PTC: The CAD Revolution That Built the Digital Thread

I. Introduction & Episode Roadmap

Picture this: It's 1985, and engineers at Boeing are hunched over drafting tables, meticulously drawing aircraft components by hand. Each design change ripples through hundreds of paper drawings, taking weeks to propagate. Meanwhile, in a modest office in Massachusetts, a Russian mathematician named Samuel Geisberg is scribbling equations that would fundamentally transform how humanity designs and builds everything from coffee makers to spacecraft. Today, that company—PTC Inc.—commands ARR growth in the low double-digits with 11% year-over-year constant currency ARR growth in its most recent quarter. What began as a parametric CAD revolution has morphed into something far more ambitious: a digital thread connecting every aspect of how products are conceived, designed, manufactured, and serviced. It's a $2+ billion revenue business that touches nearly every physical product you interact with daily.

Yet here's what's fascinating: PTC isn't the CAD market leader by revenue. It's not the biggest PLM vendor. It doesn't dominate IoT platforms. But somehow, this Boston-based company has carved out one of the most defensible positions in industrial software by being perpetually ahead of the curve—parametric modeling in 1988, internet-based PLM in 1998, IoT platforms in 2013, and now industrial AI and digital twins.

The PTC story is really three stories intertwined. First, it's a tale of technical innovation—how a mathematical insight about parametric relationships revolutionized engineering design. Second, it's a masterclass in strategic pivots—how a company reinvented itself from a CAD vendor to a digital transformation platform without losing its core. And third, it's a case study in the economics of enterprise software—how switching costs, network effects, and platform dynamics create extraordinary moats in seemingly commoditized markets.

So how did a company that nearly everyone in tech has heard of, but few truly understand, become the connective tissue of modern manufacturing? How did they navigate four decades of technological upheaval while competitors with deeper pockets fell behind? And what does their journey tell us about the future of industrial software in an AI-powered world?

Let's start where all great enterprise software stories begin: with a painful problem that everyone had accepted as unsolvable.

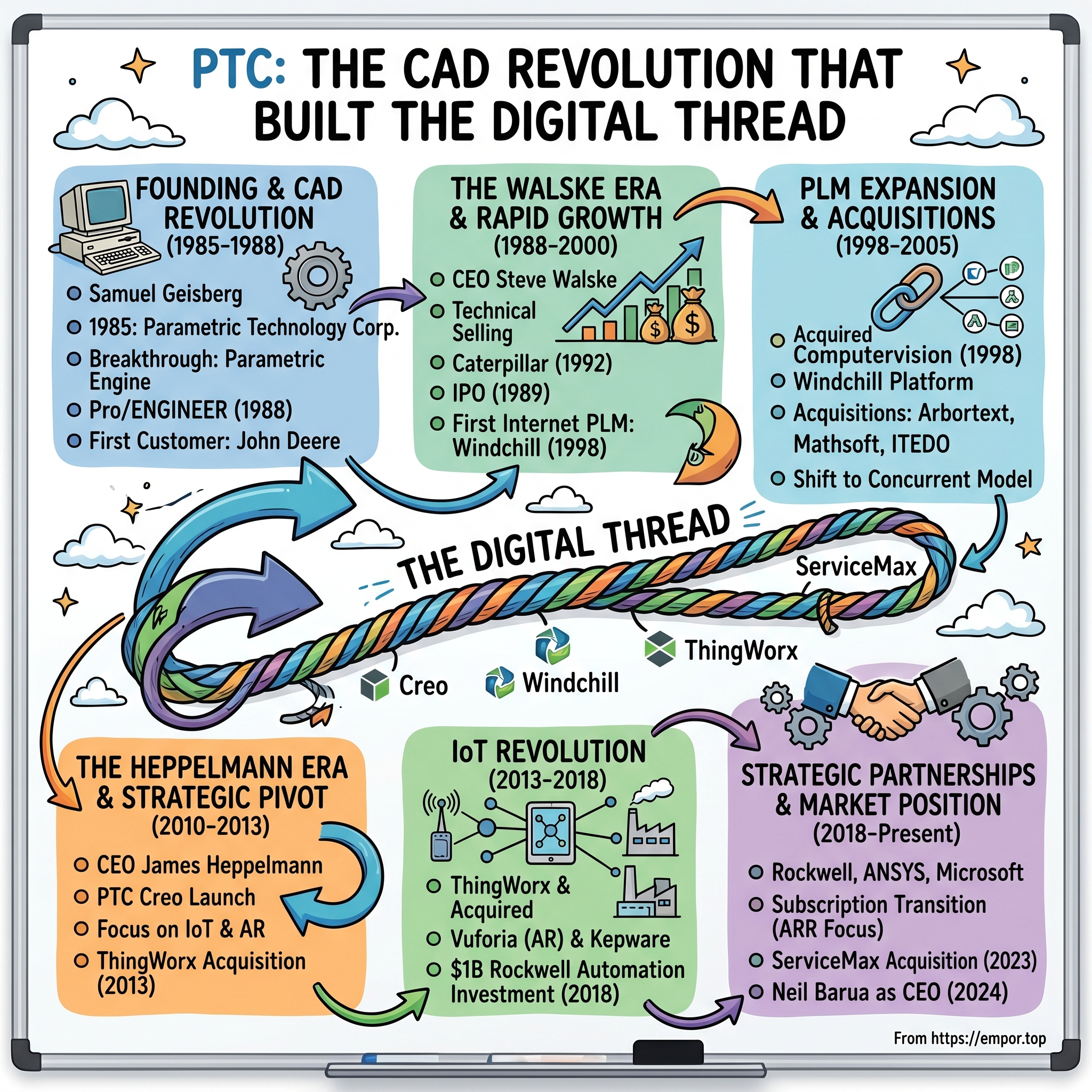

II. The Founding Story & CAD Revolution (1985–1988)

The year was 1985, and the computer-aided design industry was in a peculiar state. Companies like Computervision and Intergraph dominated with systems that cost upward of $100,000 per seat. Engineers worked on proprietary Unix workstations, drawing lines and curves that were essentially digital versions of paper blueprints. Change a single dimension? You'd better be prepared to manually update every related drawing—a process that could take days or weeks for complex assemblies.

Enter Samuel Geisberg, a mathematics professor who had emigrated from the Soviet Union with a radically different vision for how computers should handle design. While working at Computervision, Geisberg had grown frustrated with the fundamental limitation of existing CAD systems: they captured the what of a design but not the why. Every line was just a line, every circle just a circle, with no understanding of the relationships between them.

Geisberg's breakthrough was deceptively simple yet mathematically elegant. What if, instead of drawing static geometry, engineers could define relationships between design elements? What if changing a single parameter—say, the diameter of a hole—could automatically cascade through an entire assembly, updating every dependent dimension? This wasn't just an incremental improvement; it was a complete reconceptualization of how computers should understand design intent.

In May 1985, Geisberg left Computervision to found Parametric Technology Corporation with Mike Payne, another Computervision veteran who had previously worked at Prime Computer and Applicon. They weren't the typical Silicon Valley entrepreneurs—no garage, no venture capital pilgrimage to Sand Hill Road. Instead, they raised $5 million from Burr, Egan, Deleage & Company, a Boston-based venture firm that specialized in enterprise software. The investors weren't buying into hype; they were betting on a fundamental technological shift.

The technical challenge was immense. Geisberg needed to create what he called a "parametric engine"—a constraint solver that could handle thousands of interdependent relationships in real-time. This wasn't just a coding problem; it required innovations in computational geometry, numerical methods, and user interface design. The team worked in almost monastic isolation, burning through their initial capital as they built and rebuilt the core engine.

By late 1987, they had a working prototype that they quietly began showing to potential customers. The demonstrations were almost magical to engineers who had spent their careers manually propagating design changes. Change the length of a shaft, and watch as every bearing, housing, and mounting bracket automatically adjusted. Modify a clearance specification, and see the entire assembly reconfigure itself to maintain proper tolerances.

But the real validation came in early 1988 when John Deere, the agricultural equipment giant, became PTC's first customer. This wasn't a small pilot or proof of concept—Deere's engineers immediately recognized that parametric modeling could fundamentally change how they designed everything from tractors to harvesting equipment. They didn't just buy licenses; they became evangelists, showing other companies what was possible when design intent was captured alongside geometry.

When PTC officially shipped Pro/ENGINEER in 1988, it wasn't entering a market—it was creating one. The product was expensive, difficult to learn, and required powerful workstations. But for companies designing complex mechanical systems, the productivity gains were undeniable. An engineer could accomplish in hours what previously took days. Design iterations that once required armies of drafters could be explored by a single person.

The industry giants initially dismissed Pro/ENGINEER as a niche product for power users. Computervision executives privately called it "too complex for mainstream adoption." Autodesk, focused on the lower end of the market with AutoCAD, saw it as irrelevant to their 2D drafting customers. This dismissive attitude would prove to be a fatal strategic error.

What the incumbents missed was that PTC wasn't just selling software—they were selling a new way of thinking about design. Parametric modeling wasn't just faster; it fundamentally changed what was possible. Engineers could now explore "what-if" scenarios, optimize designs through iterative refinement, and maintain design intent throughout the product development process. Companies that adopted Pro/ENGINEER didn't just become more efficient; they became more innovative.

By the end of 1988, PTC had generated over $10 million in revenue—extraordinary for a company selling a completely new category of software. But revenue was almost beside the point. What mattered was that they had proven something revolutionary: computers could understand not just the geometry of a design, but the intelligence behind it. The CAD industry would never be the same.

As word spread through the engineering community, a curious phenomenon emerged: Pro/ENGINEER users became almost cultish in their devotion. They formed user groups, shared techniques, and lobbied their companies to standardize on the platform. This wasn't just software adoption; it was a movement. And at its head was a new CEO who would transform PTC from a technology pioneer into an enterprise software juggernaut.

III. The Walske Era & Rapid Growth (1988–2000)

Steve Walske arrived at PTC in 1988 with a reputation as a hard-charging sales executive who had previously run worldwide sales at Metaphor Computer Systems. The board's decision to bring him in as CEO while Geisberg remained as CTO was strategic—they needed someone who could scale a sales organization while the founders focused on technology. What they got was a leader who would transform PTC into one of the most aggressive and successful enterprise software companies of the 1990s.

Walske's first insight was that Pro/ENGINEER's complexity was actually its moat. While competitors scrambled to add parametric features to their existing products, they were constrained by legacy architectures and customer bases that expected backward compatibility. PTC, starting from scratch, had built parametric modeling into the foundation. This wasn't a feature you could bolt on—it required rethinking the entire system from the ground up.

The company went public in 1989 at a $60 million valuation, raising capital that Walske immediately deployed into building a global sales force. But this wasn't traditional enterprise sales. Walske pioneered what he called "technical selling"—every sales rep was paired with an application engineer who could demonstrate Pro/ENGINEER's capabilities in the customer's specific domain. They didn't sell features; they solved engineering problems.

The breakthrough year was 1992 when Caterpillar Inc. became PTC's largest customer, standardizing on Pro/ENGINEER across their entire global engineering organization. This wasn't just a big deal financially—though the contract was worth tens of millions—it was a defining moment strategically. Caterpillar's adoption sent a signal to the entire discrete manufacturing industry: parametric modeling wasn't experimental anymore. It was the future.

Walske's sales strategy was brilliantly ruthless. He identified that once an engineering team adopted Pro/ENGINEER, switching costs became astronomical. It wasn't just about learning new software—all the parametric relationships, design intent, and institutional knowledge became locked into PTC's proprietary format. He priced accordingly, knowing that once customers were in, they were essentially captured.

By 1994, PTC had grown to over $200 million in revenue with operating margins exceeding 30%. But Walske saw a bigger opportunity. Engineers were creating incredible designs in Pro/ENGINEER, but the rest of the organization—manufacturing, purchasing, service—couldn't access this rich design data. The design might be parametric, but the business process was still paper-based.

This led to PTC's second major innovation: Windchill, launched in 1998 as the industry's first internet-based Product Lifecycle Management (PLM) system. While Pro/ENGINEER captured design intelligence, Windchill managed it across the entire product lifecycle. It was a browser-based system that allowed anyone in the organization to access, review, and collaborate on product data without needing expensive CAD software.

The Windchill development was a massive bet—PTC invested over $100 million in building the platform while maintaining its CAD market position. Walske was essentially funding a startup inside a public company. The technical challenges were immense: managing complex CAD data over 1990s internet connections, ensuring data security, handling version control across global organizations. Many board members were skeptical. Why risk the CAD cash cow to chase an unproven market?

But Walske understood something fundamental about enterprise software: the company that controls the data controls the customer. Windchill wasn't just about collaboration; it was about making PTC indispensable to the entire product development process. Once a company's product data lived in Windchill, switching to a competitor became almost impossible. The validation came spectacularly in 1998 when PTC acquired its former rival Computervision Corporation. This wasn't just any acquisition—Computervision had been the CAD industry leader in the 1980s, the company Geisberg had left to start PTC. Now, a decade later, the student was buying the master. While the acquisition price wasn't publicly disclosed, industry analysts estimated it at several hundred million dollars, giving PTC access to Computervision's extensive customer base and distribution network.

By 1999, PTC announced it had 25,000 customers, spanning aerospace, automotive, industrial equipment, and consumer products. The company had grown from a startup challenging the establishment to becoming the establishment itself. Revenue approached $800 million annually, with Pro/ENGINEER and Windchill forming a product development platform that competitors struggled to match.

But perhaps Walske's greatest achievement was cultural. He instilled a fierce competitiveness at PTC that bordered on aggression. Sales teams were incentivized not just to win deals but to displace competitors entirely. The company became known for its "rip and replace" strategy—going into accounts dominated by competitors and systematically converting entire engineering organizations to PTC. It was expensive, time-consuming, and often brutal. It was also remarkably effective.

The financial performance during this period was extraordinary. PTC's stock price increased over 20-fold from its IPO to the peak in 2000. The company consistently delivered 30%+ revenue growth with operating margins that made other software companies envious. Wall Street loved the story: recurring maintenance revenue, high switching costs, and a massive market opportunity as companies digitized their product development processes.

Yet by 2000, cracks were beginning to show. The CAD market was maturing, with new competitors like SolidWorks (ironically founded by former PTC employees) attacking from below with easier-to-use, lower-cost solutions. The dot-com bubble was inflating, and enterprise software spending was about to hit a wall. Most importantly, Walske's aggressive culture, while effective for conquest, was less suited for retention and organic growth.

The transition from Walske's growth-at-all-costs mentality to a more sustainable business model would require new leadership and a fundamental rethinking of PTC's strategy. The company had won the CAD war, but the battlefield was about to shift dramatically.

IV. The Computervision Acquisition & PLM Expansion (1998–2005)

The Computervision acquisition in December 1998 was more than a business transaction—it was PTC swallowing its philosophical opposite. Where PTC had built everything from scratch with parametric modeling at its core, Computervision had accumulated technologies through acquisitions, creating a patchwork of solutions held together by integration layers. Where PTC targeted power users with complex but capable software, Computervision served a broader market with simpler tools. The cultural clash was immediate and profound.

Jim Heppelmann, then running the Windchill division, later recalled the integration meetings as "like mixing oil and water." Computervision engineers, many of whom had been in the industry since the mainframe era, viewed PTC's parametric approach as unnecessarily complex. PTC engineers saw Computervision's CADDS software as outdated legacy code. The tension was palpable in the newly combined offices, with employees literally sitting on opposite sides of the cafeteria.

But Walske and his team saw something beyond the technology assets. Between the two companies, they had over 190,000 seats of high-end design software installed at over 20,000 customers. This wasn't just market share—it was data gravity. Every one of those seats represented years or decades of design data that would be extraordinarily painful to migrate to a competitor. The acquisition wasn't about technology convergence; it was about customer capture.

The real prize, however, was Windchill's emergence as a true PLM platform. While competitors were still thinking about CAD data management, PTC was building something far more ambitious: a system that could manage every piece of information about a product from conception through retirement. The browser-based architecture that had seemed risky in 1998 now looked prescient as companies embraced web technologies.

By 2002, PTC made another bold move with the release of Pro/ENGINEER Wildfire, the first CAD system to support web-based services. This wasn't just a feature update—it was a fundamental rearchitecting that allowed Pro/ENGINEER to operate as part of a connected ecosystem rather than a standalone tool. Engineers could now collaborate in real-time, share designs across the globe, and integrate CAD data directly with enterprise systems.

The acquisition spree continued through the early 2000s, but now with a different strategy. Instead of buying competitors for market share, PTC targeted specific technologies that extended the PLM vision. In 2005, they acquired Arbortext for technical publishing technology, recognizing that product documentation was as important as product design. In 2006, they acquired Mathsoft for its engineering calculation software, bringing analytical capabilities directly into the design environment. That same year, they acquired ITEDO for its 3D technical illustration software, addressing the growing need for visual communication of complex products.

Each acquisition followed a pattern: identify a critical but fragmented part of the product lifecycle, acquire the best-in-class solution, and integrate it into the Windchill platform. This wasn't the conglomerate approach of the old Computervision—it was systematic platform building. The message to customers was clear: you could cobble together solutions from multiple vendors, or you could get everything from PTC, fully integrated and managed through a single platform.

The financial impact was significant. By 2005, PTC had crossed $700 million in annual revenue with over 40% coming from PLM-related products and services. More importantly, the business model was shifting. Where CAD licenses were typically one-time purchases with annual maintenance, PLM solutions involved ongoing subscriptions, implementation services, and continuous expansion. The revenue became more predictable, the customer relationships deeper.

But the real transformation was in how PTC's customers thought about product development. The old model was sequential: design, then manufacture, then service. PLM enabled a concurrent model where manufacturing constraints informed design decisions, service data drove product improvements, and everyone worked from a single source of truth. Companies that fully embraced this approach reported 25-50% reductions in product development time and dramatic improvements in product quality.

The challenge was complexity. As PTC's portfolio expanded, so did the difficulty of implementation. A full PLM deployment could take years and cost millions of dollars. Smaller companies that had embraced Pro/ENGINEER found themselves priced out of the broader PLM vision. Meanwhile, competitors like Dassault Systèmes with CATIA and Siemens with NX were building their own PLM platforms, often with more elegant architectures unburdened by legacy code.

By 2007, PTC made another strategic acquisition that would prove pivotal: CoCreate for its direct modeling technology. This addressed a fundamental limitation of parametric modeling—the difficulty of making late-stage design changes without breaking the parametric history tree. CoCreate's approach allowed engineers to directly manipulate geometry without worrying about constraints and relationships. It was heresy to parametric purists, but it solved real problems for real customers.

The PLM expansion era established PTC as more than a CAD company—it was now a platform company. But success brought new challenges. The software had become so complex that even expert users struggled to leverage its full capabilities. Implementation costs often exceeded software costs. And most critically, the market was shifting again. The cloud was coming, software-as-a-service was disrupting enterprise software, and a new generation of companies was emerging that had never used traditional CAD/PLM tools.

The company needed fresh leadership and a new vision. It would find both in an unexpected place: a startup CEO who had never worked in CAD but understood something fundamental about where the industry was heading.

V. The Heppelmann Era & Strategic Pivot (2010–2013)

On October 1, 2010, James Heppelmann assumed the role of president and chief executive officer of Parametric. His appointment raised eyebrows across the industry. While Heppelmann had been with PTC since the Windchill acquisition in 1998, he wasn't a CAD guy. He came from the enterprise software world, having founded Windchill Technology before its acquisition. His competitors at Autodesk, Dassault, and Siemens were led by mechanical engineers who had grown up in the industry. Heppelmann was a computer scientist who saw the world differently.

His first major decision sent shockwaves through the PTC user community: renaming Pro/ENGINEER to PTC Creo and promising the market product design software that was scalable, open, and easy-to-use. This wasn't just a rebranding—it was a fundamental rethinking of PTC's flagship product. The new Creo platform would unite PTC's parametric modeling from Pro/ENGINEER with the direct modeling from CoCreate, allowing users to work in whichever paradigm made sense for their task.

The old guard was horrified. Pro/ENGINEER users had invested decades mastering the software's complexities. They wore their expertise like a badge of honor. Now Heppelmann was talking about making it "easy-to-use"? It felt like betrayal. User forums erupted with complaints. Several large customers threatened to switch to competitors.

But Heppelmann saw what others missed: the CAD market was bifurcating. At the high end, customers needed ever more sophisticated capabilities for designing jet engines, medical devices, and automobiles. At the low end, a new generation of engineers raised on SketchUp and consumer-friendly interfaces expected software to be intuitive. The old Pro/ENGINEER served neither market well—too complex for casual users, too rigid for power users who needed flexibility.

The Creo strategy was brilliant in its simplicity. Instead of one monolithic application, PTC created a family of apps, each focused on specific tasks. Creo Parametric for detailed design. Creo Direct for quick modifications. Creo Simulate for analysis. Creo Illustrate for technical documentation. Users could move seamlessly between apps, using the right tool for each job. It was the CAD equivalent of moving from Microsoft Office to Google's suite of focused web apps.

But Heppelmann's real insight was recognizing that the future of manufacturing wasn't in the design office—it was on the factory floor and in the field. Products were becoming smarter, embedded with sensors and connectivity. The Internet of Things (IoT), still a buzzword in 2010, was about to transform manufacturing. And PTC, with its deep relationships with manufacturers and its PLM platform managing product data, was uniquely positioned to capitalize on this shift.

The company began investing heavily in what Heppelmann called "closed-loop lifecycle management." The idea was elegant: connect smart products back to their digital twins in PLM, creating a continuous feedback loop from field performance to design improvement. A jet engine could report its operating parameters back to Windchill, where engineers could compare actual performance to design intent. Manufacturing defects discovered in the field could automatically trigger design reviews. Service technicians could access complete product information through augmented reality interfaces.

This vision required capabilities PTC didn't have. The company had spent 25 years perfecting tools for creating products but had no expertise in connecting to them, analyzing their data, or visualizing information in new ways. Heppelmann knew that building these capabilities organically would take too long. The market was moving too fast, and competitors like GE and Siemens were already making big IoT moves. So in December 2013, PTC made its boldest move yet: acquiring ThingWorx, an Exton, Pennsylvania-based IoT platform company, for $112 million, plus a possible earn-out of up to $18 million. The acquisition raised eyebrows across the industry. This implied a 12x revenue multiple for the purchase price—an extraordinary valuation even in the frothy tech market of 2013. ThingWorx had less than $10 million in annual revenue. PTC was essentially paying for potential, not performance.

But Heppelmann understood something his critics didn't: PTC's formula was to find the best-in-breed components of an IoT Platform, in approximately the $100M range, and integrate them under the PTC brand. ThingWorx wasn't just software—it was a rapid application development platform that could connect any device, analyze its data, and build applications without traditional coding. It was the missing piece that would transform PTC from a company that helped design products to one that could make them intelligent.

The integration strategy was crucial. Rather than keeping ThingWorx as a standalone division, Heppelmann embedded it deeply into PTC's existing products. Windchill could now manage not just product designs but also real-time operational data from those products. Creo designers could simulate how their products would perform based on actual field data. Service technicians could use augmented reality to see inside machines, overlaying digital information on physical products.

By 2013, Heppelmann was articulating a vision that seemed almost prophetic: "Products are becoming smart and connected. Every product will eventually have sensors, software, and connectivity. The companies that can design these products, connect them, analyze their data, and service them through their entire lifecycle will win. Everything else is just features."

The strategic pivot was working. While traditional CAD/PLM revenue growth had slowed to single digits, the new IoT and AR initiatives were growing at 40%+ annually. More importantly, they were pulling through sales of traditional products. Companies bought ThingWorx to connect their products, then realized they needed Windchill to manage the data and Creo to redesign for connectivity. The ecosystem effect that Heppelmann had envisioned was becoming reality.

As 2013 ended, PTC stood at an inflection point. It had successfully navigated the transition from growth to maturity in its core markets while positioning itself at the forefront of the next wave of industrial innovation. But the real test was yet to come: could PTC execute on this ambitious vision while competing against giants like GE, Siemens, and a host of IoT startups flush with venture capital?

VI. The IoT Revolution: ThingWorx & Beyond (2013–2018)

The ThingWorx acquisition closed on December 30, 2013—literally the last business day of the year. Within 48 hours, Heppelmann had the ThingWorx founders, Russell Fadel and Rick Bullotta, in Boston mapping out an integration plan that would typically take months. The urgency was palpable. GE had just announced Predix, their industrial IoT platform. Siemens was investing billions in MindSphere. The race for industrial IoT dominance had begun, and PTC couldn't afford to stumble.

The first challenge was cultural. ThingWorx was a 45-person startup that had operated like a skunkworks—fast, agile, unburdened by process. PTC was a 6,000-person public company with quarterly earnings calls, SOX compliance, and enterprise customers expecting five-nines reliability. Fadel later described the early days as "drinking from a firehose while building the firehose."

Heppelmann's masterstroke was keeping ThingWorx's development velocity while wrapping it in PTC's enterprise capabilities. The ThingWorx team retained significant autonomy, operating almost like an internal startup. They could push updates weekly while PTC's traditional products followed annual release cycles. This dual-speed IT model was revolutionary for a company of PTC's vintage. By mid-2014, the ThingWorx momentum was undeniable. But Heppelmann spotted a critical gap: while ThingWorx could build applications quickly, it lacked deep expertise in device connectivity and management. Enter Axeda, the largest of PTC's IoT acquisitions. In July 2014, PTC announced it would acquire Axeda for $170 million in cash—a company with 150+ customers processing hundreds of millions of machine messages daily.

Axeda wasn't as sexy as ThingWorx. It was infrastructure—the plumbing that connected devices to the cloud securely and reliably. But Axeda's remote monitoring and management software was utilized to add advanced device management and remote management capabilities to their IoT stack. While ThingWorx was the brain, Axeda was the nervous system. Together, they formed a complete IoT platform that could compete with anyone.

The acquisition pace was relentless. In 2015, PTC acquired Vuforia from Qualcomm for $65 million—an augmented reality platform that seemed disconnected from PTC's core business. Industry analysts were puzzled. What did AR have to do with CAD or IoT? But Heppelmann saw the connection clearly: AR was how humans would interact with smart, connected products. A service technician could point a tablet at a machine and see its operational data overlaid on the physical product. An engineer could visualize IoT data in the context of the actual device.

The strategic vision was crystallizing: PTC was building what Heppelmann called the "digital thread"—a continuous flow of data from initial design through manufacturing, operation, and service. Every acquisition added a new capability to this thread. Kepware (acquired in 2016 for $105 million) provided industrial connectivity, supporting over 150 different industrial protocols. ColdLight (acquired in 2015) brought machine learning and predictive analytics.

After 5 acquisitions, PTC is now seen as a visionary in industrial IoT both by industry peers and by market analysts. PTCs formula is to find the best-in-breed components of an IoT Platform, in approximately the $100M range, and integrate them under the PTC brand.

But the real validation came from customers. In 2016, Caterpillar—still PTC's largest customer—deployed ThingWorx to monitor over 400,000 connected assets globally. They could predict equipment failures days or weeks in advance, optimize fuel consumption based on real-world usage patterns, and offer new service models based on actual equipment utilization. The ROI was measured in hundreds of millions of dollars.

The transformation wasn't without casualties. PTC's traditional CAD business, while still profitable, was increasingly seen as legacy. Long-time employees who had built their careers on Pro/ENGINEER felt marginalized as resources shifted to IoT and AR. User conferences that once focused on parametric modeling techniques now featured keynotes on digital transformation and Industry 4.0.The financial markets also loved the story. By 2017, PTC was generating over $1.1 billion in annual revenue. But the real validation came in June 2018 when Rockwell Automation announced a $1 billion equity investment in PTC, acquiring an 8.4% ownership stake at $94.50 per share—an 8.6% premium to the closing price. Blake Moret, Rockwell's CEO, joined PTC's board. This wasn't just an investment; it was a strategic partnership that would combine PTC's ThingWorx IoT, Kepware industrial connectivity, and Vuforia AR platforms with Rockwell's FactoryTalk MES and Analytics platforms.

The Rockwell investment of $1B for 8% of PTC is further evidence of the brilliance of PTC's IoT acquisition strategy. Rockwell wasn't just buying equity; they were buying into a vision where IT and OT (operational technology) converged, where the digital and physical worlds merged seamlessly. The partnership gave PTC instant credibility with process manufacturers who had traditionally been Rockwell's domain, while Rockwell gained access to cutting-edge IoT and AR capabilities without having to build them from scratch.

By 2018, the transformation was complete. PTC had successfully pivoted from a CAD company to a digital transformation platform. The company that had started by revolutionizing how products were designed now enabled those products to be smart, connected, and continuously optimized throughout their lifecycle. Revenue from IoT and AR solutions was growing at 30-40% annually, while traditional CAD/PLM grew in the low single digits.

But perhaps the most impressive achievement was maintaining customer loyalty through this massive transition. Despite the strategic shifts, despite the resource reallocation, despite the cultural changes, PTC retained its core enterprise customers. Companies like Caterpillar, John Deere, and Boeing didn't just stick with PTC—they embraced the new vision, becoming showcase examples of digital transformation.

The IoT revolution at PTC proved that even mature enterprise software companies could reinvent themselves. But it required courage to cannibalize existing revenue streams, vision to see where the market was heading, and execution excellence to integrate multiple acquisitions while maintaining operational stability. As 2018 ended, PTC stood as a fundamentally different company than it had been just five years earlier, positioned at the intersection of every major trend in industrial technology.

VII. Strategic Partnerships & Market Position (2018–Present)

The Rockwell partnership announcement in June 2018 marked more than a financial milestone—it signaled PTC's arrival as a kingmaker in the industrial software ecosystem. Within months, competitors scrambled to form their own alliances. Siemens doubled down on MindSphere partnerships. Dassault Systèmes accelerated its 3DEXPERIENCE platform strategy. The message was clear: the future of industrial software would be determined not by individual vendors but by ecosystems.

PTC also announced major strategic partnerships with ANSYS and Microsoft in 2018, each addressing different pieces of the digital transformation puzzle. The ANSYS partnership integrated simulation directly into the design process, allowing engineers to validate designs in real-time without switching applications. The Microsoft alliance brought Azure cloud capabilities to PTC's solutions, enabling global deployments at unprecedented scale.

But Heppelmann understood that partnerships alone wouldn't sustain growth. The company needed to fundamentally change its business model. The traditional perpetual license model—where customers paid large upfront fees—was becoming obsolete. Software-as-a-Service was eating the enterprise software world, and PTC couldn't remain immune.

The subscription transition, announced in earnest in 2019, was brutal. Revenue recognition rules meant that deals that would have generated $1 million in immediate revenue under the perpetual model now recognized only $200,000 in the first year under subscriptions. Wall Street hammered the stock. Activist investors circled. Employees worried about compensation tied to revenue targets that suddenly seemed impossible to hit. But Heppelmann held firm. He knew that strategically shifted towards a subscription-based revenue model would provide more predictable revenue streams and strengthen customer relationships. By 2020, the transition was largely complete. ARR (Annual Recurring Revenue) became the key metric, not license revenue. The predictability allowed PTC to invest more aggressively in R&D, knowing exactly what revenue would come in each quarter.

The strategy paid off spectacularly. By 2021, PTC's ARR exceeded $1.5 billion, with retention rates above 90%. The subscription model also enabled new pricing strategies—usage-based pricing for IoT, per-user pricing for AR, outcome-based pricing for digital twin solutions. Customers could start small and expand as they saw value, reducing the initial barrier to adoption.

In January 2023, PTC completed its acquisition of ServiceMax for $1.46 billion—paid in two stages with $808 million at closing and $650 million in October 2023. This wasn't just another tuck-in acquisition. ServiceMax brought cloud-native field service management (FSM) capabilities that completed PTC's vision of closed-loop lifecycle management. Now PTC could track a product from initial design through manufacturing, operation, and service—the complete digital thread.

The ServiceMax acquisition was particularly strategic because it was built on the Salesforce platform, giving PTC deep integration with CRM systems. This bridged a critical gap—PTC understood the product, Salesforce understood the customer, and together they could deliver unprecedented insights about how products performed in the field and how customers actually used them.

By 2024, PTC delivered solid ARR and cash flow, with year-over-year ARR growth in the low double-digits and cash flow growth above 20%. The company now serves aerospace, retail/footwear/apparel, automotive, industrial equipment, consumer products, electronics, and high tech industries. More impressively, 95% of the Fortune 500 discrete manufacturing companies are customers—a testament to PTC's entrenchment in critical business processes.

The competitive landscape has evolved dramatically. Autodesk, once dismissed as a low-end competitor, has moved aggressively upmarket with Fusion 360. Dassault Systèmes has built a formidable platform with 3DEXPERIENCE. Siemens has integrated its software acquisitions into a comprehensive digital industries portfolio. Yet PTC has maintained its differentiation through the completeness of its digital thread vision and the depth of its IoT/AR capabilities. Leadership transition came in February 2024 when Neil Barua, the former CEO of ServiceMax, succeeded James Heppelmann as CEO. Barua brought a different perspective—he wasn't from the CAD world but understood SaaS, field service, and digital transformation from the customer's viewpoint. His appointment signaled PTC's evolution from a technology company selling to engineers to a business transformation partner selling to the C-suite.

Under Barua's leadership, PTC has focused on what he calls "the digital thread at scale"—helping enterprises not just pilot digital transformation but deploy it across thousands of products and millions of instances. The company's ARR growth of 11% year-over-year on a constant currency basis in Q1'25 demonstrates the durability of the business model even in challenging macroeconomic conditions.

The partnership ecosystem continues to expand. The Rockwell relationship has been extended multiple times, with nearly 250 new customers added through the partnership. Microsoft's investment in industrial IoT has made Azure the preferred cloud platform for PTC's solutions. The ANSYS partnership has evolved into deep technical integration that blurs the line between design and simulation.

Today, PTC's market position is paradoxical. It's neither the largest CAD vendor (that's Autodesk by user count), nor the most valuable (that's Dassault Systèmes by market cap), nor the most comprehensive (that's Siemens by portfolio breadth). Yet PTC has arguably the most complete vision for how physical products will be designed, manufactured, and serviced in the digital age. The digital thread isn't just marketing speak—it's a technical reality that connects every aspect of a product's lifecycle.

VIII. Technology Deep Dive: The Product Portfolio

The elegance of PTC's product portfolio lies not in individual components but in how they interconnect. Eight core product families: Creo, Windchill, Mathcad, Integrity, Servigistics, ThingWorx, ServiceMax, and Arbortext Editor each serve specific functions, but their true power emerges when deployed as an integrated digital thread.

Start with Creo, the descendant of Pro/ENGINEER that still forms PTC's technical foundation. Modern Creo is barely recognizable from its parametric modeling origins. It now encompasses generative design, where AI algorithms create thousands of design options based on constraints and objectives. Real-time simulation runs in the background, validating designs as they're created. Augmented reality capabilities allow designers to visualize products at full scale in real environments. The software that once required weeks of training now includes role-based apps that casual users can master in hours.

But Creo's real innovation is its openness. Unlike competitors who lock users into proprietary formats, Creo can read and write virtually any CAD format without translation. This "United Nations of CAD" approach reflects a pragmatic reality: no enterprise uses a single CAD system. Boeing might design airframes in CATIA, engines from GE arrive in NX format, and suppliers send components in SolidWorks. Creo becomes the universal translator, maintaining associativity across this Tower of Babel of formats.

Windchill, the PLM backbone, has evolved from a data management system to what PTC calls a "digital thread orchestrator." It doesn't just store CAD files; it manages the entire product definition—requirements, specifications, simulations, manufacturing instructions, service procedures. Every piece of product information lives in Windchill with full traceability from initial concept to end-of-life disposal.

The sophistication shows in details. Change a material specification in Windchill, and it automatically triggers compliance checks against environmental regulations, updates cost projections based on commodity prices, and alerts manufacturing about required process changes. This isn't just automation—it's intelligence embedded in the platform.

ThingWorx represents PTC's bet on the future: that every product will eventually be connected. But unlike consumer IoT platforms focused on simple sensors, ThingWorx handles industrial complexity. A single jet engine generates terabytes of data per flight. A manufacturing line might have thousands of sensors updating every millisecond. ThingWorx doesn't just collect this data—it contextualizes it against the digital twin, identifies anomalies through machine learning, and triggers workflows across the enterprise.

The platform's brilliance lies in its abstraction layers. Developers don't need to understand industrial protocols or real-time databases. They build applications using visual tools, dragging and dropping widgets that represent complex industrial processes. A dashboard showing real-time equipment effectiveness that would have taken months to develop can be created in days.

Vuforia, the AR platform acquired from Qualcomm, seemed like an odd addition until you understand Heppelmann's vision: AR is how humans will interact with digital twins. A service technician points a tablet at a machine and sees its internal components, operating parameters, and service history overlaid on the physical device. Assembly workers see step-by-step instructions projected onto their work surface. Quality inspectors compare physical products to their digital definitions in real-time.

The technology is sophisticated—computer vision algorithms that can recognize objects from any angle, tracking systems that maintain registration even as users move, rendering engines that seamlessly blend digital and physical. But the interface is simple: point, look, understand. It's the consumerization of industrial technology.

ServiceMax brings the last mile of the digital thread: what happens after products leave the factory. Every service call, every part replacement, every software update is captured and fed back into the product definition. This isn't just about tracking warranty claims—it's about understanding how products actually perform in the field versus how they were designed to perform.

The integration with IoT creates predictive service models. A pump showing early signs of cavitation triggers a service ticket before failure occurs. The system automatically schedules a technician with the right skills, ensures the correct parts are available, and provides AR-guided repair instructions. The entire service history feeds back to engineering, informing the next generation of designs.

Mathcad, often overlooked in discussions of PTC's portfolio, provides the mathematical foundation for engineering calculations. While Excel might suffice for simple calculations, Mathcad handles the complex mathematics of engineering—differential equations, matrix operations, unit conversions. More importantly, it maintains the intellectual property of engineering knowledge. The calculations that determine safety factors, performance margins, and design limits live in Mathcad, fully traceable and auditable.

The integration story extends beyond PTC's own products. CAD portfolio solutions enable companies to author product data. PLM portfolio solutions enable companies to manage product data and orchestrate processes. Software can be delivered on premises, in the cloud or in a hybrid model. This flexibility reflects the reality of enterprise IT—some data must remain on-premises for security reasons, while other processes benefit from cloud scale and accessibility.

The technical architecture underlying this portfolio is remarkably sophisticated. Microservices allow independent scaling of components. GraphQL APIs enable efficient data queries across systems. Event-driven architectures ensure real-time synchronization. Container orchestration provides deployment flexibility. Yet this complexity is hidden from users, who see only a unified interface to their product data.

AI and machine learning are embedded throughout, not as buzzword features but as fundamental capabilities. Generative design in Creo uses evolutionary algorithms to explore design spaces. Windchill employs natural language processing to extract requirements from documents. ThingWorx applies anomaly detection to identify equipment issues. ServiceMax uses predictive analytics to optimize technician scheduling. These aren't separate AI products—they're intelligence woven into the fabric of the platform.

The result is a product portfolio that mirrors the complexity of modern manufacturing while hiding that complexity from users. An engineer in Creo doesn't need to know that their design change triggered seventeen downstream processes. A service technician using AR doesn't understand the computer vision algorithms making it possible. A executive viewing a digital twin dashboard doesn't see the billions of data points being processed in real-time. The technology becomes invisible, letting users focus on their work rather than their tools.

IX. Playbook: Business & Investing Lessons

The PTC story offers a masterclass in enterprise software strategy, particularly relevant as every software company claims to be a "platform." But what distinguishes PTC's platform evolution from countless failed attempts? The answer lies in understanding the physics of enterprise software moats.

First lesson: Platform transitions require customer captivity before vision. When PTC began its pivot from CAD to PLM to IoT, it already had thousands of customers with millions of parametric models that couldn't easily migrate to competitors. This captive base provided the cash flow and patience needed for transformation. Companies attempting platform pivots without this foundation often run out of runway before achieving liftoff.

Consider the acquisition-led growth strategy. PTCs formula is to find the best-in-breed components of an IoT Platform, in approximately the $100M range, and integrate them under the PTC brand. This wasn't random shopping—it was systematic capability building. Each acquisition addressed a specific gap in the digital thread vision. ThingWorx for application development, Axeda for device management, Kepware for connectivity, Vuforia for visualization, ServiceMax for field service. The discipline was remarkable: PTC walked away from larger deals that didn't fit the strategy and overpaid for smaller ones that did.

The integration philosophy was equally important. Rather than maintaining acquired products as standalone divisions (the Oracle model) or completely absorbing them (the Cisco model), PTC chose selective integration. Core capabilities were woven into the platform while maintaining product identity where customers expected it. ThingWorx remained ThingWorx, but its data model integrated with Windchill. This preserved acquisition value while creating platform synergies.

Second lesson: Navigating technology disruptions requires cannabalizing yourself before others do. PTC's subscription transition was brutal—revenue declined, stock price crashed, employees revolted. But waiting would have been worse. By moving aggressively to subscriptions while they still had pricing power, PTC could set terms favorable to long-term value creation. Companies that wait until forced by competition typically transition on unfavorable terms.

The timing of technology adoption shows similar pattern recognition. PTC wasn't first to cloud CAD (that was Onshape), first to IoT platforms (that was GE), or first to AR (that was Microsoft). But they were first among traditional engineering software companies to commit fully to these technologies. This "fast follower" strategy avoided bleeding-edge risk while capturing early-mover advantages in their specific market.

Third lesson: Customer lock-in in enterprise software comes from workflow integration, not data hostage-taking. While competitors focused on proprietary formats to lock in customers, PTC built switching costs through process integration. A company using Windchill doesn't just store data there—their entire product development process runs through it. Engineering change orders, compliance workflows, supplier collaboration, manufacturing releases—all orchestrated by Windchill. Extracting data might be possible; extracting processes is practically impossible.

This extends to the partner ecosystem. By integrating deeply with ERP systems like SAP, simulation tools like ANSYS, and automation platforms like Rockwell, PTC made itself structurally important to enterprise IT architecture. Replacing PTC would require replacing or reconfiguring dozens of connected systems—a risk no IT organization willingly takes.

Fourth lesson: The subscription model playbook for enterprise software requires managing three constituencies simultaneously. Wall Street wants predictable growth, customers want cost predictability, and employees want achievable targets. PTC's solution was elegant: multi-year contracts with annual payment terms. Customers got price protection, Wall Street got revenue visibility, and sales teams got credit for total contract value. This triangulation is harder than it appears—most companies optimize for one constituency at the expense of others.

The financial engineering was sophisticated. Rather than a binary shift from perpetual to subscription, PTC offered multiple transition paths. Large customers could maintain perpetual licenses with subscription support. New customers defaulted to subscription. Mid-market customers got hybrid models. This segmented approach minimized revenue disruption while moving inexorably toward the subscription end state.

Fifth lesson: Building moats in industrial software requires domain expertise plus technology innovation. Pure technology companies like Google or Amazon struggle in industrial markets because they lack domain knowledge. Traditional industrial companies like GE or Honeywell struggle with software because they think like equipment manufacturers. PTC's advantage came from being a software company that deeply understood engineering workflows.

This shows in product decisions. While competitors added features engineers requested, PTC added capabilities engineers didn't know they needed. Generative design wasn't on any requirements list—engineers didn't know it was possible. IoT connectivity wasn't a CAD requirement—until PTC showed how it transformed product development. AR visualization seemed like science fiction—until service technicians experienced 50% reduction in repair times.

The moat compounds over time. Each customer deployment generates domain expertise that improves the product. Each product improvement attracts more sophisticated customers who push the platform further. Each platform enhancement creates more integration points that deepen lock-in. It's a virtuous cycle that becomes increasingly difficult for competitors to break.

The capital allocation strategy deserves particular attention. PTC has spent over $3 billion on acquisitions since 2010, yet maintained reasonable leverage ratios. The secret was timing: buying when targets were subscale, integrating to achieve synergies, then using improved cash flow for the next acquisition. This self-funding model reduced dilution while maintaining strategic flexibility.

For investors, PTC illustrates the power of transformation when executed properly. The company's evolution from perpetual licenses to subscriptions, from CAD to PLM to IoT, from desktop to cloud—each transition destroyed short-term value while creating long-term value. Understanding these J-curves is crucial for evaluating enterprise software companies. The worst time to sell is often during the transition; the best time to buy is when the transition seems riskiest.

X. Analysis & Bear vs. Bull Case

The investment case for PTC requires understanding both its remarkable transformation and the substantial challenges ahead. At current levels, with ARR growing 12% year-over-year on a constant currency basis, the company presents a fascinating study in mature software economics.

Financial Performance: The Numbers Behind the Narrative

PTC's financial evolution reflects its strategic transformation. Revenue growth has moderated from the 30%+ rates of the early 2000s to low double-digits ARR growth today, but the quality of that revenue has dramatically improved. Subscription revenue now dominates, providing predictability that perpetual licenses never could. Free cash flow grew 25% year-over-year, demonstrating the model's cash generation capabilities even during heavy investment periods.

Operating margins tell a nuanced story. The shift to subscriptions initially compressed margins as revenue recognition rules deferred income. But as the subscription base has matured, margins have expanded. The company now balances growth investment with profitability, a discipline that eluded it during the Walske era's growth-at-any-cost mentality.

The Bull Case: Platform Power in the Digital Age

The optimistic view starts with PTC's position at the intersection of every major industrial trend. Digital transformation, Industry 4.0, IoT, AI, sustainability—PTC has solutions for each. More importantly, these aren't disconnected point products but integrated capabilities within a unified platform.

The competitive moat appears formidable. With 95% of Fortune 500 discrete manufacturers as customers, PTC has relationships that span decades. The digital thread vision—connecting design through manufacturing to service—is more complete than any competitor's offering. While Autodesk excels at design, Siemens at manufacturing, and Salesforce at service, only PTC credibly spans the entire lifecycle.

Market dynamics favor PTC's positioning. As products become more complex—think electric vehicles with millions of lines of code—the need for sophisticated PLM grows exponentially. Traditional document-based approaches simply can't handle modern product complexity. PTC's model-based systems engineering capabilities position it to capture this complexity-driven growth.

The subscription transition, while painful, has created a superior business model. ARR growth of 12% might seem modest, but it's remarkably consistent. Customer retention rates above 90% provide a stable base for growth. The predictability allows for more aggressive R&D investment, creating a virtuous cycle of product improvement and customer satisfaction.

Geographic expansion offers another growth vector. While PTC is strong in North America and Europe, Asia-Pacific remains underpenetrated. As manufacturing shifts to these regions, PTC's global platform becomes increasingly valuable. The ability to manage product development across time zones and languages is a competitive advantage that's difficult to replicate.

The ServiceMax acquisition opens an entirely new market. Field service management is a $20+ billion market growing at 15% annually. PTC's ability to connect service data with design and manufacturing data creates unique value propositions. When a field failure occurs, engineers can immediately understand whether it's a design issue, manufacturing defect, or service problem.

The Bear Case: Structural Headwinds and Execution Risks

The pessimistic view starts with competition. Autodesk has successfully moved upmarket with Fusion 360, offering cloud-native CAD at a fraction of Creo's cost. Dassault Systèmes continues to win flagship accounts with its 3DEXPERIENCE platform. Siemens has integrated its acquisitions into a formidable digital industries portfolio. PTC no longer competes against stumbling giants but agile, well-funded rivals.

Technology risk looms large. PTC's core products were architected in the pre-cloud era. While they've been adapted for cloud deployment, they're not cloud-native. Startups like Onshape (ironically founded by former PTC employees and later acquired by PTC) show what's possible with modern architectures. The technical debt of legacy code could become an increasing burden.

Integration complexity threatens the platform vision. PTC has acquired over 20 companies in the past decade. While each acquisition made strategic sense individually, the collective complexity is staggering. Different code bases, data models, and user interfaces create integration challenges that consume enormous resources. Customers complain about the difficulty of implementing the full platform vision.

Market saturation in core verticals presents growth challenges. PTC already serves most large discrete manufacturers. Growing within these accounts requires either displacing entrenched competitors or expanding into new use cases. Both paths face resistance. IT organizations, burned by failed digital transformation initiatives, are increasingly skeptical of vendor promises.

The macroeconomic environment adds uncertainty. Manufacturing is cyclical, and PTC's revenue correlates with industrial production. Economic downturns don't just slow new sales—they can trigger downgrades as customers cut costs. While subscription models provide some insulation, they're not immune to economic cycles.

Valuation concerns persist. At current multiples, PTC trades at a premium to both traditional CAD/PLM vendors and modern SaaS companies. This premium assumes successful execution of the digital thread vision. Any stumble in integration, customer adoption, or competitive positioning could trigger multiple compression.

Technology Risks: The Innovator's Dilemma

PTC faces the classic innovator's dilemma. Its most profitable customers are large manufacturers with complex needs and conservative IT approaches. Serving these customers well requires maintaining compatibility with legacy systems, supporting on-premise deployments, and moving cautiously on new technologies.

Meanwhile, digital natives are building products differently. They use cloud-native tools, embrace agile methodologies, and expect software to be intuitive and self-service. PTC's enterprise-grade solutions, with their power and complexity, can seem overwrought to this new generation.

Artificial intelligence presents both opportunity and threat. While PTC has embedded AI throughout its portfolio, it lacks the data scale of Google or the computing infrastructure of Amazon. Specialized AI companies are targeting specific use cases—generative design, predictive maintenance, quality inspection—with point solutions that may be superior to PTC's integrated approach.

The Verdict: Transformation Complete, Evolution Continues

PTC stands at an inflection point. The heroic transformation from CAD vendor to digital thread platform is largely complete. The company has successfully navigated multiple technology transitions, built a comprehensive portfolio, and established a sustainable business model. But past success doesn't guarantee future performance.

The bull case rests on execution—continuing to integrate acquisitions, delivering on the platform vision, and maintaining technology leadership. The bear case assumes that complexity, competition, or complacency will slow growth and compress multiples. Reality will likely fall somewhere between these extremes.

For long-term investors, PTC represents a bet on the digitization of physical products. If you believe that every manufactured product will eventually have a digital twin, that AR will transform how humans interact with machines, and that IoT will make everything connected and intelligent, then PTC is positioned to capture enormous value. If you believe these trends are overhyped or that nimbler competitors will win, then PTC's premium valuation seems unjustified.

XI. Epilogue & "If We Were CEOs"

Standing at the precipice of 2025, PTC embodies the paradox of successful transformation: the very achievement of your vision necessitates a new one. The company that revolutionized CAD with parametric modeling, pioneered internet-based PLM, and led the charge into industrial IoT must once again reimagine itself—not from weakness, but from strength.

If we were running PTC, the strategic priorities would focus on three horizons: defending the core, scaling the platform, and inventing the future.

Defending the Core: The Unglamorous Necessity

The first priority would be addressing the technical debt accumulated through two decades of acquisitions and architectural evolution. This isn't sexy work—refactoring code, standardizing data models, harmonizing user interfaces—but it's essential. The promise of the digital thread rings hollow if customers need professional services armies to connect products that are supposedly integrated.

We'd establish a "Platform 3.0" initiative, rebuilding core components with cloud-native architectures while maintaining backward compatibility. This would be a five-year, billion-dollar investment that Wall Street would hate and customers would barely notice—until they experienced 10x performance improvements and 90% reduction in implementation time.

The competitive response would be surgical rather than sweeping. Instead of trying to match Autodesk's broad market approach or Siemens' manufacturing depth, we'd double down on PTC's sweet spot: complex, regulated products with long lifecycles. Aerospace, defense, medical devices, industrial equipment—industries where the cost of failure is catastrophic and the value of complete digital threads is highest.

Scaling the Platform: The Network Effects Play

The second priority would be transforming PTC from a vendor to an ecosystem orchestrator. The digital thread vision is too broad for any single company to deliver. Instead of trying to build everything, we'd open the platform to third-party developers, creating the "iOS of industrial software."

This means exposing every API, documenting every interface, and providing development tools that make building on PTC as easy as creating iPhone apps. Revenue sharing models would incentivize innovation while maintaining quality through certification programs. Imagine thousands of developers creating specialized applications for specific industries, use cases, or regions—all running on PTC's platform.

The Rockwell partnership provides the template. Rather than competing with automation vendors, we'd form similar alliances with leaders in adjacent spaces: simulation (deeper ANSYS integration), manufacturing execution (partnership with Tulip or similar), quality management (alignment with Sparta or equivalents). Each partnership would be more than reselling—it would be technical integration that creates unique value.

Geographic expansion would follow a "land and expand" model. Rather than trying to replicate the direct sales model globally, we'd partner with regional champions who understand local markets. They'd provide implementation and support while PTC provided the platform. This asset-light approach would accelerate international growth while minimizing risk.

Inventing the Future: The Bold Bets

The third priority would be placing aggressive bets on technologies that could transform manufacturing. Three areas stand out:

Quantum Computing for Design Optimization: Current generative design algorithms are constrained by classical computing limitations. Quantum computers could explore design spaces that are computationally intractable today. We'd partner with quantum computing companies to develop algorithms for materials optimization, topology optimization, and multi-physics simulation. The company that cracks quantum-enhanced design will have an insurmountable advantage.

Industrial Metaverse Infrastructure: While Meta focuses on consumer virtual worlds, the real value is in industrial applications. Engineers collaborating in virtual spaces, AI agents participating in design reviews, digital twins that are indistinguishable from physical products. We'd build the infrastructure layer that makes industrial metaverse applications possible—not the applications themselves, but the platforms others build upon.

Sustainability as a Core Constraint: Every product decision now has environmental implications. We'd embed sustainability metrics throughout the digital thread—carbon footprint in design, energy consumption in manufacturing, recyclability in service. This isn't corporate virtue signaling; it's recognizing that sustainability is becoming a fundamental design constraint like cost or performance.

The Cultural Revolution

Technology and strategy mean nothing without culture. PTC's culture has evolved from engineering excellence to sales aggression to platform innovation. The next evolution must be customer obsession—not in the clichéd sense, but in fundamental restructuring around customer outcomes.

This means changing incentive structures. Sales compensation based on customer success metrics, not just bookings. Engineering bonuses tied to customer adoption rates, not feature delivery. Support evaluated on problem prevention, not ticket closure. Every employee should wake up thinking about customer outcomes, not internal metrics.

We'd also address the talent challenge. PTC competes for engineers with Google, for salespeople with Salesforce, for data scientists with Tesla. Winning requires more than competitive compensation—it requires mission. The story we'd tell: PTC is building the software infrastructure for physical products that will define the next century. Every plane that flies safer, every medical device that saves lives, every machine that runs cleaner exists because of PTC's digital thread.

The Acquisition Strategy

The acquisition playbook would evolve from capability buying to ecosystem building. Instead of acquiring competitors or adjacent technologies, we'd focus on companies that accelerate platform adoption. This might include:

- Vertical SaaS companies that have deep domain expertise in specific industries

- System integrators with implementation expertise and customer relationships

- Data analytics companies that can extract insights from the digital thread

- Workflow automation companies that can orchestrate processes across the platform

Each acquisition would be evaluated not on standalone value but on ecosystem contribution. How does this accelerate platform adoption? How does it strengthen network effects? How does it deepen customer lock-in?

The 10-Year Vision

By 2035, we envision PTC not as a software company but as the central nervous system of global manufacturing. Every product designed, built, and serviced would touch PTC's platform in some way. Not because PTC does everything, but because PTC enables everything.

The financial model would evolve accordingly. Revenue would come not just from software licenses but from transaction fees on platform usage, success fees on outcome improvements, and data monetization from anonymized insights. The company would be valued not on revenue multiples but on the economic value flowing through its platform.

This vision requires courage. Courage to cannibalize existing revenue streams. Courage to partner with potential competitors. Courage to invest in unproven technologies. Courage to admit when strategies aren't working and pivot quickly.

Most importantly, it requires remembering what made PTC great in the first place: solving impossible problems. Parametric modeling was impossible until it wasn't. Internet-based PLM was impossible until it wasn't. Connecting every product to the internet was impossible until it wasn't.

The next impossible problem is creating truly intelligent products—not just connected, but genuinely intelligent. Products that learn from their environment, adapt to their users, and improve over time. Products that are sustainable by design, resilient by nature, and delightful to use. This is the future PTC must enable.

The path won't be linear. There will be failed acquisitions, competitive threats, and technology disruptions we can't foresee. But the company that survived the transition from minicomputers to PCs, from desktop to internet, from perpetual to subscription, from CAD to IoT—that company has proven its adaptability.

PTC's next chapter won't be written in code or quarterly earnings. It will be written in the products that its software enables—the electric aircraft that transform transportation, the personalized medical devices that save lives, the sustainable manufacturing processes that preserve our planet. That's the real measure of success: not what PTC builds, but what PTC enables others to build.

The digital thread that Sam Geisberg envisioned when he sketched those first parametric equations is no longer just about connecting design to manufacturing. It's about connecting human creativity to physical reality, transforming ideas into products that improve lives. That thread, woven through four decades of innovation, continues to strengthen. And its most important patterns are yet to be woven.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube