Wintrust Financial: Chicago's Community Banking Empire

I. Introduction & Episode Roadmap

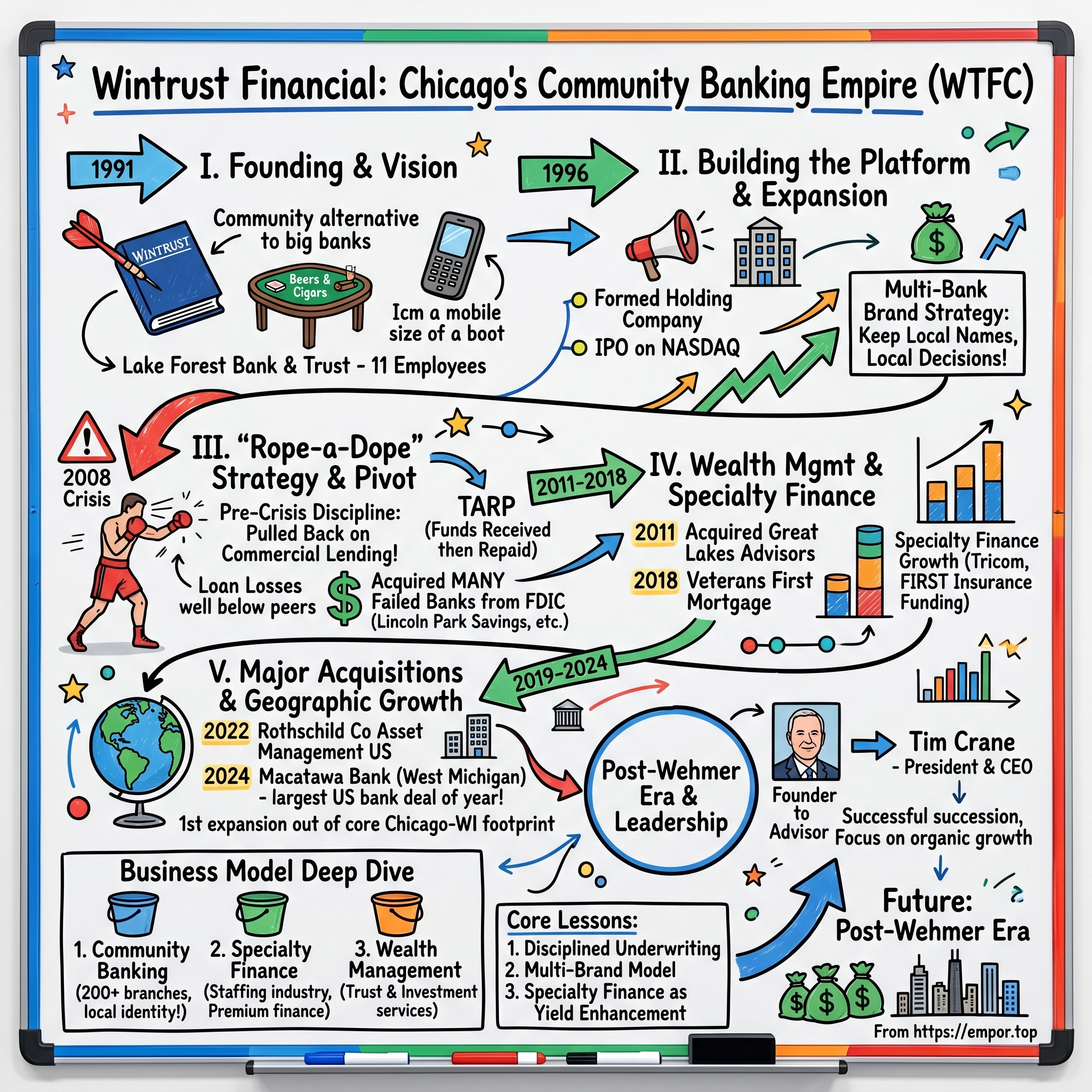

The fluorescent lights of a cramped 1,100-square-foot storefront flickered in Lake Forest, Illinois, one autumn morning in 1991. Ed Wehmer, a CPA-turned-banker with a mobile phone "the size of a boot," surveyed his new domain: eleven employees, not enough chairs, and a name chosen by throwing a dart at a book of English company names. The dart landed on "Wintrust."

Thirty-four years later, that dart throw has yielded something extraordinary: a $64.9 billion financial services enterprise that stands as the Midwest's most compelling example of contrarian community banking done right. Slowly and painstakingly, Wintrust Financial has grown to become the third largest bank in the six-county Chicago area when measured by deposits, with $49.5 billion in local deposits representing 8.6% of the market, trailing just Chase (20.1%) and BMO (18.3%).

This is the story of how a bank born over beers and cigars around a card table became Chicago's banking flag bearer—the rare hometown institution that survived every wave of consolidation that washed away Continental Illinois, Bank One, LaSalle Bank, Harris Bank, PrivateBancorp, MB Financial, and First Midwest into the hands of out-of-town acquirers.

Wintrust Financial Corp reported record net income of $695 million for 2024, marking an 11.5% increase from 2023. The company now operates sixteen community bank subsidiaries, with over 200 banking locations located in the greater Chicago, southern Wisconsin, west Michigan and southwest Florida markets.

The Wintrust story contains multitudes: a founding myth involving darts and cigars, a pre-crisis discipline that rivals Warren Buffett's "be fearful when others are greedy" maxim, an acquisition spree that gobbled up more failed banks than any competitor during the Great Recession, and a business model that defies the conventional wisdom about how banking empires are built.

The themes we'll explore run deep: the economics of community banking versus national scale, the counterintuitive strategy of retaining acquired bank brands rather than consolidating them, the art of disciplined underwriting through cycles, and the question of whether Wintrust's model can endure the post-Wehmer era.

II. Founding Story & Ed Wehmer's Vision (1991–1996)

The Card Table Genesis

In the affluent suburbs north of Chicago, where old money meets new ambition, Ed Wehmer gathered a small group of friends around a card table in the early 1990s. The agenda: beers, cigars, and the question of whether they could build a bank that served customers the way the big institutions no longer bothered to.

Ed Wehmer, along with a few friends, started Wintrust over a card table with some beers and cigars. The idea was to open a bank that would be the alternative to the big banks, and it became a reality in 1991 with the first Wintrust Community Bank location, Lake Forest Bank & Trust.

The name itself became corporate legend. When they got stuck trying to think up a name for the new bank they were starting in the early 1990s, Ed Wehmer and his friends decided to save themselves some time, money and hassle. Instead of holding focus groups and brainstorming sessions, they found a book of English company names, opened it up and threw a dart. It landed on the word Wintrust.

"Kids always ask how we came up with the name," says Ed. "Is it because we win people's trust? No, it's because we threw a dart at a book. We were kind of just knuckleheads messing around back then. But it turned out really well."

The physical reality was far humbler than the ambition. They started out with a 1,100-square-foot branch in a northern Chicago suburb called Lake Forest with 11 employees and not enough chairs. "The first day I showed up, I had nowhere to sit," Ed recalls.

The Accountant Who Built an Empire

Understanding Ed Wehmer requires understanding his unusual path to banking. He wasn't a lending officer who climbed the ranks at Continental Illinois or a trust fund scion who inherited a bank charter. He was an accountant who specialized in autopsies—financial autopsies of banks being bought and sold.

Banking has been the primary focus of Ed's career, beginning at the accounting firm Ernst & Young, LLP, where he specialized in the banking field focusing mainly in the area of bank mergers and acquisitions for seven years. After leaving Ernst & Young, Ed was Senior Vice President and Chief Financial Officer of Corus Bankshares, Inc. (formerly River Forest Bancorp), a $4 billion banking holding company in Chicago, Illinois from 1985 to 1991.

Those seven years at Ernst & Young coincided with a transformative period in American banking. "Right about then, Illinois and the US started changing their laws and allowing bank mergers to happen," he says. "So I figured out how to do bank mergers and ended up running it for the firm nationally. That was a lot of fun."

But the education came at a price. The job was hugely educational for Ed, but it also required working 13-hour days and rarely seeing his children. So he decided to start his own bank – one that would offer an alternative to the larger institutions with highly personal, community-focused service.

At his core, Ed is a family man. Along with providing customers with an alternative to the big banks, the impetus for starting a hometown bank was to spend time with his six children.

The leap required unusual confidence—or perhaps fear-driven motivation. "I said, what the heck? What's the worst thing that could happen? I'm going to start a bank. If it doesn't work I can always go back and be a CPA," he remembers.

Even though getting Wintrust off the ground was a lot of work, Ed got to see more of his kids and drive them to school every day. It was enormously rewarding, but just like when he was flying around the country speaking to boards of directors in his 20s, he was scared of failure. "Fear is a great motivator," he reveals.

The Community Banking Philosophy

Wehmer's background as a deal advisor gave him unusual insight into what destroyed banks and what preserved them. The discipline that would later define Wintrust was embedded from day one.

The company began with modest capital. The founders' vision wasn't to build a regional behemoth—at least not initially. It was to prove that community banking could survive the consolidation wave that was swallowing smaller institutions across America.

It turned out there was high demand in Chicago and the surrounding area for banking that put the customer first and made them feel truly taken care of.

What made Wehmer's approach distinctive was the multi-bank holding company structure he would later formalize. Rather than building a single monolithic brand, he envisioned a federation of community banks—each with local identity and local decision-making, but backed by shared infrastructure and capital.

This wasn't just philosophical preference. Wehmer's M&A experience had shown him that customers developed relationships with local banks, local bankers, local brands. When acquirers erased those identities, customers often left. The multi-brand strategy was designed to prevent that attrition.

III. Building the Platform: Early Expansion (1996–2007)

Going Public

By the mid-1990s, Wintrust had proven the concept. Multiple community banks were operating under the informal Wintrust umbrella. The question became: how to formalize the structure and access capital for continued growth?

In 1995, the team formed Wintrust Financial Corporation as a multi-bank holding company. In 1996, Wintrust completed its initial public offering on NASDAQ under ticker symbol WTFC. This provided capital for continued growth and expansion.

"We were at about a billion dollars when we went public and put all the banks together under one holding company," Ed shares. "Now we're pushing US$50 billion, one of the top 30 commercial banks in the country and growing like a weed."

The IPO timing proved fortuitous. 1996 was a boom year for public offerings, with over 800 companies going public. But Wintrust wasn't a dot-com speculative play—it was a profitable, growing community bank with a clear business model. The capital raised would fund what became a relentless expansion through de novo branches and acquisitions.

The Multi-Bank Brand Strategy

Unlike virtually every other U.S. bank pursuing scale, Wintrust made a strategic decision that would define its culture: each community bank uses the tagline, "A Wintrust Community Bank." But critically, the acquired and de novo banks retained their local names.

The logic was counterintuitive to conventional banking wisdom, which emphasized the cost savings from brand consolidation. But Wehmer understood something his competitors missed: in community banking, the brand is the relationship.

By the end of the decade, Wintrust had established a multi-bank holding company structure with several community banks operating under local brands but sharing back-office operations and technology infrastructure. This gave customers the best of both worlds: local identity and relationship banking, backed by the capital and technology of a larger organization.

Diversification into Specialty Finance

The 1999 acquisition of FIRST Insurance Funding marked a pivotal strategic shift. Wintrust wasn't content to be merely a community bank—it wanted to build specialty finance businesses that could generate higher yields and diversify revenue streams.

FIRST is one of the largest premium finance companies in North America and also Wintrust's oldest and largest niche-lending business. The division has more than 30 years in the premium financing industry.

The premium finance business proved to be a strategic masterpiece. Insurance premium financing—lending to businesses and individuals who need to finance their insurance premiums over time—generates attractive yields with modest credit risk (since the collateral is the insurance policy itself, which can be cancelled if payments stop).

FIRST has grown from $400 million in annual commercial property and casualty loan volume in 1997 to over $10 billion today.

Wintrust Life is the largest traditional life insurance premium finance lender in North America. Its lending programs enable high net worth clients and corporations to obtain life insurance while retaining assets for other investment opportunities.

In 2003, Wintrust acquired WestAmerica Mortgage Company, later renamed Wintrust Mortgage. This added residential mortgage origination to the business mix—a fee-generating business that would prove both blessing and curse depending on rate cycles and housing market conditions.

The Acquisition Playbook Takes Shape

By the early 2000s, Wintrust had developed a distinctive acquisition philosophy that would serve it well in the crisis years ahead. The company wasn't looking for distressed assets or forced sellers—it was looking for well-run community banks with good management teams that simply lacked the capital to grow.

The pitch to acquisition targets was compelling: keep your identity, keep your team, keep your customer relationships—but gain access to Wintrust's capital, technology, and product platform.

In 2004, Wintrust expanded its community banking franchises by adding a record fourteen new banking facilities in key Chicagoland markets and the southern Wisconsin markets of suburban Milwaukee and Madison—eight on a de novo basis and six by acquisition.

The growth was remarkable. Record growth was achieved in net income, net revenue, assets, deposits, and loans. Wintrust stock price increased 26% in 2004, on top of a 44% increase in 2003 and a 54% increase in 2002.

But even as competitors were reaching for growth at any cost during the mid-2000s housing boom, Wehmer was getting nervous. The deals weren't making sense anymore. Underwriting standards were slipping across the industry. Something was wrong.

IV. Key Inflection Point #1: The 2008 Financial Crisis—The "Rope-a-Dope" Strategy

Pre-Crisis Discipline

What separates legendary investors from ordinary ones often isn't what they do in good times—it's what they don't do. In 2006 and 2007, as the subprime mortgage machine roared and competitors gorged on questionable loans, Ed Wehmer made a decision that would define Wintrust's future.

Wintrust was far better prepared to weather the housing bust than most banks as Wehmer had pulled back on commercial lending in the year or two before the financial crisis in 2008. That left far fewer bad loans to work out and write off. Wintrust's loan losses ended up well below most Chicago commercial banks, and it was equipped to lend actively before most of its competitors.

Wehmer borrowed a boxing metaphor to describe his strategy. He called it his "rope-a-dope" strategy, after Muhammad Ali's famous strategy of dodging his opponent's flailing punches and tiring him out before going on offense.

"So I went into what I call rope-a-dope," Ed says, referring to a strategy in boxing where you allow your opponent to tire themselves out by going against the ropes and blocking their punches.

This wasn't passive defense. It was active restraint that required telling shareholders and employees that Wintrust was walking away from deals that competitors were winning. In a business that rewards volume, saying "no" required unusual conviction.

The Crisis Environment

The restraint proved prescient. The 2008 financial crisis led to many bank failures in the United States. The Federal Deposit Insurance Corporation (FDIC) closed 465 failed banks from 2008 to 2012. In contrast, in the five years prior to 2008, only 10 banks failed.

A majority of the community banks that became problem banks or failed during 2008 had similar risk profiles. These banks often had extremely high concentrations, relative to their capital, in residential acquisition, development, and construction lending. Loan underwriting and credit administration functions at these institutions typically were criticized by examiners. Frequently these institutions had exhibited rapid asset growth funded with brokered deposits.

Wintrust had avoided all of these traps. No outsized construction lending concentrations. No brokered deposit dependency. No deteriorating underwriting standards.

"So in 2008 when it all went down, we put the pedal to the metal – healthy as a horse. We had record years during the downturn and bought more failed banks than anybody in the country."

TARP and the Strategic Pivot

Wintrust was among the recipients of capital from the United States government through the U.S. Treasury's Troubled Asset Relief Program. The bank used the 2008 financial crisis to acquire small troubled banks in the Chicago area, backed by its pre-crisis capital supplemented by TARP funds. This positioned it to become one of the area's largest retail banks by eliminating costs and deepening its geographical footprint in the area.

The TARP participation was controversial for Wintrust. Unlike many TARP recipients that needed the funds to survive, Wintrust was genuinely healthy. "CEO Edward Wehmer hopes that happens for Wintrust, which remained profitable through the economic crisis as many rivals spewed red ink. 'Things holding our stock back were the TARP overhang, and we kept getting lumped in with the rest of the Chicago market,' Mr. Wehmer says."

Pressure built on Chicago's mid-sized commercial banks to repay federal bailout money. Moving first was Lake Forest-based Wintrust Financial Corp., which raised $328 million in a stock offering and then redeemed $250 million in preferred shares held by the federal government.

The FDIC Acquisition Spree

The real strategic opportunity wasn't TARP—it was failed bank acquisitions. Under a shared loss agreement, FDIC absorbs a portion of the loss on specified assets of a failed bank that are purchased by an acquiring bank. FDIC officials, state bank regulators, community banking associations, and acquiring banks of failed institutions said that shared loss agreements helped to attract potential bidders for failed banks during the financial crisis. Bank officials that acquired failed banks confirmed that they would not have purchased them without FDIC's shared loss agreements because of uncertainty of the market and valuation of assets.

During 2008-2011, FDIC resolved 281 of 414 failures using shared loss agreements on assets purchased by the acquiring bank.

Wintrust was uniquely positioned to bid on these failed institutions. It had the capital, it had the local presence, it had the management capacity, and crucially, it had relationships with the FDIC from Wehmer's M&A background.

The 2009 acquisition of certain assets and deposits of failed banks from FDIC, including Lincoln Park Savings Bank, exemplified the strategy. Each failed bank acquisition brought deposits, branches, and customer relationships at attractive prices—with the FDIC absorbing much of the credit risk.

Wintrust hired some of the city's best-known business bankers like John McKinnon, who had run middle-market banking at Bank One and, before that, American National Bank & Trust, and scooped up customers of JPMorgan Chase and Bank of America, the acquirers of Bank One and LaSalle Bank. He also bought dozens of small banks—some after regulators closed them, others struggling—expanding Wintrust to communities throughout the area as well as the city itself.

The crisis that destroyed competitors became the foundation for Wintrust's transformation into a regional powerhouse. This wasn't luck—it was the payoff from years of disciplined restraint when restraint was unfashionable.

V. Key Inflection Point #2: Wealth Management & Specialty Finance Expansion (2011–2018)

Building the Wealth Management Arm

With the community banking franchise solidified, Wintrust turned attention to building higher-margin fee businesses. In 2011, Wintrust acquired Great Lakes Advisors, expanding wealth management capabilities.

The wealth management segment provides trust and investment services, tax-deferred like-kind exchange services, asset management, and securities brokerage services. The acquisition of Great Lakes Advisors gave Wintrust institutional asset management capabilities to complement its private client trust business.

The strategic logic was compelling. Wealth management generates fee income that doesn't depend on interest rate spreads. It deepens customer relationships. And it leverages the community banking franchise—affluent customers of Wintrust's suburban banks often needed sophisticated wealth planning.

Wintrust invested aggressively to expand the wealth management side of its business. In 2004 and early 2005, the company had added Wayne Hummer Financial Advisors to Wintrust banking offices with Wayne Hummer Wealth Management representatives in fifteen facilities in Illinois and Wisconsin.

Continued Bank Acquisitions

The bank acquisition machine continued to run through the post-crisis recovery. In 2012, Wintrust acquired HPK Financial Corporation, parent company of Hyde Park Bank—bringing Wintrust into the heart of Chicago's South Side and connecting it to the University of Chicago community. In 2013, Wintrust acquired Diamond Bancorp, Inc. and its subsidiary Diamond Bank.

Each acquisition followed the same playbook: preserve the local brand, retain key employees, integrate back-office operations, and cross-sell Wintrust's broader product platform.

In 2015 Wintrust began to expand into equipment financing, both directly through its bank branches and indirectly through dealers. This added yet another specialty finance capability to the growing product portfolio.

Specialty Finance Growth Engine

The specialty finance segment became an increasingly important profit contributor. For the years ended December 31, 2017, 2016 and 2015, the specialty finance segment had net revenues of $179 million, $148 million and $119 million, respectively, and net income of $66 million, $49 million and $42 million, respectively. The specialty finance segment had total assets of $4.5 billion, $3.9 billion and $3.1 billion. The specialty finance segment accounted for 15% of consolidated net revenues for 2017.

Through wholly-owned subsidiary Tricom, Wintrust provides high-yielding, short-term accounts receivable financing and value-added, outsourced administrative services, such as data processing of payrolls, billing and cash management services to the temporary staffing industry. In 2017, Tricom processed payrolls with associated client billings of approximately $686 million.

Mortgage Business Expansion

In 2018, Wintrust completed its acquisition of Veterans First Mortgage, a Utah-based corporation with approximately 400 employees. This significantly expanded Wintrust's mortgage origination capabilities beyond the Midwest footprint.

The mortgage business presents both opportunity and risk. Origination volumes swing dramatically with interest rate cycles, and the business has significant operating leverage. But for a community bank seeking fee income diversification, mortgage banking provides a valuable complement to traditional spread lending.

VI. Key Inflection Point #3: Rothschild Acquisition & Geographic Expansion (2019–2024)

Continued Tuck-In Acquisitions

The late 2010s saw Wintrust continue its methodical expansion through smaller acquisitions. In May 2019, Wintrust acquired Rush-Oak Corporation, the parent company of Oak Bank, an Illinois state-chartered bank which had approximately $201 million in assets. In October 2019, Wintrust acquired STC Bancshares Corp, the parent company of STC Capital Bank, an Illinois state-chartered bank with approximately $275 million in assets.

These weren't needle-moving deals—they were community bank acquisitions that filled geographic gaps and added deposits at reasonable prices. The Wintrust playbook remained consistent: buy well-run banks, preserve local identity, integrate operations.

The Rothschild Deal

In November 2022, Wintrust announced a deal that signaled serious ambitions in wealth management. Wintrust's subsidiary, Great Lakes Advisors, LLC, agreed to purchase Rothschild Co Asset Management US Inc. and Rothschild Co Risk Based Investments LLC (collectively, "Rothschild Co Asset Management U.S."), investment managers with approximately $8 billion in assets under management specializing in equity investment strategies for institutional, intermediary and other clients.

The Rothschild name carries weight in global finance—the family has been at the center of European banking for over 200 years. While this was merely the U.S. asset management unit rather than the storied European operations, the acquisition still represented a meaningful step-up in sophistication for Wintrust's wealth platform.

The deal will add $8 billion in assets under management to the Rosemont-based bank's wealth-management arm and make it a top 20 Chicago-area asset manager.

The pending acquisition will add about $8 billion in assets under management to Wintrust-owned Great Lakes Advisors, bringing Great Lakes' assets to about $18.5 billion. Overall, Wintrust's wealth-management unit will have more than $40 billion under management after the deal closes.

Rothschild & Co completed the sale of its North American Asset Management units to Wintrust Financial Corporation further to the agreement first announced on 14 November 2022. The deal closed in early 2023.

The Macatawa Merger—West Michigan Expansion

The most significant strategic move of recent years came in 2024. Wintrust Financial Corporation and Macatawa Bank Corporation jointly announced that they have entered into a definitive merger agreement for Wintrust to acquire Macatawa in an all-stock transaction.

Macatawa is the parent company of Macatawa Bank, a Michigan state-chartered bank, which is headquartered in Holland, Michigan and operates a network of 26 full-service branches located throughout communities in Kent, Ottawa and northern Allegan counties, including Grand Rapids. Founded in 1997, Macatawa has an exemplary history of serving its communities. As of December 31, 2023, it had approximately $2.7 billion in assets, $2.4 billion in deposits and $1.3 billion in loans.

Subject to possible adjustment as provided in the merger agreement, the aggregate purchase price to Macatawa shareholders was estimated to be approximately $510.3 million, or $14.85 per share.

With a deal value of $512.4 million at announcement, the transaction is the largest US bank deal announced so far this year and the fifth-largest among the bank deals announced since 2022.

On August 1, 2024, Wintrust and Macatawa jointly announced the completion of their previously announced merger whereby Wintrust acquired Macatawa in an all-stock transaction.

The deal represented Wintrust's first significant geographic expansion outside its core Chicago-Wisconsin footprint. "Macatawa Bank provides an ideal platform to expand into West Michigan with a very solid bank. The bank has a strong core deposit base, exceptional asset quality, a client focused culture, and a committed leadership team. Together, we will be a formidable, community-minded competitor to the other banks in the area."

Critically, Wintrust applied its standard playbook: "Wintrust provides Macatawa Bank with the ability to retain and enhance its uniquely personalized consumer and commercial community presence in the West Michigan area by retaining the Macatawa Bank name, its key employees, branches, and a legally constituted community bank board, as a separately chartered bank and the only Wintrust subsidiary bank located within the State of Michigan."

VII. Leadership Transition: The Post-Wehmer Era (2020–2025)

The End of an Era

Every founder-led company must eventually face the succession question. For Wintrust, after more than three decades of Ed Wehmer's leadership, that moment arrived in January 2023.

Wintrust Financial Corporation announced the planned transition of the Chief Executive Officer role. Effective May 1, 2023, Timothy S. Crane, who currently served as Wintrust's President, would assume the additional role of Chief Executive Officer. Crane also was appointed to the Wintrust Board of Directors effective immediately. To ensure a smooth leadership transition, Edward J. Wehmer continued to serve as Founder and Chief Executive Officer of Wintrust through April 30, 2023.

Mr. Wehmer, a founder of the Company, has served as Founder and Senior Advisor since May 2023. Prior to May 2023, Mr. Wehmer served as Founder and Chief Executive Officer since February 2020. He also served as President and Chief Executive Officer of the Company from May 1998 to February 2020.

As he prepares to hand Wintrust Financial's CEO job to Tim Crane, Edward Wehmer leaves the executive ranks as few others who've built major Chicago banking institutions have—without selling to an out-of-town acquirer. With well over $50 billion in assets and a status as the fourth-largest bank in the region by deposits, Rosemont-based Wintrust is Chicago's last remaining locally based commercial bank of size.

Tim Crane Takes the Helm

His 40-year banking career has touched all facets of retail, commercial, and wealth banking. Tim joined Wintrust in 2008. During his nearly 16-year career at Wintrust, he has been responsible for a banking business that has grown by over $50 billion in assets.

Crane's background is instructive. He previously worked at Harris Bank / Bank of Montreal U.S. as a President. Tim Crane attended the University of Chicago. Unlike Wehmer the accountant-founder, Crane is a career banker who worked his way through major institutions before joining Wintrust.

Crane served as President of the Company since February 2020, after previously holding the title of Executive Vice President, Senior Market Head and Treasurer since February 2017, during which time he was responsible for oversight of Wintrust's subsidiary banks, banking operations and treasury.

The transition was carefully orchestrated. H. Patrick Hackett Jr., the company's chairman, said the announcement was part of a "rigorous multi-year succession planning process" that the board and Wehmer developed.

Wehmer's Final Exit from the Board

In 2025, the final chapter of Wehmer's active involvement concluded. On April 3, 2025, Wintrust announced Edward J. Wehmer and Scott K. Heitmann would conclude their long-time service as members of the Board of Directors at the Annual Meeting of Shareholders held May 22, 2025.

Wehmer opened the first Wintrust Community Bank location in 1991 when he launched Lake Forest Bank & Trust. He has served on the Board since the initial formation of Wintrust as a public company in 1996 and was President and Chief Executive Officer until May 2023.

At that time, under the previously announced transition plan, Tim Crane was appointed President and Chief Executive Officer and Wehmer transitioned to Executive Chairman, a role he held until May 2024, as well as Founder and Senior Advisor, a role he continues to hold. He will be appointed Chairman Emeritus following the 2025 Annual Meeting.

"Wintrust is coming off its best year ever," Wehmer said. "The future for our company is bright. I will very much continue to be a resource and a sounding board for Tim and the management team in my role as Founder and Senior Advisor of the company."

Strategic Refinancing Signals Focus on Organic Growth

An interesting development is Wintrust's successful May 2025 refinancing, raising US$415 million to redeem preferred securities and reinforcing its focus on organic growth and financial stability.

In May 2025, Wintrust completed a strategic refinancing move that demonstrated management's proactive approach to capital management. The company raised $415 million through a 7.875% fixed-to-floating preferred offering, using these funds to redeem $125 million in Series D preferred securities and $288 million in Series E preferred securities, both of which were scheduled to reprice to higher floating rates on July 15, 2025.

The refinancing demonstrated that under Crane's leadership, Wintrust maintains the financial discipline that defined Wehmer's tenure while continuing to optimize the capital structure.

VIII. Business Model Deep Dive

Three-Segment Structure

Wintrust operates through three distinct segments that together create a diversified financial services platform:

Community Banking offers non-interest-bearing deposits, non-brokered interest-bearing transaction accounts, and savings and domestic time deposits; home equity, consumer, and real estate loans; safe deposit facilities; and automatic teller machine, online and mobile banking services. This segment also engages in retail origination of residential mortgages; provision of lending, deposits, and treasury management services to condominium, homeowner, and community associations; and asset-based lending for middle-market companies.

Specialty Finance offers commercial and life insurance premiums financing for businesses and individuals; accounts receivable financing, value-added, and out-sourced administrative services, including data processing of payrolls, billing, and cash management services to temporary staffing industry; other specialty finance services; equipment financing through structured loan and lease products; and property and casualty insurance premium financing.

Wealth Management provides trust and investment services, tax-deferred like-kind exchange services, asset management, and securities brokerage services.

The Community Bank Brand Strategy

The strategic decision to retain acquired bank identities remains central to Wintrust's model. Wintrust is the second largest banking company in Chicago. The company provides traditional retail and commercial banking services, as well as wealth management services, commercial and life insurance premium financing, and certain treasury management services such as data processing of payrolls and billings.

The community-banking model gives Wintrust a strong local presence and deep understanding of the markets it serves. This allows them to build strong relationships with customers and compete effectively against larger national banks.

Currently, Wintrust operates more than 200 retail banking locations through 16 community bank subsidiaries in the greater Chicago, southern Wisconsin, west Michigan, northwest Indiana, and southwest Florida market areas.

Each subsidiary bank maintains its own charter, its own board of directors, and its own local identity. Lake Forest Bank & Trust serves affluent North Shore suburbs. Hyde Park Bank serves the University of Chicago community. The various suburban banks serve their respective communities with bankers who live and work in those areas.

Loan Portfolio Composition

Wintrust's loan portfolio reflects its commercial banking orientation. The loan portfolio is heavily weighted towards commercial loans, which constitute around 60% of total loans. Within this segment, commercial real estate (CRE) loans represent only about a third, while the remainder comprises high-quality, high-yielding loans, such as insurance premium financing.

This composition matters because it demonstrates Wintrust's disciplined approach to concentration risk. Many community banks that failed during the 2008 crisis had excessive concentrations in residential construction and development lending. Wintrust avoided that trap and continues to maintain diversified exposures.

The specialty finance contribution is particularly significant. Premium finance loans generate attractive yields with low credit losses—the collateral structure (insurance policies that can be cancelled) provides strong protection.

Geographic Footprint Evolution

Nearly three-quarters of Wintrust's branches are in northern Illinois, but the bank has a significant presence in Wisconsin and Michigan too. "We like the Midwest," Crane said. "We think there's a place for community banking," he added. "We don't think you have to sacrifice capabilities and sophistication" while remaining high-touch.

The Macatawa acquisition marked Wintrust's entry into Michigan, demonstrating willingness to expand geographically when the right opportunity presents itself. The southwest Florida reference in recent company descriptions suggests further geographic diversification may be underway.

IX. Playbook: Business & Investing Lessons

Lesson 1: Disciplined Underwriting Through Cycles

The "rope-a-dope" strategy represents the core lesson of the Wintrust story. Wehmer's willingness to miss opportunities rather than compromise standards during the 2005-2007 bubble period enabled the crisis-era acquisition spree that transformed the company.

This requires unusual institutional discipline. Most banks are managed to maximize near-term earnings. Loan officers are compensated on production. Boards pressure management for growth. Walking away from deals that competitors are winning—in real time, before the crisis proves you right—requires conviction that few management teams possess.

For investors, this suggests focusing on banks that maintain underwriting discipline even when it costs them market share. The banks that look "slow" during boom times often become the acquirers during busts.

Lesson 2: The Multi-Brand Community Bank Model

Wintrust's diversified business model, with revenue streams from community banking, commercial banking, wealth management, and mortgage banking, reduces reliance on any single line of business and provides stability through cycles.

The multi-brand strategy defies conventional banking wisdom. Most acquirers consolidate brands to cut costs. Wintrust's approach accepts higher operating costs in exchange for preserved customer relationships and local market knowledge.

For this model to work, the shared services infrastructure must be efficient enough to offset the cost of maintaining multiple brands. Wintrust has demonstrated this is achievable, but it requires careful execution.

Lesson 3: Specialty Finance as Yield Enhancement

The premium finance and staffing industry receivables businesses provide yields that community banking alone cannot generate. These businesses require specialized expertise, but once established, they create durable competitive advantages.

FIRST Insurance Funding's growth from $400 million to $10 billion in annual volume demonstrates how these niches can scale. The key insight is that specialty finance businesses need not compete on price with national banks—they compete on service, speed, and relationship in markets that large banks overlook.

Porter's Five Forces Analysis

Threat of New Entrants (Low-Medium): Banking is heavily regulated, requiring charters, capital, and regulatory approval. However, digital-first banks and fintech lenders have reduced barriers in specific product categories.

Bargaining Power of Buyers (Medium): Commercial customers have significant negotiating power and can switch banks. Consumer deposits are stickier, especially when relationships are deep.

Bargaining Power of Suppliers (Low): Banks are capital providers rather than capital users. Deposit funding comes from many small depositors with limited individual power.

Threat of Substitutes (Medium-High): Alternative lending sources (private credit, direct lending), fintech payment solutions, and digital banks offer substitutes for traditional banking services.

Competitive Rivalry (High): The Chicago market includes large national banks with scale advantages and remaining community banks competing for the same customers.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: Wintrust's shared infrastructure across community banks provides scale benefits while maintaining local identity. Not as powerful as Chase's national scale, but meaningful within the regional market.

Network Effects: Limited direct network effects, though the multi-bank structure creates some internal network benefits.

Counter-Positioning: The multi-brand community bank model represents genuine counter-positioning against national banks that cannot credibly offer local identity and relationships. Large banks would face cannibalization if they tried to replicate Wintrust's approach.

Switching Costs: Commercial banking relationships create meaningful switching costs—treasury management systems, established credit facilities, and personal banker relationships.

Branding: The "Chicago's Bank" positioning creates emotional resonance in a city that has lost its major homegrown banks. This matters for customer acquisition and employee recruitment.

Cornered Resource: The collection of community bank brands, local relationships, and specialty finance businesses represents a bundle of resources that would be difficult for competitors to assemble.

Process Power: The acquisition integration playbook—preserving local identity while consolidating operations—represents accumulated expertise that creates execution advantages.

X. The Bull Case

Wintrust enters the post-Wehmer era with several compelling attributes:

Market Position: Wintrust in the past year leapfrogged Bank of America, the longtime No. 3 in the Chicago market. In an era in which Chicago's sputtering economy has been an unfortunate storyline, the emergence of Wintrust as a major player on the local banking scene counts as some sorely needed good news.

"There's a lot of share left for us to get," Crane said. The Chicago market remains large enough to support significant continued growth without geographic expansion.

Financial Performance: Wintrust Financial Corporation reported a strong financial performance for the year ended December 31, 2024, with net income rising to $695 million, or $10.31 per diluted share, up from $622.6 million in 2023.

The company's pre-tax, pre-provision income reached a record $1.0 billion for the year, enhancing its financial stability and growth potential.

Organic Growth: The company recorded $1 billion of loan growth and $1.1 billion of deposit growth in Q4 2024. This growth, at an annualized rate of 8% for loans and 9% for deposits, was supported by the company's differentiated business model and strong client relationships.

Credit Quality: Non-performing loans as a percentage of total loans decreased to 36 basis points, with charge-offs down to 13 basis points. The improvement in credit quality was attributed to enhanced underwriting, tighter loan structures, and proactive management of stressed portfolios.

Analyst Sentiment: Wintrust's financial outlook appears robust based on analyst projections. The company is expected to maintain respectable profitability metrics, with returns on assets (ROA) projected between 1.1% and 1.3%, while returns on tangible common equity (ROTCE) are anticipated to range from 13% to 14%. For the fourth quarter of 2025, earnings per share (EPS) estimates stand at approximately $2.90.

XI. The Bear Case

Several risks warrant consideration:

Interest Rate Sensitivity: Net interest margin remained flat at 3.49%, indicating potential challenges in maintaining profitability amid changing interest rates. A prolonged low-rate environment would compress spreads.

Competitive Pressure: There is increased competitive pressure in the market, particularly in the commercial real estate sector, affecting pricing and structure.

Commercial Real Estate Exposure: The company faces challenges from a prolonged higher interest rate environment, particularly affecting commercial real estate valuations. CRE stress has already impacted regional banks nationally, and continued pressure could affect credit quality.

Scale Disadvantages: Wintrust competes against national banks with significantly greater technology spending capacity. Digital banking capabilities increasingly matter for customer acquisition.

Post-Founder Risk: The transition from a founder-led organization always carries execution risk. Wehmer's relationships, judgment, and institutional knowledge cannot be fully transferred.

Geographic Concentration: Despite the Macatawa acquisition, Wintrust remains heavily concentrated in Chicagoland, which exposes it to regional economic conditions.

XII. Key Metrics to Track

For investors following Wintrust, three KPIs deserve particular attention:

1. Net Interest Margin (NIM): As a spread lender, NIM drives core profitability. Watch for compression in declining rate environments or expansion during rate rises. The 3.49% figure for Q4 2024 provides the current baseline.

2. Organic Loan Growth: Distinguishing organic growth from acquisition-driven growth reveals the health of the underlying franchise. The 8% annualized loan growth in Q4 2024 demonstrates strong organic momentum.

3. Credit Quality Metrics (NPLs/Charge-offs): Given Wintrust's historical discipline around credit, any deterioration in non-performing loans or charge-off rates would warrant attention. The 36 basis point NPL ratio and 13 basis point charge-off rate represent excellent current performance.

XIII. Conclusion: The Dart That Won Trust

When Jamie Dimon sold Bank One to New York's JPMorgan Chase in 2004, the city's days as a relevant banking center seemed over. They're not, thanks to Wintrust.

The Wintrust story is ultimately about contrarianism—the willingness to be different when being different meant missing short-term opportunities. Ed Wehmer's refusal to chase deals during the bubble, his insistence on maintaining local bank identities, his discipline around underwriting—all of these choices looked suboptimal at various moments. They proved essential.

As founder transitions go, Wintrust's appears well-executed. Tim Crane has deep experience with the organization, the strategic direction is clear, and the balance sheet is strong. "Wintrust is coming off its best year ever," Wehmer said.

The dart that landed on "Wintrust" in the early 1990s started something far larger than a Lake Forest storefront with not enough chairs. It became Chicago's last major homegrown commercial bank—and potentially, if the next generation of leadership executes as well as Wehmer did, something more.

"We've never been for sale," Wehmer says, adding that as a public company, Wintrust always must be willing to look at offers. He credits the bank's unusual set-up—it's made up of more than a dozen separately chartered banks serving specific parts of the metro area as well as southern Wisconsin—and tightknit culture.

In an industry where consolidation has been the dominant theme for decades, Wintrust represents an alternative path: community banking at scale, disciplined through cycles, and still rooted in the hometown that made it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube