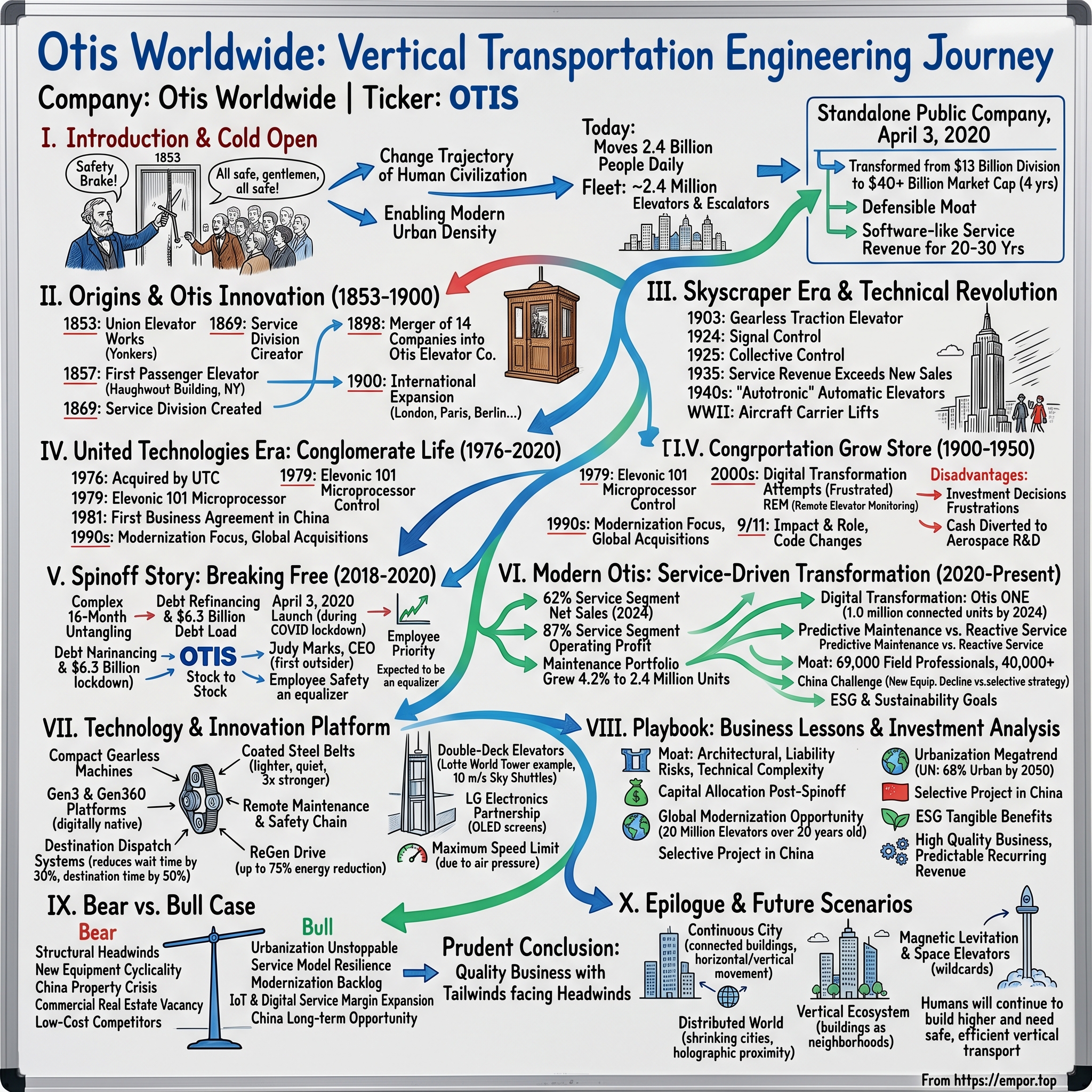

Otis Worldwide: The Engineering of Vertical Transportation

I. Introduction & Cold Open

Picture this: May 1853, New York's Crystal Palace Exhibition. A crowd gathers around a peculiar contraption—an open platform suspended by a single rope, hovering three stories above the ground. On it stands a bearded man in a top hat, Elisha Graves Otis, founder of what would become the world's largest elevator company. With theatrical flair borrowed from P.T. Barnum's playbook, he raises an axe high above his head. "Cut the rope!" he commands his assistant. The crowd gasps. The rope snaps. The platform drops—then jerks to a stop after falling mere inches. Otis removes his hat with a flourish: "All safe, gentlemen, all safe!"

That moment—equal parts engineering breakthrough and vaudeville showmanship—changed the trajectory of human civilization. Before Otis's safety brake, buildings rarely exceeded five stories. Climbing stairs was the price of vertical living, and elevators were death traps used primarily for hauling freight. His invention didn't just make tall buildings possible; it fundamentally rewired how humans organize themselves in space, enabling the density that defines modern urban life.

Today, Otis moves 2.4 billion people daily—equivalent to one-third of humanity—through its fleet of approximately 2.4 million elevators and escalators worldwide. The company that started in a Yonkers sawdust-strewn factory has become synonymous with vertical transportation itself. When you press an elevator button anywhere from Manhattan to Mumbai, there's a 20% chance you're summoning an Otis machine. The company's equipment operates in the world's most iconic structures: the Empire State Building, the Eiffel Tower, the Burj Khalifa, and until their tragic destruction, the World Trade Center towers.

Yet for all its ubiquity, Otis remained buried inside United Technologies Corporation for 44 years, its story subsumed within a sprawling industrial conglomerate. That changed on April 3, 2020, when Otis Worldwide Corporation began trading independently on the New York Stock Exchange—emerging as a standalone public company in the midst of the COVID-19 pandemic, perhaps the worst possible timing for a company dependent on urban density and commercial real estate.

The timing proved irrelevant. Within four years, Otis has transformed from a $13 billion division into a $40+ billion market capitalization powerhouse, demonstrating that sometimes the oldest business models—moving people up and down—remain the most durable. This is the story of how a safety mechanism invented 171 years ago became the foundation of modern urbanization, evolved through multiple technological revolutions, survived conglomerate captivity, and emerged as one of the most successful industrial spinoffs in recent memory.

The elevator industry operates on a business model that would make any software executive envious: sell the hardware once, then collect service revenues for the next 20-30 years. It's the original subscription business, predating SaaS by a century. With switching costs that make enterprise software look flexible—try changing elevator brands in a 50-story building—and network effects in dense urban markets where technician proximity determines response times, Otis has built one of the most defensible moats in industrial history.

But this isn't just a business story. It's a tale of how engineering excellence, patient capital, and perfect timing can create enduring value. It's about recognizing that the most boring businesses—the ones we literally don't think about—often generate the most extraordinary returns. And it's about understanding that in an age obsessed with disruption, sometimes the real opportunity lies in businesses that have been doing the same thing, incrementally better, for over a century and a half.

II. Origins & The Otis Innovation (1853-1900)

The year 1851 found Elisha Graves Otis not as an inventor but as a master mechanic at a bedstead factory in Bergen Hill, New Jersey. At 40 years old, he had already failed at multiple businesses—a gristmill, a sawmill, a machine shop—each venture teaching him something about mechanical systems while emptying his pockets. When the bedstead factory needed to move heavy equipment between floors, Otis was tasked with installing a hoisting platform. The assignment would have been forgettable except for one detail: two workers had recently died when a hoisting rope snapped at another factory.

Otis's solution was elegantly simple. He attached wagon springs to the platform's guide rails, connected to a ratchet system. If the lifting rope broke, the springs would engage, locking the platform in place. It wasn't the first safety mechanism for hoists—others had tried complex counterweight systems—but Otis's design was reliable, cheap to manufacture, and easy to maintain. The bedstead factory installed it and promptly forgot about it.

When that factory burned down in 1852, Otis planned to join the California Gold Rush. But fate intervened in the form of Benjamin Newhouse, a furniture maker who had heard about Otis's safety device. Newhouse wanted two freight elevators for his Hudson River factory. The order was worth $300—enough to delay California. Otis set up shop in Yonkers, New York, in September 1853, founding what he called the Union Elevator Works. His first year was disastrous: he sold just three elevators for $900 total, barely covering expenses.

The turning point came through P.T. Barnum, the master showman who ran the American Museum. Barnum understood that spectacle sold, and when he learned about Otis's invention, he arranged for a demonstration at New York's Crystal Palace Exhibition in 1853. The rope-cutting stunt wasn't just theater—it was brilliant marketing that addressed the core customer concern: safety. Orders jumped from 3 in 1853 to 15 in 1854 to 27 in 1855.

The first passenger elevator was installed in 1857 at the E.V. Haughwout & Co. department store on Broadway—a five-story cast-iron building that still stands today. At $300 per floor, it was expensive, but Haughwout understood something revolutionary: customers would climb one flight of stairs to shop, maybe two, but five flights meant the upper floors were essentially worthless retail space. The elevator changed that calculus entirely. Suddenly, upper floors could command premium rents because they offered better light and less street noise.

When Elisha died suddenly of diphtheria in 1861 at age 49, the company employed just a dozen workers and had installed fewer than 100 elevators. His sons, Charles and Norton, ages 26 and 21 respectively, inherited a business generating about $15,000 annually—decent but hardly remarkable. What they also inherited was impeccable timing: the Civil War had just begun.

The war transformed Otis from a specialty manufacturer into an industrial supplier. The Union Army needed elevators for arsenals, hospitals, and supply depots. Navy shipyards required heavy-duty hoists for moving artillery and ammunition. By 1864, the company was shipping an elevator every three days, a tenfold increase from pre-war levels. Charles handled engineering and manufacturing while Norton managed sales and administration—a partnership that would last four decades.

The post-war boom brought unprecedented urban growth. Chicago, rebuilt after the 1871 fire, became a laboratory for vertical construction. New York competed with ever-taller buildings. The Otis brothers made two crucial decisions during this period. First, they refused to license their patents, maintaining quality control even as demand exploded. Second, they established a service division in 1869, recognizing that ongoing maintenance contracts could provide steady revenue between new installations.

By 1873, Otis had installed 2,000 elevators—more than all competitors combined. But the Panic of 1873, one of the worst depressions in American history, nearly destroyed the company. Orders evaporated. The brothers cut their own salaries to zero and borrowed heavily to meet payroll. They survived by pivoting to modernization—convincing building owners to upgrade their freight elevators for passenger use, a lower-cost sale during tight times.

The 1880s brought technological revolution. In 1889, Otis introduced the first successful direct-connected electric elevator, eliminating the need for basement hydraulic pumps that had limited building height to about 20 stories. The electric elevator was faster, smoother, and could theoretically rise indefinitely—though no one yet imagined buildings exceeding 30 floors.

Competition intensified as fourteen elevator companies emerged, many founded by former Otis employees. Price wars erupted. Patent disputes clogged courts. In 1898, Charles and Norton orchestrated a remarkable solution: they merged all fourteen companies into Otis Elevator Company, capitalized at $11 million (roughly $400 million in 2024 dollars). The consolidated entity controlled 65% of the U.S. elevator market and held 186 patents.

International expansion began almost immediately. By 1900, Otis had offices in London, Paris, Berlin, and St. Petersburg. The company didn't just export American elevators; it adapted designs for local preferences. European customers preferred enclosed cars with ornate ironwork. Russian clients demanded extra heating systems. The French wanted operators' stools upholstered in velvet.

As the 19th century closed, Otis had installed roughly 20,000 elevators worldwide. Cities were beginning their vertical ascent, though the true skyscraper age remained a few years away. The safety elevator had proven its worth, but it would take one more innovation—the gearless traction elevator—to unleash the full potential of vertical cities.

III. The Skyscraper Era & Technical Revolution (1900-1950)

The problem with early electric elevators was speed—or rather, the lack of it. Gear-driven systems could manage perhaps 300 feet per minute, fine for buildings under 20 stories but impractical for anything taller. The gears themselves were massive, noisy contraptions that required constant lubrication and frequent replacement. Building owners complained about the grinding sounds that echoed through elevator shafts at all hours.

In 1903, Otis engineer David Lindquist achieved a breakthrough that would redefine urban architecture. Instead of using gears to reduce motor speed, Lindquist's design connected the drive sheave directly to a slow-speed, high-torque motor. The gearless traction elevator could achieve speeds of 700 feet per minute—later pushing past 1,200—while operating so smoothly that passengers often couldn't tell they were moving.

The first gearless traction installation went into New York's Beaver Building in 1904. Within months, every architect planning a building over 20 stories specified Otis gearless systems. The technology arrived just as steel-frame construction and improved foundation techniques made true skyscrapers feasible. It was a perfect convergence of enabling technologies.

The 1920s roared vertically. Manhattan became an architectural arms race as developers competed to build higher. The Woolworth Building (1913, 57 stories), the Chrysler Building (1930, 77 stories), and the Empire State Building (1931, 102 stories) each pushed the boundaries of what elevators could accomplish. The Empire State Building alone required 73 Otis elevators, including express cars that could travel from the lobby to the 80th floor in under a minute—a feat that seemed like science fiction just a decade earlier.

But Otis's most important innovation of the era wasn't about speed or height—it was about traffic flow. In 1924, the company introduced "Signal Control," the first system where passengers could register their floor destination before entering the elevator. The system would then automatically group passengers going to similar floors, dramatically reducing travel time. A year later came "Collective Control," which allowed a single operator to manage multiple elevators from a central panel, cutting building operating costs by 40%.

The real genius was recognizing that elevator efficiency wasn't just about mechanical performance but about managing human behavior. Otis hired psychologists to study passenger patterns. They discovered that people consistently overestimate wait times by a factor of three, that mirrors near elevators reduce perceived wait time by 25%, and that displaying floor indicators decreased anxiety even when they didn't speed up service. These insights led to design changes that had nothing to do with engineering but everything to do with user experience.

The 1929 crash and subsequent Depression should have devastated Otis. New construction plummeted 95% between 1929 and 1933. The Empire State Building, completed in 1931, stood largely empty for years, earning the nickname "Empty State Building." Yet Otis not only survived but strengthened its market position through a counterintuitive strategy: it shifted focus from selling elevators to servicing them.

Norton Otis, who had become president after Charles's death in 1914, recognized that thousands of elevators installed during the 1920s boom still needed maintenance. He offered building owners a deal: Otis would guarantee elevator performance through comprehensive service contracts, assuming all repair costs in exchange for a predictable monthly fee. Competitors, desperate for any revenue, typically charged for individual service calls.

The service contract model was transformative. By 1935, service revenue exceeded new equipment sales for the first time. The contracts provided steady cash flow during the worst economic crisis in American history while creating switching costs that locked in customers for decades. When construction eventually recovered, building owners naturally turned to Otis for new installations.

World War II brought unexpected challenges and opportunities. The War Production Board banned new elevator installations in non-essential buildings, but military contracts more than compensated. Otis built specialized elevators for aircraft carriers, including high-speed lifts that could move fully loaded fighter planes from hangar to flight deck in 45 seconds. The company also developed the first explosion-proof elevators for munitions factories.

The war accelerated technological development. Military requirements for reliability in extreme conditions led to improved seal designs, better electrical components, and new safety systems. Many of these innovations found their way into civilian elevators after 1945. The company also gained expertise in hydraulic systems from building aircraft carrier elevators, knowledge that would prove valuable in the post-war suburban boom where low-rise hydraulic elevators became standard.

By 1950, Otis had installed its 500,000th elevator, more than all competitors combined. The company dominated not through monopolistic practices but through relentless innovation and superior service. It held over 2,000 patents, operated factories on five continents, and maintained service operations in every major city worldwide.

The introduction of automatic elevators—requiring no human operator—began in the late 1940s with Otis's "Autotronic" system. Using a room-sized computer with 17,000 relays, Autotronic could manage traffic patterns, optimize wait times, and even "learn" from usage patterns. It was primitive by modern standards but revolutionary for its time, pointing toward a future where elevators would become increasingly intelligent and autonomous.

IV. United Technologies Era: Conglomerate Life (1976-2020)

The boardroom at United Technologies headquarters in Hartford, Connecticut, was tense on October 6, 1975. Harry Jack Gray, UTC's CEO for barely a year, had just presented his hostile takeover offer for Otis Elevator Company—$42 per share for 55% of outstanding stock, a 12% premium to market price. Otis management, led by CEO Ralph Weller, sat across the mahogany table, stone-faced. "We built this company for 122 years," Weller said. "We're not interested in becoming someone's division."

Gray leaned back, unperturbed. The former Litton Industries executive had been brought to UTC specifically to diversify away from military contracts as Vietnam wound down. UTC's motivation was to end its heavy dependence on military contracts at the end of the Vietnam War, with the diversification partially to balance civilian business against any overreliance on military business. Otis, with its steady service revenues and global footprint, was the perfect hedge against defense spending cycles.

Otis's management at first resisted the offer but dropped its opposition in November after UTC agreed to pay an additional $2 per share and buy up all of Otis's common stock. The cost was estimated at $276 million. The untendered shares were exchanged for shares of a new convertible preferred United Technologies stock under a 1976 merger. What changed Otis's mind wasn't just the sweetened offer—it was Gray's promise to maintain operational autonomy and invest heavily in R&D, areas where independent Otis had been struggling to fund adequately.

The timing of the acquisition coincided with an embarrassing revelation. In 1976 the company revealed to a federal agency that it estimated it had made between $5 million and $6 million in improper payments during the past five years, some of them to foreign government officials and employees. These payments were made in connection with installations in large buildings where government involvement was substantial and bribery and kickbacks were allegedly normal procedures. The scandal, while not devastating, weakened Otis's negotiating position and made UTC's deep pockets and compliance infrastructure more attractive.

Life inside a conglomerate brought immediate benefits. UTC's aerospace division, particularly Hamilton Standard which had helped put astronauts on the moon, possessed advanced microprocessor technology that Otis's engineers had only dreamed about. 1977 saw the introduction of "Elevonic" - the successor to Autotronic - which was the first solid state, digital microprocessor-based elevator control system. Otis introduced the Elevonic™ 101 elevator in 1979, a system controlled by microprocessors. The compact operation cuts travel time by coordinating elevator speed, position and direction with a building's traffic flow. Otis engineers develop the technology with Hamilton Standard, the UTC aerospace unit that had helped put astronauts on the moon.

The Elevonic system represented a quantum leap from the relay-based controls that had dominated since the 1940s. Where traditional systems required entire rooms filled with clicking relays, Elevonic fit into a cabinet the size of a refrigerator. More importantly, it could be reprogrammed without rewiring—building managers could optimize traffic patterns for morning rush, lunch, or evening exodus with software changes rather than hardware modifications.

But the real strategic masterstroke came in 1981, not through technology but through geography. In 1981, Otis signed a business agreement with an elevator company in China. While competitors dismissed China as too poor and politically unstable, Otis saw the world's largest future construction market. The company established joint ventures, transferred technology, and most crucially, trained thousands of Chinese technicians who would become the backbone of its Asian operations.

The same year brought a symbolic end to an era: In 1981, the Yonkers factory closed. The flagship Yonkers factory, parts of which dated back to 1868, was deemed obsolete and abandoned in 1983. The closure of Elisha Otis's original factory might have been traumatic for an independent company, but within UTC's portfolio, it was simply rational capital allocation. Production shifted to more modern facilities in Connecticut, South Carolina, and increasingly, overseas.

During the 1980s, Otis developed the Remote Elevator Monitoring (REM) system that collected behavioral data from 300,000 elevators. REM was revolutionary—sensors tracked door operations, motor temperature, brake wear, and hundreds of other parameters, transmitting data via phone lines to regional service centers. Technicians could diagnose problems before customers noticed them, shifting from reactive to predictive maintenance. This wasn't just about service quality; it fundamentally changed the economics of the service business by reducing emergency calls and extending equipment life.

The 1967 World Trade Center project deserves special attention, though it predated the UTC acquisition. Otis wins the contract to engineer, manufacture and install elevators and escalators for the Twin Towers at the World Trade Center in New York City, the tallest buildings in the complex, rising 110 floors each. Otis overcomes numerous technical challenges to deliver arguably the largest vertical transportation system in history at the time. A terrorist attack on September 11, 2001, destroyed the towers and sadly claimed many lives. The technical challenge was unprecedented: moving 50,000 workers efficiently through 110 floors required revolutionary thinking. Otis created the "sky lobby" system—express elevators to the 44th and 78th floors where passengers transferred to local elevators. This three-zone approach became the template for all future supertall buildings.

The tragedy of September 11, 2001, hit Otis particularly hard. Not only were 99 Otis elevators destroyed, but the company's service technicians were among the heroes who kept elevators running during evacuation, with several losing their lives. The disaster led to fundamental changes in elevator safety codes worldwide, with Otis leading development of fire-service modes, emergency communication systems, and evacuation protocols that are now standard.

Throughout the 1990s and 2000s, Otis embarked on an acquisition spree funded by UTC's balance sheet. Otis Elevator Company purchased Evans Lifts in the UK when Evans Lifts Ltd went bankrupt in 1997, giving Otis access to the lucrative UK modernization market. The LG partnership in Korea was particularly complex—negotiations took three years and involved creating multiple joint venture structures to satisfy Korean ownership requirements.

Otis also took over the shares of LG Industrial Systems Elevator in December 1999 and changed the name of LG Industrial Systems Elevator to LG-OTIS. At the same time, the existing Korea OTIS was merged with it. In 2000, LG-OTIS founded Sigma Elevator and used Sigma brand to replace LG-OTIS, LG and Goldstar Brand at Overseas (International). The company name was also changed back to OTIS-LG. After the acquisition of shares was completed in 2005, LG Industrial Systems was separated into LS Industrial Systems and the 'LG' trade name was removed to become 'Otis Elevator Korea'. This complicated corporate maneuvering gave Otis dominant position in Korea's rapidly growing market.

In 2011, Otis acquired its competitor Marshall Elevator for an undisclosed amount, eliminating a regional competitor while acquiring valuable service contracts in the southeastern United States.

Yet for all these successes, life inside UTC wasn't without frustrations. Investment decisions required multiple layers of approval. Talented executives were routinely rotated to other UTC divisions—good for the conglomerate, disruptive for Otis. Most gallingly, Otis's steady cash flows were often diverted to support UTC's more volatile aerospace ventures. Between 1990 and 2010, Otis generated over $15 billion in operating profit, much of which funded Pratt & Whitney's engine development programs rather than elevator innovation.

Digital transformation attempts in the 2000s highlighted these constraints. Otis engineers proposed an IoT platform in 2008 that would connect every elevator to the cloud, enabling predictive analytics and remote diagnostics. UTC management killed the project, deeming it too expensive and outside core competencies. Competitors KONE and Schindler, unencumbered by conglomerate bureaucracy, launched similar platforms that gained market share.

By 2015, activist investors began circling UTC, arguing that the conglomerate structure destroyed value. Otis, generating consistent 20% operating margins, was worth more to shareholders as an independent company than as a cash cow for aerospace ventures. The pressure intensified when UTC announced its $30 billion acquisition of Rockwell Collins in 2017—a deal that would require significant cash and potentially starve Otis of growth capital.

On November 26, 2018, United Technologies announced it would spin off Otis Elevator into an independent company. After 44 years inside the conglomerate, Otis would finally regain its independence. The announcement sent UTC stock up 5%—Wall Street clearly agreed that the sum of the parts exceeded the whole.

V. The Spinoff Story: Breaking Free (2018-2020)

March 11, 2020. The world was about to change in ways no one could imagine. In Farmington, Connecticut, Judy Marks sat in UTC's boardroom as directors approved the final mechanics of the Otis spinoff. United Technologies Corp. (NYSE: UTX) announced today that its Board of Directors approved the previously announced separations of Carrier and Otis. The NBA had suspended its season the night before. Tom Hanks had just announced he had COVID-19. Markets were in freefall.

"We're really doing this," Marks thought, watching the vote. Three weeks before becoming CEO of an independent public company, and the world was shutting down.

The spinoff announcement in November 2018 had triggered a complex 16-month untangling of a business that had been woven into UTC's fabric for 44 years. Hayes told industry analysts in January 2019 that costs to separate UTC into three businesses — aerospace, Otis and Carrier — are estimated at between $2.5 billion and $3 billion. This wasn't just corporate surgery—it was separating conjoined triplets, each with distinct organs but sharing critical systems.

The numbers were staggering. UTC had to restructure 1,200 legal entities across 200 countries. Otis alone operated in virtually every jurisdiction on Earth, each with its own tax code, labor laws, and regulatory requirements. Transfer and other taxes in jurisdictions worldwide are pegged at nearly $2 billion. Transaction costs to restructure 1,200 legal entities in UTC and put information technology and treasury systems in place are estimated at $500 million. Debt refinancing was expected to be about $300 million, he said.

But the real challenge wasn't legal or financial—it was psychological. Otis employees had UTC badges for two generations. Their email addresses ended in @utc.com. Their stock options, retirement plans, healthcare—everything tied back to the conglomerate. Now they had to recreate an independent identity while maintaining service for 2.4 million elevators that couldn't stop running for even a day.

Judy Marks had been preparing for this moment since joining Otis as President in October 2017. Judy joined Otis in October 2017 as President. She was appointed CEO in June 2019 and in April 2020 led the successful spin of Otis to an independent publicly traded company on the NYSE. Her appointment itself was revolutionary—I came in as the first outsider to ever run Otis. After 164 years of internal succession, UTC had brought in someone with zero elevator experience.

But Marks's background was precisely what Otis needed. Prior to Otis, she held senior leadership roles at three global icons – IBM, Lockheed Martin and Siemens AG where she served as CEO of both Siemens USA and Dresser-Rand, a Siemens business. She understood complex global operations, had managed through multiple business cycles, and most importantly, had experience with corporate transformations. At Siemens, she'd overseen the integration and subsequent spinoff of Dresser-Rand, learning firsthand how to maintain operational excellence while restructuring ownership.

Her first challenge was winning over a skeptical workforce. So it wasn't even just first outsider and oh, by the way, quite a few of the people who were coming to work for me interviewed for the role internally. So you had that dynamic, too. Long-tenured executives who'd spent decades climbing Otis's ladder suddenly reported to an outsider who couldn't distinguish between a governor and a controller.

Marks addressed this head-on, spending her first six months visiting field operations. She rode with service technicians at 3 AM, attended safety meetings in multiple languages, and most importantly, listened. Her message was consistent: "I'm not here to tell you how to fix elevators. I'm here to help you build a company that can thrive independently."

The financial engineering of the spinoff was equally complex. Otis needed to establish its own credit rating, arrange independent financing, and determine an optimal capital structure—all while attached to UTC. In connection with the distribution, we have completed certain financing transactions, and we intend to complete one or more additional financing transactions on or prior to the completion of the distribution, with an aggregate of approximately $6.3 billion of the proceeds of such financings expected to be used to distribute cash to UTC. As a result of these transactions, we anticipate having approximately $6.3 billion in aggregate principal amount of outstanding indebtedness when the distribution is completed.

The $6.3 billion debt load was controversial. Critics argued it handicapped Otis from day one, saddling the company with interest payments that would constrain growth investment. Defenders countered that the leverage was appropriate for a business with Otis's stable cash flows and that the debt markets were offering historically low rates.

The mechanics of the distribution were straightforward but the timing was anything but. To effect the separations, the UTC Board of Directors declared a pro rata dividend of Carrier Global Corporation (NYSE: CARR) common stock and Otis Worldwide Corporation (NYSE: OTIS) common stock to be made effective at 12:01 a.m. EDT on April 3, 2020 to UTC's shareowners of record as of 5:00 p.m. EDT on March 19, 2020, the record date for the distribution. Each UTC shareowner will receive one (1) share of Carrier common stock and one-half (0.5) share of Otis common stock for every one (1) share of UTC common stock held on the record date.

March 19, 2020—the record date—came as global markets were experiencing their worst volatility since 2008. The S&P 500 had fallen 30% in three weeks. Liquidity was evaporating. Companies were drawing down credit lines in panic. Into this maelstrom, UTC was launching two new public companies.

The irony was palpable. Otis, whose business depended on people moving through buildings, was going public as the world implemented lockdowns. Elevators in office towers sat idle. Hotels were empty. Shopping malls closed. The very premise of vertical transportation was being questioned as people asked whether dense urban living was sustainable in a pandemic world.

Yet the April 3, 2020 launch proceeded on schedule. Raytheon Technologies Corporation announced on Friday, April 3, that the all-stock merger between the company and United Technologies Corporation (UTC) has been completed. This merger follows the completion of the spin-offs of UTC's Carrier and Otis businesses. There was no bell-ringing ceremony at the New York Stock Exchange—the trading floor was closed. No champagne toasts or employee celebrations. Just Judy Marks in her home office, watching OTIS appear on screens for the first time in 100 years (the company had first listed in 1920).

So, there was actually this very unique community and almost an equalizer amongst CEOs where we would all jump on, you pick it, WebEx, Teams, Zoom, whatever anybody had, and they'd say, What are you doing? What are you doing? And it was a great equalizer because even though I was relatively new, even the experienced leaders hadn't been through it. Everyone was new. The pandemic created an unexpected camaraderie among newly independent companies. Marks found herself on daily calls with the CEOs of Carrier, DowDuPont's spinoffs, and other recent separations, sharing playbooks for managing through crisis while building new corporate functions.

The immediate priority was employee safety. Otis service technicians were deemed essential workers—someone had to keep hospital elevators running. The company implemented new safety protocols within days, sourced PPE when it was scarce, and most critically, guaranteed no COVID-related layoffs. This last decision, made in the first week of independence, sent a powerful message: Otis would protect its people even in crisis.

VI. Modern Otis: Service-Driven Transformation (2020-Present)

The elevator at One Vanderbilt in Manhattan rises so smoothly that passengers often don't realize they're moving until the floor indicator shows they've climbed 20 stories in 30 seconds. This imperceptible acceleration—a triumph of engineering that would have amazed Elisha Otis—represents modern Otis's approach to business: invisible excellence generating visible returns.

Full year net sales of $14.3 billion increased 0.4%, with a 1.4% increase in organic sales, driven by Service. Adjusted operating profit of $2.4 billion increased $87 million at actual currency and $118 million at constant currency, driven by Service. GAAP operating profit margin contracted 130 basis points to 14.1%, and adjusted operating profit margin expanded 50 basis points to 16.5%, driven by favorable Service segment performance and mix.

The numbers tell a story of transformation. In 2024, the New Equipment segment contributed 38% of net sales, while the Service segment contributed 62%. The Service segment also accounted for 87% of the segment operating profit, highlighting its significance in the company's operations. This isn't just a business mix shift—it's a fundamental reimagining of what an elevator company can be.

To understand Otis's modern strategy, forget everything you think you know about elevators. The real business isn't selling metal boxes that go up and down—it's managing the lifecycle of vertical transportation assets over decades. A new elevator installation might generate $500,000 in revenue with 5-10% margins. But that same elevator, serviced for 25 years, generates $1.5 million in service revenue at 25% margins. The math is compelling: lose money on the razor, make a fortune on the blades.

Our industry-leading maintenance portfolio grew 4.2% to approximately 2.4 million units, a number that represents both scale and stickiness. Each unit in the portfolio generates recurring monthly revenue through maintenance contracts that rarely churn. Building owners don't switch elevator service providers lightly—the liability risks, tenant disruption, and technical complexity create switching costs that software companies dream about.

The modernization business has emerged as the hidden growth engine. Organic maintenance and repair sales increased 5.7% and organic modernization sales increased 11.7%. Modernization sits between new equipment and routine service—upgrading 20-year-old elevators with new controls, cabin interiors, or safety systems. It's a $10 billion global market growing at 5-7% annually, driven by aging building stock and evolving safety codes.

Consider the typical modernization project: a 1990s-era office building in Chicago needs to upgrade its elevators to meet new energy efficiency standards and provide touchless controls post-COVID. Otis proposes a $2 million modernization that reduces energy consumption by 30%, increases speed by 20%, and adds predictive maintenance capabilities. The building owner gets modern elevators without the disruption of full replacement. Otis gets high-margin revenue and locks in the service contract for another decade.

Digital transformation, long promised but slow to deliver, is finally bearing fruit. Otis ONE, a cloud-based IoT technology, continues to expand, with approximately 1.0 million units connected globally by the end of 2024. This isn't just about remote monitoring—it's about fundamentally changing the service model.

Traditional elevator service operated on fixed schedules: monthly inspections, quarterly adjustments, annual overhauls. Technicians would arrive, run diagnostics, fix problems, and leave. If an elevator broke between visits, tenants suffered and emergency calls were expensive.

Otis ONE flips this model. Sensors track door operations, motor temperature, brake wear, and hundreds of other parameters in real-time. Machine learning algorithms identify patterns that predict failures before they occur. A slight vibration in the motor bearing that human technicians might miss triggers an alert. A technician arrives with the right part before the elevator fails, turning emergency repairs into routine maintenance.

The economics are transformative. Emergency service calls cost Otis 3-5 times more than scheduled maintenance due to overtime, expedited parts, and customer credits. By shifting from reactive to predictive service, Otis reduces service costs while improving uptime—a rare win-win that drops straight to the bottom line.

But technology alone doesn't explain Otis's service dominance. The real moat is the field force—69,000 employees, with over 40,000 field professionals who know every elevator in their territory. These technicians, many with 20+ years of experience, possess institutional knowledge that can't be replicated by competitors or disrupted by startups.

Geographic density creates network effects. In Manhattan, Otis services elevators in over 3,000 buildings within a 23-square-mile area. A technician can service multiple buildings in a single day, parts can be shared across locations, and emergency response times are measured in minutes. A new entrant trying to compete would need to build similar density from scratch—an investment measured in decades, not quarters.

The China challenge looms large over the business. The New Equipment segment saw a significant decline in China, with sales dropping by more than 20%, reflecting the broader property crisis. China represented 35% of global new equipment installations in 2020; that's dropped to under 25% as developers default and construction slows.

Yet Otis's response demonstrates strategic discipline. Rather than chase volume with price cuts, the company has focused on selective projects with creditworthy developers and government infrastructure. Market share has actually increased even as absolute volumes declined—a textbook example of profitable retreat.

The Americas and EMEA markets provide counterbalance. Americas and Asia Pacific regions experienced mid single-digit growth, and EMEA saw low single-digit growth. The U.S. commercial real estate market, despite headlines about office vacancies, continues to invest in elevator modernization. Building owners recognize that premium tenants demand premium vertical transportation—outdated elevators can literally devalue a property.

The UpLift productivity program represents management's commitment to operational excellence. The company also expects the UpLift program to generate approximately $200 million in annual run-rate savings by the second half of 2025, with restructuring and transformation costs of approximately $300 million. This isn't typical corporate cost-cutting—it's systematic process improvement. Standardizing components across product lines, automating back-office functions, and optimizing service routes all contribute to structural margin improvement.

ESG initiatives, often dismissed as corporate virtue signaling, have tangible business benefits for Otis. Otis has set ambitious ESG goals, including reducing absolute scope 1 and 2 GHG emissions by 55% by 2033 and sourcing 100% of factory electricity from renewable energy by 2030. The company is committed to achieving zero-waste-to-landfill certification for all factories by 2025. Energy-efficient elevators command premium pricing, green building certifications require modern elevator systems, and sustainability commitments resonate with the facility managers who influence purchase decisions.

The financial model has proven remarkably resilient. Through COVID lockdowns, China property crises, and interest rate spikes, Otis has delivered consistent results. For the full year, we delivered organic sales growth and strong adjusted margin expansion for the fourth consecutive year. The quarter and the year show that our strategic New Equipment, Service and modernization flywheel is working with more growth in the higher margin elements of the business.

This isn't just financial engineering—it's the result of a business model that aligns perfectly with long-term trends. Urbanization continues despite remote work. Aging infrastructure requires modernization. Safety regulations tighten, not loosen. Building owners need partners, not vendors. Every trend points toward more demand for exactly what Otis provides: reliable, efficient, safe vertical transportation backed by comprehensive service.

VII. Technology & Innovation Platform

Stand in the machine room of a modern skyscraper and you'll hear something remarkable: silence. Gone are the grinding gears and whirring motors that defined elevators for a century. In their place, compact gearless machines no larger than a washing machine move 30-passenger cars at speeds approaching 40 miles per hour with barely a whisper.

The physics of vertical transportation hasn't changed since Elisha Otis—gravity still pulls down, motors still pull up—but the engineering has achieved near-magical efficiency. Consider the Lotte World Tower in Seoul, where Otis designed a pair of high-tech double-deck elevators that make the trip in just 60 seconds, travelling at 10 meters per second, making these Sky Shuttles among the world's fastest doubledeck elevators. This isn't just speed for speed's sake—it's a mathematical necessity. Moving 50,000 people daily through 123 floors requires velocities that would have seemed impossible just decades ago.

The secret lies in three converging technologies: materials science, control systems, and energy regeneration. Modern elevator cables aren't cables at all—they're smooth coated steel belts that reduce noise from metal-to-metal contact of steel ropes to deliver a smooth, quiet, ride. These polyurethane-coated steel belts, pioneered in Otis's Gen2 system and evolved in the Gen3 and Gen360 platforms, last twice as long as conventional ropes while requiring no lubrication. The belts are 20% lighter than cables but 3 times stronger, enabling higher speeds with smaller motors.

The Gen3 and Gen360 platforms represent Otis's strategic bet on standardization. The Gen3 elevator is a new, digitally native elevator platform that combines the proven design of the Gen2 elevator with the connectivity of the Otis ONE IoT digital platform. Rather than custom-engineering each installation, Otis created modular systems that can be configured for different building types. This isn't just manufacturing efficiency—it's about embedding intelligence from day one.

Otis ONE monitors equipment health and performance in real time, 24/7. The information is collected and analyzed and accessible to customers immediately with full transparency. Every door operation, every floor stop, every acceleration curve feeds data to machine learning algorithms that predict maintenance needs weeks in advance. A slight degradation in door-close time might indicate worn rollers. An imperceptible vibration could signal bearing wear. The system schedules maintenance before passengers notice anything wrong.

The energy equation has been revolutionized by regenerative drives. Combined with ReGen™ Drive, reduces energy consumption up to 75%. When an empty elevator goes up or a full elevator comes down, gravity does the work. The motor becomes a generator, feeding electricity back into the building's grid. In a busy office building, elevators can generate 30% of their own power—enough to light entire floors.

But the real innovation in modern elevators isn't mechanical—it's algorithmic. Destination dispatch systems fundamentally reimagined elevator logic. Instead of pressing "up" and hoping for the best, passengers enter their floor on a keypad in the lobby. The system assigns them to a specific elevator that will make the fewest stops. Studies show this reduces average wait time by 30% and destination time by 50%.

The mathematics are complex. The system must solve a real-time optimization problem considering current car positions, passenger destinations, traffic patterns, and even time of day. During morning rush, the algorithm might dedicate certain elevators to express service to upper floors. At lunch, it might prioritize restaurant floors. The system learns patterns—the 42nd floor empties at 5:47 PM every weekday—and pre-positions elevators accordingly.

The Gen360™ platform eliminates the need to perform any maintenance operation from the top of the car. As a result, you no longer need refuge space at the top of the hoistway, nor do you need "protrusion" on the roof of the building. This isn't just convenience—it's architectural freedom. Buildings can have flat roofs, simpler structural designs, and more rentable space. The maintenance platform folds into the ceiling, allowing technicians to work safely from inside the car rather than on top of it.

Safety systems have evolved from mechanical to electronic intelligence. Moving from mechanical to electronic, the brand-new design of Gen360's safety chain allows 24/7 monitoring, immediate situational evaluation and remote actions while increasing the overall performance and efficiency of the elevator for peace of mind. Traditional safety brakes were binary—engaged or not. Modern systems modulate braking force based on load, speed, and position. If a cable snaps (virtually impossible with modern redundancy), the elevator doesn't just stop—it decelerates at a rate that won't injure passengers.

The Lotte World Tower installation showcases what's possible when engineering pushes boundaries. The total installation includes 30 elevators — 11 SkyRise® units (including two double-deck elevators) and 19 Gen2® elevators, along with 19 escalators, in the country's tallest vertical structure at 555 m. Sky Shuttle, the double-deck elevator, runs 496 m from the second basement to the building's observation deck, Seoul Sky, on the 121st floor. Using a single hoistway, it can carry 54 passengers to the top in 1 min.

The engineering challenges were staggering. To bear the elevator's speed, weight and traveling distance, Otis used cables that weigh more than 10 T, as well as traction machines specially designed to stand the weight of 100 T each. To install the two double-deck passenger elevators, as well as two other, single-deck elevators for emergency use, Otis needed to lift and place four 100-T traction machines (with a machine weight of 21.6 T each) in the machine room at the top of the skyscraper.

The installation process itself required innovation. Typically, buildings have a flat roof that is still open when elevator machines are lifted from the ground and then lowered into the machine room at the top of the building. But the Lotte World Tower pinnacle resembles two spires – an architectural element that complicated installation of four 100-ton traction machines, each weighing more than 21 tons. Special rigging had to be built to maneuver the machines into place without damaging the two spires. In a complex procedure rehearsed multiple times, the traction machines first had to lifted from the ground to a spot on the 124th floor. Once inside, special rigging was used to move the heavy machines into their correct position, safely and precisely – without damaging the spires.

But technology is only part of the story. The passenger experience has been completely reimagined. Created by LG Electronics, 60, 55-inch organic LED (OLED) screens cover the entire elevator interior surface, including the ceiling, excluding only the doors. Otis provided software to precisely synchronize the OLED signage's digital content with the elevator controls. During the 60-second journey, passengers don't just ride—they experience a virtual tour through Seoul's history, creating an attraction that draws visitors independent of the observation deck itself.

Looking forward, the limitations of traditional elevator technology are becoming clear. "I predict the maximum speed of a vertical lift cabin cannot be more than 79 feet per second," he says. "This is not because we can't make lifts that go faster than this, but because of the air pressure." If a lift traveled faster than this, he says, it wouldn't give passengers enough time to acclimatize to the air pressure on the top floor. Engineers would need to pressurize the entire building, like an airplane cabin.

This physical limit is driving innovation in new directions. Magnetic levitation elevators, eliminating cables entirely, could enable horizontal as well as vertical movement. Twin elevator systems, with two independent cars in one shaft, could double capacity without additional hoistways. Predictive dispatching using AI could reduce wait times to near zero.

The real revolution may be in reimagining vertical transportation entirely. Why move people when you can move spaces? Rotating buildings, transformable floors, and virtual presence might make physical transportation obsolete. But until that science fiction becomes reality, companies like Otis continue pushing the boundaries of what's possible within the laws of physics.

The data advantage Otis possesses—2.4 million units generating billions of data points daily—creates an insurmountable moat for competitors. Every elevator trip teaches the system something new. Every service call improves predictive algorithms. Every modernization adds to the knowledge base. It's a learning system that gets smarter with scale, and no competitor can match Otis's scale.

VIII. Playbook: Business Lessons & Investment Analysis

The best business models hide in plain sight. Warren Buffett famously looks for companies with "moats"—competitive advantages that protect profits from competition. Elevators might be the perfect example: a 170-year-old technology that's both indispensable and invisible, generating returns that would make software executives envious.

The elevator industry operates on what venture capitalists would recognize as a "land and expand" strategy, though Otis was executing it when Silicon Valley was still orchards. Sell the elevator at breakeven or even a loss—that's the land. Then expand through decades of service contracts, modernizations, and eventual replacement. A building owner might grudgingly pay $500,000 for a new elevator, but they'll happily pay $2,000 monthly for service that keeps tenants happy. Over 25 years, that service contract generates $600,000 in revenue at 25% margins versus 5-10% on the original sale.

This isn't the razor/razorblade model—it's better. Gillette customers can switch to Dollar Shave Club with a click. But try switching elevator brands in a 40-story building. The switching costs aren't just financial; they're architectural. Elevator shafts are literally built around specific equipment dimensions. Control systems integrate with building management systems. Service technicians know every quirk of every installation. Switching providers might save 10% on service costs but risks 90% more downtime.

Network effects compound these switching costs in dense urban markets. In Manhattan, Otis services elevators in buildings literally next door to each other. A technician can walk from one service call to the next. Parts inventory serves multiple buildings. Emergency response time is measured in minutes. A competitor trying to service a single building in Otis territory faces impossible economics—they need dedicated technicians and parts inventory for one contract while Otis spreads those costs across hundreds.

The capital allocation story post-spinoff demonstrates how independence unlocks value. Under UTC, Otis's cash flow funded aerospace R&D and acquisitions. Investment decisions required multiple approvals from executives who didn't understand elevators. Now, management can act quickly on opportunities specific to their industry.

Consider the modernization opportunity. Globally, there are approximately 20 million elevators over 20 years old. These units are functional but inefficient—using 50% more energy than modern systems, lacking digital capabilities, and requiring increasing maintenance. For building owners, modernization is a capital expense that can be depreciated. For Otis, it's a high-margin service that extends equipment life and locks in service contracts.

The math is compelling. A typical modernization costs $150,000—new controller, motors, and cabin interior while reusing the shaft and rails. Otis earns 20% margins on the project, then extends the service contract for another 10-15 years. The building owner gets a "new" elevator for 30% less than replacement cost. Tenants get modern features and reliability. Otis gets recurring revenue. Everyone wins except competitors locked out for another generation.

Geography becomes destiny in this business. Urbanization is the megatrend that matters—not just population growth but density. Every prediction about distributed work, suburban flight, or virtual reality runs into a simple reality: humans are social animals who cluster in cities. The UN projects 68% of humanity will live in cities by 2050, up from 55% today. That's 2.5 billion additional urban dwellers, each needing vertical transportation.

But not all geography is equal. China's property crisis demonstrates the risk of overexposure to new construction. In 2019, China represented 60% of global new elevator installations. By 2024, that's fallen to 40% as developers default and projects stall. Otis's response—focusing on quality over quantity, government infrastructure over private development—shows strategic discipline. Better to lose market share than chase bad revenue.

Service margin expansion represents the most predictable value creation opportunity. Current service margins of 25% could expand to 30%+ through three levers: IoT-enabled predictive maintenance reducing costs, price increases on captive customers, and mix shift toward higher-margin modernization. Each 100 basis points of margin expansion adds roughly $90 million to operating profit—straight to the bottom line.

The IoT transformation is still early innings. With 1 million units connected out of 2.4 million in the portfolio, Otis has years of runway. Each connected unit reduces service cost by 15-20% through predictive maintenance while improving customer satisfaction through reduced downtime. The data collected enables new revenue streams—energy optimization services, traffic flow consulting, predictive analytics for building managers.

ESG considerations, often dismissed as virtue signaling, have real business impact in elevators. Buildings account for 40% of global energy consumption, with elevators representing 5-10% of a building's energy use. Energy-efficient elevators with regenerative drives can reduce consumption by 75%. For a building owner facing ESG reporting requirements or seeking LEED certification, Otis's green technology isn't nice-to-have—it's necessary.

The competitive landscape favors scale. KONE, Schindler, ThyssenKrupp, and Otis control 65% of the global market. Regional players struggle to match R&D spending, global service capabilities, and purchasing power. Chinese manufacturers have gained share in their home market but struggle internationally due to service requirements and safety concerns. The industry is consolidating toward a stable oligopoly where competition is rational and margins are protected.

Capital allocation under independent management has been exemplary. Rather than empire-building acquisitions, Otis has focused on bolt-on deals that add service density or technical capabilities. Share buybacks have reduced share count by 8% since the spinoff, effectively increasing per-share value. The dividend, yielding approximately 2%, provides income while leaving flexibility for growth investment.

The risk factors are real but manageable. Commercial real estate headwinds affect new installations but not the service base. Technology disruption from ropeless elevators or alternative transportation remains decades away. Labor relations require careful management but haven't resulted in major disruptions. China exposure is concerning but decreasing as a percentage of revenue.

Understanding Otis requires thinking in decades, not quarters. The elevator installed today will operate for 20-30 years, generating service revenue every month. The building constructed today will stand for 50-100 years, requiring multiple modernizations. The city growing today will densify for centuries, requiring ever more vertical transportation.

This is a business model perfected over 170 years, now enhanced with digital capabilities and global scale. It's boring, predictable, and essential—exactly the characteristics that generate superior long-term returns. While markets obsess over the next disruptive technology, Otis quietly compounds value by moving people up and down, day after day, year after year.

IX. Bear vs. Bull Case

The investment case for Otis splits cleanly between those who see inevitable decline and those who see inexorable growth. Both sides marshal compelling evidence. The truth, as always, lies in understanding which factors matter most.

The Bull Case: Urbanization's Unstoppable Force

Start with the mega-trend that matters: humanity is moving to cities. This isn't a prediction—it's happening now. Every week, 3 million people move to cities globally. By 2050, cities will add 2.5 billion residents. Each requires vertical transportation because horizontal sprawl has limits—commute times, infrastructure costs, environmental impact. The only direction is up.

The service model resilience has been battle-tested through COVID, the 2008 financial crisis, and countless regional downturns. Service revenue never declined more than 5% in any crisis because elevators must keep running. Hospitals need functioning elevators. Apartment buildings can't leave residents stranded. Even vacant office buildings maintain elevator service to preserve property value and enable showings.

The modernization backlog provides multi-year visibility that most companies dream about. With 20 million elevators globally over 20 years old, and modernization cycles accelerating due to energy efficiency requirements and safety regulations, Otis has identified $40+ billion in modernization opportunities just within its existing service base. Building owners can defer new construction but can't defer keeping existing elevators operational.

IoT and digital services are still in their infancy, with margin expansion potential that's only beginning to be realized. Connected elevators reduce service costs by 20% while improving uptime. Predictive maintenance transforms the P&L—fewer emergency calls, optimized technician routes, reduced parts inventory. As the connected base grows from 1 million to 2.4 million units, the incremental margins are extraordinary because the digital infrastructure already exists.

China's eventual recovery, though timing remains uncertain, represents massive optionality. China urbanization is only 65% complete versus 82% in the U.S. and 75% in Europe. When China's property market stabilizes—and history suggests it will—Otis is positioned with local manufacturing, trained technicians, and government relationships. A return to even half of peak installation rates would add $500+ million in revenue.

The competitive dynamics favor rational behavior. With four players controlling 65% of the market, price wars are self-defeating. Everyone understands that service contracts are the prize, not equipment sales. This leads to stable pricing, rational competition for new installations, and focus on service quality rather than price. It's closer to a regulated utility than a commodity business.

Valuation remains reasonable despite strong performance. At 22x forward earnings, Otis trades at a discount to quality industrials and a significant discount to software companies with similar recurring revenue characteristics. If the market recognized Otis's service business as subscription revenue—which it essentially is—the multiple would be 30x or higher.

Management has proven execution capability through the spinoff, pandemic navigation, and China downturn. They've delivered on every financial target, expanded margins despite inflation, and returned capital efficiently. This isn't a turnaround story requiring faith—it's a proven model requiring continued execution.

The Bear Case: Structural Headwinds Intensify

New equipment cyclicality can't be ignored forever. New equipment is 38% of revenue and drives future service growth. When new construction stops, service growth eventually slows. We're seeing this in China now—new equipment down 20%+ with no recovery in sight. The same could happen in Western markets as commercial real estate struggles with remote work impacts.

China's structural slowdown might not be cyclical but secular. Demographics are destiny—China's population is shrinking, aging, and already more urbanized than optimists acknowledge. The property bubble isn't just deflating; the entire model of debt-fueled construction is broken. Ghost cities don't need elevators. Empty apartments don't generate service revenue. Otis's China exposure, still 20% of revenue, is a melting ice cube.

Commercial real estate faces existential challenges. Office vacancy rates in major U.S. cities exceed 20%. San Francisco, Seattle, and other tech hubs see 30%+ vacancy. These aren't temporary dislocations—they're permanent changes in how humans work. Empty offices don't just reduce new equipment sales; they pressure service contracts as building owners desperately cut costs.

Competition from low-cost providers is intensifying. Chinese manufacturers, desperate for growth as their home market shrinks, are exporting aggressively. They're winning on price in Southeast Asia, Africa, and Latin America. While they can't match Otis's service network today, they're learning. In 10 years, CREC and Canny might be global competitors.

Technology disruption risk is real, even if timing is uncertain. ThyssenKrupp's MULTI system—magnetic levitation elevators moving horizontally and vertically—isn't science fiction. It's operating in test towers. Once perfected, it obsoletes traditional elevators in new construction. Otis's installed base provides protection, but what happens when new installations dry up?

Labor challenges are intensifying globally. Elevator technicians require years of training. Young workers aren't entering the trades. In developed markets, the average technician is over 45 years old. Rising labor costs pressure service margins. Unions have leverage because specialized skills can't be quickly replaced. The equation of rising costs and worker shortages threatens the service model's profitability.

Interest rate impacts haven't fully materialized. Higher rates increase construction financing costs, reducing new building starts. They also pressure building owners' economics, making modernization projects harder to justify. While Otis has navigated the initial rate shock, sustained higher rates could create a multi-year construction drought.

Valuation assumes perfection. At 22x earnings with organic growth of 1-2%, Otis is priced for flawless execution. Any disappointment—China recovering slower, service margins compressing, modernization projects delayed—would trigger multiple compression. The stock has tripled since the spinoff; easy gains are behind us.

Weighing the Evidence

The bull case rests on inexorable trends—urbanization, aging infrastructure, service model resilience. These are powerful forces operating on decade-long timescales. Cities aren't going away. Buildings aren't getting shorter. Elevators aren't becoming optional.

The bear case highlights immediate pressures—China's property crisis, office vacancies, rising costs. These are real challenges affecting quarterly results. But they're also potentially temporary, or at least manageable through cycle.

The key question: Is Otis a cyclical business facing structural challenges or a secular growth story experiencing cyclical headwinds? The answer determines whether current valuation represents opportunity or risk.

History suggests betting against urbanization is foolish. Every prediction of city decline—from cars enabling suburbs to COVID enabling remote work—has proven premature. Humans cluster for economic opportunity, social interaction, and cultural amenities. That won't change because of Zoom.

But history also warns that no business model is permanent. Kodak dominated film. IBM dominated mainframes. AT&T dominated telecommunications. Each seemed invincible until technology shifted. Could magnetic levitation or hyperloops make traditional elevators obsolete? Perhaps, but probably not for decades.

The prudent conclusion: Otis is a high-quality business with secular tailwinds facing cyclical headwinds. The service model provides downside protection. The modernization opportunity offers growth. The technology transition presents both risk and opportunity. At current valuation, it's neither compelling value nor excessive speculation—it's a reasonable price for a good business.

For investors with decade-long horizons, the bull case dominates. For those focused on next quarter's earnings, the bear case looms large. As with elevators themselves, the destination matters more than temporary stops along the way.

X. Epilogue & Future Scenarios

Imagine Elisha Otis visiting Manhattan today. The bearded inventor who demonstrated his safety brake by cutting a rope in 1853 would find a city that exists because of his invention. Not despite it, not alongside it, but because of it. Without the safety elevator, New York would be Amsterdam—charming, flat, constrained. With it, Manhattan became the vertical city that defines urban possibility.

Would he recognize his invention in a modern elevator? The safety principle remains—elevators still have brakes that engage if cables fail. But everything else has transformed. Where he used steam power and hemp ropes, modern elevators use permanent magnet motors and polyurethane-coated steel belts. Where he achieved 40 feet per minute, modern systems reach 4,000. Where he manually operated a single car, algorithms now coordinate dozens of elevators in millisecond precision.

Yet the fundamental human need hasn't changed. We still need to move vertically through our built environment. We still demand safety, speed, and reliability. We still take for granted that pressing a button will summon a metal box that carries us skyward. Otis's invention didn't just enable tall buildings—it rewired human psychology to think vertically.

Looking forward 50 years, vertical transportation faces three possible futures, each with profound implications for Otis and society.

Scenario 1: The Continuous City

By 2075, cities have become three-dimensional organisms. Buildings connect not just at ground level but at multiple sky bridges. Elevators move horizontally as well as vertically, creating continuous interior environments. You could travel from your apartment to your office to dinner without ever going outside, moving through a network of interconnected vertical transportation.

Otis evolved from moving people to orchestrating movement. Their systems don't just operate individual elevators but manage entire transportation networks within buildings and between them. AI predicts movement patterns down to individual preferences. Your elevator is waiting before you've decided to leave.

This future favors Otis's installed base advantage. Retrofitting existing buildings with magnetic levitation systems that enable horizontal movement is easier than complete reconstruction. The company's service network evolves into a transportation management platform, optimizing flow through entire cities.

Scenario 2: The Distributed World

Climate change and pandemic memories drive massive de-urbanization. Cities shrink as virtual presence technology makes physical proximity unnecessary. Holographic meetings are indistinguishable from in-person. Robotic avatars allow remote physical presence. The age of concentration reverses into an age of distribution.

Vertical transportation becomes niche—servicing hospitals, hotels, and historical preservation sites. The installed base generates cash but doesn't grow. Otis pivots to other forms of automated movement—warehouse robotics, autonomous logistics, home automation. The company's expertise in moving things safely and efficiently translates to new domains.

This scenario challenges everything about Otis's model. Service contracts on a shrinking base face pricing pressure. New installations disappear. Yet the company's engineering expertise, safety culture, and global service network remain valuable. The question becomes whether management can redeploy these assets quickly enough.

Scenario 3: The Vertical Ecosystem

Cities don't just grow taller—they become vertical ecosystems. Buildings reach 300+ stories, housing 50,000 people in vertical neighborhoods. Elevators aren't just transportation but social spaces, with cars large enough for meetings, meals, and recreation during 5-minute journeys.

Vertical farms feed cities from within towers. Manufacturing happens on industrial floors. Recreation occurs on sky parks. The elevator becomes as important as roads were to horizontal cities—the crucial infrastructure that makes everything else possible.

Otis thrives in this scenario. Ultra-high-speed elevators using vacuum tube technology move at airplane speeds. Multi-directional systems create three-dimensional transportation networks. Service evolves from mechanical maintenance to ecosystem management. The company's role expands from moving people to enabling vertical civilization.

Technology Wildcards

Several technologies could fundamentally disrupt vertical transportation:

- Room-temperature superconductors would enable magnetic levitation without cooling, making ropeless elevators economical

- Anti-gravity technology (however unlikely) would obsolete mechanical elevation entirely

- Teleportation (even less likely) would eliminate physical movement altogether

- Carbon nanotube cables could enable space elevators, making Otis's expertise in vertical transportation literally universal

More realistically, incremental innovations will compound: - Predictive AI eliminates wait times by anticipating movement patterns - Biometric integration customizes every journey to individual preferences - Energy generation turns elevators into power plants, generating more electricity than they consume - Autonomous maintenance with robots servicing elevators without human intervention

Climate and Sustainability Imperatives

The next 50 years will be defined by climate adaptation. Buildings must achieve net-zero emissions. Cities must reduce energy consumption while growing denser. Vertical transportation sits at the intersection of both challenges.

Otis's regenerative drives, already reducing energy consumption by 75%, could evolve to make elevators net energy positive. Kinetic energy from millions of daily journeys could power entire buildings. The company's role shifts from energy consumer to energy infrastructure.

Green building certifications could mandate elevator efficiency standards, creating forced modernization cycles. Just as cars face emissions standards, elevators might face efficiency requirements. This regulatory pressure would accelerate modernization, benefiting Otis's high-margin service business.

Will Otis Remain Independent?

The spinoff from UTC proved that focus creates value. But industrial logic might argue for reconsolidation. Potential scenarios include:

- Private equity acquisition, focusing on cash extraction from the service base

- Strategic merger with KONE or Schindler, creating global dominance

- Technology company acquisition, with Google or Amazon seeking physical infrastructure for smart cities

- Chinese acquisition, though regulatory barriers seem insurmountable

- Remaining independent, the most likely scenario given successful execution

The company's strategic value extends beyond financial metrics. Control over vertical transportation in major cities worldwide represents critical infrastructure. Governments might block foreign acquisitions on national security grounds. The service network, with technicians accessing every major building, has intelligence value that transcends commercial considerations.

Final Reflections on the Spinoff Playbook

Otis's journey from conglomerate division to independent company offers lessons for industrial companies contemplating separation:

- Timing matters less than execution - Spinning off during COVID seemed disastrous but forced rapid adaptation

- Service businesses deserve freedom - Predictable cash flows shouldn't subsidize volatile businesses

- Culture change takes years - Moving from cost center to independent company requires fundamental mindset shifts

- Focus enables innovation - Independent Otis invested in IoT and digital services UTC never would have funded

- Market recognition takes time - Three years post-spinoff, investors still discovering Otis's quality

The broader lesson: industrial conglomerates often destroy value by combining unrelated businesses. The supposed synergies rarely materialize. The complexity tax is real. The market values focus, transparency, and aligned incentives.

For investors, spinoffs remain a fertile hunting ground. Forced selling by index funds, initial complexity, and lack of coverage create opportunities. But not all spinoffs succeed. The business quality matters more than the corporate structure.

Otis succeeded because the underlying business is exceptional—recurring revenue, high switching costs, secular growth drivers. The spinoff simply revealed value that already existed. No financial engineering can transform a bad business into a good one.

Looking back from 2075, the Otis spinoff might seem quaint—a $40 billion market cap company worried about quarterly earnings while cities were transforming into vertical ecosystems. Or it might seem prescient—management recognizing that independent focus was essential to navigating the transformation ahead.

Either way, one truth remains: humans will continue reaching skyward. Whether through cables and motors, magnetic fields, or technologies not yet imagined, we'll keep building higher. And someone needs to move us up and down safely, efficiently, reliably.

That's been Otis's job for 171 years. It likely will be for centuries more. The technology will change. The physics might change. But the human ambition to rise—literally and figuratively—remains constant. As long as we keep building up, Otis keeps moving us. All safe, ladies and gentlemen, all safe.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube