Zimmer Biomet: The Engineering of Human Movement

I. Introduction & Episode Teaser

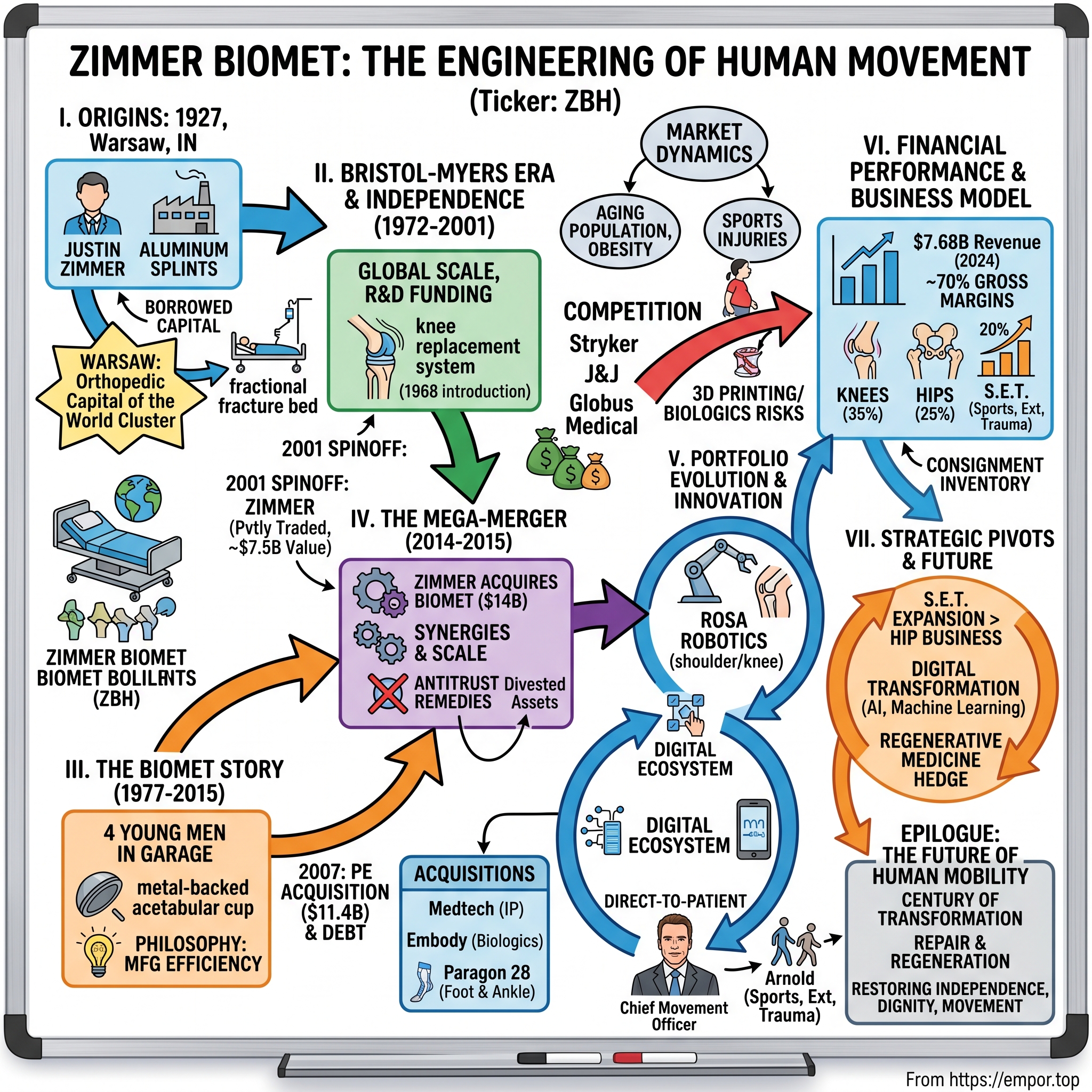

Picture this: Warsaw, Indiana, 1927. Population: 5,621. A small Midwestern town known for little more than its lakes and farmland. A Czech immigrant named Justin Zimmer borrows money from friends and family to start making aluminum splints in a modest workshop. Fast forward nearly a century, and that humble splint manufacturer has morphed into a $7.7 billion orthopedic colossus, wielding surgical robots, AI-powered implants, and a portfolio that touches nearly every joint in the human body.

The transformation defies logic. How does a company selling basic metal strips to local doctors evolve into one deploying the ROSA robotic surgery platform—technology so sophisticated it can position a shoulder implant within fractions of a millimeter? How does a town of fewer than 15,000 people today become the undisputed "Orthopedic Capital of the World," housing not just Zimmer Biomet but spawning competitors like DePuy and Biomet itself?

This is a story of industrial clustering at its finest—Warsaw now produces roughly one-third of all orthopedic manufacturing revenue globally. It's a tale of relentless consolidation, where a $13.4 billion mega-merger created today's giant. And it's a preview of humanity's future, where the line between biology and technology blurs with each passing quarter.

What we'll unpack: How geographic accidents create trillion-dollar industries. Why medical device consolidation follows different rules than pharma or tech. How a company founded when Charles Lindbergh crossed the Atlantic now partners with Arnold Schwarzenegger as its "Chief Movement Officer." And perhaps most critically—whether the moats protecting this near-century-old business can withstand the coming waves of 3D-printed bones, regenerative medicine, and AI-designed implants.

The numbers tell one story: $7.679 billion in 2024 revenue, with operations spanning more than 40 countries. But the human story reveals something deeper: a relentless pursuit to, as their mission states, "alleviate pain and improve the quality of life for people around the world."

Buckle up. We're about to trace how a splint becomes a robot, how a town becomes an empire, and how fixing bones becomes humanity's next frontier.

II. Origins: Justin Zimmer & The Warsaw Cluster

The year is 1927. Calvin Coolidge occupies the White House. The first transatlantic telephone call has just connected New York to London. And in Warsaw, Indiana—a town so small it barely merits a dot on most maps—Justin O. Zimmer is about to make a bet that will reshape human mobility for the next century.

Justin Zimmer wasn't supposed to be an industrialist. A Czech immigrant who arrived in America with more determination than capital, he possessed the classic immigrant's cocktail of ambition: part desperation, part vision, all hustle. When he approached friends and family for startup capital, his pitch was almost comically modest: he wanted to manufacture aluminum splints. Not revolutionize medicine. Not build an empire. Just make better splints than what local doctors could fashion from wooden boards and cloth strips.

The choice of Warsaw wasn't random, though it seemed so at the time. The town sat at the intersection of three critical factors that would later prove decisive: proximity to Chicago's medical schools (close enough for collaboration, far enough for low costs), access to skilled metalworkers from the region's agricultural equipment industry, and perhaps most importantly, a culture of Midwestern craftsmanship where precision mattered whether you were building a barn or a medical device.

Zimmer's timing was exquisite. The aftermath of World War I had accelerated orthopedic medicine—thousands of veterans needed prosthetics and rehabilitation devices. Aluminum, that miracle metal of the early 20th century, offered the perfect combination: lightweight, moldable, and crucially, it didn't rust when exposed to bodily fluids. While competitors stuck with heavy steel or unreliable wood, Zimmer bet everything on aluminum.

By 1928, just one year after founding, the company developed its first breakthrough: a fracture bed system that allowed doctors to apply traction while keeping patients immobile. The innovation caught the attention of a Scottish hospital, leading to Zimmer's first international order. Think about that trajectory—from local splint maker to international supplier in twelve months. In an era before email, before commercial aviation, before modern logistics, a Warsaw workshop was shipping medical devices across the Atlantic.

The numbers tell the story of explosive early growth. By 1930, just three years after that initial friends-and-family round, sales topped $200,000—roughly $3.5 million in today's dollars. This wasn't Silicon Valley-style blitzscaling; this was methodical, profitable growth built on solving real problems for real doctors treating real patients.

But here's what made Warsaw special, and what would transform it into the "Orthopedic Capital of the World": Zimmer's success didn't create a monopoly—it created an ecosystem. Employees left to start competitors. Suppliers specialized in medical-grade manufacturing. The local community college began training programs specifically for medical device production. By 1960, when Zimmer's annual sales hit $4 million and the company opened its Export Department, Warsaw wasn't just home to one orthopedic company—it was becoming the industry's gravitational center.

The Warsaw cluster phenomenon deserves deeper examination because it defies conventional wisdom about industrial geography. Why didn't the industry concentrate in Boston near Harvard Medical School, or Minnesota near the Mayo Clinic? The answer lies in what economists call "path dependence"—once an industry takes root, self-reinforcing mechanisms make it nearly impossible to dislodge. Skilled workers don't want to leave town. Suppliers invest in specialized capabilities. Knowledge spillovers accelerate innovation. Warsaw had accidentally stumbled into becoming for orthopedics what Detroit was for automobiles or Silicon Valley would become for semiconductors.

Justin Zimmer himself embodied the paradox of the immigrant entrepreneur: conservative in operations, radical in vision. He insisted on paying cash for equipment, avoiding debt that could sink the company during downturns. Yet he invested aggressively in R&D, understanding that medical device companies live or die by innovation. His management philosophy, according to early employees, was simple: "Make it better than it needs to be, because someone's life depends on it."

By the 1960s, Zimmer had grown from that initial splint workshop into a serious industrial concern. The company's product line had expanded from simple immobilization devices to complex surgical instruments. More importantly, Zimmer had begun the transformation from hardware supplier to surgical partner—working directly with surgeons to design tools for emerging procedures.

The foundation was set. What started as one man's immigrant dream had become an institution. But the real transformation was yet to come, as a pharmaceutical giant would soon recognize the treasure hiding in Indiana's heartland.

III. The Bristol-Myers Era & Independence (1972–2001)

The acquisition announcement in 1972 must have felt like Warsaw's worst nightmare. Bristol-Myers, the pharmaceutical giant from New York, was swallowing their homegrown champion. Local business leaders feared the classic corporate raid: strip the technology, fire the workforce, move operations to a "real" city. They couldn't have been more wrong.

Bristol-Myers didn't come to plunder—they came to scale. The pharmaceutical industry in the early 1970s was beginning to understand a crucial truth: drugs and devices would converge. As surgical techniques grew more sophisticated, the companies that could offer complete solutions—pharmaceutical therapies plus surgical interventions—would dominate. Bristol-Myers saw in Zimmer not just a profitable division but a beachhead into the future of medicine.

The marriage brought immediate advantages. Bristol-Myers' global distribution network meant Zimmer products could reach hospitals from Tokyo to São Paulo overnight. Their deep pockets funded R&D projects that independent Zimmer could never have afforded. In 1983, Bristol-Myers began offering research grants through the newly established Orthopedic Research and Education Foundation, essentially subsidizing the entire orthopedic research ecosystem.

But the real revolution came in 1968, four years before the acquisition, when Zimmer introduced its first knee replacement system. This wasn't just another product launch—it was a paradigm shift. For millennia, a destroyed knee joint meant permanent disability. Now, surgeons could install a mechanical replacement that would last decades. The technology was crude by today's standards—essentially a hinge made of metal and plastic—but for patients, it was miraculous.

Under Bristol-Myers' ownership, Zimmer transformed from instrument maker to implant innovator. The company developed increasingly sophisticated hip and knee systems, each generation lasting longer, requiring less invasive surgery, and providing more natural movement. By the 1990s, Zimmer implants weren't just functional—they were becoming biomechanically elegant, designed using computer modeling to match natural joint kinematics.

The numbers during this era tell a story of steady, spectacular growth. By 2000, Zimmer employed more than 3,200 people and generated $1 billion in annual sales. The Warsaw facility had expanded from a single building to a sprawling campus. The company's implants were installed in millions of patients worldwide. Yet within Bristol-Myers' massive portfolio—which included everything from Excedrin to HIV drugs—Zimmer was becoming increasingly incongruous.

The pharmaceutical industry was consolidating around pure-play strategies. Investors wanted focused bets, not conglomerates. Medical devices required different sales forces, different regulatory pathways, different manufacturing capabilities than drugs. By the late 1990s, the whispers on Wall Street grew louder: Bristol-Myers needed to choose.

The spinoff announcement in 2001 felt inevitable in retrospect but shocking at the time. Bristol-Myers would separate Zimmer into an independent, publicly traded company—returning it to its roots as a standalone orthopedic pure-play. The transaction valued Zimmer at roughly $7.5 billion, a testament to three decades of value creation under corporate ownership.

The first quarter as a public company—Q3 2001—exceeded all expectations. Sales increased 14% worldwide and 22% in North and South America. The market loved the story: a focused orthopedic leader, freed from pharmaceutical bureaucracy, with dominant positions in the fastest-growing segments of medical devices. The stock soared.

But independence brought challenges Bristol-Myers had shielded them from. Suddenly, Zimmer had to fund its own R&D, build its own international infrastructure, and most critically, compete for acquisitions against cash-rich rivals. The orthopedic industry was entering a consolidation phase, and Zimmer needed to decide: acquire or be acquired.

What made this transition remarkable was how seamlessly Zimmer shifted from division to independent company. The management team, led by Ray Elliott, had been preparing for this moment. They'd built autonomous capabilities even while under Bristol-Myers' umbrella. They'd maintained the Warsaw culture despite corporate ownership. Most importantly, they'd never lost sight of what made Zimmer special: deep surgeon relationships and relentless innovation.

The Bristol-Myers era, often overlooked in company histories, was actually transformative. It provided the capital and scale to transform from regional manufacturer to global leader. It funded the R&D that created modern joint replacement. And perhaps most importantly, it proved that Zimmer could thrive under any ownership structure—a lesson that would prove valuable in the mega-merger to come.

IV. The Biomet Story: Parallel Innovation (1977–2015)

While Zimmer was navigating corporate ownership, four young men in their twenties were sitting in a Warsaw garage in 1977, plotting revolution. Dane Miller, a biomedical engineer aged 26; Niles Noblitt, sales executive aged 28; and two other colleagues had just done something that seemed insane: they'd quit stable jobs at established orthopedic companies to start their own. Their company name—Biomet, short for Biomedical Technology—reflected ambition that far exceeded their resources.

The founding story reads like Silicon Valley lore transplanted to the Midwest. In 1978, the four entrepreneurs aged 26 to 31 officially launched operations with minimal capital and maximum confidence. Their first year was brutal: only $17,000 in sales against $63,000 in losses. They were hemorrhaging money, burning through savings, testing friendships. Most startups would have folded. But by 1980—just two years later—they'd turned profitable. How? By doing what Warsaw did best: solving specific surgeon problems with ingenious engineering.

Biomet's breakthrough came in 1980 with the introduction of their metal-backed acetabular cup for hip replacements. This wasn't sexy technology—it was a component that fit into the socket side of artificial hip joints. But it solved a critical problem: previous designs would loosen over time, requiring painful revision surgeries. Biomet's metal backing provided better fixation to bone, potentially lasting decades longer. Surgeons loved it. Orders poured in.

The growth trajectory from there defied gravity. By 1984, just six years after those crushing initial losses, annual sales hit $10.6 million with $1.6 million in earnings. The company was doubling revenue every two years, all while maintaining profitability—a combination that's nearly impossible in capital-intensive industries.

What made Biomet special wasn't just products—it was philosophy. While Zimmer pursued technological sophistication, Biomet obsessed over manufacturing efficiency. They pioneered just-in-time inventory systems for medical devices. They invested in automation before it was fashionable. In 1989, they began using CAD systems for 3D imaging—technology that wouldn't become standard for another decade.

Dane Miller, who became CEO and the company's spiritual leader, embodied a different kind of medical device executive. An engineer by training, he could discuss biomechanics with surgeons and manufacturing tolerances with floor workers. He famously kept his office in Warsaw, refusing to relocate to Chicago or New York despite investor pressure. His philosophy was simple: stay close to the customers (surgeons) and the capability (Warsaw's unique ecosystem).

The company's growth attracted inevitable attention from financial buyers. In 2007, a consortium including Blackstone, Goldman Sachs, Kohlberg Kravis Roberts (KKR), and TPG Capital acquired Biomet for $11.4 billion—one of the largest leveraged buyouts in medical device history. The private equity owners brought financial discipline and acquisition capital, but they also loaded the company with debt that would constrain investment.

Under private equity ownership, Biomet continued innovating but also began aggressive cost-cutting. The PE playbook was classic: improve margins, pursue bolt-on acquisitions, prepare for exit. They expanded internationally, streamlined operations, and pushed into adjacent markets. But the debt burden meant less investment in breakthrough R&D—a decision that would have long-term consequences.

By 2014, Biomet had grown to nearly $3 billion in annual revenue with leading positions in knees, hips, and dental implants. They'd survived the financial crisis, navigated regulatory challenges, and maintained profitability despite crushing debt payments. But the orthopedic industry was consolidating rapidly. Scale was becoming essential for R&D investment, global distribution, and regulatory compliance. The PE owners knew it was time to exit.

The parallel stories of Zimmer and Biomet reveal something profound about innovation ecosystems. Two companies, founded 50 years apart, in the same small town, pursuing the same market, could both become multi-billion dollar enterprises. This wasn't competition that destroyed value—it was rivalry that created it. Zimmer and Biomet pushed each other, poached from each other, and learned from each other. Their employees would leave to start other companies, their suppliers would develop specialized capabilities, their success would attract talent from around the world.

Warsaw's orthopedic cluster had produced not one but two giants, plus dozens of smaller specialists. The combined employment in orthopedics exceeded 10,000 people in a town of 15,000. The industry generated more than $10 billion in annual revenue from a few square miles of Indiana farmland. It was, by any measure, one of the most successful industrial clusters in American history.

The stage was set for a merger that would reshape the industry—combining Warsaw's two champions into a single orthopedic colossus.

V. The Mega-Merger: Creating an Orthopedic Giant (2014–2015)

The boardroom at Zimmer headquarters in Warsaw must have felt electric on April 24, 2014. After months of secret negotiations, CEO David Dvorak was about to announce the unthinkable: Zimmer had agreed to purchase crosstown rival Biomet for $13.4 billion. Two companies that had competed for decades, poached each other's talent, and defined Warsaw's orthopedic identity would become one. It was like Ford buying Chrysler if both were headquartered in the same small Michigan town.

The strategic logic was compelling. The orthopedic industry was consolidating rapidly as hospitals gained pricing power and regulatory costs soared. Scale meant survival. Combined, Zimmer-Biomet would command roughly 15% of the global orthopedic market, second only to Johnson & Johnson's DePuy division. They'd have the heft to invest in next-generation technologies like robotics and AI while maintaining profitability despite pricing pressures.

But the financial engineering was equally attractive. Zimmer would pay $10.35 billion in cash and $3.0 billion in common stock, while assuming Biomet's outstanding debt. The private equity owners—KKR, TPG, Blackstone, and Goldman Sachs—would finally exit their seven-year investment with substantial returns. The combined company expected to save $135 million in the first year and $270 million by the third year through classic merger synergies: eliminating duplicate functions, leveraging combined purchasing power, optimizing manufacturing footprints.

But almost immediately, the deal hit turbulence. In October 2014, the EU's antitrust regulators opened an extensive investigation due to concerns about competition. The problem was market concentration in specific product categories. In unicondylar knee implants—partial knee replacements used for less severe arthritis—Zimmer and Biomet were two of only three significant competitors. Their merger would create a near-duopoly with Smith & Nephew, likely leading to higher prices for hospitals and patients.

The regulatory review dragged on for months, creating uncertainty that rippled through both organizations. Integration planning teams worked in legal limbo, unable to fully coordinate while the companies remained separate. Competitors used the uncertainty to poach talent and customers. The original closing target of Q1 2015 came and went. The resolution came through classic antitrust remedies. The FTC required Zimmer to divest U.S. assets and rights to certain products within 10 days after the acquisition became final. Zimmer would sell its ZUK unicondylar knee implant to Smith & Nephew, while Biomet would divest its Discovery Total Elbow implant and Cobalt Bone Cement to DJO Global. The divestitures were surgical—removing just enough to preserve competition while keeping the merger's core value intact.

Finally, on June 24, 2015, after 14 months of negotiations, reviews, and remedies, Zimmer completed the acquisition of Biomet in a cash and equity transaction valued at approximately $14.0 billion. The combined company would be known as Zimmer Biomet Holdings, trading under the ticker symbol ZBH—a subtle nod to both legacies.

The integration challenges were immense. Two companies with distinct cultures, overlapping product lines, and competing sales forces needed to become one. Integration plans included termination of employees and certain contracts, with expectations to incur $170 million for employee termination benefits and $130 million for contract termination expense through 2018. These weren't just numbers—they represented thousands of careers disrupted, relationships severed, and the human cost of corporate consolidation.

But the strategic benefits began materializing quickly. The combined entity had unmatched scale in orthopedics, with leading positions in knees, hips, and emerging categories. They could spread R&D costs across a larger revenue base, negotiate better terms with suppliers, and present hospitals with complete solutions rather than piecemeal products. The projected synergies—$135 million in year one, $270 million by year three—proved conservative.

The cultural integration proved surprisingly smooth, aided by geographic proximity. Both companies were Warsaw natives, their employees often neighbors, their cultures shaped by Midwestern values of hard work and innovation. Rather than a hostile takeover, it felt more like a family reunion—competitive cousins finally joining forces against outside threats.

The Zimmer-Biomet merger stands as a case study in industrial consolidation done right. It created value not through financial engineering but through genuine operational synergies. It preserved the Warsaw cluster's vitality while creating a champion with global scale. Most importantly, it positioned the combined company to invest in the technologies—robotics, AI, digital health—that would define orthopedics' future.

The mega-merger era in medical devices wasn't over, but Zimmer Biomet had secured its seat at the table, ready to shape the industry's next chapter.

VI. Portfolio Evolution & Innovation Strategy

Walk into a modern operating room where a ROSA robot assists in knee replacement surgery, and you're witnessing the culmination of Zimmer Biomet's decades-long transformation from hardware supplier to technology platform. The surgeon still leads, but now aided by real-time data, computer-assisted planning, and robotic precision that would have seemed like science fiction when Justin Zimmer was crafting aluminum splints.

Today's Zimmer Biomet portfolio reads like an anatomy textbook: knee and hip products, sports medicine, biologics, foot and ankle, trauma, craniomaxillofacial and thoracic products. But calling them "products" understates their sophistication. Modern knee implants aren't just metal and plastic—they're engineered systems designed through AI modeling, manufactured with aerospace-grade precision, and increasingly, connected to digital ecosystems that monitor patient outcomes.

The ROSA Robotics portfolio represents the company's boldest bet on the future. In 2024, Zimmer introduced the ROSA Shoulder, the world's first robotic surgery system for shoulder replacement, expanding their ROSA portfolio which includes systems for knee and hip replacements. Think about that progression: from manual surgery dependent entirely on surgeon skill, to computer-assisted navigation, to active robotic systems that can execute pre-planned cuts with sub-millimeter accuracy.

But ROSA isn't just about precision—it's about data. Every procedure generates information about surgical technique, implant positioning, and patient anatomy. This data feeds back into product design, surgical training, and eventually, predictive models that can forecast which patients will have the best outcomes with which implants. It's a virtuous cycle where each surgery makes the next one better.

The digital revolution extends beyond the OR. The mymobility app transforms patient engagement, allowing remote monitoring of recovery progress, medication compliance, and rehabilitation exercises. Patients upload videos of themselves walking; AI analyzes their gait and alerts surgeons to potential complications before symptoms appear. This isn't just convenience—it's a fundamental reimagining of the patient-surgeon relationship from episodic encounters to continuous care.

The acquisition strategy reveals how Zimmer Biomet builds these capabilities. The purchase of French surgical robotics company Medtech brought critical IP in robotic navigation. The $155 million acquisition of Embody, Inc. (plus up to $120 million in milestones) added collagen-based implants for rotator cuff repair—biologics that don't just replace tissue but encourage regeneration. Each deal fills a specific gap in the technology stack. The recent Paragon 28 acquisition, announced in January 2025 and completed in April for $1.2 billion enterprise value, signals Zimmer Biomet's most aggressive portfolio expansion yet. Paragon 28 generated net revenue of $255.9 to $256.2 million in 2024, representing 18.2% to 18.4% growth—nearly five times Zimmer Biomet's organic growth rate. The strategic significance runs deeper: once the transaction closed, Zimmer Biomet expected its S.E.T. (Sports Medicine, Extremities, and Trauma) business to be larger than its Hip business, and to grow at a much faster pace.

This isn't just buying growth—it's buying optionality. The foot and ankle market, estimated at $5 billion globally, grows faster than traditional joint replacement as aging populations stay active longer and diabetes drives complications. Paragon 28's specialized sales force—experts who speak the unique language of podiatric surgery—provides access to a customer base Zimmer Biomet couldn't efficiently reach with its existing organization.

The innovation strategy reveals a three-pronged approach: organic R&D for incremental improvements, acquisitions for breakthrough technologies, and partnerships for emerging capabilities. The company invests approximately 5% of revenue in R&D—substantial but not excessive, reflecting the mature nature of many product categories. The real innovation happens at the intersection of disciplines: materials science meets biology in bioactive coatings, software engineering meets surgery in robotic systems, data science meets patient care in predictive analytics.

Consider the evolution of a knee implant. First generation: simple hinges that prevented collapse but limited movement. Second generation: anatomically shaped components that better mimicked natural motion. Third generation: patient-specific implants designed from CT scans. Fourth generation (emerging): smart implants with embedded sensors tracking wear, alignment, and activity. Fifth generation (in development): regenerative scaffolds that encourage tissue regrowth rather than replacement. Each leap requires different capabilities—metallurgy, biomechanics, electronics, tissue engineering—explaining why portfolio breadth matters.

The competitive response has been swift. Stryker doubled down on robotics with its Mako system. Johnson & Johnson leveraged its pharmaceutical heritage for combination drug-device products. Smith & Nephew pursued value positioning. But Zimmer Biomet's strategy—building a comprehensive platform spanning prevention through recovery—creates unique differentiation.

The portfolio evolution from aluminum splints to AI-powered surgical systems captures something essential about medical technology: progress happens not through sudden breakthroughs but through relentless, incremental innovation. Each generation builds on the last, each acquisition fills a gap, each technology enables the next. The result isn't just a product catalog—it's an integrated system for restoring human movement.

VII. Industry Dynamics & Competition

The global orthopedic implants market size was estimated at USD 26.05 billion in 2024 and is anticipated to reach USD 32.47 billion by 2030, growing at a CAGR of 3.78% from 2025 to 2030. North America dominated with over 45.69% market share. These numbers frame the battlefield where Zimmer Biomet competes—a massive, growing market driven by inexorable demographic forces.

The competitive landscape reads like a who's who of medical technology: Johnson & Johnson (through DePuy Synthes), Stryker, Globus Medical, Smith & Nephew, and Zimmer Biomet itself forming the oligopoly that controls most of the market. Each player brings distinct advantages—J&J's pharmaceutical synergies, Stryker's robotic leadership with Mako, Smith & Nephew's value positioning, Globus Medical's spine focus. But none match Zimmer Biomet's breadth across all major joint categories combined with deep Warsaw heritage.

What drives this market's relentless growth? Start with demographics: the global population aged 60+ will reach 1.4 billion by 2030, up from 1 billion today. Each year brings millions more candidates for joint replacement as cartilage wears down, bones weaken, and mobility decreases. Obesity compounds the problem—excess weight accelerates joint deterioration, lowering the average age for first replacements and increasing the likelihood of revisions.

Sports injuries represent another growth vector, paradoxically driven by both fitness trends and sedentary lifestyles. Weekend warriors tear ACLs attempting activities their bodies aren't conditioned for. Professional athletes push boundaries, requiring increasingly sophisticated reconstruction techniques. Even youth sports drive demand as early specialization leads to overuse injuries requiring surgical intervention.

The market is driven by the growing prevalence of reduced bone density, weakened bones, and musculoskeletal disorders. The surging risk of degenerative bone disorders is another factor driving market growth. These aren't just medical conditions—they're quality of life crises that patients will pay to solve, creating a market with remarkable pricing resilience even during economic downturns.

Geographic dynamics reveal interesting asymmetries. North America dominates revenue due to high procedure volumes, premium pricing, and favorable reimbursement. But Asia-Pacific grows fastest, with multiple sources projecting 6-7% CAGRs as healthcare infrastructure develops and middle classes expand. China and India represent massive untapped markets where joint replacement penetration remains a fraction of Western levels.

The regulatory environment creates both barriers and opportunities. FDA approval for new implants can take years and cost tens of millions—a moat protecting incumbents. But recent regulatory harmonization efforts, particularly between FDA and European CE marking, reduce duplicate testing and accelerate global launches. The EU's Medical Device Regulation (MDR), while initially disruptive, ultimately favors large players with resources to navigate complex compliance requirements.

Pricing pressures intensify as hospital systems consolidate and gain negotiating leverage. Group purchasing organizations (GPOs) aggregate demand, demanding volume discounts. Value-based care models shift focus from implant sales to total episode costs, rewarding companies that can demonstrate superior outcomes and lower readmission rates. This explains the rush toward digital health platforms—whoever owns the data demonstrating clinical superiority commands pricing power.

Technology disruption looms from multiple directions. 3D printing promises customized implants manufactured on-demand, potentially disrupting traditional inventory models. Biologics and regenerative medicine could eventually eliminate the need for mechanical implants altogether—imagine injecting stem cells that regrow cartilage rather than replacing entire joints. Smart materials that adapt to patient movement or release drugs to prevent infection blur the line between device and pharmaceutical.

Yet the industry's fundamentals remain remarkably stable. Unlike pharmaceuticals facing patent cliffs or tech companies vulnerable to platform shifts, orthopedic implants benefit from high switching costs. Surgeons train for years on specific systems—muscle memory matters when operating. Hospitals invest millions in instrument sets compatible with particular implants. Patients rarely switch brands mid-treatment. These lock-in effects create recurring revenue streams surprisingly resistant to disruption.

The competitive dynamics increasingly favor scale. R&D costs for next-generation technologies—robotics, AI, smart implants—require massive investment only the largest players can afford. Regulatory compliance grows more complex and expensive. Global distribution demands infrastructure beyond most companies' reach. The result: continuing consolidation as subscale players either get acquired or exit.

Zimmer Biomet's position in this landscape appears strong but not unassailable. They have the scale to invest, the portfolio breadth to offer complete solutions, and the Warsaw heritage providing deep expertise. But Stryker's robotic leadership and J&J's resources pose real threats. The next decade will likely determine whether orthopedics remains a fragmented oligopoly or consolidates further into a true duopoly.

VIII. Financial Performance & Business Model

Full-year net sales of $7.679 billion increased 3.8% and 4.8% on a constant currency basis. Behind these headline numbers lies a business model engineered for predictability in an unpredictable world—a feat of financial architecture that transforms metal and plastic into recurring revenue streams.

The revenue composition tells the strategic story. Knees generate approximately 35% of revenue, hips 25%, S.E.T. (Sports Medicine, Extremities, and Trauma) 20%, with the remainder split between spine, dental, and other categories. But these aren't just product sales—they're ecosystem plays. A knee replacement involves the implant itself (one-time revenue), surgical instruments (often provided on consignment), planning software (subscription revenue), and potentially robotic assistance (capital equipment sale or lease). Each component reinforces the others, creating switching costs that lock in customers for decades.

The margin structure reveals operational excellence despite complexity. Gross margins hover around 70%—remarkable for manufactured products. How? First, the actual material cost of an implant is minimal—titanium and polyethylene are commodities. The value lies in design, regulatory approval, and surgical education. Second, manufacturing automation and Warsaw's cluster efficiencies drive down production costs. Third, premium pricing for innovative products like ROSA-assisted implants commands higher margins than commodity offerings.

Operating margins of approximately 20% seem modest compared to software companies but are impressive for capital-intensive manufacturing. The company spends roughly 5% of revenue on R&D—enough to maintain innovation leadership without the pharmaceutical industry's boom-bust cycles. Sales and marketing expenses consume about 30% of revenue, reflecting the high-touch nature of surgeon relationships and the need for extensive clinical education.

Cash flow generation remains robust, with free cash flow consistently exceeding $1 billion annually. This funds a balanced capital allocation strategy: dividends consuming 15-20% of net income provide income to shareholders while maintaining flexibility for acquisitions. Share buybacks opportunistically return excess capital. But the real story is M&A—the company has completed dozens of acquisitions over the past decade, each adding capabilities or geographic reach.

The geographic revenue split—approximately 60% Americas, 25% EMEA, 15% Asia-Pacific—reveals both concentration risk and opportunity. U.S. dominance provides stable, high-margin revenue but exposes the company to American healthcare policy changes. International expansion, particularly in Asia, offers growth potential but at lower initial margins and higher execution risk.

Working capital management deserves attention. The company maintains substantial inventory—finished implants in multiple sizes ready for immediate shipment. This seems inefficient until you understand the business model: hospitals can't wait for manufacturing when a patient is on the operating table. Consignment inventory—implants physically located at hospitals but owned by Zimmer Biomet until used—ties up capital but creates powerful switching costs. No hospital administrator wants to explain why surgeries were cancelled due to implant availability.

The recurring revenue transformation is perhaps most interesting. Traditionally, orthopedics was purely transactional—sell an implant, recognize revenue, move on. But digital health platforms change this dynamic. The mymobility app generates subscription revenue from hospitals. Surgical planning software creates ongoing fees. Data analytics services provide insights hospitals will pay for continuously. While still small relative to implant sales, these revenue streams carry software-like margins and create ongoing customer relationships beyond the operating room.

Currency impacts merit consideration given international exposure. Fourth quarter net sales of $2.023 billion increased 4.3% and 4.9% on a constant currency basis. That 60 basis point headwind from currency demonstrates how foreign exchange can mask underlying operational performance. The company hedges tactically but accepts currency risk as the cost of global diversification.

Reimbursement dynamics fundamentally drive the business model. In the U.S., Medicare sets rates for joint replacement that hospitals must operate within—the implant is just one component of the total episode cost. This creates pressure for value demonstration but also opportunity for companies that can prove superior outcomes. Bundled payments, where providers receive a fixed amount for the entire episode of care, favor integrated solutions providers over component suppliers.

The COVID pandemic stress-tested the model. Elective surgeries—the core of orthopedic revenue—virtually stopped for months in 2020. Yet the company survived and recovered quickly. Why? First, delayed surgeries eventually happen—joints don't heal themselves. Second, the financial flexibility from strong cash generation provided cushion. Third, geographic and product diversification meant not all revenue streams stopped simultaneously.

Private equity's historical involvement (through Biomet) provides an interesting financial lens. PE firms saw orthopedics as ideal for leverage: predictable cash flows, high margins, limited technological disruption risk. The debt burden constrained innovation investment, but the financial discipline introduced valuable operational improvements that persist today.

Looking forward, the financial model must evolve. Pure implant sales face pricing pressure and commoditization. The future lies in outcome-based contracting where payment depends on patient results, not just successful surgery. This requires massive data collection, sophisticated analytics, and risk-bearing capacity—capabilities only the largest players possess.

The financial performance reflects a business model in transition—from selling products to providing solutions, from transactions to relationships, from hardware to integrated hardware-software systems. The numbers suggest this transition is working, but the real test comes as healthcare systems worldwide grapple with unsustainable cost growth. Companies that can demonstrably improve outcomes while reducing total episode costs will thrive. Those that can't will become acquisition targets or irrelevant.

IX. Strategic Pivots & Future Bets

The announcement hit like a thunderbolt at the 2024 investor day: Zimmer Biomet's S.E.T. business, after the Paragon 28 acquisition, would be larger than their Hip business and grow at a much faster pace. For a company built on hip and knee replacements, this represented nothing short of an identity transformation—like Ford declaring it would make more money from software than trucks.

The S.E.T. expansion strategy reflects brutal mathematical reality. Hip and knee replacements, while massive markets, grow at GDP-plus rates—call it 3-4% annually in developed markets. S.E.T. markets—sports medicine, extremities, trauma—grow at 6-8%, sometimes double digits in specific niches. The math is inescapable: to accelerate overall growth, you must shift portfolio weight toward faster-growing segments.

But the real strategic genius lies deeper. S.E.T. procedures typically involve younger patients—athletes with torn ACLs, workers with shoulder injuries, diabetics with foot complications. These patients will likely need joint replacements eventually. By treating them earlier in their orthopedic journey, Zimmer Biomet builds relationships that could last decades, creating a patient pipeline for future hip and knee procedures.

Arnold Schwarzenegger joined as Chief Movement Officer, collaborating to motivate individuals to increase mobility and support the Company's Direct-to-Patient efforts. This isn't celebrity endorsement fluff—it's a strategic bet on direct-to-consumer healthcare. Historically, medical device companies sold to surgeons who influenced hospital purchasing. But as patients become healthcare consumers, armed with information and often bearing more costs, they increasingly influence implant selection. Who better than the Terminator to convince aging baby boomers that joint replacement can restore their active lifestyles?

The Direct-to-Patient initiative represents a fundamental channel strategy shift. Traditional medical device marketing focuses on surgeon education and hospital administrators. But younger patients research online, join communities, seek peer reviews. Zimmer Biomet is building digital platforms where prospective patients can learn about procedures, find surgeons, track recovery, and connect with others who've had similar surgeries. It's Amazon-meets-WebMD for orthopedics.

Digital transformation permeates every strategic bet. The company isn't just digitizing existing processes—it's reimagining the entire patient journey. AI algorithms analyze pre-operative imaging to predict optimal implant size and positioning. Machine learning models identify patients at risk for complications before symptoms appear. Digital twins—virtual replicas of patient anatomy—allow surgeons to practice complex procedures before entering the OR.

The data play deserves special attention. Every ROSA-assisted surgery generates gigabytes of information: surgical technique, implant positioning, patient anatomy, outcomes data. Aggregated across thousands of procedures, patterns emerge. Which surgical approaches yield best outcomes for specific patient types? What implant positions correlate with longest survivorship? This isn't just academic research—it's competitive advantage that compounds over time.

Emerging markets strategy reflects portfolio theory applied to geography. Developed markets offer predictability but limited growth. Emerging markets promise explosive growth but with political risk, currency volatility, and infrastructure challenges. The solution: localized manufacturing in key markets like China and India, reducing currency exposure and satisfying local content requirements. Partnerships with local distributors who understand regulatory and cultural nuances. Tiered product offerings—premium implants for private-pay patients, value options for government programs.

The sustainability pivot isn't just ESG window dressing—it's operational necessity. Hospitals increasingly demand environmental scorecards from suppliers. European regulations require device recyclability. Younger surgeons preferentially adopt products from sustainable manufacturers. Zimmer Biomet is developing biodegradable implant coatings, reducing packaging waste, and investigating closed-loop recycling for explanted devices. One fascinating initiative: recovering precious metals from removed implants, creating a circular economy for medical devices.

Platform thinking represents perhaps the most profound strategic shift. Instead of selling individual products, create integrated ecosystems where each component reinforces others. The ROSA robot works best with Zimmer Biomet implants designed for robotic assistance. The mymobility app integrates with surgical planning software. Data from all touchpoints feeds predictive analytics. Competitors can match individual products but struggle to replicate the entire ecosystem.

The personalized medicine bet acknowledges that one-size-fits-all implants are becoming obsolete. Using patient-specific imaging and 3D printing, Zimmer Biomet can create custom implants tailored to individual anatomy. Initially reserved for complex revision surgeries, personalization is moving mainstream as costs decline and outcomes improve. Imagine: your knee replacement designed specifically for your body, optimized for your activity level, manufactured while you're being prepped for surgery.

Regulatory strategy has shifted from compliance to competitive advantage. By actively engaging with FDA on new regulatory pathways—like the Q-Submission program for breakthrough devices—Zimmer Biomet helps shape the rules while gaining early insights into regulatory expectations. They're betting that regulatory complexity favors large, sophisticated players who can navigate approval processes competitors can't afford.

The regenerative medicine hedge reveals strategic optionality. While continuing to improve mechanical implants, the company simultaneously invests in biological alternatives. Acquisitions like Embody bring tissue engineering capabilities. Research partnerships explore stem cell therapies and cartilage regeneration. The message: we'll profit from mechanical implants as long as they're needed, but we're also positioning for a future where biology replaces machinery.

Risk management undergirds all strategic pivots. Each bet—S.E.T. expansion, digital transformation, emerging markets—diversifies risk while maintaining optionality. If robotics adoption slows, digital health provides growth. If emerging markets disappoint, developed market share gains compensate. If mechanical implants become obsolete, regenerative medicine capabilities provide a bridge.

These strategic pivots aren't random experiments—they're carefully orchestrated moves to transform from an implant manufacturer to a human mobility company. The vision: wherever people need to restore movement—from professional athletes to nursing home residents, from trauma victims to arthritis sufferers—Zimmer Biomet provides solutions. It's ambitious, risky, and exactly what's needed to thrive in healthcare's uncertain future.

X. Playbook: Lessons for Builders & Investors

Study Zimmer Biomet's century-long journey, and patterns emerge—not just for medical devices but for any industry where technology meets critical human needs. These lessons, earned through aluminum splints and algorithmic surgery, apply whether you're building the next biotech or investing in industrial champions.

Lesson 1: Geographic Clusters Create Compounding Advantages

Warsaw's transformation into the "Orthopedic Capital of the World" wasn't planned—it emerged from Justin Zimmer's initial success. But once established, the cluster became self-reinforcing. Talented engineers didn't need to leave town to find opportunities. Suppliers specialized in medical-grade manufacturing. Community colleges created targeted training programs. Competitors became collaborators on industry standards while fierce rivals in the market.

For builders: Don't underestimate the power of physical proximity, even in our digital age. Complex manufacturing, deep R&D, and specialized expertise still benefit from concentration. For investors: Companies anchored in industry clusters enjoy advantages—talent access, knowledge spillovers, supplier ecosystems—nearly impossible to replicate elsewhere.

Lesson 2: Industrial Consolidation Follows Predictable Patterns

The Zimmer-Biomet merger wasn't unique—it was inevitable. When industries mature, consolidation becomes mathematical necessity. R&D costs rise faster than individual company growth. Regulatory complexity favors scale. Customers prefer dealing with fewer suppliers. The orthopedic industry's consolidation from dozens of players to a handful of giants mirrors pharmaceuticals, aerospace, and increasingly, technology.

For builders: In consolidating industries, you have three choices: become the consolidator, be consolidated, or find a defensible niche. Middle ground is death. For investors: Consolidation creates predictable opportunities. Buy future consolidators early. Short subscale players without differentiation. Arbitrage valuation disparities between acquirers and targets.

Lesson 3: Regulatory Complexity Can Be a Moat

FDA approval for a new hip implant requires years of testing, millions in investment, and navigational expertise few possess. This seems like a burden, but Zimmer Biomet has transformed it into competitive advantage. They shape regulations through active engagement. They maintain regulatory affairs teams that smaller competitors can't afford. They've built institutional knowledge about approval pathways that takes decades to accumulate.

For builders: In regulated industries, lean into complexity rather than fighting it. Become the company regulators trust, the one they consult when writing new rules. For investors: Regulatory barriers create predictable cash flows. Companies that master regulatory navigation enjoy pricing power and competitive protection worth paying premiums for.

Lesson 4: Building Moats in Commoditizing Markets

A hip implant is fundamentally a piece of shaped metal—seemingly a commodity. Yet Zimmer Biomet maintains 70% gross margins. How? By surrounding the commodity with non-commoditizable elements: surgeon training, surgical planning software, outcome data, robotic assistance. The implant becomes just one component of an integrated solution where switching costs overwhelm any savings from cheaper alternatives.

For builders: When your core product commoditizes, expand the definition of your product. Bundle services, add software, create ecosystems. For investors: Beware companies with high margins on seemingly simple products without surrounding moats—they're vulnerable to disruption.

Lesson 5: The Innovation Dilemma—Incremental vs. Disruptive

Zimmer Biomet faces a classic innovator's dilemma: their mechanical implants generate massive profits, but biological alternatives could make them obsolete. Their response—investing in both incremental improvements and potentially disruptive technologies—seems obvious but is psychologically difficult. It requires funding research that could cannibalize your core business.

For builders: Create separate organizations for disruptive innovation, with different metrics and incentives. Accept that you might disrupt yourself. For investors: Companies that can't articulate how they'd respond to disruption of their core business are uninvestable, regardless of current profitability.

Lesson 6: Capital Intensity Shapes Returns

Manufacturing orthopedic implants requires massive capital investment—production facilities, inventory, surgical instruments provided on consignment. This capital intensity depresses returns on invested capital compared to asset-light businesses. But it also creates barriers to entry. Startups can't easily replicate decades of manufacturing investment.

For builders: If you choose a capital-intensive business, ensure the capital creates genuine barriers, not just costs. For investors: Adjust return expectations for capital intensity, but recognize that capital requirements can create competitive advantages worth owning.

Lesson 7: Platform Thinking in Physical Products

Software companies understand platforms—create an ecosystem where third parties add value, increasing your product's stickiness. Zimmer Biomet applies this thinking to physical products. Their ROSA robot becomes more valuable as more surgeons train on it. Their outcome database improves with each procedure. Their digital health apps create network effects among patients.

For builders: Even physical products can become platforms. The key is creating interconnections where each user makes the product more valuable for others. For investors: Companies describing themselves as "platforms" without demonstrable network effects are using buzzwords, not building moats.

Lesson 8: The Power of Switching Costs in B2B Markets

A surgeon who's performed 1,000 knee replacements using Zimmer Biomet's techniques won't switch for a 10% price reduction. The muscle memory, the specialized instruments, the familiar sales rep—all create switching costs that trump financial incentives. This dynamic, replicated across thousands of surgeons, creates remarkable customer retention.

For builders: Design switching costs into your product from day one. Training, integration, customization—anything that makes switching painful. For investors: High customer retention in B2B markets often signals switching costs, creating predictable revenue streams worth premium valuations.

Lesson 9: Managing Technology Transitions

Zimmer Biomet has navigated multiple technology transitions: from splints to implants, from mechanical to robotic, from hardware to digital. Each transition required new capabilities while maintaining legacy revenue. The key: overlapping transitions rather than sudden shifts, using profits from mature technologies to fund emerging ones.

For builders: Technology transitions are marathons, not sprints. Maintain legacy products longer than seems optimal—they fund your future. For investors: Companies managing multiple technology generations simultaneously are complex but often undervalued, as markets struggle to value portfolios spanning different maturity curves.

Lesson 10: The Durability of Mission-Driven Organizations

"Alleviate pain and improve the quality of life for people around the world"—Zimmer Biomet's mission hasn't changed in nearly a century. This consistency provides organizational clarity that survives leadership changes, economic cycles, and technology shifts. Employees, customers, and investors know what the company stands for.

For builders: A clear, durable mission attracts talent, guides decisions, and provides resilience during challenges. For investors: Companies with authentic missions that align with business models often outperform financially engineered competitors over long time horizons.

These lessons from Warsaw's workshops to global operating rooms reveal timeless principles: geography matters, scale advantages compound, complexity creates moats, and mission provides resilience. Whether you're building the next medical device giant or investing in industrial champions, Zimmer Biomet's playbook offers a template for creating enduring value in industries where innovation meets human need.

XI. Bear vs. Bull Case & Valuation

The investment community remains split on Zimmer Biomet, with bears and bulls marshaling compelling evidence for diametrically opposed conclusions. The debate isn't about whether the company will survive—its market position ensures that—but whether it can generate returns justifying its valuation in a rapidly evolving healthcare landscape.

The Bear Case: Structural Headwinds Intensifying

Bears begin with the commoditization reality. Strip away the marketing and medical jargon, and a knee implant is shaped metal and plastic—materials costing perhaps $300 selling for $5,000+. This markup attracted numerous entrants, from Chinese manufacturers to 3D-printing startups. While regulatory barriers slow them, bears argue it's just a matter of time before "good enough" imports pressure pricing, especially in cost-conscious emerging markets.

Hospital consolidation creates monopsony power that bears believe will crush margins. When a three-hospital system becomes a thirty-hospital network, their negotiating leverage multiplies. Group purchasing organizations (GPOs) aggregate demand further, demanding ever-steeper discounts. The recent emergence of hospital-owned implant manufacturers—Kaiser Permanente exploring in-house production—represents an existential threat to traditional pricing models.

The regulatory overhang looms larger than bulls acknowledge. The EU's Medical Device Regulation (MDR) has already forced product withdrawals and delayed launches. FDA's increased scrutiny following high-profile recalls makes approval timelines longer and less predictable. The threat of substitutes is expected to be moderate in the industry because, even though substitutes are available for orthopedic implants, some key products still hold a strong place. Bears interpret this "moderate" threat as gradually intensifying, not diminishing.

Product liability represents an underappreciated risk. Unlike pharmaceuticals where side effects emerge in subpopulations, a faulty implant design affects everyone who receives it. The metal-on-metal hip settlements that plagued the industry demonstrate how single product issues can generate billions in liabilities. With millions of Zimmer Biomet implants in patients worldwide, the liability tail is long and unpredictable.

Bears see disruption approaching from multiple vectors. Regenerative medicine promises to regrow cartilage rather than replace joints—Zimmer Biomet's investments here seem defensive rather than offensive. Pharmaceutical alternatives like disease-modifying osteoarthritis drugs could delay or eliminate the need for surgery. Even within medical devices, bears note that Stryker's robotic leadership and Smith & Nephew's value positioning are taking share.

The stringent regulatory framework that protects incumbents also hampers innovation. While barriers slow new entrants, they also make introducing breakthrough products expensive and time-consuming. Bears argue this regulatory sclerosis favors incremental improvements over transformative innovation, gradually eroding competitive differentiation.

Demographic tailwinds might be weaker than assumed. Yes, populations are aging, but they're also staying healthier longer. Improved obesity treatments, better preventive care, and lifestyle modifications could reduce the pool of surgical candidates. The assumption that every aging knee needs replacement might prove overly optimistic.

The Bull Case: Structural Growth with Competitive Advantages

Bulls counter with inexorable demographic math. The global geriatric population is estimated to increase from 1 billion to 1.4 billion people by 2030. These aren't statistics—they're future patients. Cartilage doesn't regenerate, bones weaken with age, and no pharmaceutical can reverse decades of joint wear. The orthopedic implant market isn't just growing—it's guaranteed to grow.

Technology differentiation is accelerating, not diminishing. ROSA robotics, AI-powered planning, smart implants with embedded sensors—these aren't incremental improvements but paradigm shifts in surgical capability. Robotic systems such as Mako SmartRobotics cut variability in procedures. Zimmer Biomet performed the first robotic shoulder replacement in 2024. First-mover advantages in robotics create switching costs as surgeons invest time learning specific systems.

Emerging markets represent massive untapped opportunity. Joint replacement penetration in China and India remains a fraction of Western levels. As middle classes expand and healthcare infrastructure develops, procedure volumes could multiply. Zimmer Biomet's early investments in local manufacturing and distribution position them to capture disproportionate share as these markets mature.

The recurring revenue transformation is real and accelerating. Digital health subscriptions, surgical planning software, data analytics services—these create predictable, high-margin revenue streams beyond one-time implant sales. Bulls see Zimmer Biomet evolving into a healthcare technology company that happens to make implants, deserving software-like valuation multiples.

M&A optionality provides multiple paths to growth. With strong cash generation and modest leverage, Zimmer Biomet can acquire technologies or market access. The Paragon 28 acquisition demonstrates management's willingness to pay for growth in attractive segments. Bulls see a rollup opportunity in fragmented markets like spine and sports medicine.

The innovation pipeline suggests sustained differentiation. Personalized implants using 3D printing, bioactive coatings that prevent infection, regenerative scaffolds that encourage bone growth—these aren't science fiction but products in development. The combination of internal R&D and acquisition-driven innovation ensures a steady stream of premium-priced launches.

Switching costs and surgeon relationships create durability that bears underestimate. Orthopedic surgery isn't commoditized labor—it's highly skilled work where familiarity with specific implant systems affects outcomes. The installed base of surgeons trained on Zimmer Biomet techniques provides decades of recurring revenue.

Valuation: The Market's Verdict

The valuation debate reflects these conflicting narratives. Bears point to declining ROIC as evidence of commoditization. Bulls highlight free cash flow yield as demonstrating earnings quality. Trading at roughly 15-18x forward earnings, Zimmer Biomet sits between high-growth medical technology (20-25x) and mature industrials (12-15x)—exactly where you'd expect for a company with characteristics of both.

The EV/Sales multiple around 2.5-3x seems reasonable for a medical device company but expensive for a manufacturer. The disconnect: Is Zimmer Biomet a technology company applying innovation to orthopedics, or an industrial company with good marketing? Your answer determines whether the stock is cheap or expensive.

Relative valuation provides limited clarity. Zimmer Biomet trades at a discount to pure-play robotics companies like Intuitive Surgical but at a premium to diversified medical device companies like Medtronic. Again, the valuation depends on your categorization—innovation leader or mature incumbent?

The sum-of-the-parts analysis suggests potential undervaluation. The high-growth S.E.T. business alone could justify a significant portion of enterprise value. The installed base of ROSA robots represents recurring revenue potential not fully reflected in current multiples. The digital health initiatives, while nascent, could warrant venture-like valuations if separated.

DCF models produce wildly different results based on assumptions. Bears modeling 2-3% terminal growth rates and contracting margins arrive at downside to current prices. Bulls assuming successful platform transformation and emerging market penetration see 50% upside. The sensitivity to assumptions reflects the fundamental uncertainty about Zimmer Biomet's future identity.

The Verdict: A Battle for the Future

The bear-bull debate ultimately centers on whether Zimmer Biomet can transform from a traditional medical device manufacturer into a medical technology platform. Bears see inevitable commoditization and margin pressure. Bulls see sustainable differentiation through technology and scale. Both can point to evidence supporting their case.

The truth likely lies between extremes. Zimmer Biomet faces real challenges—pricing pressure, regulatory burden, and technological disruption. But they also possess genuine advantages—scale, innovation capability, and customer relationships—that provide resilience. The company probably won't achieve software-like margins, but neither will it become a commoditized manufacturer.

For investors, Zimmer Biomet represents a classic "show me" story. The strategic pivots—S.E.T. expansion, digital transformation, emerging markets—are correct directionally but unproven at scale. The next 2-3 years will reveal whether management can execute these transitions while maintaining core business performance. Until then, the stock will likely trade sideways, range-bound between bear fears and bull hopes, waiting for evidence that breaks the stalemate.

XII. Epilogue: The Future of Human Mobility

Stand in Zimmer Biomet's Warsaw headquarters, and you can feel the weight of history. Display cases showcase aluminum splints from the 1920s, early joint replacements from the 1960s, and today's ROSA robots—a tangible timeline of humanity's quest to preserve movement. The mission statement, etched in steel, reads simply: "Alleviate pain and improve the quality of life for people around the world."

Nearly 100 years after Justin Zimmer borrowed money from friends to start making splints, his company has transformed into something he could never have imagined yet would instantly recognize. The tools have evolved from bent aluminum to AI-powered robots, but the purpose remains unchanged: restore human mobility when biology fails.

The convergence of biology and technology accelerates daily. Today's mechanical implants will seem primitive compared to tomorrow's bioengineered joints that grow with the patient. Smart implants that monitor their own wear and predict failure before symptoms appear are leaving laboratories for operating rooms. The line between replacement and regeneration blurs as scaffolds seeded with stem cells begin rebuilding rather than replacing damaged tissue.

What would Justin Zimmer think of today's company? He'd marvel at robots performing surgery with superhuman precision. He'd be astounded by implants lasting decades rather than years. But he'd likely be most impressed by the scale of impact—millions of people walking, running, and living because of innovations that started in his Warsaw workshop.

The next century promises transformations as profound as the last. Imagine implants that adapt to patient activity, stiffening for stability during walking and softening for comfort during rest. Picture surgical planning so sophisticated that outcomes can be predicted before the first incision. Envision a world where joint failure is prevented through early intervention rather than fixed through late-stage replacement.

Yet challenges loom as large as opportunities. Healthcare systems worldwide strain under demographic pressure. Regulatory frameworks struggle to keep pace with innovation. Ethical questions about human enhancement versus restoration grow more complex. The companies that navigate these challenges while maintaining focus on patient outcomes will define the industry's next chapter.

Zimmer Biomet stands at an inflection point. The acquisitions are complete, the technologies are emerging, and the strategies are set. Now comes execution—the mundane but critical work of transforming vision into reality. Can they integrate Paragon 28 while maintaining momentum? Will ROSA robotics achieve the ubiquity of traditional instruments? Can digital health platforms create genuine competitive advantages?

The answers won't come from PowerPoint presentations or earnings calls but from operating rooms where surgeons use these tools to restore mobility. From rehabilitation centers where patients regain independence. From research laboratories where the next breakthrough gestates. The future of human mobility isn't written in strategic plans but carved in bone and measured in steps regained.

Building century-old businesses requires a different mindset than building unicorns. It demands patience measured in decades, not quarters. Investment in relationships that outlast products. Commitment to missions that transcend financial metrics. Zimmer Biomet's first century proves that such businesses can be built, can evolve, and can thrive through depressions, wars, and technological revolutions.

As we look toward a future where humans live longer but not necessarily healthier, where activity expectations rise even as bodies wear down, where the definition of "quality of life" expands beyond mere survival, companies like Zimmer Biomet become essential infrastructure for aging societies. They're not just selling implants—they're selling independence, dignity, and the fundamental human right to movement.

The story that began with a Czech immigrant making aluminum splints in small-town Indiana has become a global saga of innovation, consolidation, and transformation. But in a deeper sense, the story hasn't changed at all. It remains what it always was: humans helping humans overcome physical limitations, one joint at a time.

The next chapter is being written now, in Warsaw and Warsaw's offspring clusters worldwide, by engineers and surgeons, by entrepreneurs and incumbents, by anyone who believes that mobility is not a luxury but a necessity. Zimmer Biomet's second century won't look like its first, but if history is any guide, it will be equally transformative.

The mission endures: Alleviate pain and improve the quality of life for people around the world. Nearly 100 years of transformation, and not even close to being done.

XIII. Recent News### **

Latest Earnings Updates** Second quarter 2025 results show net sales of $2.077 billion, up 7.0% reported and 5.4% constant currency, with net earnings of $152.8 million ($411.2 million adjusted) and diluted EPS of $0.77 ($2.07 adjusted). The company raised full-year 2025 guidance citing reduced tariff headwinds and strong demand.

Recent M&A Activity

-

Paragon 28 Acquisition (Completed April 2025): The $1.2 billion enterprise value acquisition of the foot and ankle specialist closed April 21, 2025, expanding Zimmer Biomet's S.E.T. business into the fast-growing $5 billion foot and ankle segment

-

Monogram Technologies (Announced July 2025): Zimmer Biomet announced a definitive agreement to acquire Monogram Technologies (NASDAQ: MGRM), an AI-driven robotics company, to expand its robotics suite with semi- and fully autonomous solutions

-

OrthoGrid Systems (2024): Recent acquisition of OrthoGrid Systems, an AI surgical guidance company, to expand market share in hip replacement procedures

Product Launches and Innovations

- The OsseoFit Stemless Shoulder System represents the company's latest innovation in shoulder replacement technology

- Two major knee products are scheduled for launch in the second half of 2025, expected to boost U.S. knee sales

- The ROSA Shoulder robotic application has received positive feedback, supporting long-term growth potential in robotic orthopedic surgery

Strategic Partnerships

- Strategic partnership with Getinge announced, where Zimmer Biomet will distribute Getinge's Operating Room capital products to Ambulatory Surgery Center customers

- Partnership with RevelAi Health, a patient care AI company, to enhance digital health capabilities

Direct-to-Patient Initiatives

- Launched "This, You Can Do," a new direct-to-patient campaign and online resource to drive awareness of Zimmer Biomet's knee solutions in key U.S. markets

Financial Outlook and Challenges

- Fiscal year 2025 guidance predicts 3-5% constant currency sales growth and adjusted EPS growth of 3% at the midpoint ($8.25)

- Significant tariff headwinds expected to affect operating profit by $60-80 million after mitigation in H2 2025, with uncertainty for 2026

- Free cash flow forecast reduced by $350 million at midpoint, attributed equally to tariffs and Paragon 28 acquisition

Recognition and Culture

- Recognized as a Great Place to Work® in Colombia, India, Ireland, Poland, Puerto Rico, Saudi Arabia, Switzerland and the United States

XIV. Links & Resources

Company Resources

- Investor Relations: investor.zimmerbiomet.com

- Corporate Website: zimmerbiomet.com

- SEC Filings: sec.gov/edgar (search ticker: ZBH)

- Annual Reports & 10-Ks: Available through investor relations portal

- Earnings Call Transcripts: Quarterly updates via investor relations

Industry Reports and Analysis

- Grand View Research: Orthopedic Implants Market Analysis

- Fortune Business Insights: Medical Device Industry Reports

- MarketsandMarkets: Orthopedic Devices Market Forecasts

- Allied Market Research: Global Orthopedic Market Studies

- Mordor Intelligence: Medical Technology Industry Analysis

Medical and Scientific Resources

- Journal of Bone and Joint Surgery (JBJS)

- Clinical Orthopaedics and Related Research (CORR)

- The Orthopedic Research and Education Foundation

- American Academy of Orthopaedic Surgeons (AAOS)

- International Orthopaedics (SICOT)

Technology and Innovation

- ROSA Robotics Platform Information

- mymobility Patient App Resources

- FDA Medical Device Database (510k clearances)

- ClinicalTrials.gov (ongoing Zimmer Biomet studies)

Historical Archives

- Warsaw History Museum: Orthopedic Industry Collection

- Zimmer Biomet Heritage Timeline

- Bristol-Myers Squibb Historical Archives (1972-2001 era)

- Biomet Company History Documentation

Regulatory and Compliance

- FDA Medical Device Regulations

- European Union Medical Device Regulation (MDR)

- Centers for Medicare & Medicaid Services (CMS) reimbursement data

- International Medical Device Regulators Forum (IMDRF)

Books and Publications

- "The Orthopedic Capital of the World" - History of Warsaw's Medical Device Industry

- "Medical Device Innovation: Concept to Market" by Stuart R. Gallant

- "The Business of Healthcare Innovation" by Lawton R. Burns

- Academic case studies from Harvard Business School and Wharton

Industry Associations

- AdvaMed (Advanced Medical Technology Association)

- Medical Device Manufacturers Association (MDMA)

- Orthopaedic Surgical Manufacturers Association (OSMA)

- BioIndiana (Life Sciences Association)

Competitive Intelligence

- Stryker Corporation investor relations

- Johnson & Johnson (DePuy Synthes) resources

- Smith & Nephew corporate information

- Globus Medical investor materials

Patient Resources

- Patient testimonials and case studies (via corporate website)

- Joint replacement education materials

- Surgeon locator tools

- Recovery and rehabilitation guides

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube