Toll Brothers: America's Luxury Home Builder

I. Introduction: The House That Dreams Built

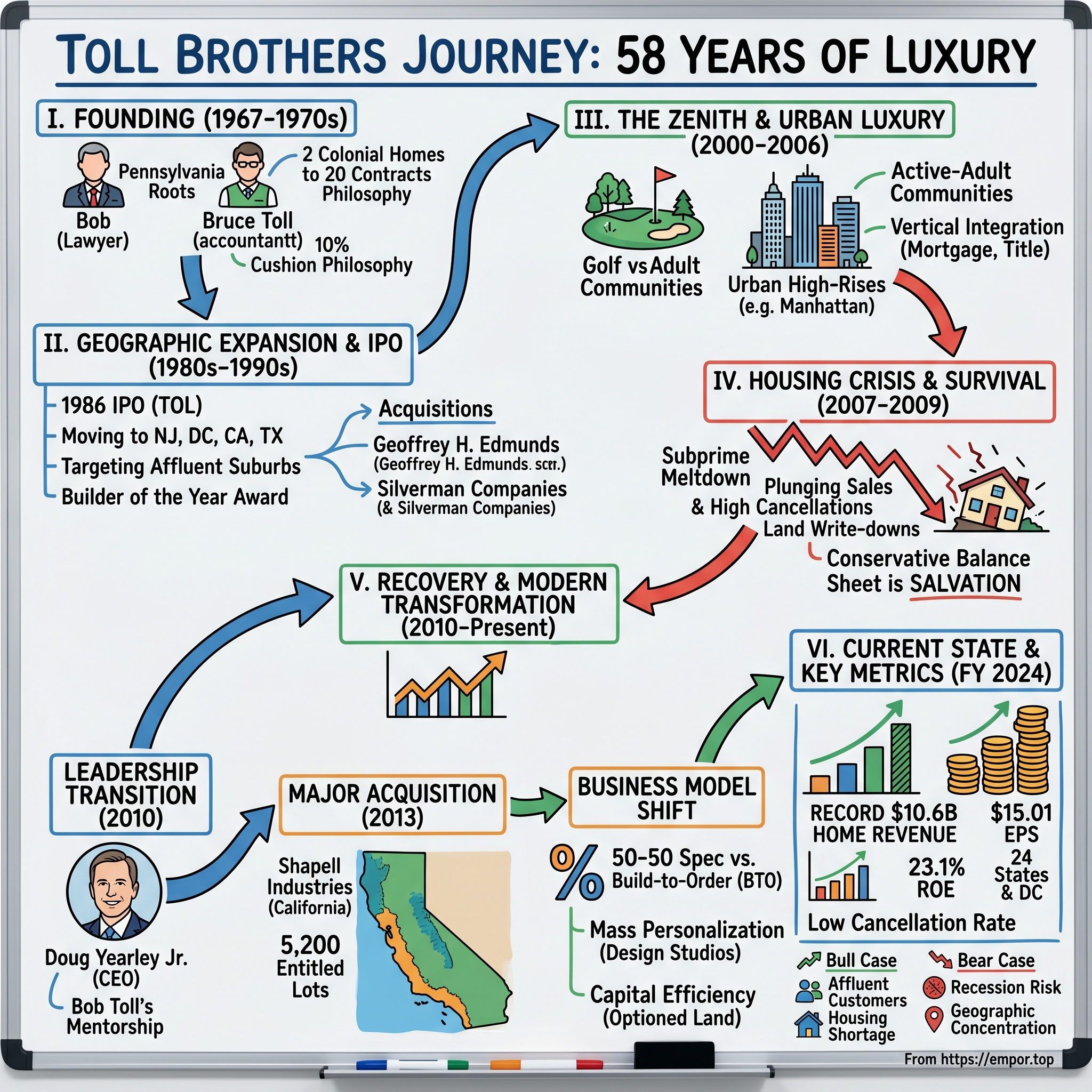

In December 2024, Toll Brothers delivered results that would have seemed impossible to anyone watching the company white-knuckle its way through the 2008 financial crisis. The company generated a record $10.6 billion of home sales revenue, earned $15.01 per diluted share, and grew contracts by 27% in both units and dollars. For a company that once saw its stock crater 80% during the subprime meltdown, these numbers represented not just survival but genuine triumph.

Toll Brothers, Inc. is an American homebuilding company that builds, markets, and finances residential and commercial properties in the United States. In 2020, the company was the fifth largest home builder in the United States, based on homebuilding revenue. The company is ranked 411th on the Fortune 500.

But the financial metrics only tell part of the story. What makes Toll Brothers truly fascinating is how two brothers—one a lawyer, one an accountant—created and sustained a luxury brand in one of America's most cyclical and commodity-like industries. In an era of tract homes and cookie-cutter developments, Bob and Bruce Toll built dream houses. "We're really not a home builder," Bob Toll said in 1988. "We're in the entertainment business. We satisfy dreams and egos."

That philosophy—viewing homebuilding as aspiration rather than mere construction—created a business model that has proven remarkably durable across nearly six decades. At October 31, 2024, the company was operating in 24 states and in the District of Columbia. In the five years ended October 31, 2024, they delivered 49,407 homes from 986 communities, including 10,813 homes from 527 communities in fiscal 2024.

The central question animating this deep dive is deceptively simple: How did a regional Pennsylvania homebuilder become America's luxury housing brand? The answer involves family entrepreneurship, contrarian financial discipline, a near-death experience during the Great Recession, and a strategic transformation that has fundamentally changed how the company operates. Understanding this journey reveals timeless principles about brand positioning, capital allocation, and the art of surviving cyclical industries.

The company is now well positioned with communities in over 60 markets across 24 states featuring the widest offering of luxury homes and serving the most affluent customers in the industry. Last year, they increased community count by 10% and are targeting a similar increase in fiscal 2025. They also owned or controlled approximately 74,700 lots at year end, providing sufficient land for further growth in fiscal 2026 and beyond.

The transformation from two colonial homes in southeastern Pennsylvania to 150,000 families living in Toll Brothers homes represents one of the great business-building stories in American construction history—though one far less celebrated than it deserves. Let's begin at the beginning.

II. The Toll Family Origins & Founding Context (1967–1970s)

Picture southeastern Pennsylvania in 1967. The postwar housing boom that had fueled suburban expansion was maturing. Levittown—the mass-produced housing development that became synonymous with American suburbia—had been built two decades earlier just 20 miles away. The homebuilding playbook was established: buy land, build as many identical homes as cheaply as possible, move fast.

Bob Toll had other ideas.

Bob Toll was only 26 years old at the time and had received his B.A. from Cornell University as well as a law degree from the University of Pennsylvania. Bob served a brief stint as an attorney at a firm called Wolf, Block, Shorr and Solis before determining that his future didn't lie in the legal profession. Both Bob and Bruce had been exposed to the construction business by their father, Albert, who built homes, and Bob believed that industry had more to offer.

Born Dec. 30, 1940, in Philadelphia, Bob Toll grew up in Elkins Park and graduated from Germantown Academy. The son of a real estate developer, he earned a bachelor's degree in political science at Cornell University in 1963 and law degree from Penn in 1966.

In 1967 Bob teamed up with his brother to start building houses. Bruce, who had an accounting degree from the University of Miami, was 24 years old at the time. Their educational backgrounds were a comfortable fit; Bob had a good foundation in principles related to buying land and conducting legal transactions, while Bruce held a firm grip on the basics of the financial side of the business.

The complementary skill sets weren't coincidental—they were foundational. A lawyer who understood land acquisition and contracts. An accountant who could manage cash flow and costs. Together, they possessed the core competencies needed to navigate homebuilding's treacherous economics.

To start out, "we built two homes," Bob Toll recalled. "Instead of selling them, we used them as samples for the lots we owned down the street." These sample homes landed the brothers contracts to build 20 more homes, which each sold for $17,500.

This approach—building demonstrable quality before asking for deposits—embodied a philosophy that would define the company. Rather than racing to the bottom on price, the Tolls bet that buyers would pay more for better homes. They made houses aspirational.

So the company purchased as many lots as possible in desirable locations over the years and displayed eye-popping sample homes to attract buyers before the real construction even began. Today, the company estimates that more than 150,000 families across the United States live in a home built by Toll Brothers. "Everything has to have pizzazz," Mr. Toll told The Inquirer in 1983.

They grew the business using a conservative financial model always including a 10 percent cushion into all their projects and never assuming price appreciation during construction. Bruce was responsible for the book-keeping and Robert the legal side of the business. In the late 1980s, they expanded out of the Northeast to Washington, D.C. and in the mid-1990s, to California. The Tolls are credited with mass-producing luxury housing by taking a few standard home styles and increasing the scale several fold.

That 10 percent cushion became legend in the industry. While competitors operated on razor-thin margins assuming everything would go right, the Tolls built in protection against the inevitable moments when things went wrong. In a cyclical industry where leverage has bankrupted countless builders, this conservatism proved prescient.

By the end of the 1970s, the Toll brothers' patience had paid off. Annual revenues approached $50 million. After spending nearly 15 years constructing houses only in southern Pennsylvania, they decided that it was time to branch out geographically. The regional success had validated their model—now they needed scale.

The playbook was clear: target affluent buyers, build quality homes with options for customization, control land acquisition carefully, and never over-leverage the balance sheet. These principles, established in the company's first decade, would carry Toll Brothers through the next fifty years of booms, busts, and everything in between.

III. Geographic Expansion & Going Public (1980s–1990s)

The 1980s marked Toll Brothers' transition from scrappy regional operator to national ambition. In 1982 they began building homes in central New Jersey. Four years later came the move that would unlock decades of growth.

In May 1986, Toll Brothers incorporated a successor entity in Delaware as Toll Brothers, Inc., and completed its initial public offering (IPO) on the New York Stock Exchange under the ticker symbol TOL, raising $40 million to fund growth. The IPO, executed on July 16, occurred amid a housing market recovery following the early 1980s recession, enabling the company to leverage public capital for scaling operations beyond its Pennsylvania base.

Toll Brothers, Inc. (NYSE: TOL) completed its initial public offering on July 8, 1986, pricing 1.2 million shares at $12.50 each. The IPO provided capital for national expansion amid a favorable housing market in the late 1980s.

For a luxury homebuilder, going public was somewhat counterintuitive. The quarterly earnings pressure that comes with public markets can push companies toward short-term thinking—the last thing a builder needs when land acquisition decisions often don't pay off for 5-10 years. But the Tolls recognized that access to capital markets would be essential for geographic expansion without dangerous leverage.

For fiscal year 1986, the company reported revenues of $124.6 million from 15 communities, reflecting initial post-IPO momentum driven by demand for luxury single-family homes. The public listing facilitated national expansion by providing access to equity financing for land acquisition and market entry, with Toll Brothers adopting a strategy of targeting affluent suburbs and emphasizing high-end customization to differentiate from volume builders.

The expansion strategy was methodical. In 1987 they expanded into northern Delaware and Massachusetts and in 1988 tapped the Maryland market. They typically entered new markets by building their mid-range homes, called "Executive" models. The Executive homes were priced from $170,000 to about $300,000, sported 2,400 to 3,000 square feet, and were located on lots ranging from one-quarter to three-quarters of an acre in size. Once the brothers established the Toll Brothers name in an area with their Executive homes, the company would start building its lower-end and high-end models.

This land-and-expand approach minimized risk while building brand awareness. Start with proven products, establish credibility, then expand the offering. It was brand management as much as homebuilding.

The industry recognized the quality. In 1988, Toll Brothers received Professional Builder magazine's coveted "Builder of the Year" award—a remarkable achievement for a company barely two decades old. By the early 1990s, Toll Brothers had become the largest builder of luxury homes in the U.S.

The mid-1990s brought truly national scale. By 1990, their footprint stretched from Baltimore to Boston. Their transition to a national builder began with their expansion into California and Texas in the early 1990s. Today, they operate in over 60 markets in 24 states and Washington, DC.

In 1994, the Geoffrey H. Edmunds acquisition granted access to Sunbelt markets including Palm Beach County, Florida; Charlotte, North Carolina; and Dallas, Texas, thereby diversifying beyond the Northeast. Revenues grew to $504 million by 1994, underscoring the benefits of geographic broadening and vertical integration, such as owning a lumber mill for cost control. Further incursions included Las Vegas and Nashville in 1997, Rhode Island, New Hampshire, and Colorado in 2000–2001, and South Carolina in 2002, alongside urban condominium projects like those in Hoboken, New Jersey, by 2004. Acquisitions bolstered this footprint, including Detroit's Silverman Companies in 1999.

By the late 1990s, the transformation was undeniable. By 1999, revenues had surged to $1.46 billion, and to $3.9 billion in 2004, reflecting compounded annual growth fueled by low interest rates, rising home prices, and a luxury segment less affected.

The diversification wasn't just geographic. Toll Brothers began building golf communities with the 1991 acquisition of Blue Bell Country Club in Montgomery County, Pennsylvania. The company entered the resort market. Vertical integration followed—title companies, mortgage services, landscaping operations. Each addition strengthened margins and created stickiness with customers who could get everything they needed under one roof.

For investors, the 1990s demonstrated that luxury positioning could provide some insulation from the cycles that ravaged volume builders. When markets softened, Toll Brothers' affluent customers proved more resilient. When markets boomed, aspirational buyers stretched for the Toll Brothers brand. The company had created an enviable position—premium pricing with national scale.

IV. The Housing Boom & Toll Brothers at Its Zenith (2000–2006)

The early 2000s represented American homebuilding's most intoxicating—and ultimately dangerous—era. Fueled by historically low interest rates, loose lending standards, and a collective belief that home prices could never fall nationally, the industry gorged on growth.

Toll Brothers rode the wave magnificently. The company's shares underwent two 2-for-1 stock splits, the first on April 1, 2002, and the second on July 11, 2005, reflecting periods of strong growth prior to the housing market downturn. For shareholders who had bought at the 1986 IPO, the returns were staggering.

In 2006, Toll Brothers expanded into a market segment that seemed to embody the era's excess: Manhattan luxury condominiums. Toll Brothers later expanded into building "active-adult" communities for the elderly affluent and urban high-rises for the newly affluent (Toll Brothers City Living). The first Toll Brothers City Living project—One Ten Third in Manhattan—offered 21 stories and 77 residences to buyers seeking the Toll Brothers brand in an urban setting.

The luxury positioning thesis reached its logical conclusion during these years. Toll Brothers argued that targeting affluent buyers created a moat against cyclicality. Rich buyers were less sensitive to interest rate fluctuations. They had larger down payments. They didn't need to sell existing homes to finance purchases. The logic was elegant and, for several years, appeared to be validated by results.

The vertical integration strategy deepened. Title companies. Mortgage subsidiaries. Landscaping operations. Security systems. Smart home technology. Each service created margin opportunity and customer lock-in. A Toll Brothers buyer could finance, insure, landscape, and secure their home without ever leaving the Toll Brothers ecosystem.

But the boom also brought temptations. Land prices soared. To maintain growth, builders needed to pay ever-higher prices for entitled lots. Toll Brothers, despite its conservative reputation, aggressively expanded its land position. The company reasoned that supply-constrained coastal markets—California, the Northeast—would hold their value even if national prices softened.

This reasoning would prove partially correct and partially catastrophic. The coastal markets did prove more resilient over the long term. But the timing mismatch—between when land was acquired and when homes could be sold—would create enormous pain.

By 2006, warning signs were emerging. Bob Toll himself acknowledged the challenges publicly. "It would be difficult to characterize the position of home builders as other than in a hard landing," said Robert I. Toll, CEO of Toll Brothers. But the full scope of what was coming remained unclear to nearly everyone in the industry.

V. The 2007–2009 Housing Crisis: Near-Death Experience

The Great Recession nearly destroyed American homebuilding. The 2008 financial crisis, also known as the global financial crisis (GFC), was a major worldwide financial crisis centered in the United States. The causes included excessive speculation on property values by both homeowners and financial institutions, leading to the 2000s United States housing bubble. This was exacerbated by predatory lending for subprime mortgages and by deficiencies in regulation.

Large, nationwide declines in home prices had been relatively rare in the US historical data, but the run-up in home prices also had been unprecedented in its scale and scope. Ultimately, home prices fell by over a fifth on average across the nation from the first quarter of 2007 to the second quarter of 2011. This decline in home prices helped to spark the financial crisis of 2007-08.

For Toll Brothers, the crisis cut especially deep. As the largest luxury American homebuilder, the company was "whipsawed by the housing meltdown as much as anyone in construction." The very positioning that had seemed like protection became vulnerability. Luxury homes took longer to sell. Inventory carrying costs mounted. Wealthy buyers—while less desperate than first-time purchasers—simply stopped buying as confidence evaporated.

Homebuilder Toll Brothers Inc. reported a 41 percent plunge in fourth-quarter sales and called on government intervention to help shore up the housing market. The Horsham, Pa.-based company's preliminary results for its fiscal fourth quarter reflected worsening fortunes as the financial crisis took hold: Cancelations jumped 30 percent, while demand and traffic from prospective buyers fell last month to a record low, the company said.

Toll said preliminary home-building revenue declined to $691 million in the three months ended Oct. 31 from $1.17 billion, while backlog dropped 54 percent to $1.33 billion from $2.85 billion. Net signed contracts for the quarter also slid 27 percent to $266.7 million from $365.3 million. For the fiscal year, home-building revenue declined 32 percent to $3.15 billion, and net signed contracts declined 47 percent to $1.61 billion.

Toll Brothers stock price exhibited significant volatility during the 2007–2009 financial crisis, declining sharply as the subprime mortgage collapse impacted homebuilders; it bottomed out in early 2009 before embarking on a multi-year recovery aligned with broader housing sector rebound.

Legal troubles compounded operational challenges. Toll Brothers was sued in April 2007 by a group of investors claiming they were misled by directors about their ability to maintain historically high earnings during the downturn. The lawsuit would eventually settle for $25 million without admission of wrongdoing, but it added uncertainty at the worst possible moment.

The survival playbook required painful measures. Land write-downs devastated earnings as previously valuable lots were marked down to reflect collapsed market values. Workforce reductions cut deeply into an organization that had grown accustomed to expansion. Communities were mothballed. The construction pipeline ground to a halt.

But Toll Brothers' conservative balance sheet—the discipline that had seemed overly cautious during the boom years—proved to be salvation. The company entered the crisis with manageable debt levels and substantial liquidity. While competitors toppled into bankruptcy or were acquired at fire-sale prices, Toll Brothers survived independently.

The crisis reinforced a lesson that Bob and Bruce Toll had learned from their father: homebuilding cycles are brutal and unpredictable. The 10% cushion philosophy that seemed old-fashioned during boom times was revealed as essential wisdom. Companies that had leveraged aggressively to chase growth found themselves with no margin for error when the music stopped.

During the recovery period, Pennsylvania-based public builder Toll Brothers beefed up its attached, active adult, and apartment and condo divisions. The firm also entered several new geographic areas, including western markets such as Denver and Seattle.

The crisis also accelerated industry consolidation that would reshape competitive dynamics for years to come. Smaller builders without access to capital markets vanished. Regional operators retreated. Public builders with strong balance sheets—Toll Brothers among them—emerged in position to capture market share as recovery eventually arrived.

VI. Leadership Transition: The Doug Yearley Era (2010)

In the depths of the crisis, Toll Brothers executed one of the most critical decisions in company history: leadership succession. Douglas C. Yearley Jr. joined Toll Brothers in 1990 and was promoted as chief executive officer in June 2010 and currently holds the position of chairman and chief executive officer.

The transition from founder-led to professional management is notoriously treacherous in family businesses. Many companies that thrive under charismatic founders struggle when that founder steps back. Toll Brothers' succession worked because Doug Yearley wasn't an outsider parachuting in—he had been groomed for two decades.

He has been an officer of the Company since 1994, holding the position of Vice President from January 1994 until January 2002, Senior Vice President from January 2002 until November 2005, and Regional President from November 2005 until November 2009, when he managed home building operations in nine markets throughout the country, oversaw the creation of the Toll Brothers City Living division, and managed the Marketing department. In November 2009, Doug was promoted to Executive Vice President, and then to Chief Executive Officer in June 2010.

The depth of Yearley's preparation was extraordinary. "I spent over 900 Monday nights with Bob," Yearley recalled in a recent interview. "That was his night to teach. That was his night to talk strategy and to do land deals." Every Monday, "Toll University," Bob Toll holding court and teaching. "And finally, after like 10 years, I got the courage to say, Bob, would it be OK if like maybe now I could go a little earlier on a Monday night because other people were leaving at 9 p.m., and we must stay till 2 a.m. And he says to me, 'You and I are going to turn the lights off every Monday night.'"

Initially joining Toll Brothers to specialize in land acquisitions and project management, Yearley learned the home building business from the ground up thanks to his connection with the late and well-loved Bob Toll, who spent every Monday night teaching him the ins and outs of the business.

Yearley brought different skills than the founders. A lawyer by training like Bob Toll, Yearley described his management focus: "I travel a bit; I need to get out and see all the divisions, and we build in 26 states. I know the importance of getting out there and cheerleading the divisions. I spend a lot of time on strategy, there's not a land deal of any size that I don't approve. That's the lawyer in me, I am a lawyer by background. So, I just like to have that control. Bob Toll gave me the marketing department when I was 35, and I will never give that up because our brand is so important."

The emphasis on brand protection reflected Yearley's understanding of Toll Brothers' competitive advantage. In an industry where most players competed on price and volume, the Toll Brothers brand commanded premium pricing. Protecting that brand required vigilance.

In October 2018, Doug was elected to succeed Toll Brothers founder Bob Toll as Chairman of the Board. In 2024, Doug was named one of 25 Top CEOs by Barron's magazine in recognition of his strategic leadership that has positioned the Company for continued success.

Robert Toll stepped down as chairman in 2018 and served exclusively as special advisor to the company. Robert Irwin Toll (December 30, 1940 – October 7, 2022) was an American businessman who co-founded the luxury homebuilder company Toll Brothers. Toll died in New York City from complications of Parkinson's disease on October 7, 2022, at the age of 81.

"Bob had such a profound impact on so many of us in so many unique ways," said Douglas C. Yearley Jr., chairman and CEO of Toll Brothers. "His huge heart, unique sense of humor, zest for life, and profound intelligence."

The founder's death in 2022 marked the end of an era, but the leadership transition had been accomplished years earlier. Yearley had proven himself through the crisis and positioned the company for its next chapter. The challenge facing him was formidable: transform Toll Brothers from a company that had survived the Great Recession into one that could thrive in whatever came next.

VII. The Shapell Acquisition: Doubling Down on California (2013)

In late 2013, with the housing market showing signs of recovery, Toll Brothers executed the largest acquisition in its history. Toll Brothers, Inc., the nation's leading builder of luxury homes, and Shapell Industries, Inc., a premier private California builder, announced that they have entered into a definitive purchase agreement under which Toll Brothers will acquire the home building business of Shapell in a stock acquisition for approximately $1.60 billion in cash. Shapell has a long and illustrious history as one of California's largest and most successful land development and home building companies in the affluent coastal markets of Northern and Southern California. Since its founding in 1955 by brothers Nathan and David Shapell, and brother-in-law Max Webb, Shapell has delivered more than 70,000 homes. Shapell's land portfolio, which Toll Brothers is acquiring, consists of approximately 5,200 home sites, 97.5% of which are entitled, in established communities.

The timing was audacious. Housing markets remained fragile. Many builders were still licking wounds from the crisis. Committing $1.6 billion to expand in California—a market that had experienced some of the most severe price declines—required conviction.

This land was assembled over many decades in many of the state's most affluent and high-growth markets: the San Francisco Bay area, metro Los Angeles, Orange County and the Carlsbad market. Through August 31st of calendar year 2013, Shapell has delivered 347 homes at an average price of $791,000. Having entered the California market in 1994, Toll Brothers has delivered over 7,700 homes, generating approximately $6.5 billion in revenue from more than 90 communities in the state. Toll Brothers is currently offering homes in 9 communities in affluent Coastal California markets at an average price of approximately $1,000,000. The approximately 5,200 lots Toll Brothers expects to acquire from Shapell would bring Toll Brothers' total lots owned and controlled in California to approximately 9,200.

Doug Yearley's enthusiasm was evident: "We are honored and thrilled to have been selected by the Shapell family to continue the legacy of such an amazing company. The tremendous land portfolio the Shapell family has amassed over decades in California presents an incredible opportunity for Toll Brothers. This acquisition will provide significant growth over the coming years and, we believe, will be accretive to earnings in the first year, excluding transaction costs. Shapell's current portfolio dovetails perfectly with our own California footprint and luxury brand, and adds meaningfully to our presence in premier coastal locations in California."

Robert Toll, still active as executive chairman, articulated the strategic rationale: "We believe this is the right acquisition at the right time in the right location for Toll Brothers. We believe this positive side of the housing cycle has significant distance to run, and that this acquisition should mesh well with the strength in the market."

"The portfolio of entitled land we are acquiring may be the last great concentrated assemblage of this scale and quality in coastal California. The combination of the Shapell and Toll Brothers teams and land holdings gives us one of the premier platforms in several of the nation's most dynamic housing markets."

The entitlement angle was crucial. In California, securing building permits can take years and cost millions. Shapell's land portfolio consists of approximately 5,200 home sites, 97.5 percent of which are entitled, in established communities. Toll Brothers was essentially buying years of regulatory work already completed.

Toll Brothers financed the acquisition with a new $485 million 5-year senior unsecured floating rate bank term loan, as well as $600 million of recently issued 5-year and 10-year senior unsecured debt and $230 million of common stock. The balance of the funds will consist of a $370 million draw from its existing $1.035 billion 5-year bank revolving credit facility. In addition, the Company closed on a $500 million 364-day unsecured bank revolving credit facility.

Between cash and untapped bank credit facilities, the company still had approximately $1.5 billion of available liquidity to support current operations and future growth. As previously announced post-closing, Toll Brothers intended to selectively sell approximately $500 million of land to return some expended capital and manage its California concentration.

The Shapell acquisition proved transformative. California became one of Toll Brothers' most important markets, contributing outsized margins due to the supply-constrained nature of coastal real estate. The entitled land portfolio provided years of development pipeline without the risk and cost of new entitlement processes.

More broadly, the deal demonstrated that Toll Brothers had emerged from the crisis with both the financial capacity and management confidence to pursue major strategic initiatives. The company wasn't just surviving—it was positioning for the next decade of growth.

VIII. The Modern Transformation (2015–Present)

The post-Shapell era has seen Toll Brothers fundamentally reimagine how it operates. These and other initiatives have helped improve margins. Since fiscal 2020, adjusted gross margin has steadily improved from around 23.5% to above 28.0%.

The most dramatic shift has been in the balance between build-to-order and speculative construction. Historically, Toll Brothers operated with just 10–15% of homes built on spec. Today, that figure has surged to roughly 50%. The shift reflects evolving consumer demand, particularly among affluent millennials and move-up buyers who prioritize speed and convenience over lengthy design cycles. Toll Brothers' spec homes are not simple stock models; many are curated with design packages that allow personalization, blending efficiency with the premium experience that underpins its luxury brand.

A significant driver of Toll Brothers' success is its operational pivot to a 50-50 balance between spec homes and build-to-order (BTO) homes. This shift has enabled the company to combine efficiency with the personalization options that its buyers demand.

Doug Yearley described the strategy as "mass personalization." "Our spec strategy has allowed us to grow EPS faster, increase our ROE, and increase our operating margin by leveraging overhead," Yearley explains. This balance is critical in today's market, where discretionary buyers expect homes tailored to their preferences. As Yearley notes: "Our buyers personalize their homes with us at our design studios, which generated over $1 billion in sales this year."

Spec homes reduce construction cycle times, improve capital efficiency, and allow Toll Brothers to react nimbly to market demand. In the third quarter of fiscal 2025, the company had 3,200 specs in process and 1,800 permits ready, giving it flexibility as rates ease and demand revives. Meanwhile, build-to-order homes—often tied to premium lots and significant upgrades—remain vital for driving margins, with some topping 30%.

Yearley explained on an earnings call: "When we were building 5% of our communities with spec, in today's market, you would be driving a higher margin because the build-to-order business at the luxury, luxury end of the business, which is what built Toll Brothers, had a higher margin. We would be a much smaller company and we wouldn't be able to drive the same ROE because that land is very expensive. It takes much longer to build the houses and it's much harder to turn the money. So we are very happy with a blend that may be a little bit below that build-to-order margin because we recognize the spec margin, it's at a lower price point. It tends at times to have to be incentivized a little bit more. But when you put it all together, it's still a great margin."

The land strategy has also evolved toward capital efficiency. The company has been strategically shifting its land position, increasing the percentage of optioned land to reduce risk and improve capital efficiency. Rather than owning all lots outright, Toll Brothers increasingly uses option contracts that provide development rights without requiring full capital commitment upfront.

Shareholder returns have been substantial. From May 2022 through December 12, 2023, the Company repurchased approximately 13.3 million shares, or 12% of shares outstanding in May 2022, for an aggregate purchase price of approximately $800 million, or approximately $60.15 per share. Douglas C. Yearley, Jr., chairman and chief executive officer, stated: "Over the past decade, we have demonstrated our commitment to shareholder returns. We have reduced our outstanding share count by nearly 40% through buybacks, net of share issuances, and have increased our dividend from $0.08 per share since commencing it in 2017 to $0.21 per share today."

In FY 2024, Toll Brothers repurchased approximately 4.9 million shares at an average price of $127.79 per share, totaling $627.9 million. The company also paid a quarterly dividend of $0.23 per share and ended the fiscal year with $1.30 billion in cash and cash equivalents.

The transformation has made Toll Brothers a larger, more capital-efficient company. The trade-off is somewhat lower margins on individual spec homes compared to fully customized builds. But the return on equity has improved because capital turns faster. It's a fundamentally different business model than what Bob and Bruce Toll built in 1967—but it's proven remarkably effective.

IX. Current State & Financials

Douglas C. Yearley, Jr., chairman and chief executive officer, stated: "I am very pleased with our fourth quarter results, which cap the strongest year ever for Toll Brothers. For the full year, we generated a record $10.6 billion of home sales revenue, earned $15.01 per diluted share and grew contracts by 27% in both units and dollars. In the fourth quarter, we delivered 3,431 homes and generated $3.3 billion in home sales revenues, up 25% in units and 10% in dollars compared to last year's fourth quarter. Our fourth quarter adjusted gross margin was 27.9%, beating guidance by 40 basis points, and our SG&A expense was 8.3% of home sales revenues, or 30 basis points better than guidance. Our strong margin performance and better than projected home sales revenues drove earnings of $4.63 per diluted share in the quarter, up 13% compared to last year.

Fiscal 2024 was a milestone year for Toll Brothers. For the first time in our history, we generated $10.6 billion of home sales revenues, over $2.0 billion of pre-tax income and over $1.5 billion of net income. We produced record earnings per diluted share of $15.01, a 21% increase.

The company's customer profile reveals its differentiated positioning. As Yearley notes, "In our fourth quarter, approximately 28% of our buyers paid all cash, significantly above our long-term average of approximately 20%. For those who took a mortgage, the average loan-to-value ratio was just 69%."

"In fiscal 2024, we generated a return on beginning equity of 23.1%, driven by our record earnings and strong cash flows that allowed us to return approximately $720 million of capital to shareholders. Our healthy balance sheet, low leverage, and ample liquidity, including significant projected cash flows from operations in fiscal 2025, should allow us to continue investing in our business while returning cash to shareholders well into the future."

The balance sheet remains conservatively positioned. TOL had cash and cash equivalents of $1.303 billion at the fiscal 2024-end compared with $1.3 billion at the fiscal 2023-end. The debt-to-capital ratio improved to 27% from 29.6% at the end of fiscal 2023. The net debt-to-capital ratio also improved to 15.3% from 17.7% in the prior year. At the close of the fourth quarter of fiscal 2024, the company had $1.77 billion available on its $1.96 billion revolving credit facility, set to mature in February 2028.

The geographic and product diversification has reached substantial scale. The company builds high-rise urban luxury condominiums with third-party joint venture partners through Toll Brothers City Living. At October 31, 2024, they were operating in 24 states and in the District of Columbia. At October 31, 2024, they had 1,041 communities in various stages of planning, development or operations containing approximately 74,700 home sites that they owned or controlled through options.

They had a backlog of $6.47 billion (5,996 homes) at October 31, 2024; they expect to deliver approximately 97% of these homes in fiscal 2025.

The industry recognition reflects operational excellence. In 2024, Toll Brothers marked 10 years in a row being named to the Fortune World's Most Admired Companies list and the Company's Chairman and CEO Douglas C. Yearley, Jr. was named one of 25 Top CEOs by Barron's magazine. Toll Brothers has also been named Builder of the Year by Builder magazine and is the first two-time recipient of Builder of the Year from Professional Builder magazine.

The Barron's article noted that under Mr. Yearley's leadership, Toll Brothers has "continued to court well-to-do move-up buyers while widening its price points to attract affluent first-timers," a strategy that has "paid off." The article further stated, "Toll Brothers CEO Douglas Yearley has turned a shortage of existing homes for sale into bumper profits for new ones," citing Toll Brothers' margins as "among the highest in the industry."

X. Playbook: Business & Investing Lessons

Toll Brothers' 58-year history offers a masterclass in building and sustaining a premium brand in a commodity industry. Several principles stand out.

Luxury positioning as a moat. Toll Brothers has aligned its business with buyers insulated from the affordability constraints that have hampered much of the housing market. When mortgage rates spiked in 2022-2024, volume builders offering entry-level homes saw demand crater. Toll Brothers' affluent customers—with larger down payments and less sensitivity to financing costs—continued buying. The company doesn't need lower rates to succeed because it targets customers for whom rates matter less.

Conservative financial management. The founders' philosophy of building in a 10% cushion and never assuming price appreciation during construction proved prescient during the Great Recession. At the end of the first quarter of fiscal 2025, Toll Brothers had more than $2.3 billion of total liquidity, comprising $574.8 million in cash and cash equivalents and $1.77 billion available under the revolver capacity. Also, total debt at the fiscal first-quarter end was $2.75 billion, down from $2.83 billion at fiscal 2024-end. Debt to capital was 26%, down from 27% at fiscal 2024-end.

Vertical integration benefits. The Company operates its own architectural, engineering, mortgage, title, land development, smart home technology, and landscape subsidiaries. These services create margin opportunity and customer stickiness while differentiating from competitors who outsource everything.

Counter-cyclical land acquisition. The Shapell acquisition—buying $1.6 billion of entitled California land in 2013 when competitors were still recovering from the crisis—exemplified opportunistic capital deployment. Bob Toll stated: "The scale and quality of the land that the Shapell family amassed coupled with the dynamism of the markets where their sites are located make this a once-in-a-lifetime opportunity."

Leadership continuity. Doug Yearley's 35+ year tenure before becoming CEO enabled seamless transition. Toll Brothers' CEO is Doug Yearley, appointed in Jun 2010, has a tenure of 15.25 years. The company avoided the disruption that often accompanies founder succession because Yearley had been groomed for decades.

Patience with capital. Land development horizons often stretch 5-10 years. Toll Brothers has consistently taken a long-term view, acquiring land when prices are favorable and holding through cycles. This requires both financial strength and management patience—qualities that distinguish the company from builders focused on quarterly results.

XI. Competitive Landscape & Porter's Five Forces

Understanding Toll Brothers' competitive position requires examining industry structure:

Threat of New Entrants: LOW-MODERATE. Giant homebuilders keep eating up more market share. Back in 2005, publicly-traded homebuilders made up 25% of U.S. new home closings. That figure slowly ticked up to 37% by 2019. However, the recent mortgage rate shock has coincided with publicly traded homebuilders' market share spiking to 51% in 2023. Zonda chief economist Ali Wolf predicts it could soon top 60%. High barriers including capital requirements, land acquisition expertise, entitlement processes, and brand building make new entry difficult. The company has strategically acquired and developed land in desirable locations, often in supply-constrained markets with high barriers to entry.

Bargaining Power of Suppliers: MODERATE. Public builders dominated the marketplace in Q3 2024, purchasing 66% of finished lots. Comparatively, in 2019, public home builders made up just 37% of the market share. Large builders have increasing leverage with suppliers due to scale, though labor shortages persist across the industry.

Bargaining Power of Buyers: LOW-MODERATE. Affluent buyers have less price sensitivity. The company's remarkably low cancellation rate—just 2.5% in Q4 2024—reflects customers' financial stability and commitment. When buyers put down substantial deposits and can afford their purchases, they tend to close.

Threat of Substitutes: MODERATE. Existing homes compete with new construction, but structural factors favor new builds. The "lock-in effect"—existing homeowners reluctant to give up low-rate mortgages—has reduced resale inventory significantly. Rental housing provides an alternative for some, but Toll Brothers targets customers who generally prefer ownership.

Competitive Rivalry: HIGH but differentiated. The top five highest producing builders did not change from 2023 to 2024, with D.R. Horton maintaining its position as America's largest single-family home builder. D.R. Horton captured 13.6% of the market with 93,311 closings, marking a fourth consecutive year with a market share above 10%, and a 23rd consecutive year atop the list. Results also show that 2024 marked the third year in a row where the top three builders accounted for more than a quarter (29.9%) of overall closings, with Lennar and PulteGroup achieving 11.7% and 4.6%, respectively.

KB Home (2.1%), Taylor Morrison (1.9%), Century Communities (1.6%), and Toll Brothers (1.6%) round out the top 10 builders for 2024.

Two major homebuilding peers—Lennar and D.R. Horton—offer useful contrasts to Toll Brothers. Lennar, one of the largest U.S. builders, has long leaned heavily on a spec-driven approach. Its focus on quick delivery and standardized product lines makes Lennar highly efficient in capturing volume demand, particularly in entry-level and move-up segments. By contrast, D.R. Horton, the nation's largest builder by volume, also emphasizes spec production to maintain scale but has diversified with higher-end offerings in certain markets. D.R. Horton has demonstrated that scale-driven spec building can still coexist with premium positioning. Compared to these peers, Toll Brothers targets the luxury niche, where its curated spec homes complement traditional build-to-order offerings. The contrast underscores how Lennar, D.R. Horton, and Toll Brothers are each shaping their future models around different market segments.

XII. Hamilton's 7 Powers Analysis

Hamilton Helmer's framework helps identify sources of durable competitive advantage:

| Power | Applicable? | Analysis |

|---|---|---|

| Scale Economies | PARTIAL | Toll Brothers benefits from purchasing leverage and SG&A absorption, but homebuilding is ultimately local and labor-intensive, limiting scale benefits vs. volume builders |

| Network Effects | LIMITED | Some network effects exist through referrals and reputation, but homebuying isn't inherently networked |

| Counter-Positioning | STRONG | Luxury focus positions Toll differently than volume builders; competitors would cannibalize existing business by moving upmarket |

| Switching Costs | LIMITED | Buyers choose one home at a time; vertical integration creates some stickiness through mortgage and title services |

| Branding | STRONG | 58 years of luxury positioning creates genuine brand premium; "America's Luxury Home Builder" resonates with target customers |

| Cornered Resource | MODERATE | Entitled land in supply-constrained markets (California coastal, Northeast suburbs) provides years of pipeline that competitors cannot easily replicate |

| Process Power | GROWING | The 50-50 spec/BTO model with design studio personalization creates operational efficiency that combines scale with customization |

The strongest Powers for Toll Brothers are Branding (decades of luxury positioning) and Counter-Positioning (volume builders would sacrifice their economics to compete directly). The company's process innovations around spec homes with personalization represent an emerging source of advantage.

XIII. Bull Case vs. Bear Case

Bull Case

The structural shortage of U.S. housing creates a long runway for growth. These trends include the structural shortage of homes in the U.S. (estimated at between 3 and 6 million homes) resulting from well over a decade of underproduction, and favorable demographics driven by millennials, many of whom are buying their first home later in life when they have higher incomes and accumulated wealth, and baby boomers who are moving in retirement. Due primarily to the well-known affordability issues in this country, the average age and wealth of a homebuyer has increased.

The affluent customer base provides resilience. When first-time buyers struggle with affordability, Toll Brothers' customers—with larger down payments and less rate sensitivity—continue transacting. The company doesn't need lower rates to thrive.

The top ten builders captured a record 44.7% of all new U.S. single-family home closings in 2024, up 2.4 percentage points from 2023 (42.3%). This is the highest share ever captured by the top ten builders since NAHB began tracking data in 1989. Industry consolidation benefits well-capitalized public builders who can access land and financing that smaller competitors cannot.

The business model transformation has improved capital efficiency. The spec strategy enables faster turns, higher ROE, and better leverage of overhead. Margins remain strong despite the shift.

Management has demonstrated disciplined capital allocation. Share repurchases have reduced the float by ~40% over a decade while the dividend has grown. The balance sheet remains conservative.

Bear Case

Luxury housing is discretionary spending. In a severe recession, even affluent buyers defer major purchases. The 2008 crisis demonstrated that Toll Brothers isn't immune to cycles—the company saw revenues collapse alongside the broader market.

Geographic concentration creates risk. California and the Northeast—while supply-constrained—are also subject to regulatory headwinds, high taxes, and potential population outflows. Policy changes could impact these markets disproportionately.

The spec strategy involves higher inventory risk. Building before having buyers committed means holding more completed inventory that could require incentives or write-downs if demand softens.

Homebuilding remains fundamentally cyclical and capital-intensive. Even well-managed builders face margin compression and volume declines during downturns. The industry structure limits sustainable competitive advantages.

Valuation has expanded following strong performance. Any earnings disappointment could result in multiple compression in addition to earnings declines.

XIV. Key Performance Indicators to Track

For investors monitoring Toll Brothers' ongoing performance, three metrics matter most:

1. Net Signed Contracts (units and dollars): This leading indicator reveals demand trends before they appear in delivered revenue. Contract growth drives future backlog and ultimately deliveries. Watch for trends in both unit volume and average selling price—divergence between the two signals mix shifts.

2. Adjusted Gross Margin: The spec strategy introduces different margin dynamics than pure build-to-order. Monitoring adjusted gross margin (excluding interest and inventory write-downs) reveals underlying profitability trends. The company has guided to 27-28% as sustainable; significant deviation signals either improving pricing power or competitive pressure.

3. Cancellation Rate: Toll Brothers' historically low cancellation rate reflects customer financial strength. Rising cancellations would indicate stress among the affluent buyer base—an early warning sign of potential volume and margin pressure.

Secondary metrics worth tracking include community count growth (drives selling opportunities), net debt-to-capital ratio (balance sheet health), and share repurchase activity (capital allocation discipline).

XV. Conclusion: The House That Discipline Built

In 1967, two brothers built their first colonial homes in southeastern Pennsylvania with $10,000 in capital and a philosophy that quality mattered. Nearly six decades later, their company has delivered more than 150,000 homes, generated over $10 billion in annual revenue, and established itself as America's preeminent luxury homebuilder.

The journey wasn't linear. The Great Recession nearly destroyed the company. Leadership transitions posed existential risk. Market cycles repeatedly tested the business model. But Toll Brothers survived and ultimately thrived because the foundational principles—conservative financial management, luxury positioning, patient land development—proved durable.

"We're really not a home builder," Bob Toll said in 1988. "We're in the entertainment business. We satisfy dreams and egos."

That insight—understanding that buying a luxury home is emotional, aspirational, almost theatrical—has guided Toll Brothers for decades. The company doesn't sell houses. It sells the dream of the perfect house, customized to each buyer's vision of success.

The modern transformation under Doug Yearley has updated the model for contemporary realities. The 50-50 spec/BTO balance. The design studios generating a billion dollars annually. The disciplined capital returns. These innovations have made Toll Brothers more capital-efficient without sacrificing the brand promise.

For investors, Toll Brothers represents a bet on several converging forces: structural housing shortages, demographic tailwinds from millennials and baby boomers, the continuing consolidation of homebuilding among well-capitalized public companies, and the durability of a 58-year-old luxury brand.

The risks are real—cyclicality, geographic concentration, the inherent leverage of homebuilding. But the Tolls built their company to survive cycles, and that philosophy persists. When the next downturn arrives—and it will—Toll Brothers' conservative balance sheet and affluent customer base should provide relative resilience.

When asked about inspirational leaders, Yearley responded: "Oh, well, I've mentioned Bob like 20 times in this podcast. So, he's at the top, for sure. There's no one like Bob Toll, and you can ask anybody in the industry."

Bob Toll's legacy extends beyond the company that bears his name. He proved that luxury positioning could work in homebuilding—an industry where most players race to the bottom on cost. He demonstrated that conservative financial management, while seemingly old-fashioned during booms, creates survival during busts. And he built a culture strong enough to transcend his own leadership.

Those are lessons worth far more than the price of any house.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube