Tapestry: From American Leather Workshop to Modern Luxury House

I. Introduction & Episode Roadmap

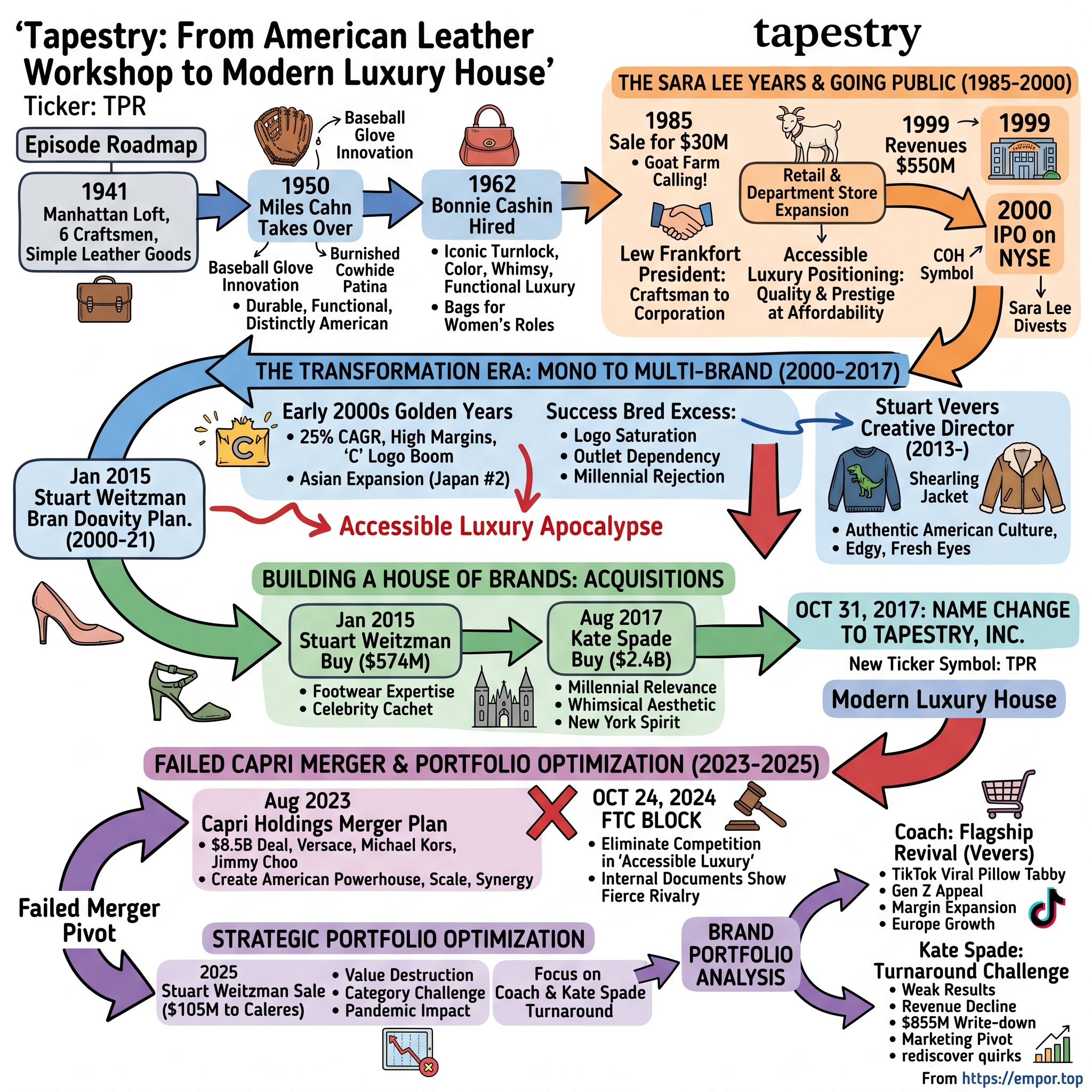

Picture this: Halloween 2017, New York Stock Exchange. As traders in costume mill about the trading floor, a 76-year-old American luxury company is shedding its skin. At 9:30 AM sharp, the ticker symbol COH—synonymous with Coach handbags for seventeen years—vanishes. In its place appears TPR: Tapestry, Inc. The transformation isn't just cosmetic. After acquiring Stuart Weitzman shoes and with Kate Spade freshly added to its portfolio for $2.4 billion, the company that began as six leather craftsmen in a Manhattan loft is declaring itself something entirely new: an American luxury house built to rival the European giants.CEO Victor Luis stands at the podium, addressing skeptical investors and fashion media. "We're no longer just Coach," he declares. "Three years ago we laid out our vision to transform Coach and announced our intention to grow beyond the Coach brand. Through the execution of our strategic plan and with the acquisitions of Stuart Weitzman in 2015 and Kate Spade & Company just this summer, we have realized these goals. We are now at a defining moment in our corporate reinvention, having evolved from a mono-brand specialty retailer to a true house of emotional, desirable brands, all leveraging our strong operational foundation."

The central question driving this story: How does a company born from six leather craftsmen in 1941 Manhattan transform into a multi-billion dollar luxury conglomerate attempting to challenge European powerhouses like LVMH and Kering? It's a distinctly American tale of reinvention—multiple reinventions, actually—each marked by bold bets, painful missteps, and the constant tension between heritage and evolution.

What makes Tapestry's journey particularly fascinating is how it reflects the broader story of American luxury itself. Unlike European luxury houses built on centuries of aristocratic patronage, American luxury brands must earn their stripes through democracy and accessibility—then somehow transcend those very qualities to achieve prestige. It's a paradox Coach has wrestled with for decades, and one that now defines Tapestry's entire portfolio strategy.

Over the next several hours, we'll trace this evolution from workshop to Wall Street, examining the key inflection points: the baseball glove innovation that revolutionized handbag design, the Sara Lee years that brought corporate discipline but nearly killed the soul, the explosive growth and subsequent identity crisis of the 2000s, the bold acquisitions meant to create an American answer to European conglomerates, and the recent failed Capri merger that forced a strategic pivot. We'll explore how each brand in the portfolio—Coach, Kate Spade, and until recently Stuart Weitzman—fits into the larger tapestry (yes, they knew what they were doing with that name).

Most importantly, we'll decode what this all means for investors evaluating TPR today. Is this truly the foundation of an American luxury powerhouse, or merely a collection of brands struggling to find coherence? The answer lies in understanding not just where Tapestry has been, but the fundamental dynamics of luxury retail, brand portfolio management, and the shifting consumer psyche that will determine its future.

II. The Coach Foundation: Baseball Gloves to Handbags (1941-1985)

The year is 1959. Miles Cahn sits in the bleachers at Yankee Stadium, but he's not watching Mickey Mantle at the plate. His eyes are fixed on a worn baseball glove in the hands of the fan next to him. The leather is burnished to a deep patina, soft as butter yet structurally intact after years of use. While others see America's pastime, Cahn sees the future of American luxury. Coach was founded in 1941, as a family-run workshop in a loft on 34th Street in Manhattan, with six leather-workers who made wallets and billfolds by hand. This wasn't glamorous work. In a cramped space above the bustle of midtown, these artisans—whose names history hasn't preserved—spent their days cutting, stitching, and burnishing leather into simple, functional goods. No one imagined they were laying the foundation for what would become a multi-billion dollar luxury empire. In 1946, Miles Cahn and his wife Lillian joined the company. By 1950, Cahn had taken over the company. The Cahns brought something revolutionary: vision. Miles was a craftsman who scrutinized every piece of leather he encountered. During the early years, Cahn noticed the distinctive properties and qualities of the leather used to make baseball gloves. With wear and use, the leather in a glove became softer and suppler. Attempting to mimic this process, Cahn developed a process to make the leather stronger, softer, and more flexible.

But the real innovation came from Lillian. Having grown up during the Depression, she'd delivered noodles in paper shopping bags for her family's struggling business. She understood functionality in a way that fashion designers of the era didn't. "One of her suggestions early on was: Why can't we make a shopping bag, but out of leather?" recalls her husband, Miles Cahn. Miles initially scoffed at the idea—New York was already full of handbag companies churning out European knockoffs. But Lillian persisted.

The purses, given the brand name Coach, were made of sturdy cowhide, in which the grain of the leather could still be seen, instead of the thin leather pasted over cardboard that was used for most women's handbags at the time. This innovation marked the company's entry into the field of classic, long-lasting, luxury women's handbags that Coach would come to define. The turning point came in 1962 when Miles Cahn hired Bonnie Cashin to be Coach's first lead designer. Then came Bonnie Cashin: hired by Miles Cahn in 1962 to be Coach's first lead designer. Cashin was already a legend in American sportswear, having designed costumes for Hollywood and uniforms for American Airlines. She brought something revolutionary to Coach: color, whimsy, and hardware that would become iconic.

The story of Coach's most recognizable design element—the turnlock—reads like design serendipity. Inspired by the brass turnlocks that secured the top of her 1940s convertible, the hardware became a signature feature of Cashin's designs. The brass turnlock, introduced by Cashin in 1961, is now a hallmark of the brand. This wasn't just ornamentation; it was functional luxury, allowing bags to be secured with a satisfying twist rather than fumbling with zippers or snaps.

Her classic designs for Gail's Coach division during the early 1960s included the shopping bag tote, the bucket bag, shoulder bag and a clutch-style purse with a removable shoulder strap. Each design reflected Cashin's philosophy: she wasn't designing for fashion trends but for the roles women actually played in their lives. The bags had to work as hard as the women carrying them.

Under the Cahns' leadership and Cashin's creative vision, Coach grew from a six-person workshop into a recognizable brand. By the early 1980s, they had built something remarkable: an American luxury leather goods company with its own aesthetic language, distinct from European competitors. The bags were practical where European luxury was precious, durable where others were delicate, and accessible where others were exclusive.

But by 1983, the Cahns were ready for a different kind of life. They'd started a goat farm in upstate New York—Coach Farm, naturally—and were increasingly drawn to cheesemaking over handbag-making. In 1985, the Cahns sold Coach Leatherware to Sara Lee Corporation for a reported $30 million, a sum that seemed substantial at the time but would prove to be one of the great bargains in luxury retail history. The Cahns were leaving behind more than a business; they were handing over an American original, a brand that had found a way to make luxury democratic without sacrificing quality or desire.

III. The Sara Lee Years & Going Public (1985-2000)

The scene: Sara Lee Corporation headquarters, Chicago, 1985. Executives who'd built their careers selling pound cake and pantyhose are now the proud owners of a Manhattan leather goods company. The juxtaposition was almost comedic—a conglomerate known for "Nobody doesn't like Sara Lee" now controlled America's premier leather craftsman. Yet this unlikely marriage would transform Coach from a family workshop into a global luxury powerhouse.

In 1985, the Cahns sold Coach Leatherware to Sara Lee Corporation for a reported $30 million, having decided to "devote more time to their growing goat farm and cheese production business called Coach Farm in Gallatinville, New York, which they began in 1983". Lew Frankfort succeeded Cahn as president. Sara Lee structured Coach under its Hanes Group branch of subsidiaries of brands.

The appointment of Lew Frankfort as president marked the beginning of Coach's transformation from craftsman to corporation. Frankfort, who'd joined Coach in 1979 as vice president of new business development, understood something his Sara Lee bosses initially didn't: Coach wasn't just another consumer brand to be optimized and distributed. It was a luxury business hiding in plain sight, constrained by limited distribution and an aging customer base.

Frankfort's first moves were surgical. In early 1986, the company opened new boutiques in Macy's stores in New York City and San Francisco. Additional Coach stores were under construction, and similar boutiques were to be opened in other major department stores later that year. By November 1986, the company was operating 12 stores, along with nearly 50 boutiques within larger department stores.

The expansion strategy was deliberate: maintain the brand's premium positioning while dramatically increasing points of distribution. Department store boutiques gave Coach visibility to affluent shoppers who might never venture into a standalone store. The Madison Avenue flagship, opened in 1981 under the Cahns, became a laboratory for testing new concepts before rolling them out nationally. But the real revolution was happening behind the scenes. Frankfort was quietly transforming Coach from a manufacturing company into a lifestyle brand. He invested heavily in consumer research, discovering that Coach's customer base was aging and the brand was losing relevance with younger consumers. The solution wasn't to abandon heritage but to modernize it—maintaining quality while accelerating fashion cycles and expanding price points.

The late 1990s brought a critical innovation: the "accessible luxury" positioning. While European luxury houses maintained astronomical prices as a barrier to entry, Coach offered quality and prestige at prices that aspirational consumers could actually afford. A Coach bag might cost $300-500, not the $3,000+ commanded by Hermès or Chanel. This wasn't about being cheap; it was about democratizing luxury without sacrificing margin or brand equity.

By 1999, the transformation was bearing fruit. Coach had evolved from a dusty heritage brand into a growth story, with revenues approaching $550 million. But Sara Lee, facing pressure from activist investors and struggling with its sprawling conglomerate structure, decided Coach no longer fit its strategic vision. The decision to spin off Coach wasn't about failure—it was about unlocking value trapped inside a food and consumer goods conglomerate.

In early October 2000, Sara Lee sold off 17 percent of the newly named Coach, Inc. to the public. Through the IPO, 7.38 million shares of Coach stock were sold at $16 per share, raising $118 million on the New York Stock Exchange. The shares opened at $20, well above their initial public offering price, a clear signal that investors saw something Sara Lee's management hadn't: Coach wasn't just a leather goods company, it was a luxury brand with global potential.

Frankfort remained Coach's chairman and CEO. In April 2001 Sara Lee fully divested itself of its Coach holdings by spinning off the remaining interest to Sara Lee shareholders. The complete separation marked the end of the Sara Lee era and the beginning of Coach's life as an independent public company.

As part of the much larger Sara Lee, Coach had seen its revenues increase from about $19 million in 1985 to $540.4 million in 1997, before declining to $507.8 million in 1999. Prior to the IPO, the improved financial condition of Coach was already evident, as revenues for fiscal 2000 climbed 8.1 percent to $548.9 million and net income surged 130.9 percent, jumping from $16.7 million to $38.6 million.

The Sara Lee years had been transformative, if not always comfortable. Coach emerged from corporate ownership with professional management, sophisticated systems, and national distribution. But it also emerged with questions about its identity. Was it a heritage brand or a fashion brand? American craftsman or global luxury player? These questions would define the next chapter of Coach's evolution, as Frankfort and his team set out to prove that an American brand could compete on the global luxury stage.

IV. The Transformation Era: From Mono-Brand to Multi-Brand (2000-2017)

Reed Krakoff stands in Coach's design studio, 2001, surrounded by mood boards that would horrify the brand's traditionalists. Gone are the understated browns and blacks of classic Coach. In their place: hot pink leather, logo-covered canvas, and bags that weigh ounces instead of pounds. "We're not your grandmother's Coach anymore," he tells his team. Within five years, this radical reimagining would drive Coach's market value from $1 billion to over $15 billion.

The early 2000s were Coach's golden years, a period when everything Frankfort and Krakoff touched turned to retail gold. The strategy was brilliantly simple: take Coach's heritage of quality and craftsmanship, inject it with fashion-forward design and faster product cycles, and price it at the sweet spot where aspiration meets affordability. While Hermès made customers wait years for a Birkin bag, Coach delivered instant gratification with monthly new arrivals.

The numbers were staggering. From 2000 to 2007, Coach's revenues grew from $548 million to $2.6 billion, a compound annual growth rate exceeding 25%. Same-store sales consistently grew double digits. Operating margins expanded from 17% to over 35%. The stock price increased twenty-fold. Wall Street analysts ran out of superlatives.

The secret sauce was Coach's pioneering approach to "accessible luxury"—a term the company essentially invented. By maintaining prices 50-70% below European luxury brands while delivering comparable quality, Coach tapped into a massive market of consumers who wanted to participate in luxury culture without mortgaging their futures. A Coach bag became the entry drug to the luxury lifestyle, the first "real" handbag for millions of American women.

International expansion, particularly in Asia, turbocharged growth. Japan became Coach's second-largest market, contributing nearly 20% of total revenues by 2010. Chinese consumers, newly wealthy and brand-obsessed, couldn't get enough of Coach's logo-emblazoned products. The company opened stores at a breakneck pace—by 2012, Coach operated over 350 stores in North America and 160 in Japan alone.

But success bred excess. The very strategies that drove Coach's meteoric rise contained the seeds of its near-destruction. The proliferation of outlet stores—initially a smart way to clear excess inventory—became a drug the company couldn't quit. By 2013, Coach operated 193 outlet stores in North America, nearly matching its 198 full-price locations. Worse, outlets weren't just selling last season's merchandise; they were producing made-for-outlet products that looked suspiciously similar to mainline offerings at 30-50% lower prices.

The logo saturation that Chinese consumers loved became toxic in America. The "C" pattern that once signified aspiration now screamed "trying too hard." Younger consumers, particularly millennials, rejected logo-heavy products in favor of understated, authentic brands. Instagram changed everything—suddenly, wearing the same recognizable Coach bag as everyone else wasn't aspirational; it was basic. Competition intensified from all directions. Michael Kors, once dismissed as Coach's downmarket imitator, was suddenly eating Coach's lunch with fresher designs and savvier marketing. Kate Spade appealed to the whimsical millennial sensibility Coach had lost. European brands like Gucci and Saint Laurent, reinvigorated under new creative leadership, made Coach look staid and middle-aged.

By 2013, the crisis was undeniable. Same-store sales turned negative. The stock price fell 50% from its 2012 peak. Wall Street analysts who'd once fawned over Coach now questioned whether the brand could survive the "accessible luxury apocalypse" it had helped create.

Enter Stuart Vevers. On 25 June 2013, it was announced that Stuart would be leaving Loewe to join American label Coach as executive creative director. Vevers succeeds Reed Krakoff at the leather goods label, who stepped down (following a 16-year tenure) to focus on his eponymous fashion line. The British designer brought impeccable European luxury credentials—stints at Bottega Veneta, Givenchy, Louis Vuitton, Mulberry, and Loewe—but more importantly, he brought fresh eyes and an outsider's perspective on American style.

Vevers' vision was radical: stop trying to be a European luxury brand with an American accent. Instead, embrace authentic American culture—not the polished, aspirational version, but the real, messy, creative energy of contemporary America. His first collection featured dinosaur sweaters, shearling biker jackets, and bags adorned with punk-rock studs. Fashion critics were bewildered. But something interesting happened: young consumers started paying attention. While Vevers worked on reinventing the Coach brand, management pursued a different strategy for growth: acquisitions. In January 2015, Coach agreed to buy shoemaker Stuart Weitzman for up to $574 million in cash. The transaction will complement Coach's current leadership position in premium handbags and accessories, while immediately adding to the company's earnings. The logic was sound: diversify beyond handbags, acquire expertise in a complementary category, and leverage Coach's infrastructure to accelerate growth.

Stuart Weitzman was a premium footwear brand with $300 million in annual revenues and significant celebrity cachet. The Highland boot and Nudist sandal were red carpet staples. The brand brought technical expertise in footwear that Coach lacked. But Wall Street was skeptical—the price seemed high for a brand with limited growth potential, and some questioned whether Coach management could handle an acquisition while trying to fix their core business.

The transformation accelerated in 2017 with the boldest move yet: acquiring Kate Spade for $2.4 billion. Unlike Stuart Weitzman, this wasn't about category expansion—it was about building a multi-brand portfolio, creating an American answer to European luxury conglomerates. The Kate Spade acquisition would prove to be the catalyst for Coach Inc.'s complete reinvention as Tapestry, marking the end of the mono-brand era and the beginning of something entirely new.

V. The Kate Spade Acquisition: Building a House of Brands (2017)

May 8, 2017. Kate Spade Bea Handbag, age 55, is found dead in her Park Avenue apartment. The fashion world mourns the loss of a creative icon whose whimsical, optimistic designs had defined accessible luxury for a generation of women. Two months later, Coach Inc. announces it will acquire the company bearing her name for $2.4 billion. The timing is tragic, the optics complicated, but the strategic logic is undeniable: Coach needs to become something bigger than Coach. The strategic rationale was compelling. Kate Spade & Company operates principally under two global, multichannel lifestyle brands: kate spade new york and Jack Spade New York. The brand had something Coach desperately needed: relevance with millennials. Kate Spade's focus is on a younger consumer that Coach has some difficulty in attracting.

Coach, Inc. completed the acquisition of Kate Spade & Company for $18.50 per share in cash for a total $2.4 billion purchase price. The deal represented a 27.5% premium to Kate Spade's unaffected closing price, but analysts largely viewed it as reasonable given the strategic benefits.

Victor Luis, Coach's CEO, laid out an ambitious vision: Kate Spade has a truly unique and differentiated brand positioning with a broad lifestyle assortment and strong awareness among consumers, especially millennials. Through this acquisition, we will create the first New York-based house of modern luxury lifestyle brands, defined by authentic, distinctive products and fashion innovation. In addition, we believe Coach's extensive experience in opening and operating specialty retail stores globally, and brand building in international markets can unlock Kate Spade's largely untapped global growth potential.

The numbers told a story of untapped potential. Kate Spade generated approximately $1.4 billion in annual revenues but was underperforming operationally. Same-store sales were declining, margins were under pressure from excessive promotional activity, and international expansion had stalled. Coach management saw opportunity where others saw problems—they'd successfully navigated similar challenges with their own brand transformation.

Integration planning revealed both synergies and challenges. Coach CFO Kevin Wills says that because the businesses are complementary, he believes they'll be able to save $50 million in the three years after the deal closed, through "operational efficiencies, improved scale and inventor management, and the optimization of Kate Spade's supply chain network". But achieving these synergies would require delicate balance—maintaining brand independence while leveraging shared infrastructure.

The cultural fit seemed natural on paper. Both brands were New York-based with accessible luxury positioning. Both emphasized lifestyle over pure fashion. Both had strong heritage stories rooted in American optimism. But beneath the surface lay fundamental differences. Kate Spade's whimsical, colorful aesthetic contrasted sharply with Coach's increasingly edgy, streetwise vibe under Stuart Vevers. Kate Spade customers skewed younger and more aspirational; Coach's were older and more affluent.

The company officially changed its name and ticker symbol on the New York Stock Exchange from COH to TPR on October 31, 2017. The transformation from Coach Inc. to Tapestry Inc. was more than symbolic—it represented a fundamental shift in corporate strategy. No longer would the company be defined by a single brand. Instead, it would operate as a house of brands, each maintaining its distinct identity while benefiting from shared capabilities.

The name "Tapestry" itself was carefully chosen. In Tapestry, we found a name that speaks to creativity, craftsmanship, authenticity and inclusivity on a shared platform and values. But the market's initial reaction was skeptical. The stock fell 2% on the announcement, with investors questioning whether a name that sounded more like home furnishings than luxury fashion was the right choice.

The real test would come in execution. Could Tapestry successfully manage multiple brands without diluting their individual identities? Could Kate Spade be turned around while maintaining its quirky charm? And most importantly, could an American luxury conglomerate truly compete with European houses that had been perfecting the multi-brand model for decades?

VI. The Failed Capri Merger & Portfolio Optimization (2023-2025)

August 10, 2023. Joanne Crevoiserat, Tapestry's CEO since 2020, stands before Wall Street analysts with the biggest announcement of her tenure: Tapestry will acquire Capri Holdings—owner of Versace, Michael Kors, and Jimmy Choo—for $8.5 billion. If successful, the combined entity would create an American luxury powerhouse with over $12 billion in annual revenues, finally achieving the scale to challenge European giants. Fourteen months later, the dream would be dead, killed by a single federal judge who saw not opportunity but antitrust violation. Tapestry announced it would acquire Capri Holdings in August 2023 for $8.5 billion. Capri owns the brands Versace, Michael Kors, and Jimmy Choo. The deal represented Tapestry's boldest strategic move yet—a transformative acquisition that would instantly double the company's size and create a portfolio spanning from accessible luxury (Coach, Kate Spade, Michael Kors) to true luxury (Versace, Jimmy Choo).

The strategic logic seemed irrefutable. Combined, the companies would have the scale to negotiate better terms with suppliers, landlords, and marketing partners. The enlarged portfolio would provide leverage with department stores struggling to maintain relevance. Geographic complementarity—Tapestry's strength in Asia, Capri's in Europe—offered clear synergy opportunities. Most compellingly, the deal would create critical mass in the fragmented American luxury market, potentially catalyzing further consolidation.

But the Federal Trade Commission saw something different: a threat to competition. The Commission issued an administrative complaint and authorized a lawsuit in federal court to block the proposed acquisition, alleging that Tapestry's acquisition of Capri will eliminate fierce competition between the two companies. The proposed merger threatens to deprive millions of American consumers of the benefits of Tapestry and Capri's head-to-head competition, which includes competition on price, discounts and promotions, innovation, design, marketing, and advertising.

The FTC's case centered on a novel market definition: "accessible luxury handbags." Where Tapestry and Capri most vigorously compete against one another – mainly between Tapestry's Coach and Kate Spade brands against Capri's Michael Kors brand – is in the "accessible luxury" handbag market. Today, Coach, Kate Spade and Michael Kors continuously monitor each other's handbag brands to determine pricing and performance, and they each use that information to make strategic decisions, including whether to raise or lower handbag prices.

The eight-day trial in September 2024 became a masterclass in how internal documents can doom a merger. The court focused on a Tapestry presentation outlining M&A prospects, which included a slide suggesting that a merger with Capri would create an "opportunity to reduce MK discounting". Emails between executives discussing competitive responses, pricing strategies, and market positioning painted a picture of fierce rivalry that the merger would eliminate.

On October 24, 2024, the Federal Trade Commission (FTC) succeeded in blocking the proposed merger of Tapestry and Capri Holdings. Judge Jennifer Rochon's decision was devastating for Tapestry. If Tapestry acquires Capri, Tapestry would gain a dominant market share in the "accessible luxury" handbag market, dwarfing every other competitor, the FTC alleges. The judge agreed, finding that the combined entity would control an unacceptable share of the market.

The merger was blocked on 24 October 2024. Tapestry and Capri committed to appealing the decision, but called off the merger the following month citing the regulatory hurdles. The termination triggered a $200 million breakup fee to Capri, but the real cost was strategic: years of planning, hundreds of millions in advisory fees, and the opportunity cost of not pursuing other growth initiatives.

The failed merger forced an immediate strategic pivot. Without the transformative growth that Capri would have provided, Tapestry needed to optimize its existing portfolio. The answer came quickly: divest underperforming assets and double down on what's working. Tapestry, Inc. entered into a definitive agreement to sell the Stuart Weitzman brand to Caleres for $105 million in cash, subject to customary adjustments. The transaction is expected to close in the summer of 2025. The sale price—barely 20% of the $574 million Tapestry paid in 2015—represented a stunning destruction of value, but management framed it as strategic portfolio optimization.

Tapestry had owned Stuart Weitzman since 2015, when it bought the footwear brand for $574 million from Sycamore Partners. A decade later, the brand had never lived up to its promise. Integration challenges, creative turnover, and an inability to expand beyond core footwear categories had limited growth. The COVID-19 pandemic, which devastated demand for dressy footwear, delivered the final blow.

CEO Joanne Crevoiserat positioned the divestiture as capital discipline: "As diligent stewards of our portfolio and disciplined allocators of capital, this transaction ensures that all our brands are positioned for long-term success and that we maintain a sharp focus on our largest value creation opportunities. At Tapestry, this means harnessing our position of strength to sustain Coach's leadership and momentum while reinvigorating Kate Spade to drive durable organic growth and shareholder value."

The failed Capri merger and Stuart Weitzman divestiture marked the end of Tapestry's ambitions to become a large-scale multi-brand luxury conglomerate. Instead, the company would focus on what it could control: making Coach and Kate Spade the best versions of themselves. Sometimes strategic retreat is the bravest move of all.

VII. Brand Portfolio Analysis: Coach, Kate Spade, and Beyond

Walk into any American mall today and you'll witness a retail phenomenon: the Coach store is packed with Gen Z shoppers filming TikToks with their new Pillow Tabby bags, while three stores down, Kate Spade struggles to attract foot traffic despite aggressive promotions. This tale of two brands within the same corporate umbrella encapsulates both the promise and peril of Tapestry's portfolio strategy.

Coach: The flagship revival story

Coach remained the company's top performer in the holiday quarter, with revenue up 11% year over year. Under Stuart Vevers' creative direction since 2013, the brand has engineered one of retail's most impressive turnarounds. The company's Q2 2025 results showed Coach revenue at $1.7 billion, up 10% year-over-year, demonstrating sustained momentum.

The secret to Coach's revival lies in Vevers' ability to reframe American heritage through a contemporary lens. Rather than chasing European luxury aesthetics, he's embraced distinctly American cultural references—from prairie dresses to punk rock, dinosaur sweaters to shearling jackets. This authenticity has resonated powerfully with younger consumers. The company welcomed approximately 2.7 million new customers in North America, with over half being Gen Z and Millennials.

Product innovation has been crucial. The Pillow Tabby bag became a viral sensation on TikTok, while the brand's leather goods achieved consistent average unit retail (AUR) gains through reduced promotional activity and improved product mix. Digital engagement soared, with high-single digit growth in digital revenue, while brick-and-mortar stores saw renewed relevance through experiential retail concepts.

Operationally, Coach has achieved remarkable efficiency. The brand drove 280 basis points of gross margin expansion, reflecting both pricing power and operational excellence. The brand's success in Europe (+42%) demonstrates untapped international potential, while maintaining strength in core North American markets.

Kate Spade: The turnaround challenge

The Kate Spade story presents a stark contrast. Kate Spade put up weaker results, with revenue declines of 10% in Q2 2025, bringing sales to $416.4 million. The brand that Tapestry acquired for $2.4 billion in 2017 has struggled to find its footing, prompting an $855 million write-down largely because of a decline in both current and future expected cash flows.

The challenges are multifaceted. Kate Spade's whimsical, optimistic aesthetic—once its greatest strength—feels disconnected from contemporary consumer preferences. While the brand maintains strong awareness, particularly among millennials, converting that awareness into purchases has proven difficult. In the fiscal year ended in June, Kate Spade sales came in at almost $1.2 billion, a touch lower than where they were the year the company was acquired, and well below their apex three years ago when they neared $1.5 billion.

Management's turnaround strategy focuses on several key initiatives. For Kate Spade, the company will increase marketing targeting Gen Z shoppers and streamline its handbag offerings. CEO Joanne Crevoiserat acknowledges the challenge: "While a turnaround takes time, we are confident in our path forward and the brand's opportunity for healthy and profitable growth".

The brand positioning requires fundamental recalibration. Kate Spade must rediscover what made it special—that unique combination of accessibility, whimsy, and sophistication—while updating its expression for contemporary consumers. "We know from work that we've done that there's great demand for the Kate Spade brand, we just frankly haven't executed very well over the last several years. But as we said here today, we're smarter from a brand-building capability standpoint," said Scott Roe, Tapestry's CFO.

Stuart Weitzman: Why the divestiture made sense

The Stuart Weitzman story serves as a cautionary tale about the challenges of brand integration and category expansion. Acquired in 2015 for $574 million, the luxury footwear brand never achieved the synergies Tapestry envisioned. The decision to sell to Caleres for $105 million—barely 20% of the purchase price—represents a stunning destruction of value but ultimately the right strategic move.

Several factors contributed to Stuart Weitzman's struggles. The brand remained stubbornly dependent on dressy footwear at a time when consumer preferences shifted toward casual styles. COVID-19 accelerated this trend, devastating demand for the brand's core occasion-based products. International expansion stalled, particularly in Asia where the brand failed to gain traction. Multiple creative director changes created inconsistency in brand vision and product direction.

The divestiture allows Tapestry to focus resources on its two remaining brands, where the potential for value creation is clearer. As management noted, this ensures "all our brands are positioned for long-term success and that we maintain a sharp focus on our largest value creation opportunities."

Portfolio synergies and operational excellence

Despite Kate Spade's challenges, Tapestry's multi-brand model delivers meaningful operational advantages. Shared infrastructure across sourcing, logistics, and technology creates cost efficiencies that would be impossible for standalone brands. The company's data and analytics platform, serving 120 million customer profiles, enables sophisticated customer acquisition and retention strategies across brands.

Supply chain excellence has become a competitive advantage. Tapestry's agile manufacturing network, with limited exposure to any single country, provides resilience against tariff impacts and geopolitical risks. Less than 10% of the company's sourcing comes from China, while Tapestry does not have any production in Canada or Mexico.

The company's digital capabilities, developed primarily for Coach but leveraged across brands, drive operational efficiency. Unified e-commerce platforms, shared customer service infrastructure, and coordinated marketing technologies reduce costs while maintaining brand independence. These synergies contributed to the remarkable margin expansion achieved despite challenging market conditions.

VIII. The Luxury Market Landscape & Competitive Dynamics

The accessible luxury segment Tapestry inhabits represents one of retail's most complex competitive battlegrounds. Positioned between mass market and true luxury, these brands must deliver aspiration without exclusivity, quality without astronomical prices, and prestige without pretension. It's a delicate balance that few master successfully.

Tapestry's positioning as an American luxury house creates both opportunities and constraints. Unlike European luxury conglomerates built on centuries of craftsmanship heritage, American luxury must earn its status through innovation, quality, and cultural relevance. Coach's revival demonstrates this is possible, but Kate Spade's struggles show how easily brands can lose their way.

The competitive landscape has intensified dramatically. Michael Kors, despite its own challenges within Capri Holdings, remains a formidable competitor in accessible luxury handbags. Tory Burch has successfully claimed the premium contemporary space. Meanwhile, European luxury brands have increasingly pushed into accessible price points through diffusion lines and entry-level products, squeezing the middle market from above.

From below, contemporary brands and direct-to-consumer upstarts challenge traditional notions of luxury. Brands like Polene, Mansur Gavriel, and Staud offer design-forward products at accessible prices without the overhead of legacy retail networks. These digital-native competitors move faster, test constantly, and build community through social media rather than traditional advertising.

Digital transformation has become table stakes. Digital revenue saw high-single digit growth for Tapestry, but this channel now represents critical strategic importance beyond just sales. Digital provides direct customer relationships, data collection opportunities, and the ability to test new products and marketing approaches with minimal risk. The company's investment in modern data and analytics platforms positions it well for continued digital evolution.

The China opportunity remains compelling despite recent volatility. While luxury spending has softened, the long-term demographics—a growing middle class, increasing fashion consciousness, and cultural emphasis on status symbols—suggest continued growth potential. Tapestry's relatively small presence in China compared to European luxury houses provides runway for expansion, though execution will be critical.

Sustainability has evolved from nice-to-have to strategic imperative. Younger consumers increasingly factor environmental and social responsibility into purchase decisions. Tapestry's initiatives around sustainable materials, ethical sourcing, and circular economy principles aren't just about corporate responsibility—they're about maintaining relevance with future luxury consumers.

IX. Financial Deep Dive & Investment Analysis

Tapestry's financial profile reflects a company in transition—strong operational performance at Coach offsetting Kate Spade's challenges, with the failed Capri merger and Stuart Weitzman divestiture reshaping the strategic landscape.

Revenue composition tells the story clearly. With the shriveling of Kate Spade (and excluding Stuart Weitzman, which Tapestry recently unloaded), Coach represents nearly 80% of Tapestry sales. This concentration creates both opportunity and risk—Coach's momentum drives overall performance, but any stumble would significantly impact results.

Geographic diversification provides some balance. Tapestry's largest market is North America, with nearly 70% of its quarterly sales coming from the region in the holiday quarter. However, international growth, particularly Europe's 45% revenue growth in the quarter, suggests meaningful expansion opportunities remain.

Margin structure has improved dramatically. Significant gross margin expansion of 280 basis points, which included operational outperformance (+260 basis points) and lower freight expense (+20 basis points) demonstrates pricing power and operational efficiency. This margin expansion comes despite inflationary pressures and supply chain challenges, suggesting sustainable competitive advantages.

Capital allocation reflects confidence in the business model. Tapestry's board approved a 14% increase to its quarterly dividend, to 40 cents a share. The annualized dividend rate is now $1.60 per share. Additionally, the company executed a $2 billion accelerated share repurchase program, returning substantial capital to shareholders.

The balance sheet remains strong despite recent strategic pivots. Cash, cash equivalents and short-term investments totaled $1.0 billion and total borrowings outstanding were $2.7 billion, representing net debt of $1.7 billion. The Company's leverage ratio, based on gross debt to adjusted EBITDA, was 1.6x at quarter-end, providing financial flexibility for investments and opportunistic moves.

Looking forward, guidance suggests measured optimism. Fiscal Year 2025 Revenue Guidance: Over $6.85 billion, approximately 3% growth. Fiscal Year 2025 EPS Guidance: Raised to $4.85 to $4.90, representing 13% to 14% growth. These targets appear achievable given Coach's momentum, though Kate Spade remains a wildcard.

The bull case centers on Coach's continued strength and operational excellence. If Coach maintains double-digit growth while margins expand, earnings could surprise to the upside. Successful Kate Spade stabilization, even without growth, would remove a key overhang. International expansion, particularly in underpenetrated European and Asian markets, provides multi-year growth runway. The company's shareholder-friendly capital allocation and strong free cash flow generation support attractive returns even without dramatic top-line growth.

The bear case focuses on concentration risk and execution challenges. Coach represents an uncomfortable percentage of profits—any brand fatigue or competitive pressure could devastate results. Kate Spade's turnaround has already taken eight years with little progress; continued struggles could necessitate further write-downs or divestiture. Tariff impacts, while manageable so far, could escalate with policy changes. The accessible luxury segment faces structural pressure from both above and below, potentially compressing the addressable market.

Valuation remains reasonable despite the stock's strong performance. Trading at approximately 12-14x forward earnings, Tapestry offers attractive value relative to both luxury peers and its own growth prospects. The dividend yield near 3% provides income while waiting for the growth story to play out.

X. Playbook: Lessons in Brand Building & Portfolio Management

Tapestry's journey offers invaluable lessons for understanding luxury brand management, portfolio strategy, and the unique challenges of building an American luxury house.

The Art of Brand Revival: Coach's transformation demonstrates that heritage brands can be revitalized without abandoning their core identity. The key lies in reinterpreting—not replacing—brand DNA for contemporary consumers. Stuart Vevers didn't try to make Coach into Gucci; he made it the best version of Coach. This authenticity resonates more powerfully than imitation ever could.

The Perils of Portfolio Expansion: The Stuart Weitzman acquisition and disposal, resulting in an 80% loss, illustrates the difficulty of category expansion through M&A. Footwear requires different expertise than leather goods—from design and development to manufacturing and distribution. Simply applying operational excellence from one category to another rarely works without deep domain expertise.

The Integration Paradox: Kate Spade's struggles highlight a fundamental tension in multi-brand management. Brands need independence to maintain their unique identity, but they also need integration to achieve synergies. Too much corporate oversight kills creativity; too little fails to capture value. Finding the right balance requires sophisticated organizational design and cultural sensitivity.

Digital as Enabler, Not Strategy: Tapestry's digital success comes not from chasing every trend but from using technology to enhance fundamental brand experiences. Digital amplifies what's already working—it doesn't fix what's broken. Kate Spade's challenges won't be solved by better Instagram posts; they require fundamental brand repositioning.

The American Luxury Challenge: Building luxury without European heritage requires different strategies. American brands must earn prestige through innovation, quality, and cultural relevance rather than inherited status. This creates both vulnerability—prestige can be lost quickly—and opportunity—brands can evolve more freely without historical constraints.

Operational Excellence as Competitive Advantage: In accessible luxury, where price points constrain margins, operational efficiency becomes crucial. Tapestry's supply chain agility, inventory management, and cost discipline create competitive advantages that are difficult to replicate. These capabilities matter more than brand heat in driving sustainable returns.

The Patience Imperative: Brand building operates on different timescales than financial markets prefer. Coach's revival took years of consistent investment before results materialized. Kate Spade's turnaround, if successful, will require similar patience. Short-term pressure can force decisions that undermine long-term brand value.

XI. Looking Forward: The Future of American Luxury

As Tapestry moves beyond the failed Capri merger, its future hinges on executing a focused two-brand strategy while navigating an increasingly complex luxury landscape.

The post-Capri strategy represents strategic focus rather than retreat. By concentrating resources on Coach and Kate Spade, Tapestry can invest more deeply in brand building, customer experience, and operational capabilities. The company has explicitly stated it will avoid acquisitions until Kate Spade returns to sustainable growth—a disciplined approach that should reassure investors tired of empire-building CEOs.

Digital innovation will accelerate beyond simple e-commerce. Augmented reality try-ons, personalized product recommendations powered by AI, and seamless omnichannel experiences will become table stakes. Tapestry's data platform, covering 120 million profiles, provides the foundation for sophisticated personalization that smaller competitors cannot match.

Sustainability will evolve from corporate initiative to brand differentiator. Younger consumers increasingly view environmental responsibility as non-negotiable. Tapestry's investments in sustainable materials, circular economy initiatives, and supply chain transparency position it well for this shift. The challenge lies in communicating these efforts authentically without greenwashing.

The next generation of luxury consumers—Gen Z and younger millennials—exhibits different values and behaviors than previous cohorts. They prize authenticity over aspiration, experiences over possessions, and values alignment over pure status. Coach's success with these consumers provides a template, but each brand must find its own authentic voice.

Geographic expansion remains compelling despite recent volatility. Europe's 42% growth demonstrates untapped potential in markets where Tapestry remains underpenetrated. China's long-term demographics support continued investment despite near-term softness. Other emerging markets—India, Southeast Asia, Latin America—offer longer-term growth opportunities as middle classes expand.

Can Tapestry become the "American LVMH"? The Capri failure suggests not through large-scale M&A. Instead, Tapestry must chart a different course—building fewer brands more deeply, leveraging operational excellence over portfolio scale, and embracing American luxury's unique attributes rather than imitating European models. Success means becoming the best version of Tapestry, not a pale imitation of someone else.

The path forward is clear if not easy: sustain Coach's momentum through continued innovation and global expansion, execute Kate Spade's turnaround with patience and discipline, and maintain operational excellence while investing in future capabilities. If management executes, Tapestry could emerge as a focused, profitable, and growing American luxury house—perhaps not the empire once envisioned, but something more valuable: a sustainable, differentiated player in global luxury.

XII. Recent News

Q2 FY2025 Earnings Exceed Expectations: Tapestry reported strong fiscal 2025 second quarter results, achieving record revenue of $2.2 billion, representing a 5% increase year-over-year. The growth was primarily driven by Coach's 10% revenue increase. The company delivered a diluted EPS of $1.38 on a reported basis and a record non-GAAP diluted EPS of $2.00.

Raised Full-Year Guidance: Based on these strong results, Tapestry raised its fiscal 2025 outlook, now expecting revenue over $6.85 billion (approximately 3% growth) and EPS of $4.85-$4.90 (13-14% growth).

Strong Customer Acquisition: Tapestry attracted about 2.7 million new customers in North America in the quarter and over half of those customers were Gen Z and millennials, demonstrating the brands' resonance with younger consumers.

European Momentum: Tapestry's "runway for growth is significant" in Europe, since it has lower sales and fewer customers there, with the region showing 45% revenue growth in the holiday quarter.

Kate Spade Write-down: Tapestry said on Thursday it had taken a $855 million write-down on Kate Spade largely because of a decline in both current and future expected cash flows along with investments the company is making.

Dividend Increase Announced: Tapestry's board approved a 14% increase to its quarterly dividend, to 40 cents a share. The annualized dividend rate is now $1.60 per share.

XIII. Links & Resources

Official Tapestry Resources: - Investor Relations: tapestry.gcs-web.com - Annual Reports and SEC Filings - Quarterly Earnings Presentations - Corporate Responsibility Reports

Brand Websites: - Coach: coach.com - Kate Spade New York: katespade.com

Industry Analysis: - Bain & Company Luxury Goods Worldwide Market Study - McKinsey State of Fashion Reports - Business of Fashion insights and analysis - WWD coverage of luxury and fashion markets

Financial Analysis: - SEC EDGAR database for official filings - Analyst reports from major investment banks - Trade publications: WWD, Business of Fashion, Vogue Business

Books on Luxury Brand Management: - "The Luxury Strategy" by Jean-Noël Kapferer and Vincent Bastien - "Deluxe: How Luxury Lost Its Luster" by Dana Thomas - "The End of Fashion" by Teri Agins

Historical Resources: - Fashion Institute of Technology Archives - Cooper Hewitt Design Museum Collections - Coach Archive Collection materials

[Note: This analysis represents a point-in-time examination of Tapestry, Inc. based on publicly available information through August 2025. The luxury retail landscape continues to evolve rapidly, and investors should conduct their own due diligence before making investment decisions.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube