SouthState Bank: The Art of Serial Acquisition in Community Banking

I. Introduction & Episode Roadmap

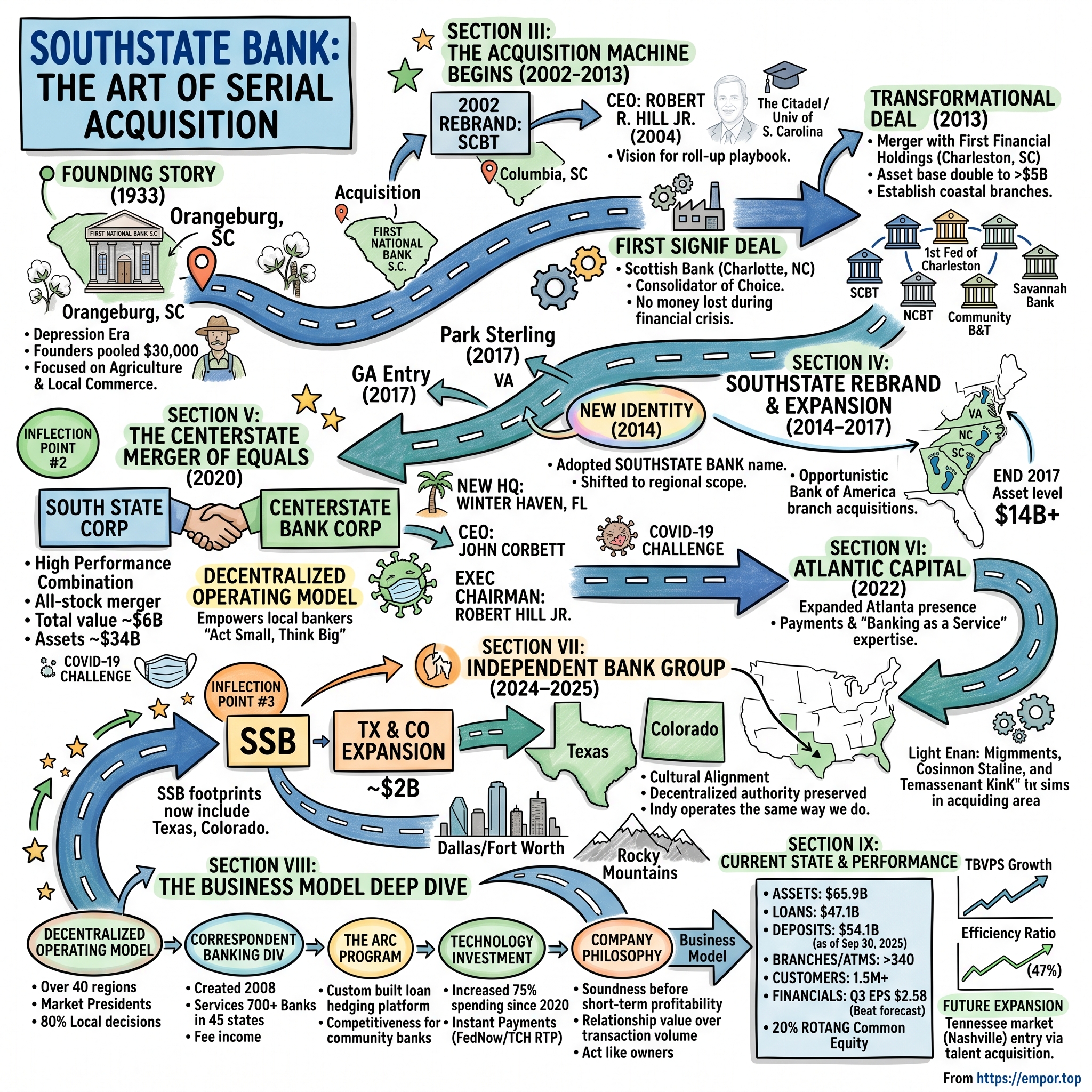

Picture a map of the American Southeast in 1933. The Great Depression has ravaged the financial system—over 9,000 banks have failed in the past four years. Yet in Orangeburg, South Carolina, a small town of barely 10,000 people nestled in the state's agricultural midlands, a group of local businessmen pool together $30,000 to charter what would become First National Bank. S.C. Forney's vision was modest: provide stable banking services to farmers and merchants in a community that had watched its savings evaporate when the larger institutions collapsed.

The company was established in 1933, originally located in Orangeburg, South Carolina. The founder of the company was S.C. Forney. The initial capital was $30,000.

Fast forward ninety-two years. Founded in 1933, SouthState has grown from a community bank into a major regional player through strategic mergers and acquisitions, including the 2020 rebranding from CenterState Bank and the recent $2 billion all-stock acquisition of Independent Bank Group, Inc., completed on January 2, 2025, which expanded its presence into Texas and Colorado by adding 92 branches.

Today, SouthState Bank Corporation (NYSE: SSB) is a financial holding company headquartered in Winter Haven, Florida, that operates SouthState Bank, N.A., a regional bank offering commercial, consumer, mortgage, and wealth management services to individuals, businesses, and municipalities across eight states in the southeastern and south-central United States.

The central question that animates this deep dive: How did a $30,000 community bank in rural South Carolina become a $65+ billion regional banking powerhouse? The answer lies in what might be called the "roll-up playbook"—a methodical approach to M&A that has defined SouthState's trajectory for two decades. But this isn't simply a story of buying competitors and consolidating costs. It's a masterclass in cultural integration, decentralized operating models, and the patient accumulation of scale in America's fastest-growing markets.

This article will explore the origins of both SouthState and its merger partner CenterState, trace the acquisition machine that Robert Hill Jr. built during his tenure as CEO, examine the transformative 2020 merger of equals, analyze the business model that powers today's operation, and assess what lies ahead for investors watching this regional banking story unfold.

II. Origins: A Depression-Era Community Bank (1933-2000)

The Founding Story

The story of SouthState begins not with a grand vision for regional dominance, but with the simple imperative of survival. In 1933, America's banking system was in ruins. President Roosevelt had declared a bank holiday in March of that year, and the new Federal Deposit Insurance Corporation was just beginning to restore public confidence. Against this backdrop, First National Bank began in Orangeburg, South Carolina in 1933.

Orangeburg was cotton country—a community where the agricultural cycle dictated everything from loan demand to deposit flows. The founders understood something fundamental about community banking that would echo through the decades: banking in small towns is about relationships, not transactions. When a farmer needed credit to plant his crop, the banker knew his family, his land, and his character. When a merchant needed working capital, the decision was made down the street, not in some distant headquarters.

This relationship-based model would prove remarkably durable. While the megabanks that would eventually dominate American finance focused on scale and standardization, community banks like First National carved out defensible positions in markets too small to attract serious competition. The margins were thinner, the growth slower, but the deposit relationships were sticky in ways that urban banking could never replicate.

The Community Banking Model

What made community banking work in rural America was precisely what made it difficult to scale. Local decision-making meant that loan officers had the authority to approve credits based on their direct knowledge of borrowers. This reduced information asymmetries but also meant that growth required finding and training people who could replicate that judgment in new markets.

The model also depended on a certain kind of community involvement. Bankers served on local boards, sponsored Little League teams, and attended the same churches as their customers. This wasn't mere marketing—it was the information-gathering mechanism that allowed small banks to underwrite credits that larger institutions would reject or misprice.

For sixty-seven years, First National Bank operated in this mode: slow, steady, deeply embedded in its community. As of 2013, 240 people still worked in Orangeburg. SCBT added offices in the Greenville, South Carolina area as well.

Parallel Timeline: CenterState's Florida Origins

While First National was serving South Carolina's agricultural communities, a parallel story was unfolding in Central Florida. The story of CenterState begins not with a single founding but with a merger of three existing banks.

On June 30, 2000, these entities—First National Bank of Polk County, CenterState Bank, and First National Bank of Osceola County—merged to form CenterState Banks of Florida, Inc., as a multi-bank holding company, reorganizing operations under a unified structure to support coordinated growth in the region.

This organizational structure—a holding company sitting atop multiple community banks—would prove prescient. It allowed CenterState to maintain local identities and decision-making while achieving operational efficiencies at the holding company level. In January 2006, further consolidation occurred when First National Bank of Polk County merged into CenterState Bank of Florida, National Association, adopting the latter's name to streamline branding and emphasize its Florida-centric identity.

These two origin stories—one in the rural Carolina midlands, one in Florida's rapidly growing Central corridor—would converge two decades later in one of regional banking's most consequential mergers. But first, the South Carolina institution needed to transform itself from a sleepy community bank into a disciplined acquisition machine.

III. The Transformation Begins: SCBT & The Acquisition Machine (2002-2013)

Rebranding and Repositioning

The early 2000s marked a decisive break with First National's past. In 2002, the bank changed its name to South Carolina Bank and Trust and moved its headquarters to Columbia, South Carolina. First National Corp. changed its name to SCBT Financial Corp. in 2003. The bank was South Carolina's fourth largest with $1 billion in assets.

This wasn't merely cosmetic rebranding. Moving headquarters from Orangeburg to Columbia signaled an ambition to compete at a different level. Columbia, the state capital and a regional economic hub, offered access to larger commercial relationships, a deeper talent pool, and the infrastructure needed to support expansion.

At the helm of this transformation was Robert R. Hill Jr., a native of Columbia who had joined the bank in 1995 and risen through the ranks. Robert joined SouthState in 1995 as President of its subsidiary bank and was named CEO of the corporation in 2004. Hill's background was pure South Carolina: A native of Columbia, SC, Hill is a graduate of The Citadel and also earned an MBA from the University of South Carolina Moore School of Business.

The Citadel graduate and Columbia resident had a long and prolific run at the top, rising to the corner office at SCBT Financial Corp. in 2003, just eight years after joining the tiny Midlands lender. Hill brought something crucial to the CEO role: a clear vision for how to build scale in a fragmented industry where organic growth alone would never be sufficient.

Early Acquisition Strategy

The first significant deal came in late 2007. On November 30, 2007, SCBT Financial Corp. completed its acquisition of TSB Financial Corporation and its bank The Scottish Bank, giving SCBT four Charlotte, North Carolina locations and a loan production office in Cornelius, North Carolina.

This deal revealed the playbook that Hill would refine over the next decade: acquire community banks in adjacent markets, retain local talent, integrate carefully. Charlotte was a logical first step beyond South Carolina—it was the Southeast's largest banking center, home to Bank of America's headquarters and Wells Fargo's East Coast operations, yet still offered niches where well-capitalized community banks could compete.

The timing proved serendipitous. The global financial crisis that erupted in 2008 devastated many community banks while leaving well-managed institutions like SCBT relatively unscathed. The global banking industry meltdown a few years later was an unlikely growth catalyst. The turmoil created an opening for SCBT to become what Hill liked to call a "consolidator of choice" for banks weakened by the downturn and seeking out well-capitalized buyers. "We never had a year where we lost money during the financial crisis," he said.

The First Major Deal: First Financial Holdings (2013)

By 2013, SCBT was ready for a transformational acquisition. In 2013, SCBT Financial Corp. announced a merger with First Financial Holdings of Charleston, started in 1934, which had 66 Carolinas locations and was the third-largest financial institution with headquarters in South Carolina.

The $447 million deal for First Financial was the biggest ever for SCBT Financial, which became the owner of five banks—SCBT; First Federal Bank of Charleston; NCBT of Charlotte, North Carolina; Community Bank & Trust of Cornelia, Georgia; and the Savannah Bank of coastal Georgia.

The transaction mechanics revealed thoughtful structuring. SCBT president and CEO Robert R. Hill Jr. would remain as CEO, and chair Robert R. Horger would be chair. First Financial president and CEO R. Wayne Hall would become president of the merged company, and First Financial chair Paula Harper Bethea would be vice chair.

Completed on July 26, 2013, the merger integrated First Financial's operations, adding 66 branches across North and South Carolina and significantly boosting SouthState's asset base to over $5 billion. This acquisition not only doubled the bank's footprint in coastal markets but also positioned it as a leading community bank in the region by combining complementary branch networks and customer bases.

The First Financial deal established several patterns that would characterize subsequent acquisitions. First, retain key leaders from acquired institutions—their relationships and local knowledge were often the most valuable assets. Second, move quickly on integration but preserve local autonomy where it mattered. Third, use the combined scale to invest in technology and products that neither institution could afford alone.

By 2019, he had helped engineer 15 acquisitions. The acquisition machine was now fully operational.

IV. Inflection Point #1: The SouthState Rebrand & Expansion (2014-2017)

The New Identity

The First Financial merger demanded a new identity. Following SCBT Financial Corporation's merger with First Financial Holdings, Inc., the holding company rebranded as SouthState Corporation in 2014 to signify its evolving scale across multiple states. In June 2014, the banking subsidiary adopted the SouthState Bank name, reflecting its expanded regional scope in the Southeast and commitment to integrated community banking beyond South Carolina.

The name change was strategic on multiple levels. "South Carolina Bank and Trust" limited the franchise geographically just as it was pushing into Georgia, North Carolina, and beyond. "SouthState" conveyed regional ambition while retaining the Southern identity that resonated with customers across the franchise.

The merger added coastal South Carolina branches to the Midlands and Upstate and gave the bank $8 billion in assets. The Charleston market was particularly valuable—a rapidly growing economy driven by the port, Boeing's manufacturing expansion, and a booming tourism sector.

But SouthState wasn't content to wait for the next transformational deal. Also, in August, SouthState took over 13 Bank of America branches in areas it did not serve. These opportunistic branch acquisitions from larger banks became a recurring theme. As the megabanks rationalized their networks, they often exited smaller markets where SouthState could provide superior service.

Georgia Entry: Southeastern Bank Financial (2017)

SouthState's entry into Georgia came through a deliberate market expansion. On January 4, 2017, SouthState announced completion of a deal valued at about $335 million for Augusta, Georgia-based Southeastern Bank Financial Corp., which gave SouthState nine Georgia Bank & Trust branches and three Southern Bank & Trust branches in South Carolina.

The Augusta market made strategic sense—it straddled the Georgia-South Carolina border, allowing SouthState to serve customers whose lives and businesses crossed state lines. The medical complex anchored by Augusta University Health, the military presence at Fort Gordon, and the annual Masters Tournament all contributed to a diversified economy.

Park Sterling: Building Regional Scale

Later in 2017, SouthState made its move into Virginia. On April 27, 2017, SouthState Corp. agreed to acquire Park Sterling Corp. of Charlotte, North Carolina, for $690.8 million. The deal was completed November 30, 2017 with signs changed in April 2018. SouthState added 43 branches, five in Georgia, 23 in South Carolina, 17 in North Carolina and 8 in Virginia.

Park Sterling brought more than branches—it brought commercial banking expertise and deeper penetration in the Charlotte market where SouthState had been building since the 2007 Scottish Bank acquisition. The deal also established a Virginia presence in Richmond and its suburbs, opening another growth vector.

By the end of 2017, SouthState had grown from $1 billion to over $14 billion in assets in just fifteen years. The question was no longer whether the bank could execute acquisitions—that capability was proven. The question was whether the playbook could scale further, and what kind of partner might accelerate the journey from regional player to Southeast powerhouse.

V. Inflection Point #2: The CenterState Merger of Equals (2020)

The Strategic Logic

On January 27, 2020, the banking world learned that two of the Southeast's most respected regional banks would combine. South State and CenterState to Combine in Merger of Equals to Create Leading Southeast Regional Bank. Combined Company Positioned to be a High Performance Financial Institution with Approximately $34 Billion in Assets Serving 18 High Growth Markets in six Southeastern States.

The deal's origins reflected the relationship-driven culture both institutions prized. "We have known and admired Robert and his team for over a decade, and we believe our two organizations are an outstanding fit," said John C. Corbett, CEO of CenterState. "Combining these two high-performing teams will allow us to build an even stronger company together."

The 2020 merger of CenterState Bank and SouthState Bank made sense: SouthState and CenterState management teams were well-known to each other and both operated under a decentralized model that empowers local bankers to make decisions for their clients. It also allowed CenterState to provide more products and services to its clients. In addition, the two banks had no geographic overlap, serving 10 of the 15 largest MSAs in Florida, Virginia, North Carolina, South Carolina, Georgia and Alabama.

Deal Structure & Governance

The transaction mechanics reflected careful negotiation. CenterState Bank Corporation and South State Corporation jointly announced today that they have entered into a definitive agreement under which the companies will combine in an all-stock merger of equals with a total market value of approximately $6 billion. Under the terms of the merger agreement, CenterState shareholders will receive 0.3001 shares of South State common stock for each share of CenterState common stock they own. CenterState shareholders will own approximately 53% and South State shareholders will own approximately 47% of the combined company. The combined company will operate under the South State Bank name and will trade under the South State ticker symbol SSB.

The deal will create a bank with $34 billion in assets and operations stretching from the Carolinas to Florida.

The governance structure embodied the merger-of-equals philosophy. The Board of the new company will consist of 16 directors, eight current South State directors and eight current CenterState directors. Robert R. Hill, Jr., President and CEO of South State Corporation, will serve as Executive Chairman of the combined company. John Corbett at Centerstate will remain CEO, while Robert Hill Jr., South State's CEO, will become executive chairman. Each company will have eight directors on the board.

John Corbett brought a different but complementary skillset. Mr. Corbett was the President & CEO of CenterState Bank Corporation and served as a director of both CenterState Bank and its bank subsidiary. Prior to becoming President and CEO of the bank, he served as its Executive Vice President and Chief Credit Officer. Before joining the CenterState group in 1999, he served as Vice President of Commercial Banking at First Union National Bank in Florida.

SouthState's John Corbett is among the most respected CEOs in the banking industry today. In this discussion, Corbett recounts the story of his career, growing a De Novo community bank in central Florida two decades ago to the southeast regional force that SouthState Bank is today. Along the way, we gain insight into a managerial style that prioritizes innovative and creative thinking, teamwork, the importance of culture, the value of humility, "thinking big" while "acting small".

COVID-19 Context & Integration

The timing could hardly have been more challenging. In connection with the Merger, we brought together an executive leadership team with the appropriate strategic vision and experience to guide the Company as it grows into a Southeast regional institution and completed a large, complex integration effort in the midst of the COVID-19 pandemic.

On June 8, 2020, SouthState completed a merger with CenterState Bank. The new bank will keep the SouthState name, but move its headquarters to Winter Haven, Florida. The combined bank has $34 billion in assets.

The move to Winter Haven—CenterState's home base—was significant. Florida had become the growth engine of the Southeast, and centering operations there signaled where management saw the most opportunity. Yet the company maintained substantial presence in Columbia and Charleston, preserving the institutional knowledge and relationships that Hill had built over two decades.

Technology & Digital Strategy

CenterState brought something SouthState needed: recognition that the future would be digital. The integration discussions surfaced a key insight—CenterState's rapid acquisition pace had left less bandwidth for technology investment, while SouthState had moved ahead on digital initiatives.

The combined company could now invest at scale in capabilities that neither could have built alone. This would prove crucial as the banking industry accelerated its digital transformation during the pandemic.

The financial outcomes justified the deal's complexity. The combined experience of both management teams—The pro forma organization, with approximately $34 billion in assets and $26 billion in deposits, combines two high-quality companies with comparable credit and management philosophies.—created an institution large enough to compete with regional powers while retaining the community bank ethos that customers valued.

VI. Post-Merger Consolidation: Atlantic Capital (2022)

Atlanta Market Expansion

With the CenterState integration substantially complete, SouthState turned its attention to Atlanta. The Southeast's largest metropolitan economy had been a gap in the franchise—the company had peripheral presence but lacked the scale to compete effectively in the region's most dynamic market.

ATLANTA, March 1, 2022 /PRNewswire/ -- SouthState Corporation today announced the closing of its acquisition of Atlantic Capital Bancshares, Inc.

The combined company has an expanded presence in the Atlanta market, with $5 billion in deposits and ranks 8th in market share.

"We are pleased to welcome the talented bankers and expanded corporate banking focus and expertise in payments and 'banking as a service' from Atlantic Capital," said John C. Corbett, CEO of SouthState. "Atlanta is a strategically important market for us, and to assist with that growth and focus, we're pleased to welcome Doug Williams and his team in Atlanta."

Atlantic Capital brought specialized capabilities. The Atlantic Capital executive leadership team will continue to serve the Atlantic Capital customers and the Atlanta community, most notably: Douglas L. Williams, former Atlantic Capital CEO, now serves as president of Atlanta Banking Group & head of Corporate Banking. Kurt A. Shreiner will continue as president of the Corporate Financial Services division and will continue to focus on the growth of the FinTech and Payments businesses.

The payments and "banking as a service" expertise was particularly valuable. As fintech companies sought banking partners, Atlantic Capital had built relationships that SouthState could now leverage across its larger platform.

The deal also brought board diversity. Douglas J. Hertz, president & CEO United Distributors, has served on the Atlantic Capital board since 2011. A native of Atlanta since 1984, Hertz has grown United Distributors, a privately held beverage distribution business, to one of the top 25 private companies in Atlanta. He began his career with KPMG, LLP.

Hertz would later become independent Chairman of the Board, bringing Atlanta connections and operating company experience to governance.

VII. Inflection Point #3: Independent Bank Group & Texas Expansion (2024-2025)

The Texas Play

On May 20, 2024, SouthState announced its most geographically ambitious acquisition. SouthState Corporation and Independent Bank Group, Inc. jointly announced today that they have entered into a definitive agreement under which SouthState will acquire Independent Bank Group, in an all-stock transaction valued at approximately $2 billion. Independent Bank Group, based in McKinney, Texas, has approximately $18.9 billion in total assets, $15.7 billion in total deposits and $14.6 billion in total loans as of March 31, 2024, and operates in four market regions located in Dallas/Fort Worth, Austin and Houston areas in Texas and the Colorado Front Range. With a presence in 12 of the 15 fastest growing MSAs in the United States, the combined company will have pro forma total assets of $65 billion.

The transaction represented a strategic bet on Texas, the state that has led U.S. population growth for years. Dallas-Fort Worth, Austin, and Houston are among America's fastest-growing metropolitan areas, with demographics and business formation rates that dwarf most of the Southeast.

The merger closed on January 1, 2025, through the merger of Independent Financial with and into SouthState. Immediately after the merger, also on January 1, 2025, Independent Financial's subsidiary bank, Independent Bank, merged into SouthState Bank.

Cultural Alignment

The Independent deal worked because cultural fit was paramount. Independent also shares SouthState's belief in decentralized authority. So, every decision made doesn't need to go through headquarters first. "SouthState has over 40 regions, each run by a market president," Dreyer said. "They're involved in local chambers and economic development groups. They are Kiwanians and Rotarians. You really know what's going on in your local markets, and you make 80% of decisions. Independent operates the same way we do. They fit our operating model and culture."

David R. Brooks, former Independent Financial chairman and CEO, began his banking career in the early 1980s and has been active in community banking since he led the investor group that acquired Independent Bank in 1988. Brooks currently serves as Chairman of Capital Southwest Corporation, and previously served as the Chief Financial Officer at Baylor University from 2000 to 2004. In 2018, Brooks was inducted into The Texas Bankers Hall of Fame.

Integration & Results

The integration proceeded rapidly. If you recall, we closed on the Independent Financial transaction in January. We converted the computer systems in May, and now we're beginning to realize the full earnings power of the combined company. Loan production was up a little in the third quarter to nearly $3.4 billion, and we saw moderate growth in both loans and deposits. Payoffs were about $100 million higher in the quarter. Loan production in Texas and Colorado is up 67% since the first quarter of the year, and loan pipelines across the company continue to grow.

The numbers told a compelling story of successful execution. South State Corp demonstrated robust financial performance in Q3 2025, with a notable 30% year-over-year increase in EPS. The company reported a return on tangible equity of 20%, highlighting its strong capital efficiency.

VIII. The Business Model Deep Dive

Decentralized Operating Model

What distinguishes SouthState from many regional bank competitors is its operating philosophy. "SouthState has over 40 regions, each run by a market president," Dreyer said. "They're involved in local chambers and economic development groups. They are Kiwanians and Rotarians. You really know what's going on in your local markets, and you make 80% of decisions."

This decentralized model represents a deliberate tradeoff. It's harder to manage than a centralized structure—you need strong market presidents and robust risk management to ensure consistency. But it preserves the relationship advantage that made community banking successful in the first place. When a business owner needs a loan decision, they're talking to someone who knows their market, not a distant credit committee.

Correspondent Banking Division

One of SouthState's most distinctive assets is its correspondent banking division. The SouthState Correspondent Division is a full-service unit with an extensive network of bank and other institutional relationships throughout the United States. Created in 2008, the Correspondent Division manages over 700 relationships in 45 states.

This business serves other community banks—providing services they can't economically build themselves. It's a capital-light revenue stream that leverages SouthState's scale without requiring branch networks.

The ARC Program

The centerpiece of the correspondent division's offering is the ARC (Assumable Rate Conversion) program. The ARC Program is a loan hedging platform that was custom-built for community banks and their borrowers. The program offers simplicity, ease of use, and documentation and accounting advantages that can make community banks more competitive than their national or regional competitors.

At SouthState, we use a program called ARC (Assumable Rate Conversion) that allows borrowers to pay a fixed rate of interest for as long as 20 years, but the bank retains a floating rate asset. ARC allows a more sophisticated commercial borrower the option to fix term loans out to 20 years. We find that the program enables us to differentiate our loan offering from most banks.

This is exactly the kind of capability that scale enables. Building a loan hedging platform requires significant technology investment and expertise that small community banks can't justify. By offering it as a service, SouthState generates fee income while helping its correspondent clients compete more effectively.

The revenue contribution is meaningful. Noninterest Income of $99.1 million, up $12 million compared to the prior quarter, primarily due to an increase in correspondent banking and capital markets income.

Technology Investment

Scale has enabled substantial technology investment. "We've gone from being under $1 billion locally to a $45 billion bank. Along the way we've had to invest in more technology."

The investment has been material: technology spending increased approximately 75%—almost $70 million more annually—since 2020 to stay current. This includes instant payments capability, SouthState Bank today announced its Treasury customers now have access to send and receive instant payments. During the past year, SouthState has conducted an instant payments pilot program with a group of clients. Throughout this time, more than 600,000 instant payment transactions totaling more than $400 million have been processed.

SouthState Bank, a financial institution serving over one million customers, modernized its payments infrastructure to meet growing customer expectations and industry demands. Partnering with Volante Technologies, SouthState launched an Instant Payments initiative as part of a multi-year strategy. This initiative enabled faster, more secure, and more flexible payment experiences via The Clearing House RTP platform and the Federal Reserve Financial Services' FedNow Service. By leveraging Volante's cloud-native Payments as a Service (PaaS) platform, SouthState not only enhanced operational efficiency but also positioned itself as a leader in real-time payments.

Company Philosophy

The stated philosophy reflects the community banking heritage: soundness before short-term profitability, relationship value over transactional volume. Management describes thinking and acting like owners, measuring success over entire economic cycles rather than quarter to quarter.

This long-term orientation is evident in the acquisition approach. SouthState has consistently paid reasonable multiples for high-quality franchises rather than chasing accretion through distressed asset purchases. The result is a portfolio of well-integrated acquisitions rather than a collection of disparate pieces.

IX. Current State & Financial Performance

Scale Achieved

As of the third quarter of 2025, SouthState has achieved scale that would have been unimaginable to the founders in Orangeburg. As of September 30, 2025, the company manages total assets of $65.9 billion, net loans of $47.1 billion, and total deposits of $54.1 billion, while operating more than 340 branches and ATMs.

SouthState Bank, N.A., the company's nationally chartered bank subsidiary, provides consumer, commercial, mortgage and wealth management solutions to more than 1.5 million customers throughout Florida, Texas, the Carolinas, Georgia, Colorado, Alabama, and Virginia. The bank also serves clients nationwide through its correspondent banking division.

Financial Metrics

The most recent quarterly results demonstrate the earnings power of the combined franchise. Revenue: $699 million, exceeding the forecast of $660.72 million. Earnings per share: $2.58, a 22.86% surprise over the forecast of $2.10. Net interest income: $600 million, up $22 million from Q2. Loan production: $3.4 billion, with strong growth in key markets. Return on tangible equity: 20%.

Return on Average Common Equity of 11.0%; Return on Average Tangible Common Equity (Non-GAAP) of 19.6% and Adjusted Return on Average Tangible Common Equity (Non-GAAP) of 20.8%. Return on Average Assets ("ROAA") of 1.49% and Adjusted ROAA (Non-GAAP) of 1.59%.

The efficiency ratio has improved substantially: Efficiency Ratio of 50% and Adjusted Efficiency Ratio (Non-GAAP) of 47%. For context, the average regional bank efficiency ratio tends to run in the mid-50s to low-60s, making SouthState's performance indicative of successful cost integration.

Capital position remains strong. The company redeemed $405 million of subordinated debentures, and its capital position remained strong with a tangible common equity ratio of 8.8% and a total risk-based capital ratio of 14%.

Ongoing Expansion

Even as management integrates Independent Financial, expansion continues. SouthState Bank has hired an experienced team, based in Nashville, to help the bank expand to Tennessee. Cameron Wells, an experienced leader in the Middle Tennessee market, has joined SouthState as division president, responsible for leading the team and the bank's presence in the region.

"SouthState is excited to have a presence in the growing, thriving Nashville market, and we are thrilled to have Cameron's strong leadership," said Richard Murray, president. "Tennessee, and Nashville, in particular, is a natural geographic and demographic expansion for SouthState. We are eager to open our office here so we can fully serve our Commercial and Middle Market customers."

The talent acquisition strategy is notable—poaching teams from larger competitors. Wells brings more than 20 years of experience with BB&T and Truist to the division president role at SouthState. For almost eight years, he has served as Nashville Market president at Truist. He has extensive experience in Commercial, Consumer and Small Business Banking.

X. Porter's Five Forces Analysis

Understanding SouthState's competitive position requires examining the structural forces that shape regional banking economics.

1. Threat of New Entrants: MODERATE-LOW

The barriers to entry in banking remain formidable. Obtaining a banking charter requires substantial capital, regulatory approval, and compliance infrastructure. FDIC insurance, while essential for deposit-taking, comes with examination requirements and restrictions.

However, the threat picture has evolved. Traditional de novo bank formation has slowed dramatically since the financial crisis—regulatory scrutiny increased and returns made the effort less attractive. But fintech challengers have found alternative paths, obtaining state licenses for specific activities or partnering with existing banks to offer deposit-like products.

SouthState's scale advantages—technology investment, correspondent banking services, broad product capabilities—create barriers that new entrants struggle to replicate. A startup can build an attractive mobile interface, but building the correspondent banking relationships that generate fee income takes decades.

2. Bargaining Power of Suppliers: LOW

Banks' primary "suppliers" are depositors, and here the power dynamics favor institutions with strong retail franchises. SouthState's low-cost deposit base—built through decades of community banking relationships—provides funding cost advantages that translate directly to margins.

The Federal Reserve sets baseline funding costs, limiting supplier differentiation. Interbank lending markets provide backup funding, though reliance on wholesale funding signals weakness in the core deposit franchise.

3. Bargaining Power of Buyers (Customers): MODERATE-HIGH

This is where competitive pressure is most acute. Basic banking services face low switching costs—opening a new checking account takes minutes online. Commercial customers have multiple lending options, including direct lenders, credit funds, and fintech platforms.

Price transparency has increased dramatically. Rate comparison websites and mobile apps make it trivial to identify better deposit rates or loan terms. The commoditization of basic banking products forces differentiation on service, convenience, and relationship quality.

SouthState's response is the decentralized model—empowering local bankers to build relationships that justify premium pricing. When the market president knows your business, understands your challenges, and can make decisions quickly, that's worth something. How much? That's the ongoing competitive question.

4. Threat of Substitutes: HIGH & INCREASING

This is the force that keeps bank executives awake at night. Massive white space remains: fintechs still only penetrate 3% of global banking and insurance revenue pools—leaving vertical and geographic gaps to be filled.

The substitute threats are varied: fintech lenders like SoFi and LendingClub, credit unions with tax advantages, non-bank payment solutions from PayPal, Venmo, and Square, and direct lending from private credit and PE firms.

A set of established scaled fintechs—those generating more than $500 million in annual revenue—account for roughly $231 billion, or 60%, of the global fintech industry's total revenue. Fintechs have penetrated only about 3% of banking and insurance revenues—but are growing three times more quickly than incumbent banks.

Don't get me wrong, Fintech companies achieved a lot! Banks might be losing (or have already lost?) payment acceptance business to Fintech companies. JPMorgan Chase is probably the last big bank weathering competition well, but Stripe and Adyen are quickly catching up.

However, the disruption narrative requires nuance. JPMorgan Chase, Bank of America, Wells Fargo, and Citi all reported, small, but nevertheless growth in retail deposits. Regional banks did well too. "Firm-wide deposits have stabilized, and we expect to see a more visible growth trend assert itself in the second half of 2025. It's notable that we can already see that trend in consumer checking deposits."

5. Competitive Rivalry: HIGH

Regional banking competition has intensified as scale economics favor consolidation. The largest banks have advantages in technology investment and brand marketing. Smaller community banks struggle to invest in digital capabilities. Mid-sized regionals like SouthState occupy a challenging middle ground—too large to ignore economies of scale, too small to compete on marketing spend with the megabanks.

The response is the roll-up strategy SouthState has executed: use acquisitions to achieve scale, invest the resulting efficiency gains in technology and talent, and compete on relationship quality in markets where the megabanks are less interested.

XI. Competitive Position & Strategic Analysis

Hamilton Helmer's 7 Powers Framework

Applying Helmer's framework illuminates SouthState's competitive moat—or lack thereof:

Scale Economies: SouthState has achieved meaningful scale, enabling technology investments and correspondent banking services that smaller competitors cannot match. The efficiency ratio improvement demonstrates operational leverage. However, the megabanks have greater scale, limiting this advantage to mid-market competition.

Network Effects: Limited in traditional banking, but the correspondent banking division creates a mild network effect—more community bank relationships enable better service offerings, attracting additional relationships.

Counter-Positioning: This may be SouthState's strongest power. The decentralized model that empowers local decision-making is difficult for large banks to adopt—their cost structures assume centralized credit decisions and standardized products. Adopting SouthState's model would require incumbents to disrupt their existing operations.

Switching Costs: Moderate in commercial banking relationships where the value of banker knowledge creates friction. Lower in consumer banking where digital onboarding has reduced transition costs.

Branding: Regional recognition but limited national brand power. The "community bank with scale" positioning differentiates within the Southeast but doesn't travel to new markets without acquisition.

Cornered Resource: The management team's M&A experience represents accumulated knowledge that's difficult to replicate quickly. The correspondent banking relationships built over 15+ years would take competitors years to establish.

Process Power: The integration playbook—retain talent, maintain local autonomy, invest in technology—represents learned capability that improves with each acquisition.

Myth vs. Reality: The "Community Bank" Narrative

Myth: SouthState is just a collection of acquired banks stitched together.

Reality: The integration track record suggests genuine cultural cohesion. The decentralized model creates local accountability while the holding company provides scale resources. Employee retention metrics and customer satisfaction scores would be key metrics to validate this narrative.

Myth: Regional banks are dying as customers move online.

Reality: We cannot really say that Fintech companies are disrupting banks, at least the big banks are fine. Fintech companies might be disrupting community banks, but was that the ambition? I am pretty sure investors didn't pour billions into the Fintech industry to disrupt community banks. After all, about a dozen or so largest banks (with $250+ in assets) generate 60% of the industry's profit. Well-capitalized regionals with digital capabilities can compete effectively.

Myth: Acquisitions destroy value through integration costs.

Reality: SouthState's track record suggests otherwise—efficiency ratios have improved, earnings have grown, and tangible book value has compounded. The key is disciplined pricing and cultural fit, both of which management has demonstrated.

XII. Bull and Bear Cases

The Bull Case

The optimistic thesis rests on several pillars:

Demographic Tailwinds: SouthState operates in America's growth corridor. Florida, Texas, the Carolinas, Georgia—these are the states gaining population while the Northeast and Midwest lose residents. Business formation follows population, creating natural loan demand growth.

Scale Benefits Compounding: Each acquisition brings cost synergies, and those savings fund technology investments that make the next acquisition more valuable. The correspondent banking division spreads fixed costs over an expanding customer base.

Management Track Record: Robert E. Hill Jr. recently stepped down as executive chairman of SouthState Bank, where he oversaw 15 acquisitions in as many years while CEO. The team has executed through financial crises, pandemic disruptions, and competitive upheaval. John Corbett brings continuity and a demonstrated ability to integrate large transactions.

Interest Rate Environment: Regional banks with strong core deposit franchises benefit disproportionately from higher rates. Net interest margins have expanded, and deposit betas have remained manageable.

Dividend Growth: SouthState Bank has an annual dividend of $2.40 per share, with a yield of 2.73%. The dividend is paid every three months. SouthState Bank Corporation has a moderate payout ratio of 30.41%, which may indicate a balance between reinvesting earnings and rewarding shareholders with dividends.

The Bear Case

The cautionary thesis focuses on:

Commercial Real Estate Exposure: Regional banks have historically concentrated lending in commercial real estate. Office property distress, rising vacancies, and refinancing walls create credit risk that may not be fully provisioned.

Technology Competition: Smaller regional banks might be more dependent on the collaboration with such a FinTech company as a way to modernize their services. Irrespective of the size, disruptive force of FinTech serves as an agent of change that urges banks to innovate or die out.

Integration Execution Risk: The Independent Financial deal is the largest geographic leap in company history. Texas is a competitive market with strong regional players. Integration challenges in new markets could prove more difficult than in adjacent Southeast expansion.

Regulatory Complexity: Stablecoins could herald a new era of money, presenting both challenges and opportunities for banks and payment companies. 2026 could be a pivotal year to develop strategies and address the risks related to stablecoins. In response, banks will likely need to bolster their infrastructure and capabilities as alternatives to deposits and payment rails emerge.

Economic Cycle Exposure: Regional banks typically underperform during recessions as credit losses mount. The portfolio concentration in growth markets could amplify cyclical exposure.

XIII. Key Performance Indicators for Investors

When monitoring SouthState's ongoing performance, three KPIs deserve particular attention:

1. Net Interest Margin (NIM)

NIM measures the difference between interest income earned and interest paid, divided by average earning assets. For a bank built on relationship lending and core deposits, NIM captures the fundamental economics of the franchise.

SouthState's current NIM of approximately 4% reflects successful integration of acquired portfolios and the benefit of higher rates. Watch for compression as rates decline and deposit competition intensifies. The trend matters more than the level—stable or expanding NIM indicates successful balance sheet management.

2. Efficiency Ratio

The efficiency ratio (non-interest expense divided by revenue) measures operating leverage. SouthState's current adjusted efficiency ratio of 47% is excellent for a regional bank, demonstrating successful cost integration from recent acquisitions.

Monitor this metric for signs of integration strain or competitive pressure requiring increased investment. Rising efficiency ratios would suggest that scale benefits are not materializing as expected.

3. Tangible Book Value Per Share (TBVPS) Growth

SouthState's TBVPS grew at a solid 6.5% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 13.5% annually over the last two years from $42.27 to $54.48 per share. Over the next 12 months, Consensus estimates call for SouthState's TBVPS to grow by 11.6% to $60.79.

TBVPS strips out intangible assets from acquisitions, providing a clean measure of underlying equity accumulation. For serial acquirers, this metric reveals whether deals are creating or destroying value over time.

XIV. Conclusion: The Roll-Up Playbook

SouthState's journey from a $30,000 Depression-era community bank to a $65+ billion regional powerhouse offers lessons that extend beyond banking. The company demonstrates that industry fragmentation creates opportunities for disciplined consolidators willing to invest in integration capability.

The key insights:

Culture Matters: Every acquisition discussion started with cultural fit assessment. Banks that shared the decentralized philosophy integrated smoothly; those that didn't were passed over regardless of financial attractiveness.

Scale Enables Investment: The correspondent banking division, ARC program, instant payments capability—none of these would exist without scale. Each acquisition justified investments that made the next acquisition more valuable.

Demographics Are Destiny: Positioning in growth markets—Florida, Texas, the Southeast—creates organic growth that supplements M&A. You can't consolidate your way to prosperity in declining markets.

Integration Is a Competency: The management team has executed dozens of integrations and refined the playbook with each one. This accumulated knowledge is difficult for competitors to replicate quickly.

The strategic pivot underway is notable. CEO John Corbett highlighted the company's strategic position, stating, "We're now in a perfect position to capitalize on the disruption occurring in our markets." He emphasized the focus on organic growth, saying, "With our particular fact pattern, investing in SouthState is more interesting right now than doing an M&A deal."

After two decades of acquisition-driven growth, management sees greater opportunity in organic expansion. The Texas and Tennessee entries represent bets on internal talent acquisition rather than whole-bank purchases. This shift suggests management believes the integration platform is complete and the opportunity now lies in filling in the footprint.

For investors, SouthState represents a bet on several themes: Southeast and Texas demographic growth, the durability of relationship banking in an increasingly digital world, and management's ability to compound value through disciplined capital allocation. The track record supports cautious optimism, though commercial real estate credit quality and integration execution in Texas bear watching.

From Orangeburg to Winter Haven, from $30,000 to $65 billion, SouthState's story isn't finished. But the arc is clear: methodical acquisition, careful integration, relentless investment in scale. In an industry where most roll-ups destroy value through cultural collisions and integration failures, SouthState has built something that endures. The next chapter—organic growth in America's fastest-growing markets—may prove even more interesting than the roll-up story that preceded it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube