Ryan Specialty: Building the Specialty Insurance Powerhouse

I. Introduction & Episode Roadmap

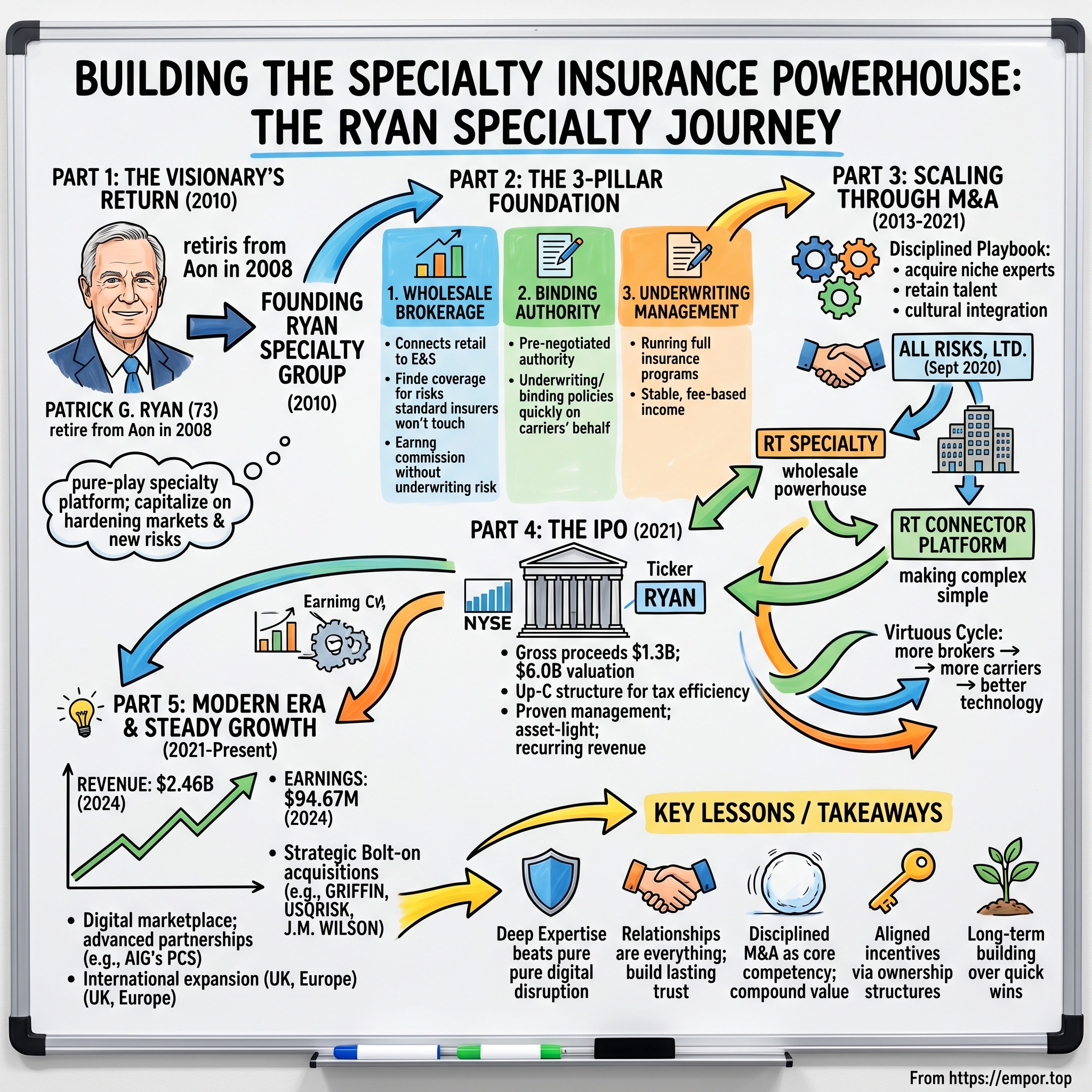

Picture this: It's 2010, and a 73-year-old billionaire walks away from a comfortable retirement to start over. Not with a hobby business or a vanity project, but with the audacious goal of building a specialty insurance powerhouse from scratch. Within thirteen years, that startup would be worth $20 billion—a feat that most entrepreneurs half his age could only dream of.

This is the story of Ryan Specialty Group, but more fundamentally, it's the story of Patrick G. Ryan—a man who built Aon into one of the world's largest insurance brokers, retired as a legend, then came back to prove that the first act wasn't just luck. It's about the unglamorous world of wholesale insurance distribution, where relationships forged over decades matter more than algorithms, and where understanding risk isn't just math—it's an art form. The wholesale insurance brokerage business is perhaps the least sexy corner of finance. No flashing Bloomberg terminals, no IPO roadshows with champagne—just relationships, risk assessment, and the unglamorous work of finding coverage for risks that standard insurers won't touch. Yet this is precisely where Patrick Ryan chose to make his comeback, recognizing that the specialty insurance market was on the cusp of a generational transformation.

As of August 2025, Ryan Specialty Group has a market cap of $15.59 Billion USD, making it a remarkable success story that few saw coming. The company operates in the excess and surplus (E&S) lines market—essentially the insurance industry's island of misfit toys, where unusual, complex, or high-risk coverages find a home. Think cyber liability for cryptocurrency exchanges, coverage for music festivals, or protection for buildings in wildfire zones. These aren't your grandmother's homeowner's policies.

What makes this story particularly compelling is the timing. Ryan didn't just build another insurance brokerage; he architected a platform designed to capitalize on three converging megatrends: the hardening of insurance markets post-financial crisis, the explosion of new and emerging risks in a digital economy, and the generational transition of independent insurance agencies seeking succession solutions. It's a masterclass in reading market cycles and building for the long term.

This episode explores how relationships forged over six decades, deep industry expertise, and the patience to build rather than disrupt created one of the most successful insurance platforms of the 21st century. We'll examine the three-pillar business model that sets Ryan Specialty apart, dissect the aggressive M&A playbook that has fueled its growth, and understand why, in an age of InsurTech disruption, an octogenarian's relationship-first approach is winning.

The themes that emerge are timeless: the power of second acts in business, why industry expertise often trumps technological disruption, and how building enduring value through relationships can create compounding returns that algorithms can't replicate. As we'll see, sometimes the best innovations aren't about moving fast and breaking things—they're about understanding deeply and building deliberately.

II. The Patrick Ryan Origin Story & Aon Legacy

The year was 1962, and a young Patrick Ryan was hustling cars at Dick Fencl Chevrolet in suburban Chicago. But while his colleagues focused on moving metal, Ryan saw something different: an opportunity in the moments after the sale, when customers needed insurance for their new vehicles. He convinced Continental Casualty Company to let him sell insurance products right there in the dealership, creating what would become the first Finance and Insurance (F&I) department—a model that "forever changed how auto dealerships operate."

Think about that for a moment. Every time you've bought a car and been ushered into that back office for the insurance and warranty pitch? That was Patrick Ryan's innovation. From day one, he understood that distribution was everything in insurance, and that meeting customers where they already were could transform a business model.

By 1964, the 27-year-old Ryan had seen enough to know this was bigger than car dealerships. He founded Pat Ryan & Associates, initially just a small brokerage and underwriting agency. But Ryan had a gift for relationships and an intuitive understanding of risk that set him apart. Within four years, the firm was selling $15 million in premiums annually—serious money in 1968 dollars.

Then came the move that would define his career: Ryan borrowed heavily to acquire a dormant insurance company. This wasn't just about owning another asset; it gave him the ability to underwrite the products his company was selling. Suddenly, Pat Ryan & Associates wasn't just a broker—it was a full-stack insurance operation. The transformation was immediate and dramatic. By 1971, with $25 million in annual sales, Ryan took the company public. He was 34 years old.

The Aon story that followed reads like a business school case study in empire building. In 1982, Ryan Insurance Group merged with Combined International, with Ryan becoming CEO of the combined entity. Where others might have been content with regional success, Ryan had global ambitions. He renamed the company Aon in 1987—derived from the Gaelic word for "oneness"—signaling his vision of creating a unified global insurance powerhouse.

For 41 years, Ryan built Aon brick by brick, acquisition by acquisition, relationship by relationship. The company expanded through both organic growth and strategic acquisitions, eventually operating more than 500 offices in 120 countries. By his retirement in 2008, Aon was generating revenues exceeding $7 billion annually. Ryan had built one of the world's largest insurance brokerages from scratch, creating thousands of millionaires among his employees along the way.

Most people would have called it a career. Ryan was 73, wealthy beyond measure, with nothing left to prove. He'd revolutionized auto insurance, built a global empire, and secured his legacy as one of the titans of the insurance industry. Golf courses and philanthropy beckoned.

But 2008 was also the year of the financial crisis, and Ryan watched as the insurance industry convulsed. Traditional carriers pulled back from complex risks. The specialty insurance market—always a niche within a niche—suddenly became critical as standard markets couldn't handle the new risk landscape. Ryan saw an opportunity that perhaps only someone with his experience could fully appreciate: the chance to build a pure-play specialty insurance platform from scratch, unencumbered by legacy systems or traditional market obligations.

His vision was crystalline in its simplicity: create a specialty-only platform that would be to wholesale insurance what Amazon had become to retail—not through technology disruption, but through relentless focus on selection, service, and scale. No distractions from standard lines, no conflicts with retail brokers, just pure specialty expertise.

The insurance establishment thought he was crazy. Why would a 73-year-old billionaire want to start over? But they underestimated two things: Ryan's competitive drive and his understanding that the specialty insurance market was about to enter a golden age. As we entered the era of cyber risks, climate change, and emerging technologies, the need for specialty coverage would only grow. The question wasn't whether to build such a platform, but who had the relationships, expertise, and patience to do it right.

III. The Founding & Early Strategy (2010–2015)

Ryan Specialty opened its doors in 2010 with a simple premise: be the trusted trading partner for specialty risk solutions to retail agents, brokers, and insurance carriers. The timing was deliberate. The financial crisis had created a perfect storm of opportunity—distressed assets were available, talented professionals were looking for stability, and the hardening insurance market meant specialty coverage was more valuable than ever.

From the beginning, Ryan understood that this wasn't about building just another wholesale broker. The vision was to create a three-pillar platform that could capture value across the entire specialty insurance value chain. The first pillar, wholesale brokerage, would leverage relationships to help retail brokers place complex risks. The second, binding authority, would allow the firm to underwrite on behalf of carriers. The third, underwriting management, would provide full-service program administration. Each pillar would reinforce the others, creating a flywheel effect.

The first major move came with acquiring certain assets from Wells Fargo's American E&S Insurance Services. This wasn't just about adding revenue; it was about acquiring established relationships and proven talent in the excess and surplus lines space. Ryan knew that in specialty insurance, you don't just buy a book of business—you buy decades of expertise and trust that can't be replicated overnight. The early strategy was methodical: build trust first, scale second. Ryan knew that wholesale brokers lived and died by their reputations. A single blown placement or mishandled claim could destroy years of relationship building. So he recruited seasoned professionals who brought not just books of business but decades of credibility. The company's early hires read like an all-star team of specialty insurance veterans, many of whom had worked with Ryan at Aon and were willing to bet their careers on his vision.

Since 2010, RSG has completed 40 acquisitions in various specialties and geographies, with strategic bolt-on acquisitions adding scale and differentiating skills towards achieving the company's goals. Each deal was carefully selected not just for financial metrics but for cultural fit and strategic positioning. The company wasn't just buying revenue—it was assembling a mosaic of specialty expertise that would be nearly impossible for competitors to replicate.

The wholesale brokerage model itself deserves explanation, as it's often misunderstood even within the insurance industry. Retail brokers—the ones most businesses interact with directly—often encounter risks they can't place with standard carriers. Maybe it's a cannabis dispensary needing liability coverage, or a concert promoter insuring against weather cancellations. These retail brokers turn to wholesale specialists like Ryan Specialty, who have the expertise and carrier relationships to find coverage. The wholesale broker acts as an intermediary's intermediary, adding value through specialized knowledge and access.

What made Ryan's approach different was the integration of binding authority from day one. This meant the company could not only find coverage but actually underwrite and bind policies on behalf of carriers—a massive efficiency gain that eliminated layers of bureaucracy and accelerated placement times. In an industry where speed often meant the difference between winning and losing business, this was a crucial competitive advantage.

Culture became the invisible infrastructure holding everything together. Ryan instituted what he called the "One Team" philosophy—a direct contrast to the eat-what-you-kill mentality prevalent in many insurance brokerages. Producers were incentivized not just on their individual production but on the success of their teams and the broader organization. This created a collaborative environment where expertise was shared rather than hoarded, and where client relationships were viewed as firm assets rather than individual possessions.

By 2015, the foundation was set. The company had established itself as a serious player in the wholesale space, built out its three-pillar platform, and created a culture that could sustain aggressive growth. But Ryan knew that to achieve his vision of building the definitive specialty insurance platform, he would need more than organic growth. He would need capital, expertise, and a partner who understood the long game. That partner would come in the form of Onex Corporation, setting the stage for the next phase of explosive growth.

IV. Understanding the Business Model

To truly appreciate Ryan Specialty's success, you need to understand the elegant complexity of its business model. The company provides distribution, underwriting, product development, administration and risk management services by acting as a wholesale broker and a managing underwriter with delegated authority from insurance carriers. Think of it as a three-legged stool, where each leg reinforces the others, creating stability and leverage that pure-play competitors can't match.

The first leg, wholesale brokerage, is the company's heritage business and still its largest revenue generator. Here's how it works in practice: A retail broker in Denver has a client opening a chain of axe-throwing venues (yes, that's a real thing). Standard insurers won't touch it—too novel, too risky, no actuarial data. The retail broker calls Ryan Specialty, where a specialist who's placed similar risks knows exactly which carriers might be interested, how to structure the coverage, and what pricing makes sense. Ryan Specialty earns a commission from the carrier, typically 10-20% of the premium, without taking any underwriting risk.

The second leg, binding authority, takes this a step further. Instead of having to go back to carriers for approval on every risk, Ryan Specialty has pre-negotiated authority to bind coverage within certain parameters. This transforms the customer experience—what might have taken weeks can now happen in hours or even minutes. The company can quote, bind, and issue policies on the spot, capturing business that speed-sensitive competitors miss.

The third leg, underwriting management, is where things get really interesting. Here, Ryan Specialty essentially runs entire insurance programs on behalf of carriers. They handle everything from product development to claims management, earning fee income that's more stable and predictable than commission-based revenue. This is the highest-margin business, often generating EBITDA margins north of 40%.The E&S market has seen remarkable growth, with direct statutory premiums written reaching approximately $99 billion in 2022, nearly 9% of the total property/casualty (P/C) industry premium. Historically accounting for about 5% of total P/C premiums, the E&S market has expanded significantly since 2018. From 2018 to 2022, the market grew from under $30 billion to almost $100 billion in direct written premiums, marking five consecutive years of double-digit growth.

This explosive growth isn't just a cyclical uptick—it's a structural shift in how insurance gets distributed. Climate change, cyber risks, social inflation, nuclear verdicts—all these factors are pushing more business from admitted carriers to the E&S market. When State Farm won't write your California home insurance because of wildfire risk, or when traditional carriers balk at insuring a cryptocurrency exchange, that business flows to the E&S market through wholesalers like Ryan Specialty.

The beauty of Ryan Specialty's model is its capital-light nature. Unlike traditional insurers, the company takes no underwriting risk—it's purely a fee-based business. When a policy is placed, Ryan Specialty earns a commission. When a policy renews, they earn again. This creates remarkably predictable revenue streams with minimal capital requirements. The company doesn't need massive reserves or worry about catastrophic losses. It's essentially a toll booth on the highway of specialty insurance transactions.

But here's where it gets really interesting: operating leverage. Once you've built the infrastructure—the technology platforms, the carrier relationships, the underwriting expertise—incremental business drops almost straight to the bottom line. Adding another billion in premiums doesn't require proportionally more underwriters or office space. This is why Ryan Specialty's EBITDA margins have steadily expanded from the mid-20s to over 30%, with a clear path to 35% or higher.

The revenue model breaks down into three streams. Commissions from wholesale brokerage typically range from 10-20% of premiums placed. Binding authority generates similar commission rates but with faster turnaround times and higher retention. Underwriting management fees are often structured as a percentage of premiums plus performance bonuses, creating alignment with carrier partners. In aggregate, every dollar of premium flowing through the platform generates 15-20 cents of revenue for Ryan Specialty.

What's often misunderstood is how recession-resistant this model can be. During economic downturns, standard markets typically tighten, pushing more business to E&S markets. Hard markets mean higher premiums, which means higher commissions. Unlike traditional insurers who suffer when claims spike, Ryan Specialty actually benefits from market dislocations. It's a beautiful hedge against the very risks it helps place.

The network effects are powerful and compounding. The more retail brokers rely on Ryan Specialty, the more carriers want to work with them. The more carriers they represent, the more attractive they become to retail brokers. It's a virtuous cycle that becomes increasingly difficult for competitors to break. Scale begets scale in wholesale distribution.

V. The Private Equity Years & Scaling (2013–2021)

The pivotal moment came in June 2018, though not in the way many expected. Rather than selling the entire company to private equity, Ryan orchestrated something more clever: Onex Corporation invested $150 million of preferred equity and $25 million of common equity in Ryan Specialty Group. This wasn't a buyout—it was strategic growth capital with a sophisticated partner who understood the long game. Bobby Le Blanc, Senior Managing Director of Onex, saw what Ryan was building: "Pat is building an outstanding organization comprised of top talent from around the insurance industry and has established clear and ambitious, yet achievable goals." The investment provided capital to continue RSG's successful growth strategy and M&A activity, but more importantly, it brought institutional discipline and access to capital markets expertise that would prove invaluable.

The M&A machine kicked into high gear. Between 2013 and 2021, Ryan Specialty executed dozens of acquisitions, each carefully orchestrated to fill a strategic gap or add critical capabilities. The playbook was consistent: identify best-in-class operators in specific niches, pay fair prices, retain key talent, and integrate operations while preserving entrepreneurial culture. It wasn't about rolling up mediocre assets—it was about assembling an all-star team.

The crown jewel acquisition came in September 2020 with All Risks, Ltd. Formed in 1964, All Risks had grown from a one-office excess and surplus lines brokerage to a national wholesale broker, managing general agency, and program administrator with offices across the country and over 850 employees. The deal brought nearly $2.6 billion in premium to Ryan Specialty's platform, but more importantly, it brought 36 specialty programs, an industry-leading training platform in All Risks University, and deep relationships across the industry.

The timing of the All Risks acquisition was masterful. Announced in June 2020, in the depths of COVID uncertainty, Ryan saw opportunity where others saw risk. As Patrick Ryan explained, "The world has become a much riskier place, and our clients' needs have expanded. As hazards continue to evolve, they are becoming larger and more complex. Social inflation liability, cyber and transactional exposures, among a myriad of other emerging and ever-present unforeseen threats, require forward-thinking responses."

RT Specialty emerged as the wholesale brokerage powerhouse within the Ryan Specialty ecosystem. By combining Ryan Specialty's organic growth with All Risks' established platform, RT Specialty became the second-largest wholesale broker in the United States, trailing only AmWINS. The combined entity had roughly 3,300 employees and more than 70 offices across the United States, the United Kingdom, and Europe.

But scale alone doesn't explain the success. Ryan Specialty invested heavily in technology during these years, building what would become the RT Connector platform. This wasn't about disrupting the industry with Silicon Valley-style innovation—it was about making the complex simple. The platform allowed retail brokers to submit risks, receive quotes, and bind coverage in minutes rather than days. It was evolutionary, not revolutionary, and that's exactly what the market needed.

The integration playbook became a core competency. Unlike many PE-backed roll-ups that slash costs and destroy culture, Ryan Specialty took a different approach. New acquisitions kept their identities as specialized units within the broader platform. Leaders were retained and incentivized with equity. Back-office functions were centralized for efficiency, but front-office teams maintained their entrepreneurial spirit and client relationships.

According to its SEC filing for the IPO, RSG had become the second-largest U.S. property/casualty insurance wholesale broker and the third-largest U.S. property/casualty managing general agency and underwriter. Its distribution network had grown to more than 650 producers who had access to more than 15,500 retail insurance firms and over 200 excess and surplus lines carriers.

The numbers tell only part of the story. What Ryan and Onex had built was a platform effect—each acquisition made the next one more valuable. More specialty expertise meant more solutions for retail brokers. More volume meant better terms from carriers. Better technology meant faster service. It was a virtuous cycle that competitors struggled to replicate.

By early 2021, the company was generating over $1 billion in annual revenue with EBITDA margins approaching 30%. The business had scale, momentum, and a clear path to continued growth. The private equity playbook had worked, but not in the traditional slash-and-burn way. Instead, Ryan Specialty had used patient capital and disciplined execution to build something enduring. The stage was set for the next chapter: going public.

VI. The IPO Story (2021)

The IPO window opened in the spring of 2021, and Ryan Specialty was ready. Markets were frothy, SPACs were everywhere, and anything with recurring revenue was trading at nosebleed valuations. But Ryan didn't rush. The company had been preparing for this moment for years, with Onex's guidance proving invaluable in navigating the complexities of going public. Ryan Specialty announced the pricing of its initial public offering of 56,918,278 shares of its Class A common stock at a price to the public of $23.50 per share, before underwriting discounts and commissions, for gross proceeds of $1,337.6 million. At a midpoint of $23.50, this would raise net proceeds of up to $1.27 billion, equivalent to a $6.0 billion fully diluted market valuation for the wholesale broker and underwriting management specialist.

The structure was complex but elegant—an Up-C arrangement that allowed existing owners to maintain tax efficiency while giving public investors access to the growth story. In simple terms, the public would own economic interests in the business through a newly created corporation, while the founders and early investors retained their partnership interests with the ability to exchange them for public shares over time. It's a structure common in financial services IPOs, but one that requires sophisticated investors to understand.

The timing couldn't have been better. Total net commissions and fees had surged 34 percent in 2020 to $1.02 billion, including 32.4 percent growth to $673.1 million in wholesale brokerage. In the first quarter of 2021, there was even more significant growth as revenues surged to $311.5 million, including the impact of the All Risks acquisition. Q1 2021 revenue included organic growth of 18.4 percent—a staggering number for a business of this scale.

The roadshow was a victory lap for Patrick Ryan. At 84 years old, he was taking a company public for the second time in his career, this time with his sons Patrick Jr. and Mike actively involved in the business. Investors loved the story: recurring revenue, asset-light model, secular growth tailwinds, proven management, and a clear path to margin expansion. The company wasn't trying to disrupt insurance; it was perfecting it.

J.P. Morgan, Barclays, Goldman Sachs, and Wells Fargo Securities led the offering, with UBS, William Blair, RBC Capital Markets, BMO Capital Markets, and Keefe Bruyette Woods rounding out an all-star banking syndicate. The breadth of coverage signaled institutional confidence in the story. This wasn't a speculative tech IPO—it was a real business with real profits and a proven model.

The shares began trading on the New York Stock Exchange on July 22, 2021, under the ticker "RYAN"—a perfect symbol for a company so closely tied to its founder's legacy. The stock opened at $24.75, above the IPO price, and climbed steadily in early trading. For Patrick Ryan, it was vindication. The market understood and valued what he had built.

Post-IPO performance validated the thesis. The company continued its aggressive growth trajectory, with organic revenue growth consistently in the mid-to-high teens and margins expanding as promised. The public currency also enabled more strategic acquisitions, as sellers could now receive liquid stock rather than illiquid partnership interests.

What made the Ryan Specialty IPO particularly interesting was what it represented for the broader insurance industry. Here was a company that had succeeded not by trying to eliminate brokers with technology, but by empowering them with better tools and access. It was a reminder that in complex, relationship-driven industries, the winners are often those who perfect the existing model rather than those who try to destroy it.

The IPO also marked a transition for Onex, which began a gradual exit from its investment. Having more than tripled its money, Onex could declare victory while Ryan Specialty gained a more diverse shareholder base. The partnership had worked exactly as designed—patient capital enabling aggressive growth, culminating in a successful public offering.

VII. Modern Era & Strategic Evolution (2021–Present)

The public company era has been defined by acceleration rather than moderation. In 2024, Ryan Specialty Holdings's revenue was $2.46 billion, an increase of 21.17% compared to the previous year's $2.03 billion. Earnings were $94.67 million, an increase of 55.12%. These aren't the numbers of a mature company coasting on past success—they're the metrics of a business hitting its stride. The acquisition strategy has become more surgical and strategic. Take Griffin Underwriting Services, completed in January 2023. Founded in 1928, Griffin brought deep relationships with retail insurance brokers both in the Pacific Northwest and across the country. Griffin offers a broad array of solutions across various specialty insurance lines, including earthquake and transportation. Griffin's technical acumen and consistent underwriting results have attracted the support of numerous leading carriers. This wasn't just about adding $23 million in revenue—it was about strengthening the binding authority capabilities that differentiate Ryan Specialty from pure brokers.

The digital transformation has accelerated without abandoning the relationship-first ethos. The RT Connector platform has evolved into a comprehensive digital marketplace where retail brokers can access multiple carriers, compare quotes, and bind coverage in real-time. But unlike pure InsurTech plays that try to eliminate human interaction, RT Connector enhances rather than replaces the broker relationship. It's technology in service of expertise, not instead of it. Partnership strategies have become increasingly sophisticated. The exclusive distribution deal with AIG's Private Client Select (PCS) for high-net-worth business demonstrates the power of Ryan Specialty's platform. As Peter Zaffino, AIG's CEO, noted: "PCS's exclusive wholesale distribution partnership with Ryan Specialty is a major milestone for PCS and AIG and creates the ability to access the market with an industry leader in the wholesale segment." This isn't just distribution—it's strategic alignment between carriers seeking efficient distribution and Ryan Specialty's unmatched wholesale network.

International expansion has accelerated thoughtfully. Rather than planting flags globally, Ryan Specialty has followed its clients and opportunities into select markets. The UK and European operations, strengthened through acquisitions like Castel Underwriting Agencies, provide a platform for transatlantic business and access to Lloyd's of London—still the gold standard for specialty risks.

The company's approach to talent and culture in the modern era deserves special attention. While tech companies struggle with remote work policies and cultural fragmentation, Ryan Specialty has maintained its collaborative ethos while embracing flexibility. The company continues to attract top talent from competitors, often entire teams who see the opportunity to build something special within the Ryan Specialty platform.

Looking at the numbers, the story is one of consistent execution. Organic growth remains in the high single to low double digits—remarkable for a business of this scale. Margins continue to expand toward the stated goal of 35% EBITDA margins by 2027. The company generates substantial free cash flow, funding both acquisitions and returning capital to shareholders through share buybacks.

The strategic evolution continues with initiatives like the alternative risk business, addressing the growing demand for captive insurance solutions and other non-traditional risk transfer mechanisms. As risks become more complex and traditional insurance more expensive, these alternative solutions represent a significant growth opportunity.

What's remarkable about the modern era is how little the fundamental strategy has changed. Ryan Specialty isn't pivoting to become a tech company or trying to eliminate brokers with AI. Instead, it's doubling down on what works: deep expertise, strong relationships, strategic acquisitions, and operational excellence. In a world obsessed with disruption, Ryan Specialty's success comes from perfection of the existing model.

VIII. Playbook: Building in Specialty Markets

After dissecting Ryan Specialty's journey, clear patterns emerge that form a playbook for building dominant positions in specialty markets. These aren't abstract theories—they're battle-tested principles that have created billions in value.

The Power of Focus vs. Diversification

Ryan Specialty's unwavering focus on specialty lines stands in stark contrast to the diversification strategies pursued by many competitors. While others chase growth by expanding into personal lines, employee benefits, or wealth management, Ryan Specialty stays in its lane. This focus creates compounding advantages: deeper expertise, stronger carrier relationships, and unmatched credibility with retail brokers. When you're the acknowledged expert in placing hard-to-place risks, you become the first call, not the backup option.

Relationship Capital and the Insurance Trust Equation

In an industry where a handshake still means something, relationships aren't just important—they're everything. Ryan Specialty doesn't just maintain relationships; it cultivates them across generations. When Patrick Ryan started the company, he brought relationships dating back to the 1960s. Those connections opened doors that would have taken newcomers decades to unlock. But it goes deeper than personal relationships. It's about institutional trust—the confidence that comes from consistent execution over decades.

M&A as a Core Competency: Culture-First Integration

Most companies treat M&A as an occasional growth tactic. For Ryan Specialty, it's a core competency refined over 40+ acquisitions. The secret isn't financial engineering—it's cultural integration. New acquisitions keep their identity and entrepreneurial spirit while gaining access to Ryan Specialty's platform, technology, and carrier relationships. Leaders become equity partners, aligning long-term incentives. Back-office functions consolidate for efficiency, but client-facing teams maintain autonomy. This balance between standardization and independence is delicate but crucial.

Technology as an Enabler, Not a Disruptor

While InsurTech startups promised to eliminate brokers with algorithms, Ryan Specialty took a different approach: use technology to make brokers more effective. The RT Connector platform doesn't try to replace human judgment in complex risk assessment—it accelerates the mundane parts of the process. Quote comparison, submission management, policy issuance—these can be automated. But understanding a client's unique risk profile, structuring appropriate coverage, and negotiating with carriers? That still requires human expertise. Technology amplifies expertise rather than replacing it.

Managing Through Insurance Cycles

Insurance is cyclical, alternating between hard markets (rising prices, restricted capacity) and soft markets (falling prices, abundant capacity). Many brokers suffer in soft markets as commission income falls with premiums. Ryan Specialty's model provides natural hedges. In hard markets, higher premiums drive higher commissions. In soft markets, more business flows to E&S lines as admitted carriers compete aggressively for standard risks. The managing general underwriter business provides steady fee income regardless of market conditions. This diversification within specialty lines smooths earnings without diluting focus.

The Importance of Delegated Authority and Binding Capabilities

Having binding authority transforms the customer experience and competitive position. Instead of going back to carriers for every quote, Ryan Specialty can provide immediate answers. In a world where speed often determines who wins the business, this capability is invaluable. But binding authority isn't given lightly—it requires deep carrier trust built over years of profitable underwriting. Once established, it becomes a powerful moat that new entrants can't quickly replicate.

Building a Platform for the Next Generation

Perhaps most impressively, Ryan Specialty has solved the succession challenge that plagues many founder-led companies. Patrick Ryan may be the patriarch, but the company isn't dependent on him. Tim Turner, who joined in 2010 as President, has emerged as a capable operator. The next generation of leadership is already in place, with clear succession planning at every level. This isn't just about replacing individuals—it's about institutionalizing the culture and capabilities that make Ryan Specialty special.

The playbook ultimately comes down to patient building rather than quick flipping. It's about compound growth through hundreds of small improvements rather than betting everything on one big disruption. It's old-fashioned in some ways—relationships matter, expertise counts, trust takes time to build. But it's also thoroughly modern in its use of technology, data, and scale to create competitive advantages. Most importantly, it's proven to work, creating enormous value for all stakeholders.

IX. Competition & Market Dynamics

The competitive landscape in wholesale insurance brokerage resembles a heavyweight boxing match where the combatants know each other's moves intimately. Ryan Specialty faces formidable competitors, each with their own strengths and strategies.

Brown & Brown stands as perhaps the most direct competitor, with its wholesale division generating substantial revenue through RT Specialty's primary rivals. Their acquisition strategy mirrors Ryan Specialty's in many ways, but with a broader focus that includes retail operations. This diversification provides stability but potentially dilutes focus on specialty lines.

Amwins remains the 800-pound gorilla of wholesale distribution, the largest player in the space with deep carrier relationships and broad market coverage. Their scale advantages are real—better terms from carriers, wider geographic coverage, and the ability to handle the largest, most complex placements. Yet their size may also be a weakness, making them less nimble and potentially less entrepreneurial than Ryan Specialty.

CRC Group, backed by private equity, represents another well-capitalized competitor pursuing an aggressive growth strategy. Their focus on technology and digital initiatives positions them as a modern alternative, though questions remain about whether technology alone can overcome Ryan Specialty's relationship advantages.

The competitive dynamics are shaped by several macro forces. First, the hardening market that began in 2019 continues to drive business to wholesale brokers as standard markets tighten. Climate change, social inflation, cyber risks, and economic uncertainty all push more risks into the E&S market where wholesale brokers operate. This rising tide lifts all boats, but execution still determines who captures the most value.

The Hardening Market Tailwind and Sustainability

The current hard market represents one of the longest and most sustained in recent memory. Unlike previous cycles driven by catastrophic events, this hardening stems from structural factors: years of underpricing risk, social inflation driving up jury awards, and emerging risks that traditional actuarial models struggle to price. This suggests the tailwind supporting E&S growth may persist longer than typical cycles.

Threats from InsurTech and Digital Disruption

The InsurTech threat that seemed so menacing in 2018-2020 has largely failed to materialize. Companies like Lemonade and Root promised to eliminate brokers with AI and behavioral economics. Instead, they've discovered what industry veterans always knew: insurance is complicated, regulation is complex, and earning trust takes time. Most InsurTechs have either failed, pivoted to enabling traditional players, or accepted that distribution through brokers remains essential.

That said, digital innovation remains a real force. New MGAs powered by technology can achieve profitability faster than traditional players. Data analytics enable better risk selection and pricing. Digital distribution platforms reduce friction in the placement process. Ryan Specialty has responded by partnering with or acquiring innovative firms rather than viewing them as threats.

Climate Change as Both Risk and Opportunity

Climate change fundamentally reshapes the insurance landscape. Traditional carriers pull back from catastrophe-exposed areas, creating opportunities for E&S markets. New risks emerge—from supply chain disruptions to stranded assets—that require specialty solutions. Ryan Specialty benefits from this disruption as a distributor, without taking the underwriting risk that challenges carriers.

Yet climate change also poses risks. If losses become truly unpredictable or catastrophic, even E&S markets may struggle to provide capacity. Regulatory responses to climate risk could reshape the industry in unpredictable ways. The company's success depends on markets remaining functional, even if disrupted.

Regulatory Considerations and State-by-State Complexity

Insurance remains regulated at the state level in the U.S., creating 50 different regulatory regimes with varying rules, rates, and requirements. This complexity favors incumbents like Ryan Specialty who have already built the infrastructure to navigate this maze. New entrants, particularly technology companies accustomed to uniform national markets, often underestimate this challenge.

Recent regulatory trends actually favor Ryan Specialty's model. As admitted carriers face increasing regulatory scrutiny and rate pressure, more business flows to E&S markets where pricing flexibility remains. The NAIC's efforts to modernize surplus lines regulation through initiatives like the Nonadmitted Insurance Model Act have generally made interstate E&S transactions easier, benefiting wholesale brokers.

The competitive landscape ultimately favors scaled players with deep expertise. While new entrants will continue to emerge and technology will evolve, the fundamental dynamics of specialty insurance—complexity, relationships, and trust—create lasting advantages for established players. Ryan Specialty's position as the pure-play specialty leader, combined with its culture of innovation and execution, positions it well for continued success regardless of competitive pressures.

X. Bull vs. Bear Case

Bull Case: The Compounding Machine

The bull case for Ryan Specialty starts with the secular growth in E&S lines. As standard markets become increasingly selective and new risks emerge faster than traditional carriers can adapt, the E&S market's share of total P&C premiums continues to expand. From 5% in 2018 to nearly 9% of the total property/casualty (P/C) industry premium in 2022, this isn't a cyclical blip—it's a structural shift.

Operating leverage is just beginning to show its power. With EBITDA margins expanding from the mid-20s to over 30%, and a clear path to 35% by 2027, incremental revenue increasingly drops to the bottom line. The beauty of the wholesale brokerage model is that once you've built the infrastructure, additional volume requires minimal incremental investment. This isn't a capital-intensive business requiring constant reinvestment—it's a cash flow machine.

The M&A pipeline remains robust with hundreds of potential targets. The insurance brokerage space remains highly fragmented, with thousands of small specialty brokers and MGAs that would benefit from Ryan Specialty's platform. As baby boomer owners seek succession solutions, Ryan Specialty offers an attractive option: immediate liquidity, continued autonomy, and participation in future upside through equity rollover. The company's acquisition machine is well-oiled and disciplined, creating value through both strategic fit and operational improvement.

Market share gains continue to accelerate. Despite being the second-largest wholesale broker, Ryan Specialty still has only a single-digit share of the wholesale market. The company consistently grows faster than the market, taking share from smaller competitors who lack scale advantages and larger ones who lack focus. The combination of organic growth and acquisitions creates a compounding effect that's difficult for competitors to match.

Technology investments are beginning to pay dividends. The RT Connector platform and other digital initiatives improve efficiency, enhance customer experience, and create switching costs. While not flashy, these incremental improvements compound over time, widening the moat around Ryan Specialty's business.

Bear Case: The Risks Beneath the Surface

The bear case begins with founder risk and succession questions. Patrick Ryan is 87 years old. While succession planning appears solid with Tim Turner and other executives in place, losing the founder's relationships, vision, and deal-making ability could impact growth and culture. The insurance industry is built on trust, and that trust is often personal rather than institutional.

The insurance cycle will eventually turn. Hard markets don't last forever. When pricing softens and capacity returns to admitted markets, E&S premiums could contract. While Ryan Specialty has navigated soft markets before, it hasn't faced a prolonged soft market as a public company with quarterly earnings pressure. Commission income is directly tied to premiums—when premiums fall, revenues fall proportionally.

Integration risks from aggressive M&A could emerge. With 40+ acquisitions since 2010, there's always risk that cultural integration fails, key talent leaves, or synergies don't materialize. The company's decentralized model preserves entrepreneurial spirit but may also harbor inefficiencies or inconsistencies that become problematic at scale.

Competition is intensifying from multiple angles. Private equity continues to pour capital into insurance brokerage, funding new competitors and consolidation among existing ones. Large retail brokers are building their own wholesale capabilities. MGAs are going direct to retail brokers, potentially disintermediating wholesalers. While Ryan Specialty has defended against these threats so far, the competitive moat may be narrower than it appears.

Valuation at premium multiples leaves little room for error. Trading at elevated multiples to both earnings and book value, the stock price embeds high growth expectations. Any stumble—a missed quarter, a failed acquisition, a key departure—could trigger multiple compression. For a business that's ultimately tied to insurance market cycles, paying growth multiples may prove risky.

The Balanced View

The truth likely lies between these extremes. Ryan Specialty has built a remarkable business with real competitive advantages and attractive financial characteristics. The secular growth trends are real, the execution has been excellent, and the market opportunity remains vast. However, the company isn't immune to insurance cycles, competitive pressures, or execution risks.

The key question for investors isn't whether Ryan Specialty is a good business—it clearly is. The question is whether the current valuation adequately compensates for the risks while providing attractive upside potential. That depends on one's view of insurance market cycles, the sustainability of E&S growth, and the company's ability to execute its strategy over the long term.

XI. What Would We Do?

If we were running Ryan Specialty today, several strategic opportunities and imperatives would top our agenda.

International Expansion Opportunities

The international opportunity is massively underpenetrated. While Ryan Specialty has operations in the UK and Europe, these represent a small fraction of total revenue. The global specialty insurance market is multiples larger than the U.S. market, yet cultural, regulatory, and competitive differences make expansion challenging. We would pursue a targeted strategy: follow existing clients internationally, partner with local brokers rather than competing directly, and focus on truly global risks that require coordinated placement across multiple jurisdictions. London remains the global hub for specialty insurance—deepening the Lloyd's relationships and potentially establishing a syndicate could provide unique advantages.

Building vs. Buying Technology Capabilities

The technology question is nuanced. Ryan Specialty doesn't need to become a technology company, but it needs world-class technology capabilities. We would pursue a hybrid strategy: build core platforms that provide competitive advantage (like RT Connector), buy proven solutions for commoditized functions, and partner with InsurTechs for emerging capabilities. The key is maintaining control over the customer experience while leveraging external innovation where appropriate.

Vertical Integration Considerations

The temptation to integrate vertically—perhaps by acquiring an insurance carrier—should be resisted. Ryan Specialty's value comes from independence and the ability to access multiple markets for clients. Owning a carrier would create channel conflict and compromise the company's positioning as a trusted intermediary. However, selective integration into adjacent services—claims advocacy, risk consulting, or data analytics—could add value without creating conflicts.

Human Capital and Next Generation Leadership

The most critical challenge is ensuring continuity of culture and capability as the founder generation retires. We would implement a formal mentorship program pairing senior leaders with high-potential employees. Create "tiger teams" of emerging leaders to work on strategic initiatives. Expand equity participation deeper into the organization to align incentives and retain talent. Most importantly, document and institutionalize the relationship networks that drive the business—client relationships can't be dependent on individual producers.

The Succession Planning Imperative

Succession planning needs to extend beyond the C-suite to every key relationship and capability. This means identifying single points of failure throughout the organization and developing redundancy. It means creating formal transition plans for major client relationships. It means building institutional knowledge management systems so expertise doesn't walk out the door when people retire. The goal is to transform Ryan Specialty from a founder-led company to an institution that endures for generations.

We would also explore strategic options that might seem counterintuitive. Consider taking the company private again if market valuations become disconnected from fundamental value—the business model is ideally suited for private ownership given its predictable cash flows and long-term investment horizon. Explore strategic partnerships with carriers to co-create new products rather than just distributing existing ones. Invest more aggressively in data and analytics to move from reactive risk placement to proactive risk prevention.

The overarching priority would be maintaining the delicate balance that makes Ryan Specialty special: entrepreneurial but disciplined, aggressive but prudent, relationship-driven but technology-enabled, focused but flexible. It's harder than it sounds, but that's exactly why it's valuable.

XII. Lessons & Takeaways

The Power of Second Acts in Business

Patrick Ryan's story demolishes the myth that entrepreneurial energy diminishes with age. At 73, when most executives are perfecting their golf game, Ryan saw an opportunity to build something perhaps even greater than Aon. His second act demonstrates that experience, relationships, and wisdom can trump youthful energy. The key insight: industries ripe for disruption aren't always disrupted by outsiders with new models—sometimes they're transformed by insiders who deeply understand what needs to change and, more importantly, what shouldn't.

Why Industry Expertise Trumps Disruption

The InsurTech boom of the late 2010s was supposed to eliminate brokers and transform insurance distribution. Billions in venture capital funded startups promising to revolutionize the industry. Most failed or pivoted. Why? Because insurance is complex, regulated, and ultimately about trust—things that can't be coded away. Ryan Specialty succeeded not by disrupting the industry but by perfecting it. Deep expertise allowed them to identify inefficiencies and fix them without destroying the underlying value creation mechanisms. The lesson: in complex, regulated industries, evolution beats revolution.

Building Enduring Value Through Relationships

In an age of digital transformation and automated everything, Ryan Specialty's success reaffirms an ancient truth: relationships matter. But not the superficial networking kind—deep, trust-based relationships built over decades. These relationships create switching costs that no technology can overcome. When a retail broker needs to place a difficult risk, they call the wholesaler they trust, not the one with the best app. Building and maintaining these relationships requires patience, consistency, and genuine value creation—qualities that can't be growth-hacked or disrupted.

The Compounding Effect of Disciplined M&A

Ryan Specialty's 40+ acquisitions demonstrate that successful M&A isn't about financial engineering or cost synergies—it's about strategic fit and cultural integration. Each acquisition made the platform more valuable, creating a compounding effect. The discipline to walk away from bad deals, the patience to cultivate relationships before transactions, and the wisdom to preserve entrepreneurial culture post-acquisition—these are the differentiators. The lesson: in fragmented industries, disciplined consolidation can create enormous value, but only if executed with strategic clarity and operational excellence.

Creating Alignment Through Ownership Structures

The Up-C structure, equity participation for acquired company leaders, and broad-based employee ownership create powerful alignment mechanisms. When producers own equity, they think like owners, not employees. When acquired companies roll equity, they're invested in long-term success, not just the initial purchase price. This ownership mentality permeates the culture, driving behaviors that maximize long-term value rather than short-term commissions. The lesson: structure drives behavior, and equity alignment remains one of the most powerful tools for building enduring businesses.

The ultimate takeaway from Ryan Specialty's story is that building exceptional businesses doesn't require revolutionary innovation or disruptive technology. Sometimes, the biggest opportunities lie in taking a good business model and executing it exceptionally well. In Ryan Specialty's case, that meant combining deep industry expertise, patient capital, disciplined execution, and a relentless focus on serving customers better than anyone else.

XIII. Recent News**

Latest Quarterly Earnings and Guidance**

Ryan Specialty reported EPS of $0.66, beating the forecast of $0.65. Revenue reached $855.2 million, surpassing the expected $832.02 million. The Q2 2025 results demonstrated continued strength, with total revenue growth of 23% fueled by organic revenue growth of 7.1%, substantial contributions from M&A which added 13 percentage points to the top line, and contingent commissions across all three specialties.

However, challenges emerged in the property insurance market. The company saw a rapid decline in property pricing throughout June, which resulted in the organic growth number of 7.1% falling short of expectations. Management is no longer expecting stabilization or modest improvement in the back half of the year, now reflecting the same trends from June continuing for the remainder of the year and resulting in a modest decline in property for the full year of 2025.

Recent Acquisition Announcements

The company continues its aggressive M&A strategy with several strategic acquisitions in 2024-2025. The USQRisk acquisition, completed in May 2025, brought specialized alternative risk capabilities. The Velocity Risk Underwriters acquisition expanded transportation insurance expertise. Most recently, the acquisition of J.M. Wilson in July 2025 strengthened the company's position in specific niche markets.

Executive Changes and Board Updates

Leadership continuity remains strong with Tim Turner firmly established as CEO and Patrick Ryan continuing as Executive Chairman. The company has made strategic hires in key growth areas, particularly in alternative risk and reinsurance, positioning for future expansion.

Market Developments and Industry Trends

The E&S market continues its structural growth story, though with some moderation. Property insurance markets are softening faster than expected, while casualty lines remain relatively stable. The company is adapting by focusing more on casualty lines and expanding into alternative risk solutions where demand remains robust.

Analyst Coverage and Rating Changes

Wall Street remains generally positive on Ryan Specialty, with most analysts maintaining Buy ratings despite near-term headwinds. According to InvestingPro analysis, the company is currently trading below its Fair Value, with analysts setting price targets ranging from $63 to $90. The consensus view is that temporary market challenges don't diminish the long-term growth story.

XIV. Links & Resources

Ryan Specialty Investor Relations Materials - Official Investor Relations Site: ir.ryanspecialty.com - SEC Filings: SEC EDGAR Database - RYAN - Annual Reports and Proxy Statements - Quarterly Earnings Presentations and Webcasts

Industry Reports and E&S Market Studies - WSIA (Wholesale & Specialty Insurance Association) Market Reports - S&P Global Market Intelligence E&S Insurance Reports - AM Best Surplus Lines Market Reviews - Conning Research on Specialty Insurance Markets

Patrick Ryan Interviews and Speeches - Insurance Journal Executive Interviews - WSIA Conference Keynotes - Northwestern Kellogg School Case Studies - Chicago Business Hall of Fame Induction Speech

Insurance Trade Publication Coverage - Insurance Journal - Business Insurance Magazine - The Insurance Insider - Reinsurance News - Risk & Insurance Magazine

Competitor Analysis and Benchmarking - Brown & Brown Investor Relations - Amwins Company Information - CRC Group Market Updates - Marsh McLennan Public Filings

Books on Insurance Industry and Aon History - "The Man from Mayberry: Patrick G. Ryan and the Remaking of American Business" (if published) - "Against the Gods: The Remarkable Story of Risk" by Peter L. Bernstein - "The Invisible Bankers" by Andrew Tobias

Academic Papers on Specialty Insurance Markets - Journal of Risk and Insurance - NBER Working Papers on Insurance Markets - Wharton Insurance and Risk Management Research

Regulatory Filings and Documents - NAIC (National Association of Insurance Commissioners) Reports - State Insurance Department Filings - Lloyd's of London Market Reports

Podcast Episodes and Video Content - Insurance Speak Podcast Episodes - WSIA Marketplace Conference Recordings - Bloomberg and CNBC Interview Segments

Northwestern University Case Studies - Kellogg School of Management Case Studies on Aon - Northwestern Alumni Association Features on Patrick Ryan - Chicago Booth Insurance Industry Research

Note: This analysis is based on publicly available information and does not constitute investment advice. Ryan Specialty Group is a complex business operating in dynamic markets, and potential investors should conduct their own due diligence and consult with financial advisors before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube