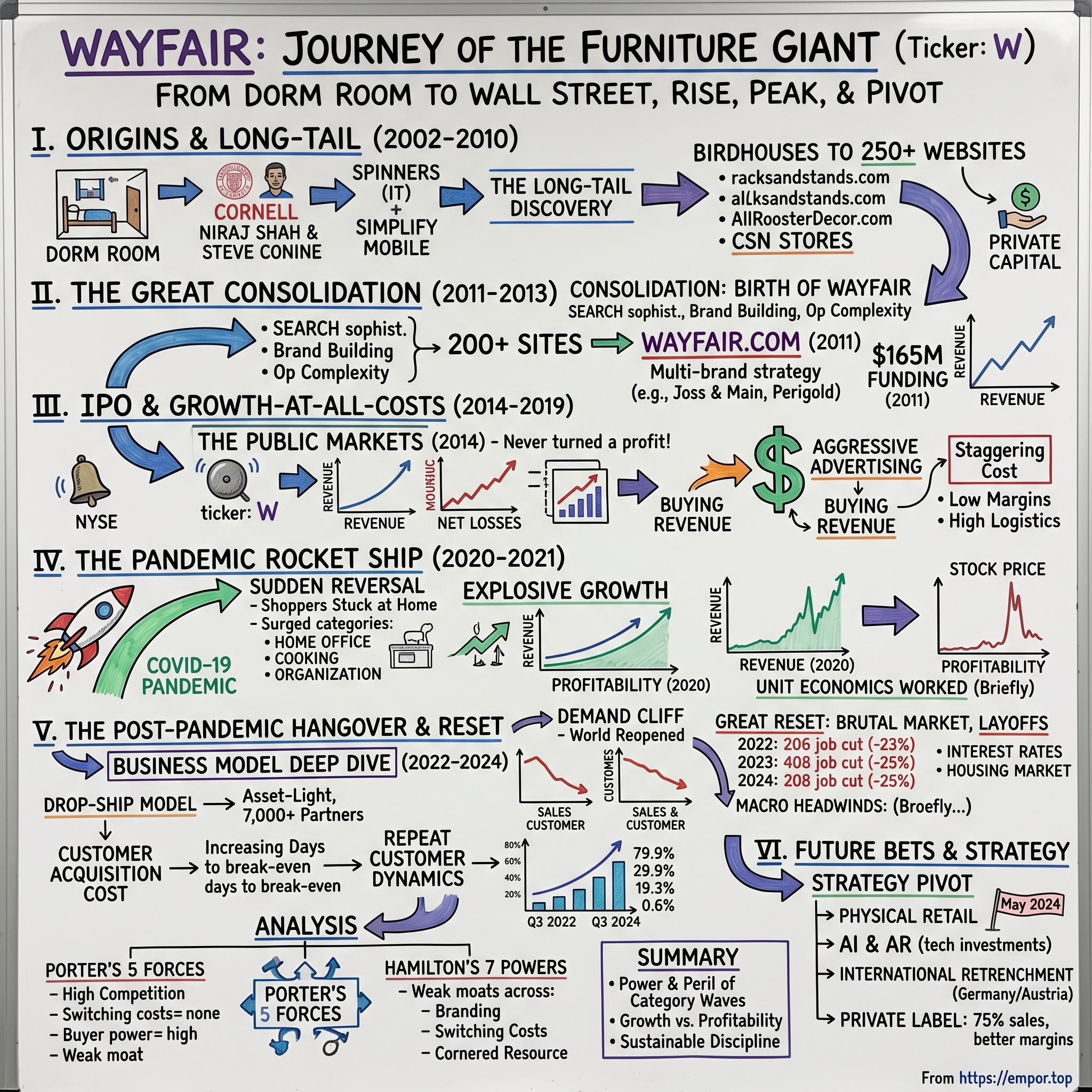

Wayfair: From Dorm Room to Wall Street—The Rise, Peak, and Pivot of E-Commerce's Furniture Giant

I. Introduction & Episode Roadmap

[5 minutes]

Wayfair stands today as one of the world's largest online furniture retailers, with $11.8 billion in net revenue for the twelve months ended September 30, 2024. The company's journey from a Cornell dorm room to the New York Stock Exchange represents one of the most dramatic narratives in e-commerce history—a tale of entrepreneurial vision, aggressive expansion, pandemic-driven euphoria, and ultimately, a painful reckoning with the fundamental economics of online retail.

How did two Cornell engineers build 250+ websites, consolidate them into one brand, survive the post-pandemic reckoning, and struggle to find sustainable profitability? This is the story of Wayfair—a company that mastered the art of growth but has struggled with the science of profit.

The episode structure follows Wayfair's evolution through distinct phases: from the early days as CSN Stores operating hundreds of niche websites to the great consolidation under the Wayfair brand, the IPO and growth-at-all-costs era, the pandemic rocket ship that briefly made profitability possible, and the post-pandemic hangover that continues to challenge the company today.

Key themes emerge throughout: the power and peril of long-tail e-commerce, the seductive trap of growth-at-all-costs, and the fundamental challenge of achieving profitability in a low-margin, high-logistics-cost business.

II. Cornell Origins & The Entrepreneurial Bug

[8 minutes]

The Wayfair story begins not in a garage or a basement, but in the dormitories of Cornell University. Niraj Shah and Steve Conine met during a special six-week summer program for high school students at Cornell, discovering they lived just a few doors away from each other in their freshman dorm. This proximity would forge a partnership that would last decades.

Both took Professor David BenDaniel's popular entrepreneurship class, a course that would fundamentally alter their trajectories. Shah had been headed to graduate school or law school, while Conine was on track to join his family's business. But after writing a business plan for that class assignment, they caught the entrepreneurial bug that would define their careers.

Their first venture together was Spinners, a small IT services firm based on that classroom business plan. The company grew to employ 40 people before being sold to global tech firm iXL during the heady days of the dot-com boom. The duo then founded Simplify Mobile, an early developer of software for mobile phones, which they sold to a telecommunications company.

Shah's personal story adds another dimension to the Wayfair narrative. He grew up in Pittsfield, Massachusetts, the son of immigrants from India. His grandfather ran a steel manufacturing business in India, making pots and pans. His father worked for General Electric as a mechanical engineer and, after retirement, joined Wayfair early on, providing financial advice. This immigrant success story would become part of Wayfair's cultural DNA.

III. The Long-Tail Discovery: From Birdhouses to 250 Websites (2002-2010)

[12 minutes]

After their early successes, Shah and Conine made a counterintuitive discovery that would define their next venture. They decided their bigger opportunity wasn't actually big at all—it was rather small: birdhouses. The entrepreneurs were observing niche businesses popping up across the web, recognizing a pattern before the term "long tail" was even coined to describe products that lack mass appeal but represent a sizable market on a global scale.

The logic was compelling: it wouldn't make sense to set up a brick-and-mortar shop that only sells birdhouses, but when you have access to the entire world as a potential customer base, a birdhouse shop could make a tidy profit catering to that long tail.

In August 2002, Shah and Conine founded what would become Wayfair as a two-person company with a makeshift headquarters in Conine's nursery in Boston, Massachusetts. Originally known as CSN Stores, the pair bought the domain name "racksandstands.com," which sold only entertainment furniture. By December 2002, the company made $250,000 in sales.

The niche website explosion that followed was remarkable. The company established a roster of more than 200 niche e-commerce sites with names that seem outlandish in today's formalized e-commerce landscape, including HotPlates.com and AllRoosterDecor.com. Each site merchandised products based on a narrow theme, like TV stands, grandfather clocks, and stamps.

In 2003, the company added patio and garden goods suppliers, three online stores, and more than a dozen employees, moving its headquarters to an office on Newbury Street in Boston. Over the next two years, it expanded its catalog to include home décor; office, institutional, and kitchen and dining furniture. The Boston Business Journal ranked it the #1 fastest-growing private e-commerce company in Massachusetts, and the #4 fastest-growing private company overall.

IV. The Great Consolidation: Birth of Wayfair (2011)

[10 minutes]

By 2011, CSN Stores owned over 200 online shops—largely niche shops for specific products, like cookware.com, everyatomicclock.com, and strollers.com. The proliferation of sites had served its purpose in capturing long-tail demand, but the model was becoming increasingly unwieldy. Shah and Conine recognized that to scale effectively, they needed to direct traffic to a single site and unify the company aesthetic.

The strategic pivot to consolidation was driven by multiple factors. Search engine optimization was becoming more sophisticated, and maintaining hundreds of separate sites was increasingly inefficient. Brand building was nearly impossible across so many properties. Operational complexity was mounting, from inventory management to customer service.

In June 2011, the company raised $165 million in funding from Battery Ventures, Great Hill Partners, HarbourVest Partners and Spark Capital. This war chest would fund the transformation. The company rebranded CSN Stores as Wayfair—a name chosen by a branding firm, with no particular meaning beyond its pleasant sound and available domain.

Wayfair.com launched on September 1, 2011, marking a new era for the company. But the consolidation wasn't just about bringing everything under one roof. At the end of 2010, the company had launched Joss & Main, a members-only online store focused on flash sales and curated collections. This would become the template for a multi-brand strategy within a unified operational structure.

The technology and quantitative approach that had served the company well continued under the new structure. They used paid media tools from Google and Yahoo to advertise against very specific keywords, track where traffic was coming from, and make judgments about what was working based on incoming search data. This data-driven approach would become a hallmark of Wayfair's operations.

V. The IPO & Growth-at-All-Costs Era (2014-2019)

[15 minutes]

The path to public markets began in March 2014 when T. Rowe Price led a $157 million pre-IPO financing, valuing the company at more than $2 billion. This set the stage for one of the most controversial IPOs of the decade.

In October 2014, Wayfair raised over $300 million through an IPO on the New York Stock Exchange under the ticker symbol W. The price talk was $25-$28, but the stock opened at $29 and closed at $37.72, up 30 percent—a remarkable performance for a company that had never turned a profit.

The IPO sparked intense debate on Wall Street. How could a company that doesn't make any profits command such a valuation? The answer lay in the growth narrative. Even though the company wasn't making money, it was increasing revenues at about 35 percent a year. In a world starved for growth, investors were willing to pay up for it. And for big growth, like 35 percent a year, they would pay up big.

As of January 2014, Wayfair had become the largest online-only retailer for home furniture in the United States. The revenue trajectory was impressive: $380 million in 2010, over $500 million in 2011, over $600 million in 2012, over $900 million in 2013, and over $1.3 billion in 2014. The growth continued: net revenue increased to $2.25 billion in 2015, $3.4 billion in 2016, and $4.7 billion in 2017.

But this growth came at a staggering cost. In 2019, Wayfair spent $1.1 billion on advertising, which represented about 12% of total revenue. The company was essentially buying revenue through massive marketing expenditures, a strategy that worked as long as capital remained cheap and investors remained patient.

The results were predictable: since 2014, when the company entered the public markets, Wayfair failed to report an annual net profit in every year but one: 2020. In the fiscal year ended December 31, 2019, the company reported a net loss of $985 million. The growth-at-all-costs mentality had created a business that could scale revenue but couldn't generate sustainable profits.

VI. The Pandemic Rocket Ship (2020-2021)

[18 minutes]

The COVID-19 pandemic initially looked like it might destroy Wayfair. In February 2020, the company cut 3% of its workforce, or about 500 jobs, because of mounting losses. By mid-March, the stock was down over 70% for the year. The future looked bleak.

Then came the sudden reversal that nobody saw coming. As lockdowns spread across the globe and consumers found themselves stuck at home, Wayfair became an unexpected beneficiary. From April 1 to May 5, 2020, online sales surged 90% year over year. The company that had been struggling to justify its existence suddenly found itself at the center of a new economy.

Sales increased 20.1% to reach $2.33 billion in the first quarter ended March 31, 2020, up from $1.94 billion in Q1 2019. Sales from January to mid-March were growing in the mid-teen range, but the final two weeks of the quarter saw explosive growth as panic buying set in.

The category winners were predictable but dramatic. Shoppers were buying home office furnishings as remote work became the norm, products for cooking at home as restaurants closed, organization products as people spent more time in their spaces, and children's playroom and furniture products as schools went virtual.

Both Wayfair and peer Etsy became havens for consumers trying to weather the pandemic, resulting in two straight quarters of triple-digit revenue growth at Etsy and Wayfair's fastest expansion since going public in 2014. The transformation was remarkable—a company that had been written off was suddenly a pandemic winner.

The stock market responded with euphoria. Shares of both Etsy and Wayfair surged more than 170% for the year. By the end of 2020, both stocks were up over 180%. Wayfair's market cap topped $24 billion, a stunning reversal from its March lows.

Most importantly, the pandemic achieved what years of growth initiatives couldn't: profitability. For the first and only time in its history as a public company, Wayfair reported an annual net profit in 2020. The combination of surging demand and reduced marketing spend (as organic traffic soared) created a brief window where the unit economics actually worked.

VII. The Post-Pandemic Hangover & Great Reset (2022-2024)

[20 minutes]

The pandemic boom was always unsustainable, but the speed and severity of the reversal caught many by surprise. As the world reopened and stimulus checks stopped flowing, Wayfair faced a demand cliff. Sales declined 15% year-over-year in the second quarter of 2022. The brand lost 24% of its active customers. Overall, Wayfair posted a net loss of $378 million during the quarter.

The stock market's reaction was brutal. Wayfair's shares lost about 70% of their value by the start of 2022. The company that had briefly been worth over $24 billion saw its market capitalization collapse as investors fled.

Management's response was a cascade of layoffs that would define this era: - August 2022: Wayfair cut nearly 900 jobs, or about 5% of its global workforce - January 2023: A significant round of layoffs eliminated 1,750 jobs, or 10% of its workforce - January 2024: Another 1,650 employees were let go, amounting to 13% of its global workforce

These actions were expected to deliver annualized cost savings of more than $280 million, but they came at a significant human cost. CEO Niraj Shah's messaging during this period became controversial, with leaked memos calling for employees to work harder and "negotiate aggressively" with suppliers.

The broader context made recovery even more challenging. The furniture and home sector fell 7.5% year over year in January 2024. Rising interest rates crushed the housing market, which historically drives furniture sales. Competition intensified as retailers like Ikea and Walmart plotted expansions in the U.S., recognizing the opportunity to take share from a weakened Wayfair.

By Q3 2024, the company reported total net revenue of $2.9 billion, down 2.0% year over year, with 21.7 million active customers, a 2.7% decrease year-over-year. Orders delivered in the quarter totaled 9.3 million, a 6.1% decline from the previous year, though the average order value rose to $310 from $297 in Q3 2023.

VIII. The Physical Retail Experiment & Future Bets

[8 minutes]

In a striking reversal of its digital-only origins, Wayfair opened its first non-outlet, Wayfair-branded physical location in May 2024 at Edens Plaza in Wilmette, Illinois. This marked a fundamental shift in strategy for a company that had built its entire identity around being online-only.

The physical retail push extends beyond the flagship Wayfair brand. The company has expansion plans including new locations in Atlanta and Denver next year, and New York in 2027. Wayfair also opened its first Perigold store in Houston, with a second coming to West Palm Beach.

Technology investments remain central to Wayfair's strategy. The company continues to invest in augmented reality tools that allow customers to visualize furniture in their homes, AI-powered recommendation engines, and proprietary logistics systems. The goal is to solve the fundamental challenge of selling furniture online: helping customers buy products they can't physically touch or sit on.

The international strategy has taken a dramatic turn. In January 2025, Wayfair announced its withdrawal from the German and Austrian markets, leading to layoffs of an estimated 730 positions or 3% of its global workforce. CFO Kate Gulliver explained that the company's aim was to grow market share where the potential return on investment was higher.

The specialty brand strategy continues to evolve. Beyond the flagship Wayfair brand, the company operates Birch Lane (traditional and farmhouse styles), AllModern (contemporary furniture), Joss & Main (stylish designs at accessible prices), and Perigold (luxury home goods). Each brand targets a different customer segment, but all leverage the same operational infrastructure.

IX. Business Model Deep Dive & Unit Economics

[12 minutes]

Wayfair's business model centers on the drop-ship approach, with approximately 95% of products in home/garden categories and 95% fulfilled through drop shipping with 7,000 merchant partners. This asset-light model means Wayfair doesn't hold most inventory, reducing capital requirements but also limiting control over the customer experience.

The customer acquisition cost problem has plagued Wayfair throughout its history. Management stated that in 2013 it took 123 days to reach contribution break-even for new customers compared to 77 days for the same break-even point in 2011. In essence, Wayfair was spending twice as much to acquire new customers than it did just two years earlier, and this trend has largely continued.

Repeat customer dynamics offer some hope. In 2019, more than half (54%) of Wayfair.com orders were from shoppers who made three or more purchases. By the first quarter of 2020, repeat shoppers placed nearly 70% of orders, up from 66% in Q1 2019. By Q3 2024, repeat customers placed 79.9% of total orders delivered.

The private label strategy has become increasingly important. Approximately 75% of Wayfair's sales come from its house or private-label brands. These products offer higher margins and greater control over quality and design, but also require more investment in product development and quality control.

The advertising treadmill problem remains Wayfair's fundamental challenge. The company must continuously spend heavily on advertising to maintain revenue growth, but this spending makes profitability elusive. When advertising is reduced, revenue quickly declines, creating a vicious cycle that has trapped the company since its inception.

LTM net revenue per active customer was $545 as of September 30, 2024, showing that while Wayfair has succeeded in increasing customer value, the cost to acquire and retain these customers remains stubbornly high.

X. Porter's 5 Forces & Hamilton's 7 Powers Analysis

[15 minutes]

Porter's 5 Forces:

Threat of New Entrants: The e-commerce landscape presents low technical barriers to entry, but achieving scale requires massive capital for logistics and marketing. New entrants can easily launch online furniture stores, but competing with Wayfair's selection and logistics network requires billions in investment.

Bargaining Power of Suppliers: With 7,000+ suppliers, Wayfair has significant leverage over individual vendors. The company's scale allows it to negotiate favorable terms, and suppliers depend on Wayfair for access to customers. However, suppliers can also sell through Amazon and other channels, limiting Wayfair's power.

Bargaining Power of Buyers: Extremely high. Customers can easily compare prices across multiple sites, switching costs are zero, and furniture purchases are infrequent. Price transparency and infinite choice give consumers unprecedented power.

Threat of Substitutes: Traditional retail stores, Amazon's growing furniture selection, and direct-to-consumer brands all represent viable substitutes. The rise of social commerce and manufacturer-direct sales further intensifies this threat.

Competitive Rivalry: Intense and increasing. Amazon continues expanding its furniture offerings, traditional retailers like Walmart and Target have strengthened their online presence, and specialty e-tailers compete for the same customers. Price competition is fierce, and differentiation is minimal.

Hamilton's 7 Powers:

Scale Economies: Wayfair possesses some scale advantages in logistics and advertising efficiency, but these haven't translated to sustainable profitability. The scale benefits are offset by the need for continuous marketing spend.

Network Effects: Limited. While there are some supplier network effects (more suppliers attract more customers, which attracts more suppliers), these are weak compared to true platform businesses.

Counter-Positioning: Initially, Wayfair counter-positioned against traditional furniture retail by offering infinite selection online. Now, it's being counter-positioned by newer models like direct-to-consumer brands and social commerce.

Switching Costs: Virtually none for consumers. Customers can easily shop elsewhere with no penalty, making retention expensive and difficult.

Branding: Weak power. Despite spending billions on marketing, Wayfair hasn't built a brand that commands premium pricing or strong loyalty. The market remains highly commoditized.

Cornered Resource: No significant exclusive assets. Wayfair doesn't own unique technology, exclusive supplier relationships, or proprietary products that competitors can't replicate.

Process Power: Some advantages in logistics and technology operations, but these are replicable with sufficient investment. Wayfair's processes are good but not uniquely valuable.

XI. Bear vs. Bull Case

[10 minutes]

Bear Case:

The bear thesis on Wayfair rests on structural challenges that appear insurmountable. The business model seems fundamentally unprofitable—customer acquisition costs remain too high, lifetime values too low, and competition too intense. Without the artificial boost of pandemic demand, the company has returned to losing money.

The competitive landscape continues to deteriorate. Amazon's furniture business grows stronger, traditional retailers have successfully adapted to e-commerce, and new direct-to-consumer brands bypass Wayfair entirely. The company lacks any meaningful moat or differentiation beyond selection, which competitors can match.

Home category headwinds could persist for years. High interest rates have crushed home sales, and even when rates fall, demographic trends suggest fewer household formations. The work-from-home boom that drove furniture sales has reversed, with many workers returning to offices.

The balance sheet remains concerning despite cost cuts. With over $3 billion in debt and continued losses, Wayfair has limited financial flexibility. Another economic downturn could prove existential.

Bull Case:

The bull thesis sees Wayfair as the largest pure-play in a massive market that's still early in its digital transformation. Online furniture penetration remains around 20% of total sales, suggesting significant room for growth as consumers become more comfortable buying furniture online.

Management has demonstrated an ability to scale revenue to nearly $12 billion annually and is showing newfound discipline on costs. As CEO Niraj Shah noted, the company achieved "a mid-single-digit Adjusted EBITDA margin for the second quarter in a row" and remains "laser-focused on delivering healthy profitability while setting ourselves up for success as the category rebounds".

Technology and logistics investments are creating real advantages. The company's AR tools, recommendation engines, and delivery network represent billions in cumulative investment that new entrants can't easily replicate. These capabilities should drive improving unit economics over time.

S&P now forecasts Wayfair's leverage will be 3.4x for 2025, significantly better than its previous forecast of 4.3x, suggesting improving financial health. The rating agency sees the marketplace model keeping prices competitive despite inflation pressures.

Category penetration remains low with significant upside. As younger consumers who are comfortable buying everything online age into prime furniture-buying years, Wayfair is well-positioned to capture this demand.

XII. Playbook: Key Lessons

[8 minutes]

The Wayfair story offers crucial lessons for entrepreneurs and investors alike:

The power and peril of riding category waves: Wayfair rode the e-commerce wave brilliantly in its early years, then caught the pandemic wave at just the right moment. But waves eventually crash, and companies built on temporary tailwinds often struggle when conditions normalize.

Why unit economics matter more than growth: The market's 2010s obsession with growth at all costs enabled Wayfair to raise billions despite persistent losses. But eventually, physics reasserts itself—businesses must generate more value than they consume.

The challenge of building moats in commoditized markets: Despite spending billions on technology and marketing, Wayfair never built a defensible competitive position. In commoditized markets, scale alone isn't enough.

The importance of financial discipline before crisis hits: Wayfair's pandemic profitability proved the business could work with discipline, but old habits returned quickly. Companies must build sustainable practices during good times, not wait for crisis.

When to consolidate vs. stay fragmented: The decision to consolidate 250 websites into Wayfair was correct for its time, enabling the IPO and subsequent growth. But it also eliminated the focus and efficiency of the niche model.

The danger of mistaking temporary tailwinds for permanent shifts: Wayfair and investors convinced themselves that pandemic behaviors represented a permanent acceleration of e-commerce adoption. This misread led to over-hiring, over-spending, and ultimately, painful corrections.

XIII. Epilogue & Final Thoughts

[5 minutes]

Wayfair stands today at a crossroads. With Q3 2024 net revenue of $2.9 billion and 21.7 million active customers, the company remains a major force in online furniture retail. Yet the path to sustainable profitability remains elusive, with a net loss of $74 million in Q3 2024 despite years of cost-cutting and optimization efforts.

The broader e-commerce reckoning post-pandemic has been particularly harsh for Wayfair. The company that epitomized growth-at-all-costs now symbolizes the dangers of that approach. While competitors with physical stores benefited from omnichannel strategies, Wayfair's digital-only model—once its greatest strength—became a limitation.

For Wayfair to thrive again, several things must align. The housing market must recover, driving furniture demand. The company must continue improving unit economics without sacrificing growth. Competition must stabilize, allowing for rational pricing. And management must maintain cost discipline while investing in differentiation.

The ultimate question remains: Was Wayfair simply a timing play that got too big? The company brilliantly identified and exploited the long-tail e-commerce opportunity, scaled impressively through the 2010s, and briefly achieved the holy grail of profitability during the pandemic. But without a true moat or differentiated value proposition, Wayfair may be destined to remain a subscale player in an increasingly competitive market.

The lessons for the next generation of e-commerce entrepreneurs are clear. Growth is intoxicating, but profitability is essential. Scale provides advantages, but only if unit economics work. And perhaps most importantly, building a sustainable business requires more than riding waves—it requires creating lasting value that transcends temporary market conditions.

Wayfair's story isn't over. With its brand recognition, customer base, and operational capabilities, the company has the assets to potentially engineer a successful transformation. But time is running short, competition is intensifying, and the margin for error continues to shrink. Whether Wayfair becomes a cautionary tale or a comeback story will be determined in the months and years ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube