Omega Healthcare Investors: The Landlord of America's Aging Future

I. Introduction & Episode Roadmap

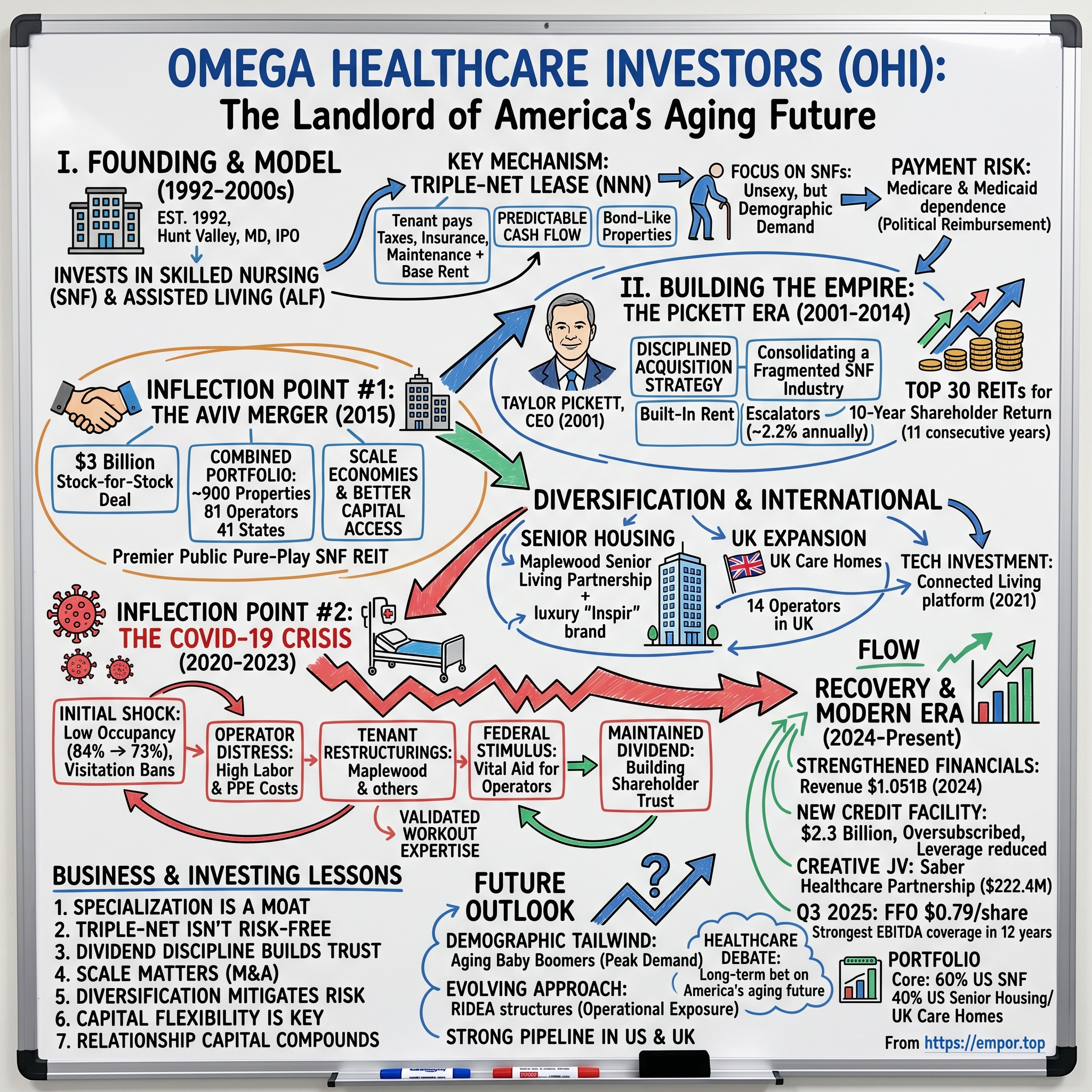

Picture this: A family stands in the lobby of a skilled nursing facility in suburban Ohio, watching their grandmother being wheeled toward rehabilitation therapy after a hip replacement. The walls are freshly painted, the staff moves with quiet efficiency, and the equipment looks modern. What that family almost certainly doesn't know—what almost no one pausing in such hallways ever considers—is that the building they're standing in is owned not by the healthcare company whose logo graces the entrance, but by a publicly traded real estate investment trust headquartered 400 miles away in Hunt Valley, Maryland.

Omega Healthcare Investors, Inc. is a Real Estate Investment Trust ("REIT") that provides financing and capital to the long-term healthcare industry, with a particular focus on skilled nursing facility and assisted living facility operators across the United States and the United Kingdom. As of September 30, 2025, Omega has a portfolio of investments that includes 1,024 operating facilities located in 42 states, the District of Columbia and the United Kingdom/Jersey (290 facilities) and operated by 88 different operators.

This is one of the most unusual landlords in America—and quite possibly one of the most consequential for the coming decades. Omega doesn't run nursing homes. It doesn't employ nurses or physical therapists. It doesn't decide which medications get administered or which residents get the corner room with the view. Instead, Omega does something deceptively simple: it owns the buildings and collects rent. But in that simplicity lies a business model that has weathered multiple existential crises, generated enormous shareholder returns, and positioned itself squarely at the intersection of two powerful forces—America's aging population and the peculiar economics of healthcare real estate.

The central question we'll explore: How did a niche healthcare REIT become the dominant landlord in America's skilled nursing industry—and survive multiple existential crises along the way?

The themes that emerge from this story are universal to any investor studying capital-intensive industries: demographic destiny (can you actually invest in megatrends?), the triple-net lease model (who really bears the risk?), regulatory dependency (what happens when your tenant's revenue depends on government decisions?), and navigating operator crises (when your tenant can't pay rent, whose problem is it really?).

II. Origins & The Healthcare REIT Landscape (1992–2000s)

To understand Omega, you first have to understand what makes healthcare real estate fundamentally different from owning an office building or a shopping mall. The company was founded on March 31, 1992 and is headquartered in Hunt Valley, MD. Omega was formed as a self-administered real estate investment trust (REIT). The company went public through an Initial Public Offering (IPO) in 1992, raising capital to begin acquiring healthcare facilities.

The early 1990s were a peculiar moment for healthcare real estate. Medicare and Medicaid spending had been expanding dramatically, creating what appeared to be a reliable revenue stream for skilled nursing facilities. But operating these facilities was capital-intensive, and many regional operators lacked the balance sheet strength to own their real estate outright. Enter the healthcare REIT model: companies that would buy the buildings and lease them back to operators under long-term arrangements.

Established in 1992, Omega Healthcare Investors Inc is a real estate investment trust that mainly invests in skilled nursing and assisted living facilities. Its portfolio of properties is managed by a broad collection of healthcare organisations, with the majority of its leases being triple-net leases.

The triple-net lease is the cornerstone of Omega's business model, and understanding it is essential to understanding the company. Let's first define what a Triple Net Lease is. A Triple Net Lease (NNN) can be defined as a form of commercial lease where, in addition to base rent, the tenant/occupier also pays the three main operating expenses that are associated with the property: Property Taxes, Insurance, and Maintenance—extending to items such as landscaping and roof repairs. Contrary to an NNN, in a "Gross Lease," the landlord typically bears most or all of the property's operating expenses.

Why does this matter? "Net lease" refers to the triple-net lease structure, whereby tenants pay all expenses related to property management: property taxes, insurance, and maintenance. One of the more "bond-like" property sectors, Net Lease REITs tend to operate more like a financing company than a property manager and have investment characteristics similar to corporate bonds due to the long-term nature of most net leases and the underlying "credit" exposure through their tenants' ability to pay rent.

This structure creates remarkably predictable cash flows for the landlord. Omega doesn't worry about whether the roof needs replacing or property taxes are increasing—that's the operator's problem. Triple-Net Lease Focus: The NNN lease structure creates predictable cash flows and significantly reduces property-level operational responsibilities and expenses.

But here's the crucial nuance that many investors miss: triple-net doesn't mean risk-free. If your tenant goes bankrupt, you're stuck with a highly specialized building designed for one purpose—caring for elderly or medically complex patients—and you need to find a new operator fast. As we'll see, this theoretical risk became very real during COVID-19.

Scale and Diversification: OHI possesses one of the largest portfolios of SNFs and ALFs, diversified across numerous operators and geographic locations, mitigating operator-specific and regional risks. Sector Specialization: Decades of focus on the healthcare real estate sector provide deep industry knowledge and strong relationships with operators.

From its inception, Omega made a strategic choice that differentiated it from larger, more diversified healthcare REITs like Welltower and Ventas: it would focus primarily on skilled nursing facilities. This wasn't the sexy part of healthcare real estate. Medical office buildings near prestigious hospital systems? Glamorous. Life science labs in Boston's biotech corridor? High-growth. Senior living communities with tennis courts and wine bars? Aspirational. Skilled nursing facilities where Medicare patients go for rehabilitation after hip surgery, or where Medicaid patients receive long-term care? That's the unsexy, highly regulated, politically fraught world Omega chose to dominate.

The skilled nursing industry is unique in commercial real estate because of its payment structure. These properties differ from other senior housing assets because third-party payment, notably Medicare and Medicaid, is the primary source of rental income. That puts a very political spin on revenues and can lead to changes in the business environment, potentially material ones, that are hard to predict.

This meant Omega's entire investment thesis depended on operators who depended on government reimbursement. It was an indirect bet on the American social safety net—a bet that proved both more durable and more volatile than anyone expected.

III. Building the SNF Empire: The Early Growth Years (2000–2014)

The arrival of Taylor Pickett as CEO in 2001 marked a turning point in Omega's trajectory. Mr. C Taylor Pickett has been the Chief Executive Officer and Director of the company since 2001. Prior to this, he served for Integrated Health Services (IHS) in various positions including an Executive Vice President and the Chief Financial Officer.

Pickett's background at Integrated Health Services was both a credential and a cautionary tale. IHS had been one of the largest post-acute healthcare providers in America before financial difficulties forced it into restructuring. Pickett had seen firsthand how operational challenges at healthcare providers could spiral—knowledge that would prove invaluable for a landlord whose fortunes were tied to operator health.

Previously, C. was the Board Member at COPT Defense Properties and also held positions at KPMG. C. received a bachelor's degree from University of Delaware and a JD from University of Maryland Francis King Carey School of Law.

Under Pickett's leadership, Omega developed a disciplined acquisition strategy in what remained a highly fragmented industry. The skilled nursing sector included thousands of facilities owned by regional operators, mom-and-pop businesses, and nonprofit organizations. Omega became the go-to capital partner for operators looking to expand or monetize their real estate without giving up operational control.

The strategy was methodical: acquire properties, structure long-term leases with built-in rent escalators, and use the cash flow to pay dividends while gradually expanding the portfolio. Their revenue primarily comes from rent and interest collections, with built-in lease escalators, often averaging around 2.2% annually, providing a foundation for organic growth.

This approach produced remarkable results. In 2021, Omega was ranked in the top 30 of all REITs in terms of 10-year total shareholder return for the eleventh consecutive year.

The consistency of this performance reflected several advantages Omega had cultivated: deep operator relationships that generated proprietary deal flow, underwriting expertise that allowed the company to price risk appropriately, and a capital structure that provided flexibility through market cycles.

By 2014, Omega had established itself as a major force in skilled nursing real estate. But the company's leadership recognized that to become truly dominant, they needed scale. The fragmented industry was consolidating, and bigger balance sheets meant better access to capital markets and more negotiating leverage with operators. The opportunity for transformational growth arrived in late 2014.

IV. INFLECTION POINT #1: The Aviv REIT Merger (2015)

On October 30, 2014, Omega and Aviv REIT announced what would become the most significant transaction in the skilled nursing REIT sector. Omega Healthcare Investors, Inc. and Aviv REIT, Inc. today announced that the Boards of Directors of both companies have unanimously approved a definitive agreement under which Omega will acquire all of the outstanding shares of Aviv in a stock-for-stock merger. The transaction values Aviv at $3.0 billion, and creates the premier publicly traded pure-play skilled nursing facility real estate investment trust ("REIT").

Omega Healthcare Investors is poised to own nearly 875 skilled nursing properties across 41 states, following its merger with Aviv REIT in a $3 billion deal. The all-stock deal will create the nation's "premier publicly traded pure-play skilled nursing facility real estate investment trust."

The deal mechanics were carefully structured. Under the terms of the merger agreement, each outstanding share of Aviv common stock was converted into 0.90 of a share of Omega common stock. In connection with the merger, Omega issued approximately 43.9 million shares of common stock to former Aviv stockholders. On a fully diluted basis following the closing of the merger transaction, legacy Omega stockholders own approximately 72% of the combined company, and former Aviv stockholders beneficially own approximately 28%.

Under the terms of the deal, each Aviv shareholder would receive 0.90 Omega shares for each of Aviv share, which would be the equivalent of about $35 of Omega stock for each Aviv share. This represents a 16% premium for Aviv shareholders.

The strategic rationale was compelling. "We believe that the combination with Aviv and the expertise and proven track records of the combined management team firmly positions Omega to continue as the leading consolidator in the large, highly fragmented SNF industry," said Taylor Pickett, Omega's Chief Executive Officer.

The merger closed on April 1, 2015. Omega Healthcare Investors, Inc. and Aviv REIT, Inc. announced the completion of Omega's acquisition of all of the outstanding shares of Aviv in a stock-for-stock merger, forming a combined company with equity market capitalization of approximately $7.8 billion and a total market capitalization of approximately $11.1 billion. The combined company will be the premier publicly traded real estate investment trust (REIT) focused principally on skilled nursing facilities (SNFs), with a diversified portfolio of investments including over 900 properties located in 41 states and operated by 81 different operators.

Leadership continuity was maintained. Taylor Pickett will continue to serve as Omega's Chief Executive Officer following the closing of the merger transaction. Craig M. Bernfield, former Aviv Chairman and Chief Executive Officer, and Norman R. Bobins and Ben W. Perks, former directors of Aviv, were appointed to the Omega Board of Directors effective as of the closing of the merger transaction. In addition, Steven J. Insoft, former President and Chief Operating Officer of Aviv, was appointed Omega's Chief Corporate Development Officer.

The financial firepower expanded immediately. On April 1, 2015, Omega also closed an amendment to its revolving credit and term loan facility, increasing the size of the revolving credit facility to $1.25 billion, and adding a new $200 million term loan facility. On April 1, 2015, OHI Healthcare Properties Limited Partnership also closed on a new $100 million term loan facility.

The Aviv merger wasn't just about getting bigger—it was about getting better. Aviv brought additional operator relationships, geographic diversification, and development expertise. The combined entity had the scale to be taken seriously by institutional investors, the balance sheet to pursue large transactions, and the market position to be the partner of choice for operators seeking capital.

V. Diversification Strategy: Senior Housing & UK Expansion

Following the Aviv merger, Omega began gradually diversifying beyond its pure-play skilled nursing focus. While SNFs remained the core of the portfolio, management recognized the value of expanding into adjacent asset classes and geographies.

The partnership with Maplewood Senior Living represented one of Omega's most ambitious senior housing investments. The relationship began with promise—Maplewood was developing luxury senior living communities under the Inspir brand, targeting affluent urban markets with high-end amenities and design.

The flagship project, Inspir Carnegie Hill, was envisioned as a transformative property. Work is continuing on Maplewood Senior Living's Inspir Carnegie Hill assisted living / memory care high-rise in Manhattan. The pandemic in New York City has posed challenges to the schedule and cost of the project, which now stands at $310 million. A slowdown of construction, combined with certain supply chain challenges and the need for innovative enhanced infection control protocols, will create a safe work environment, will delay the opening to the third quarter at the earliest and will increase project costs.

This was a departure from Omega's typical investment profile—instead of acquiring stabilized facilities with established cash flows, Omega was partnering on ground-up development of luxury urban senior living. The risk profile was markedly different, and as we'll see, the COVID-19 pandemic would test this investment severely.

Beyond senior housing, Omega pursued international expansion into the United Kingdom. Omega Healthcare Investors continues to see opportunity investing in senior housing in the United Kingdom, while also growing its senior living investment pipeline in the U.S. The Hunt Valley, Maryland-based real estate investment trust (REIT) highlighted the acquisition of a 45-property portfolio of care homes in Scotland and Jersey for approximately £259.8 million, which at today's exchange rates total about $344 million.

The UK care home market offered several attractive characteristics: an aging population similar to the United States, a regulatory framework that provided revenue visibility, and fragmented ownership that created acquisition opportunities.

Omega also made strategic investments beyond traditional real estate. With its focus on the long-term healthcare sector, Omega announced in March 2021 that it had acquired Connected Living, a technology platform that seeks to help ageing communities better connect and communicate with one another.

These diversification moves reflected management's recognition that the healthcare real estate landscape was evolving. Pure-play SNF concentration had served Omega well, but building optionality through senior housing and international exposure provided additional growth vectors and risk mitigation.

VI. INFLECTION POINT #2: The COVID-19 Crisis (2020–2023)

No event in Omega's history tested the company's business model more severely than the COVID-19 pandemic. The crisis exposed every vulnerability in the skilled nursing sector—and by extension, in Omega's investment thesis.

The Initial Shock

When COVID-19 emerged in early 2020, skilled nursing facilities immediately became the epicenter of the pandemic. The elderly population these facilities served was the most vulnerable to severe COVID outcomes. Visitation bans prevented new admissions. Staff shortages escalated as workers fell ill or refused to enter high-risk environments.

It's been an absolutely horrible few months for the long-term care (LTC) industry because of the major impact of the COVID-19 pandemic. And that's not good news for Omega Healthcare Investors. Shares of the LTC-focused real estate investment trust (REIT) have fallen 35% year to date after plunging more than 60% in March.

The human toll was staggering. Omega Chief Operating Officer Daniel J. Booth said the impact of COVID-19 on operators, residents and frontline employees is "unprecedented." Omega reported 4,136 confirmed cases among residents and employees across 250 of its senior living and skilled nursing facilities in its portfolio, with at least 350 deaths.

Occupancy collapsed. The real estate investment trust reported its cumulative occupancy fell from a rate of 84% in January 2020 to a low of about 73% in December. Occupancy declined ~13% between 2020 and 2021 due to COVID. Now, with the worst in the rearview mirror, occupancy began to show signs of rebounding.

For Omega, the occupancy decline wasn't a direct problem—the company doesn't run the facilities or bear the operating costs. But when occupancy falls, operator revenues fall. When operator revenues fall, their ability to pay rent becomes questionable. This is the fundamental tension in the triple-net model: the landlord is theoretically insulated from operating risk, but that insulation breaks down when tenant distress becomes severe enough.

Tenant Distress & Restructuring

The pandemic pushed multiple Omega tenants to the brink. Omega Healthcare executives expect operator performance to be "significantly affected" for the foreseeable future after reporting an 8% decline in overall occupancy since February. "Although occupancy levels have appeared to stabilize, it remains uncertain when occupancy will return to pre-COVID levels," CEO C. Taylor Pickett said.

The operational pressures were multi-faceted. Many of our operators are experiencing significant cost increases as a result of the pandemic. These increases primarily stem from elevated labor costs, including increased use of overtime and bonus pay, as well as a significant increase in both the cost and usage of personal protective equipment and supplies.

Management navigated this crisis through a combination of restructuring agreements, asset sales, and patient capital deployment. Rather than attempting to immediately collect contractual rents from distressed tenants—which could push operators into bankruptcy and leave Omega with vacant buildings—the company worked collaboratively to find solutions.

Government Support & Recovery

Federal and state government support proved critical. Omega's operators also reported receiving $115 million in federal stimulus funds during the fourth quarter, and $102 million in aid during the third quarter. Executives said the relief was vital for ensuring operators' earnings remained stable during the quarters.

Throughout the crisis, Omega maintained its dividend—a decision that built significant credibility with income-focused shareholders. Omega has stood by its dividend payment, holding it steady through the pandemic, as it believes the industry will recover.

The Maplewood Restructuring

Perhaps no tenant relationship illustrated COVID's lingering effects more clearly than Maplewood Senior Living. Omega Healthcare Investors is making headway on its plan to restructure a 17-community portfolio operated by Maplewood Senior Living after the senior living operator faced a "modest liquidity crunch" in January. Omega and Maplewood announced a plan to restructure their operating relationship earlier this year. Under the plan, Maplewood and Omega have agreed to fix the operator's annual rent at $69.3 million and defer annual 2.5% rent escalators through 2025.

The situation was complicated by tragedy. Smith was president and CEO of Maplewood and its Inspīr luxury brand when he died unexpectedly on March 31. Gregory Smith had been the visionary behind Maplewood's luxury senior living concept, and his sudden passing created uncertainty about the operator's direction.

Omega Healthcare Investors has reached a deal with the estate of Greg Smith, the late president and CEO of Maplewood Senior Living, to transition control of Maplewood to some members of the existing Maplewood management team. The agreement was reached July 31, two days before the REIT's latest earnings call.

By late 2024, the Maplewood situation had stabilized significantly. Maplewood Senior Living has reached a 95% average occupancy rate across its senior housing portfolio. Maplewood Senior Living has reached a 95% average occupancy rate across its senior living portfolio (independent living, assisted living and memory care), with multiple communities currently at 100% occupancy.

The COVID experience validated Omega's core competency: workout expertise. The company had built institutional knowledge over decades about how to manage distressed tenant situations, and this capability proved invaluable during the pandemic's aftermath.

VII. The Recovery & Modern Era (2024–Present)

Omega emerged from the COVID crisis fundamentally stronger. Omega Healthcare Investors annual revenue for 2024 was $1.051B, a 10.7% increase from 2023.

The recovery was evident across multiple metrics. Completed $340 Million in New Investments in Q4 2024. Net income for the quarter of $116 million, or $0.41 per common share, compared to $57 million, or $0.22 per common share, for Q4 2023. Nareit Funds From Operations for the quarter of $196 million, or $0.68 per common share, compared to $129 million, or $0.50 per common share, for Q4 2023. Adjusted Funds From Operations for the quarter of $214 million, or $0.74 per common share, compared to $173 million, or $0.68 per common share, for Q4 2023.

Capital Structure Strengthening

In September 2025, Omega completed a major refinancing that significantly enhanced financial flexibility. Omega Healthcare Investors, Inc. announced it has closed a new $2.3 billion senior unsecured credit facility, replacing its previous $1.45 billion revolving credit facility. The new package includes a four-year $2.0 billion revolving credit facility and a three-year $300 million delayed draw term loan facility. The company also amended its existing $428.5 million term loan agreement to reduce interest rate margins.

The Credit Facility was supported by over 20 incumbent and new financial institutions and was substantially oversubscribed.

This oversubscription reflected lender confidence in Omega's credit profile—a notable validation given the stress the company's operators had experienced during COVID.

Strategic Transactions

The most significant recent transaction was the Saber Healthcare partnership. Executives at Omega Healthcare Investors said the company's third quarter was marked by operational improvements and high occupancy, enabling the company to pursue additional investments, as they shared details on its latest $222.4 million joint venture with affiliates of Saber Healthcare.

CEO Taylor Pickett lauded the Saber deal as one of a kind. "They're essentially the private Ensign, and they're set up to grow really significantly in a very creative way over the next five plus years," Pickett said during the company's third quarter conference call, likening Saber's model to the publicly traded Ensign Group. "We're really excited to be part of that because [there's] upside in our investment, plus the yield we're getting on that investment is really remarkable."

Affiliates of Saber will retain a 51% equity interest in the JV. The 64 facilities held by the JV are subject to triple net leases, with subsidiaries of Saber, that generate $69.4 million in contractual rent per annum.

This transaction represented an evolution in Omega's approach—rather than simply acquiring properties, the company was partnering with high-quality operators through creative structures that aligned incentives.

UK Expansion Continues

The properties have an initial cash yield of 10% and the transaction was closed last month, with U.K.-based transactions representing 93% of the company's investments made in the first quarter. At present, Omega has 14 operators it works with in the U.K.

Current Portfolio Composition

Omega's triple-net portfolio is its "core portfolio." In total, Omega owns 408 senior living communities spanning assisted living, memory care and independent living.

Omega's core portfolio consists of 1,024 facilities, of which around 60% percent are skilled nursing facilities and other transitional care facilities in the U.S., while the other 40% is U.S.-based senior housing and U.K.-based care homes.

The third quarter of 2025 demonstrated the company's momentum. Net income for the quarter of $185 million, or $0.59 per diluted share, compared to $115 million, or $0.42 per diluted share, for Q3 2024. Adjusted Funds From Operations for the quarter of $243 million, or $0.79 per diluted share, compared to $203 million, or $0.74 per diluted share, for Q3 2024. Funds Available for Distribution for the quarter of $231 million, or $0.75 per diluted share, compared to FAD of $192 million, or $0.70 per diluted share, for Q3 2024.

Omega posted funds from operations (FFO) of $0.79 cents per share during the third quarter, above analysts' consensus estimate of $0.75 cents a share, with the company raising full-year 2025 FFO guidance to $3.08 to $3.10 per share, reflecting 8% year-over-year growth. Omega's EBITDA coverage rose to the company's strongest level in 12 years.

VIII. Business Model Deep Dive: How Omega Makes Money

Omega's business model is elegantly simple in concept but nuanced in execution. The company serves as a specialized capital provider to healthcare operators, converting long-term lease agreements into predictable cash flows.

The Triple-Net Foundation

Through our triple-net lease structure, we provide customized financing to a diverse group of healthcare providers.

Triple Net Lease: Tenant pays all or part of the property taxes, insurance and common area maintenance on top of a base monthly rent. These tend to be more landlord friendly as they ensure predictability, which can help landlords better manage expenses down the road.

The beauty of this structure for Omega is that revenue recognition is remarkably clean. The company collects rent, and essentially all of that rent drops to the bottom line (minus corporate overhead, interest expense, and depreciation). There's no need for property management staff, no worry about maintenance budgets, no exposure to utility cost fluctuations.

Organic Growth Through Escalators

Their revenue primarily comes from rent and interest collections, with built-in lease escalators, often averaging around 2.2% annually, providing a foundation for organic growth.

Under triple-net leases, REITs generally receive 2.5%-3.5% annual rent increases, as specified by the lease agreement.

These contractual escalators provide inflation protection and organic growth without requiring additional capital deployment. A 2% annual escalator compounds meaningfully over a 15-year master lease.

REIT Distribution Requirements

As a REIT, Omega must distribute at least 90% of taxable income to shareholders. REITs must distribute at least 90% of their taxable net income to shareholders via dividend payments.

This creates the high dividend yield that attracts income-focused investors. OHI has an annual dividend of $2.68 per share, with a yield of 5.99%. The dividend is paid every three months.

Capital Recycling

Omega actively manages its portfolio, selling underperforming assets and redeploying capital into higher-quality properties. $81 Million in Asset Sales – In the third quarter of 2025, the Company sold 11 facilities for $81.1 million in cash, recognizing a gain of $28.2 million.

This capital recycling is essential for maintaining portfolio quality and avoiding the trap of holding onto distressed assets too long.

Balance Sheet Management

Balance sheet -- $737 million in cash as of September 30, 2025. Entered into a new $2.3 billion credit facility (including a $2 billion revolver) in the third quarter of 2025; leverage reduced to 3.59x as of September 30, 2025. Fixed charge coverage ratio was 5.1x in the third quarter of 2025.

The leverage reduction to 3.59x debt-to-EBITDA provides significant headroom compared to historical levels and positions Omega to pursue acquisitions opportunistically.

IX. Porter's Five Forces Analysis

Threat of New Entrants: LOW-MODERATE

The barriers to entering the healthcare REIT space are substantial but not insurmountable. Scale matters enormously—Omega's size provides access to investment-grade debt, diversification across operators and geographies, and underwriting expertise that takes decades to develop. New entrants would need to build relationships with operators, develop regulatory knowledge, and accumulate capital—a multi-year process.

However, private equity has proven capable of competing for acquisitions, and well-capitalized new entrants could eventually challenge incumbents.

Bargaining Power of Suppliers (Operators): MODERATE

Omega's portfolio diversification mitigates individual operator leverage. Omega has a portfolio of investments that includes 1,024 operating facilities operated by 88 different operators.

No single operator accounts for an overwhelming share of revenue, which limits any individual tenant's negotiating power. However, the COVID experience demonstrated that operator distress can become Omega's problem—when tenants can't pay rent, Omega must either work through restructurings or face the costly process of re-tenanting specialized healthcare facilities.

Bargaining Power of Buyers (Tenants/Operators): MODERATE-HIGH

Operators have multiple financing options available: traditional banks, private equity, other healthcare REITs, and government programs. Omega competes on relationship quality, execution speed, and financing flexibility rather than just price. Larger operators with strong credit profiles have significant negotiating leverage; smaller operators may be more dependent on Omega's capital.

Threat of Substitutes: MODERATE

Skilled nursing facilities are floundering while both home care and assisted living facilities are growing in popularity, particularly for those with chronic but manageable conditions. The capital markets, including private equity sources, are accelerating the decline in nursing homes by shifting investment into assisted living facilities and home-based technologies.

Home healthcare, aging-in-place technologies, and hospital-at-home programs represent potential substitutes for skilled nursing care. However, skilled nursing facilities serve patients requiring 24/7 medical supervision—a need that can't be met by lower-acuity alternatives. The core demand driver remains: patients requiring rehabilitation after surgery or long-term care for complex medical conditions have limited alternatives.

Competitive Rivalry: MODERATE-HIGH

Company name LTC Properties, Inc., Company name Medical Properties Trust Inc., Company name National Health Investors, Inc., Company name Omega Healthcare Investors, Inc., Company name Sabra Health Care REIT, Inc.

A $4.2 billion REIT, SBRA invests in an interesting variety of health care facilities in the U.S. and Canada. It owns skilled nursing facilities, rehabilitation centers, assisted living centers, senior housing communities and small specialty hospitals. Its properties are mostly leased to third-party operators on a long-term basis. In total, SBRA has an equity interest in 377 health care properties.

Competition for acquisition targets can drive pricing to levels that compress returns. However, Omega's scale and operator relationships provide advantages in sourcing off-market deals.

X. Hamilton's 7 Powers Analysis

Scale Economies: STRONG

Omega's scale creates multiple advantages: access to lower-cost debt capital, ability to absorb tenant failures across a diversified portfolio, and underwriting expertise that compounds over decades. As of December 31, 2024, Omega Healthcare Investors Inc reported $4.9 billion in outstanding indebtedness with a weighted-average annual interest rate of 4.6%. The company maintained a strong liquidity position with $518.3 million in cash and cash equivalents and $1.45 billion of undrawn capacity under its unsecured revolving credit facility. This financial flexibility is essential for navigating potential market fluctuations and capitalizing on future investment opportunities.

Network Effects: WEAK

Healthcare REITs don't exhibit traditional network effects. More properties don't make the next property intrinsically more valuable in the way that more users make a social network more valuable. Some indirect effects exist through operator relationships—a satisfied tenant may bring additional acquisition opportunities—but these are relationship effects rather than true network dynamics.

Counter-Positioning: MODERATE

Omega's pure-play SNF focus was initially a form of counter-positioning versus diversified healthcare REITs. Larger competitors would have had to dilute their existing strategies to match Omega's specialization. However, as Omega has diversified into senior housing and UK care homes, this differentiation has blurred.

Switching Costs: MODERATE

Long-term master leases create contractual switching costs—operators can't simply walk away from lease obligations. Relationship depth creates soft switching costs—operators value Omega's execution capabilities, restructuring expertise, and industry knowledge. However, operators can still choose alternative capital sources for growth capital without terminating existing Omega relationships.

Branding: MODERATE

Omega Healthcare Investors executives said Friday that they plan to continue using an investment strategy that has produced more than 1,200% in total shareholder returns over the past 20 years.

Omega's track record through multiple cycles builds trust with operators and lenders. This reputation as a reliable capital partner creates value, though "brand" in healthcare real estate is more about relationship credibility than consumer recognition.

Cornered Resource: MODERATE

Omega's deepest operator relationships represent a form of cornered resource—these relationships took decades to develop and provide proprietary deal flow. We are evaluating numerous opportunities from individual owner-operators and regional sellers. Most of which Omega has sourced from existing relationships.

Process Power: STRONG

Omega's workout and restructuring capabilities represent genuine process power. Sixteen of the 17 senior living communities in the core Maplewood portfolio "do incredibly well," Omega CEO Taylor Pickett said. "So you have this solid base that fully supports the current rent, and we feel really good about the outlook."

The company's ability to navigate complex tenant situations—demonstrated through COVID and multiple operator bankruptcies—is a capability that takes institutional memory and expertise to develop.

XI. Bull vs. Bear Case

Bull Case

Demographic Tailwinds Are Real: The aging of the baby boomer generation will be the most significant factor increasing the demand for long-term care services over the next half century. The number of elderly individuals using either nursing facilities, alternative residential care facilities such as assisted living facilities, or home care services is expected to more than double over the next 50 years.

The country is entering a period of "peak demand" for aging baby boomers.

In 2024 alone, around 12,000 Americans will turn 65 every day. By 2030, every baby boomer will be 65 or older, meaning one in five Americans will be a senior citizen.

Supply Discipline: Limited new construction of skilled nursing facilities creates supply discipline that supports occupancy and rental rates over time.

Proven Crisis Management: Omega's EBITDA coverage rose to the company's strongest level in 12 years.

Strong Capital Position: With our strong acquisition pipeline, a favorable operating environment, and over $2 billion in liquidity with very low leverage, we are ideally positioned to grow both our senior housing and skilled nursing portfolios.

Active Pipeline: Omega completed $1.1 billion in new deals year-to-date in 2025 including skilled nursing and senior living assets.

Bear Case

Reimbursement Risk: Medicare and Medicaid policy changes could devastate operator economics, ultimately flowing through to landlords. These properties differ from other senior housing assets because third-party payment, notably Medicare and Medicaid, is the primary source of rental income. That puts a very political spin on revenues and can lead to changes in the business environment, potentially material ones, that are hard to predict.

Labor Shortages: Families searching for beds for aged or sick loved ones soon may find that there isn't a skilled nursing facility available, if there aren't enough nurses and other workers to fill the growing labor shortage. Experts say that the skilled-care industry is facing a perfect storm. First, the U.S. population is aging and living longer.

The country is entering a period of "peak demand" for aging baby boomers, creating a situation where rising demand and pay do not sufficiently match up, leading to a "critical labor shortage." On top of that, the jobs at nursing homes are often strenuous and vary in skills depending on the specific needs of each senior.

Operator Concentration Risk: Despite diversification across 88 operators, significant exposure to any single large operator creates risk if that operator encounters difficulties.

Home Healthcare Disruption: Like many older adults, the Baby Boomer generation often prefer to age in their own homes and communities rather than move to institutional care settings. This preference is expected to drive a shift towards home and community-based care options.

High Payout Ratio: Omega Healthcare Investors, Inc.'s payout ratio is 141.72% which means that 141.72% of the company's earnings are paid out as dividends. A payout ratio above 100% on a GAAP basis (though lower on AFFO) limits financial flexibility.

XII. Key Metrics to Watch

For investors tracking Omega Healthcare Investors, three metrics matter most:

1. Rent Coverage Ratio

This measures operators' ability to pay contractual rent from their operating cash flows. Coverage above 1.2x suggests operators have adequate cushion; coverage below 1.0x indicates distress risk. Omega's occupancy increased by 40 bps quarter over quarter to 82.6%. Rising occupancy typically translates to improved rent coverage.

2. AFFO Payout Ratio

Adjusted Funds From Operations is the key profitability metric for REITs, adjusting net income for non-cash items like depreciation. The ratio of dividends to AFFO indicates dividend sustainability. A payout ratio consistently above 90% leaves little margin for error.

3. Same-Store Rent Growth

The annual rent escalators embedded in Omega's leases (typically 2-2.5%) provide organic growth. Monitoring whether these escalators are being collected or deferred due to tenant distress reveals portfolio health.

XIII. Playbook: Business & Investing Lessons

1. Specialization Creates Expertise Moats: Omega's decades of focus on skilled nursing developed institutional knowledge that proved invaluable during crises. Deep expertise in underwriting, restructuring, and operator relationships represents durable competitive advantage.

2. Triple-Net Isn't Risk-Free: The structure theoretically transfers operating risk to tenants, but when tenants fail, landlords inherit the problem. Re-tenanting specialized healthcare facilities is difficult and time-consuming.

3. Dividend Discipline Builds Trust: Maintaining the dividend through COVID—when many REITs cut or suspended payouts—built enormous credibility with income-focused shareholders. This credibility has real value when accessing capital markets.

4. M&A for Platform Scale: The Aviv merger created a dominant platform that enables better capital access, more operator relationships, and geographic diversification. Scale matters in capital-intensive industries.

5. Geographic/Operator Diversification: Having 88 operators across 42 states mitigates idiosyncratic risk. No single operator failure can threaten the enterprise.

6. Capital Structure Flexibility Matters: Investment-grade credit ratings and significant liquidity enable Omega to pursue opportunities when competitors are capital-constrained and work through distressed tenant situations without forced asset sales.

7. Relationship Capital Compounds: Long-term operator partnerships create deal flow that new entrants cannot replicate. Trust built over decades generates proprietary investment opportunities.

XIV. Epilogue: What's Next for Omega?

As Omega approaches its fourth decade, the company stands at an interesting inflection point. The COVID crisis stress-tested the business model and revealed both vulnerabilities and strengths. The demographic wave that long-term care bulls have anticipated for years is now arriving—By 2030, every baby boomer will be 65 or older, meaning one in five Americans will be a senior citizen.

Management is evolving the investment approach. Omega Healthcare Investors anticipates that 2026 will include "a decent amount of" U.S.-based senior living transaction opportunities "predominantly in a non-triple-net [lease] format."

This suggests a willingness to take on more operational exposure through RIDEA structures where Omega participates directly in facility economics rather than just collecting rent. It's a calculated bet that the demographic tailwind justifies accepting more operating risk in exchange for greater upside.

Our pipeline transaction outlook for the remainder of 2025 and into 2026 continues to be very favorable. Market opportunities both in The US and UK continue to be substantial. And we are witnessing an increase in our ability to secure off-market opportunities that our operating partners and other relationships bring us. We are seeing individual and regional clusters of senior housing assets many of which are underperforming or non-stabilized that can be acquired at prices meaningfully below replacement costs and the ultimate stabilized value.

The leadership team is also evolving. Taylor Pickett, Omega's Chief Executive Officer, stated, "The Company has been fortunate to enjoy a stable executive team for many years, while augmenting the long-standing team with the next generation of leaders." Pickett continued, "Having worked with Matthew and Vikas since they joined the team, I believe their significant industry experience, strong business acumen, and exceptional work ethic will help drive the next stage of growth at the company."

Matthew P. Gourmand is our President and has served in this capacity since January 2025. Mr. Gourmand previously served as our Senior Vice President of Corporate Strategy & Investor Relations since October 2017.

Vikas Gupta is our Chief Investment Officer and has served in this capacity since January 2025. Mr. Gupta joined the company in July 2011 and most recently served as our Senior Vice President of Acquisitions & Development as of April 2015.

For long-term investors, Omega represents a bet on several propositions: that America's aging population will require skilled nursing and senior housing care in large and growing numbers, that government reimbursement will remain adequate to support operator economics, that labor markets will eventually stabilize, and that Omega's management team can continue navigating the inevitable crises that arise in any capital-intensive, highly regulated industry.

The company has proven remarkably resilient through multiple cycles. Whether that resilience can be sustained as demographics shift, technology evolves, and healthcare delivery models transform remains the central question for the decades ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube