Rexford Industrial Realty: The Pure-Play Southern California Industrial Sharpshooter

I. Introduction & Episode Roadmap

Picture a map of the United States, and zoom into Southern California. Trace the coastline from the Ports of Los Angeles and Long Beach—together handling roughly 31% of all containerized waterborne trade entering America—and follow the arteries of commerce inland: the I-710, the I-10, the endless grid of warehouses and distribution centers that keep the world's fifth-largest economy humming. Now imagine owning 51 million square feet of that irreplaceable real estate, scattered across more than 420 properties in neighborhoods where new development is nearly impossible and land hasn't been rezoned for industrial use in decades.

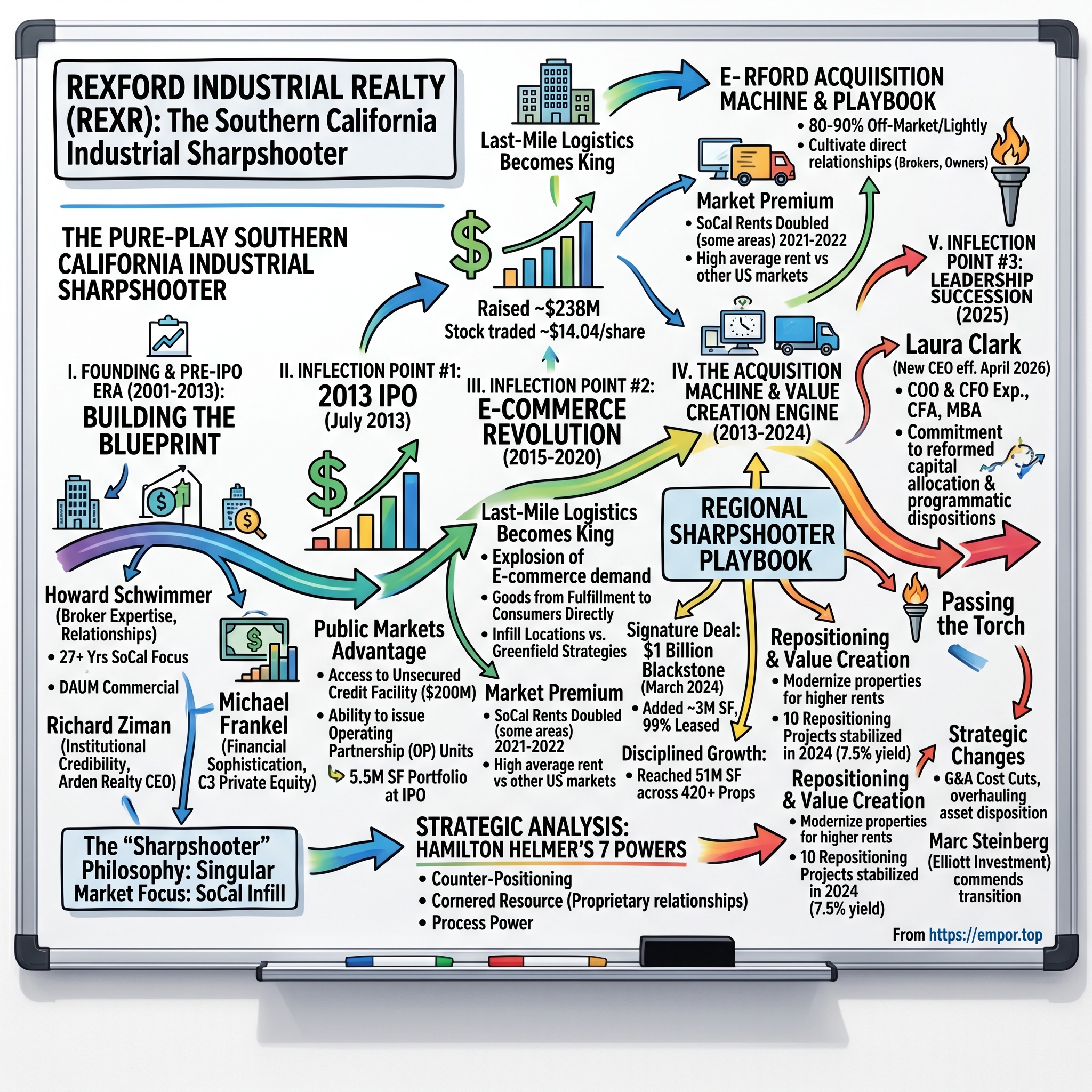

This is the empire that Howard Schwimmer and Michael Frankel built over more than two decades. As co-founders, they drove Rexford's growth from 5.5 million square feet of industrial property, with an equity market capitalization of $406 million at the time of their 2013 IPO, into an irreplaceable, best-in-class, 51-million-square-foot industrial property portfolio with a nearly $10 billion equity market capitalization today. Over the same period, the Rexford team grew annual revenue to nearly $1 billion.

The central question of the Rexford story is deceptively simple: How did a hyper-focused regional REIT become the dominant owner in America's most supply-constrained industrial market? While competitors like Prologis spread across four continents, Rexford made a contrarian bet that depth would beat breadth—that knowing every broker, every block, every quirk of Southern California's Byzantine zoning codes would compound into an unassailable competitive advantage.

The answer lies in understanding four intertwined themes: geographic focus as a competitive moat, the e-commerce revolution that transformed industrial real estate into the hottest asset class in commercial property, the superiority of infill over greenfield strategies in constrained markets, and the power of specialized expertise that takes decades to accumulate. Rexford didn't just ride these tailwinds—it positioned itself at the nexus of all four.

This is the story of a "regional sharpshooter" that outmaneuvered global giants, a case study in how strategic focus can generate outsized returns, and a look at what happens when that sharpshooter faces its first real leadership transition while navigating the most challenging industrial market conditions in years.

II. Setting the Stage: Why Southern California Industrial Real Estate Matters

The Fourth Largest Industrial Market in the World

Before understanding Rexford, one must first understand the theater in which it operates. Rexford Industrial creates value by investing in, operating and redeveloping industrial properties throughout infill Southern California, the world's fourth largest industrial market and consistently the highest-demand with lowest-supply major market in the nation over the long term.

Southern California's industrial market benefits from a massive population base of 18 million people and a staggering GDP of $1.6 trillion—an economy that rivals major European nations. If it were a country, California would have the world's 11th-largest economy. This isn't just any industrial market; it's a logistics hub of global significance positioned as the gateway between Asia and the American consumer.

The scale of commerce flowing through Southern California defies comprehension. When data for the Port of Los Angeles is combined with the Port of Long Beach, the two ports handled approximately 31% of all containerized international waterborne trade in the U.S. Los Angeles County is the second-largest industrial market in the U.S., with 948 million square feet of space.

The neighboring ports of Los Angeles and Long Beach have attracted substantial attention as a surge in imports during the COVID-19 pandemic continues unabated. Increased shipments have translated to long lines of container ships anchored off the coast of Southern California and similar congestion within each port and at adjacent warehouses as the area's logistical infrastructure operates near maximum capacity.

This is precisely why Rexford's geographic focus matters. This is an interesting location because it is right next to one of the largest ports in the United States. Vacancy rates in the markets Rexford serves have historically been well below the average for other important U.S. markets. Supply of new warehouses is low because there is little available land to build on, so rent growth is expected to be well above the U.S. average for industrial space for the foreseeable future.

The Structural Supply Constraint Story

What makes Southern California industrial real estate fundamentally different from most other markets comes down to a single word: scarcity. Unlike the Inland Empire, where developers can still find parcels on the fringes, or Phoenix, where desert land awaits conversion, the core infill markets of Los Angeles and Orange County are functionally built out. This isn't a temporary condition—it's a permanent structural constraint that gets more acute with each passing year.

The dynamics are remarkably simple to understand yet nearly impossible to replicate elsewhere. California's regulatory environment, particularly regarding zoning and environmental restrictions, makes industrial development extraordinarily difficult. Assembly Bill 98, approved by the California State Legislature in late August and signed into law by Governor Gavin Newsom in September, is a response to the vast surge of warehouse development throughout the state and its accompanying baggage, like noise, traffic and diesel emissions. The law attempts to push new industrial development away from more populated areas by requiring that projects be built on major roads rather than residential streets, and introducing stringent regulations on large projects near "sensitive receptors" such as homes, hospitals, day cares and schools.

Commencing January 1, 2026, any proposed new or expanded logistics use development 250,000 square feet or more where the loading bay is within 900 feet of a sensitive receptor must include all Tier 1 21st century warehouse design elements, orient truck loading bays on the opposite side of the logistics use development away from sensitive receptors, and locate truck loading bays a minimum of 300 feet from the property line.

These regulations create what analysts call a "barrier to entry" moat—but that understates the protection. As panelists at a recent NAIOP conference noted, "The uncertainty in the market because of AB 98 has impacted the valuation of land and existing assets. Land that had once been valuable and had potential for future industrial development has been negatively affected because AB 98 would now impose increased costs. Alternatively, existing infill sites could become more valuable as development slows. In that scenario, it would be preferable to be a property owner rather than a developer."

This regulatory tightening benefits established owners like Rexford while making it nearly impossible for new competitors to build their way into the market. Each new restriction makes existing industrial inventory more valuable and harder to replicate.

Understanding this supply-constrained environment explains why Rexford has been able to generate extraordinary rent growth even in challenging periods. Nationwide, industrial rents increased 18% in 2021, followed by an even more impressive 26% in 2022 based on analysis from Green Street Advisors. In some of the hottest markets (e.g., Southern California), rents more than doubled over the same period. While that growth has moderated, the embedded mark-to-market opportunity remains substantial.

III. Founding & Pre-IPO Era: Building the Blueprint (2001–2013)

Howard Schwimmer's Vision

The story of Rexford Industrial begins not with a spreadsheet or an investment thesis, but with a career steeped in the unglamorous minutiae of Southern California industrial real estate. Howard Schwimmer didn't just know the market—he had lived it for decades before founding what would become one of the most successful specialized REITs in American history.

From May 1983 until November 2001, Mr. Schwimmer, a licensed California real estate broker, served at various times as manager, executive vice president and broker of record for DAUM Commercial Real Estate, one of California's oldest industrial brokerage companies. DAUM founded Los Angeles' first commercial real estate brokerage firm in 1904, a venture that was instrumental in bringing more than 6,500 companies into the fledgling Los Angeles market and helping the city grow into one of the most commercially and culturally relevant marketplaces in the world.

Those 18 years at DAUM gave Schwimmer something no amount of capital could buy: relationships. In the fragmented world of industrial real estate, where deals are often done off-market between parties who've known each other for decades, these connections would prove invaluable. Mr. Schwimmer's forty-one year professional career has been dedicated entirely and exclusively to Southern California infill industrial real estate, including its acquisition, value-add improvement, management, sales, leasing and disposition.

According to Schwimmer in a Wall Street Transcript interview: "I co-founded Rexford in 2001 with Richard Ziman, who today is the Chairman of our public company."

Richard Ziman brought a different kind of credibility to the venture. Richard Ziman is Co-Founder and Chairman of Rexford Industrial Realty, one of Southern California's leading owners and operators of infill industrial real estate and he was also Founder Chairman and CEO of New York Stock Exchange Arden Realty, Inc. which was the largest owner of office space in Southern California until its $5 billion merger with General Electric (GE), the largest single real estate transaction in the history of Southern California.

The partnership was strategic: Schwimmer brought deep operational expertise and brokerage relationships; Ziman brought institutional credibility and capital-raising prowess. Together, they would build a platform that combined boots-on-the-ground market knowledge with sophisticated financial engineering.

Enter Michael Frankel

Mr. Frankel has served as the Chief Financial Officer of Rexford Industrial Realty & Management Inc. since May 2005 and as Managing Partner of Rexford Industrial LLC and Rexford Sponsor LLC since December 2007 and September 2010, respectively.

Frankel's background was markedly different from Schwimmer's—less brokerage relationships, more institutional finance. Mr. Frankel was previously responsible for investments at the private equity firm "C3," a subsidiary of the Comcast Corporation. Mr. Frankel also served with LEK Consulting, providing strategic advisory services to several of the world's leading investment institutions. Mr. Frankel began his career as Vice President at Melchers & Co., a European-based firm, where he was responsible for Melchers' U.S.-Asia operations, principally based in Beijing.

This combination—Schwimmer's market intimacy paired with Frankel's financial sophistication—created a leadership team that could both source deals that competitors couldn't see and structure them in ways that maximized returns. Mr. Frankel's career includes 20 years co-managing Rexford's predecessor and current businesses, which have exclusively focused on investing in infill Southern California industrial real estate.

The "Sharpshooter" Philosophy Takes Shape

In the pre-IPO years, Schwimmer and Frankel developed what would become Rexford's defining strategic orientation: singular Market Focus: The early and unwavering commitment to exclusively target Southern California infill industrial properties. This wasn't a constraint born of necessity—it was a deliberate choice that shaped everything from hiring to deal sourcing to capital allocation.

Mr. Schwimmer has exclusively focused on Southern California industrial real estate for more than 27 years and has extensive expertise in the areas of property acquisition, development, value-add repositioning, management, sales and leasing. Mr. Schwimmer has demonstrated a successful track record of acquiring, repositioning, developing, leasing, selling and adding value to more than 27 million square feet of industrial properties.

By 2013, the predecessor entities had assembled a portfolio of approximately 5.5 million square feet across multiple private investment funds. The strategy was already working. The question was whether to remain private or access the public markets to accelerate growth.

IV. Inflection Point #1: The 2013 IPO

Going Public

On July 24, 2013, Rexford Industrial Realty transformed from a private investment vehicle into a publicly traded REIT. On July 24, 2013, the Company consummated its IPO, issuing 16,000,000 shares of its common stock in exchange for net proceeds of approximately $202.8 million after the underwriting discount and offering expenses. On August 21, 2013, the Company issued a total of 451,972 shares of its common stock, pursuant to a partial exercise by the underwriters of their over-allotment option, in exchange for proceeds of approximately $5.9 million net of the underwriting discount.

The Los Angeles, CA-based company plans to raise $224 million by offering 16 million shares at a price range of $13 to $15. At the midpoint of the proposed range, Rexford Industrial Realty would command a market value of $353 million.

The 2013 IPO was a pivotal funding event, raising approximately $238 million in net proceeds, fueling its initial growth phase as a public entity.

What did investors get for their money? The Company owns interests in 61 properties with approximately 6.7 million rentable square feet and manages an additional 20 properties with approximately 1.2 million rentable square feet. A modest portfolio by industry standards, but one positioned in what Rexford believed was the most attractive industrial market in America.

Why Public Markets Changed Everything

The decision to go public wasn't primarily about prestige or liquidity for founders—it was about competitive advantage. We believe our recent IPO and public company capital structure enhance our ability to achieve our growth objectives within our target 1.6 billion square-foot infill Southern California industrial markets.

The advantages of public capital became immediately apparent. In connection with the IPO, on July 24, 2013 the Company entered into a $200 million unsecured revolving credit facility with a July 24, 2016 maturity date. Borrowings under the facility bear interest at LIBOR plus a margin, based upon the Company's leverage ratio, of 135 to 205 basis points.

For a company competing against private equity funds and family offices for deals, access to a revolving credit facility and the ability to issue equity on demand represented a significant edge. More importantly, the REIT structure enabled Operating Partnership (OP) unit transactions—a tax-efficient acquisition currency that allows sellers to defer capital gains by exchanging property for OP units rather than cash. In a market where many properties are held by long-time family owners with low cost bases, this capability opened doors that remained closed to cash-only buyers.

Early Operating Performance

The early results validated the thesis. Quarterly NOI for our Same Property Portfolio increased 19.0% and Cash NOI for our Same Property Portfolio increased 14.6% compared to the third quarter of 2012. Same Property Portfolio occupancy increased 5.7 percentage points to 87.3% compared to the third quarter of 2012.

The growth trajectory was swift. Year-to-date, including the Yorba Linda and The Park acquisitions completed subsequent to the end of the third quarter, the Company has acquired 8 properties, with a total of 1.1 million square feet, for an aggregate investment of $111.1 million.

At its IPO, the company's stock traded around $14.04 per share in 2013. If you had invested $1,000, you could have bought approximately 71 Rexford Industrial Realty stock shares. This means a total return of 318.9% since the IPO. In comparison, the S&P 500 total return for the same period is 270.19%.

V. Inflection Point #2: The E-Commerce Revolution (2015–2020)

Last-Mile Logistics Becomes King

The years following Rexford's IPO coincided with one of the most significant structural shifts in retail history: the explosion of e-commerce. What had been a niche channel became mainstream, and the implications for industrial real estate were profound.

Traditional retail required inventory to flow from manufacturers to distribution centers to retail stores, with consumers making the final mile themselves. E-commerce inverted this model: goods now had to travel from fulfillment centers directly to consumers' doors, often within 48 hours or less. This seemingly simple change revolutionized the value proposition of industrial real estate near population centers.

For industrial real estate, the continued increase in e-commerce sales should bolster demand. E-commerce accounted for 15.9% of the total retail sales in the United States in the first half of 2024 and is projected to total $1.22 trillion by the close of 2024—an increase of nearly 11% over 2023. The market will continue growing at a compound annual growth rate (CAGR) of 8.99% until 2029 and reach $1.88 trillion.

Rexford's portfolio, concentrated in infill locations near the 18-million-person consumer base of Southern California, was ideally positioned. The company's focus on smaller, multi-tenant industrial properties—rather than massive big-box logistics centers—aligned perfectly with fragmented e-commerce demand.

Rexford Industrial is even more concentrated, with a portfolio of 100% infill Southern California. The company points out that it operates exclusively in areas where the average rent is more than 80% higher than the average of the next five highest U.S. markets.

Why Infill Wins

The geographic premium for infill locations became increasingly apparent as e-commerce matured. A warehouse in Riverside might be 60 miles from downtown Los Angeles; a property in Vernon or Commerce is minutes away. When Amazon, FedEx, and UPS began promising same-day and next-day delivery, that difference became decisive.

Southern California exemplifies the attributes we find attractive in our nationwide outlook with strong demand and barriers to new entrants. As such, we've been increasing our position in Rexford, a 100% focused Southern California industrial REIT.

Nationwide, industrial rents increased 18% in 2021, followed by an even more impressive 26% in 2022 based on analysis from Green Street Advisors. In some of the hottest markets (e.g., Southern California), rents more than doubled over the same period.

The COVID Accelerant

The pandemic reshaped the industrial market. During COVID-19, supply chain disruptions led companies to stockpile inventory, skyrocketing demand for warehousing space. As experts explained, prices surged during this period, but the market is now leveling off.

What happened in 2020-2022 represented an acceleration of trends that were already in motion. Consumers who might have taken years to adopt e-commerce shifted overnight. Companies that had operated lean just-in-time supply chains suddenly needed buffer inventory. And industrial landlords in supply-constrained markets like Southern California found themselves in an extraordinary position: demand was surging while new supply remained physically constrained.

Rexford Industrial, a 100% Southern California industrial REIT, had a lease mark-to-market over 50% as of 12/31/23. If we assume ~15% of the portfolio expires annually and the non-expiring portion of the portfolio has 3% annual escalators, cash revenue growth would be +10.1% per year without any additional market rent growth.

VI. The Acquisition Machine: Scaling Through Disciplined Growth (2013–2024)

The "Regional Sharpshooter" Playbook

What distinguishes Rexford from other industrial REITs isn't just where it operates—it's how it sources deals. In a competitive market where institutional investors throw billions at industrial assets, Rexford has consistently accessed transactions that never reach the broader market.

The company frequently describes its approach as the "regional sharpshooter" strategy—a term that captures both the geographic precision and the deal-sourcing advantage that comes from deep local relationships. Unlike national platforms that rely on investment banking processes and marketed deals, Rexford cultivates direct relationships with property owners, brokers, and local investors who might not want the uncertainty of a public sale process.

Rexford Industrial's proprietary sourcing advantage and value add expertise continue to deliver accretive current and long-term portfolio cash flow growth within infill Southern California, the nation's lowest-supply and highest-demand industrial market.

The off-market sourcing capability has proven remarkably consistent. The company regularly reports that 80-90% of acquisitions come through off-market or "lightly marketed" transactions—deals where Rexford either had exclusive access or competed against only a handful of bidders rather than dozens.

Year-by-Year Growth Trajectory

The numbers tell the story of disciplined, sustained growth. In 2022, the Company announced the acquisition of ten industrial properties for an aggregate purchase price of $336.2 million, bringing full year 2022 acquisitions to $2.4 billion total.

For full year 2024, the company completed nine acquisitions for an aggregate purchase price of $1.5 billion and sold five properties for an aggregate sales price of $44.3 million. Net income attributable to common stockholders reached $262.9 million, or $1.20 per diluted share. Company share of Core FFO was $511.7 million, an increase of 15.0% as compared to the prior year.

Same Property Portfolio NOI increased 4.1% and Same Property Portfolio Cash NOI increased 7.1% as compared to the prior year. Average Same Property Portfolio occupancy was 96.6%. Comparable rental rates increased by 38.9% compared to prior rents on a net effective basis and by 28.6% on a cash basis on 8.1 million rentable square feet of new and renewal leases.

The Signature Deal: $1 Billion Blackstone Acquisition (March 2024)

In March 2024, Rexford completed what stands as one of the largest industrial portfolio transactions in Southern California history—a $1 billion acquisition from Blackstone that added nearly 7% to the company's square footage in a single transaction.

Rexford Industrial acquired approximately 3 million square feet of industrial properties pursuant to separate transactions with Blackstone Real Estate, including the Blackstone Property Partners strategy as well as Blackstone Real Estate Partners and Blackstone Real Estate Income Trust, for an aggregate purchase price of $1.0 billion. The combined portfolio comprises 48 properties, totaling 3,008,000 square feet, acquired for $1.0 billion or $332 per square foot on average. The combined portfolio is 98% leased, with 99% of the property square footage located within core, infill submarkets in Los Angeles and Orange counties.

The deal is among Southern California's largest by total price for industrial properties of the past year. Industrial portfolio deals over $1 billion have been rare overall since Blackstone's $13.4 billion acquisition of an 839-property portfolio from investment firm GLP in September 2019.

Rexford Industrial Realty has bought 3 million square feet of industrial properties in Southern California from Blackstone in a whopping $1 billion deal, adding almost 7 percent of square footage to its portfolio.

The deal demonstrated both Rexford's access to institutional-quality deal flow and its ability to execute complex transactions quickly. The deal is expected to generate a weighted average initial unlevered cash yield of 4.7% and an anticipated stabilized unlevered cash yield of 5.6%. Rexford Industrial funded the purchase using proceeds from its recent exchangeable senior note offerings and cash on hand.

VII. The Repositioning & Value Creation Engine

Beyond Acquisitions: The Internal Growth Machine

What separates Rexford from a simple property aggregator is its systematic approach to value creation within its existing portfolio. The company doesn't just buy buildings and collect rent—it actively repositions, redevelops, and modernizes properties to capture higher rents and attract higher-quality tenants.

For the full year 2024, the Company stabilized ten repositioning and redevelopment projects totaling 826,442 square feet, representing a total investment of $288.6 million. The projects achieved a weighted average unlevered stabilized yield on total investment of 7.5%.

This 7.5% yield on repositioning investments compares favorably to the 4.7-5.6% yields on external acquisitions—and it comes with lower execution risk since the properties are already owned and the local market dynamics are well understood.

During the fourth quarter of 2024, the Company rent commenced and stabilized three repositioning projects totaling 375,965 square feet, representing a total investment of $123.5 million. The projects achieved a weighted average unlevered stabilized yield on total investment of 6.2%.

Rental Rate Growth Outperformance

Even as Southern California's industrial market normalized from its pandemic-era peaks, Rexford continued to generate substantial rent increases on lease renewals. This reflects both the quality of the portfolio's locations and the embedded mark-to-market opportunity from leases signed years ago at lower rates.

Rexford executed 3.3 million square feet of leases in Q3 2025 with net effective rent increases of 26.1% on comparable leases.

The persistence of these double-digit rent spreads, even as market conditions softened, demonstrates the structural advantage of owning irreplaceable infill assets. Tenants may negotiate harder on new leases, but they have few alternatives when their leases expire—there simply isn't new competitive supply being delivered in most of Rexford's submarkets.

VIII. Financial Performance & Capital Discipline

The Numbers Tell the Story

In 2024, Rexford Industrial Realty's revenue was $936.41 million, an increase of 17.37% compared to the previous year's $797.83 million. Earnings were $262.87 million, an increase of 15.57%.

The progression from IPO to today is remarkable. The company went from approximately $60 million in annual revenue at the time of its IPO to approaching $1 billion in trailing twelve-month revenue—a compound annual growth rate exceeding 25%.

Company share of Core FFO per diluted share was $2.34, an increase of 6.8% as compared to the prior year. Consolidated Portfolio NOI was $711.8 million, an increase of 17.3% as compared to the prior year.

In Q3 2025, the company continued to deliver solid results: Net income attributable to common stockholders of $87.1 million, or $0.37 per diluted share, as compared to $65.1 million, or $0.30 per diluted share, for the prior year quarter. Company share of Core FFO of $141.7 million, an increase of 9.0% as compared to the prior year quarter. Company share of Core FFO per diluted share of $0.60, an increase of 1.7% as compared to the prior year quarter. Total Portfolio NOI of $188.9 million, an increase of 2.9% as compared to the prior year quarter.

Balance Sheet Strength

The company ended the year with a low-leverage balance sheet measured by a net debt-to-enterprise value ratio of 26.5% and net debt to Adjusted EBITDAre of 4.6x.

Rexford ended Q3 2025 with $1.6B total liquidity, $3.3B outstanding debt at a 3.7% average interest rate and Net Debt/Enterprise Value of 23.2%.

This conservative balance sheet provides significant flexibility for opportunistic acquisitions during periods of market distress while maintaining investment-grade credit metrics.

Dividend Growth Track Record

Rexford Industrial Realty, Inc. (REXR) has increased its dividends for 10 consecutive years.

Subsequent to year end, declared a quarterly common stock dividend of $0.43 per share, an increase of 3.0%. Subsequent to year end, authorized a $300 million share repurchase program.

Rexford Industrial Realty has an annual dividend of $1.72 per share, with a yield of 4.11%. The dividend is paid every three months.

IX. Inflection Point #3: Leadership Succession (2025)

Passing the Torch

In November 2025, Rexford announced the most significant leadership transition in its history. Laura Clark, Rexford Industrial's Chief Operating Officer, will serve as Chief Executive Officer effective April 1, 2026, and was appointed as a member of the Company's Board of Directors effective November 17, 2025. Ms. Clark will succeed Michael Frankel and Howard Schwimmer, both of whom will depart from their roles as Co-CEOs effective March 31, 2026.

Tyler Rose, Chairman of the Board of Directors, said, "This transition is the culmination of the Board's multi-year succession planning process that will ensure a seamless handoff of leadership responsibilities. The Board is confident that Laura is the right executive to lead the Company through the execution of its go-forward strategy."

The transition comes at a pivotal moment. The leadership change follows New York-based hedge fund Elliott Investment's newfound status as one of Rexford's top five shareholders. Elliott Partner Marc Steinberg commended the transition and other significant strategy changes—which will include re-evaluating the REIT's development pipeline to focus on "highest return opportunities," overhauling its asset disposition program, and continuing general and administrative cost cuts that began in 2025.

Laura Clark's Background

Ms. Clark is a recognized real estate executive with more than two decades of finance and operational experience in the industry. She joined Rexford Industrial as Chief Financial Officer in 2020 and was appointed Chief Operating Officer in 2024. Prior to joining Rexford Industrial, Ms. Clark held various leadership positions at Regency Centers, a publicly-traded retail REIT. Additionally, she held leadership roles across various institutions in real estate capital markets, equity research and investment management.

Clark is a Chartered Financial Analyst (CFA), holds a Bachelor of Science degree in finance from DePaul University in Chicago and earned her Master of Business Administration degree from Ball State University.

The incoming CEO has articulated a clear set of priorities. "I am committed to a reformed capital allocation strategy that aligns with market conditions and our cost of capital, with a clear focus on maximizing risk-adjusted returns and our per-share NAV," said Laura Clark. "Our near-term priority is maximizing returns through a programmatic disposition strategy that strengthens the quality of our future cash flows and recycles capital into high-yielding repositioning projects and share repurchases."

Looking forward to 2026, the Company expects to realize an additional $20 million to $25 million of net G&A savings following the CEO leadership transition at the end of the first quarter. Full year 2026 G&A is projected to be in the range of $57 million to $62 million. These savings are expected to reduce G&A as a percentage of revenues to below the Industrial REIT peer average of 6.2%.

X. Porter's Five Forces & Strategic Analysis

Threat of New Entrants: LOW

The barriers to entry in Rexford's target markets are formidable and growing more so. California's Assembly Bill 98 (AB 98), signed into law on September 29, 2024, is reshaping the way industrial buildings are designed and operated. The legislation aligns industrial activities with California's decarbonization and sustainability objectives while addressing environmental and community health concerns. Mandatory standards for industrial and logistics facilities over 100,000 square feet, applicable to new developments and expansions, effective January 1, 2026. Cities and counties must align their truck route planning and zoning regulations by January 1, 2028.

AB 98 prescribes different standards depending on the size of the proposed project and the project's current zoning. Developments of 250,000 square feet or more, must comply with Tier 1 21st Century Warehouse design elements, orient loading bays on the opposite side of the building from sensitive receptors, have a separate entrance for heavy-duty trucks. If the project is currently zoned industrial, all truck loading bays must be setback 300 feet from any property line abutting a sensitive receptor. If the project is not zoned industrial or requires a rezone, loading bays must be setback at least 500 feet and must include at least 100 feet of landscape buffering.

Beyond regulation, the fundamental constraint is land availability. Unlike markets where developers can expand outward, Los Angeles and Orange County are geographically bounded by ocean, mountains, and already-developed residential communities. The industrial land that exists is what was zoned decades ago—and that inventory has been steadily shrinking as some parcels convert to higher-value uses.

Bargaining Power of Suppliers: LOW

Rexford's "supplier" relationships primarily involve construction contractors, property managers, and maintenance providers. The company's internal capabilities and diversified contractor base minimize dependency on any single provider. More importantly, as an acquirer rather than a developer, Rexford faces less construction risk than peers focused on ground-up development.

Bargaining Power of Tenants: LOW-MODERATE

This is where the structural supply constraint manifests most directly. Rent growth has slowed considerably—which is a small victory for tenants, until one remembers that those seeking to renew or relocate will be paying a 40% to 60% premium over their pre-pandemic rental rates.

While tenants have gained some leverage as the market normalized from pandemic peaks, Rexford's infill locations offer limited alternatives. A company needing last-mile distribution near Los Angeles' population centers has few options beyond the existing building stock.

"Overall, market vacancy is about 5 percent, and importantly, when you drill down and look at the high-quality, well-located product that's comparable to our portfolio, that market vacancy is substantially lower," Frankel said during the latest earnings call.

Competitive Rivalry: MODERATE

Prologis, Inc. is a real estate investment trust headquartered in San Francisco, California that invests in logistics facilities. The company was formed through the merger of AMB Property Corporation and Prologis in June 2011, which made Prologis the largest industrial real estate company in the world. As of 2025, the company operates more than 15,000 land acres and over 6,000 buildings comprising about 1.3 billion square feet in 20 countries across North America, Latin America, Europe, and Asia.

While Prologis has operations across four continents, Rexford is basically focused on just one U.S. state. With a roughly-$11 billion market cap, Rexford is much smaller than Prologis but is still one of the largest REITs in the sector.

Rexford's strong industry position is largely thanks to its laser-like focus on just one market, the exact opposite of Prologis' approach.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Moderate. Rexford benefits from scale in property management and tenant relationships, but industrial real estate lacks the winner-take-all dynamics of some industries.

Network Effects: Limited. Unlike a marketplace or platform business, owning more industrial buildings doesn't directly make each building more valuable.

Counter-Positioning: Strong. Rexford's geographic focus represents a strategic choice that national competitors cannot easily replicate without abandoning their diversification advantages. Prologis cannot become "Southern California only" without unwinding its global platform.

Switching Costs: Moderate. While tenants face costs in relocating operations, industrial leases are typically 5-7 years—meaningful stickiness but not permanent lock-in.

Branding: Limited. Industrial real estate is a B2B business where tenant decisions are driven by location and economics rather than brand preference.

Cornered Resource: Strong. This is perhaps Rexford's most powerful advantage. The company's proprietary relationships with brokers, sellers, and local market participants represent an intangible asset built over decades. This specialization allowed for deep market knowledge and relationship advantages in one of the world's tightest and most dynamic industrial markets.

Process Power: Moderate. Rexford's repositioning capabilities and off-market sourcing represent embedded organizational knowledge that improves with experience.

XI. The Bull and Bear Cases

The Bull Case

Structural supply constraints intensify. AB-98 and similar regulations make new development increasingly difficult, enhancing the value of existing industrial inventory. Land that had once been valuable and had potential for future industrial development has been negatively affected because AB 98 would now impose increased costs. Alternatively, existing infill sites could become more valuable as development slows.

Embedded rent growth materializes. The mark-to-market opportunity from below-market leases provides years of organic NOI growth even without market rent appreciation. With average lease terms of 5-7 years, roughly 15% of the portfolio comes up for renewal annually at substantially higher rates.

E-commerce penetration continues. At 16% of retail sales, e-commerce has significant runway for growth. Each percentage point increase drives incremental demand for last-mile distribution space in infill markets.

Port traffic remains robust. Southern California's position as the gateway to Asia should sustain logistics demand regardless of short-term trade tensions. Port volumes entering Southern California have regained share against the Gulf of Mexico and East Coast ports. Safety issues around the Suez and drought conditions in Panama have further solidified Southern California's position.

Leadership transition preserves strategy while improving execution. Laura Clark's focus on G&A reduction and capital allocation discipline could enhance shareholder returns while maintaining the core infill focus.

The Bear Case

Southern California industrial softness persists. In Q3 2025, the overall vacancy rate in Los Angeles industrial market climbed to 4.8%, up 10 basis points quarter-over-quarter and 40 bps YOY, the highest level seen in the past decade.

The move follows more than a year of cooling tenant demand in Southern California's industrial market, where vacancy has climbed to 6.4% in the fourth quarter from a historic low of 1.7% in early 2022, according to CoStar data.

Trade tensions disrupt port volumes. Tariffs on Chinese imports and supply chain diversification could shift logistics flows away from West Coast ports toward alternative entry points.

Interest rates remain elevated. Higher rates compress cap rates and make acquisitions less accretive while increasing borrowing costs for the company's floating-rate debt.

Geographic concentration becomes a liability. What functions as an advantage in good times could prove problematic if Southern California-specific risks materialize—whether from natural disasters, regulatory changes, or regional economic weakness.

Leadership transition creates execution risk. While planned and orderly, the departure of founders who built the company's proprietary sourcing relationships could impact deal flow.

XII. Key Performance Indicators for Investors

For long-term investors monitoring Rexford's ongoing performance, three KPIs deserve particular attention:

1. Net Effective Rent Spreads on Comparable Leases

This metric captures the embedded value creation as below-market leases roll to current rates. Spreads in the 20-40% range indicate that the mark-to-market opportunity remains intact; declining spreads would suggest the portfolio is catching up to market and organic growth is moderating.

2. Same Property NOI Growth

This metric strips out the impact of acquisitions to show how the existing portfolio is performing. Consistent mid-single-digit growth demonstrates the value of infill locations; negative same-store performance would signal market stress impacting even the best-positioned assets.

3. Off-Market Deal Sourcing Percentage

Rexford's competitive advantage depends on accessing deals that competitors cannot. If the percentage of acquisitions sourced off-market declines meaningfully, it could indicate that the company's proprietary relationships are weakening or that capital allocation is shifting toward marketed deals.

XIII. Conclusion: The Next Chapter

Rexford Industrial Realty stands at an inflection point. The founders who built the company from a 5.5-million-square-foot portfolio to a 51-million-square-foot empire are stepping back. The industrial market that carried the company to extraordinary returns has normalized from pandemic-era peaks. And activist investors are now among the largest shareholders, bringing new pressures for capital discipline and operational efficiency.

Yet the structural advantages that made Rexford successful remain intact. Southern California's 1.6-billion-square-foot industrial market remains the largest and most supply-constrained in the nation. The embedded rent growth from below-market leases provides years of organic NOI expansion. And the relationships and local knowledge accumulated over more than two decades cannot be easily replicated.

"We're proud of the Rexford team that has enabled the Company's entrepreneurial approach to creating value, and we're excited about Rexford's ongoing opportunity to create significant value for shareholders," stated departing Co-CEOs Michael Frankel and Howard Schwimmer.

The question for investors is whether Laura Clark and the next generation of leadership can maintain what made Rexford special—the sharpshooter's precision, the operator's discipline, the deep market intimacy—while adapting to changed market conditions and new capital allocation priorities.

As of September 30, 2025, Rexford Industrial's high-quality, irreplaceable portfolio comprised 420 properties with approximately 50.9 million rentable square feet occupied by a stable and diverse tenant base.

What began as a contrarian bet on geographic focus over global diversification has been vindicated by more than a decade of market-beating returns. Whether the next decade proves equally rewarding will depend on factors both within management's control—operational execution, capital allocation, cost discipline—and beyond it: trade flows, e-commerce growth, interest rates, and the regulatory environment in California.

For investors who believe in the durability of Southern California's logistics infrastructure and the irreplaceability of infill industrial real estate, Rexford remains the purest expression of that thesis. For those more skeptical, the current market normalization and leadership transition create obvious points of concern.

Either way, the Rexford story illuminates a broader truth about competitive advantage in real estate: sometimes the sharpshooter beats the shotgun. Sometimes depth beats breadth. And sometimes, knowing every block of a single market matters more than having a presence on every continent.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube