Ritchie Bros. Auctioneers: From Furniture Store to $16 Billion Marketplace Empire

I. Introduction & Episode Roadmap

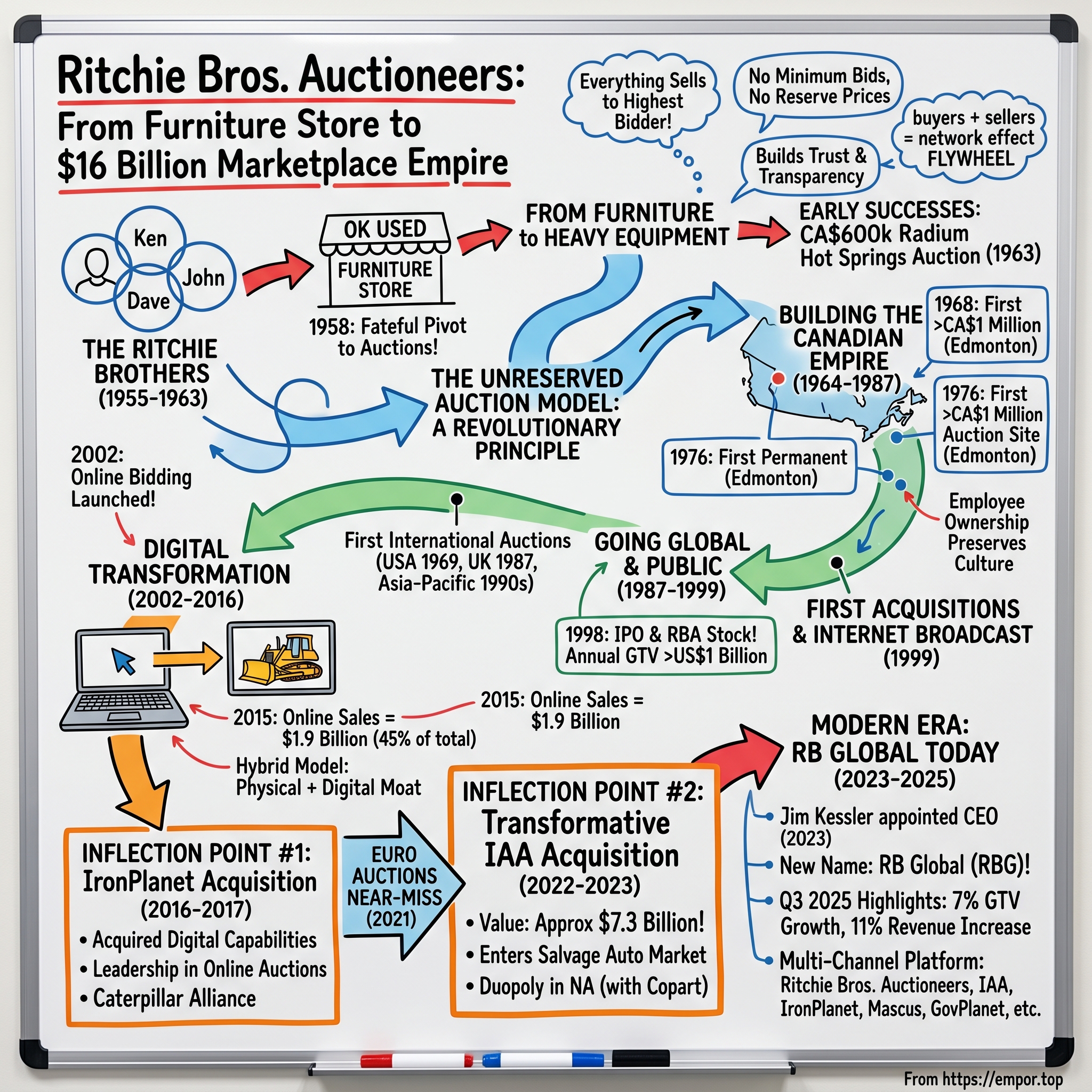

On a rainy Saturday morning in 1958, three brothers in Kelowna, British Columbia stood before a Scout hall full of chrome-legged tables and vinyl chairs. They weren't furniture dealers anymore—they had become, quite by accident, auctioneers. Sixty-seven years later, the company those brothers built now orchestrates nearly $16 billion in annual gross transaction value, operates in 170 countries, and employs thousands across an intricate web of digital platforms, permanent auction yards, and value-added services.

In 2024, RB Global's revenue reached $4.28 billion, an increase of 16.43% compared to the previous year's $3.68 billion. Earnings were $372.70 million, an increase of 113.09%. This isn't just a Canadian success story—it's a masterclass in building durable competitive advantages through an unwavering commitment to a counterintuitive business model, strategic digital transformation, and bold M&A.

The name on the door may now be RB Global, but the DNA of those Kelowna brothers—particularly their radical commitment to unreserved auctions—remains the company's animating force. Through its auction sites in 14 countries and digital platform, RB Global serves customers in more than 170 countries across a variety of asset classes, including automotive, commercial transportation, construction, government surplus, lifting and material handling, energy, mining, and agriculture.

The company's marketplace brands include Ritchie Bros., the world's largest auctioneer of commercial assets and vehicles offering online bidding, and IAA, a leading global digital marketplace connecting vehicle buyers and sellers.

This article tells the story of how three brothers selling furniture in British Columbia built the world's largest industrial equipment marketplace—and then transformed it again through the $7.3 billion acquisition of IAA, entering the vast automotive salvage market. The themes are timeless: the power of trust in two-sided marketplaces, the art of digital transformation without abandoning physical infrastructure, and the courage to make bet-the-company acquisitions when the strategic logic is compelling.

II. Origins: The Ritchie Brothers & the Furniture Store Pivot (1955–1963)

A Family's Struggle and a Friend's Suggestion

David Ritchie was the youngest of six children. By the time he was born in 1936 in Kelowna, British Columbia, his father had lost all he owned. A practicing attorney, Ritchie's father had lost a legal battle against agricultural co-ops. As a result, he was disbarred and forced to give up his ownership of several orchards. Penniless, the Ritchie family moved into a rented home on a tobacco farm, and Ritchie's father eventually found work as a fruit inspector.

"My family was going through a very rough time when I was young," Dave would later recall. "We often ate nothing but porridge two or three times a day. We all tried to help as much as we could. I remember as a little wee boy joining my brothers and sisters to pick potatoes."

His older brother was later killed in the invasion of Normandy on D-Day. "That was a very sad time for my family," said Ritchie. "He was the oldest son and my father was bitter over his death."

This childhood of hardship instilled in young Dave a work ethic that would prove essential to building a global business. When he was 12, Ritchie worked on a farm three miles from home, making $2 a day herding cattle, milking cows, and weeding corn. His father bought him his first bicycle for $8—a modest machine that Dave traded up for a better English-made Hummer through installment payments. "That made me the proudest kid in Canada. From then on, I always had cash in my pocket."

"I'd get up early on Sunday morning and go to the park to collect beer bottles, which I traded in on Monday after school. I loved to sell things and did a lot of door-to-door sales in Christmas trees and greeting cards. I was happy to have these jobs. They taught me the importance of self-reliance and the value of hard work."

The Furniture Store and the Fateful Auction

After the war ended, Ritchie's father bought a second-hand furniture store, the OK Used Furniture Store, which fascinated young Dave. After school, Ritchie maintained the store's potbellied stove and swept the floors.

Ritchie Bros. Auctioneers was established in Kelowna, British Columbia, Canada, when the three Ritchie brothers – Ken, John and Dave Ritchie – took over the OK Used Furniture Store from their father in 1955. They entered the auction business in 1958.

The pivot came from desperation. Ritchie Bros. Auctioneers is a global corporation and a Canadian business success story, but it started off as a used furniture shop with a big problem: The bank had called in a $2,000 loan. It was the 1950s and the three Ritchie brothers — Ken, Dave and John — had taken over the family furniture store in Kelowna, B.C. Short on cash and in a bind, they took someone's suggestion to hold an auction to sell surplus tables and chairs. The following Saturday, they rented the local Scout hall and sold enough furniture to keep the bankers at bay.

The sale was a revelation for the brothers. The auction convinced them to move on from the O.K. Used Furniture Store and try their hand at a new line of work.

From Furniture to Heavy Equipment

Their early auction work brought them in contact with heavy equipment used in road building. In 1962, the Ritchie brothers noticed a void in the industrial end of the auction business and decided to try their hand in that area. They had to put up $50,000 for their first industrial auction. For years, they remembered how hard they worked in Canada's north country to get equipment to market. That first equipment auction realized a $250,000 profit.

In the early 1960s, the Ritchies transitioned from sporadic sales to conducting regular auctions focused on used industrial equipment, beginning with small-scale events in rented community halls and school gymnasiums across British Columbia and Alberta. A pivotal milestone came in 1963 with their first major unreserved industrial auction in Radium Hot Springs, British Columbia, where gross proceeds exceeded CA$600,000 from equipment sourced primarily from local construction and forestry operations.

The Birth of a Business Model

Dave Ritchie was an innovator from his first equipment auction in 1963. With the auction set to start, the rain began to fall. Instead of making bidders walk the yard in the rain, Dave and his brothers set up the auction under the eaves of a nearby shop and drove the equipment piece by piece in front of bidders. The crowd stayed dry, and the "ramp-and-stage method" became a fixture at Ritchie Bros. and eventually other auctioneer houses around the world.

From the very beginning, for Dave and Ritchie Bros., the customer has always been the focus. In the words of Dave, "Treat your customers like your friends, and they will always be your customers". So, Dave started to make friends, lots of them. Across Western Canada, then into the United States, and then around the world. All these relationships were important to Dave, and many of these friends were experts in their field.

For investors: The origin story matters because it reveals the foundational DNA—scrappy resourcefulness, customer obsession, and a willingness to innovate out of necessity. These traits would define the company's culture for decades.

III. The Unreserved Auction Model: A Revolutionary Principle

What "Unreserved" Really Means

At the heart of Ritchie Bros.' competitive moat lies a simple but profound principle: every item sells to the highest bidder, regardless of price. There are no minimum bids, no reserve prices, and consignors cannot bid on or buy back their own equipment.

The brothers and their customers taught each other about the industry—what they liked and didn't like about auctions—and served as "silent salesmen" around the world, helping to point Dave and his team to the next equipment package or region to go after. With Ritchie Bros., Dave was committed to professionally conducted unreserved auctions, where the bidders set the prices, not the auctioneer or the sellers. No bid-ups. No buy backs. This transparency won the company customers around the world.

Dave Ritchie, along with his brothers Ken and John, founded Ritchie Bros. Auctioneers in 1958 on two core principles: conducting strictly unreserved auctions and treating every customer with fairness and respect. He was pivotal in leading the Company to its current position as the world's largest auctioneer.

The Psychology Behind "Everything Sells"

The unreserved model seems counterintuitive. Why would sellers accept the risk that their $500,000 excavator might sell for $300,000? The answer lies in the marketplace dynamics that unreserved auctions create.

The commitment to the unreserved auction model built trust and transparency. Sellers knew their assets would sell, and buyers knew items sold to the highest bidder without reserve prices, attracting significant volume and establishing market leadership.

For buyers, the certainty that every item will sell creates urgency. If you're the high bidder, you own the equipment—there's no seller who can pull it back because the price didn't meet their secret threshold. This certainty draws more bidders, which creates more competition, which ultimately drives prices higher.

A key attraction of unreserved auctions is their unreserved status, meaning all items will sell to the highest bidder regardless of price. This presents a significant opportunity for buyers seeking value in today's competitive equipment market.

For sellers, the unreserved format provides two critical benefits: certainty of sale and access to a global buyer pool. Construction companies that need to liquidate equipment quickly for cash flow purposes can schedule an auction and know exactly when they'll receive payment. And because Ritchie Bros. attracts such massive bidder pools—often 10,000-15,000 at their mega auctions—sellers typically achieve fair market value despite the absence of a reserve.

The Two-Sided Marketplace Flywheel

The unreserved model created a powerful network effect that became increasingly difficult for competitors to replicate:

More buyers → Higher prices → More sellers → More inventory → More buyers

The mega auctions in Edmonton, Alberta and Orlando are outliers in the Ritchie Bros. world and attract anywhere from 10,000 to 15,000 bidders. These yards also yield many of the record-breaking stats that Ritchie Bros. auctions are known for. "We have two mega yards that generate our biggest volumes and largest sales," according to company executives. "Those are Orlando, which typically has a large event in February that tends to be in the $150 million to $200 million range. Edmonton is the other large yard."

"It has created liquidity in the marketplace, which is really important. That has been a major factor in enabling contractors and transportation companies to get financing for their equipment."

This liquidity effect extends beyond Ritchie Bros.' own auctions. Lenders became more willing to finance equipment purchases because they knew a deep, liquid resale market existed if the borrower defaulted. The mere existence of Ritchie Bros. made the entire equipment ecosystem function more efficiently.

Why Competitors Can't Easily Replicate

The unreserved model requires massive scale to work. A small auction house that promises unreserved sales but attracts only 50 bidders will deliver terrible results for sellers. Word spreads quickly in the equipment world, and sellers will migrate to platforms with larger buyer pools.

One longtime customer noted: "The unreserved auction business model he and his employees developed has set a standard in the equipment business for fair and unbiased auctions that allow equipment owners to obtain instant liquidity for their surplus fleet. The auction values established at Ritchie auctions are often the benchmark used throughout the industry."

For investors: The unreserved model is harder to replicate than it appears. It requires building buyer liquidity first, which requires seller inventory, which requires buyer liquidity. Ritchie Bros. spent decades building this flywheel, creating an organic barrier to entry that complements their physical infrastructure moat.

IV. Building the Canadian Empire (1964–1987)

Westward and Northward Expansion

Most of the company's earliest auctions were held in British Columbia. Ritchie Bros. began expanding into other parts of Canada in the mid-1960s, conducting its first auctions in Alberta (in 1964), the Yukon (1964), Saskatchewan (1965), Manitoba (1968), and other parts of Eastern Canada shortly thereafter.

Early operations presented significant challenges, including sourcing inventory from scattered local farmers, loggers, and small contractors in remote areas of the Okanagan Valley and Kootenays, often requiring extensive travel over rugged terrain and in harsh winter conditions. The brothers developed innovative live auction formats to engage bidders, adapting to logistical hurdles like temporary venues and weather-related delays, such as constructing ice bridges for access in northern regions. By 1967, they established their first dedicated auction site near Kelowna to streamline operations and support growing demand.

The physical demands of these early years were immense. Brother Dave is said to have once driven 17 hours straight through to San Diego to bring a boat back to a customer. Entrepreneurs at heart, the brothers would spare no effort to finalize the deal.

The Million-Dollar Milestone and Permanent Infrastructure

In 1968, Ritchie Bros. Auctioneers held its first auction with gross proceeds in excess of CA$1 million, in Edmonton, Alberta, Canada. Edmonton was also the site of the company's first permanent auction site (on company-owned land), which was established in 1976. Until then, Ritchie Bros. had been conducting its auctions on leased land.

A key breakthrough occurred in 1968 with the company's first auction surpassing CA$1 million in gross proceeds, held in Edmonton, Alberta, marking a shift toward larger-scale events.

The decision to invest in permanent, company-owned auction sites proved transformational. Unlike leased facilities, permanent yards allowed Ritchie Bros. to configure spaces optimally for equipment sales, build relationships with local contractors, and establish a consistent presence in key markets. This physical infrastructure would become an enduring competitive advantage—one that online-only competitors would later struggle to replicate.

Family Transitions and Employee Ownership

In 1965, Ken Ritchie left the company to spend more time with his family and the company's name was changed from Ritchie Bros. Auction Galleries Ltd. to Ritchie Bros. Auctioneers Ltd. Ken established his own auction company, but returned to work with his brothers in 1968. He stayed with Ritchie Bros. Auctioneers until 1980.

In 1974, John Ritchie left the company, selling his share of the business to his brother Dave. In 1975, Dave Ritchie – the sole company shareholder – sold partnerships in Ritchie Bros. Auctioneers to some of his key employees.

Dave's decision to share ownership with key employees was prescient. By creating economic alignment with his best people, he ensured the company could continue growing even as the founders stepped back. This ownership culture would persist through the company's IPO and beyond.

Record-Breaking Growth

By the early 1980s, Ritchie Bros. had established itself as the dominant force in Canadian heavy equipment auctions. By the early 1970s, Ritchie Bros. Auctioneers employed 25 people and was handling sales approaching C$1.5 million. Major sales were carefully planned. Ritchie employees visited the site two months ahead of the sale; they carefully cataloged the equipment, inspected it, and prepared advertising and brochures that guaranteed that the items offered were as described. The sales also featured on-spot financing for those who needed it.

For investors: The Canadian expansion years established the operational playbook—permanent sites, meticulous preparation, customer relationships—that would scale globally. The employee ownership culture created alignment that would drive disciplined growth.

V. Going Global & Going Public (1987–1999)

The First International Auctions

Ritchie Bros. established its first presence outside Canada in 1969 when it became incorporated in Washington, USA. The company held its first auction outside Canada in 1970, in Beaverton, Oregon, and gradually began expanding throughout the United States.

The European expansion was triggered by an unusual opportunity. In 1987, the company held its first Ritchie Bros. auction in Europe. The sale, held in Liverpool, England, sold off equipment that had been used to rebuild the infrastructure of the Falkland Islands following the war there. Later that year, the company held its first auction in The Netherlands.

In the late 1980s, Ritchie Bros. Auctioneers began to look overseas for further growth opportunities, in the UK and the Netherlands, and then in Australia and other countries.

The 1990s brought several interesting auctions, along with further international expansion. In 1990, Ritchie Bros. began conducting unreserved auctions throughout the Asia-Pacific region. Ritchie auctions were held in Australia, New Zealand, the Philippines, Hong Kong, Japan, and Thailand. Moreover, Ritchie Bros. auctioned more than 20 hectares of new and used equipment accumulated by Exxon during the cleanup of the Exxon Valdez oil spill in Prince William Sound. Exxon sold most of its equipment to Ritchie Bros. for an undisclosed price, and over 8,000 bidders from around the world registered for this sale held in Anchorage, Alaska.

The 1998 IPO

In 1998, the year that Ritchie Bros. went public, the company's annual gross auction proceeds exceeded US$1 billion for the first time ever. Its common shares were listed on the New York Stock Exchange under the symbol RBA in March 1998, followed by listing on the Toronto Stock Exchange in April 2004.

The 1998 Initial Public Offering (IPO) listed the company on the New York Stock Exchange (NYSE: RBA), providing capital for further expansion and acquisitions.

The IPO timing proved excellent. With gross auction proceeds crossing $1 billion for the first time, Ritchie Bros. demonstrated that its model could scale globally. The public listing provided capital for permanent site expansion, technology investments, and acquisitions.

Dave was regarded as a visionary and was the company's first chairman after it went public in 1998. Even though he retired in 2006, he still seems at home at the auction yard with customers.

Ritchie served as CEO until 2004, and as chairman of the board until 2006. In 2005, he received the University of Victoria, Peter B. Gustavson School of Business' Distinguished Entrepreneur of the Year Award.

First Acquisition and Internet Broadcast

In February 1999, the company purchased Forke Auctioneers, a major auctioneer of industrial equipment with headquarters in Lincoln, Nebraska. This was the first acquisition in Ritchie Bros.'s 36-year history. The Forke acquisition added sites in Florida, North Carolina, and New Mexico to the company's existing 21 sites and also provided it with the option to assume leases held by Forke on a number of auction sites.

In March 1999 the company broadcast an auction live on the Internet for the first time. The event took place during ConExpo, the Las Vegas-based premier construction and construction materials exposition.

For investors: The IPO and subsequent acquisitions established a growth playbook—use public market capital to acquire regional competitors, consolidate market share, and invest in technology. The 1999 internet broadcast was an early signal of the digital transformation to come.

VI. Digital Transformation: The First Wave (2002–2016)

Real-Time Online Bidding

Launching online bidding in 2002 and later acquiring IronPlanet in 2017 were pivotal. These moves transformed the company from a primarily live-auction business into a multi-channel, technology-driven marketplace.

Under Dave's leadership, Ritchie Bros. conducted auctions across North America, Europe, Australia, and the Middle East, but Dave wasn't satisfied and was excited to see where technology could take the company next. Dave pushed Ritchie Bros. to conduct auctions via video in the late 1980s and 1990s, along with in-person bidding, and launched one of the equipment industry's first equipment websites in 1996.

After Ritchie Bros. went public in 1998, the company established an increasing number of auction locations and started working on a system that would allow customers to bid from home on their computer. With Dave as CEO Ritchie Bros. conducted its first online auction in 2002 and has never looked back.

The Hybrid Model Emerges

Unlike pure-play internet startups that dismissed physical infrastructure, Ritchie Bros. understood that heavy equipment sales required a hybrid approach. Buyers wanted to see equipment in person before bidding on $200,000 excavators. But they also wanted the convenience of bidding remotely if they couldn't attend.

One of the reasons for the increased bidder numbers is the pervasive reach of the internet and Ritchie Bros.' online bidding portal. Buyers have the ability to make purchases in real-time no matter where they live, and the popularity of online bidding is growing. In 2015, online buyers accounted for $1.9 billion or 45 percent of the company's total sales. If a buyer finds the right asset at the right price, they will buy it from anywhere.

"Customers, they buy shoes online. They can buy bulldozers online too," said one senior executive.

Company executives describe live auctions as "mini-Super Bowls," considering the energy level at the events and the sheer size of the facility, crowds and equipment. The company needs 250 workers during the Edmonton sale for security, shuttles, catering and other roles.

Building the Data Advantage

By conducting thousands of auctions annually and recording every transaction, Ritchie Bros. accumulated an invaluable database of equipment prices. This data became increasingly valuable as the company evolved:

- For buyers: Historical pricing data enabled better bidding decisions

- For sellers: Market intelligence helped optimize timing and reserve expectations

- For lenders: Residual value forecasts improved financing decisions

- For Ritchie Bros.: Proprietary data created switching costs and service opportunities

For investors: The hybrid physical-digital model proved more durable than pure online players expected. Equipment buyers value the ability to inspect $500,000 machines before purchase—but they also value bidding remotely when convenient. The accumulated data created an information advantage that would expand through acquisitions.

VII. INFLECTION POINT #1: The IronPlanet Acquisition (2016–2017)

Strategic Rationale

In August 2016, the company announced its plan to acquire IronPlanet, Inc., an online auction company. The deal was approved by the DOJ and closed in May 2017.

Ritchie Bros., the world's largest heavy equipment auctioneer and provider of end-to-end services, completed its acquisition of IronPlanet®, a leading online marketplace for heavy equipment and other durable assets. Ritchie Bros. acquired IronPlanet for approximately $758.5 million, subject to customary closing adjustments. The acquisition was financed through a combination of Ritchie Bros.' previously announced senior note offering and secured term loan facility.

The IronPlanet acquisition wasn't about eliminating a competitor—it was about acquiring digital capabilities that Ritchie Bros. had struggled to build internally. "IronPlanet catapulted Ritchie into a leadership position in the online industrial equipment auction space, providing Ritchie with enhanced digital capabilities and a scalable platform to drive long-term growth," wrote RBC Capital Markets analyst Derek Spronck.

The Caterpillar Alliance

As a part of this acquisition, Ritchie Bros. also entered into an initial five-year strategic alliance with Caterpillar which is expected to strengthen its relationship with Caterpillar's independent dealers around the world by providing them enhanced and continued access to a global auction marketplace to sell their used equipment. The company also will continue to coordinate and manage Cat® auctions in respective Cat dealer geographies.

Under the alliance, Ritchie Bros. became Caterpillar's preferred global partner for live onsite and online auctions for used Cat equipment, and will complement existing offerings within Cat® dealer channels. Ritchie Bros. will provide Caterpillar and its dealers with access to proprietary auction platforms, software and other value-added services, enhancing the exchange of information and services between customers, dealers and suppliers. The strategic alliance is expected to strengthen Ritchie Bros. relationship with independent Cat dealers around the world by providing them enhanced and continued access to a global auction marketplace to sell their used equipment.

Prior to the acquisition, Caterpillar and its dealers owned a minority position in IronPlanet.

Integration and Multichannel Strategy

The acquisition of IronPlanet accelerates Ritchie Bros.' strategy of becoming a one-stop, multichannel company where customers can buy, sell or list equipment, when, how and where they choose – both onsite and online.

The acquisition of IronPlanet accelerates Ritchie Bros.' strategy of becoming a one-stop, multichannel company where customers can buy, sell or list equipment, when, how and where they choose – both onsite and online. Later, Ritchie Bros. combined its online EquipmentOne brand with the IronPlanet DailyMarketplace, creating a harmonized brand offering called Marketplace E that gives customers more ways to set reserve pricing. Ritchie Bros. also gains expanded growth capabilities in the oil and gas and government sectors.

The company plans to combine the Ritchie Bros. and IronPlanet sales forces in the US, Canada and Europe, in line with its strategy to provide customers a one-stop, multichannel experience.

For investors: The IronPlanet deal demonstrated management's willingness to acquire digital capabilities rather than build them organically—a pragmatic approach given the pace of technological change. The Caterpillar alliance added relationship value that pure-play online competitors couldn't match.

VIII. Continued Acquisitions & Platform Building (2017–2022)

Expanding the Suite of Services

Following IronPlanet, Ritchie Bros. continued building out its technology and service capabilities through targeted acquisitions. The company's selling channels expanded to include Private Treaty, offering privately negotiated sales, and sector-specific solutions GovPlanet, TruckPlanet, and Ritchie Bros. Energy. The company's suite of solutions also includes Ritchie Bros. Asset Solutions and Rouse Services LLC, which together provides a complete end-to-end asset management, data-driven intelligence and performance benchmarking system; SmartEquip, an innovative technology platform that supports customers' management of the equipment lifecycle and integrates parts procurement with both OEMs and dealers; plus equipment financing and leasing through Ritchie Bros. Financial Services.

Ritchie Bros. made its foray into the agricultural equipment auction business with the acquisitions of All Peace Auctions of Grande Prairie, Alberta in 2002; LeBlanc Auction Service of Estevan, Saskatchewan in 2004; Dennis Biliske Auctioneers of Buxton, North Dakota in 2006; Clarke Auctioneers of Rouleau, Saskatchewan in 2007; and Martella Auction Company of Tipton, CA in 2009. In February, Ritchie Bros. acquired a used heavy equipment listing service, Mascus.

The Euro Auctions Near-Miss

In August 2021, Ritchie Bros. and Europe's leading plant and machinery auction house, Euro Auctions, announced that they entered into an agreement under which Ritchie Bros. would acquire Euro Auctions group for an enterprise value of £775 million (approximately US$1.08 billion). Founded in 1998, Euro Auctions conducts unreserved heavy equipment auctions with onsite and online bidding under the brands Euro Auctions and Yoder & Frey, with 200+ employees in 14 countries. In 2020 the company conducted 60 auctions, selling close to 90,000 items for £484+ million across its nine locations.

Euro Auctions Founder and Director Derek Keys commented: "Dave Ritchie and his brothers were a big inspiration for my brothers and I in the creation of Euro Auctions. We modelled much of what we do off Dave's customer-centric philosophy, which still runs through Ritchie Bros. today."

In August 2021, the acquisition of Euro Auctions, a Northern Ireland auction house that buys and sells industrial plant, construction equipment, and agricultural machinery for £775 million was announced. That acquisition attempt was discontinued in April 2022.

The Euro Auctions deal ultimately fell through, but it signaled management's appetite for transformative M&A—an appetite that would manifest dramatically with the IAA acquisition announced later in 2022.

For investors: The platform strategy evolved from pure transaction facilitation to comprehensive asset lifecycle management. Each additional service—financing, logistics, data analytics, parts procurement—deepened customer relationships and created switching costs.

IX. INFLECTION POINT #2: The Transformative IAA Acquisition (2022–2023)

The Deal

In November 2022, Ritchie Bros. Auctioneers and IAA, Inc. announced that they entered into a definitive agreement under which Ritchie Bros. would acquire IAA in a stock and cash transaction valued at approximately $7.3 billion including the assumption of $1.0 billion of net debt. The transaction has the unanimous support of both boards of directors. Under the terms of the merger agreement, IAA stockholders would receive $10.00 in cash and 0.5804 shares of Ritchie Bros. common stock for each share of IAA common stock they own.

IAA Inc., acquired by RB Global in March 2023, serves as a leading digital marketplace for total loss, damaged, and low-value vehicles. The platform primarily supports insurance companies, rental car fleets, and charitable organizations by providing online auctions and transportation services for salvaged assets. Post-acquisition, IAA has been integrated into RB Global's offerings, allowing seamless access to its extensive inventory of over 2.5 million vehicles annually through unified digital channels.

The Salvage Auto Auction Market

The strategic logic centered on entering the vast automotive salvage market, which operates as a duopoly in North America. IAA estimated that IAA and Copart, Inc. together represent over 80% of the North American salvage vehicle market.

While over five million vehicles are sold annually in salvage vehicle marketplaces in North America, this represents less than 2% of total vehicles in operation (approximately 300 million). The industry currently benefits from several thematic tailwinds, including (i) Growing and Aging Automotive Car Parc, (ii) increasing vehicle complexity and total loss frequency, (iii) increasing accident frequency and (iv) increasing utilization of recycled and alternative automotive parts.

The salvage market is dominated by two companies, Copart and Insurance Auto Auctions (IAA), who each have roughly ~40% share, with the next largest operator claiming just 3%. But unlike the whole car auction market, which is closely tied to transaction "flow", salvage auto auctions are supported by the "stock" of outstanding vehicles, providing a stable source of volume as every year some reasonably predictable percentage of the ~280mn cars on US roads get into accidents. Around ~13mn are removed from the fleet every year, of which 4mn are siphoned to salvage auctions. Insurers bring 80%-85% of the cars that run through these auctions.

Shareholder Drama and Deal Amendment

The IAA acquisition faced significant opposition. As CEO, Ann Fandozzi had pushed forward with the IAA deal despite opposition from proxy advisory firms Institutional Shareholder Services and Glass Lewis, as well as shareholders Luxor Capital Group and Eminence Capital.

A number of shareholders including New York-based Luxor Capital and Eminence Capital (as well as two Proxy advisory firms) had earlier expressed concerns about the risks posed by the acquisition and had indicated they planned to vote against it, but Ritchie Bros secured the backing of a key IAA shareholder and another proxy advisory firm and the final acquisition deal cleared all hurdles.

In connection with the amended merger agreement, Ancora entered into a mutual cooperation agreement with IAA and agreed to vote its shares, representing approximately 4% of IAA's voting power, in favor of the transaction. Cooley also advised IAA on Ritchie Bros.' concurrent $500 million investment from Starboard Value. Ancora, a top shareholder of IAA, and Starboard Value, a new investor in Ritchie Bros., supported the agreement.

As previously announced on January 23, 2023, under the terms of the amended merger agreement, IAA shareholders received $12.80 per share in cash and 0.5252 common shares of Ritchie Bros. for each share of IAA common stock they owned.

Integration and the Birth of RB Global

Ritchie Bros. acquired IronPlanet, an online marketplace for heavy equipment, for approximately $758.5 million, enabling the integration of digital inspection reports and online sales platforms to complement traditional auctions. The company's most significant expansion came in March 2023 with the acquisition of IAA Inc., a leading provider of vehicle remarketing services, for approximately $7.3 billion in stock and cash, which broadened its portfolio into salvage and insurance auction markets.

In March 2023, Ritchie Bros. completed the acquisition of U.S. auto retailer IAA Inc. in a stock and cash deal worth $7 billion. It was announced in May 2023 a new name for the parent company, RB Global.

For investors: The IAA acquisition fundamentally transformed the company's growth profile and competitive position. By entering the salvage auto duopoly, RB Global gained exposure to secular tailwinds (rising vehicle complexity, aging car parc, increasing total loss frequency) while diversifying away from construction cycle sensitivity.

X. Modern Era: RB Global Today (2023–2025)

Leadership Transition

RB Global, formerly known as Ritchie Bros. Auctioneers Inc, said in August 2023 that Chief Operating Officer Jim Kessler would become its CEO with immediate effect following the departure of Ann Fandozzi after a dispute over compensation. The company also disclosed the exit of Chief Financial Officer Eric Jacobs.

Ann Fandozzi demanded a "front-loaded compensation" program that would bring forward five-years of equity compensation to continue as CEO, which the board determined reaches far beyond peer group benchmarks.

Mr. Kessler was appointed Chief Operating Officer of RB Global in 2020 and was promoted to President and Chief Operating Officer in 2021. RB Global, Inc. announced the appointment of Jim Kessler, most recently the Company's President and Chief Operating Officer, as Chief Executive Officer. Mr. Kessler will also join RB Global's Board of Directors. Mr. Kessler has a proven record of driving growth and value creation, including through M&A. Since joining RB Global as COO in 2020, Mr. Kessler has been integral in developing and executing the customer engagement strategies and offerings that have transformed RB Global from a traditional auctioneer into a premier, global omnichannel marketplace.

Recent Financial Performance

In Q3 2025, total gross transaction value ("GTV") increased 7% year over year to $3.9 billion. Total revenue increased 11% year over year to $1.1 billion. Service revenue increased 8% year over year to $845.0 million.

Net income increased 25% year over year to $95.2 million. Net income available to common stockholders increased 21% year over year to $80.7 million. Diluted adjusted earnings per share available to common stockholders increased 31% year over year to $0.93 per share. Adjusted earnings before interest, taxes, depreciation and amortization ("EBITDA") increased 16% year over year to $327.7 million.

"GTV growth this quarter was broad-based across every sector, reflecting the dedication of our teammates and our commitment to being trusted partners," said Jim Kessler, CEO of RB Global. "Our newly implemented operating model brings the leaders closer to the customer and sets the stage for the next generation of growth and shareholder value creation."

Operational Improvements

"By reducing the sign-to-settle cycle time through a combination of branch incentives, IAA loan payoff, total procurement and our virtual inspection platform, we have effectively added approximately 25% incremental capacity in our yards compared to pre-transaction levels," according to the CEO.

For insurance partners, RB Global reported significant operational improvements, including enhanced tow performance (from 89% to 99.5%), approximately 20% reduction in assign-to-settle cycle time, and a 200 basis point increase in gross returns. These improvements were achieved through strategic tow asset deployment, data-driven incentives, and AI-powered sales decision tools.

2025 Outlook

Looking ahead, RB Global has updated its full-year 2025 financial outlook, projecting GTV growth between 0% to 1% and adjusted EBITDA ranging from $1,350 to $1,380 million. The company remains focused on enhancing customer experience and expanding its market presence to drive sustainable long-term growth.

RB Global agreed to acquire Smith Broughton Auctioneers and Allied Equipment Sales in Western Australia for $38 million. Kessler called the businesses "a highly capable team of sales professionals with deep local relationships and market knowledge."

For investors: The post-IAA integration is progressing well, with operational synergies materializing through reduced cycle times and enhanced yard capacity. Management's decision to tighten GTV guidance while raising EBITDA guidance signals focus on margin improvement over top-line growth in the near term.

XI. The Business Model Deep Dive

Revenue Streams

RB Global generates revenue through multiple channels that together create a diversified, resilient model:

Service Revenue (78.5% of total): The core transaction-based revenue from conducting auctions and marketplace sales. This includes:

- Seller Commissions: Fees charged to consignors for selling their equipment through auctions, typically a percentage of the sale price

- Buyer Premiums: Fees charged to successful bidders on top of the hammer price

- Marketplace Services: Fees for transportation, logistics, inspection, and other value-added services

Inventory Sales Revenue: On rare occasions, Ritchie Bros. purchases equipment directly and resells it. This provides flexibility to accommodate customer needs but involves balance sheet risk.

RB Global's shift to service-based revenue, now 78.5% of total, drives robust growth, supported by acquisitions and higher take rates from value-added services. The IAA acquisition has pivoted growth dynamics.

The Multi-Channel Platform

RB Global now operates one of the most comprehensive asset disposition platforms globally:

- Ritchie Bros. Auctioneers: Live unreserved auctions with online bidding at 40+ permanent sites

- IAA: Digital marketplace for salvage vehicles with 210+ facilities

- IronPlanet: Online marketplace with IronClad Assurance equipment certification

- Marketplace-E: Reserved price online marketplace

- GovPlanet: Government surplus equipment platform

- TruckPlanet: Commercial truck and trailer marketplace

- Mascus: European equipment listing service

- Rouse Services: Data analytics and fleet management

- SmartEquip: Equipment lifecycle and parts procurement platform

Network Effects and the Flywheel

The core competitive advantage remains the two-sided network effect:

In total, more than $200 million of equipment can be sold at major auctions, but the majority of money is spent by online bidders in Canada, the United States and around the world.

Cross-selling opportunities: IAA's 210+ locations create potential touchpoints for Ritchie Bros. equipment sales, while IAA customers gain access to broader disposition options. The combined yard network provides logistics advantages neither business could achieve alone.

Data advantage: Combined transaction data across construction equipment and automotive salvage creates unique market intelligence that informs pricing, demand forecasting, and customer acquisition.

XII. Competitive Analysis: Porter's Five Forces & Strategic Position

Threat of New Entrants: LOW-MEDIUM

Barriers are substantial but not insurmountable:

- Physical Infrastructure: RB Global operates 250+ facilities globally. Replicating this yard network would require billions in capital and years of execution.

- Network Effects: The buyer-seller flywheel took decades to build. New entrants must solve the chicken-and-egg problem of attracting sellers without buyers and vice versa.

- Data Moat: Decades of transaction history create pricing intelligence that newcomers cannot replicate.

- Brand Trust: The unreserved auction model requires trust that takes years to establish.

However: Technology has lowered some barriers for online-only players targeting specific niches. Pure-play digital marketplaces can compete for certain segments without physical infrastructure.

Bargaining Power of Suppliers (Consignors): MEDIUM

Large equipment owners (construction companies, rental fleets, insurance companies) have alternatives:

- Direct sales to dealers or end users

- Competitor auction houses

- Online marketplaces (Facebook Marketplace, Machinery Trader)

Mitigating factors: The unreserved model's liquidity and price realization attract sellers. Value-added services (financing, logistics, data) create switching costs. For insurance companies in the salvage market, the duopoly structure limits alternatives.

Bargaining Power of Buyers: LOW-MEDIUM

Buyers benefit from: - Price transparency through the auction format - Access to massive inventory selection - Online bidding convenience

Limiting factors: Premium equipment often sells at only one or two major auction houses. Buyers seeking specific assets have limited alternatives, especially in the salvage market duopoly.

Threat of Substitutes: MEDIUM

Alternative disposition methods include: - Direct dealer trade-ins - Private sales through brokers - Online classifieds (eBay, Facebook Marketplace) - Manufacturer remarketing programs

Mitigating factors: For insurance total-loss vehicles, the salvage auction remains the most efficient disposition method. For construction equipment, the liquidity and global buyer reach of major auction houses is difficult to replicate through alternatives.

Competitive Rivalry: MEDIUM-HIGH

In construction equipment: The market is fragmented with 200+ competitors. Ritchie Bros. is dominant but faces ongoing pressure from regional auctioneers and online marketplaces.

In automotive salvage: A durable duopoly with IAA/RBA controls 80% of the U.S. salvage market. Copart is dominant in its industry. For decades, Copart has acquired land in key cities around the US. As a result of zoning restrictions and the growth of American cities, Copart's land position would be impossible to replicate today.

The competitive dynamic with Copart is crucial. While the salvage market is a duopoly, Copart has historically operated with higher margins and stronger technology investments. The difference between IAA and Copart beyond sheer scale is that Copart has been more on the leading edge of technology. Copart, heading into the pandemic, was already fully online with virtual bidding and virtual auctions, whereas IAA wasn't fully online at the start of the pandemic.

Hamilton Helmer's 7 Powers Framework

Network Effects: ✓ Strong in both construction equipment and salvage automotive. More buyers attract more sellers, which attracts more buyers. The combined IAA-Ritchie Bros. network amplifies this effect.

Counter-Positioning: Partial. The unreserved model was counter-positioning in the 1960s-1990s. Today, competitors have largely adopted similar formats.

Switching Costs: ✓ Moderate-high. Insurance companies and large fleet operators have operational integrations with IAA/Ritchie Bros. Data history, inspection reports, and logistics relationships create friction.

Branding: ✓ The Ritchie Bros. name carries significant trust in the equipment world. IAA is a recognized brand among insurance adjusters.

Cornered Resource: ✓ Physical yard network represents a cornered resource in the salvage market. Zoning restrictions make replication nearly impossible in key markets.

Scale Economies: ✓ Technology platform costs spread across larger transaction volumes. Yard infrastructure amortizes over higher throughput.

Process Power: Partial. The unreserved auction process is well-established but not uniquely proprietary.

XIII. Key Risks and Overhangs

Cyclicality Exposure

Construction equipment volumes correlate with capital investment cycles. During downturns, consignment volumes can decline significantly as projects are delayed or cancelled.

Mitigation: The IAA acquisition diversified revenue toward automotive salvage, which is less cyclical. Total-loss vehicles occur throughout economic cycles, and higher vehicle complexity actually increases salvage volumes during challenging economic periods.

Integration Execution Risk

The IAA acquisition was transformative but complex. Integration of different technology platforms, sales cultures, and operating models creates execution risk.

Current status: Management reports significant progress on integration, with cycle time improvements and capacity gains materializing. CEO Jim Kessler expressed pride in the company's 2024 achievements, highlighting significant progress on strategic priorities. CFO Eric J. Guerin emphasized the team's financial discipline, noting enhanced operational efficiency, strategic investments in long-term growth, and a substantial reduction in leverage.

Competition from Copart

In the salvage market, Copart operates with higher margins, stronger technology, and owns rather than leases most of its land. Copart operates with a 33.45% net margin versus 21.34% industry average.

If Copart continues to widen its operational advantages, IAA/RB Global could lose market share over time despite the duopoly structure.

Leverage

The IAA acquisition was partially debt-financed. While leverage is being reduced, elevated debt levels constrain financial flexibility and increase vulnerability to unexpected downturns.

Management Turnover

The departure of CEO Ann Fandozzi and CFO Eric Jacobs in 2023 created temporary uncertainty. New CEO Jim Kessler appears to have stabilized operations, but leadership transitions in the midst of major integrations add execution risk.

XIV. Investment Thesis: Bull & Bear Cases

Bull Case

-

Secular Tailwinds in Salvage: Rising vehicle complexity, aging car parc, and increasing repair costs will continue driving total-loss frequency higher. This creates durable volume growth in the salvage market regardless of economic cycles.

-

Integration Synergies Materializing: The operational improvements already visible (25% capacity increase, 20% cycle time reduction) suggest meaningful cost synergies beyond initial projections.

-

Data Moat Deepening: Combined equipment and automotive transaction data creates unique market intelligence. AI-powered pricing and inspection tools will enhance competitive positioning.

-

Global Expansion Opportunity: IAA's international footprint was limited compared to Copart. The combined company can accelerate international growth, particularly in Europe and emerging markets.

-

Multiple Re-Rating Potential: If margins expand toward Copart levels, the stock could command a higher multiple. The transformation from cyclical auctioneer to diversified marketplace platform may not be fully reflected in valuation.

Bear Case

-

Copart's Structural Advantages: Copart owns most of its land, has higher margins, and invests more aggressively in technology. The competitive gap could widen despite the duopoly structure.

-

Construction Cycle Risk: Equipment volumes remain exposed to construction spending cycles. A prolonged downturn could pressure the CC&T segment.

-

Leverage Constraints: Elevated debt limits flexibility for opportunistic M&A and exposes the company to interest rate risk.

-

Integration Complexity: Large acquisitions frequently destroy value. Technology platform integration and cultural alignment remain ongoing challenges.

-

Disintermediation Risk: Digital platforms (Facebook Marketplace, equipment-specific marketplaces) could gradually erode market share at the margin, particularly for smaller equipment.

XV. Key Performance Indicators (KPIs) to Watch

For investors tracking RB Global's ongoing performance, three metrics matter most:

1. Gross Transaction Value (GTV) Growth

GTV measures the total value of assets sold through RB Global's platforms. This is the top-line metric that drives service revenue and indicates market share trajectory.

Why it matters: GTV growth reflects the health of the buyer-seller flywheel. Declining GTV signals either market share loss or cyclical weakness.

Current status: Management tightened full-year GTV guidance to 0%-1%, down from 0%-3%. The guidance was tightened rather than raised, reflecting conservative outlook for Q4.

2. Service Revenue Take Rate

Take rate measures service revenue as a percentage of GTV. This metric reflects pricing power and the success of value-added services.

Why it matters: Rising take rates indicate ability to capture more value from each transaction through buyer premiums and ancillary services.

Current status: Service revenue take rate expanded 20 basis points year over year to 21.7% driven by a higher buyer fee rate structure, partially offset by lower marketplace services revenue and a lower average seller commission rate.

3. Adjusted EBITDA Margin (as % of GTV)

This measures operating profitability relative to transaction volume, the most relevant efficiency metric for a marketplace business.

Why it matters: Margin expansion indicates operating leverage and integration synergy realization. Margin compression signals competitive pressure or cost inefficiency.

Current status: Adjusted EBITDA as a percentage of GTV expanded to 8.4%, up from 7.8% in the prior year. This margin improvement reflects the early impact of transformation initiatives and underscores ability to drive leverage in the model as the company scales.

XVI. Conclusion: The Furniture Store Legacy

In that Scout hall in Kelowna in 1958, three brothers discovered something profound: when you remove the friction and uncertainty from a marketplace—when buyers know that the highest bid wins and sellers know their assets will sell—extraordinary value creation becomes possible.

Dave Ritchie's insight wasn't complicated. Treat customers fairly. Keep your word. Make the auction transparent. These principles built a $16 billion marketplace empire across 170 countries.

The company Dave and his brothers built has transformed dramatically—from furniture to bulldozers, from Scout halls to 250+ permanent facilities, from shouted bids to AI-powered virtual inspections. But the core insight remains unchanged: trust is the ultimate competitive advantage in marketplace businesses.

"Treat your customers like your friends, and they will always be your customers," Dave Ritchie would say. Simple wisdom, but hard to execute consistently across decades and continents. RB Global's market position today reflects that consistency.

The IAA acquisition represents the biggest bet in company history—a $7.3 billion wager that the Ritchie Bros. operating model can improve an underperforming asset in the attractive salvage duopoly. Early results are encouraging. But the competitive battle with Copart will play out over years, not quarters.

For long-term investors, the question is whether RB Global can close the margin and technology gap with Copart while maintaining its position in construction equipment. The physical infrastructure moat, combined with network effects and data advantages, creates durable competitive positioning. But complacency in a consolidating industry is always dangerous.

As one longtime executive noted: "I wouldn't say the year I started that we were a one-trick pony, but we were probably a two- or three-trick pony. Now, we've got so many channels and opportunities to provide that we didn't have before."

From chrome-legged tables in a furniture store to $16 billion in annual transactions—the Ritchie brothers' accidental discovery continues to compound.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube