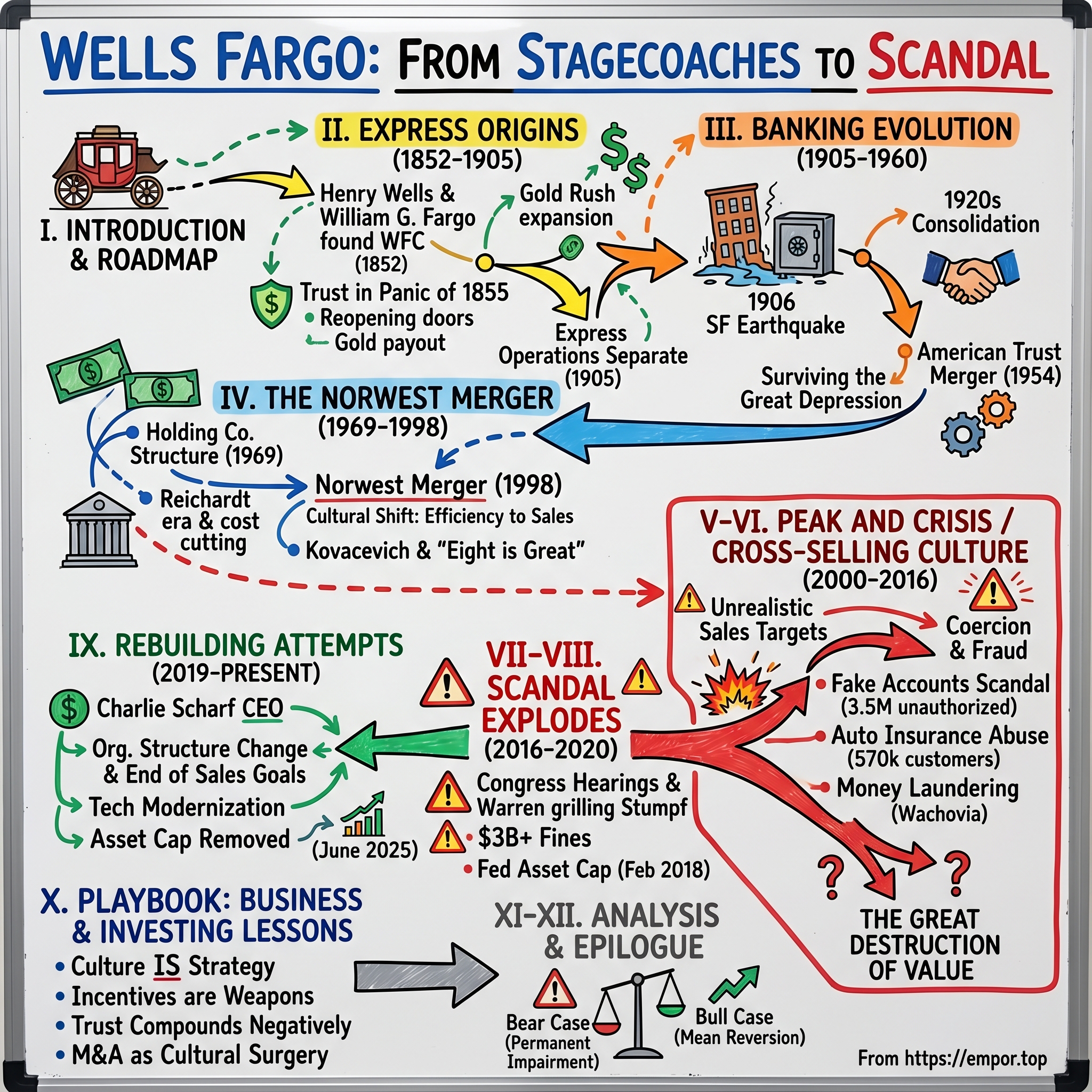

Wells Fargo: From Stagecoaches to Scandal

I. Introduction & Episode Roadmap

Picture this: March 18, 1852. Two titans of the express industry, Henry Wells and William G. Fargo, sit in a New York City office, having just been rebuffed by their own board at American Express. The directors thought expanding west during the California Gold Rush was too risky. Too volatile. Too far from their East Coast comfort zone. Wells and Fargo exchanged glances, walked out, and started their own company that very day. That act of defiance would create an institution that survived 170 years of American capitalism—the Gold Rush, the Civil War, the 1906 San Francisco earthquake that literally melted their building but not their vaults, two world wars, the Great Depression, and countless financial panics.

Yet this same institution, which once epitomized trust in the American West where a Wells Fargo strongbox meant your gold was safe, would nearly destroy itself in the 2010s. Not from external shocks or market crashes, but from within. From fake accounts. From a culture that transformed from serving customers to exploiting them. From incentives so twisted that employees felt they had no choice but to commit fraud at industrial scale.

The paradox is staggering. How does a company that built its reputation delivering gold through bandit-infested territories, that literally created the financial infrastructure of the American West, that merged its way to becoming the most valuable bank in America—how does that company nearly implode from something as banal as sales targets? How does "Eight is Great"—a cross-selling slogan—become the epitaph for 164 years of accumulated trust? At its peak, Wells Fargo's market cap reached its highest value in 2017, before the full weight of the scandals crushed its valuation. Today, the story is one of the greatest destructions of shareholder value through reputational damage in modern corporate history.

This episode will take you through the full arc—from Henry Wells and William G. Fargo's express company that helped build the American West, through the mega-mergers that created a coast-to-coast banking behemoth, to the cultural rot that nearly destroyed it all. We'll examine how a simple metric—products per customer—morphed from a sensible business strategy into a weapon that destroyed both customers and the company itself.

What makes this story particularly instructive for investors and operators alike is that Wells Fargo did almost everything right strategically. They made brilliant acquisitions. They had dominant market positions. They generated enormous profits. But they forgot the most fundamental rule of banking: trust is your only real product. Everything else—the loans, the deposits, the wealth management—is just a manifestation of that trust.

By the end of this journey, you'll understand not just what happened at Wells Fargo, but why it matters for every company that depends on customer relationships. Because if a 170-year-old institution can nearly destroy itself through misaligned incentives, what does that mean for the startups and growth companies trying to build sustainable cultures today?

II. The Express Origins: Gold Rush to Banking (1852–1905)

The California gold fields of 1849 were lawless, violent, and absurdly profitable. A miner could pull $1,000 worth of gold from a riverbed in a week—if he didn't get robbed, murdered, or die of dysentery first. The problem wasn't finding gold; it was keeping it. And more importantly, getting it back East where it could buy something more than overpriced pickaxes and rotgut whiskey.

Enter Henry Wells and William G. Fargo. These weren't wide-eyed fortune seekers but hardened express men who'd already built American Express into the dominant player east of the Mississippi. When gold was discovered at Sutter's Mill in 1848, they saw opportunity not in the streams but in the entire financial infrastructure that would need to emerge. California had gold but no banks. Miners had wealth but no way to move it. Merchants had customers but no credit system.

The American Express board meeting of March 1852 should have been routine. Wells and Fargo proposed expanding operations to California, arguing the risk was worth the reward. The board disagreed—too far, too dangerous, too uncertain. Wells and Fargo didn't argue. They resigned on the spot and that same day, March 18, 1852, founded Wells, Fargo & Company with initial capital of $300,000.

Their business model was elegantly simple and surprisingly modern. They didn't run stagecoaches initially—they contracted with existing lines. They didn't just move gold—they bought it from miners at fair prices, gave them drafts drawn on New York banks, and made money on the spread. They didn't just transport—they provided banking services, extending credit to merchants and miners alike. Within months, they had offices in San Francisco, Sacramento, and dozens of mining camps.

The Panic of 1855 was their first existential test. California's banking system, built on speculation and inadequate reserves, collapsed like a house of cards. Page, Bacon & Company, their main rival, failed spectacularly. Adams & Company, another competitor, shuttered overnight. Desperate customers stormed bank offices. In San Francisco, Wells Fargo's doors were mobbed by panicked depositors demanding their money.

Here's where corporate culture first proved decisive. Wells Fargo had maintained what seemed like excessive cash reserves—actual gold and currency, not just paper promises. When Page, Bacon failed on February 23, 1855, Wells Fargo closed for exactly one day to count every asset. On February 24, they reopened with a simple announcement: every depositor would be paid in full, in gold if requested. The crowds expecting a bank run instead found tellers calmly dispensing funds. Within weeks, Wells Fargo had absorbed most of their competitors' business. Trust, it turned out, was worth more than gold.

By 1860, Wells Fargo had evolved from express company to de facto central bank of the American West. They operated 147 offices from the Pacific to the Rockies. Their green strongboxes became so synonymous with security that bandits often wouldn't even attempt robberies when they saw the Wells Fargo name. The company's agents, armed and authorized to shoot, had a reputation for relentless pursuit of thieves. When Black Bart robbed 28 Wells Fargo stagecoaches between 1875 and 1883, the company spent a fortune tracking him down—not for the money, but for the principle.

The stagecoach operation reached industrial scale by 1866. Wells Fargo operated the largest stagecoach empire in world history—3,000 miles of routes, 1,500 horses, and connections to virtually every meaningful commercial center west of the Mississippi. They didn't just carry gold and mail; they carried the entire communication and commerce infrastructure of half a continent. When the Pony Express launched in 1860, Wells Fargo operated its western portion. When the transcontinental railroad was completed in 1869, rather than fighting it, they partnered with it, using rail for long-haul transport and stagecoaches for the last mile.

The numbers tell a story of network effects before anyone had coined the term. By 1885, Wells Fargo had 916 offices and was processing 3.3 million express packages annually. By 1910, their shipping network connected 6,000 locations—from East Coast urban centers to Pacific Northwest lumber mills, from Mexican border towns to Canadian mining camps. Revenue grew from $3 million in 1870 to $40 million by 1905. More importantly, they had something no competitor could quickly replicate: trusted relationships in every economically significant location in the western United States.

But the most prescient decision came in the 1890s as the founders aged and eastern railroads began consolidating express operations. Wells Fargo's board saw that express was becoming commoditized while banking was becoming essential. They began emphasizing their financial services—commercial loans, letters of credit, foreign exchange. By 1905, when the banking and express operations formally separated, it wasn't a retreat but a strategic focus. The express business had built the network; banking would monetize it.

The split was remarkably clean. Wells Fargo & Company continued as an express operation (eventually nationalized during WWI), while Wells Fargo Nevada National Bank, formed through merger with the Nevada National Bank, took the banking charter and the crucial California branch network. They kept the name, the reputation, and most importantly, the relationships. In every town where Wells Fargo had delivered mail and gold, they could now take deposits and make loans. The stagecoach had evolved into a bank, but the underlying business—trust at scale—remained unchanged.

III. Separation and Evolution: Banking Takes Center Stage (1905–1960)

April 18, 1906, 5:12 AM. The San Andreas Fault ruptured with a force that would later be estimated at 7.9 on the Richter scale. In San Francisco, buildings didn't just fall—they danced, twisted, and collapsed into themselves. The Wells Fargo Bank building at Market and Montgomery swayed so violently that workers later found pencils driven through inch-thick boards like arrows. Then came the fires, fed by ruptured gas mains, that would burn for three days and destroy 80% of the city.

When the smoke cleared, the Wells Fargo building was gone. Melted. The ornate marble facade had crumbled, the wooden interiors incinerated. But deep in the basement, behind steel doors that had warped from heat but held, sat the vaults. Inside, $3 million in gold and currency remained intact—every depositor's dollar accounted for. Wells Fargo set up temporary offices in the home of senior executive Frederick Lipman and began business the next day. The message was clear: San Francisco might burn, but Wells Fargo endures.

This moment crystallized what would become Wells Fargo's operating philosophy for the next century: conservative management, fortress-like capital reserves, and expansion through crisis when competitors retreated. While other banks waited for government assistance or simply failed, Wells Fargo extended emergency loans to rebuild the city, earning gratitude that would translate into generations of customer loyalty.

The separation from express operations in 1905 had been prescient. By 1918, when the U.S. government nationalized express services to support the war effort, creating the Railway Express Agency, Wells Fargo's identity had already shifted entirely to banking. The iconic stagecoaches were now just marketing imagery, but powerful imagery nonetheless—evoking reliability, western expansion, and American enterprise.

Isaias W. Hellman, who had become president in 1905, represented a new breed of Wells Fargo leader—less frontier entrepreneur, more sophisticated financier. Under his leadership through 1920, the bank pioneered what would now be called relationship banking. They didn't just take deposits and make loans; they became integral to California's agricultural revolution, financing everything from irrigation projects to fruit packing operations. By 1920, California produced more agricultural wealth than any other state, and Wells Fargo had a piece of most of it.

The 1920s brought consolidation opportunities that Hellman's successors seized aggressively. In 1923, Wells Fargo Nevada National Bank merged with the Union Trust Company to form Wells Fargo Bank & Union Trust Company, combining commercial banking strength with trust services for the emerging California wealthy class. The timing was perfect—the 1920s California boom created fortunes in real estate, oil, and entertainment. Wells Fargo managed the money.

Then came October 29, 1929. As Wall Street crashed and banks across America failed—9,000 would close between 1930 and 1933—Wells Fargo did something remarkable: it stayed open, liquid, and lending. Not only did they not fail, they didn't even cut their dividend. This wasn't luck but discipline. While eastern banks had leveraged themselves speculating on stocks, Wells Fargo had stuck to boring, profitable California real estate and agricultural loans. Their loan-to-deposit ratio never exceeded 65%, leaving enormous cushion for defaults.

The Great Depression became Wells Fargo's competitive moat. As rivals failed, Wells Fargo absorbed their deposits and customers. Between 1929 and 1933, while total U.S. bank deposits fell by 35%, Wells Fargo's deposits actually grew by 15%. They acquired failed banks' prime real estate locations for pennies on the dollar. Most importantly, they earned a reputation for safety that would drive customer acquisition for decades.

World War II transformed California from agricultural powerhouse to industrial giant, and Wells Fargo financed the transformation. They provided working capital for shipyards that built Liberty ships, funded aerospace companies that would become Boeing and Lockheed suppliers, and most presciently, began lending to a strange new industry in a place called Silicon Valley where companies like Hewlett-Packard were making electronic equipment.

The 1954 merger with American Trust Company wasn't just another acquisition—it was a cultural fusion that would define modern Wells Fargo. American Trust, founded in 1854, brought sophistication, international connections, and crucially, a presence in Southern California where post-war growth was explosive. The combined entity, Wells Fargo Bank American Trust Company (shortened to Wells Fargo Bank in 1962), had 187 branches and $2.3 billion in deposits, making it the 11th largest bank in America.

But size wasn't the point. The merger created something more valuable: a statewide network in America's fastest-growing state. California's population had grown from 5.7 million in 1930 to 15.7 million by 1960. Every new resident needed a bank account, a mortgage, a car loan. Wells Fargo was perfectly positioned—branches in every major city, agricultural loans funding the food supply, commercial loans building the suburbs.

By 1960, Wells Fargo had evolved from frontier express company to modern financial institution. They had survived panics, earthquakes, depressions, and wars not through luck but through a consistent philosophy: maintain capital strength, expand in crisis, and never forget that banking is ultimately about trust. The stagecoach might be retired, but the journey was just beginning. The next challenge would be breaking out of California to become a truly national player—a transformation that would require not just organic growth but the kind of bold acquisitions that would have made Henry Wells and William Fargo proud.

IV. The Norwest Merger: Creating a National Player (1969–1998)

The regulatory letter that arrived at Wells Fargo headquarters in early 1969 should have been routine. The Federal Reserve was approving their conversion from a state charter to a national bank charter—bureaucratic reshuffling that would let them operate more freely across state lines. But CEO Richard Cooley saw it as something more: the starting gun for a transformation from California institution to national powerhouse.

The holding company structure Wells Fargo & Company adopted that year was architectural genius disguised as legal maneuvering. The bank became a subsidiary of the holding company, which could now own insurance companies, investment firms, mortgage companies—anything financial. More importantly, it could acquire aggressively while navigating the byzantine interstate banking regulations that still Balkanized American finance.

Carl Reichardt, who became CEO in 1983, was the antithesis of a glad-handing banker. An intense, numbers-obsessed former controller, he was known for turning off hallway lights to save electricity and questioning every expense over $1,000. His motto: "Costs are like fingernails—you have to keep cutting them." Under Reichardt, Wells Fargo's efficiency ratio dropped from 63% to 48%, making it the most profitable major bank in America per dollar of assets.

But Reichardt wasn't just cutting costs—he was positioning for conquest. When federal regulations began loosening in the mid-1980s, allowing interstate banking through regional compacts, Wells Fargo was sitting on a war chest of capital and a playbook for integration. The opportunity came in 1986 when Crocker National Bank, California's fourth-largest bank, found itself overexposed to Latin American debt and energy loans.

The Crocker acquisition for $1.1 billion was brutal and brilliant. Wells Fargo fired 1,600 Crocker employees in the first week. They closed 120 overlapping branches. They eliminated entire departments. The press howled about heartlessness, but the numbers were undeniable: Wells Fargo doubled its size while reducing combined costs by 20%. The Crocker name disappeared, its century-old history erased. But Wells Fargo's stock price rose 48% in the year following the merger.

This established what became known as the "Wells Fargo Way" of acquisitions: buy distressed or underperforming banks, slash costs mercilessly, impose disciplined underwriting standards, and watch profits soar. It was financial Darwinism, and Reichardt was its prophet. Between 1986 and 1995, Wells Fargo acquired 17 smaller banks, each integration following the same playbook.

The 1996 First Interstate acquisition was Reichardt's masterpiece and swan song. First Interstate, with $58 billion in assets and branches across thirteen western states, was the prize every major bank coveted. When hostile raider H.F. Ahmanson launched a $10.8 billion unsolicited bid in October 1995, First Interstate ran into Wells Fargo's arms with an $11.6 billion friendly merger—the largest U.S. bank deal since 1929.

The integration was Crocker on steroids. Wells Fargo eliminated 9,000 jobs—nearly a third of First Interstate's workforce. They closed 365 branches. They shuttered First Interstate's Portland headquarters entirely. Customer service complaints skyrocketed as systems were merged too quickly. The California attorney general launched an investigation. But when the dust settled, Wells Fargo had doubled again, becoming the eighth-largest bank in America with a dominant position across the entire West.

Paul Hazen, who succeeded Reichardt as CEO in 1995, was supposed to be the kinder, gentler face of Wells Fargo. Instead, he became the architect of the most transformative deal in the company's history. In June 1998, he announced Wells Fargo would merge with Norwest Corporation of Minneapolis in a $31 billion stock swap. The press release called it a "merger of equals." Everyone knew better.

Norwest, led by CEO Richard Kovacevich, was actually acquiring Wells Fargo, but taking the more famous Wells Fargo name. This wasn't just financial engineering—it was cultural revolution. Where Wells Fargo was cost-obsessed and efficiency-driven, Norwest was sales-focused and growth-oriented. Where Wells Fargo talked about expense ratios, Norwest talked about "cross-selling ratios." Where Wells Fargo saw customers as account holders, Norwest saw them as relationships to be deepened.

Kovacevich himself was a force of nature—a charismatic former General Mills executive who referred to branches as "stores" and bankers as "salespeople." At Norwest, he'd implemented a system where success was measured not by assets or deposits but by products per customer. The average Norwest customer had 5.4 products versus 2.9 at Wells Fargo. Kovacevich's mantra was simple: "Banking is necessary, banks are not." He wanted Wells Fargo to be a financial supermarket where customers got everything from checking accounts to insurance to investments.

The cultural clash was immediate and intense. Wells Fargo executives, proud of their analytical rigor, found themselves in meetings where Kovacevich would pound the table about "solutions" and "needs-based selling." Norwest managers, accustomed to autonomy and incentive-based compensation, chafed at Wells Fargo's bureaucracy. In the first year post-merger, over 40% of senior Wells Fargo executives left or were forced out.

But the numbers were undeniable. The combined entity had $196 billion in assets, 6,000 branches in 21 states, and 90,000 employees. More importantly, it had complementary geography—Wells Fargo's western dominance and Norwest's Midwest presence created a true nationwide footprint. The stock market loved it, driving shares up 38% in the first year post-merger.

What observers missed was the fundamental shift in corporate DNA. The old Wells Fargo culture—conservative, disciplined, focused on credit quality and efficiency—was being overwritten by Norwest's sales culture. Those product-per-customer metrics that seemed so innovative? They would become "Eight is Great." That needs-based selling that sounded so customer-friendly? It would mutate into pressure so intense that employees would create millions of fake accounts.

By the end of 1998, Wells Fargo was unrecognizable from the institution that had emerged from the 1906 earthquake. It was now a coast-to-coast financial colossus, the seventh-largest bank in America by assets. The stagecoach logo still evoked western heritage, but the company was now run from Minneapolis by executives who'd never worked west of Minnesota until the merger. The transformation from regional bank to national player was complete. The seeds of destruction, hidden in those innovative sales metrics and aggressive culture, were already planted.

V. The Wachovia Acquisition: Peak and Crisis (2000–2009)

September 15, 2008, 1:45 AM. Lehman Brothers, 158 years old with $639 billion in assets, filed for bankruptcy. By sunrise, the fourth-largest investment bank in America was gone. Credit markets froze. Banks stopped lending to each other. The TED spread—the difference between interbank rates and Treasury bills—exploded to 458 basis points, signaling pure panic. Every financial CEO in America was calculating how many hours their institution could survive without access to overnight funding.

At Wells Fargo's San Francisco headquarters, CEO John Stumpf watched the chaos with an emotion his competitors would have found incomprehensible: excitement. Wells Fargo had spent the housing boom years being mocked as boring. While Countrywide originated $490 billion in mortgages in 2006 alone, while Wachovia bought Golden West Financial and its portfolio of option-ARM bombs, while everyone else leveraged up to chase yields, Wells Fargo had stuck to plain vanilla lending. Their Tier 1 capital ratio was 8.8%. They had $40 billion in liquid assets. They were a loaded gun in a knife fight.

Stumpf, who'd risen from a Minnesota farm to CEO in 2007, was Kovacevich's protégé and true believer. Where Kovacevich preached cross-selling, Stumpf evangelized it. He could recite product-per-household statistics like scripture: 5.95 in 2007, targeting 8 by 2010. He genuinely believed Wells Fargo was different—not a bank but a financial services company that happened to have a bank charter. The financial crisis wasn't a threat; it was an opportunity to prove the model's superiority.

Wachovia was dying in real-time. The Charlotte-based bank, America's fourth-largest with $782 billion in assets, had gorged on toxic mortgages through its 2006 acquisition of Golden West Financial for $25 billion. Golden West's specialty was option-ARMs—mortgages where borrowers could choose their payment, often less than the interest owed, with the difference added to principal. It was financial nitroglycerin, and Wachovia had $122 billion worth.

By September 26, 2008, Wachovia was experiencing a silent bank run. Commercial customers were pulling $5 billion a day. The stock had fallen from $59 to $10. CEO Bob Steel, a former Goldman Sachs executive who'd been on the job just three months, was simultaneously negotiating with potential acquirers and Federal Reserve officials about emergency lending. The FDIC was preparing for the largest bank failure in American history.

Citigroup struck first. Over the weekend of September 27-28, they negotiated a deal with the FDIC's blessing: Citi would buy Wachovia's banking operations for $2.2 billion in stock. The FDIC would absorb losses above $42 billion on Wachovia's $312 billion loan portfolio. It was a sweetheart deal for Citi—acquiring 3,300 branches and $448 billion in deposits with taxpayer protection against catastrophic losses.

The deal was announced Monday, September 29. Wells Fargo executives were furious. They'd been interested in Wachovia for years but walked away when the FDIC demanded they take the entire company, including the toxic Golden West portfolio, without government assistance. Now Citi was getting FDIC protection? Stumpf called Steel directly. Too late, Steel said. The deal was done.

Then came the gift from heaven, or more precisely, the IRS. On September 30, the tax agency issued Notice 2008-83, an obscure ruling that would change banking history. It allowed acquiring banks to use target banks' losses to offset their own taxable income—effectively turning Wachovia's mortgage disasters into tax assets. Wells Fargo's tax attorneys calculated the benefit: $19.7 billion in tax savings, enough to offset most of Golden West's expected losses.

October 2, 2008, Wells Fargo's board met at 6 AM Pacific. The discussion was brief. With the tax benefit, they could pay more than Citi, take no government assistance, and still make money. The vote was unanimous. At 9:15 AM Eastern, just as Citi executives were celebrating their deal, Wells Fargo announced a competing bid: $15.1 billion in stock for all of Wachovia, no FDIC assistance required.

Wachovia's board meeting that morning was pandemonium. Citi threatened to sue. The FDIC expressed "surprise." Steel was getting calls from Treasury Secretary Hank Paulson. But the math was simple: Wells Fargo was offering $7 per share versus Citi's $1. At 11:30 AM, Wachovia's board voted to accept Wells Fargo's offer.

Citigroup went ballistic. They sued Wells Fargo, Wachovia, and Wachovia's directors for $60 billion. They claimed contractual interference, arguing their deal was binding. The financial media was calling it the "Battle for Wachovia." Behind the scenes, Federal Reserve officials were terrified that the fight would further destabilize markets. Fed Chairman Ben Bernanke personally called both CEOs, urging resolution.

The legal battle lasted a week. On October 9, Citi withdrew its bid in exchange for a $100 million breakup fee and the right to buy certain Wachovia assets. Wells Fargo had won. When the deal closed on December 31, 2008, Wells Fargo became America's fourth-largest bank with $1.4 trillion in assets, 11,000 branches, and 280,000 employees. The stock market loved it—Wells Fargo shares rose 18% on the announcement.

The integration was shocking in its efficiency. Where previous mergers had taken years, Wachovia was absorbed in 18 months. Wells Fargo kept Wachovia's superior securities and investment banking platforms but imposed their own risk management. They wrote off $37 billion in bad loans immediately, cleaning the balance sheet. Most remarkably, they did it while the financial world was melting down around them.

The TARP episode revealed Wells Fargo's complicated relationship with government. On October 13, 2008, Paulson summoned the nine largest bank CEOs to Treasury and informed them—didn't ask—that they would each take TARP capital injections. Stumpf protested that Wells Fargo didn't need the money. Paulson's response was blunt: take it or be blamed when weaker banks fail. Wells Fargo took $25 billion.

They paid it back as soon as legally permitted—December 2009—along with $1.441 billion in dividends to taxpayers, an annualized return of 19%. Stumpf would later say taking TARP was his biggest regret, that it unfairly branded Wells Fargo as weak when they were actually strong. But the numbers told a different story: Wells Fargo earned $12.3 billion in 2009, more than JPMorgan Chase and Bank of America combined.

By the end of 2009, Wells Fargo looked invincible. They'd navigated the worst financial crisis since the Depression, acquired a major competitor at a bargain price, and emerged as one of only four truly national U.S. banks. The stock had recovered from a March 2009 low of $7.80 to $26.99 by year-end. Warren Buffett, Wells Fargo's largest shareholder with 7.6% ownership, was calling it his favorite bank investment.

But success was masking a metastasizing cancer. The Wachovia acquisition had brought 15,000 new branches into the Wells Fargo system, all now subject to the aggressive sales culture. The pressure to hit product targets, already intense, became crushing as managers tried to justify the merger's premium. "Eight is Great" wasn't just a slogan anymore—it was a commandment. Regional managers who missed targets weren't just criticized; they were humiliated in conference calls, threatened with termination.

Carrie Tolstedt, who ran the community banking division, had turned cross-selling into a science of coercion. Daily sales reports. Hourly check-ins. Employees who opened the most accounts got cash bonuses and Hawaii trips. Those who missed targets got written up, coached out, or fired. The message from the top was clear: hit your numbers or hit the road. In the euphoria of post-crisis success, nobody wanted to hear that the numbers might be fake.

VI. The Cross-Selling Culture: Seeds of Destruction (2000–2016)

The PowerPoint slide that Carrie Tolstedt displayed at the 2010 regional managers meeting in San Diego should have been triumphant. A simple bar chart showing products per household: 5.47 in 2006, 5.73 in 2008, 5.98 in 2010. The trajectory toward "Eight is Great" seemed inevitable. Tolstedt, immaculate in her navy suit, smiled at the 500 managers assembled in the Marriott ballroom. "We're not there yet," she said, her Minnesota accent hardening. "I know you can do better."

What happened next became Wells Fargo legend. She clicked to the next slide: a ranking of all 58 regions by cross-sell ratio. The bottom ten were highlighted in red. "These regions," she said, "are failing our customers by not meeting their financial needs." She read each region's name slowly, letting the shame sink in. Then she announced that the bottom five regional managers would be joining her for remedial training. At 6 AM. Every day. For a month.

Tolstedt, who joined Wells Fargo through the Norwest merger, had built community banking into a $60 billion revenue machine—40% of Wells Fargo's total earnings. She was Stumpf's most trusted lieutenant, earning $9 million annually, more than executives running divisions twice her size. Her secret weapon wasn't technology or innovation; it was pressure so relentless that employees would later describe it as psychological torture.

The sales system was engineered for exploitation. Every morning, branch employees would receive their "solution sheet"—a printout showing exactly how many products they needed to sell that day. Checking accounts: 15. Credit cards: 10. Every two hours, managers would call for updates. Miss your morning numbers? Stay through lunch. Miss your daily numbers? Stay until 9 PM. Miss your weekly numbers? Come in Saturday.

The incentive structure was equally precise. Base salary for a personal banker: $30,000. But hit 120% of your sales target? Add $5,000 in bonuses. Hit 150%? Add $10,000 plus a chance at the quarterly Hawaii trip. The difference between poverty wages and middle-class income was forcing products on customers who didn't need them.

The language itself was Orwellian. Customers weren't customers; they were "solutions opportunities." Selling wasn't selling; it was "needs-based conversations." Pressure wasn't pressure; it was "coaching." When employees complained about unrealistic targets, managers would respond with corporate speak: "We're not asking you to sell anything—we're asking you to meet customer needs."

By 2011, the system was generating extraordinary numbers and extraordinary fraud. In Los Angeles, branch manager Rita Murillo noticed something odd: new accounts being opened and closed within days, sometimes hours. When she investigated, she discovered employees were opening accounts without customer permission, funding them with automatic $25 transfers from existing accounts, then closing them after they'd been counted toward sales goals.

Murillo reported it up the chain. The response was swift: she was written up for "not supporting the sales culture." When she persisted, she was transferred to a branch 50 miles from her home. When she continued complaining, she was terminated for "performance issues." Her story would later become Exhibit A in congressional hearings, but in 2011, she was just another casualty of the culture.

The Los Angeles Times began investigating in 2013 after receiving dozens of employee tips. Reporter E. Scott Reckard spent months documenting the pressure-cooker environment. His October 2013 article, "Wells Fargo's pressure-cooker sales culture comes at a cost," was devastating. It featured employees describing panic attacks, crying in their cars, and vomiting from stress. One employee said she started drinking alcohol at her desk to cope.

Wells Fargo's response was a masterclass in corporate deflection. They acknowledged "isolated incidents" but insisted the vast majority of employees were ethical. They pointed to their ethics hotline, which received 40,000 calls annually. What they didn't mention: employees who called the hotline often found themselves fired within weeks for unrelated "violations."

The mathematics of fraud were staggering. Internal documents would later reveal that between 2011 and 2016, employees opened approximately 3.5 million unauthorized accounts. The methods were creative and criminal. Employees would:

- Create email addresses like [email protected] without customer knowledge

- Sign customers up for online banking without telling them

- Order credit cards and destroy them when they arrived at branches

- Transfer money between accounts to generate fees

- Forge signatures on account applications

The term "sandbagging" entered Wells Fargo lexicon—deliberately holding account openings until the next reporting period to ensure future targets were met. "Bundling" meant forcing customers to open multiple accounts for simple services. "Pinning" was when employees reset customer PINs without permission to activate online services that counted toward goals.

The consumer credit card division was particularly egregious. Employees would tell customers they were signing for account updates but actually enrolling them in credit cards. One elderly customer in Florida discovered she had seven Wells Fargo credit cards she'd never applied for. A college student in Arizona learned about his three checking accounts only when overdraft fees appeared.

By 2015, the pressure had evolved into something resembling a cult. Branches held daily "Jump into January" rallies where employees would literally jump up and down chanting sales goals. Managers created "Motivation Mondays" featuring videos of sports heroes talking about never giving up. One region instituted "Red Fridays" where employees who hadn't hit weekly targets had to wear red—a scarlet letter of sales shame.

The community banking division's internal newsletter, "The Golden Quarter," read like propaganda from a authoritarian regime. Headlines celebrated "Sales Heroes" who'd opened 100 accounts in a day. Articles featured "Tips from Top Performers" that were thinly veiled instructions for gaming the system. One infamous piece advised: "Remember, every customer interaction is a sales opportunity—even complaints!"

John Stumpf, meanwhile, was becoming the face of American banking recovery. He testified before Congress about responsible lending, gave speeches about ethics, and wrote op-eds about rebuilding trust. In every investor presentation, he highlighted Wells Fargo's industry-leading cross-sell ratio—6.11 products per household by 2015—as proof of superior customer relationships.

What Stumpf didn't know, or chose not to know, was that approximately 2% of those products were fake. That might sound small, but it represented millions of fraudulent accounts generating hundreds of millions in fees. More importantly, it represented a complete breakdown of corporate ethics, a culture where hitting numbers mattered more than customer trust.

The Office of the Comptroller of the Currency (OCC) had been investigating since 2014. The Consumer Financial Protection Bureau (CFPB) joined in 2015. By early 2016, both agencies had enough evidence to prove systematic fraud. Wells Fargo's legal team was negotiating settlements, hoping to keep the scandal quiet with a fine and promises to do better.

But the Los Angeles City Attorney, Mike Feuer, wouldn't play ball. His office had been building a criminal case, interviewing hundreds of employees, documenting thousands of fraudulent accounts. He wanted accountability, not just money. When Wells Fargo offered to settle for $50 million in May 2016, Feuer countered with a demand: the settlement must be public, with detailed admissions of wrongdoing.

Wells Fargo had no choice. The alternative was a public trial that would expose even more damaging details. On September 8, 2016, they agreed to pay $185 million in fines and penalties: $100 million to the CFPB (the largest fine in the agency's history), $50 million to Los Angeles, and $35 million to the OCC. They also agreed to fire 5,300 employees for sales violations.

The press release was meant to be the end of the scandal—take responsibility, pay the fine, move on. Instead, it was just the beginning of Wells Fargo's corporate nightmare.

VII. The Fake Accounts Scandal Explodes (2016–2020)

September 20, 2016. Senate Banking Committee Hearing Room, Dirksen Senate Office Building, Washington D.C. John Stumpf sat alone at the witness table, 20 senators arranged in a horseshoe around him, C-SPAN cameras rolling. Behind him, hundreds of Wells Fargo customers and former employees packed the gallery. Some held signs: "Wells Fargo Ruined My Credit." Others simply glared. Stumpf, who'd testified before Congress dozens of times, had never faced anything like this.

Senator Elizabeth Warren didn't wait for pleasantries. "Mr. Stumpf," she began, her voice sharp as breaking glass, "you should resign. You should give back the money you took while this scam was going on, and you should be criminally investigated." The room erupted in applause before the chairman could gavel for order.

For two hours, Stumpf was eviscerated on live television. Senator after senator—Republicans and Democrats alike—took turns expressing disgust. When Stumpf tried his prepared talking points about "wrongful behavior" by terminated employees, Warren cut him off: "This is about accountability. You squeezed your employees to the breaking point so they would cheat customers and you could drive up the value of your stock and put hundreds of millions of dollars in your own pocket."

The most damaging moment came when Senator Jon Tester asked a simple question: "Exactly how much money did you make from these fake accounts?" Stumpf hesitated, stammered, then admitted he didn't know. Tester's follow-up was devastating: "You fired 5,300 employees for doing exactly what they were incentivized to do, but you don't know how much money you made from it?"

Stumpf's defense—that the fraud represented only 2% of accounts, that the vast majority of employees were honest—fell flat. Senator Pat Toomey, usually a bank-friendly Republican, said what everyone was thinking: "The fundamental problem is you had terrible business practices and an outrageous culture that drove people to do things they shouldn't have done."

The testimony went viral. #WellsFargoFraud trended globally. The clip of Warren calling Stumpf "gutless" was viewed 50 million times in 48 hours. Wells Fargo's stock fell 9% in two days. Customer satisfaction scores, tracked by J.D. Power, plummeted from positive 5.8 to negative 23.1—the largest drop ever recorded.

Inside Wells Fargo, panic set in. The board, which had stood behind Stumpf initially, began wavering. Institutional investors, led by Warren Buffett's Berkshire Hathaway, were asking hard questions. The independent directors hired law firm Shearman & Sterling to conduct an investigation. Their preliminary findings were damning: the board had been repeatedly warned about sales practice issues but did nothing substantive.

October 12, 2016. After weeks of pressure, Stumpf resigned as CEO and chairman, forfeiting $41 million in unvested equity awards. But the gesture was too little, too late. The same day, Wells Fargo reported third-quarter earnings showing new account openings had dropped 25% since the scandal broke. Credit card applications fell 35%. The brand was toxic.

Tim Sloan, Wells Fargo's COO and Stumpf's hand-picked successor, promised change. A 29-year Wells veteran, Sloan was supposed to be the steady hand who could reform from within. His first act was firing Carrie Tolstedt, clawing back $19 million of her compensation. But the investigations were just beginning.

The initial 2.1 million fake accounts turned out to be the tip of the iceberg. An expanded review covering 2009 to 2016 found 3.5 million unauthorized accounts. Then auditors looked at other products. They found:

- 570,000 auto loan customers charged for insurance they didn't need

- 110,000 mortgage customers charged improper fees

- 528,000 online bill pay services enrolled without authorization

- Thousands of small business accounts opened without permission

Each revelation brought new fines, new hearings, new humiliations. The Federal Reserve, which had largely stayed quiet, dropped a nuclear bomb on February 2, 2018: an asset cap limiting Wells Fargo to $1.95 trillion in assets until the bank proved it had fixed its governance and risk management. It was an unprecedented punishment for a major U.S. bank—essentially freezing Wells Fargo's growth indefinitely.

Fed Chair Janet Yellen's statement was scathing: "We cannot tolerate pervasive and persistent misconduct at any bank." The asset cap was particularly painful because it came during an economic boom when competitors were growing rapidly. JPMorgan Chase, Bank of America, and Citigroup would add hundreds of billions in assets while Wells Fargo was frozen.

The legal bills were staggering. Wells Fargo paid: - $1 billion to the CFPB and OCC in April 2018 - $2.09 billion to the Department of Justice in February 2020 - $500 million to the SEC in February 2020 - $3 billion total to resolve criminal and civil investigations

But the real cost was reputational. Wells Fargo's net promoter score—measuring customer likelihood to recommend the bank—went negative and stayed there. Checking account openings fell 43% from 2016 to 2019. The company that had built its identity on trust had become synonymous with fraud.

The human toll was equally devastating. Thousands of employees suffered mental health crises. Many required therapy for anxiety and depression. Several committed suicide, though Wells Fargo disputed any connection. Class action lawsuits on behalf of employees forced to engage in fraud were settled for $240 million.

For customers, the damage went beyond unauthorized accounts. Credit scores were damaged by credit cards they didn't apply for. Small businesses lost financing when fraudulent accounts triggered banking covenant violations. Elderly customers paid thousands in fees for services they didn't understand or authorize.

The cultural reckoning was painful. Wells Fargo eliminated product sales goals entirely in 2017—an admission that the core strategy of two decades was fundamentally flawed. They hired 40,000 new employees to replace those terminated or who quit in disgust. They spent $1 billion on "remediation"—refunding fees, fixing credit reports, apologizing to customers.

Tim Sloan's tenure as CEO was a disaster. Despite promises of reform, new scandals kept emerging. When he testified before Congress in March 2019, the reception was even more hostile than Stumpf had faced. Representative Maxine Waters, chair of the House Financial Services Committee, opened with: "Mr. Sloan, you keep saying you've made changes, but the problems keep coming. When will it stop?"

It wouldn't stop under Sloan. Two weeks after that hearing, he resigned, becoming the second Wells Fargo CEO casualty of the scandal. The board conducted an external search for the first time in the bank's history, eventually hiring Charles Scharf from BNY Mellon in October 2019. Scharf's first public statement was telling: "We have much work to do to rebuild trust."

The numbers told the story of destruction. Wells Fargo's market capitalization, which peaked at $308 billion in early 2018, fell to $170 billion by March 2020. Return on equity dropped from 13% to 9%. The efficiency ratio—once Wells Fargo's pride—ballooned from 48% to 68% as revenues fell and expenses for legal and remediation soared.

The investigation's final report, released in April 2020, was a 100-page indictment of corporate governance failure. The board had ignored warning signs for years. Internal audit had raised concerns as early as 2004. The chief risk officer had flagged sales practices in 2012. But nothing changed because the sales numbers looked good and the stock price kept rising.

Perhaps most damning was the revelation about incentives. Carrie Tolstedt had earned $125 million between 2010 and 2016 while overseeing the fraud. John Stumpf made $286 million during the same period. The 5,300 fired employees, meanwhile, earned an average of $35,000 annually. The architects of the fraud got rich; the foot soldiers got fired.

By 2020, Wells Fargo was a shadow of its former self—still enormous by assets but diminished in every way that mattered. The stagecoach that had symbolized western expansion and reliability now evoked corporate greed and customer betrayal. The company that had survived the 1906 earthquake and 2008 financial crisis had nearly been destroyed by something as preventable as bad incentives and worse oversight.

VIII. Additional Scandals and Systemic Issues (2016–2020)

The forensic accountant from the Office of the Comptroller of the Currency couldn't believe what she was seeing. It was March 2017, six months after the fake accounts scandal broke, and she was reviewing Wells Fargo's auto lending division. The pattern was unmistakable: between 2012 and 2017, Wells Fargo had forced 570,000 auto loan customers to buy insurance they didn't need, couldn't afford, and in many cases, already had.

The scheme was diabolically simple. When customers financed cars through Wells Fargo, the bank required comprehensive insurance—standard practice. But Wells Fargo's system would automatically purchase "collateral protection insurance" on the customer's behalf, adding it to their monthly payment, even when customers already had coverage. The insurance was expensive—sometimes $1,000 annually—and pushed 20,000 customers into default. Their cars were repossessed. Their credit destroyed. All for insurance they never needed.

One victim, Patricia Santos of California, had her 2008 Honda Civic repossessed in 2015 after Wells Fargo added $800 in unwanted insurance to her loan. She had perfect payment history for two years until the insurance charges pushed her payment from $275 to $340 monthly. She couldn't afford it on her waitress salary. Wells Fargo sold her car at auction for $3,000, then sued her for the $8,000 deficiency. She declared bankruptcy. She was one of thousands.

While investigators were uncovering the auto insurance fraud, another team was examining Wells Fargo's mortgage division. What they found was equally appalling. Between 2013 and 2017, Wells Fargo had charged 110,000 mortgage customers for "rate lock extensions"—fees for delays in closing—even when Wells Fargo caused the delays. Some customers paid thousands in unnecessary fees. Others lost homes they were trying to buy when deals fell through.

The mortgage investigation revealed something worse: systematic discrimination. Wells Fargo had charged higher fees and interest rates to Black and Hispanic borrowers, even when they qualified for better terms. The pattern was so consistent it couldn't be explained by credit scores or income. It was redlining dressed up in algorithms.

But nothing compared to what investigators found when they looked at Wachovia's pre-merger history. Between 2004 and 2007, Wachovia had failed to monitor $378 billion in transactions from Mexican currency exchanges. Drug cartels had used Wachovia to launder money so brazenly that they designed special boxes to fit precisely through teller windows. The investigation found that 22 tons of cocaine had been seized from planes purchased with money laundered through Wachovia accounts.

The details were like something from a crime novel. Mexican cartels would deposit hundreds of thousands in cash at casa de cambios (currency exchanges), which would wire the money to Wachovia accounts. The money would then purchase planes, boats, and equipment for drug trafficking. Wachovia's anti-money laundering systems had flagged the transactions repeatedly. Management ignored the warnings.

When Wells Fargo acquired Wachovia in 2008, they inherited this criminal liability. In 2010, Wells Fargo paid $160 million to settle the money laundering charges—a rounding error against the profits from the Wachovia acquisition. No executives were prosecuted. The DEA agent who led the investigation later said: "Wachovia's blatant disregard for banking laws gave international cocaine cartels a virtual carte blanche to finance their operations."

The pattern of malfeasance extended to wealth management. Wells Fargo financial advisors had recommended inappropriate investments to retirees, pushing them into high-fee products that generated commissions but destroyed retirement savings. One 70-year-old widow in Florida lost $400,000—her entire life savings—after her Wells Fargo advisor put her in speculative investments unsuitable for her age and risk tolerance.

The foreign exchange division was running its own scam. Corporate customers exchanging currency were systematically overcharged through hidden markups. A manufacturer doing business in Mexico discovered Wells Fargo had cost them $2 million over five years through inflated exchange rates. When they complained, Wells Fargo offered a "courtesy credit" of $50,000 and a non-disclosure agreement.

Even the employee 401(k) plan was corrupted. Wells Fargo used its own expensive, underperforming funds in employee retirement accounts, collecting fees from both ends. Employees were literally paying their employer to mismanage their retirement. A class action lawsuit revealed Wells Fargo made $40 million annually from these hidden fees.

The scope suggested not isolated problems but systematic institutional failure. Every division, every product line, every customer segment showed evidence of exploitation. The common thread was always the same: aggressive sales targets, insufficient oversight, and a culture that prioritized revenue over everything.

Former employees described a company that had completely lost its moral compass. One former wealth manager said: "We were told that every customer interaction was a sales opportunity. Grandma coming in to check her balance? Sell her a credit card. Small business owner making a deposit? Pitch a line of credit. It was relentless."

The technological infrastructure enabled the fraud. Wells Fargo's systems were designed to make opening accounts easy but closing them hard. Customers would spend hours on hold trying to cancel unwanted services. Many gave up, paying fees for months or years rather than navigate the bureaucracy.

The international implications were staggering. Wells Fargo operated in 35 countries, and investigators found problems everywhere. In Japan, Wells Fargo overcharged corporate customers on derivatives. In London, they manipulated foreign exchange rates. In Hong Kong, they facilitated tax evasion. The stagecoach had become a global getaway vehicle for financial crime.

By 2020, regulators had identified 15 distinct patterns of consumer abuse at Wells Fargo. The bank was operating under 14 different consent orders from various agencies. They had 100 full-time employees whose only job was interfacing with regulators. The legal department had grown from 600 to 3,000 lawyers.

The cost went beyond fines. Wells Fargo spent $2.7 billion on consultants to fix problems. They hired McKinsey, Accenture, Oliver Wyman—every major firm—to redesign processes, rebuild systems, reform culture. The consultants produced thousands of pages of recommendations. Little changed.

The board of directors, supposedly reformed after Stumpf's departure, remained problematic. Several directors had served during the fraud years but stayed on. When shareholders proposed replacing them, the board recommended voting against the proposals. The message was clear: accountability was for employees, not directors.

Charlie Scharf, the new CEO, inherited a company where corruption wasn't a bug but a feature. In his first town hall, he said: "We have to acknowledge that our culture is broken. We've hurt millions of customers. We've destroyed our reputation. The path back will take years, maybe decades."

He was being optimistic.

IX. Rebuilding Attempts and Current State (2019–Present)

Charlie Scharf's first day as CEO, October 21, 2019, began at 5 AM with a security briefing about death threats against Wells Fargo executives. By 6 AM, he was reviewing a regulatory report documenting 73 different "matters requiring attention." By 7 AM, he was on a conference call with the Federal Reserve about the asset cap. Welcome to Wells Fargo.

Scharf was an unusual choice—a New Yorker who'd never worked at Wells Fargo, had no California ties, and whose previous job running BNY Mellon was notable mainly for cost-cutting. But that was the point. The board wanted an outsider with no loyalty to the old guard. Someone who could perform corporate chemotherapy—killing the diseased culture even if it meant damaging healthy tissue.

His first all-hands meeting set the tone. "I know many of you are tired of hearing about our problems," he said via videoconference to 260,000 employees. "Too bad. We're going to talk about them until they're fixed. And if you were part of creating them, you won't be here much longer."

The executive bloodletting was swift. Within six months, Scharf replaced the heads of consumer banking, wealth management, technology, human resources, and legal. The infamous community banking division was dismantled entirely, split into multiple units with separate reporting lines. The message was clear: the old Wells Fargo was dead. The structural changes were radical. Scharf eliminated product sales goals entirely—the foundation of Wells Fargo's business model for two decades. Instead, employees would be evaluated on customer satisfaction, risk management, and ethical behavior. The shift was so fundamental that many veteran bankers quit, unable to adapt to a world where opening accounts wasn't the primary metric.

Technology transformation became Scharf's obsession. Wells Fargo was running on systems from the 1980s, held together with digital duct tape. The mobile app crashed regularly. The website looked like it was designed in 2005. Meanwhile, competitors like JPMorgan were spending $12 billion annually on technology. Scharf committed $8 billion to modernization, hiring 5,000 engineers and partnering with Microsoft and Google.

But the biggest challenge was the asset cap. In June 2025, after seven years of restrictions, the Federal Reserve finally announced Wells Fargo was no longer subject to the asset growth restriction from the Board's 2018 enforcement action, with the removal representing successful remediation based on focused management leadership, strong board oversight, and strict supervision. The punitive $1.95 trillion cap that had restricted the bank's growth was lifted, handing CEO Charlie Scharf a major victory and sending the bank's shares up 2.7% in after-hours trading.

The lifting of the cap was transformative. While Wells Fargo had been frozen, JPMorgan Chase's assets had swelled by nearly $2 trillion since the start of 2018, while Bank of America and PNC Financial added about $1 trillion and nearly $200 billion respectively. Wells Fargo could finally compete again, particularly in areas like corporate deposits, trading, and wealth management where the cap had been most constraining.

Yet the celebration was muted. Senator Elizabeth Warren called the Fed's decision "an outrageous giveaway to one of Wall Street's most derelict banks," arguing the Fed couldn't wait even a full year without the company breaking the law before wiping its slate clean. The political risk remained acute—any new scandal would bring crushing scrutiny.

The branch footprint transformation was dramatic. Wells Fargo closed 1,000 branches between 2020 and 2024, reducing from 5,400 to 4,400 locations. This wasn't just cost-cutting but strategic repositioning. Physical branches were expensive—$2 million annually to operate—while 80% of transactions were now digital. The future was mobile, not marble lobbies.

The workforce restructuring was equally aggressive. Wells Fargo eliminated 40,000 positions between 2020 and 2024, mostly in branches and back-office operations. But they hired 20,000 technology and risk management professionals. The message was clear: Wells Fargo was becoming a technology company that happened to have a banking license.

Customer acquisition remained challenging. Despite spending $500 million on marketing featuring feel-good commercials about "rebuilding trust," new account openings remained 30% below 2015 levels. Millennials and Gen Z customers, who associated Wells Fargo with fraud, banked elsewhere. The average Wells Fargo customer was 47 years old, versus 38 at Chase and 35 at digital banks like Chime.

The competitive landscape had shifted dramatically. While Wells Fargo was frozen under the asset cap, fintech companies had exploded. Stripe was processing $640 billion in payments annually. Square's Cash App had 51 million users. Robinhood had democratized investing. These weren't traditional competitors, but they were stealing Wells Fargo's future customers.

Even traditional banking had evolved. JPMorgan Chase had become a technology powerhouse, with CEO Jamie Dimon calling it a "technology company." Bank of America had invested heavily in AI and automation. Regional banks like PNC and US Bank had grabbed market share in commercial lending. Wells Fargo was playing catch-up in every segment.

The financial performance reflected these challenges. Return on equity, which had exceeded 13% before the scandals, struggled to reach 10%. The efficiency ratio remained elevated at 64%, compared to 57% at peers. Net interest margin compressed as Wells Fargo paid up for deposits to fund growth post-asset cap. The stock, which traded at 1.8x book value in 2015, now traded at 1.1x.

Yet there were green shoots. Commercial banking, freed from the asset cap, grew loans 15% in the six months after the restriction lifted. Wealth management assets under management reached $2.2 trillion. The investment banking division, rebuilt from scratch, was winning mandates. Credit quality remained strong with net charge-offs at just 0.4% of loans.

Scharf's transformation was showing results, albeit slowly. Employee satisfaction scores, measured by Gallup, improved from the 15th percentile in 2019 to the 45th percentile by 2025. Customer complaint volumes to the CFPB fell 40%. The number of consent orders dropped from 14 to 8. Progress, not perfection.

The culture change was perhaps most evident in small details. The executive floor at headquarters, once known as "Mahogany Row" for its wood paneling and exclusive elevator, was converted to an open floor plan. Executive bonuses were tied to customer satisfaction and risk metrics, not sales. Town halls featured real customer complaints, not sales celebrations.

But the ultimate test remained ahead. Could Wells Fargo grow without reverting to aggressive sales tactics? Could they compete with both traditional banks and fintech disruptors? Could they ever truly rebuild trust? The asset cap was gone, but the scarlet letter remained.

X. Playbook: Business & Investing Lessons

The Stanford Graduate School of Business case study on Wells Fargo, published in 2023, opens with a simple question: "How does a 150-year-old institution destroy itself in five years?" The answer, documented across 47 pages of analysis, isn't simple at all. It's a masterclass in how intelligent people can create catastrophically stupid systems.

Lesson 1: Culture Is Strategy's Breakfast, Lunch, and Dinner

Peter Drucker's famous quote that "culture eats strategy for breakfast" understates the case at Wells Fargo. Culture devoured everything. The bank had brilliant strategy—coast-to-coast presence, diversified revenue streams, disciplined underwriting. None of it mattered when the culture became toxic.

The Norwest merger in 1998 was strategically perfect but culturally catastrophic. Wells Fargo's conservative, risk-averse culture was overwritten by Norwest's aggressive sales culture. It's like replacing a building's foundation while keeping the facade—eventually, everything collapses. For investors, the lesson is clear: when two companies merge, the culture that emerges matters more than any synergy spreadsheet.

Lesson 2: Incentives Are Nuclear Weapons

Charlie Munger says "Show me the incentive and I'll show you the outcome." Wells Fargo showed us what happens when incentives become weapons of mass destruction. The sales targets weren't just aggressive—they were mathematically impossible. When you tell someone their children's healthcare depends on opening 20 accounts per day, they'll open 20 accounts. Whether customers want them is irrelevant.

The perversity was in the precision. Wells Fargo didn't just say "sell more." They created elaborate scorecards, tracked hourly performance, and tied everything to compensation. It was scientific management applied to fraud. The lesson: be terrified of any metric that becomes a target, especially when people's livelihoods depend on it.

Lesson 3: Trust Compounds Negatively Faster Than Positively

Wells Fargo spent 164 years building trust and destroyed it in 5. The asymmetry is brutal. Trust compounds slowly, like interest in a savings account. Distrust compounds quickly, like interest on a payday loan. Once customers believe you're trying to exploit them, every interaction becomes suspicious. That helpful banker suggesting a credit card? Probably scamming you.

The numbers prove it. Wells Fargo's net promoter score went from +5.8 to -23.1 in six months. It took seven years to crawl back to -3.9. For every customer who had a fake account opened, ten others heard the story and switched banks. Social media amplified the damage—#WellsFargoFraud had 500 million impressions. In the attention economy, scandal scales exponentially.

Lesson 4: Regulatory Capture Works Until It Doesn't

For years, Wells Fargo operated in regulatory capture paradise. They hired former regulators, donated to political campaigns, and lobbied against consumer protections. When problems emerged, they negotiated settlements with NDAs. It worked perfectly until it didn't.

The CFPB, created after the 2008 crisis, was different. It had public complaint databases, aggressive enforcement powers, and political protection from Elizabeth Warren. When they fined Wells Fargo $100 million, they required public admission of wrongdoing. That triggered congressional hearings, which triggered more investigations, which triggered more scandals. Regulatory capture is like picking up pennies in front of a steamroller—profitable until you're flattened.

Lesson 5: M&A Integration Is Cultural Surgery

The Wachovia acquisition was financially brilliant—$15 billion for a bank worth $30 billion once cleaned up. But spreading Wells Fargo's already-toxic culture to 15,000 new branches was like metastasizing cancer. Every acquisition amplified the sales pressure because managers had to justify the premium paid.

The playbook was always the same: acquire, fire thousands, impose sales targets, demand results. It worked when the target was efficiency. It failed catastrophically when the target was impossible sales goals. For investors, the lesson is that serial acquirers often confuse integration with multiplication—they don't just add problems, they multiply them.

Lesson 6: Network Effects Can Become Network Defects

Wells Fargo's branch network was its moat—5,400 locations where customers could bank in person. But when every branch became a pressure cooker of sales abuse, the network effect reversed. Instead of convenience, branches became sites of exploitation. Customers started banking online not for efficiency but for safety.

The digital transformation that Wells Fargo resisted for years became mandatory overnight. But they were a decade behind. While they were pushing credit cards in branches, fintech companies were building mobile-first experiences. The lesson: network effects are only valuable if the network creates value. When it destroys value, size becomes liability.

Lesson 7: Short-Term Thinking in Long-Term Businesses Is Fatal

Banking is fundamentally about time arbitrage—borrow short, lend long, profit from the spread. It requires thinking in decades. But Wells Fargo's sales culture operated in hours. Hit your numbers by noon or stay late. Make quota this month or get fired. The temporal mismatch was fatal.

The average customer relationship at Wells Fargo before the scandal was 11 years. The average fake account lasted 4 months. They sacrificed centuries of cumulative trust for quarters of fabricated growth. It's like burning your furniture to heat your house—warm today, homeless tomorrow.

Lesson 8: Crisis Management Is About Speed and Sincerity

Wells Fargo's crisis management was a casebook in what not to do. They denied, deflected, and delayed. When caught, they blamed low-level employees. When executives were implicated, they negotiated exit packages. When forced to apologize, they used corporate speak. Every step made it worse.

Compare this to Johnson & Johnson's Tylenol crisis in 1982. Within days of cyanide-laced capsules killing seven people, J&J recalled 31 million bottles, created tamper-proof packaging, and communicated transparently. The brand recovered within a year. Wells Fargo is still recovering after eight years. The difference? Speed and sincerity. J&J acted like they cared about customers. Wells Fargo acted like they cared about litigation.

Lesson 9: Operational Leverage Cuts Both Ways

Wells Fargo's efficiency ratio was its pride—48% meant they spent 48 cents to generate a dollar of revenue. But operational leverage is symmetrical. When revenue collapsed due to scandal, the fixed costs remained. The efficiency ratio ballooned to 68%. The very operational discipline that created profits amplified losses.

This is the hidden risk in highly efficient operations—they're optimized for steady state, not crisis. It's like a Formula 1 car: incredibly fast on a track, but try driving it off-road. For investors, companies bragging about operational efficiency should trigger questions about operational flexibility.

Lesson 10: The Cost of Compliance Is Less Than the Cost of Non-Compliance

Wells Fargo saved maybe $100 million annually by understaffing compliance and risk management. They've now paid over $10 billion in fines and spent $3 billion on remediation. The ratio is 100-to-1. This doesn't include lost revenue, elevated expenses, or destroyed market value.

The math of compliance is like insurance—it seems expensive until you need it. But unlike insurance, compliance failures compound. One violation triggers investigations that uncover more violations. Wells Fargo had 15 distinct patterns of abuse because each investigation revealed new problems. It's archaeological fraud—the deeper you dig, the more you find.

The Meta-Lesson: Complex Systems Fail in Complex Ways

Wells Fargo wasn't destroyed by one bad decision but by thousands of small compromises. Each seemed rational in isolation. Sales targets? Everyone has them. Aggressive goals? That's capitalism. Firing underperformers? That's management. But together, they created a system that could only produce fraud.

This is the challenge for investors analyzing any large institution: the risk isn't in what you can see but in what emerges from complexity. Wells Fargo's board included former Federal Reserve governors, Fortune 500 CEOs, and respected academics. They had risk committees, audit committees, and compliance committees. None of it mattered because the system's emergent property was corruption.

The only defense is culture, and culture can't be measured in spreadsheets. It lives in the space between what's legal and what's right, between what's possible and what's proper. Wells Fargo forgot that distinction. The cost was everything.

XI. Analysis & Bear vs. Bull Case

The Bull Case: Resurrection Through Rationalization

The optimists' spreadsheet is compelling. Wells Fargo trades at 1.1x tangible book value versus 1.8x for JPMorgan. The price-to-earnings ratio is 11x versus 13x for Bank of America. If Wells Fargo simply re-rates to peer multiples, that's 40% upside. This isn't speculation—it's mean reversion.

With the Federal Reserve's June 2025 removal of the $1.95 trillion asset cap that had restricted Wells Fargo's size for more than seven years, the bank is finally unleashed from unprecedented punishment, with the Fed confirming Wells Fargo met all conditions required by the 2018 enforcement action. This changes everything. Wells Fargo can now compete for corporate deposits, expand trading operations, and grow wealth management without artificial constraints.

The scale advantages remain intact. Wells Fargo is still the third-largest U.S. bank with $1.9 trillion in assets, 4,400 branches, and relationships with 70 million customers. One in three American households has a Wells Fargo product. That's not easily replicated. Network effects in banking are real—the more customers you have, the more valuable your payment systems, the lower your funding costs.

Digital transformation is finally happening. The $8 billion technology investment is modernizing systems that hadn't been updated since the 1990s. The new mobile app has 31 million active users, up 40% since 2020. Digital sales now represent 60% of new accounts. Wells Fargo is becoming the technology-enabled bank it should have been a decade ago.

The revenue diversification is attractive. Unlike investment banks exposed to volatile trading revenues, Wells Fargo generates 60% of revenue from net interest income—boring, predictable, profitable. With interest rates likely to remain elevated, net interest margins should expand. Every 25 basis point increase in rates adds $1.2 billion to annual profits.

Credit quality is pristine. Net charge-offs are 0.4% of loans versus historical averages of 1.2%. The commercial real estate portfolio, everyone's current worry, is conservatively underwritten with average loan-to-value of 58%. Wells Fargo learned from 2008—they didn't chase yield during the recent boom. When the next crisis comes, they'll be buyers, not sellers.

The expense trajectory is compelling. Scharf has committed to $8 billion in annual cost saves by 2026. That's not fantasy—1,000 branches have already closed, 40,000 positions eliminated. The efficiency ratio should improve from 64% to 55%, generating $4 billion in additional pre-tax income. At a 12x multiple, that's $48 billion in market value creation.

Most importantly, the cultural transformation might actually be working. Employee satisfaction scores have improved. Customer complaints are declining. The sales pressure is gone. Wells Fargo is becoming boring—and in banking, boring is beautiful. No news is good news when your recent history is perpetual scandal.

The Bear Case: Permanent Impairment

The pessimists' model is equally convincing. Wells Fargo hasn't just lost customers—they've lost a generation. Only 18% of Gen Z consumers would consider banking with Wells Fargo versus 45% for Chase. That's not a temporary preference—it's demographic destiny. Every year, Wells Fargo's customer base gets older, poorer, and smaller.

The competitive position has permanently deteriorated. While Wells Fargo was frozen under the asset cap, competitors didn't just grow—they transformed. JPMorgan spends $12 billion annually on technology versus Wells Fargo's $8 billion. Bank of America has 50 million digital users versus Wells Fargo's 31 million. The gap isn't closing; it's widening.

Fintech disruption is accelerating. Why would anyone use Wells Fargo for payments when Venmo is free and instant? Why get a Wells Fargo credit card when Apple Card has no fees and 2% cash back? Why open a Wells Fargo savings account paying 0.01% when Marcus pays 4.5%? Every product Wells Fargo offers has a better digital alternative.

The regulatory scrutiny remains intense. Senator Elizabeth Warren and Congresswoman Maxine Waters wrote to the Federal Reserve calling the asset cap removal "embarrassing and unwarranted," arguing it would have "a profound impact on its credibility as an impartial, consistent, and effective bank regulator" and noting Wells Fargo's series of "outrageous scandals that affected millions of customers". Any minor infraction will trigger disproportionate punishment.

The expense base is structurally disadvantaged. Wells Fargo has 4,400 branches that cost $8.8 billion annually to operate. Digital banks have zero branches and 90% lower costs. Wells Fargo's efficiency ratio of 64% compares to 35% at digital banks. This isn't a temporary disadvantage—it's structural obsolescence.

The talent exodus is real. Wells Fargo has lost thousands of experienced bankers who've joined competitors or fintechs. The average tenure has dropped from 12 years to 7 years. Institutional knowledge is evaporating. Meanwhile, top graduates won't join Wells Fargo—it's reputational suicide. The human capital deficit compounds annually.

Most fundamentally, trust once broken is nearly impossible to rebuild. Wells Fargo's net promoter score remains negative. Customer acquisition costs are 3x higher than peers. The stagecoach brand, once synonymous with reliability, now evokes exploitation. That's not fixable with marketing—it's a generational stain.

The Synthesis: Slow Grind to Mediocrity

The reality likely lies between extremes. Wells Fargo won't collapse—it's too big, too diversified, too systemically important. But it won't thrive either. It's destined for a decade of mediocrity, generating adequate returns for shareholders but never escaping the shadow of scandal.

The bank will muddle through, growing slowly as the asset cap removal enables expansion, but constrained by competitive disadvantages and reputational damage. Return on equity will hover around 10%—not terrible, but not great. The stock will trade at a permanent discount to peers—justified by execution risk and regulatory overhang.

This is what corporate purgatory looks like: profitable enough to survive, damaged enough to never truly succeed. Wells Fargo will be a value trap for aggressive investors and a value play for patient ones. The difference is time horizon and pain tolerance.

For fundamental investors, the question isn't whether Wells Fargo is cheap—it clearly is. The question is whether cheap is cheap enough given the structural challenges. At 0.8x book value, probably yes. At 1.1x book, probably no. The margin of safety needs to account for permanent impairment, not temporary setback.

The ultimate irony is that Wells Fargo's scandal created the conditions for its own recovery. The cultural revolution, forced by crisis, might produce a better bank—not excellent, but acceptable. The cost discipline, learned through necessity, might drive efficiency. The digital transformation, delayed but not denied, might enable competition.

But might isn't certainty, and Wells Fargo's history suggests skepticism is warranted. This is a bank that turned cross-selling into crime, efficiency into exploitation, and trust into betrayal. The burden of proof is on management to demonstrate change, not on critics to assume it.

XII. Epilogue: What Would the Founders Think?

Henry Wells died in 1878, having retired to Aurora, New York, where he founded Wells College for women—progressive for his era. William Fargo passed in 1881 in Buffalo, after serving as mayor and building the city's first permanent opera house. Neither man lived to see their express company become a bank, let alone a national financial institution. But they understood something about business that their successors forgot: reputation is capital.

In 1855, when California's banking system collapsed, Wells and Fargo could have done what every other bank did—close their doors, blame the panic, and negotiate settlements with depositors for cents on the dollar. Instead, they paid every claim in full, in gold, immediately. It nearly bankrupted them. But it built something more valuable than money: unshakeable trust.

That trust manifested in physical symbols. The Wells Fargo strongbox became so synonymous with security that competitors painted their boxes green to confuse customers. The company's agents were known for incorruptibility—when Black Bart robbed 28 stagecoaches, he never killed a single guard because he knew they'd die before surrendering the cargo. The slogan "Ocean to Ocean" wasn't just about geography; it was about reliability across vast distances where law was suggestion and trust was survival.

What would these founders think of "Eight is Great"? Of 3.5 million fake accounts? Of employees crying in bathroom stalls and vomiting from stress? Wells fought in the Civil War, surviving Confederate capture and 18 months in Libby Prison. Fargo built a business empire through multiple financial panics. They understood pressure. But they would have been baffled by pressure applied not by external forces but by the company against its own employees and customers.