Midea Group: The Invisible Giant of Global Industry

I. Introduction: The $60 Billion Behemoth You Already Own

Walk into any kitchen in America. Open the microwave. Glance at the air conditioner humming in the window. Check the label on the toaster. Even if it says Toshiba, or Eureka, or Teka on the outside, there is a startlingly high chance that the machine was designed, engineered, and assembled by a company most Western consumers have never heard of: Midea Group.

This is a company that generated over 400 billion renminbi in revenue in 2024, roughly $56 billion at prevailing exchange rates, making it one of the largest appliance manufacturers on the planet. It employs nearly 200,000 people across more than 200 countries. It is the world's number one producer of major household appliances by volume.

And yet, at industry conferences in the West, the reaction to Midea's name is often a polite blank stare followed by, "Wait, who?"

That anonymity is not an accident. It is, in many ways, the strategy itself.

Midea is the original equipment manufacturer behind the curtain. It is the company behind the company, the factory that builds the products other brands slap their names on. But over the past decade, something remarkable has happened. Midea stopped being content as the invisible workshop. It began acquiring the brands, the patents, and the robotics technology that would transform it from a contract manufacturer into a vertically integrated technology conglomerate. In 2016 alone, it bought Toshiba's home appliance division, the legendary German robotics firm KUKA, and the century-old American vacuum brand Eureka. That single year of acquisitions would be the defining strategic moment for most companies. For Midea, it was just the opening move.

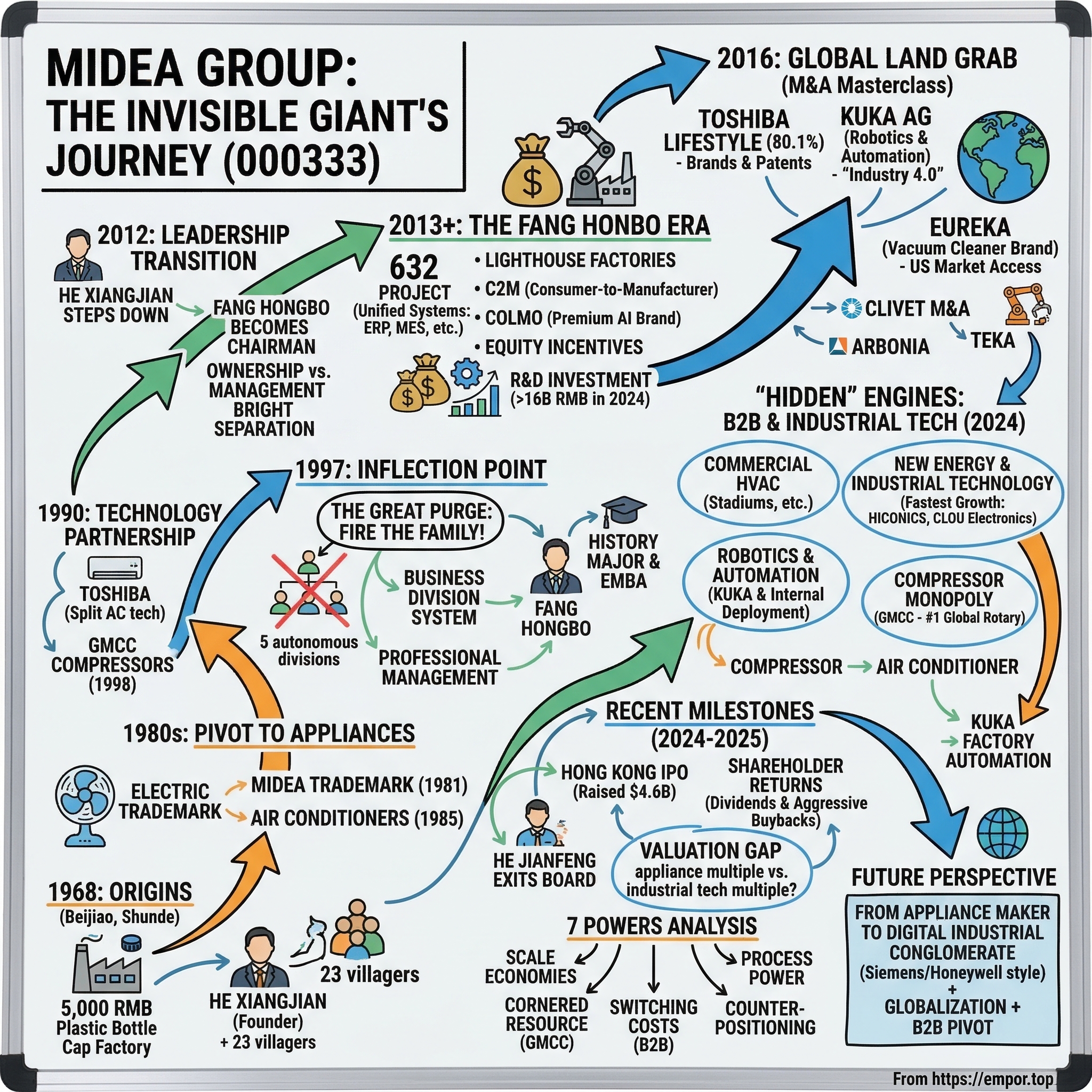

The story of Midea is the story of China's economic transformation compressed into a single corporate biography. It begins in 1968, during the Cultural Revolution, when a man with a primary school education pooled 5,000 renminbi with 23 villagers to make plastic bottle caps. It passes through the chaotic reforms of the 1980s and 1990s, the explosion of the Chinese consumer class, the professionalization of management, and the audacious globalization of Chinese capital. And it arrives at the present moment, where Midea sits at the intersection of smart homes, industrial automation, energy storage, and building technology, trading at a price-to-earnings ratio of roughly 14 times, which is to say, the market still prices it like a washing machine company.

The thesis of this deep dive is straightforward: Midea may be the most important global industrial company that most investors outside of China have never seriously analyzed. And the reason it reached this position is a sequence of decisions, each one more improbable than the last, made by two men across two very different eras: He Xiangjian, the founder who had the courage to fire his own family, and Fang Hongbo, the history major who turned a bloated appliance conglomerate into one of the most efficient manufacturing operations on earth.

This is the story of how a bottle cap factory became an invisible empire.

Before diving in, a word on the numbers. Midea reports in Chinese renminbi, and exchange rate fluctuations can make year-over-year comparisons in dollar terms misleading. For 2024, the company reported revenue of 409.1 billion renminbi, net income of 38.5 billion renminbi, and operating cash flow of 60.5 billion renminbi, all record highs. The market capitalization, as of early 2026, sits at approximately 578 billion renminbi, or roughly $80 billion. To put that in perspective, Whirlpool, the largest American appliance maker, has a market cap of roughly $6 billion. Midea is more than ten times the size of its closest Western pure-play peer, and yet most Western investors could not tell you what it does.

That gap between reality and perception is where this story begins.

A final note before we start. Midea's financial reporting can be complex. The company operates five reported segments: Smart Home, Commercial and Industrial Solutions, New Energy and Industrial Technology, Robotics and Automation, and Smart Building Technology. The segment boundaries do not always map cleanly onto the product categories that consumers would recognize. Where possible, this article uses revenue and profit figures from official company filings. Where specific figures are not publicly disclosed, that fact is noted explicitly.

II. Origins: The Entrepreneurship of Necessity (1968–1990)

The Shunde district of Foshan, in Guangdong Province, is one of the most unlikely birthplaces of a global industrial champion. Today, it is a prosperous manufacturing hub in the Pearl River Delta, home to dozens of appliance companies, furniture makers, and electronics manufacturers. Midea's gleaming headquarters building dominates the Beijiao skyline, a physical monument to what grew out of these streets.

But in 1968, it was a different world entirely.

Picture Beijiao in 1968. A small township in Shunde district, deep in the Pearl River Delta. The Cultural Revolution is in full swing. Private enterprise is not merely discouraged; it is, in the strictest sense, illegal. Mao's ideology holds that individual profit is a bourgeois disease. And yet, in this small village, a 26-year-old man named He Xiangjian is about to do something extraordinarily dangerous: he is going to start a business.

He Xiangjian's background offers no hint of the empire he would build. Born in 1942, he had only a primary school education. He had worked as a factory apprentice, a cashier, and a commune cadre. He was not an engineer. He was not a visionary in any recognizable Silicon Valley sense. What he was, above all, was practical. Shunde was poor. The villagers needed income. And He Xiangjian saw an opportunity in the gaps of the planned economy.

On May 2, 1968, He Xiangjian and 23 fellow villagers pooled together 5,000 renminbi, roughly $600 at the time, and formed the "Beijiao Subdistrict Plastic Production Group." The name was deliberately bureaucratic. The entity was structured as a commune workshop, the only legal form of collective enterprise permitted under Mao's regime. This was not entrepreneurship in the Western sense. This was camouflage. The workshop made medicinal glass bottles and plastic bottle caps, the most mundane products imaginable, chosen precisely because they were too small to attract the attention of ideological enforcers. If a Red Guard had walked through the door, there was nothing to see here: just a commune doing its patriotic duty by producing useful goods for the people. The brilliance of He Xiangjian's early strategy was that it hid capitalism inside the shell of communism.

For more than a decade, the workshop survived by staying invisible and staying useful. Through the early 1970s, products shifted from bottle caps to rubber balls, glass tubes, and eventually small automotive components. The entity was renamed the "Shunde County Beijiao Commune Auto Parts Factory," a title that reveals both the ambition and the constraint of the era. Every pivot was driven by the same logic: find what the local economy needs, make it cheaply, and reinvest the profits before anyone notices you are making a profit.

Then came the pivot that changed everything.

In 1980, Deng Xiaoping's economic reforms cracked open the door to private enterprise, and He Xiangjian walked through it at a dead sprint. He looked at the emerging Chinese consumer and asked a deceptively simple question: what is the first "luxury" item that a family earning its first disposable income will buy? The answer, in subtropical Guangdong, was obvious. An electric fan.

The decision to pivot to fans was not just about product-market fit. It was about timing. Guangdong is subtropical, with oppressive summer heat and humidity. The Chinese government was beginning to encourage consumer spending as part of Deng's modernization drive. And the domestic fan market, while nascent, had almost no established competition. He Xiangjian saw a market that was about to explode, and he positioned Midea to ride the wave.

Midea pivoted to fan manufacturing with the intensity of a company that understood this was a once-in-a-generation window. In 1981, the "Midea" trademark was officially registered. The Chinese name, 美的 (Meidi), translates to "beautiful," a word chosen to evoke aspiration and quality in a market where domestic brands were synonymous with shoddy construction. He Xiangjian became the factory director of the newly christened "Shunde County Midea Fan Factory."

The fan business was transformative in ways that went far beyond revenue. It gave Midea its first real brand identity and, more importantly, its first experience with mass-market consumer manufacturing at scale. Fans were simple products, but selling millions of them taught Midea about distribution networks, quality control at volume, seasonal demand patterns, and the power of brand recognition in a market where consumers had almost no established brand loyalties. Every lesson learned selling fans would be applied, at greater complexity and greater scale, to the products that followed.

By the mid-1980s, the company had enough confidence and cash flow to make its second major product bet: air conditioning. In 1985, Midea established the Midea Air Conditioning Equipment Factory. Air conditioners were a far more complex product than fans, requiring compressor technology, refrigerant management, and precision manufacturing capabilities that Midea simply did not possess.

This is where He Xiangjian's most important strategic instinct emerged: the willingness to learn from the best, rather than reinvent everything from scratch.

The Chinese technology sector in the 1980s was decades behind Japan, Europe, and the United States. Chinese companies had two choices: they could try to develop advanced manufacturing capabilities on their own, a process that would take years or decades and might never close the gap, or they could partner with established leaders, absorb their knowledge, and then apply Chinese scale economics to produce at lower cost. He Xiangjian chose the second path, and it would become the defining strategy of Midea's first half-century.

In 1990, Midea signed a technology partnership agreement with Toshiba to co-develop air conditioning technology. The partnership gave Midea access to split-system air conditioner designs, a significant upgrade from the clunky window units it had been producing. A split-system air conditioner, for those unfamiliar, separates the noisy compressor unit (which sits outside) from the quiet air-handling unit (which sits inside the room). It was a technology that Japanese companies like Toshiba, Daikin, and Mitsubishi had perfected, and that Chinese manufacturers desperately wanted to master.

More importantly, the Toshiba partnership established a template that would define Midea's approach for the next three decades. Find a global technology leader. Study their manufacturing process. Absorb the knowledge. Then execute at Chinese scale and Chinese cost. It is a strategy that has been derided by Western critics as "copying," but in practice it requires enormous discipline, investment, and organizational capability. Plenty of Chinese companies attempted the same approach and failed because they lacked the manufacturing execution to match the quality of their technology partners.

The Toshiba relationship deepened over the decade. In 1998, Midea acquired the Macro-Toshiba compressor factory, which was later renamed GMCC, with Midea holding 60 percent and Toshiba retaining 40 percent. This was not just a joint venture; it was the seed of what would become one of the most powerful component businesses in the global appliance industry. But that part of the story comes later.

The irony of the Toshiba partnership would become apparent 26 years later, when Midea would acquire Toshiba's entire home appliance division. The student would buy the teacher. But in 1990, that outcome was unimaginable. Midea was still a regional Chinese manufacturer. Toshiba was a global technology titan. The distance between them seemed uncrossable.

By 1990, Midea had completed its first great transformation: from a bottle cap commune to a legitimate consumer brand with real manufacturing capability. He Xiangjian had proven that a Chinese private company could compete on quality, not just price. But the next decade would test whether the company could survive its own success, and whether its founder had the ruthlessness to do what almost no Chinese entrepreneur of his generation was willing to do.

III. The 1997 Inflection Point: The Great Purge

By the mid-1990s, Midea had a problem that success creates in every fast-growing private company, but one that was especially acute in China: the founder's family had become the company's management, and the company had outgrown the family's ability to manage it.

The numbers told the story. Sales growth, which had been explosive through the early 1990s as China's consumer economy boomed, began to stall in 1997. The Asian financial crisis was battering confidence across the region. Domestically, a price war had erupted in the appliance industry as dozens of regional manufacturers slashed prices to survive.

Midea was bloated. Decision-making was slow. The company had expanded into too many product lines without the operational discipline to manage them. And everywhere you looked in the organizational chart, you found a He. Cousins, brothers-in-law, childhood friends of the founder, all occupying positions of authority not because of their competence but because of their proximity to He Xiangjian.

This was not unique to Midea. It was the default operating model for virtually every successful private enterprise in China. The concept of "family business" in the Chinese context goes far beyond Western notions of nepotism. In a society where legal protections for private property were still fragile, where the rule of law was subordinate to the rule of relationships, and where trust outside the family circle was a genuine operational risk, putting relatives in charge was not laziness. It was survival strategy. You could trust your brother-in-law not to steal from you. You could not necessarily say the same about a professional manager you had hired from a competitor.

But He Xiangjian saw what others in his position refused to see: the survival strategy had become the survival threat. The family members in management were not bad people. Many of them had been there from the beginning, sweating alongside He Xiangjian in the bottle cap workshop. But the skills required to run a multi-billion-renminbi manufacturing operation with thousands of employees and dozens of product lines were fundamentally different from the skills required to manage a small factory in Beijiao. Loyalty and trust, the very qualities that had made family management essential in the early years, were no longer sufficient. Midea was losing ground to local rivals like Kelon and Galanz. It was being outmaneuvered by companies with more agile management structures. And He Xiangjian, who had spent three decades building this company from nothing, made a decision that was as close to heresy as Chinese business culture permits.

He fired the family.

That phrase deserves to sit alone for a moment, because it is almost impossible to overstate how radical this was. In the late 1990s, China's most successful private companies were essentially clan enterprises. The founder was the patriarch. The family was the organization. To remove the family from management was to challenge not just a business model but a cultural institution that was thousands of years old. It was the equivalent of a medieval king dismissing his entire court of nobles and replacing them with meritocratic bureaucrats. It had been done before in Chinese history, but rarely, and never without consequences.

Not all at once, and not without resistance. But beginning in 1997, He Xiangjian systematically pushed founding members and relatives out of operational roles and implemented what he called the "Business Division System." The reform created five autonomous divisions: Air Conditioners, Household Appliances, Compressors, Motors, and Kitchenware. Each division was given complete control over its own value chain, from R&D to manufacturing to sales and after-service. The group headquarters retained authority over only four functions: finance, budgeting, capital investment, and the appointment of professional managers.

The structure was modeled, consciously or not, on the multidivisional organizational form that had defined American corporate management since Alfred Sloan redesigned General Motors in the 1920s. Each division was a semi-autonomous business, competing in its own market, with its own profit and loss statement. The group center provided capital, talent, and strategic direction, but the operational decisions were made at the division level.

The philosophical shift was as important as the structural one. He Xiangjian articulated a principle that was radical for a Chinese private enterprise of that era: "The family should only exercise an ownership role and not be involved with managing the company." This was, in effect, a declaration that Midea would operate like a Western corporation, with professional management accountable to performance metrics rather than bloodlines.

The immediate result was chaos. Family members who had spent years in comfortable positions suddenly found themselves without titles or authority. Some left bitterly. The internal politics were brutal in ways that rarely make it into official corporate histories. But the medium-term result was transformative. The Business Division System created a Darwinian environment where young, talented, non-family managers could rise based on results. Each division head was, in effect, running a mini-company, with full profit-and-loss accountability and the autonomy to make decisions without waiting for approval from a family patriarch.

The reform also imposed a kind of market discipline within the company itself. Division heads who delivered results were rewarded with more autonomy and more resources. Those who did not were replaced. The internal competition was fierce, sometimes brutally so, but it produced a management bench that was deep, battle-tested, and selected on merit rather than lineage. It is no coincidence that the generation of managers who came of age in the post-1997 Midea would go on to lead the company's most ambitious period of growth.

One of the young managers who thrived in this new environment was a 30-year-old from Anhui Province who had joined Midea's marketing department just five years earlier. His name was Fang Hongbo. He had a bachelor's degree in history from East China Normal University, which is to say, he had no engineering background whatsoever. He had started in internal communications, writing newsletters and managing public relations. But in the meritocratic vacuum created by the family purge, Fang Hongbo began to rise. He moved from marketing to general management, taking over the air conditioning business division, then the refrigeration group. He was methodical, data-driven, and possessed an unusual combination of strategic vision and operational obsession. Colleagues described him as someone who could discuss long-term industry trends in the morning and drill into the details of a factory production line in the afternoon.

Fang Hongbo also possessed a quality that is rare in corporate China: intellectual curiosity about Western management practices. He had earned an EMBA from the National University of Singapore, exposing him to global best practices in corporate governance, supply chain management, and organizational design. He was not copying the West blindly, but he was absorbing ideas and adapting them to the specific context of a Chinese industrial company.

What made Fang Hongbo stand out from the other rising managers was not just his competence but his ambition for the company itself. He did not play corporate politics or build personal fiefdoms. He focused relentlessly on making his division the most profitable, the most efficient, and the most forward-looking in the entire group. That single-mindedness caught He Xiangjian's attention.

He Xiangjian watched Fang Hongbo's ascent with the eye of a man who was already thinking about succession. The founder was in his mid-fifties. He had seen enough family-run Chinese companies implode during generational transitions to know that the biggest risk to Midea's future was not competition from Gree or Haier. It was the assumption that his son would inherit the throne. And He Xiangjian, with the same cold-eyed pragmatism that had guided him since the bottle cap days, began preparing for the most consequential decision of his career.

The 1997 reforms did not just save Midea from stagnation. They created the institutional DNA, the decentralized structure, the meritocratic culture, the separation of ownership and management, that would allow Midea to scale far beyond what any family-run appliance maker could achieve. And they set the stage for a leadership transition that would become a case study in Chinese corporate governance.

IV. The Fang Hongbo Era: Founder Exit and Professionalization (2012)

On August 25, 2012, He Xiangjian did something that made headlines across China's business press. He stepped down as Chairman of Midea Group and handed the company not to his son, He Jianfeng, but to Fang Hongbo, the history major from Anhui who had spent twenty years working his way up from the PR department.

To understand why this was so remarkable, consider the context. In 2012, Midea was a company with a market value exceeding 100 billion renminbi. He Xiangjian's net worth made him one of the richest men in China. His son, He Jianfeng, born in 1967, was the same age as Fang Hongbo and sat on Midea's board. By every convention of Chinese business culture, the son should have inherited the company. It was not merely expected; it was assumed.

He Xiangjian rejected the assumption with a clarity that stunned the Chinese business establishment. He had watched too many of his contemporaries, the first generation of Chinese private entrepreneurs who built empires in the 1980s and 1990s, destroy their companies by treating them as family heirlooms rather than professional institutions. He had studied the failures: companies where the founder's son lacked the competence to lead but had the bloodline to demand the title, where professional managers were undermined by family members who could always appeal to the patriarch, where strategic decisions were made based on family dynamics rather than market reality. He Xiangjian decided that his legacy would not be a dynasty. It would be an institution.

He Jianfeng was given a board seat and the freedom to run Infore Holding Group, the family's separate investment vehicle, which would go on to make significant investments in robotics and technology. But the operational control of Midea, the company that represented the life's work of its founder, went to the professional manager.

This was described at the time as "a precedent for Chinese private enterprises to hand over a company with a market value of 100 billion yuan to a professional manager." And it was not just symbolically important. It was structurally important. He Xiangjian had spent fifteen years, from the 1997 reforms to the 2012 handover, building an institutional architecture that would survive the founder's departure. The Business Division System, the professional management culture, the separation of ownership from operations, all of it had been preparation for this moment.

Fang Hongbo took the chair and immediately began remaking Midea in his own image.

The contrast between the two leaders is instructive. He Xiangjian was the classic Chinese entrepreneur: intuitive, relationship-driven, willing to make enormous bets based on gut feeling. He operated in a world where a handshake mattered more than a contract, where personal relationships with local government officials could make or break a business, and where the ability to read the political winds was as important as reading a balance sheet.

Fang Hongbo came from a different world. He was an intellectual, trained in the humanities, who believed in systems, processes, and data. Where He Xiangjian would walk a factory floor and sense something was wrong, Fang Hongbo wanted dashboards, metrics, and real-time analytics. Where the founder built the company on instinct and relationships, his successor would rebuild it on technology and institutional discipline.

If He Xiangjian was the entrepreneur, the intuitive dealmaker who could sense a market shift before it showed up in the data, Fang Hongbo was the institutionalizer. He was the person who took the founder's instincts and turned them into systems.

His first major initiative was the "632 Project," launched in 2013. The name sounds like a government program, which is appropriate because its ambition was essentially governmental in scale. The "6" referred to six unified operational systems spanning the entire enterprise: ERP for resource planning, MES for manufacturing execution, SRM for supplier relationship management, PLM for product lifecycle management, APS for advanced planning and scheduling, and a centralized finance and controlling system. The "3" referred to three management platforms that standardized data governance and cross-divisional coordination. The "2" referred to two technical platforms that provided the underlying digital infrastructure.

The scale of this undertaking cannot be overstated. In 2013, Midea was a company with revenue approaching 150 billion renminbi, operating dozens of factories across China and increasingly around the world, with hundreds of product lines spanning everything from rice cookers to commercial chillers. Its IT infrastructure had grown organically over two decades, with each business division running its own systems, its own databases, and its own processes. The 632 Project was not an IT upgrade. It was an organizational revolution disguised as a technology project.

For a non-technical audience, the simplest way to understand the 632 Project is this: imagine a company with dozens of factories, hundreds of product lines, and operations in dozens of countries, all running on different software systems that cannot talk to each other. The sales team in Brazil cannot see the inventory data in Guangzhou. The engineering team designing a new refrigerator cannot access the supplier pricing data that the procurement team in Wuxi is negotiating. Every division is, in effect, running its own information fiefdom. The 632 Project tore down all of those fiefdoms and replaced them with a single, unified digital nervous system. One system. One standard. One truth.

The impact was profound and measurable. Before the 632 Project, Midea's order-to-delivery cycle for many products was measured in weeks. After implementation, it shrank dramatically. Inventory levels dropped. Overproduction, the chronic disease of Chinese manufacturers who had historically built to forecast rather than to demand, was brought under control.

The 632 Project also enabled what Midea calls "C2M," or Consumer-to-Manufacturer, a model where real-time demand signals from retail channels flow directly to the factory floor, allowing production schedules to be adjusted in near real-time. Think of it as the manufacturing equivalent of just-in-time inventory, but extended all the way from the retail shelf back to the raw materials procurement office. When a particular model of air conditioner starts selling faster in Chengdu, the system automatically adjusts production schedules in Foshan. When sales of a particular refrigerator model slow in Southeast Asia, the factory reduces output before warehouses fill up with unsold inventory. It also enabled Midea's "Lighthouse" factory program, which would eventually earn the company recognition from the World Economic Forum as one of the most advanced manufacturers on earth. By 2018, the system had been rolled out internationally, with the "i632" program extending the architecture to operations in the United States, Vietnam, and other overseas markets.

The C2M model dramatically reduced inventory carrying costs and overproduction waste. It also gave Midea a speed-to-market advantage: when consumer preferences shifted, Midea could adapt its product mix faster than competitors still running on quarterly planning cycles.

But Fang Hongbo's impact went beyond technology. He fundamentally restructured how Midea's people were motivated. Under his leadership, Midea implemented a multi-layered equity incentive system that would be more recognizable at a Silicon Valley technology company than at a traditional manufacturer. The system included restricted share incentive schemes, global partner stock ownership plans for senior management, business partner plans for key middle-level staff, and core employee stock ownership programs. Six rounds of global partner plans had been executed by 2023, creating an equity architecture where management interests and shareholder interests were tightly aligned.

Fang Hongbo himself held approximately 1.7 percent of Midea Group, a stake worth well over a billion dollars. This was not a token gesture. It meant that Fang Hongbo's personal wealth rose and fell with the same stock price that every public market investor owned. When he made a capital allocation decision, whether to acquire a company, buy back shares, or invest in a new factory, he was betting his own money alongside the shareholders.

The incentive structure also extends to how Midea thinks about R&D investment. Under Fang Hongbo, R&D spending has risen consistently, exceeding 16 billion renminbi in 2024 and cumulatively surpassing 100 billion renminbi over the past decade. The company holds more than 100,000 patents globally and employs over 25,000 R&D personnel. In the first half of 2025 alone, Midea filed over 5,500 new patents. For a company that the market still categorizes as a "home appliance maker," this level of R&D investment is more typically associated with technology companies. It reflects Fang Hongbo's conviction that the future of manufacturing is digital, automated, and data-driven, and that the companies that invest in these capabilities today will dominate the industry tomorrow.

In 2018, Midea also launched Colmo, a premium AI-technology appliance brand, timed to the company's 50th anniversary. Colmo represented Midea's aspiration to move beyond the mass market and compete in the premium segment, where margins are higher and brand loyalty is stronger. The brand uses artificial intelligence for product features like adaptive cooking, predictive maintenance, and personalized climate control, positioning it as a technology product that happens to be an appliance rather than an appliance with technology bolted on.

The results since the 2012 transition speak for themselves. Between 2012 and 2024, Midea's net profit grew by more than 900 percent. Revenue expanded from roughly 100 billion renminbi to over 400 billion. The trajectory has been remarkably consistent: 284 billion in 2020, 342 billion in 2021, 344 billion in 2022, 372 billion in 2023, and 409 billion in 2024. Even in 2022, when China's zero-Covid policy disrupted manufacturing across the country, Midea managed to maintain revenue and grow earnings. The first quarter of 2025 showed continued acceleration, with revenue of 128.4 billion renminbi, up 20.6 percent year-over-year, and net profit of 12.4 billion, up 38 percent. The company's return on equity consistently hovered near 20 percent, a figure that would be impressive for a technology company and is extraordinary for a manufacturer. Earnings per share climbed from under one renminbi to over five.

In June 2024, He Jianfeng was not reappointed to the Midea board after serving twelve years as a director. The founder's son had quietly exited the last formal link to the company his father built.

The transition was almost anticlimactic in its smoothness. No public drama. No legal battles. No activist campaigns. Just a press release noting that a board seat had not been renewed. Compare this to the succession crises that have consumed other Asian family empires, from Samsung's Lee family to the Ambanis at Reliance, and the discipline of the He family's exit becomes all the more remarkable.

The professionalization that He Xiangjian began in 1997 was, a quarter-century later, complete.

For investors, the 2012 transition is the single most important event in Midea's modern history. It is what separates Midea from the dozens of other Chinese private enterprises that rose during the reform era and then declined when the founder aged out. The willingness to install professional management, align incentives through equity ownership, and build systems that outlast any individual is the reason Midea can compound earnings at 15 to 20 percent annually. It is the institutional advantage that no amount of factory automation can replicate.

V. M&A Masterclass: The 2016 Global Land Grab

If the 2012 leadership transition was Midea's internal transformation, then 2016 was the year it announced itself to the world. In a span of months, Fang Hongbo executed three acquisitions that collectively represented the most ambitious globalization campaign ever undertaken by a Chinese manufacturer. Each deal was different in character, but together they revealed a unified strategic vision: Midea would no longer compete by making other companies' products cheaper. It would own the brands, the patents, and the automation technology to compete on its own terms.

The context matters. In 2015 and 2016, Chinese companies were on a global buying spree unlike anything the world had seen since the Japanese acquisitions of the late 1980s. Chinese firms spent over $220 billion on overseas acquisitions in 2016 alone. Much of that spending was poorly conceived, driven by prestige rather than strategy, and financed by debt that would later become a burden. Insurance companies were buying hotel chains. Real estate developers were buying Hollywood studios. The phrase "trophy asset" was used without irony.

Midea's acquisitions in 2016 were the opposite of trophy hunting. Each deal targeted a specific strategic gap. Each was integrated into a coherent industrial logic. And each was negotiated by a management team that understood exactly what they were buying and why.

The first deal was, in some ways, the most elegant.

On March 30, 2016, Midea signed a definitive agreement to acquire 80.1 percent of Toshiba Lifestyle Products and Services Corporation for approximately $473 million. Toshiba retained the remaining 19.9 percent. The deal closed on June 30, 2016, just three months from signing to completion, a speed that would be remarkable for any cross-border deal and was nearly unheard of for a Chinese-Japanese transaction in a politically sensitive industry.

To appreciate why this was remarkable, consider what Midea got for the price. Toshiba's appliance division had annual revenue of approximately 240 billion yen, roughly $2 billion. It came with over 5,000 intellectual property assets spanning decades of Japanese engineering innovation. And it included a 40-year worldwide license to use the Toshiba brand name on home appliances. For less than half a billion dollars, Midea acquired a globally recognized premium brand, a vast patent portfolio, and the engineering know-how of one of Japan's most storied technology companies.

Now compare this to Midea's main Chinese rival. In the same year, Haier Group acquired GE Appliances for $5.4 billion. Haier got an iconic American brand and a massive distribution network in North America. But Midea, for roughly one-tenth the price, arguably got more durable strategic assets. Patents do not depreciate like distribution relationships. A 40-year brand license provides decades of runway. And Toshiba's engineering culture, particularly in compressor and inverter technology, was directly synergistic with Midea's existing capabilities in ways that GE's American-centric appliance business was not with Haier's.

The Toshiba deal revealed something important about Midea's M&A philosophy. The company was not interested in paying top dollar for trophy assets. It was interested in finding situations where a seller's distress, in this case Toshiba's broader corporate crisis involving an accounting scandal and the bankruptcy of its nuclear subsidiary Westinghouse, created an opportunity to acquire premium assets at a discount. Midea was, in effect, a vulture investor disguised as an industrial acquirer.

The Toshiba deal was the appetizer. The main course was KUKA.

On May 18, 2016, just weeks after signing the Toshiba agreement, Midea began acquiring shares in KUKA AG, the Augsburg-based robotics and automation company that is one of the "Big Four" industrial robotics firms alongside ABB, Fanuc, and Yaskawa. By June 16, Midea had launched a formal tender offer at 115 euros per share, a premium of roughly 36 percent over the pre-announcement trading price. The total enterprise value was approximately 4.5 billion euros, or about $5.2 billion.

To understand the magnitude of what Midea was attempting, consider what KUKA represented. KUKA's iconic orange robots are ubiquitous in automotive assembly plants around the world. BMW, Mercedes-Benz, Volkswagen, and virtually every major European automaker relied on KUKA robots for their production lines. The company's software and systems integration capabilities were at the cutting edge of the Fourth Industrial Revolution. Buying KUKA was not like buying an appliance brand. It was like buying a piece of the future of manufacturing itself.

The reaction in Germany was seismic. KUKA was not just any company. It was a national symbol of German engineering excellence and a cornerstone of the "Industry 4.0" initiative, the German government's strategic plan to maintain manufacturing supremacy through automation and data integration. Economy Minister Sigmar Gabriel actively sought a European counter-bidder. Chancellor Angela Merkel was personally briefed on the situation. German media ran breathless coverage about China "buying up" the country's industrial crown jewels.

The controversy was understandable. At 30-plus times EBITDA, Midea had unquestionably paid a premium price. On a pure financial basis, the deal was hard to justify using traditional discounted cash flow analysis. But Fang Hongbo was not buying cash flow. He was buying capability.

The strategic logic was rooted in a simple demographic reality: labor costs in China were rising rapidly. The era of limitless cheap labor that had powered China's manufacturing boom was ending. Midea operated dozens of factories employing tens of thousands of assembly line workers. If the company was going to maintain its cost advantage as wages rose, it needed to automate. And if it was going to automate, it wanted to own the automation rather than depend on external suppliers who could raise prices or restrict access.

KUKA gave Midea exactly that. Industrial robots for factory assembly lines. Automated logistics systems for warehouses. Servo drives and motion control technology. And perhaps most importantly, the systems integration capability to design and build entire automated production lines from scratch. Midea was not just buying robots; it was buying the ability to build the factory of the future.

The political drama played out over months. Behind the scenes, Midea's team, led by Fang Hongbo personally, engaged in extensive negotiations with German officials, KUKA's management, and the company's key customers. The key question was not whether Midea could afford to buy KUKA. It was whether Germany would allow it.

The German government ultimately decided not to block the deal, but Midea made significant commitments to secure approval. It agreed to maintain KUKA's headquarters in Augsburg, preserve jobs, and keep management independent. For several years, KUKA continued to operate as a publicly listed company on the Frankfurt Stock Exchange. But by 2022, Midea completed a squeeze-out of remaining minority shareholders at 80.77 euros per share and delisted KUKA entirely. The robotics giant was now a wholly owned subsidiary.

The third major acquisition of 2016 was quieter but strategically significant. In December, Midea completed the purchase of Eureka, the 107-year-old American vacuum cleaner brand, from Electrolux. The price was not publicly disclosed, but Eureka's trailing revenue was approximately $60 million, suggesting a relatively modest purchase price for a brand with significant consumer recognition in North America.

Together, these three deals in a single year revealed the full scope of Midea's ambition. Toshiba gave it patents and a premium Asian brand. KUKA gave it automation technology and a path to the factory of the future. Eureka gave it a direct-to-consumer brand presence in the American market. The strategy was not "buy cheap and cut costs," the typical caricature of Chinese acquirers. It was "buy the capabilities we cannot build fast enough organically, and integrate them into a platform that creates value greater than the sum of the parts."

The M&A program continued beyond 2016, though at a more measured pace. In February 2017, Midea acquired Servotronix, an Israeli motion control and automation company, for approximately $170 million, deepening the robotics capability stack. In June 2016, it had also acquired 80 percent of Clivet, an Italian HVAC specialist, signaling its move into commercial and industrial building technology.

More recently, in April 2024, Midea agreed to acquire the climate division of Swiss company Arbonia for 760 million euros. That deal closed in early 2025, and Arbonia's climate operations were merged with Clivet to form MBT Climate, creating a pan-European HVAC powerhouse. And in June 2024, Midea agreed to acquire 97.38 percent of Teka Group, the century-old Madrid-based kitchen appliance manufacturer, for 175 million euros. That deal closed in April 2025.

The Teka acquisition is particularly noteworthy because it illustrates how Midea's acquisition strategy has evolved from "buy technology" to "buy market access." Teka, founded in 1924, operates ten factories across Europe, Asia, and the Americas, and sells in over 120 countries. Its product line covers ovens, cooktops, range hoods, sinks, and dishwashers, segments where Midea had a relatively thin presence in European and Latin American markets. By acquiring Teka's distribution network and brand recognition in markets where a Chinese brand name would face significant consumer resistance, Midea effectively bought a decade of market-building work for a fraction of what it would cost to replicate organically.

Each acquisition follows the same pattern established by the Toshiba deal: identify a company with strong brands, deep patent portfolios, or irreplaceable technical capabilities, buy it at a price that reflects the seller's distress rather than the asset's strategic value, and then integrate it into Midea's global platform where Chinese manufacturing scale can dramatically improve the economics.

What is perhaps most impressive about Midea's M&A track record is not the deals themselves but the integration. Many Chinese companies that went on overseas buying sprees in 2015 and 2016 struggled badly with post-acquisition integration. Cultural clashes between Chinese and Western management teams, disagreements over strategy and capital allocation, and the sheer complexity of managing global operations led to value destruction in many cases. Midea, by contrast, has largely avoided these pitfalls by adopting a decentralized approach: acquired companies retain significant operational autonomy, while Midea provides manufacturing scale, supply chain optimization, and capital allocation discipline from the center. It is a model similar to Danaher's or Berkshire Hathaway's approach to acquisitions, adapted for the realities of Chinese-Western cross-border deals.

The cumulative effect is staggering. Midea now owns premium brands across virtually every tier of the global appliance market. It owns the robotics technology to automate its own factories. It owns the HVAC engineering to bid for commercial building projects from Milan to Munich. And it assembled this portfolio over less than a decade, spending a fraction of what Western conglomerates would have paid.

VI. The "Hidden" Engines: B2B and Industrial Technology

Imagine two analysts covering Midea. The first analyst follows consumer electronics and home appliances. She sees a mature business, cyclically exposed to Chinese real estate, competing in a crowded market with thin margins. Her model assigns a 12 to 15 times earnings multiple, consistent with global appliance peers.

The second analyst follows industrial technology. He sees a robotics company, a building technology company, an energy storage company, and a compressor monopoly, all growing at double digits. His model assigns a 20 to 25 times multiple.

They are looking at the same company. And the tension between these two perspectives is perhaps the single most important valuation question in Chinese equities today.

There is a version of Midea's story that ends with washing machines and air conditioners. It is the version most casual observers know, and it leads to a valuation that prices the company as a mature consumer appliance maker, essentially a bond with a better dividend. That version misses the most important thing happening inside the company.

Midea's business-to-business and industrial technology segments crossed 100 billion renminbi in revenue in 2024, representing more than 25 percent of the company's total sales for the first time. This is not a rounding error. This is a second company, roughly the size of a Fortune 500 firm, growing at double-digit rates and hidden inside the financial statements of what the market still thinks of as a refrigerator manufacturer.

To illustrate the point concretely: in 2024, Midea's revenue segmentation showed Smart Home at 269.5 billion renminbi, growing at 9.4 percent. But the combined B2B segments, encompassing Commercial and Industrial Solutions at 104.5 billion, New Energy and Industrial Technology at 33.6 billion, Robotics and Automation at 28.7 billion, and Smart Building Technology at 28.5 billion, collectively added up to nearly 200 billion renminbi. These are not side projects. They are, in aggregate, a massive industrial conglomerate in their own right.

The crown jewel of this hidden empire is GMCC, Midea's compressor business. GMCC, formally the Guangdong Midea Toshiba Compressor Corporation, is a joint venture with Toshiba Carrier in which Midea holds 60 percent. It is the world's largest manufacturer of rotary compressors for air conditioners. Since 2006, GMCC has held the number one global market share in rotary compressor production and sales, with a share exceeding 30 percent. Annual production exceeds 100 million units. It also ranks among the top two globally in refrigerator compressors.

Think of a compressor as the engine of a car. You can change the body panels, the paint color, the interior trim, and the infotainment system, but the engine determines the vehicle's fundamental performance, efficiency, and reliability. In the appliance world, the compressor plays the same role. It is the component that determines how efficiently an air conditioner cools a room, how quietly a refrigerator runs, and how long the appliance lasts before failing. A compressor is the heart of any refrigeration or air conditioning system. It is the most technically demanding component to manufacture, requiring precision engineering, proprietary refrigerant chemistry, and massive capital investment in production lines. A company that controls the compressor supply controls the cost structure of the entire finished product. GMCC gives Midea a structural cost advantage over every competitor that must purchase compressors on the open market. It is Midea's "Intel Inside" moment, a component business that is invisible to the end consumer but indispensable to the economics of the industry.

Alongside GMCC, Midea's component business includes Welling, its motor manufacturing subsidiary. Welling produces the electric motors that drive compressors, fan blades, drum rotations in washing machines, and countless other mechanical functions inside appliances. If the compressor is the heart, the motor is the muscle.

Between GMCC compressors and Welling motors, Midea controls two of the three core components in virtually every air conditioner and refrigerator on the planet. The third, the electronic control board, is increasingly being brought in-house as well through Midea's investments in chip design and variable frequency drive technology.

The GMCC business also illustrates a classic competitive strategy: selling ammunition to both sides. GMCC compressors are found not only in Midea's own products but in the products of its competitors. Rival appliance makers who buy GMCC compressors are, in effect, subsidizing Midea's R&D and contributing to the scale economies that make Midea's own products cheaper. It is a beautifully paradoxical competitive position: the more your competitors buy from your component division, the stronger your consumer division becomes.

The building technology division represents another axis of the B2B expansion. Midea is no longer just selling residential air conditioners through retail channels. Through its acquisition of Clivet in Italy and the recent formation of MBT Climate, incorporating the Arbonia climate operations, Midea is now competing for large-scale commercial HVAC contracts. Think stadiums, hospitals, data centers, and high-rise office towers. The 2022 FIFA World Cup stadiums in Qatar, for instance, used Midea's commercial HVAC systems, a high-profile reference project that demonstrates the company's capability to compete at the highest tier of building technology.

These are multi-year, multi-million-dollar projects with switching costs that are fundamentally different from a consumer choosing between a Midea and a Gree window unit. Once a building's HVAC system is designed around a specific manufacturer's equipment, the cost and complexity of switching to a competitor are enormous.

Then there is the energy and industrial technology segment, the fastest-growing part of the business and perhaps the most consequential for Midea's long-term identity.

In 2024, new energy and industrial technology revenue reached 33.6 billion renminbi, growing at more than 20 percent year-over-year, making it the fastest-expanding segment in the entire company. This segment includes Midea's investments in Hiconics Eco-Energy Technology, a maker of industrial frequency converters and servo drives that Midea acquired control of in 2020, and Clou Electronics, a smart meter and energy storage company in which Midea became the largest shareholder in 2023. Hiconics provides the power electronics that drive electric vehicle motors and industrial automation systems. Clou Electronics provides smart grid infrastructure and energy storage solutions.

To put the energy investments in context, consider the global energy storage market. As renewable energy sources like solar and wind become a larger share of the power grid, the need for large-scale battery storage and smart grid management grows exponentially. The sun does not always shine and the wind does not always blow, so the grid needs massive batteries and intelligent management systems to match supply with demand. Clou Electronics makes the smart meters that monitor energy flow, and the storage systems that buffer it. Hiconics makes the power conversion equipment that translates between different voltage levels and frequencies. Together, they give Midea a foothold in a market that barely existed a decade ago but is expected to grow at 20 to 30 percent annually for years to come.

The strategic logic connecting these investments is the same logic that drove the KUKA acquisition: Midea is positioning itself at the intersection of electrification, automation, and energy management. As the world transitions from fossil fuels to renewable energy, the demand for power conversion equipment, energy storage systems, and smart grid infrastructure will grow exponentially. Midea is building the portfolio to serve that demand, not as a startup entering a new market, but as an industrial manufacturer applying its existing competencies in motors, compressors, and power electronics to adjacent markets.

What makes this energy play particularly clever is that it leverages Midea's existing core competencies. The company already knows how to build efficient electric motors. It already knows how to manufacture precision compressors. It already knows how to design and mass-produce power electronics. Energy storage and EV components are, in many ways, extensions of technologies Midea has been refining for decades. This is not a company making a blind bet on a new industry. It is a company applying its manufacturing DNA to adjacent markets where the underlying physics and engineering are familiar.

The KUKA robotics division itself, while it experienced a 7.6 percent revenue decline in 2024 to 28.7 billion renminbi, reflects the cyclical nature of industrial capital expenditure rather than a structural problem. KUKA remains one of the four dominant global players in industrial robotics, and its order book is closely tied to automotive and electronics manufacturing cycles. As the global auto industry pivots to electric vehicles, which require different assembly processes and new factory configurations, KUKA is positioned to benefit from a wave of retooling investment by automakers worldwide. More importantly, KUKA's technology is being deployed internally across Midea's own factory network. The company now operates at least seven factories designated as "Lighthouse" facilities by the World Economic Forum, a recognition of their world-leading deployment of automation, artificial intelligence, and data analytics in manufacturing. These include facilities in Guangzhou, Hefei, Shunde, Jingzhou, Chongqing, and, as of September 2025, a factory in Thailand that became the first overseas lighthouse factory in the home appliance industry. The reported impact metrics are striking: 28 percent improvement in labor efficiency, 14 percent reduction in unit cost, and 56 percent shorter order lead times.

For investors, the B2B transformation is the single most important variable in Midea's valuation. If the market continues to price Midea as a consumer appliance company, the stock trades at a reasonable but unexciting multiple. But if the B2B and industrial technology businesses continue growing at 15 to 20 percent annually and reach 35 to 40 percent of revenue, the character of the earnings stream fundamentally changes. B2B revenue is stickier, higher-margin, and less cyclically sensitive than consumer appliance sales. A Midea that derives 40 percent of its revenue from robotics, building technology, and energy systems is a very different company than a Midea that derives 75 percent from refrigerators, and it deserves a very different multiple.

VII. The "7 Powers" Analysis: Why Midea Is So Hard to Beat

Hamilton Helmer's "7 Powers" framework asks a simple question: what is the durable source of a company's competitive advantage? In Midea's case, the answer is not one power but an unusual combination of several, layered on top of each other in a way that creates a competitive position that is genuinely difficult for any single rival to replicate.

The first and most obvious power is scale economies. Midea's manufacturing volume in air conditioners, refrigerators, and washing machines is unmatched globally. This volume allows the company to negotiate raw material prices, amortize fixed costs, and invest in automation at levels that smaller competitors simply cannot afford.

When Midea buys steel or copper or plastic resin, it buys in quantities that give it pricing power over its suppliers. When it invests $100 million in automating a factory line, it spreads that cost over tens of millions of units. A smaller competitor making the same investment would need to spread it over a fraction of the volume, resulting in higher per-unit costs. This is the classic scale advantage, and in manufacturing, it compounds over time. The bigger you are, the cheaper your products become, which allows you to sell more, which makes you bigger still. It is a virtuous cycle that is extraordinarily difficult to break into from the outside.

The second power is process power, what Helmer defines as a superior production methodology that competitors cannot easily copy. The "Midea Way" is the culmination of the 632 Project, the Lighthouse factory program, and the KUKA-driven automation initiative. Midea's factories are not just big; they are among the most technologically advanced manufacturing facilities on earth. The World Economic Forum does not hand out Lighthouse designations casually. Achieving that recognition requires demonstrating measurable improvements in productivity, quality, and sustainability through the deployment of Fourth Industrial Revolution technologies. Midea has earned at least seven such designations, more than virtually any other single company. The process advantage is not just about robots on the factory floor. It is about the entire digital infrastructure, the unified data systems, the real-time demand sensing, the automated quality control, that connects the factory to the customer.

The third power is cornered resource, and this is where Midea's advantage becomes truly structural. The ownership of GMCC compressors and Welling motors gives Midea control over the core components that define the performance and cost of every air conditioner and refrigerator. This is vertical integration of a kind that even Samsung, which manufactures its own compressors, struggles to match in breadth. Gree, Midea's primary Chinese rival, is vertically integrated in air conditioning but lacks Midea's diversification across refrigeration, laundry, and small appliances. Whirlpool and Electrolux, the major Western players, are essentially assemblers that purchase components from third parties. When commodity prices spike or supply chains are disrupted, Midea's component ownership provides both a cost buffer and a supply security advantage that assemblers cannot replicate.

The fourth power is switching costs, particularly in the B2B segments. This is where Midea's competitive advantage shifts from "hard to beat" to "nearly impossible to displace."

Once a factory has been designed and built around KUKA robots, with KUKA's proprietary software, KUKA's training programs, and KUKA's maintenance contracts, the cost of switching to ABB or Fanuc is not just the price of new robots. It is the cost of retraining every technician, rewriting every automation program, re-qualifying every production process, and absorbing weeks or months of downtime during the transition. For a major automaker running three shifts a day, the production loss alone from switching robot platforms could cost more than the robots themselves.

Similarly, once a building's HVAC system has been designed around Midea's commercial equipment, the switching cost for the building owner is measured in years of disruption and millions in capital expenditure. These are not consumer purchase decisions that can be reversed with a trip to the store. They are multi-year infrastructure commitments.

The fifth power is counter-positioning, and this is perhaps the most underappreciated element of Midea's strategy. For decades, Midea operated primarily as an OEM and ODM manufacturer, building products that were sold under other companies' brand names. This position was seen by Western competitors as non-threatening. A company that makes your products for you is a supplier, not a competitor. Whirlpool, Electrolux, and other Western brands happily outsourced manufacturing to Midea while focusing on brand marketing and distribution.

But Midea used the OEM business as a funding mechanism for its own brand expansion. The cash flow from making other companies' products financed the R&D, the factory automation, and the acquisitions that allowed Midea to build its own branded business. By the time Western incumbents realized that their supplier had become their competitor, Midea had already acquired Toshiba's brand, Eureka's brand, Teka's brand, and the manufacturing efficiency to undercut incumbents on price while matching them on quality. The counter-positioning was elegant: the incumbents could not respond by pulling their OEM orders without disrupting their own supply chains, and they could not match Midea's cost structure because they did not own their own component manufacturing.

Looking at it from the perspective of potential competitors, the barriers to entry in Midea's core markets are now almost impossibly high. A new entrant would need to simultaneously build massive manufacturing scale, develop or acquire compressor and motor technology, establish brand recognition in dozens of countries, deploy world-class automation, and build a digital infrastructure spanning the entire value chain. The capital required would be measured in tens of billions of dollars. The time required would be measured in decades. No venture capitalist is funding that, and no startup is attempting it.

Applying Porter's Five Forces framework reinforces this picture. The threat of new entrants is low because the capital investment and component technology required to compete at Midea's scale are prohibitive. Supplier power is neutralized by Midea's vertical integration into compressors and motors. Buyer power is moderated by the breadth of Midea's product portfolio and the switching costs in B2B. The threat of substitutes is limited because mechanical refrigeration and climate control have no viable alternatives. And rivalry among existing competitors, while intense in consumer appliances, is increasingly favorable to the scale leaders as smaller players are squeezed out.

Two powers from Helmer's framework are less applicable but worth noting for completeness. Network effects are largely absent in Midea's business; appliances do not become more valuable as more people buy them. Branding power, in the Helmer sense of a willingness to pay a premium based purely on brand perception, is present in some segments, particularly with the Toshiba and Colmo brands in premium markets, but it is not yet a defining competitive advantage for Midea the way it is for, say, Apple or Louis Vuitton. The branding power is nascent and growing, particularly as Midea invests in its own Original Brand Manufacturing (OBM) business, but it has not yet reached the level where consumers will pay a significant premium purely because of the Midea name.

The net effect is a competitive position that is defensible across multiple dimensions simultaneously. A competitor could theoretically match Midea's scale in a single product category. But matching the scale, the vertical integration, the automation capability, the multi-brand portfolio, and the B2B diversification all at once is a challenge that no single rival has yet demonstrated the ability to meet.

VIII. Current Management and Capital Allocation

Midea's capital allocation under Fang Hongbo deserves special attention because it is, in many respects, more reminiscent of a Berkshire Hathaway or a technology company than a traditional Chinese manufacturer.

The framework is deceptively simple. Midea generates enormous free cash flow, roughly 50 to 60 billion renminbi annually. That cash is deployed according to a clear hierarchy. First, invest in the core business: R&D spending has exceeded 16 billion renminbi annually, with cumulative R&D investment surpassing 100 billion renminbi over the past decade. The company filed over 5,500 new patents in the first half of 2025 alone. Second, make acquisitions that clear a high hurdle rate: the Toshiba, KUKA, Clivet, Arbonia, and Teka deals all targeted specific strategic gaps. Third, return capital to shareholders when neither organic investment nor M&A offers attractive returns.

It is the third element, shareholder returns, where Midea stands out most dramatically among Chinese industrials. Since its 2013 listing restructuring, Midea has returned over 134 billion renminbi to shareholders through dividends and buybacks. The 2024 dividend was 3.5 renminbi per share, representing a total payout of 26.7 billion renminbi and approximately a 70 percent payout ratio. But the dividends are only half the story.

Midea has become one of the most aggressive share repurchasers in the Chinese market. To understand why this matters, consider how most Chinese industrial companies handle excess cash. They sit on it. They put it in low-yielding bank deposits. They use it to diversify into unrelated businesses, often with disastrous results. The Chinese corporate landscape is littered with appliance companies that decided they should also be in real estate, or mining, or financial services.

Midea does none of this. In 2025, the company completed a buyback program that repurchased 135 million shares, representing 1.76 percent of total share capital, at a total cost of approximately 10 billion renminbi. Seventy percent of those repurchased shares were canceled, directly reducing the share count and boosting earnings per share for remaining shareholders. An additional buyback program of 1.5 to 3 billion renminbi was announced in April 2025.

The share cancellation detail is critical and worth dwelling on. Many companies around the world, including in the United States, repurchase shares but hold them in treasury rather than canceling them. Treasury shares can be reissued later, diluting shareholders at a future date. By canceling 70 percent of repurchased shares, Midea is making a permanent commitment to reducing its share count. This is capital return in its purest form: the company is literally shrinking its equity base to concentrate ownership among remaining shareholders.

This approach to capital return is rare in Chinese corporate culture, where empire-building and cash hoarding are far more common than share cancellation. It signals a management team that thinks like owners, not like bureaucrats. The willingness to shrink the equity base when the stock is undervalued, rather than using the cash to diversify into unrelated businesses, is a hallmark of disciplined capital allocation.

The September 2024 Hong Kong IPO adds another dimension to the capital allocation story. On September 17, 2024, Midea listed on the Main Board of the Hong Kong Stock Exchange in what became the largest Hong Kong IPO in three years. The offering raised approximately $4 billion, upsized from an initial $3.5 billion target. With the full exercise of the greenshoe option, total proceeds reached approximately $4.6 billion. The stock surged roughly 8 percent on its first day and gained more than 40 percent within three weeks.

The obvious question is: why raise $4 billion when you already have billions in cash on the balance sheet?

The answer is not about the money. It is about currency. A Hong Kong listing gives Midea shares that are denominated in Hong Kong dollars, freely tradable by international investors, and usable as acquisition currency in future cross-border deals without the regulatory complexity of using Shenzhen-listed A-shares. It also raises Midea's profile among global institutional investors who cannot or will not invest in mainland Chinese stocks. The Hong Kong listing was, in effect, an investment in future optionality: the ability to do larger, faster, and more complex international deals using shares that the global market recognizes and trusts.

Fang Hongbo's personal alignment with shareholders is worth emphasizing. His approximate 1.7 percent stake in Midea Group is worth over a billion dollars at current prices. He Xiangjian, through Midea Holding, retains roughly 31 percent. The combined insider ownership means that management and the founding family together hold more than a third of the company. When Fang Hongbo decides to buy back shares, he is increasing the value of his own holdings. When he decides to pay a 70 percent dividend, he is paying himself alongside every other shareholder. The incentive alignment is as tight as you will find anywhere in Chinese public markets.

One accounting judgment worth flagging for investors: Midea's balance sheet carries significant goodwill from its acquisition spree, particularly from KUKA. Goodwill impairment testing is inherently subjective, and the assumptions used to justify carrying values, particularly revenue growth projections and discount rates for the robotics segment, deserve scrutiny. If KUKA's performance deteriorates materially, a goodwill write-down could create a one-time earnings hit. This is not an imminent risk, but it is a contingency that investors should monitor.

For investors monitoring Midea's ongoing performance, two key performance indicators stand above all others. The first is B2B revenue as a percentage of total revenue, currently at approximately 25.5 percent and rising. This metric captures the company's transformation from consumer appliance maker to diversified industrial technology company. The trajectory of this number will determine whether Midea deserves a consumer discretionary multiple or an industrial technology multiple. The second is operating cash flow conversion, meaning the ratio of operating cash flow to net income. In 2024, Midea generated 60.5 billion renminbi in operating cash flow against 38.5 billion in net income, a conversion ratio of approximately 1.57. This consistently above-one ratio demonstrates that reported earnings are backed by real cash generation, not accounting artifacts. A company that converts earnings into cash at this rate can fund its own growth, return capital to shareholders, and weather economic downturns without relying on external financing.

IX. Bear vs. Bull Case

Every investment thesis has a mirror image, and Midea's is no exception.

What follows is an attempt to lay out both sides with intellectual honesty. The bear case and the bull case are both credible, which is ultimately what makes the stock interesting rather than obvious. Great investment opportunities rarely come with unanimous consensus. They come with legitimate disagreement about the future, and the investor's job is to assess which side of that disagreement is more likely to be proven right by events.

The Bear Case

Start with the elephant in the room: China itself. Midea is a Chinese company, listed primarily on the Shenzhen Stock Exchange, operating in a political and regulatory environment that many international investors view with deep skepticism. The risk of arbitrary regulatory intervention, the opacity of corporate governance relative to Western standards, and the ever-present possibility of geopolitical escalation between China and the West all contribute to what analysts call the "China discount," a persistent valuation gap between Chinese companies and their Western peers with similar financial profiles.

Beyond the broad China risk, the most specific threat to Midea is geopolitical. The KUKA acquisition in 2016 was completed before the current era of US-China trade tensions, European investment screening regimes, and technology export controls. In 2016, Germany chose not to block the deal. It is far from clear that the same decision would be made today. The European Union has since implemented a formal foreign direct investment screening framework. Multiple European governments have blocked or restricted Chinese acquisitions in sensitive technology sectors. If Midea's growth strategy depends on continuing to acquire Western technology companies, the pipeline of available targets may be shrinking.

The second major bear concern is the Chinese domestic real estate market. Residential construction and home sales are among the primary demand drivers for household appliances. When Chinese consumers buy new apartments, they buy new air conditioners, refrigerators, and washing machines. The prolonged downturn in Chinese real estate, with property sales declining significantly from their 2021 peaks, directly impacts Midea's domestic consumer appliance business. While Midea has partially offset this through international expansion and the B2B pivot, the Smart Home segment still represents approximately 66 percent of total revenue and remains heavily weighted toward Chinese domestic consumption.

The third concern is the KUKA investment itself. At the price Midea paid, roughly 30-plus times EBITDA, and given the subsequent delisting and squeeze-out, it is difficult to argue that KUKA has generated a return on invested capital that justifies the acquisition premium on a standalone basis. KUKA's revenue has been volatile, declining 7.6 percent in 2024. The global industrial robotics market is competitive, with ABB, Fanuc, and Yaskawa all investing heavily in next-generation technologies including collaborative robots and AI-driven automation. If KUKA fails to maintain its technological edge, Midea could be left with an expensive asset that underperforms.

There is also the question of margins. Midea's gross margin, while improving, still hovers around 26 percent, well below the 35 to 40 percent that premium appliance brands or industrial technology companies typically achieve. The consumer appliance business, which still represents the majority of revenue, is inherently a low-margin, high-volume game where price competition is fierce and brand loyalty is weak. If the B2B transition stalls or takes longer than expected, Midea could remain trapped in a low-margin, low-multiple box.

Finally, there is concentration risk at the management level. Midea's transformation is inseparable from Fang Hongbo. He has been at the helm since 2012 and is now approaching sixty. Succession planning for professional managers is inherently different from succession planning for founders, because the incoming executive does not carry the founder's accumulated institutional knowledge or the board's implicit trust. The question of who succeeds Fang Hongbo, and whether the institutional systems he has built are truly robust enough to survive his departure, is an open one. To the company's credit, the 632 infrastructure and the Business Division system are designed to be leader-independent. But the strategic vision, the M&A judgment, and the capital allocation discipline that have defined the Fang era are ultimately human qualities, and they are not easily encoded into organizational processes.

There is also currency risk to consider. Midea earns revenue in dozens of currencies but reports in renminbi. A significant appreciation of the renminbi against the dollar or euro would erode the competitiveness of its exports and reduce the renminbi value of overseas earnings. Conversely, renminbi depreciation would boost reported earnings but could trigger protectionist responses in export markets. This is not a risk unique to Midea, but for a company with over 40 percent of revenue from international markets, it is a material consideration.

The Bull Case

The core bull argument is the B2B transformation. Midea's consumer appliance business, while mature, is a cash cow that funds the investment in higher-growth, higher-margin industrial businesses. If the B2B segment, encompassing robotics, building technology, energy storage, and industrial components, continues to grow at 15 to 20 percent annually, the composition of Midea's revenue will fundamentally shift over the next five years.

This matters because the market assigns very different valuations to different types of earnings. Consumer appliance companies trade at 10 to 15 times earnings globally. Industrial technology companies trade at 20 to 30 times. If Midea's B2B revenue reaches 35 to 40 percent of total sales, the blended multiple the market applies to the company should rerate upward, even if the consumer appliance business grows only modestly. The bull case is not about Midea selling more refrigerators. It is about Midea being recognized as a company whose earnings quality and growth profile more closely resemble Honeywell or Siemens than Whirlpool.

Consider the comparison to Siemens. Siemens trades at roughly 18 to 22 times earnings. It operates in industrial automation, building technology, and digital infrastructure. Midea operates in the same segments, with comparable or superior growth rates, and trades at 14 times. The gap is partly explained by the China discount, but it also reflects the market's failure to recognize that Midea is no longer primarily a consumer appliance company.

The second bull argument is the international expansion. Midea's overseas revenue has been growing faster than domestic revenue, with international sales up 17.7 percent in the first half of 2025. The company now owns premium brands, Toshiba, Eureka, Teka, Clivet, that give it access to markets where "Made in China" still carries a brand discount. As Midea continues to invest in local manufacturing and distribution, particularly through acquisitions like Teka and Arbonia, the company is building a genuinely global presence that reduces its dependence on any single market.

The third bull argument is the emerging markets opportunity. Midea's appliance business in Southeast Asia, India, the Middle East, and Africa is still relatively underpenetrated. As hundreds of millions of consumers in these regions enter the middle class over the next decade, demand for air conditioners, refrigerators, and washing machines will grow substantially. Midea's combination of cost-competitive manufacturing, global brands, and local production capability positions it to capture a significant share of this growth.

The fourth bull argument is the capital allocation discipline. A company that returns 70 percent of earnings through dividends, actively cancels repurchased shares, and applies a rigorous hurdle rate to acquisitions is a company that compounds shareholder value over time. Midea's free cash flow yield, at approximately 10 percent based on recent metrics, suggests the market is not fully pricing the quality of the cash generation.