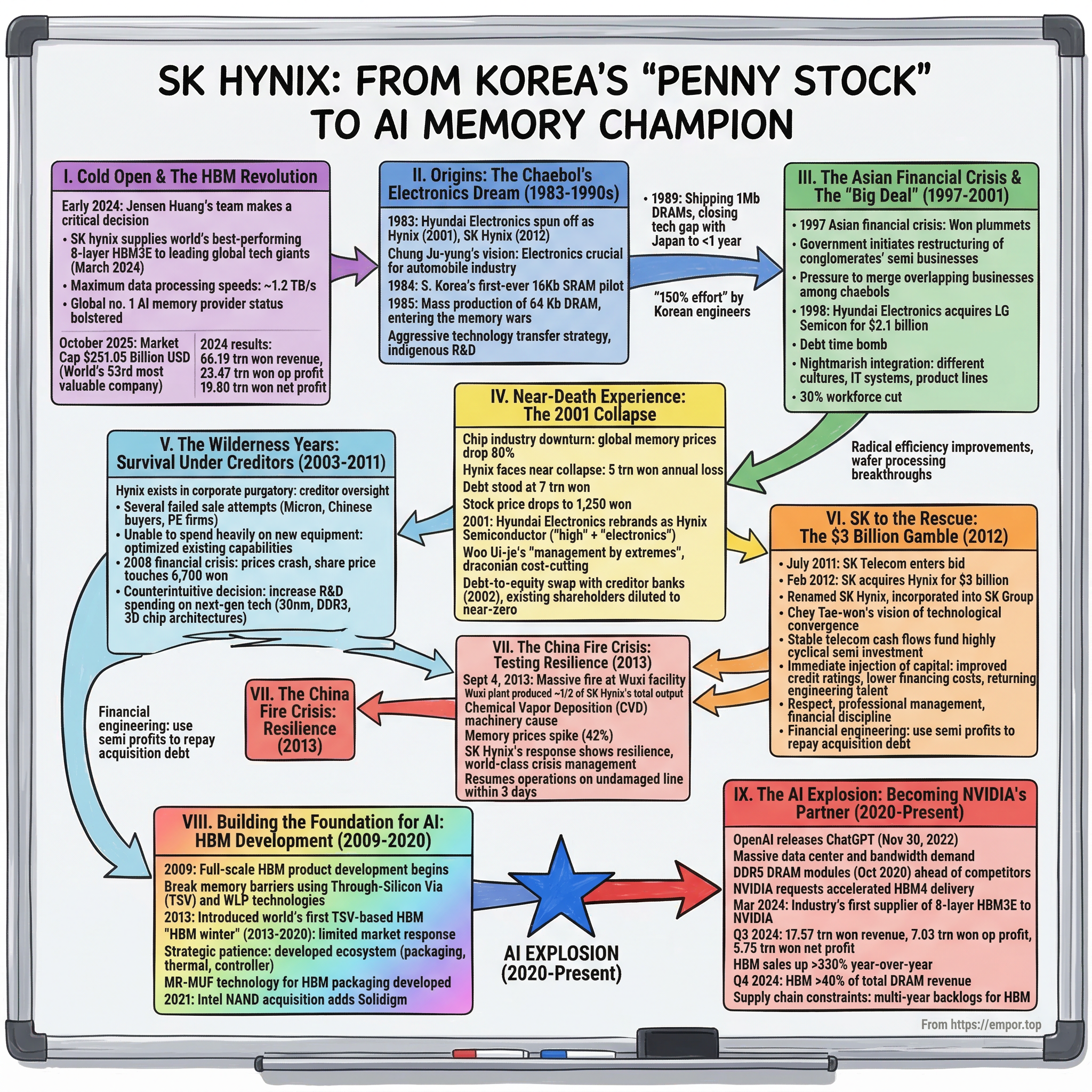

The conference room at NVIDIA headquarters hummed with tension. It was early 2024, and Jensen Huang's team faced a critical decision: who would supply the high-bandwidth memory chips that would power the next generation of AI? The answer, remarkably, was a Korean company that just two decades earlier traded at 125 won per share—essentially a penny stock. SK hynix began supplying the world's best-performing 8-layer HBM3E to leading global tech giants in March 2024, offering maximum data processing speeds of around 1.2 terabytes per second, which helped the company bolster its status as the global no. 1 AI memory provider.

Picture this transformation: As of October 2025 SK Hynix has a market cap of $251.05 Billion USD, making it the world's 53rd most valuable company. The journey from near-bankruptcy survivor to AI kingmaker reads like a silicon fairytale, yet every twist was earned through engineering brilliance, strategic gambles, and sheer survival instinct. SK hynix recorded 66.1930 trillion won in revenues, 23.4673 trillion won in operating profit, and 19.7969 trillion won in net profit in 2024—numbers that would have seemed impossible when creditor banks were deciding whether to liquidate the company in 2001.

How does a company once dismissed as Korea's most troubled conglomerate spinoff become indispensable to humanity's AI revolution? The answer lies not just in semiconductor physics, but in a uniquely Korean story of resilience, strategic patience, and the unexpected synergy between a telecom giant and a memory maker. This is the story of how SK Hynix went from trading at rock bottom to commanding the heights of the AI economy.

II. Origins: The Chaebol's Electronics Dream (1983-1990s)

The year was 1983. Ronald Reagan occupied the White House, Michael Jackson's "Thriller" dominated airwaves, and in South Korea, a construction magnate named Chung Ju-yung made a decision that would reshape the global semiconductor industry. Hyundai Electronics, a major chip maker founded in 1983, was spun off as Hynix in 2001 and renamed SK Hynix in 2012. But the founding story begins with Chung's vision—In the early 1980s, Chung recognized the growing importance of electronics in the automobile industry, one of Hyundai's primary business areas.

Chung Ju-yung wasn't your typical tech founder. The man who built Hyundai from a rice store into Korea's largest conglomerate understood viscerally that Korea's future lay in high technology. While Samsung had already entered semiconductors in 1974 and LG followed suit, Hyundai's entry marked a different approach—they weren't just chasing profits but building capabilities for their entire industrial ecosystem.

The early wins came quickly. SK hynix's pilot production of South Korea's first-ever 16Kb SRAM in 1984 represented more than a technical achievement—it was a declaration of intent. When mass production of the company's first DRAM product—a 64 Kb DRAM—began just a year later in 1985, Korea had officially entered the memory wars. The David-versus-Goliath narrative was irresistible: Korean companies with no prior semiconductor experience taking on Japanese giants like NEC and Toshiba, who dominated 80% of the global DRAM market.

The late 1980s witnessed what industry veterans still call "the great DRAM chase." Hyundai Electronics pursued an aggressive technology transfer strategy, licensing designs from American companies while simultaneously building indigenous R&D capabilities. By 1989, they had achieved something remarkable: shipping 1 megabit DRAMs to international customers, closing the technology gap with Japan from seven years to less than one. The achievement came through what one executive later described as "150% effort"—Korean engineers working 80-hour weeks, sleeping in the fab, treating each wafer like a sacred object.

What distinguished Hyundai Electronics wasn't just technical capability but timing. They entered the market during a severe downturn in 1985-1986, when memory prices had collapsed by 80%. While established players retreated, Hyundai built capacity. It was a pattern that would repeat throughout the company's history: using downturns as opportunities for aggressive expansion.

III. The Asian Financial Crisis & The "Big Deal" (1997-2001)

November 1997. The Korean won plummeted from 800 to nearly 2,000 against the dollar. Companies that had borrowed heavily in foreign currency watched their debts double overnight. During the 1997 Asian financial crisis, the South Korean government initiated the restructuring of the nation's five major conglomerates, including their semiconductor businesses. Among five chaebols, Samsung, LG, and Hyundai were engaged in the semiconductor business. Samsung was exempt from the restructuring due to its competitive position in the global market. However, LG and Hyundai were pressured by the government to merge, as both companies faced significant losses during the semiconductor recession of early 1996.

The government's "Big Deal" policy aimed to consolidate overlapping businesses among chaebols. For semiconductors, the prescription was clear: merge the struggling operations of LG and Hyundai. In 1998, Hyundai Electronics acquired LG Semicon for US$2.1 billion, positioning itself in direct competition with Micron Technology. Subsequently, LG Semicon was rebranded as Hyundai Semiconductor and later merged with Hyundai Electronics.

On paper, the merger created Korea's semiconductor "national champion." In reality, it created a debt time bomb. The combined entity carried obligations from both companies, including LG Semicon's legacy of losses and Hyundai's aggressive expansion debts. The $2.1 billion acquisition price looked increasingly burdensome as memory prices continued their downward spiral. One former executive recalled the merger negotiations: "We knew we were taking on poison, but the government made it clear—merge or lose all support."

The integration proved nightmarish. Two different corporate cultures, incompatible IT systems, overlapping product lines, and redundant facilities. Engineers from LG Semicon faced an identity crisis, suddenly wearing Hyundai badges while working in the same buildings. The Gumi factory, LG Semicon's pride, became a stepchild in the Hyundai system. Morale plummeted as layoffs began—nearly 30% of the combined workforce would eventually be cut.

Yet amid the chaos, something unexpected happened. The crisis forced radical efficiency improvements. The company pioneered new approaches to wafer processing, squeezing more chips from each silicon disc. They developed what became known as the "crisis recipe"—a manufacturing philosophy that assumed resources were always scarce. This mentality would prove invaluable when the next crisis arrived.

IV. Near-Death Experience: The 2001 Collapse

The numbers from 2001 still shock semiconductor veterans. Hyundai faced near collapse during the chip industry's downturn in 2001, when global memory chip prices dropped by 80 percent, resulting in a 5 trillion won annual loss for the company. For context, this meant the company was losing more money than most Korean corporations generated in revenue. In 2001, Hynix recorded sales of 4 trillion won but losses of 5 trillion won, while its debt stood at 7 trillion won.

The perfect storm had arrived. The dot-com bubble burst, decimating demand for PCs and servers. Memory prices fell below production costs—a 256-megabit DRAM that sold for $30 in 2000 fetched less than $3 by late 2001. Hyundai Electronics, already weakened by the LG Semicon acquisition debt, faced insolvency. Credit lines evaporated. Suppliers demanded cash on delivery. The stock price—already depressed—fell to 1,250 won, valuing the entire company at less than a single fab would cost to build.

Creditor banks, many of them under government control at the time, intervened to provide assistance. In 2001, Hyundai Electronics rebranded as Hynix Semiconductor, a portmanteau of "high" and "electronics". Alongside this change, Hynix began selling or spinning off business units to recover from a cash squeeze. Hynix separated several business units, including Hyundai Curitel, a mobile phone manufacturer; Hyundai SysComm, a CDMA mobile communication chip maker; Hyundai Autonet, a car navigation system producer; ImageQuest, a flat panel display company; and its TFT-LCD unit, among others.

The rebranding to "Hynix" symbolized more than a name change—it represented a severing from the Hyundai chaebol structure that had both nurtured and constrained the company. The founding family's "Prince's War"—a succession battle among Chung Ju-yung's sons—meant the semiconductor operation became an orphan. In 2003, Hyundai Group affiliates, including Hyundai Merchant Marine, Hyundai Heavy Industries, Hyundai Elevator, and Chung Mong-hun, the chairman of Hyundai Asan, consented to forfeit their voting rights and sell their stakes in Hynix. Hynix was then formally spun-off from the Hyundai Group in August 2003.

Enter Woo Ui-je, the CEO who would save Hynix through what employees called "management by extremes." Woo implemented draconian cost-cutting: salaries slashed by 30%, R&D budgets cut to the bone, non-essential facilities sold. But crucially, he never stopped wafer production. "If we stop the lines, we die," became the company mantra. Engineers worked without air conditioning in summer, without heating in winter. Yet they kept the fabs running, kept shipping products, kept generating cash flow—however meager.

The debt-to-equity swap with creditor banks in 2002 diluted existing shareholders to near-zero but kept the company alive. Banks became reluctant semiconductor operators, owning 36% of a company they didn't understand in an industry famous for its volatility. They wanted out, but who would buy Korea's most troubled semiconductor company?

V. The Wilderness Years: Survival Under Creditors (2003-2011)

Between 2003 and 2011, Hynix existed in corporate purgatory—neither fully alive nor allowed to die. The Hynix creditors, including Korea Exchange Bank, Woori Bank, Shinhan Bank and Korea Finance Corporation, attempted to sell their stake in Hynix several times but failed. Korean companies such as Hyosung, Dongbu CNI, and former stakeholders, including Hyundai Heavy Industries and LG, were considered potential bidders but were either denied or withdrew from the bidding.

The failed sale attempts became a recurring nightmare. In 2004, Micron Technology seemed poised to acquire Hynix for $3.4 billion, only to walk away citing "valuation concerns"—code for discovering the true extent of Hynix's challenges. Chinese buyers circled in 2006, triggering national security concerns. Private equity firms conducted due diligence, ran the numbers, and inevitably concluded the risks outweighed rewards. Each failed sale attempt further damaged morale and market confidence.

Yet paradoxically, these wilderness years forged Hynix's competitive advantages. Unable to spend heavily on new equipment, engineers became masters of optimization. They developed techniques to extend equipment life far beyond specifications, to increase yields through software rather than hardware upgrades. The "Hynix way" emerged—a manufacturing philosophy emphasizing incremental improvement over revolutionary change.

The 2008 financial crisis brought another near-death experience. Memory prices crashed again as the global economy contracted. Hynix's share price touched 6,700 won—barely above the 2001 crisis lows. Industry analysts openly discussed bankruptcy scenarios. The "second chicken game" had begun—which memory maker would cut production first? Hynix, with its creditor oversight and limited financial flexibility, seemed the obvious candidate to blink.

Instead, CEO Kim Jong-kap made a counterintuitive decision: increase R&D spending on next-generation technologies. While competitors focused on surviving the present, Hynix quietly developed capabilities in what would become crucial technologies: 30-nanometer process technology, DDR3 high-speed memory, and early experiments with 3D chip architectures. "We had nothing to lose," Kim later explained. "When you're already at the bottom, the only direction is up."

The workforce during these years developed an almost mythical resilience. Engineers who stayed—and many left for Samsung or foreign companies—spoke of a siege mentality. They were the guardians of Korea's semiconductor sovereignty, keeping the technology alive against all odds. The company culture became paradoxically both fatalistic and fiercely determined. Every successful tape-out, every yield improvement, every design win was celebrated like a military victory.

By 2010, something had shifted. Hynix posted its first substantial profit in years. The technologies developed during the crisis years began paying dividends. The company that creditors had tried desperately to sell suddenly looked valuable again. The stage was set for the most unlikely acquirer imaginable.

VI. SK to the Rescue: The $3 Billion Gamble (2012)

The Seoul financial district buzzed with disbelief in July 2011. In July 2011, SK Telecom, the nation's largest telecommunication company, and STX Group officially entered the bid. STX dropped its deal in September 2011, leaving SK Telecom as the sole bidder. SK Telecom—a mobile carrier with zero semiconductor experience—wanted to buy Korea's most troubled memory maker? Industry analysts called it "the deal that made no sense."

In the end, SK acquired Hynix for US$3 billion in February 2012. As Hynix was incorporated into SK Group, its name was changed to SK Hynix. But why would SK Group Chairman Chey Tae-won risk his conglomerate's crown jewel on a semiconductor gamble?

The answer lay in Chey's vision of technological convergence. While others saw a troubled memory maker, SK saw the foundation for a data-driven future. After years of analyzing the semiconductor industry, SK had confidence that semiconductors would represent Korea beyond the SK group. Accordingly, SKT acquired a 20.1% stake in Hynix for approximately KRW 3.4 trillion in 2012.

The funding strategy revealed SK's financial engineering brilliance. SK Telecom's huge acquisition funding background was stable communication business. SK Telecom was able to raise acquisition funds through accumulated in-house reservations and financial loans, based on the nature of the telecommunications industry, which generates hundreds of billions of cash every month based on the frequency. Essentially, SK Telecom used its predictable telecom cash flows to fund a highly cyclical semiconductor investment—a financial arbitrage that traditional semiconductor companies couldn't replicate.

The cultural transformation began immediately. SK brought professional management practices that Hynix desperately needed: systematic planning, financial discipline, and crucially, patient capital. Unlike the creditor banks that managed quarter-to-quarter, SK could afford to think in decades. The first SK-appointed CEO, Park Sung-wook, arrived with a mandate: "Make Hynix a company SK can be proud of."

By covering the acquisition loan repayment costs spent by SK Telecom with SK Hynix's dividends, SK Group effectively created SK Hynix, which generates operating cash flow of more than 4 trillion won per year with 1.7 trillion won (SK Telecom's cash holdings). It had the same effect as acquiring. The financial engineering was elegant: use telecom's stable cash to buy semiconductors at the cycle bottom, then use semiconductor profits at the cycle peak to repay the acquisition debt.

The injection of capital had immediate effects. Credit ratings improved, lowering financing costs by hundreds of basis points. Suppliers extended payment terms. Customers—who had been diversifying away from the troubled Hynix—returned. Most critically, top engineering talent that had fled during the creditor years began returning, lured by competitive salaries and the promise of stability.

SK also brought something intangible but crucial: respect. After years as creditor-controlled "penny stock," SK Hynix employees suddenly worked for one of Korea's most prestigious conglomerates. The psychological impact was profound. "We went from corporate orphans to SK family," recalled one engineer. "It changed everything about how we saw ourselves."

VII. The China Fire Crisis: Testing Resilience (2013)

September 4, 2013, 3:50 PM China time. Black smoke billowed from SK Hynix's Wuxi facility, visible for miles across the Jiangsu province industrial zone. A massive fire broke out this afternoon (local time), at a SK Hynix production facility in Wuxi, China. At this moment, pictures and videos of the fire are swarming through local social networks, and there are no official announcements by either the local authorities, or the company itself. The facility hit by fire is rumored to be one that handles packaging (placing bumped dies inside ceramic or plastic shells, and labeling them). If the extant of damage to the facility is high, it might affect NAND flash prices more than DRAM, since the company recently prioritized NAND flash over DRAM for the facility.

The Wuxi complex wasn't just another factory—it produced nearly half of SK Hynix's total output. The Wuxi plant produces nearly half of SK Hynix's monthly 260K wafers. This includes 100K of its PC DRAM, and 30K of its mobile DRAM, including MCP. In the hyperconnected world of global electronics, this single facility's output touched everything from smartphones to servers.

The fire's origin told a story of industrial hazard meeting Murphy's Law. The fire accident experienced by SK Hynix's Wuxi Plant on September 4 is now revealed to have originated from its Chemical Vapor Deposition (CVD) machinery. Other than the severely burned down equipments, the fire, heavy smoke, and power shortages are known to have also contributed to the direct contamination of the clean room and the notably damaged wafer production lines.

Within hours, the semiconductor world panicked. Memory prices, which had been relatively stable, spiked immediately. The price of the benchmark DDR3 2-gigabit dynamic random-access memory chip reached $2.27 yesterday, compared with $1.60 on Sept. 4, when a fire forced the closing of SK Hynix's factory in Wuxi—a 42% increase that sent shockwaves through the supply chain.

But here's where the story turns: SK Hynix's response revealed how much had changed under SK Group's ownership. Within 72 hours, the company had dispatched hundreds of engineers from Korea to Wuxi. SK Hynix dispatched many experts from our headquarters and established a 24 hour restoration system with partner companies. Our plan is to resume normal operations with full production capacity in the shortest time by ramping up operations in stages as soon as the damaged facilities are replaced. We will continue to make every effort to minimize the impact on supply with our inventories of finished products and completely processed wafers as well as production support from our headquarters.

The crisis management was exemplary. The line which was not affected by the fire in our fab in Wuxi, China has resumed operations from Saturday, September 7, 2013 after completing all safety inspections. We are continuing our inspection of utilities and equipments to restore the line that was partly damaged by the fire under the cooperation of the Chinese government. The "Gemini" architecture of the facility—where clean rooms operated independently—proved its worth, limiting damage to roughly half the facility.

The financial markets' reaction was telling. While SK Hynix stock initially dropped on the news, it quickly recovered as investors realized something counterintuitive: the fire would likely strengthen SK Hynix's market position. The supply shortage drove prices up across the industry, but SK Hynix—with its insurance coverage and rapid recovery—would benefit from higher prices while competitors scrambled to fill supply gaps. Micron's stock rose 6% on news of their competitor's troubles, but SK Hynix would have the last laugh.

What the Wuxi fire truly tested wasn't SK Hynix's facilities but its resilience as an organization. The company that might have collapsed from such a blow in 2001 now demonstrated world-class crisis management. The difference? Twelve years of struggle had created institutional memory of crisis, while SK's resources provided the means to respond effectively. The fire that could have been a catastrophe became, perversely, a demonstration of strength.

VIII. Building the Foundation for AI: HBM Development (2009-2020)

Long before ChatGPT captured the world's imagination, in a conference room in Icheon, SK Hynix engineers debated a radical proposition: what if memory chips could be stacked like pancakes? The year was 2009, and the concept seemed almost absurd. SK hynix's HBM success story can be traced back to 2009 when the company began full-scale product development after discovering that TSV and WLP technologies could break memory performance barriers, introducing the first-generation HBM four years later in 2013.

The journey from concept to product was tortuous. Through-Silicon Via (TSV) technology—drilling microscopic holes through silicon wafers to connect stacked chips—required completely reimagining semiconductor manufacturing. Early yields were abysmal. One engineer recalled producing wafers where 95% of chips were defective. "We were burning money faster than the 2013 Wuxi fire," he joked darkly.

When SK Hynix introduced the world's first TSV-based HBM in 2013, the market response was... silence. Although HBM was hailed as an innovative memory solution, it did not receive an explosive market response because the HPC sector had not yet sufficiently matured enough for widespread HBM adoption. The technology was a solution in search of a problem. Graphics cards didn't need the bandwidth. Servers found it too expensive. For years, HBM remained a technical curiosity—impressive engineering that generated minimal revenue.

The "HBM winter" lasted from 2013 to 2020. During these seven years, SK Hynix faced intense internal pressure to abandon the technology. Why continue investing hundreds of millions in a product nobody wanted? The answer came from an unlikely source: gaming. As graphics processors grew more powerful, traditional memory became a bottleneck. AMD's 2015 adoption of HBM for its Radeon graphics cards provided the first commercial validation.

But the real breakthrough was strategic. While competitors viewed HBM as just another product, SK Hynix recognized it as a platform technology. They developed not just the memory chips but the entire ecosystem: packaging technology, thermal solutions, controller interfaces. When AI's computational demands exploded, SK Hynix had seven years of learning curve advantage that money couldn't buy.

The 2021 Intel NAND acquisition added another piece to the puzzle. In 2021, Hynix acquired Intel's NAND business for $9 billion, resulting in the establishment of Solidigm. Critics called it expensive, but SK Hynix saw synergy: Intel's enterprise SSD technology combined with SK Hynix's memory expertise would create complete storage solutions for AI data centers.

The MR-MUF revolution deserves its own mention. This advanced molding technology, developed by SK Hynix for HBM packaging, solved the critical challenge of chip warpage during stacking. SK hynix applied MR-MUF technology to HBM2E which changed the market landscape, then developed Advanced MR-MUF technology for HBM3 and HBM3E. It was precisely this kind of process innovation—unglamorous but essential—that would make SK Hynix indispensable to the AI revolution.

By 2020, as the world discovered large language models and neural networks, SK Hynix possessed something priceless: a decade of HBM experience, proven manufacturing capability, and most crucially, the trust of NVIDIA. The winter had been long, but spring was about to arrive in spectacular fashion.

IX. The AI Explosion: Becoming NVIDIA's Partner (2020-Present)

The moment everything changed can be pinpointed precisely: November 30, 2022, when OpenAI released ChatGPT. Within five days, one million users had signed up. Within two months, 100 million. The world suddenly understood what AI could do, and equally important, what AI required: massive computational power and memory bandwidth that only HBM could provide.

SK Hynix launched the industry's first DDR5 DRAM modules in October 2020, ahead of competitors. This wasn't just about being first—it was about being ready. When the AI explosion arrived, SK Hynix had the production capacity, the technical expertise, and crucially, the trust relationship with NVIDIA that competitors couldn't quickly replicate.

The HBM3E announcement in March 2024 marked SK Hynix's coronation as AI memory king. In March, SK Hynix became the industry's first supplier of eight-layer HBM3E to Nvidia. SK hynix was the first chipmaker in the world to supply fifth-generation HBM3E chips in March to Nvidia, who designs graphic processing units essential for AI computing. The numbers were staggering: 1.2 terabytes per second of bandwidth, 36 gigabytes of capacity, all in a package smaller than a thumbnail.

SK Hynix began producing fifth-generation HBM chips, eight-layer HBM3E, in March, with initial shipments to Nvidia. Sources said it will begin mass production of the more advanced 12-layer HBM3E chip in the third quarter and begin supplying them in large quantities to Nvidia from the fourth quarter. The progression from 8-layer to 12-layer within a single year demonstrated manufacturing prowess that left competitors scrambling.

The financial transformation was breathtaking. SK hynix Inc. announced that it recorded 17.5731 trillion won in revenues, 7.03 trillion won in operating profit, and 5.7534 trillion won in net profit in 3Q24. More remarkably, HBM sales showed excellent growth, up more than 70% from the previous quarter and more than 330% from the same period last year. By Q4 2024, HBM continued its high growth in fourth quarter marking over 40% of total DRAM revenue.

The company that once begged for creditor patience now chose its customers. SK hynix, September 26, 2024, said it has begun mass production of 12-layer high bandwidth memory (HBM) chips, the first in the world. This wasn't just a technical achievement—it was a strategic moat. Each new HBM generation required years of development, billions in investment, and deep customer collaboration. SK Hynix had all three.

In May, SK Hynix Chief Executive Kwak Noh-Jung said its HBM chips were sold out for this year and its capacity is almost fully booked for 2025. When was the last time a semiconductor company had multi-year backlogs? The transformation from commodity supplier to strategic partner was complete.

The company established itself as a key partner in the AI and data center markets by supplying HBM products to NVIDIA, achieving a 50% market share in the HBM sector. This wasn't market share won through price competition—it was earned through technological superiority and flawless execution. NVIDIA's Jensen Huang, notorious for his exacting standards, personally requested accelerated HBM4 delivery timelines, a testament to SK Hynix's irreplaceable position in the AI supply chain.

The numbers from 2024 tell the story: revenues of 66.19 trillion won, operating profit of 23.47 trillion won, net profit of 19.80 trillion won. For context, the entire company was valued at less than 3 trillion won during the 2001 crisis. The ugly duckling had become a swan, and the transformation was complete.

X. Playbook: Lessons from the Semiconductor Battlefield

The SK Hynix story offers a masterclass in strategic resilience, but the lessons extend far beyond semiconductors. First, consider the power of crisis-forged capabilities. Every near-death experience—1997, 2001, 2008, 2013—created organizational capabilities that competitors who avoided such crises never developed. SK Hynix engineers joke about their "crisis DNA," but there's truth in the humor. The company's ability to operate profitably at price points that would bankrupt competitors comes from decades of forced efficiency.

The patient capital lesson deserves special attention. Between 2009 and 2020, SK Hynix invested continuously in HBM technology despite minimal returns. Samsung, with its deeper pockets, could have done the same but didn't. The difference? SK Group's strategic patience, born from their telecom heritage where infrastructure investments take decades to pay off. The creditor banks that controlled Hynix from 2001-2012 would never have approved such long-term bets.

Technology cycles and timing represent another crucial lesson. SK Hynix consistently entered new technologies during downturns when equipment was cheap and competitors retreated. They built 30nm capacity during the 2008 crisis, developed HBM during the "memory winter" of 2013-2019, and now push toward HBM4 even as others question AI sustainability. This countercyclical investment strategy requires both courage and capital—SK Hynix finally had both.

The consolidation economics of the memory industry offer broader insights. Unlike software where margins expand with scale, memory manufacturing becomes more capital intensive over time. Each new process node costs more than the last—a 3nm fab costs $20 billion versus $1 billion for 90nm. This creates a natural oligopoly: only companies with massive scale can afford to compete. SK Hynix's survival through multiple consolidation waves positioned it as one of three remaining players.

Geopolitics adds another layer. SK Hynix operates major facilities in China (Wuxi and Dalian) while serving primarily American customers. This precarious position—manufacturing in China, designing in Korea, selling to America—requires diplomatic sophistication. The company maintains technology transfer restrictions, carefully managing what intellectual property goes where. It's semiconductor diplomacy at its finest.

Finally, the moat-building lesson: in commoditized industries, sustainable advantage comes from doing what others cannot or will not do. For SK Hynix, that meant seven years of HBM investment when nobody cared, developing MR-MUF packaging when others focused on chip design, and maintaining excess capacity during downturns. These decisions looked foolish at the time but created the barriers that protect today's profits.

XI. Power & Competition: The Memory Oligopoly

The global memory industry in 2025 resembles a three-player poker game where everyone knows everyone else's cards. SK hynix held a 31.8% share of the DRAM market and a 21.6% share of the NAND flash market in the fourth quarter of 2023. Samsung leads with roughly 40% of DRAM, while Micron holds the remainder. This triumvirate controls over 95% of global production—an oligopoly that makes oil cartels look fragmented.

But memory isn't like oil. Each generation requires exponentially more capital investment. A state-of-the-art extreme ultraviolet (EUV) lithography machine costs $200 million—and you need dozens. The Yongin semiconductor cluster where SK Hynix plans its next mega-fab will cost $40 billion. These aren't businesses you enter casually.

The barrier to entry isn't just capital—it's accumulated knowledge. SK Hynix employs over 10,000 engineers who've spent decades perfecting processes measured in nanometers. When defects are counted in parts per billion, experience matters. China's YMTC and CXMT have spent billions trying to catch up, achieving perhaps 60% of the leaders' capability after a decade of effort.

The oligopoly creates unusual dynamics. Competitors are also customers—Samsung buys SK Hynix memory for some products while competing fiercely in others. Industry conferences feature executives who've worked at all three companies, creating an informal knowledge network. "We compete Monday through Friday, then play golf together on weekends," one executive explained.

Government support complicates the picture. Korea treats semiconductors as a national strategic asset, providing tax breaks, infrastructure, and R&D support. The U.S. CHIPS Act promises $52 billion to rebuild American semiconductor capacity. China's 14th Five-Year Plan allocates even more. It's industrial policy on steroids, with governments picking winners in a game where only three can play.

The future challenger question looms large. Chinese companies have technology gaps but unlimited government support. Intel abandoned memory but could return. New technologies—quantum, neuromorphic, photonic—might obsolesce silicon entirely. Yet for now, the triumvirate seems unassailable. The capital requirements, technological complexity, and customer relationships create moats that grow wider each year.

XII. Bull & Bear Case: The Future of SK Hynix

The Bull Case rests on an almost religious faith in AI's transformative power. If artificial general intelligence arrives, if every device becomes AI-enabled, if data centers multiply like digital rabbits, then SK Hynix's HBM dominance makes it the arms dealer to the AI revolution. The company's 50% HBM market share and first-mover advantage in each generation create a virtuous cycle: higher profits fund more R&D, which extends the technological lead, which attracts more customers.

The numbers support optimism. The HBM market is expected to continue to boom over the next few years to around $43 billion by 2027, and SK Hynix to maintain its dominant leadership in the HBM market through next year, thanks to its technological edge. The company is likely to sustain around 60% global HBM market share, underpinned by its position as the primary supplier to key customers such as Nvidia, Google and other leading customers. The SK Group's commitment—$77 billion in AI and semiconductor investment through 2028—signals confidence that this isn't a bubble but a paradigm shift.

Geographic diversification adds resilience. While the Wuxi facility represents concentration risk, new fabs in Korea and potential U.S. expansion hedge against geopolitical tensions. SK Hynix's $3.9 billion Indiana packaging facility, announced for AI products, shows strategic thinking about supply chain localization.

The Bear Case starts with history: every semiconductor boom ends in a bust. Memory prices are already showing weakness in commodity DRAM. If AI investment slows—whether due to regulation, disappointing returns, or simply capital exhaustion—HBM demand could evaporate. The company generating 40% of DRAM revenue from a single product category faces concentration risk that would make any risk manager nervous.

China represents an existential wild card. SK Hynix's Wuxi and Dalian facilities produce roughly 40% of total output. U.S.-China tensions could force choosing sides, potentially losing either production capacity or customer access. The nightmare scenario: U.S. restrictions on selling to China while China restricts operations of Korean companies. SK Hynix would be caught in the crossfire.

Technology transitions pose another threat. Samsung's aggressive HBM development could erode SK Hynix's premium pricing. New memory architectures—from Intel's Optane successor to novel computing paradigms—might obsolesce current technology. In semiconductors, today's moat can become tomorrow's stranded asset.

Customer concentration amplifies risks. NVIDIA represents an estimated 30-40% of HBM revenue. Apple, Microsoft, and Amazon comprise much of the remainder. Losing any major customer—whether to vertical integration or competitive bidding—would crater earnings. When five customers drive your supercycle, their capital allocation decisions become your destiny.

XIII. Epilogue: What Would Have Happened?

Imagine if SK hadn't acquired Hynix in 2012. The creditor banks, exhausted after a decade of ownership, might have accepted any offer—perhaps from Chinese buyers who later faced U.S. restrictions. Korea would have lost its second semiconductor champion, leaving Samsung as a monopolist facing less domestic competition. The global memory industry might have evolved into a duopoly, with higher prices but less innovation.

What if the 2001 crisis had led to Micron acquiring Hyundai Electronics? The American company would have gained Korean engineering talent and fab capacity, potentially dominating today's market. But would Micron, with its conservative Idaho culture, have made the aggressive HBM investments that SK Hynix pursued? The AI revolution might have unfolded differently, with NVIDIA facing memory bottlenecks that constrained growth.

Consider an alternative where the 1997 crisis never forced LG Semicon and Hyundai Electronics to merge. Korea might have had three subscale players instead of two giants. None might have survived the successive industry downturns. The memory industry could have consolidated entirely into American and Japanese hands, leaving Korea dependent on foreign technology for its electronic exports.

The importance of maintaining domestic semiconductor capabilities resonates beyond Korea. Taiwan's TSMC obsession, America's CHIPS Act, Europe's semiconductor sovereignty push—all recognize that advanced semiconductors are the new oil. Countries without domestic capability face economic dependency that no amount of financial reserves can offset.

For other nations building semiconductor industries, SK Hynix offers sobering lessons. Success required not just government support and capital, but decades of accumulated expertise, multiple near-death experiences that forged resilience, and extraordinary timing. The window for creating national champions may be closing as capital requirements explode and technological complexity compounds.

The SK Hynix story ultimately demonstrates that in semiconductors, survival is victory. The company that barely existed in 2001 now shapes humanity's technological future. Every AI interaction, every generated image, every large language model inference runs through memory chips that SK Hynix produces. From Korea's penny stock to AI's memory champion—it's a transformation that rewrites what's possible when engineering excellence meets patient capital meets perfect timing.

The next chapter remains unwritten. Will SK Hynix maintain its HBM leadership as competitors intensify efforts? Can it navigate the U.S.-China technology cold war? Will AI demand continue its exponential growth or flame out like previous bubbles? These questions will determine whether SK Hynix's remarkable journey continues or becomes another cautionary tale in semiconductor history's graveyard of former champions.

What seems certain is that the company forged in crisis, refined through bankruptcy's fire, and elevated by strategic vision has earned its place in technology history. The orphan became royalty. The penny stock became precious. And Korean engineers who once worked without heating now design the memory architecture powering humanity's artificial intelligence ambitions. It's a story that could only happen in semiconductors, and perhaps, only in Korea.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube