Aedifica: Building Europe's Healthcare Real Estate Empire

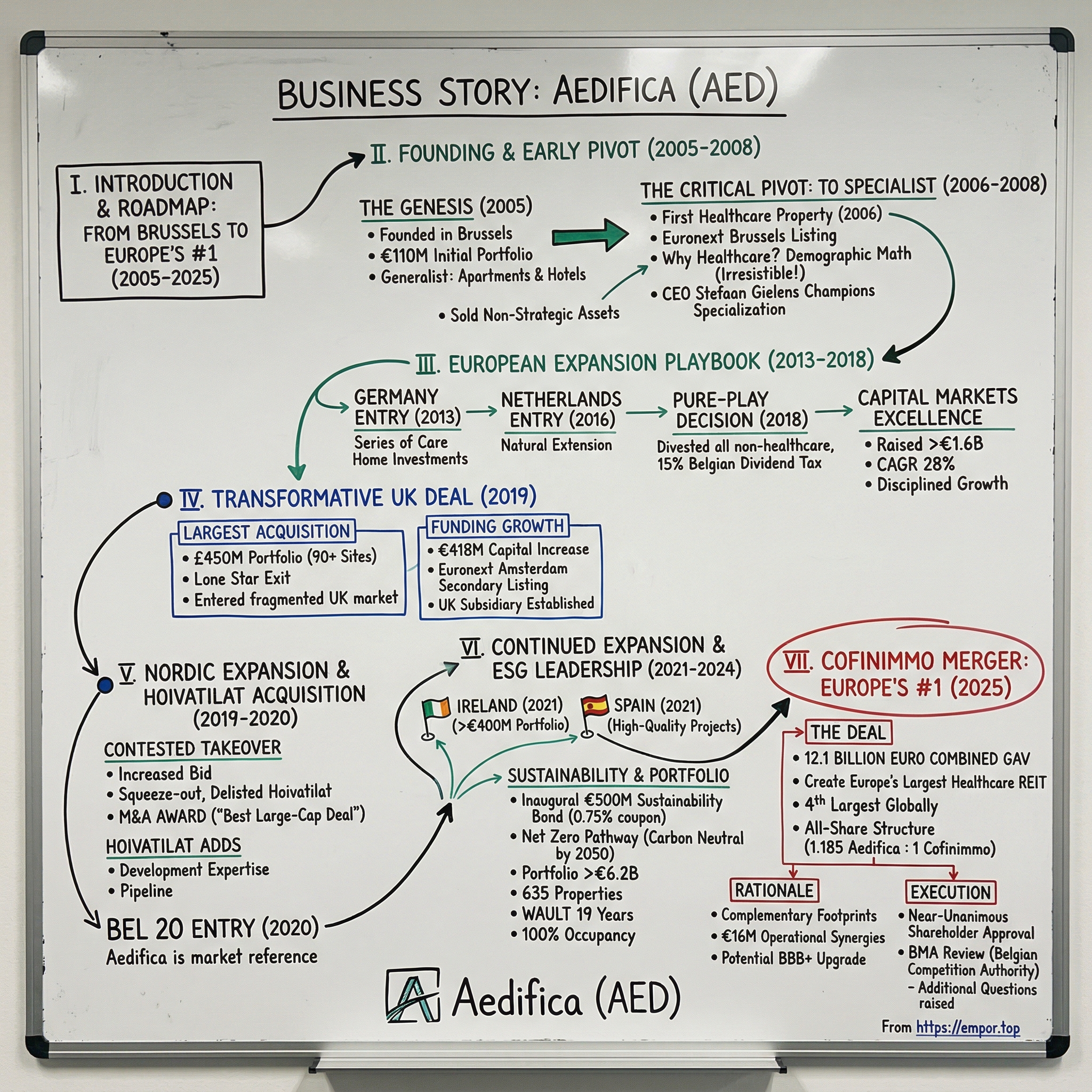

I. Introduction & Episode Roadmap

Picture a November evening in Brussels in 2005. In a modest office not far from the European Quarter, a small team finalizes paperwork for what they hope will become Belgium's newest real estate investment company. When Aedifica took its first steps on 7 November 2005, its 110-million-euro portfolio was entirely invested in apartment buildings and hotels. Twenty years later, that same company stands at the precipice of creating Europe's largest healthcare REIT through a €12.1 billion merger—a transformation so remarkable it belongs in a business school case study about specialization, timing, and disciplined capital allocation.

Belgian healthcare real estate firms Aedifica and Cofinimmo announced plans to merge, creating what they say will be Europe's largest real estate investment trust (REIT) and the fourth largest globally, with a combined gross asset value of €12.1 billion ($13.8 billion).

How does a company grow from €110 million to €12 billion in two decades? The answer lies at the intersection of demographic inevitability, strategic clarity, and relentless execution. By 2060 more than 10% of the European population will be over 80 years old, healthcare real estate will be in high demand for the next 40 years. Aedifica didn't just spot this megatrend—they built an entire company around it.

Aedifica is a Regulated Real Estate Company under Belgian law specialised in European healthcare real estate, particularly in elderly care. Aedifica has developed a portfolio of approx. 615 sites in Belgium, Germany, the Netherlands, the United Kingdom, Finland, Ireland and Spain, worth approx. 6.2 billion.

Aedifica is listed on Euronext Brussels (2006) and Euronext Amsterdam (2019). Since March 2020, Aedifica is part of the BEL20, the leading share index of Euronext Brussels. The company joined the BEL ESG index in 2023, cementing its position as a sustainability-focused leader in European real estate.

This article traces Aedifica's evolution across four distinct phases: the founding and pivotal decision to specialize (2005-2008); the European expansion playbook (2013-2018); the transformative UK and Nordic deals (2019-2020); and the culminating Cofinimmo merger (2025). Along the way, we'll examine the business model mechanics, competitive dynamics, and key investor metrics that define success in healthcare real estate.

What emerges is a masterclass in patient capital deployment backed by an unstoppable demographic tailwind.

II. The Founding & Early Pivot (2005-2008)

The Genesis

Belgium in 2005 offered fertile ground for ambitious real estate entrepreneurs. The country's REIT framework—known locally as a "Regulated Real Estate Company" or RREC—provided tax advantages and regulatory credibility that attracted capital. Aedifica has far fewer years on the counter. It was founded at the end of 2005 and went public one year later.

The company was founded on November 7, 2005 and is headquartered in Brussels, Belgium. At founding, Aedifica was a generalist property investor—hardly unusual for the era. The initial portfolio of €110 million comprised residential apartments and hotels, bread-and-butter assets that any Belgian REIT might own.

What made the founding team unusual was their willingness to question the generalist approach almost immediately. Within twelve months of going public, Aedifica began acquiring its first healthcare properties. The 2006 timeline shows Aedifica's listing on Euronext Brussels and first investments in healthcare real estate.

The Critical Pivot: From Generalist to Specialist

The transformation happened faster than anyone anticipated. Three years later, healthcare real estate already represented Aedifica's most important real estate segment. By 2008, what had started as opportunistic diversification had become the company's defining thesis.

Why healthcare? The demographic math was irresistible. Europe's population was aging faster than facilities could be built. Specialized care homes required significant capital investment that operators—focused on caregiving—preferred to lease rather than own. And the regulatory complexity of healthcare created barriers to entry that would protect well-positioned investors.

Care providers are further expanding and adapting their activities. Private and public operators increasingly rely on private investors to fund healthcare real estate infrastructure that meets the changing needs of society.

The decision to abandon generalist investing—selling apartments and hotels to concentrate on healthcare—represented Aedifica's first major inflection point. Management recognized that specialization created compounding advantages: deeper operator relationships, refined underwriting expertise, and investor clarity that attracted capital at lower costs.

This pivot wasn't merely strategic—it was existential. A small Belgian REIT competing with larger diversified players had limited paths to differentiation. By focusing exclusively on healthcare, Aedifica could build capabilities that general investors would find nearly impossible to replicate.

We have a track record of entering new markets and rapidly creating a platform for further growth. Aedifica acquired its first Belgian care homes in 2006.

Stefaan Gielens, who has served as CEO since February 2006, championed this specialist approach from the beginning. Mr. Stefaan Gielens has performed the duties of Chief Executive Officer for the Company since 1 February 2006. He is chairman of the Management Committee. His office as CEO and chairman of the Management Committee is of indefinite duration.

Prior to this, Stefaan Gielens was the Managing Director at Almafin Real Estate (KBC group) from October 2002 to January 2006. Stefaan Gielens holds a master's degree in law from KU Leuven.

Gielens' legal background proved useful in navigating the complex regulatory landscapes across multiple jurisdictions. His tenure spanning nearly two decades created continuity rare in public company leadership—a stability that operators valued when considering multi-decade lease commitments.

By 2008, Aedifica had established the playbook that would define its next fifteen years: find aging demographics, build local teams, cultivate operator relationships, and deploy capital through long-term triple-net leases. The foundation was set. Now came the hard work of scaling it across Europe.

III. The European Expansion Playbook (2013-2018)

Germany: The First International Market (2013)

If Belgium proved the concept, Germany would test its scalability. Europe's largest economy presented both enormous opportunity and operational complexity—different regulations, different operator relationships, different cultural expectations around elder care.

In 2013, the Group started its first activities outside Belgium with a series of investments in German care homes.

The German market offered compelling fundamentals. With over 84 million inhabitants in September 2024, Germany is the most populous country in the European Union. However, its fertility rate of 1.596 children per woman in 2020 is very low. A shrinking workforce supporting a growing elderly population created structural demand for care facilities that would only intensify over time.

Aedifica's approach in Germany became the template for all subsequent expansions: establish a local subsidiary with experienced professionals who understood regional operator needs, build credibility through smaller initial investments, then scale rapidly once relationships proved durable.

Aedifica SA holds a German subsidiary Aedifica Asset Management GmbH, which advises and supports the Company in the development and management of its real estate portfolio in Germany.

Netherlands Entry (2016)

In 2016, we moved to the Netherlands and from 2019 onwards, we stepped up our efforts and set foot in the United Kingdom, Finland and Sweden.

The Netherlands represented a natural extension—geographic proximity to Belgium, similar healthcare structures, and strong rule of law protecting property rights. By now, Aedifica had refined its due diligence processes and understood how to evaluate operator creditworthiness across different regulatory regimes.

The Pure-Play Decision (2018)

Eight years after pivoting toward healthcare, Aedifica made the commitment total. Another ten years later, in 2018, the Group divested all non-strategic segments and developed into a pure-play healthcare real estate investor.

This wasn't mere portfolio cleanup—it was a statement of conviction. By eliminating diversification, Aedifica accepted concentration risk in exchange for unmatched sector expertise. For Belgian investors, there was also a tax incentive: Because Aedifica invests more than 60% in healthcare real estate, the Belgian tax authorities only have to pay a 15% dividend tax. For Cofinimmo this is 30%.

The pure-play positioning attracted ESG-focused capital increasingly seeking healthcare exposure without the complexity of diversified REITs. It also forced competitors to decide whether to follow—creating strategic clarity throughout the industry.

Capital Markets Excellence

Growth of this magnitude required constant access to capital. To finance this growth, we called on our existing shareholders and new investors a number of times. Since 2010, Aedifica has raised more than 1.6 billion euro in seven capital increases.

We have never failed to meet our ambitions: in 15 years' time we have expanded our portfolio with a compound annual growth rate of 28%.

That 28% CAGR tells the story of disciplined growth—not frenzied acquisition, but systematic expansion backed by equity raises that preserved balance sheet strength. Management understood that healthcare real estate investing is a marathon, not a sprint. Overleveraging for short-term growth would undermine the multi-decade lease commitments that defined their business model.

By 2018, Aedifica had transformed from a €110 million Belgian generalist into a €1.8 billion pan-European specialist. The next phase would take them across the English Channel and to the Nordic countries—expansions that would more than double the portfolio in just two years.

IV. The Transformative UK Deal (2019)

The Largest Acquisition in Company History

The United Kingdom represented the largest and most fragmented healthcare real estate market in Western Europe. London's capital markets offered liquidity unavailable on the continent. British operators needed modern facilities. And demographic projections were staggering.

The UK healthcare real estate market offers Aedifica many opportunities for further growth. The UK's population aged 80 and over is expected to double to 10% of the total population by 2050.

In February 2019, Aedifica made its move. In February 2019, Aedifica invested approx. £450 million in a portfolio of 90 heathcare sites in the UK, completing its largest acquisition to date. By investing in a new European market, Aedifica not only diversifies its portfolio geographically.

Belgian healthcare real estate company Aedifica has moved into the UK market with the acquisition of a £450m (€498.8m) property portfolio. The deal, one of the largest UK healthcare transactions of 2018, will see the listed firm acquiring the portfolio of 93 properties, comprising more than 5,700 ensuite beds, from an affiliate of Lone Star Real Estate Fund IV.

The seller—Lone Star Real Estate Fund IV—was a private equity firm seeking exits from care home investments. Aedifica offered certainty of execution and an ability to hold long-term that private equity could not match. Aedifica said the £450m paid for the portfolio is a 5% discount to the fair value as estimated by an independent valuation expert.

"This transaction marks the first time a specialist European healthcare real estate investment trust has invested in the UK and one of the largest transaction for the UK market for 2018."

Funding the Growth

An acquisition of this scale required significant capital. 2019 saw first investment in the UK (£450 million), 5th public capital increase of €418 million, divestment of apartments and hotel portfolio, and secondary listing on Euronext Amsterdam.

On 7 May 2019, Aedifica successfully completed a €418 million capital increase, the largest ever in the history of the company.

The Amsterdam listing expanded Aedifica's investor base beyond Belgium, providing access to Dutch pension funds and institutional investors with specific allocations to healthcare real estate. Cross-listing also improved liquidity, reducing trading costs and expanding analyst coverage.

Market Rationale

In addition, the healthcare real estate market is still very fragmented due to the large number of local private players operating predominantly small and outdated buildings.

Market fragmentation created both opportunity and challenge. Opportunity because it meant significant consolidation potential—Aedifica could acquire portfolios that smaller players couldn't. Challenge because fragmentation meant diffuse operator relationships requiring local expertise to manage effectively.

Aedifica's response was to establish a dedicated UK subsidiary with a country manager and local team. This "hub-and-spoke" model—Brussels as strategic center with autonomous country operations—became the standard approach for all geographic expansions.

The UK acquisition achieved immediate scale, transforming Aedifica from a continental European player into a truly pan-European one. It also diversified currency exposure and regulatory risk across multiple jurisdictions—reducing reliance on any single healthcare system.

V. The Nordic Expansion & Hoivatilat Acquisition (2019-2020)

The Hoivatilat Takeover: A Contested Deal

If the UK acquisition demonstrated Aedifica's ability to execute large portfolio purchases, the Hoivatilat deal revealed something more sophisticated: the capacity to acquire a listed competitor through contested public markets.

In November 2019, Aedifica launched a public tender offer for all shares in Hoivatilat, a listed Finnish healthcare real estate developer and investor. The bid was backed by Hoivatilat's management and Board of Directors.

But management support didn't guarantee shareholder acceptance. After some major shareholders publicly announced that they would not accept the offer, Aedifica increased its takeover bid, after which the offer was eventually accepted by these major shareholders.

The contested nature of the deal—requiring a raised bid to secure acceptance—demonstrated both the value embedded in Nordic healthcare real estate and Aedifica's disciplined approach to M&A. Management didn't simply pay any price; they negotiated until terms made strategic and financial sense.

In early January 2020, Aedifica held about 95.9% of the shares, after which a squeeze-out bid for the remaining shares was launched and Hoivatilat was delisted from the Finnish stock exchange.

Recognition and Strategic Importance

Following the completion of the takeover, Aedifica was awarded an M&A award for "Best Large-Cap Corporate Deal". In its award rationale, the jury highlighted the company's "intelligent expansion" and the strategic importance of the deal.

Hoivatilat is an attractive partner to enter the Northern European healthcare real estate market with a high-quality, purpose-built portfolio, a substantial pipeline of development projects and a very experienced management team. The company has a build-and-hold strategy and develops itself the care buildings that are rented out. This transaction offers an excellent opportunity for Hoivatilat to continue its growth strategy, both in Finland and in the other countries of Northern Europe.

Hoivatilat brought capabilities Aedifica lacked: development expertise and a pipeline of projects under construction. While Aedifica primarily acquired existing buildings, Hoivatilat developed purpose-built facilities from the ground up. The combination created a vertically integrated platform capable of both acquisition-led and development-led growth.

2020 marked first investments in Finland and Sweden through the Hoivatilat acquisition, with over €700 million raised on capital markets.

BEL 20 Entry: Coming of Age

Aedifica's rapid growth was rewarded on Friday 20 March this year with a place in the Bel 20. You don't just get a spot there so it's a positive sign for the performance of the healthcare REIT Aedifica.

That is why in 2020, thanks to our 3.5 billion euro portfolio, we became one of the largest listed healthcare real estate investors in Europe and a European market reference.

BEL 20 inclusion brought passive investment flows from index-tracking funds and elevated Aedifica's profile among institutional investors who limit allocations to benchmark constituents. It also served as external validation—a recognition that Aedifica had evolved from startup to blue-chip.

The timing proved fortuitous. Just as Aedifica achieved scale, the COVID-19 pandemic arrived—testing the resilience of care home operators worldwide. Companies with weak balance sheets struggled; Aedifica's conservative leverage and diversified operator base provided stability through the crisis.

VI. Continued Expansion & ESG Leadership (2021-2024)

Ireland and Spain Entry

Geographic expansion continued relentlessly. Aedifica made its first investments in Irish healthcare real estate in early 2021.

In just four years, we have already created a portfolio of over €400 million.

In December 2021, Aedifica announced that it will invest in a series of high-quality care home projects to be developed in Spain.

Southern European expansion represented a calculated bet on underdeveloped healthcare infrastructure. Spain's elderly population was growing but care home penetration lagged Northern Europe. Ireland's strong economic growth supported private-pay care facilities at premium price points.

Sustainability Bond and ESG Commitment

Please find below a press release from Aedifica (a public regulated real estate company under Belgian law, listed on Euronext Brussels), regarding the successful issuance of its inaugural €500 million Sustainability Bond.

Aedifica, the Belgian real estate company with a focus on senior care, priced its first benchmark Sustainability Bond at the end of last week, tapping into the growing pool of funds looking for assets in the ESG space. The €500m (US$m) 10-year notes pay a fixed coupon of just 0.75%.

A 0.75% coupon on ten-year debt—during an era when interest rates were rising—demonstrated the "greenium" premium investors awarded to sustainability-linked issuers. Aedifica's social mission—housing for elderly people with care needs—aligned naturally with impact investing mandates.

2021 saw first investments in Ireland & Spain, €330m raised on capital markets, and a €500m sustainability bond. 2022 brought €310m raised on capital markets and the launch of net zero GHG pathway.

Net zero emissions Aedifica will be carbon neutral by 2050.

Portfolio Milestone

Real estate portfolio* of over €6.2 billion as at 31 December 2024. 635 healthcare properties for nearly 49,400 end users across 8 countries. Valuation of marketable investment properties increased, on a like-for-like basis, by 0.4% in Q4 and 0.7% YTD.

Weighted average unexpired lease term of 19 years and occupancy rate of 100%.

Those two metrics—19-year average lease term and 100% occupancy—tell investors everything about business model durability. With leases stretching into the 2040s, Aedifica's rental income visibility rivals that of government bonds. And 100% occupancy means every bed is generating revenue.

VII. The Cofinimmo Merger: Becoming Europe's #1 (2025)

The Deal That Changes Everything

On May 1, 2025, Aedifica announced the transaction that would culminate twenty years of building. Stibbe advised Aedifica on its proposed conditional exchange offer to Cofinimmo and the resulting agreement to combine and create Europe's leading healthcare REIT. The transaction stands among the largest – if not the largest – European real estate transactions of 2025.

Belgian healthcare real estate company Aedifica has agreed to merge with real estate investment trust Cofinimmo, the companies said in a joint statement on Tuesday. The combined group will have a gross asset value of 12.1 billion euros ($13.8 billion), making it the largest real estate investment trust (REIT) in Europe and the fourth largest in the world, they said.

Deal Structure and Rationale

"The deal is expected to generate operational synergies of around €16 million and boost EPRA earnings per share for shareholders of both companies. "Complementary geographic footprints, aligned strategic focus on healthcare, and comparable portfolio sizes, earnings profiles, and capital structures will provide a strong foundation for value creation," the companies said. Under the terms of the agreement, Aedifica is offering 1.185 of its new shares for each Cofinimmo share.

The all-share structure avoided the need for debt financing and aligned shareholder interests. Cofinimmo holders would become Aedifica shareholders, sharing in synergies and scale benefits.

Aedifica is a pure healthcare property player and Cofinimmo is a diversified property group. The merger would effectively convert Cofinimmo into a healthcare-focused entity—a strategic pivot that Cofinimmo had been gradually executing through organic portfolio rotation.

Cofinimmo and Aedifica have complementary geographic footprints and aligned strategic focus on healthcare as well as comparable portfolio sizes, earnings' profile and capital structures.

Execution Progress

At the Extraordinary General Meeting of 11 July 2025, Aedifica shareholders expressed strong support for the exchange offer. Of the 54.6% of outstanding shares represented, which amply met the quorum requirement of at least half of existing shares, over 99.9% voted in favour of the capital increase.

Near-unanimous shareholder approval signaled conviction that the merger created value. The board composition would transition over time—Upon completion, Cofinimmo chair Jean Hilgers is set to take over from Aedifica's Serge Wibaut as chair of the new group.

The combination of the two companies is expected to generate significant operational and financial synergies. This was confirmed on 4 June 2025, when S&P Global announced in a release that it had placed Aedifica's BBB ratings on CreditWatch with positive implications, reflecting the likelihood that S&P Global could raise Aedifica's ratings by one notch to BBB+ if the transaction proceeds in line with the proposed terms.

A potential upgrade to BBB+ would reduce borrowing costs on future debt issuance—a tangible financial benefit from increased scale and diversification.

Approval has already been obtained from competition authorities in the Netherlands and Germany and France has provided FDI clearance.

However, Aedifica, which launched an exchange offer to combine the two companies in June 2025, confirmed that the BMA has raised additional questions, potentially delaying the approval process beyond the original timeline. The planned merger between Belgian real estate groups Aedifica and Cofinimmo to form a leading European healthcare REIT is still under review by the Belgian Competition Authority (BMA).

Regulatory review remains the primary execution risk, though both companies have expressed confidence in ultimate approval given limited market concentration concerns.

VIII. The Business Model Deep Dive

How Healthcare REITs Work

Understanding Aedifica requires understanding triple-net lease economics. Triple net lease REITs are built around a simple but durable model where the tenant, not the landlord, pays for three major property expenses, which means these REITs receive rental income net of taxes, insurance, and maintenance.

A Triple Net Lease (NNN) can be defined as a form of commercial lease where, in addition to base rent, the tenant/occupier also pays the three main operating expenses that are associated with the property: Property Taxes: All state and local taxes. Insurance: Property insurance including speciality needs like flood, wind, or fire. Maintenance: Extending to items such as landscaping and roof repairs.

For Aedifica, this structure means operators bear facility maintenance costs while Aedifica collects predictable rent. For healthcare real estate, the gross yield and the net yield are generally equal ('triple net' contracts), with the operating charges, the maintenance costs and the rents on empty spaces related to the operations generally being supported by the operator in Belgium, the United Kingdom and (often) the Netherlands.

Aedifica is a Belgian listed company that is specialised in offering innovative and sustainable real estate concepts to our care operators and their residents across Europe, focusing in particular on housing for elderly people with care needs.

The Demographic Thesis

Currently, in the European Union (EU), more than a fifth of the population is aged 65 years or older, with a ratio of three working-age individuals to each older person. However, projections suggest that older individuals will account for nearly a third of the population by 2050, with less than two working-age individuals for every older person.

The population aged 60 and older in the WHO European Region is rapidly growing – from 215 million in 2021 to a projected 247 million by 2030, and over 300 million by 2050. The number of people aged 80 and over – those most likely to need support – is expected to more than double by 2050, placing additional demands on health and care systems.

The European population aged over 80 is set to rise significantly. In 1960 just 1.4% of Europeans were over 80. This figure reached 4.1% in 2010 and is projected to increase to 11.5% by 2060.

This demographic shift creates non-discretionary demand for care facilities. Unlike retail or office properties—which face structural challenges from e-commerce and remote work—care homes address essential human needs that cannot be digitized.

Operator Partnerships

Aedifica develops long-term partnerships with its care operators, understanding their specific needs while supporting their long-term growth.

Diversified income streams: no single tenant generates more than 10% of the Group's total rental income.

Tenant diversification protects against operator-specific risk. If one care home provider faces financial difficulties, Aedifica's overall rental income remains largely unaffected. With over 110 different operators across the portfolio, concentration risk is minimal.

Also investing in real estate for other types of care: childcare, specialist care for people with a disability, mental health care, rehabilitation care, (special) education, etc.

This diversification within healthcare—beyond just elderly care—provides additional protection against regulatory changes affecting any single segment.

IX. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MODERATE

The Europe REIT market remains moderately fragmented, with the largest entities holding a notable but not dominant share of total market capitalization. This fragmentation leaves room for further consolidation, which could unlock scale-driven operating efficiencies and competitive advantages.

Entry barriers include: regulatory complexity across 7+ jurisdictions, established operator relationships that take years to build, specialized underwriting expertise, and scale advantages in financing. New entrants can't simply buy properties—they must convince operators that they understand healthcare operations and will be reliable long-term partners.

Proven track record in entering new markets and creating a platform for further growth: local proximity combined with economies of scale. 'Plug-and-play' business model that can be rolled out to new markets.

2. Bargaining Power of Suppliers (Developers/Sellers): MODERATE

The healthcare real estate market is still very fragmented due to the large number of local private players operating predominantly small and outdated buildings.

Market fragmentation provides acquisition opportunities but also means sellers have multiple potential buyers. Aedifica's development capabilities through Hoivatilat reduce dependence on acquisitions alone.

3. Bargaining Power of Buyers (Operators/Tenants): LOW-MODERATE

19-year average lease terms lock in operators for decades. Once a care provider establishes operations at a specific location, switching costs are enormous—patients have relationships with staff, families expect continuity, and regulatory approvals are site-specific.

100% occupancy demonstrates operators need Aedifica more than Aedifica needs any individual operator.

4. Threat of Substitutes: LOW

Alternative care models—home care, assisted living technology, family caregiving—address different population segments. Purpose-built care facilities serve residents requiring 24/7 professional supervision that cannot be replicated in home settings.

Also investing in real estate for other types of care: childcare, specialist care for people with a disability, mental health care, rehabilitation care, (special) education, etc.

5. Competitive Rivalry: MODERATE-HIGH (but consolidating)

Specialization is the reigning strategy: Segro dominates logistics, Vonovia leads residential, Digital Realty spearheads data centers, and Aedifica-Cofinimmo forges healthcare supremacy.

Post-merger, the combined Aedifica-Cofinimmo entity will be the clear European leader in healthcare real estate—creating a scale advantage that smaller competitors will struggle to match.

X. Hamilton's 7 Powers Analysis

1. Scale Economies: STRONG

July 2025: Aedifica and Cofinimmo shareholders approved their proposed merger to create a EUR 12 billion (USD 12.84 billion) pan-European healthcare real estate platform, combining complementary geographic footprints across Belgium, the Netherlands, Germany, and France with specialized expertise in senior housing and medical facilities.

Scale economies manifest through lower cost of capital (BBB rating with potential BBB+ upgrade), spread fixed overhead across larger portfolios, and negotiating leverage with service providers.

2. Network Economies: MODERATE

Operator relationships create referral networks—a care provider satisfied with Aedifica's German properties considers them first for UK expansion. Knowledge sharing across markets improves deal sourcing and underwriting.

3. Counter-Positioning: STRONG (historically)

Aedifica is a pure healthcare property player and Cofinimmo is a diversified property group. Because Aedifica invests more than 60% in healthcare real estate, the Belgian tax authorities only have to pay a 15% dividend tax. For Cofinimmo this is 30%.

Pure-play positioning attracted ESG-focused investors that diversified competitors couldn't access as efficiently.

4. Switching Costs: STRONG

Long-term leases (19 years average) create contractual lock-in. Operators build businesses around specific locations—relocating would require relocating patients, staff, and regulatory approvals.

5. Branding: MODERATE

"We don't just invest in properties, we invest in society."

Reputation with operators as a "partner" rather than merely a landlord creates differentiation in competitive situations.

6. Cornered Resource: MODERATE

Prime locations in demographic hotspots. To support this strong European growth, we have ensured that we are firmly anchored in our six countries with local teams, allowing us to respond closely to the needs of our tenants and keep up to date with the ins and outs of the different markets in which we operate.

Relationships with top-tier healthcare operators cannot be easily replicated.

7. Process Power: DEVELOPING

Proven track record in entering new markets and creating a platform for further growth. Standardized acquisition and development processes across markets. Proven "plug-and-play" business model for new market entry reduces execution risk in geographic expansion.

XI. Financial Deep Dive & Performance

Current Financial Position

EPRA Earnings* amounted to €234.6 million (+7% compared to 31 Dec. 2023) or €4.93/share. Rental income increased to €338.1 million (+8% compared to 31 Dec. 2023). In 2024, 31 projects were delivered for a total investment budget of €297 million. 15 divestments totalling €98 million realised as part of strategic asset rotation programme.

This increase is mainly explained by the projects delivered from the pipeline and the indexation of rents, amounting to 3.1% on a like-for-like basis. This resulted in EPRA Earnings* above budget reaching €234.6 million (€219.6 million in 2023, an increase of approx. 7%), i.e. €4.93 per share.

Like-for-like rental growth of 3.1% reflects inflation indexation embedded in lease contracts—a natural hedge against rising costs that many other asset classes lack.

Proposed dividend of €3.90/share (gross) is confirmed (distribution in May 2025), representing a pay-out ratio of 79% of consolidated EPRA Earnings.

A 79% payout ratio leaves meaningful retained earnings for reinvestment while providing attractive current income. Belgian REITs must distribute at least 80% of profits, so Aedifica operates near the regulatory minimum—preserving financial flexibility.

Forward Guidance

EPRA Earnings* for 2025 are estimated at €238 million, or €5.01/share. An increasing dividend of €4.00/share (gross) proposed for the 2025 financial year.

Management guides to dividend growth—a 2.5% increase to €4.00 per share—reflecting confidence in continued operational performance.

Market Position

Its market capitalisation was approx. 3.0 billion as at 31 October 2025.

52 Week Range: €54.00 - €70.70. Market Cap (intraday) 3.114B. PE Ratio (TTM) 13.67. Forward Dividend & Yield 3.90 (5.95%).

At approximately €3 billion market capitalization pre-merger, Aedifica offers a dividend yield around 6%—competitive with other income-focused investments while providing demographic-driven growth potential.

XII. Key Performance Indicators for Investors

For investors monitoring Aedifica's ongoing performance, three metrics matter most:

1. Weighted Average Unexpired Lease Term (WAULT)

The 19-year average lease term is Aedifica's most important competitive moat. As leases roll off or new properties are acquired, this metric reveals whether the company maintains long-duration income visibility. A declining WAULT would signal reduced predictability; stable or increasing WAULT confirms continued access to long-term operator commitments.

2. Like-for-Like Rental Growth

This metric captures organic income growth from existing properties—excluding acquisitions and development completions. It reflects inflation indexation pass-through and operator rent reset negotiations. Healthy like-for-like growth (3%+ annually) indicates pricing power; negative growth signals operator distress.

3. Rent Cover Ratio

This operator-level metric measures tenant profitability relative to rent obligations. Strong rent cover (1.5x+ EBITDAR to rent) indicates healthy operators who can maintain lease payments through economic cycles. Deteriorating rent cover warns of potential operator defaults requiring lease renegotiation.

These three KPIs—WAULT, like-for-like rental growth, and rent cover—provide early warning of business model stress long before it appears in headline earnings.

XIII. Bull vs. Bear Case

Bull Case

By 2060 more than 10% of the European population will be over 80 years old—structural tailwind for decades.

The demographic thesis is nearly unassailable. European population aging isn't a forecast requiring assumptions—it's mathematical destiny based on people already born. Every year, the elderly population grows while care home supply struggles to keep pace.

Health care REITs have seen solid gains so far in 2025, posting returns of 8.5% as of May 28, which positions them as one of the top-performing REIT sectors this year. Analysts point to favorable supply/demand dynamics, demographic tailwinds, and the recession-resilient nature of the sector as key reasons supporting the sector.

Post-merger scale creates financing advantages (potential BBB+ rating) and operational synergies (€16 million annually). The combined entity will be the undisputed European healthcare REIT leader—a position competitors will find nearly impossible to challenge.

Inflation-linked rental contracts provide natural income protection. Impact's homes are let on long-term, triple net leases with rents indexed to inflation. The resilience of tenants is demonstrated by strong rent cover, supporting 100% rent collection.

ESG credentials attract sustainability-focused capital seeking healthcare exposure. The €500 million sustainability bond demonstrated investor appetite for Aedifica's social mission.

Bear Case

Interest rate risk: REITs are highly sensitive to changes in interest rates. Higher rates increase their cost of debt, given the sector's use of leverage. In addition, higher interest rates give income-focused investors more investment options.

Interest Rate Sensitivity: REITs and 10-year Treasury notes tend to have an inverse relationship. So as Treasury yield rates increase, REIT performance often decreases.

In a prolonged high-rate environment, Aedifica's ~6% dividend yield competes directly with risk-free government bonds. Rising rates increase financing costs for new acquisitions and put downward pressure on property valuations.

Merger integration across multiple jurisdictions creates execution risk. Combining two organizations with different cultures, systems, and regulatory filings is operationally complex. Synergy estimates may prove optimistic.

The BMA has raised additional questions, potentially delaying the approval process beyond the original timeline.

Regulatory delays or conditions could affect merger economics. While approval seems likely, the process introduces uncertainty.

Pandemic/flu season risk: Virus outbreaks can significantly affect healthcare REITs, especially those focused on senior housing. It can cause occupancy to decline as more patients check out than are admitted.

COVID-19 demonstrated that care homes face outsized pandemic risk. Future health crises could again disrupt operations—even if Aedifica's long-term lease structure protects against short-term revenue volatility.

XIV. The Investment Framework

Myth vs. Reality

Myth: Healthcare REITs are "bond substitutes" with no growth.

Reality: Aedifica achieved 28% compound annual portfolio growth over 15 years through disciplined acquisition and development. Inflation indexation provides organic growth; new market entry offers external expansion.

Myth: Demographic tailwinds are "priced in."

Reality: The healthcare and care-home sector is still a small fraction of the institutional market in Europe. Healthcare real estate remains underpenetrated compared to other commercial property sectors. Institutional capital allocation to healthcare real estate continues growing.

Myth: The Cofinimmo merger is just "empire building."

Reality: €16 million in quantified synergies, potential credit rating upgrade, and clear strategic rationale (eliminating a major competitor while gaining complementary geographic exposure) create identifiable shareholder value.

Key Risk Factors

Interest Rate Sensitivity: Monitor ECB policy and 10-year government bond yields. Rising rates compress valuations and increase financing costs.

Operator Credit Quality: Care home operators face staffing shortages and reimbursement pressures in some markets. Deteriorating rent cover ratios would signal trouble.

Regulatory Changes: Healthcare is heavily regulated. Policy changes affecting reimbursement rates, staffing requirements, or building standards could impact operator profitability and property values.

Merger Execution: Until the Cofinimmo transaction closes, regulatory and integration risks persist.

Valuation Context

At approximately 6% dividend yield and 13-14x earnings, Aedifica trades at valuations consistent with stable-growth healthcare REITs globally. Premium valuation relative to diversified REITs reflects healthcare's superior growth visibility and defensive characteristics.

The stock trades at a modest discount to EPRA NAV, suggesting the market prices some execution risk into the merger. Successful integration could unlock valuation expansion toward historical premiums.

XV. Conclusion: Platform for the Next Forty Years

Twenty years ago, Aedifica was a €110 million Belgian generalist searching for its identity. Today, the company stands at the threshold of creating a €12 billion pan-European healthcare empire positioned to serve structural demand extending to 2060 and beyond.

Aedifica is blowing out 15 candles this year. Since its start in 2005, Aedifica has grown as a small Belgian start-up into a BEL20 company and international reference in European healthcare real estate. For 15 years Aedifica and its investors have been building the healthcare real estate of the future – and we are far from finished.

The Aedifica story illustrates several principles that transcend healthcare real estate:

Specialization creates compounding advantages. By abandoning diversification, Aedifica built expertise, relationships, and reputation that general competitors couldn't match. The cost was concentration risk; the benefit was strategic clarity.

Demographic tailwinds are the most durable competitive advantages. Unlike technological trends that shift rapidly, population aging unfolds over decades with mathematical certainty. Companies positioned against such tailwinds have exceptional visibility.

Patient capital deployment trumps frenzied acquisition. Aedifica's 28% CAGR came through disciplined growth backed by equity raises—not overleveraged asset accumulation. Conservative balance sheets enabled counter-cyclical investing when others retreated.

Platform thinking enables non-linear scaling. Each geographic expansion followed a proven playbook: local teams, operator relationships, regulatory expertise. This "plug-and-play" model converted single-market success into pan-European platform.

For the European healthcare real estate industry, the Aedifica-Cofinimmo merger represents a watershed moment. Specialization is the reigning strategy: Segro dominates logistics, Vonovia leads residential, Digital Realty spearheads data centers, and Aedifica-Cofinimmo forges healthcare supremacy.

The combined entity will set standards for scale, operational excellence, and investor communication that competitors must match or cede market position. Consolidation benefits flow disproportionately to leaders; fragmented competitors face strategic choices about specialization, scale, or exit.

"We don't just invest in properties, we invest in society."

In the end, Aedifica's success derives from a simple insight: there is dignity in serving aging populations, and considerable returns from doing so thoughtfully. As Europe grays, the need for quality care facilities will only intensify. Aedifica has spent two decades building the infrastructure to meet that need.

The platform is built. The tailwinds are strengthening. The question now is whether management can execute the largest European real estate merger of 2025 while maintaining the disciplined culture that made Aedifica exceptional in the first place.

Note: This analysis is for informational purposes only. Investors should conduct their own due diligence and consider consulting financial advisors before making investment decisions. The merger described remains subject to regulatory approvals and other conditions that may not be satisfied.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube