Target Corporation: The Rise, Reign, and Reinvention of America's "Cheap Chic" Retailer

I. Introduction & Episode Roadmap

Picture this: It's a Saturday afternoon in suburban Minneapolis, 1962. While construction crews hammer away at a new strip mall on the outskirts of town, Douglas Dayton stands in what will soon become the first Target store, surveying bare concrete floors and imagining something radical—a discount store that doesn't feel like one. His family's department store empire, built over six decades of Minneapolis retail dominance, is about to bet its future on an audacious idea: that American shoppers will pay a little more for a lot more style.

Fast forward to today, and Target Corporation stands as America's seventh-largest retailer, operating over 1,900 stores across all 50 states. With its bullseye logo as recognizable as any brand in America, Target has carved out a unique position in retail's most brutal battlefield—the space between Walmart's everyday low prices and department stores' premium experiences. This is the company that convinced millions of Americans to pronounce its name with a French accent ("Tar-zhay"), that made designer collaborations a retail phenomenon, and that somehow made buying toilet paper feel aspirational.

But here's the tension: after four consecutive years of stagnant sales and a stock price that's down 23% while Walmart gained 13%, Target finds itself at perhaps the most critical juncture in its 63-year discount retail history. The company that once defined "cheap chic" is struggling to maintain what made it special—those eye-catching merchandise displays, immaculate stores, and attentive customer service that justified paying 10-15% more than Walmart.

This February, Michael Fiddelke, a 49-year-old company lifer who's been with Target for 21 years, will take the helm as CEO from Brian Cornell, inheriting both incredible assets and existential challenges. His mandate? Reclaim Target's crown as the retailer that makes mundane shopping feel like small discoveries. The stakes couldn't be higher—in retail, you're either differentiating or dying.

Our journey begins in 1902 with a Presbyterian banker named George Dayton who believed retail could be both profitable and principled. We'll trace how his family built a Minnesota department store dynasty, why they launched into discount retail at the exact same moment as Sam Walton, and how they created a third way in American retail. We'll examine the designer collaboration playbook that changed fashion forever, dissect the Canadian expansion disaster that cost billions, and explore how Target transformed its stores into fulfillment hubs that handle 96% of all sales.

Most critically, we'll answer the question every investor and retail observer is asking: Can Target reclaim its magic, or has the era of "cheap chic" passed into retail history? The answer lies not just in understanding where Target has been, but in recognizing the fundamental tension at its core—the perpetual balance between being accessible enough to compete with Walmart and aspirational enough to command a premium. It's a tightrope walk that's defined Target for six decades, and one that will determine whether this Minneapolis-born retailer thrives or merely survives in the next chapter of American retail.

II. The Dayton Dynasty: Building the Foundation (1902–1960s)

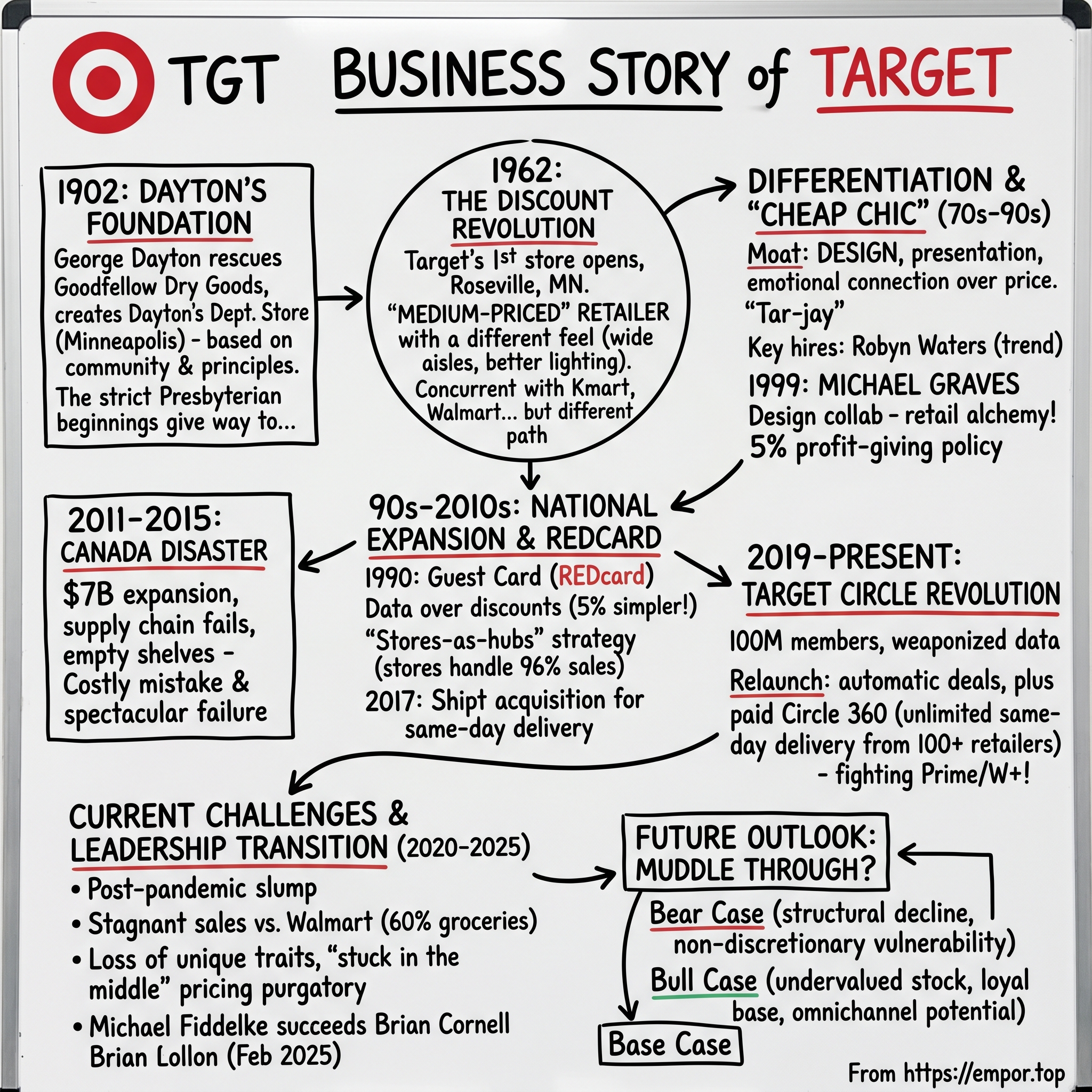

The year was 1902, and George Draper Dayton, a devout Presbyterian banker from New York, arrived in Minneapolis with $1 million in capital and an unusual philosophy for a Gilded Age businessman. While his contemporaries built fortunes through ruthless competition and worker exploitation, Dayton believed commerce could be a force for community good. His first move wasn't to build a store but to rescue one—purchasing the struggling Goodfellow Dry Goods Company on the corner of Nicollet Avenue and Seventh Street in downtown Minneapolis. Within a year, he renamed it the Dayton Dry Goods Company, establishing what would become one of American retail's most enduring dynasties. Unlike the robber barons of his era, Dayton operated the company as a family enterprise over which he held tight control and enforced strict Presbyterian guidelines. The store forbade the selling of alcohol, refused to advertise in newspapers that sponsored liquor ads, and would not allow any business activity on Sundays.

This wasn't just religious conviction—it was shrewd business strategy. In an era when department stores often felt seedy and transactional, Dayton created an oasis of middle-class respectability. His store soon became known for dependable merchandise, fair business practices and a generous spirit of giving. The formula worked spectacularly: The store made its first annual profit and continued to make a profit every year thereafter.

In 1918, Dayton, who donated most of his money to charity, founded the Dayton Foundation with $1 million—an astronomical sum when the average American earned less than $1,500 annually. This wasn't mere philanthropy; it was the beginning of a revolutionary corporate philosophy that would later inspire Target's famous "5% giving policy," dedicating that percentage of profits to community causes.

By the 1920s, the Dayton Company was a multimillion-dollar business that had filled the entire six-story building. The timing of the company's first major acquisition reveals both courage and catastrophic timing: The company made its first expansion with the acquisition of the Minneapolis-based jeweler J.B. Hudson & Son right before the Wall Street Crash of 1929; its jewelry store operated in a net loss during the Great Depression, but its department store weathered the economic crisis.

Tragedy struck the family in 1923 when David died at age 43, forcing George to increasingly rely on his other son, Nelson. When George Dayton died in 1938, he was succeeded by his son Nelson as the president of the $14 million business, who maintained the strict Presbyterian guidelines and conservative management style of his father. Nelson Dayton took over the presidency and saw it grow to a $50 million enterprise.

The real revolution came in 1950 when Nelson died and was replaced as president by his son Donald, who ran the company alongside four of his cousins instead of under a single person. This third generation fundamentally transformed the company's culture. They replaced the Presbyterian guidelines with a more secular approach. It began selling alcohol and operating on Sundays and favored a more radical, aggressive, innovative, costly, and expansive management style.

The Dayton cousins weren't just liberalizing store policies—they were reimagining what a department store could be. In 1956, the Dayton Company opened Southdale Center, a two-level shopping center in the Minneapolis suburb of Edina. Because there were only 113 good shopping days in a year in Minneapolis, the architect built the mall under a cover, making it the world's first fully enclosed shopping mall. This wasn't just about weather—it was about creating a new kind of social space, a climate-controlled Main Street where shopping became entertainment.

By the early 1960s, the Dayton Company had built an empire worth hundreds of millions, with Dayton's becoming the country's second-largest privately owned department store chain by 1964. But the cousins saw storm clouds gathering. Discount chains were sprouting across America, threatening to make traditional department stores obsolete. The family faced a choice: protect their premium brand and slowly decline, or cannibalize themselves before someone else did.

The answer came from an unlikely source: John F. Geisse, a Dayton's employee who had been studying a new breed of retailer. While working for the Dayton company, John F. Geisse developed the concept of upscale discount retailing. His radical idea? Create a discount store that didn't feel like one—cleaner, brighter, better organized than the competition, with wider aisles and higher-quality merchandise. The Dayton board was skeptical. Why risk their sterling reputation on a down-market venture? But Geisse and Douglas Dayton, the youngest of the five cousins, persisted. They weren't proposing to create just another discount store. They were proposing to invent an entirely new category.

III. The Class of 1962: Birth of a Discount Revolution

The date was May 1, 1962, and Douglas Dayton stood in a former suburban bowling alley in Roseville, Minnesota, watching workers hang the last of the red and white signs. The Dayton Company, using Geisse's concepts, opened its first Target discount store, located at 1515 West County Road B in Roseville, a suburb of Saint Paul, Minnesota. The company's marketing team had agonized over the name for months. The name "Target" originated from Dayton's publicity director, Stewart K. Widdess, and was intended to prevent consumers from associating the new discount store chain with the department store. The bullseye logo—clean, modern, memorable—suggested precision rather than cheapness. The remarkable synchronicity of 1962 wasn't mere coincidence—it was a response to seismic shifts in American society. Under the leadership of executive Harry Cunningham, S.S. Kresge Company opened the first Kmart on March 1, 1962, in Garden City, Michigan, while on July 2, 1962, Walton opened the first Wal-Mart Discount City store in Rogers, Arkansas, and Dayton's opened the first Target store in Roseville, Minnesota on May 1, 1962. The concept reflected a wider retail trend of the early 1960s, when chains were experimenting with discount formats that offered department-store goods at lower prices by reducing services and overhead, with several other discount chains including Woolco (a division of F.W. Woolworth Co.) also opening their first stores that year, reflecting suburban growth and increasing consumer demand for lower prices and self-service shopping.

But while Kmart, Walmart, and even the mighty Woolco (backed by F.W. Woolworth's vast resources) focused on rock-bottom prices, Target took a contrarian path. The name "Target" originated from Dayton's publicity director, Stewart K. Widdess, and was intended to prevent consumers from associating the new discount store chain with the department store. This wasn't just branding—it was strategic positioning. When Dayton's opened its first Target store, the company refused to call it a discount store, preferring to call Target a "medium-priced" retailer.

The original Target retail store was co-founded by John Geisse and Douglas Dayton, with Douglas Dayton serving as the first president of Target. The Roseville store was 68,800 square feet of revolutionary retail thinking. Where competitors crammed merchandise into narrow aisles under harsh fluorescent lights, Target invested in wider aisles, better lighting, and color-coordinated displays. The difference was immediately apparent—and immediately successful.

The new subsidiary ended its first year with four units, all in Minnesota, and Target Stores lost money in its initial years but reported its first gain in 1965, with sales reaching $39 million, allowing a fifth store to open in the Minneapolis suburb of Bloomington. This early struggle revealed a crucial insight: Target's model required scale to work. The higher costs of better store design, employee training, and merchandise curation meant thinner margins that could only be offset through volume.

Target didn't initially intend to become a nationwide chain, spending four years tweaking its brand at its Twin Cities home base before expanding to Denver. This patience—almost unthinkable in today's growth-at-all-costs environment—allowed Target to perfect what would become its signature approach. While Sam Walton was rapidly expanding Walmart across rural Arkansas and Oklahoma, targeting underserved small towns, Target methodically refined its suburban strategy.

The geographic strategies of the three discount giants revealed their fundamental differences. While Kmart and Target focused on urban and suburban areas, Walmart founder Sam Walton zeroed in on rural towns overlooked by competitors, and that geographic focus helped Walmart grow quickly—without fighting for space in crowded markets. Target, meanwhile, planted its flag firmly in America's growing suburbs, betting that the new suburban middle class would pay slightly more for a significantly better shopping experience.

In the 1970s, Target committed to setting itself apart by focusing on "better merchandise in every line that stresses good taste and high fashion with careful attention to design." This wasn't just marketing speak—it represented a fundamental reimagining of discount retail. Where Walmart and Kmart competed on price, racing to the bottom with ever-thinner margins, Target chose to compete on experience.

The 1975 "race track" store layout innovation exemplified this approach. Rather than the maze-like layouts of traditional discount stores, Target created a circular path that naturally guided shoppers through the entire store, with clear sightlines and logical product adjacencies. Combined with intensive employee training for expedited checkout—revolutionary in an era of surly discount store service—Target was creating something entirely new: a discount store that didn't feel like one.

By decade's end, the bet was paying off spectacularly. By 1975, Target had become Dayton-Hudson Corporation's leading revenue producer, and four years later its annual sales surpassed $1 billion. The company that had started as an experiment, a hedge against the decline of department stores, had become the engine of the entire Dayton enterprise. More importantly, it had proven that there was indeed a middle ground in American retail—a space between Walmart's relentless price focus and department stores' premium positioning. This was the birth of a new retail category, one that Target would dominate for decades to come.

IV. Differentiation Strategy: Creating "Cheap Chic" (1970s–1990s)

The moment that crystallized Target's destiny came in 1984, when a buyer named Robyn Waters walked through a Target store in Minneapolis and had an epiphany. The merchandise was fine, the stores were clean, but something was missing—soul. Waters, who would become Target's first vice president of trend, design, and product development, saw an opportunity that her competitors couldn't even imagine: What if a discount store could make people feel something?

Rather than compete on price with Walmart, Target distinguished its brand as a more fashionable alternative, justifying slightly higher prices with a more luxurious-feeling shopping experience. This wasn't just repositioning—it was retail alchemy, transforming the mundane act of buying detergent and diapers into something approaching retail therapy.

The transformation began with small touches that revealed big ambitions. In 1982, Target introduced Honors, its first private label line—not just cheaper alternatives to national brands, but products with distinct design sensibilities. Where Kmart's private labels screamed "generic," Target's whispered "sophisticated." The packaging was cleaner, the fonts more modern, the color palettes more considered. These weren't just products; they were signals that Target understood its customers wanted to feel smart about their purchases, not just thrifty. The breakthrough moment came through serendipity. In 1997–98, when Graves designed the scaffolding used in the restoration of the Washington Monument in Washington D.C., he met Ron Johnson, a Target executive who appreciated his product designs. (The Target Corporation contributed $6 million toward restoration of the monument.) The result of their acquaintance was the formation of a business relationship between Graves and the U.S. retailer that lasted until 2012. The Michael Graves Design® Collection for Target debuted in January 1999 and pioneered the movement to bring innovative design to all. Throughout the last 13 years, Target and Graves collaborated on more than 2,000 products, including the now famous Pop Art Toaster and Spinning Whistle Teakettle.

This wasn't just another vendor relationship—it was retail revolution. In 1997, Target trailed behind Walmart and Kmart. Target knew they couldn't beat Walmart on price. Michael Graves helped them realize they could stand out with a differentiating merchandise strategy. The teakettle alone told the entire story: where Walmart sold a $7 kettle that worked, Target sold a $20 kettle that made you smile. The difference wasn't function—it was feeling.

Target evolved into a destination that blurs the line between department store and upscale discount store, earning the nickname "Tar-jay" through strategic partnerships with designers. This French pronunciation, initially used mockingly by competitors, was embraced by Target customers as a badge of honor. It signified membership in a tribe that understood value didn't just mean cheap—it meant getting more than you paid for, including the intangible pleasure of owning something beautiful.

The economics of "cheap chic" were counterintuitive but brilliant. By investing in design and presentation, Target could command price premiums of 10-20% over Walmart on comparable items. A basic white t-shirt might cost $5 at Walmart and $7 at Target, but Target's version came with better packaging, more thoughtful store placement, and the psychological satisfaction of shopping somewhere that didn't feel like a warehouse. These small premiums, multiplied across millions of transactions, funded the very improvements that justified them—a virtuous cycle of differentiation.

Building the foundation for designer collaborations and exclusive brands became Target's moat. Where Walmart competed through supply chain efficiency and Kmart through promotional pricing, Target competed through curation. The company's buyers weren't just looking for the lowest cost goods—they were searching for products that told a story, that made customers feel clever for finding them.

By 1975, it had become Dayton-Hudson Corporation's leading revenue producer, and four years later its annual sales surpassed $1 billion. This growth validated a crucial insight: American consumers, especially suburban women aged 25-54 who comprised Target's core demographic, would pay for the psychological benefits of smart shopping. They wanted to feel both thrifty and tasteful, practical and indulgent.

The strategic decision to focus on suburban markets and customer experience was paying massive dividends. While Walmart conquered rural America and Kmart battled for urban dollars, Target owned the suburbs—the fastest-growing, most affluent demographic in America. These customers had disposable income but also mortgages, children's college funds, and 401(k)s to consider. They couldn't shop at Nordstrom for everything, but they didn't want to feel like they were settling when they shopped for necessities.

How Target created a unique position between Walmart's low prices and department store quality became a Harvard Business School case study in positioning. The company had discovered retail's holy grail: a sustainable competitive advantage based not on operational excellence (which could be copied) or price (which could be undercut) but on brand perception and emotional connection. As one retail analyst put it, "Target made shopping for toothpaste feel like shopping for shoes."

By the 1990s, Target had codified its "cheap chic" formula into a repeatable playbook: identify emerging trends in high-end retail, translate them for mass market, partner with name designers for credibility, present products in an elevated store environment, and price just high enough to maintain quality perception but low enough to drive volume. It was a strategy that would soon transform Target from regional player to national powerhouse, setting the stage for explosive growth in the decades ahead.

V. National Expansion & The Rise of RedCard (1990s–2010s)

The morning of March 19, 1990, marked a turning point that would define Target's next chapter. In a nondescript conference room in Minneapolis, executives unveiled what seemed like a modest plastic card but represented a radical rethinking of discount retail: the Target Guest Card, later to become the REDcard. This wasn't just another store credit card—it was a Trojan horse designed to transform one-time bargain hunters into lifetime brand advocates.

The introduction and evolution of the REDcard program reflected Target's sophisticated understanding of customer psychology. While competitors offered complex point systems and rotating categories, Target kept it brilliantly simple: Target RedCard credit and debit cards offering 5% savings on every purchase versus 1% for regular members. No math required, no hoops to jump through—just instant gratification at checkout. The genius lay in the behavioral economics: that 5% discount psychologically offset the price premium Target charged versus Walmart, making customers feel like insiders getting a special deal.

But the REDcard's true power wasn't the discount—it was the data. Every swipe gave Target unprecedented visibility into customer behavior, allowing them to track not just what people bought, but when, how often, and in what combinations. This data would become the foundation for Target's legendary predictive analytics, including the famous (and controversial) ability to identify pregnant customers before they'd announced it based on their purchasing patterns.

The aggressive store expansion and the race for national footprint accelerated through the 1990s. Target opened its 500th store in 1990, its 1,000th in 2000, and by 2005 operated over 1,400 locations. But unlike Walmart's scatter-shot approach of entering any market that would have them, Target's expansion followed a disciplined strategy: clusters of stores in affluent suburban markets, creating density that justified advertising spend and distribution infrastructure. Target Corporation's 1998 acquisition of Associated Merchandising Corporation signaled ambitions beyond domestic retail, providing sourcing capabilities that would theoretically support international expansion. The stage was set for what should have been Target's crowning achievement: conquering Canada.

The Canada expansion disaster (2011-2015) remains one of the most spectacular retail failures in history. Under Gregg Steinhafel (Target's CEO at the time), the company paid $1.8 billion for the leases to the entire Zellers department store chain in 2011 and formulated a plan to open 124 locations by the end of 2013. The corporation's entry into Canada was uncharacteristically bold—not just for Target, but for any retailer. Not only that, but the chain expected to be profitable within its first year of operations.

The numbers tell a story of corporate hubris meeting operational reality: For Target it was a costly mistake: it is taking a $5.4 billion writedown on the Canada business and had a total net loss in the Great White North of some $2 billion. It had spent $7 billion on the expansion so far, and it didn't project turning a profit until at least 2021. The end result was that Target Canada filed for bankruptcy, wasted billions of dollars, tarnished its reputation and left approximately 17,600 people without jobs.

What went wrong reads like a business school case study in overconfidence. The supply chain systems didn't communicate properly—product dimensions were frequently wrong, inventory data was corrupted, and the three separate systems for different operations couldn't sync. Empty shelves became the defining image of Target Canada, the antithesis of everything the brand represented. Canadian shoppers, who had crossed the border for years to shop at U.S. Target stores, found higher prices, less selection, and a shopping experience that felt like a pale imitation of the original.

The lessons learned were brutal but valuable. Target discovered that its success wasn't just about red bullseyes and wide aisles—it was about decades of refined supply chain excellence, vendor relationships, and operational know-how that couldn't be replicated overnight. The company that had spent 50 years perfecting suburban American retail tried to compress that learning curve into two years in a foreign market.

Meanwhile, back home, the digital revolution was accelerating. Building omnichannel capabilities became essential for survival. Target.com, launched in 1999, had long been an afterthought—a necessary evil in the internet age rather than a strategic priority. But as Amazon's growth trajectory went vertical and Walmart poured billions into e-commerce, Target faced an existential question: Could a company built on the in-store experience compete in a world moving online?

The answer came through acquisition and innovation. Target acquired Shipt in 2017 for $550 million, instantly gaining same-day delivery capabilities. But more importantly, the company reimagined its stores not as liabilities in the digital age but as assets—mini-fulfillment centers positioned within miles of most Americans. This "stores-as-hubs" strategy would become the foundation of Target's digital transformation.

Competition intensifies across all fronts. Walmart's supercenters, with their one-stop shopping convenience and grocery dominance, pulled price-conscious consumers away. Amazon's rise transformed not just how people shopped but what they expected—infinite selection, instant gratification, algorithmic personalization. Dollar stores nibbled from below, offering convenience and rock-bottom prices for everyday essentials.

Yet through it all, the REDcard remained Target's secret weapon. By 2019, REDcard penetration reached nearly 25% of transactions, creating a loyal customer base that was both more profitable and more predictable. These weren't just customers—they were members of the Target tribe, psychologically invested in the brand's success. The 5% discount had become almost irrelevant; what mattered was belonging to something that felt special in an increasingly commoditized retail landscape.

VI. The Digital Transformation Era (2010s–2020)

The boardroom at Target headquarters was silent as Brian Cornell walked in for his first meeting as CEO in August 2014. The former Pepsi and Sam's Club executive was Target's first outside CEO in its history—a signal that the board knew dramatic change was needed. Cornell surveyed the room and delivered his assessment with characteristic bluntness: "We're trying to be all things to all people, and we're not winning at anything. "Brian Cornell taking the helm in 2014 represented more than just a leadership change—it was an admission that Target's insular culture needed disruption. In 2014, Cornell became the first outsider CEO in Target's history, a move signaling the company's desire to transform its culture and image after a massive data breach and disappointing Canada expansion. Cornell replaced former CEO Gregg Steinhafel, who stepped down nearly five months after Target disclosed a huge data breach in which hackers stole millions of customers' credit- and debit-card records.

Cornell's diagnosis was swift and brutal. The Canada disaster had cost billions. The data breach had shattered customer trust. And most fundamentally, Target had lost its way strategically—trying to compete with Walmart on price while matching Amazon on selection, succeeding at neither. His prescription was radical: shrink to grow, focus to win.

The Store-as-fulfillment-hub strategy became Cornell's signature innovation. Brian and team made significant investments in digital, and supply chain capabilities, placing the company's fleet of popular stores at the center both of physical shopping and digital fulfillment. Rather than viewing stores as liabilities in the digital age, Cornell reimagined them as assets—1,900 mini-distribution centers positioned within 10 miles of 75% of Americans. Stores serving as fulfillment hubs handling 96% of sales transformed what had been Target's weakness into its greatest strength.

The 2017 acquisition of Shipt for $550 million was the linchpin of this strategy. Target's 2017 acquisition of Shipt helped bolster the discounter's same-day, store-based fulfillment services. But this wasn't just about delivery—it was about redefining convenience. Same-day services expanded rapidly: Drive Up, where employees loaded groceries directly into customers' cars; Order Pickup, allowing customers to grab online orders within hours; and Shipt's personal shopping service competing directly with Amazon's immediacy.

The numbers validated the strategy spectacularly. Digital sales grew from a rounding error to over $10 billion annually by 2020. More importantly, these weren't purely incremental sales—they were defensive moves that prevented customer defection to Amazon. A customer who used Drive Up visited Target 2.5x more frequently than one who didn't, spending 50% more annually.

Small-format stores and urban expansion represented another counterintuitive bet. While competitors were building ever-larger supercenters, Cornell launched stores as small as 20,000 square feet in dense urban neighborhoods and college campuses. These weren't just stores—they were brand ambassadors, introducing Target to demographics that had never experienced the brand's magic.

The Store-within-a-store concepts with brands like Walt Disney, Apple, and Ulta Beauty serving as customer magnets revolutionized the shopping experience. The Ulta partnership, launched in 2020, brought prestige beauty to Target's aisles—a category the retailer had never successfully cracked. Disney shops created destination experiences that drew families. Apple sections legitimized Target's consumer electronics offerings. Each partnership wasn't just about products—it was about borrowing brand equity and creating reasons to visit beyond routine shopping.

Then came 2020, and everything changed. The COVID-19 pandemic could have been Target's undoing—a retailer dependent on the joy of discovery suddenly faced with terrified customers avoiding stores. Instead, it became Target's finest hour. Comparable in-store sales increased 6.9% and digital sales grew 118%. The investments Cornell had made in digital infrastructure, once criticized as excessive, suddenly looked prescient.

But the real genius wasn't in the technology—it was in the execution. Target's employees, trained for years in the company's guest-first culture, pivoted seamlessly to become personal shoppers, fulfillment experts, and safety ambassadors. The company's decision to give employees hazard pay and implement generous sick leave policies created loyalty that translated into exceptional service during the crisis.

The pandemic also accelerated behavioral changes that might have taken a decade to unfold. Customers who had never ordered groceries online became Drive Up converts. Digital penetration jumped from 7% to 18% of sales in mere months. Target had spent years building capabilities for a future that arrived all at once.

Yet success bred new challenges. The surge in digital fulfillment stressed store operations. Employees rushing to fill online orders sometimes neglected in-store customers. The carefully curated store experience that defined Target began to fray as aisles became fulfillment highways. Cornell spearheaded the company's mission to transform its stores into delivery hubs to cut down on costs and speed up deliveries, but the move helped to reduce costs and speed up deliveries, but the in-person experience for shoppers suffered as Target diverted store workers to fulfilling orders placed online.

By 2022, cracks were showing. The company bought too much merchandise, so it had to deal with a glut of unsold inventory just as decades-high inflation pressured the wallets of many of its shoppers. Target reported a 52% drop in profits during its 2022 first quarter compared with a year earlier. The pandemic boom was over, and Target faced a harsh new reality: it had built massive digital capabilities but hadn't figured out how to make them consistently profitable.

The digital transformation had succeeded in keeping Target relevant, but at a cost. The company that once stood for the joy of discovery now excelled at the efficiency of fulfillment. The question looming as Cornell prepared his succession was whether Target could reclaim its soul while maintaining its digital edge—whether it could once again make shopping feel special in an age of algorithmic convenience.

VII. Target Circle Revolution & Modern Loyalty (2019–Present)

The launch event for Target Circle in October 2019 felt more like a tech product unveiling than a retail loyalty program announcement. Gone were the plastic cards and paper coupons of the REDcard era. In their place: a sleek mobile experience that promised to transform every Target run into a personalized shopping journey. But behind the Silicon Valley aesthetics lay a more fundamental shift—Target was finally ready to weaponize its data. Since rolling out in 2019, Target Circle has helped over 100 million members save millions of dollars every year. But the real revolution came with the April 2024 relaunch with three membership options including free-to-join with automatic deals at checkout and paid Target Circle 360 at $49 for same-day delivery for Target Circle Card holders, or $99 for others. This wasn't just a loyalty program refresh—it was Target's declaration of war in the membership economy dominated by Amazon Prime and Walmart+.

The genius of the new structure lay in its simplicity. The newness kicks off when Target Circle launches on April 7, with every member getting access to automatic deals applied at checkout — so you can feel confident you're getting the best deal every time, without having to search for or add individual offers. Gone were the days of clipping digital coupons or remembering to activate offers. The friction that had plagued digital loyalty programs disappeared overnight.

The program offering 1% rewards on every Target trip, early access to special sales, and allowing cardholders to vote on non-profit organizations Target will support created an ecosystem of benefits that went beyond transactional savings. The voting mechanism was particularly clever—it transformed routine shopping into a form of civic engagement, making customers feel their purchases had purpose beyond personal consumption.

Target Circle Card (formerly RedCard) earning 5% off every purchase, plus 2% back on dining and gas for Mastercard version maintained its position as the program's crown jewel. With over 20 million active cardholders, the renamed card continued to drive both loyalty and profitability. The 5% discount effectively neutralized Target's price premium versus Walmart for cardholders, while the transaction data provided invaluable customer insights.

But the real game-changer was Target Circle 360. Target Circle 360 is our paid membership that builds on the value of Target Circle with unlimited same-day delivery on $35+ orders, early access to big sales and brand collabs, a selection of free gifts and exclusive discounts to choose from each month. At $99 annually (or $49 for Target Circle Card holders), it undercut Amazon Prime's $139 price while offering comparable benefits.

The May 2025 enhancement transformed the value proposition entirely: Target Circle 360 members can now get same-day delivery from 100-plus retailers with no markups. This benefit makes Target Circle 360 the only membership program to offer no price markups on same-day delivery orders across Shipt's full network of more than 100 grocers and specialty retailers. Suddenly, Target wasn't just competing with Amazon—it was offering something Amazon couldn't: access to local favorites and regional chains through a single membership.

Technology integration and mobile-first approach became the backbone of the new Circle ecosystem. The Target app, downloaded over 70 million times, became a digital Swiss Army knife—price scanner, payment method, delivery tracker, and personalized shopping assistant all in one. Machine learning algorithms analyzed purchase patterns to surface relevant deals, predict needs, and even suggest complementary products.

Data analytics and personalization strategies reached new levels of sophistication. Target could now predict with startling accuracy not just what customers might buy, but when and why. A customer buying certain vitamins and yoga mats might receive offers for athletic wear. Someone purchasing diapers in progressively larger sizes would see age-appropriate toy recommendations. The personalization felt helpful rather than creepy—a delicate balance few retailers managed to achieve.

The numbers validated the strategy. Since the relaunch, Target has welcomed 13 million new members to Target Circle. Members enjoy saving seven hours a month and over $300 a year on average with Target Circle 360. More importantly, Circle members visited 2.5x more frequently and spent 50% more annually than non-members.

Yet challenges emerged. The complexity of three different membership tiers (free Circle, paid Circle 360, and Circle Card) confused some customers. The technology that enabled frictionless shopping also created new pain points when systems failed. Store employees struggled to explain the nuanced benefits of each program tier while managing increasingly complex fulfillment operations.

Competition intensified as well. Walmart+ added streaming services and fuel discounts Target couldn't match. Amazon's ecosystem remained more comprehensive, with Prime Video, Music, and Whole Foods benefits. Dollar General launched its own loyalty program, targeting the price-conscious customers Target had largely abandoned.

Most concerning was the commoditization of same-day delivery. What had been a differentiator in 2020 became table stakes by 2024. Every major retailer offered some form of rapid fulfillment, often at comparable or lower prices. Target's carefully constructed moat was becoming a crowded marketplace.

As 2025 progressed, Target Circle faced an existential question: In a world where every retailer has a loyalty program, every store offers same-day delivery, and every app provides personalized recommendations, what makes Target special? The answer would determine whether Target Circle represented the future of retail loyalty or merely the latest iteration of an old idea. The program had succeeded in creating members, but whether it could create true loyalty—the kind that transcends price and convenience—remained to be seen.

VIII. Current Challenges & Leadership Transition (2020–2025)

The November 2024 earnings call began with an ominous silence. Brian Cornell, typically effusive and optimistic, looked tired as he delivered news that sent Target's stock tumbling 10% in after-hours trading: Comparable sales fell 1.9% in fiscal 2024 with 3.2% drop at stores. After four years of stagnant sales reality, the company that had once defined retail innovation was struggling to grow. The stark numbers told a story of divergence: Walmart stock is up 8% this year, compared to a 27% decline for Target. Over the past three years, Walmart's stock rallied more than 140% as Target's stock sank nearly 40%. The company that had once commanded a premium for its "cheap chic" positioning was now trading at a massive discount to its Arkansas rival.

The Loss of unique traits became painfully apparent to anyone walking Target's aisles. The eye-catching merchandise that once made Target a destination had given way to predictable basics. The well-kept stores that justified premium pricing now felt cluttered as employees rushed to fulfill online orders. The attentive customer service that defined the Target experience had been replaced by harried workers more focused on their fulfillment metrics than helping customers find products.

The root causes ran deeper than operational issues. The key to Walmart and Target's divergent paths lies within their product mixes. Per analysts, 60% of Walmart's sales come from groceries, while 10% come from health and wellness, and the remaining 30% from general merchandise, making it "better positioned for traffic consistency" compared to Target's "50% food, beauty and essentials" mix, with Target's sales mix breaking down to 20% food, 10% beauty, 15% essentials, 15% apparel, 20% home, and 20% hard goods like toys and baby strollers.

This product mix vulnerability became acute as inflation squeezed consumer budgets. When faced with choosing between necessities and nice-to-haves, customers chose necessities—and increasingly bought them at Walmart, where prices were 15-20% lower on average. Target's attempts to compete on price in categories like groceries only confused its brand positioning without winning significant market share.

The Ulta Beauty partnership ending in August 2026 represented another blow to Target's differentiation strategy. The partnership, launched with fanfare in 2020, had brought prestige beauty to hundreds of Target stores, creating a compelling reason for higher-income shoppers to visit. Its dissolution—reportedly due to disagreements over expansion pace and profit sharing—left Target scrambling to fill a crucial gap in its merchandising strategy. The Leadership transition announcement came with mixed reactions. Michael Fiddelke, 49-year-old COO and former CFO, succeeding Brian Cornell as CEO on Feb. 1, with Cornell becoming executive chair. The choice of an insider surprised Wall Street—About 96% of investors polled favored an external hire for Target's next CEO. The board chose Fiddelke after "an extensive external search and assessment of many strong candidates" over several years, but investors clearly wanted fresh blood.

Fiddelke's three priorities revealed both clarity of diagnosis and the magnitude of the challenge ahead: On a call with reporters, Fiddelke said he is "stepping in with urgency to rebuild momentum and return to profitable growth." He laid out three priorities: Reestablishing Target's reputation as a retailer with stylish and unique items, providing a more consistent customer experience and using technology more effectively to operate an efficient business.

The first priority—reestablishing reputation for stylish items—acknowledged that Target had lost its most fundamental differentiator. The company that once made Michael Graves teakettles a cultural phenomenon now struggled to create any products that sparked joy or conversation. Private label brands that once felt special now felt generic, indistinguishable from Walmart's Great Value or Amazon Basics.

The second priority—consistent customer experience—addressed the operational chaos created by the digital transformation. Stores had become fulfillment centers first, shopping destinations second. The carefully orchestrated "race track" layout that once guided customers through delightful discoveries now felt like an obstacle course of fulfillment carts and harried employees.

The third priority—effective technology use—represented both opportunity and challenge. Target's technology infrastructure, while improved, still lagged behind both Walmart's scale-driven efficiency and Amazon's innovation. The company needed to catch up technologically while maintaining the human touch that differentiated physical retail.

Fiddelke's background offered both promise and concern. As chief operating officer and previously chief financial officer, he has overseen efforts that enabled exponential growth across the business, including investments to build and scale the company's stores, supply chain, and digital capabilities. His operational expertise was unquestioned. But whether a longtime insider could provide the fresh perspective needed to reinvent Target remained uncertain.

The market's reaction was brutal but predictable: Target shares fell more than 6% on Wednesday after the company made the CEO announcement. Investors saw an insider taking over at a company that desperately needed an outsider's perspective. They saw continuity when transformation was required.

Yet Fiddelke's words suggested he understood the gravity of the moment: "I am eager to refocus our strategy and build on the assets and capabilities that have made Target a beloved destination for incredible products and a one-of-a-kind shopping experience. And to be clear, we have work to do to reach our full potential."

The challenges facing the incoming CEO were formidable. Target's product mix—heavily weighted toward discretionary categories—made it vulnerable to any economic downturn. Its store footprint, while extensive, lacked the density of Dollar General or the scale of Walmart. Its digital capabilities, while improved, still operated at a loss. And most fundamentally, its brand positioning—caught between Walmart's prices and Amazon's convenience—felt increasingly untenable.

The path forward required nothing less than reinvention. Target needed to rediscover what made it special without abandoning what made it profitable. It needed to serve digital customers without alienating store shoppers. It needed to compete on price without becoming another Walmart. These weren't just operational challenges—they were existential questions about what Target stood for in 21st-century retail.

As 2025 progressed, the clock was ticking. Every day of stagnant sales was another day competitors pulled further ahead. Every quarter of declining traffic was another quarter of lost relevance. Fiddelke would have a brief honeymoon period to articulate his vision and begin executing. But in retail's unforgiving environment, where Amazon added Target's entire annual revenue every few years and Walmart's scale advantages continued to compound, time was a luxury Target couldn't afford.

IX. Competitive Landscape & Market Position

The retail battlefield of 2025 looks nothing like the one Target conquered in the 1990s. Where once stood clear boundaries between discount stores, department stores, and specialty retail, now exists an omnichannel free-for-all where everyone sells everything to everyone, everywhere, all at once. Walmart and Target as household names for affordable shopping, each with unique identity and place in US shoppers' hearts, but with contrasting strategies—yet that uniqueness is increasingly difficult to maintain.

Target's odd position becomes clearer when mapped against its competition: Walmart's bigger brick-and-mortar footprint with over 4,700 U.S. stores dwarfs Target's 1,900. Amazon's online prominence makes Target's digital efforts look quaint by comparison—Amazon's retail revenue exceeds Target's total revenue by nearly 5x. Target will never catch or overtake Walmart but that's not necessary for success—except that not catching up increasingly means becoming irrelevant.

The numbers tell a story of gradual marginalization. Walmart's U.S. market share in general merchandise has grown from 15% to nearly 22% over the past decade. Amazon's share exploded from 5% to 18%. Target's? Stuck at around 4%, neither gaining nor losing significant ground—the definition of treading water in a rising tide.

Yet Target shoppers' brand loyalty remaining secure and distinct from Walmart customers offers a glimmer of hope. Target's customer base skews younger (median age 40 vs. 46 for Walmart), more educated (42% college-educated vs. 28%), and more affluent (median income $70,000 vs. $55,000). These aren't just demographics—they're a tribe, united by shared values around style, quality, and conscious consumption.

But loyalty has limits, especially when Dollar stores and Aldi disrupting from below offer increasing value. Dollar General now operates over 19,000 stores—ten times Target's footprint—bringing $5-and-under convenience to rural and urban America alike. Aldi's 2,400 U.S. stores offer private-label quality that often exceeds Target's at prices 30-40% lower. These aren't competitors for Target's core customers today, but they're training a generation of shoppers that extreme value doesn't require sacrifice.

The battle for grocery market share exemplifies Target's strategic dilemma. Grocery drives traffic—the average American visits a grocery store 1.6 times per week versus 0.3 times for general merchandise. Yet Target's grocery operation remains subscale and unprofitable. With only 20% of sales from food versus Walmart's 60%, Target lacks the volume to negotiate competitive prices or justify fresh distribution infrastructure.

Target's attempts to compete in grocery have been halfhearted at best. The company operates only 250 Super Target stores with full grocery sections, having largely abandoned the format's expansion. Its smaller-format stores carry limited grocery selections that feel more like expensive convenience stores than competitive food retailers. The Good & Gather private label food brand, while successful, can't overcome fundamental scale disadvantages.

The competitive dynamics vary dramatically by category. In apparel, Target holds its own with exclusive brands and designer collaborations. In home goods, Target's aesthetic advantage remains strong. But in electronics, toys, and household essentials—categories that comprise 40% of sales—Target offers little differentiation beyond store experience.

Amazon's impact extends beyond direct competition. By setting expectations for infinite selection, instant gratification, and algorithmic personalization, Amazon has fundamentally changed consumer psychology. Target's 75,000 SKUs feel limited compared to Amazon's 350 million. Target's same-day delivery feels slow compared to Amazon's two-hour windows. Target's personalization feels primitive compared to Amazon's AI-driven recommendations.

Walmart's transformation under Doug McMillon represents perhaps the greatest threat. No longer content to be America's low-price leader, Walmart has systematically attacked Target's advantages. Walmart+ membership program matches Target Circle's benefits. Walmart's store remodels create more appealing shopping environments. Walmart's fashion and home goods offerings increasingly overlap with Target's. When your biggest competitor with 5x your scale starts copying your playbook, differentiation becomes exponentially harder.

The emergence of Chinese competitors adds another dimension of pressure. Shein and Temu have redefined fast fashion and impulse purchasing, offering styles similar to Target's at 70-80% lower prices. While quality and ethics concerns limit their current impact, they're training young consumers that extreme affordability is possible, further pressuring Target's value perception.

Regional competitors pose localized threats that collectively matter. Meijer's 250 supercenters dominate the upper Midwest. H-E-B's 400 stores own Texas. Wegmans, Publix, and Fred Meyer each command fierce loyalty in their regions. While none threatens Target nationally, collectively they constrain expansion opportunities and pressure existing stores.

The most insidious competition comes from specialty retailers going broad. Ulta and Sephora's expansion into mass retail threatens Target's beauty business. Best Buy's health initiatives compete with Target's pharmacy expansion. Dick's Sporting Goods and Lululemon's community engagement rivals Target's local connection. Everyone is becoming everything, making differentiation increasingly difficult.

Target's response has been tactical rather than strategic—matching prices here, adding services there, launching private labels everywhere. But tactical moves can't overcome structural disadvantages. Target needs a strategy that acknowledges it will never beat Walmart on price or Amazon on selection, but offers something neither can match. Whether that something exists in 2025's retail landscape—and whether Michael Fiddelke can find it—will determine if Target thrives or merely survives in the decade ahead.

X. Playbook: Business & Investing Lessons

The Target story offers a masterclass in both retail excellence and the perils of strategic drift. For investors and operators alike, the company's journey from regional department store to national powerhouse to current struggles illuminates timeless principles about competitive advantage, capital allocation, and the challenges of staying relevant across generations.

The power of positioning: Finding white space between competitors remains Target's greatest historical achievement and current challenge. For decades, Target occupied a sweet spot that seemed obvious only in retrospect—more stylish than Walmart, more affordable than department stores. This positioning wasn't just about price points; it was about creating a distinct emotional territory. Target made customers feel smart, not cheap. The lesson: sustainable competitive advantage often comes not from being the best at something, but from being the only one at something.

Maintaining competitive advantage through in-store innovations, collaborations, and preserving unique "chic and accessible" identity worked until it didn't. Target's designer collaborations weren't just merchandise strategies—they were brand statements that said "good design belongs to everyone." The "race track" store layout wasn't just operational efficiency—it was choreographed discovery. But these advantages proved more fragile than expected. When every retailer started chasing "cheap chic," Target's differentiation evaporated. The lesson: competitive advantages based on tactics can be copied; those based on capabilities and culture endure longer.

Loyalty program innovation and customer data utilization shows both promise and limitation. Target Circle's 100 million members generate invaluable data, but data without differentiated action is just storage cost. Target knows its customers' preferences intimately but struggles to translate that knowledge into compelling experiences. Compare this to Costco, whose simple membership model creates both recurring revenue and genuine customer partnership. The lesson: loyalty programs work when they align customer and company incentives, not when they're just discount delivery mechanisms.

The challenges of being "stuck in the middle" have become Target's defining struggle. Porter's generic strategies framework suggests companies must choose: cost leadership or differentiation. Target attempted both and increasingly achieves neither. Its prices aren't low enough to compete with Walmart, its experience isn't premium enough to justify the premium. This strategic purgatory manifests in every decision—should stores prioritize shopping or fulfillment? Should merchandise emphasize style or value? The lesson: strategy is about choosing what not to do as much as what to do.

Omnichannel excellence: When physical stores become an asset, not a liability represents Target's most successful strategic pivot. The store-as-fulfillment-hub model turned potential weakness into strength. With 95% of Americans living within 10 miles of a Target, the company has distribution advantages Amazon can't replicate. Same-day services like Drive Up grew from experiment to essential, handling billions in sales. The lesson: existing assets can be reimagined for new purposes, but only if you're willing to cannibalize old models.

Brand perception vs. operational excellence reveals a fundamental tension. Target's brand remains remarkably strong—awareness exceeds 95%, favorability exceeds 70%. But operational metrics tell a different story: declining traffic, falling comparable sales, market share stagnation. This disconnect suggests brand affinity without behavioral loyalty—customers like Target but increasingly shop elsewhere. The lesson: brand equity is a lagging indicator; by the time it erodes, the business has already declined.

Capital allocation in retail: Store refreshes vs. technology vs. shareholder returns presents impossible tradeoffs. Every dollar spent on store remodels can't be invested in digital capabilities. Every dollar returned to shareholders can't fund merchandise innovation. Target's capital allocation reveals its priorities: maintaining dividends despite declining earnings, underinvesting in technology relative to competitors, and accepting gradual store deterioration. The lesson: capital allocation is strategy in its purest form—follow the money to understand true priorities.

For investors evaluating Target today, several factors demand consideration:

The bear case sees structural decline accelerating: Target's discretionary-heavy mix makes it vulnerable to any economic slowdown. Its subscale grocery operation bleeds cash while failing to drive sufficient traffic. Digital sales remain unprofitable despite massive investment. The brand's differentiation continues eroding while cost disadvantages compound. In this view, Target is a melting ice cube—generating cash today while its competitive position steadily deteriorates.

The bull case sees hidden value and turnaround potential: Target trades at just 11x forward earnings versus Walmart's 35x, suggesting massive multiple expansion opportunity if execution improves. The company's real estate portfolio—largely owned, not leased—provides hidden value and financial flexibility. The new CEO could catalyze strategic transformation, potentially divesting underperforming categories while doubling down on strengths. Customer loyalty, while tested, remains strong enough to support recovery.

The base case sees continued mediocrity: Target muddles through with flattish sales, gradual margin pressure, and market share erosion. The company remains profitable but uninspiring, generating sufficient cash to maintain dividends while slowly losing relevance. This scenario—neither disaster nor triumph—may be the most likely and the most dangerous, as slow decline is harder to address than crisis.

The meta-lesson from Target's journey is that retail success requires constant reinvention. What worked in 1962, 1999, or even 2019 won't work in 2025. The companies that survive retail's brutal natural selection aren't necessarily the strongest or smartest, but the most adaptable. Whether Target can adapt once more—finding new white space in an increasingly crowded market—will determine if this icon of American retail writes another successful chapter or becomes another cautionary tale of former greatness.

XI. Analysis & Future Outlook

Standing at the precipice of a new era under Michael Fiddelke's leadership, Target faces a stark reality: incremental improvement won't suffice. The company needs transformation as dramatic as its 1962 leap into discount retail, but the path forward is far more treacherous than the one George Dayton's descendants navigated six decades ago.

Target's plan for 300 new locations in the next decade sounds ambitious until you realize Dollar General opens that many stores every four months. These new Target stores, primarily small-format urban locations, represent tactical expansion rather than strategic revolution. They'll add $3-4 billion in revenue—meaningful but not transformative for a $100 billion company. More critically, they don't address the fundamental question: what makes Target worth visiting in an age of infinite digital choice?

Can Target reclaim its "cheap chic" crown? The honest answer is probably not—at least not in its original form. The cultural moment that created "cheap chic" has passed. In the 2000s, designer goods were scarce, accessible luxury was novel, and mass fashion moved slowly. Today, Shein drops 6,000 new styles daily, Amazon Basics offers acceptable quality at rock-bottom prices, and social media has democratized style inspiration. Target's quarterly designer collaborations feel quaint against this backdrop of infinite variety and instant gratification.

But Target could create something new—call it "conscious chic." The company's customer base increasingly values sustainability, ethical sourcing, and community impact. The sustainability and ESG angle offers differentiation: Goals like sourcing 100% sustainable materials for owned brands by 2030 create both brand differentiation and potential cost advantages as regulations tighten and consumer preferences shift. Target's commitment to racial equity, LGBTQ+ rights, and community investment resonates with younger consumers who increasingly vote with their wallets.

Private label strategy and margin expansion opportunities remain Target's most underutilized weapon. With 40 owned brands generating $30 billion in sales, Target has scale few retailers can match. But most private labels remain undifferentiated—acceptable alternatives rather than destination products. Imagine if every Target-owned brand had the personality of the original Michael Graves collection, the quality of Kirkland Signature, and the social mission of Patagonia. This isn't impossible—it just requires choosing differentiation over volume.

Target's niche within discount retail and investment in technology for e-commerce and customer pick-up positions it uniquely for a hybrid future. While pure-play e-commerce players struggle with last-mile economics and traditional retailers struggle with digital transformation, Target's stores-as-hubs model could evolve into something revolutionary: stores as community centers, fulfillment nodes, service hubs, and discovery destinations simultaneously.

The technology investments needed aren't in fulfillment automation or app features—they're in reimagining the store experience. Imagine stores where augmented reality transforms shopping into entertainment, where AI stylists provide personalized recommendations, where local entrepreneurs showcase products alongside national brands, where community events make stores gathering places rather than transaction venues. The technology exists; the vision doesn't—yet.

The Bear case remains compelling: Squeezed between Walmart's scale and Amazon's convenience, Target lacks sustainable differentiation. The company's heavy exposure to discretionary categories makes it vulnerable to economic downturns. Its subscale grocery operation drains resources without driving sufficient traffic. Digital investments remain dilutive to profitability. The new CEO, as an insider, may lack the fresh perspective needed for transformation. In this scenario, Target becomes the next Sears—a formerly great retailer that couldn't adapt quickly enough.

The Bull case sees untapped potential: Differentiated positioning, loyal customer base, omnichannel excellence. Target's brand equity, while challenged, remains strong. Its customer base, while shopping less frequently, hasn't defected entirely. The company's omnichannel capabilities, particularly Drive Up and same-day delivery, match anyone's. With the right strategy, Target could leverage these assets into renewed growth. The stock's depressed valuation—trading at decade-low multiples—suggests significant upside if execution improves.

The most likely scenario falls between these extremes. Target will probably stabilize under Fiddelke's leadership, improving operations while maintaining market position. Same-store sales will return to low-single-digit growth. Margins will remain pressured but manageable. The company will remain solidly profitable, generating $6-7 billion in annual cash flow. This "muddle through" scenario isn't exciting, but it's not catastrophic either.

Yet history suggests betting against Target's reinvention is dangerous. This is the company that transformed from department store to discount pioneer, from regional player to national powerhouse, from brick-and-mortar retailer to omnichannel leader. Each transformation seemed impossible until it happened. Each required abandoning successful strategies for uncertain futures.

The next transformation won't come from copying others or perfecting operations. It will come from answering a simple question: What can Target offer that no one else can? The answer isn't lower prices (Walmart wins), infinite selection (Amazon wins), or trendy fashion (fast fashion wins). The answer lies in synthesis—creating experiences that blend physical and digital, global and local, style and value, profit and purpose in ways no algorithm or supply chain can replicate.

Target's future depends not on reclaiming its past but on inventing a new future. The company that taught America that discount didn't mean compromise must now teach us that retail can be more than transaction—it can be transformation. Whether Michael Fiddelke has the vision and courage to lead this transformation will determine if Target's best days are behind it or still to come. The stage is set, the stakes are clear, and the clock is ticking. In retail, as in life, fortune favors the bold. The question is: Will Target be bold enough?

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube