Oshkosh Corporation: America's Purpose-Built Vehicle Empire

Introduction: The Unlikely Titan of Specialty Vehicles

In the fall of 2015, somewhere in the rugged testing grounds of the U.S. Army's Aberdeen Proving Ground, a light tactical vehicle made an impressive run—one that would reshape American military mobility for a generation. The vehicle, developed by a century-old Wisconsin company most Americans had never heard of, had just outperformed proposals from Lockheed Martin and AM General in one of the Pentagon's most competitive procurement battles in years. When the dust settled, Oshkosh Corporation walked away with a $6.7 billion contract to build the Humvee's replacement.

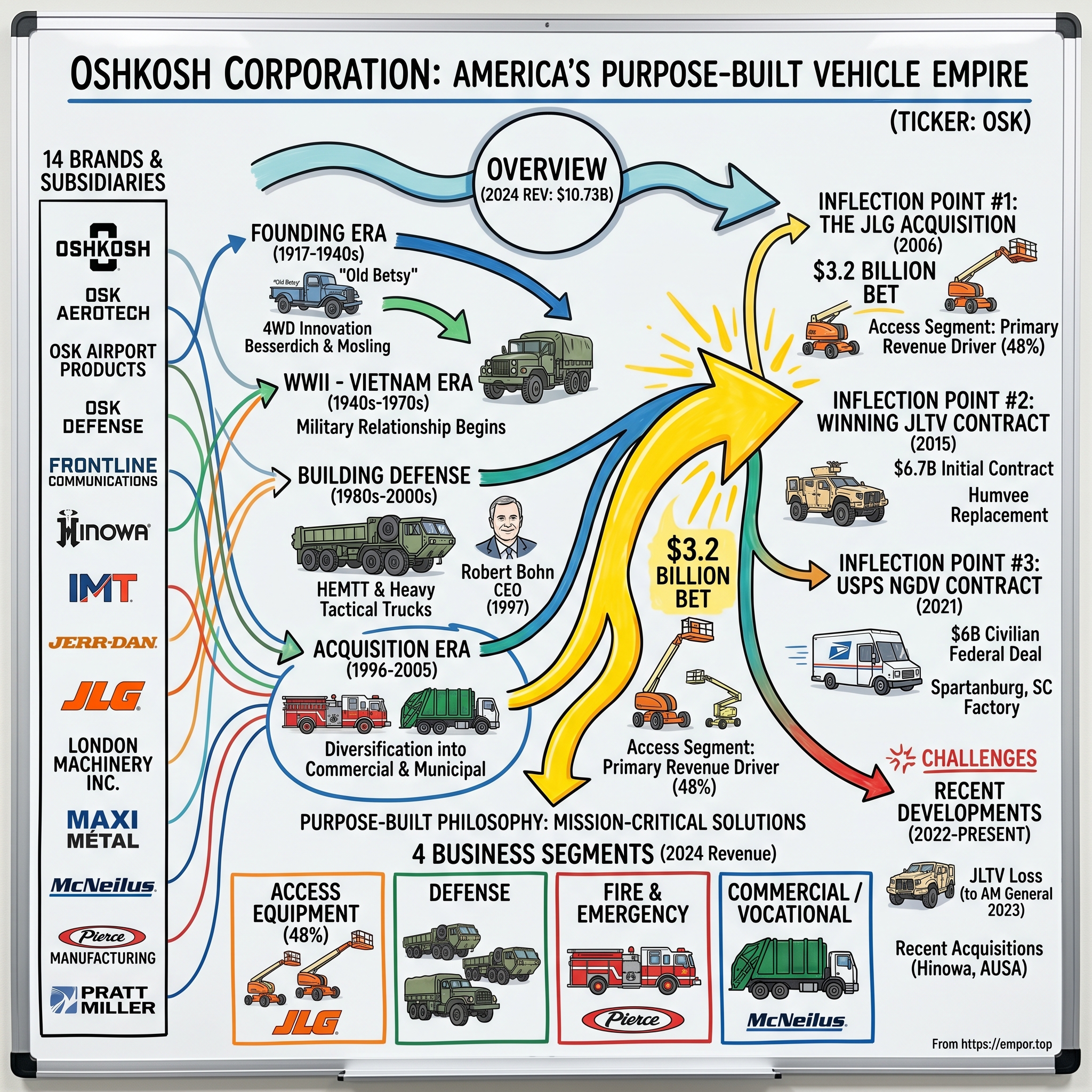

In 2024, Oshkosh achieved a $10.73 billion revenue—a staggering figure for a company that traces its roots to a small workshop in the frozen Wisconsin heartland. Today, the company is organized in four primary business groups: access equipment, defense, fire and emergency, and commercial. But how did a regional truck maker founded during World War I become the company that builds the Humvee replacement, virtually every fire truck you see on America's streets, the equipment that constructs the nation's skyscrapers, AND the new mail trucks about to populate every neighborhood in America?

The answer lies in a remarkable strategic playbook executed over decades: vertical integration through acquisition, masterful navigation of government contract cycles, and an unwavering commitment to what the company calls the "purpose-built" philosophy—designing vehicles for specific missions rather than adapting general platforms.

Oshkosh Corp. manufactures, distributes, and services products under fourteen brands: Oshkosh, Oshkosh AeroTech, Oshkosh Airport Products, Oshkosh Defense, Frontline Communications, Hinowa, IMT, Jerr-Dan, JLG, London Machinery Inc., Maxi Métal, McNeilus, Pierce Manufacturing, and Pratt Miller. Each represents a deliberate expansion into a niche where Oshkosh could dominate—or at least achieve number-two market position—while leveraging shared purchasing power and engineering expertise across its portfolio.

The primary driver behind last 12 months revenue was the Access segment contributing a total revenue of US$5.16b (48% of total revenue). What was once a defense-dependent truck maker has transformed into a diversified industrial company, though the story of that transformation reads like a business school case study in strategic reinvention—complete with billion-dollar bets, Congressional drama, and the high-stakes world of federal procurement.

Founding Era: The Four-Wheel Drive Innovation (1917–1940s)

The genesis of Oshkosh Corporation lies in a seemingly simple innovation that, in the harsh Wisconsin winters of the early twentieth century, meant the difference between mobility and being stranded in snowdrifts.

Oshkosh Truck was founded by William R. Besserdich and Bernhard A. Mosling in 1917. The two men were an unlikely pairing—Besserdich was the quintessential engineer-inventor, while Mosling possessed the commercial instincts to transform innovation into enterprise. Besserdich and Mosling approached several established automobile manufacturers—including Ford, Packard, and Studebaker—about using their designs to produce a four-wheel-drive vehicle. After a series of rejections, they decided to start their own company.

Handling the business end of the operation, Mosling sold stock in the new company, raising $250,000 in capital. Meanwhile, master engineer Besserdich was busy coming up with a prototype vehicle design. The entrepreneurial division of labor proved effective: Besserdich focused on what would become the company's defining technological edge, while Mosling navigated the complex task of financing and business development.

In May of 1917, the Wisconsin Duplex Auto Company, located in Clintonville, Wisconsin, was incorporated. Besserdich was the company's president, and Mosling was listed as its manager and secretary. The prototype vehicle was a four-cylinder, three-speed, 3,000-pound truck called Old Betsy.

Old Betsy wasn't just a prototype—it became a founding artifact, a physical embodiment of the company's origin story that persists to this day. This first four-wheel-drive truck, known today as "Old Betsy", is still owned by Oshkosh Corporation and housed in the new Global Headquarters building in Oshkosh. The vehicle still runs and is used frequently in demonstrations and parades.

The success of Old Betsy's four-wheel-drive components attracted investors. Since many of the investors were based in Oshkosh, 47 miles south of Clintonville, the company relocated there toward the end of 1917. In 1917, the Chamber of Commerce in Oshkosh offered to help them, if they moved and formed a new company in Oshkosh. The relocation represented an early example of the kind of pragmatic decision-making that would characterize the company's century-long history—following capital and opportunity rather than geographical sentiment.

The company name was changed to the Oshkosh Motor Truck Company on August 28, 1918, and it's been located there ever since. Immediately upon moving to Oshkosh, the company began the design and construction of its first production truck, what became the 2-ton Model A four-wheel drive.

The post-war period posed immediate challenges. Sales were slow initially and that was attributable both to a postwar slump and to the U.S. Government dumping thousands of World War I surplus trucks on the market. That act put the kibosh on a lot of truck sales through a big portion of the 1920s. But the company's founders understood something crucial about their market position: their four-wheel-drive capability gave them an edge in severe conditions that no surplus military truck could match.

In 1925 Oshkosh introduced the Model H, a powerful truck with a six-cylinder engine. The Model H proved to be useful for road construction and snow plowing, and therefore sold well to municipalities. Sales of the Model H kept Oshkosh in business through the second half of the 1920s.

The Model H's success with municipal buyers established a pattern that would recur throughout Oshkosh's history: finding institutional customers—governments, municipalities, large enterprises—who valued capability over price and who offered predictable, repeatable business. This wasn't a company chasing consumer fads; it was a company building mission-critical equipment for buyers who couldn't afford failure.

The company fell victim to the Great Depression, however, and in 1930 was forced to reorganize. It re-emerged as Oshkosh Motor Truck Company. R. W. Mackie was president of the company's new incarnation, while Mosling concentrated on improving the company's sales.

Even during the darkest economic period in American history, Oshkosh found a lifeline in product innovation. The Model TR, introduced in 1933, was a diversification for the company and was the first rubber tired earthmover ever built. This wasn't just incremental improvement—it was the kind of pioneering product development that expanded the company's addressable market into construction equipment.

The lessons from this founding era would echo through the next century: technical differentiation matters in severe-duty applications; institutional buyers provide stability; diversification protects against cyclicality; and Wisconsin's brutal winters were actually a competitive advantage for a company building vehicles engineered to operate where others couldn't.

The Military Relationship Begins: WWII to Vietnam Era (1940s–1970s)

The eve of World War II marked a pivotal transformation for Oshkosh Truck—one that would fundamentally reshape the company's identity and destiny. What had been a regional specialty truck manufacturer was about to become a contractor to the most powerful military in history.

The first ARFF built by Oshkosh was a W Series truck delivered to the U.S. Coast Guard in 1953. This aircraft rescue and firefighting vehicle represented Oshkosh's entry into a specialized niche that would become one of its enduring strengths: vehicles designed for the extreme demands of aviation safety.

Oshkosh has also produced aircraft tow tractors, and in 1968 the company designed and built the U-30, 45 of which were built for the U.S. Air Force to tow the Lockheed C-5 Galaxy transport aircraft. The C-5 Galaxy was, at the time, the largest aircraft ever to enter service with the U.S. military—and Oshkosh built the tractors powerful enough to move these behemoths around Air Force bases.

The 1970s brought a watershed moment that would define Oshkosh's defense business for decades to come. In 1976 the company won a U.S. Army contract to supply 744 M911 heavy equipment transporters, the first in a long line of U.S. Army contracts that now sees Oshkosh Defense as the sole supplier of medium and heavy tactical trucks to the U.S. Army and Marines.

This contract wasn't just significant for its size—it established the institutional relationships and proven track record that would give Oshkosh a substantial advantage in future competitions. In the world of defense contracting, incumbency matters enormously. Each successfully executed contract builds trust, demonstrates capability, and creates organizational knowledge that is extremely difficult for competitors to replicate.

The military relationship also accelerated Oshkosh's engineering capabilities. Building for the Department of Defense meant meeting some of the most demanding specifications in the world—specifications that required vehicles to operate in desert heat, Arctic cold, mountain terrain, and combat conditions. This engineering discipline would prove invaluable across all of Oshkosh's businesses.

By the end of this era, Oshkosh had established itself as something more than a Wisconsin truck maker. It had become a trusted partner to the U.S. military—a position that would prove invaluable when the Pentagon's largest ground vehicle programs came up for competition in subsequent decades.

Building the Defense Business: HEMTT & Heavy Tactical Trucks (1980s–2000s)

The early 1980s brought Oshkosh its defining defense program—one that would cement the company's position as the U.S. Army's premier supplier of heavy tactical trucks for over four decades.

The M977 HEMTT entered service in 1982 with the United States Army as a replacement for the M520 Goer, and has remained in production for the U.S. Army and other nations. The Heavy Expanded Mobility Tactical Truck—known in Army parlance as the HEMTT—would become one of the most successful military vehicle programs in American history.

The Heavy Expanded Mobility Tactical Truck (HEMTT) is an eight-wheel drive, diesel-powered, 10-short-ton tactical truck. But that clinical description understates the vehicle's importance. The HEMTT became the logistical backbone that supported every major American military operation from the Cold War through the Global War on Terror.

Oshkosh was the cheaper bid and was thus awarded a 5-year contract for the development of the HEMTT. The Firm-Fixed-Price contract had a value of 251 million USD and included the delivery of several prototypes and 2,140 serial production vehicles with an option for an additional 5,350 vehicles. Oshkosh Truck Corporation, out of Oshkosh, Wisconsin, had participated in this tender with its new 8×8 truck design, which boasted an "extreme" level of offroad mobility while also incorporating a high number of off-the-shelf parts, reducing expected maintenance costs.

By Q2 2021, around 35,800 HEMTTs in various configurations had been produced by Oshkosh Defense through new-build contracts and around 14,000 of them had been re-manufactured. The remanufacturing business represented an important secondary revenue stream—a way to extend the program's value well beyond initial production.

The HEMTT is the U.S. Army's standard 10-ton truck. In evolving configurations it has been in continuous production since 1982. Four decades of continuous production is extraordinary in any industry—and in defense contracting, it represents a dominant market position that competitors found nearly impossible to dislodge.

But Oshkosh's leadership understood that defense dependency carried significant risks. Post-Cold War budget cuts in the early 1990s hit defense contractors hard, and Oshkosh was no exception. The company's forward-looking executives recognized that diversification wasn't just a growth strategy—it was existential risk management.

Under Bohn's leadership, Oshkosh Corporation has been transformed from a $400 million Midwest Company into a multi-billion dollar international corporation and a Fortune 350 Company. Robert Bohn, who would become one of the most consequential leaders in Oshkosh's history, joined the company during this pivotal period.

Mr. Bohn joined our company in 1992 as Vice President-Operations. He was appointed President and Chief Operating Officer in 1994. He was appointed our President and Chief Executive Officer in 1997, and Chairman of the Board of Directors in 2000. Mr. Bohn's title was changed to Chairman and Chief Executive Officer in 2007. Prior to joining our company, Mr. Bohn held various executive positions with Johnson Controls, Inc. from 1984 until 1992.

Upon joining the Company in 1992, Bohn introduced multiple-product manufacturing on a single production line to Oshkosh long before mainstream industry embraced it. He led Oshkosh Corporation to significantly expand its product portfolio and build leading positions in multiple markets.

The Bohn era would prove transformative. His background at Johnson Controls—a company known for operational excellence and diversified industrial operations—informed an acquisition-driven strategy that would reshape Oshkosh over the following decades.

The Acquisition Era: Pierce, McNeilus & Building the Portfolio (1996–2005)

The mid-1990s marked the beginning of Oshkosh's transformation from a defense-focused truck maker into a diversified specialty vehicle conglomerate. The acquisitions made during this period weren't random portfolio additions—they were calculated moves to enter adjacent markets with dominant niche positions.

In 1996, Pierce was wholly acquired by Oshkosh Corporation. In 1996, Oshkosh Truck Corporation acquired Pierce for $158 million, integrating it into a broader portfolio of specialty vehicles.

Pierce Manufacturing represented far more than just another acquisition. Pierce Manufacturing is a U.S. subsidiary of Oshkosh Corporation, based in Appleton, Wisconsin, that manufactures customized fire and rescue apparatus. Pierce was founded in 1913 by Humphrey Pierce and his son Dudley as the Pierce Auto Body Works Inc., which concentrated on building custom truck bodies for the Ford Model T.

The strategic logic was compelling: fire apparatus represented a stable, recession-resistant market with high barriers to entry. Municipal fire departments don't stop buying trucks during economic downturns—public safety is non-discretionary spending. And the customization requirements created natural advantages for established players with engineering expertise and dealer networks.

Pierce proudly builds American-made fire trucks manufactured by over 3,000 craftsmen, welders, and engineers across 10 principal facilities in Wisconsin, Florida, and Tennessee. Our story is uniquely American. We started in 1913 as a father-and-son shop building truck bodies on Model T Ford chassis in an old, converted church at the corner of Fremont and Jefferson Streets in Appleton, Wisconsin, where we remain headquartered. The firefighters we serve are represented in our workforce, and I have the pleasure of working alongside more than 100 active and former firefighters, as well as other first responders, at Pierce.

The firm was created by Garwin and his brother Dennis McNeilus on July 21, 1970, and later sold to Oshkosh Corporation in 1997. McNeilus Truck and Manufacturing manufactures refuse collection vehicles in Dodge Center, Minnesota, United States, where it is the largest employer.

The McNeilus acquisition brought Oshkosh into the concrete mixer and refuse collection businesses—unglamorous but essential vehicles that operated in predictable cycles tied to construction activity and municipal waste management. Like fire trucks, refuse collection represented steady municipal spending that provided ballast against the volatility of defense contracts.

While Oshkosh, based in Oshkosh, Wis., may not be well known to the rental industry, the company has been on an acquisition mode in recent years. One of the world's largest builders of military trucks, the company has sought other acquisitions to diversify itself. Since 1996, more than half of the company's revenue has come from companies it has acquired.

The acquisition playbook that emerged during this period would become the template for Oshkosh's growth strategy: identify market leaders in adjacent specialty vehicle niches, acquire them, maintain their brand identity and existing management, and achieve purchasing synergies through scale. The acquisition represents the 15th purchase Oshkosh Truck has made over the past decade, and the company is widely considered to be both a savvy buyer and a skillful integrator of new operations.

This multi-brand strategy—letting acquired companies maintain their distinct identities while leveraging corporate resources—proved remarkably effective at retaining customer relationships and institutional knowledge while achieving the cost advantages of scale.

INFLECTION POINT #1: The JLG Acquisition – A Transformative $3.2 Billion Bet (2006)

If the Pierce and McNeilus acquisitions represented tactical diversification, the JLG acquisition was something altogether different—a transformative, bet-the-company move that would fundamentally reshape Oshkosh's identity and market position.

Specialty vehicle manufacturer Oshkosh Truck Corp. last week announced it has signed a definitive agreement to acquire JLG Industries, global leader in aerial work platforms and telehandlers. In a deal that surprised rental industry participants as much as the majority of JLG officials, Oshkosh will acquire all outstanding shares of JLG for $28 per share. The total price, including transaction costs and assumed debt, is $3.2 billion in cash on a fully diluted basis.

This transaction will create a $6 billion global specialty vehicle manufacturer. The scale of the combination was staggering—JLG alone had revenues roughly equivalent to Oshkosh's entire business.

It also meets our major acquisition criteria, which include market leadership, strong management, double digit growth opportunities and the expectation of earnings in excess of our cost of capital. JLG had $2.3 billion in revenues during fiscal 2006 and has estimated a 20 to 25 percent increase in sales in fiscal 2007. It has the top market position in North America and Europe for aerial work platforms and is the top producer of telehandlers in the United States. JLG placed 22nd on FORTUNE magazine's 2006 list of the 100 Fastest-Growing Companies.

JLG was founded in 1969 and operated independently until its acquisition by Oshkosh Corporation in 2006. Founded in 1969, John Landis Grove formed a partnership with two close friends and purchased a small metal fabrication business. The company's founder had built an empire in access equipment—the scissor lifts, boom lifts, and telehandlers that enable workers to reach elevated areas safely across construction sites, warehouses, and industrial facilities.

"We have consistently executed strategies to grow this company, creating significant shareholder value during the last decade," said Oshkosh's chairman, president and CEO Robert Bohn. "The acquisition of JLG is the latest broad-based initiative in the continuing transformation of Oshkosh Truck Corp. It is aligned with our historic acquisition strategy as we expand into complementary markets, and it will be instrumental in building our global focus and scale that are increasingly needed to be successful."

Oshkosh officials said the company was attracted by JLG's 20-year agreement to produce Caterpillar-branded telehandlers. The acquisition also gives the combined companies enhanced buying power, buying more than $4 billion worth of raw materials, parts and supplies per year.

Once the integration is complete, Oshkosh Truck said, JLG Industries' operations will represent the company's biggest segment, generating about 40 percent of the company's total revenue and earnings.

Oshkosh, which plans to finance the purchase with a $3.5 billion line of credit from Bank of America, expects the deal to add "modestly" to per-share earnings in fiscal 2007. JLG, based in McConnellsburg, Pa., had $2.3 billion in revenues this fiscal year, with sales estimated to grow between 20 and 25 percent next year, Oshkosh said. The company is the top provider of aerial platforms in North America and Europe.

Not everyone on Wall Street was immediately convinced. "Predictably, shares of JLG Industries rose, jumping $6.81, or 33 percent, to $27.60, on the New York Stock Exchange. But Oshkosh Truck stock dropped 10 percent early in Monday's session, and even after partially recovering, closed on the Big Board down $3.05, or 5.5 percent, to $52.49. "At first blush, the size and nature of the deal are a bit surprising," Morningstar equity analyst Ben Butwin told investors following the acquisition's announcement."

The skeptics were right to note the risks. The acquisition required Oshkosh to take on substantial debt, and JLG's business was heavily tied to construction cycles—cyclical in ways that Oshkosh's defense business was not. But Bohn and his team were executing a deliberate strategy: using defense revenue stability to underwrite diversification into adjacent markets with strong growth potential.

Oshkosh Truck Corp., a leading manufacturer of specialty vehicles and vehicle bodies, last week announced that it completed the acquisition of JLG Industries for $28 per share in an all-cash transaction valued at approximately $3.2 billion. With the addition of JLG's forecasted revenues, Oshkosh Truck now expects to surpass $6 billion in net sales for fiscal 2007.

The JLG acquisition fundamentally changed Oshkosh's risk profile—and its growth trajectory. The primary driver behind last 12 months revenue was the Access segment contributing a total revenue of US$5.16b (48% of total revenue). What was once a defense contractor with some commercial businesses had become a diversified industrial company where access equipment represented nearly half of revenues.

Access International, a magazine under KHL Group, released the 2024 AccessM20 ranking of the world's top aerial work platform (AWP) manufacturers. The results show that JLG (USA) retains its top position with an annual revenue of USD 3.0445 billion (approximately RMB 22 billion), followed by Terex AWP (Genie) in second place.

INFLECTION POINT #2: Winning the $30 Billion JLTV Contract (2015)

The Joint Light Tactical Vehicle program represented the Pentagon's largest ground vehicle acquisition in a generation—and winning it would validate Oshkosh's position as America's premier tactical vehicle manufacturer.

The idea for the Joint Light Tactical Vehicle (JLTV) first emerged in 2006 from threats experienced during the Iraq War. The primary tactical wheeled vehicle used by the U.S. military at the start of the war was the Humvee. However, most were unarmored and the type (including armored examples) incurred heavy losses when improvised explosive devices (IEDs) began being employed by insurgents. The initial response was to add armor, or more armor to armored models, and primarily on the sides. This improved side protection against direct fire and associated threats, but since the chassis was not designed to handle any further additional weight, there was little room for underbody protection.

The vulnerability of up-armored Humvees to IEDs had become one of the defining tragedies of the Iraq War. American troops were dying in vehicles never designed to protect against sophisticated explosive attacks. The military's response included rapid procurement of Mine Resistant Ambush Protected (MRAP) vehicles—including Oshkosh's own M-ATV—but these were heavy, less maneuverable stop-gap solutions.

The US Army, in its largest contract award in years, selected Oshkosh to build its Humvee replacement, the Joint Light Tactical Vehicle (JLTV). Oshkosh beat out Humvee-maker AM General and defense titan Lockheed Martin to walk away with a $6.7 billion contract in low rate initial production, for a program estimated to be worth $30 billion through 2024.

Three years of low-rate initial production and five years of full-rate production are set to produce a total of 49,100 for the Army and 5,500 for the Marine Corps. In the JLTV, the Army is seeking a replacement for the Humvee that is as mobile, but with the same protection as a mine resistant ambush protected vehicle (MRAP).

"Our JLTV has been extensively tested and is proven to provide the ballistic protection of a light tank, the underbody protection of an MRAP-class vehicle, and the off-road mobility of a Baja racer. The Oshkosh JLTV allows troops to travel over rugged terrain at speeds 70% faster than today's gold standard, which is our Oshkosh M-ATV."

The victory wasn't immediate or uncontested. Lockheed Martin protested the award in the Court of Federal Claims, but withdrew it February 2016, potentially as a result of the release of JLTV testing data showing that the L-ATV lasted nearly six times longer between significant breakdown than Lockheed's vehicle.

The U.S. Government Accountability Office (GAO) dismissed Lockheed Martin's protest earlier today based on Lockheed's notice that it intends to file a protest in the U.S. Court of Federal Claims. Shortly thereafter, the U.S. Army lifted the stop work order and instructed Oshkosh to resume performance of the JLTV contract.

To date, Oshkosh has produced 19,000 JLTVs, company Vice President and General Manager of Joint Programs George Mansfield said in a statement. The scale of production was enormous—representing one of the most successful defense vehicle programs in modern American history.

The JLTV contract represented more than just revenue. It validated Oshkosh's engineering capabilities, its manufacturing prowess, and its ability to compete against much larger defense contractors. In a competition that included Lockheed Martin—one of the world's largest defense companies—Oshkosh's purpose-built approach and tactical vehicle expertise won the day.

INFLECTION POINT #3: The USPS Next Generation Delivery Vehicle Contract (2021)

In February 2021, while America was still grappling with the COVID-19 pandemic, Oshkosh received news that would open an entirely new chapter in its history—and potentially transform the company's relationship with the federal government beyond defense.

The contract, which is valued at $6 billion, was awarded to Oshkosh Defense of the Oshkosh Corporation in February 2021. Up to 160,000 vehicles will be built in a new South Carolina factory.

Under the contract's initial $482 million investment, Oshkosh Defense will finalize the production design of the Next Generation Delivery Vehicle (NGDV) — a purpose-built, right-hand-drive vehicle for mail and package delivery — and will assemble 50,000 to 165,000 of them over 10 years.

The USPS contract represented something unprecedented for Oshkosh: a massive civilian federal contract outside the defense sector. The U.S. Postal Service fleet includes some of the most recognizable vehicles in America—the iconic white and blue mail trucks that visit virtually every address in the country. Replacing them was an enormous undertaking.

The vehicles will be equipped with either fuel-efficient internal combustion engines or battery electric powertrains and can be retrofitted to keep pace with advances in electric vehicle technologies. The initial investment includes plant tooling and build-out for the U.S. manufacturing facility where final vehicle assembly will occur.

In June 2021, Oshkosh stated that after a long search, the company will assemble the new mail truck at a new, dedicated factory in Spartanburg, South Carolina, and will employ more than 1,000 local non-union workers. Oshkosh expects to spend $155 million to retool the facility.

The award wasn't without controversy. The Workhorse Group, an electric truck builder based in Loveland, Ohio and one of the losing bidders, initially protested the award to Oshkosh by filing a lawsuit, but dropped the case in September 2021, one day before the case would be heard in court.

Environmental groups criticized the initial plan for including a high proportion of internal combustion vehicles rather than electric options. But the USPS ultimately increased its electrification commitments. After the USPS was sued by multiple groups in April 2022 to block the procurement, the USPS announced plans in July to increase the proportion of electric NGDVs in the initial procurement to 50% and add 34,500 more commercially available battery-electric vehicles. Later that December, the USPS announced the addition of $3 billion from the Inflation Reduction Act would allow the procurement of 45,000 battery-electric NGDVs out of at least 60,000 NGDVs in total.

In August 2024, the first vehicles were delivered and began operating delivery routes in Augusta, Georgia. Early feedback from mail carriers has been overwhelmingly positive—particularly appreciation for features like air conditioning, which the aging Grumman Long Life Vehicles lacked.

Among USPS drivers, the single most appreciated feature of the NGDVs was one LLVs never offered: air conditioning. Oshkosh execs related the story of a USPS test driver who burst into tears after the drive because the new vehicle was so much more comfortable and usable than the LLV they drove every day.

The NGDV contract's strategic significance extends beyond its immediate value. It represents Oshkosh's expansion into civilian federal markets—diversifying its government business away from pure defense dependence. As postal carriers across America begin using these vehicles, Oshkosh's presence in everyday American life will become more visible than ever before.

Recent Developments & Challenges (2022–Present)

The past several years have brought Oshkosh both triumphs and setbacks—a reminder that even dominant market positions require constant defense in the competitive landscape of government contracting.

The most significant blow came in the JLTV program. In February 2023, the Army selected the AM General bid. Oshkosh submitted a protest of the award, which GAO denied. Oshkosh expects to produce JLTVs into early 2025.

Spurning the incumbent provider, on 9 February 2023 the US Army awarded AM General a five-year contract (plus five-year option) worth USD 8.66 Bn to produce up to 20,682 Joint Light Tactical Vehicles (JLTVs) and up to 9,883 JLTV Trailers for the US armed forces and Foreign Military Sales customers.

"We were disappointed to learn that we did not win the JLTV follow on contract," said Oshkosh Corp. CEO John Pfeifer. "The contract was won at a pricing level that would be unacceptable to Oshkosh." He said the JLTV contract could affect the company's 2025 financial targets, as it expected to retain it when setting its goals last year. "That was kind of a negative hit to our 2025 targets," Pfeifer said.

The loss stung particularly because Oshkosh had been the original developer and manufacturer of the JLTV. Oshkosh Defense has built more than 20,000 JLTVs since being awarded the initial contract in 2015. But the Army's decision to recompete the contract—with the goal of reducing costs—opened the door for AM General's successful bid.

Adding further complexity to the defense outlook, on April 30, 2025, US Secretary of Defense Pete Hegseth ordered the Secretary of the Army to "end procurement of obsolete systems, and cancel or scale back ineffective or redundant programs, including manned aircraft, excess ground vehicles (e.g., HMMWV), and outdated UAVs". The Army said it would stop procuring Humvees and JLTVs.

Oshkosh expects to produce JLTVs into early 2025 and retains the right to produce JLTVs for direct commercial sale. Foreign military sales provide some ongoing opportunity, but the domestic JLTV program represents a significant revenue headwind.

On the positive side, Oshkosh has continued its acquisition strategy in the Access segment. Following the acquisition of Hinowa in 2023, the AUSA acquisition further supports the Oshkosh accelerated growth strategy and strengthens the JLG® equipment portfolio. Established in 1956, AUSA specializes in designing, manufacturing and selling wheeled dumpers, rough terrain forklifts and compact telehandlers.

Oshkosh has completed the acquisition of AUSACorp S.L. (AUSA), adding the brand's compact all-terrain machines for transportation and material handling to the company's Access segment. The acquisition includes AUSA's 250,000-square-foot manufacturing facility in Barcelona, Spain, approximately 350 team members and access to 200 equipment dealers worldwide.

The Vocational segment showed impressive growth with a 19.8% revenue increase, while Access segment remained flat and Defense segment maintained steady performance. Full-year 2024 results included net sales of $10.76 billion and net income of $681.4 million ($10.35 per share).

Business Model Deep Dive: The "Purpose-Built" Philosophy

At the heart of Oshkosh's strategy lies a deceptively simple concept: purpose-built vehicles designed for specific missions rather than adapted general platforms. This philosophy runs through every segment of the company and explains much of its competitive positioning.

The corporation operates approximately 125 facilities worldwide across 19 countries on five continents, employing around 18,000 team members. While the majority of manufacturing occurs in the United States—at sites including Oshkosh, Wisconsin; McHenry, Illinois; and Spartanburg, South Carolina—international production capabilities include plants in Belgium, Brazil, France, Mexico, and the United Kingdom.

The multi-brand strategy allows Oshkosh to maintain distinct market positions while achieving scale benefits. Oshkosh Corp. manufactures, distributes, and services products under fourteen brands: Oshkosh, Oshkosh AeroTech, Oshkosh Airport Products, Oshkosh Defense, Frontline Communications, Hinowa, IMT, Jerr-Dan, JLG, London Machinery Inc., Maxi Métal, McNeilus, Pierce Manufacturing, and Pratt Miller.

Each brand serves a specific market with deep expertise. Pierce builds fire trucks; McNeilus builds refuse collection vehicles; JLG builds aerial work platforms; Oshkosh Defense builds military tactical vehicles. A fire chief buying a Pierce pumper is buying from a company with over a century of fire apparatus expertise—not from a corporate conglomerate.

Yet behind the scenes, these brands share engineering resources, supply chain relationships, and manufacturing best practices. The acquisition also gives the combined companies enhanced buying power, buying more than $4 billion worth of raw materials, parts and supplies per year.

The purpose-built philosophy extends to product design itself. An Oshkosh military truck isn't a commercial truck with armor bolted on—it's designed from the ground up for the specific demands of military operations. A JLG boom lift isn't a general-purpose construction vehicle—it's engineered specifically for workers who need to reach elevated areas safely. This specialization creates products that excel in their specific applications but would be poorly suited for general-purpose use.

This focus on specialization creates natural barriers to entry. Building effective specialty vehicles requires deep knowledge of customer workflows, regulatory requirements, and application-specific engineering challenges. A general equipment manufacturer entering the fire truck market, for example, would need years to develop the institutional knowledge that Pierce has accumulated over more than a century.

Porter's Five Forces & Competitive Analysis

Threat of New Entrants: LOW

The specialty vehicle market presents formidable barriers to new competitors. Capital requirements for specialized manufacturing facilities are substantial—Oshkosh's investment in the Spartanburg NGDV facility alone ran to $155 million. Defense contracts require security clearances, established relationships with procurement offices, and proven track records that new entrants cannot quickly establish.

Regulatory hurdles compound these barriers. FAA certification requirements for airport equipment, federal specifications for fire apparatus, and military vehicle procurement regulations all favor established players with compliance infrastructure already in place.

Bargaining Power of Suppliers: MODERATE

The combined companies have enhanced buying power, buying more than $4 billion worth of raw materials, parts and supplies per year. Oshkosh's scale provides significant negotiating leverage with suppliers. However, specialized components—engines, transmissions, and proprietary systems—come from a limited supplier base, constraining Oshkosh's power in certain categories.

Bargaining Power of Buyers: VARIES BY SEGMENT

In the Defense segment, the U.S. government is effectively a monopsony buyer with enormous leverage—as demonstrated when the Army recompeted the JLTV contract and selected a lower-cost bidder. Government contracts operate under procurement rules that prioritize cost efficiency and competitive bidding.

In Fire & Emergency, fragmented municipal buyers have less concentrated purchasing power, and safety considerations often outweigh price sensitivity. In Access Equipment, large rental companies like United Rentals and Sunbelt Rentals represent concentrated buying power and can influence equipment specifications and pricing.

Threat of Substitutes: LOW

For most Oshkosh products, substitutes are limited. There is no substitute for a fire truck that meets NFPA standards; there is no substitute for a military tactical vehicle that meets Department of Defense specifications. In Access Equipment, alternatives like scaffolding and ladders exist but are inferior for most applications where aerial work platforms are used.

Industry Rivalry: MODERATE TO HIGH

JLG (USA) retains its top position with an annual revenue of USD 3.0445 billion, followed by Terex AWP (Genie) in second place. Five Chinese manufacturers—XCMG, Dingli, Zoomlion, Sinoboom, and LGMG—ranked in the global top ten, underscoring their growing international competitiveness.

In Access Equipment, JLG faces strong competition from Genie (owned by Terex) and an increasingly competitive group of Chinese manufacturers. In defense, the JLTV recompete demonstrated that even incumbent positions can be challenged when the government opens contracts to competition.

Hamilton's Seven Powers Analysis

Scale Economies: Oshkosh benefits from significant scale advantages, particularly in purchasing and manufacturing. The combination of fourteen brands creates procurement leverage that smaller competitors cannot match.

Network Effects: Limited direct network effects, though dealer networks and service infrastructure create some advantages in aftermarket support.

Counter-Positioning: Oshkosh's purpose-built philosophy may represent counter-positioning against general equipment manufacturers who cannot easily replicate specialized expertise without cannibalizing their existing business models.

Switching Costs: Moderate. Once customers invest in Oshkosh equipment—particularly fleet purchases with training, spare parts inventory, and service relationships—switching costs create retention advantages.

Branding: Strong within specific verticals. Pierce is a premium brand in fire apparatus; JLG is synonymous with aerial work platforms; Oshkosh Defense carries credibility in military procurement. However, brand power varies by customer segment.

Cornered Resource: Oshkosh's century of engineering knowledge, proven track records with government customers, and established dealer networks represent resources that competitors cannot easily replicate.

Process Power: Manufacturing excellence and operational efficiency create some process advantages, though these are not unique to Oshkosh among industrial companies.

Investment Considerations: What Investors Should Watch

Key Performance Indicators

For long-term fundamental investors, three KPIs merit close attention:

1. Defense Segment Backlog and Contract Pipeline The loss of the JLTV follow-on contract and the subsequent Army decision to end JLTV procurement creates meaningful headwinds for the Defense segment. Investors should track: - Remaining JLTV production under existing contracts - FHTV and FMTV contract extensions and renewals - Foreign military sales momentum - New program wins in the Common Tactical Truck or other competitions

2. Access Equipment Utilization and Order Rates JLG's business is cyclical, tied to construction activity and equipment rental fleet decisions. The Access segment's health signals broader industrial economy conditions and provides early warning of construction cycle turns.

3. NGDV Production Ramp Progress The USPS was scheduled to start receiving the vehicles October 2023, but repeated delays meant that only 2500 vehicles had been delivered by November 2025. The production ramp represents a significant execution challenge. Full-rate production achievement will validate Oshkosh's ability to execute large-scale civilian manufacturing programs.

Bull Case

- Diversified Revenue Base: With Access Equipment at 48% of revenue and Vocational growing rapidly, Oshkosh is less defense-dependent than its historical reputation suggests

- NGDV Upside: Successful production ramp creates a template for additional civilian federal contracts

- JLG Market Leadership: JLG retains its top position in aerial work platforms globally

- Municipal Spending Resilience: Fire apparatus and refuse collection vehicles represent non-discretionary municipal spending

- Infrastructure Tailwinds: Infrastructure investment and data center construction support Access Equipment demand

Bear Case

- Defense Headwinds: JLTV program termination and Army transformation initiative create near-term revenue pressure

- Cyclical Exposure: Access Equipment business tied to construction cycles; softening demand noted in recent guidance

- NGDV Execution Risk: Production delays have pushed timelines; sustained ramp challenges could impact profitability

- Government Contract Risk: Federal contracts remain subject to political decisions, as demonstrated by JLTV recompete loss

- Chinese Competition: Five Chinese manufacturers ranked in the global top ten for aerial work platforms

Myth vs. Reality

Myth: Oshkosh is primarily a defense contractor. Reality: The Access segment contributed 48% of total revenue, making JLG the largest business. Defense represents important but not dominant revenue.

Myth: Losing the JLTV recompete was catastrophic. Reality: While significant, "We're a growing organization," said CEO Pfeifer. A spokesperson said the company can deliver JLTVs through September 2025 under the current contract. Oshkosh has other defense programs and is diversifying its federal business.

Myth: The NGDV contract guarantees decades of postal vehicle revenue. Reality: The competitively awarded indefinite delivery, indefinite quantity (IDIQ) contract allows for the delivery of between 50,000 and 165,000 vehicles over a period of 10 years. Actual orders depend on USPS funding and timing decisions.

Conclusion: A Century of Purpose-Built Excellence

From Old Betsy in 1917 to the Next Generation Delivery Vehicle in 2024, Oshkosh Corporation has built its success on a remarkably consistent formula: identify mission-critical applications where vehicle performance is paramount, develop purpose-built solutions that excel in those specific applications, and build institutional relationships that create durable competitive advantages.

The company achieved a $10.73 billion revenue in 2024—a remarkable transformation from the $400 million Midwest company that Robert Bohn took over in 1997. The acquisition-driven growth strategy has created a diversified industrial company with leading positions across access equipment, fire apparatus, refuse collection, and defense vehicles.

Yet challenges remain. The Defense segment faces headwinds from the JLTV program termination and Army transformation initiatives. Access Equipment operates in cyclical markets where demand can shift quickly. The NGDV production ramp represents a significant execution challenge that will test Oshkosh's ability to manufacture at scale for civilian federal customers.

What hasn't changed is the fundamental value proposition that has sustained this company for over a century: when the mission matters, purpose-built beats general-purpose. Whether it's soldiers needing protection from IEDs, firefighters rushing to emergencies, mail carriers delivering to every address in America, or construction workers reaching elevated areas safely—Oshkosh builds the vehicles that enable these everyday heroes to do their jobs.

The next century will bring new challenges: electrification, autonomous vehicles, changing defense priorities, and emerging competitors. But the company that built Old Betsy when four-wheel drive was revolutionary has demonstrated remarkable adaptability across multiple technological transitions. That institutional capability—the ability to engineer for specific missions, manufacture at scale, and navigate complex government relationships—remains Oshkosh's most durable competitive advantage.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube