Essential Utilities: The Roll-Up Masters of America's Hidden Infrastructure

The Monsoon Moment for American Water

Picture the suburban sprawl of West Chester, Pennsylvania in the winter of 1998. Not exactly monsoon weather, but for Nicholas DeBenedictis—the environmental engineer turned CEO who had taken the helm of Philadelphia Suburban Water Company just five years earlier—it was a moment of profound clarity. The West Chester municipal water utility, with its aging pipes and constrained capital budget, had just agreed to sell its assets to his company for a sum that local politicians could use for other priorities. What DeBenedictis realized that day was something that would take the rest of America decades to understand: the hidden infrastructure beneath every street corner, every suburban lawn, and every school building was quietly falling apart. And someone with access to capital markets could acquire these systems, fix them, and create shareholder value in perpetuity.

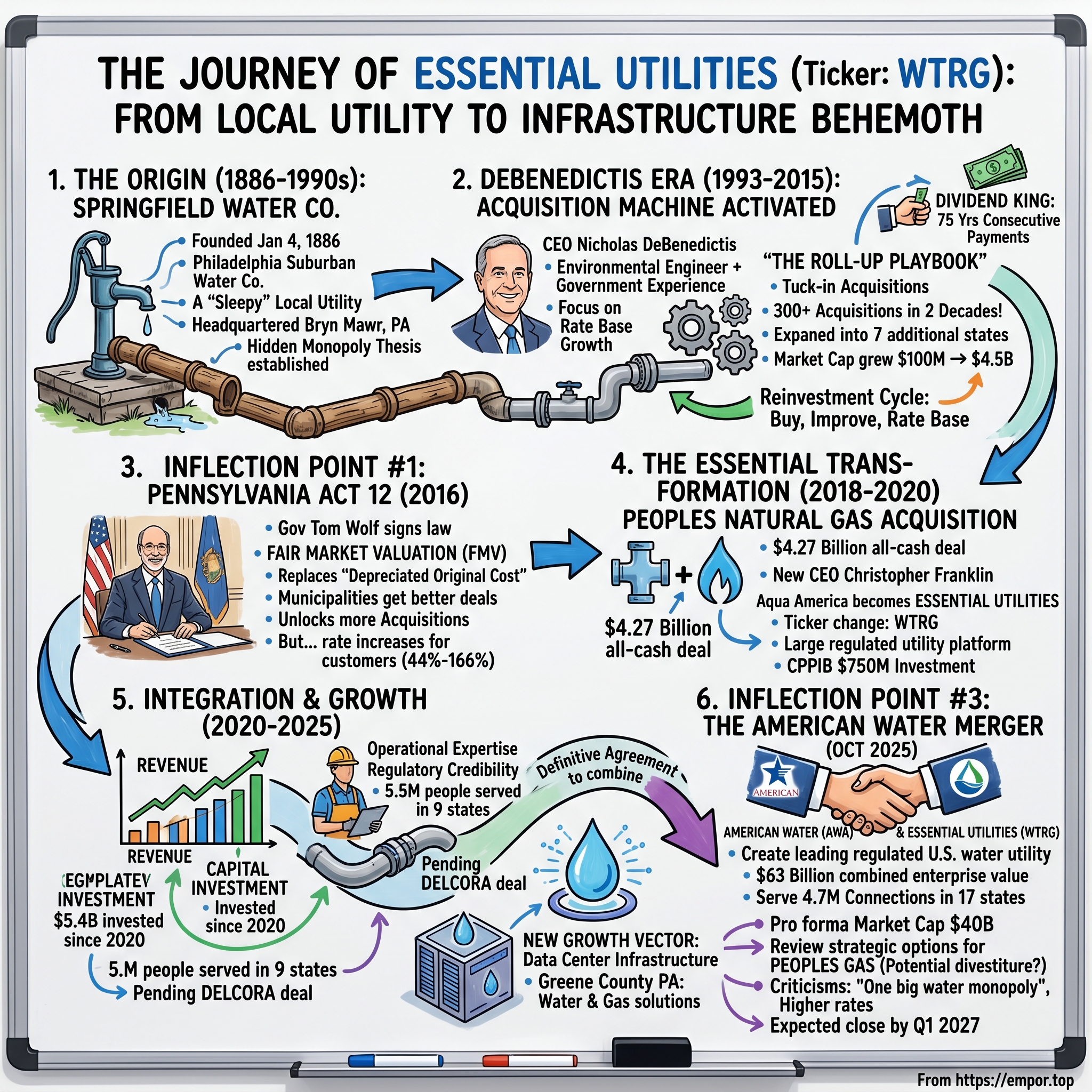

The company began January 4, 1886, by the founding of the Springfield Water Company. The name would change to Philadelphia Suburban Water Company, then to Aqua America, and eventually to Essential Utilities—but the thesis remained constant. Water infrastructure is the ultimate hidden monopoly. You cannot build competing pipes. Customers cannot switch providers. And most importantly for investors: people will always need water.

This is the story of how a small suburban Philadelphia water company became one of America's largest utility roll-ups, completing over 300 acquisitions in just two decades, expanding into natural gas, and now, in October 2025, agreeing to merge with its only major competitor to create a $63 billion infrastructure behemoth. It's also a story about the quiet crisis nobody talks about—the trillions of dollars of aging pipes beneath American streets—and what it tells us about the future of essential infrastructure investing.

This month Essential Utilities commemorates its fifth anniversary as a unified company, reinforcing its position as one of the largest regulated utilities. Since the integration of Aqua and Peoples in 2020, Essential has demonstrated the power of bringing together operational expertise, financial strength, and regulatory credibility to enhance infrastructure, improve environmental sustainability, and provide long-term value to customers and investors. But the journey from a sleepy local water company to a major force in American infrastructure didn't happen overnight—and understanding that journey is essential for any investor contemplating this sector.

From Springfield to Bryn Mawr: The Origin Myth

When the Springfield Water Company incorporated on January 4, 1886, Grover Cleveland was president, the Statue of Liberty had just been dedicated, and America was in the midst of its greatest infrastructure boom. Cities and towns across the nation were racing to build water systems, sewers, and the basic plumbing that would transform American life. The timing was not accidental.

The company began in Pennsylvania and remains headquartered in Bryn Mawr. The company changed its name to the Philadelphia Suburban Water Company (PSW). For nearly a century, it operated as exactly what its name suggested: a modest utility serving the growing suburbs around Philadelphia. The economics were simple and beautiful—regulated returns on capital invested in pipes, pumps, and treatment plants, with rates set by state utility commissions that ensured a "fair" return to shareholders.

But something strange happened to the American water industry in the 20th century. Unlike electricity or telecommunications, water never consolidated. The fragmentation was—and remains—astonishing. The U.S. water and wastewater landscape is heavily fragmented across 48,587 community water systems serving 313 million people and 23,481 wastewater treatment facilities serving an estimated 267 million people. To put this in perspective: America has more water utilities than McDonald's restaurants.

The reason for this fragmentation is both political and practical. Water is fundamentally local—drawn from local aquifers, rivers, and reservoirs. Municipal ownership created jobs and gave local politicians control over a visible public service. Small systems serving fewer than 3,300 people make up 78% of these assets, many of which are undercapitalized and incapable of keeping pace with the rising costs of compliance.

For decades, this fragmented structure worked well enough. But by the 1990s, cracks—quite literally—were beginning to show.

The Hidden Infrastructure Crisis Nobody Discusses

Most Americans don't think about water infrastructure until their tap runs brown or their street floods with sewage. But beneath every American city lies a ticking time bomb of aging pipes, many installed during the Eisenhower administration or earlier.

A significant proportion of the nation's water pipes were installed during the early- to mid-20th century. Cast iron pipes, prevalent in older systems, have an average lifespan of 75-100 years, meaning many have already reached or exceeded their operational limits.

The numbers are sobering. There are 240,000 water main breaks per year and one every two minutes in the United States because of aging pipes. With over 240,000 water main breaks occurring annually, the nation loses an estimated 6 billion gallons of treated water daily. That's water that's been pumped, treated, and disinfected—only to leak into the ground before reaching anyone's tap.

The American Society of Civil Engineers (ASCE) grades America's drinking water infrastructure at a concerning "C-" in its latest Infrastructure Report Card. Additionally, the report graded the nation's aging and underfunded drinking water infrastructure as a "C-" and wastewater infrastructure as a "D+," urging continuous investment to address contaminants and meet evolving regulations as systems age.

The funding gap is staggering. The U.S. water and wastewater infrastructure is deteriorating, with water main breaks occurring every few minutes, according to the American Society of Civil Engineers (ASCE). The Environmental Protection Agency estimates that $1.25 trillion in investments will be needed over the next 20 years to maintain and upgrade drinking water systems.

Here's the key insight for investors: municipalities—especially small ones—simply cannot fund these repairs. They lack the expertise, the capital, and often the political will to raise rates to levels that would cover true replacement costs. Additionally, cash-strapped municipalities see benefit to selling their water supply assets.

This is the structural opportunity that Nicholas DeBenedictis recognized in the 1990s—and that continues to drive the industry today.

The DeBenedictis Era: Building the Acquisition Machine (1993-2015)

When Nicholas DeBenedictis took over as CEO in 1993, Philadelphia Suburban Water Company was a $100 million market cap utility serving suburban Philadelphia. By the time he stepped down in 2015, it had become Aqua America—the company expanded out of Pennsylvania into seven additional states serving 3 million people. The company's market capitalization grew from $100 million to $4.5 billion during that time.

DeBenedictis was an unlikely water baron. DeBenedictis received a Bachelor's degree in business administration from Drexel University in 1968, and a Master's degree in environmental engineering and science from Drexel in 1969. He served in the Army Corps of Engineers between 1970 and 1973 reaching the rank of Captain.

His career path was equally unconventional. In 1983, he was named secretary of the Department of Environmental Resources, where he worked on issues like acid mine drainage, trash-to-steam operations, the mine fire in Centralia, and water quality initiatives. In 1989, PECO hired him to be senior vice president of corporate and public affairs during the permitting process of the Limerick nuclear plant.

This combination of environmental engineering expertise, government experience, and corporate savvy proved perfect for the water business. In 1993, DeBenedictis was selected through a nationwide search to take the helm of Philadelphia Suburban Corp. – the private water utility that would become Aqua America and, more recently, Essential Utilities.

DeBenedictis understood something crucial: in a regulated utility, the key to growth isn't cutting costs (though that helps). The key is deploying capital into the rate base—the total invested capital on which regulators allow a "fair return." Buy a water system, invest in improvements, get those improvements into the rate base, and you've created permanent shareholder value.

The Acquisition Playbook

From 1993 to 2013 Aqua America completed 300 acquisitions. That's roughly 15 acquisitions per year, or more than one per month, sustained for two decades.

The acquisitions followed a clear pattern. In recent years, the company has purchased smaller private utilities across 12 states, gradually extending southward. The strategy was what industry insiders call "tuck-in" acquisitions—buying small systems adjacent to existing operations, then integrating them to capture operating efficiencies.

In January 1998 Aqua America, then known as the Philadelphia Suburban Water Company (PSW) purchased the West Chester, PA municipal water utility assets. Acquisitions of large private companies included the purchases of AquaSource in 2003, Heater and Florida Water Services in 2004, and the New York Water Service Corporation in 2007.

The AquaSource deal was particularly strategic—it brought systems in multiple states, accelerating geographic expansion. Aqua America's subsidiary, Aqua New York, Inc., acquired New York Water Service Corporation from Utilities & Industries Corp., LLC in a transaction valued at approximately $51 million. The transaction included a cash payment of $27.4 million, subject to certain post-closing adjustments, and the assumption of $23.5 million of debt.

The company's largest water subsidiary is Aqua Pennsylvania, which has been a part of Aqua America since 1996 and accounts for slightly more than half of 2007 operating revenue and provides water services to 50% of the company's total customer base. This Pennsylvania concentration wasn't accidental—it was the result of deep regulatory relationships and operational density.

The Dividend Record

While growing through acquisitions, DeBenedictis never forgot income investors. Aqua America has paid consecutive quarterly cash dividends for 75 years and has increased the dividend 29 times in the last 28 years. This record—now extended to 80 consecutive years—makes Essential one of the longest-tenured dividend payers in American corporate history.

The dividend strategy served multiple purposes. It attracted institutional investors seeking stable income. It provided discipline—you can't pay dividends you don't earn. And it signaled confidence in the durability of the business model.

"He's the Joe DiMaggio of utility executives," Former Pennsylvania Public Utility Commission Chairman Wendell F. Holland said, having achieved 15 straight years of record earnings at Aqua America and amassed a $4.7 billion corporate valuation.

KEY INFLECTION POINT #1: Pennsylvania Act 12 (2016)

If the DeBenedictis era was about proving the roll-up model worked, the next phase was about regulatory arbitrage—and no piece of legislation mattered more than Pennsylvania Act 12 of 2016.

To understand why this law changed everything, you need to understand how utility acquisitions traditionally worked. When a private utility bought a municipal system, regulators historically valued the acquired assets at "depreciated original cost"—essentially, what the municipality paid to build the system minus accumulated depreciation. This created a problem: municipalities had often underinvested for decades, so the book value was low, but the replacement cost (and fair market value) was much higher.

On April 14, 2016, Governor Tom Wolf signed Act 12 of 2016 amending Chapter 13 of the Pennsylvania Public Utility Code. Section 1329 of the Code enables a public utility or entity (buyer) to utilize fair market valuation when acquiring water and wastewater systems located in the Commonwealth that are owned by a municipal corporation or authority.

Section 1329 established a procedure for an acquiring public utility to use fair market valuation, instead of depreciated original cost, when the acquiring utility purchases a water and wastewater system.

How Fair Market Value Works

Utility valuation experts will appraise the system to establish its "fair market value" (FMV). FMV is the average of two utility valuation expert appraisals.

The mechanics matter: both buyer and seller hire licensed engineers to assess the tangible assets. Each party then engages separate utility valuation experts who provide independent appraisals. The average becomes the "fair market value" for regulatory purposes.

This sounds technical, but the implications were profound. The law allows municipal water and sewer utilities to negotiate with for-profit utilities for the fair market value rather than the actual value of the system. The higher purchase prices, in turn, give new owners a basis to seek approval to charge higher rates.

From the municipality's perspective, they could suddenly get market prices for systems they'd undervalued on their books for decades. From Aqua's perspective, they could now offer prices that made deals attractive to politicians—and then recover those costs through future rate increases.

The Results—and the Controversy

In the first seven years after Pennsylvania passed Act 12 legislation that allows Aqua Pennsylvania and Pennsylvania American Water free reign to acquire municipal water and sewer systems. They have made 17 acquisitions costing over $850 million.

The pace of acquisitions accelerated dramatically. But so did controversy. The result, state Consumer Advocate Patrick Cicero said, is that customers of public water and sewer utilities acquired by for-profit companies since the law took effect pay about $85 million more annually for service.

Pennsylvania customers of former municipal water and sewer utilities sold since 2016 have seen bills increase by 44% to 166%.

The industry defended these increases. "Municipal officials in Illinois, like their peers throughout the country, understand the important benefits of regionalizing water and wastewater systems. They also understand that the proceeds, from the sale of a water system, could allow them to pursue meaningful and needed local projects and initiatives," said Aqua America Chairman and CEO Christopher Franklin.

The debate crystallizes a fundamental question: are rate increases the price of fixing decades of deferred maintenance? Or are they simply wealth transfer from ratepayers to shareholders?

The Model Spreads

Pennsylvania wasn't alone. Illinois was one of the first states to adopt fair market value legislation, when in 2013, the Illinois Water System Viability Act allowed municipalities to receive "fair market value" for their water systems. Illinois, Ohio, Pennsylvania, and Indiana have all adopted forms of fair market value legislation that rewrite the rules for how water systems are appraised and acquired.

For Essential, fair market value legislation created a virtuous cycle: higher acquisition prices meant more goodwill on the balance sheet, but regulators allowed recovery through rates. The company could outbid smaller competitors while still generating acceptable returns.

KEY INFLECTION POINT #2: The Peoples Natural Gas Acquisition (2018-2020)

By 2018, Christopher Franklin had been CEO for three years. A fixture of the Essential leadership team, Christopher Franklin is chairman and Chief Executive Officer. He has served as CEO since July 2015, and as chairman since December 2017.

Franklin, a 22-year veteran of Aqua, has held positions of increased responsibility in various areas of the company throughout his tenure, most recently as president and chief operating officer, regulated operations. Franklin earned his B.S. from West Chester University and his M.B.A. from Villanova University.

Under Franklin, the company had continued its acquisition pace. But he had a bigger vision: diversification beyond water into another essential infrastructure business with similar economics—natural gas distribution.

In October 2018 Aqua announced that it was going to purchase Peoples Natural Gas in Pittsburgh PA for $4.27 billion. This deal entered Aqua into the competitive Pittsburgh water market while taking their first step into gas utilities.

The Deal Structure

Essential Utilities Inc. announced it has successfully completed the acquisition of Peoples, a Pittsburgh-based natural gas distribution company, in an all-cash transaction that reflects an enterprise value of $4.275 billion, including the assumption of approximately $1.1 billion of debt.

The Pennsylvania Public Utility Commission, in a 4-1 vote, endorsed Aqua's acquisition of Peoples Natural Gas, owned by SteelRiver Infrastructure Partners, a California private equity company.

Peoples Gas has 662,000 customers in Pittsburgh and Western Pennsylvania. It also operates smaller systems in West Virginia and Kentucky.

The Strategic Logic

The rationale was compelling on paper. Both water and natural gas are distributed through underground pipes. Both require the same core competencies: regulatory management, capital investment, pipe maintenance, and customer service. Both are essential services with inelastic demand.

The combined enterprise will be among the largest publicly traded water utilities and natural gas local distribution companies in the U.S., uniquely positioned to meaningfully contribute to the nation's natural gas and water infrastructure reliability. The transaction will bring together two companies that each have more than 130 years of service and proven track records of operational efficiency, complementary service territories and strong regulatory compliance.

Total rate base is expected to exceed $7.2 billion, with approximately 70 percent in water and wastewater and 30 percent in natural gas.

The Skeptics

Not everyone was convinced. The critics objected that Aqua, though it operates water utilities in eight states, has no experience operating a gas utility.

The financial engineering also raised eyebrows. Aqua was paying $4.3 billion for a company with a book value far below that price. The difference would be carried as "goodwill" on Essential's balance sheet—a bet that future rate cases would justify the premium.

The Transformation

Essential, which changed its name from Aqua America on Feb. 3, began trading under the NYSE ticker symbol (WTRG) the same day. The acquisition received regulatory approval from the Pennsylvania Public Utility Commission on Jan. 16 and marks the creation of a new infrastructure company uniquely positioned to have a significant impact on improving infrastructure reliability.

The name change was symbolic. "Aqua" signaled a water company. "Essential" signaled something broader—an infrastructure company focused on essential services.

The combined company plans to replace nearly 3,000 miles of aged natural gas mains over approximately 15 years.

In connection with the completion of Essential's acquisition of Peoples, Essential also closed the previously announced $750 million investment from the Canada Pension Plan Investment Board (CPP Investments). Having one of Canada's largest pension funds as a cornerstone investor provided validation of the strategy.

The Essential Era: Integration and Growth (2020-2025)

The Peoples acquisition closed in March 2020—just as COVID-19 was beginning to reshape American life. For an essential services company, the timing proved fortuitous. While many businesses shuttered, Essential's customers continued to flush toilets, take showers, and heat their homes.

Since the integration of Aqua and Peoples in 2020, Essential has demonstrated the power of bringing together operational expertise, financial strength, and regulatory credibility. Both Aqua and Peoples bring a rich history of nearly 140 years of delivering essential water and natural gas service.

The Numbers Tell the Story

Since 2020, Essential has invested more than $5.4 billion toward critical infrastructure projects.

Operating as the Aqua and Peoples brands, Essential serves approximately 5.5 million people across nine states.

Essential reported operating revenues of $477.0 million for Q3 2025, a 9.6% increase from $435.3 million in the same period last year. Net income rose 32.7% to $92.1 million, compared to $69.4 million in Q3 2024.

The Acquisition Engine Continues

Since 2015, the company has added over 135,000 customers through acquisitions, representing approximately $550 million in rate base. In 2025 alone, Essential closed three acquisitions: Beaver Falls (wastewater, 7,000 customers), Greenville (wastewater, 2,300 customers), and Midvale (water, 900 customers).

The company has several pending transactions, including the significant DELCORA acquisition (wastewater, 198,000 customers, $276.5 million purchase price).

New Growth Vectors: Data Centers

Perhaps most intriguing is Essential's pivot into data center infrastructure. Essential Utilities today announced an agreement with International Electric Power III, LLC (IEP), to become an investor in a 1,400 acre, data center facility in Greene County, Pennsylvania. Based on the agreement, Essential Utilities, through its subsidiary Aqua, plans to design, build, and operate an 18 million gallons per day (MGD) water treatment plant to service the power plant and data center.

Using raw water from the adjacent Monongahela River, the water plant will support both power generation and data center cooling needs. In addition, Essential's subsidiary Peoples, the largest natural gas utility in Pennsylvania, will provide gas consulting services and energy management services to the project.

Essential previously informed investors that the company was in active discussions with data center developers representing over 5 gigawatts of power demand.

This represents a fascinating new application of Essential's core competencies. Data centers consume enormous amounts of water for cooling and natural gas for power generation. Essential can provide both—and potentially earn returns well beyond traditional regulated utility rates.

KEY INFLECTION POINT #3: The American Water Merger (October 2025)

And then came the bombshell.

American Water Works Company, Inc. (NYSE: AWK) and Essential Utilities, Inc. (NYSE: WTRG) today announced that each company's board of directors has unanimously approved a definitive agreement to combine in an all-stock, tax-free merger as a leading regulated U.S. water and wastewater public utility with a pro forma market capitalization of approximately $40 billion and a combined enterprise value of approximately $63 billion, based on closing stock prices as of October 24, 2025.

Combined Company Will Serve 4.7 Million Water and Wastewater Connections Across 17 States; Combined Water and Wastewater Rate Base of Approximately $29.3 Billion.

The Deal Terms

Under the terms of the agreement, Essential shareholders will receive 0.305 shares of American Water for each share of Essential they own at the closing of the transaction. This exchange ratio implies a premium of approximately 10% to Essential shareholders based on the average of the daily volume weighted average price of each company's common stock over the 60-trading-day period ending October 24, 2025.

Upon completion of the merger, American Water shareholders will own approximately 69% and Essential shareholders will own approximately 31% of the combined company on a fully diluted basis.

The Strategic Rationale

"This combination brings together two industry leaders united by our shared mission to provide safe, clean, reliable and affordable water and wastewater services to our customers. By joining forces with Essential, the combined company's enhanced scale and operational efficiency will support continued investment in our critical infrastructure, enabling us to continue providing superior customer service at affordable rates."

Essential Chairman and CEO Christopher Franklin will serve as executive vice chair of the board of directors and as executive sponsor of the integration task force. The merged company will serve about 19.5 million people – or 4.7 million customer connections – across 17 states and on 18 military installations.

What About Peoples Natural Gas?

Here's where it gets interesting. American Water said that it plans to review strategic options for its non-water and non-wastewater businesses once the deal closes.

This strongly implies that Peoples Natural Gas—the $4.3 billion acquisition that transformed Aqua into Essential just five years ago—may be divested. American Water is a pure-play water company and seems intent to remain one.

The Critics Speak

Mary Grant, the Public Water for All campaign director at the nonprofit Food and Water Watch, said the merger is "alarming." "We are very worried about a future where there's one big water monopoly."

"When a town or a city goes out to bid, often, they already only get one or two bids, and it's going to typically Essential or American," she said. "And so now this town only gets one bid, right, from the newly-merged American Water."

"Control of our nation's dwindling water resources is rapidly consolidating into the hands of fewer and larger profit-driven mega-corporations. When finalized, this merger will eliminate any pretense of competition in the private water sector. Monopoly power over basic water services leads to higher rates for households and local businesses."

Timeline and Approvals

The deal is expected to close by the end of the first quarter of 2027. Between now and then, the companies must obtain shareholder approval, Hart-Scott-Rodino clearance, and regulatory approvals from multiple state utility commissions.

Strategic Analysis: Porter's Five Forces

Understanding Essential's competitive position requires examining the structural characteristics of its industry:

Threat of New Entrants: VERY LOW

Water distribution is the textbook definition of a natural monopoly. Water utilities oversee a vast network of nearly 2.2 million miles of aging pipelines. To ensure reliability and expand service, operators continually replace old infrastructure and invest in new pipeline systems. You cannot economically build a competing pipe network to someone's house. Regulatory barriers—requiring state utility commission approval for any new entrant—add another layer of protection.

Bargaining Power of Suppliers: LOW

Water itself is essentially free—it falls from the sky, flows in rivers, and sits in underground aquifers. Treatment chemicals, pipes, and equipment are commodity inputs available from multiple suppliers. Labor is skilled but not scarce.

Bargaining Power of Buyers: LOW TO MODERATE

Customers cannot switch water providers—they're captive to whoever owns the pipes connected to their home. However, the regulated utility model means state commissions set rates, providing some check on pricing power. The report addresses hazardous waste concerns, highlighting contaminants like PFAS chemicals and lead. Additionally, the report graded the nation's aging and underfunded drinking water infrastructure as a "C-" and wastewater infrastructure as a "D+."

Threat of Substitutes: VERY LOW

There is no substitute for water. It's required for human survival. Natural gas faces some substitution threat from electrification, but for heating and industrial processes, it remains essential for many customers. This is perhaps the most defensible position in any industry.

Competitive Rivalry: LOW (and declining)

American Water and Essential Utilities, the parent company of Aqua Water and Peoples Natural Gas, are the two largest municipal water and wastewater management companies nationwide. Post-merger, this duopoly becomes essentially a monopoly among large-scale private water utilities. Geographic territories create natural separation even where both exist.

Hamilton Helmer's Seven Powers Analysis

1. Scale Economies: STRONG

The estimates reveal considerable scale economies in terms of volume, particularly for small utilities that tend to have less output density. Larger customer bases spread fixed costs (treatment plants, administrative overhead, regulatory compliance) across more customers. Essential's national scale enables investments in technology, specialized expertise, and procurement leverage that small municipal systems cannot match.

2. Network Effects: MODERATE

Not traditional network effects, but "footprint density" matters enormously. Contiguous service areas create operating efficiencies—shared trucks, crews, and management. Each acquisition near an existing system is more valuable than a standalone purchase.

3. Counter-Positioning: STRONG

Municipalities cannot replicate private capital access. Small municipal systems lack the ability to issue equity, access debt markets efficiently, or achieve investment-grade credit ratings. Private utilities can raise capital that municipalities cannot—and critically, can spend it without voter approval.

4. Switching Costs: INFINITE

Once infrastructure is sold, it's essentially impossible to take back. No customer can switch water providers. Regulatory capture creates long-term lock-in. This may be the strongest switching cost moat in any industry.

5. Branding: MODERATE

Less important in monopoly utility than in competitive markets, but matters for municipal negotiations. A reputation for reliable service, regulatory cooperation, and community involvement helps win new acquisitions.

6. Cornered Resource: STRONG

We are advocates for the communities we serve and are dedicated stewards of natural lands, protecting more than 7,600 acres of forests and other habitats throughout our footprint. Water sources (aquifers, watersheds, river access rights) are finite and controlled. Watershed protection creates long-term resource security.

7. Process Power: MODERATE TO STRONG

Nearly 140 years of operational expertise. Regulatory know-how and relationships built over decades. The ability to navigate rate cases, manage capital programs, and integrate acquisitions represents institutional knowledge that cannot be easily replicated.

The Bull Case

Structural Tailwinds America's water infrastructure crisis isn't going away. The total addressable market opportunity for utility ownership of the country's 183 million customer connections has reached US$977 billion. On average, there are 148 utility acquisition deals per year, according to Bluefield's M&A data. Essential is one of only a handful of companies positioned to consolidate this fragmented industry.

Regulatory Support Fair market value legislation continues spreading to new states. Illinois, Ohio, Pennsylvania, and Indiana have all adopted forms of fair market value legislation. Each new state opens new acquisition opportunities.

Capital Deployment Visibility Looking ahead, Essential plans to invest more than $1.4 billion in 2025 and a projected $7.8 billion through 2029, tackling critical infrastructure challenges while preparing for future needs. This represents visible, predictable capital deployment at attractive regulated returns.

Dividend Reliability Essential Utilities has paid consecutive quarterly cash dividends for 78 years and has increased the dividend 33 times in the last 32 years. For income-focused investors, this track record is nearly unmatched.

New Growth Vectors The data center opportunity represents a potential new avenue for growth beyond traditional utility rates.

The Bear Case

Regulatory Risk Pennsylvania customers of former municipal water and sewer utilities sold since 2016 have seen bills increase by 44% to 166%. Political backlash against rate increases could result in less favorable regulatory treatment. Several bills to amend or repeal Act 12 have been introduced in Pennsylvania.

Merger Execution Risk The American Water merger requires approval from multiple state utility commissions, shareholder votes, and antitrust clearance. The proposal "is part of an alarming trend of water utility consolidation," said Mary Grant, water program director at Food & Water Watch. Opposition from consumer advocates could complicate approvals.

Natural Gas Stranded Asset Risk The likely divestiture of Peoples Natural Gas raises questions about the original strategic logic. If American Water sells Peoples for less than Essential paid, shareholders will have effectively subsidized a five-year round trip.

Interest Rate Sensitivity As a capital-intensive regulated utility, Essential is sensitive to interest rates. Higher rates increase borrowing costs and make dividend yields relatively less attractive versus bonds.

Climate and ESG Concerns Natural gas distribution faces increasing scrutiny as electrification advances. PFAS contamination and lead pipe replacement represent significant compliance costs. In 2024, Essential invested $27 million in PFAS mitigation, seeking low-interest grants and loans to minimize financial impact on customers.

Key Performance Indicators to Track

For investors monitoring Essential Utilities (or the combined American Water post-merger), three metrics deserve particular attention:

1. Rate Base Growth This is the single most important metric for regulated utility earnings. Rate base represents the invested capital on which regulators allow a return. These investments are expected to drive a regulated utility rate base growth of 8% through 2029. Tracking actual rate base growth versus guidance provides insight into capital deployment effectiveness and regulatory relationships.

2. Customer Growth (Acquisitions + Organic) Acquisitions remain a key growth driver, with the company reporting over 135,000 water and wastewater customers acquired through M&A since 2015, resulting in approximately $550 million in rate base increase. The pace and economics of acquisitions indicate management's ability to continue the roll-up strategy.

3. Regulatory Lag / Rate Case Success As of November 4, 2025, the company's regulated water segment received rate awards and infrastructure surcharges in North Carolina, New Jersey, Ohio, and Pennsylvania, of $92.6 million. The company currently has base rate cases pending in North Carolina, Ohio, Texas, and Virginia for an estimated $96.5 million in incremental annual revenues. The ability to recover infrastructure investments through timely rate cases is essential to the business model.

Playbook: Business & Investment Lessons

1. The Power of Roll-Ups in Fragmented Industries Essential's 300+ acquisitions over two decades demonstrate how patient capital deployment in fragmented industries can create massive value. The key ingredients: a large addressable market of subscale operators, economies of scale, and access to capital markets that smaller players lack.

2. Regulatory Navigation is a Competitive Advantage In regulated industries, the ability to work constructively with regulators—building relationships, managing rate cases effectively, demonstrating community benefit—is as important as operational excellence. DeBenedictis's government experience proved invaluable in building these capabilities.

3. Infrastructure Investment Has Generational Compounding Effects Pipes last 75-100 years. When Essential invests in infrastructure today, it creates rate base that will earn returns for decades. This long-duration compounding is difficult for competitors to replicate quickly.

4. Fair Market Value Legislation Creates Acquisition Optionality The spread of FMV laws across states demonstrates how policy changes can unlock acquisition opportunities. Companies that anticipate and advocate for favorable regulatory frameworks create competitive advantages.

5. Essential Services Generate Pricing Power "Essential" is in the company's name for a reason. Services that customers cannot live without—literally, in the case of water—generate pricing power that discretionary businesses lack. In inflationary environments, essential services utilities can often pass through cost increases.

Conclusion: What's Actually Being Bought Here?

Essential Utilities stands at a pivotal moment. The announced merger with American Water will—if approved—transform the company from an independent roll-up into a 31% stake in America's dominant private water utility. Christopher Franklin will transition from CEO to executive vice chairman. The Essential name will disappear, absorbed into American Water.

For long-term shareholders, the key question is whether this merger creates or destroys value. The 10% premium is modest by acquisition standards. The strategic logic of combining the two largest players is compelling from a scale perspective but raises legitimate concerns about competition in municipal utility sales.

Meanwhile, the fate of Peoples Natural Gas—the $4.3 billion acquisition that transformed Aqua into Essential—remains uncertain. American Water's stated intention to "review strategic options" for non-water businesses suggests divestiture is likely. Five years after the transformational deal, Essential's natural gas diversification may prove to be a detour rather than a destination.

But zooming out, the bigger picture remains bullish for infrastructure investors. The U.S. water and wastewater infrastructure is deteriorating, with water main breaks occurring every few minutes. The Environmental Protection Agency estimates that $1.25 trillion in investments will be needed over the next 20 years.

Someone has to fix America's broken pipes. Whether under the Essential banner or as part of American Water, the business model—deploying capital into essential infrastructure at regulated returns—will endure. The pipes don't care what name is on the trucks.

Both Aqua and Peoples bring a rich history of nearly 140 years of delivering essential water and natural gas service and look forward to delivering life-sustaining water and natural gas to millions of customers for decades to come.

From Springfield Water Company in 1886 to a $63 billion combined enterprise in 2027, that's quite a journey. And the roll-up playbook that made it possible—patient capital deployment in fragmented essential services—may prove to be one of the most durable investment strategies of our time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube