PulteGroup: From One House to America's Homebuilding Giant

I. Introduction & The Hook

Picture this: March 2009. The American housing market is a smoking crater. Home prices have plummeted 30% from their peak. Lehman Brothers is six months dead. Bear Stearns and Washington Mutual are distant memories. Foreclosure notices paper suburban lawns from Phoenix to Fort Lauderdale. And in this apocalyptic landscape, Bill Pulte's successor Richard Dugas Jr. walks into a boardroom and proposes something that sounds utterly insane: let's buy our biggest competitor.

The target? Centex Corporation, once the nation's largest homebuilder, now bleeding cash and trading at fire-sale prices. The price tag? $1.3 billion in stock—not cash, because even Pulte didn't have that kind of liquidity in the depths of the crisis. The entire homebuilding industry thought Dugas had lost his mind. Wall Street analysts called it "catching a falling knife." One competitor CEO privately called it "corporate suicide."

They were all wrong.

That audacious bet would transform PulteGroup into America's third-largest homebuilder, a company that would go on to generate $17.95 billion in revenue by 2024. But to understand how a company finds the courage—or perhaps the madness—to double down during the worst housing crisis since the Great Depression, we need to go back to where it all began: with an 18-year-old kid in Detroit who thought he could build houses better than anyone else.

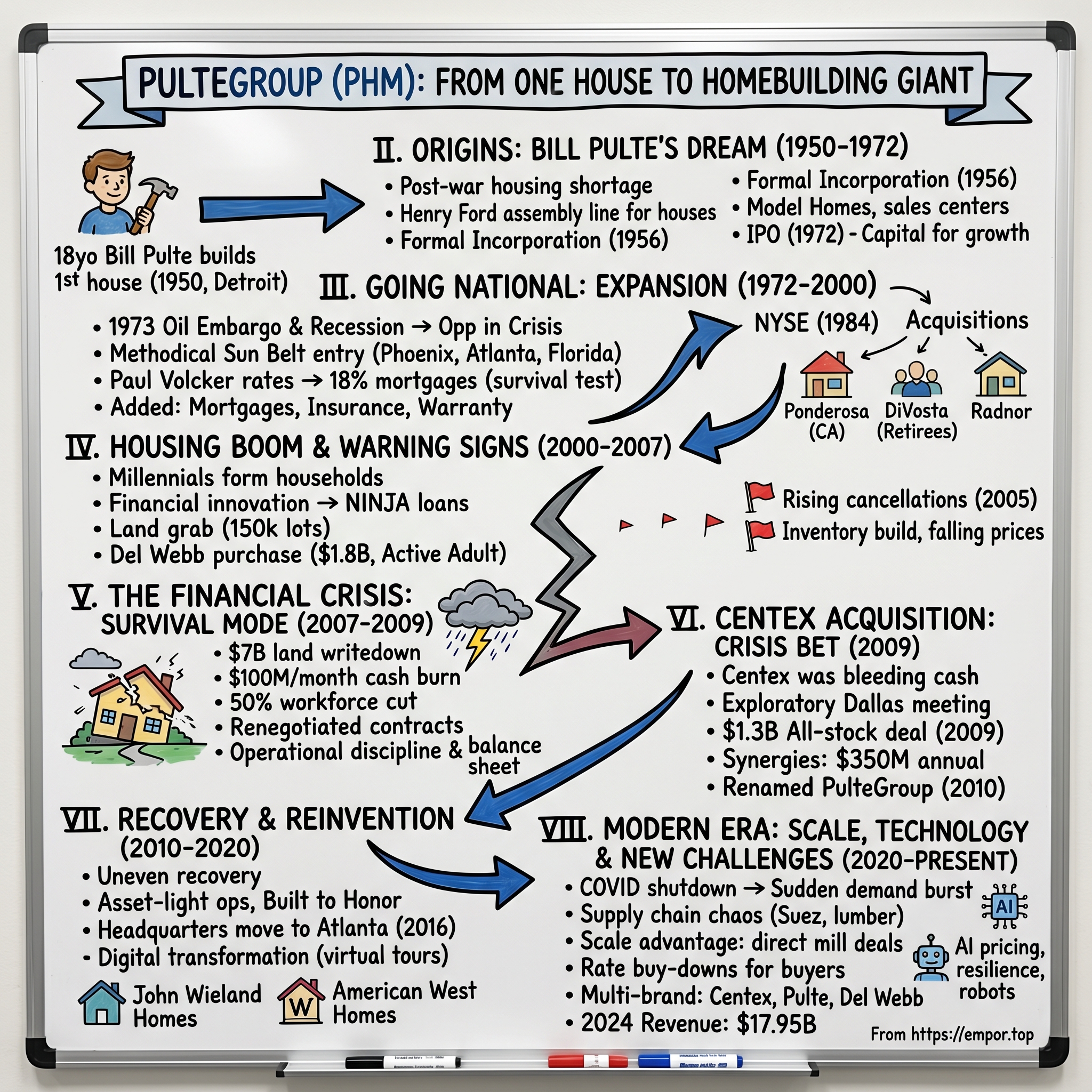

The year was 1950. Harry Truman was president. The Korean War had just begun. And in Detroit—the beating heart of American industry—William J. Pulte picked up a hammer and started building his first house. He had no formal training, no family money, no connections to speak of. What he had was timing: millions of GIs were returning home, starting families, and desperately searching for homes that didn't exist. The post-war housing shortage was so acute that families were living in converted chicken coops and Quonset huts.

Young Bill Pulte saw opportunity where others saw chaos. At 18, most kids were heading to college or the factory floor. Bill went straight to construction sites, learned by watching, and figured he could do it himself—only better, faster, and cheaper.

By 1956, he'd built enough houses and confidence to incorporate Pulte Homes, Inc., headquartered in Bloomfield Hills, Michigan—a tony Detroit suburb where the Big Three auto executives lived. The name on the door was simple, but the ambition was enormous: Pulte didn't just want to build houses. He wanted to revolutionize how America built homes.

What followed over the next seven decades is a story of relentless expansion, near-death experiences, brilliant acquisitions, and the kind of operational excellence that turns a local Michigan builder into a company that has constructed over 775,000 homes across America. It's a story about reading economic cycles, understanding demographic shifts, and having the guts to zig when everyone else zags.

Today, PulteGroup operates in 44 markets across 23 states. Its brands—Pulte Homes, Centex, Del Webb, DiVosta, American West, and John Wieland—target everyone from first-time buyers scraping together down payments to affluent retirees seeking golf course estates. The company that started with one teenager's hammer now employs thousands and shapes how millions of Americans live.

But between that first house in 1950 and today's sprawling empire lies a journey filled with boom-bust cycles, existential crises, and strategic decisions that would make or break the company. How does a homebuilder survive when interest rates hit 18%? What happens when your entire industry essentially goes bankrupt? And perhaps most importantly: in a business that many consider a commodity—after all, houses are just wood, concrete, and drywall—how do you build something that endures?

The answers reveal not just the PulteGroup story, but the story of American homebuilding itself—an industry that's simultaneously primitive and sophisticated, local and national, cyclical yet fundamental to the American Dream. So let's start where Bill Pulte started: in post-war Detroit, with a simple belief that he could build better homes for American families.

II. Origins: Bill Pulte's American Dream (1950-1972)

Detroit in 1950 wasn't just the Motor City—it was the epicenter of American prosperity. The auto plants ran three shifts. Money flowed like the Detroit River. And everywhere you looked, the landscape was transforming. Farmland became subdivisions overnight. Dirt roads sprouted traffic lights. The suburbs were being invented in real-time, and young Bill Pulte had a front-row seat.

But Pulte wasn't content to watch. While his high school classmates were heading to work at Ford or General Motors, Bill was studying construction sites with the intensity of a medical student examining anatomy. He'd show up at job sites uninvited, watching how foundations were poured, how frames went up, how problems got solved. The foremen would shoo him away, but he'd return the next day, and the next.

His first house, built when he was just 18, was an exercise in controlled chaos. Pulte had scraped together $5,000—some borrowed from relatives, some saved from odd jobs—and bought a lot in Detroit's expanding suburbs. He acted as his own general contractor, hiring subcontractors, managing schedules, dealing with suppliers. The learning curve was vertical. The first plumber he hired disappeared mid-job. The foundation had to be re-poured after he miscalculated the grade. But when that first house sold—for a modest profit of about $1,000—Bill Pulte had found his calling.

What separated Pulte from the hundreds of other small builders sprouting up across post-war America? Speed and systemization. While traditional builders treated each house as a custom project, Pulte began thinking in terms of repeatable processes. He studied Henry Ford's assembly line principles—ironic, given that he was building homes for Ford's workers—and wondered: why couldn't houses be built with the same efficiency as cars?

By 1954, Pulte was building five houses simultaneously, rotating crews between sites to minimize downtime. He negotiated bulk deals with suppliers, standardized floor plans while allowing superficial customization, and—critically—began buying land in larger parcels. This wasn't revolutionary on paper, but in practice, few builders had the discipline to execute it consistently.

The formal incorporation of Pulte Homes, Inc. in 1956 marked a transition from entrepreneur to executive. Pulte moved the operation to Bloomfield Hills, a signal of ambition—this was where the Detroit elite lived, and Bill wanted a seat at that table. The company's first real office was a modest space above a shopping center, but the location mattered. Bloomfield Hills meant credibility with banks, suppliers, and the increasingly sophisticated buyers moving to Detroit's suburbs.

The late 1950s and 1960s were boom times for Detroit and Pulte Homes. The company was building entire subdivisions now—50, 100, sometimes 200 homes at a time. Pulte had discovered something crucial: the real money in homebuilding wasn't in construction margins (typically 10-15%) but in land appreciation. Buy raw land at $1,000 an acre, develop it with roads and utilities, subdivide it, and suddenly it's worth $10,000 an acre or more. The homes were almost secondary—they were the mechanism to unlock land value.

But Pulte's real innovation was understanding his customer better than competitors. While other builders focused on square footage and features, Pulte obsessed over the buying experience. He pioneered the model home concept in Detroit—fully furnished, decorated houses that helped buyers envision their lives, not just visualize floor plans. He hired interior designers when other builders thought that was frivolous. He created sales centers with financing specialists on-site, turning home buying from a fragmented nightmare into a one-stop shop.

By the late 1960s, Pulte Homes was building over 1,000 homes annually, generating revenues in the tens of millions. But Bill Pulte knew that to truly scale, he needed capital—more than local banks could provide. The decision to go public wasn't just about money; it was about ambition. Pulte didn't want to be Detroit's best builder. He wanted to be America's.

The IPO in 1972 was modest by today's standards—raising just a few million dollars on the American Stock Exchange. But it represented a fundamental shift. Pulte Homes was no longer Bill's company; it was now accountable to shareholders, quarterly earnings, and the relentless demands of Wall Street. Some founders would have struggled with this transition. Bill Pulte thrived on it. The discipline of public markets forced operational improvements. The access to capital enabled geographic expansion. And the stock currency would eventually enable acquisitions that would transform Pulte from regional player to national powerhouse.

As 1972 ended, Pulte Homes had built roughly 15,000 homes total in its 22-year history. It was a successful regional builder with national aspirations, public stock, and a founder-CEO who believed the American suburbs had only just begun their growth. He was right about the suburbs. But nobody—not Bill Pulte, not his executives, not Wall Street—could have predicted the roller coaster that American housing was about to become. The smooth growth of the 1950s and 1960s was ending. The volatile, boom-bust cycles that would define modern homebuilding were about to begin.

III. Going National: The Expansion Years (1972-2000)

The morning after Pulte Homes rang the opening bell at the American Stock Exchange in 1972, Bill Pulte gathered his senior team in Bloomfield Hills. "Gentlemen," he said, spreading a map of the United States across the conference table, "it's time to think bigger." He placed pins in Phoenix, Atlanta, Houston, and Florida. "These are tomorrow's Detroits."

It was a prescient observation. The Rust Belt was beginning its slow decline, while the Sun Belt was about to explode. But Pulte's expansion strategy wasn't just about following population growth—it was about a fundamental rethinking of what a homebuilder could be.

The first challenge hit almost immediately. In 1973, the Arab oil embargo sent the economy into recession. Interest rates spiked. In 1974, housing starts nationally dropped 35%. Smaller builders went bankrupt by the dozens. Pulte's stock, which had IPO'd at $8, fell to $3. Wall Street analysts questioned whether the company had gone public at exactly the wrong time.

But Pulte saw opportunity in crisis—a pattern that would repeat throughout the company's history. While competitors retreated, Pulte used its public company balance sheet to cherry-pick land from distressed sellers. The company entered Florida in 1974, buying prime parcels at 40 cents on the dollar. When the market recovered in 1975-76, Pulte was positioned perfectly.

The geographic expansion through the late 1970s was methodical. Rather than carpet-bombing multiple markets simultaneously, Pulte would enter one new market, establish operations, achieve profitability, then move to the next. Each market entry followed a playbook: hire experienced local managers (often poached from competitors), acquire land positions, build model homes, establish supplier relationships, and scale carefully.

Then came 1979-1982, years that would test every homebuilder in America. Federal Reserve Chairman Paul Volcker, determined to break inflation, drove interest rates to unprecedented levels. Mortgage rates hit 18%. Housing starts fell to their lowest level since World War II. Of the top 20 builders in 1979, eight wouldn't survive to 1983.

Pulte not only survived but used the downturn to transform itself. The company made a crucial strategic pivot: instead of just building homes, it would become a full-service housing company. This meant moving into mortgage origination, title insurance, and even home warranties. The logic was simple but powerful—capture more of the value chain and smooth out the inherent cyclicality of construction.

The move to the New York Stock Exchange in 1984 signaled Pulte's arrival as a major corporation. The company was now building in dozen states, generating hundreds of millions in revenue. But Bill Pulte, now in his 50s, knew that organic growth alone wouldn't achieve his vision. The company needed to accelerate through acquisitions.

The acquisition strategy that emerged in the 1980s and 1990s was sophisticated for its time. Rather than buying competitors for market share, Pulte targeted companies that brought specific capabilities or market positions. Each deal had a strategic rationale beyond simple scale.

In 1988, Pulte acquired Ponderosa Homes, giving it a significant presence in California's booming markets. The integration was textbook—keep the best local managers, apply Pulte's systems and purchasing power, maintain local brand recognition where valuable. The company had learned that homebuilding, despite its scale economies, remained stubbornly local. Buyers in Phoenix wanted different things than buyers in Atlanta.

The 1990s brought new challenges and opportunities. The savings and loan crisis created another land-buying opportunity. The technology boom created entirely new demographics of buyers. And perhaps most importantly, the American household was changing—more single-parent families, more retirees, more diversity in what "home" meant.

Pulte responded by diversifying its product line. The company wasn't just building suburban single-family homes anymore. It developed townhome communities for urban professionals, master-planned communities for move-up buyers, and increasingly, active adult communities for the massive baby boomer generation approaching retirement.

The 1998 acquisition of DiVosta for approximately $150 million was particularly strategic. DiVosta had pioneered the active adult community concept in Florida, building amenity-rich developments for retirees who wanted resort-style living. This wasn't just about adding units—it was about understanding that the largest generation in American history was about to redefine retirement.

The Radnor Homes acquisition the same year brought different capabilities—expertise in the mid-Atlantic markets and a reputation for quality that exceeded even Pulte's standards. Bill Pulte had always said, "We're not just building houses, we're building homes." Radnor showed them how to build even better ones.

As the millennium approached, Pulte Homes had been transformed beyond recognition. The company that had built 15,000 homes in its first 22 years was now building that many annually. Revenue exceeded $4 billion. The company operated in 40 markets across 25 states. It had survived multiple recessions, integrated numerous acquisitions, and built a reputation as one of America's premier builders.

But the transformation went deeper than numbers. Pulte had evolved from a production builder—focused on volume and efficiency—to what executives called a "consumer solutions company." This meant understanding that a home wasn't just shelter but the platform for a family's life. It meant offering mortgages, insurance, and warranties. It meant building communities, not just subdivisions.

Bill Pulte stepped back from day-to-day operations in the late 1990s, though he remained chairman. His successor faced an enviable but challenging position: leading America's largest homebuilder (a title Pulte would claim by 2001) at what appeared to be the start of an unprecedented housing boom. Nobody could have imagined just how unprecedented—or how unsustainable—that boom would become.

IV. The Housing Boom & Warning Signs (2000-2007)

The new millennium opened with Pulte executives popping champagne. Y2K had fizzled. The dot-com crash, while painful for tech stocks, had driven interest rates lower, making mortgages cheaper. And demographic trends looked spectacular—77 million baby boomers were entering peak earning years while their kids, the millennials, were forming households. At Pulte's 2001 investor day, CEO Richard Dugas declared, "We're not just riding a wave; we're riding a tsunami."

He wasn't wrong about the wave. He just didn't realize it would eventually crash on the rocks.

By 2001, Pulte had officially become the largest homebuilder in the United States by revenue—a title it would trade back and forth with competitors throughout the decade. But raw size mattered less than what was happening beneath the surface. The housing market was undergoing a fundamental transformation, driven by financial innovation that would eventually bring the global economy to its knees.

The mortgage revolution started innocuously enough. In 2000, getting a mortgage required 20% down, proof of income, and good credit. By 2005, you could get a "NINJA" loan—no income, no job, no assets. The degradation happened gradually, then suddenly. First, down payments dropped to 10%, then 5%, then zero. Documentation requirements loosened from "full doc" to "stated income" to "no doc." Credit score requirements fell from 700 to 620 to 580 to "if you can fog a mirror."

Pulte, to its credit, never directly originated subprime mortgages through its financial services arm. But the company certainly benefited from the broader loosening of credit. Buyers who couldn't have qualified for a Pulte home in 2000 were suddenly approved in 2005. The company's average selling price rose from $246,000 in 2000 to $342,000 by 2005—a 39% increase that far outpaced inflation or income growth.

The land grab of 2003-2006 would later be seen as the height of the bubble's insanity, but at the time it felt perfectly rational. Pulte spent billions acquiring land positions in hot markets—Phoenix, Las Vegas, Florida, and the Inland Empire of California. The company's land bank swelled to over 150,000 lots. Executives justified the spending with PowerPoints showing inexorable population growth and housing demand.

One acquisition during this period would prove transformative: Del Webb, purchased in 2001 for $1.8 billion. Del Webb wasn't just another builder—it was the inventor of the active adult community concept. Its Sun City developments in Arizona had become the gold standard for retirement living, complete with golf courses, recreation centers, and age-restricted covenants that kept the kids away.

The Del Webb deal looked expensive at the time, but it positioned Pulte perfectly for the baby boomer retirement wave. By 2005, Pulte's active adult communities were generating over $2 billion in annual revenue, with operating margins significantly higher than traditional homebuilding. These communities weren't just profitable—they were culturally significant, redefining American retirement from rocking chairs on the porch to golf carts on the fairway.

The geographic expansion during the boom was breathtaking. Pulte entered or expanded in virtually every hot market—adding positions in Nevada, Arizona, California's Central Valley, and Florida's west coast. In Cape Coral-Fort Myers alone, the company was building over 2,000 homes annually by 2005. Las Vegas became a gold rush, with Pulte competing against dozens of builders for labor, land, and buyers who often flipped contracts before homes were even completed.

But warning signs were emerging for those willing to see them. In 2005, Pulte's cancellation rates began creeping up—from a historical 15% to 20%, then 25%. Spec investors, who had been buying homes to flip, started walking away from deposits. In markets like Phoenix, Pulte sales offices that had seen lines of buyers in 2004 were suddenly empty on weekends.

The company's response was to accelerate sales through incentives—free upgrades, covered closing costs, even free cars with home purchases in some markets. These incentives, buried in the footnotes of financial statements, were eating into margins. But Wall Street focused on the top line: revenues hit $14.7 billion in 2005, earnings exceeded $1.4 billion. The stock reached an all-time high of $47.

Inside Pulte, there were debates about the sustainability of the boom. Some regional presidents argued for pulling back, reducing land purchases, and conserving cash. But the prevailing view, reinforced by economists and industry consultants, was that any slowdown would be modest and regional. "Housing doesn't decline nationally," became a mantra, backed by data showing that home prices hadn't fallen nationwide since the Depression.

The operational complexity during this period was staggering. Pulte was managing construction on tens of thousands of homes simultaneously, dealing with material shortages as Chinese demand drove up commodity prices, and struggling to find skilled labor as Mexican immigration tightened. The company was building a new home every 17 minutes, 24 hours a day, 365 days a year.

Technology became crucial for managing this scale. Pulte invested heavily in systems for scheduling, purchasing, and customer management. The company pioneered online design centers where buyers could customize homes virtually. It developed sophisticated models for predicting which floor plans would sell in which markets. This wasn't your grandfather's homebuilding—it was industrial-scale manufacturing with customization at the edges.

By late 2006, even the optimists at Pulte couldn't ignore reality. Home sales were slowing dramatically. Inventories were building. Prices had stopped rising and were beginning to fall in bubble markets. The company took its first major land writedown in Q4 2006—$350 million, shocking Wall Street.

But that was just the beginning. As 2007 opened, Pulte executives faced a terrifying reality: they were sitting on a land bank worth far less than they'd paid, demand was evaporating, and buyers who had signed contracts were walking away in droves. The tsunami that Dugas had celebrated six years earlier was about to break, and Pulte was directly in its path.

V. The Financial Crisis: Survival Mode (2007-2009)

The September 2007 board meeting at Pulte headquarters started with Richard Dugas displaying a single slide: a photo of a half-built house, abandoned, weeds growing through the foundation. "This is our Phoenix division," he said quietly. "We have 1,400 of these."

The numbers that followed were brutal. Cancellation rates had hit 48%. The company's land bank, valued at $7 billion on the books, was worth perhaps half that at market prices. Cash burn was $100 million per month. And this was before Lehman Brothers collapsed, before the credit markets froze, before the word "recession" was even official.

Pulte's third-quarter 2007 earnings call was a masterclass in controlled panic. The company reported a $1.6 billion loss, driven primarily by land writedowns. Dugas tried to sound optimistic: "We believe we're being appropriately conservative in our valuations." But analysts weren't buying it. One asked pointedly: "How do you value land when there are literally no buyers?"

The answer was: you couldn't. And that was the existential problem facing every homebuilder in America. The entire industry's business model—buy land, develop it, build homes, sell for profit—had broken down at every step. You couldn't buy land rationally because you didn't know future values. You couldn't develop it because you couldn't get construction loans. You couldn't build because buyers couldn't get mortgages. And you couldn't sell because prices were in free fall.

Inside Pulte, the response was swift and brutal. The company cut its workforce by 50%—from 14,000 employees to 7,000. Entire divisions were shuttered. The Las Vegas office, which had employed 400 people in 2006, was reduced to 25. Marketing budgets were slashed 70%. Executive compensation was cut, bonuses eliminated, perks stripped away.

But the real action was in land renegotiations. Pulte had billions in land purchase contracts signed during the boom, with deposits at risk. The company assembled a team of lawyers and negotiators whose sole job was to get out of these contracts or renegotiate terms. It was trench warfare—every deal contested, every deposit fought over. Pulte walked away from $500 million in deposits rather than close on land that would generate larger losses.

The financial gymnastics required to survive were extraordinary. Pulte had to maintain enough liquidity to operate while bleeding cash, satisfy debt covenants while asset values plummeted, and somehow convince rating agencies not to downgrade its bonds to junk status, which would have triggered a death spiral.

The fourth quarter of 2008 brought the crisis to its apex. Lehman Brothers had collapsed in September. The credit markets were frozen. And Pulte reported another massive loss—$787.9 million, including $842 million in land charges. The company's stock, which had peaked at $47 in 2005, hit $5. Market capitalization had fallen from $12 billion to $1.3 billion.

But here's what separated Pulte from builders that didn't survive: operational discipline and balance sheet management. While competitors were desperately slashing prices to generate any cash flow, Pulte made a counterintuitive decision—maintain pricing discipline even if it meant fewer sales. The logic was simple: selling homes at massive losses just to generate cash would destroy the company's long-term viability.

The company also got creative with its existing inventory. Rather than building new homes, Pulte converted spec homes to rental properties in some markets, generating cash flow while waiting for prices to stabilize. It offered lease-to-own programs for buyers who wanted homes but couldn't qualify for mortgages. It even experimented with bulk sales to institutional investors who were beginning to see opportunity in distressed housing.

The human toll was immense. Regional presidents who had been kings of their markets were laid off. Construction superintendents who'd built thousands of homes were let go. Sales agents who'd made six figures during the boom were unemployed. At Pulte's 2008 holiday party—a subdued affair with beer and pizza replacing the usual champagne and steaks—Dugas spoke to the remaining employees: "If you're here, you're essential. And if we survive this, we'll emerge stronger than ever."

Survival wasn't guaranteed. By early 2009, industry analysts were openly discussing which major builders would declare bankruptcy. Pulte's bonds were trading at 60 cents on the dollar, implying significant default risk. The company was burning through cash reserves that had taken decades to accumulate.

But Pulte had three advantages that would prove decisive. First, it had entered the crisis with a relatively strong balance sheet—the result of conservative financial management during even the boom years. Second, it had diversified revenue streams through its financial services operations, which continued generating modest profits. And third, its leadership team had experience with downturns, having navigated the early 1990s recession.

As 2009 began, with the economy in free fall and housing seemingly in permanent decline, Pulte's board faced a crucial decision. The company could hunker down, preserve cash, and wait for recovery. Or it could do something audacious—use the crisis to transform itself through acquisition. The target under discussion was Centex, once the industry's largest builder, now trading at a fraction of its former value.

The board debate was intense. How could Pulte justify a major acquisition when it was losing money? How could it integrate another company while simultaneously restructuring its own operations? And most fundamentally: what if housing never recovered?

But Dugas and his team saw opportunity where others saw only risk. Centex would bring geographic diversification, a lower price point product line, and most importantly, a land bank that could be acquired at distressed values. If housing did recover—and demographics suggested it eventually must—the combined company would be positioned to dominate.

The decision to pursue Centex would either be remembered as brilliant opportunism or reckless gambling. As winter turned to spring in 2009, with the economy still in recession and housing still in free fall, Pulte made its move.

VI. The Centex Acquisition: Doubling Down in Crisis (2009)

The phone call came at 6 AM on a Sunday in February 2009. Richard Dugas was in his home office, reviewing another dismal weekly sales report, when Centex CEO Tim Eller called. "Richard," Eller said without preamble, "we need to talk."

Both men knew what this meant. Centex, once the undisputed king of American homebuilding, was drowning. The company had been particularly aggressive during the boom, loading up on land in California, Florida, and Nevada—the very markets now experiencing the worst crashes. Its stock had fallen from $80 to $8. More critically, Centex was burning cash faster than Pulte and had less cushion to absorb losses.

The first meeting between the companies took place in a nondescript airport hotel in Dallas—neutral territory between Pulte's Atlanta operations and Centex's Dallas headquarters. The initial discussions were exploratory, feeling each other out. But both sides knew the clock was ticking. Housing markets were still deteriorating. Credit remained frozen. And neither company could afford a prolonged courtship.

The strategic logic was compelling on paper. Centex brought strength in first-time buyer homes—a segment where Pulte was weak. Its Fox & Jacobs brand in Texas was legendary for efficient, affordable construction. Centex's geographic footprint overlapped with Pulte's but also added density in key markets. Combined, the companies would have unmatched scale advantages in purchasing, overhead absorption, and market presence.

But the financial engineering required was complex. Neither company had much cash—that was being preserved for survival. So any deal would have to be all-stock. But how do you value stocks when both are in free fall? How do you project synergies when you're not even sure what future demand looks like?

The negotiation process was unlike any M&A deal either company had experienced. Usually, buyers and sellers argue about growth projections and multiples. Here, they were arguing about how bad things could get. Centex wanted a higher exchange ratio, arguing its land positions would be valuable in recovery. Pulte countered that those same positions were massive liabilities if housing remained depressed.

The breakthrough came when both sides agreed to stop pretending they could predict the future. Instead of complex models and projections, they focused on a simple question: would the combined company be more likely to survive and thrive than either company alone? The answer was unequivocally yes.

On April 7, 2009, the deal was announced: Pulte would acquire Centex in an all-stock transaction, with Centex shareholders receiving 0.975 Pulte shares for each Centex share. Based on the previous day's closing prices, this valued Centex at $10.50 per share—a 38% premium to its trading price but still 87% below its 2006 peak.

Wall Street's reaction was mixed. Some analysts praised the strategic logic and long-term vision. Others questioned the timing. "It's like watching two drowning swimmers grab onto each other," one analyst told the Financial Times. "Either they save each other, or they both go down faster."

Inside both companies, the reaction was more complex. Pulte employees worried about job security—clearly, there would be massive redundancies. Centex employees felt both relief (their company would survive) and resentment (they were being absorbed by a competitor). Both cultures were proud, successful, and convinced their way was superior.

The integration planning began immediately, even before regulatory approval. Pulte assembled a 100-person integration team, drawing from both companies. Their mandate was straightforward but daunting: capture $350 million in annual synergies while maintaining operational continuity in the worst housing market in generations.

The first major decision was branding. Would Centex disappear? Would both brands continue? The solution was nuanced—the Centex corporate brand would be retired, but its valuable sub-brands like Fox & Jacobs would continue. The combined company would be called PulteGroup, signaling both continuity and transformation.

The organizational restructuring was massive. The companies had overlapping operations in most major markets. Two sets of division presidents, land acquisition teams, construction managers, and sales staff had to be consolidated into one. The decisions were brutal but necessary—ultimately, about 30% of the combined workforce would be eliminated.

But the real value creation came from operational improvements. Centex had been superior at certain things—its construction cycle times were 20% faster than Pulte's in comparable products. Pulte excelled in other areas—its customer satisfaction scores were industry-leading. The integration team's job was to identify and spread best practices across the combined entity.

The land portfolio optimization was particularly complex. The combined company now controlled over 200,000 lots—far too many for even an eventual recovery. But which ones to keep? Which to abandon? The team developed sophisticated models evaluating each position on multiple criteria: location quality, carrying costs, competitive dynamics, and recovery potential.

The financial results of the merger became apparent quickly. In Q3 2009, the first full quarter as a combined company, PulteGroup reported its cash burn had been reduced to $25 million—down from over $100 million quarterly for each standalone company. The company had $3.4 billion in liquidity, enough to survive even a prolonged downturn.

More importantly, green shoots were appearing. The federal homebuyer tax credit was stimulating demand. Mortgage rates were at historic lows. And in certain markets—particularly Texas, where Centex was strong—sales were actually increasing. The combined company was perfectly positioned to capitalize on any recovery.

The cultural integration proved more challenging than the operational one. Centex had been entrepreneurial, decentralized, and aggressive. Pulte was process-oriented, centralized, and conservative. The clash was inevitable and sometimes heated. But gradually, a new culture emerged—one that valued both discipline and initiative, both standardization and local market knowledge.

By March 2010, exactly one year after the merger announcement, PulteGroup had achieved something remarkable. It had successfully integrated two major companies during the worst housing crisis in history. It had maintained operational continuity while cutting costs dramatically. And it had positioned itself as the clear industry leader for the eventual recovery.

The new company name—PulteGroup, officially adopted in March 2010—symbolized this transformation. This wasn't just Pulte anymore, nor was it Centex. It was something new: a homebuilding platform with unmatched scale, geographic diversity, and operational capability. The question now was whether the housing market would recover enough to validate this audacious bet.

VII. Recovery & Reinvention (2010-2020)

The spring of 2010 found PulteGroup CFO Roger Cregg staring at a peculiar spreadsheet. For the first time in three years, weekly sales were consistently exceeding prior year comparisons. Not by much—maybe 5-10%—but the trend was unmistakable. "Either we've hit bottom," he told the executive team, "or we're about to fall off another cliff."

It was bottom. What followed was a recovery as gradual as the crash had been sudden. Housing didn't roar back—it crawled, stumbled, then slowly found its footing. And PulteGroup, now the industry's undisputed giant after digesting Centex, had to learn how to operate in an entirely new environment.

The post-crisis housing market bore little resemblance to the boom years. Mortgage lending had swung from absurdly loose to incredibly tight. The FHA became the dominant force, backing loans that private markets wouldn't touch. First-time buyers, who needed help with down payments, became precious commodities. And an entire generation—millennials who'd watched their parents lose homes—seemed skeptical of homeownership itself.

PulteGroup's response was to fundamentally rethink its product mix. The company shifted dramatically toward entry-level homes, leveraging the Centex acquisition's expertise in this segment. Average selling prices actually declined from 2010 to 2012, even as the broader economy recovered—a deliberate strategy to meet buyers where they were, not where Pulte wished they were.

The operational discipline instilled during the crisis became a permanent feature. The company implemented what executives called "asset-light" operations—using options and joint ventures to control land rather than outright purchases, turning inventory faster, and maintaining minimal spec home inventory. The old model of betting billions on land appreciation was dead.

In 2013, PulteGroup launched a program that captured the company's evolution: Built to Honor. The initiative provided mortgage-free homes to wounded veterans, but it was more than charity. It was a recognition that homebuilding was fundamentally about serving communities and that corporate purpose mattered in attracting both customers and talent. The program resonated deeply in a country grappling with two decades of war and its aftermath.

The leadership transition in 2016 marked another inflection point. Richard Dugas, who'd guided the company through the crisis and merger, stepped down. His replacement, Ryan Marshall, was a different breed of executive—younger, tech-savvy, and focused on the customer experience in ways that transcended traditional homebuilding metrics.

Marshall's first major strategic decision was surprising: move the company headquarters from Bloomfield Hills, Michigan, to Atlanta. The symbolism was powerful. Michigan represented the company's manufacturing heritage, its Rust Belt roots. Atlanta represented the future—a diverse, growing Sun Belt metropolis at the center of the new American economy.

But the real changes under Marshall were operational. He pushed digital transformation aggressively, recognizing that home buyers—especially millennials—expected Amazon-level digital experiences even when making the biggest purchase of their lives. PulteGroup developed virtual tour capabilities, online customization tools, and digital mortgage applications. The goal was to let buyers do everything except physically sign papers from their phones.

The 2016 acquisition of John Wieland Homes assets added another dimension. Wieland had built luxury homes for Atlanta's elite—the kinds of custom estates that Pulte had historically avoided. But Marshall saw opportunity in the high-end market, particularly as wealth inequality widened and luxury buyers sought new construction over existing homes.

Market dynamics during this period were fascinating. The recovery was deeply uneven—coastal California and tech hubs boomed while Rust Belt markets remained depressed. Labor shortages became acute as Mexican immigration tightened and American workers showed little interest in construction jobs. Material costs swung wildly with Chinese demand and trade policy.

PulteGroup navigated these challenges through scale and sophistication. The company's purchasing power helped moderate material cost increases. Its brand portfolio allowed it to attack different market segments simultaneously. And its geographic diversity meant it could shift resources to hot markets while pulling back from weak ones.

The April 2019 acquisition of American West Homes for $150 million showed the company's continued appetite for strategic growth. American West brought expertise in the Phoenix market and a reputation for innovative design. But more importantly, it showed that PulteGroup wasn't resting on its laurels—it was still hunting for ways to improve and expand.

Technology became increasingly central to operations. The company implemented sophisticated pricing algorithms that adjusted home prices daily based on traffic, sales pace, and competitive dynamics. Construction schedules were optimized using project management software adapted from aerospace. Customer satisfaction was tracked in real-time through digital surveys.

The financial results validated the strategy. By 2019, PulteGroup was generating returns on equity above 20%—exceptional for a capital-intensive business like homebuilding. Gross margins had expanded to 24%, well above historical norms. And the company was generating so much cash that it was returning billions to shareholders through dividends and buybacks.

But beneath the surface, new challenges were emerging. Housing affordability was deteriorating as home prices rose faster than incomes. Regulatory constraints and NIMBYism were making it increasingly difficult to build in coastal markets. Climate change was raising questions about building in flood zones and wildfire areas. And demographics suggested that the millennial home-buying wave might be smaller than expected due to student debt and delayed family formation.

As 2019 ended, PulteGroup executives were cautiously optimistic. The company had never been stronger operationally or financially. It had survived the worst crisis in industry history and emerged larger and more capable. But nobody was getting complacent. In homebuilding, the next crisis is always just around the corner.

What nobody expected was that the next crisis would come from a virus in Wuhan, China. And even more surprisingly, that this crisis would trigger not a housing collapse but the opposite—a boom that would rival anything from the bubble years, just with entirely different dynamics.

VIII. Modern Era: Scale, Technology & New Challenges (2020-Present)

Ryan Marshall was in his Atlanta home office on March 15, 2020, when he made the call that would have seemed insane just weeks earlier: "Shut down all our sales centers. Every single one. Immediately."

COVID-19 had arrived in America, and nobody knew what it meant for housing. The last pandemic to hit during modern times—the 1918 flu—had occurred before suburbs, before 30-year mortgages, before homebuilding was even an industry. PulteGroup, like every company in America, was flying blind.

The initial weeks were chaos. Construction sites shut down in some states, stayed open in others. Sales centers were closed to physical traffic, forcing agents to conduct virtual tours from empty model homes. The company's 12,000 employees shifted to remote work overnight—a transformation that would have taken years under normal circumstances.

Then something unexpected happened. Instead of collapsing, housing demand exploded. By May 2020, PulteGroup's online traffic had doubled. Virtual tours were booked solid. Sales agents were conducting Zoom calls from morning to night. The Federal Reserve had dropped rates to zero, pushing mortgage rates to historic lows. And suddenly, every knowledge worker in America wanted a home office.

The demand shift wasn't just quantitative—it was qualitative. Buyers didn't want condos in cities; they wanted houses in suburbs. They didn't care about short commutes; they wanted space. The very features that had seemed outdated in 2019—large lots, suburban locations, extra bedrooms—were now essential.

PulteGroup scrambled to adapt. The company accelerated its digital transformation by years in mere months. Virtual tours became sophisticated productions with drone footage and 3D walkthroughs. Digital closings were implemented where legally permissible. The entire customer journey was reimagined for a contactless world.

But the real challenge was operational. Lumber prices began a ascent that would see them quadruple from pre-pandemic levels. The Suez Canal blockage in March 2021 disrupted supply chains globally. Appliances became so scarce that PulteGroup was storing them in warehouses like precious commodities. Labor shortages reached crisis levels as workers stayed home and immigration remained restricted.

The company's response revealed the advantages of scale. PulteGroup could negotiate directly with lumber mills, securing supply when smaller builders couldn't buy at any price. Its purchasing power allowed it to pre-buy materials, locking in costs. And its geographic diversity meant it could shift production to markets with available labor.

The financial results were extraordinary. In 2021, PulteGroup generated $13.9 billion in revenue and $1.9 billion in net income—approaching the records set during the bubble years but with much healthier fundamentals. Home prices rose 20% annually, but unlike 2005, buyers could actually afford the payments thanks to 2.5% mortgage rates.

By 2023, new challenges emerged as the Fed aggressively raised rates to combat inflation. Mortgage rates spiked from 3% to 7%, triggering the most dramatic affordability crisis in decades. A family that could afford a $400,000 home in 2021 could only afford $300,000 by 2023—but home prices hadn't fallen commensurately.

PulteGroup's response was nuanced. Rather than slash prices, the company bought down mortgage rates for buyers, offering 5% rates when market rates were 7%. It shifted product mix toward smaller, more affordable homes. And crucially, it maintained pricing discipline, accepting lower volumes rather than destroying margins.

The company's 2024 performance validated this strategy. Revenue hit $17.95 billion, up 11.74% from 2023. Earnings reached $3.08 billion, up 18.91%. These weren't bubble-era results built on speculation—they were the product of operational excellence, scale advantages, and disciplined capital allocation.

The multi-brand strategy proved particularly valuable in this environment. Centex targeted first-time buyers struggling with affordability. Pulte served move-up buyers with existing equity. Del Webb captured baby boomers flush with retirement savings. DiVosta and John Wieland attacked the luxury segment. American West leveraged its Phoenix expertise as that market boomed. Each brand could optimize for its specific customer segment without diluting the others.

Technology investments accelerated under Marshall's leadership. The company implemented AI-powered pricing models that could adjust to market conditions in real-time. Construction management shifted to tablet-based systems that tracked every nail and board. Customer data was unified across brands, creating insights into buyer preferences and behaviors.

But perhaps the most significant change was in land strategy. Instead of speculating on raw land, PulteGroup increasingly used options and joint ventures to control lots. The company would partner with land developers, taking options on finished lots rather than buying raw acreage. This reduced capital requirements and risk while maintaining growth potential.

The labor challenge required creative solutions. PulteGroup established training programs with community colleges, creating pipelines of skilled workers. It invested in construction techniques that required less skilled labor—more factory-built components, simplified designs, and standardized processes. The company even experimented with construction robotics, though that remained more promise than reality.

Climate change added another layer of complexity. Hurricanes, floods, and wildfires were no longer rare events but regular occurrences. PulteGroup had to rethink where and how it built. The company developed new building standards for resilience, even when not required by code. It began avoiding certain geographic areas altogether, despite strong demand.

As 2024 progresses, PulteGroup faces a familiar but evolved set of challenges. Interest rates remain elevated, crimping affordability. Regulatory constraints make building increasingly difficult and expensive. Labor shortages show no signs of abating. And a new generation of buyers—Gen Z—has different preferences and less wealth than their predecessors.

Yet the company has never been stronger. With 775,000 homes built over seven decades, operations in 44 markets across 23 states, and a war chest of experience navigating every conceivable market condition, PulteGroup stands as testament to American homebuilding's evolution from mom-and-pop operations to sophisticated enterprises.

The question facing Marshall and his team isn't whether PulteGroup will survive—it's proven that capability repeatedly. The question is how homebuilding itself will evolve in an era of climate change, demographic shifts, technological disruption, and persistent affordability challenges. The answers will determine not just PulteGroup's future, but how America houses itself in the 21st century.

IX. Playbook: The PulteGroup Operating System

Walk into any PulteGroup division office from Phoenix to Charlotte, and you'll find the same document pinned to the wall: "The Five Pillars of Capital Allocation." It's not inspirational corporate speak—it's the mathematical framework that governs billions in annual investment decisions. This systematic approach to capital, refined over decades and stress-tested through multiple crises, forms the backbone of what insiders call the PulteGroup Operating System.

The first pillar is land acquisition, but not in the way most people understand it. During the bubble years, builders would buy raw land and pray for appreciation. PulteGroup's modern approach treats land like options trading. The company maintains a sophisticated model that evaluates every land parcel on dozens of variables: absorption rates, competing supply, infrastructure timing, regulatory risk, and demographic trends. But here's the key: instead of buying land outright, PulteGroup increasingly uses option contracts and joint ventures. A typical deal might involve putting down 10% to control land for three years, with multiple walkaway points if market conditions deteriorate.

This optionality proved invaluable during COVID. When demand exploded in 2020, PulteGroup could quickly exercise options to secure land. When rates spiked in 2022, the company could let expensive options expire. It's portfolio theory applied to dirt—diversification across markets, time horizons, and risk levels.

The second pillar involves construction efficiency, where PulteGroup has turned homebuilding into something approaching manufacturing. The company's construction cycle times are 20% faster than industry average—not through corner-cutting but through systematic process improvement. Every house follows a choreographed sequence of 200+ steps, with sophisticated software tracking progress and automatically scheduling inspections, deliveries, and labor.

The innovation here isn't technological—it's organizational. Each construction superintendent manages no more than 15 homes simultaneously, allowing deep focus on execution. Trades are scheduled in waves to minimize downtime. And critically, PulteGroup maintains preferred vendor relationships that guarantee labor availability even during shortages. These vendors get consistent volume and prompt payment; PulteGroup gets priority service and better pricing.

Multi-brand portfolio management forms the third pillar, and it's more complex than simply having different names on signs. Each brand has distinct product specifications, marketing strategies, and operational metrics. Centex homes are value-engineered for affordability—smaller lots, efficient floor plans, limited customization. Del Webb communities invest heavily in amenities that create lifestyle value. John Wieland homes offer extensive customization and premium finishes.

But the real sophistication is in market allocation. PulteGroup's planning team uses demographic data, economic projections, and competitive analysis to determine which brands to deploy where. Austin might get Centex for first-time buyers and Pulte for move-up buyers but no Del Webb because the retiree population is insufficient. This surgical precision maximizes returns while minimizing brand cannibalization.

The fourth pillar—mortgage and financial services integration—generates profits that most observers miss. PulteGroup Mortgage captures about 75% of buyers, generating not just origination fees but also gain-on-sale revenue when loans are sold to investors. The company's title and insurance operations add another layer of profitability. Combined, financial services contribute roughly 10% of PulteGroup's earnings but with minimal capital requirements.

The strategic value extends beyond profits. Having an in-house lender means PulteGroup can smooth transactions, reducing fall-through rates. During the rate spike of 2022-2023, PulteGroup Mortgage could offer below-market rates by accepting lower margins, keeping home sales flowing when competitors struggled.

The fifth pillar—managing through cycles—might be PulteGroup's greatest competitive advantage. The company maintains what executives call a "fortress balance sheet": debt-to-capital below 30%, over $1 billion in cash, and a $1.8 billion credit facility. This isn't conservatism for its own sake—it's recognition that homebuilding is inherently cyclical and leverage kills companies in downturns.

PulteGroup's cycle management extends to operations. The company maintains flexible cost structures, with significant portions of expenses variable. Land options can be abandoned. Construction can be slowed. Marketing can be dialed back. This flexibility allowed PulteGroup to reduce quarterly cash burn from $500 million to $25 million during the financial crisis—the difference between survival and bankruptcy.

The cultural elements binding this system together are less visible but equally important. PulteGroup pushes significant decision-making to division presidents, who function almost as CEOs of their markets. These executives have broad autonomy on product, pricing, and land decisions within corporate guidelines. But they're also held accountable through rigorous monthly reviews where performance is dissected and compared across markets.

This decentralized model creates entrepreneurial energy while maintaining corporate discipline. Division presidents who exceed targets earn significant bonuses and consideration for promotion. Those who underperform face scrutiny and potential replacement. It's Darwinian capitalism within a corporate structure.

The company's approach to innovation is deliberately measured. PulteGroup isn't trying to disrupt homebuilding—it's trying to perfect it. The company tests new ideas in limited markets before broad rollout. Digital closings were piloted in Texas for two years before national implementation. New floor plans are tested with focus groups and refined based on sales data.

This systematic approach extends to talent development. PulteGroup runs extensive training programs for construction managers, sales agents, and division leaders. The company recruits from top universities but also promotes from within, creating career paths from construction sites to executive suites. The result is institutional knowledge that compounds over decades.

Risk management permeates every decision. Land deals require multiple layers of approval. Construction defects are tracked obsessively, with root cause analysis preventing recurrence. Customer satisfaction scores are monitored in real-time, with problems addressed before they become widespread.

The PulteGroup Operating System isn't revolutionary—it's evolutionary, refined through 70 years of trial, error, and optimization. It's why the company can generate 20% returns on equity in a capital-intensive industry. It's why PulteGroup survived 2008 when peers didn't. And it's why, despite all the challenges facing homebuilding, PulteGroup continues to compound value year after year.

X. Analysis: Bull vs. Bear Case

The investment debate around PulteGroup crystallizes into two radically different visions of America's housing future. Bulls see a demographic destiny—millions of millennials finally buying homes, constrained supply, and a company perfectly positioned to capitalize. Bears see an affordability crisis spiraling toward collapse, with PulteGroup sitting atop a mountain of risk. Both sides marshal compelling evidence.

The Bull Case: Demographic Destiny Meets Supply Reality

The bulls start with simple math: America adds 1.5 million households annually but builds only 1.2 million housing units. This structural deficit, accumulating since 2008, has created a shortage estimated between 3 and 7 million homes. PulteGroup, as the third-largest builder, stands to capture outsized share of whatever building does occur.

The demographic argument is even more compelling. Millennials—America's largest generation at 72 million strong—are entering prime homebuying years. The median millennial is now 33, exactly the age when homeownership rates historically spike. Despite narratives about millennials preferring urban rentals, surveys consistently show 85% want to own homes eventually. They've just been delayed by student debt, late career starts, and the affordability challenges of the 2020s.

But here's what bulls find most exciting: household formation accelerated during COVID and hasn't slowed. Young adults who moved back with parents during the recession are finally leaving. Remote work has made homeownership feasible in affordable markets. And millennials are belatedly having children, driving demand for single-family homes over apartments.

The supply constraints appear almost insurmountable. Zoning restrictions make new development increasingly difficult. Environmental regulations add years to project timelines. Labor shortages in construction seem permanent—young Americans don't want these jobs, and immigration remains restricted. Material costs may moderate but won't return to pre-COVID levels. These factors create a protective moat around existing builders like PulteGroup who have scale, expertise, and relationships to navigate the complexity.

PulteGroup's specific advantages multiply these macro tailwinds. The company's balance sheet strength allows it to buy land when competitors can't access capital. Its multi-brand strategy captures every buyer segment from first-time to luxury. The Centex acquisition looks prescient in retrospect—providing exposure to entry-level buyers just as millennials enter the market.

Financial metrics support the bullish case. PulteGroup generates returns on equity above 20%, exceptional for any industry. The company's 24% gross margins are near historical highs but sustainable given supply constraints. Free cash flow generation is robust, funding both growth and billions in shareholder returns.

The technology investments position PulteGroup for continued market share gains. Digital marketing reaches buyers more efficiently than traditional methods. Virtual tours and online customization accelerate sales cycles. Data analytics optimize pricing and product mix. These aren't revolutionary advantages, but compound benefits that incrementally improve returns.

Bulls also point to optionality. If the government intervenes to address housing affordability—through subsidies, regulatory relief, or immigration reform—PulteGroup benefits disproportionately. If institutional investors continue buying single-family rentals, PulteGroup can sell in bulk. If manufacturing innovations like 3D printing or modular construction achieve scale, PulteGroup has the resources to adopt them.

The Bear Case: Peak Housing Meets Structural Headwinds

Bears start with a stark reality: at current prices and interest rates, only 15% of Americans can afford the median new home. This isn't a temporary disruption—it's a fundamental breakdown in housing mathematics. The monthly payment on a median PulteGroup home has doubled since 2020. Incomes haven't come close to keeping pace.

The interest rate environment looks particularly threatening. The Fed may have paused hiking, but rates aren't returning to the 2010s lows that made expensive homes affordable. Every percentage point increase in mortgage rates reduces buying power by 10%. If rates stay elevated—which seems likely given persistent inflation—demand destruction could be severe.

Bears see demographic headwinds where bulls see tailwinds. Yes, millennials are numerous, but they're also financially stressed. Student debt averaging $30,000 per borrower delays home purchases. Gig economy jobs don't qualify for traditional mortgages. And culturally, this generation seems less attached to homeownership as a life goal.

The next generation—Gen Z—looks even more challenging. They're smaller in number, more urban-oriented, and entering a job market where wages haven't kept up with housing costs. The traditional progression from apartment to starter home to move-up home may be breaking down.

Climate change poses existential risks that markets haven't priced. PulteGroup has significant exposure in Florida, Arizona, and Texas—states facing escalating natural disasters. Insurance costs are already spiking in these markets. At some point, areas simply become uninsurable or require such expensive mitigation that development becomes uneconomic.

Regulatory and political risks are mounting. The Biden administration's focus on affordable housing could lead to policies that crimp builder profits. Rent control initiatives, though typically focused on apartments, signal broader political hostility to housing profits. And local opposition to development—NIMBYism—grows stronger even as housing shortages worsen.

Bears question the sustainability of current margins. The 24% gross margins PulteGroup enjoys resulted from extraordinary circumstances—pandemic demand surge, low rates, desperate buyers. As conditions normalize, margins should compress to historical averages around 18-20%. That's a massive earnings headwind.

Competition is intensifying from unexpected directions. Tech-enabled builders like Lennar's digital initiatives threaten PulteGroup's traditional advantages. Build-to-rent operators compete for land and labor. And if modular or 3D-printed homes achieve breakthrough cost reductions, PulteGroup's conventional building methods could become obsolete.

The cyclical nature of homebuilding remains inescapable. Every past boom has ended in bust. The 2005 peak led to 2009's disaster. The current cycle, fueled by COVID and ultra-low rates, shows classic late-stage characteristics: stretched valuations, aggressive land acquisition, and universal bullishness. Bears see PulteGroup trading at 8x earnings not as cheap but as appropriate for a cyclical company near peak earnings.

Execution risks multiply with scale. PulteGroup operates in 44 markets with distinct dynamics. Managing construction quality, customer satisfaction, and regulatory compliance across this footprint is enormously complex. One bad development—a construction defect crisis, a discrimination lawsuit, a environmental violation—could damage the brand and trigger massive liabilities.

The Synthesis: Time Horizon Determines Truth

Both cases contain truth, but on different time horizons. The near-term (1-2 years) likely favors bears—affordability challenges and elevated rates will pressure volumes and margins. The medium-term (3-5 years) looks mixed—demographic demand meets affordability constraints, creating a grinding market. The long-term (5+ years) probably favors bulls—supply shortages and demographic destiny ultimately overwhelm temporary disruptions.

For investors, the question becomes: can PulteGroup navigate the near-term challenges while maintaining positioning for long-term opportunity? History suggests yes—this company has survived every crisis homebuilding has faced. But past performance, as they say, doesn't guarantee future results. The next crisis is always different from the last one.

XI. Power & Counter-Positioning

In Silicon Valley, they talk about "network effects" and "platform dynamics." In homebuilding, the power laws are different—older, more tangible, but no less decisive. PulteGroup's competitive advantages don't come from software or viral growth. They come from scale economics that compound relentlessly, brand power that takes decades to build, and operational excellence that's nearly impossible to replicate.

Start with scale, the most obvious but underappreciated advantage. When PulteGroup negotiates with a lumber supplier, it's not buying for one subdivision—it's buying for hundreds of active communities across 44 markets. This purchasing power translates to cost advantages of 5-10% on materials, which in a business with 24% gross margins is enormous. But scale goes beyond procurement. PulteGroup can spread fixed costs—technology investments, corporate overhead, marketing campaigns—across far more units than smaller competitors. The company spends $50 million annually on technology; spread across 30,000 homes, that's manageable. For a builder doing 1,000 homes, it's prohibitive.

The scale advantages compound in subtle ways. PulteGroup can afford specialists that smaller builders can't—architects who optimize floor plans for construction efficiency, lawyers who navigate complex entitlements, data scientists who model pricing dynamics. These capabilities create a virtuous cycle: better execution leads to higher returns, which fund more capabilities, which improve execution further.

Brand power in homebuilding seems paradoxical—houses are ultimately commodities, right? Wrong. The largest purchase most families ever make carries enormous emotional and financial risk. Buyers gravitate toward builders they trust, and trust takes decades to establish. PulteGroup's portfolio of brands each carry distinct associations. Del Webb means active adult communities with resort amenities. Pulte signals quality construction and good value. Centex represents affordability without compromising safety.

These brand associations translate to pricing power—typically 3-5% premiums versus unknown builders—and faster sales velocity. In hot markets, this might seem irrelevant. But in balanced or soft markets, brand recognition determines who sells homes and who sits on inventory.

The financial services integration creates another layer of advantage. PulteGroup Mortgage doesn't just generate profits—it creates a seamless customer experience that reduces transaction friction. When 75% of buyers use PulteGroup's mortgage services, the company controls more of the value chain and customer relationship. This integration also provides information advantages—PulteGroup knows exactly what buyers can afford and tailors products accordingly.

Counter-positioning against traditional competitors is straightforward—PulteGroup has advantages they can't match. But the more interesting dynamic is how PulteGroup positions against potential disruptors. Tech-enabled builders promise to revolutionize construction through automation, prefabrication, or AI-driven design. The reality has proven more complex.

Katerra, the SoftBank-backed construction unicorn, burned through $2 billion before collapsing in 2021. Its premise—vertically integrated, tech-enabled building—failed because construction is stubbornly local, regulated, and complex. Each municipality has different codes. Each site has unique characteristics. Each buyer wants customization. Software can optimize these variables but can't eliminate them.

PulteGroup's response to tech disruption has been selective adoption rather than wholesale transformation. The company uses technology extensively—BIM modeling, scheduling software, CRM systems—but within traditional construction methods. This pragmatic approach captures efficiency gains without the execution risk of revolutionary change.

The platform versus product debate illuminates PulteGroup's strategic positioning. Pure product companies—those just building houses—face commodity competition. Pure platform companies—those trying to be "Uber for housing"—struggle with the physical complexity of construction. PulteGroup operates in the middle: a platform of capabilities (land acquisition, construction, sales, financing) delivering physical products (homes).

This positioning creates defensive moats. A new entrant can't just build houses—they need land expertise, subcontractor relationships, regulatory knowledge, and customer acquisition capabilities. Tech companies can't just write software—they need to manage construction sites, deal with weather delays, and handle customer complaints about squeaky floors.

Network effects in homebuilding are subtle but real. As PulteGroup builds more homes in a market, it gains better subcontractor relationships, deeper regulatory knowledge, and stronger brand recognition. These advantages compound—the company that built 1,000 homes in Phoenix has inherent advantages building the 1,001st that a new entrant can't match.

The land market creates particularly powerful dynamics. Landowners prefer selling to established builders who can close with certainty. Municipalities prefer working with builders who have track records of successful development. These preferences give PulteGroup preferential access to the best land positions—a crucial advantage in a business where location drives value.

But perhaps PulteGroup's greatest power is optionality. The company can build anything from $200,000 starter homes to $2 million custom estates. It can develop master-planned communities or infill townhome projects. It can sell to individual families or bulk sell to institutions. This flexibility allows PulteGroup to adapt to market changes faster than specialized competitors.

The counter-positioning extends to capital markets. PulteGroup's investment-grade credit rating and NYSE listing provide access to capital that private builders can't match. During downturns, this becomes decisive—PulteGroup can buy distressed assets while competitors struggle to survive.

The synthesis of these advantages creates what strategists call "increasing returns to scale"—the bigger PulteGroup gets, the harder it becomes to compete against. This isn't monopolistic—there are thousands of builders in America. But at the scale of building hundreds of communities and tens of thousands of homes annually, only a handful of companies can compete. And the barriers to reaching that scale grow higher each year.

XII. What Would Happen Next?

The year is 2030. The housing industry looks fundamentally different, shaped by forces already visible but not yet fully realized. Demographics, technology, climate change, and policy have transformed not just how homes are built but what "home" itself means. PulteGroup's strategic choices over the next five years will determine whether it leads this transformation or becomes its casualty.

The consolidation endgame accelerates first. Today's top 10 builders control 30% of new home sales. By 2030, that figure reaches 50%. The math is inexorable—scale advantages compound, regulatory complexity favors large players, and capital requirements exclude subscale competitors. PulteGroup faces a critical decision: be an acquirer, be acquired, or watch market share erode.

The most likely scenario sees PulteGroup absorbing regional builders in strategic markets. These aren't billion-dollar deals like Centex but surgical acquisitions—a strong Houston builder here, a California land portfolio there. Each deal adds density, capabilities, or geographic coverage. The cumulative effect transforms PulteGroup from number three to challenging for number one.

But consolidation could take unexpected turns. What if Amazon or another tech giant decides housing is the next frontier? They have capital, technology, and customer relationships. A partnership or acquisition wouldn't be unprecedented—look at Amazon's Whole Foods deal. PulteGroup's brand portfolio and operational expertise combined with Amazon's technology and customer reach could create something unprecedented.

Technology disruption remains the wildcard. By 2030, several innovations reach inflection points. 3D-printed homes, still experimental today, achieve cost parity with traditional construction for certain designs. Modular construction, refined over decades, finally cracks the code on quality and customization. Autonomous vehicles reshape land values—if commuting is productive time, distant suburbs become more attractive.

PulteGroup's response shapes its future. The conservative path involves incremental adoption—use 3D printing for certain components, partner with modular manufacturers for specific products, optimize for autonomous vehicle communities in select markets. The aggressive path means fundamental transformation—acquiring technology companies, retrofitting factories, retraining workforces. History suggests PulteGroup chooses the former, but competitive pressure might force the latter.

Demographic shifts create new imperatives. The baby boom generation, PulteGroup's profitable Del Webb customers, begins aging out of active adult communities into assisted living. Millennials finally become the dominant buyer cohort but with different preferences—smaller homes, urban-adjacent locations, sustainable features. Gen Z emerges as first-time buyers, bringing expectations shaped by sharing economy and environmental consciousness.

PulteGroup's multi-generational strategy evolves accordingly. Del Webb communities add healthcare components, partnering with providers to create continuum-of-care campuses. Pulte homes shrink in size but increase in efficiency, with home offices and multi-functional spaces. Centex develops new models for Gen Z—perhaps rent-to-own programs or co-housing arrangements that acknowledge this generation's financial constraints.

Climate change forces geographic strategy reconsideration. By 2030, certain markets become untenable. Phoenix faces water crises that restrict new development. Florida coastal areas face insurance costs that destroy affordability. California wildfire zones become unbuildable. Meanwhile, previously overlooked markets—Michigan, Wisconsin, the Carolinas—experience climate-driven migration booms.

PulteGroup must make hard choices about market presence. Exiting Florida or Arizona means abandoning decades of infrastructure and relationships. But staying might mean accepting lower returns or catastrophic risks. The likely outcome involves strategic retreats from the most vulnerable areas while doubling down on climate-resilient markets.

Policy interventions reshape industry economics. The housing affordability crisis reaches breaking points by 2027-2028, forcing government action. This could take multiple forms: massive subsidy programs, zoning reform mandates, public-private partnerships for affordable development, or even direct government construction programs.

Each scenario impacts PulteGroup differently. Subsidies might boost demand but come with strings—affordability requirements, wage mandates, diversity commitments. Zoning reform could unlock land supply but increase competition. Public-private partnerships might provide steady revenue but lower margins. PulteGroup's lobbying efforts and strategic positioning determine whether policy changes become tailwinds or headwinds.

The next housing cycle provides the ultimate test. Whether triggered by recession, interest rate shocks, or black swan events, another downturn is inevitable. But the next cycle might differ from historical patterns. Institutional ownership of single-family rentals creates new demand dynamics. Remote work permanently alters geographic preferences. Government intervention might prevent the free-fall seen in 2008.

PulteGroup's preparation determines survival and opportunity. The company might shift to more capital-light models—building for institutional owners rather than individuals. It might expand services revenue—property management, renovation, technology platforms. Or it might simply execute its historical playbook—maintain discipline, preserve capital, and acquire distressed assets.

The international question looms larger. American homebuilders have historically been domestic-focused, but that might change. Canada offers similar markets with less competition. Mexico presents massive affordable housing opportunities. Even Europe, with its different building traditions, might welcome American efficiency and scale.

PulteGroup testing international waters wouldn't be shocking. Start with Canada—similar regulations, integrated economies, familiar dynamics. Success there could lead to broader expansion. By 2030, "PulteGroup International" might contribute 10-20% of revenues.

The cultural evolution might be most profound. Homeownership itself faces existential questions. If young Americans can't afford homes, does the ownership model break? Do new models emerge—fractional ownership, blockchain-based housing cooperatives, corporate-owned housing with lifetime leases? PulteGroup must decide whether to defend traditional ownership or embrace new models.

The scenario planning suggests multiple futures, each requiring different capabilities. PulteGroup might become a technology company that happens to build houses. Or a services company managing housing assets others own. Or double down on traditional building with unprecedented efficiency. Most likely, it becomes all of these simultaneously—different models for different markets, customers, and conditions.

What seems certain is that linear extrapolation fails. The PulteGroup of 2030 won't be today's company with bigger numbers. It will be fundamentally transformed—by choice or by force. The only question is whether PulteGroup drives that transformation or merely responds to it. History suggests the former, but history also suggests that every industry leader eventually faces disruption it didn't see coming.

XIII. Recent News**

Latest Quarterly Earnings Performance**

PulteGroup delivered exceptional third-quarter 2024 results that exceeded Wall Street expectations across all key metrics. The company reported earnings of $3.35 per share, beating the Zacks Consensus Estimate of $3.10 per share and representing a 16% increase from $2.90 per share a year ago. Revenue reached $4.48 billion, up 12% from the prior year's $4 billion.