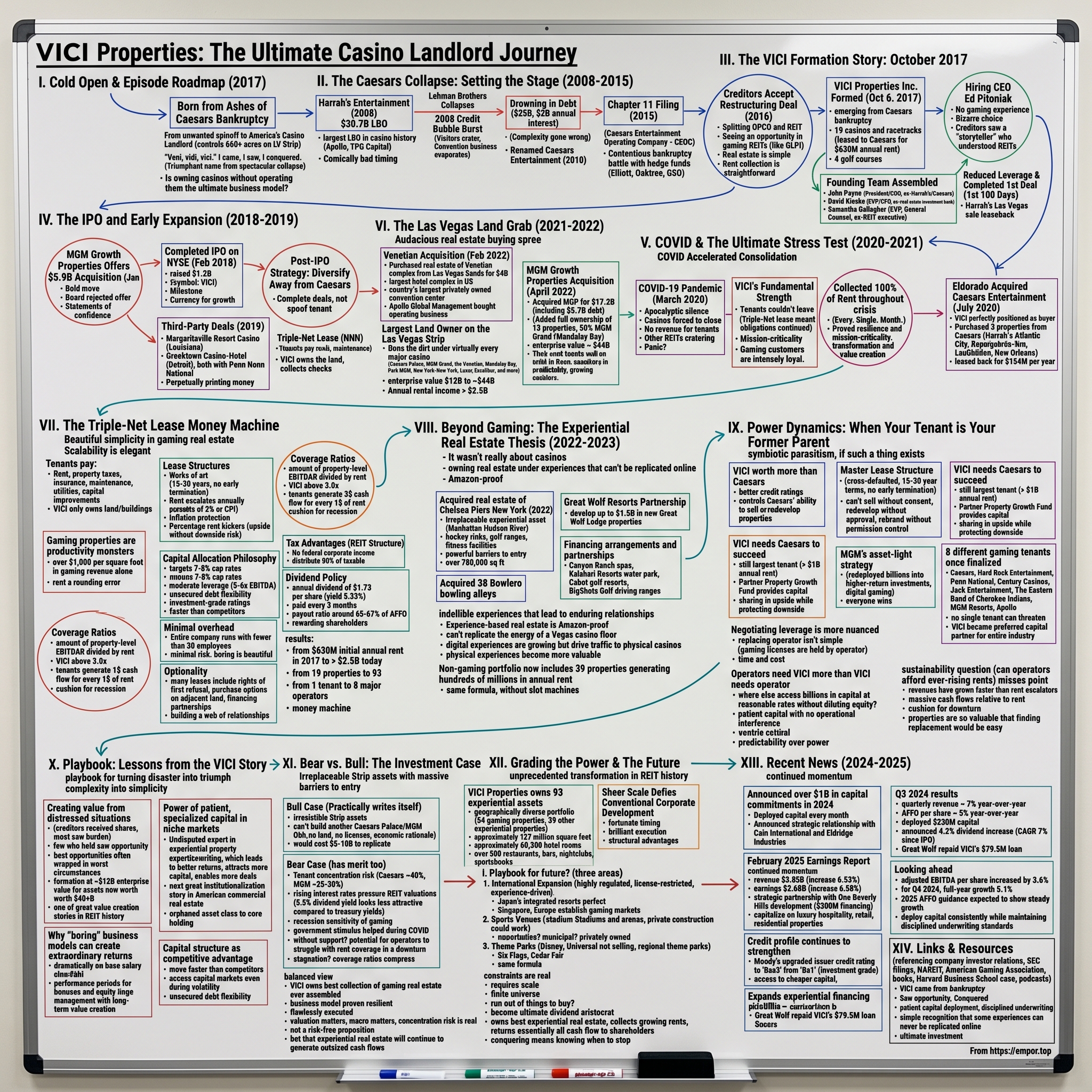

VICI Properties: From Bankruptcy Spinoff to America's Casino Landlord

I. Cold Open & Episode Roadmap

The name tells you everything and nothing at once. VICI—pronounced "VEE-chee"—comes from Julius Caesar's immortal boast: "Veni, vidi, vici." I came, I saw, I conquered. It's a curiously triumphant name for a company born from the ashes of one of corporate America's most spectacular bankruptcies. Yet somehow, it fits perfectly.

Picture this paradox: In October 2017, creditors of the collapsed Caesars Entertainment were handed ownership of a hodgepodge of casino properties they never wanted, structured as a real estate investment trust nobody asked for. The distressed debt investors who ended up with VICI shares weren't celebrating—they were trying to figure out how to dump this strange spinoff as quickly as possible. Fast forward to today, and VICI Properties controls over 660 acres of the Las Vegas Strip, owns the land under Caesars Palace, MGM Grand, and the Venetian, and has quietly become one of the most successful REITs in America. With a market cap of approximately $34 billion, VICI has become the ultimate landlord play in American gaming—a company that owns the casinos without operating them, collects the rent without dealing with the drunk bachelor parties, and somehow turned a bankruptcy restructuring into one of the most compelling REIT stories of the last decade.

Here's the big question we're exploring: Is owning casinos without operating them the ultimate business model? When you strip away the slot machines, the free drinks, and the complicated regulatory compliance, what you're left with might just be the perfect real estate play—trophy assets that can't be replicated, tenants who literally can't move, and a business model so simple that even the most distressed creditors couldn't mess it up.

The journey from unwanted spinoff to Strip landlord is a masterclass in turning lemons into a very expensive lemonade stand. It's a story about patient capital, the power of specialization, and why sometimes the best businesses are born not from grand visions, but from the messy realities of restructuring. As we'll see, VICI didn't conquer—it simply outlasted, out-executed, and out-thought everyone else in the room.

II. The Caesars Collapse: Setting the Stage

To understand VICI, you have to understand the spectacular disaster that birthed it. In January 2008, at the absolute peak of the credit bubble, Apollo Global Management and TPG Capital pulled off what seemed like the deal of the century: acquiring Harrah's Entertainment for $30.7 billion, including debt. It was the largest leveraged buyout in casino history. Within months, it would become one of the worst-timed deals in private equity history.

The timing was almost comically bad. Lehman Brothers collapsed eight months later. Las Vegas visitor volumes cratered. Convention business evaporated. The company—renamed Caesars Entertainment in 2010—was drowning in $25 billion of debt, paying $2 billion annually just in interest. The capital structure looked like a Jenga tower designed by someone who'd had too many complimentary casino drinks: senior debt, subordinated debt, mezzanine financing, and equity stakes scattered across multiple entities. By January 2015, Caesars Entertainment Operating Company (CEOC), the company's largest subsidiary, filed for Chapter 11, setting up one of the most contentious bankruptcy battles in corporate history. The proceedings pitted aggressive and deep-pocketed distressed debt hedge funds—including Elliott Management, Appaloosa Management, Oaktree Capital, and GSO Capital Partners—against private equity owners Apollo and TPG.

The bankruptcy was a masterclass in corporate complexity gone wrong. The company's high leverage and complicated ownership structure made the bankruptcy proceedings messy and contentious. By 2016, the company's junior creditors agreed to a restructuring deal, which called for the separation of Caesar's assets into two separate companies. The creditors had endured years of watching Apollo and TPG try every financial engineering trick in the book—asset shuffles, guarantee releases, and what some called "Good Caesars/Bad Caesars" maneuvers.

But here's where the story takes an unexpected turn. Gaming REITs weren't a new concept. In 2013, Penn National Gaming had spun off Gaming and Leisure Properties (GLPI), proving that separating casino real estate from operations could work. The creditors saw an opportunity: instead of trying to run casinos—a business they knew nothing about—they could own the dirt underneath them. Real estate is simple. Rent collection is straightforward. And casinos, unlike retail stores or office buildings, literally cannot pick up and move.

In September 2016, junior creditors agreed to a restructuring deal that included separation of the operating company and a real estate trust with land and building assets. Junior creditors would receive equity and debt in both entities. The creditors weren't celebrating—they just wanted to salvage whatever value they could from this disaster. Little did they know they were about to create one of the most successful REITs of the next decade.

III. The VICI Formation Story: October 2017

The waning days of September 2017 found a group of distressed debt creditors staring at a problem they never anticipated: they needed to name and staff a real estate company they never wanted to own. VICI Properties Inc. was formally born on October 6, 2017, emerging from the Caesars bankruptcy with nineteen casinos and racetracks, all leased back to Caesars at an initial annual rent of $630 million, plus four golf courses that nobody quite knew what to do with.

The creditors' first masterstroke was hiring Edward Pitoniak as founding CEO—a choice that seemed bizarre at first glance. Pitoniak had never worked in gaming. His background was a patchwork quilt of experiences: nine years as a magazine editor culminating as editor-in-chief of Ski Magazine, nearly eight years at ski resort operator Intrawest, and a string of Canadian hospitality REIT turnarounds. But the creditors saw something others missed: "The craft of creating a compelling story is partly founded on thinking long and hard about what people don't know, that they would benefit from knowing," Pitoniak would later explain. VICI didn't need a casino operator—it needed a storyteller who could make institutional investors understand why owning casino real estate was fundamentally different from running casinos. Pitoniak assembled a founding team that balanced casino knowledge with REIT expertise. John Payne, an executive who spent decades in operations at Harrah's and then Caesars, was named President and COO; David Kieske, a former real estate investment banker, was hired as EVP, CFO; and Samantha Gallagher, a former law firm partner and REIT executive with extensive REIT and public company experience, was named EVP, General Counsel. Payne had actually served as CEO of Caesars Entertainment Operating Company during the bankruptcy—he knew where every skeleton was buried. Kieske brought the Wall Street credibility from his years at real estate investment bank Eastdil. Gallagher understood the intricate dance of REIT governance and capital markets.

The challenge facing this team was monumental. VICI had no natural investor base and no readily available pool of capital to access at a time when it was highly levered, without a board, without a CEO, without a track record, and without a strategy. Gaming REITs were still a nascent category. Most of VICI's original owners—the distressed debt investors—were looking to exit their investment, not provide additional capital.

Given the circumstances of its formation, VICI began with a complex and highly leveraged capital structure. Yet, within its first 100 days, the management team was able to significantly reduce VICI's leverage ratio and complete its first sale leaseback transaction for the real estate of Harrah's Las Vegas. This wasn't just financial engineering—it was a statement of intent. VICI could execute deals, reduce leverage, and generate cash flow even while emerging from the chaos of bankruptcy.

The first 100 days set a pattern that would define VICI's trajectory: move fast, be opportunistic, and turn complexity into simplicity. While other REITs spent months analyzing deals, VICI was closing them. While competitors worried about the stigma of bankruptcy origins, Pitoniak was crafting a narrative about transformation and value creation. The creditors who had reluctantly become real estate owners were starting to realize they might have stumbled into something special.

IV. The IPO and Early Expansion (2018-2019)

January 2018 opened with a dramatic flourish. MGM Growth Properties, the REIT affiliated with Caesars competitor MGM Resorts International, offered to acquire VICI for an estimated $5.9 billion—about $19.50 per share. It was a bold move to consolidate the gaming REIT space before VICI could establish itself. But VICI's board, advised by Pitoniak's team, saw something MGM didn't: the potential for a much bigger story.

MGM Growth Properties, a REIT affiliated with Caesars competitor MGM Resorts International, offered in January 2018 to acquire Vici for an estimated $5.9 billion. Vici's board rejected the offer, deciding instead to proceed with a planned initial public offering. The rejection was a statement of confidence—or perhaps hubris. Here was a company barely three months out of bankruptcy turning down a premium offer.

Vici completed its IPO on the New York Stock Exchange in February 2018, raising $1.2 billion. The offering priced at $20 per share, right at the midpoint of the expected range, with 60.5 million shares sold. For a company with no operating history as a public REIT, no analyst coverage, and the stigma of bankruptcy origins, it was a remarkable achievement. The IPO gave VICI the currency it needed—both literal capital and the credibility of public market validation.

The post-IPO strategy was simple but brilliant: diversify away from Caesars as quickly as possible without spooking the tenant that provided most of the rent. Vici completed two transactions with Caesars in 2018, purchasing the Octavius Tower at Caesars Palace for $508 million and Harrah's Philadelphia for $242 million, and leasing them back to Caesars for $35 million and $21 million per year, respectively. These deals served dual purposes: they showed Caesars that VICI could be a source of capital, not just a landlord, while proving to investors that the relationship could generate incremental growth.

But the real breakthrough came with third-party deals. In 2019, Vici made two purchases in conjunction with Penn National Gaming. Vici bought the real estate of the Margaritaville Resort Casino in Louisiana and Greektown Casino–Hotel in Detroit for $261 million and $700 million, respectively, with Penn operating the properties under long-term leases.

The triple-net lease model was the secret sauce that made everything work. Under these agreements, tenants paid not just rent but also property taxes, insurance, and maintenance—essentially everything except the mortgage. VICI's role was beautifully simple: own the land, collect the checks, and let someone else deal with the drunk bachelor parties and regulatory headaches. The leases typically ran 15-20 years with automatic rent escalators tied to inflation or a fixed percentage, whichever was higher. It was as close to a perpetual money machine as real estate gets.

By the end of 2019, VICI had transformed from a captive Caesars landlord to a diversified gaming REIT with multiple tenants and a growing pipeline of opportunities. The company that nobody wanted in 2017 was becoming the buyer everyone wanted to sell to. The stage was set for what should have been continued steady growth. Then March 2020 happened.

V. COVID & The Ultimate Stress Test (2020-2021)

March 17, 2020: Nevada Governor Steve Sisolak orders all casinos to close. Within days, every gaming property in America shuts down. For an industry that operates 24/7/365, where the lights never dim and the slots never stop spinning, the silence was apocalyptic.

VICI's executive team gathered for what should have been a panic meeting. They owned $12 billion worth of casino real estate. Their tenants had zero revenue. Hotel REITs were already announcing they couldn't collect rent. Shopping mall REITs were negotiating deferrals. The conventional wisdom was clear: gaming REITs were toast.

But here's what everyone missed: casino operators couldn't leave. A retail tenant can abandon a store and open somewhere else. An office tenant can go remote. But where exactly was Caesars Palace going to move? To the empty lot next door that doesn't exist? The triple-net lease structure meant tenants were obligated to maintain the properties even if closed. And most importantly, casino licenses are tied to specific physical locations—you can't just pick up a gaming license and move it down the street.

Despite the COVID-19 pandemic's impact on the gaming industry, VICI demonstrated resilience by collecting 100% of its rent throughout the crisis. Every. Single. Month. VICI ended 2020 with 100% rent collection across its diverse tenant base. While mall REITs collected 50% of rent and hotel REITs saw collections crater, VICI never missed a payment.

President John Payne was characteristically blunt about it: "While many of you enjoy asking questions about on the ground operating trends, I would like to remind you that we are a triple-net lease landlord. We collect fixed rent streams with annual escalations over very long periods of time. Those who have followed our story will recall that we continued to collect 100 percent of cash rent when every one of our properties was forced to close".

The pandemic actually accelerated industry consolidation in VICI's favor. In July 2020, Eldorado Resorts acquired Caesars Entertainment, becoming Vici's primary tenant, and renamed itself to Caesars Entertainment. The merger required asset sales for regulatory approval, and VICI was perfectly positioned as the buyer. In connection with this acquisition, Vici bought three properties (Harrah's Atlantic City, Harrah's Laughlin, and Harrah's New Orleans) from Caesars for a total of $1.8 billion, and leased them back to the new Caesars for $154 million per year.

CEO Ed Pitoniak summed up the COVID experience with characteristic understatement: "Thanks to our tenants' operating excellence and liquidity, thanks to the intense loyalty gaming customers have to the gaming experience, and thanks to the mission-criticality of our assets, VICI's business model has proven itself".

The stress test revealed a fundamental truth: gaming real estate wasn't just resilient—it was essentially irreplaceable. Properties that had been valued based on cash flow multiples were actually worth far more as scarce, licensed assets that couldn't be replicated at any price. The pandemic that should have destroyed VICI instead proved its thesis: own the dirt under experiences people can't get anywhere else, and you'll always get paid.

VI. The Las Vegas Land Grab (2021-2022)

The post-pandemic period saw VICI execute one of the most audacious real estate buying sprees in American history. While other REITs were still licking their wounds, VICI went shopping for the crown jewels of American gaming.

The first mega-deal dropped in March 2021: Vici purchased the real estate of the Venetian complex from Las Vegas Sands in February 2022 for $4 billion. The acquisition included the Venetian and Palazzo casino hotels and the Sands Expo convention center. Apollo Global Management bought the operating business and leased the property from Vici for $250 million per year.

The Venetian acquisition was transformative on multiple levels. This wasn't just another casino—it was the largest hotel complex in the United States and included the country's largest privately owned convention center. Las Vegas Sands, under pressure from activist investors and wanting to focus on Asia, was eager to sell. Apollo wanted to operate casinos without tying up capital in real estate. VICI sat in the middle, solving everyone's problem while collecting $250 million in annual rent.

But the Venetian deal was just the appetizer. In April 2022, VICI announced the acquisition that would nearly double its size: Vici acquired MGM Growth Properties for $17.2 billion (including $5.7 billion in assumed debt). The purchase added full ownership of thirteen properties to Vici's portfolio, and half ownership of the MGM Grand Las Vegas and Mandalay Bay resorts, and increased Vici's annual revenue by $1 billion, along with making it the largest land owner on the Las Vegas Strip, with over 660 acres.

The MGM Growth Properties deal was a masterclass in strategic positioning. MGM Resorts had created MGM Growth Properties as its own REIT in 2016, but the structure had become unwieldy. MGM wanted to be asset-light, focusing on operations and brand management rather than real estate ownership. VICI offered the perfect solution: take over the real estate, let MGM operate, everyone wins.

The consolidation didn't stop there. VICI then turned to Blackstone, which owned the other 50% stakes in MGM Grand and Mandalay Bay through a previous joint venture. In a deal that closed in early 2023, VICI bought out Blackstone's interests for $1.27 billion plus $1.5 billion in assumed debt, giving VICI full ownership of these trophy assets.

By the end of 2022, VICI owned the land under virtually every major casino on the Las Vegas Strip: Caesars Palace, MGM Grand, the Venetian, Mandalay Bay, Park MGM, New York-New York, Luxor, Excalibur, and more. The company that hadn't existed five years earlier now controlled over 660 acres of the most valuable entertainment real estate in America.

The numbers were staggering. VICI's enterprise value had grown from roughly $12 billion at its IPO to approximately $44 billion. Annual rental income exceeded $2.5 billion. The company owned properties with over 60,000 hotel rooms and 500 restaurants, bars, and nightclubs. It had become not just the largest gaming REIT but one of the largest REITs period.

What made this land grab possible wasn't just capital—it was timing and relationships. VICI had built trust with operators by being a reliable partner during COVID. While private equity firms might squeeze operators for higher rents, VICI understood that sustainable rents meant sustainable tenants. The company's triple-net lease model, with 15-30 year terms and built-in escalators, provided operators with certainty while giving VICI predictable, growing cash flows.

The transformation was complete. VICI had gone from unwanted bankruptcy spinoff to the landlord of the Las Vegas Strip. As one analyst put it: "They didn't just win the game—they bought the board."

VII. The Triple-Net Lease Money Machine

To understand VICI's dominance, you need to understand the beautiful simplicity of the triple-net lease model in the context of gaming real estate. It's a business model so elegant that it seems almost unfair.

Under a triple-net lease, the tenant pays everything: rent, property taxes, insurance, maintenance, utilities, even capital improvements. VICI's only job is to own the land and buildings. No employees to manage. No inventory to track. No customer service issues. Just collect rent checks and occasionally sign acquisition documents.

But here's what makes gaming properties perfect for this model: they're productivity monsters. A typical office building might generate $30-50 per square foot in rent. A good retail property might hit $60-100. The Venetian generates over $1,000 per square foot in gaming revenue alone, before counting rooms, food, or entertainment. When your tenant is printing that much money per square foot, paying $20-30 per square foot in rent is a rounding error.

The lease structures are works of art. Terms typically run 15-30 years with no early termination rights. Rent escalates annually at the greater of 2% or CPI, providing inflation protection. These leases are all long-term, often spanning decades, and have built-in annual rent increases that protect VICI from inflation. Many leases include percentage rent kickers if gaming revenues exceed certain thresholds, giving VICI upside participation without downside risk.

Coverage ratios—the amount of property-level EBITDAR (earnings before interest, taxes, depreciation, amortization, and rent) divided by rent—tell the story of sustainability. VICI's portfolio maintains coverage ratios above 3.0x, meaning tenants generate three dollars of cash flow for every dollar of rent. Even in a severe recession, there's substantial cushion before rent becomes unpayable.

The tax advantages of the REIT structure amplify returns. REITs pay no federal corporate income tax as long as they distribute 90% of taxable income to shareholders. This isn't a loophole—it's intentional policy designed to democratize real estate ownership. Instead of tax-inefficient corporate structures, REITs pass income directly to shareholders who pay tax at their individual rates.

VICI's capital allocation philosophy is boringly brilliant. The company targets acquisitions at 7-8% cap rates (net operating income divided by purchase price) in an environment where treasuries yield 4-5%. With leverage at 5-6x EBITDA and debt costs around 4-5%, the spread math is compelling. Buy at a 7.5% cap rate, finance at 4.5%, pocket the 300 basis point spread, multiply by billions of dollars. The dividend policy tells the story of disciplined capital allocation. VICI Properties has an annual dividend of $1.73 per share, with a yield of 5.33%. The dividend is paid every three months and the last ex-dividend date was Jun 18, 2025. With a payout ratio around 65-67% of AFFO (adjusted funds from operations), VICI retains enough capital to fund growth while rewarding shareholders with consistent income.

The beauty of the model is its scalability. Adding a new property doesn't require hiring hundreds of employees or building complex operating systems. VICI's entire company runs with fewer than 30 employees—that's less than one shift at a single casino. The overhead is minimal, the margins are exceptional (over 90%), and the growth is almost mechanical: acquire property, sign lease, collect rent, repeat.

But perhaps the most underappreciated aspect of VICI's model is optionality. Many leases include rights of first refusal on tenant property sales, purchase options on adjacent land, and financing partnerships that could convert to ownership. VICI isn't just collecting rent—it's building a web of relationships and rights that position it for decades of growth.

The numbers speak for themselves: from $630 million in initial annual rent in 2017 to over $2.5 billion today. From 19 properties to 93. From one tenant to eight major operators. It's not exciting. It's not innovative. It's just a money machine that compounds at mid-teens rates with minimal risk. Sometimes boring is beautiful.

VIII. Beyond Gaming: The Experiential Real Estate Thesis

By 2022, VICI had essentially conquered gaming real estate. The question became: what's next? The answer revealed the deeper insight behind VICI's strategy—it wasn't really about casinos at all. It was about owning real estate under experiences that can't be replicated online. In 2022, the company acquired the real estate of Chelsea Piers New York for $173 million and entered into a partnership with Great Wolf Resorts to develop up to $1.5 billion in new Great Wolf Lodge properties. VICI Properties has a growing array of real estate and financing partnerships with leading developers and operators in other experiential sectors, including Cabot, Cain International, Canyon Ranch, Chelsea Piers, Great Wolf Resorts, Homefield, Kalahari Resorts and Lucky Strike Entertainment.

The Chelsea Piers acquisition was particularly symbolic. Here was a property with zero gaming, located in Manhattan, with ice rinks, golf ranges, and fitness facilities. But it embodied the same principles as a casino: a unique location (28 acres on Manhattan's Hudson River), experiences you can't replicate online (try playing hockey over Zoom), and powerful barriers to entry (good luck finding another 28 acres of Manhattan waterfront). Comprised of over 780,000 square feet of real estate, Chelsea Piers is a truly irreplaceable experiential asset with state-of-the-art sports facilities, commercial space primarily used for production studios, three flexible and expansive event spaces, a marina and more.

The Great Wolf Resorts partnership revealed VICI's financing-to-ownership strategy. VICI provides construction financing at attractive rates (typically 7-9%) with purchase options upon completion. It's a brilliant model: VICI gets to evaluate the property's performance before committing to ownership while earning high yields during construction. If the property succeeds, VICI exercises its option. If not, it gets repaid with interest.

By 2023, Vici had announced financing arrangements for Canyon Ranch spas, Great Wolf Resorts water parks, a Kalahari Resorts water park, Cabot golf resorts, and BigShots Golf driving ranges. It also acquired 38 Bowlero bowling alleys. The common thread wasn't the specific activity—it was the irreplaceable nature of the experience.

CEO Ed Pitoniak articulated the thesis: "We are honored to expand our partnerships with two of the world's best experiential place makers and operators, Chelsea Piers and Cabot. Our total commitment of nearly $550 million of capital expresses our conviction in the ability of Cabot and Chelsea Piers to create indelible experiences that lead, for decades to come, to enduring relationships with their very valuable customer bases."

The thesis is elegant: Experience-based real estate is Amazon-proof. You can buy clothes online, but you can't bowl online. You can watch golf on TV, but you can't play St. Andrews from your couch. You can gamble on your phone, but you can't replicate the energy of a Vegas casino floor. In a world increasingly dominated by digital experiences, physical experiences become more valuable, not less.

VICI's non-gaming portfolio now includes 39 properties generating hundreds of millions in annual rent. These aren't random acquisitions—they're carefully selected assets that share gaming's key characteristics: location-dependent, experience-driven, and impossible to replicate digitally. It's the same formula, just without the slot machines.

IX. Power Dynamics: When Your Tenant is Your Former Parent

The relationship between VICI and Caesars Entertainment presents one of the most fascinating power dynamics in corporate America. VICI was literally birthed from Caesars' bankruptcy, spun off to creditors who never wanted to own it. Now VICI is worth more than Caesars, has better credit ratings, and essentially controls Caesars' ability to sell or redevelop its most valuable properties.

The master lease structure is a masterpiece of aligned incentives and subtle control. Caesars operates under multiple leases with VICI, but many are cross-defaulted—miss rent on one property, and you're in default on all. The leases run 15-30 years with no early termination rights. Caesars can't sell a property without VICI's consent. They can't redevelop without approval. They can't even rebrand without permission.

Yet this isn't a hostage situation. VICI needs Caesars to succeed—they're still the largest tenant, generating over $1 billion in annual rent. When Caesars wants to invest in a property, VICI often provides the capital through its Partner Property Growth Fund, sharing in the upside while protecting the downside. It's symbiotic parasitism, if such a thing exists.

The MGM relationship represents the evolution of the operator-REIT dynamic. MGM Resorts explicitly adopted an "asset-light" strategy, selling real estate to focus on operations and brand management. They view real estate ownership as a distraction from their core competency: running casinos and hotels. MGM gets to redeploy billions in capital from real estate sales into higher-return investments like digital gaming and new market expansion.

VICI will have eight different gaming tenants—Caesars, Hard Rock Entertainment, Penn National, Century Casinos, Jack Entertainment, The Eastern Band of Cherokee Indians, MGM Resorts and Apollo—managing casinos once the two deals are finalized. This diversification fundamentally changes the power dynamic. No single tenant can threaten VICI. But more importantly, VICI has become the preferred capital partner for the entire industry.

The negotiating leverage question is more nuanced than it appears. Yes, VICI owns the real estate. But replacing an operator isn't simple—gaming licenses are typically held by the operator, not the landlord. If Caesars defaulted on Caesars Palace, VICI couldn't just bring in a new operator tomorrow. They'd need regulatory approval, new licensing, and potentially significant time and cost.

But here's the key insight: the operators need VICI more than VICI needs any individual operator. Where else can casino companies access billions in capital at reasonable rates without diluting equity? Banks are nervous about gaming. Public markets punish casino companies for high leverage. Private equity wants control. VICI offers something unique: patient capital with no operational interference.

The sustainability question—can operators afford ever-rising rents—misses the point. Gaming revenues have grown faster than rent escalators for decades. More importantly, the properties VICI owns generate massive cash flows relative to rent. Even in downturns, the coverage ratios provide substantial cushion. And in the worst-case scenario of operator distress, VICI's properties are so valuable that finding a replacement tenant or buyer wouldn't be difficult.

John Payne captured the reality perfectly: "We collect fixed rent streams with annual escalations over very long periods of time". It's not about power—it's about predictability. Both sides know exactly what they're getting for the next two decades. In a world of uncertainty, that clarity is worth billions.

X. Playbook: Lessons from the VICI Story

The VICI story offers a masterclass in value creation that extends far beyond real estate. It's a playbook for turning disaster into triumph, complexity into simplicity, and "boring" into beautiful.

Creating value from distressed situations requires seeing beyond the immediate chaos. When creditors received VICI shares in 2017, most saw a burden to be dumped. The few who held saw an opportunity to own irreplaceable assets at distressed prices. The lesson: the best opportunities often come wrapped in the worst circumstances. VICI's formation at a ~$12 billion enterprise value for assets that would be worth $40+ billion five years later represents one of the great value creation stories in REIT history.

The power of patient, specialized capital in niche markets cannot be overstated. VICI didn't try to compete with Blackstone in all real estate—they became the undisputed expert in experiential property. When casino operators need capital, they call VICI first. This specialization creates a virtuous cycle: expertise leads to better underwriting, which leads to better returns, which attracts more capital, which enables more deals.

VICI CEO Ed Pitoniak said "I saw VICI and gaming real estate as the next great institutionalization story in American commercial real estate". He was right. Gaming real estate went from an orphaned asset class that institutional investors wouldn't touch to a core holding for pension funds and sovereign wealth funds. VICI didn't just participate in this transformation—they led it.

Why "boring" business models can create extraordinary returns is perhaps the most important lesson. VICI doesn't develop new technology. They don't create content. They don't even operate anything. They just own land and collect rent. Yet from 2018 to 2024, VICI stock has dramatically outperformed the broader market while paying steadily growing dividends. Sometimes the best business model is the simplest one.

The importance of management alignment and expertise shows in every decision. Pitoniak took lower base salary than his COO—unheard of in corporate America—because he cared more about building value than ego. The compensation structure, with two-year performance periods for bonuses and three-year periods for equity, aligns management with long-term value creation rather than quick flips.

Capital structure as competitive advantage enabled VICI to move faster than competitors. By maintaining moderate leverage (5-6x EBITDA) and investment-grade ratings, VICI could access capital markets even during volatility. Their unsecured debt structure provides flexibility that mortgage-dependent competitors lack. When opportunities arose—like the Venetian or MGM Growth—VICI could move quickly with committed financing.

The playbook ultimately reduces to this: Find an asset class others misunderstand. Become the undisputed expert. Structure intelligently. Execute relentlessly. And never, ever compromise on quality. It's not revolutionary. It's not exciting. But it works.

XI. Bear vs. Bull: The Investment Case

The Bull case for VICI practically writes itself:

VICI owns irreplaceable Strip assets with massive barriers to entry. You literally cannot build another Caesars Palace or MGM Grand—there's no land, no licenses, and no economic rationale at today's construction costs. These properties would cost $5-10 billion each to replicate, if it were even possible. VICI owns them at a fraction of replacement cost.

The company achieved the fastest migration from IPO to S&P 500 inclusion on June 3, 2022—less than five years. This wasn't luck or timing—it was execution. VICI went from bankruptcy spinoff to one of America's largest REITs through disciplined acquisition and intelligent capital allocation.

Gaming expansion nationwide through sports betting and new states provides secular tailwinds. States need tax revenue. Sports betting is exploding. Online gaming is growing but drives traffic to physical casinos rather than replacing them. Every trend in gaming benefits the landlord who collects rent regardless of who wins or loses.

The experiential real estate thesis is playing out exactly as predicted. VICI's expansion into water parks, entertainment complexes, and golf resorts proves the model works beyond gaming. These properties share gaming's key characteristics: location-dependent, experience-driven, and recession-resilient.

But the Bear case has merit too:

Tenant concentration risk remains real despite diversification. Caesars still generates about 40% of rent. MGM is another 25-30%. If either faced serious distress, VICI would feel it. Yes, the properties are valuable, but transitioning operators isn't seamless.

Rising interest rates pressure REIT valuations across the board. REITs are essentially bond substitutes for many investors. When treasury yields rise from 1% to 5%, a 5.5% dividend yield looks less attractive. VICI isn't immune from these macro forces.

Recession sensitivity of gaming can't be ignored. While VICI collected all rent during COVID, that was with massive government stimulus. In a real recession without support, gaming revenues could fall 20-30%. Coverage ratios provide cushion, but not infinite cushion.

The potential for operators to struggle with rent coverage in a downturn is the ultimate risk. VICI's model depends on operators generating enough cash flow to pay rent. Rent escalators are typically 2% annually or CPI, whichever is greater. If gaming revenues stagnate while rents rise, coverage ratios compress. At some point, the math stops working.

The balanced view recognizes both perspectives. VICI owns the best collection of gaming real estate ever assembled. The business model has proven resilient through the ultimate stress test. Management has executed flawlessly. But valuation matters, macro matters, and concentration risk is real. This isn't a risk-free proposition—it's a bet that experiential real estate will continue to generate outsized cash flows relative to other property types.

XII. Grading the Power & The Future

From distressed spinoff to S&P 500 in under 5 years—the transformation is unprecedented in REIT history. VICI Properties owns 93 experiential assets across a geographically diverse portfolio consisting of 54 gaming properties and 39 other experiential properties across the United States and Canada. The portfolio is comprised of approximately 127 million square feet and features approximately 60,300 hotel rooms and over 500 restaurants, bars, nightclubs and sportsbooks.

The sheer scale achieved in such a short time defies conventional corporate development. Most REITs take decades to build what VICI assembled in five years. They did it through a combination of fortunate timing (emerging from bankruptcy just as gaming REITs gained acceptance), brilliant execution (never missing an opportunity to deploy capital), and structural advantages (access to capital when competitors didn't).

What would happen if we were running VICI? The playbook would focus on three areas:

First, international expansion into markets with similar characteristics to U.S. gaming: highly regulated, license-restricted, and experience-driven. Macau is obvious but complicated by politics. Singapore is interesting but small. Japan's integrated resorts, when they finally happen, would be perfect. Europe's established gaming markets offer opportunities without the regulatory uncertainty of emerging markets.

Second, sports venues represent the next frontier. Stadiums and arenas share every characteristic VICI seeks: irreplaceable locations, experience-driven attendance, and long-term leases with creditworthy tenants. The challenge is that many are municipally owned. But private venues, particularly new construction, could work perfectly in the VICI model.

Third, theme parks would be the holy grail. Disney and Universal aren't selling, but regional theme parks could work. Six Flags, Cedar Fair, and similar operators own valuable real estate under experiential assets. The model would be identical to gaming: buy the land, lease it back, collect rent for decades.

The constraints are real though. VICI's model requires scale—small acquisitions don't move the needle on a $35 billion enterprise value. The universe of experiential real estate that meets VICI's criteria (irreplaceable, cash-flowing, with creditworthy operators) is finite. At some point, they'll run out of things to buy.

But perhaps that's not a bad thing. VICI could become the ultimate dividend aristocrat—a company that owns the best experiential real estate in America, collects growing rents for decades, and returns essentially all cash flow to shareholders. It's not a growth story forever, but it doesn't need to be. Sometimes conquering means knowing when to stop conquering.

XIII. Recent News

VICI announced over $1 billion in capital commitments in 2024 and deployed capital every month, along with announcing a strategic relationship with Cain International and Eldridge Industries. The February 2025 earnings report showed continued momentum with 2024 revenue of $3.85 billion, an increase of 6.53% compared to the previous year's $3.61 billion, with earnings of $2.68 billion, an increase of 6.58%.

The strategic partnership with Cain International and Eldridge Industries includes an investment in the One Beverly Hills development, providing $300 million in financing, with the partnership aiming to capitalize on opportunities in experiential investments including luxury hospitality, retail, and residential properties.

The company's credit profile continues to strengthen. In November 2024, Moody's Investors Service upgraded its issuer credit rating for VICI Properties L.P. to 'Baa3' from 'Ba1', with a stable outlook. This upgrade to investment grade from all three major rating agencies provides VICI with access to cheaper capital and a broader investor base.

In Q3 2024, VICI increased quarterly revenue by approximately 7% year-over-year and AFFO per share by approximately 5% year-over-year, deployed $230 million of capital during the quarter, announced a 4.2% dividend increase, achieving a dividend CAGR of 7% since IPO.

The company continues to expand its experiential financing pipeline. VICI originated a $250 million mezzanine loan as part of a $1.55 billion financing for Great Wolf Resorts, with an annual fixed interest rate and an initial term of two years with three 12-month extension options, with Great Wolf repaying VICI's $79.5 million mezzanine loan for Great Wolf Lodge Maryland in connection with the new financing.

Looking ahead, VICI reported adjusted EBITDA per share increased by 3.6% for Q4 2024 compared to the same period the prior year, with full-year growth of 5.1%, with 2025 AFFO guidance expected to continue showing steady growth. The company's ability to deploy capital consistently while maintaining disciplined underwriting standards positions it well for continued growth.

XIV. Links & Resources

Company Resources: - VICI Properties Investor Relations: investors.viciproperties.com - SEC Filings: sec.gov/edgar (search ticker: VICI) - Annual Reports and Proxy Statements

Key Industry Research: - National Association of Real Estate Investment Trusts (NAREIT): reit.com - American Gaming Association: americangaming.org - CBRE Gaming & Leisure Group Reports

Books on the Caesars Story: - "The Caesars Palace Coup" by Max Frumes and Sujeet Indap - The definitive account of the bankruptcy - "Winner Takes All" by Christina Binkley - History of Las Vegas casino competition

Academic & Professional Analysis: - Harvard Business School Case: "Bankruptcy at Caesars Entertainment" (2016) - Stanford GSB Case: "VICI Properties: Creating Value from the Ashes" (2022)

Podcast Episodes & Interviews: - The Fort Podcast #326: Ed Pitoniak, CEO of VICI Properties - Walker & Dunlop's "Driven by Insight" featuring Ed Pitoniak - REIT Report Podcast: "Gaming REITs Post-Pandemic"

Industry Publications: - Casino.org - Gaming industry news and analysis - GlobeSt.com - Commercial real estate coverage - Green Street Advisors - REIT research (subscription required)

The VICI story isn't finished. From bankruptcy spinoff to Strip landlord, from gaming pure-play to experiential real estate platform, the company has defied every expectation. The creditors who reluctantly received VICI shares in 2017 and held them have seen extraordinary returns. The management team that took a complex, overleveraged spinoff and turned it into an S&P 500 component has created a template for value creation.

Perhaps Julius Caesar's phrase was the perfect name after all. VICI came from bankruptcy. They saw opportunity where others saw disaster. And they conquered—not through force, but through patient capital deployment, disciplined underwriting, and the simple recognition that some experiences can never be replicated online. In a digital world, owning the land under irreplaceable physical experiences might just be the ultimate investment. Veni, vidi, VICI indeed.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube