Block, Inc.: The Story of Building the Next Financial Ecosystem

I. Introduction & Episode Roadmap

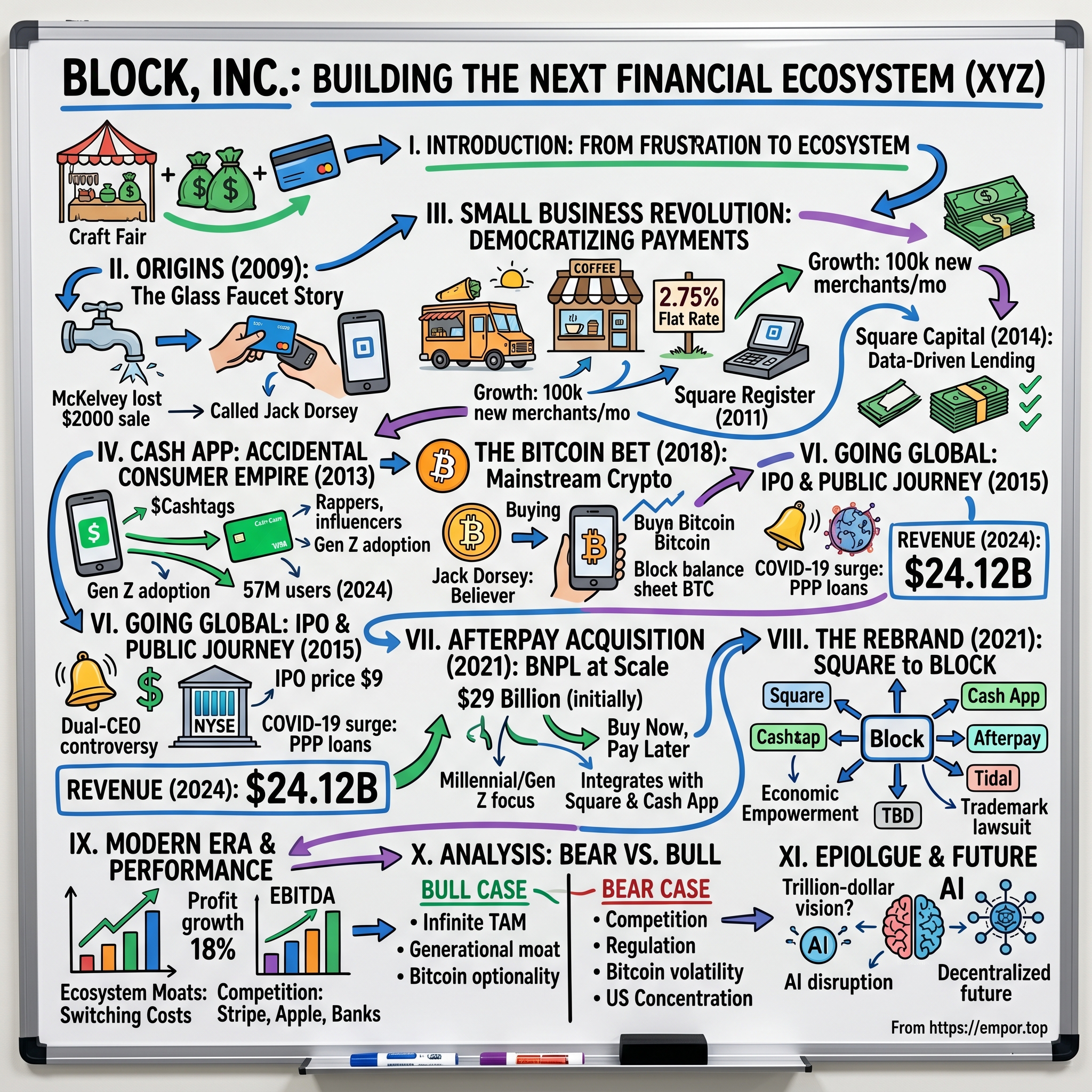

Picture this: A glass artist in St. Louis loses a $2,000 sale because he can't accept credit cards. His friend, a programmer who just helped create Twitter, watches this unfold and thinks—"This is insane. In 2009, why is accepting payments still this hard?" That moment of frustration would spawn Block, Inc., a company that today processes $241 billion in payments annually and serves 57 million users worldwide. Block isn't just another fintech unicorn—it's a case study in how to build multiple billion-dollar businesses under one roof. From the original Square card reader that democratized payments for small businesses, to Cash App's emergence as Gen Z's preferred banking alternative, to bold bets on Bitcoin and buy-now-pay-later through Afterpay, this is a company that has consistently zigged when the industry zagged.

In the year 2024, Block had annual revenue of $24.12B with 10.06% growth, but revenue alone doesn't tell the story. What makes Block fascinating is its portfolio approach to financial services—building distinct brands that serve different audiences while creating powerful network effects between them. Think of it as the Berkshire Hathaway of fintech, except instead of insurance companies and railroads, Jack Dorsey has assembled payment processors, consumer apps, and crypto infrastructure.

This journey from a simple card reader to a financial ecosystem worth examining through multiple lenses: the product decisions that created new markets, the strategic acquisitions that expanded the playing field, the controversial dual-CEO structure that somehow worked, and the massive bet on Bitcoin that positioned Block as the bridge between traditional finance and crypto. We'll explore how a company born from frustration at a craft fair became the infrastructure powering millions of businesses and the financial backbone for a generation that trusts apps more than banks.

What you're about to read isn't just Block's history—it's a blueprint for how technology companies can reshape entire industries by solving real problems with elegant solutions. From the glass faucet that started it all to becoming a $240 billion payment processing powerhouse, this is that story.

II. Origins: The Glass Faucet Story & Early Days

The rain was coming down hard in St. Louis when Jim McKelvey lost that sale. A successful glass artist with pieces in galleries across the country, McKelvey had just spent hours discussing a custom installation with a customer—beautiful hand-blown glass faucets worth $2,000. The client loved them, wanted them, reached for her American Express card... and McKelvey had to watch her walk away. His merchant account didn't accept Amex, and she didn't have another card. In that moment of frustration, watching money literally walk out the door, McKelvey called his friend Jack Dorsey.

Dorsey wasn't your typical Silicon Valley founder. Born in St. Louis, he'd grown up fascinated by dispatch systems—the way cities moved taxis and emergency vehicles around like pieces on a chess board. That obsession with real-time coordination had led him to co-found Twitter in 2006, but by 2009, he was looking for his next challenge. When McKelvey called with his payment problem, Dorsey saw something bigger than a lost sale. He saw an entire industry built on exclusion.

The payments landscape in 2009 was a fortress designed to keep small businesses out. Want to accept credit cards? First, you'd need a merchant account, which required good credit, substantial documentation, and weeks of waiting. Then came the hardware—clunky terminals that cost hundreds of dollars and required phone lines. The fee structure? A masterpiece of obfuscation: monthly minimums, statement fees, batch fees, PCI compliance fees, and interchange rates that varied by card type. Small businesses either couldn't qualify or couldn't understand what they were signing up for.

"We looked at the entire payments stack," Dorsey would later recall, "and realized it was built for a different era. It assumed you had a store, a counter, a phone line. It assumed you were big enough to matter." The Square concept was radical in its simplicity: What if accepting payments was as easy as plugging something into your phone? The company they built started in a tiny office above a gelato shop in St. Louis, far from Silicon Valley's sand hill road empires. Dorsey and McKelvey began with a simple prototype: a headphone jack attachment that could read magnetic stripe data from credit cards. The engineering was harder than they expected—credit card readers need precise timing and analog-to-digital conversion that smartphones weren't designed for. They went through dozens of iterations, each one slightly better at reading cards reliably.

The name "Square" came from the shape of their card reader, but also from the concept of settling up—making things square between buyer and seller. It was perfect branding: simple, memorable, and conveying fairness and transparency in an industry notorious for neither.

In 2009, Vinod Khosla's venture firm led a $10 million investment round, valuing shares at 22 cents each. The $10 million investment gave the company a $40 million valuation, before it had even launched its square-shaped mobile credit card swipers to the public. Khosla was betting on more than just a product—he was betting on Dorsey's ability to reimagine an entire industry, just as he had with Twitter.

The hardware challenge nearly killed them. Traditional card readers cost hundreds of dollars to manufacture. Square needed to get their cost down to under $10 to make the economics work. They achieved this through radical simplification: instead of building a full terminal, they created a "dumb" reader that relied on the smartphone's processing power. The audio jack became their data port—a hack that turned every iPhone into a point-of-sale terminal.

But the real disruption wasn't the hardware—it was the pricing. The payments industry in 2009 was a labyrinth of fees: interchange fees, assessment fees, processor markup, monthly minimums, statement fees, PCI compliance fees, chargeback fees, batch fees, and address verification fees. Merchants needed spreadsheets to understand what they were paying. Square's radical move? One rate: 2.75% per swipe. No monthly fees, no minimums, no contracts.

Industry veterans called them crazy. "You'll lose money on small transactions," they said. "You'll get killed on rewards cards with high interchange." They were right about the economics—Square did lose money on many transactions. But Dorsey and his team understood something the industry didn't: simplicity has value. Small businesses would pay a premium for predictability and transparency.

The early days were scrappy. The team hand-assembled card readers in their office, sometimes staying up all night to fulfill orders. Square was unveiled in December 2009 as a small credit card reader that could turn any iPhone into a mobile cash register, and by 2011 had steadily gained traction as a simple payments option for small businesses, processing millions of dollars a week in transactions.

The Twitter connection proved both blessing and curse. On one hand, Dorsey's reputation opened doors—investors, partners, and early adopters all wanted to see what Twitter's co-founder would do next. On the other hand, skeptics wondered if he could focus on two companies simultaneously. Dorsey's response was to maintain a rigid schedule: mornings at Square, afternoons at Twitter, themed days for different aspects of each business.

What made Square different wasn't just technology or pricing—it was philosophy. While traditional payment processors saw small businesses as necessary evils (unprofitable but needed for volume), Square saw them as the future. Food trucks, farmers market vendors, freelance designers, personal trainers—these were entrepreneurs who had been locked out of the electronic payments ecosystem. Square didn't just give them a card reader; it gave them legitimacy.

By late 2010, the company was ready to scale, but they needed more capital and expertise. In January 2011, Square raised $27.5 million in new funding led by Sequoia Capital with existing investor Khosla Ventures participating, at a valuation around $240 million—up from a $45 million valuation in the startup's Series A round in 2009. The addition of Sequoia wasn't just about money—partner Roelof Botha, PayPal's former CFO, joined the board, bringing crucial payments industry expertise.

The stage was set. Square had product, funding, and most importantly, product-market fit. Small businesses were signing up faster than the company could ship card readers. The payments revolution was about to begin.

III. Product-Market Fit & The Small Business Revolution

The summer of 2010 was a crucible. Square was testing its payment method on 50,000 merchants, watching every transaction like new parents watching their baby's first steps. The results were staggering: In February 2011, Square was reportedly valued at approximately US$240 million, signing up 100,000 new merchants every month. The chargeback rate—fraudulent or disputed transactions—was less than 0.05%, demolishing the industry assumption that small merchants were risky.

What drove this explosive growth wasn't just the hardware—it was the entire experience Square created around payments. Traditional merchant services required a credit check, weeks of paperwork, and a dedicated phone line. Square? Download an app, wait for your reader in the mail, and start accepting payments. The onboarding process took minutes, not weeks. For a food truck owner or a freelance photographer, this wasn't just convenient—it was revolutionary.

Square's Keith Rabois revealed that the payments service was processing $2 billion in payments volume per year. To date, Square had been activated by 800,000 merchants which was up from 500,000 card readers shipped in May. The growth was geometric, not linear—each new merchant brought credibility that attracted more merchants.

The genius of the 2.75% flat rate became clearer as Square scaled. Yes, they lost money on small transactions and high-interchange cards. But they made it up on volume and simplicity. More importantly, they changed merchant behavior. Businesses that previously only accepted cash for small purchases now accepted cards for everything. A $3 coffee? Swipe away. The psychological barrier to electronic payments had been shattered.

Square's approach to risk was equally revolutionary. Traditional processors held merchant funds for days or weeks, especially for new accounts. Square's radical move in October 2011: abolishing those limits so all new businesses who use card reader will have funds triggered for processing the same day, the proceeds arriving in the merchants bank accounts the next business day. This wasn't just faster—it fundamentally changed cash flow for small businesses.

The hardware itself became a marketing tool. That distinctive white square reader plugged into an iPhone was a conversation starter. "What's that?" customers would ask. "It's how I take credit cards now," merchants would reply, becoming evangelists for the product. Square didn't need a massive sales force—every merchant became a salesperson.

But hardware was always just the wedge. Once Square had a merchant's payment processing, they could see their entire business: sales patterns, busy hours, popular products, seasonal trends. This data became the foundation for an ecosystem of services. Square Register launched in May 2011—essentially an iPad preloaded with Square software, designed to replace entire cash register systems. By the time Square debuted Register, the company had already shipped more than 500,000 Readers and processed more than $1B in gross payments.

The traditional payments industry watched in disbelief. How could Square survive on such thin margins? How could they take such risks with instant settlements? The answer was that Square wasn't playing by industry rules. They weren't trying to maximize revenue per transaction—they were trying to maximize the number of businesses that could accept electronic payments.

This philosophy attracted not just merchants but investors. In June, the company raised an additional $100M as part of its Series C round led by Kleiner Perkins. In December, Square accepted another $30M, bringing the company's total venture funding to more than $150M in just two years. The valuation trajectory told the story: from $240 million in early 2011 to over $1 billion by year's end.

The small business revolution wasn't just about payments—it was about legitimacy. A massage therapist could now accept cards as easily as a department store. A farmer's market vendor could process transactions as smoothly as a supermarket. Square didn't just democratize payments; they professionalized the informal economy. The ecosystem play accelerated in 2014 with the launch of Square Capital. This marked a significant expansion from payment processing into lending, providing advances to merchants based on their sales data. The genius wasn't the lending itself—it was the data advantage. Square could see every transaction, every seasonal pattern, every growth trajectory. Traditional banks asked for tax returns and business plans. Square already knew if you could repay.

Originally launched as Square Capital in 2014, the company initially offered a merchant cash advance product, providing businesses with a lump-sum advance in exchange for a percentage of future sales. Since Square Capital's launch less than a year ago, it has reportedly issued more than $225 million in financing to 20,000 businesses. The average loan size was roughly $6,000—perfect for a food truck needing a new refrigerator or a boutique stocking up for the holidays.

The lending model was revolutionary in its simplicity. No credit checks, no paperwork, no waiting weeks for approval. Square would simply offer eligible merchants a loan through their dashboard, with repayment automatically deducted as a percentage of daily sales. If sales were slow, payments were lower. If business boomed, the loan was paid off faster. It aligned Square's interests perfectly with their merchants'—both succeeded when sales grew.

By 2016, Square had loaned $1 billion to companies through Square Capital since the program's inception. The default rates were remarkably low because Square's data gave them unprecedented insight into merchant health. They could see trouble coming months before a traditional lender would notice.

The small business revolution wasn't just happening in payments and lending—it was transforming the entire merchant experience. Square was building what traditional banks had promised but never delivered: a complete financial operating system for small businesses. From the card reader that started it all to payroll, inventory, appointments, and capital, Square had become indispensable infrastructure for millions of entrepreneurs.

This ecosystem approach created powerful lock-in effects. Once a business ran on Square, switching became nearly impossible. Your payment history, your customer data, your inventory system, your loan repayments—everything was interconnected. The 2.75% processing fee that seemed high in isolation became a bargain when bundled with all these services.

The transformation of America's small business landscape was profound. Coffee shops that once operated on cash and intuition now had real-time analytics. Food trucks could accept cards as easily as brick-and-mortar restaurants. Artists at craft fairs had the same payment capabilities as department stores. Square hadn't just democratized payments—they had professionalized an entire tier of the economy that banks had abandoned.

IV. Cash App: The Accidental Consumer Empire

The room was buzzing with caffeine and competitive energy during Square's 2013 hackathon. Engineers had 24 hours to build something—anything—that might become Square's next product. In one corner, a small team was working on something that seemed almost too simple: an app that let you email money to friends. No card reader required, no merchant account needed. Just type in an email address and a dollar amount. They called it Square Cash.

Jack Dorsey almost killed it. "We're a merchant company," he reportedly said when first shown the prototype. "Why would we build something for consumers?" But the team persisted, arguing that peer-to-peer payments could complement their merchant business. Reluctantly, Dorsey gave them a few months to prove the concept. Cash App was launched by Block, Inc. (then named Square, Inc.) on 13 October 2013. It was originally branded as Square Cash. While it has become commonplace for social platforms to offer one-step payment services, in 2013, Square Cash was an innovative solution that did away with the intermediaries. Users only had to connect a debit card and then they could pay people with an email address.

The early days were brutal. Square was losing money on every single user who signed up. Transaction costs, fraud losses, and customer support ate up more than the minimal interchange revenue from debit card transactions. Inside Square, there were serious discussions about shutting it down. "We're a B2B company," executives argued. "Why are we bleeding money on consumers?"

But something unexpected happened. The app found an audience Square never anticipated: young, unbanked, and underbanked Americans, particularly in the Southeast. These weren't the Silicon Valley early adopters that Venmo was attracting. These were people who'd been shut out of traditional banking—either because of past financial mistakes, lack of documentation, or simple distrust of banks. For them, Cash App wasn't just convenient; it was their first real entry into the digital economy. In 2015, Square was losing money each time a customer signed up, but in 2017 the average customer generated $15 in revenue and that has continued to increase. The transformation was driven by a fundamental shift in strategy: instead of viewing Cash App as a loss leader, Square began building an entire financial ecosystem around it.

The pivot moment came with the introduction of $Cashtags in 2015—usernames that functioned like Twitter handles but for money. This wasn't just a feature; it was a cultural phenomenon. Suddenly, rappers were putting their $Cashtags in music videos. Instagram influencers added them to their bios. The phrase "Cash App me" entered the vernacular. Square had accidentally created the first social payment network that actually felt social.

Due to strong network effects associated with P2P payments (give me your $Cashtag and I'll pay you back for lunch), Cash App has maintained an average customer acquisition cost of less than $5 per customer. That's astonishingly good compared to traditional banks, which would be hard pressed to acquire a new checking account customer for less than $250.

The network effects were powerful but subtle. Every transaction required two people—one with Cash App, one who might download it to receive money. Unlike Venmo, which kept transactions within its walled garden, Cash App made it easy to cash out instantly (for a small fee) or for free within a few days. This reduced friction meant people were more willing to try it, even if they didn't plan to become regular users.

In 2017, Square debuted the Cash Card, a physical debit card linked to Cash App balances. This was the masterstroke that transformed Cash App from a money transfer tool into a banking alternative. For customers that move beyond the app's core P2P functionality and start using the Cash Card, average revenue increases by 3-4 times. The card wasn't just functional—it was customizable, with users able to add designs, colors, even make it glow in the dark. Gen Z loved it.

The cultural cachet of Cash App became its moat. By 2018, Cash App surpassed Venmo in total downloads (33.5 million cumulative), becoming one of the most popular peer-to-peer payment platforms. Cash App is mentioned by about 200 hip-hop artists in their song lyrics, leading some to assert that it is now "ingrained in hip-hop culture." This wasn't manufactured—it was organic adoption by communities that traditional banking had ignored.

Square's marketing strategy for Cash App was unconventional: instead of buying Facebook ads, they gave money directly to users and influencers. #CashAppFriday became a phenomenon where users could win thousands of dollars just by retweeting. Partnerships with Travis Scott, Megan Thee Stallion, and Cardi B weren't traditional endorsements—they were cultural collaborations that made Cash App feel less like a financial product and more like a lifestyle brand.

The accidental consumer empire kept growing. By the fourth quarter of 2020, Cash App generated $385 million in gross profit, representing half of Square's entire gross profit. The app that Dorsey almost killed had become the company's growth engine. What started as a hackathon project to send money via email had evolved into a full-stack financial services platform serving 57 million monthly users by 2024.

But the real genius of Cash App wasn't any single feature—it was the recognition that an entire generation didn't want traditional banking. They wanted something that felt native to their phones, spoke their language, and didn't judge them for having imperfect credit or irregular income. Cash App gave them that, and in return, they gave Cash App something priceless: cultural relevance that no amount of marketing could buy.

V. The Bitcoin Bet: Mainstream Crypto

Jack Dorsey stood at the Bitcoin 2021 conference in Miami wearing a t-shirt that read "Bitcoin is my safe word." The crowd roared. This wasn't a tech CEO hedging his bets on blockchain technology—this was a true believer. Dorsey's Bitcoin maximalism wasn't just personal philosophy; it had become Square's most controversial strategic bet. The decision to add Bitcoin to Cash App in January 2018 wasn't made in a boardroom—it was made on Twitter. Dorsey had been tweeting about Bitcoin for years, calling it "the best candidate to be the internet's native currency." When Cash App users started asking why they couldn't buy Bitcoin as easily as they could send money to friends, the team had their answer.

The implementation was vintage Square: take something complex and make it simple. While Coinbase required bank verification, identity documents, and days of waiting, Cash App let existing users buy Bitcoin in seconds. No wallet addresses to manage, no private keys to lose—just tap, buy, done. They abstracted away all the complexity that scared normal people away from crypto.

In 2019, its Bitcoin revenue was a little more than $500 million. In 2020, Bitcoin revenue increased to $4.57 billion in Q4 2020 alone. The numbers were staggering, but the margins were thin—Square was making only about 2% on Bitcoin transactions. Critics called it a vanity metric, revenue without profit. But Dorsey saw something else: Bitcoin brought new users, increased engagement, and positioned Cash App as the bridge between traditional and crypto finance.

The timing was perfect. The 2020-2021 crypto bull run coincided with stimulus checks and a generation discovering investing through their phones. Cash App became the easiest way for millions of Americans to get their first Bitcoin. By the third quarter of 2020, Bitcoin transactions accounted for $1.63 billion, or 79%, of Cash App's $2.065 billion revenue. The bitcoin-based volume provided $32 million in third-quarter gross profit for Square, 15 times more than it did a year earlier.

But Dorsey's Bitcoin vision went beyond just trading. In October 2020, Square put approximately 1% of their total assets ($50 million) in Bitcoin, citing Bitcoin's "potential to be a more ubiquitous currency in the future." By 2024, Block had 8,584 BTC on its balance sheet valued at almost 1 billion dollars, with an average purchase price of 30,405 dollars per bitcoin.

The cultural impact was as significant as the financial one. Cash App made Bitcoin accessible not just technically but culturally. While crypto Twitter debated DeFi protocols and layer-2 solutions, Cash App users were buying $10 of Bitcoin because their favorite rapper tweeted about it. This wasn't the crypto revolution that maximalists imagined, but it was the one that actually happened.

Square didn't stop at simple buying and selling. They built the entire stack: Bitcoin deposits and withdrawals, integration with the Lightning Network for instant transactions, and eventually even Bitcoin mining systems. The goal wasn't just to facilitate Bitcoin transactions but to accelerate Bitcoin adoption. "If Bitcoin succeeds," Dorsey said at the Bitcoin conference, "we succeed."

The risk was enormous. Bitcoin's volatility meant revenue could swing wildly quarter to quarter. Regulatory uncertainty loomed—what if the government banned crypto? What if Bitcoin crashed and never recovered? In 2022, when crypto winter arrived, Bitcoin revenue did decline significantly, but Cash App's diversified revenue streams kept it profitable. Today, Block holds 8,692 BTC on its balance sheet, approximately 9% of its total cash, cash equivalents, and marketable securities. With Bitcoin trading above $100,000, those holdings are worth nearly a billion dollars—a massive unrealized gain from their average purchase price of around $30,000 per Bitcoin.

But the real impact of the Bitcoin bet wasn't financial—it was strategic. By making Bitcoin mainstream through Cash App, Square positioned itself at the intersection of traditional and crypto finance. When regulators come calling, when banks want to understand crypto, when institutions need a bridge to Bitcoin—they come to Block. The Bitcoin bet transformed Square from a payments company into a financial infrastructure company for the crypto age.

VI. Going Global: The IPO and Public Market Journey

The morning of November 19, 2015, Jack Dorsey stood on the floor of the New York Stock Exchange wearing two hats—literally and figuratively. As CEO of both Twitter and Square, he was about to take his second company public in one of the most scrutinized IPOs of the year. The financial press had already written the narrative: Square was overvalued, bleeding money, and its dual-CEO structure was a disaster waiting to happen. The numbers were brutal. Square priced its IPO at just $9 per share, well below the expected range of $11-$13. The implied market value of around $2.9 billion was less than half the $6 billion valuation from its last private funding round just a year earlier. On October 14, 2015, Square filed for an IPO to be listed on the New York Stock Exchange. As of that date, Dorsey owned 24.4 percent of the company.

Although the firm was yet to make a profit as of 2015 and had lost $420 million since 2012, it had decreased its losses from 44% of revenues to 16% in the six months leading up to its IPO. Progress, but not profitability. Wall Street wasn't buying the story.

The dual-CEO controversy dominated headlines. How could Dorsey run both Twitter—which was struggling with user growth—and Square simultaneously? Critics pointed to Steve Jobs' famous quote about focus: "Focus means saying no to the hundred other good ideas." Dorsey was saying yes to running two public companies. It seemed like hubris.

But Dorsey had a different philosophy. He structured his weeks with militant precision: Mondays for meetings and management, Tuesdays for product, Wednesdays for marketing and growth, Thursdays for developers and partnerships, Fridays for company culture and recruiting. He applied this schedule to both companies, spending mornings at Square and afternoons at Twitter. It was exhausting, but it worked.

The market's initial reaction was harsh. Square opened at $11.20 but the damage was done—late-stage private investors who had bought in at the $6 billion valuation were underwater. The financial press declared it a "unicorn massacre," proof that Silicon Valley's private market valuations were divorced from reality.

But something interesting happened in the months after the IPO. Square's business kept growing. Revenue for 2016 came in at $1.7 billion, up 51% year-over-year. Gross payment volume hit $50 billion. The company was still losing money, but the losses were shrinking as a percentage of revenue. The market began to notice.

For the fiscal year 2018, Block reported losses of US$38 million, with an annual revenue of US$3.299 billion, an increase of 49.0% over the previous fiscal cycle. The company was approaching profitability while maintaining aggressive growth—a combination Wall Street loved.

Then came COVID-19, and everything changed. The pandemic was devastating for Square's core small business customers—restaurants closed, retail shops shuttered, service providers couldn't operate. Square responded quickly, becoming one of the first companies to facilitate Paycheck Protection Program (PPP) loans for its merchants. They processed $873 million in PPP loans across 80,000 businesses in Q2 2020 alone.

But while the merchant business suffered, Cash App exploded. Stimulus checks, unemployment benefits, and the shift to digital payments drove unprecedented growth. Monthly active users doubled. Bitcoin trading volume soared. The stock, which had IPO'd at $9, crossed $200 per share by late 2020.

The irony wasn't lost on anyone. The company that Wall Street had dismissed as overvalued at $2.9 billion was now worth over $100 billion. Those who had mocked the dual-CEO structure watched as Dorsey proved that unconventional leadership could work. The company that couldn't turn a profit was now generating billions in gross profit.

Square's journey from failed IPO to market darling became a case study in the disconnect between private and public markets. Private investors valued potential and vision. Public markets demanded profits and predictability. Square had to learn to speak both languages, to balance growth with discipline, innovation with execution.

By 2021, when Square rebranded to Block, the transformation was complete. The struggling payments startup had become a diversified financial services giant. The dual-CEO controversy had faded—Dorsey had stepped down from Twitter to focus entirely on Block. The company that had IPO'd in distress was now one of the most valuable fintech companies in the world.

The IPO hadn't been the triumphant moment Dorsey had imagined that morning at the NYSE. But in failing to meet expectations, Square had been forced to prove itself the hard way—through execution, through results, through building real value rather than hype. The public market journey hadn't started well, but it had made Square stronger.

VII. The Afterpay Acquisition: BNPL at Scale

The boardroom at Square's San Francisco headquarters was tense in July 2021. Jack Dorsey was proposing the largest acquisition in the company's history: buying Australian buy-now-pay-later pioneer Afterpay for $29 billion. The CFO team had run the numbers—it would dilute shareholders by over 20%. The M&A advisors warned about integration risks. But Dorsey saw something bigger: the missing piece that would finally connect Square's merchant and Cash App ecosystems.

When Block announced in August 2021 that it was acquiring Afterpay in an all-stock deal, Block's share price valued the Australian buy now-pay late purchase at $29 billion. But by the time the deal closed on Jan. 31, 2022, Block's stock had dropped so much that the acquisition price tag was only $13.9 billion, based on the 113,387,895 shares offered.

The timing seemed terrible. BNPL was at peak hype in mid-2021. Klarna had just raised at a $46 billion valuation. Affirm had gone public at a massive premium. Every retailer was scrambling to offer installment payments. Critics argued Square was buying at the top, overpaying for a commodity service that any company could build.

But Dorsey and his team saw BNPL differently. This wasn't about the four-payment installment product—that was just the entry point. This was about reimagining credit for a generation that had watched their parents drown in credit card debt during the 2008 financial crisis. Millennials and Gen Z didn't want credit cards; they wanted transparent, fixed-cost financing with no surprises.

As of 2023, Afterpay serves 24 million users, processes US$27.3 billion in annual payments, and ranks among the three most-used BNPL services globally. The Australian company had cracked something Square hadn't: making credit feel good. No interest if you pay on time. No revolving debt. No hidden fees. Just split your purchase into four payments and you're done.

The strategic rationale went deeper than just adding BNPL. Afterpay brought three critical assets: a massive consumer base outside the U.S. (especially in Australia and the UK), relationships with major enterprise retailers that Square had struggled to win, and most importantly, a bridge between Square's two ecosystems. For the first time, Cash App users could discover Square merchants, and Square merchants could tap into Cash App's 50+ million users.

Integration began immediately. Within days of closing, Square launched Afterpay integration for Square Online merchants in the U.S. and Australia. Cash App users could now manage Afterpay payments directly in the app. Square merchants of all sizes—from food trucks to fashion retailers—could offer BNPL at checkout without any additional setup.

The cultural integration was equally important. Afterpay's co-founders Nick Molnar and Anthony Eisen didn't just sell and leave—they joined Block's leadership team. Molnar took on an expanded role leading Block's global seller organization. This wasn't an acquisition where the parent company strips out the technology and discards the team. Block wanted Afterpay's DNA—its merchant relationships, its consumer trust, its product philosophy.

Critics pointed to the massive decline in BNPL valuations post-acquisition. Affirm's stock crashed 90% from its peak. Klarna's valuation was slashed by 85% in its next funding round. The narrative shifted from "BNPL is the future" to "BNPL is dead." Some analysts suggested Block should write down the Afterpay purchase by $10 billion or more.

But Block's vision for Afterpay was never about standalone BNPL. It was about embedded finance—making payment options invisible infrastructure rather than branded products. When you check out with a Square merchant, Afterpay is just an option, seamlessly integrated. When you open Cash App, merchants offering Afterpay deals appear naturally. The brand matters less than the capability.

The numbers started to prove the thesis. Afterpay drove higher average transaction values for Square merchants—customers spent 20-30% more when BNPL was available. Cash App users who connected Afterpay showed 2-3x higher engagement. The cross-pollination between ecosystems created network effects that neither company could have achieved alone.

More importantly, Afterpay gave Block something invaluable: a credit product that didn't feel like credit. While traditional banks pushed credit cards with 20%+ interest rates, Block could offer transparent, fixed-cost financing that actually helped consumers manage their money better. In an era of rising interest rates and inflation, this positioning became even more valuable.

The Afterpay acquisition also accelerated Block's international expansion. Instead of slowly building country by country, Block inherited Afterpay's established presence in Australia, New Zealand, the UK, and beyond. These weren't just payment rails—they were regulatory approvals, banking relationships, merchant partnerships, and consumer trust that would have taken years to build organically.

By 2024, the integration was largely complete. Afterpay was no longer a separate company but a capability woven throughout Block's ecosystem. The $29 billion price tag that seemed absurd in 2021 looked prescient as Block captured more of the commerce value chain. The acquisition hadn't just added BNPL—it had transformed Block from a collection of services into an integrated commerce platform.

VIII. The Rebrand: From Square to Block

The email went out to all employees on Wednesday afternoon, December 1, 2021: "We're changing our name to Block." The internal Slack channels exploded. Twitter—the actual Twitter, not Block's Twitter—went into overdrive with hot takes and memes. The consensus was swift and brutal: this was either the dumbest rebrand in tech history or Jack Dorsey playing 4D chess. There was no middle ground.

The name itself was vintage Dorsey—simple, abstract, loaded with meaning. "Block references the neighborhood blocks where we find our sellers, a blockchain, block parties full of music, obstacles to overcome, a section of code, building blocks, and of course, tungsten cubes," the announcement read. Only Dorsey could connect neighborhood commerce to cryptocurrency to his infamous tungsten cube obsession in a single sentence.

On December 1, 2021, Square announced that it would change its company name to Block, Inc. The change was announced shortly after Dorsey resigned as CEO of Twitter. The timing wasn't coincidental—freed from the dual-CEO controversy, Dorsey could finally build the company he envisioned without the distraction of running Twitter alongside it.

But not everyone was celebrating. On December 16, less than a week into the rebrand, H&R Block, sued the company for trademark infringement, claiming that the name seeks to confuse customers by misappropriating the Block brand name. The tax preparation giant, which had been using "Block" since 2015, argued that Square's rebrand was a deliberate attempt to capitalize on their 65-year-old brand equity.

The newly named Block, Inc. competes directly with Block in several areas of financial services, including tax preparation through its recent purchase of Credit Karma Tax, now called Cash App Taxes. This wasn't just a trademark dispute—it was two financial services companies fighting over the same name in overlapping markets.

The lawsuit became a masterclass in corporate legal theater. H&R Block submitted articles and social media posts as evidence of consumer confusion. Block Inc.'s lawyers countered that their "house of brands" model—where Square, Cash App, and other properties maintained their own identities—prevented any real confusion. The legal battle raged for over a year.

In January 2023, a split Eighth Circuit panel ruled 2-1 in Block's favor, reversing a preliminary injunction. "Because the evidence in the record is inadequate to establish substantial consumer confusion by an appreciable number of ordinary consumers, nor irreparable harm that is concrete and imminent, H&R Block failed to satisfy its burden," U.S. Circuit Judge Ralph R. Erickson wrote. The lawsuit was finally resolved in April 2023 when the two companies jointly agreed to dismiss the suit.

But the rebrand was about more than just avoiding confusion—it was about strategic clarity. Square had become too small a box for Dorsey's ambitions. The company now encompassed Square (merchant services), Cash App (consumer finance), Afterpay (BNPL), Tidal (music streaming), TBD (decentralized finance projects), and various Bitcoin initiatives. Each needed room to grow without being constrained by the Square brand.

The change to Block acknowledged the company's evolution from a single product to an ecosystem. "Block is an overarching ecosystem of many businesses united by their purpose of economic empowerment," the company stated. The building blocks metaphor wasn't just clever marketing—it represented a fundamental shift in how the company saw itself. Not as a payments processor with some side projects, but as a collection of complementary businesses that could be assembled in different configurations for different needs.

For employees, the rebrand meant more than new business cards. It signaled a shift from being "Square employees" to being part of something bigger. Each division gained more autonomy, more identity, more ability to chart its own course while still benefiting from shared infrastructure and resources. Square could focus on merchants, Cash App on consumers, Afterpay on credit, without confusion about who they served or why.

The market initially struggled to understand the rebrand. Was this just corporate navel-gazing? Another tech company with delusions of grandeur? But as the strategy became clearer—with each brand serving distinct audiences while creating synergies between them—investors began to appreciate the logic. Block wasn't trying to be one thing to everyone; it was trying to be many things to many people, all connected by a common infrastructure and philosophy.

The rebrand also freed Block to make bolder bets. Under the Square name, buying a music streaming service seemed bizarre. Under Block, Tidal was just another building block in the creator economy ecosystem. Bitcoin initiatives that seemed risky for a payments company made perfect sense for a company building the future of money. The broader identity gave permission for broader ambitions.

IX. Modern Era: Financial Performance & Market Position

The numbers tell a story of transformation at scale. In 2024, Block's revenue was $24.12 billion, an increase of 10.06% compared to the previous year's $21.92 billion. But revenue alone obscures the real achievement—Block had evolved from a transaction processor living on thin margins to a diversified financial services powerhouse generating substantial profits.

Block Inc reported a significant gross profit growth of 18% year-over-year, reaching $8.89 billion in 2024. This metric, which Block prefers over revenue as it strips out the pass-through costs of Bitcoin trading and transaction processing, revealed the true health of the business. The company achieved a substantial increase in profitability, with adjusted EBITDA rising 69% year-over-year to $3.03 billion.

The ecosystem strategy was working. Block Inc maintained a strong gross profit retention of over 100% for both Square and Cash App. Customers weren't just staying—they were expanding their usage, adopting more products, generating more revenue per user each year. The flywheel Dorsey had envisioned was spinning faster.

In February 2024, Cash App reported 57 million monthly transacting user accounts. While user growth had plateaued—Cash App monthly active users have been relatively flat at around 57 million, with only a 2% year-over-year growth—the company was extracting more value from each user. During the last quarter of 2024, monthly active users of the Cash App card reached 25 million, up from 23 million for the year-ago quarter.

The demographics revealed Block's moat. Block estimates 21% of all 18-to-21-year-olds in the United States used the Cash App Card in 2024. This wasn't just market share—it was cultural dominance among a generation that would define banking for the next forty years. About 72% of Cash App's users are from Generation Z or millennial age groups.

Competition had intensified dramatically. Stripe, once content to power online payments invisibly, was moving into visible financial services. PayPal's Venmo maintained its social payment dominance among millennials. Traditional banks, after years of denial, were finally building competitive digital products. Apple's financial services ambitions grew monthly. Everyone wanted a piece of the digital finance pie.

But Block's integrated ecosystem provided defensive moats. A Square merchant using Square Capital for loans, Square Payroll for employees, and accepting Afterpay for customer financing wasn't easily poached. A Cash App user with direct deposit, a Cash Card, Bitcoin holdings, and stock investments had high switching costs. The ecosystem created gravity—the more services you used, the harder it became to leave.

International expansion remained a challenge. Despite Afterpay's presence in Australia and the UK, Block remained overwhelmingly American. In June 2024, Block announced it was dropping its plan to launch Cash App in Australia. In the following month, Cash App announced it would cease operations in the United Kingdom on September 15, 2024. The retreat highlighted how difficult it was to export Block's model—built on American banking infrastructure and regulations—to other markets.

The regulatory environment was tightening. In January 2025, Block agreed to pay, as part of a settlement, a fine of $80 million to a group of 48 state financial regulators after the agencies determined the company had insufficient policies for policing money laundering through Cash App. As Block became more bank-like in function, regulators expected bank-like compliance and controls.

Cash App's financial services offerings were enhanced, with paycheck deposit actives growing 25% year-over-year to 2.5 million in December. Each paycheck deposited was a vote of confidence—users trusting Cash App not just for payments but as their primary financial institution. Cash App Borrow, a feature within Cash App that allows eligible users to access small, short-term loans, reached 5 million monthly active users by the end of 2024.

The modern Block operated at a scale that would have seemed impossible when Dorsey and McKelvey were hand-assembling card readers above that gelato shop. The company reported that as a whole it processed $240.8 billion in gross payment volume in 2024, up 5.8% from 2023. Every second, thousands of transactions flowed through Block's infrastructure—coffee purchases, Bitcoin trades, peer-to-peer payments, BNPL installments, all happening simultaneously across different products but within one company.

The bear case remained compelling: margins were thin, competition was fierce, regulatory risks were mounting, and the company's valuation assumed continued growth that might not materialize. The stock's volatility reflected this uncertainty—massive swings based on quarterly results, Bitcoin prices, or regulatory headlines.

But the bull case was equally strong: Block had built irreplaceable infrastructure for the digital economy, served customer segments others couldn't or wouldn't reach, and created network effects that strengthened with scale. Most importantly, it had proven the skeptics wrong before—from the IPO disaster to the Bitcoin bet to the Afterpay acquisition, Block had consistently turned controversial decisions into competitive advantages.

X. Playbook: Business & Investing Lessons

The hardware wedge strategy that launched Square remains one of the most elegant in tech history. Give away a simple device that costs $10 to manufacture, use it to acquire merchants at near-zero cost, then expand into software and services worth thousands per customer annually. The genius wasn't the card reader—it was recognizing that hardware created trust and habit in a way that pure software couldn't. Every time a merchant plugged that white square into their phone, they were making a physical commitment to the platform.

Network effects in financial services work differently than in social networks. Facebook gets more valuable as more friends join. Block gets more valuable through interconnection—merchants want Cash App customers, Cash App users want Afterpay, Afterpay needs merchant acceptance. It's not about everyone being on the same network; it's about different networks reinforcing each other. The sum becomes exponentially greater than the parts.

Simplicity as a moat sounds paradoxical in an industry that profits from complexity, but Block proved its power. That flat 2.75% rate that seemed suicidal to industry veterans became Block's greatest marketing tool. Merchants could understand it, trust it, budget for it. In financial services, where trust is everything and complexity breeds suspicion, simplicity became a competitive advantage that was surprisingly hard to copy.

The vertical integration versus partnership decision plagued every expansion. Should Block build its own Bitcoin exchange or partner with existing ones? Create a banking charter or work with partner banks? Develop tax software or acquire it? The answer was consistently "both/and" rather than "either/or"—build core infrastructure, partner for specialized capabilities, acquire when speed matters more than cost. This hybrid approach avoided the brittleness of pure partnerships and the slowness of pure building.

Building trust in financial services requires a different playbook than other industries. You can't "move fast and break things" with people's money. Block's approach was radical transparency—publish your fees, admit your mistakes, make your policies clear. When Cash App had outages, they communicated constantly. When fraud occurred, they made users whole. Trust was earned transaction by transaction, refund by refund, over years not months.

The ecosystem play only works if you resist the temptation to force it. Block could have required Square merchants to use Cash App, or forced Cash App users to shop at Square merchants. They didn't. Each product had to win on its own merits, creating genuine value rather than artificial lock-in. The connections emerged organically—merchants discovered Cash App customers spent more, Cash App users appreciated Square merchants, Afterpay brought them together. Forced synergies fail; emergent synergies endure.

Capital allocation at Block followed a power law—a few massive bets rather than many small ones. The Bitcoin investment, the Afterpay acquisition, the Tidal purchase—each was large enough to matter, focused enough to execute, bold enough to create separation from competitors. This wasn't a company hedging its bets; it was a company making concentrated bets with conviction.

Managing multiple business lines requires accepting different economics for different purposes. Cash App's peer-to-peer payments lose money but drive engagement. Bitcoin trading generates huge revenue but tiny profits. Afterpay takes years to pay back acquisition costs. Square's core processing business funds it all. Understanding which businesses are for growth, which for profit, which for strategic position—and not confusing them—enables portfolio management that looks chaotic from outside but follows clear internal logic.

The timing lesson from Block's history is counterintuitive: being too early is better than being too late, but only if you can afford to wait. Square launched in 2009, before smartphones were ubiquitous. Cash App entered peer-to-peer payments years after Venmo. Bitcoin integration happened before mainstream adoption. In each case, Block was early enough to learn, iterate, and build infrastructure, then perfectly positioned when the market arrived. Patience plus persistence equals perfect timing.

XI. Analysis & Bear vs. Bull Case

The bull case for Block starts with an addressable market that's essentially infinite. Every transaction in the global economy—currently $150 trillion annually—could theoretically flow through digital payments. Block has barely scratched the surface. In the U.S. alone, cash still represents 20% of transactions. Globally, that number exceeds 50%. The secular shift from physical to digital money has decades left to run, and Block is positioned at every crucial intersection.

The ecosystem synergies are just beginning to compound. When a Square merchant accepts an Afterpay transaction from a Cash App user who bought Bitcoin through Block and pays with a Cash Card, that's four different revenue streams from a single purchase. These interconnections are growing geometrically—each new product creates multiple new combination possibilities. The company hasn't even begun to fully integrate these services. Imagine Cash App users getting automatic discounts at Square merchants, or Afterpay being embedded into every Square invoice, or Bitcoin Lightning payments processed instantly between any Block products. The potential permutations are endless.

The Bitcoin optionality alone could justify the current valuation. With Bitcoin trading above $100,000 and Block holding nearly 9,000 BTC, the company has an unrealized gain approaching $700 million. But that's just the balance sheet. The real option value is in the infrastructure—if Bitcoin becomes a mainstream currency, Block is one of the few companies with the rails to process it at scale. If it remains a speculative asset, Block profits from trading. If it fails entirely, Block survives. Heads they win, tails they don't lose.

Generational positioning might be Block's greatest asset. While traditional banks fight for baby boomers' declining balances, Block owns the financial lives of Gen Z and millennials. These aren't just current customers—they're future high earners who will need mortgages, investment products, insurance, and every other financial service over the next forty years. Customer acquisition costs approach zero when you're already the default financial app for an entire generation.

International expansion opportunities remain largely untapped. Despite recent retreats, the global opportunity dwarfs the U.S. market. Square's merchant services could work in any country with smartphones. Cash App's model could serve the billions globally who lack traditional banking. Afterpay has proven the BNPL model works internationally. When Block figures out international—and they will—the growth could be explosive.

But the bear case is equally compelling. Competition is intensifying from every direction. Apple's financial services ambitions grow monthly—Apple Pay, Apple Card, Apple Pay Later, and potentially Apple Bank. They have better distribution, deeper pockets, and stronger brand loyalty. Traditional banks have finally awakened—JP Morgan, Bank of America, and others are pouring billions into digital transformation. Fintech competitors multiply daily, each targeting Block's most profitable segments. The moats that seemed impregnable in 2015 look more like speed bumps in 2025.

Regulatory risks loom larger as Block becomes more bank-like. The $80 million anti-money laundering settlement was just the beginning. Regulators are scrutinizing BNPL, questioning crypto integration, examining peer-to-peer payment fraud. Banking regulations exist for reasons—consumer protection, system stability, crime prevention—and Block's "move fast" culture clashes with regulatory requirements to "move carefully." One major regulatory action could cripple growth or impose costs that destroy profitability.

Bitcoin volatility remains a double-edged sword. When Bitcoin rises, Block looks genius. When it crashes, questions multiply. The company's deep integration with crypto—from balance sheet holdings to transaction processing to mining systems—creates correlation with an asset known for 50% drawdowns. In a crypto winter, Block faces reduced transaction revenue, balance sheet losses, and investor skepticism simultaneously.

Profitability challenges persist despite the growth. Gross profit margins are healthy, but operating margins remain thin. The company burns cash on user acquisition, subsidizes numerous services, and invests heavily in new initiatives. The path to sustainable profitability requires either raising prices (risking user loss) or achieving unprecedented scale efficiencies (harder as competition intensifies).

The U.S. concentration risk cannot be ignored. Despite global ambitions, Block generates virtually all revenue domestically. This concentration makes them vulnerable to U.S. economic downturns, regulatory changes, or market saturation. The failed international expansions suggest the model might not translate easily to other markets, limiting growth potential.

Valuation poses perhaps the biggest challenge. Even after recent corrections, Block trades at premium multiples that assume continued high growth. Any stumble—a quarter of missed expectations, a regulatory setback, a successful competitive attack—could trigger multiple compression that overwhelms operational progress. The stock remains a high-beta play on multiple uncertain trends.

The path forward requires threading numerous needles: growing users while improving monetization, expanding services while maintaining simplicity, pushing innovation while ensuring compliance, investing for growth while demonstrating profitability. It's a high-wire act that few companies successfully maintain for long.

XII. Epilogue & Future Vision

Jack Dorsey's departure as Twitter CEO in 2021 was supposed to end the doubts about his commitment to Block. Yet questions about succession planning persist. Dorsey, now 48, shows no signs of stepping aside, but Block needs to demonstrate it can thrive beyond its co-founder. The company's deep bench of talent—from CFO Amrita Ahuja to the Afterpay founders—suggests continuity is possible, but the reality is that Block and Dorsey remain inextricably linked in investors' minds.

The decentralized finance vision that Dorsey evangelizes represents both Block's biggest opportunity and its greatest risk. Through initiatives like TBD, Block is building open-source, permissionless financial infrastructure. The goal is finance without intermediaries—peer-to-peer transactions, self-custody wallets, programmable money. If successful, it could revolutionize finance. If not, it's a expensive distraction from the core business.

Artificial intelligence and machine learning are quietly transforming Block's operations. Cash App's fraud detection, Square's underwriting algorithms, Afterpay's credit decisions—all increasingly powered by AI that learns from billions of transactions. The company processing $240 billion in payments annually has a data advantage that compounds daily. The question isn't whether AI will matter, but whether Block can deploy it faster than competitors with deeper AI expertise.

What does Block look like in 2030? The optimistic scenario sees a trillion-dollar financial ecosystem serving a billion users globally. Square powers commerce everywhere from food trucks to Fortune 500s. Cash App becomes the primary bank for two generations. Afterpay makes credit transparent and fair. Bitcoin integration makes Block the bridge between traditional and crypto finance. The pieces exist—execution determines success.

Key metrics to watch tell the story: gross profit growth (sustainable above 15%?), Cash App monetization rates (can they double from current levels?), Square retention rates (maintaining above 100%?), Afterpay integration metrics (cross-sell rates between products), and Bitcoin correlation (decreasing as other revenue streams grow?). These numbers, more than stock price, reveal whether the ecosystem thesis is working.

The biggest surprise from researching Block's history isn't what they've built—it's what they've survived. The failed IPO that priced below private valuations. The dual-CEO controversy that dominated headlines for years. The Bitcoin bet that seemed insane. The Afterpay acquisition at peak valuations. The rebrand lawsuit. The international retreats. Any of these could have been fatal. None were.

This resilience suggests something deeper than luck. Block has developed an organizational capacity to absorb shocks, learn from failures, and emerge stronger. The company that hand-assembled card readers in 2009 now processes nearly a quarter-trillion dollars annually. The hackathon project that became Cash App serves 57 million users. The Bitcoin experiment generates billions in revenue. The pattern is clear: Block thrives on challenges others avoid.

The future of money is being written in code, decided in board rooms, and shaped by consumer choices happening millions of times daily. Block sits at the intersection of all three—building the infrastructure, making strategic bets, and serving users others ignore or underserve. Whether that positioning leads to dominance or disruption remains uncertain. What's certain is that the financial system of 2040 will look radically different from today's, and Block intends to build it.

The story that began with a lost sale at a craft fair has become something nobody could have predicted—a financial ecosystem serving everyone from street vendors to stock traders, artists to accountants, teenagers getting their first debit card to retirees managing their savings. It's messy, ambitious, controversial, and incomplete. In other words, it's exactly what you'd expect from Jack Dorsey.

XIII. Recent News

Block's fourth quarter 2024 results, announced February 20, 2025, shocked Wall Street despite strong full-year performance. Block reported fourth-quarter results on Thursday that fell short of Wall Street expectations. The stock dropped more than 6% in extended trading. Earnings per share: 71 cents adjusted vs. 87 cents expected. Revenue: $6.03 billion vs. $6.29 billion expected.

The miss obscured significant operational improvements. Block posted $2.31 billion in gross profit, a 14% increase from $2.03 billion a year ago. More importantly, the company's two main segments showed strong performance: Cash App gross profit totaled $5.24 billion for the year, up 21% from 2023, and Square gross profit came to $3.6 billion, up 15% year-over-year.

Product launches accelerated in early 2025. This week, Afterpay on the Cash App card begins rolling out. CEO Jack Dorsey expressed enthusiasm about the integration: "We have a huge base of Cash Card customers that we can deploy this to. We can do that extremely quickly. It's easy to roll out for us and alert people proactively of entirely new utility that they can use that day, instantly."

The Bitcoin mining initiative showed progress. Block's open bitcoin mining system is called Proto. Ahuja said on the earnings call that the company expects the initiative to start benefitting growth in the second half of 2025. This represents Block's continued push into Bitcoin infrastructure beyond just trading.

Regulatory settlements dominated headlines in January 2025. Beyond the $80 million anti-money laundering fine, Block reached another settlement with the Consumer Financial Protection Bureau. The agreement includes a $55 million fine and up to $120 million in refunds for users. The agency's investigation found that Cash App's weak security and poor customer service left users vulnerable to fraud.

Looking ahead, management provided cautiously optimistic guidance. Block has set a gross profit guidance of at least $10.22 billion for 2025, representing a projected growth of 15%. The company continues to focus on profitability, with adjusted operating income margins reaching record levels.

Executive confidence remained high despite near-term challenges. Dorsey articulated the long-term vision of integrating Cash App and Square into a single financial ecosystem: "There will be a significant reason to use Cash App and not have to go to the App Store for 10 different apps. Everything is in one app, and that will be the Cash App."

XIV. Links & References

For those seeking deeper understanding of Block's journey, the primary sources start with SEC filings available at investors.block.xyz, providing quarterly earnings, annual reports, and detailed financial statements. The company's investor relations site offers transcripts of all earnings calls, where Jack Dorsey and Amrita Ahuja provide unfiltered insights into strategy and execution.

Key interviews with Jack Dorsey illuminate the philosophy behind Block's decisions. His appearances at the Bitcoin Conference, particularly the 2021 and 2022 keynotes, reveal his crypto maximalism. The 2019 interview with 60 Minutes shows him defending the dual-CEO structure. His 2020 conversation with Andrew Ross Sorkin at the DealBook Conference explains the Square Capital model.

Academic research on payment processing includes "The Economics of Payment Card Markets" by Jean-Charles Rochet and Jean Tirole, essential for understanding interchange fees. "Network Effects in Two-Sided Markets" by Geoffrey Parker and Marshall Van Alstyne explains the dynamics Block exploits. Harvard Business School's case studies on Square's early days provide detailed operational insights.

Industry reports from McKinsey's Global Payments Report track the secular shift to digital payments. The Nilson Report offers authoritative data on payment volumes and market share. CB Insights' fintech reports analyze competitive dynamics and emerging threats.

Books capturing Block's history include "The Innovation Stack" by Square co-founder Jim McKelvey, providing an insider's account of the early days. "The Everything Store" by Brad Stone, while focused on Amazon, offers relevant parallels on platform building. "Zero to One" by Peter Thiel articulates the philosophy of building monopolies through innovation that Block exemplifies.

Technical papers on Bitcoin and Lightning Network from the Bitcoin Developer mailing lists help understand Block's crypto infrastructure investments. The Lightning Network whitepaper by Joseph Poon and Thaddeus Dryja explains the scaling solution Block is implementing. Satoshi Nakamoto's original Bitcoin whitepaper remains essential reading.

The Afterpay acquisition documents, available through Australian securities filings, detail the strategic rationale and financial terms. Analysis from investment banks including Goldman Sachs and Morgan Stanley provide institutional perspectives on the deal's implications.

Analyst coverage from Mizuho's Dan Dolev, consistently bullish on Block, offers detailed financial modeling. Wolfe Research provides skeptical counterpoints. MoffettNathanson's payments industry analysis places Block in broader context.

Community and developer resources include Block's open-source repositories on GitHub, showing actual code implementations. The Square Developer documentation reveals API capabilities and integration possibilities. Cash App's Reddit community provides grassroots user feedback and feature requests.

Podcast appearances by Block executives on "This Week in Startups," "The Tim Ferriss Show," and "Invest Like the Best" offer long-form discussions of strategy. The Acquired podcast's two-part series on Square provides comprehensive historical analysis similar to this piece.

For ongoing coverage, the Financial Times' fintech section, The Information's payments coverage, and Reuters' financial services reporting provide breaking news and analysis. Twitter remains ironically essential—Dorsey's account offers real-time thoughts, while accounts like @CashApp and @Square provide product updates.

The complete picture emerges only by synthesizing these sources—financial filings reveal what happened, interviews explain why, academic research provides context, and ongoing coverage tracks what's next. Block's story isn't finished; these resources help readers write the next chapters themselves.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube