Terex Corporation: The King of the Earth – From Dump Trucks to Industrial Diversification

Introduction: A Company Forged in Reinvention

Picture a massive yellow dump truck thundering across a mid-century American construction site, kicking up clouds of dust as it hauls tons of earth from a fresh excavation. The year is 1955, and the truck bears the name "Euclid"—a brand so dominant that it controls more than half of all U.S. off-highway dump truck sales. This was the golden age of American industrial might, and Euclid was its workhorse.

Fast forward seven decades, and the corporate descendant of that legendary truck maker is preparing to exit the aerial lift business entirely while merging with a manufacturer of fire trucks and ambulances. The transformation from earthmoving behemoth to diversified specialty equipment maker is one of the most remarkable corporate metamorphoses in American industrial history.

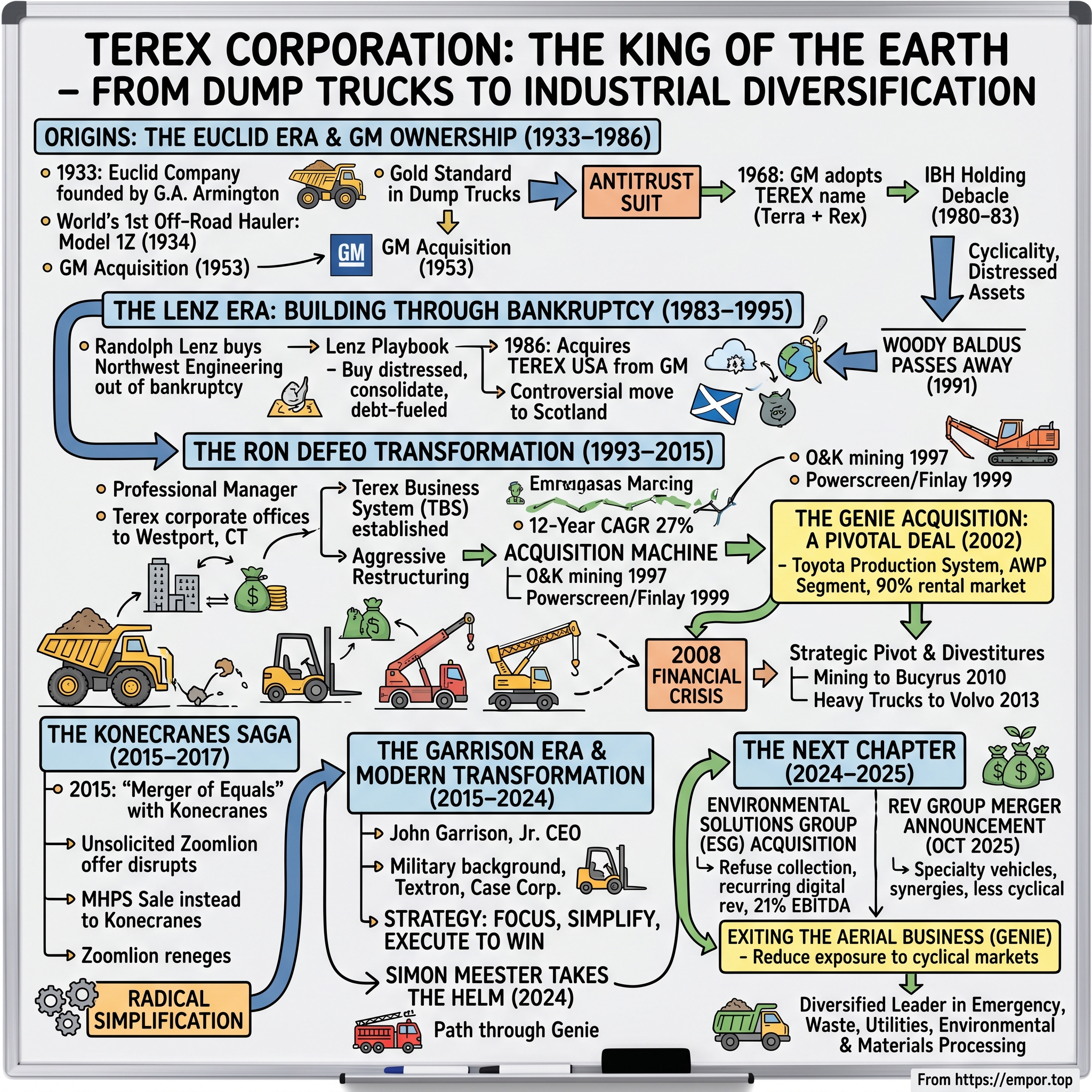

The origins of Terex date to 1933, when the Euclid Company was founded by George A. Armington to build hauling dump trucks. Today, Terex posted full-year sales of $5.1 billion with full-year operating margins of 10.3%. The company's portfolio now spans materials processing machinery, waste and recycling solutions, mobile elevating work platforms, and equipment for the electric utility industry—a far cry from the dump trucks that defined its origins.

The central question of the Terex story is this: How did a collection of bankrupt equipment companies become a focused industrial powerhouse—and what lessons does this serial acquirer teach about portfolio management?

GM coined the "Terex" name in 1968 from the Latin words "terra" (earth) and "rex" (king) for its construction equipment products and trucks not covered by the ruling. The name was prophetic in ways its creators could never have imagined. Terex would indeed become a king—not of earthmoving, but of industrial reinvention.

The themes that define Terex's journey—roll-up strategy, portfolio transformation, cyclicality versus resilience, and the art of knowing when to exit businesses—offer a masterclass in industrial capitalism. Three distinct leadership eras have shaped this company: the debt-fueled roll-up of Randolph Lenz, the acquisition machine of Ron DeFeo, and the strategic simplification under John Garrison and now Simon Meester. Each leader faced different challenges and brought different tools to the task.

Origins: The Euclid Era & GM Ownership (1933–1986)

The Founding Story

In the depths of the Great Depression, when most entrepreneurs were struggling to survive, George A. Armington saw opportunity in the most basic of human activities: moving earth. The company that became Euclid was founded in 1907 in Wickliffe, Ohio, by George A. Armington as Armington Electric Hoist. It was renamed Euclid Crane & Hoist when the plant was relocated to Euclid, Ohio. Euclid built experimental tractors, one crawler and several wheeled, in the 1920s, and entered the construction equipment industry when it introduced the Automatic Rotary Scraper in 1924.

The Model 1Z truck was built by Euclid—considered to be the first true off-highway rear dump truck. This innovation—launching the world's first off-road hauler in 1934—established Euclid as the pioneer of an entirely new category of construction equipment. The Trac-Truk wasn't just a product; it was a proof of concept that massive vehicles could operate effectively beyond the constraints of paved roads.

For the next two decades, Euclid would establish itself as the gold standard in dump trucks. The company's engineering prowess and rugged reliability made its name synonymous with off-highway hauling. Construction crews across America came to depend on Euclid trucks the way farmers depended on John Deere tractors.

The GM Years: From Acquisition to Antitrust

In 1953, General Motors purchased Euclid, expanding the business to include more than half of all U.S. off-highway dump truck sales. The acquisition by the world's largest corporation seemed like validation of Euclid's value—and it was. But dominance came with consequences.

The dominant performance of Euclid had a negative consequence, however, when the US Department of Justice brought an antitrust suit against GM, forcing it to stop manufacturing and selling off-highway trucks in the US for four years, and to divest parts of its Euclid business and the Euclid brand name.

This was the era of aggressive antitrust enforcement, and GM's control of more than half the market triggered government action. The Justice Department forced GM to divest the Euclid brand name and certain product lines—a devastating blow to a business built on brand recognition.

GM adopted Terex as the brand name for the Earthmoving Equipment Division in October, 1968. The British operation retained the Euclid (Great Britain), Ltd. name until December, 1968, when it was renamed General Motors Scotland, Ltd. The Earthmoving Equipment Division was officially renamed the Terex Division on July 1, 1970.

The Terex name was an act of creative necessity. GM needed a new identity for the business it was allowed to keep, and someone in the corporate bureaucracy crafted an elegant solution from classical languages. "Terra" plus "rex" equaled "Terex"—king of the earth. The brand would outlast every other aspect of the original business.

The IBH Holding Debacle

By the early 1980s, GM had grown weary of the cyclical heavy equipment business. The automaker wanted to focus on its core automotive operations, and Terex represented a distraction.

In 1980, in an effort to focus on its automotive business, General Motors agreed to sell Terex to IBH Holding AG, a maker of light- and medium-duty construction equipment in the former Federal Republic of Germany. However, in 1983 IBH Holding filed for bankruptcy, and with pressure from the United Auto Workers, ownership of Terex reverted to General Motors.

The IBH debacle illustrated a pattern that would repeat throughout the heavy equipment industry: international acquirers, unfamiliar with American market dynamics and over-leveraged from the purchase, struggled to manage their new assets. IBH's bankruptcy left Terex in limbo—an orphaned business unit that GM never wanted back but couldn't simply abandon.

GM reorganized the company into separate entities: Terex Equipment Limited in Scotland, Terex do Brasil in Brazil, and Terex USA in Ohio. The corporation was looking for any viable exit, and a most unlikely buyer was about to appear.

The Lenz Era: Building Through Bankruptcy (1983–1995)

The Maverick Investor

A Forbes reporter described Terex's rise: "Randolph W. Lenz was an obscure Wisconsin businessman in 1983 when he was struck by a simple idea. Some of the best buy-out values in the country, Lenz reasoned, could be found among bankrupt and near-bankrupt manufacturers of earth-moving equipment companies with low prices, cleansed assets and a newly pragmatic work force of survivors. From such down-and-outers Lenz, in just six years, has built Terex Corp."

Randolph Lenz was not your typical corporate titan. The story of Terex is also the story of Lenz, an ex-Marine with a degree in psychology from the University of Wisconsin. Born in 1947, Lenz began buying and selling real estate in the late 1960s. He served as president of Milwaukee-based Ranmar Enterprises, Inc. and the Network Investment Real Estate Corporation, in Brookfield, Wisconsin. It was in 1981 that Lenz moved into heavy-equipment manufacturing, buying the assets of the FWD Corporation, a bankrupt manufacturer of snowplows and fire trucks in Clintonville, Wisconsin.

The insight that would define Lenz's career was deceptively simple: distressed industrial companies often retained valuable assets—brands, distribution networks, manufacturing capabilities—even as their balance sheets collapsed. The key was buying at the right price and applying operational discipline.

Lenz, 44, the son of a TV repairman, scavenges among bankrupt and near-bankrupt industrial companies. He owns about half of Terex, formerly Northwest Engineering of Green Bay, Wis.

He buys companies with strong brand names and weak income statements and then tries to fix them by making profitable parts more profitable, consolidating operations, closing plants and selling surplus facilities and real estate. He plays sophisticated financial games, but if he doesn't produce, he's in big trouble. That's because he uses borrowed money. Lots of it.

Building the Roll-Up

Northwest Engineering Co., manufacturer of cranes, power shovels, and draglines, is founded. Randolph W. Lenz buys Northwest Engineering, which had declared bankruptcy.

In 1983, Lenz acquired Northwest Engineering out of bankruptcy. This would become his platform for assembling a heavy equipment empire.

Northwest Engineering, in turn, bought the construction-machinery division of the Pennsylvania-based Bucyrus-Erie Company in March of 1985. At its peak, Bucyrus-Erie had employed more than 700 people, but the company had shut down its production lines in 1983, and the employees that remained were concentrating on spare parts and service. Less than a month out of bankruptcy, Northwest Engineering paid less than $9 million for a company with $20 million a year in sales. Lenz then revived the company's defunct Dynahoe product line: the new Bucyrus Construction Products (BCP) division of Northwest Engineering produced its first backhoe loader in November of 1985. By 1988, Industry Week reported that BCP held a 40 percent share of the market in which its products were sold.

The Bucyrus-Erie acquisition exemplified the Lenz playbook: buy a distressed asset at a fraction of its replacement cost, restart production of proven product lines, and capture market share from competitors who had written off the business.

Lenz and Terex came together in 1986 when Northwest Engineering purchased Terex USA from General Motors Corporation. When Northwest Engineering bought Terex USA in 1986, the agreement included an option to purchase Terex Equipment Limited. Northwest Engineering exercised that option in 1987. Then, in a controversial move, Lenz closed the Terex plant in Ohio, and moved all operations to Scotland.

The Terex acquisition was strategic on multiple levels. The brand name carried recognition value. The Scottish manufacturing facility offered lower costs and access to European markets. And the option structure allowed Lenz to verify the business's viability before committing to the full purchase.

Terex Corporation was incorporated in Delaware in 1986 and listed on the New York Stock Exchange in 1991.

The public listing represented a crucial inflection point. Lenz had built his empire with borrowed money; the stock market offered access to permanent capital and liquidity for his personal holdings. But public markets also demanded a different kind of management discipline than the entrepreneurial approach that had created the company.

Woody Baldus, CEO, passed away in the fall of 1991. Randolph Lenz assumed the title of Chairman and CEO. This led to the recruitment of Ron DeFeo in May 1992.

The death of CEO Woody Baldus created an unexpected succession challenge. Lenz was a dealmaker, not an operator. He needed a professional manager who understood both the equipment industry and public company requirements. His search would lead to one of the most consequential hires in the company's history.

The Ron DeFeo Transformation (1993–2015)

The New Leader

Ron DeFeo joined Terex as President of the company's Heavy Equipment Group in Tulsa, Oklahoma. In 1993, Terex corporate offices were relocated to Westport Connecticut. Then, in October 1993, Ron DeFeo was appointed president and COO of Terex and a member of the Terex board of directors.

Ron DeFeo brought credentials that Lenz lacked. Before joining Terex, Mr. DeFeo was a senior vice president and managing director of Tenneco Inc.'s J. I. Case construction-equipment business in Europe. He also held several managerial positions at Tenneco Inc.'s automotive business.

DeFeo understood heavy equipment—he had run construction equipment operations across Europe. He also understood corporate complexity—J.I. Case was a major agricultural and construction machinery manufacturer with global operations. This combination of industry expertise and corporate experience made him ideal for professionalizing Terex.

DeFeo joined Terex in 1992, as President of the company's then Heavy Equipment Group. He was appointed President and Chief Operating Officer in 1993, became Chief Executive Officer in 1995 and Chairman of the Board in 1998.

Facing a recessionary environment, DeFeo began an aggressive operational and financial restructuring of Terex that included raising additional capital, selling assets, and restructuring operations. Among the actions taken by Terex was a focused effort on turning around Clark Material Handling and the sale of its Fruehauf stock in the private market for $28 million. Terex acquired PPM in 1995 and combined it with earlier acquisitions, solidifying Terex as a leading manufacturer and distributor of cranes.

Randolph Lenz retired from Terex in 1995 and Ron DeFeo became CEO of Terex.

The transition from Lenz to DeFeo marked a fundamental shift in Terex's identity. Under Lenz, the company had been a leveraged collection of distressed assets. Under DeFeo, it would become an operating company with genuine strategic direction.

DeFeo instituted the Terex Business System (TBS) as he led Terex from a financial holding company to an operating model that melded together a collection of more than 50 companies. Under his leadership, the company has experienced a 12-year compound annual growth rate of 27 percent.

A 27% compound annual growth rate over 12 years is extraordinary by any measure. It required constant acquisition activity, disciplined integration, and shrewd portfolio management.

The Acquisition Machine

In 1997, Terex acquired mining business from O&K, including the world's largest hydraulic excavator RH 400, later produced as Cat 6090.

The O&K acquisition expanded Terex's mining capabilities and brought world-class engineering into the fold. The RH 400 excavator was an engineering marvel—the largest hydraulic excavator ever built, capable of loading massive mining trucks in just a few passes.

Powerscreen was founded in 1966 as Ulster Plant, introducing mobile screening by taking machines to the quarry face.

Building out materials processing capabilities, Terex acquired Powerscreen, Finlay, and other crushing and screening brands. These Northern Ireland-based businesses would eventually form the backbone of what remains one of Terex's core segments today.

The Genie Acquisition: A Pivotal Deal (2002)

Terex Corporation today announced that it has signed an Agreement and Plan of Merger with Genie Holdings, Inc., a leading global manufacturer of aerial work platforms with 2001 revenues of $575 million. The purchase consideration will be $75 million, consisting of $64.9 million in Terex common stock and $10.1 million in cash, subject to adjustment.

The Genie acquisition was transformational for reasons that went far beyond the financial terms. At $75 million for a company with $575 million in revenues, the price seemed almost impossibly low. But context matters: Genie was struggling after the post-2000 downturn, and the aerial platform market was consolidating.

Genie Industries was founded in 1966 when Bud Bushnell bought the manufacturing rights to a material lift that operated on compressed air. Customers seemed to be impressed with the "magic in the bottle" that was used to raise and lower the hoist — and, the "Genie" name was born. With growing demand for material lifts and aerial work platforms, products such as man-lifts, stick booms, articulated booms, light towers and telehandlers have been added to the Genie® product line. By the early 2000s, due to the economic downturn, the company decided to seek a partner that held the same values. Terex Corporation, with a history of acquiring equipment manufacturers worldwide proved a good match for the business. In 2002, Genie Industries was sold and became the Terex Aerial Work Platforms (AWP) segment of Terex.

Genie Industries was founded in 1966 by Bud Bushnell. At the time, Bushnell was working for Seattle Bronze, a company that produced hoists in Kent, Washington. Bushnell bought the manufacturing rights to a material lift that operated on compressed air. Bushnell named the product Genie because he thought the hissing sound of the compressed air used to raise the machine's operator sounded like a genie rising from its bottle. The Genie Hoist was patented by Bushnell in 1968.

The Genie deal brought something more valuable than aerial platforms: it brought the Toyota Production System to Terex.

The Genie acquisition was also significant because it introduced Terex to the Toyota Production System management philosophy. Genie had incorporated aspects of this philosophy into its business operations with great success. Terex realized the opportunity to apply these practices to all its business. This led to the establishment of the Terex Business System, or TBS.

The Terex Business System would become the connective tissue that allowed Terex to integrate dozens of acquisitions into a coherent operating company. The principles of continuous improvement, waste elimination, and respect for people—all pillars of Toyota's approach—gave Terex a common language and methodology across its disparate businesses.

Terex understood the value of the institutional knowledge in Genie's people. Bob Wilkerson had been integral to 30 years of leadership. He stayed for over four years after the merger to help the transition of Genie, and its culture, to Terex.

Information and values flowed both ways between Genie and Terex. Many Genie managers became Terex managers. Many ways of working that were Genie's are now adopted by our parent company.

Genie products are commonly used in aviation, construction, entertainment, government and military, industrial, warehousing and retail applications. The equipment rental industry accounts for 90 percent of all Genie product domestic sales and 80 percent of sales outside of the United States.

This concentration of sales through rental companies would prove both a strength and a vulnerability. The rental industry offered large, sophisticated customers who bought in volume and provided recurring revenue. But it also meant Terex was exposed to the buying decisions of a relatively small number of major players—United Rentals, Sunbelt Rentals, and their peers.

The 2008 Financial Crisis & Strategic Pivot (2008–2015)

The Downturn

The global recession of 2008 hit Terex hard, with many markets seeing declines. Terex placed an increased focus on cash management and managing inventory levels during these uncertain times.

The 2008 financial crisis exposed a fundamental vulnerability in Terex's business model: cyclicality. Construction equipment demand is highly sensitive to economic conditions, and the severe recession crushed demand across most of Terex's end markets simultaneously. The company that had grown 27% annually found itself fighting for survival.

Strategic Divestitures Begin

The crisis forced a strategic reckoning. Which businesses offered sustainable competitive positions, and which were simply cyclical commodity operations?

In 2010 Terex sold its mining business to Bucyrus. In December 2013, Volvo Construction Equipment (VCE) acquired the Terex line of heavy haul trucks.

The mining business sale to Bucyrus was particularly significant. Mining equipment was highly cyclical, with demand swinging wildly based on commodity prices. The business also required massive capital investments to stay competitive against giants like Caterpillar. Terex had acquired the mining business in 1997; selling it in 2010 represented a strategic retreat from a market where scale mattered enormously.

The truck sale to Volvo closed the book on Terex's original identity. The company that had begun as a dump truck manufacturer had now exited the truck business entirely. The Terex name—"king of the earth"—now adorned products that had nothing to do with earthmoving.

Port and Material Handling Expansion

In 2009, Terex acquired the port equipment businesses of Fantuzzi and Noell, now part of the material handling and port solutions segment.

Even as it divested cyclical earthmoving businesses, Terex expanded in material handling and port solutions. This represented a bet on global trade growth and port modernization—secular trends that seemed more predictable than construction cycles.

The Konecranes Saga: The Deal That Changed Everything (2015–2017)

The Original Merger Plan

Few corporate transactions have been as convoluted as Terex's dance with Konecranes and Zoomlion. The saga began in 2015 with what seemed like a straightforward strategic combination.

Terex previously had agreed in August 2015 to a "merger of equals" with Konecranes, but an unsolicited $30-per-share takeover offer from Zoomlion in February 2016 derailed those plans.

The Konecranes merger would have created a global leader in lifting and material handling solutions. The Finnish company brought strength in industrial cranes and service; Terex brought port equipment and broader geographic reach. The combination made strategic sense.

After announcing what appeared to a be done deal in the fall of 2015 with Konecranes, Terex officially walked away from the merger in May 2016 after receiving an all-cash, $31-per-share offer from Zoomlion.

Zoomlion Heavy Industries, a major Chinese equipment manufacturer, disrupted everything with an unsolicited bid. The all-cash offer at a significant premium created a fiduciary obligation for Terex's board to explore the opportunity.

In Jan 2016, Terex received an unsolicited, non-binding acquisition proposal, with or without the Material Handling & Port Solutions (MHPS) segment, from Zoomlion to acquire all of Terex's outstanding shares for $30 per share in cash. Although Terex rebuffed Zoomlion's first bid of $30 per share in Mar 2016, the latter raised its bid to $31 a share.

The MHPS Sale Instead

May 16, 2016- Terex Corporation today announced that it has agreed with Konecranes Plc to mutually terminate the Business Combination Agreement (BCA) the companies entered into on August 10, 2015, without payment of a fee by either party. In connection with the termination of the BCA, Terex has signed a definitive agreement to sell its Material Handling and Port Solutions business (MHPS) to Konecranes for total consideration of approximately $1.3 billion. The consideration being paid is comprised of $820 million in cash and 19.6 million newly issued shares of Konecranes.

This was elegant financial engineering. Terex walked away from the merger, but locked in a sale of its MHPS business at attractive terms. The cash and Konecranes shares would strengthen Terex's balance sheet while retaining upside participation in the combined MHPS-Konecranes entity.

However, before it dropped talks with Konecranes, Terex agreed to sell its MHPS business to the Finnish OEM. But once the MHPS business was no longer part of the deal, Zoomlion reneged on its offer to Terex. Subsequently, Terex divested all of its remaining earthmoving equipment offerings. The company sold off its compact construction equipment business—which manufactures midi/mini excavators, wheeled excavators and compact wheel loaders—to Yanmar; exited the skid-steer and compact track loader business; and sold its UK-based operation—which manufactures backhoes, site dumpers and compact compaction rollers—to French manufacturer Mecalac. In just one calendar year, Terex consolidated its corporate structure from five segments to three: aerial work platforms (Genie), cranes (Demag and Terex) and materials processing (Powerscreen, Finley, Evoquip).

The Zoomlion reversal created an unexpected outcome: radical simplification. Without the MHPS business, Zoomlion lost interest. Without a Zoomlion deal, Terex was free to reshape itself. The compact construction and earthmoving divestitures that followed represented a decisive break with the company's past.

According to a release from Zoomlion, though the company remained interested in pursuing a deal with Terex even after the MHPS sale, it "concluded that it would not be able to agree on a price for Terex's business after excluding" that segment. "Zoomlion has concluded that Terex's expectations on the valuation do not adequately reflect the impact of the sale of the MHPS segment," the release reads.

The Garrison Era & Modern Transformation (2015–2024)

New Leadership, New Strategy

Terex Corporation today named John L. Garrison, Jr. Chief Executive Officer and President effective November 2, 2015. He will also become a member of the Terex Board of Directors effective November 2, 2015. Mr. Garrison will succeed outgoing CEO Ronald M. DeFeo, who will continue to serve as Executive Chairman of the Company through December 31, 2015. Mr. DeFeo will continue as a consultant for Terex after December 31, 2015 through December 31, 2016.

John Garrison brought a different profile to the CEO role. Mr. Garrison joins Terex from Textron, Inc. where he served as President and CEO of their Bell Helicopter Segment. Prior to that, Mr. Garrison was President of Textron's Industrial Segment and E-Z-GO. He was also President and CEO at Azurix Corporation and held senior leadership positions at Case Corporation, and served as an officer in the United States Army.

He also served 10 years on active duty in the U.S. Army as an Airborne Ranger qualified Artillery Officer and taught in the Department of Social Sciences at the United States Military Academy at West Point.

Mr. Garrison is a 1982 graduate of the United States Military Academy at West Point and received a Master of Business Administration from the Harvard Business School.

Garrison's military background and experience running complex manufacturing operations at Bell Helicopter prepared him for the transformation ahead. "Focus, Simplify, Execute to Win" became the new strategic mantra—a stark contrast to the acquisition-driven growth of the DeFeo era.

Terex hosts "Investor Day" to introduce the new senior team to shareholders and analysts, and to present a five-year plan and three-part business program: Focus, Simplify, and Execute to Win.

The strategy represented a fundamental philosophical shift. Instead of growing through acquisitions and managing complexity, Terex would shrink to strength and optimize what remained.

Simon Meester Takes the Helm (2024)

After five years in the organization, I am honored, humbled and excited to be Terex's next CEO. Terex is in a very good place, and I look forward to a bright future," said Terex President and Chief Executive Officer Simon Meester. He added, "We are pleased by our strong 2023 performance, and believe Terex is well-positioned to continue to deliver value to its customers and shareholders, with strong demand for its products and favorable megatrends for the long term.

Prior to joining Terex, he was VP and General Manager of the Industrial Control Division at Eaton Corporation. Earlier, he spent 14 years in progressively senior roles at Caterpillar, Inc., before becoming President, Sandvik Mining and Construction in India. He has managed global teams and operations for more than 20 years, based in seven countries, including 11 years in the United States. He holds an MBA from the University of Surrey, England and a Bachelor of Science in automotive engineering, Apeldoom, Netherlands.

Meester joined Genie in 2018 from Eaton Corporation, where he was Vice President and General Manager of the Industrial Control Division. Previously, he held senior roles at Caterpillar and Sandvik.

Meester's path to the CEO role—through Genie, Terex's most successful business—signaled continuity with the operational excellence culture that had defined the company's best years.

The ESG Acquisition & REV Group Merger: The Next Chapter (2024–2025)

Environmental Solutions Group Acquisition

Terex Corporation today announced completion of its acquisition of Environmental Solutions Group ("ESG") from Dover Corporation. Terex anticipates that ESG will drive increased revenue growth, free cash flow, earnings before interest, taxes, depreciation, and amortization ("EBITDA") margin, and EPS accretion. The transaction is expected to be double-digit percentage adjusted EPS accretive in 2025, with meaningful growth thereafter. The all-cash transaction is for $2.0 billion, or $1.725 billion when adjusted for the present value of expected tax benefits of approximately $275 million.

ESG has demonstrated a track record of consistent, resilient growth, delivering a 7%+ long-term organic revenue compound annual growth rate ("CAGR") over the past 10 years. ESG holds the #1 position in North America in refuse collection vehicles, waste compaction equipment, and associated parts and digital solutions.

ESG's industry-leading product brands include Heil, Marathon, Curotto-Can, Bayne Thinline, and Parts Central as well as digital solutions offerings 3rd Eye and Soft-Pak.

The ESG acquisition represented a strategic bet on waste and recycling—industries characterized by more stable demand than traditional construction equipment. People generate garbage in recessions and expansions alike, and regulatory pressure continues to drive investment in waste management infrastructure.

With ESG, Terex will now derive 67% of its total revenue from North America, an increase from 61% based on trailing 12 months results ended Q2 2024.

ESG is a strong performer with 21% Adjusted EBITDA margin. ESG is a proven, resilient and recession-resistant business with significant aftermarket and recurring digital revenues (~50% of EBITDA). ESG brings Terex highly attractive end-market dynamics of increasing per capita waste generation and multi-year growth in RCV ("Refuse Collection Vehicle").

The 21% adjusted EBITDA margin significantly exceeded Terex's corporate average, promising meaningful margin accretion as ESG became a larger portion of the portfolio.

The REV Group Merger Announcement (October 2025)

The combined company is expected to have approximately $7.8 billion in net sales and an attractive combined Adjusted EBITDA margin of approximately 11% as of year-end 2025 excluding benefit of synergies. Creates a scaled specialty equipment manufacturer with complementary, leading brands in attractive, low cyclical, highly resilient and growing end markets.

The Merger will create a diversified leader in emergency, waste, utilities, environmental and materials processing equipment with attractive end markets characterized by low cyclicality, resilient demand and long-term growth profiles. With a substantial U.S. manufacturing footprint, the combined organization will be well-positioned to benefit from domestic demand growth.

Under the terms of the agreement, which has been unanimously approved by the Boards of Directors of both companies, REV Group shareholders will receive, for each REV Group share, 0.9809 of a share of the combined company and $8.71 in cash ($425 million in total). Upon closing, Terex shareholders will own approximately 58%, while REV Group shareholders will own approximately 42%, of the combined company's fully diluted shares on a pro forma basis. Following the close, the combined company will continue to be traded on the NYSE under the symbol TEX.

The companies expect $75 million run-rate synergies by 2028 (≈50% of which is expected within 12 months) and plan to close in H1 2026, subject to approvals.

Rev Group designs and manufactures specialty vehicles, including fire apparatus, emergency vehicles and commercial infrastructure vehicles. Segments and brands include: Aerials, pumpers, AARFs, rescue and wildland apparatus: E-One, Ferrara, KME, Spartan Emergency Response, Smeal, Spartan Fire Chassis, Ladder Tower. Emergency vehicles: Horton, AEV, Road Rescue, Wheeled Coach, Leader. Commercial infrastructure vehicles: Capacity Trucks, LayMor. Recreational vehicles: American Coach, Fleetwood RV, Holiday Rambler, Renegade RV, Midwest Automotive Designs.

Exiting the Aerial Business

Today, Terex also announced that it will initiate a process to exit its Aerials segment, including the assessment of a potential sale or spin-off. Upon closing of the Merger, Terex CEO, Simon Meester, will serve as President & Chief Executive Officer of the combined company.

Terex says it is assessing the sale or spin-off of its aerial business, which is sold under the Genie brand, to "reduce its exposure to cyclical end markets."

The planned exit from aerials—the Genie business that DeFeo acquired for $75 million in 2002—represents the most dramatic strategic pivot in Terex's modern history. The business that introduced the Toyota Production System to Terex, that represented the company's highest-profile brand, and that accounted for a substantial portion of revenues is now viewed as too cyclical for the company's strategic direction.

Excluding Aerials and including US$75 million of synergies, it is estimated that the combined company would have an even stronger pro forma adjusted EBITDA margin of approximately 14% for 2025.

The math tells the story: without Aerials, the combined company's margins improve substantially. The cyclicality that made aerial platforms volatile also compressed their average margins relative to waste equipment and emergency vehicles.

Business Model & Operating System Deep Dive

The Terex Business System (TBS)

Genie also introduces Terex to the Toyota Production System management philosophy, which Genie had incorporated into its business operations with success and led to creation of the Terex Business System, or TBS.

The Terex Business System emerged from the Genie acquisition but evolved into something uniquely suited to Terex's multi-business structure. TBS provides a common language and methodology across disparate operations—from crushing equipment in Northern Ireland to aerial platforms in Washington State to waste collection vehicles in the American South.

The system emphasizes continuous improvement (kaizen), waste elimination, visual management, and respect for people. These principles apply regardless of what specific equipment a facility produces, allowing Terex to integrate acquisitions rapidly and achieve operational synergies.

Current Business Segments

Per a Company SEC filing on May 2, 2025, effective in the first quarter of 2025 Terex reported its business in three reportable segments: (1) Materials Processing ("MP"), (2) Aerials, and (3) Environmental Solutions ("ES"): MP manufactures crushers, washing systems, screens, trommels, apron feeders, material handlers, pick and carry cranes, rough terrain cranes, tower cranes, wood processing, biomass and recycling equipment, concrete mixer trucks and pavers, and conveyors. Customers use these products in construction, infrastructure and recycling projects, quarrying and mining, landscaping and biomass production, material handling, maintenance, moving materials on rugged terrain, lifting construction material, and placing material at point of use.

Terex Materials Processing (MP) is a portfolio of brands that serve five key verticals—Aggregates, Environmental, Concrete, Handling, and Lifting. The Aggregates industry is the backbone of infrastructure development and needs efficient, reliable equipment.

ES manufactures waste, recycling, and utility equipment including refuse collection bodies, hydraulic cart lifters, automated carry cans, compaction, balers, recycling equipment, digger derricks, insulated aerial devices, self-propelled articulating insulated booms, cameras with integrated smart technology, and waste hauler software solutions. Customers use these products in the solid waste and recycling industry, and for construction and maintenance of transmission and distribution lines, tree trimming, and foundation drilling applications. ES brands include Heil, Marathon, Curotto-Can, Bayne Thinline, Parts Central, digital solutions 3rd Eye and Soft-Pak, and Terex Utilities.

Financial Performance

Full-year sales of $5.2 billion increased 17%.

Our full-year 2024 adjusted earnings per share of $6.11 is the second highest in Terex history reflecting the strength of our portfolio and ability to perform better throughout the cycle than in the past.

Overall, we expect 2025 net sales of $5.3 to $5.5 billion, earnings per share between $4.70 and $5.10 and free cash flow of $300 to $350 million.

Playbook: Business & Investing Lessons

The Roll-Up Playbook

Randolph Lenz's insight—that distressed industrial companies retain value even through bankruptcy—created the foundation for Terex. The key elements of his approach:

-

Focus on strong brands with weak balance sheets: The brand equity of Terex, Euclid, and other legacy names persisted even as corporate structures collapsed.

-

Buy at the right price: Paying $9 million for a company with $20 million in annual sales creates margin of safety.

-

Consolidate operations aggressively: Close redundant facilities, standardize processes, eliminate overhead.

-

Use leverage strategically but understand the risks: Debt magnifies returns but also magnifies risk during downturns.

The Portfolio Management Lesson

Terex's journey from dump trucks to waste management equipment illustrates the importance of strategic portfolio evolution. Businesses that made sense in one era—mining equipment, compact construction machinery—became strategic liabilities in another.

The key insight: knowing when to exit is as important as knowing what to acquire. The mining business sale to Bucyrus, the truck line sale to Volvo, the MHPS sale to Konecranes, and the planned aerial exit all represented disciplined recognition that some businesses no longer fit the portfolio.

Cyclicality Management

The strategic shift toward "low cyclicality, resilient demand and long-term growth profiles" reflects hard-won lessons from the 2008 financial crisis and subsequent cycles. Construction equipment demand swings wildly with economic conditions; waste collection demand does not.

The ESG acquisition and REV Group merger represent deliberate moves toward businesses where: - Demand is driven by essential services (garbage collection, emergency response) - Municipal and institutional customers provide stability - Regulatory requirements create ongoing replacement cycles - Aftermarket and service revenues smooth earnings

Operating System Transfer

The Toyota Production System principles that came with Genie became Terex's operational DNA. This demonstrates an often-overlooked aspect of M&A: acquiring operational capabilities, not just products or market positions.

TBS allowed Terex to integrate dozens of acquisitions while maintaining operational discipline. The system provided a common framework for improvement regardless of what specific equipment a facility produced.

CEO Succession

Three distinct leadership eras shaped Terex:

Lenz (1983-1995): Entrepreneurial dealmaker who built the platform through distressed acquisitions. His approach required high risk tolerance and financial engineering skills.

DeFeo (1995-2015): Professional manager who transformed a collection of acquisitions into an operating company. His acquisition machine expanded Terex dramatically while implementing systematic operational improvements.

Garrison/Meester (2015-Present): Strategic simplifiers who focused the portfolio on defensible, less cyclical positions. Their "Focus, Simplify, Execute to Win" approach represented a philosophical reversal from acquisition-driven growth.

Each leader was right for their era. The transition from one approach to another required recognizing when circumstances demanded different capabilities.

Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

Threat of New Entrants: MODERATE-LOW

Heavy equipment manufacturing requires substantial capital investment in facilities, tooling, and engineering capabilities. Dealer networks and customer relationships take decades to build—rental companies don't switch suppliers casually. Brand reputation matters significantly; Genie and Powerscreen are trusted names that command premium pricing.

However, global competitors from China—Zoomlion, XCMG, and others—represent emerging threats. Vendors include Caterpillar, Komatsu, Volvo Construction Equipment, Hitachi Construction Machinery, Liebherr, SANY, Xuzhou Construction Machinery Group (XCMG), JCB, Kobelco, Zoomlion Heavy Industry Science & Technology Co., Ltd. Chinese manufacturers have demonstrated willingness to accept lower margins for market share, and they continue improving product quality.

Bargaining Power of Suppliers: MODERATE

Steel, hydraulics, and specialty components represent significant cost inputs. Multiple suppliers exist, but supply chain disruptions during 2021-2022 demonstrated vulnerability. Our annual results demonstrate significant improvement over the prior year and highlight our ability to successfully manage cost inflation and supply chain challenges.

Bargaining Power of Buyers: MODERATE-HIGH

The equipment rental industry accounts for 90 percent of all Genie product domestic sales and 80 percent of sales outside of the United States.

This concentration creates significant buyer power. United Rentals, Sunbelt Rentals, and other major rental companies can negotiate aggressively because they represent such a large portion of demand. However, brand loyalty and equipment reliability create some stickiness—rental companies develop preferences based on uptime, parts availability, and technician familiarity.

Threat of Substitutes: LOW

There is no real substitute for aerial work platforms when work must be performed at height, or for crushing equipment when rock must be processed. Potential automation and robotics developments could change labor dynamics long-term, but current technology does not threaten core product categories.

Industry Rivalry: HIGH

In the Aerial Work Platforms segment, Terex's primary competitors include JLG Industries (owned by OSK), Skyjack (a division of LIMC), and Haulotte Group. JLG is the market leader in North America with approximately 40% market share, followed by Terex's Genie brand with roughly 30% share.

Multiple well-funded competitors—JLG (owned by Oshkosh), Caterpillar, Sandvik, Metso in materials processing—create intense competition. Cyclicality creates pricing pressure during downturns as manufacturers fight for limited volume.

Hamilton's 7 Powers Analysis

Scale Economies: MODERATE

Manufacturing scale helps with procurement and fixed cost absorption. Terex operates manufacturing facilities across multiple continents, providing some production flexibility and geographic reach. However, heavy equipment manufacturing is generally less scale-sensitive than many industries—niche products can be profitable at relatively modest volumes.

Network Effects: WEAK

Limited network effects exist in equipment manufacturing. Dealer network density provides some benefit for service and parts availability, but customers don't derive value from other customers using the same equipment.

Counter-Positioning: MODERATE

The strategic shift toward waste/recycling versus cyclical construction represents a form of counter-positioning. Legacy competitors focused on construction equipment may struggle to follow this pivot because their organizations, dealer networks, and customer relationships are optimized for different end markets. Caterpillar's core business is construction and mining; entering waste collection would require significant capability building.

Switching Costs: MODERATE

Parts availability and service networks create some lock-in. Fleet standardization by rental companies creates repeat purchasing patterns—once a rental company builds expertise around Genie equipment, switching to JLG creates training costs and parts inventory complications. Operator familiarity also creates preference; technicians and operators develop muscle memory around specific equipment.

Cornered Resource: WEAK

Terex does not possess unique resources that competitors cannot replicate. Brand names have value, but are not irreplaceable. Manufacturing capabilities are sophisticated but not unique.

Process Power: MODERATE

The Terex Business System represents genuine process power—organizational capabilities that competitors cannot easily replicate. The systematic approach to operational excellence, developed over decades, provides ongoing advantages in quality, cost, and delivery.

Branding: MODERATE

Genie and Powerscreen carry strong brand recognition in their respective markets. These brands command some pricing power and customer preference, but not to the degree of truly iconic consumer brands.

Key Performance Indicators for Ongoing Monitoring

For investors tracking Terex's ongoing performance, three KPIs deserve particular attention:

1. Segment Operating Margins

Operating margins by segment reveal the health of each business and the success of operational improvements. The ESG acquisition promised margin accretion; tracking whether Environmental Solutions maintains its 21%+ adjusted EBITDA margins after integration will indicate deal success. Materials Processing margins reflect competitive dynamics in aggregates and recycling equipment. If Aerials are retained, their margins indicate pricing power relative to JLG and other competitors.

2. Revenue Mix by End Market Cyclicality

As Terex pivots toward less cyclical businesses, monitoring the percentage of revenue derived from construction-exposed markets versus essential services (waste collection, emergency vehicles, utilities) reveals strategic progress. Higher percentages from low-cyclicality markets should reduce earnings volatility through economic cycles.

3. Free Cash Flow Conversion

Terex has guided to $300-350 million of free cash flow on approximately $5.4 billion in revenue (midpoint of 2025 guidance), implying approximately 6% free cash flow margins. Monitoring FCF conversion relative to net income indicates capital efficiency and working capital management—critical for a company using debt to fund acquisitions.

Bull and Bear Cases

Bull Case

The strategic transformation positions Terex for sustained success through economic cycles. The ESG acquisition brings a market-leading position in waste collection equipment—an industry with secular tailwinds from urbanization, environmental regulation, and infrastructure investment. The REV Group merger adds fire trucks and ambulances, categories where municipal purchasing provides demand stability.

If Terex successfully exits Aerials at an attractive valuation (either through sale or spin-off), the remaining company will feature significantly higher margins and lower cyclicality than historical Terex. The $75 million of expected synergies from the REV combination provides earnings upside. Management's track record of integration success—most recently demonstrated with ESG—suggests capability to realize these synergies.

The Terex Business System provides ongoing operational improvement opportunities across the enlarged portfolio. As TBS practices spread to REV Group operations, additional efficiency gains become possible.

Bear Case

The REV Group merger represents significant execution risk. Combining two large industrial companies creates integration challenges, especially with simultaneous Aerials disposition. Management attention will be divided across multiple major initiatives.

The aerial business disposition may prove difficult. The market for large industrial businesses is not always liquid, and strategic buyers may negotiate aggressively knowing Terex is committed to exiting. A spin-off would create a separate public company with associated costs and management distraction.

The waste collection business, while less cyclical than construction equipment, is not immune to economic conditions. Municipal budget pressures during recessions can delay fleet replacement decisions. Competition from other waste equipment manufacturers and potential new entrants could pressure margins.

Rising interest rates increase the cost of the debt used to fund the ESG acquisition. Higher leverage limits financial flexibility and increases risk during downturns.

Myth vs. Reality

MYTH: Terex is a construction equipment company.

REALITY: Following the ESG acquisition, REV Group merger, and planned Aerials exit, Terex will derive minimal revenue from traditional construction end markets. The company is becoming a specialty equipment manufacturer focused on waste, emergency response, utilities, and materials processing. The "king of the earth" name has become a historical artifact.

MYTH: The Genie brand was undervalued when Terex acquired it.

REALITY: The $75 million purchase price reflected distressed industry conditions following the 2000-2002 economic downturn. The aerial platform market was consolidating, and Genie needed capital and scale to compete effectively. Terex provided both, making the acquisition value-creating for both parties. The fact that Terex is now exiting Aerials doesn't mean the acquisition was wrong—the business generated substantial returns over two decades and taught Terex operational excellence principles that transformed the entire company.

MYTH: Serial acquirers destroy value.

REALITY: Academic studies often show that acquisitions destroy shareholder value on average. But Terex's history demonstrates that disciplined serial acquisition—buying at the right price, integrating effectively, and knowing when to divest—can create substantial value. The key is having a genuine operating system (TBS) that improves acquired businesses, rather than relying solely on financial engineering.

Conclusion: The Art of Industrial Transformation

Terex's nine-decade journey from dump truck pioneer to specialty equipment conglomerate offers lessons that transcend any single industry. The company demonstrates that corporate identity is not fixed—that businesses can transform themselves repeatedly in response to changing markets and competitive dynamics.

Randolph Lenz showed that distressed assets retain hidden value. Ron DeFeo showed that acquisitions can be transformational when integrated with operational discipline. John Garrison and Simon Meester are showing that knowing when to exit is as important as knowing what to acquire.

The planned exit from Aerials—the business that taught Terex the Toyota Production System—carries particular poignancy. The student has outgrown the teacher; the lessons remain embedded in organizational DNA even as the original business departs.

For investors, Terex represents an ongoing case study in industrial portfolio management. The company's value will depend on execution of the REV Group merger, successful disposition of the Aerials segment, and continued operational excellence in the remaining businesses. The strategic direction is clear; the execution risk is real.

The "king of the earth" has evolved far from its origins. Whether that evolution creates lasting value depends on whether management can complete the transformation they've begun—and whether the less cyclical businesses they're assembling deliver the stability they promise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube