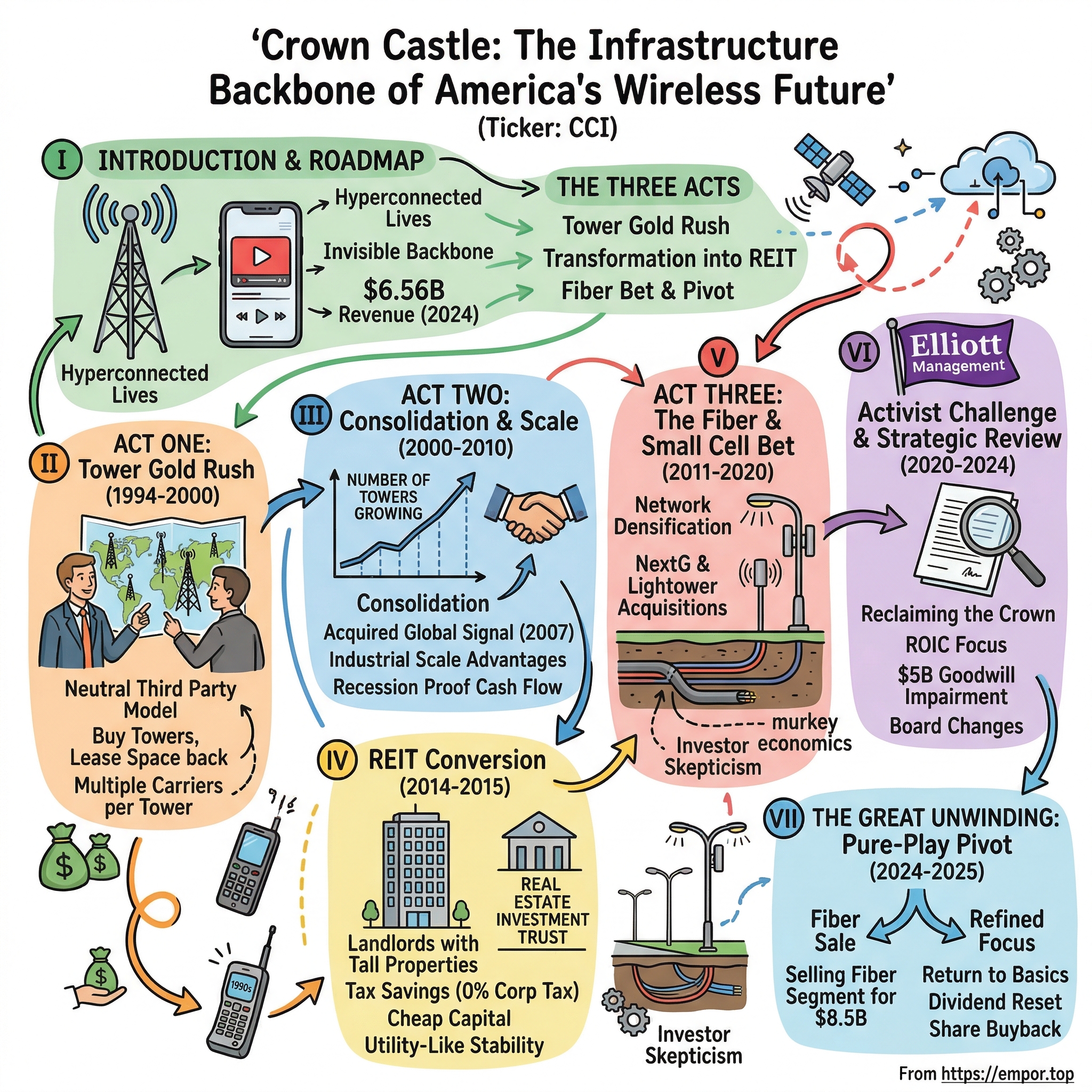

Crown Castle: The Infrastructure Backbone of America's Wireless Future

I. Introduction & Episode Roadmap

Picture this: You're streaming Netflix on your phone while sitting in traffic on I-95. Your video doesn't buffer. Your call doesn't drop. This seemingly mundane miracle happens because somewhere nearby—perhaps disguised as a flagpole or tucked behind a shopping center—stands a piece of steel and fiber infrastructure that Crown Castle owns. With over 40,000 cell towers and approximately 85,000 route miles of fiber crisscrossing America, Crown Castle has quietly become the invisible backbone enabling our hyperconnected lives, generating $6.56 billion in revenue in 2024.

Here's the paradox that makes Crown Castle fascinating: How did a company built on leasing what are essentially "dumb" steel towers—glorified vertical real estate—position itself at the center of America's 5G revolution? How did a business model that started with renting space on metal poles evolve into a sophisticated infrastructure play that had activist investors circling and ultimately forced a dramatic strategic pivot?

The Crown Castle story is really three acts. Act One: The wild west days of the tower gold rush in the 1990s, when deregulation unleashed a land grab for vertical real estate. Act Two: The transformation into a REIT, where financial engineering met infrastructure monopoly. Act Three: The ambitious fiber bet that promised to revolutionize the business but ultimately led to a $5 billion write-down and a return to basics.

What makes this story particularly compelling is how it illuminates broader themes about American infrastructure. This is a tale about network effects without software, about monopolies built one tower at a time, about the tension between focus and diversification, and about what happens when Wall Street's demand for growth collides with the patient capital requirements of infrastructure investing.

Crown Castle's journey from a Pittsburgh startup to a Fortune 500 infrastructure giant reveals fundamental truths about how digital infrastructure really works, why some bets on technological convergence fail, and what it takes to build—and nearly destroy—competitive moats in capital-intensive businesses. As we'll see, sometimes the boring businesses are the best businesses, until they try to be something they're not.

II. Origins & The Tower Gold Rush (1994-2000)

Ted Miller had a problem in 1994. As an executive at a Pennsylvania construction company, he kept hearing the same complaint from wireless carriers: they needed cell towers, lots of them, and they needed them yesterday. The Telecommunications Act hadn't even been signed yet, but Miller could smell opportunity. He called up his colleague Walter Rakowich with a proposition that sounded almost too simple: "What if we just owned the towers and leased space to multiple carriers?"

The duo secured backing from Brown Brothers Harriman & Co., the white-shoe investment bank that had financed everyone from railroads to the Marshall Plan. BBH wasn't known for speculative ventures, but they saw what Miller and Rakowich saw: wireless wasn't a fad. Americans were buying cell phones at a rate that would make even the most optimistic projections look conservative. Someone had to own the infrastructure.

Crown Castle International was born in Houston—not Pittsburgh, interestingly, as the founders quickly realized Texas offered better business conditions and proximity to the telecom corridor. They started with just 133 cell towers, most of them acquired from carriers who were happy to get these capital-intensive assets off their balance sheets. The early strategy was brilliantly simple: buy towers from carriers who needed cash, lease the space back to them, then lease additional space on the same tower to their competitors.

The Telecommunications Act of 1996 changed everything. Suddenly, the barriers that had protected local monopolies crumbled. New carriers emerged overnight. Existing carriers rushed to expand coverage. Everyone needed towers, and they needed them in places where zoning boards weren't exactly thrilled about 200-foot steel structures. Crown Castle positioned itself as the solution—the neutral third party who could host equipment from competing carriers on the same tower.

By 1998, with approximately 1,400 towers in their portfolio, Miller and Rakowich took Crown Castle public on the NASDAQ. The timing was perfect—or so it seemed. The dot-com bubble was inflating, telecom stocks were soaring, and anything touching the internet was gold. Crown Castle raised capital like a Silicon Valley startup but deployed it like a real estate company, methodically acquiring tower portfolios across the country.

The tower mania of 1999-2000 was something to behold. Competitors emerged from everywhere—American Tower, SBA Communications, SpectraSite. Valuations soared to absurd levels. Crown Castle paid multiples for tower portfolios that would make today's private equity firms blush. But here's what the skeptics missed: unlike dot-com vaporware, these towers were real assets generating real cash flow from credit-worthy tenants locked into long-term contracts.

The psychology of the era was fascinating. While everyone was obsessed with sexy telecom equipment makers and software companies, Crown Castle was essentially becoming a landlord. But what a landlord—one whose tenants couldn't easily move, whose properties became more valuable with each additional tenant, and whose business model had almost no variable costs. The dot-com crash was coming, but Crown Castle had built something that would survive the wreckage.

III. Building Scale Through Consolidation (2000-2010)

The NASDAQ crash of 2000 should have been catastrophic for Crown Castle. Telecom companies were imploding—WorldCom, Global Crossing, dozens of CLECs (Competitive Local Exchange Carriers) that nobody remembers today. But Crown Castle did something clever: on April 25, 2001, they moved from NASDAQ to the NYSE, trading under "CCI." It was a symbolic shift from growth stock to infrastructure play, from speculation to stability.

While competitors panicked, Crown Castle went shopping. The early 2000s became a buyer's market for tower assets. Distressed carriers needed cash. Bankrupt operators were liquidating portfolios. Crown Castle, with its NYSE listing providing credibility and access to capital markets, methodically expanded. By 2003, they had over 10,000 towers spanning the continental United States, Hawaii, and Puerto Rico.

Then came the surprise move that defined Crown Castle's discipline. In 2004, they owned Crown Castle UK, a promising subsidiary with significant tower assets across Britain. The business was growing, international expansion seemed logical, and competitors like American Tower were aggressively going global. But Crown Castle's board saw something different: complexity without commensurate returns. On August 31, 2004, they sold Crown Castle UK to National Grid Transco for over $2 billion—a stunning price that validated their domestic focus.

The UK sale provided war chest capital just as the U.S. market was about to explode. Smartphones were still years away, but data usage was beginning its inexorable climb. Crown Castle deployed the UK proceeds into U.S. acquisitions, culminating in the blockbuster deal: acquiring Global Signal Inc. in 2007. Global Signal wasn't just any competitor—they had premium assets in dense urban markets where zoning made new towers nearly impossible.

The Global Signal acquisition was a masterclass in industrial consolidation. Crown Castle paid $4.03 billion, a price that made analysts gasp. But they understood something fundamental: in infrastructure, scale creates insurmountable advantages. More towers meant more negotiating leverage with carriers. Dense geographic clusters meant lower maintenance costs per tower. Most importantly, having the best locations meant carriers had no choice but to lease from you.

The shared infrastructure model was evolving beyond simple co-location. Crown Castle pioneered "build-to-suit" arrangements where they'd construct custom towers for anchor tenants, then market remaining capacity to others. They developed master lease agreements covering hundreds of sites, reducing transaction costs. They even started offering managed network services, though this would later prove a distraction.

By 2010, Crown Castle had emerged from the financial crisis remarkably unscathed. While banks collapsed and real estate imploded, cell phone usage actually increased during the recession—apparently, people would give up almost anything before their mobile phones. Crown Castle's towers, generating steady cash flow from investment-grade tenants, looked less like tech assets and more like utilities. The boring business was beautiful.

IV. The Carrier Agreements & Tower Economics (2010-2014)

The September 2012 morning when Crown Castle announced its $2.4 billion deal with T-Mobile wasn't just another tower transaction—it was the opening bell of a new era in infrastructure economics. Crown Castle was acquiring rights to approximately 7,200 T-Mobile towers for $2.4 billion in cash at closing, with the exclusive right to lease and operate the towers for a weighted average term of approximately 28 years. But what made this deal fascinating wasn't the headline number—it was the structure that would become the template for transforming carriers from tower owners into tenants.

Crown Castle secured the option to purchase the towers at the end of the respective lease terms for aggregate option payments of approximately $2.4 billion, with payments primarily between 2025 and 2048. Think about that structure for a moment: Crown Castle essentially got a 28-year option on infrastructure that was becoming more valuable every year. T-Mobile committed to maintain its communications facilities on the towers from Crown Castle for a minimum of 10 years with annual rent escalation provisions tied to the consumer price index.

The economics were beautiful in their simplicity. Crown Castle estimated the T-Mobile towers would produce approximately $125 million to $130 million in adjusted funds from operations before financing costs in 2013, with sufficient capacity to accommodate at least one additional tenant per tower without significant incremental capital. With an average of 1.6 tenants per tower, these assets had massive room to grow.

Just over a year later, Crown Castle pulled off an even bigger coup. On October 20, 2013, Crown Castle announced it would acquire rights to approximately 9,700 AT&T towers for $4.85 billion in cash, with the exclusive right to lease and operate the towers for a weighted average term of approximately 28 years. The AT&T portfolio was even more attractive than T-Mobile's—nearly half of the AT&T towers were located in the top 50 markets, where Crown Castle expected the majority of network densification and upgrade activity to occur.

AT&T would sublease capacity on the towers from Crown Castle for a minimum of 10 years for $1,900 per month per site, with annual rent increases of 2 percent. The deal structure was elegant: Crown Castle would have fixed price purchase options, totaling approximately $4.2 billion, for these towers based on their estimated fair market values at the end of the lease terms.

Now let's talk about the real magic—the tower economics that made Crown Castle's business model so compelling. Imagine you own a 200-foot steel tower. Your first tenant, say Verizon, pays you $2,000 per month. Your costs—land lease, maintenance, utilities—are largely fixed at around $500 per month. So you're making $1,500 in gross profit, a respectable 75% margin.

Here's where it gets interesting. When AT&T comes along wanting space on the same tower, they also pay $2,000 per month. But your incremental costs? Maybe $50 for slightly higher electricity usage. That second tenant brings you to $3,950 in revenue against $550 in costs—suddenly you're at 86% margins. Add a third tenant, and you're approaching 90% margins. The fourth tenant? You're printing money at 92-93% margins.

This is why Crown Castle could confidently state that adding a new tenant bringing in about $25,000 of additional annual rental revenue would translate to about $24,000 in gross profits—a staggering 96% incremental margin. No software company, no matter how sophisticated its code, could match these unit economics on physical infrastructure.

The customer concentration that would terrify most investors actually worked in Crown Castle's favor. After the AT&T deal, approximately 84% of Crown Castle's consolidated site rental revenue would come from the Big 4 US wireless carriers. These weren't fly-by-night startups that might disappear—these were investment-grade companies with multi-billion-dollar networks that literally couldn't function without Crown Castle's towers.

The contracts themselves were works of art in risk mitigation. Multi-year terms with built-in escalators, typically around 3% annually. Master lease agreements covering hundreds of sites, reducing administrative overhead. Most importantly, the switching costs for carriers were astronomical—not just financially, but operationally. Moving equipment from one tower to another meant service disruptions, regulatory approvals, and customer fury. Once a carrier was on your tower, they were essentially married to it.

By 2014, Crown Castle had assembled a portfolio that would make any infrastructure investor salivate: predictable cash flows, minimal maintenance capex, pricing power through escalators, and customers who couldn't leave even if they wanted to. The boring business of owning vertical real estate had evolved into one of the most elegant business models in American capitalism. The stage was set for Crown Castle's next transformation—one that would fundamentally alter not just its business model, but its very identity as a company.

V. REIT Conversion & Capital Structure Evolution (2014-2015)

Jay Brown stood before Crown Castle's board in late 2013 with a radical proposition: "We're not really a telecom company. We're landlords with very tall properties." The room fell silent. For two decades, Crown Castle had thought of itself as a wireless infrastructure company. But Brown, then CFO, saw something different—a real estate empire that happened to specialize in vertical property.

Crown Castle officially became a Real Estate Investment Trust (REIT) in January 2014, joining an exclusive club that included shopping mall owners, apartment landlords, and office building operators. But Crown Castle wasn't your typical REIT. While Simon Property Group worried about foot traffic and Equity Residential fretted over vacancy rates, Crown Castle's tenants were locked into decades-long contracts with no ability to negotiate rent down when times got tough.

The REIT conversion was financial engineering at its finest, but it wasn't without controversy. Traditional REITs owned their land and buildings outright. Crown Castle's towers sat on leased land, and much of their value came from contracts, not physical assets. The IRS had to be convinced that cell towers constituted "real property" for REIT purposes—a determination that seems obvious now but required extensive legal argumentation at the time.

Why did the REIT structure make sense? Start with taxes. As a REIT, Crown Castle could avoid corporate income tax entirely as long as it distributed at least 90% of its taxable income to shareholders as dividends. For a company generating massive cash flows with minimal reinvestment needs, this was like getting a 35% raise overnight. The tax savings alone justified the conversion costs.

But the real genius was how REIT status transformed Crown Castle's cost of capital. Traditional tower companies were valued like telecom firms—volatile, technology-dependent, subject to disruption. REITs were valued like utilities—stable, predictable, boring. Boring meant cheap capital. Crown Castle's cost of debt dropped significantly as REIT-focused investors, hungry for yield in a low-rate environment, poured money into the company's bonds.

The dividend obligation that came with REIT status—that mandatory 90% payout—actually became a feature, not a bug. It imposed discipline on management. No empire-building acquisitions, no speculative technology bets. Every dollar had to earn its keep or get returned to shareholders. This forced focus would later become crucial when the fiber strategy began consuming capital.

Crown Castle now competed directly with American Tower and SBA Communications, the other two members of the tower oligopoly. American Tower, also a REIT, had gone global, with operations in India, Africa, and Latin America. SBA remained a traditional C-corp, giving it more flexibility but higher tax costs. Crown Castle staked out the middle ground: REIT efficiency with pure-play U.S. focus.

The market loved it—initially. Crown Castle's stock price rose over 20% in the year following REIT conversion. Dividend-focused investors who had never looked at tower companies suddenly became buyers. The company could raise capital at rates that made competitors envious. Everything was working perfectly. Perhaps too perfectly.

The REIT structure created its own trap. Once you become a REIT, it's nearly impossible to go back without massive tax consequences. The dividend obligations meant Crown Castle needed predictable, growing cash flows forever. This pushed management toward what seemed like the logical next step: densification through small cells and fiber. After all, if you're going to be a real estate company, why not own all the real estate that wireless networks would need?

VI. The Fiber & Small Cell Bet (2011-2020)

Ben Moreland had seen the future, and it was dense. Standing atop a Crown Castle tower in Manhattan in 2011, the CEO could see the problem clearly: you couldn't build more towers in cities. Zoning boards would revolt. Property was too expensive. But data demand was exploding, and physics demanded that signals get closer to users. The solution seemed obvious—small cells connected by fiber.

In December 2011, Crown Castle announced a definitive agreement to purchase NextG Networks for about $1.0 billion. NextG had over 7,000 distributed antenna system nodes on-air, with another 1,500 nodes under construction, as well as rights to more than 4,600 miles of fiber optic cables. This wasn't just an acquisition; it was a declaration of intent. Crown Castle would own not just the towers, but the entire network densification layer.

The strategic rationale was compelling. As Moreland explained to investors, "Think of towers as the highways and small cells as the local roads. You need both for a complete transportation system." The pitch resonated. Mobile data was growing at 40-50% annually. Networks needed to get denser. Someone had to own the infrastructure.

In 2015, Crown Castle expanded into small cell technology in order to boost the capability and widen the scope of its network. They acquired Sunesys, adding over 10,000 route miles of fiber in key markets like Los Angeles, Philadelphia, Chicago, and Atlanta. Each acquisition built on the last, creating what management saw as an unassailable position in network densification.

Then came the big one. On July 19, 2017, Crown Castle signed an agreement to acquire Lightower, a fiber network operator in the northeast U.S., for approximately $7.1 billion. The transaction increased Crown Castle's fiber network to approximately 60,000 route miles. Lightower wasn't just fiber—it was premium fiber in the most valuable markets, serving not just wireless carriers but enterprises and governments.

The numbers initially looked good. Revenue increased by 3.3% and small cells increased sales by 42% following the Lightower acquisition. Crown Castle combined all its fiber assets under a single brand—Crown Castle Fiber—and pitched a unified infrastructure story to carriers. Towers for coverage, small cells for capacity, fiber to connect it all.

But early struggles emerged that management downplayed. Small cells took forever to deploy—18 to 24 months versus 3 to 6 months for tower amendments. Each small cell required negotiations with municipalities, utility companies, and property owners. The economics were murky. While a tower amendment might cost $25,000 and generate $25,000 in annual revenue, a small cell could cost $100,000 to build and generate only $15,000 to $20,000 per year.

Investor skepticism grew. On earnings calls, analysts pressed: What were the returns on fiber investment? How much of the fiber revenue came from wireless versus enterprise? Why was the growth so slow? Management's answers became increasingly complex, involving "holistic solutions" and "strategic positioning." The simple elegance of the tower model was getting lost in fiber complexity.

By 2019, Crown Castle had become a Fortune 500 company for the first time, operating with 100 offices worldwide, its network including over 40,000 cell towers and approximately 85,000 route miles of fiber supporting small cells and fiber systems. On paper, they were the undisputed infrastructure leader. But underneath, two businesses were emerging—one wildly profitable, one struggling to justify its existence.

The fiber bet was predicated on a simple assumption: 5G would require massive densification, and Crown Castle would own the infrastructure. But as 5G rolled out, carriers found ways to squeeze more capacity from existing towers through technological improvements. Small cells remained important in dense urban areas, but the revolution in densification was happening slower than expected. Crown Castle had built a fiber network for a future that was arriving late.

VII. The 5G Revolution & Peak Growth (2018-2023)

The year 2018 should have been just another year of steady growth for Crown Castle. Instead, it became the inflection point when 5G transformed from PowerPoint promise to physical reality. Jay Brown, now CEO, stood before investors at the company's annual meeting with a bold proclamation: "We're witnessing the beginning of the most significant network upgrade cycle in wireless history."

The numbers told a story of explosive growth. According to the latest statistics from the CTIA trade group, there were a total of 418,887 operational cell sites across the US at the end of 2021, with the US wireless industry collectively building almost 70,000 new cell sites between 2019 and 2021, up from the 42,000 sites constructed during the period from 2016 to 2018. This wasn't just growth—it was acceleration on steroids.

All the major providers launched networks that support the next-generation wireless data technology in 2019. As a result, Crown Castle's profits jumped 38 percent to $860 million from $622 million the previous year, with revenues rising 7 percent to $5.8 billion from $5.4 billion in 2018. These weren't incremental improvements—they were step-function changes that validated every infrastructure bet Crown Castle had made.

The deployment statistics were staggering. Cell sites exploded from over 25,000 sites in 2017 to 349,344 cell sites in 2019—a fourteen-fold increase that caught even optimists off guard. The reason was simple physics: 5G networks needed to be 10 times denser than 4G networks. Every carrier needed more towers, more small cells, more fiber—and they needed them yesterday.

Jay Brown noted in 2019: "We experienced our highest level of tower leasing activity in more than a decade as the continued growth in mobile data demand is driving our customers to make significant investments in their existing 4G networks, while they are also positioning their businesses for 5G." Crown Castle wasn't just riding the wave—they were the wave itself.

The data explosion driving this growth was mind-boggling. Mobile data demand was set to triple between the end of 2022 and 2028, representing a cumulative average growth rate of 21%. By 2028, 5G was expected to grow from 17% of all traffic to 69%. Every percentage point of that growth meant more equipment on Crown Castle's towers, more amendments to existing contracts, more revenue dropping straight to the bottom line.

The C-Band spectrum auction in 2021 became Crown Castle's Christmas morning. Carriers spent over $80 billion acquiring mid-band spectrum that would form the backbone of true 5G service. But spectrum without infrastructure is useless—you need towers to hang the radios, fiber to backhaul the data. Crown Castle owned both. The auction wasn't just a windfall for the government; it was a guarantee of years of infrastructure spending that would flow directly into Crown Castle's coffers.

Despite the challenges 2020 presented, Crown Castle generated industry leading tower revenue growth in the U.S., with approximately 6% growth in Organic Contribution to Site Rental Revenue for their Towers segment in 2021. While the pandemic disrupted everything else, it accelerated digital transformation and made wireless connectivity more critical than ever.

The tower amendment economics during this upgrade cycle were particularly beautiful. When a carrier wanted to add 5G equipment to an existing 4G tower, Crown Castle could charge amendment fees plus increased monthly rent. The carrier bore all the equipment and installation costs. Crown Castle's only expense was processing paperwork. It was like being a landlord whose tenants voluntarily renovated their apartments and paid higher rent for the privilege.

By the end of 2020, Crown Castle finished the year with approximately 50,000 small cells on air, and meaningfully increased their backlog of small cells committed or under construction to approximately 30,000 with the 5G small cell agreement with Verizon. The small cell business, despite its challenges, was finally gaining momentum.

But beneath the surface, cracks were forming. The fiber segment that was supposed to be the growth engine was becoming an albatross. Small cells took forever to deploy, returns were uncertain, and the synergies with towers remained elusive. The market started asking uncomfortable questions: Was Crown Castle a tower company that happened to own fiber, or a fiber company that happened to own towers? The answer would determine everything.

VIII. The Activist Challenge & Strategic Review (2020-2024)

Jesse Cohn didn't mince words in his July 2020 letter to Crown Castle's board. Elliott, with an investment of approximately $2 billion in Crown Castle, highlighted that the Company's fiber strategy was "detracting from shareholder returns and would continue to do so unless significant changes were made." The hedge fund's "Reclaiming the Crown" campaign was surgical in its precision, attacking not just the fiber strategy but the entire governance structure that enabled it.

Elliott's analysis was devastating. The Company's strategy, led by CEO Jay Brown since 2016, had been a failure. During the tenure of the current executive team, Crown Castle had underperformed its direct peers by an average of 85 percent in total return, which translates into nearly $26 billion of unfulfilled shareholder value. Twenty-six billion dollars—enough to build a small nation's infrastructure—had evaporated through strategic missteps.

The initial response from Crown Castle was classic corporate stonewalling. Management dismissed Elliott's concerns, arguing that fiber was essential for future growth, that synergies would eventually materialize, that patience would be rewarded. But Elliott had done something clever—they'd spoken to customers, competitors, and industry experts. The verdict was unanimous: Crown Castle's fiber business was subscale, poorly managed, and destroying value.

What made Elliott's campaign particularly potent was their focus on return on invested capital (ROIC). One of the critical proposals Elliott made in 2020 was the implementation of a ROIC-based management incentive program. The Board and its Compensation Committee had continued to dismiss a ROIC-based management-incentive program, which enabled aggressive capital deployment without any penalty for delivering a woeful ROIC. Management must be held accountable for capital allocation.

Crown Castle's board made a tactical retreat. Only after Elliott released a public letter and presentation on July 6, 2020 did Crown Castle address the exceptionally long tenure of its directors. Less than four weeks later, Crown Castle announced that five directors (including the Chairman of the Board) with an average tenure of 20 years would not stand for reelection. But they didn't address the core issue—the fiber strategy remained unchanged.

Fast forward to 2023, and Elliott was back with a vengeance. Elliott's 2023 "Restoring the Castle" campaign followed its 2020 "Reclaiming the Crown" campaign. The Company "disregarded our data-driven analysis, and our recommended changes were neither made nor taken seriously." As a result, Crown Castle had continued to underperform its peers over all time periods in the last 15 years and had seen its stock price recently hit a six-year low.

The timing was exquisite. Crown Castle had just announced a $5 billion goodwill impairment charge in 2024, essentially admitting that the fiber assets they'd bought for billions were worth far less than they'd paid. The market had already rendered its verdict—Crown Castle's stock was trading at multiples below its tower-pure peers. The diversification discount had become a diversification disaster.

Management turnover accelerated. Steven Moskowitz was terminated as CEO. Daniel Schlanger stepped in as interim CEO, while Sunit Patel took over as EVP and CFO on April 1, 2025. The revolving door of executives signaled deep institutional dysfunction. Employee morale cratered—Glassdoor reviews painted a picture of a company in crisis, with CEO approval ratings far below industry peers.

The board changes were even more dramatic. Crown Castle had enacted extraordinarily shareholder-unfriendly amendments to its bylaws in 2021, compromising the ability of shareholders to exercise their fundamental right to nominate directors and seek change in the boardroom, which Elliott believed violated Delaware law. These defensive measures only emboldened the activists.

By December 2023, Crown Castle capitulated. Under the terms of the settlement agreement, Crown Castle appointed two new independent directors to the board and formed a committee to review Crown Castle's fiber business with the goal of enhancing shareholder value. The strategic review that management had resisted for years was finally underway.

The strategic review process itself became a case study in corporate drama. Investment bankers from every major firm descended on Houston, pitching various scenarios: split the company, sell the fiber, go private, merge with a competitor. Should Crown Castle explore the sale of the fiber unit, as Elliott was demanding, the business could fetch $11 billion-$15 billion from a suitor. Private equity firms circled like vultures, seeing opportunity in the distress.

What Elliott understood—and what Crown Castle's management had missed—was that the market valued focus over diversification in infrastructure. American Tower and SBA Communications, Crown Castle's pure-play tower competitors, traded at significant premiums despite having less fiber. The market was sending a clear message: stick to what you're good at.

The activist pressure exposed a fundamental truth about Crown Castle's fiber bet: it wasn't just a bad investment, it was a betrayal of the company's core competency. Towers were simple, beautiful businesses with 90%+ margins. Fiber was complex, capital-intensive, and marginally profitable. By trying to be everything to everyone, Crown Castle had become nothing to anyone. The great unwinding was inevitable.

IX. The Great Unwinding: Fiber Sale & Pure-Play Pivot (2024-2025)

The March 13, 2025 announcement landed like a thunderclap in Houston's energy corridor. Crown Castle was selling all of its Fiber segment—the business it had spent over a decade and tens of billions building—to EQT Active Core Infrastructure fund and Zayo Group Holdings for $8.5 billion in aggregate. The great unwinding wasn't just happening; it was complete.

The structure of the deal revealed how far Crown Castle had fallen. EQT would acquire the small cells business for $4.25 billion, while Zayo would take the fiber solutions business for another $4.25 billion. Combined, these assets had cost Crown Castle over $15 billion to build and acquire. The math was brutal—they were selling for roughly 57 cents on the dollar.

Steven Moskowitz, who'd been brought in to clean up the mess, didn't mince words: "Selling our Fiber segment represents a significant step on Crown Castle's path towards a refined focus as a pure-play provider of multi-tenant tower assets." Translation: We're admitting defeat and going back to what we actually know how to do.

The 2024 results that accompanied the sale announcement told the story of a company in crisis. The company reported key 2024 results including: 4.5% tower organic growth, site rental revenues decrease of 2.7%, and a net loss of $3.9 billion primarily due to a $5.0 billion goodwill impairment charge in the Fiber segment. That goodwill impairment was essentially Crown Castle writing a $5 billion check to reality—an admission that the fiber assets they'd bought weren't worth anywhere near what they'd paid.

The leadership chaos continued unabated. Daniel Schlanger appointed as interim CEO following Steven Moskowitz's termination, with Sunit Patel taking over as EVP and CFO on April 1, 2025. In less than eighteen months, Crown Castle had churned through three CEOs—a level of instability that would cripple most companies but was somehow becoming normal in Houston's telecom sector.

The capital allocation changes were perhaps the most dramatic admission of failure. Reducing annual dividend to approximately $4.25 per share in Q2 2025, implementing a $3.0 billion share repurchase program. For a REIT that had built its entire investor base on steady, growing dividends, cutting the payout was like admitting the business model had failed. The $3 billion buyback was a desperate attempt to prop up the stock price—using the proceeds from selling assets at a loss to buy back shares that had been crushed by those very losses.

In December 2023, Crown Castle's Board of Directors established a Fiber Review Committee to conduct a strategic and operating review of the Company's small cells and fiber solutions businesses, with the goal of enhancing shareholder value. In consultation with its financial, legal and strategic advisors, the Fiber Review Committee, the Company's Board of Directors and Company management conducted a comprehensive review of a broad range of potential options. Based on that review and after assessing offers from financial and strategic buyers that proposed a variety of transaction structures, the Company's Board of Directors approved the sale of its small cells business to EQT and fiber solutions business to Zayo.

The buyers were telling in their own right. Zayo, backed by DigitalBridge and EQT, was a fiber specialist that actually understood the business. "Zayo has spent more than $20 billion over the past five years on fiber infrastructure across the country and intends to continue investing billions in expanding the AI ecosystem in the United States through a robust fiber broadband solutions buildout, supporting the country's role as a global leader in AI." What Crown Castle couldn't make work, Zayo believed it could—because Zayo was actually a fiber company, not a tower company pretending to be one.

With this acquisition, Zayo will add approximately 90,000 route miles of fiber to its network, increasing its overall reach to more than 70,000 on-net locations. For Zayo, this was strategic expansion. For Crown Castle, it was strategic retreat.

The transaction timeline—closing in the first half of 2026—meant Crown Castle would spend another year in purgatory, operating assets it had already admitted were failures, with employees who knew they'd soon be working for someone else. It was corporate hospice care, keeping the patient comfortable while everyone waited for the inevitable.

The market reaction was mixed but telling. Crown Castle's stock jumped on the announcement—not because investors were excited about the price, but because they were relieved the bleeding would finally stop. The company would emerge smaller, simpler, and poorer, but at least it would emerge.

"As we look ahead, with our expansive and capital efficient portfolio of approximately 40,000 towers across key locations in the U.S., which we believe is the best wireless market in the world, and greater focus on customer service and operational initiatives, we anticipate that we can generate durable and growing cash flows that will provide attractive returns to our shareholders."

The language was corporate boilerplate, but the message was clear: Crown Castle was returning to its roots. After a decade-long, multi-billion-dollar detour through fiber and small cells, they were going back to being a boring tower company. Sometimes, boring is beautiful.

X. Business Model Deep Dive & Unit Economics

The beauty of Crown Castle's tower business lies in its elegant simplicity. Take a 200-foot steel structure, divide it into vertical real estate, and watch the money flow. Towers account for about 70% of Crown Castle's revenue, but they generate far more than 70% of the company's actual economic value.

Start with capacity. Most towers have capacity for at least four tenants, yet the average Crown Castle tower hosts just 2.2 tenants. This isn't a bug—it's an opportunity. Almost all of Crown Castle's wireless infrastructure can accommodate additional tenancy without meaningful incremental investment. Every new tenant is essentially pure profit dropping to the bottom line.

The revenue model is a thing of beauty. Over 80% of Crown Castle's recurring revenue comes from long-term leases with initial five- to 15-year terms. The average remaining customer contract term of five years represents $23 billion of contracted lease payments. These aren't hopeful projections or aggressive sales forecasts—this is money already committed, just waiting to be collected.

The built-in price escalators add around 3% to annual earnings growth without Crown Castle lifting a finger. These aren't negotiated annually or tied to complex metrics. They're contractual, automatic, and compound over time. A tower generating $5,000 per month today will generate $5,150 next year, $5,305 the year after. Over a 20-year lease, these escalators can double the revenue from a single tenant.

Customer concentration, typically a risk factor, becomes a strength in Crown Castle's model. AT&T represents 22% of revenue, T-Mobile 20%, Verizon 19%, and the legacy Sprint 15%. These aren't startup customers who might disappear—these are the titans of American telecommunications with hundreds of billions invested in networks that depend on Crown Castle's infrastructure.

The switching costs create an almost impenetrable moat. For a carrier to move equipment from a Crown Castle tower to a competitor's, they'd need to: find alternative tower space in the same coverage area (often impossible in urban zones), obtain new permits and zoning approvals (6-18 months minimum), physically move tons of equipment (service disruption guaranteed), and reconnect all backhaul and power systems. The cost? Millions per site. The benefit? Saving perhaps $500 per month in rent. The math never works.

REIT dynamics add another layer of attractiveness. As a REIT, Crown Castle must distribute at least 90% of taxable income to shareholders. This isn't a choice—it's a legal requirement that ensures management can't hoard cash for empire-building acquisitions. The discipline is built into the structure.

The AFFO (Adjusted Funds From Operations) metrics tell the real story. Unlike traditional earnings, which get distorted by depreciation on assets that don't actually depreciate (when was the last time a cell tower lost value?), AFFO shows the actual cash generation. Crown Castle's AFFO margins consistently exceed 60%, meaning three dollars of every five that come in the door can be distributed to shareholders or reinvested in high-return opportunities.

Now compare this to American Tower and SBA Communications. American Tower went global, adding complexity and currency risk for marginally higher growth. SBA remained a C-corp, paying full corporate taxes but maintaining more flexibility. Crown Castle chose the middle path: REIT efficiency, U.S. focus, operational simplicity.

The competitive positioning reveals itself in the numbers. Crown Castle trades at lower multiples than its peers despite having similar or better tower assets. Why? The fiber overhang. Once that's removed, Crown Castle becomes the only pure-play, publicly-traded U.S. tower company—a unique position that should command a premium, not a discount.

The operational leverage is staggering. When a carrier adds new equipment to an existing tower—say for 5G deployment—Crown Castle's costs increase by essentially zero. Maybe some additional electricity usage, perhaps some paperwork processing. But the revenue? That might jump by $2,000 per month. Multiply that across 40,000 towers, and you're talking about real money.

Ground lease management represents the one real operational challenge. Crown Castle doesn't own the land under many of its towers—they lease it. Managing thousands of ground leases, each with different terms, escalators, and renewal options, requires sophisticated systems and careful attention. One missed renewal could mean losing a tower generating hundreds of thousands in annual revenue.

The technology risk that keeps executives awake? It's not 5G or 6G—Crown Castle wins regardless of which G we're on. The real threat is satellite communications or some other technology that bypasses terrestrial infrastructure entirely. But physics is on Crown Castle's side. Radio waves propagating from space will never match the capacity and reliability of terrestrial networks for dense, high-bandwidth applications.

This is the business model Crown Castle should have stuck with—simple, profitable, defensible. Instead, they spent a decade and billions of dollars learning that sometimes the best strategy is to do one thing extraordinarily well rather than many things poorly.

XI. The 5G Future & Growth Prospects

The numbers paint a picture of unstoppable growth. It is projected that Western Europe will have the highest 5G subscription penetration in 2030 at 93 percent, followed closely by North America at 91 percent and the GCC at 90 percent. Looking ahead to 2028, projections indicate that North America's 5G connections will reach 669 million by 2028, with the broader picture showing the number of 5G subscribers at a global level is expected to reach 8 billion by 2028, up from the current 1.4 billion 5G connections.

For Crown Castle, now focused purely on towers, these projections aren't just statistics—they're a roadmap to revenue. Every new 5G subscription requires network capacity. Every gigabyte of data consumed needs to traverse infrastructure. And in the United States, that infrastructure overwhelmingly sits on Crown Castle's 40,000 towers.

Mobile network data traffic continues to grow, but with a declining year-on-year growth rate to 15 percent in 2030. This results in a CAGR of 17 percent over the full forecast period. Total global mobile data traffic – excluding traffic generated by Fixed Wireless Access (FWA) – is expected to grow by a factor of around 2.3 to reach 280 EB per month in 2030. Even with declining growth rates, we're talking about data volumes that would have seemed like science fiction a decade ago.

In 2025, Crown Castle is expecting organic growth of 4.5% in towers, excluding Sprint consolidation impact, with increased lease applications as carriers expand 5G networks. This might seem modest compared to the explosive growth projections, but remember: Crown Castle gets paid whether data grows 10% or 100%. Their contracts are for space and power, not gigabytes transmitted.

The network densification requirements for true 5G remain Crown Castle's ace in the hole. 5G's share of mobile data traffic reached 35 percent by the end of 2024. This share is forecast to grow to 80 percent in 2030. As 5G traffic dominates, carriers will need more equipment on more towers to handle the load. Physics hasn't changed—higher frequencies mean shorter range mean more infrastructure.

Fixed wireless access represents a particularly intriguing opportunity. The rapid network build-out has enabled 5G smartphone subscriptions to grow faster than any previous generation. Today, 59 percent of North American smartphone subscriptions are 5G. With 5G, service providers have been able to turn the declining revenues per subscriber that characterized 4G into growth. FWA turns wireless networks into home broadband competitors, driving even more infrastructure demand.

Edge computing and new use cases multiply the opportunity. Autonomous vehicles, augmented reality, industrial IoT—each requires ultra-low latency that only comes from computing at the edge of the network. And where does edge computing equipment live? On towers, of course. Crown Castle's vertical real estate becomes even more valuable as it hosts not just radios but servers.

But let's acknowledge the competitive threats. Satellite constellations like Starlink promise ubiquitous coverage without terrestrial infrastructure. The technology is impressive, the execution remarkable. But physics remains stubborn. Satellite latency will always exceed terrestrial. Capacity constraints are real. Urban density makes satellite uneconomical. Crown Castle's towers aren't being replaced—they're being complemented.

The technological disruption risks are real but manageable. Could some breakthrough technology obsolete towers? Perhaps. But every generation has predicted the death of towers, and every generation has needed more of them. 2G was supposed to cover everything with a few sites. 3G required densification. 4G required even more. 5G needs density that would have seemed absurd in the 1G era.

Omdia principal analyst Kristin Paulin points out, "With this forecast, 5G will reach the global milestone of accounting for more than half of all connections by 2028. For North America, as an early leader, 5G will be more than 80% of connections." Additionally, 5G data traffic is expected to be 76% of all technology data traffic as it reaches a staggering 2.6 billion TB (or 2600 EB), with all technology data traffic reaching 3.4 billion TB (or 3400 EB) by 2028.

The real question isn't whether Crown Castle will benefit from 5G growth—it's whether they can execute operationally to capture the opportunity. Without the distraction of fiber, with a simplified business model, with management focused on one thing, the answer should be yes. The infrastructure is in place, the contracts are signed, the growth is coming. All Crown Castle has to do is not screw it up.

XII. Playbook: Lessons from Crown Castle

The Crown Castle saga offers a masterclass in both strategic success and catastrophic failure. The lessons are worth billions—literally, in Crown Castle's case—and apply far beyond telecommunications infrastructure.

Lesson 1: Infrastructure Monopolies Are Beautiful Until You Try to Be Something Else

Crown Castle's tower business is a textbook infrastructure monopoly. High barriers to entry (try getting zoning approval for a new tower in Manhattan), network effects (each additional tenant makes the tower more valuable), and switching costs that border on prohibitive. These dynamics created a business that printed money with 90%+ incremental margins.

The mistake was thinking these advantages were transferable. Fiber is infrastructure, but it's not monopolistic infrastructure. Multiple providers can serve the same building. Switching costs exist but are manageable. The network effects are weak. Crown Castle tried to apply tower economics to fiber and discovered that physics and economics are different disciplines.

Lesson 2: The Challenge of Diversification in Focused Businesses

Every focused company eventually faces the diversification temptation. You've dominated your niche, growth is slowing, and adjacent markets look attractive. The board pushes for growth. Analysts want a growth story. Management wants new challenges. The logic seems impeccable: leverage your existing relationships, capture synergies, become a one-stop shop.

Crown Castle fell into this trap perfectly. They had relationships with every major carrier. They understood infrastructure. Fiber and small cells seemed like natural extensions. But they missed the crucial insight: sometimes the capabilities that make you successful in one business make you terrible at another. Tower operations require patience and capital discipline. Fiber requires speed and operational excellence. These are not the same skill set.

Lesson 3: REIT Structure Creates Its Own Destiny

The REIT conversion that seemed so clever in 2014 became a straightjacket by 2020. REITs must distribute 90% of taxable income, leaving little room for error in capital allocation. When your mistakes are immediately visible in reduced dividends, there's nowhere to hide.

But the REIT structure also saved Crown Castle from even worse outcomes. Without the dividend requirement, management might have doubled down on fiber, acquiring more assets at higher prices. The REIT rules forced a reckoning that a traditional C-corp might have delayed for years. Sometimes constraints are features, not bugs.

Lesson 4: Capital Allocation in Capital-Intensive Businesses

Crown Castle's fiber adventure cost shareholders over $10 billion in destroyed value. But the real lesson isn't about fiber—it's about capital allocation in capital-intensive businesses. When every decision involves billions of dollars and decade-long commitments, mistakes compound catastrophically.

The key insight: in capital-intensive businesses, the cost of capital is everything. Crown Castle's tower business had a cost of capital around 5-6%. The fiber business, being riskier and more competitive, probably had a true cost of capital closer to 10-12%. When you invest $15 billion at a 10% hurdle rate but earn 5% returns, you destroy $750 million in value annually. Do that for a decade, and you've destroyed a generation of shareholder wealth.

Lesson 5: When Activists Are Right (and Wrong)

Elliott Management was right about everything that mattered: the fiber strategy was destroying value, management incentives were misaligned, the board lacked oversight. But being right isn't enough in activism. You need a mechanism to force change, and Elliott found it in the ROIC metrics that laid bare the fiber disaster.

The lesson for companies: when activists show up with detailed financial analysis and specific criticisms, dismissing them as short-term focused is dangerous. Elliott held Crown Castle stock for over five years—hardly a short-term play. They understood the business better than management did. Sometimes the outsiders see more clearly than insiders.

Lesson 6: The Importance of Focus vs. Synergies Debate

The synergy trap catches smart companies constantly. Crown Castle's logic for fiber seemed impeccable: towers need fiber backhaul, small cells need fiber connections, we already have the carrier relationships. Synergies everywhere! But synergies are often mirages that disappear when you get close.

The reality: operational focus beats theoretical synergies almost every time. American Tower stayed focused on towers and traded at premium multiples. SBA Communications remained even more focused and generated superior returns. Crown Castle chased synergies and destroyed billions in value. In business, doing one thing extraordinarily well beats doing multiple things adequately.

The Meta-Lesson: Simple Businesses Are Underrated

Perhaps the biggest lesson from Crown Castle is the most obvious: simple businesses that generate predictable cash flows are incredibly valuable, and making them complex usually destroys that value. Crown Castle had built one of the great infrastructure businesses in American capitalism—40,000 towers generating rivers of cash flow with minimal maintenance.

They threw it away chasing growth, chasing complexity, chasing the approval of analysts who would forget their Buy ratings the moment the stock crashed. The boring business of owning vertical real estate and renting it to creditworthy tenants was beautiful in its simplicity. The exciting business of building the infrastructure for 5G was a disaster in its complexity.

In the end, Crown Castle's journey from Pittsburgh startup to fiber debacle to pure-play pivot teaches us that in business, as in life, knowing what you're good at—and sticking to it—is worth more than all the strategic visions and synergy slides in the world. Sometimes the best strategy is not to have a strategy at all, just a very good business that you don't screw up.

XIII. Bear vs. Bull Case Analysis

Bull Case: The Infrastructure Monopoly Thesis

Crown Castle bulls see a company that just shed $8.5 billion worth of problems and emerged as the only pure-play U.S. tower company. Start with the irreplaceable infrastructure assets—40,000 towers in the best locations across America. These aren't just steel structures; they're permitted, powered, connected monopolies in their micro-geographies. Try building a new tower in San Francisco or Manhattan. The permits alone would take years, if you could get them at all.

The secular growth in mobile data demand is inexorable. Every new iPhone is more capable than the last. Every app uses more data. Every consumer expects faster speeds. Mobile network data traffic continues to grow, but with a declining year-on-year growth rate to 15 percent in 2030. This results in a CAGR of 17 percent over the full forecast period. Total global mobile data traffic is expected to grow by a factor of around 2.3 to reach 280 EB per month in 2030. Even slowing growth rates mean massive absolute increases in data consumption.

The operating leverage from additional tenants remains the killer app of the tower business model. That 96% incremental margin when adding new tenants isn't theoretical—it's proven over decades. With average tenancy at just 2.2 per tower and capacity for 4+, there's enormous room for growth without incremental capital.

The simplified pure-play story post-fiber sale could trigger a re-rating. Without the complexity and capital drain of fiber, Crown Castle becomes easy to understand, easy to model, easy to value. The company estimates saving $200 million annually in operating expenses just from not running the fiber business. That's pure margin expansion.

The 5G densification tailwinds are still in the early innings. Despite all the 5G hype, we're maybe 30% through the deployment cycle. C-Band equipment is still being deployed. Millimeter wave is barely started. Each new spectrum band means new equipment on towers, new amendments to contracts, new revenue streams. Crown Castle doesn't need to win the 5G race—they win regardless of who's running.

Bear Case: The Structural Challenges Thesis

Crown Castle bears point to customer concentration risk that's only getting worse. Three customers—AT&T, Verizon, and T-Mobile—represent roughly 75% of revenue after the Sprint consolidation. These aren't just customers; they're oligopolists with increasing negotiating power. When T-Mobile merged with Sprint, Crown Castle lost hundreds of millions in annual revenue from decommissioned sites. The next merger could be even worse.

Technological disruption isn't science fiction anymore. Starlink has over 2 million subscribers and growing. Amazon's Kuiper is coming. These aren't replacing towers tomorrow, but they're pressure on pricing. More importantly, they provide carriers with negotiating leverage: "Lower our rates or we'll explore satellite options for rural coverage."

Rising interest rate sensitivity hits REITs particularly hard. Crown Castle must distribute 90% of taxable income, leaving little cushion for refinancing debt in a higher-rate environment. With billions in debt and rates potentially staying higher for longer, interest expense could consume an increasingly large share of cash flow.

The loss of fiber synergies might prove more painful than expected. Fiber backhaul to towers was a real synergy, even if small cells weren't. Now Crown Castle will pay market rates for fiber connections to its towers. That's a permanent increase in operating costs that bulls are underestimating.

Competition from other tower operators remains fierce. American Tower has global scale and diversification. SBA has operational excellence and lower costs. Crown Castle is stuck in the middle—not the biggest, not the most efficient, not the most diversified. In commodity businesses, being average is dangerous.

The Balanced View: Probability-Weighted Outcomes

The truth likely lies between these extremes. Crown Castle is neither the monopolistic cash machine bulls envision nor the structurally challenged dinosaur bears fear. It's a good business that made bad decisions, now trying to return to being just a good business.

The bull case probably has a 60% probability. The assets are real, the demand is real, the cash flows are real. Post-fiber sale, Crown Castle will be simpler, more focused, more profitable. The stock will likely re-rate higher as the complexity discount disappears.

The bear case has perhaps a 30% probability of a serious structural challenge emerging. A major carrier bankruptcy, a technological disruption, a catastrophic merger—any could seriously impair Crown Castle's value. These are low-probability but high-impact risks.

The remaining 10% is the tail risk—either extremely positive (a new use case drives massive densification) or extremely negative (the U.S. government nationalizes wireless infrastructure). These are the black swans that make or break fortunes.

For investors, the key question isn't whether Crown Castle is good or bad—it's whether it's better or worse than priced. At current valuations, reflecting the fiber disaster and management turmoil, the risk-reward may finally be attractive. The company doesn't need to be great; it just needs to be boring. And boring, as Crown Castle has learned the hard way, can be beautiful.

XIV. Links & References

Primary Sources: - Crown Castle Investor Relations (investor.crowncastle.com) - SEC EDGAR Database - Crown Castle Filings - Crown Castle Annual Reports (2014-2024) - Crown Castle Quarterly Earnings Transcripts

Industry Analysis: - CTIA Annual Wireless Industry Survey - Ericsson Mobility Report (Quarterly) - 5G Americas White Papers - FCC Spectrum Auction Database - American Tower Corporation Investor Materials - SBA Communications Investor Presentations

Activist & Strategic Review Documentation: - Elliott Management "Reclaiming the Crown" Presentation (July 2020) - Elliott Management "Restoring the Castle" Materials (November 2023) - Crown Castle Fiber Review Committee Findings (December 2023) - Proxy Statements and Settlement Agreements

Transaction Documents: - T-Mobile Tower Agreement SEC Filings (2012) - AT&T Tower Agreement SEC Filings (2013) - NextG Networks Acquisition Documents (2011) - Lightower Acquisition Filings (2017) - Fiber Segment Sale Agreement (2025)

Industry Research: - Mobile Experts Small Cell Market Reports - Dell'Oro Group RAN Market Analysis - Fierce Wireless Tower Industry Coverage - Light Reading Infrastructure Analysis - RCR Wireless 5G Deployment Tracking

Financial Analysis: - Wells Fargo Equity Research - Crown Castle Coverage - J.P. Morgan Tower Sector Analysis - Goldman Sachs REIT Research - KeyBanc Capital Markets Infrastructure Reports - Raymond James Communications Infrastructure Coverage

Regulatory & Spectrum: - FCC C-Band Auction 107 Results - FCC 5G FAST Plan Documentation - CTIA 5G Deployment Statistics - State and Local Small Cell Legislation Tracking - NEPA and Historic Preservation Tower Regulations

Technology & Market Forecasts: - Omdia 5G Subscription Forecasts - GSMA Intelligence Mobile Economy Reports - Statista Telecommunications Statistics - Strategy Analytics Network Infrastructure Forecasts - Kagan Wireless Infrastructure Market Sizing

XV. Recent News

Q1 2025 - Corporate Transformation: Crown Castle announced the definitive agreement to sell its Fiber segment to EQT and Zayo for $8.5 billion (March 13, 2025). The transaction marks the conclusion of the strategic review initiated in December 2023, positioning Crown Castle as the only pure-play publicly-traded U.S. tower company.

Leadership Transition: The company continues its CEO search following Steven Moskowitz's termination, with Daniel Schlanger serving as interim CEO. The board announced it is conducting a comprehensive search for a permanent chief executive to lead the simplified tower-focused company.

Dividend Policy Reset: Crown Castle announced a reduction in its annualized dividend to approximately $4.25 per share in Q2 2025, reflecting the new capital allocation framework focused on financial flexibility and shareholder returns through a combination of dividends and share buybacks.

Share Buyback Program: The board approved a $3.0 billion share repurchase program to be implemented following the closing of the fiber sale, representing approximately 7% of the company's market capitalization and signaling confidence in the pure-play tower strategy.

5G Deployment Acceleration: Major carriers continue aggressive 5G deployments, with tower amendment activity remaining robust. Crown Castle reported 4.5% organic tower growth excluding Sprint cancellations, indicating healthy underlying demand for tower infrastructure.

Competitive Dynamics: American Tower and SBA Communications reported strong quarterly results, validating the tower model's resilience. The sector continues to benefit from carrier network investments despite macroeconomic uncertainties.

Regulatory Developments: The FCC's latest initiatives to streamline infrastructure deployment continue to benefit tower operators, with reduced permitting times and simplified approval processes for 5G equipment modifications.

Technology Evolution: The emergence of Open RAN and network virtualization technologies is creating new opportunities for tower companies, potentially driving additional equipment deployments as carriers modernize networks.

Market Response: Following the fiber sale announcement, analyst upgrades highlighted the improved clarity and simplified investment thesis. The removal of the fiber segment's complexity and capital intensity is viewed positively by the investment community.

Industry Consolidation: Speculation continues about potential consolidation in the tower sector, though regulatory concerns make large-scale mergers unlikely. Crown Castle's pure-play status potentially makes it more attractive as either acquirer or target in future transactions.

The transformation of Crown Castle from a complex fiber-and-tower hybrid back to a focused tower operator represents one of the most significant strategic pivots in the telecommunications infrastructure sector, setting the stage for a simpler but potentially more profitable future.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube