Powell Industries: The Electrification Play Nobody Saw Coming

The William Powell Foundation Story

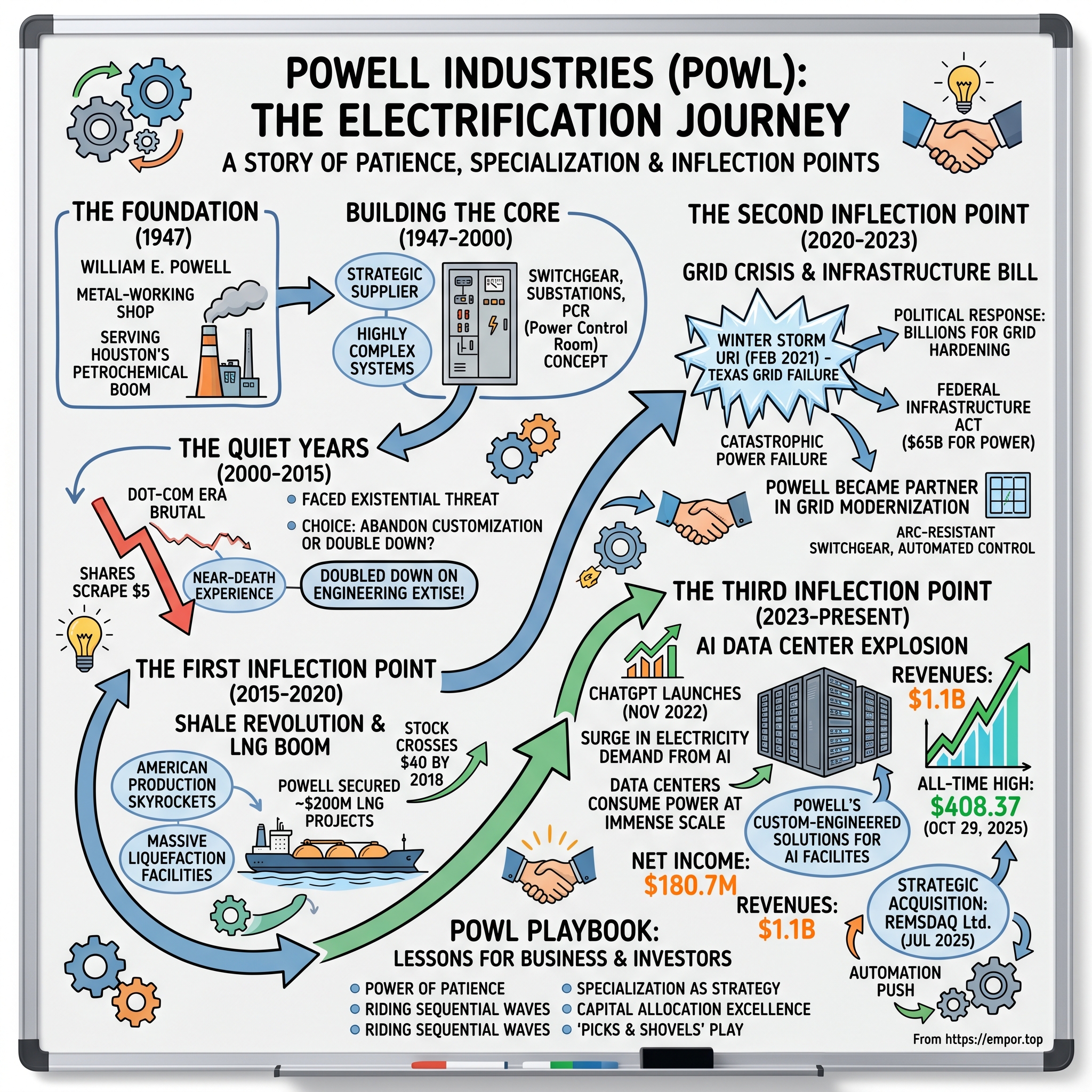

William E. Powell didn't set out to build an empire when he opened his metal-working shop in 1947. Post-war Houston was booming, its skyline punctuated by refinery stacks and chemical plants that seemed to multiply by the month. Powell was founded in 1947 as a metal-working shop to support the local Houston, Texas petrochemical facilities. The timing was no accident—Houston was emerging as the undisputed energy capital of America, and Powell saw opportunity in the unglamorous work of keeping the lights on and the motors running.

The founder of Powell Industries was William E. Powell, who envisioned a business focused on metal-working to serve the growing petrochemical industry in the region. In those early days, Powell's shop was indistinguishable from dozens of others scattered across Houston's industrial districts. What set William Powell apart wasn't revolutionary technology or venture capital—it was an obsessive focus on solving the specific electrical problems that plagued Gulf Coast industries. Salt air corroded equipment. Hundred-degree summers stressed systems. Hurricane seasons brought challenges that manufacturers in Ohio or Pennsylvania never imagined.

The company's first breakthrough came in 1968, a full two decades after its founding. Powell developed the Power Control Room (PCR) concept for a project in Ponce, Puerto Rico for the Union Carbide Company. The PCR wasn't just a product—it was a philosophy. Rather than shipping individual components for field assembly, Powell pre-fabricated entire electrical control rooms that could be transported and installed as complete units. For chemical plants operating in remote locations or harsh environments, this was revolutionary. It cut installation time from months to weeks and reduced the risk of field errors that could cause catastrophic failures.

While they began small, the company has grown over the past six decades to become the strategic supplier of choice for highly complex and integrated systems for distribution and control of electrical energy and other critical processes. By the 1970s, Powell had established itself as the go-to provider for custom electrical solutions in the most demanding industrial environments on earth. But this was still very much a regional player, known along the Gulf Coast but virtually invisible to the broader industrial world.

The decision to go public in 1968 on the NASDAQ exchange marked Powell's first step toward national ambitions. Yet even as a public company, Powell retained its family business DNA. The company first offered its shares to the public on January 6, 1978, with its stock becoming available on Nasdaq under the ticker POWL. The Powell family maintained significant ownership and operational control, with leadership passing from William to his son Thomas, who would serve as CEO and Chairman for multiple stints spanning nearly four decades.

Building the Core Business (1947-2000)

The half-century from Powell's founding to the millennium represents a masterclass in patient, methodical business building. While tech startups chased exponential growth and quick exits, Powell pursued something different: becoming indispensable to the industries that literally powered America.

The company grew to become the strategic supplier of choice for highly complex and integrated systems for the distribution and control of electrical energy and other critical processes, with Powell now operating as a global company focusing on the future of electrical infrastructure through innovative technologies. Powell's product line evolved to encompass the full spectrum of electrical distribution and control equipment: integrated power control room substations, custom-engineered modules, electrical houses with integrated control systems, medium-voltage circuit breakers, monitoring and control communications systems, motor control centers, and bus duct systems.

What distinguished Powell wasn't just what they made, but how they approached each project. Every refinery had unique layouts. Every chemical plant faced different hazards. Every offshore platform battled distinct environmental challenges. Powell's engineers didn't offer catalog solutions—they designed bespoke systems that accounted for everything from seismic activity to salt spray to the specific chemical compounds that might escape during a plant emergency.

This customization came at a price. Powell's products cost significantly more than standardized alternatives from giants like General Electric or Siemens. But for customers operating facilities where a single electrical failure could cause millions in downtime—or worse, loss of life—Powell's premium was insurance well bought. A refinery manager once explained it simply: "When you're processing 400,000 barrels a day, the difference between 99% and 99.9% reliability is measured in millions of dollars."

The company's principal products include integrated power control room substations, custom-engineered modules, electrical houses, medium-voltage circuit breakers, monitoring and control communications systems, motor control centers, switches, and bus duct systems, as well as traditional and arc-resistant distribution switchgears and control gears. These weren't just components—they were complete systems designed to work in voltages ranging from 480 volts to 38,000 volts, often in the harshest environments imaginable.

Through the oil crises of the 1970s, the industrial recession of the early 1980s, and the consolidation waves of the 1990s, Powell maintained its focus. While competitors chased diversification—moving into consumer products or financial services—Powell doubled down on industrial electrical systems. They expanded gradually, adding facilities when demand justified it, acquiring small specialized firms that enhanced their capabilities, but never straying from their core mission.

By 2000, Powell had built an enviable position: they were the premium provider in a niche market with high barriers to entry. Their engineers had decades of accumulated knowledge about the specific challenges facing petrochemical and energy facilities. They had longstanding relationships with every major oil company and chemical producer on the Gulf Coast. But as the new millennium dawned, these advantages suddenly seemed less valuable. The future appeared to belong to software, not switchgear.

The Quiet Years and Near-Death Experience (2000-2015)

The dot-com era was brutal for old-line industrial companies. As investors poured billions into anything with a website, manufacturers like Powell watched their valuations crater. The stock, which had traded in the $30 range through much of the late 1990s, began a long, grinding descent. By 2003, shares touched $8. By 2009, in the depths of the financial crisis, they scraped $5. For years, Powell shares languished below $20, forgotten by Wall Street, ignored by growth investors, written off as a dying relic of the rust belt somehow misplaced in Houston.

The existential threat wasn't just financial—it was strategic. Global giants like Siemens, ABB, and General Electric were consolidating the electrical equipment industry, using their scale to drive down costs and commoditize products that Powell had spent decades perfecting. These behemoths could lose money on switchgear while making it up in turbines or medical equipment. Powell had no such luxury. Every project had to pay its way.

Inside Powell's Houston headquarters, the mood was grim but not defeated. The company faced a choice that would define its next decade: abandon customization and compete on price, or double down on engineering expertise and accept being a niche player. Under the leadership of Thomas Powell, William's son who had taken the reins in the 1980s, the company chose the harder path. They would remain the Rolls-Royce of electrical distribution systems, even if it meant watching competitors capture market share with cheaper, standardized products.

This decision required painful discipline. While competitors automated production and moved manufacturing overseas, Powell kept its core operations in Houston. They invested in engineer training programs when others were cutting R&D budgets. They maintained excess capacity in their fabrication yards, knowing that when large projects came, customers would pay premiums for Powell's ability to deliver on tight deadlines.

The company also made strategic bets on emerging markets within their niche. As aging refineries required electrical system upgrades, Powell developed specialized retrofit solutions. When new environmental regulations demanded better monitoring and control systems, Powell's engineers designed products that exceeded requirements. They began exploring opportunities in renewable energy, though these remained a tiny fraction of revenues.

The financial results during this period tell a story of survival, not success. Revenues bounced between $200 million and $500 million annually, largely dependent on the timing of major projects. Margins compressed as customers, facing their own competitive pressures, demanded price concessions. Several times, Powell came close to being acquired by larger competitors, saved only by the Powell family's determination to maintain independence and a board that believed better days lay ahead.

By 2015, Powell Industries looked like a competent but unremarkable industrial company. Fiscal 2024 would eventually show tremendous growth in their largest markets, with the top line growing by 45%, but no one could have predicted that transformation during these lean years. The company had survived the commoditization threat, maintained its engineering excellence, and preserved its customer relationships. But survival isn't the same as success. Powell needed a catalyst—or better yet, multiple catalysts—to transform from a regional specialist into a critical enabler of American infrastructure.

The First Inflection Point: Shale Revolution & LNG Boom (2015-2020)

George Mitchell, the Texas wildcatter who pioneered hydraulic fracturing, probably never heard of Powell Industries. But Mitchell's innovation in extracting natural gas from shale rock would transform Powell's fortunes as dramatically as any Silicon Valley disruption. The shale revolution that exploded across Texas, North Dakota, and Pennsylvania in the mid-2010s created demand for electrical infrastructure on a scale unseen since the original oil boom.

The Permian Basin, that vast expanse of West Texas and southeastern New Mexico, became the epicenter of American energy renaissance. American production of LNG skyrocketed since the Shale Revolution, with LNG export capacity estimated to increase by around 50% over the next four years, proving to be a boon for Powell Industries as increased upstream drilling activity across major US basins and associated infrastructure gets built. Every drilling pad needed power distribution. Every pipeline compressor station required control systems. Every processing facility demanded electrical infrastructure that could operate reliably in the desert heat and dusty conditions.

But the real transformation came from liquefied natural gas. As America shifted from LNG importer to the world's largest exporter, massive liquefaction facilities sprouted along the Gulf Coast—directly in Powell's backyard. These weren't just big projects; they were behemoths. A single LNG train could cost $10 billion and require electrical systems comparable to a small city. Powell was awarded a large LNG project situated along the U.S. Gulf Coast during the quarter, marking just one of many such projects that would define this era.

Powell secured two large greenfield LNG projects along the US Gulf Coast, totaling ~$200 million during this period, but these numbers only hint at the transformation. Each LNG facility required thousands of electrical components operating in perfect synchronization. The cooling systems that liquefied natural gas to -260°F demanded precise control. The safety systems that prevented catastrophic failures needed triple redundancy. The harsh coastal environment—salt air, hurricanes, flooding—required equipment built to standards that few manufacturers could achieve.

Powell's decades of experience in Gulf Coast industrial projects suddenly became invaluable. They knew how to design systems that could survive Category 5 hurricanes. Their engineers understood the specific challenges of building on coastal soil that could liquefy during construction. They had relationships with every engineering firm and construction company working on these mega-projects. While international competitors struggled with American regulations and standards, Powell executed with the efficiency born from 70 years of regional expertise.

The financial impact was immediate and dramatic. Having recorded their second consecutive year of more than $1.0 billion in new orders, Powell continued to grow in traditional markets of oil & gas, petrochemical and electrical utilities, while diversifying in markets such as data centers, hydrogen, carbon capture and other alternative fuels. Order backlogs, which had languished around $200-300 million during the dark years, exploded past $1 billion. The stock, which had traded below $20 for most of the decade, crossed $40 by 2018.

But Powell's leadership, now under Brett Cope who had joined the company in 2010 and became CEO in 2016, understood this was just the beginning. Cope joined Powell in December 2010 as Vice President of Sales and Marketing and served as Senior Vice President and Chief Operating Officer since December 2015, after 20 years at ABB in roles of increasing responsibility. Cope brought a different perspective from his decades at ABB—he had seen how global players operated and understood that Powell's regional dominance could become a launching pad for something bigger.

The Second Inflection Point: Grid Crisis & Infrastructure Bill (2020-2023)

February 2021's Winter Storm Uri changed everything. The failure of Texas' power grid in February 2021 was one of the most severe energy crises in U.S. history, leaving millions without power for days in freezing temperatures. The images were surreal: Houston highways turned into ice rinks, Dallas skyscrapers dark against frozen skylines, and millions of Texans huddled around fireplaces and portable heaters while the most energy-rich state in America couldn't keep the lights on.

At least 246 people were killed directly or indirectly as a result of the crisis. The technical failure was comprehensive. Not only was there insufficient power generation capacity online, but also insufficient natural gas supply to power plants, with gas infrastructure failing due to inadequate winterization, causing gas supply to fall by 85%. Powell Industries, whose equipment had performed relatively well during the crisis, suddenly found itself at the center of a conversation about grid resilience that extended far beyond Texas.

The political and regulatory response was swift and unprecedented. Governor Greg Abbott declared that ERCOT reform was an emergency priority for the state legislature, and Congress launched an investigation into the power crisis requesting documents relating to winter weather preparedness. Texas allocated billions for grid hardening. The federal Infrastructure Investment and Jobs Act, passed in November 2021, included $65 billion for power infrastructure upgrades. Utilities that had deferred maintenance for decades suddenly had both the mandate and the money to modernize.

For Powell, this represented a fundamental shift in their market opportunity. Their end markets traditionally included oil and gas refineries and petrochemical plants, but now utilities became major customers. Electric Utility sector revenue increased 26% to $51.2 million in just one quarter of fiscal 2025, signaling a transformation in Powell's customer base.

The company's products—particularly their arc-resistant switchgear and automated control systems—were exactly what utilities needed to prevent another Uri-style catastrophe. These systems could detect and isolate faults before they cascaded through the grid. They could automatically reroute power during emergencies. Most importantly, they were built to operate in extreme weather conditions that standard equipment couldn't survive.

There have been significant improvements to the Texas electrical grid over the past two years, though the occurrence of no blackouts since February 2021 is a low bar to meet. The cold snap demonstrated that progress has been made, but exposed remaining vulnerabilities as electricity demand increases and extreme weather becomes more common.

Powell's response to this opportunity was strategic rather than opportunistic. They didn't just sell products to utilities; they became partners in grid modernization. Their engineers worked with utility planning departments to identify vulnerabilities. They developed new products specifically for grid resilience, including cold-weather packages that could maintain operations at temperatures that would have been unthinkable for Texas equipment just years earlier.

The infrastructure bill's impact extended beyond direct utility spending. Manufacturing reshoring, accelerated by supply chain disruptions during COVID-19, required massive investments in electrical infrastructure. New semiconductor fabs, battery plants, and steel mills—many supported by federal incentives—all needed the kind of sophisticated electrical systems that were Powell's specialty. The company that had spent decades serving Gulf Coast refineries suddenly found its expertise relevant to the entire American industrial renaissance.

By 2023, Powell's transformation was undeniable. Revenues totaled $1.0 billion, an increase of 45% compared to $699.3 million in the prior year, driven primarily by growth within the Oil & Gas and Petrochemical sectors which grew 53% and 97% respectively, while net income of $149.8 million increased 175%. The stock, which had traded around $40 at the beginning of 2021, crossed $100 by early 2023. But the biggest catalyst was yet to come.

The Third Inflection Point: AI Data Center Explosion (2023-Present)

November 30, 2022: ChatGPT launches. Within five days, it had a million users. Within two months, 100 million. The world suddenly understood that artificial intelligence wasn't science fiction—it was here, it was transformative, and it was hungry. Unimaginably hungry for electricity.

The numbers are staggering. Analysts project a 192.7% surge in EPS for Powell in 2024, jumping from $4.12 in 2023 to an estimated $12.06, with revenue expected to hit $1.05 billion—a 50.2% increase from 2023's $699 million. But these financial metrics only tell part of the story. The real transformation was in Powell's customer base and market position.

Training a large language model like GPT-4 requires as much electricity as thousands of American homes use in a year. Running these models for millions of users demands data centers that consume power at scales previously reserved for aluminum smelters or steel mills. The energy sector boomed as electricity demand surged, particularly from AI-driven data centres. Every major technology company—Amazon, Microsoft, Google, Meta—began a construction spree that dwarfed anything seen during the original internet boom.

These weren't traditional data centers with neat rows of servers. AI computing requires different architecture—massive GPU clusters generating tremendous heat, requiring cooling systems that themselves consume as much power as small towns. The electrical infrastructure for these facilities pushed into territory where Powell's expertise in industrial-grade power distribution became invaluable. Powell's diversification efforts continue to present new opportunities and awards across markets such as data centers, utilities, carbon capture, hydrogen, and more.

Powell's backlog today is more diverse across market sectors than ever before, increasingly comprised of rapidly expanding applications for custom-engineered products. Data centers now account for a significant and growing portion of Powell's revenue. But unlike the commodity server farms of the previous era, these AI facilities required customized solutions. Each hyperscaler had different architectures, different redundancy requirements, different expansion plans. Powell's decades of experience in custom engineering for industrial clients translated perfectly to these new digital factories.

The geographic distribution of these projects also played to Powell's strengths. While early data centers clustered in Northern Virginia and Silicon Valley, AI facilities spread across the country, seeking cheap power and favorable climates. Texas, with its deregulated energy market and business-friendly environment, became a major hub. Powell's relationships with Texas utilities and contractors, built over decades, provided a competitive advantage that no amount of marketing could replicate.

The technical challenges were immense. Data centers require 99.999% uptime—the famous "five nines" of reliability. Powell Industries designs tailored electrical solutions that manage power distribution, control, and monitoring across a voltage range of 480 to over 38,000 volts, with advanced insulation technology that safely handles high-energy electrical arcs. This wasn't just about keeping servers running; it was about maintaining precise power quality, managing harmonics from thousands of switching power supplies, and coordinating with utility grids that were themselves straining under unprecedented demand.

Powell's response revealed the company's evolution from equipment supplier to solutions provider. They didn't just ship switchgear; they designed complete electrical architectures. Their engineers worked with data center designers from conceptual planning through commissioning. They developed new products specifically for AI workloads—systems that could handle the rapid power fluctuations as GPU clusters cycled through training runs, equipment that could scale modularly as facilities expanded.

The stock market's reaction was explosive. From around $100 in early 2023, Powell shares rocketed past $400 by late 2024. The all-time high Powell Industries stock closing price was $408.37 on October 29, 2025, with the 52-week high stock price at $413.00. Volume surged as institutional investors discovered this hidden beneficiary of the AI boom. Unlike semiconductor stocks trading at nosebleed valuations or software companies with uncertain monetization paths, Powell offered something tangible: they made the physical infrastructure that every AI ambition required.

Strategic Acquisitions & Automation Push

July 15, 2025, marked a strategic inflection point that went largely unnoticed by mainstream financial media. Powell announced it had entered into a definitive agreement to acquire Remsdaq Ltd., a U.K.-based manufacturer of Remote Terminal Units for approximately $16.3 million. The combination of Powell's hardware and detection sensors with Remsdaq's Supervisory Control and Data Acquisition (SCADA) RTUs creates a highly synergistic integration.

To understand why this modest acquisition matters, consider the evolution of electrical infrastructure. For decades, substations and control rooms operated with minimal intelligence—circuit breakers tripped when overloaded, alarms sounded during faults, and human operators made decisions based on analog gauges and experience. But the complexity of modern grids, especially with renewable energy sources and bidirectional power flows from electric vehicles, demands something more sophisticated.

The acquisition advances Powell's key strategic initiative to expand its automation platform capabilities, positioning the Company to effectively meet the growing demand for more sophisticated solutions that enhance utility operational efficiency, system reliability and security. Remsdaq's RTUs act as the nervous system of smart grids, collecting thousands of data points per second, analyzing patterns, and enabling predictive maintenance that can prevent failures before they occur.

Brett Cope articulated the vision clearly: The addition of Remsdaq's people and technology are an important step towards our strategy to grow our Electrical Automation solutions. This wasn't about adding revenue—Remsdaq's contribution would barely move Powell's top line. It was about capability building, moving Powell from hardware provider to intelligent systems integrator.

The structure of the deal revealed Powell's financial discipline. The consideration includes an upfront payment of £9.2 million Pounds Sterling with the remaining portion contingent upon Remsdaq meeting certain technical and financial milestones. In an era of blank-check acquisitions and SPAC excess, Powell negotiated earn-outs that aligned incentives and protected shareholder value.

Ray Colston, Managing Director of Remsdaq, noted that Powell's customer-centric philosophy and culture not only complements their market leadership and scale within the Electric Utility space but also aligns closely with Remsdaq's own values, creating deep technological and cultural alignment for their products and services.

The automation push extends beyond acquisitions. Powell has been steadily building software capabilities, hiring data scientists and software engineers who might have seemed out of place in an industrial manufacturer just years ago. They're developing predictive analytics that can forecast equipment failures weeks in advance. They're creating digital twins of electrical systems that allow operators to simulate different scenarios and optimize performance.

This technological evolution positions Powell for the next wave of infrastructure investment. As grids become more complex—integrating solar farms, wind turbines, battery storage, and millions of electric vehicles—the ability to manage these systems intelligently becomes crucial. Powell isn't trying to become a software company; they're becoming an intelligence layer for critical infrastructure, combining their deep hardware expertise with enough software capability to deliver complete solutions.

Playbook: Business & Investing Lessons

The Power of Patience: Powell Industries waited 70 years to become an overnight success. From 1947 to 2015, the company methodically built expertise, relationships, and capabilities without a single transformative moment. When the convergence of shale gas, grid crisis, and AI data centers created unprecedented demand, Powell had the foundation to capture it. In an era obsessed with disruption and first-mover advantages, Powell demonstrates that sometimes the best strategy is to build excellence and wait for the world to need what you've perfected.

Specialization as Strategy: During the dark years of 2000-2015, Powell faced constant pressure to diversify. Consultants undoubtedly pitched adjacent markets. Investment bankers proposed transformative acquisitions. The board surely questioned whether focusing on custom electrical equipment for industrial customers was too narrow. But Powell's refusal to dilute its focus meant that when demand exploded, they were the unquestioned expert. Specialization that seems like a limitation during downturns becomes a moat during upturns.

Riding Sequential Waves: Powell didn't bet everything on a single trend. The shale boom provided the first boost, but Powell was already preparing for grid modernization before Winter Storm Uri made it urgent. They were building utility relationships before the infrastructure bill passed. They were developing data center capabilities before ChatGPT launched. Each wave built on the previous one, creating cumulative advantages that competitors couldn't quickly replicate.

Capital Allocation Excellence: Cash and short-term investments as of September 30, 2024 totaled $358 million. Powell maintained a fortress balance sheet with no debt, allowing them to invest countercyclically. During downturns, they maintained engineering capabilities and manufacturing capacity that seemed excessive. When demand surged, they could capture it immediately rather than scrambling to build capabilities. The Remsdaq acquisition, funded entirely with cash, exemplifies their disciplined approach—strategic additions paid for without leverage or dilution.

The "Picks and Shovels" Play: During gold rushes, sell shovels. During the AI boom, Powell sells the electrical infrastructure that every data center requires. They don't need to predict which AI model will win or which applications will succeed. They just need AI to keep growing—and given the computational requirements of modern AI, that growth translates directly to electrical demand. Powell captures value from the AI revolution without taking technology risk.

Timing Market Transitions: Powell's history reveals an uncanny ability to position for transitions just before they become obvious. They were building LNG capabilities before American gas exports exploded. They were developing grid resilience products before Texas froze. They were creating data center solutions before AI went mainstream. This isn't luck—it's the result of deep industry relationships and engineers who understand where technology is heading before it arrives.

Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's 5 Forces Analysis

Supplier Power: Moderate. Powell sources specialized components like circuit breakers and control systems from multiple suppliers, providing some negotiating leverage. However, certain critical components have limited suppliers, and Powell's customization requirements mean they can't easily switch sources. The company's long-term supplier relationships and volume commitments help manage this dynamic, but raw material costs (copper, steel, specialized alloys) can impact margins during commodity cycles.

Buyer Power: High. Powell's customers—utilities, oil majors, hyperscale data center operators—are sophisticated buyers with significant negotiating leverage. They run competitive bidding processes, demand extensive warranties, and can delay projects based on capital allocation decisions. However, Powell's specialization in complex, mission-critical systems provides some protection. When a refinery needs equipment that won't fail in a Category 5 hurricane, or a data center requires five-nines reliability, price becomes secondary to capability.

Threat of Substitutes: Low. There are no practical substitutes for electrical distribution and control equipment in industrial applications. While configurations might change—distributed generation might reduce the need for certain transmission equipment—the fundamental need for switchgear, control systems, and power distribution remains. The trend toward electrification actually increases demand as industries that previously relied on mechanical or hydraulic systems convert to electrical alternatives.

Threat of New Entrants: Low. The barriers to competing with Powell are formidable. Beyond the capital required for manufacturing facilities, new entrants would need decades of engineering expertise, extensive testing and certification processes, and relationships with conservative customers who won't risk critical infrastructure on unproven suppliers. The liability exposure alone—imagine causing a refinery explosion or data center outage—deters casual entry. Chinese competitors might have cost advantages, but they lack certifications and face "Buy American" requirements in many projects.

Competitive Rivalry: Moderate. Powell competes with divisions of industrial giants like Siemens, ABB, Schneider Electric, and Eaton. These competitors have greater resources and broader product portfolios. However, the market is large enough and growing fast enough that competition focuses more on capturing new demand than stealing existing customers. Powell's specialization in custom solutions for harsh environments provides differentiation, and their US manufacturing base becomes increasingly valuable as supply chain security gains importance.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Emerging but not dominant. Powell's growing volume allows better supplier terms and efficiency improvements in their manufacturing processes. The expansion of their Jacintoport facility leverages fixed costs across more units. However, unlike software or network businesses, Powell's scale economies are linear rather than exponential. Each new project requires real resources and manufacturing capacity.

Switching Costs: High and growing. Once Powell equipment is installed in a facility, switching vendors requires significant expense and operational risk. Powell's equipment must integrate with existing systems, and their engineers develop intimate knowledge of each customer's operations. The recent push into automation and SCADA systems dramatically increases switching costs—these systems become the nervous system of facilities, making replacement almost unthinkable without complete overhauls.

Network Economies: Limited but developing. Powell doesn't benefit from traditional network effects where each new user makes the product more valuable for existing users. However, their growing installed base creates indirect benefits: more Powell equipment in operation means more engineers familiar with their systems, more standardization around their designs, and more third-party contractors trained on their equipment. The Remsdaq acquisition could enable data network effects if Powell aggregates operational data across installations to improve predictive maintenance algorithms.

Counter-Positioning: Strong. Powell's strategy of hyper-customization runs counter to the standardization approach of larger competitors. Siemens or ABB optimize for mass production and global scale; Powell optimizes for solving specific, complex problems. This isn't a strategy the giants can easily adopt—their entire operations are built around standardization and volume. Powell's counter-positioning becomes stronger as projects become more complex and customers demand solutions rather than products.

Cornered Resource: Meaningful. Powell's relationships with hyperscale data center operators and major utilities represent a cornered resource that took decades to build. Their certifications and approved vendor status with critical infrastructure operators can't be quickly replicated. Most importantly, their specialized engineering knowledge for harsh environment applications—accumulated over 77 years—provides solutions that competitors simply can't match. The institutional knowledge of building equipment that survives Gulf Coast hurricanes or West Texas dust storms resides in Powell's engineers, not in any manual.

Process Power: Significant. Powell's ability to design, manufacture, test, and deliver complete electrical systems for complex projects involves countless small optimizations and tacit knowledge that competitors can't easily observe or copy. Their process for managing custom projects—from initial consultation through commissioning—has been refined over thousands of installations. The company culture of engineering excellence and customer focus, reinforced over generations, creates behavioral norms that new entrants can't quickly replicate.

Branding: Moderate but growing. Powell lacks the consumer recognition of a General Electric, but within their niche, the brand carries significant weight. For engineers specifying equipment for critical applications, Powell represents reliability and expertise. The brand power is B2B rather than B2C—it's about trust and track record rather than marketing appeal. As Powell's equipment proves itself in high-profile applications like hyperscale data centers, brand value increases.

Bear vs. Bull Case

Bear Case: The Peak Has Passed

The bear thesis starts with valuation. Powell's all-time high stock closing price was $408.37 on October 29, 2025, representing a multiple that assumes continued hypergrowth. At these levels, Powell trades at historically unprecedented multiples for an industrial manufacturer. The stock has risen over 1,000% from its 2020 lows—a move that typically marks tops, not beginnings.

The margin story contains warning signs. Recent results benefited from favorable project mix and one-time closeouts that inflated profitability. As Powell works through its backlog of high-margin projects signed during the post-COVID boom, new projects might carry lower margins as competition intensifies and customers become more price-sensitive. The company's gross margins improved 590 basis points year-over-year, but such dramatic improvements rarely sustain.

Data center growth, the current darling of Powell's investor story, faces potential headwinds. The AI boom has driven a construction frenzy, but history shows that technology infrastructure buildouts often overshoot demand. Just as the dot-com era saw massive overcapacity in fiber optic cables and server farms, the AI infrastructure boom could pause as companies digest capacity and await actual AI revenue generation to justify further investment.

Powell's backlog, while robust at $1.4 billion, has stopped growing at previous rates. Backlog totaled $1.4 billion as of September 30, 2025, a decrease of 2% compared to June 30, 2025. This deceleration might signal that the order surge has peaked. Large LNG projects that drove recent growth face an uncertain future as global gas markets rebalance and environmental pressures mount against fossil fuel infrastructure.

Competition from global giants remains a constant threat. Siemens, ABB, and Schneider Electric have resources that dwarf Powell's. If they decide to seriously target Powell's niches—custom solutions for harsh environments—they could leverage their scale to underprice Powell while absorbing short-term losses. Chinese competitors, while currently excluded from many projects, continue to improve their capabilities and could eventually challenge Powell in international markets.

The cyclical nature of Powell's end markets presents ongoing risk. Oil and gas, still Powell's largest segment, faces long-term decline as energy transition accelerates. Utility spending depends on regulatory approvals and rate cases that can be delayed or denied. Even data center construction, currently booming, will eventually normalize as AI compute becomes more efficient and distributed.

Bull Case: The Infrastructure Supercycle Has Just Begun

The bull thesis rests on a simple observation: America's electrical infrastructure is old, inadequate, and facing unprecedented new demands. The grid modernization required to support electrification of transport, renewable energy integration, and AI computation will take decades and tens of billions of dollars. Powell sits at the nexus of all these trends.

Full year fiscal 2025 revenues totaled $1.1 billion, an increase of 9%, but this modest growth masks explosive expansion in key segments. Electric Utility revenue increased 26% to $51.2 million, while Commercial & Other Industrial revenue surged 80% to $44.3 million. These emerging segments could dwarf Powell's traditional oil and gas business within five years.

The data center opportunity alone justifies optimism. The $186 billion global SCADA market is growing at 6.5% annually, and Powell's automation capabilities position them to capture an outsized share. Unlike the dot-com era's speculative buildout, current data center construction responds to real, revenue-generating AI applications. Every major corporation is implementing AI, and each implementation requires computing power that doesn't exist today.

Powell's balance sheet provides enormous strategic flexibility. With over $400 million in cash and no debt, the company can pursue acquisitions, expand manufacturing capacity, or weather downturns without dilution or financial stress. This financial strength becomes a competitive advantage as customers increasingly evaluate supplier stability when making critical infrastructure decisions.

The Made-in-USA advantage continues strengthening. Federal infrastructure spending includes "Buy American" provisions that effectively exclude foreign competitors from many projects. Supply chain concerns post-COVID make domestic manufacturing a strategic imperative for critical infrastructure. Powell's Houston manufacturing base, once seen as a cost disadvantage, now provides resilience that customers value.

Grid resilience requirements will only intensify. Climate change means more extreme weather events like Winter Storm Uri. Cybersecurity threats require hardened, intelligent infrastructure. The electrification of everything—from vehicles to heating systems to industrial processes—makes electrical reliability existentially important. Powell's products aren't optional; they're essential for a functioning modern economy.

Management's track record inspires confidence. Brett Cope's ethos of 'Know your passion' and Powell Industries' foundation stone laid in 1947 as a metal-working shop have evolved into a leading supplier of highly complex systems. The company has navigated multiple cycles, avoided the diversification mistakes that destroyed many industrial conglomerates, and positioned perfectly for current trends without abandoning their core strengths.

Epilogue & Looking Forward

The story of Powell Industries challenges everything modern business culture teaches about success. No viral growth hacks. No software eating the world. No move-fast-and-break-things. Just seven decades of patient competence, waiting for the moment when boring became beautiful and switchgear became strategic.

Looking ahead, Powell faces opportunities that dwarf even their recent success. The energy transition isn't replacing Powell's market—it's multiplying it. Every solar farm needs switchgear. Every wind turbine requires control systems. Every battery storage facility demands sophisticated power management. The electrification of transportation alone could create demand exceeding Powell's entire current market.

Three key metrics will determine Powell's trajectory. First, backlog quality and duration—not just the headline number but the mix of projects and their margin profiles. Second, the data center percentage of revenue—this segment's growth rate will signal whether Powell has successfully diversified beyond traditional industrial markets. Third, automation software adoption—the success of acquisitions like Remsdaq will determine whether Powell can capture the intelligence layer value that commands premium multiples.

The biggest risk isn't competition or cyclicality—it's execution. Powell must scale manufacturing capacity without compromising quality. They must integrate acquisitions without losing focus. They must hire and train thousands of engineers while maintaining their culture of customization and customer focus. The company that thrived as a regional specialist must become a national champion without losing what made them special.

The investment lesson from Powell transcends any single stock. Sometimes the best opportunities hide in plain sight, disguised as boring businesses in unfashionable industries. While venture capitalists funded the hundredth food delivery app and retail investors chased meme stocks, Powell Industries quietly positioned itself at the intersection of every major infrastructure trend reshaping America.

The next decade will determine whether Powell's transformation from regional supplier to critical infrastructure enabler represents a permanent rerating or a cyclical peak. But one thing seems certain: in a world increasingly dependent on reliable, intelligent electrical infrastructure, the company that spent 77 years perfecting the mundane art of keeping the lights on has never been more essential.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube