Gree Electric Appliances: The Iron Lady and the Air Conditioning Empire

I. Introduction: The Billion-Yuan Bet

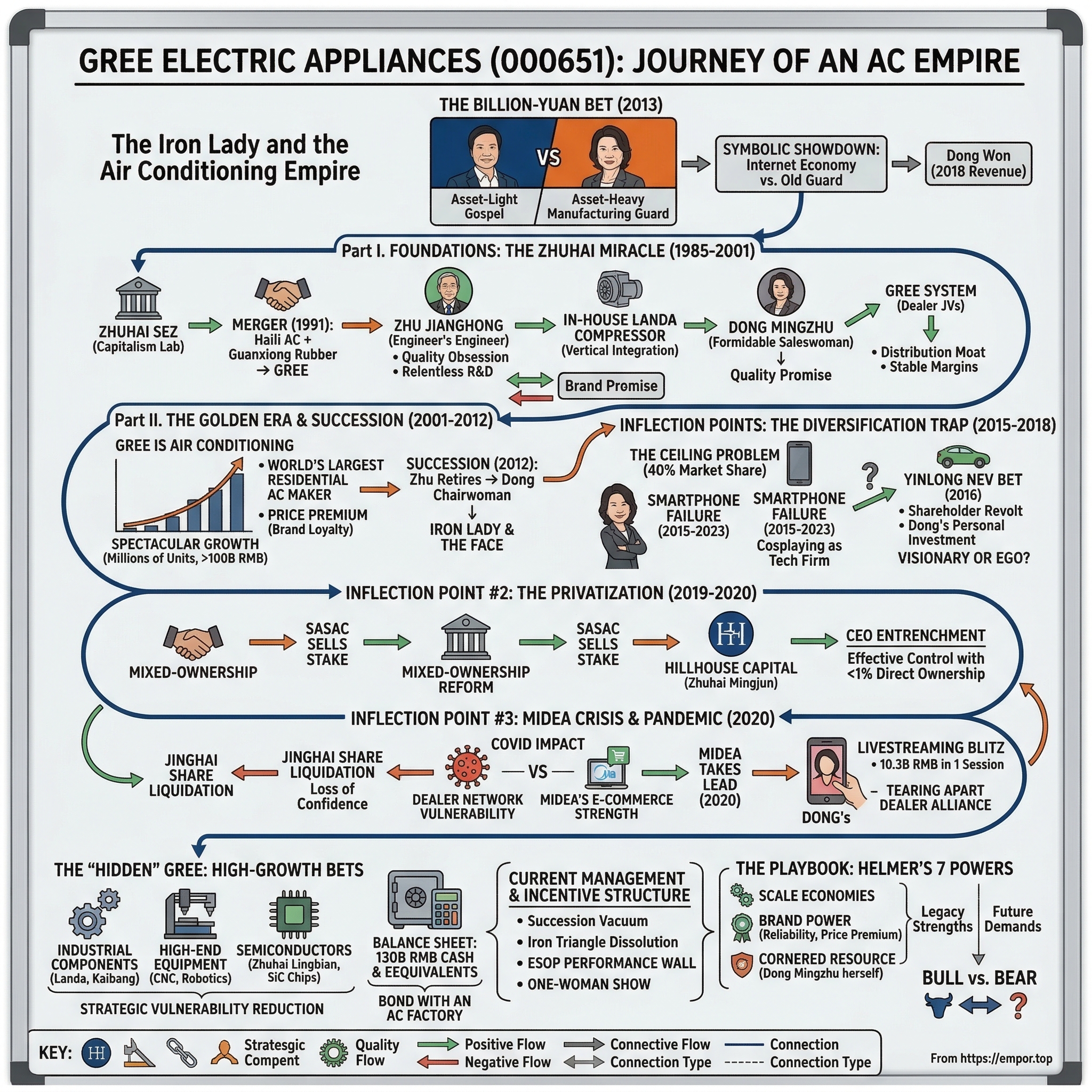

Picture the scene: December 12, 2013, Beijing. The 14th annual CCTV "China Economic Person of the Year" awards ceremony is being broadcast live to hundreds of millions of viewers on the CCTV Finance Channel. Two of that year's co-winners stand face to face on stage. On one side is Lei Jun, the boyish, hoodie-wearing founder of Xiaomi, China's hottest tech startup, a man who worships at the altar of Silicon Valley's asset-light gospel. On the other side stands Dong Mingzhu, the formidable chairwoman of Gree Electric Appliances, her hair swept back in her trademark no-nonsense style, a woman who has spent two decades in the trenches of Chinese manufacturing and has the battle scars to prove it.

Lei Jun, ever the showman, proposes a friendly wager. He bets that Xiaomi's revenue will surpass Gree's within five years. The stakes? A symbolic one yuan—about fourteen US cents. The audience chuckles. But Dong Mingzhu does not chuckle. She fires back with a line that would echo across China's business press for years: "Make it one billion yuan." The host freezes. Lei Jun later revealed that Dong had gone completely off script. The escalation from one yuan to one billion was pure Dong Mingzhu—spontaneous, combative, and utterly unafraid of what might follow. The host, scrambling to regain control, had the two lock eyes for three awkward seconds on live television to seal the deal.

It was not really about the money. Everyone in that audience understood what they were watching: a symbolic showdown between China's new internet economy and its old manufacturing guard. Lei Jun represented the future—smartphones, ecosystems, fans who camped outside stores. Dong Mingzhu represented the past—or at least that was what the internet commentators assumed. Factories, supply chains, physical retail networks, the unglamorous plumbing of the real economy.

Five years later, in 2018, Gree reported revenue of approximately 198 billion RMB. Xiaomi came in at 175 billion. Dong won. She declined to collect, calling it "just an argument about two different business ideas." But the bet had accomplished something more important: it crystallized the central question of Chinese business in the 2010s. Could the old manufacturing titans adapt to the internet age? Or would they be swept away by asset-light disruptors who never touched a factory floor?

This is the story of Gree Electric Appliances—ticker 000651 on the Shenzhen Stock Exchange—a company that went from a nameless air conditioning factory in a southern Chinese special economic zone to becoming the world's largest residential AC manufacturer. It is the story of the woman who built it into a fortress, the privatization that freed it from the state, and the existential fight it now wages against Midea, e-commerce, and the creeping realization that the fortress walls, however thick, may not hold forever. Along the way, there are smartphones nobody bought, an electric vehicle company that nearly destroyed the board, billions in livestream sales, and a succession vacuum that makes corporate governance analysts break out in a cold sweat. This is the Gree story, and it is one of the most instructive case studies in Chinese capitalism.

II. Foundations: The Zhuhai Miracle (1985–2001)

To understand Gree, you first have to understand Zhuhai. In 1980, Deng Xiaoping designated Zhuhai as one of China's first Special Economic Zones, a laboratory for capitalism tucked into the Pearl River Delta just across the border from Macau. While neighboring Shenzhen became the poster child for SEZ success, Zhuhai took a quieter path. It attracted light manufacturing—electronics, appliances, small factories cranking out goods for export. It was in this environment that two small enterprises, Haili Air Conditioning and Guanxiong Rubber Company, merged in 1991 to form Gree Electrical Equipment Company. The name was new, the ambition modest: produce air conditioners for a domestic market that was just beginning to afford them.

The man who shaped the company's DNA was Zhu Jianghong, and his story deserves more attention than it typically receives. Born in 1945, Zhu graduated from South China University of Technology in 1970 with a degree in machinery, then spent nearly two decades at a mining equipment factory in the remote Guangxi province before returning to his hometown of Zhuhai in 1988. He was not a natural entrepreneur or a charismatic leader. He was an engineer's engineer—quiet, methodical, obsessed with precision. When he took over the merged entity in 1992, the factory was producing roughly 20,000 air conditioning units a year. Chinese AC manufacturers at the time were essentially assemblers, importing compressors from Japanese firms like Daikin and slapping local brands on finished products. Quality was an afterthought. Returns and warranty claims were endemic.

Zhu refused to accept this. His defining philosophy could be boiled down to a single sentence that became Gree's internal creed: "A company without core technology has no soul." Rather than competing on price—the default strategy for Chinese manufacturers in the 1990s—he invested relentlessly in quality control and in-house R&D. He established a joint venture with Daikin, but rather than remaining dependent on the Japanese giant's technology, he used the partnership as a learning engine. Gree engineers studied Daikin's inverter technology, compressor design, and precision manufacturing techniques, then methodically built their own capabilities. Over the following decade, Gree would develop 24 technologies independently assessed as "internationally leading," including ultra-low temperature digital systems, high-efficiency centrifugal chillers, and the proprietary G-Matrik low-frequency control technology. Perhaps most critically, Zhu built Landa Compressor as an in-house subsidiary, achieving vertical integration in the most expensive and technically demanding component of an air conditioner. Think of this as the equivalent of Apple designing its own chips instead of buying Intel processors—it was a bet on self-sufficiency that would pay enormous dividends.

But technical excellence alone does not build an empire. For that, Gree needed Dong Mingzhu. She arrived in 1990, a 36-year-old widow with a young son and zero sales experience. She had been working at a chemistry research institute in Nanjing before deciding, in a moment of personal reinvention, to move to Zhuhai and start over. The air conditioning business was rough territory for a newcomer, and Gree's sales operation was chaotic—dealers routinely took products on credit and then vanished, leaving the company with uncollectable debts. Dong's first assignment was to recover a 420,000 RMB debt from a delinquent dealer in Anhui province. She traveled there and essentially camped at the dealer's office for days, refusing to leave until payment was made. Through sheer persistence, she recovered 200,000 RMB and ensured the remaining products were returned. It was not elegant. It was not strategic. It was simply relentless. That first year, she generated 6.8 million RMB in personal sales—a figure that put seasoned colleagues to shame.

The experience in Anhui crystallized something in Dong's mind. The problem was not individual bad dealers; it was the system itself. Chinese appliance distribution in the 1990s was the Wild West—fragmented, disloyal, and prone to destructive price wars. In 1996, four of Gree's largest dealers in Hubei province began undercutting each other so aggressively that they were destroying the brand's pricing power. Dong's response was radical and, at the time, unprecedented in Chinese consumer goods. She convinced the competing dealers to merge their operations into a single joint-venture entity: Hubei Gree Air-Conditioning Sales Company. Gree held equity alongside the dealers, creating what she called an "interest community." The joint venture exclusively sold Gree products, unified pricing, distributed to second- and third-tier retailers, and shared profits. Cross-regional sales were strictly prohibited, enforced through a barcode tracking system that could trace every unit. Violators faced immediate supply cuts.

The results were staggering. In its first full year, the Hubei sales company generated 510 million RMB in revenue within a single province, with zero cross-regional leakage, and each dealer's dividend exceeded their initial investment. The model was rapidly replicated across roughly 30 provinces. This was the "Gree System"—and it was a masterwork of channel strategy. By binding dealers as equity partners rather than mere customers, Dong had created a private army of retailers whose financial interests were perfectly aligned with Gree's. The system delivered stable margins—Gree maintained around 36% gross margins compared to Midea's 31% and budget competitor Aux's 25%—while simultaneously reducing inventory risk. For a manufacturer, this was as close to a distribution moat as you could get. But moats, as we will see, can also become prisons when the landscape shifts.

III. The Golden Era and the Succession (2001–2012)

By the early 2000s, China's residential air conditioning market was exploding. Urbanization was accelerating at a pace the world had never seen—hundreds of millions of people moving into apartments that needed climate control. The market leader at the time was Chunlan, a brand that had dominated the 1990s. But Chunlan made a fateful mistake: it diversified. The company poured resources into motorcycles, trucks, and other products, spreading itself thin and losing focus on its core AC business. Dong Mingzhu watched this unfold and drew a lesson she would repeat like a mantra for the next two decades: "Gree is air conditioning." While competitors chased adjacent markets, Gree doubled down on a single product category with almost monastic discipline.

The strategy worked spectacularly. By the mid-2000s, Gree had overtaken Chunlan to become China's undisputed AC king, and by the end of the decade, it was the world's largest residential air conditioning manufacturer by volume. The company's production scaled from Zhu Jianghong's original 20,000 units per year to millions. Revenue grew from a few billion RMB to over 100 billion. The "Gree System" of dealer joint ventures had created a distribution network that competitors simply could not replicate—by the time a rival understood the model, Gree's dealers had been locked into equity partnerships for years. In China, where brand loyalty for appliances was notoriously fickle, Gree achieved something remarkable: a price premium. Consumers would pay 10 to 15 percent more for a Gree unit than for a comparable Midea or Haier product, because "Gree" had become synonymous with "unbreakable." The brand promise was simple and brutally effective: this machine will not fail.

Behind this promise sat Zhu Jianghong's relentless engineering culture. Under his leadership, Gree offered an industry-leading six-year free warranty—at a time when most competitors offered one or two years. This was not marketing gimmickry; it was a bet on quality. Every warranty claim that did not happen was pure margin. Every AC unit that ran for a decade without service became a walking advertisement. Zhu had essentially turned product reliability into a competitive weapon, and the economics were self-reinforcing: better quality meant fewer returns, fewer returns meant higher margins, higher margins funded more R&D, and more R&D produced even better quality.

In May 2012, Zhu Jianghong retired as chairman, and Dong Mingzhu formally succeeded him. In the annals of Chinese corporate history, this was a remarkably smooth transition—the quiet engineer handing the keys to the charismatic saleswoman. But it was also a fundamental shift in the company's personality. Zhu had been the soul; Dong would become the face. And what a face it was. Dong did not merely represent the brand; she consumed it. Her image appeared on Gree advertisements across China—on buses, billboards, and eventually on the startup screens of Gree-branded smartphones. She gave combative interviews, feuded publicly with competitors, and cultivated a persona that Chinese media dubbed the "Iron Lady"—a reference to Margaret Thatcher that Dong appeared to relish.

This was not vanity for its own sake, though vanity was certainly part of the equation. Dong understood something that few manufacturing CEOs grasp: in a commodity market, the brand needs a human face. Apple had Steve Jobs. Tesla had Elon Musk. Gree would have Dong Mingzhu. She became, in effect, the company's marketing budget. Every time she appeared on a talk show or made a provocative statement in the press, Gree received millions of RMB in free publicity. Her personal brand became inseparable from the corporate brand, and this created a powerful flywheel—but also a dangerous single point of failure, as we will see.

Under Dong's early chairmanship, Gree pushed hard on the narrative shift from "Made in China" to "Created in China." This was not just corporate messaging; it reflected a genuine technological evolution. Gree's R&D spending climbed steadily, and the company began winning national science and technology awards. The magnetic suspension variable-frequency centrifugal refrigeration compressor—a mouthful that essentially means "a massive, ultra-efficient cooling system for commercial buildings that floats its moving parts on magnets instead of oil"—was developed entirely in-house and recognized as a world-leading technology. For investors, the early Dong era was a golden period: revenue growth, margin expansion, and a stock price that compounded beautifully. But beneath the surface, a more difficult question was forming. When you already own 40 percent of the world's largest AC market, where exactly do you go next?

IV. Inflection Point #1: The Diversification Trap (2015–2018)

The ceiling problem is one of the oldest dilemmas in business strategy, and by 2015, Dong Mingzhu was staring directly at it. Gree's domestic AC market share hovered around 40 percent—a dominant position, but one that left very little room for organic growth in the core business. China's urbanization wave, while far from over, was maturing. The low-hanging fruit of equipping hundreds of millions of new apartments with their first air conditioner was giving way to a replacement cycle that was inherently slower and more competitive. Revenue had plateaued near the 100 billion RMB mark and then briefly declined—a humbling experience for a company accustomed to double-digit growth. The stock market noticed.

Dong's first diversification move was, in hindsight, baffling. In March 2015, Gree launched a smartphone. Not a partnership with an existing handset maker, not a white-label experiment—a full Gree-branded smartphone that Dong herself championed with the kind of intensity she normally reserved for air conditioning compressors. The first model was priced at 1,600 RMB, featured unremarkable specifications, and most infamously, booted up to a full-screen image of Dong Mingzhu's smiling face. The phone was a commercial disaster. In a market dominated by Huawei, Xiaomi, Oppo, and Vivo—companies that spent billions on mobile R&D and had built sophisticated software ecosystems—Gree's offering felt like an air conditioning company cosplaying as a tech firm. Subsequent iterations fared no better. By 2023, the smartphone team was quietly disbanded.

The smartphone episode was instructive not because the product failed—plenty of diversification attempts fail—but because of what it revealed about Gree's decision-making process under Dong. There was no market research suggesting consumers wanted a phone from an AC company. There was no strategic rationale linking smartphones to Gree's core competencies. What there was, by multiple accounts, was Dong's personal conviction that Gree could conquer any hardware category through sheer will and engineering prowess. The same force of personality that had been an asset in building the dealer network and driving quality improvements was now manifesting as an inability to distinguish between confidence and hubris.

But the smartphone was a sideshow compared to what came next. In August 2016, Gree announced its intention to acquire Zhuhai Yinlong New Energy, a maker of electric buses and lithium titanate batteries, for approximately 13 billion RMB. The deal would have been paid entirely in new Gree shares, diluting existing shareholders by roughly 25 percent. On paper, the strategic logic was not absurd—Yinlong's battery technology used lithium titanate oxide, which offers extreme durability (up to 30 years of battery life), fast charging, and operation in temperatures from minus 40 to plus 60 degrees Celsius. These were characteristics potentially relevant to Gree's HVAC business and to the broader energy storage market. But the price was eye-watering, the dilution massive, and Yinlong's financials were, to put it charitably, opaque.

What happened next was extraordinary by the standards of Chinese corporate governance. In November 2016, Gree's shareholders voted the deal down. This was not a quiet institutional investor grumble—it was a full-scale revolt. The stock market had already punished the announcement, and minority shareholders made clear that they were not going to rubber-stamp what they perceived as an overpriced vanity acquisition. It was the first major crack in Dong Mingzhu's aura of invincibility. She was visibly furious at the shareholder meeting, reportedly telling the assembled investors: "I have never asked shareholders for anything. I have given you dividends year after year. But you cannot see the future."

And then she did something that stunned the market. Dong personally invested approximately 2.6 billion RMB—her own money, supplemented by loans—to acquire a stake in Yinlong. She brought along a consortium of wealthy friends, including Wang Jianlin of Wanda Group and Liu Qiangdong of JD.com, who collectively invested 3 billion RMB. If the board would not let her buy Yinlong through Gree, she would buy it herself. This was the moment when Dong crossed a line that many CEOs contemplate but few actually cross: she began using personal capital to pursue strategic visions that the market had explicitly rejected. It was either visionary conviction or dangerous ego—and five years later, it would look far more like the latter, when Yinlong's largest original shareholder was prosecuted for embezzlement and Gree eventually acquired a 30 percent stake through judicial auction at a fraction of the original asking price.

The Yinlong saga left deep scars. It introduced genuine doubt about Dong's judgment among institutional investors, it demonstrated that Gree's governance mechanisms were only as strong as Dong's willingness to respect them, and it foreshadowed a pattern that would repeat: Dong identifying a strategic priority, meeting resistance, and then finding a way around that resistance through sheer force of will. For a company whose competitive advantage was built on discipline and focus, this was a troubling development. The iron lady who had told the world "Gree is air conditioning" was now spending billions on phones and electric buses, and the market was beginning to wonder whether the discipline had been Zhu Jianghong's all along.

V. Inflection Point #2: The Privatization

In April 2019, a brief announcement from the Zhuhai State-Owned Assets Supervision and Administration Commission sent shockwaves through Chinese capital markets. SASAC, which controlled Gree Group—itself the controlling shareholder of Gree Electric Appliances—announced its intention to sell its entire stake. After decades as a state-owned enterprise, Gree was about to become private.

The context matters enormously. By 2019, China was in the midst of a broader push toward "mixed-ownership reform"—a policy initiative encouraging private capital to take stakes in state enterprises to improve efficiency and governance. But selling control of the country's most valuable appliance manufacturer was something else entirely. Gree was not a struggling SOE in need of a turnaround. It was a crown jewel, throwing off billions in cash flow, paying generous dividends, and commanding enormous brand equity. The sale was partly ideological—a signal that the Zhuhai government trusted the private sector to run this asset better—and partly practical. SASAC had watched Dong Mingzhu's increasingly willful management style and perhaps concluded that the state's nominal control was already an illusion.

The bidding process attracted intense interest. Multiple consortia, including one led by Hopu Investment and another by Hillhouse Capital, submitted bids. The winner was Zhuhai Mingjun Investment Partnership, a consortium assembled by Zhang Lei, the founder of Hillhouse Capital and one of the most respected investors in Asia. Zhang, who had famously made early bets on JD.com and Tencent, was not a typical private equity buyer. His investment philosophy, articulated in his book "The Hillhouse Way," emphasized long-term value creation over financial engineering. He was buying Gree not to strip it for parts, but because he believed in the underlying business.

The deal closed in January 2020. Zhuhai Mingjun acquired 902.36 million shares—approximately 15 percent of Gree Electric—for 41.7 billion RMB, or roughly 46.17 RMB per share. Gree Group's stake dropped from 18.22 percent to approximately 3.22 percent, and crucially, no single entity remained as controlling shareholder. Gree had become what Chinese securities regulations call a "company without a controlling shareholder"—a status with profound implications for governance.

Was 46 RMB per share a good price? At the time, it implied a price-to-earnings multiple of roughly 13 to 14 times—a premium to Gree's then-trading levels, but not extravagant for a company with Gree's cash generation and market position. The real question was what Hillhouse was buying beyond the financial metrics. The answer was access to Dong Mingzhu. Unlike a typical PE acquisition where new owners install their own management team and demand operational changes, Hillhouse explicitly took a backseat. Zhang Lei gave Dong more autonomy, not less. The GP structure of the Zhuhai Mingjun consortium was designed in a way that gave Dong effective influence over how the 15 percent stake was voted. Through an entity called Zhuhai Xianying, in which she held a 41 percent income interest and significant voting influence, Dong could effectively direct the largest single block of shares without owning them directly.

This was a pivotal structural transformation. Before the privatization, Gree had been a state-owned enterprise with a strong CEO who frequently clashed with her government overseers. After the privatization, Gree was a nominally independent company with no controlling shareholder, led by a CEO who had consolidated more power than ever. The paradox of the Hillhouse deal was that it was advertised as "market reform" but in practice delivered something closer to "CEO entrenchment." For investors who believed Dong was the right leader for the next decade, this was excellent news. For those who worried about governance and succession, it was deeply concerning. Time would prove both camps partially right.

The privatization also marked the end of an era in terms of Gree's capital allocation philosophy. As an SOE, Gree had been an exceptionally generous dividend payer—partly because SASAC demanded it. The question now was whether a privately controlled Gree would maintain that discipline, or whether Dong would redirect cash flows toward her diversification ambitions. The answer, as it turned out, was "both"—Gree continued paying substantial dividends while simultaneously funding share buybacks, employee stock plans, and strategic investments. But the tension between these competing uses of capital would become a recurring theme.

VI. Inflection Point #3: The Midea Crisis and the Pandemic

The year 2020 was supposed to be Gree's victory lap. The privatization was complete, Dong Mingzhu had more power than ever, and the company was generating enormous cash flows. Instead, it became the year everything changed—and not in Gree's favor.

The COVID-19 pandemic hit China's appliance industry with devastating force in the first quarter. Factories shut down, installation crews could not enter customers' homes (and air conditioning, unlike a television, requires professional installation), and consumer spending cratered. Every AC maker suffered, but the pandemic exposed a vulnerability in Gree's business model that competitors had been quietly exploiting for years: the dealer network. Gree's entire go-to-market strategy depended on a physical retail infrastructure—showrooms, installers, regional sales companies. When physical retail shut down, Gree's revenue fell off a cliff. Meanwhile, Midea—which had been aggressively building its e-commerce capabilities since the mid-2010s—kept selling. Online orders could be placed instantly and fulfilled once lockdowns eased. The physical channel was a bottleneck; the digital channel was a buffer.

The numbers told a stark story. In 2020, Midea overtook Gree in overall AC market share for the first time—34.9 percent versus 32.7 percent. For a company that had defined itself as the undisputed market leader for nearly two decades, this was not merely a statistical shift; it was an identity crisis. The very dealer network that had been Gree's greatest competitive advantage—the "private army" that Dong Mingzhu had built through joint-venture partnerships—was now a structural liability in the e-commerce age. Midea's CEO, Fang Hongbo, a deliberately low-profile leader who had started his career editing Midea's internal company magazine, had executed a strategic pivot that was the mirror image of Gree's approach: diversify aggressively, embrace e-commerce early, and expand overseas to reduce dependence on the Chinese domestic market.

Dong Mingzhu's response to the pandemic was characteristically bold and characteristically controversial. On April 24, 2020, she conducted her first-ever livestream on Douyin, China's TikTok. It was a disaster. The internet connection was spotty, Dong was visibly uncomfortable with the format, and total sales came to just 220,000 RMB—roughly the price of a few dozen air conditioners. But Dong, as always, was undeterred by failure. She tried again on May 10, this time on the Kuaishou platform. Sixteen million viewers tuned in. Sales hit 100 million RMB in the first thirty minutes. By the end of the three-hour session, orders totaled 310 million RMB—nearly matching Gree's entire online sales for the previous year in a single evening.

What followed was a livestreaming blitz that rewrote the rules for CEO-led e-commerce in China. On June 1, Dong conducted a multi-platform session with participation from 30,000 brick-and-mortar stores, generating 6.54 billion RMB in orders. On June 18—China's annual mid-year shopping festival—she broke every record, moving 10.3 billion RMB worth of product in a single session. Across thirteen livestream events in 2020, Dong personally drove approximately 47.6 billion RMB in total orders. These were staggering numbers by any measure, and they transformed Dong's public image from "out-of-touch manufacturing boss" to "the most effective salesperson in Chinese e-commerce."

But the livestream revolution came at an enormous hidden cost: it was tearing apart the dealer network. The core issue was pricing. An air conditioner available through Dong's livestream for 1,999 RMB cost dealers 2,200 RMB to procure at wholesale. Physical retailers were being undercut by their own supplier's CEO. Dealers who had invested years of capital and effort into exclusive Gree showrooms watched helplessly as customers walked in, inspected the product, and then ordered it online at a lower price. Some dealers began purchasing directly from Gree's livestream studio rather than through the official wholesale channel—a complete breakdown of the distribution hierarchy.

The most dramatic signal came from Jinghai Internet, the shareholding platform that represented Gree's core regional sales companies—the very entities at the heart of the "Gree System." On June 19, 2020—the day after Dong's record-breaking 618 livestream—Jinghai announced its first share reduction plan in five years, selling approximately 0.71 percent of Gree's total shares. The message was unmistakable: the dealer alliance was losing confidence in Dong's channel strategy. By June 2022, Jinghai executed a massive block trade of 110 million shares at a steep discount, liquidating roughly 3.5 billion RMB in Gree stock. The "private army" was deserting.

Meanwhile, the competitive landscape continued to shift against Gree. Midea's 2016 acquisition of Kuka, the German industrial robotics firm, for approximately 4.66 billion euros was paying strategic dividends even as Kuka's financial performance disappointed. The deal gave Midea capabilities in automation, smart manufacturing, and Industry 4.0 that Gree lacked. Compare this with Gree's own diversification bet: the Yinlong battery investment, which had been plagued by governance scandals and management turmoil. In August 2021, after Yinlong's largest original shareholder was arrested for embezzlement, Gree finally acquired a 30.47 percent stake through judicial auction for 1.828 billion RMB—roughly one-seventh of the original 13 billion RMB price tag that shareholders had rejected five years earlier. It was a vindication of sorts for Dong's strategic instinct about the importance of energy storage, but the route to get there had been chaotic and value-destructive.

Gree's defensive response to the Midea threat also included a more disciplined acquisition. In 2021, Gree acquired a 38.78 percent stake in Zhejiang Dun'an Artificial Environment for approximately 2.2 billion RMB. Dun'an is a global leader in refrigeration components—four-way valves, expansion valves, the intricate parts that make HVAC systems function. Think of it as a plumbing supplier for the air conditioning industry. This was classic vertical integration: by controlling a key upstream supplier, Gree reduced its cost base, secured supply chain access, and extended its component capabilities into adjacent markets like heat pump thermal management. Compared to the Yinlong melodrama, it was a quiet, sensible deal that received a fraction of the press coverage but probably created more shareholder value.

VII. The "Hidden" Gree: Segments and High-Growth Bets

Strip away the headlines about Dong Mingzhu's livestreams and feuds, and a more nuanced Gree emerges from the financial statements—a company that is quietly placing a series of bets that could reshape its future, even as air conditioning continues to dominate the present.

As of the most recent annual filings, air conditioning still accounts for approximately 70 percent of Gree's revenue. The company reclassified its segment reporting in 2024, collapsing seven categories into five: Consumer Appliances (which merges AC with household products), Industrial Products and Green Energy, Intelligent Equipment, Other Main Businesses, and Other Businesses. The reclassification makes precise AC-only analysis harder, but the picture is clear enough: Gree remains overwhelmingly an air conditioning company, and that business continues to generate high margins. In fiscal year 2024, Gree posted revenue of 189.2 billion RMB—a 7.3 percent decline year-over-year—but net income actually grew 10.9 percent to 32.2 billion RMB, implying significant margin expansion and cost discipline. The net margin hit 17 percent, a remarkable figure for a hardware manufacturer selling what is essentially a commodity appliance.

The first "hidden" business worth examining is industrial components, anchored by Landa Compressor and Kaibang Motors. If Gree is the biggest air conditioning brand, Landa is the "Intel Inside" of the AC world—manufacturing the compressors that sit at the heart of air conditioning systems. To use a simple analogy: the compressor is to an AC unit what the engine is to a car. It is the most technically demanding and most expensive component. Landa does not just supply Gree; it sells compressors to Gree's competitors, making it a pick-and-shovel play on the entire Chinese HVAC market. Kaibang Motors performs a similar role for electric motors. These businesses are not glamorous, but they are highly profitable and strategically defensive—every competitor who buys a Landa compressor is effectively paying a toll to Gree.

The second bet is high-end equipment: CNC machines and industrial robotics. This segment has been growing at rates above 20 percent annually, though off a small base. The strategic logic connects back to Gree's manufacturing DNA—the same precision engineering that produces world-class compressors can be applied to machining equipment. The challenge is that this market is dominated by established Japanese and German firms (think Fanuc and Siemens), and Gree is still an early-stage player. The segment matters less for its current revenue contribution and more as a signal of where Dong Mingzhu wants to take the company.

The third and arguably most strategically important bet is semiconductors. In 2018, Gree established Zhuhai Lingbian Integrated Circuits—sometimes translated as "Gree Zero Boundary"—to design chips for air conditioning systems. To understand why an AC company would get into the chip business, consider this: a modern inverter air conditioner uses microcontroller chips to regulate compressor speed, power management chips to handle electrical conversion, and sensor chips to monitor temperature and humidity. Gree was spending roughly 4 billion RMB per year importing these chips, primarily from American and Japanese suppliers. In the context of escalating US-China trade tensions and the broader Chinese national push for semiconductor self-sufficiency, this dependency represented both a cost burden and a strategic vulnerability.

Gree's chip ambitions have expanded significantly since those early days. In 2019, the company invested 3 billion RMB for a nearly 11 percent stake in Wingtech Technology, which controls Nexperia—a Dutch semiconductor firm—giving Gree indirect access to advanced chip technology. By 2022, Gree had established a separate entity, Zhuhai Gree Electronic Components, focused specifically on third-generation silicon carbide, or SiC, chips. Silicon carbide is a semiconductor material that operates at higher voltages and temperatures than traditional silicon, making it ideal for power electronics in EVs, solar inverters, and—notably—high-efficiency HVAC systems. The SiC chip factory broke ground in late 2022, achieved production-line readiness by end of 2023, and Phase 1 is expected to reach full capacity of 240,000 six-inch SiC wafers annually by 2026. With a team of approximately 1,000 employees and cumulative chip sales exceeding 300 million units, this is no longer a side project—it is a genuine semiconductor operation.

And then there is what might be called Gree's "secret power": its balance sheet. As of the most recent reports, Gree sits on roughly 130 billion RMB in total cash and equivalents, with net cash of approximately 56 billion RMB after netting out all debt. The company has returned enormous sums to shareholders—cumulative dividends disbursed historically exceed 139 billion RMB, and share repurchases total approximately 27 billion RMB. Since 2020, Gree has bought back and cancelled roughly 384 million shares. The dividend yield frequently ranges between 4 and 7 percent, and the stock trades at a trailing price-to-earnings ratio around 8 times. For a company generating free cash flow in the range of 25 to 50 billion RMB per year, this makes Gree look less like a growth stock and more like—as one Hong Kong-based analyst memorably put it—"a bond with an AC factory attached."

VIII. Current Management and Incentive Structure

To understand Gree's governance in 2026, consider this thought experiment: imagine a Fortune 500 company where the CEO's face appears in every advertisement, where the most likely successors have all departed under acrimonious circumstances, where the board has no independent chairman, and where the largest shareholder block is structured in a way that gives the CEO effective control without proportionate ownership. Now ask yourself: is this a feature or a bug?

Dong Mingzhu directly owns approximately 0.73 percent of Gree Electric's shares. That is a modest stake for a CEO of a company valued in the hundreds of billions of RMB. But the Hillhouse privatization created a structure that gave Dong influence far exceeding her direct ownership. Through Zhuhai Xianying, a general partner entity in the Zhuhai Mingjun consortium, Dong holds a 41 percent income interest and significant board voting rights over the 15 percent stake that Hillhouse acquired. In practice, this means Dong can effectively direct the single largest block of shares while personally owning less than 1 percent. It is an elegant structure from Dong's perspective—maximum control, minimum capital at risk.

The departure of key lieutenants tells a story that no organizational chart can capture. Wang Jingdong, Gree's long-serving CFO and one of Dong's closest allies, resigned in August 2020. Huang Hui, who had served as CEO while Dong held the chairwoman title, departed in February 2021. Together with Dong, these three had formed what insiders called the "iron triangle" of Gree's leadership. The triangle's dissolution left Dong as the lone apex, with no clear second-in-command.

The succession drama escalated with the case of Meng Yutong, a young executive widely seen as Dong's protégée and potential heir. Meng was promoted rapidly within Gree's marketing organization and appeared alongside Dong in public appearances that many observers interpreted as a deliberate grooming process. But in May 2023, Meng departed the company amid reports of a public falling-out with Dong. The details remain murky, but the pattern is unmistakable: Gree has cycled through multiple potential successors without landing on one. Whether this reflects Dong's impossibly high standards, her reluctance to relinquish control, or simply the difficulty of following a once-in-a-generation leader is a matter of interpretation.

The employee share ownership plans launched in 2021 and 2022 provide another window into Gree's internal culture. On paper, ESOPs are standard corporate practice—give employees skin in the game, align interests with shareholders. But Gree's implementation drew controversy. The shares were offered at a 50 percent discount to market price, and Dong herself received 27.68 percent of the total allocation—an unusually large share for a single individual. The vesting conditions were aggressive: shares only converted if Gree hit specific profit growth targets in subsequent years. If the targets were missed, the shares were forfeited. This created what analysts called a "performance wall"—a sink-or-swim culture where the gap between hitting the target and missing it could mean the difference between a life-changing windfall and nothing. The design philosophy is pure Dong Mingzhu: no room for mediocrity, no prizes for participation.

The governance picture is further complicated by the absence of the checks and balances that typically exist in publicly traded companies. With no controlling shareholder, no strong independent board presence, and a dispersed institutional investor base, the practical constraint on Dong's decision-making is the stock price itself. If Gree's share performance deteriorates severely enough, activist pressure could theoretically mount. But in the Shenzhen A-share market, where retail investors dominate and activist campaigns are culturally and legally far less common than in New York or London, this is a relatively weak constraint. The result is a company that is, for better or worse, a one-woman show—a structure that has produced extraordinary operational results but carries extraordinary key-person risk.

IX. The Playbook: Strategic Framework Analysis

Hamilton Helmer's "7 Powers" framework offers a useful lens for understanding what makes Gree durable and where the cracks lie. Start with scale economies—Gree's most obvious structural advantage. The company operates the largest residential AC manufacturing base in the world, concentrated in southern China's Pearl River Delta, one of the most efficient manufacturing ecosystems on the planet. At Gree's volumes, the per-unit cost of everything from raw copper tubing to logistics is lower than any competitor can achieve. Midea is close, but Midea spreads its manufacturing across dozens of product categories; Gree's concentration in a single product magnifies its scale advantage in that specific category. For a new entrant trying to compete in residential AC, the cost gap is simply prohibitive.

Brand power is the second clear strength. In China, "Gree" occupies a cognitive position analogous to "Toyota" in automobiles or "Bosch" in power tools—it is the default choice for consumers who prioritize reliability over price. This perception was built over decades of Zhu Jianghong's quality obsession and reinforced by the six-year warranty that became an industry standard only after Gree proved it was viable. The brand commands a 10 to 15 percent price premium, which translates directly into margin advantage. Importantly, this brand power is primarily domestic. Outside China, Gree is known mainly as an OEM supplier; it has not achieved consumer brand recognition in the way that Haier has in the US or Midea has in Southeast Asia. This is both a limitation and an untapped opportunity.

The most provocative "power" in Gree's arsenal is what Helmer would call a "cornered resource"—and in this case, the resource is Dong Mingzhu herself. She is simultaneously the CEO, the brand ambassador, the chief salesperson, the primary dealmaker, and the public face of the company. No other Chinese appliance CEO commands remotely comparable media attention or consumer recognition. When Dong sells air conditioners on livestream, she generates billions in revenue that no subordinate could replicate. When she appears on a talk show, the brand benefits in ways that no advertising agency could manufacture. But a cornered resource is only an advantage as long as you have it. The day Dong Mingzhu retires—and she turned 71 in 2025—Gree loses its single most valuable marketing asset with no obvious replacement.

Turning to Porter's Five Forces, the picture grows more complex. Competitive rivalry is intense and getting worse. Midea is no longer a challenger—it is the market leader, with 2024 revenue of 409 billion RMB, more than double Gree's 189 billion. Midea's overseas revenue exceeds 40 percent of total sales, giving it geographic diversification that Gree lacks. In the first half of 2025, Midea's all-channel AC market share reached 29 percent compared to Gree's 17 percent—a gap that had been unimaginable a decade earlier. Xiaomi, meanwhile, has emerged as a disruptive force in the budget AC segment, capturing 15 percent of online AC market share by mid-2025. A brutal price war is, as one industry observer noted, always just one unusually hot summer away.

The bargaining power of buyers has shifted dramatically against Gree. In the dealer-dominated era, Gree controlled distribution and therefore controlled pricing. But as e-commerce platforms like JD.com, Alibaba's Tmall, and Pinduoduo have become dominant channels for appliance purchases, platform operators have gained significant pricing leverage. They can place Gree products alongside Midea and Haier products on the same screen, enabling instant price comparison. They can promote discounts during shopping festivals that compress margins. And they charge commissions that eat into the profitability that Gree's proprietary dealer network once preserved. The shift from owned distribution to platform distribution is structurally margin-negative for any brand, and Gree has been slower than Midea to adapt.

On capital allocation, the record is decidedly mixed. The cash generation is world-class—Gree has consistently produced free cash flow in the tens of billions of RMB per year, and the cumulative shareholder returns through dividends and buybacks are genuinely impressive. But the deployment of capital into non-AC ventures—smartphones, Yinlong, and various smaller bets—has destroyed value. The smartphone effort was a total write-off. The Yinlong investment, even at the reduced judicial auction price, has yet to deliver meaningful returns. The contrast with Midea's more disciplined (if imperfect) M&A strategy is stark. Midea's Kuka acquisition was expensive and initially disappointing, but it gave the company genuine capabilities in robotics and automation that are increasingly relevant. Gree's equivalent bets have been cheaper but less strategically coherent.

X. Conclusion: The Bull and Bear Case

Gree Electric Appliances in March 2026 presents one of the most polarized investment debates in Chinese equities. The bull case and the bear case are both compelling, and they hinge on the same central variable: Dong Mingzhu.

The bear case begins with what might be called the "single-key risk." Gree's brand, its dealer relationships, its media presence, and its strategic direction all run through one person. When that person departs—whether through retirement, health, or political developments—the entire edifice is at risk. There is no identified successor. Every promising candidate has left the company. The governance structure, far from mitigating this risk, amplifies it by concentrating control in Dong's hands. Add to this the competitive reality: Midea's revenue now approaches Gree and Haier combined, and the gap is widening. In online channels, where growth is concentrated, Gree's market share has been declining—falling from 18 percent in late 2024 to 17 percent by mid-2025, while Xiaomi gained ground rapidly. The dealer network, once an impregnable moat, has been damaged by the livestreaming pivot, with Jinghai Internet's share liquidation serving as a vote of no confidence. And the diversification attempts—smartphones, EVs, chips—have consumed capital and management attention without producing a meaningful second revenue pillar. At 70 percent AC concentration, Gree remains a one-product company in a market where the leader has already passed it.

The bull case is built on different foundations. Gree manufactures what is arguably the best residential air conditioner in the world, backed by proprietary compressor technology, a vertically integrated supply chain, and a brand that still commands a meaningful price premium in the world's largest AC market. The financial profile is extraordinary: net margins approaching 17 percent for a hardware company, a fortress balance sheet with 56 billion RMB in net cash, and a track record of returning capital to shareholders that few Asian manufacturers can match. The stock trades at roughly 8 times trailing earnings—a valuation that implies the market expects decline, which means that anything better than decline is potentially rewarded. The green energy transition is a genuine tailwind: heat pumps, which are essentially air conditioners that run in reverse, represent a massive global growth opportunity as Europe and Asia decarbonize building heating. Gree's thermal management expertise, combined with Dun'an Environment's components and Altainano's battery technology, positions the company well for this transition. And the semiconductor initiative, while still early, addresses a genuine strategic vulnerability and could become a meaningful profit center as China's domestic chip ecosystem matures.

For investors tracking Gree's trajectory, two KPIs matter above all others. The first is AC market share in online channels—this is the leading indicator of whether Gree is adapting to the structural shift in Chinese retail or falling further behind Midea and Xiaomi. The second is non-AC revenue as a percentage of total revenue, which measures whether the diversification efforts are finally gaining scale or whether the company remains locked into a single product category with limited growth. Together, these two metrics capture the essential tension at the heart of the Gree story: the battle between the legacy that made the company great and the future that demands it change.

Can a 20th-century manufacturing icon survive the 21st-century software-defined world? The answer, for Gree, will depend on whether the Iron Lady's successor—whenever that person emerges—can preserve the engineering discipline and brand equity that Zhu Jianghong and Dong Mingzhu built, while simultaneously embracing the digital channels and diversified revenue streams that the market now demands. It is the oldest question in business strategy, applied to one of China's most remarkable companies: how do you honor the past without becoming trapped by it?

References for Further Reading

- Regretless Pursuit — Dong Mingzhu's autobiography, providing first-person perspective on the dealer network's creation and early Gree culture.

- Jianghong Autobiography: 24 Years at the Helm of Gree — Zhu Jianghong's account of building Gree's engineering foundation.

- The Hillhouse Way — Zhang Lei's investment philosophy, essential context for the 2019 privatization deal structure.

- Gree Electric Annual Reports (2019–2024) — Focus on segment reclassification, industrial components growth, and cash flow statements.

- Caixin Global Archives — The definitive source for the Yinlong acquisition saga and ongoing governance debates.

- Daikin Industries Annual Reports — For comparative analysis of the 20-year joint venture relationship and its dissolution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube