POSCO Holdings: The Iron Throne of the Electric Age

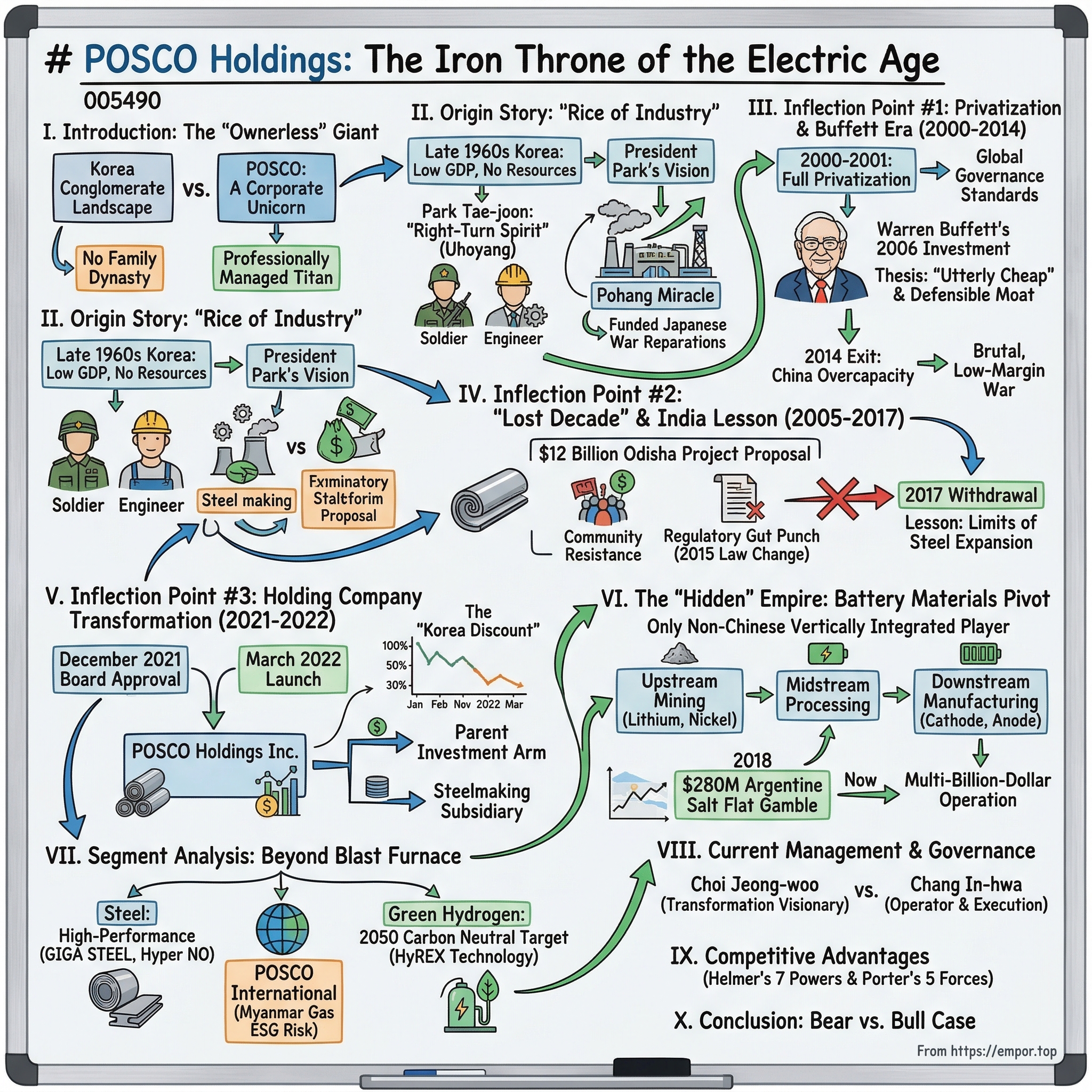

I. Introduction: The "Ownerless" Giant

Walk through the corridors of any major Korean conglomerate and you will feel the gravitational pull of a founding family. At Samsung, the Lee dynasty. At Hyundai, the Chungs. At LG, the Koos. These are the Chaebols—dynastic empires where bloodlines determine boardroom succession and where a founding patriarch's portrait hangs above every conference table. Now walk into the headquarters of POSCO Holdings in Gangnam, Seoul, and you will notice something conspicuously absent: there is no family portrait. There is no dynasty. There is no heir apparent nursing an MBA at Wharton while waiting for the throne.

POSCO is arguably the most important "ownerless" corporation in South Korea. Its largest shareholder is the National Pension Service, holding roughly eight percent. No individual, no family, no single entity calls the shots. This makes POSCO a corporate unicorn in the Korean landscape—a professionally managed industrial titan in a country where professional management is the exception, not the rule. And yet, for all its structural oddity, POSCO built the literal backbone of modern Korea. Every Hyundai car that rolled off a Ulsan assembly line, every Samsung shipyard hull, every LG refrigerator casing—the steel came from POSCO's furnaces. If Samsung is the brain of Korea Inc., POSCO is the skeleton.

But here is the question that makes this story worth telling in 2026: How does the world's most efficient steelmaker—a company synonymous with molten iron, blast furnaces, and coking coal—successfully reinvent itself as the only vertically integrated player in the global EV battery materials supply chain? How does a "boring" commodity business trading at a price-to-earnings ratio of four suddenly become the darling of every automaker scrambling to secure lithium, nickel, and cathode materials outside of China?

The answer involves a founding myth built on Japanese war reparations and a suicide pact. A decade-long debacle in the jungles of Odisha, India, that taught management the limits of steel expansion. A $280 million gamble on an Argentine salt flat that critics called reckless and that history has called one of the greatest capital deployment moves in mining. And a corporate restructuring in 2022 that split the company in two, finally forcing the market to see what management had been building in the shadows for years.

This is the story of POSCO Holdings—from the "Pohang Miracle" to the lithium age. And it begins, as all great Korean stories do, with a general, a president, and an impossible mandate.

II. Origin Story: "Rice of Industry"

Picture the Korean peninsula in the late 1960s. The country's per capita GDP was lower than Ghana's. There was no iron ore. No coking coal. No industrial capital to speak of. The World Bank had looked at a proposal for an integrated steel mill and flatly declared it "economically unfeasible." International lenders passed. Western steelmakers scoffed. South Korea, in their view, had no business making steel.

President Park Chung-hee saw it differently. Steel, he believed, was the "rice of industry"—the foundational commodity without which no modern economy could feed itself. You could not build cars, ships, bridges, or skyscrapers without it. And so, in 1968, he turned to a man he had known since their days at the Korean Military Academy: Park Tae-joon, a retired Major General with an engineer's mind and a soldier's tolerance for impossible odds.

Park Tae-joon's biography reads like a Korean epic. Born in Busan in 1927, he moved to Japan as a child, entered Waseda University, and returned to Korea after independence without graduating. He fought in the Korean War, participated in the 1961 military coup alongside Park Chung-hee, and rose to the rank of Major General. He was not a metallurgist. He was not a businessman. He was a military commander who understood logistics, discipline, and the art of turning chaos into order. On April 1, 1968, he was handed the mandate of a lifetime: build an integrated steel mill from scratch.

The money came from an unlikely source. Under the 1965 Korea-Japan normalization treaty, Japan agreed to pay reparations for its colonial occupation of Korea. From this pool, specific allocations were channeled to the steel project: $52.5 million from Japan's Export-Import Bank, $46 million from the Economic Cooperation Fund, roughly $29 million in commercial loans, and $24 million from other Japanese sources. Japanese firms Nippon Kokan and Nippon Steel Corporation supplied the critical technology and expertise. The irony was thick—Korea was using money and know-how from its former colonizer to build the industrial foundation of its independence.

Park Tae-joon's leadership style became the stuff of corporate legend. Standing on the construction site overlooking the East Sea, he reportedly told his team: "If we fail in the construction of this steel mill, let's all turn right and jump into Yeongil Bay." This was not metaphor. Pohang sits on Korea's southeast coast; turning right from the construction site meant marching directly into the ocean. It was a pledge to die rather than accept failure. This "Right-Turn Spirit"—Uhoyang in Korean—became POSCO's founding ethos. Workers gave up holidays. Engineers slept on-site. The construction proceeded with military precision.

Phase 1 of the Pohang plant was completed on July 3, 1973—one month ahead of schedule—with an initial crude steel capacity of 1.03 million metric tons per year. And then something remarkable happened: POSCO turned a profit in its very first year of operation. In an industry where new mills typically hemorrhage cash for years while ramping up, Pohang was profitable from day one. By 1981, the final Pohang expansion was complete, bringing capacity to 8.5 million tonnes annually.

The impact on Korea's industrial ecosystem was immediate and transformative. Hyundai Motors, which had been importing steel at enormous cost, suddenly had a domestic supplier providing high-quality material at competitive prices. Samsung's shipbuilding division, Daewoo's construction arm, and dozens of smaller manufacturers all fed from the same trough. POSCO did not just build a steel mill. It built the platform upon which the entire Korean economic miracle—the "Miracle on the Han River"—was constructed.

Park Tae-joon's legacy extended beyond steel. He founded POSTECH, the Pohang University of Science and Technology, which became one of Asia's premier research institutions. He created the Pohang Steelers soccer team. He entered politics, served in the National Assembly, and briefly served as Prime Minister in 2000 before resigning amid what courts later determined were politically motivated accusations. He died in December 2011, but his "Right-Turn Spirit" remains embedded in POSCO's corporate DNA—a reminder that the company was born not from commercial ambition but from national necessity.

But national necessity is a double-edged sword. The same state that gave POSCO its mandate also kept it on a leash. And as Korea's economy matured and the world changed, that leash would need to be cut.

III. Inflection Point #1: The Privatization and the Buffett Era (2000–2014)

For its first three decades, POSCO operated as an arm of the Korean government—efficient, disciplined, and deeply entangled with the state. The government held over seventy percent of its shares. Board appointments flowed through the Blue House. Strategic decisions reflected national industrial policy as much as shareholder value. This arrangement had served Korea well during the rapid industrialization era, but by the late 1990s, it was becoming a liability.

The Asian financial crisis of 1997 changed everything. The IMF bailout imposed sweeping structural reforms on Korea's economy, and among the conditions was the privatization of state-owned enterprises. POSCO was exhibit A. Partial privatization had actually begun in 1988, when the government reduced its stake through a public offering. In 1994, POSCO became the first Korean company listed on the New York Stock Exchange under the ticker PKX—a move that signaled ambition but not yet independence. The government still held a significant stake and still called the shots.

Full privatization came between 2000 and 2001, when the government divested its remaining direct holdings. Chairman Lee Ku-taek introduced professional management practices and global governance standards. POSCO was now, for the first time in its history, a fully independent corporation—answerable to shareholders, not to politicians. Or at least, that was the theory.

What happened next validated the privatization thesis spectacularly. POSCO's capital efficiency, already impressive under state ownership, improved further. The company invested in its Gwangyang works, which by the mid-2000s had become one of the world's largest single-site steel plants with crude steel capacity approaching 23 million tonnes per year. The combined Pohang-Gwangyang complex made POSCO one of the top five steelmakers globally by volume. More importantly, POSCO was not just making commodity steel—it was making the specialized, high-margin automotive steel that companies like Toyota, Hyundai, and Volkswagen needed for their vehicles.

This combination—massive scale, high capital efficiency, and a defensible niche in automotive-grade steel—caught the attention of an investor in Omaha, Nebraska. In 2006, Berkshire Hathaway began accumulating shares of POSCO, eventually building a position of roughly 3.5 million shares at a cost of approximately $572 million. By early 2007, Berkshire owned about four percent of the company, and the stake would grow to roughly five percent at its peak.

Why did Warren Buffett love a Korean steel mill? The reasoning was vintage Buffett. POSCO was, in his assessment, "utterly cheap"—trading at valuation multiples that dramatically underpriced its earnings power and asset base. This was not a macro bet on Korea or a thematic bet on steel. It was a specific-company-at-a-specific-price bet. POSCO had enormous barriers to entry (try building an integrated steel mill from scratch), massive moats in specialized automotive steel where switching costs kept customers locked in, and a level of capital efficiency that made Western steelmakers look wasteful. Buffett's investment was a ringing endorsement: this was a world-class business hiding in plain sight, penalized by geography and the market's allergy to anything labeled "commodity."

For several years, the thesis played out beautifully. POSCO's earnings were robust, dividends flowed, and the Buffett stamp of approval attracted a wave of institutional capital. But the Oracle of Omaha is also a pragmatist, and by 2014, the landscape had shifted dramatically.

China was the problem. Through the 2000s, China had embarked on the largest steel capacity buildout in human history, adding hundreds of millions of tonnes of annual production in a construction and infrastructure binge that defied all precedent. When China's domestic demand growth began to slow, that capacity did not disappear—it was dumped onto global markets at prices below the cost of production for most competitors. Steel became a brutal, low-margin war of attrition. POSCO's annual earnings fell roughly 59 percent from their peak. Margins compressed. The "moat" that Buffett had identified was being undermined not by a competitor copying POSCO's playbook, but by an entire nation flooding the market with cheap steel.

By the end of 2014, POSCO was no longer in Berkshire Hathaway's portfolio. Charlie Munger also reduced his personal stake. The exit was not a commentary on POSCO's management or operations—it was an acknowledgment that the structural economics of the global steel industry had changed in ways that even the most efficient producer could not fully offset. The China overcapacity era had begun, and it would last for years.

For POSCO's leadership, the Buffett exit was a wake-up call. If even the world's most patient long-term investor could not stomach the steel cycle anymore, then "more steel" was not a viable growth strategy. The company needed a Plan B. But first, it would learn a painful lesson about what Plan B should not look like.

IV. Inflection Point #2: The "Lost Decade" and the India Lesson (2005–2017)

In June 2005, POSCO signed a memorandum of understanding with the government of Odisha, a state on India's eastern coast, to build a 12-million-tonne integrated steel plant in Jagatsinghpur district. The price tag was $12 billion, making it the largest foreign direct investment proposal in Indian history at that time. The vision was breathtaking: a "Second POSCO" that would replicate the Pohang miracle on Indian soil, serving India's booming construction and automotive sectors with the same high-quality steel that had built Korea.

On paper, it looked like genius. India had vast iron ore reserves. Its economy was growing rapidly. Demand for steel was projected to soar for decades. And Odisha's state government was eager, committing 4,004 acres of coastal land and promising mining concessions for captive iron ore supply. POSCO's engineers drew up plans for what would have been one of the largest steel mills on Earth.

What happened over the next twelve years was a masterclass in the gap between grand strategy and local reality. The project area in Jagatsinghpur was not empty land. It sustained a betel-leaf-based economy supporting roughly 20,000 people across eight villages. These communities had no interest in being displaced, regardless of the rehabilitation packages offered. Villagers formed the POSCO Pratirodh Sangram Samiti—the Anti-POSCO People's Movement—and mounted sustained, organized resistance.

Land acquisition, which was supposed to be a formality, did not even begin until 2010—five years after the MOU was signed. The state's Industrial Infrastructure Development Corporation discovered that it did not actually have possession of a single acre of the committed land. Protests escalated. Clashes between pro-POSCO and anti-POSCO groups claimed five lives. International human rights organizations filed complaints with the OECD National Contact Point. Environmental clearances were challenged in court after court.

Then came the regulatory gut punch. In January 2015, India amended its Mine and Minerals Development and Regulation Act, requiring companies to obtain captive mining rights through competitive auctions rather than direct government allocation. The guaranteed iron ore supply that had been the economic foundation of the entire project was no longer guaranteed. Without captive ore, the mill's economics crumbled.

POSCO officially withdrew from the project in March 2017, having spent twelve years and untold management bandwidth on a venture that produced exactly zero tonnes of steel. The Odisha saga became a landmark case in the literature on community resistance to large-scale industrial development. But for POSCO's leadership, the lesson was more specific and more consequential: expanding "more of the same" globally—building bigger steel mills in new geographies—was no longer the path to outsized returns. The regulatory complexity, the social license challenges, the political volatility of resource-dependent projects in developing countries—all of it pointed to a fundamental truth. The future of POSCO could not be built on more blast furnaces.

What, then, could it be built on? The answer was already taking shape inside the company's research labs and strategic planning offices. And it had nothing to do with molten iron.

V. Inflection Point #3: The Holding Company Transformation (2021–2022)

By the early 2020s, POSCO was living a corporate double life. On one hand, it was still one of the world's premier steelmakers, producing roughly 40 million tonnes annually, dominating automotive steel, and running two of the most efficient integrated mills on Earth. On the other hand, it had spent the better part of a decade quietly building a battery materials business that was, by any measure, world-class. The problem was that nobody on Wall Street or in Yeouido could see it.

The "Korea Discount" is a well-documented phenomenon in global finance. Korean holding companies trade at an average discount of roughly 56 percent to their net asset value, penalized by opaque governance, complex cross-shareholdings, and the market's perception that minority shareholders are an afterthought. POSCO suffered from a particularly acute version of this malady. The market looked at POSCO and saw a steel company—full stop. The battery materials business, the lithium assets, the cathode technology, the hydrogen ambitions—all of it was buried inside the consolidated financials of a company that the market had categorized as a "dirty smokestack industry" stock. POSCO was trading at a price-to-earnings ratio of around four times. To put that in context, POSCO Future M—the battery materials subsidiary—would eventually trade at multiples several times higher on its own. The value was there. The market simply could not see it through the blast furnace smoke.

Chairman Choi Jeong-woo, who had taken the helm in July 2018, understood that incremental communication would not solve this problem. You could put out investor presentations, host analyst days, and trumpet your lithium assets until you were blue in the face—but as long as POSCO was structured as a single operating entity, the market would apply a steel multiple to the entire business. The solution was structural.

In December 2021, the board approved a plan to split POSCO into two entities. On January 28, 2022, shareholders voted overwhelmingly to approve the restructuring. And on March 2, 2022, POSCO Holdings Inc. officially launched as the parent and investment arm, while POSCO—the steelmaking unit—became a wholly owned subsidiary with a pledge that it would never be separately listed.

The logic was elegant. POSCO Holdings would function as a "Materials Platform"—deploying capital into battery materials, hydrogen, and other high-growth sectors, funded by the steady dividend stream from the steel subsidiary. The steel business would continue doing what it did best: generating cash. But that cash would no longer be trapped inside a structure that the market valued at commodity multiples. Instead, it would flow upward to the holding company, which could allocate it toward ventures that the market was willing to value at growth multiples.

The restructuring was advised by PwC, and management laid out an ambitious vision: triple the group's corporate value from approximately KRW 40 trillion by aggressively scaling EV battery materials and hydrogen production. The holding company structure also addressed a governance concern. Without a controlling family, POSCO's management had always faced tension between the steel division's demand for reinvestment and the growth businesses' need for capital. The split gave each side its own economic logic and its own accountability.

Whether the market has fully rerated POSCO Holdings remains an open question. The Korea Discount has not disappeared, and cyclical headwinds in both steel and lithium have complicated the narrative. But the structural foundation is now in place. And the crown jewel of that structure—the battery materials empire—deserves its own chapter.

VI. The "Hidden" Empire: The Battery Materials Pivot

To understand why POSCO Holdings matters in the electric vehicle era, you need to understand a simple fact about the battery supply chain: it is fragmented, geographically concentrated, and deeply vulnerable to geopolitical disruption. Most lithium comes from Australia, Chile, and Argentina. Most of it is refined in China. Most cathode and anode materials are manufactured in China, Japan, or South Korea. Most battery cells are assembled in China. At every stage, different companies control different pieces. No single non-Chinese company controls the full chain from mine to finished battery material.

Except one. POSCO Holdings, through its subsidiaries and joint ventures, is the only company in the world that participates at every stage of the battery materials value chain: from upstream lithium and nickel mining, through midstream processing of lithium hydroxide and precursor materials, to downstream manufacturing of cathode active materials and anode materials. This vertical integration is not a marketing claim—it is an operational reality, and it is the single most important strategic asset the company possesses.

The story begins in a vast, blindingly white salt flat in northwestern Argentina called the Salar del Hombre Muerto—the "Salt Flat of the Dead Man." In May 2018, POSCO entered an agreement with Galaxy Resources, an Australian mining company, to acquire the northern tenement package at this site for $280 million. The tenements contained approximately 1.58 million tonnes of lithium carbonate equivalent in measured and indicated resources, with a total resource base of 2.54 million tonnes.

At the time, the deal was met with skepticism. Two hundred and eighty million dollars was a significant sum for brine rights in a remote corner of Argentina, a country with a long history of political instability, capital controls, and resource nationalism. Critics argued that POSCO, a steelmaker, had no business venturing into lithium mining. The word "overpaid" was used freely.

History has rendered a different verdict. The total investment in the Argentine operation—now called the "Sal de Oro" complex—has grown to over $4 billion as POSCO has expanded processing capacity and infrastructure. In October 2024, Argentina's first commercial lithium hydroxide production plant was inaugurated at the General Guemes Industrial Park in Salta Province, with an initial capacity of 25,000 tonnes per year and an investment exceeding $800 million. Phase 2 targets 50,000 tonnes per year, with a dual lithium hydroxide and lithium carbonate production target of 100,000 tonnes per year by 2027. POSCO Argentina secured a $668 million loan for the second phase expansion. What began as a $280 million acquisition has become a multi-billion-dollar operation that gives POSCO a captive, non-Chinese source of lithium—a commodity that every automaker on Earth is scrambling to secure.

The Argentine gamble is one of the great capital deployment stories in recent mining history. But lithium is only one piece of the puzzle. The real crown jewel of POSCO Holdings is POSCO Future M, the subsidiary that transforms raw materials into the cathode and anode products that go inside EV batteries.

POSCO Future M has one of the most improbable corporate origin stories in Korean industry. It was founded in 1963 as Samhwa Hwasung Co., a manufacturer of alkaline refractories—essentially, the heat-resistant bricks that line the insides of blast furnaces. For decades, it was a prosaic industrial supplier. It merged with Pohang Furnace in 1994. It was renamed POSCO Chemtech in 2010. And then, under the umbrella of POSCO's battery materials strategy, it was systematically transformed into a global leader in cathode active materials. In March 2023, the company was renamed POSCO Future M—a signal that the bricks-and-mortar past was definitively behind it.

Today, POSCO Future M produces NCM (nickel-cobalt-manganese), NCMA (nickel-cobalt-manganese-aluminum), and NCA (nickel-cobalt-aluminum) cathode active materials. It manufactures silicon-based anode materials. It is investing in solid-state battery materials. And critically, it has built the precursor manufacturing capability that allows it to offer automakers a fully integrated, mine-to-cathode supply chain—something no other non-Chinese company can match.

The joint ventures tell the strategic story. In July 2022, POSCO Future M and General Motors established Ultium CAM, a cathode active materials joint venture majority-owned by the Korean company. In June 2023, the partnership expanded with a second phase projected to exceed $1 billion, building an integrated CAM and precursor CAM processing complex in North America with production capacity supporting 360,000 EVs annually. The critical detail: POSCO Future M has built a China-free cathode material supply chain through this facility—Argentine lithium, processed in-house, manufactured into cathode materials in North America, all without touching Chinese supply chains.

This matters enormously because of the Inflation Reduction Act. Starting in 2027, vehicles using Chinese-sourced graphite and other critical minerals lose eligibility for federal EV tax credits in the United States. The IRA effectively draws a line between battery materials sourced from China and materials sourced from allied nations. POSCO, with its Argentine lithium, its Australian nickel interests, its Indonesian processing, and its North American manufacturing JVs, sits squarely on the right side of that line. It is arguably the single biggest non-Chinese beneficiary of the IRA's supply chain requirements.

In April 2024, POSCO Future M reached a basic agreement with Honda to produce cathode materials for automotive batteries in Canada, alongside Honda's CAD $15 billion EV plant in Alliston, Ontario, targeting 240,000 units per year with operations beginning in 2028. The partnership covers cathode materials, anode materials, and next-generation battery technologies.

The vertical integration strategy also extends to nickel. POSCO has invested in nickel processing operations in Indonesia and Australia, securing supply of the other critical cathode input. A $470 million anode supply deal with a major U.S. carmaker further underscores the breadth of the offering.

For investors, the battery materials pivot raises a fundamental question: what is this business worth inside the holding company structure? POSCO Future M trades publicly on the Korean market, so there is a market-based answer. But the holding company's ownership stake, combined with the captive lithium supply and the JV economics, creates a sum-of-the-parts valuation that is significantly more complex—and potentially significantly higher—than what the consolidated POSCO Holdings stock price implies. The question is whether the Korea Discount will eventually yield to the sheer scale of what has been built.

VII. Segment Analysis: Beyond the Blast Furnace

The battery materials story is compelling, but it is funded by a business that still accounts for the majority of POSCO Holdings' revenue: steel. And the steel business is not merely a cash cow waiting to be milked dry. It is, in its own right, one of the most technologically sophisticated steelmaking operations on the planet.

The Pohang and Gwangyang works remain among the largest single-site integrated steel mills in the world. Gwangyang alone has crude steel capacity of approximately 23 million tonnes per year. Pohang, the original mill, runs at 8.5 million tonnes. Together, they give POSCO a combined capacity that places it among the global top five steelmakers by volume. But volume is not what makes POSCO's steel business special—product mix is.

POSCO has spent decades developing what it calls its "eight core strategic product system," a portfolio of ultra-high-performance steels designed for applications where generic commodity steel simply will not do. The flagship product is GIGA STEEL, an advanced high-strength steel with a tensile strength of 1.5 gigapascals. To put that in non-engineering terms: a small plate of GIGA STEEL, roughly 150 square centimeters, can support the weight of 1,500 mid-size cars. This is the steel that goes into the safety-critical structural components of modern automobiles—the pillars, crash beams, and underbody reinforcements that protect passengers in a collision.

The automotive steel market is POSCO's most defensible franchise. Every one in ten cars produced globally uses POSCO steel, and the switching costs for automakers are enormous. Automotive steel is not a commodity that can be swapped out based on the lowest bid. Each grade is developed in close collaboration with the automaker's engineering team, tested over years, and qualified through rigorous certification processes. Once a POSCO steel grade is designed into a vehicle platform, it stays there for the life of that platform—typically five to seven years. This creates a recurring revenue stream with built-in pricing power that looks nothing like the spot market commodity steel that gives the industry its terrible reputation.

POSCO has also developed Hyper NO, a non-oriented electrical steel specifically designed for the motors in electric vehicles. As the automotive industry transitions from internal combustion to electric powertrains, the demand for high-performance electrical steel is growing rapidly. POSCO is positioning itself to supply both the battery materials and the motor steel for the same EV—a dual revenue stream from a single customer relationship.

Beyond steel, POSCO International—the group's trading arm, which was formed from the acquisition of Daewoo International—operates as a diversified conglomerate within the conglomerate. Its most valuable asset has historically been the Shwe gas field complex in Myanmar, where POSCO International holds production-sharing contracts for blocks that have been producing natural gas since the mid-2000s, supplying both Myanmar and China through a 793-kilometer pipeline averaging 500 million cubic feet per day.

The Myanmar gas operations have become a significant ESG liability. Following the February 2021 military coup, international criticism intensified over whether the revenue from these operations was effectively funding the junta. POSCO International has navigated this controversy carefully, but the reputational risk remains material. The subsidiary has also exited its Myanmar rice business as of early 2026, classifying the operation as an asset held for sale—a signal that the group's appetite for Myanmar exposure is diminishing.

The third strategic pillar—and the most speculative—is green hydrogen. POSCO declared a target of carbon neutrality by 2050 and has laid out a hydrogen production roadmap that is, by any measure, enormously ambitious. The plan calls for boosting by-product hydrogen capacity to 70,000 tonnes per year by 2025, scaling to 500,000 tonnes of "blue hydrogen" by 2030, reaching 2 million tonnes of "green hydrogen" by 2040, and hitting 5 million tonnes by 2050 with a target of KRW 30 trillion in hydrogen sales revenue.

The enabling technology is HyREX—Hydrogen Reduction Ironmaking—POSCO's proprietary process for producing steel using hydrogen instead of coal. A test facility with 300,000-tonne annual capacity is targeted for completion by 2027 to validate commercial viability. If HyREX works at scale, POSCO would be able to use its own demand for "green steel" to bootstrap a green hydrogen economy, creating internal demand that justifies the enormous capital required for hydrogen production infrastructure. It is a self-reinforcing loop: make hydrogen to make green steel, use the green steel profits to fund more hydrogen production, sell the surplus hydrogen to other industries.

The partnership with Australia's Fortescue Metals Group for green hydrogen projects using renewable energy adds an international dimension to this ambition. But it is important to be clear-eyed: green hydrogen at industrial scale remains unproven and economically challenged. The 2050 target is aspirational, and the capital requirements are staggering. This is a bet on the direction of global decarbonization policy, not a near-term earnings driver.

For investors tracking POSCO Holdings, the segment mix creates a layered risk-return profile. Steel provides cash flow stability and automotive-grade pricing power. Battery materials provide the growth narrative and geopolitical positioning. Hydrogen provides the long-duration optionality. The question is whether a single holding company structure can effectively manage all three without the internal competition for capital becoming dysfunctional—a question that the "ownerless" governance structure makes both more interesting and more uncertain.

VIII. Current Management: The "Professional" Era

In a country where corporate succession is typically a family affair, POSCO's leadership transitions unfold more like political campaigns—complete with internal candidates, board deliberations, and the ever-present shadow of the National Pension Service casting its vote. Understanding who runs POSCO, and why, requires understanding the unique governance dynamics of Korea's most prominent ownerless corporation.

Choi Jeong-woo, the man who orchestrated the holding company transformation, came from deep within the POSCO system. Born in 1957 in Busan, he studied economics at Pusan National University and joined POSCO in 1983 as a finance department recruit. His career was entirely within the POSCO Group—spanning roles at POSCO's Finance Office, POSCO Construction, POSCO International, and POSCO Future M. He became Head of the Finance Department in 2006 and was appointed CFO in 2015, leading a group-wide restructuring that rationalized non-core assets and tightened capital discipline.

When Choi was appointed Chairman in July 2018, the company was at a strategic crossroads. The India debacle was freshly behind it. Buffett had been gone for four years. The steel business was profitable but uninspiring. And the battery materials opportunity was emerging but embryonic. Choi's contribution was to take what had been a collection of scattered initiatives—a lithium acquisition here, a cathode joint venture there—and weave them into a coherent corporate strategy with the holding company restructuring as the structural capstone.

He also built POSCO's international credibility, being elected Chairman of the World Steel Association in October 2022—a recognition that POSCO was not just another steelmaker but a standard-setter for the industry. Choi declined to seek a third term and stepped down in March 2024, amid the kind of gentle political pressure that is endemic to Korea's ownerless corporations.

His successor, Chang In-hwa, brings a dramatically different profile. Born in 1955, Chang is an MIT-trained ocean engineer—he holds a PhD in Ocean Engineering from the Massachusetts Institute of Technology and a master's in Naval Architecture from Seoul National University. He joined POSCO's affiliated Research Institute of Industrial Science and Technology (RIST) in 1988 and built his career across the group's research and operations functions, including a stint as Head of POSCO's Steel Division in 2018.

Chang was selected from six candidates and confirmed by shareholders in March 2024. His early messaging has emphasized austerity—"tightening belts"—targeted M&A within three years, and operational discipline. Where Choi was the visionary who laid the strategic foundation, Chang appears to be the operator who will be expected to execute and, critically, to deliver returns from the billions already invested in battery materials and hydrogen.

The governance structure that produces these leaders is both POSCO's greatest strength and its most persistent vulnerability. The National Pension Service, holding roughly 8.29 percent of issued common shares as of early 2025, is the largest single shareholder. BlackRock and Vanguard hold meaningful positions. The board comprises ten members—six outside directors and four inside—and management has moved toward Long-Term Incentive Plans tied to enterprise value rather than steel tonnage, a subtle but important shift that aligns executive compensation with the holding company's diversification strategy.

But the "ownerless" structure also means that every Korean presidential transition brings a fresh round of political pressure on POSCO's leadership. The Blue House has historically treated POSCO's chairmanship as a quasi-political appointment, and while the professionalization of the board has created some insulation, the risk of political interference remains. Every change of government in Seoul prompts the question: will the new administration try to install its own person at POSCO? This is not a theoretical risk—it is a recurring feature of POSCO's corporate life, and it introduces a governance discount that purely financial analysis cannot fully capture.

IX. The Playbook: Hamilton's 7 Powers and Porter's 5 Forces

To assess whether POSCO Holdings' transformation will create durable value, it helps to apply the frameworks that serious investors use to distinguish between genuine competitive advantages and clever narratives that collapse under scrutiny.

Hamilton Helmer's 7 Powers

Start with Cornered Resource. POSCO's Argentine lithium assets—the Sal de Oro complex—represent a genuine cornered resource in the Helmer sense. High-quality lithium brine deposits are geologically scarce, take years to develop, and require both technical expertise and sovereign relationships to operate. POSCO secured these assets for $280 million and has since invested over $4 billion in development. A competitor cannot replicate this position by simply spending money—the resource is finite, the permits are granted, and the development timeline creates a multi-year head start. The Australian nickel interests add another layer. In a world where every automaker is scrambling for non-Chinese battery material supply, these resources are not just assets on a balance sheet—they are strategic leverage.

Scale Economies are self-evident in the steel business. The Gwangyang and Pohang works are among the largest single-site steel mills on Earth, and their cost structure reflects decades of continuous optimization. In battery materials, POSCO Future M's vertical integration creates scale advantages that are harder to see but equally real: by controlling precursor manufacturing, cathode production, and upstream raw materials, the company captures margin at multiple stages of the value chain rather than competing on a single node. This is the battery materials equivalent of being a vertically integrated oil major in an industry of refineries and gas stations.

Switching Costs are perhaps POSCO's most underappreciated power. In automotive steel, the switching costs are enormous—years of co-development, qualification testing, and platform-specific steel grades create lock-in that persists for the life of a vehicle platform. In battery materials, the dynamic is similar. Cathode chemistries are not interchangeable. Each automaker's battery pack is designed around specific cathode specifications, and qualifying a new supplier takes 18 to 24 months of testing. The JVs with GM and Honda are not mere supply agreements—they are deep technical partnerships that create mutual dependency.

Process Power is emerging in the hydrogen strategy. HyREX, the proprietary hydrogen reduction ironmaking technology, has the potential to create process power if it achieves commercial viability—a fundamentally different and lower-carbon way of making steel that competitors cannot easily replicate. This remains speculative, but the R&D investment is real.

Porter's Five Forces

The Threat of New Entrants in integrated steelmaking is effectively zero. The capital requirements, the technical expertise, the decades of process optimization, and the environmental permitting barriers make it virtually impossible for a new competitor to build a greenfield integrated steel mill and compete with POSCO on cost. In battery materials, the barriers are lower but still significant—particularly for the vertically integrated, mine-to-cathode model that POSCO has built.

The Threat of Substitutes deserves nuanced treatment. In automotive steel, the primary substitute threat comes from aluminum, which is lighter and increasingly favored for vehicle weight reduction. POSCO has addressed this directly with GIGA STEEL—ultra-high-strength steel that achieves equivalent weight savings through thinner gauges while maintaining superior crash performance. The argument is that you do not need to switch to aluminum if steel can be made strong enough to use less of it. In battery materials, the substitute threat is more about chemistry evolution—the shift from NCM to LFP (lithium iron phosphate) cathodes, the emergence of sodium-ion batteries, and the long-term promise of solid-state. POSCO Future M's investment in multiple cathode chemistries and solid-state research provides some hedge, but the pace of battery technology evolution is the single largest uncertainty in this business.

Bargaining Power of Buyers is high in steel—Toyota, Hyundai, and Volkswagen are sophisticated purchasers with enormous leverage. But in battery materials, the dynamic is inverted. The automakers need POSCO more than POSCO needs any single automaker, because the supply of IRA-compliant, non-Chinese cathode materials is structurally scarce. This is the strategic insight behind the entire battery materials pivot: in a world of abundant steel supply and scarce battery material supply, moving up the value chain shifts the bargaining power from buyer to supplier.

Bargaining Power of Suppliers is mitigated by vertical integration. POSCO mines its own lithium. It processes its own precursors. It makes its own cathode. This eliminates the most dangerous supply bottleneck—dependence on Chinese processing—and gives POSCO cost visibility and margin control that non-integrated competitors lack.

Competitive Rivalry remains intense across all segments. In steel, ArcelorMittal, Nippon Steel, and Chinese state-backed producers are formidable competitors. ArcelorMittal operates at roughly twice POSCO's market capitalization (approximately $36 billion versus $16 billion) and has a more globally diversified footprint. Nippon Steel, at roughly $23 billion in market cap, is POSCO's closest peer in terms of product quality and automotive steel focus—and its pending acquisition of U.S. Steel would significantly alter the competitive landscape in North America. In battery materials, the competition is primarily Chinese: CATL, BYD, and a constellation of Chinese cathode and anode producers who benefit from massive state subsidies and lower labor costs. POSCO's edge is not cost—it is compliance and geopolitical positioning.

The KPIs That Matter

For investors tracking POSCO Holdings' ongoing performance, two metrics cut through the noise. First, battery materials revenue as a percentage of total group revenue—this is the single best measure of whether the transformation is translating from strategy decks to income statements. As this number rises, it signals that the holding company's growth thesis is materializing and that the sum-of-the-parts valuation gap should narrow. Second, consolidated operating margin—because the holding company's ability to generate value depends on maintaining steel profitability while scaling the higher-margin (but capital-intensive) battery materials business. A rising operating margin would signal that the product mix shift is working; a declining margin would suggest that the growth investments are dilutive rather than accretive.

X. Conclusion: The Bear vs. Bull Case

Every investment thesis has a mirror image, and POSCO Holdings' is no exception. The bear case and the bull case both rest on legitimate arguments, and the interplay between them defines the risk-return profile of this company.

The Bear Case

The "ownerless" curse is real. Every Korean presidential transition brings the risk of political interference at POSCO. The Blue House has historically treated the chairmanship as a lever of industrial policy, and while governance reforms have created some insulation, the structural vulnerability remains. A politically motivated leadership change could derail the battery materials strategy at a critical juncture.

The EV market's cyclicality has proven harsher than many anticipated. Lithium prices, which surged past $80,000 per tonne in late 2022, collapsed below $15,000 by 2024 as Chinese producers flooded the market and EV demand growth rates decelerated in several key markets. POSCO's Argentine lithium economics remain viable at current prices given the scale of the resource, but the returns on the $4 billion-plus invested are significantly lower than what the 2022 price environment implied. Chinese lithium dumping—producing and exporting at below-cost prices to maintain market share—is a structural threat that POSCO cannot control.

The Korea Discount may prove permanent. Despite the holding company restructuring, POSCO Holdings still trades at a significant discount to the sum of its parts. If the market refuses to rerate the stock—because of governance concerns, conglomerate complexity, or simple geographic bias—then the strategic value being created in battery materials may never be fully reflected in the holding company's stock price. Shareholders in POSCO Holdings are, in a sense, making a bet not just on the business but on the market's willingness to recognize value in a Korean holding structure.

The financial results tell a sobering near-term story. Revenue in 2024 was approximately KRW 72.7 trillion, down nearly 6 percent year-over-year. Operating profit fell 38 percent to KRW 2.2 trillion. Net profit dropped nearly 49 percent to KRW 948 billion, burdened by KRW 1.3 trillion in non-cash losses from valuation adjustments and restructuring. Preliminary 2025 results showed revenue declining another 5 percent with operating margins around 5 percent. For a company asking the market to value it as a growth platform, these are sobering numbers.

The Myanmar gas operations remain an ESG overhang. While POSCO International is reducing its Myanmar exposure, the reputational damage from perceived association with the military junta has not fully dissipated, and ESG-focused institutional investors continue to flag it as a concern.

The Bull Case

The bull case rests on a simple but powerful structural argument: if you believe in the long-term adoption of electric vehicles but do not know which automaker will win, you buy the company that owns the lithium, processes the precursors, and manufactures the cathode. POSCO Holdings is the picks-and-shovels play for the EV revolution—the company that supplies the critical materials regardless of whether Tesla, GM, Hyundai, Honda, or some yet-unknown Chinese competitor captures the end market.

The IRA positioning is a genuine strategic moat. As 2027 approaches and Chinese-sourced battery materials become ineligible for U.S. federal EV tax credits, every automaker with North American production will need IRA-compliant cathode and anode supply. POSCO Future M's China-free supply chain, combined with the GM and Honda joint ventures, positions it as one of a very small number of suppliers that can meet this requirement at scale. This is not a temporary advantage—it is a regulatory-driven structural shift that will persist for as long as U.S.-China trade tensions continue, which is to say, for the foreseeable future.

The vertical integration from mine to cathode creates margin resilience that single-node competitors cannot match. When lithium prices fall, POSCO's mining operations take a hit—but its downstream processing and cathode manufacturing benefit from lower input costs. When lithium prices rise, the mining operations surge. This natural hedge does not eliminate cyclicality, but it dampens it significantly compared to a pure-play lithium miner or a pure-play cathode producer.

The steel business remains a world-class cash generator with deep automotive relationships, and the GIGA STEEL and Hyper NO product lines position it to benefit from, rather than be disrupted by, the automotive transition to EVs. The hydrogen optionality, while speculative, represents asymmetric upside: if HyREX achieves commercial viability, POSCO would be positioned at the intersection of two massive decarbonization trends—green steel and green hydrogen—with proprietary technology and captive demand.

Final Reflections

In 1968, Park Tae-joon stood on a barren stretch of Korean coastline and made a suicide pact with his team. They would build the "rice of industry" or die trying. They built it. That rice fed the Korean economic miracle for half a century. Now, his successors stand on a different frontier—not a coastal plain but an Argentine salt flat, not blast furnaces but cathode reactors—and they are making a different bet. The rice of the 21st century is not steel. It is lithium, nickel, and the cathode materials that will power the electric age.

Whether POSCO Holdings can navigate the Korea Discount, the lithium price cycle, and the geopolitical chess game of battery supply chains remains to be seen. But the company has done something that very few industrial incumbents manage: it has looked at its own obsolescence, stared it in the face, and built a credible path to relevance in a fundamentally different world. From the Pohang Miracle to the Sal de Oro complex, from Park Tae-joon's Right-Turn Spirit to Chang In-hwa's austerity agenda, the through-line is the same: an ownerless corporation, built on national necessity, perpetually reinventing itself to remain indispensable.

XI. Top 10 Reference Links

- POSCO Holdings 2030 Vision Report — The blueprint for the seven core businesses and the holding company's capital allocation framework.

- The Life of Park Tae-joon (Biography) — The definitive account of the "Andrew Carnegie of Korea" and the founding of POSCO.

- Berkshire Hathaway 2007 Shareholder Letter — Warren Buffett's original thesis on POSCO and the reasoning behind the investment.

- S&P Global: The Battle for Lithium — Analysis of the Argentine lithium acquisition and its implications for global battery supply chains.

- POSCO Future M Investor Day Presentation — Deep dive into cathode and anode material roadmaps, JV structures, and capacity expansion plans.

- The "Right-Turn" Spirit: A History of POSCO (Corporate Documentary) — The founding narrative and its enduring influence on corporate culture.

- World Steel Association Rankings — Benchmarking POSCO's efficiency, product mix, and volume against Nippon Steel and ArcelorMittal.

- The 2022 Holding Company Split FAQ — Direct management commentary on the rationale, mechanics, and expected benefits of the restructuring.

- IRA (Inflation Reduction Act) Impact Study — Why POSCO is the biggest non-Chinese winner of the U.S. battery supply chain incentive framework.

- K-Business Governance Report — Analysis of "ownerless" companies in the Korean stock market and the implications of the Korea Discount for long-term investors.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube