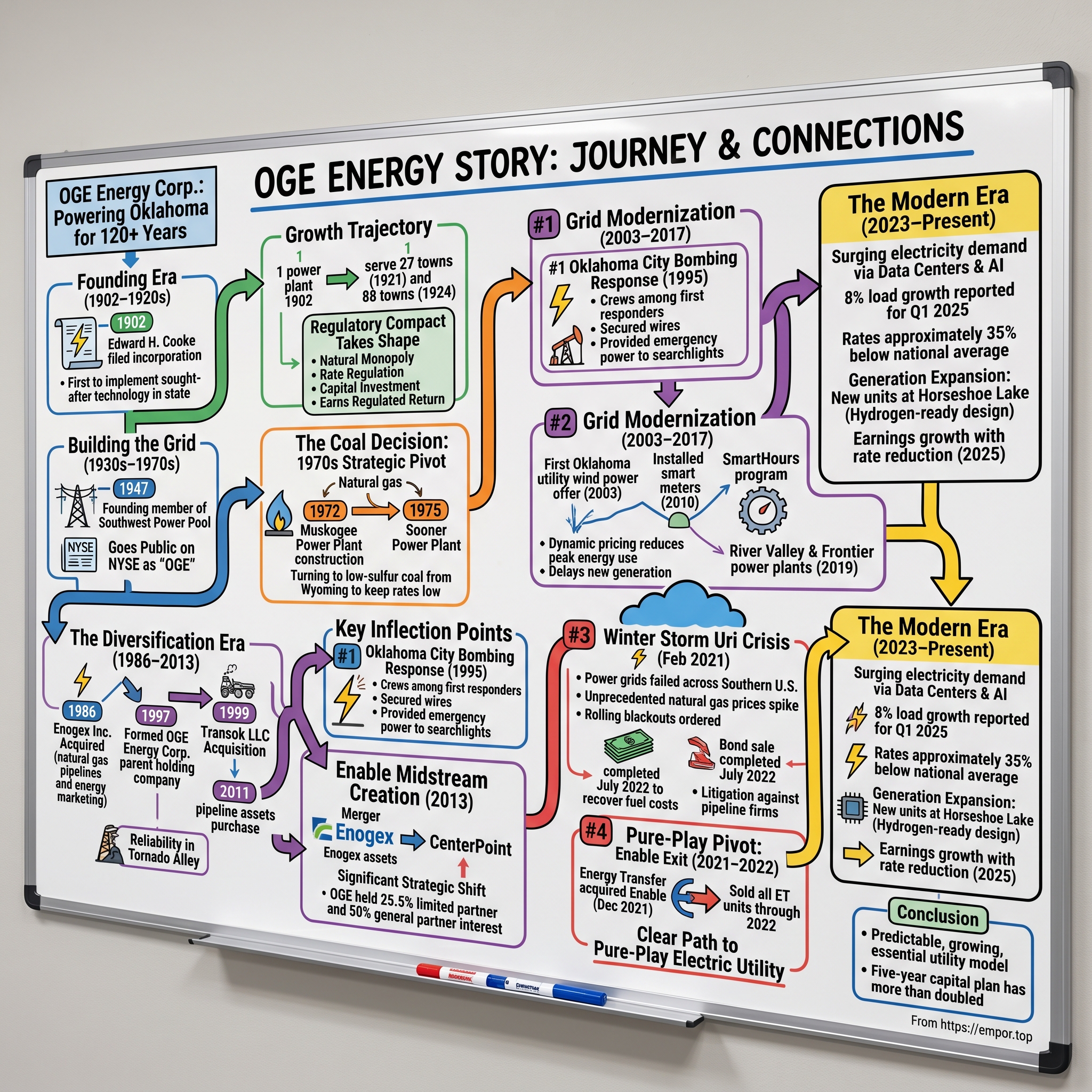

OGE Energy Corp.: Powering Oklahoma for 120+ Years

I. Introduction & Episode Roadmap

On a frigid February morning in 2021, when temperatures in Oklahoma plunged to levels not seen in decades, the control room at OGE Energy Corp.'s headquarters in downtown Oklahoma City became a war zone of difficult decisions. Natural gas prices spiked to unprecedented levels—more than 100 times normal—as the Southwest Power Pool declared emergency conditions. On February 14–15, Winter Storm Uri dropped prolific amounts of snow across Texas and Oklahoma, and power grids—unable to sustain the higher-than-normal energy and heating demand—failed across the Texas Interconnection, with SPP and ERCOT ordering rolling blackouts for 14 states amid frigid temperatures.

For a utility company that had spent over 120 years building trust in its service territory, the storm would become a defining moment—one that exposed vulnerabilities, tested the regulatory compact, and ultimately accelerated a strategic transformation already in motion. Within months, OGE Energy would complete its exit from the midstream gas business, emerging as a pure-play regulated electric utility poised to capitalize on one of the most compelling secular trends in American business: the explosive growth in electricity demand driven by data centers and artificial intelligence.

Today, OGE Energy Corp. serves 909,000 customers with generating capacity of 6,921 megawatts across 9 power plants, 3 wind farms, and 6 solar farms. The company's generation capacity mix stands at 66% natural gas, 22% coal, 7% renewable, and 5% dual generation. With approximately 2,291 employees and 2024 revenues of $2.99 billion, the company operates from a position of strength: a constructive regulatory environment, a growing service territory, and some of the lowest electric rates in the nation.

But the OGE story is far more than a simple tale of a regional utility humming along. It's a case study in strategic patience, crisis management, and the enduring power of the regulated utility business model. How did a pre-statehood utility company survive over a century of industry transformation, diversify into midstream gas, then strategically exit to become a pure-play electric utility? What does the Winter Storm Uri crisis reveal about the fragility of energy infrastructure? And can a 123-year-old company reinvent itself to serve the energy-hungry demands of artificial intelligence and cloud computing?

The answers illuminate not just OGE's journey, but the evolving landscape of American energy infrastructure itself.

II. Founding Era: Electrifying Oklahoma Before Statehood (1902–1920s)

Picture Oklahoma City in 1902: a booming frontier town of perhaps 10,000 souls, still five years away from statehood, where dusty streets gave way to oil derricks and entrepreneurs saw opportunity in an emerging technology that promised to transform American life—electricity.

On February 27, 1902, Edward H. Cooke filed incorporation papers for Oklahoma Gas and Electric Company. George H. Wheeler served as the company's first president. The timing was audacious. Oklahoma Territory was still under federal administration, and the region's sparse population offered little guarantee that an electric utility could survive, let alone prosper.

OG&E was formed following unsuccessful cooperative enterprises between the Oklahoma Ditch and Water Power Company and Oklahoma City Light and Power to provide first hydroelectricity and then steam-generated electricity to the boomtown of Oklahoma City. The company was incorporated when pioneering investors E. H. Cooke and G. E. Wheeler sold their interests in City Light and Power to F. B. Burbridge and Harry M. Blackmer, who in turn obtained East Coast financing to update existing plant and delivery systems.

The economics of early electrification were brutal. At that time, the rate per kilowatt hour for residences was approximately 20 cents, relatively expensive. One of the chief reasons for the high initial costs was that the new power source, gas, was being artificially manufactured prior to the first natural gas discovery by OG&E, which occurred in 1904. That 1904 discovery would prove transformative—suddenly, Oklahoma's abundant natural gas reserves could fuel power generation at dramatically lower costs.

In the 1890s, before Oklahoma was a state, entrepreneurs were investigating electrification. Oklahoma Gas and Electric Company was the first in the state to implement this sought-after technology and, by 1928, was Oklahoma's largest electric company.

The growth trajectory was remarkable for a frontier utility. The company served only Oklahoma City initially with a single power plant. But as statehood arrived in 1907 and Oklahoma's oil boom transformed the regional economy, demand for electricity exploded. From serving only Oklahoma City, the company grew to serve twenty-seven towns in 1921 and eighty-eight in 1924—a tripling in just three years.

In 1928, OG&E executed a bold expansion strategy. The company sold its retail gas business—an ironic move given the "Gas" retained in its name for brand recognition—and used the proceeds to pursue growth. That year, the company purchased the Belle Isle amusement park in north Oklahoma City, built Belle Isle Station power plant there, purchased the Mississippi Valley Power Company, and expanded its service into western Arkansas. The Arkansas expansion would prove strategically crucial, diversifying the company's regulatory exposure and providing access to additional customer growth.

The 1920s also saw the construction of physical symbols of the company's confidence. In 1927, OG&E began erecting a twelve-story headquarters building in Oklahoma City—a statement of permanence in a region where boom-and-bust cycles could wipe out businesses overnight.

The Regulatory Compact Takes Shape

The early 20th century utility model that OG&E adopted would shape its destiny for the next century. Utilities like OG&E operated as natural monopolies—it made no economic sense to string competing power lines down the same street. In exchange for this exclusive franchise, utilities accepted rate regulation: they couldn't charge whatever they wanted, but regulators would set rates designed to cover operating expenses, fuel costs, and provide a reasonable return on invested capital.

This "regulatory compact" created a fundamentally different business from most American enterprises. OG&E couldn't earn monopoly profits, but it also couldn't easily fail. Revenues were predictable. The path to growth was clear: invest in infrastructure, get it approved in the rate base, and earn a regulated return. Patient, steady, boring—but remarkably durable.

For investors, understanding this regulatory framework remains essential. OGE's earnings growth doesn't come from pricing power or market share gains. It comes from growing the rate base—the accumulated capital investment on which regulators allow a return. This single insight explains nearly everything about the company's strategy over the subsequent decades.

III. Building the Grid: Mid-Century Expansion (1930s–1970s)

Throughout the early 20th century, OG&E expanded its service territory across Oklahoma and into western Arkansas, building additional generation facilities to meet increasing demand. In 1947, OG&E became one of the founding members of the Southwest Power Pool, a regional transmission organization that coordinates the electric grid across multiple states. The company continued to grow throughout the mid-20th century, adding significant generation capacity to serve the post-war economic boom.

The Southwest Power Pool membership proved particularly significant. SPP was founded in 1941 when 11 regional power companies pooled their resources to keep Arkansas' Jones Mill powered around the clock in support of critical, national defense needs. The organization emerged from World War II's demands for aluminum production—critical for aircraft manufacturing—and evolved into a framework for coordinating electricity generation and transmission across the central United States.

The company went public and began trading on the New York Stock Exchange under the ticker symbol "OGE" in 1947—a milestone that provided access to capital markets for the infrastructure investments that would define the post-war decades.

When OG&E commemorated its fiftieth anniversary in 1952, it had 280,000 customers. It provided retail electric service to 228 communities and wholesale service to thirteen communities and thirteen electric cooperatives in Oklahoma and western Arkansas.

The Coal Decision: 1970s Strategic Pivot

The 1970s brought the most consequential strategic decision in OG&E's history since its founding. As the nation's energy crisis drove shortages and soaring costs for natural gas, company leadership faced a choice: continue relying on increasingly expensive natural gas, or pivot to an alternative fuel source.

The nation's energy crisis of 1972–1975 meant a shortage and ever-increasing costs of the natural gas used to operate OG&E's plants. The company turned to low-sulfur coal from Wyoming as a means for keeping customer rates low and assuring a consistent power supply. The company began construction of coal generating units at the Muskogee Power Plant in 1972 and built the Sooner Power Plant in 1975. By 1980, almost half of OG&E's power output was from coal-fired generation.

This was not an easy decision. Oklahoma sat atop vast natural gas reserves. The company's heritage was built on gas-fired generation. But management looked at the economics—the price volatility, the supply constraints—and made a pragmatic choice. Wyoming's Powder River Basin offered abundant low-sulfur coal that could be shipped economically by rail.

Notably, in 1971, OG&E decided against constructing nuclear power plants, opting instead for cleaner-burning coal as its primary fuel source. With the benefit of hindsight, this decision spared the company the cost overruns, regulatory delays, and eventual decommissioning challenges that plagued the nuclear industry.

Reliability in Tornado Alley

Operating in Oklahoma presented unique challenges that shaped OG&E's culture and operations. Tornado Alley doesn't just threaten residential customers—it can devastate transmission infrastructure, knock out generation facilities, and test every element of the grid. Beginning in 1971, the utility became the first in Oklahoma to preserve one of its cooling reservoirs, 1,350-acre Lake Konawa, as a year-round recreational area—a recognition that community goodwill mattered as much as kilowatt-hours delivered.

By the 1980s, OG&E had built a generation and transmission system capable of serving a growing service territory through the region's notorious weather extremes. The company's infrastructure investments during this era—particularly the coal plants that would generate baseload power for decades—established the foundation for future growth while keeping rates competitive.

For long-term investors, this period illustrates a fundamental truth about regulated utilities: patient capital investment, approved by regulators and earning steady returns, compounds over decades. OG&E's rate base grew methodically, and the company's earnings followed.

IV. The Diversification Era: Enogex & Midstream Gas (1986–2013)

The mid-1980s brought a strategic temptation that would reshape OGE for three decades: diversification into the unregulated midstream natural gas business.

The Enogex Acquisition (1986)

In 1986, Oklahoma Gas and Electric Company (OG&E) formed subsidiary Enogex Inc. by acquiring natural gas pipeline and energy marketing assets initially operating approximately 3,000 miles of pipelines spanning Oklahoma and other states, marking OG&E's entry into midstream natural gas services. This diversification allowed OG&E to expand beyond its core regulated electric utility operations into the unregulated natural gas sector.

The logic seemed compelling. Oklahoma's oil and gas industry was booming. Natural gas needed to be gathered from wellheads, processed to remove liquids, and transported to markets. These midstream assets could generate unregulated earnings—potentially higher returns than the regulated utility business allowed—while leveraging OGE's existing relationships and regional expertise.

OG&E acquired Enogex, a natural gas pipeline and energy marketing company with 10,000 miles of pipeline spanning west Texas, Oklahoma, Arkansas and southeastern Missouri.

Corporate Restructuring (1997)

By 1997, amid broader industry trends toward corporate restructuring, OG&E reorganized to form OGE Energy Corp. as its parent holding company, which oversaw both OG&E's regulated electric operations and Enogex's unregulated natural gas businesses; at the time, the structure employed about 3,000 people.

This holding company structure—common across the utility industry—allowed OGE Energy to operate its regulated and unregulated businesses with appropriate separation, manage distinct regulatory requirements, and potentially spin off or sell either segment more easily if circumstances warranted.

Enogex Growth & Strategic Acquisitions

Enogex pursued aggressive growth through the late 1990s and 2000s. In 1999, Enogex acquired Transok LLC from Tejas Energy for $701 million, including the assumption of $173 million in long-term debt, which doubled Enogex's pipeline mileage and strengthened its position in Oklahoma's natural gas gathering and processing.

Similarly, in 2011, Enogex purchased the pipeline assets of Wildhorse Central Gathering LLC and Roger Mills Gas Gathering LLC for $200 million from Cordillera Energy Partners, Oxbow Midstream Partners, and West Canadian Midstream, adding over 200 miles of gathering lines in northwest Oklahoma's resource-rich areas. These moves expanded Enogex's footprint in key shale plays and supported increased natural gas production volumes.

The Enable Midstream Creation (2013)

The early 2010s brought the master limited partnership (MLP) boom. Wall Street loved the structure: MLPs paid no corporate taxes, passing through income to unitholders who benefited from favorable tax treatment. Midstream assets—pipelines, processing plants, storage facilities—generated steady cash flows ideal for distribution. Valuations soared.

Throughout the 1990s and early 2000s, OGE Energy diversified its operations, including investments in natural gas midstream assets through its Enogex subsidiary. In 2013, OGE Energy combined its Enogex midstream assets with CenterPoint Energy's interstate pipelines and field services businesses to form Enable Midstream Partners, a master limited partnership. This marked a significant strategic shift for the company.

OGE Energy Corp., CenterPoint Energy Inc. and ArcLight Capital Partners LLC entered into a master limited partnership that included CenterPoint Energy's interstate pipelines and field services businesses and the midstream business of Enogex LLC. The partnership resulted in the creation of Enable Midstream Partners, LP.

The Enable Midstream transaction crystallized value that had been building in Enogex for decades. OGE Energy retained a significant stake—OGE held a 25.5 percent limited partner interest and a 50 percent general partner interest of Enable Midstream Partners LP—while gaining access to capital markets and the potential for growth through Enable's larger platform.

The MLP Hangover

But the MLP boom eventually revealed its limitations. Oil and gas prices crashed in 2014-2015. Enable Midstream's earnings became volatile, tied to commodity prices and producer activity that OGE Energy couldn't control. Investors who bought OGE for utility stability found themselves exposed to energy commodity risk.

Natural Gas Midstream Operations reported earnings of $1.92 per diluted share in 2021, driven by a $1.32 per diluted share gain on the Enable merger transaction, compared with a loss of $2.58 per diluted share in 2020, which included a loss of $2.95 per diluted share due to an investment impairment charge associated with Enable.

The 2020 impairment charge reflected the painful reality: OGE's midstream investment, which had seemed so promising in 2013, had become a drag on the company's valuation and a source of earnings volatility. Management began considering alternatives.

V. Key Inflection Point #1: The Oklahoma City Bombing Response (1995)

At 9:02 a.m. on April 19, 1995, a 4,800-pound truck bomb detonated in front of the Alfred P. Murrah Federal Building in downtown Oklahoma City. The bombing killed 168 souls, including 19 children, and injured more than 600. The blast destroyed more than 300 nearby buildings. Perpetrated by anti-government extremists Timothy McVeigh and his accomplice Terry Nichols, the bombing remains the deadliest act of domestic terrorism in U.S. history.

For OGE, headquartered just blocks away, the bombing wasn't an abstract tragedy—it was immediate, visceral, and demanded response. In 1995, OG&E crews were among the first responders during this horrific event, working to secure and disconnect live electric wires, using truck ladders to reach those stranded in the building, stringing temporary emergency service lines to provide power to searchlights for rescue operations and powering pumps to remove water from the devastated building's basement.

The company's response illustrated something that financial metrics cannot capture: the bond between a regional utility and its community. OGE employees weren't just maintaining infrastructure; they were participating in the immediate, desperate effort to save lives. That response became part of the company's institutional identity—a tangible expression of the service obligation that lies at the heart of the utility compact.

The bombing also reinforced the importance of emergency preparedness and infrastructure resilience. In the aftermath, Oklahoma's emergency response capabilities expanded significantly. For OGE, the experience informed future crisis planning that would prove valuable decades later when Winter Storm Uri tested the company's operational capabilities to their limits.

VI. Key Inflection Point #2: Grid Modernization & SmartHours (2003–2017)

The early 2000s brought a technological transformation that would position OGE as an industry leader in demand-side management and grid modernization.

In 2003, OG&E became the first Oklahoma utility to offer wind power to customers at the Oklahoma State Fair customer kick-off event. In 2007, OG&E constructed the first wind farm to be wholly owned and operated by a utility, Centennial Wind Farm.

But the most consequential innovation came with smart meters.

OG&E became the first Oklahoma utility to install smart meters in its service area, improving response times and strengthening reliability. In addition, the company was able to implement the nationally-recognized SmartHours program. More than 120,000 customers participate in the program today.

Since the smart grid program began in February 2010, OG&E installed more than 340,000 smart meters in its territory, including Moore, Norman and parts of Oklahoma City. Almost 800,000 of the new meters were planned for installation by December 2012, completing the process for OG&E's entire service territory.

The SmartHours program embodied a sophisticated approach to demand management. The SmartHours program helps customers save on energy bills by offering lower prices when they shift electricity use to off-peak times (19 hours a day, weekends, and holidays). By changing energy habits and using less electricity during peak hours (Mon-Fri 2 p.m. to 7 p.m.), customers can reduce their bills.

Study results confirmed that groups that included a Programmable Communicating Thermostat (PCT) and a Variable Peak Price (VPP) rate plan yielded highest average demand reduction during the on-peak period. Customers with a smart thermostat achieved a maximum demand reduction of 48 percent during the peak period when compared to a control group.

The strategic implications extended beyond customer savings. Smart technology coupled with dynamic pricing enabled customers to reduce their maximum peak energy use, which helped delay the need for building incremental generation until at least 2020. This delayed the addition of any new fossil-fueled generation for OG&E.

Generation Modernization

In 2015, OG&E became the first in Oklahoma to develop a utility-scale solar farm on the location of Mustang Power Plant, the company's oldest plant. In 2017, OG&E ushered in a new era in energy technology with the opening of its Mustang Energy Center, with quick-start combustion turbines capable of starting and putting electricity onto the system in under 10 minutes.

The quick-start capability proved prescient. As renewable generation grew on the SPP grid, the ability to rapidly dispatch natural gas turbines to balance intermittent wind and solar became increasingly valuable. OGE's Mustang Energy Center investment positioned the company for a grid increasingly characterized by variable renewable generation.

In 2019, OG&E added two new power plants to its generation fleet: River Valley, located near Poteau, Oklahoma, and Frontier, located in Oklahoma City—further diversifying the generation portfolio and replacing aging infrastructure.

VII. Key Inflection Point #3: Winter Storm Uri Crisis (February 2021)

No event in OGE's recent history proved more consequential than Winter Storm Uri—a crisis that tested the company's operational capabilities, strained the regulatory compact, and accelerated strategic decisions already under consideration.

The Storm Impact

On February 14–15, 2021, the storm dropped prolific amounts of snow across Texas and Oklahoma. As a result of the winter storm and a concurrent cold wave, power grids—unable to sustain the higher-than-normal energy and heating demand from residential and business customers—failed across the Texas Interconnection. Two of the electricity reliability commissions servicing the Southern U.S., the Southwest Power Pool (SPP) and the Electric Reliability Council of Texas (ERCOT), ordered rolling blackouts for 14 states amid the frigid temperatures.

The storm contributed to at least 210 deaths, and sources cited by the Federal Reserve Bank of Dallas estimated the state's storm-related financial losses would range from $80 billion to $130 billion.

Electricity demand during Winter Storm Uri caught OG&E officials by surprise, since their peak demand usually comes in the summer months. Some natural gas generating units were on planned winter maintenance and were unavailable for electricity generation. The utility also encountered icing on its wind generating units and freezing to some coal piles.

But the true shock came from natural gas prices. As demand surged and supply collapsed—Winter Storm Uri in 2021 had the largest effect on Permian region production, reducing production by almost 5 Bcf/d in that region alone. In Texas, natural gas production declined almost 45% during Uri—wholesale gas prices spiked to unprecedented levels. OGE, like other utilities, had to purchase fuel at these inflated prices to keep generators running.

The company later noted that it was "not prepared for the unthinkable and unprecedented spike in natural gas prices, which was nothing like we had ever seen before in history."

The Financial Fallout & Securitization

The utility stated in a filing with the U.S. Securities and Exchange Commission that the sale of $762 million in bonds was completed July 20, 2022 by the Oklahoma Development Finance Authority. It was carried out "for the purpose of allowing OG&E to recover the significant fuel costs it incurred as a result of Winter Storm Uri in February 2021."

The increase added to the overall cost of the bonds and resulted in additional monthly costs of $3.34 to consumers instead of $2.12 as expressed initially. It was an increase of 57% of the predicted rate to OGE customers.

The bond sale was authorized under the February 2021 Regulated Utility Consumer Protection Act which was rushed into law by the Oklahoma legislature. It was also approved by the Oklahoma Corporation Commission (on a 2-1 vote) on December 16, 2021 which adopted a Financing Order.

The unexplained costs of how Oklahoma's major utilities used a new law to extend 2021 Winter Storm Uri costs continued to concern Oklahoma Corporation Commissioner Bob Anthony. He raised questions in 2022 when PSO, OGE, and ONG used securitization and wondered aloud about the true costs to consumers.

The securitization approach spread the extraordinary fuel costs over decades rather than hitting customers with immediate massive rate increases. But it meant that electric and gas customers would be paying for decades for fuel purchased over the space of days in February 2021.

Regulatory & Political Aftermath

Oklahoma Attorney General Gentner Drummond filed a pair of lawsuits in April 2024 against natural gas pipeline firms, alleging the companies helped bid up the price of natural gas to the highest levels in history during the winter storm. The lawsuits alleged Enable subsidiaries and Symmetry Energy Solutions LLC separately manipulated their parts of the natural gas pipeline systems in the state to boost prices before and during the storm.

OGE Energy said it wasn't involved in Enable's operations during the storm. "The OGE Energy Corp. was not engaged in the day-to-day operations of Enable and, in fact, Oklahoma Gas and Electric Company was a customer of Enable."

The irony was not lost on observers: OGE Energy had partially owned the midstream assets (through Enable) that allegedly contributed to the price manipulation that then cost OG&E's customers hundreds of millions of dollars. This uncomfortable dynamic reinforced the strategic logic of exiting the midstream business entirely.

VIII. Key Inflection Point #4: Pure-Play Pivot – The Enable Midstream Exit (2021–2022)

Winter Storm Uri accelerated a strategic decision that had been building for years. The Enable Midstream investment, once a source of potential upside, had become a liability—a source of earnings volatility, regulatory complexity, and now reputational risk.

The Strategic Decision

The transaction added value for shareholders and the communities served, and placed OGE on a clear path to becoming a pure-play electric utility. The transaction significantly enhanced the liquidity of the midstream position and afforded flexibility to exit the investment in a manner that maximized value.

Energy Transfer LP and Enable Midstream Partners, LP entered into a definitive merger agreement whereby Energy Transfer would acquire Enable in an all-equity transaction valued at approximately $7.2 billion. Under the terms of the agreement, Enable common unitholders received 0.8595 ET common units for each Enable common unit.

The Execution

On December 2, 2021, OGE Energy Corp. announced the completion of the merger between Energy Transfer LP and Enable Midstream Partners LP. "We are pleased to announce the successful merger between Energy Transfer and Enable and I thank Enable and its employees for their hard work and dedication over the years," said Sean Trauschke, Chairman, President, and CEO of OGE Energy Corp. "This merger is an important step in OGE's plan to become a pure-play electric utility."

In the merger, all of the 110,982,805 common units of Enable owned by OGE Energy were exchanged for 95,389,720 common units of Energy Transfer. Upon closing of the merger, OGE Energy owned approximately three percent of the outstanding limited partner units of Energy Transfer.

In December 2021, OGE divested its 25.5% stake in Enable Midstream Partners through a unit exchange merger with Energy Transfer. OGE sold its 95.4 million limited partner units of Energy Transfer throughout 2022.

Financial Impact

Natural Gas Midstream Operations reported earnings of $1.92 per diluted share in 2021, driven by a $1.32 per diluted share gain on the Enable merger transaction, compared with a loss of $2.58 per diluted share in 2020, which included a loss of $2.95 per diluted share due to an investment impairment charge associated with Enable.

The exit crystallized the lesson: diversification that seemed smart in 2013 had become a distraction by 2021. The regulated utility business offered predictable earnings, constructive regulatory relationships, and a clear growth pathway through rate base expansion. The unregulated midstream business offered higher potential returns but also commodity exposure, complex partnerships, and management distraction.

As Trauschke noted: "As we look ahead to 2023 as a pure-play electric company, OG&E will continue to deliver reliable, resilient and secure energy for our customers with our focus on safety, operational excellence, and customer experience."

IX. The Modern Era: Data Centers, AI & Load Growth (2023–Present)

Emerging from the Winter Storm Uri crisis and the Enable Midstream exit, OGE entered a new era with remarkable tailwinds: a growing service territory, a constructive regulatory environment, and surging electricity demand driven by data centers and artificial intelligence.

OGE Energy Corp. reported earnings of $2.19 per diluted share in 2024, compared to $2.07 per diluted share in 2023. OG&E, a regulated electric company, contributed earnings of $2.33 per diluted share in 2024, compared to earnings of $2.12 per diluted share in 2023.

OGE Energy reported 8% growth in weather-normalized load for Q1 2025, with the residential sector increasing by 3% and commercial by 28%. The commercial growth is particularly striking—driven by data center development in the Oklahoma City metropolitan area.

The company noted: "Our data center demand remains strong, with ongoing discussions with multiple companies."

The company anticipates an 8.5% weather-normalized load growth in 2025, driven by potential data center opportunities.

Generation Expansion

The new natural gas units at Horseshoe Lake, designed to safely burn hydrogen when it becomes a readily available fuel source, will replace two 60-year-old units at the plant and provide approximately 450 megawatts of generation capacity. The units are equipped to reduce emissions compared to the units they will replace, increase capacity, and have the capability to supply power at peak times.

The new generation units were unanimously approved by the Oklahoma Corporation Commission in 2023 to support OG&E's growing service area. The new units are anticipated to begin providing power to customers by late 2026.

"With a direct economic impact of $536 million, this project is more than an investment in energy infrastructure—it's a commitment to the future of our communities," said Alba Weaver, OG&E's Director of Community Affairs and Economic Development.

Rate Reduction Amid Earnings Growth

In a rare combination, OGE delivered both rate reductions and earnings growth in 2025.

OG&E announced the fuel cost adjustment would cut the average Oklahoma residential electric bill by $6.75 per month starting November 1, 2025, a 4.8% decrease. The average residential customer's monthly bill became $6.75 lower per month, representing a 4.8% reduction.

The same week Oklahoma Gas and Electric announced a more than 4% drop in electric rates starting in November, its parent company, OGE Energy Corp., reported a substantial increase in third quarter 2025 earnings. OGE Energy Corp. recorded earnings of $1.14 per diluted share for the three months ending September 30, 2025.

Today, OG&E's rates are approximately 35% below the national average.

2025 Outlook

OGE provided earnings guidance for 2025 with a range of $2.21 to $2.33 per share, with a midpoint of $2.27. The company expects 5-7% annual consolidated earnings growth from 2025's midpoint.

"With approximately 550 MW of new natural gas turbines under construction and more planned, we are proactively addressing the region's growing energy needs as we maintain some of the lowest rates in the nation for our customers."

X. Leadership & Governance

Sean Trauschke serves as Chairman, President and Chief Executive Officer of OGE Energy Corp. and OG&E. Trauschke has been Chief Executive Officer of the Company since June 2015. He has been President of OG&E since July 2013 and President of OGE Energy since August 2014 and was named as Chairman of the Board in December 2015. Trauschke joined the Company in 2009 as Vice President and Chief Financial Officer.

Trauschke earned a Bachelor of Science degree in Mechanical Engineering from the University of North Carolina at Charlotte, a Master of Business Administration degree from the University of South Carolina and has completed the Advanced Management Program at the Harvard Business School. Trauschke is the past chairman of the Greater Oklahoma City Chamber and serves on the boards of Allied Arts, the Greater Oklahoma City Chamber, United Way of Central Oklahoma, the Oklahoma State Fair, and the Myriad Botanical Gardens.

Trauschke's background is notable for a utility CEO: he came up through the financial side of the business rather than operations, having served in various leadership positions including vice president of investor relations, vice president and chief risk officer, general manager of business unit finance and various roles in treasury. He also served in a variety of purchasing and strategic sourcing roles before moving into finance.

This financial orientation proved valuable during his tenure. Trauschke led OGE through the Enable Midstream exit—a complex financial transaction requiring careful navigation of partnership dynamics, tax implications, and capital allocation. He guided the company through Winter Storm Uri and its financial aftermath. And he has positioned OGE to capitalize on the data center opportunity through disciplined capital investment.

According to investor analysis, OGE has maintained consistent dividend payments for 55 consecutive years and has raised its dividend for 18 straight years, demonstrating remarkable financial stability.

Board Composition

The board of directors consists of 10 members, with nine classified as independent, emphasizing governance focused on regulatory compliance, risk management, and delivering shareholder returns through consistent dividends and growth.

XI. Business Model Deep Dive: How a Regulated Utility Works

Understanding OGE requires understanding the regulated utility business model—a framework that has shaped the company's strategy, capital allocation, and investor returns for over a century.

The Revenue Engine

OGE Energy Corp. primarily generates revenue through its regulated electric utility subsidiary, OG&E, which sells electricity to residential, commercial, and industrial customers. OG&E's investments to strengthen the grid against extreme weather provide the growing customer base across Oklahoma with reliable and safe electric service. The company continually hardens, upgrades, and maintains the electric grid and power plants to improve reliability and better serve customers. OG&E remains committed to delivering reliable electricity at some of the lowest rates in the country.

The Regulatory Framework

Rate cases seek to balance the needs of customers and the utility with public policy goals. Reasonable costs for utility service are defined, and the amount of money the utility company will collect through rates to provide that service in a safe and reliable manner is determined.

Most companies doing business in Oklahoma can simply set their own prices to sell their products and services. However, regulated utilities like OG&E, PSO and ONG are different. The prices regulated utilities charge to provide customers with electricity or natural gas are decided through an open, public process called a rate case. When a pricing adjustment is needed, the utility company files a request with the Oklahoma Corporation Commission, the body that regulates public utilities.

Allowed Return on Equity

The typical return-on-equity for a public electric or natural-gas utility in Oklahoma today is approximately 9.5%; the national average is 10%. But with utility rate hikes occurring year after year, many consumers are questioning why ROEs for monopolies such as public utilities aren't lower.

Public utilities are monopolies that have a stable, and usually growing, customer base plus a guaranteed income stream. Oklahoma Corporation Commissioner Todd Hiett noted that regulators will likely be expected to raise the ROE for public utilities even higher in the years ahead as more electricity is needed for data centers, artificial intelligence applications, and the myriad vehicles, machines and devices that are powered by electricity.

Capital Bias and Rate Base Growth

The traditional rate formula encourages capital investment because it provides a rate of return on the rate base. The more a utility invests, the more money it earns. This is why for-profit utilities prefer capital investment over operating expenses, called "capital bias".

Since 2021, OGE has directly invested over $3 billion in the grid, power generation, and technology to improve reliability for customers and support continued economic growth. This capital deployment directly increases the rate base—the foundation on which OGE earns its regulated return.

The Fuel Cost Adjustment Mechanism

Twice a year, OG&E and the Oklahoma Corporation Commission review the cost of fuel that it takes to produce electricity. "The charge can fluctuate up or down," and OGE noted that "we don't make any money on the purchases of fuel." The charge to the customer should be as close as possible to what OG&E is paying.

This pass-through mechanism means OGE doesn't profit from fuel costs—but it also means the company bears no commodity price risk in normal operations. The Winter Storm Uri crisis was exceptional precisely because it strained this mechanism to breaking point.

XII. Competitive Position & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants: Very Low OGE operates as a regulated monopoly within its service territory. New competitors cannot simply enter the market—regulatory approval, massive capital requirements, and the economic logic of natural monopolies create insurmountable barriers. The only competitive threat comes from distributed generation (rooftop solar) and potential large customers building their own generation—but even these face regulatory constraints.

Bargaining Power of Suppliers: Moderate OGE purchases fuel (natural gas, coal) and generation equipment from competitive markets. Natural gas prices can be volatile, as Winter Storm Uri dramatically demonstrated. However, the fuel cost adjustment mechanism passes most commodity risk to customers. Equipment suppliers face competition, limiting their bargaining power.

Bargaining Power of Buyers: Low Residential and small commercial customers have no choice of electric provider within OGE's service territory. Large industrial customers theoretically could build their own generation or relocate, but rarely do. The regulatory compact ensures rates are "reasonable"—neither exploitative nor insufficient.

Threat of Substitutes: Low but Growing Distributed solar, battery storage, and energy efficiency represent potential substitutes for grid electricity. However, grid reliability remains essential for most applications, and OGE's low rates reduce the economic incentive for self-generation.

Industry Rivalry: Low Within its service territory, OGE faces no direct competition for retail customers. Competition exists only at the wholesale level within SPP and for capital allocation against other utilities nationwide.

Hamilton Helmer's 7 Powers Framework

Process Power: OGE has developed operational expertise over 123 years, including grid management, storm response, and demand-side management capabilities. The SmartHours program demonstrates superior process innovation.

Scale Economies: OGE benefits from significant scale economies in generation, transmission, and distribution. Fixed costs are spread across 909,000 customers and nearly 7,000 MW of generation capacity.

Network Economies: Limited—electricity isn't more valuable because more people use it.

Counter-Positioning: Not applicable in a regulated monopoly context.

Switching Costs: Extremely high—customers cannot switch providers and would face enormous costs to relocate outside the service territory.

Branding: OGE enjoys strong brand recognition in Oklahoma, built over 123 years of service. The company's community involvement and crisis response (Oklahoma City bombing, storm restoration) strengthen customer loyalty.

Cornered Resource: OGE's franchise territory represents a cornered resource—no competitor can access these 909,000 customers without regulatory approval.

Bull Case

-

Data Center Tailwind: The AI and cloud computing boom is driving unprecedented electricity demand growth. OGE's low rates (35% below national average) and available generation capacity position it to capture significant data center development.

-

Rate Base Growth: Approximately $3 billion invested since 2021, with 550+ MW under construction. Each dollar of capital investment increases rate base and earnings potential.

-

Constructive Regulatory Environment: Oklahoma regulators have generally been supportive of utility investments, though recent CWIP denial shows limits.

-

Balance Sheet Strength: Pure-play focus and Enable exit eliminated exposure to commodity price volatility and simplified the capital structure.

-

Dividend Growth Track Record: 18 consecutive years of dividend increases demonstrate shareholder commitment.

Bear Case

-

Winter Storm Uri Overhang: Customers continue paying securitization charges for decades. Future extreme weather events could create similar cost spikes.

-

Regulatory Risk: Recent denial of CWIP recovery demonstrates regulatory constraints. ROE compression remains possible.

-

Coal Exposure: 22% of generation from coal creates potential stranded asset and environmental regulatory risk.

-

Geographic Concentration: Heavy dependence on Oklahoma economy and regulatory environment.

-

Interest Rate Sensitivity: Rising rates increase financing costs for capital-intensive utility investments.

Myth vs. Reality

| Common Narrative | Reality |

|---|---|

| "Utilities are boring, stable investments" | OGE faced a near-$3 billion impairment on Enable and weathered unprecedented crisis during Winter Storm Uri |

| "Data centers are guaranteed growth" | Data center demand remains strong, but projects require regulatory approval and large load tariff structures remain under development |

| "Low rates mean low margins" | Low rates reflect efficient operations and constructive regulation, enabling 5-7% annual earnings growth |

| "The Enable exit was a forced retreat" | The exit reflected strategic repositioning to pure-play utility model, not distressed sale |

XIII. Key Performance Indicators to Watch

For long-term investors monitoring OGE Energy, three metrics matter most:

1. Weather-Normalized Load Growth

This measures underlying electricity demand independent of weather variations. OGE reported 8% growth in weather-normalized load for Q1 2025, with the residential sector increasing by 3% and commercial by 28%. The commercial growth reflects data center and industrial development. Sustained load growth in the mid-single digits or higher supports earnings growth without requiring rate increases.

2. Rate Base Growth

Rate base—the accumulated capital investment on which regulators allow a return—is the fundamental driver of utility earnings. OGE's $3+ billion investment since 2021 and ongoing generation construction directly expand rate base. Track capital expenditure guidance and completed projects to monitor this driver.

3. Earned Return on Equity

Return on equity (average) was 9.6% in 2024, up from 9.3% in 2023. This measures how effectively OGE deploys capital within regulatory constraints. The typical return-on-equity for a public electric or natural-gas utility in Oklahoma today is approximately 9.5%. Monitoring earned ROE relative to allowed ROE reveals regulatory lag or operational efficiency.

XIV. Risk Factors & Regulatory Considerations

Winter Storm Liability

The securitization of Winter Storm Uri costs has been legally upheld, but ongoing litigation and regulatory scrutiny continue. Oklahoma Attorney General Gentner Drummond filed lawsuits against natural gas pipeline firms, alleging the companies helped bid up the price of natural gas to the highest levels in history during the storm. While OGE itself isn't a defendant, the legal proceedings may affect industry-wide practices and future storm cost recovery.

CWIP and Capital Recovery

OG&E recently asked to raise customer rates during construction of new infrastructure, but the Oklahoma Corporation Commission gave them a prompt "no." OG&E wanted to use a cost-recovery tool called Construction Work in Progress (CWIP) to have ratepayers shoulder the cost of building two new natural gas turbines at its Horseshoe Lake plant. Thanks to a recent law (Senate Bill 998), utilities can recover those costs before construction is done, but not always.

Under the regulatory order, OG&E will file a new large load tariff by July 1, 2026, to shield existing customers from increased costs associated with serving new large loads, like data centers, building and expanding in OG&E's service area.

This regulatory decision creates near-term uncertainty but reflects legitimate concerns about ratepayer protection. The large load tariff requirement may actually benefit existing residential customers by ensuring data centers pay appropriate costs for infrastructure serving their needs.

Energy Transition Risks

OGE's 22% coal generation exposure creates potential regulatory risk as environmental standards evolve. The company is actively converting coal facilities to natural gas and investing in renewables, but stranded asset risk remains. The hydrogen-ready design of new Horseshoe Lake units reflects management's hedging of longer-term energy transition scenarios.

XV. Conclusion: A 123-Year-Old Company Positioned for the AI Age

OGE Energy's journey from pre-statehood territorial electrification to AI-era power provider illuminates enduring truths about regulated utilities and American infrastructure.

The company survived the Great Depression, world wars, oil shocks, and the 2008 financial crisis not by taking outsized risks or disrupting industries, but by executing the fundamentals: reliable service, constructive regulatory relationships, and disciplined capital investment. When management strayed from this formula—diversifying into midstream gas—the results were disappointing. When they returned to core competencies, performance improved.

The Winter Storm Uri crisis revealed the vulnerabilities in America's energy infrastructure: the interconnected failures between gas supply and electric generation, the inadequate winterization standards, the regulatory frameworks unprepared for unprecedented events. OGE's response—securitization of costs, subsequent strategic simplification, and accelerated generation investment—demonstrates institutional resilience.

Looking ahead, the data center opportunity represents perhaps the most compelling demand growth story for regulated utilities in decades. OGE has managed to keep O&M per customer growth at less than 1%, rates at some of the lowest levels in the nation, load growth at a compound annual 2.2%, all while investing more. The five-year capital plan has more than doubled. The dividend has grown at a compound annual rate of 5% and consolidated earnings per share excluding midstream results has grown at a compound annual rate of approximately 6%.

These results weren't achieved through financial engineering or aggressive growth strategies. They emerged from the patient execution of a business model perfected over 123 years: invest in infrastructure, earn a regulated return, pass fuel costs through to customers, and maintain reliability in a region prone to extreme weather.

For investors, OGE represents what regulated utilities are supposed to be: predictable, growing, and essential. The 5-7% annual earnings growth guidance, combined with the dividend track record, offers a compelling total return profile for patient capital. The risks—regulatory, weather, and energy transition—are real but manageable for a company with this track record of adaptation.

Oklahoma Gas and Electric Company filed its incorporation papers on February 27, 1902—five years before Oklahoma became a state. As the company approaches its 125th anniversary, it remains what Edward H. Cooke and George H. Wheeler created: Oklahoma's oldest and largest electric utility, powering life across the heartland.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube