Constellation Brands: From Bulk Wine to Beer Empire

I. Cold Open & The Big Picture

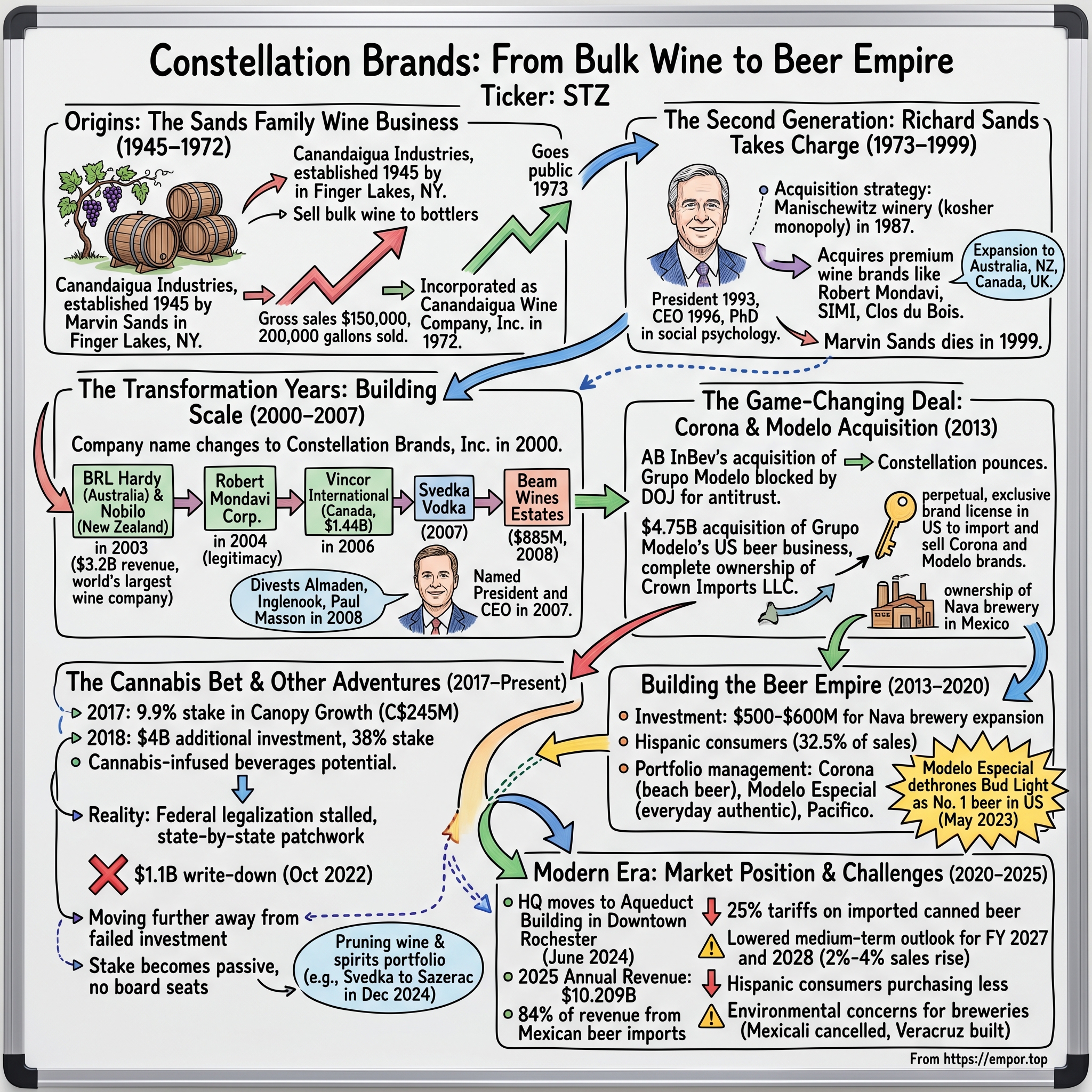

Picture this: A company that started bottling cheap wine in upstate New York now controls Corona and Modelo—the crown jewels of Mexican brewing that have conquered American beer coolers. Today, Constellation Brands stands as the largest beer import company in the United States by sales, commanding a 7.4% market share among all major beer suppliers. Let that sink in—an American company that never brewed a drop of beer until 2013 now ranks third in the entire U.S. beer market. The paradox is breathtaking: An American wine company that never brewed a drop of beer until a decade ago now owns the perpetual rights to import and sell Corona and Modelo in the United States—brands that together have dethroned Budweiser from its century-long reign. Constellation is the largest beer import company in the US, measured by sales, and has the third-largest market share (7.4 percent) of all major beer suppliers, while generating 84% of revenue from Mexican beer imports.

How did we get here? How did Marvin Sands' modest wine-bottling operation in the Finger Lakes transform into a $30 billion Fortune 500 behemoth that dominates American beer fridges? This is a story of three generations of family leadership, audacious M&A moves, and most critically, one transformative deal in 2013 that would redefine not just Constellation, but the entire American beer landscape.

The themes we'll explore today feel particularly relevant in our current era of portfolio transformation: the art of strategic pivoting, the mastery of acquisition integration, and perhaps most importantly, the ability to ride demographic waves that others either ignore or misunderstand. Because while craft breweries were busy chasing hop-obsessed millennials, Constellation was quietly building the infrastructure to serve America's fastest-growing consumer segment—and in doing so, created one of the great business transformations of the 21st century.

II. Origins: The Sands Family Wine Business (1945–1972)

The year was 1945. While returning GIs celebrated victory in Europe and the Pacific, Marvin Sands saw opportunity in America's forgotten wine country. The Finger Lakes region of upstate New York—once the heart of American winemaking before Prohibition decimated the industry—was ripe for revival. But Sands didn't start with grand ambitions of creating premium vintages. He saw a more prosaic opportunity: bulk wine.

The company was established in 1945 by Marvin Sands in the Finger Lakes region of New York as Canandaigua Industries, selling bulk wine to bottlers in the eastern United States. In its first year, the company sold approximately 200,000 gallons of wine and had gross sales of $150,000.

Think about that positioning for a moment. In post-war America, wine consumption was still largely confined to immigrant communities and special occasions. The American palate hadn't yet developed a taste for table wine—that wouldn't come until the 1970s. But Sands recognized that East Coast bottlers needed a reliable supplier of bulk wine they could label and distribute under their own brands. He wasn't selling a product; he was selling a service.

The Finger Lakes provided natural advantages: the glacial soil and microclimate could produce decent wine grapes, land was cheap, and critically, it was close to the population centers of the Northeast. While California was beginning its ascent to wine dominance, shipping costs from the West Coast made Finger Lakes wine competitive for Eastern bottlers.

For nearly three decades, Canandaigua Industries operated in this unglamorous but profitable niche. Sands built relationships with bottlers from Boston to Baltimore, becoming their trusted supplier of bulk wine. The business grew steadily if unspectacularly, reinvesting profits back into production capacity and slowly expanding its customer base.

The transformation from private company to public entity came at an inflection point. The company was incorporated as Canandaigua Wine Company, Inc. in 1972 and went public in 1973. The timing wasn't coincidental—America was on the cusp of a wine revolution. Table wine consumption was beginning to spike, driven by changing demographics, increased foreign travel, and a growing middle class interested in European sophistication.

Going public in 1973 gave Canandaigua access to capital markets just as the wine industry was about to explode. It also formalized what had been a family operation into a professional corporation, setting the stage for the ambitious expansion that would define its next chapter. The foundation was set: relationships with distributors, production expertise, and now, access to capital. All that was needed was the next generation's vision.

III. The Second Generation: Richard Sands Takes Charge (1973–1999)

If Marvin Sands was the founder who built the foundation, Richard Sands was the architect who transformed a regional wine bottler into a national beverage company. Marvin's son Richard Sands became president in 1993 and CEO in 1996. The transition wasn't abrupt—Richard had been groomed for leadership since joining the company in 1979, starting in the winemaking lab before moving through production, finance, sales, and marketing roles.

What Richard brought was a PhD in social psychology—an unusual qualification for a beverage executive but one that would prove invaluable in understanding consumer behavior and brand positioning. He served as Chief Executive Officer from October 1993 to July 2007, as President from May 1986 to December 2002, as Chief Operating Officer from May 1986 to October 1993—a progression that gave him deep operational experience across every aspect of the business.

The late 1980s marked the beginning of Richard's acquisition strategy. In 1987, the company purchased the Manischewitz winery in Canandaigua, New York—a move that might seem odd for a company trying to go upmarket, but it was brilliant portfolio management. Manischewitz gave Constellation a monopoly on kosher wine in America, a small but highly profitable niche with loyal customers and limited competition.

Under Richard's leadership through the 1990s, Constellation executed what would become its signature playbook: buy undervalued or underperforming wine brands, integrate them into its distribution network, reduce costs through scale, and invest in marketing. The company wasn't trying to compete with premium California wineries on quality—it was building a portfolio approach to wine, offering something for every price point and occasion.

The transformation from bulk to branded wine required a fundamental shift in capabilities. Instead of just producing and shipping wine, Constellation had to master brand management, consumer marketing, and retail relationships. Richard invested heavily in these areas, hiring talent from consumer packaged goods companies and building a sophisticated sales organization.

By the late 1990s, Constellation had become one of the largest wine companies in America through a combination of organic growth and strategic acquisitions. But Richard saw that domestic growth alone wouldn't be enough. The wine market was globalizing, and Constellation needed international presence to compete. During the 1990s and 2000s, under his direction Constellation acquired numerous wine companies that included legendary brands such as Robert Mondavi, SIMI, Clos du Bois and Franciscan Estates. Over the course of this expansion, the company purchased wineries in Australia, New Zealand, Canada and the United Kingdom.

The final years of the decade brought both triumph and transition. In 1999, Marvin Sands died following a brief illness. Richard, now chairman and CEO, had to lead the company through the loss of its founder while preparing for its most ambitious expansion yet. The stage was set for Constellation's transformation from a successful regional player to a global beverage powerhouse.

IV. The Transformation Years: Building Scale (2000–2007)

The millennium arrived with an exclamation point. In 2000, the company changed its name to Constellation Brands, Inc. to reflect the scope of the company and its range of brands. The rebranding wasn't just cosmetic—it signaled a fundamental shift in ambition. No longer content to be Canandaigua Wine Company, a regional player with national distribution, Constellation was announcing its intention to become a global beverage powerhouse.

Richard Sands orchestrated what can only be described as one of the most aggressive acquisition campaigns in beverage industry history. The numbers are staggering: BRL Hardy (Australia) and Nobilo (New Zealand) in 2003; Robert Mondavi Corp. for $1 billion in 2004; Vincor International, Canada's largest wine company, for $1.44 billion in 2006; Spirits Marque One (owner of Svedka Vodka) in 2007; and Beam Wines Estates, the wine operations of Fortune Brands (which included several major brands such as Clos du Bois) for $885 million in 2008.

Let's pause on the BRL Hardy deal for a moment. The transaction will accelerate Constellation's overall growth, increase its overall sales to $3.2 billion annually and, in combination with Constellation's existing wine businesses, make it the world's largest wine company at $1.7 billion in wine sales. This wasn't just buying market share—it was buying global infrastructure, distribution networks, and most importantly, Australian wine expertise at the exact moment when Australian wines were exploding in popularity worldwide.

But the crown jewel was Robert Mondavi. The $1 billion acquisition in 2004 wasn't just about buying wine brands—it was about acquiring legitimacy. Mondavi was American wine royalty, the company that had put Napa Valley on the global map. For Constellation, a company still shaking off its bulk wine roots, owning Mondavi meant instant credibility with retailers, distributors, and consumers.

"Today opens a new chapter for Constellation and the Robert Mondavi brand," stated Constellation Brands Chairman and Chief Executive Officer Richard Sands. "With the successful completion of this landmark transaction, Constellation offers an unmatched wine portfolio with expanded fine wine offerings, in addition to our broad portfolio of leading brands in the spirits and imported beer categories and unparalleled global distribution capabilities. This is a winning combination that preserves and enhances the heritage of both companies and will produce outstanding wines for generations to come".

The integration strategy was sophisticated. Rather than simply folding acquisitions into the existing structure, Constellation created distinct divisions—fine wine, popular premium, value wine—each with its own management and go-to-market strategy. This allowed them to maintain brand integrity while capturing synergies in production, distribution, and back-office functions.

In 2007, Rob Sands was named president and CEO, taking over from his brother Richard who remained chairman. The transition was seamless—Rob had been with the company since 1986, starting as general counsel before moving through operational roles. This wasn't a sudden handoff but a carefully orchestrated succession that had been years in the making.

By 2007's end, Constellation had transformed from a regional wine company into a global beverage conglomerate with operations spanning wine, spirits, and through a joint venture with Grupo Modelo, imported beer. But the company was also carrying significant debt from its acquisition spree, and the global financial crisis was about to test whether this rapid expansion had been brilliant or reckless.

The answer would come from an unexpected source: Mexican beer. The company later moved to a more premium wine portfolio, divesting Almaden Vineyards, Inglenook Winery, and the Paul Masson winery in Madera, California, in 2008—a strategic pruning that would free up capital for what would become the defining acquisition of Constellation's history.

V. The Game-Changing Deal: Corona & Modelo Acquisition (2013)

Sometimes in business, the best deals come from someone else's regulatory problems. In 2012, Anheuser-Busch InBev announced its intention to acquire Grupo Modelo for $20.1 billion—a deal that would have combined the world's two largest brewers and given AB InBev control of Corona and Modelo globally. The U.S. Department of Justice had other ideas.

The antitrust implications were obvious: AB InBev already controlled nearly half the U.S. beer market. Adding Corona and Modelo would have created an unstoppable monopoly. The DOJ filed suit to block the merger, arguing it would substantially lessen competition and lead to higher beer prices for American consumers.

Enter Constellation Brands, stage left.

Rob Sands and his team had been watching the situation closely. Constellation's connection to these brands started with importing them to the U.S. from Mexico. The company officially acquired the U.S. beer business of Groupo Modelo, which included Modelo and Corona, from Anheuser-Busch in 2013. They had been the U.S. importer for Corona through a joint venture since 2007, giving them intimate knowledge of the brands' potential.

When it became clear that AB InBev would need to divest the U.S. business to get regulatory approval, Constellation pounced. The negotiation was complex—this wasn't just buying brands or distribution rights. Constellation Brands completed its $4.75 billion acquisition of Grupo Modelo's US beer business from Anheuser-Busch InBev. Constellation's full ownership of Crown Imports LLC will give it complete control of a state-of-the-art brewery in Nava, Mexico, freedom to develop brand extensions for the U.S. market and exclusive brand license in the U.S. to import, market and sell Corona and other Modelo Brands.

Think about what Constellation actually acquired: The transaction included full ownership of Crown Imports LLC, which provided Constellation with complete, independent control of all aspects of the US commercial business; a brewery in Mexico; an exclusive perpetual brand license in the US to import, market and sell Corona and the Modelo brands and the freedom to develop brand extensions and innovations for the US market.

The word "perpetual" is doing a lot of work in that sentence. Constellation didn't just buy a temporary license or a distribution agreement that could be revoked. They bought the rights to Corona and Modelo in the United States forever. As long as Americans drink beer, Constellation will be the one selling them Corona and Modelo.

Wall Street's initial reaction was skeptical. Constellation was paying nearly $5 billion—more than half its market cap at the time—for brands it didn't fully own in a category where it had no manufacturing experience. The company's stock initially dropped on the announcement. Analysts worried about integration risk, the debt load, and whether a wine company could successfully run a beer business.

"The revised agreement with AB InBev will make Constellation's Crown beer division a fully independent competitor and the third largest producer and marketer in the U.S. beer industry. This is a transformational acquisition for our company as we will hold perpetual rights to Corona and the Modelo brands distributed by Crown in the U.S. We will have autonomous control of production, distribution, marketing and promotion of these brands in the U.S.", said Rob Sands.

The skeptics missed several critical factors. First, Corona and Modelo weren't typical American beers competing on price. They were premium imports with pricing power and brand loyalty. Second, the Hispanic population in the U.S. was growing rapidly and these brands had authentic cultural resonance. Third, Constellation wasn't starting from scratch—they had been importing these brands for years and knew the market intimately.

"Today begins a new chapter in Constellation's history," said Rob Sands, president and CEO, Constellation Brands. "We are now the proud owners of six of the top 20 imported beer brands in the US and a coveted portfolio of premium brands in the growing US imported beer category."

But perhaps most importantly, Constellation now controlled its own destiny. Unlike typical licensing deals where the brand owner can change terms, raise prices, or revoke rights, Constellation's perpetual license meant they could invest in these brands with confidence. They could build breweries, develop new products, and execute long-term strategies without fear of losing the brands.

The deal closed in June 2013. Constellation was no longer just a wine and spirits company—it was now the third-largest beer company in America. The transformation was complete, but the real work was just beginning.

VI. Building the Beer Empire (2013–2020)

The morning after closing the Modelo acquisition, Rob Sands walked into Constellation's headquarters with a simple message: "We're a beer company now." The skeptics who questioned whether a wine company could successfully run a beer business were about to get their answer.

Integration began immediately, but Constellation took a counterintuitive approach. Rather than imposing their wine playbook on the beer business, they left Bill Hackett and his Crown Imports team largely autonomous. These were the people who had been successfully importing and marketing Corona and Modelo for years—why mess with what worked?

What Constellation did bring was capital and conviction. Constellation plans to invest $500-$600 million during the next three years to expand the facility to double its current capacity to meet projected demand for products in the U.S. This wasn't cautious incrementalism; it was a massive bet that Mexican beer consumption would continue growing.

The manufacturing expansion was critical. Unlike wine, which can be stored and aged, beer requires continuous production and fresh inventory. Constellation needed to ensure they could meet demand without stockouts or quality issues. They established a brewery operations group to manage the expansion and integration of the Nava brewery, treating it as a strategic asset rather than just a production facility.

But the real genius was in the marketing approach. Hispanic- and Latino-identifying customers accounted for 32.5% of Constellation Brands' sales in 2023, according to data from consumer research firm Numerator and investment bank Jefferies. This is despite the group comprising just 19.5% of the American population that year. Constellation understood something fundamental: authentic connection beats pandering every time.

Rather than treating the Hispanic market as a monolith, Constellation recognized the diversity within it—Mexican-Americans, recent immigrants, second and third-generation families, urban and rural communities. Their marketing wasn't about slapping Spanish words on billboards; it was about understanding cultural moments, family traditions, and community values.

The results spoke for themselves. Modelo Especial's U.S. owner and distributor wants to emphasize that the brand's rise to the top of the country's beer market didn't happen overnight. "The fact that we became the No. 1 beer in America due to a competitor's moves is not accurate," said Jim Sabia, executive vice president and managing director of Constellation Brands' beer division. "We've planned on becoming the No. 1 beer in America over the next couple of years; it just happened quicker than we anticipated," he said. Sabia said the company estimated that Modelo Especial would be the No. 1 beer in the U.S. by 2025.

The portfolio management was equally sophisticated. Corona remained the beach beer, the vacation beer, the beer with a lime. Modelo Especial was positioned differently—as the authentic Mexican beer for everyday occasions. Pacifico targeted a younger, more adventurous demographic. Each brand had its lane, minimizing cannibalization while maximizing total market share.

By 2018, the transformation was undeniable. In 2018, Modelo scored a significant coup when it ousted Bud Light as the official sponsor of the UFC mixed martial arts league. By then, Modelo ranked as the fastest-growing beer in the U.S. and was second only to Corona among import beer sales. This wasn't just about sports sponsorships; it was about understanding where culture was heading.

The 2020 pandemic could have derailed everything. On-premise consumption—bars, restaurants, stadiums—collapsed overnight. But Constellation's brands proved remarkably resilient. Hispanic consumers, many of whom were essential workers, continued purchasing. The authentic positioning meant these weren't just beers; they were cultural touchstones that people weren't willing to give up even in tough times.

Meanwhile, Constellation quietly continued pruning its wine and spirits portfolio, selling off underperforming brands to focus resources on beer. They sold 30 low-cost wine labels in January 2021 to E. & J. Gallo for $810 million including Clos du Bois. Every divestiture freed up capital and management attention for the beer business.

Then came the moment that shocked the industry: Modelo Especial took over's Bud Light's top spot in the U.S. beer market in May and has held onto the title ever since, according to Nielsen IQ data analyzed by the investment firm Wedbush Securities. The data shows that on the four weeks ended on May 20, Modelo's share of total beer sales grew to 10.7%, while Bud Light's fell to 9.6%.

In 2023 Modelo scored a major coup, becoming the most popular beer in the U.S., beating out Bud Light. While Bud Light's collaboration with a transgender influencer accelerated its decline, industry insiders knew the truth: "Modelo would have overtaken Bud Light, just given the growth trajectory that they had," says Gerald Pascarelli, managing director of equity research at Needham and Company.

VII. The Cannabis Bet & Other Adventures (2017–Present)

In October 2017, the beer industry collectively gasped. Constellation agreed to pay about C$245 million ($191 million) for a 9.9% stake in Canopy Growth Corporation, a Canadian seller of medicinal-marijuana products. At the time of the agreement, Constellation became the first Fortune 500 company and the first major alcoholic beverage maker to take a minority stake in a marijuana business.

The initial investment was cautious, exploratory—a toe in the water to understand an emerging market. But within a year, Constellation dove headfirst into the deep end. In August 2018, the company announced that it would invest an additional US$4 billion in Canopy Growth Corporation, bringing its stake to approximately 38% with warrants that could push ownership above 50%.

"Through this investment, we are selecting Canopy Growth as our exclusive global cannabis partner," said Rob Sands, Chief Executive Officer, Constellation Brands. The rationale was compelling: cannabis beverages could be the next frontier in social drinking, potentially disrupting the very beer and spirits markets Constellation dominated.

The vision was intoxicating. Cannabis-infused beverages that provided a controlled, predictable experience without alcohol's calories or hangovers. A new category that could capture younger consumers who were increasingly turning away from traditional alcohol. First-mover advantage in what analysts projected could become a $200 billion global market.

"Over the past year, we've come to better understand the cannabis market, the tremendous growth opportunity it presents, and Canopy's market-leading capabilities in this space," Constellation Brands CEO Rob Sands said in a statement. The company paid a 38% premium to market price, signaling its conviction that this wasn't speculation—it was strategic positioning.

But reality proved harsher than the vision. Federal legalization in the United States, which Constellation had bet would happen within a few years, remained elusive. State-by-state legalization created a patchwork of regulations that made national distribution impossible. Both companies have no plans to sell cannabis products in any market unless it is permissible to do so at all applicable government levels.

The financial impact was brutal. Constellation Brands recorded a $1.1 billion writedown in the value of its investment in Canopy Growth, a cannabis producer it has a nearly 40% stake in, the company said in its second-quarter earnings call on Thursday. President and CEO Bill Newlands said while the result is "clearly disappointing," Constellation remains upbeat that changes to Canopy's business in Canada and the U.S. are positioning it for success.

By 2022, the cannabis investment had become an albatross. Despite betting $4 billion on cannabis' growth potential, stalled federal legislation has prevented growth in the category that Constellation and other companies were hoping for, leaving the future of their investments in question. Canopy Growth continued to burn cash, its stock price collapsed, and Constellation faced pressure from investors to cut its losses.

In March 2019, Bill Newlands became CEO, inheriting the cannabis challenge from Rob Sands. Newlands took a pragmatic approach: maintain the investment but stop throwing good money after bad. In 2018, Constellation invested $4 billion in Canopy and boosted its stake to 39% two years later on the premise that there was long-term promise in cannabis beverages in the U.S. But the market never materialized as expected, leading to a $1.1 billion write-down in its investment in October 2022.

The distancing began in earnest. Constellation Brands is moving further away from its failed multi-billion dollar investment in cannabis producer Canopy Growth, the beer giant announced last week. Canopy Growth's three directors who were nominated by Constellation said they will step down from the Canadian company's board. The Modelo maker also will convert its stake in Canopy to a new category of shares that do not give voting power or the ability to collect payments from the company. Constellation will no longer have representation on Canopy's board.

Meanwhile, Constellation continued smaller, more measured bets in adjacent categories. The company acquired craft distilleries, explored hard seltzers, and invested in premium spirits brands. These were extensions of its core competency—branded alcoholic beverages sold through its existing distribution network.

The cannabis adventure wasn't a complete failure—it demonstrated Constellation's willingness to take bold risks and explore new categories. But it also served as a cautionary tale about the difference between vision and execution, between market potential and regulatory reality.

Today, Constellation maintains its Canopy stake, now passive and non-voting, waiting for federal legalization that may or may not come. The $4 billion bet has been largely written off, a expensive lesson in the perils of being too early to a market that hasn't yet materialized. For a company that built its fortune on perfectly timed acquisitions, the cannabis investment stands as a rare miscalculation—proof that even the best acquirers can misread the future.

VIII. Modern Era: Market Position & Challenges (2020–2025)

On June 24, 2024, Constellation Brands re-located its headquarters to a 170,000 square foot campus on the site of the historic Aqueduct Building in Downtown Rochester, the first Fortune 500 company to operate in the city in two decades. The homecoming was symbolic—a company that had conquered global markets returning to its roots with the confidence of a champion.

By the numbers, Constellation's transformation was complete. Constellation Brands Inc annual revenue for 2025 was $10.209B, a 2.48% increase from 2024. Constellation Brands Inc annual revenue for 2024 was $9.962B, a 5.39% increase from 2023. The company that started selling 200,000 gallons of bulk wine for $150,000 in 1945 now generated over $10 billion annually, with beer accounting for roughly 80% of revenue.

The portfolio had been ruthlessly optimized. Wine and spirits, once the core of the business, had been pruned to focus only on premium brands. The company on Wednesday also announced that it plans to reposition its portfolio by divesting "mainstream" wines and focusing on brands that price their bottles at or above $15. In December, Constellation sold Svedka vodka to Sazerac, continuing the strategic shift away from underperforming assets.

But storm clouds were gathering. The modern era brought challenges that even Constellation's masterful execution couldn't entirely overcome. Constellation Brands gave a weaker-than-expected forecast for the fiscal year, anticipating that higher U.S. tariffs will hurt its business. The Trump administration has imposed a 25% tariff on all imported canned beer.

The tariff challenge exposed Constellation's greatest vulnerability: its complete dependence on Mexican production. Constellation imports all of its beer from Mexico. Its beer portfolio, which includes Modelo, Corona and Pacifico, accounted for 78% of the company's net sales during the quarter. What had been a strategic advantage—low-cost production with authentic Mexican heritage—suddenly became a potential liability.

The impact was immediate and severe. For fiscal 2026, Constellation anticipates comparable earnings per share in a range of $12.60 to $12.90, well below Wall Street's estimates of $13.97 per share. The company is projecting that organic net sales will range from declining 2% to rising 1%. Beer sales, which account for the bulk of its business, will range from flat to up 3%, according to the company's fiscal 2026 outlook.

Even more concerning was the medium-term outlook. Constellation also lowered its medium-term outlook for fiscal 2027 and 2028. It now projects that enterprise sales will rise between 2% and 4%, down from its prior estimate of growth between 6% and 8%. For a company that had delivered consistent high-single-digit growth for over a decade, this was a shocking reversal.

Beyond tariffs, demographic headwinds emerged. Last quarter, Newlands said Hispanic consumers were buying less of the company's beer because of fears over Trump's immigration policy. Roughly half of Constellation's beer sales come from Hispanic consumers, according to the company. The very demographic wave that had lifted Constellation to dominance was now creating vulnerability.

Competition intensified from unexpected quarters. Craft beer's decline meant those consumers weren't necessarily switching to imports. Gen Z drinking habits differed dramatically from millennials—they drank less alcohol overall and when they did, showed less brand loyalty. Cannabis legalization in multiple states provided an alternative to alcohol that particularly resonated with younger consumers.

Supply chain complexities multiplied. Constellation had invested billions in Mexican brewing capacity, but environmental concerns had forced them to abandon a partially built brewery in Mexicali. Water rights, local opposition, and climate change made expansion increasingly difficult. The company pivoted to building in Veracruz, but the delays and added costs highlighted the challenges of international manufacturing.

The market's reaction was brutal. Shares of Constellation Brands have tumbled 28% in the past 12 months. Wall Street, which had celebrated Constellation's strategic brilliance for years, suddenly questioned whether the company's growth story was over.

Yet management remained defiant. Bill Newlands, navigating his most challenging period as CEO, argued that the headwinds were temporary. The Hispanic population would continue growing. Modelo and Corona's brand strength remained intact. The company's distribution advantages and retailer relationships provided a moat competitors couldn't easily cross.

The modern era of Constellation Brands is still being written. It's a story of a company at the peak of its powers facing its greatest challenges—tariffs that threaten its cost structure, demographic shifts that complicate its market position, and competition from categories that didn't exist when the company's strategy was formed. Whether this is a temporary setback or the beginning of a secular decline remains to be seen.

IX. Playbook: Business & Investing Lessons

The Constellation Brands story offers a masterclass in strategic transformation, but not in the way most business school cases present it. This isn't a tale of visionary leadership seeing around corners—it's about patient capital allocation, decisive action when opportunities arise, and the discipline to prune relentlessly.

The Art of Strategic M&A: Knowing When to Strike

Constellation's acquisition strategy reveals a crucial insight: timing matters more than vision. The company didn't pioneer any categories—they weren't first in wine, spirits, or beer. Instead, they excelled at recognizing when industries reached inflection points and assets became available at attractive prices.

The Corona/Modelo acquisition exemplifies this perfectly. Constellation didn't create the opportunity—AB InBev's regulatory troubles did. But when the moment arrived, they were prepared with capital, conviction, and existing relationships. They paid $4.75 billion when skeptics called it expensive, but the perpetual rights to these brands in the U.S. market proved priceless.

Compare this to their cannabis investment—a rare case of Constellation trying to be first rather than fast-following. The $4 billion Canopy Growth investment has largely been written off, proving that even the best acquirers struggle when they stray from their core competency of buying proven assets at inflection points.

Portfolio Management: Build, Buy, Prune, Repeat

Constellation's portfolio evolution demonstrates a discipline most companies lack. They've consistently shown willingness to sell successful businesses when better opportunities emerged. Selling Hardy's after building it up, divesting mainstream wines to focus on premium, letting go of spirits brands to concentrate on beer—each decision freed capital for higher-return investments.

This wasn't sentiment-free financial engineering. Many divested brands had deep history with the company. But Constellation understood that in consumer goods, yesterday's growth engine becomes tomorrow's anchor. The discipline to sell winners before they become losers separates great capital allocators from merely good operators.

Riding Demographic Waves: The Hispanic Market Opportunity

Constellation's success with Hispanic consumers wasn't about Spanish-language advertising or Cinco de Mayo promotions. They understood that authentic brands with genuine cultural resonance couldn't be manufactured—they had to be acquired and carefully stewarded.

The lesson extends beyond Hispanic marketing. Constellation recognized that demographic shifts create durable competitive advantages for those positioned correctly. While competitors fought over share in declining segments, Constellation aligned with growing populations. This wasn't lucky—it was strategic positioning based on observable, long-term trends.

Brand Authenticity vs. Marketing

In an era of manufactured authenticity, Constellation's approach to Corona and Modelo stands out. They didn't try to make these brands more American or create line extensions that diluted their Mexican heritage. The authenticity was the value proposition.

This restraint is harder than it looks. The temptation to "premiumize" Corona or create Modelo sub-brands must have been enormous. But Constellation understood that brand authenticity, once lost, can never be recovered. Their light touch with these acquisitions—maintaining separate management, preserving Mexican production, respecting brand positioning—created more value than any marketing campaign could.

Capital Allocation Across Categories

Constellation's capital allocation reveals sophisticated thinking about return profiles across categories. Wine required constant innovation and SKU proliferation for declining returns. Spirits faced brutal competition from global giants with deeper pockets. But beer—specifically imported Mexican beer—offered sustainable competitive advantages.

The company's willingness to concentrate capital in its highest-return business, even if it meant becoming less diversified, shows rare discipline. Most companies add complexity over time; Constellation subtracted it, focusing resources where they had genuine competitive advantages.

Family Business Succession Done Right

Three generations of Sands family leadership without destroying the company is remarkable. The transitions from Marvin to Richard to Rob weren't just nepotistic handoffs—each generation brought different skills aligned with the company's evolution.

Marvin built the foundation through relationships and operational excellence. Richard transformed a regional player into a national force through acquisitions. Rob executed the beer transformation that defined the modern company. The family maintained control while bringing in professional management, balancing continuity with fresh perspective.

The Importance of Perpetual Licenses and Exclusive Rights

The Corona/Modelo deal structure deserves special attention. Constellation didn't just buy distribution rights or a temporary license—they secured perpetual, exclusive rights to these brands in the U.S. market. This transformed what could have been a vulnerable licensing arrangement into an unassailable competitive position.

The lesson: in any deal, the terms matter as much as the price. Constellation paid up for permanence, understanding that control over their own destiny was worth any premium. This contrasts sharply with companies that accept vulnerable positions for lower prices, only to lose everything when agreements expire.

Managing Complexity: From Wine to Beer to Cannabis

Constellation's journey shows both the benefits and perils of complexity. Their wine consolidation created scale advantages and distribution leverage that enabled the beer acquisition. But their cannabis adventure proved that not all adjacencies are created equal.

The key insight: complexity is justified when it creates synergies or options value, but destroyed value when it diverts focus or requires capabilities the company lacks. Constellation succeeded when leveraging existing strengths into adjacent areas, but struggled when venturing into truly new territories.

The Perpetual Transformation Machine

Perhaps the most important lesson is that transformation is never complete. The company that sold bulk wine in 1945 became a branded wine company, then a global beverage company, then a beer-focused importer. Each transformation required letting go of the previous identity.

Today's challenges—tariffs, changing demographics, new competition—will require another transformation. Constellation's history suggests they'll prune aggressively, acquire strategically, and emerge positioned for whatever comes next. The specifics are unknowable, but the pattern is clear: continuous evolution through disciplined capital allocation.

For investors, the Constellation playbook offers clear lessons: Look for companies with proven acquisition integration capabilities, not just acquisition appetite. Value discipline in portfolio pruning as much as growth in expansion. Recognize that demographic tailwinds create more sustainable advantages than operational improvements. And understand that in consumer goods, authenticity and distribution often matter more than innovation or marketing.

The Constellation story isn't about predicting the future—it's about positioning to capitalize when the future arrives.

X. Power & Business Quality Analysis

Scale Economies in Distribution

Constellation's distribution network represents their most durable competitive advantage. The U.S. three-tier system—producer, distributor, retailer—creates massive scale advantages for companies that can amortize costs across volume. Every additional case of Modelo shipped reduces the per-unit cost of Constellation's sales force, marketing spend, and distributor relationships.

This isn't just about cost reduction. Scale in distribution means better shelf placement, more promotional opportunities, and stronger negotiating power with retailers. When Walmart allocates beer shelf space, they prefer dealing with fewer, larger suppliers. Constellation's scale makes them indispensable to retailers while smaller competitors struggle for attention.

The network effects compound: successful brands generate cash for marketing, which drives volume, which increases distribution leverage, which improves shelf placement, which drives more volume. It's a virtuous cycle that's nearly impossible for new entrants to replicate.

Brand Power and Consumer Loyalty

Corona and Modelo possess something rarer than market share: cultural significance. These aren't just beers; they're identity markers. Modelo's "Fighting Spirit" campaign doesn't sell refreshment—it sells aspiration and authenticity to Hispanic consumers who see their values reflected.

Brand power in beer is peculiar. Unlike technology products where switching costs are real, beer switching costs are psychological. Yet they're surprisingly durable. Beer drinkers develop habitual purchase patterns, buying the same brand for decades. Constellation's brands have achieved the holy grail: they're both habitual purchases for core consumers and discovery brands for new drinkers.

The pricing power evidence is compelling. Despite inflation, supply chain challenges, and competitive pressure, Constellation has consistently raised prices faster than costs. Consumers pay premiums for Corona and Modelo relative to domestic beers, accepting that Mexican imports deserve higher prices—a remarkable achievement for what is essentially commodity brewing.

Switching Costs in the Three-Tier System

The three-tier distribution system, a relic of Prohibition-era regulation, creates unexpected moats. Distributors invest heavily in relationships, logistics, and local market knowledge for specific brands. Switching suppliers means retraining sales forces, adjusting warehouse operations, and risking retailer relationships.

For Constellation, this means their distributor network represents embedded infrastructure that competitors can't easily replicate or steal. A craft brewery might make better beer, but without distribution, it can't reach consumers. Even AB InBev, with all its resources, couldn't simply redirect Modelo distribution when they lost the brands—Constellation's control of the distribution network was part of the asset value.

Network Effects with Distributors

Beyond switching costs, Constellation benefits from true network effects in distribution. The more successful brands they have, the more valuable they become to distributors. A distributor carrying Corona, Modelo, and Pacifico can justify dedicated sales specialists, customized promotions, and deeper retailer relationships than one carrying a single brand.

This creates a feedback loop: Constellation's portfolio breadth attracts the best distributors, who provide superior execution, which drives sales success, which allows Constellation to acquire more brands, which makes them even more valuable to distributors. New entrants face a chicken-and-egg problem: they need distribution to succeed but need success to attract distribution.

Counter-Positioning vs. Craft Beer

Constellation's Mexican imports occupy a unique position—neither craft nor macro, neither premium nor value. This positioning, initially seen as vulnerable, proved brilliant. When craft beer boomed, Mexican imports weren't the enemy like Budweiser. When craft declined, Mexican imports weren't caught in the downdraft.

The counter-positioning extends beyond product. Constellation doesn't own breweries in America, avoiding the labor and regulatory challenges domestic producers face. They don't compete on freshness or local sourcing. Instead, they own authenticity and import mystique—attributes craft brewers can't claim and macro brewers can't manufacture.

Process Power in Mexican Brewing Operations

Constellation's Mexican manufacturing creates advantages beyond labor cost. The company has developed specialized knowledge in cross-border logistics, Mexican regulatory compliance, and supply chain management that would take competitors years to replicate.

The Nava brewery isn't just about capacity—it's about embedded learning. Constellation knows how to navigate Mexican water rights, manage cross-border glass supply chains, and maintain quality while shipping beer thousands of miles. This operational knowledge, accumulated over decades, represents process power that financial capital alone can't buy.

Bear Case: Tariffs, Competition, Changing Consumer Preferences

The bear case for Constellation is compelling. Tariffs could destroy their cost advantage overnight—a 25% import duty can't simply be passed to consumers without demand destruction. The geographic concentration of production in Mexico creates vulnerability to any U.S.-Mexico trade disputes.

Competition intensifies from every angle. Hard seltzers and canned cocktails attract younger drinkers. Cannabis legalization provides alternatives to alcohol. Non-alcoholic beers improve in quality. Each trend nibbles at beer's share of throat, and Constellation has limited ability to respond given their Mexican production constraints.

Most concerning are changing consumer preferences. Gen Z drinks less than Millennials, who drink less than Gen X. The trend is clear and probably irreversible. Mexican beer might be gaining share of a shrinking pie. Hispanic population growth is slowing, and second-generation Hispanic Americans show less loyalty to Mexican brands than their parents.

Bull Case: Demographics, Premiumization, Market Share Gains

Yet the bull case remains powerful. Hispanic population growth might be slowing, but it's still growing—and still younger and more urban than the general population. These demographic tailwinds will persist for decades, providing a rising floor for Constellation's brands.

Premiumization continues across consumer goods. Consumers might drink less, but they spend more per drink. Constellation's Mexican imports are perfectly positioned for this trend—premium enough to justify higher prices but accessible enough for regular consumption.

Market share gains could accelerate. Modelo Especial took over's Bud Light's top spot in the U.S. beer market in May and has held onto the title ever since, according to Nielsen IQ data analyzed by the investment firm Wedbush Securities. The data shows that on the four weeks ended on May 20, Modelo's share of total beer sales grew to 10.7%, while Bud Light's fell to 9.6%. This isn't just about one competitor's stumbles—it reflects fundamental shifts in American drinking preferences toward imports and away from traditional domestic lagers.

The international opportunity remains untapped. While Constellation only has U.S. rights to Corona and Modelo, success in America creates a template for other markets. The company's wine and spirits operations in other countries provide platforms for expansion.

The Quality Verdict

Constellation Brands possesses multiple reinforcing power sources that create a formidable moat. The distribution advantages, brand power, and embedded process knowledge won't disappear overnight. The business generates strong returns on invested capital, converts earnings to cash efficiently, and has proven resilient through multiple economic cycles.

However, the quality is deteriorating at the margins. Tariff vulnerability is real and potentially devastating. Demographic tailwinds are becoming headwinds. Competition from adjacent categories intensifies. The core beer business remains excellent, but excellence alone might not overcome structural challenges.

For investors, Constellation represents a classic debate: Is this a high-quality business facing temporary headwinds, or a good business beginning secular decline? The answer likely depends on timeline. Over the next few years, the brand strength and distribution advantages should prevail. Over the next decade, structural challenges might prove insurmountable without another transformation.

The company's history suggests they'll adapt—they always have. But each transformation becomes harder, and the cannabis misadventure shows they're not infallible. Constellation Brands remains a good business, possibly a very good business, but whether it's still a great business is increasingly debatable.

XI. Grading & Final Thoughts

Grading the Major Acquisitions

The Modelo/Corona acquisition (2013): A+ This deal defines perfection in M&A. Constellation paid $4.75 billion for perpetual rights to brands that now generate more than that in revenue annually. They bought at exactly the right moment—when regulatory pressure created a forced seller—and structured the deal brilliantly with permanent licenses rather than vulnerable distribution agreements. The integration was flawless, preserving brand authenticity while leveraging Constellation's distribution. This single acquisition transformed Constellation from a struggling wine company into a beer powerhouse.

Robert Mondavi acquisition (2004): A- At $1 billion, Mondavi seemed expensive, but it bought Constellation something money usually can't: legitimacy. The Mondavi name opened doors with retailers, distributors, and other acquisition targets. It signaled Constellation's evolution from bulk wine to fine wine. While they eventually sold many Mondavi assets, the acquisition served its strategic purpose perfectly. The only reason it's not an A+ is that the long-term value creation was limited.

BRL Hardy acquisition (2003): B+ The $1.1 billion Hardy deal made Constellation the world's largest wine company and provided critical international infrastructure. It was well-executed and reasonably priced. However, wine's structural challenges meant this deal never delivered the returns of the beer acquisition. Constellation eventually sold Hardy at a loss, but the deal served its purpose of building scale when scale mattered.

Canopy Growth investment (2017-2018): F The $4 billion cannabis bet represents Constellation's worst capital allocation decision. They paid peak prices for an unproven business in an uncertain regulatory environment. Unlike their other acquisitions, this wasn't opportunistic—it was speculative. The write-downs, board drama, and strategic distraction cost more than just money. It damaged credibility and diverted resources from the core business during a critical period.

Ballast Point acquisition (2015): D Constellation paid $1 billion for the craft brewery, then sold it four years later for undisclosed terms rumored to be under $100 million. This deal failed because it violated Constellation's key success factors: they paid a premium price rather than buying opportunistically, entered a declining category (craft beer was peaking), and couldn't leverage their Mexican production advantages.

What Could They Have Done Differently?

The biggest missed opportunity was international expansion. Constellation has perpetual rights to Corona and Modelo only in the United States. Had they negotiated global rights or even rights in other key markets, the company's growth runway would be substantially longer. This was probably impossible given AB InBev's position, but it remains a critical limitation.

The cannabis investment was preventable. The warning signs were clear: regulatory uncertainty, no proven business model, extreme valuations. Constellation could have taken a smaller position, waited for federal legalization, or simply stayed out entirely. The $4 billion would have been better spent on share buybacks, debt reduction, or expanding Mexican brewing capacity.

Portfolio pruning could have happened faster. Constellation held onto underperforming wine and spirits brands too long, trying to fix them rather than selling them. Earlier divestiture would have freed resources for beer investment and avoided the recent goodwill writedowns.

Geographic diversification of production deserved more attention. The current tariff vulnerability was predictable—trade tensions with Mexico have occurred regularly. Constellation could have built or acquired U.S. brewing capacity for risk mitigation, even if it meant higher costs.

The Road Not Taken: What if They Stayed Focused on Wine?

Imagine Constellation had never bought Corona/Modelo, instead doubling down on wine consolidation. They likely would have become the Diageo of wine—a large, profitable, slow-growth company generating steady cash flows from a portfolio of global brands. Market cap might be $15-20 billion versus today's $40 billion.

This alternative path would have avoided tariff risk and demographic challenges but condemned Constellation to wine's structural headwinds: fragmenting consumer preferences, retailer private label pressure, and declining per capita consumption. They would have achieved respectable returns but never spectacular ones.

The beer pivot was risky but right. It positioned Constellation in a better category with stronger brands and clearer competitive advantages. Even with current challenges, the beer-focused Constellation is a more valuable, defensible business than a wine-pure play would have been.

Future Outlook: Cannabis, Hard Seltzers, and Beyond

The cannabis investment might yet pay off, but it requires federal legalization and successful execution by Canopy Growth—both uncertain. More likely, Constellation will eventually exit completely, taking final writedowns to end the distraction.

Hard seltzers and beyond beer categories offer incremental growth but no transformation. Constellation will participate—they have to—but these categories lack the margins and moats of imported beer. They're tactical necessities, not strategic game-changers.

The real future lies in geographic expansion and premiumization. If Constellation can acquire rights to their brands in other markets or develop new super-premium offerings, growth could reaccelerate. The company also needs to solve its production concentration risk, whether through U.S. brewing, geographic diversification in Mexico, or creative supply chain solutions.

Key Takeaways for Founders and Investors

First, timing beats vision in M&A. Constellation's best deals came from recognizing when external forces created buying opportunities, not from predicting future trends. Patience and preparation matter more than prophecy.

Second, portfolio focus creates value. Constellation's willingness to sell good businesses to focus on great ones sets them apart. Most companies add complexity over time; the best subtract it strategically.

Third, authentic brands can't be manufactured. Constellation succeeded by acquiring and preserving authenticity rather than trying to create it. In consumer goods, heritage and credibility matter more than innovation.

Fourth, regulatory moats are double-edged. The three-tier system protects Constellation from new entrants but also creates rigidity. Tariffs exploit their inability to quickly adjust production. Regulatory advantages are powerful until regulations change.

Fifth, family control can work with professional management. The Sands family maintained control while bringing in outside expertise, balancing continuity with fresh perspective. This hybrid model enabled both stability and transformation.

Finally, transformation is perpetual. Constellation has reinvented itself every generation, and current challenges suggest another transformation is due. The companies that survive decades aren't those that never change but those that change successfully.

The Verdict

Constellation Brands is a remarkable business story—a family wine bottler that became a beer empire through brilliant M&A and disciplined execution. They've created enormous shareholder value, built enduring brands, and demonstrated that regional companies can become global powers.

But the story isn't over. Current challenges—tariffs, demographics, competition—are real and potentially existential. The company needs another transformation, but transformations get harder as companies get larger and markets get more efficient.

For investors today, Constellation presents a complex proposition. The business remains highly profitable with strong competitive advantages, but growth has slowed and risks have multiplied. It's neither a clear buy nor sell but rather a "show me" story—show me you can navigate tariffs, show me you can reignite growth, show me you can transform again.

The Sands family has proven doubters wrong before. They transformed bulk wine into branded wine, domestic into global, wine into beer. Whether they can transform once more—from Mexican beer importer to whatever comes next—will determine if Constellation Brands remains a great business or becomes merely a good one.

The only certainty is that the company won't stand still. Constellation's history is one of constant evolution, strategic pivots, and bold bets. Some bets, like Corona/Modelo, pay off spectacularly. Others, like cannabis, fail expensively. But the willingness to bet, to transform, to prune and grow anew—that's the real Constellation Brands story.

And that story is far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube