ExxonMobil: The Empire That Oil Built

I. Introduction & Episode Framing

The helicopter circles the Liza Destiny floating production vessel, 120 miles off Guyana's coast. Below, in waters deeper than the Empire State Building is tall, lies one of the most significant oil discoveries of the 21st century—11 billion barrels of recoverable oil that nobody saw coming. Not the skeptics who declared the age of oil exploration dead. Not the competitors who passed on these blocks. And certainly not the climate activists who've spent decades predicting this company's demise.

This is ExxonMobil in 2024: simultaneously the villain in every climate documentary and the hero of every energy security discussion. A company that generates more free cash flow than Amazon, Microsoft, and Meta combined during oil price spikes, yet trades at a fraction of their multiples. The last titan standing from the greatest monopoly ever assembled, now navigating between shareholders demanding higher returns and a world demanding lower emissions.

The numbers tell one story: America's 7th largest company by revenue, producing 3.8 million barrels of oil equivalent daily, with a market capitalization hovering around $500 billion. But the real story—the one we're going to unpack over the next several hours—is far more complex. It's about how a Cleveland kerosene refiner's obsession with efficiency created a corporate DNA so dominant that it survived antitrust dismemberment, two world wars, nationalization of its largest assets, and now faces its greatest existential challenge: the energy transition.

The question isn't whether ExxonMobil will survive—it's proven remarkably adept at that for 150 years. The question is what it will become. Will it follow European peers like BP and Shell into renewable energy, accepting lower returns for social license? Will it double down on being the last, best oil company standing as others retreat? Or will it thread an entirely different needle—using its engineering prowess and capital strength to dominate carbon capture and hydrogen while keeping oil profits flowing?

To understand where ExxonMobil is heading, we need to understand how it got here. Because buried in this company's history are patterns that repeat with almost algorithmic precision: consolidate during downturns, invest countercyclically, prioritize technology over dealmaking, and never, ever, chase the market. These patterns made John D. Rockefeller the richest man in modern history. They made ExxonMobil the world's most valuable company multiple times. And they're about to be tested like never before.

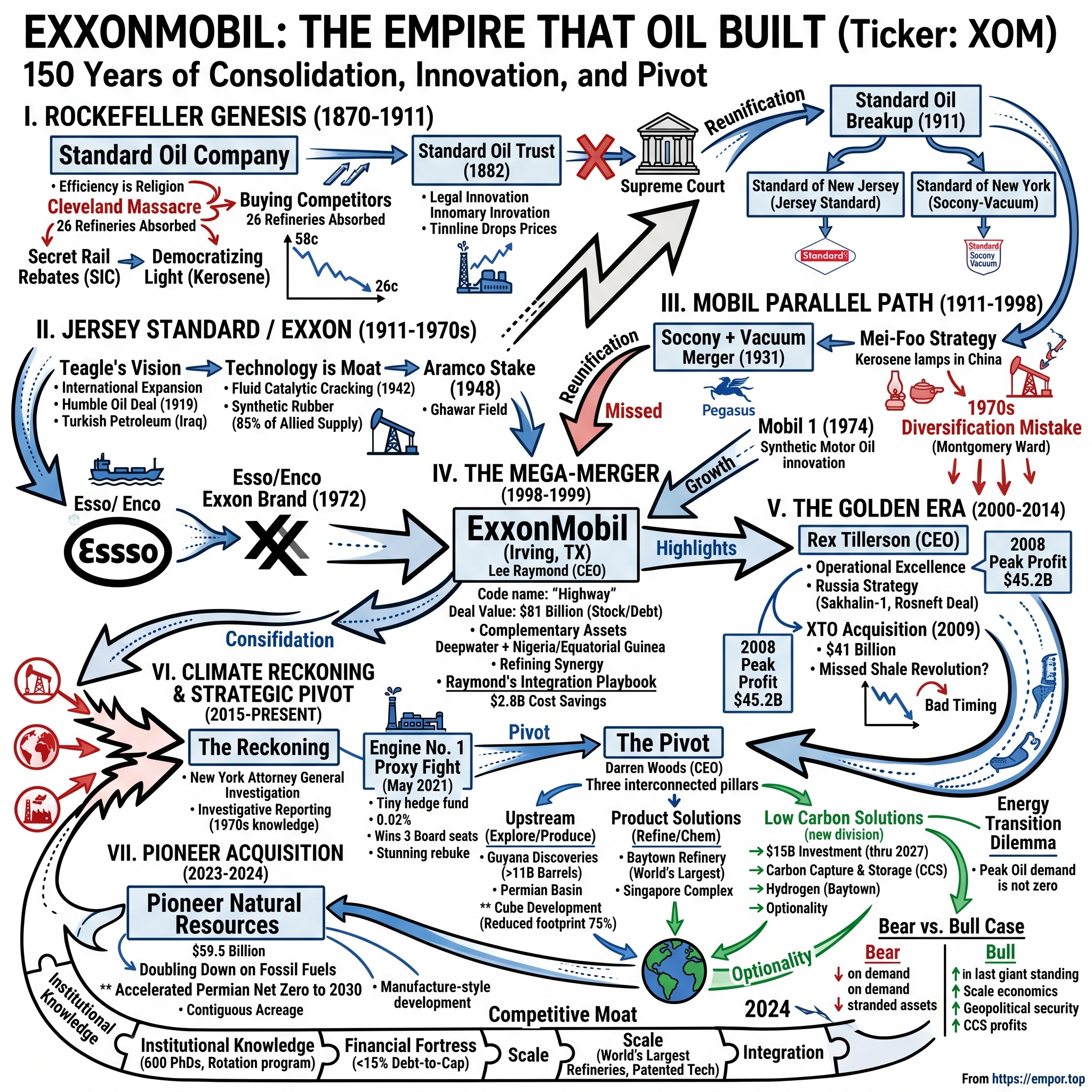

II. The Rockefeller Genesis & Standard Oil Era (1870–1911)

John D. Rockefeller didn't set out to build an empire. On September 26, 1855, the 16-year-old son of a traveling salesman was simply looking for work in Cleveland when he landed a job as an assistant bookkeeper at Hewitt & Tuttle, commission merchants dealing in grain and produce. That date—September 26—would become so sacred to him that he celebrated it as "Job Day" for the rest of his life, more important than his birthday.

What Rockefeller discovered in those ledgers wasn't just numbers—it was a language of efficiency that would become his religion. By 1863, at just 24, he'd saved enough to invest $4,000 in a Cleveland refinery with partner Maurice Clark. The timing was perfect: Colonel Edwin Drake had drilled the first commercial oil well in Pennsylvania just four years earlier, and Cleveland sat at the perfect intersection of rail lines to ship refined kerosene east.

But here's where Rockefeller diverged from his competitors. While others rushed to drill wells—chasing the volatile fortunes of oil discovery—Rockefeller focused on refining. "The man who controls refining," he observed, "controls the oil business." It was a insight that would reshape American capitalism. On January 10, 1870, Rockefeller incorporated Standard Oil Company in Ohio, transforming his partnership into a corporation with $1 million in capital. The ownership structure revealed the careful alliance-building that would define his approach: of the initial 10,000 shares, John D. Rockefeller received 2,667, Harkness received 1,334, William Rockefeller, Flagler, and Andrews received 1,333 each.

The genius of Rockefeller's strategy emerged not in what he built, but in what he bought. In February 1872, he launched what competitors would later call "The Cleveland Massacre." Using a secret rebate scheme with railroads through the South Improvement Company—which would give him not just discounts on his own shipments but actual kickbacks on his competitors' shipments—Rockefeller approached Cleveland's 26 other refineries with a simple proposition: sell to me now at a fair price, or be crushed later.

In less than two months, he absorbed or destroyed most of his competition in Cleveland. By year's end, Standard controlled nearly all the refineries in Cleveland. The speed was breathtaking, the efficiency ruthless. When one holdout refiner asked Rockefeller how he could justify such tactics, he replied with characteristic certitude: "The day of individual competition in the oil business is past and gone."

The numbers validated his vision. Standard's actions and secret transport deals helped its kerosene price drop from 58 to 26 cents from 1865 to 1870. Before 1870, oil light was only for the wealthy, provided by expensive whale oil. During the next decade, kerosene became commonly available to the working and middle classes. Rockefeller wasn't just monopolizing an industry—he was democratizing light itself.

But it was in the details that Rockefeller's true genius emerged. While most companies dumped gasoline in rivers (this was before the automobile was popular), Standard used it to fuel its machines. While other companies' refineries piled mountains of heavy waste, Rockefeller found ways to sell it. Every barrel of crude oil that entered a Standard refinery emerged as 300 different products—from tar to chewing gum. Nothing was wasted. Everything had value.

By 1880, the transformation was complete. Through elimination of competitors, mergers with other firms, and use of favorable railroad rebates, Standard controlled the refining of 90 to 95 percent of all oil produced in the United States. But Rockefeller faced a problem: Ohio law prohibited his company from owning assets outside the state. His solution would revolutionize American business.

On January 2, 1882, a group of 41 investors signed the Standard Oil Trust Agreement, which pooled their securities of 40 companies into a single holding agency managed by nine trustees. The original trust was valued at $70 million. This wasn't just a business structure—it was the invention of the modern corporation, a legal innovation that would be copied by every major industry from steel to tobacco.

The trust structure allowed Rockefeller to control a vast industrial empire while technically complying with state laws. It was brilliant, it was legal (barely), and it was absolutely devastating to competition. By 1890, Standard Oil controlled not just refining but pipelines, railroad tank cars, barrel-making plants, and even the boats that carried oil overseas. It was vertical integration on a scale never before imagined. But the public was finally pushing back. A series of exposés by journalist Ida Tarbell, whose own father had been ruined by Rockefeller's tactics, turned public opinion decisively against Standard Oil. Theodore Roosevelt's trust-busting administration filed suit in 1906. After years of legal battles, on May 15, 1911, Chief Justice Edward White delivered the Supreme Court's unanimous decision: Standard Oil had illegally monopolized the American petroleum industry and must break itself up.

The irony was delicious. The Supreme Court ordered Standard to break up into 39 independent companies with different boards of directors, the biggest two of the companies being Standard Oil of New Jersey (which became Exxon) and Standard Oil of New York (which became Mobil). The breakup was meant to punish Rockefeller, but it made him richer than ever. His wealth nearly tripled. His pre-ruling holdings in Standard Oil was approximately 25% of the company. Rockefeller received 25% of the stock in each of the 33 companies which saw his wealth increase from $300 million to $900 million shortly after the ruling.

The descendants of Standard Oil would eventually include not just Exxon and Mobil, but also Chevron, Amoco (later BP), Marathon, and ConocoPhillips. The DNA of Rockefeller's empire would spread through the entire global oil industry. And two of those pieces—Jersey Standard and Socony-Vacuum—would spend the next 88 years slowly finding their way back to each other.

III. The Jersey Standard/Exxon Evolution (1911–1970s)

Walter Teagle stood at the window of his office at 26 Broadway in Lower Manhattan, watching the protestors below. It was 1920, and Standard Oil of New Jersey—the largest piece of the broken trust—was under assault again. This time not from trustbusters but from a public that had just discovered Jersey Standard had been buying oil from the Bolsheviks. The revelation perfectly captured the company's operating philosophy: profits over politics, efficiency over ideology, expansion over everything.

Teagle, who'd become president in 1917 at just 39, understood something his critics didn't: Jersey Standard had emerged from the breakup with the crown jewels of Rockefeller's empire—the Standard Oil brand internationally, the massive Bayway refinery in New Jersey, and most importantly, the institutional knowledge of how to operate at global scale. But it had also inherited a critical weakness: almost no oil production of its own. This weakness drove Jersey Standard's strategy for the next 60 years. Unable to produce enough oil domestically, Teagle embarked on an aggressive international expansion. For $17 million Jersey acquired 50 percent of the Humble Oil Refining Company of Houston, Texas, a young but rapidly growing network of Texas producers that immediately assumed first place among Jersey's domestic suppliers. Although only the fifth leading producer in Texas at the time of its purchase, Humble would soon become the dominant drilling company in the United States.

The international push was even more dramatic. World War I had demonstrated the crucial role of oil in modern warfare and prompted the U.S. government to encourage U.S. participation in the newly formed Turkish Petroleum Company, operating in present-day Iraq. A consortium of U.S. oil companies was sold 25 percent of Turkish Petroleum. By the early 1930s only Jersey Standard and Socony were left in the partnership, with each eventually holding 12 percent.

But it was technology that truly set Jersey Standard apart. In 1942, at the Baton Rouge refinery, the company completed construction of the world's first fluid catalytic cracker—a revolutionary technology that increased gasoline yields from crude oil by 50%. The timing couldn't have been better. With World War II raging, high-octane aviation fuel was desperately needed for Allied fighters and bombers. Jersey Standard's refineries produced billions of gallons of 100-octane fuel that literally powered the Allied victory.

The company also pioneered synthetic rubber production when Japanese forces cut off natural rubber supplies from Southeast Asia. Jersey Standard's Butyl rubber, developed in its labs and produced at massive scale, kept Allied vehicles rolling and aircraft flying. By war's end, the company was producing 85% of all synthetic rubber used by the Allies. The post-war era brought Jersey Standard's most consequential deal. In 1948, Jersey Standard and Socony-Vacuum each acquired stakes in Aramco—Jersey Standard taking 30% and Socony-Vacuum 10%, alongside Socal and Texaco who each held 30%. This gave Jersey Standard access to what would prove to be the world's largest oil reserves, including the Ghawar field discovered that same year—a single field that would eventually produce more oil than all U.S. reserves combined.

But success bred vulnerability. By the 1960s, Jersey Standard faced a peculiar problem: it was too successful under too many names. In different states, it operated as Esso (from S-O, for Standard Oil), Enco (Energy Company), or Humble. Other Standard Oil descendants successfully blocked Jersey Standard from using the Esso brand in their territories. The confusion was hampering growth.

In 1972, after spending $100 million on research and legal clearances, Jersey Standard unveiled its solution: Exxon. The double X was meant to echo the double S in Esso, while being completely unique and pronounceable in any language. Critics mocked it as sounding like a pesticide. Within a decade, it would become one of the most valuable brands on Earth.

The transformation from Jersey Standard to Exxon was more than cosmetic. Under CEO Clifton Garvin in the 1970s, Exxon became the epitome of engineering excellence and operational efficiency. While competitors diversified into chemicals, retail, even office equipment, Exxon remained laser-focused on finding, producing, and refining oil as efficiently as possible. This discipline would serve it well when oil prices collapsed in the 1980s, forcing weaker players to merge or exit while Exxon continued generating profits.

IV. The Mobil Parallel Path & Competitive Dynamics (1911–1998)

In 1931, at the depth of the Great Depression, two oil companies that had been circling each other for decades finally merged. Standard Oil of New York (Socony) and Vacuum Oil created Socony-Vacuum, later to become Mobil. The merger was defensive—oil prices had collapsed, markets were shrinking, and both companies needed scale to survive. But what emerged was something neither company could have achieved alone: the first truly global American oil brand.

Vacuum Oil brought to the marriage something unique—the flying red horse, Pegasus, which it had used since 1911 in South Africa. The symbol was perfect: classical enough to signal quality, dynamic enough to suggest speed and power. Within a decade, Pegasus would fly over service stations from Tokyo to London, becoming perhaps the most recognized corporate symbol in petroleum history. But Socony-Vacuum's real genius lay in understanding emerging markets before that term existed. Socony gains a strong foothold in the vast market for kerosene in China by developing small lamps that burned kerosene efficiently. The lamps become known as Mei-Foo, from the Chinese symbols for Socony, meaning "beautiful confidence." These weren't just lamps—they were a marketing revolution. In its first year, more than 850,000 lamps were sold in China at around 7.5 cents each, a price designed to ensure as many people as possible could purchase them.

The Mei Foo strategy epitomized Mobil's approach: don't just sell a product, create a market. Where Jersey Standard focused on efficiency and scale, Mobil focused on brand and innovation. This philosophy would manifest most dramatically in 1974 when Mobil introduced the world's first synthetic motor oil—Mobil 1. While competitors scoffed at the high price point, Mobil understood that premium products create premium margins. Within a decade, Mobil 1 would become the factory fill for Mercedes, Porsche, and eventually, the official lubricant of Formula One.

The 1970s oil crises should have been Mobil's moment. Oil prices quadrupled. Profits soared. But CEO Rawleigh Warner Jr. made a fateful decision: diversify away from oil. Mobil bought Montgomery Ward, the retailer. Container Corporation of America, a packaging company. Even pursued Marcor, a conglomerate. Each acquisition diluted focus and destroyed value. By 1976, Mobil's return on capital had fallen below Exxon's despite higher oil prices.

The companies' rivalry intensified through the 1980s and 1990s, but it was a rivalry between increasingly similar entities. Both had massive downstream operations. Both had significant chemical businesses. Both were technology leaders. And crucially, both were struggling with the same fundamental problem: finding enough oil reserves to replace what they were producing.

By 1998, the logic of combination had become inescapable. Oil prices had collapsed to $11 per barrel. Finding costs were soaring. National oil companies were becoming more assertive. And both Exxon and Mobil, despite their size, were subscale compared to the emerging supermajors being created in Europe through BP-Amoco and Total-Fina-Elf mergers.

The final catalyst came from an unlikely source: Lou Noto, Mobil's CEO, who had previously rebuffed Exxon's overtures. But with Mobil's upstream position weakening and its downstream margins under pressure, Noto finally picked up the phone. The negotiation that followed would be swift, secret, and decisive.

V. The Mega-Merger: Creating Modern ExxonMobil (1998–1999)

Lee Raymond sat in his corner office at Exxon's Irving, Texas headquarters, staring at oil prices that had done the unthinkable: dropped below $11 a barrel. It was March 1998, and the Asian financial crisis had cratered demand just as Iraqi oil returned to markets. For the first time since 1986, Exxon's legendary financial discipline was being tested. The company was still profitable—barely—but Raymond knew that at these prices, the entire industry structure was unsustainable. The phone call that would reshape the oil industry came in June 1998. Lou Noto, Mobil's CEO, had finally come to the same conclusion as Raymond: in a world of $10 oil, even giants needed to merge to survive. The two men met secretly at Raymond's home in Dallas, referring to the project as "Highway"—a code name that reflected both companies' origins as sellers of motor fuel.

The negotiations were secretly conducted over the past five months under the code name "Highway". What followed was a masterclass in corporate dealmaking. Raymond and Noto understood that this wasn't just a financial transaction—it was the reunification of the two largest pieces of Rockefeller's empire, companies that had competed and cooperated, innovated and imitated each other for 87 years.

The numbers were staggering. At the announced price, Exxon would pay about $77 billion in stock for Mobil and assume about $4 billion in long-term debt, giving the deal a total value of $81 billion. Exxon shareholders would own about 70 percent of the company; Mobil shareholders would own the rest. It was the largest industrial merger in history.

But the real genius lay in the industrial logic. The consolidation facilitated the combination of Exxon's rich experience in deepwater exploration with Mobil's production and exploration acreage in Nigeria and Equatorial Guinea. The companies had complementary refining assets—Exxon strong in the Gulf Coast, Mobil dominant in the Northeast. Their chemical businesses overlapped just enough to generate synergies but not enough to create antitrust problems.

Raymond promised $2.8 billion in cost savings within three years. Wall Street scoffed—merger synergies were the corporate world's most broken promise. But Raymond wasn't making empty promises. He had a 146-page integration playbook ready before the deal was even announced. Every business unit knew its targets. Every manager knew their role. The message was clear: this wasn't a merger of equals. It was Exxon buying Mobil, and Exxon's culture would prevail.

The regulatory gauntlet was brutal. The Federal Trade Commission demanded the largest divestiture in its history—2,431 gas stations, a major refinery in California, pipeline interests, and numerous terminals. European regulators extracted their own pounds of flesh. But Raymond had anticipated this. The divestitures were surgical, leaving the combined company's core strengths intact while satisfying regulators that competition would be preserved.

Though many analysts and oil industry experts said the Exxon and Mobil cultures were like oil and water, Raymond said their cultures were similar, particularly their shared love of intense and constant analysis. This wasn't corporate spin. Both companies were engineering cultures, places where data trumped intuition, where spreadsheets were scripture. The Mobil executives who survived the merger were those who could adapt to Exxon's even more rigorous analytical approach.

The human cost was significant. The new company would save $2.8 billion in expenses over the next three years and shed at least 9,000 jobs. Entire departments were eliminated. Mobil's Fairfax headquarters became a ghost town before being converted to the company's downstream headquarters. But for those who remained, the merger created extraordinary opportunity. The combined company had the scale to tackle projects—like Sakhalin in Russia or Kashagan in Kazakhstan—that neither company could have managed alone.

The merger closed on November 30, 1999, just as oil prices began their recovery. Within a year, crude had tripled to $30 a barrel. Within five years, it would hit $70. The timing seemed impossibly fortuitous, but Raymond would later insist it was irrelevant. "We didn't merge because we thought oil prices would go up," he said. "We merged because we knew that whether oil was at $10 or $100, the combined company would outperform."

By every financial metric, he was right. The average growth rate of net income in the premerger period increased from 12.9% to 19.78% in the post-merger period. The promised synergies of $2.8 billion? The company delivered $3.8 billion. During Raymond's tenure as the head of the largest oil corporation in the world, he consistently produced results which exceeded competitors and market expectations. ExxonMobil beat the S&P 500 performance every year between 1993 and 2003.

VI. The Golden Era: Peak Oil Profits & Global Dominance (2000–2014)

Rex Tillerson stood before a map of the world in ExxonMobil's Irving war room, colored pins marking the company's global empire. It was January 2006, his first day as CEO, and oil had just crossed $60 a barrel. The company Raymond had left him was a profit-generating machine: $36 billion in net income the previous year, more than any company in history. But Tillerson, an Eagle Scout from Wichita Falls who'd joined Exxon as an engineer in 1975, saw vulnerabilities others missed. The problem was simple: conventional oil was getting harder to find. ExxonMobil's reserve replacement ratio—the amount of new oil discovered versus oil produced—had been declining for years. The easy fields were gone. What remained required drilling in Arctic waters, ultra-deepwater, or in politically unstable countries. Meanwhile, a revolution was happening in America's backyard that ExxonMobil had completely missed: shale.

Small independent companies using horizontal drilling and hydraulic fracturing were unlocking vast reserves of oil and gas from shale formations. While ExxonMobil was spending billions drilling dry holes in the Arctic, companies like XTO Energy were quietly building dominant positions in the Barnett, Marcellus, and Haynesville shales. By 2009, it was clear that shale wasn't a fad—it was the future of American energy. In December 2009, Tillerson made his defining move: a $41 billion all-stock acquisition of XTO Energy. Including $10 billion of existing XTO debt, it was ExxonMobil's largest acquisition since the merger that created the company. XTO's resource base was the equivalent of 45 trillion cubic feet of gas and included shale gas, tight gas, coal bed methane, and shale oil.

The timing seemed perfect. Natural gas prices were depressed, XTO's shareholders were eager to sell, and ExxonMobil needed to reposition itself for what many believed would be an era of abundant, cheap, clean-burning natural gas. The Wall Street Journal's Michael Corkery would later write that "Tillerson's legacy rides on the XTO deal."

It turned out to be one of the worst-timed acquisitions in oil industry history. Within months of closing, natural gas prices collapsed from $6 to $2 per thousand cubic feet and stayed there for years. The shale revolution that XTO was supposed to help ExxonMobil lead instead became a victim of its own success—so much gas was being produced that prices cratered. ExxonMobil would eventually write down much of the XTO acquisition value.

But Tillerson's other initiatives proved more successful. His focus on operational excellence pushed ExxonMobil's upstream operations to new heights of efficiency. The company's return on average capital employed consistently exceeded 20%, often double that of competitors. In 2008, during the oil price spike, ExxonMobil recorded the largest annual profit in corporate history: $45.2 billion.

Tillerson also cultivated relationships that would define his tenure—and eventually his post-ExxonMobil career. In August 2011, Putin attended a ceremony in Sochi where Tillerson and Igor Sechin, CEO of Rosneft, signed an agreement to drill the East-Prinovozemelsky field in the Arctic Ocean valued at up to $300 billion. The Rosneft deal also gave the state-owned oil company a 30% stake in Exxon owned assets in the U.S.

The relationship with Russia would prove both lucrative and problematic. ExxonMobil's Sakhalin-1 project demonstrated the company's technical prowess, using extended-reach drilling to access offshore reserves from onshore locations. But when the U.S. imposed sanctions on Russia following the 2014 annexation of Crimea, ExxonMobil was forced to abandon joint ventures that Tillerson had spent years cultivating.

Meanwhile, ExxonMobil's downstream and chemical businesses were generating extraordinary returns. The company's refineries, upgraded with billions in investment, could process the heaviest, sourest crudes—buying them at steep discounts and converting them into high-value products. The chemical business, producing everything from plastic packaging to synthetic rubber, benefited from the same shale revolution that had hurt the XTO acquisition, using cheap natural gas as feedstock.

By 2014, as oil prices began their precipitous fall from $100 to below $30, ExxonMobil faced a reckoning. The company that had seemed invincible—generating more profit than any corporation in history—suddenly looked vulnerable. Its high-cost projects in the Arctic and oil sands were underwater. The XTO acquisition was a albatross. And most troubling, its reserve replacement ratio had fallen below 100% for the first time in decades.

But the company's response demonstrated why it had survived for over a century. Capital spending was slashed from $42 billion to $23 billion. Thousands of employees were let go. Marginal projects were cancelled. The dividend—sacred at ExxonMobil—was maintained, but share buybacks were suspended. It was classic ExxonMobil: disciplined, unsentimental, focused on long-term value over short-term market appeasement.

VII. Climate Reckoning & Strategic Pivot (2015–Present)

The email landed in Darren Woods' inbox on a September morning in 2015, months before he would become CEO. It was from Mark Carney, Governor of the Bank of England, warning that climate change posed a systemic risk to the global financial system. Companies that didn't adapt, Carney suggested, would face an existential crisis. Woods, a chemical engineer who'd spent his career optimizing refineries, understood immediately: this wasn't environmental activism. This was the financial establishment signaling a fundamental shift. Woods had taken over from Tillerson in January 2017, inheriting a company under siege. The New York Attorney General had launched an investigation into whether ExxonMobil had misled investors about climate risks. Environmental activists were comparing the company to Big Tobacco. And most damaging, investigative reporting had revealed that Exxon's own scientists had accurately predicted climate change as early as the 1970s, even as the company publicly questioned the science.

The reckoning came on May 26, 2021. A tiny hedge fund called Engine No. 1, owning just 0.02% of ExxonMobil's shares—worth about $40 million—had launched a proxy fight to replace four board members. The fund's argument was devastatingly simple: ExxonMobil had destroyed shareholder value by failing to prepare for the energy transition. Over the preceding ten years, ExxonMobil had lost money while stock market indices had tripled.

Engine No. 1 spent approximately $30 million on the campaign which was almost equal to its $33 million investment in Exxon's shares. Exxon similarly spent at least $35 million in its defence. The money was spent on a sophisticated campaign targeting ExxonMobil's largest institutional shareholders—BlackRock, Vanguard, and State Street, who collectively controlled almost 21% of the total shares.

The vote was a stunning rebuke. Exxon Mobil, one of the largest corporations in the world, lost three board seats in a proxy fight with Engine No. 1, giving the dissident control of a quarter of the board. For the first time in its history, ExxonMobil had lost a proxy fight. The symbolism was unmistakable: even Big Oil couldn't ignore climate change anymore.

But Woods' response was masterful in its subtlety. Rather than fight the new reality, he co-opted it. ExxonMobil announced ambitious plans for Low Carbon Solutions, committing $15 billion through 2027 for carbon capture, hydrogen, and biofuels. The company set a target of achieving net-zero emissions from its Permian Basin operations by 2030. It began reporting Scope 3 emissions—those from customers burning its products.

Yet beneath the green rhetoric, Woods was executing a very different strategy. While European oil majors were selling assets and pivoting to renewables, ExxonMobil was doubling down on its core business. The Guyana discoveries kept getting bigger—now estimated at over 11 billion barrels. The Permian Basin assets were generating massive cash flows. And most importantly, the company was using its engineering expertise to reduce the carbon intensity of its operations, making its oil the "cleanest" in the industry. The Guyana story exemplified Woods' strategy perfectly. The Liza discovery was announced in May 2015. Liza-1 well was the first significant oil find offshore Guyana. What started as a high-risk exploration play had become one of the greatest oil discoveries of the 21st century. The gross recoverable resource for the Stabroek Block is now estimated to be nearly 11 billion oil equivalent barrels, discovered at a finding cost of less than $1 per barrel—unheard of in the modern oil industry.

More importantly, Guyana oil was among the lowest carbon-intensity barrels in the world. The offshore location meant no community disruption. The reservoir quality was exceptional, requiring minimal processing. And ExxonMobil was implementing carbon capture at the source, reinjecting CO2 into the reservoirs. It was, Woods argued, exactly the kind of oil the world would need during the energy transition: low-cost, low-carbon, highly profitable.

The financials validated the strategy. Despite the Engine No. 1 proxy fight, despite the climate litigation, despite the ESG pressure, ExxonMobil's stock had outperformed every other oil major since Woods became CEO. The company was generating so much cash that it could fund both its traditional business and its low-carbon initiatives without diluting returns.

But the real test of Woods' strategy came with the Russia-Ukraine war in 2022. As European competitors scrambled to replace Russian gas, as energy security suddenly trumped energy transition in political discourse, ExxonMobil found itself perfectly positioned. It had the production capacity to help fill the gap. It had the LNG infrastructure to deliver gas to Europe. And crucially, it had maintained the engineering capability to execute complex projects while others had downsized.

The company's response to the crisis was telling. While publicly supporting the energy transition, ExxonMobil quietly accelerated its traditional energy projects. By 2027 we'll hit production capacity of 1.3 million barrels per day, or close to 500 million barrels per year. That daily figure should climb to 1.7 million barrels by 2030. in Guyana alone. The Permian Basin was being developed at record pace. New LNG projects were being sanctioned.

The climate activists were furious. Three years after Engine No. 1's "victory," ExxonMobil was producing more oil than ever. The company had assumed the role of public tormentor to the ESG movement, even filing lawsuits against shareholders who pushed climate resolutions. But Woods had read the market correctly: the world wanted to transition to clean energy, but it needed oil and gas to function during that transition. And ExxonMobil would provide both.

VIII. The Pioneer Acquisition: Doubling Down on Oil (2023–2024)

The conference room on the 20th floor of ExxonMobil's Houston campus was silent except for the hum of air conditioning. It was September 2023, and Darren Woods was presenting to his board what would become the company's largest acquisition since the Mobil merger: a $59.5 billion all-stock purchase of Pioneer Natural Resources. The timing seemed almost deliberately provocative—just two years after the Engine No. 1 proxy fight, ExxonMobil was about to double its bet on fossil fuels.

The opportunity had emerged from an unlikely source: Scott Sheffield, Pioneer's legendary founder who had built the company into the Permian Basin's largest pure-play producer. At 71, Sheffield was ready to exit, but only to the right buyer. He'd rebuffed previous overtures, but Woods offered something unique: the chance to cement Pioneer's legacy within the world's most capable oil company while accelerating the Permian's development with unprecedented capital and technology.

The strategic rationale was compelling. Pioneer controlled 850,000 net acres in the Midland Basin, the sweet spot of the Permian. Its breakeven costs were below $35 per barrel. Most importantly, Pioneer had spent decades acquiring the choicest acreage through hundreds of small deals, creating a contiguous position that would take competitors decades to replicate—if they could at all.

Woods knew the optics were challenging. Here was ExxonMobil, supposedly pivoting toward low carbon solutions, making the largest oil acquisition in two decades. But the math was irrefutable. At $253 per share, ExxonMobil was paying roughly $71,000 per flowing barrel—expensive by historical standards but cheap considering Pioneer's 16 billion barrels of resource and decades of remaining inventory.

The integration plan was vintage ExxonMobil. Pioneer's 2050 net-zero target would be accelerated to 2035. Its scattered operations would be consolidated into ExxonMobil's manufacturing-style development approach. Most radically, ExxonMobil would deploy its proprietary drilling and completion techniques to Pioneer's acreage, potentially increasing recovery rates by 10-15%.The regulatory review stretched through spring 2024, with the Federal Trade Commission extracting an unusual concession: Scott Sheffield would be banned from joining ExxonMobil's board, addressing concerns about potential coordination with OPEC. On May 3, 2024, ExxonMobil announced it had closed the acquisition, creating a Permian powerhouse with more than 1.4 million net acres in the Delaware and Midland basins containing an estimated 16 billion barrels of oil equivalent resource.

The immediate impact was transformative. ExxonMobil's Permian production would more than double to 1.3 million barrels per day based on 2023 volumes, with projections to reach approximately 2 million barrels per day by 2027. This wasn't just about scale—it was about reshaping the economics of American oil production. The combined entity could drill longer laterals, share infrastructure, and apply ExxonMobil's cube development approach across Pioneer's premium acreage.

But the masterstroke was environmental positioning. ExxonMobil accelerated Pioneer's 2050 net-zero target to 2035, leveraging its industry-leading plans to achieve net-zero Scope 1 and 2 emissions from Permian operations by 2030. The company committed to increasing recycled water use in fracturing operations to more than 90% by 2030. Critics called it greenwashing; Woods called it pragmatic capitalism.

The deal's ripple effects were immediate. Chevron announced its $53 billion acquisition of Hess. Occidental bid for CrownRock. ConocoPhillips pursued Marathon Oil. The Permian Basin, already America's most important oil field, was consolidating into the hands of a few super-majors with the capital and technology to maximize its potential. For ExxonMobil, the Pioneer acquisition wasn't just about growth—it was about survival through dominance, ensuring that when the dust settled, it would be among the last companies standing in American oil.

IX. Business Model & Competitive Moat Analysis

ExxonMobil operates through three interconnected divisions that function like a carefully calibrated machine. The Upstream segment explores for and produces oil and gas, generating the raw materials. Product Solutions refines crude into fuels and manufactures chemicals, capturing margin at every transformation. Low Carbon Solutions, the newest division, develops technologies for carbon capture, hydrogen, and biofuels—essentially monetizing the externalities of the first two divisions.

This three-pillar structure isn't just organizational—it's a competitive fortress. When oil prices spike, Upstream prints money. When they crash, the refining business benefits from cheaper feedstock while chemical margins expand. When carbon prices eventually arrive, Low Carbon Solutions will capture that value too. It's a hedge against every scenario, engineered by people who think in decades, not quarters.

The numbers reveal the model's power. In 2023, Upstream generated $26.8 billion in earnings. Product Solutions added $11.5 billion. Even during the COVID crash of 2020, when oil prices went negative, ExxonMobil's integrated structure limited losses to $22 billion while pure-play producers faced existential crises. The company has generated positive free cash flow in 28 of the last 30 years—the exceptions being 2020's pandemic and 2016's oil price collapse.

But the real moat isn't integration—it's engineering excellence applied at massive scale. ExxonMobil operates the world's largest refinery at Baytown, Texas, processing 630,000 barrels daily. Its Singapore complex is the most sophisticated in Asia. The company holds over 10,000 active patents, from extended-reach drilling that can access reserves 40,000 feet from the drill site to proprietary catalysts that increase refinery yields by 15%.

Consider the Guyana operations. While competitors drilled dry holes, ExxonMobil's proprietary seismic imaging identified oil-bearing sandstone channels invisible to conventional technology. Its floating production vessels, each costing $2 billion, incorporate lessons from 50 years of offshore development. The result: finding costs below $1 per barrel when the industry average exceeds $10.

The technology advantage extends underground. In the Permian, ExxonMobil's cube development approach—drilling multiple horizontal wells simultaneously from a single pad—reduces surface footprint by 75% while increasing recovery rates by 30%. Its proprietary fracturing fluids, developed through decades of R&D, can be tailored to specific rock formations, maximizing production while minimizing water use. The financial fortress is formidable. In 2024, ExxonMobil reported earnings of $33.7 billion with cash flow from operations reaching some of its highest levels in a decade. Revenue reached $349.6 billion, up 3.3% from 2023. The company maintains the industry's strongest balance sheet with less than 15% debt-to-capital ratio, enabling countercyclical investment when competitors retreat.

But perhaps the most underappreciated moat is institutional knowledge. ExxonMobil employs 62,000 people, over half of them engineers and scientists. The company operates its own research facility in Clinton, New Jersey, with 600 PhDs working on everything from quantum chemistry to advanced materials. This isn't Silicon Valley innovation theater—it's methodical, decades-long research that produces actual products and processes.

The talent pipeline starts early. ExxonMobil recruits from the top 20 engineering schools globally, offering starting salaries that match tech companies but with defined benefit pensions—almost extinct elsewhere. The company's rotation program moves high-potential employees through multiple divisions and geographies, creating executives who understand every aspect of the business. When Darren Woods became CEO, he'd worked in refining, chemicals, and corporate planning—a 25-year apprenticeship in complexity.

This human capital translates into operational excellence that competitors can't replicate. ExxonMobil's refineries run at 95% utilization rates when the industry average is 85%. Its wells produce for decades longer than predicted through advanced reservoir management. Its chemical plants achieve yields that violate competitors' assumptions about theoretical limits.

The final element of the moat is optionality. With operations in 50 countries, technology leadership across the energy spectrum, and the financial strength to invest countercyclically, ExxonMobil can pivot faster than any competitor. If oil demand surprises to the upside, it has the reserves. If carbon prices materialize, it has the capture technology. If hydrogen becomes viable, it has the production capacity. This isn't hedging—it's systematic preparation for multiple futures, funded by the extraordinary cash flows of the present.

X. The Energy Transition Dilemma

The boardroom at ExxonMobil's Spring campus features a wall-sized display showing global energy flows in real-time. Natural gas flowing through pipelines. Oil tankers crossing oceans. Refineries processing crude into products. It's a reminder that while the world talks about energy transition, 80% of global energy still comes from fossil fuels—the same percentage as 30 years ago. The transition isn't replacing fossil fuels; it's adding alternatives while demand for everything grows.

This is the paradox ExxonMobil navigates. The International Energy Agency projects oil demand will peak around 2030 under current policies. But "peak" doesn't mean "disappear." Even in the IEA's most aggressive net-zero scenario, the world still needs 24 million barrels per day in 2050—about a quarter of current production. Someone has to produce that oil. ExxonMobil is betting it will be the lowest-cost, lowest-carbon producers who survive.

The company's Low Carbon Solutions business represents its hedge against transition risk, but it's a hedge that makes money. Carbon capture and storage, ExxonMobil's primary focus, leverages the same subsurface expertise used in oil production. The company already operates the world's largest CO2 pipeline network, transporting 20% of all captured carbon globally. It's targeting 100 million tonnes of CO2 storage capacity by 2030—equivalent to taking 20 million cars off the road.

The Houston Ship Channel CCS project exemplifies the strategy. ExxonMobil is developing infrastructure to capture emissions from its own refineries and petrochemical plants, plus those of competitors willing to pay for the service. With the Inflation Reduction Act's $85 per tonne tax credit, carbon capture becomes a profit center, not a cost center. The company estimates the global CCS market could reach $4 trillion by 2050.

Hydrogen represents another massive opportunity. ExxonMobil's Baytown facility will produce one billion cubic feet per day of blue hydrogen—made from natural gas with carbon captured. This isn't speculative technology; it's industrial chemistry the company has practiced for decades, now repurposed for a decarbonizing world. The hydrogen will initially fuel ExxonMobil's own operations, reducing emissions while maintaining competitiveness.

But the most controversial aspect of ExxonMobil's transition strategy is what it won't do: pivot to wind and solar. While BP and Shell have invested billions in renewable power with returns below their cost of capital, ExxonMobil has stayed disciplined. Woods argues that manufacturing solar panels or operating wind farms doesn't leverage any of ExxonMobil's competitive advantages. It's commodity power generation where Chinese manufacturers dominate and returns barely exceed utilities. The company's investment strategy reflects this measured approach. Over the next six years, ExxonMobil plans to invest more than $15 billion on initiatives to lower greenhouse gas emissions. From 2025-2030, the company is pursuing up to $30 billion in lower emissions investment opportunities, but only those meeting its return thresholds. The Baytown hydrogen facility exemplifies this discipline: expected to be the world's largest upon startup, capable of producing up to 1 billion cubic feet daily of low-carbon hydrogen with approximately 98% of CO2 removed. A final investment decision is expected in 2025 with anticipated startup in 2029.

The most intriguing development is ExxonMobil's pivot toward data centers. The oil giant is developing a groundbreaking plan to provide low-carbon power to the U.S. data centers which are vital hubs for the booming artificial intelligence (AI) sector. AI growth could account for 20% of the CCS market by 2050. This isn't environmental virtue signaling—it's recognizing that tech companies need reliable, clean power at scale, something renewable intermittency can't provide but gas with carbon capture can.

Critics argue ExxonMobil is using Low Carbon Solutions to greenwash continued fossil fuel production. The numbers suggest otherwise. The company has already secured 5.5 million tonnes per annum of carbon capture commitments from industrial customers. Its LaBarge facility in Wyoming has captured more CO2 than any facility globally. These are real projects with real revenues, not theoretical offsets.

The ultimate test will be economic. If carbon prices reach $100 per tonne—the level many economists consider necessary for net-zero—ExxonMobil's carbon capture infrastructure becomes extraordinarily valuable. If they don't, the company still has the world's lowest-cost oil production. It's heads they win, tails they don't lose—exactly the kind of asymmetric bet that's defined ExxonMobil for 150 years.

XI. Power Dynamics & Stakeholder Analysis

The conference room on the 52nd floor of BlackRock's Manhattan headquarters could fit ExxonMobil's entire board. It was here, in early 2021, that the world's largest asset manager—controlling $10 trillion and 6.61% of ExxonMobil's shares—decided to back Engine No. 1's proxy fight. That decision, more than any climate report or government regulation, forced ExxonMobil's transformation. Understanding who holds power over this $500 billion corporation is essential to predicting its future.

The institutional ownership tells the story: Vanguard leads with 8.15%, BlackRock holds 6.61%, State Street controls 4.83%. Together, these three index fund giants control nearly 20% of ExxonMobil—more than the Rockefeller family ever did. But unlike activist investors, they can't easily sell. Their passive funds must hold ExxonMobil as long as it's in the S&P 500. This creates a paradox: enormous voting power with limited exit options.

The government relationship is equally complex. ExxonMobil operates under thousands of regulations across 50 countries, yet maintains remarkable influence. Rex Tillerson's elevation to Secretary of State wasn't an anomaly—it reflected decades of quasi-diplomatic engagement. The company often knows more about certain countries' oil reserves than their own governments do. This information asymmetry translates into negotiating leverage that transcends normal corporate-government dynamics.

OPEC represents both competitor and inadvertent ally. When Saudi Aramco restricts production, ExxonMobil's assets become more valuable. When OPEC floods the market, ExxonMobil's low-cost production and downstream integration provide resilience that pure explorers lack. The relationship is symbiotic antagonism—they need each other as enemies to justify their existence and strategies.

The talent dimension is increasingly critical. ExxonMobil competes with Google and Tesla for the same Stanford chemical engineers. The company's pitch has evolved: instead of just extraction expertise, it offers the chance to solve humanity's greatest challenge—providing energy while reducing emissions. The signing bonuses now match Silicon Valley, but the real attraction is scale. An engineer at ExxonMobil might design a process that captures millions of tonnes of CO2. At a startup, they might never see commercial deployment.

Community relations vary dramatically by geography. In Guyana, ExxonMobil is transforming a nation—oil revenues will exceed Guyana's entire GDP within years. The company builds schools, funds hospitals, and trains locals for high-skilled jobs. In California, it faces constant litigation and regulatory hostility, ultimately divesting assets rather than fighting indefinitely. This geographic arbitrage—investing where welcomed, withdrawing where obstructed—shapes capital allocation more than any spreadsheet model.

Supply chain power runs both directions. ExxonMobil purchases $100 billion annually in goods and services, making suppliers dependent on its business. But specialized providers—like Schlumberger for oilfield services or Honeywell for refinery controls—possess expertise ExxonMobil can't easily replicate. The company manages this tension through long-term contracts and joint technology development, creating switching costs for both parties.

The most underappreciated stakeholder might be the U.S. military. ExxonMobil is one of the largest suppliers of jet fuel to the Defense Department. Its refineries are considered critical infrastructure. During crises, the company operates as a quasi-state entity, ensuring energy security takes precedence over profit maximization. This implicit contract—profit in peacetime, service in crisis—underpins political support that transcends party lines.

Environmental activists have evolved from protesters to shareholders, from outsiders to board members. Engine No. 1's victory demonstrated that climate concerns, framed in financial terms, could reshape corporate strategy. But the relationship remains adversarial. ExxonMobil now files lawsuits against shareholder activists it deems unreasonable, drawing boundaries around acceptable engagement.

The investment community splits into three camps. Traditional energy investors want maximum cash returns while oil prices remain high. ESG-focused funds demand aggressive transition strategies regardless of returns. Index funds want both—competitive returns and reduced climate risk. ExxonMobil's strategy of disciplined capital allocation satisfies the first group while its Low Carbon Solutions investments appease the second, leaving index funds as the swing vote on major decisions.

XII. Bear vs. Bull Case

Bear Case: The Inexorable Decline

The bear case against ExxonMobil isn't about next quarter or next year—it's about the next decade. Start with the demand curve. Electric vehicle adoption is accelerating exponentially. Norway is already 80% electric for new car sales. China, the world's largest auto market, is approaching 40%. Once EVs reach cost parity with internal combustion—expected by 2027—adoption becomes unstoppable. That's 70 million barrels per day of oil demand that begins evaporating.

The stranded asset risk is massive. ExxonMobil has 18 billion barrels of proved reserves on its books. At $50 per barrel, that's $900 billion in theoretical value. But if demand peaks and declines, those reserves become worthless. The company would face write-downs that dwarf the 2020 losses. The Permian Basin assets, bought at premium prices, would become the oil industry's equivalent of coal mines—technically operational but economically obsolete.

Climate litigation represents an existential threat. The tobacco analogy is imperfect but instructive. ExxonMobil's own documents show it understood climate risks decades ago. As damages mount—coastal flooding, extreme weather, agricultural collapse—courts will seek deep pockets. ExxonMobil has the deepest pockets in fossil fuels. A single adverse judgment could trigger cascading lawsuits that bankrupt the company.

The talent exodus is already beginning. Top engineering graduates increasingly refuse oil company offers on principle. Universities are divesting endowments and cutting research partnerships. Without fresh talent, ExxonMobil becomes a declining enterprise managed by a aging workforce, unable to innovate its way out of obsolescence.

Carbon pricing changes everything. At $200 per tonne—the level needed for Paris Agreement compliance—gasoline costs increase by $2 per gallon. Petrochemicals become uncompetitive with bio-based alternatives. Even with carbon capture, ExxonMobil's products become luxury goods in a world that can't afford them.

The capital markets are closing. Banks are restricting fossil fuel lending. Insurance companies are refusing coverage. Bond spreads are widening. The cost of capital for oil projects now exceeds returns in many scenarios. This financial suffocation forces asset sales at distressed prices, beginning a death spiral of divestment and decline.

Bull Case: The Last Giant Standing

The bull case starts with reality: the energy transition will take generations, not years. Global energy demand grows 1-2% annually. Even if renewables grow at maximum feasible rates, fossil fuels remain essential through 2050. Someone must produce that oil and gas. ExxonMobil, with the lowest costs and highest efficiency, will be the last producer standing.

The Permian-Pioneer combination creates an unassailable position. Production costs below $35 per barrel generate profits even at recession prices. The 16 billion barrels of resource provide 30+ years of production at current rates. While competitors exhaust their reserves, ExxonMobil can sustain and grow production, capturing increasing market share as others exit.

Geopolitical chaos is bullish for ExxonMobil. Russia's weaponization of energy, Middle East instability, and China's resource nationalism make energy security paramount. Governments will prioritize domestic production over climate goals when faced with shortages. ExxonMobil's American reserves become strategic assets worth protecting and promoting.

The developing world changes everything. India adds a United States worth of energy demand by 2040. Africa's population doubles by 2050. These billions of people need affordable energy to escape poverty. They'll choose coal if oil and gas aren't available. ExxonMobil's relatively cleaner fossil fuels become the pragmatic climate solution.

Carbon capture transforms the business model. At scale, ExxonMobil becomes the world's largest waste management company, charging fees to store everyone's CO2. The infrastructure required—pipelines, injection wells, monitoring systems—takes decades to build. ExxonMobil's head start becomes an insurmountable moat. The company could generate $50 billion annually from carbon storage by 2040.

The cash generation is unprecedented. Free cash flow exceeds $30 billion annually at $70 oil. The dividend yields 3.5% and grows steadily. Share buybacks reduce the float by 5% annually. Patient investors could see 15% annual returns simply from capital allocation, regardless of commodity prices.

The technology pipeline changes the game. Direct air capture of CO2. Plastic-eating enzymes that enable infinite recycling. Synthetic fuels that work in existing engines. Fusion energy that needs helium-3 from natural gas processing. ExxonMobil's R&D budget exceeds most countries' entire energy research programs. One breakthrough could redefine the company's value.

The Verdict

Both cases contain truth. The energy transition is real and accelerating. But so is energy demand growth and the complexity of replacing fossil fuels. The outcome depends on variables nobody can predict: the pace of technological change, the severity of climate impacts, the stability of governments, the choices of billions of consumers.

What's certain is that ExxonMobil won't go quietly. The company has survived antitrust dismemberment, nationalization of its largest assets, and oil price collapses. It adapts, evolves, and endures. The bear case assumes linear extrapolation of current trends. The bull case recognizes that history is discontinuous, that black swans fly in both directions, and that companies with ExxonMobil's resources and capabilities can shape their own futures.

XIII. Lessons & Playbook Takeaways

After 150 years, multiple existential crises, and radical transformations, ExxonMobil's survival offers lessons that transcend industry. These aren't management consultant platitudes but hard-won insights from operating at the edge of capitalism's possibilities.

Lesson 1: Capital Allocation Discipline Beats Strategic Brilliance

ExxonMobil has made spectacular strategic errors—missing shale, overpaying for XTO, clinging to climate denial. Yet it consistently generates superior returns. The secret: ruthless capital allocation discipline. Every project must clear a 10% real return hurdle. No exceptions for strategic importance or market momentum. This discipline means leaving money on the table during booms but surviving busts that bankrupt competitors.

The application: Build systems that prevent emotion-driven investment. Use consistent metrics across all decisions. Accept looking stupid in the short term for long-term survival. Most importantly, never confuse activity with progress. ExxonMobil's greatest value creation often comes from what it doesn't do.

Lesson 2: Vertical Integration Is Expensive Insurance Worth Buying

Modern business theory advocates focus and specialization. ExxonMobil does the opposite, maintaining massive refineries, chemical plants, and retail networks alongside oil production. This integration is expensive and complex but provides resilience that pure-plays lack. When oil prices crash, refining margins expand. When refining struggles, chemicals compensate.

The broader principle: In volatile industries, diversification within the value chain beats diversification across industries. Own the entire system, not random pieces of different puzzles. Accept lower returns during stable periods in exchange for survival during chaos.

Lesson 3: Technology Leadership Requires Patient Capital

ExxonMobil spent decades developing extended-reach drilling before it generated returns. The company invested billions in carbon capture when carbon had no price. This patient technology development seems irrational in quarterly capitalism but creates competitive advantages that last generations.

The takeaway: Fundamental research requires thinking in decades, not years. Fund multiple pathways knowing most will fail. Protect R&D budgets especially during downturns when competitors cut. Most importantly, own the intellectual property—licensing technology is admitting defeat.

Lesson 4: Culture Eats Strategy But Process Eats Everything

ExxonMobil's culture is famously rigid—standardized processes, endless analysis, consensus decision-making. This seems antithetical to innovation, yet the company consistently out-executes competitors. The secret: process excellence enables cultural consistency across 62,000 employees in 50 countries.

The insight: Don't choose between culture and process—encode culture into process. Make values operational through systems. Accept that this creates bureaucracy but prevents catastrophic failure. In high-stakes industries, consistency beats creativity.

Lesson 5: Manage Stakeholders Through Strength, Not Appeasement

When climate activists demanded board seats, ExxonMobil initially resisted, lost, then adapted on its own terms. The company now sues shareholders who push too hard while investing in low-carbon solutions that make financial sense. This selective engagement—cooperate where aligned, fight where not—maintains strategic flexibility.

The principle: Stakeholder management isn't about making everyone happy. It's about maintaining freedom to operate. Draw clear boundaries. Communicate consistently. Never apologize for core business activities while adapting to legitimate concerns. Strength paradoxically creates more space for compromise than weakness.

Lesson 6: Time Arbitrage Is the Ultimate Competitive Advantage

ExxonMobil thinks in geological time while markets think in quarters. The company will spend 10 years developing a field that produces for 40 years. This temporal mismatch creates opportunities—assets become cheap when short-term focused investors flee.

The application: Extend time horizons beyond competitors' patience. Build infrastructure that takes decades to replicate. Accept short-term underperformance for long-term dominance. Most importantly, maintain balance sheet strength to survive long enough for time arbitrage to pay off.

Lesson 7: Scale Still Matters in Physical Industries

Despite software eating the world, physical industries remain governed by scale economics. ExxonMobil's massive refineries, billion-barrel fields, and global logistics networks create costs advantages no startup can match. Digital transformation enhances these advantages rather than replacing them.

The lesson: In capital-intensive industries, scale isn't just an advantage—it's survival. Consolidate during downturns. Build facilities at maximum efficient scale. Accept utilization volatility rather than subscale operations. The winner-take-all dynamics of software are mild compared to heavy industry.

XIV. Epilogue: The Next Chapter

John D. Rockefeller died in 1937, living just long enough to see automobiles transform from curiosities to necessities, validating his bet on oil despite losing his monopoly. Were he alive today, observing his corporate descendant navigate between fossil fuel dominance and energy transition, what would he think?

He'd likely recognize the patterns. The same disciplined accumulation of advantage. The same focus on efficiency and integration. The same ability to transform opposition into opportunity. But he'd also see something new: a company preparing for its own obsolescence while maximizing value from its current position. This isn't the monopolistic expansion of Standard Oil but the strategic flexibility of a corporation that knows nothing lasts forever.

Three scenarios define ExxonMobil's next twenty years:

Scenario 1: The Long Goodbye (40% probability) Oil demand peaks around 2035 but declines gradually. ExxonMobil becomes the industry's consolidator, acquiring distressed assets cheaply and operating them efficiently. The company slowly transforms into a carbon management enterprise, storing CO2 for fees that eventually exceed oil profits. By 2045, it's primarily an environmental services company that happens to produce some oil. The stock performs like a utility—steady dividends, limited growth, but remarkable resilience.

Scenario 2: The Green Phoenix (30% probability) Breakthrough carbon capture technology makes fossil fuels climate-neutral. ExxonMobil's early investments in CCS position it to dominate this new industry. Oil demand stabilizes at 80 million barrels per day, supplied by the few companies capable of producing carbon-neutral barrels. The company's valuation soars as it becomes both the largest oil producer and largest carbon manager. The stock triples as ESG funds return, now viewing ExxonMobil as a climate solution.

Scenario 3: The Forced Transition (30% probability) Climate disasters accelerate, triggering emergency government action. Carbon taxes reach $300 per tonne. Fossil fuel production is nationalized or banned. ExxonMobil pivots entirely to chemicals, hydrogen, and carbon capture, but at much lower margins. The company survives but shrinks dramatically, returning capital to shareholders through massive buybacks and special dividends. The stock initially crashes then stabilizes at a lower plateau.

The key metrics to watch: - Permian production rates: Efficiency gains versus depletion - Carbon capture commitments: Real contracts versus press releases - Capital allocation mix: Traditional versus low-carbon investment ratios - Talent flows: Engineering recruitment versus departures - Regulatory developments: Carbon pricing and production restrictions - Technology breakthroughs: Both enabling and threatening

The ultimate question isn't whether ExxonMobil can survive—history suggests it can survive almost anything. The question is what it becomes. Will it follow Kodak, clinging to a obsolete business model until bankruptcy? Or IBM, transforming completely while maintaining corporate continuity? Or something unprecedented—a fossil fuel company that engineers its own obsolescence while profiting from the transition?

The answer lies not in predicting the future but in recognizing that ExxonMobil, perhaps more than any corporation, has the resources, expertise, and institutional knowledge to shape that future. The company that lit the world with kerosene, powered it with gasoline, and built modern life from petrochemicals now faces its greatest test: proving that the same capabilities that created climate change can help solve it.

For investors, policymakers, and citizens, ExxonMobil represents a paradox that defines our era. We need its products but fear its power. We demand it change but require it to remain stable. We want it punished for the past but need its capabilities for the future. This tension—between what was, what is, and what must be—makes ExxonMobil not just a company but a mirror reflecting humanity's struggle with its own success.

The empire that oil built will outlive oil. What it becomes next will help determine whether humanity does too.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube