Realty Income: The Monthly Dividend Company

I. Introduction & Episode Blueprint

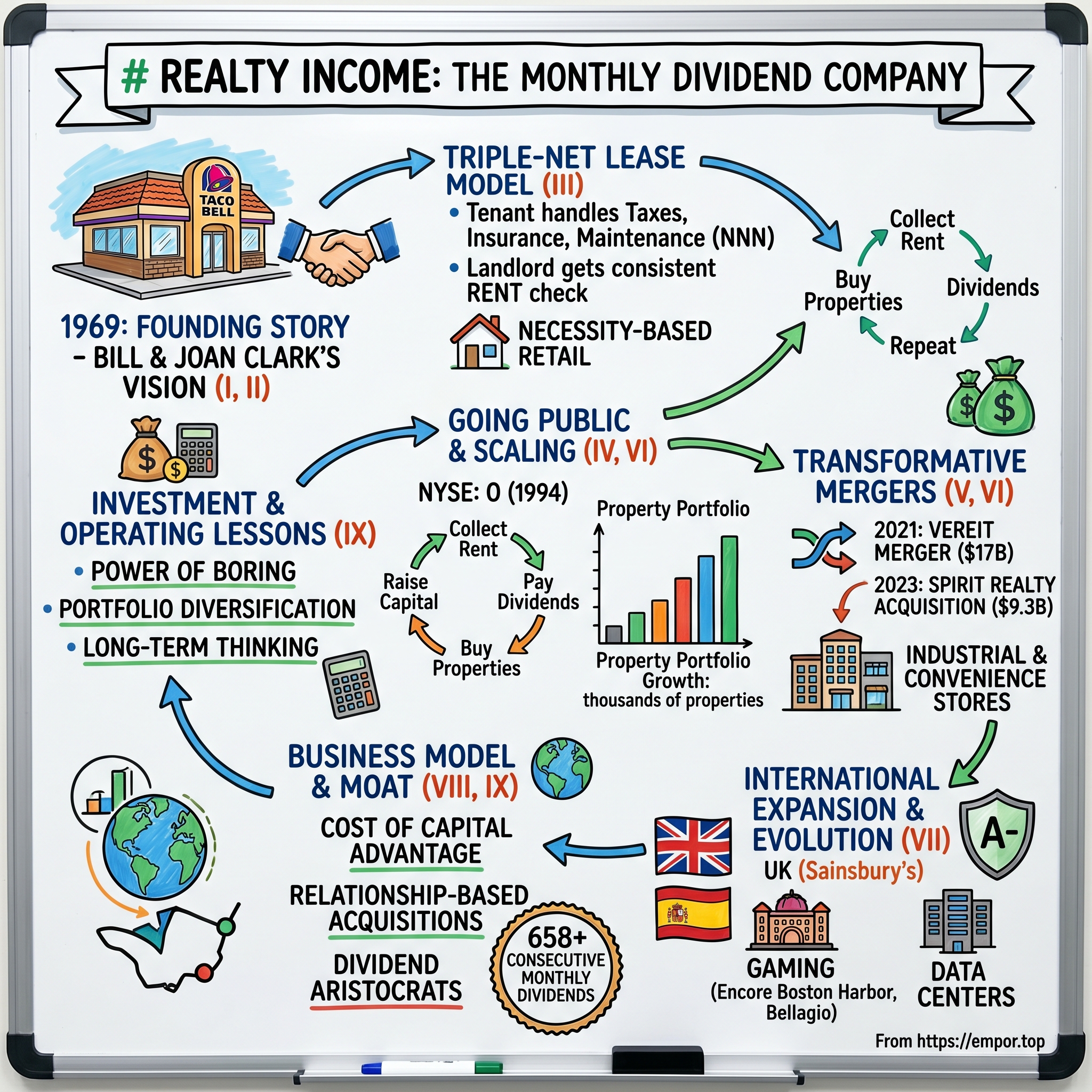

Picture this: You're sitting in a cramped office in Northridge, California, in 1969. The air conditioning barely works, the carpet is that unfortunate shade of burnt orange that defined the era, and you've just shaken hands with Glen Bell—yes, that Glen Bell, the Taco Bell founder—on a deal to buy one of his restaurant properties. You're not buying the business, mind you. Just the dirt and the building. Glen keeps running his taco operation; you collect rent. Every month. Like clockwork.

This handshake would spawn a $63 billion empire that today owns over 15,000 properties across multiple continents. Welcome to the story of Realty Income Corporation—a company that turned the mundane act of collecting rent into high art, transforming a single Taco Bell into one of the S&P 500's most reliable dividend machines.

The pitch has always been devastatingly simple: "Own real estate, collect rent monthly, never fix a toilet." While other REITs chase headlines with flashy office towers or luxury resorts, Realty Income built its fortress on drugstores, dollar stores, and gas stations—the unsexy, essential retail that Americans visit whether the economy is booming or busting. They didn't just create a real estate company; they engineered a monthly dividend factory that has now paid 658 consecutive monthly dividends and counting. What started as a radical idea—monthly dividends in an era when quarterly was the sacred standard—has evolved into something far more profound. Realty Income today commands a market capitalization of $54.47 billion, making it one of the largest REITs in America. But size alone doesn't capture the essence of what Bill and Joan Clark built. They created a business model so elegant, so resilient, that it has survived the 1970s oil crisis, Black Monday, the dot-com bubble, the Great Financial Crisis, and a global pandemic—all while never missing a monthly dividend payment.

This is not just a story about real estate. It's about how two entrepreneurs recognized a fundamental truth: that America's shift toward franchising and strip-mall retail in the late 1960s created an opportunity to separate property ownership from business operations. It's about building trust with both Wall Street sophisticates and Main Street retirees who depend on that monthly check. And it's about the relentless pursuit of boring—because in the world of commercial real estate, boring is beautiful.

Our journey takes us from that first Taco Bell to today's transcontinental property empire, through billion-dollar mergers, international expansion, and the constant evolution of retail itself. We'll explore how a company founded on leasing to tacos and burgers now owns data centers and European supermarkets, how it turned the triple-net lease from an obscure real estate structure into a wealth-creation machine, and why, after 55 years, the monthly dividend remains not just a financial commitment but a cultural obsession.

II. The Founding Story: Bill & Joan Clark's Vision (1969)

The late 1960s in Southern California was a peculiar moment in American capitalism. The Summer of Love had given way to the Summer of the Moon Landing. Nixon was in the White House. And in the sprawling suburbs of Los Angeles, a quiet revolution was taking place—not in politics or culture, but in hamburgers, tacos, and the very nature of American retail.

William "Bill" Clark wasn't your typical real estate mogul in the making. An entrepreneur with a background in various ventures, he had been watching the explosive growth of franchise restaurants with keen interest. McDonald's had gone public in 1965. Kentucky Fried Chicken was expanding like wildfire. And Glen Bell's Taco Bell, founded just seven years earlier in 1962, was beginning its transformation from a local California curiosity into a national phenomenon.

It was 1969 when Bill and his wife Joan had their fateful meeting with Glen Bell. The location: a Taco Bell in Northridge, California—a suburb in the San Fernando Valley that would later become infamous as the epicenter of the 1994 earthquake. But in 1969, it was simply another piece of Southern California sprawl, perfect for the kind of deal the Clarks had in mind.

Glen Bell needed capital to expand. The franchise model was working, but real estate was expensive, and tying up capital in property meant less money for operations and growth. The Clarks saw an opportunity that others had missed: What if you could own the real estate without operating the business? What if you could provide operators with the capital they needed while securing for yourself a steady, predictable income stream?

The structure they pioneered was elegantly simple. The Clarks would buy the property—the land and the building. Glen Bell's company would sign a long-term lease, typically 15-20 years with renewal options. But here was the twist: unlike traditional commercial leases where the landlord handles maintenance, insurance, and property taxes, this would be a "triple-net" lease. The tenant would handle everything. The Clarks would simply collect rent.

But the real innovation—the stroke of genius that would define Realty Income for the next five decades—was the decision to pay dividends monthly rather than quarterly. In 1969, this was almost unheard of. The entire financial establishment was built around the quarterly cycle: quarterly earnings, quarterly dividends, quarterly reports. Monthly dividends? That was for bonds, not stocks.

Joan Clark later recalled the thinking: "We wanted to create something that felt more like a paycheck than an investment." They understood instinctively what behavioral economists would later prove: that people value regular, predictable income streams far more than sporadic windfalls. A monthly dividend would create a psychological bond with shareholders that quarterly payments never could.

The early years were lean and scrappy. The Clarks operated out of a small office with a handful of employees. They would drive around Southern California, scouting locations, meeting with franchisees, structuring deals one property at a time. Each acquisition was carefully vetted—not just for the real estate value, but for the quality of the operator. They learned quickly that in the triple-net lease business, your tenant is everything. A bad tenant means no rent, regardless of how good the property might be.

By the early 1970s, they had assembled a portfolio of several dozen properties, mostly Taco Bells and other quick-service restaurants. The model was working. Tenants loved the flexibility of not having their capital tied up in real estate. Investors loved the monthly income. And the Clarks had discovered something profound: in an economy increasingly dominated by franchising and chain retail, there was enormous demand for this kind of sale-leaseback financing. What made the Clarks different from the real estate speculators of the 1970s was their fundamental conservatism. In stark contrast to many other companies in the 1970s and 1980s, Realty Income's philosophy was to acquire properties without the use of mortgages. While others were leveraging themselves to the hilt during the real estate boom—taking advantage of tax shelters and depreciation benefits—the Clarks paid cash or used conservative corporate debt. This would prove crucial when the tax laws changed in 1986, decimating leveraged real estate investors while leaving Realty Income unscathed.

The company's growth through the 1970s was methodical rather than meteoric. They expanded from quick-service restaurants into convenience stores, auto service centers, and childcare facilities. Each property was selected not for its speculative value but for the stability of its cash flow. The tenants they sought weren't the hottest concepts or the fastest growers—they were the survivors, the brands with proven business models and strong unit economics.

By 1984, fifteen years after its founding, Realty Income had grown to a portfolio worth several hundred million dollars. The Clarks had proven that their model worked through the inflation of the 1970s, the recession of the early 1980s, and the massive tax law changes that reshaped real estate investing. But they knew that to truly scale their vision—to become the institution they imagined—they would need to access the public markets.

The decision to go public wasn't just about capital. It was about permanence. The Clarks wanted to create something that would outlive them, a company that could deliver those monthly dividends not just for years but for generations. They had built more than a real estate portfolio; they had created a new asset class—the monthly dividend REIT. And in 1994, they would take it to Wall Street.

III. The Triple-Net Lease Model Deep Dive

To understand Realty Income's empire, you must first understand the elegance of the triple-net lease—a structure so simple it seems almost trivial, yet so powerful it has generated hundreds of billions in wealth across the American real estate landscape. Picture a typical lease agreement: thousands of pages of legalese defining who fixes what, who pays for which repair, who handles the landscaping. Now imagine reducing all that complexity to a single principle: the tenant handles everything.

The "triple" in triple-net refers to the three major expense categories that get passed to the tenant: property taxes, insurance, and maintenance. Add in utilities, and you have what amounts to a property owner's dream—all the appreciation potential of real estate ownership with virtually none of the operational headaches. The landlord becomes, in essence, a coupon clipper, collecting rent checks while the tenant handles everything from replacing the roof to mowing the lawn.

But here's where it gets interesting: Why would any tenant agree to this? The answer reveals the genius of the model. For a company like Walgreens or Dollar General, real estate is a necessary evil—crucial for operations but not their core competency. They don't want to be landlords; they want to sell prescriptions and household goods. By entering a triple-net lease, they get several critical benefits: complete control over their space, the ability to customize it exactly to their specifications, and most importantly, predictable occupancy costs that can be budgeted years in advance. For tenants, triple net leases generally provide more freedom to make alterations and customize space without having to make the substantial capital investment of purchasing a property outright. Tenants may also be able to leverage the added financial responsibility to negotiate lower rents. The tenant essentially becomes a quasi-owner, with all the control but none of the capital tied up in real estate ownership.

Consider the math from a retailer's perspective. A CVS pharmacy might generate $3 million in annual revenue from a typical location. The triple-net lease payment might be $300,000 per year—10% of revenue. If CVS had to buy that property, they'd need to deploy $4-5 million in capital. That's capital they can't use to open new stores, develop private label products, or invest in their PBM business. The triple-net lease gives them the location without the capital commitment.

As far as landlords are concerned, triple net leases are a low-risk and reliable source of income that have few overhead costs. The typical tenant in a triple net lease structure is a long-term occupant looking to invest more into its space. This creates a beautiful alignment of interests. The tenant treats the property as if they own it because, functionally, they do—for the term of the lease. The landlord gets predictable, bond-like returns without the hassle of property management.

But Realty Income took this model and refined it to near perfection. They didn't just use triple-net leases; they built an entire investment philosophy around them. First, they focused on "necessity-based" retail—businesses that provide essential goods and services. Even in recessions, people still buy groceries, fill prescriptions, and get their cars serviced. Second, they diversified ruthlessly. No single tenant would represent more than a small percentage of revenue. Third, they insisted on long-term leases with built-in rent escalators—typically 1-2% annual increases or tied to inflation.

The genius of Realty Income's approach becomes clear when you examine their portfolio composition. By focusing on businesses with low e-commerce risk—you can't download a prescription or a tank of gas—they've insulated themselves from the retail apocalypse that has devastated mall-based REITs. Their top tenants read like a who's who of recession-resistant retail: Walgreens, 7-Eleven, Dollar General, FedEx, and CVS.

The typical term for a triple net lease is 10 to 15 years, with built-in contractual rent escalation; some triple net leases can extend for 20 years or longer. This long duration provides Realty Income with remarkable visibility into future cash flows. When you know exactly what rent you'll collect for the next decade, you can make promises about dividends with unusual confidence. And that confidence becomes self-reinforcing: investors trust the dividend, which lowers Realty Income's cost of capital, which allows them to do more deals, which further diversifies the portfolio, which makes the dividend even more secure.

The model also creates interesting dynamics during different economic cycles. In boom times, Realty Income might seem boring—their tenants are paying the same rent whether sales are up 20% or 2%. But in downturns, this becomes a massive advantage. During the 2008 financial crisis, while retailers were struggling, they still paid rent because losing a prime location would be catastrophic for their business. A Walgreens might see same-store sales decline, but they're not walking away from a corner they've spent years establishing as the place to fill prescriptions in that neighborhood.

More recently, because of its high credit rating and access to virtually unlimited low-cost capital, Realty Income was able to make $700 million in acquisitions in 2010, including $269 million in Napa Valley wineries, a new type of property for the company. This ability to pivot into new property types while maintaining the triple-net structure shows the model's flexibility. Whether it's a Taco Bell or a prestigious winery, the fundamental equation remains the same: long-term, predictable cash flows from creditworthy tenants who handle all the property-level hassles.

The triple-net lease isn't just a legal structure for Realty Income—it's a philosophy, a discipline, and ultimately, a competitive moat. While others chase the latest trends or the highest yields, Realty Income has spent 55 years perfecting the art of predictable, growing cash flow. In the next chapter of our story, we'll see how they took this proven model to the public markets, transforming from a private partnership into one of America's most trusted dividend stocks.

IV. Going Public & Scaling the Machine (1994–2010)

In 1994, Realty Income began trading on the New York Stock Exchange under the ticker symbol "O." This landmark event set the stage for even more substantial growth, which included portfolio expansion to thousands of properties and annual revenue growth from $49 million to billions. The choice of ticker symbol was no accident—"O" stood for the circular nature of their business model: collect rent, pay dividends, raise capital, buy more properties, repeat. It was simplicity as brand.

The mid-1990s were a peculiar time to take a REIT public. The industry was still recovering from the real estate collapse of the early 1990s, which had devastated property values and bankrupted numerous developers. REITs were seen as the boring corner of the market—a place for widows and orphans to park money for income, not a growth vehicle. Realty Income's pitch must have seemed almost quaint: We buy strip malls and pay monthly dividends.

But timing, as they say, is everything. The 1990s saw an explosion in "power centers" and big-box retail. Walmart was conquering America one town at a time. Category killers like Home Depot, Best Buy, and PetSmart were redefining retail. And behind all this expansion was an insatiable need for capital-efficient real estate solutions. Realty Income was perfectly positioned to provide exactly that.

The public listing transformed the company's capital-raising capabilities. As a private company, growth was constrained by the Clarks' ability to raise money from banks or private investors. As a public REIT, they could tap the equity markets whenever attractive acquisition opportunities arose. And in the go-go 1990s, those opportunities seemed endless. But here's where the story gets interesting. The NYSE listing under ticker "O"—simplicity as brand—became a marketing masterstroke. Every other REIT had forgettable three or four-letter combinations. Realty Income had a single letter that formed a perfect circle, reinforcing the cyclical, perpetual nature of their business model. It was memorable, distinctive, and subtly communicated completeness.

The company's growth trajectory through the late 1990s was steady rather than spectacular. From 1994 to the second quarter of 2014, Realty Income has grown its property portfolio, in terms of size, by a massive 577%. But this measured pace was intentional. While dot-com millionaires were bidding up tech stocks to absurd valuations, Realty Income kept buying drugstores and convenience stores at 8-9% cap rates. They looked boring, even backward, in an era obsessed with the "new economy."

Then came March 2000. The NASDAQ peaked at 5,048, then proceeded to lose 78% of its value over the next thirty months. Suddenly, boring became beautiful. Investors who had lost fortunes in Pets.com and Webvan discovered the appeal of a company that simply collected rent from 7-Elevens. Realty Income's stock, which had traded sideways through the bubble, suddenly became a safe haven. The monthly dividend, which had seemed quaint during the go-go years, now felt like a life preserver in stormy seas.

The early 2000s brought new challenges and opportunities. Interest rates plummeted as the Federal Reserve fought to revive the post-bubble economy. For REITs, this was a double-edged sword. Lower rates made their dividends more attractive relative to bonds, but also made borrowing cheaper for everyone, increasing competition for properties. Realty Income navigated this by focusing on relationship-based acquisitions rather than auctions. While others fought over properties in bidding wars, Realty Income quietly approached operators directly, offering sale-leaseback financing that freed up capital for expansion.

By 2007, the company had grown to over 2,500 properties and achieved investment-grade credit ratings from all three major agencies. This was a crucial milestone—it meant Realty Income could borrow at rates previously reserved for blue-chip industrials. In the REIT world, where success is often determined by your cost of capital, this was like being handed a loaded weapon in a knife fight.

Then came 2008. The financial crisis that began with subprime mortgages quickly metastasized into a full-blown economic catastrophe. Credit markets froze. Even strong companies couldn't borrow. Retail sales plummeted. Mall REITs saw their stocks fall 70%, 80%, even 90%. Surely this would be the moment when Realty Income's model would crack.

It didn't. Realty Income, on the other hand, increased its annual distributions per share from $1.70 in 2008 to $1.82 in 2012. Though its dividend growth rate slowed during the financial crisis, Realty Income's dividend record goes to show that company management remains committed to remunerating shareholders and to delivering a dependable dividend stream.

The 2008 Financial Crisis playbook that Realty Income executed was a masterclass in countercyclical investing. While other REITs were desperately trying to survive, Realty Income had access to capital when others couldn't. They could borrow through their investment-grade ratings. They could issue equity because investors trusted their dividend. And most importantly, distressed sellers came to them, hat in hand, desperate for capital.

More recently, because of its high credit rating and access to virtually unlimited low-cost capital, Realty Income was able to make $700 million in acquisitions in 2010, including $269 million in Napa Valley wineries, a new type of property for the company. The winery acquisition was particularly clever—here were trophy properties with long-term triple-net leases to creditworthy operators, available at distressed prices simply because the capital markets had seized up.

Completed $1 billion in acquisitions for the first time. This milestone, reached in the aftermath of the crisis, showed how Realty Income had transformed from a small, specialized REIT into a major force in commercial real estate. They were no longer just buying one-off properties; they were doing portfolio deals, sale-leasebacks with major corporations, and even venturing into new property types.

By 2010, Realty Income had emerged from the financial crisis not just intact but stronger. They had proven that their model worked in the worst of times. The monthly dividend had continued uninterrupted. The portfolio had grown. And most importantly, they had built institutional credibility that would serve them well in the decade to come. The boring little REIT that started with a single Taco Bell was now ready to become a consolidator, setting the stage for the transformative mergers that would define its next chapter.

V. The VEREIT Merger: Becoming a Consolidator (2021)

The November morning in 2021 when Realty Income closed its merger with VEREIT marked a watershed moment—not just for the company, but for the entire net lease REIT sector. At $17 billion in enterprise value, it was the largest REIT merger in years, creating a combined entity with an enterprise value of approximately $50 billion. But to understand why this deal mattered, you need to understand VEREIT's tortured history.

VEREIT wasn't always VEREIT. It began life as American Realty Capital Properties, the brainchild of Nicholas Schorsch, a charismatic dealmaker who built an empire on aggressive acquisitions and creative financial engineering. By 2014, ARCP had become one of the largest REITs in America through a series of audacious deals. Then came the accounting scandal—a $23 million "intentional misstatement" that sent the stock plummeting 40% in two days and triggered a cascade of lawsuits, SEC investigations, and the spectacular unraveling of Schorsch's empire.

Enter Glenn Rufrano in 2015. A REIT industry veteran with a reputation for turnarounds, Rufrano was brought in to salvage what remained. He renamed the company VEREIT—a play on "veritas," Latin for truth—and began the painstaking work of rebuilding. "The objective of our management team from initiation in 2015 was to revitalize VEREIT and increase the value of the enterprise," Rufrano would later say. "We put an excellent team in place, enhanced the portfolio, created an investment-grade balance sheet and resolved all legacy issues."

By 2021, Rufrano had largely succeeded. VEREIT owned 3,800 properties, had achieved investment-grade ratings, and had put the scandal behind it. But the company still traded at a discount—the market's memory is long when it comes to accounting fraud. This discount created the opportunity that Sumit Roy, Realty Income's CEO since 2018, had been waiting for.

The deal structure was elegant in its simplicity: VEREIT shareholders will receive 0.705 shares of Realty Income stock for every share of VEREIT stock they own. Relative to Realty Income's 2021 AFFO per share guidance, the transaction is expected to be over 10% accretive to shareholders on an annualized, leverage-neutral basis. This wasn't just financial engineering—it was genuine value creation through scale.

The complementary nature of each company's real estate portfolio resulted in greater diversification of client credit, industry, and geography. VEREIT brought strength in industrial properties and convenience stores—sectors where Realty Income wanted more exposure. The combined portfolio would span over 10,000 properties with no single tenant representing more than 4% of rent.

But perhaps the most innovative aspect of the deal was what happened to the office properties. Both companies owned office assets—a problematic sector even before COVID accelerated remote work trends. Rather than trying to digest these properties, Realty Income spun them off into a new publicly traded REIT called Orion Office REIT. This surgical precision—keeping what fit the model, discarding what didn't—showed a level of discipline rare in mega-mergers.

On a run-rate basis, Realty Income expects to achieve estimated annualized corporate cost synergies of $45-$55 million. These weren't hypothetical "revenue synergies" that never materialize—these were hard cost savings from eliminating duplicate functions, consolidating systems, and leveraging scale in everything from audit fees to insurance costs.

Moreover, our technology and infrastructure investments following the VEREIT merger in 2021 have amplified our efficiency in integrating assets and augmented our capabilities in maximizing the value of our properties. This wasn't the Realty Income of the 1990s, manually tracking properties in spreadsheets. This was a technology-enabled platform capable of ingesting thousands of properties and immediately optimizing everything from insurance procurement to property tax appeals.

The VEREIT merger also brought two important additions to Realty Income's board: Priscilla Almodovar, CEO of Enterprise Community Partners, and Mary Hogan Preusse, a REIT industry veteran with deep capital markets expertise. This wasn't just token board expansion—it was bringing in people who could help guide the company through its next phase of growth.

"We believe the merger with VEREIT will generate immediate earnings accretion and value creation for Realty Income's shareholders while enhancing our ability to execute on our ambitious growth initiatives," said Sumit Roy. "Together, our company will enjoy increased size, scale, and diversification, continuing to distance Realty Income as the leader in the net lease industry."

The market's initial reaction was mixed—Realty Income's stock fell on the announcement, as investors worried about integration risk and the sheer size of the deal. But Roy and his team had a secret weapon: they had just spent the pandemic years building the technology infrastructure to handle exactly this kind of integration. While others were playing defense during COVID, Realty Income was building the systems that would allow them to become the industry's consolidator.

The VEREIT acquisition closed on November 1, 2021, transforming Realty Income from a large REIT into a behemoth—the undisputed king of the net lease sector. But Roy wasn't done. Even as his team was integrating VEREIT's properties, he was already eyeing the next target. The era of consolidation had begun.

VI. The Spirit Realty Acquisition: Doubling Down (2023–2024)

Less than two years after digesting VEREIT, Sumit Roy was at it again. On October 30, 2023, Realty Income announced it would acquire Spirit Realty Capital in an all-stock transaction valued at $9.3 billion. If VEREIT was about proving Realty Income could be a consolidator, Spirit was about demonstrating they could do it repeatedly, efficiently, and at scale.

Spirit Realty Capital wasn't a distressed asset like VEREIT had been. This was a well-run company with a solid portfolio and an excellent management team led by Jackson Hsieh. Since Hsieh had taken over as CEO in 2017, Spirit had dramatically improved its tenant quality, implemented sophisticated analytical tools, and built what many considered one of the best balance sheets in the REIT sector. This wasn't a rescue mission—it was a strategic combination of two healthy companies.

"Since the board appointed me CEO in 2017, our leadership team and dedicated associates have effectuated numerous accomplishments," Hsieh reflected on the deal. "This transaction is the culmination of these accomplishments, and merging with Realty Income offers Spirit's shareholders immediate value by providing a more competitive cost of capital, an A-rated balance sheet, broader tenant diversification, and the ability to leverage economies of scale."

The numbers told a compelling story. Realty Income will acquire Spirit in an all-stock transaction valued at an enterprise value of approximately $9.3 billion. The leverage-neutral transaction is expected to deliver over 2.5% accretion to Realty Income's annualized Adjusted Funds from Operations (AFFO) per share. Additionally, no new external capital is expected to be required to finance the transaction.

But what really made the Spirit deal special was what it revealed about Realty Income's evolution. The merger, once completed, will result in an enterprise value of approximately $63 billion for the combined company, enhancing Realty Income's size, scale, and diversification to expand its runway for future growth. This wasn't just about getting bigger—it was about reaching a scale where Realty Income could compete for deals that simply weren't available to smaller players.

Consider the convenience store portfolio that Spirit brought to the table. These weren't just any convenience stores—they were prime corner locations with long-term leases to operators like 7-Eleven and Circle K. In an era when everyone was worried about e-commerce killing retail, convenience stores were proving remarkably resilient. You can't download a cup of coffee or a tank of gas. These were exactly the kinds of "need-based" retail properties that fit perfectly into Realty Income's investment philosophy.

The Industrial property type is expected to represent 15.1% of annualized contractual rent for the combined portfolio, compared to 13.1% of annualized contractual rent of Realty Income on a standalone basis. This incremental exposure to industrial was crucial. While Realty Income had built its reputation on retail, the explosive growth of e-commerce was creating enormous demand for distribution centers and warehouses. Spirit's industrial portfolio gave Realty Income more exposure to this secular growth trend without abandoning their core retail focus.

Moreover, our technology and infrastructure investments following the VEREIT merger in 2021 have amplified our efficiency in integrating assets and augmented our capabilities in maximizing the value of our properties. What had taken months with VEREIT could now be done in weeks. The company had built what amounted to an acquisition machine—capable of ingesting thousands of properties, immediately identifying optimization opportunities, and seamlessly integrating them into the portfolio.

Why Spirit at that price? The answer lay in the spread between Realty Income's cost of capital and the returns available on Spirit's assets. Earnings accretion is supported by approximately $4.1 billion of existing Spirit debt at a weighted average interest rate of 3.48% and weighted average term to maturity of approximately 4.9 years. Realty Income could refinance this debt at even lower rates, creating immediate value. Meanwhile, Spirit's portfolio was generating cash yields in the 7% range. That spread—between a 3-4% cost of capital and 7% returns—was pure profit.

Creating $50M in annual synergies wasn't just corporate speak. Realty Income had identified specific, actionable cost savings: duplicate corporate functions that could be eliminated, technology systems that could be consolidated, insurance programs that could be combined for better rates. They'd done this dance before with VEREIT and knew exactly where to find the savings.

The playbook was becoming clear: Scale begets lower cost of capital begets more deals. Each acquisition made Realty Income stronger, which lowered their borrowing costs, which made the next acquisition more accretive, which made them even stronger. It was a virtuous cycle that was rapidly transforming Realty Income from a large REIT into the undisputed titan of the net lease sector.

The Spirit deal closed on January 23, 2024, remarkably smooth for a transaction of this size. "We are pleased to announce the completion of our merger with Spirit," Roy announced. "The transaction, which is immediately accretive on a leverage neutral basis, is further evidence of how our unique platform and our position as global consolidator in the fragmented net lease space creates meaningful value for stockholders."

But perhaps most importantly, the Spirit acquisition demonstrated that Realty Income had solved the innovator's dilemma that plagues most mature companies. How do you maintain growth when you're already enormous? The answer: you become the platform that consolidates an entire industry. With over 15,000 properties and a market cap approaching $60 billion, Realty Income wasn't just participating in the net lease sector—they were defining it.

VII. International Expansion & Portfolio Evolution

The boardroom at Realty Income's San Diego headquarters in early 2019 must have been electric with debate. For 50 years, the company had been quintessentially American, focused exclusively on U.S. real estate. Now Sumit Roy was proposing something radical: buying a portfolio of UK supermarkets. Not just any supermarkets—Sainsbury's, one of Britain's most established grocery chains. The leap across the Atlantic would mark a fundamental shift in Realty Income's strategy. In 2019, the company completed a sale-leaseback transaction for 12 properties of the United Kingdom supermarket chain Sainsbury's. This was the company's first purchase of property outside the United States. The £429 million deal wasn't enormous by Realty Income standards, but its significance far exceeded its size. It was a declaration: Realty Income was going global.

"We are excited to announce this strategic transaction, which supplements our robust domestic investment pipeline and represents a natural evolution of the company's strategy," Sumit Roy explained. "We believe that the size of the European net lease market and a need for a large-scale, well-capitalized institutional real estate partner creates a very propitious environment for us to increase our addressable market."

The UK expansion: Testing international waters wasn't without skeptics. Some investors worried about currency risk, regulatory differences, and the complexity of operating across the Atlantic. They pointed to Brexit uncertainty, European economic fragility, and the challenge of managing properties thousands of miles from San Diego. Why complicate a model that was working perfectly well in America?

But Roy and his team saw opportunity where others saw risk. Europe's commercial real estate market is actually larger than that of the U.S., and Realty Income estimates that there is $30 billion-$35 billion per year of single-tenant transaction volume in its target verticals in Europe. The net lease model, so well-established in America, was still relatively nascent in Europe. Large European retailers had massive real estate portfolios tied up on their balance sheets—exactly the situation American retailers had been in decades earlier.

The Sainsbury's properties themselves were exactly what Realty Income looked for: essential retail in prime locations with a creditworthy operator. The sale-leaseback transaction with Sainsbury's is executed at a 5.31% GBP initial cap rate, includes annual rent increases over the duration of the lease term, and carries a weighted average lease term of approximately 15 years. These weren't speculative developments or secondary locations—they were established supermarkets serving communities that had shopped there for generations. The success in the UK emboldened Realty Income to push further into Europe. Continental Europe push: Why now, why these markets became clear in 2021 when they announced expansion into Spain through a partnership with Carrefour, one of the world's largest retailers. The timing was no coincidence—with the VEREIT merger providing additional scale and the European Central Bank maintaining ultra-low interest rates, Realty Income could borrow in euros at historically low rates while acquiring properties at cap rates that still provided attractive spreads.

Expanded into three new European countries and completed a record year of investment volume with approximately $9.5 billion closed, including Realty Income's first investment in the data center vertical. The European expansion wasn't just about geography—it was about relationships. Many of Realty Income's existing tenants, like 7-Eleven and Dollar General's international equivalents, operated across Europe. These companies already knew and trusted Realty Income from their U.S. dealings. When they needed capital in Europe, Realty Income was the natural partner.

But perhaps the most surprising evolution in Realty Income's portfolio came in December 2022: gaming. Increased AFFO per share by 9.2%, achieved property-level occupancy of 99.0% (the highest in over 20 years), & purchased the Wynn Encore Boston Harbor Resort & Casino for $1.7 billion, representing the first investment in the gaming industry.

The Encore Boston Harbor acquisition marked a dramatic departure from Realty Income's traditional focus on necessity-based retail. This wasn't a convenience store or pharmacy—it was a luxury casino resort. But dig deeper, and the deal made perfect sense. Encore held one of only two Class I gaming licenses in Massachusetts, creating an enormous barrier to entry. The property was LEED Platinum certified, had been built just three years earlier at a cost of $2.6 billion, and Realty Income was acquiring it at a discount to replacement cost.

The 30-year triple-net lease with Wynn included favorable annual rent escalators linked to CPI. More importantly, it demonstrated that Realty Income's growth opportunities were unconstrained by industry or property type. If the economics worked and the tenant was creditworthy, Realty Income would do the deal.

Nine months later, they doubled down on gaming, investing $950 million to acquire a 21.9% stake in the Bellagio in Las Vegas. "This transaction to acquire an interest in the Bellagio, an iconic property, represents our second investment in the gaming industry and exemplifies the advantages of our size, scale and access to capital," said Sumit Roy.

Data centers and industrial: Beyond traditional retail represented another frontier. In November 2023, Realty Income entered into a joint venture with Digital Realty to facilitate the development of two build-to-suit data centers in Northern Virginia. The move marked the retail REIT's maiden foray into the data center sector and further diversified its portfolio. They invested approximately $200 million, securing an 80% equity interest in the venture.

The tenant mix evolution: From mom-and-pop to investment grade reflected a fundamental shift in strategy. In the early days, Realty Income would lease to small franchisees—individual Taco Bell operators or local convenience store owners. By 2024, the majority of their rent came from investment-grade corporations. This wasn't abandoning their roots but rather following their tenants as they consolidated and grew.

The international expansion and portfolio evolution demonstrated something crucial about Realty Income: they had become more than just a U.S. retail REIT. They were now a global net lease platform, capable of providing capital solutions to major corporations wherever they operated. The monthly dividend that started with a single Taco Bell in Northridge now flowed from British supermarkets, Spanish hypermarkets, Boston casinos, and Virginia data centers.

As Roy put it: "Because we're not constrained by geography or asset types, I don't see an end to what a company like ours can become in terms of size."

VIII. The Business Model & Competitive Moat

To truly understand Realty Income's competitive moat, imagine trying to replicate what they've built from scratch. You'd need $50+ billion in capital, relationships with hundreds of creditworthy tenants, the operational infrastructure to manage 15,000+ properties, and most crucially, a 55-year track record of never missing a monthly dividend payment. Good luck with that.

Since our public listing in 1994, we have delivered compound average annual total shareholder return of double digits, outperforming the US REIT sector and the S&P 500 during that timeframe. This isn't just beating the market—it's doing so with lower volatility, the holy grail of investing. The company has achieved what every investor dreams of: market-beating returns with bond-like stability.

Scale advantages: Cost of capital, tenant relationships, acquisition pipeline form the foundation of Realty Income's moat. When you're the largest net lease REIT in America, you get first look at deals. Major corporations don't want to negotiate sale-leasebacks with a dozen different landlords—they want one partner who can handle their entire portfolio. When 7-Eleven needs to monetize 400 stores, they call Realty Income. When Walgreens wants to free up capital from 200 locations, they call Realty Income.

This scale translates directly into cost of capital advantages. Realty Income can borrow at rates that smaller REITs can only dream of. Their A- credit rating puts them in rarified air—there are only two REITs that are members of both the S&P 500 and maintain credit ratings of A- or better. This means when Realty Income and a smaller competitor are bidding on the same property, Realty Income can pay more and still generate superior returns because their cost of capital is so much lower.

The monthly dividend as marketing genius and investor lock-in cannot be overstated. Since our founding, we have declared 658 consecutive monthly dividends and are a member of the S&P 500 Dividend Aristocrats index for having increased our dividend for over 30 consecutive years. The monthly payment creates a psychological bond with shareholders that quarterly dividends never could. It feels like a paycheck, not an investment distribution. Retirees plan their budgets around it. Once you're dependent on that monthly check, you're unlikely to sell.

The Dividend Aristocrats designation is particularly powerful. Only 69 companies in the S&P 500 have increased their dividends for 25+ consecutive years. It's a club that includes Coca-Cola, Johnson & Johnson, and Procter & Gamble—companies that have survived and thrived through every conceivable economic environment. For income-focused investors, the Dividend Aristocrats list is the starting point for portfolio construction. Realty Income's inclusion guarantees a steady flow of investment from index funds and income-focused investors.

Relationship-based acquisition model vs. auction processes represents another crucial advantage. While others fight in competitive auctions, driving down returns, Realty Income does negotiated deals directly with operators. They've spent decades building these relationships. When a CFO needs to raise capital quickly and quietly, they don't launch an auction—they call Sumit Roy. These off-market transactions often come at better prices than competitive processes.

Data and analytics: Predictive modeling for acquisitions has become increasingly important. The technology and infrastructure investments following the VEREIT merger amplified their efficiency in integrating assets and augmented their capabilities in maximizing property value. They can analyze thousands of potential acquisitions simultaneously, identifying which ones fit their criteria and projecting returns with remarkable accuracy. This isn't just about spreadsheets—it's about machine learning models trained on decades of proprietary data.

Why others can't easily replicate: Trust, track record, and time form an insurmountable barrier. Trust is earned over decades, not quarters. When Realty Income signs a 20-year lease with Walgreens, both parties know the other will be there for the duration. A startup REIT might offer better terms, but can they guarantee they'll exist in 20 years? Can they weather the next financial crisis? With Realty Income, there's no question.

The company's conservative balance sheet philosophy adds another layer to the moat. They've never been a leveraged player, never reached for yield by taking excessive risk. This conservatism might seem boring during bull markets, but it's precisely what allows them to be aggressive during downturns. When credit markets freeze—and they will freeze again—Realty Income will have access to capital while others are scrambling for survival.

Consider the network effects at play. Every new property makes Realty Income more valuable to potential tenants. A retailer with 100 locations might not want to do a sale-leaseback with a small REIT that owns 50 properties—what happens if that REIT fails? But with Realty Income's 15,000+ properties, the retailer knows their landlord is rock-solid. This attracts more tenants, which attracts more capital, which enables more acquisitions, which attracts more tenants. It's a virtuous cycle that strengthens with each turn.

The regulatory and tax advantages of REIT status, combined with Realty Income's specific structure, create additional moat width. As a REIT, they pay no corporate income tax as long as they distribute 90% of taxable income to shareholders. But unlike mortgage REITs or other specialty REITs that face regulatory restrictions, net lease REITs have tremendous flexibility in what they can own. Realty Income can pivot from retail to industrial to gaming to data centers—whatever offers the best risk-adjusted returns.

Perhaps most importantly, Realty Income has solved the innovator's dilemma that kills most mature companies. Instead of trying to grow by taking more risk or moving into adjacent businesses where they have no advantage, they've become the consolidator of their own industry. Every acquisition makes them stronger, which makes the next acquisition easier, which makes them stronger still. They're not disrupting themselves—they're absorbing the competition.

The beauty of Realty Income's model is its simplicity hiding sophisticated execution. Anyone can understand buying buildings and collecting rent. But doing it at scale, across multiple countries and property types, while maintaining 99% occupancy and never missing a dividend payment—that's the work of masters. They've turned the most boring business model in the world into one of the most successful.

IX. Playbook: Investment & Operating Lessons

Standing in Realty Income's San Diego headquarters, you might notice something unusual for a real estate company: there are no architectural models, no glamour shots of trophy properties, no walls covered with renderings of future developments. Instead, you'll find spreadsheets, analytics dashboards, and charts tracking cap rates across markets. This is a company that treats real estate not as an ego business but as a mathematical exercise in generating predictable cash flows.

The power of boring: Predictable cash flows in essential retail has been Realty Income's north star since day one. While others chase the latest trends—co-working spaces, cannabis dispensaries, axe-throwing venues—Realty Income sticks to businesses that have existed for decades and will exist for decades more. Pharmacies, grocery stores, convenience stores, dollar stores. These aren't sexy businesses, but they're essential. People need prescriptions filled, groceries bought, and gas tanks filled regardless of economic conditions.

This focus on "boring" has profound implications. Essential retail has lower bankruptcy rates, more stable cash flows, and less vulnerability to disruption. A trendy restaurant concept might generate higher rents initially, but what happens when tastes change? A Walgreens might pay lower rent, but they'll be paying it for the next 20 years. In the net lease business, duration matters more than initial yield.

Portfolio theory applied: Diversification across tenants, geographies, industries represents sophisticated financial engineering disguised as common sense. No single tenant represents more than 4% of rent. No single industry more than 11%. Properties spread across all 50 states and eight countries. This isn't diversification for its own sake—it's mathematical risk reduction.

Consider what happens during a regional economic downturn. When oil prices collapsed in 2014-2016, Texas real estate was devastated. But Realty Income, with less than 10% exposure to Texas, barely noticed. When COVID shut down casinos, their gaming properties struggled, but gaming was less than 3% of rent. Every crisis affects some properties, but no crisis affects all properties. This diversification transforms what could be volatile cash flows into something remarkably stable.

Capital allocation discipline: When to issue equity, when to acquire is perhaps the most underappreciated aspect of Realty Income's success. They're not always buying. When cap rates compress and acquisitions become less attractive, they slow down. When their stock trades at a premium, they issue equity. When it trades at a discount, they might buy back shares. This might seem obvious, but most REITs can't help themselves—they're always buying, regardless of price.

The discipline extends to property selection. Realty Income walks away from 98% of the deals they review. They'd rather do nothing than do a bad deal. This patience is excruciating for most management teams, who feel pressure to show "growth" every quarter. But Realty Income's investors aren't looking for growth—they're looking for that monthly dividend. This alignment between corporate strategy and shareholder expectations creates the patience needed for superior long-term returns.

The dividend as North Star: Every decision flows from this commitment. When evaluating an acquisition, the first question isn't "What's the IRR?" or "What's the cap rate?" It's "How does this affect our ability to pay and grow the dividend?" This focus creates remarkable clarity. Speculative developments that might generate higher returns but with more risk? Pass. Properties with uncertain cash flows? Pass. Anything that could jeopardize the dividend? Hard pass.

This dividend focus also drives operational excellence. Property taxes need to be appealed to save money? That flows to the dividend. Insurance costs can be reduced through better procurement? Dividend. Every dollar saved is a dollar that supports dividend growth. It creates a culture of continuous improvement that compounds over decades.

Building for decades, not quarters changes everything about how you run a business. Realty Income doesn't optimize for next quarter's FFO. They optimize for the next decade's cash flows. This means paying slightly more for a property with a better tenant. It means accepting lower initial yields for longer lease terms. It means spending money on technology that won't pay off for years.

This long-term orientation is especially visible in tenant relationships. Realty Income doesn't squeeze every last dollar from lease negotiations. They leave something on the table, ensuring tenants are profitable and happy. A tenant paying 10% below market rent but who never misses a payment and renews for another 20 years is worth far more than a tenant paying market rent who might default or leave.

Managing through cycles: 1980s tax changes, 2008 crisis, COVID-19 reveals the playbook's resilience. Each crisis taught lessons that strengthened the model. The 1986 tax reform that devastated leveraged real estate investors? Realty Income survived because they used minimal leverage. The 2008 financial crisis? They had access to capital when others didn't, enabling opportunistic acquisitions. COVID-19? Their essential retail focus meant most tenants stayed open even during lockdowns.

The key insight: crises are features, not bugs. They're opportunities to demonstrate reliability to investors, to acquire properties from distressed sellers, to strengthen tenant relationships by working through problems together. Every crisis Realty Income survives makes them stronger for the next one.

The value of patient capital in real estate cannot be overstated. Real estate is a slow business. Leases run for decades. Properties appreciate over generations. The temptation is always to juice returns through leverage, through development, through financial engineering. Realty Income resists all of these. They make money the old-fashioned way: buying good properties, leasing them to good tenants, and collecting rent for a very long time.

This patience extends to integration of acquisitions. After buying VEREIT, they took years to fully optimize the portfolio. After acquiring Spirit, they're methodically reviewing each property, each lease, each tenant relationship. There's no rush. The properties aren't going anywhere. Better to do it right than do it fast.

The operational playbook also includes several counterintuitive principles. First, they celebrate not doing deals. In earnings calls, management will proudly announce they reviewed 1,000 properties and bought 20. That 98% rejection rate isn't failure—it's discipline. Second, they invest in capabilities that seem unnecessary. Why does a landlord need sophisticated data analytics? Because at scale, small optimizations generate enormous value. Third, they maintain redundancy and conservative assumptions everywhere. Could they leverage up to 60% debt-to-assets and juice returns? Sure. Will they? Never.

Perhaps the most important lesson: simplicity scales, complexity kills. Every additional complication—every joint venture structure, every development project, every creative financing arrangement—adds potential points of failure. Realty Income's model is ruthlessly simple: own properties, collect rent, pay dividends. This simplicity allows them to scale to 15,000 properties without the organizational complexity crushing them.

The playbook works because it aligns all stakeholders. Tenants get a reliable, well-capitalized landlord. Investors get predictable monthly income. Employees get a stable, growing company with a clear mission. Management gets compensated for long-term value creation, not quarterly earnings beats. When everyone's interests align, magical things happen. A Taco Bell becomes a $50 billion empire. A monthly dividend check becomes a 55-year tradition. And boring becomes beautiful.

X. Bear vs. Bull Case Analysis

Walk into any investment committee meeting discussing Realty Income, and you'll hear the same debate that's been raging for decades. The bears paint a picture of retail apocalypse and rising rates crushing REIT valuations. The bulls counter with talks of essential retail resilience and endless consolidation opportunities. Both sides have merit. Both sides have blind spots. Let's examine each with the cold clarity of data.

Bear Case: The Gathering Storm

E-commerce threat to retail real estate looms largest in bear arguments. The numbers are stark: e-commerce has grown from 5% of retail sales in 2010 to over 15% today. Amazon alone has vaporized entire retail categories. Bears argue that Realty Income's retail-heavy portfolio (still ~80% of rents) is a melting ice cube. Every quarter brings more store closure announcements, more retail bankruptcies, more empty strip malls.

The bear thesis goes deeper than just "Amazon kills everything." They point to specific vulnerabilities in Realty Income's tenant base. Pharmacies like Walgreens and CVS face pressure from mail-order prescriptions and Amazon's pharmacy ambitions. Dollar stores, another major category for Realty Income, face saturation concerns—how many Dollar Generals can America support? Convenience stores face the eventual transition to electric vehicles reducing gas station visits.

Rising interest rates impact on REIT valuations creates mathematical headwinds. REITs are essentially bond substitutes for many investors. When 10-year Treasuries yield 4-5%, why take real estate risk for a 5-6% dividend yield? The math is particularly brutal for Realty Income: A big factor driving this superior yield is its appealingly low valuation -- 13 times funds from operations (FFO), versus 18 for other REITs in the S&P 500. This discount exists for a reason, bears argue—the market is pricing in future challenges.

The interest rate impact goes beyond just relative valuation. Realty Income's cost of capital rises with rates, making acquisitions less accretive. If they're borrowing at 5% to buy properties yielding 6%, that 1% spread doesn't leave much room for error. The aggressive acquisition pace that drove past growth becomes harder to maintain.

Tenant concentration risk in struggling retail sectors deserves scrutiny. Yes, no single tenant exceeds 4% of rent, but sector concentration is real. When you aggregate exposure to struggling retail categories—pharmacies, dollar stores, casual dining—you get to meaningful percentages. A sector-wide crisis, like what happened to department stores, could impact multiple tenants simultaneously.

Limited growth potential at current scale might be the biggest long-term concern. At $50+ billion in enterprise value owning 15,000+ properties, Realty Income needs to deploy billions annually just to move the needle. Where will they find $5-10 billion in attractive acquisitions every year? The law of large numbers suggests growth must slow, and with it, dividend growth.

Bears also point to management's recent moves into non-traditional areas—casinos, data centers, European retail—as evidence that core U.S. retail opportunities are exhausted. These new areas bring new risks: regulatory complexity in gaming, technological obsolescence in data centers, currency risk in international properties. The simple, boring model that worked for 50 years is becoming more complex out of necessity.

Bull Case: The Resilient Giant

Despite its low valuation, Realty Income has consistently delivered better total operational returns -- combining dividend yield and FFO growth -- than its peers, with 9.7% annualized over the past five years compared to 7.7%. This outperformance during a period of supposed retail apocalypse suggests the bears are missing something fundamental.

Essential retail proves remarkably resilient starts with a simple observation: people still shop in stores. Despite e-commerce growth, 85% of retail sales still happen in physical locations. More importantly, Realty Income's tenants operate in categories largely immune to e-commerce. You can't download a prescription (yet). You can't get gas delivered. When you need milk at 10 PM, you go to a convenience store, not Amazon.

The pandemic provided the ultimate stress test. During the worst economic disruption in generations, with forced store closures and consumer panic, Realty Income collected 85% of rents even in the worst months. By late 2020, they achieved property-level occupancy of 99.0% (the highest in over 20 years). If COVID couldn't kill their model, what could?

Platform value for continued consolidation represents enormous opportunity. The net lease sector remains highly fragmented, with thousands of small operators owning handfuls of properties. As these operators face succession issues, regulatory complexity, or capital needs, they sell to Realty Income. The company estimates there's $2+ trillion in net lease real estate in the U.S. alone. At less than 3% market share, Realty Income has decades of consolidation runway.

International expansion runway barely scratched. Europe's net lease market is larger than America's but far less institutionalized. Sale-leaseback transactions, common in the U.S., are just beginning in Europe. Realty Income's relationships with global retailers—many of whom already lease from them in the U.S.—position them perfectly to capture this opportunity. They could deploy $50+ billion in Europe over the next decade without saturating the market.

Inflation protection through rent escalators provides a crucial hedge. Most Realty Income leases include annual rent increases tied to inflation or fixed at 1-2%. As inflation persists, these escalators become increasingly valuable. While bonds lose purchasing power to inflation, Realty Income's rents adjust upward, protecting investors' real returns.

Bulls also emphasize management quality and execution. The successful integration of VEREIT, the smooth acquisition of Spirit, the expansion into Europe—all demonstrate operational excellence. This isn't a REIT coasting on past success but one actively evolving and improving. The investment in technology and analytics positions them to identify and execute opportunities competitors miss.

The Nuanced Reality

The truth, as always, lies between extremes. E-commerce is real, but so is the resilience of essential retail. Interest rates matter, but quality companies trade through rate cycles. Growth will slow, but consolidation opportunities remain vast.

What both bears and bulls might miss is the optionality embedded in Realty Income's platform. They're not just a retail REIT anymore—they're a global net lease platform capable of pivoting to whatever property types offer the best risk-adjusted returns. Today it's convenience stores and dollar stores. Tomorrow it might be data centers and logistics facilities. The platform—the relationships, the capital access, the operational excellence—matters more than the specific properties.

The valuation discount bears cite as evidence of problems might actually represent opportunity. Trading at 13 times FFO versus 18 for REIT peers, with a 30-year track record of dividend growth, suggests the market is too pessimistic. Mean reversion alone could drive substantial returns.

The interest rate argument, while mathematically sound, ignores history. Realty Income has operated through multiple rate cycles, including periods of double-digit rates in the 1980s. They've proven able to create value regardless of the rate environment through disciplined capital allocation and operational excellence.

Perhaps the strongest bull argument is the simplest: for 55 years, betting against Realty Income has been a losing proposition. Every bear thesis—tax reform, e-commerce, COVID—has eventually proven wrong. Not because the challenges weren't real, but because Realty Income adapted, evolved, and emerged stronger.

The bear case assumes the future will be fundamentally different from the past. The bull case assumes it will be fundamentally similar. History suggests the bulls have the better argument, but bears keep the bulls honest, and that tension—between optimism and skepticism—is exactly what makes markets.

XI. Power & Culture

In the corner office of Realty Income's San Diego headquarters sits a man who embodies the evolution of the company itself. Sumit Roy doesn't fit the stereotype of a REIT CEO—no background in real estate development, no family connections to the industry. Instead, he has Bachelor's and Master's degrees in Computer Science and started his career as a technology consultant at Capgemini. This unconventional background would prove to be exactly what Realty Income needed for its next chapter.

The Clarks' lasting influence on company culture remains palpable even decades after their retirement. They established principles that still guide every decision: conservative leverage, monthly dividends, relationship-based business, long-term thinking. Walk the halls and you'll hear employees quote Bill Clark's maxims: "We're not in the real estate business; we're in the dividend business." "Never risk the dividend for growth." "Treat tenants as partners, not adversaries."

But culture isn't frozen in amber. It evolves, and Sumit Roy's evolution from CFO to CEO represents that evolution perfectly. He joined Realty Income in 2011 and was promoted to Chief Investment Officer in 2013. Prior to joining the Company, Mr. Roy was an Executive Director at UBS Investment Bank where he worked for seven years. During his tenure at UBS, he was responsible for more than $57 billion in real estate capital markets and advisory transactions.

This Wall Street pedigree might seem at odds with Realty Income's Midwestern values, but Roy understood something crucial: the company needed to evolve without abandoning its core. He brought analytical rigor and technological sophistication while maintaining the fundamental conservatism that defined the company. "We process information through predictive analytics and machine learning to drive key business decisions," Roy explains, showing how technology enhances rather than replaces traditional real estate judgment.

Conservative Midwest values in a California company creates an interesting cultural dynamic. Despite being headquartered in San Diego, Realty Income feels more like a company from Omaha or Cincinnati. There's no Silicon Valley flash, no Hollywood glamour. Employees dress business casual, not because it's policy but because ostentation feels wrong. The highest-paid executive makes a fraction of what tech CEOs earn. Success is measured in decades, not quarters.

This conservatism extends to every aspect of operations. While other REITs leverage up to juice returns, Realty Income maintains fortress-like balance sheet strength. While competitors chase the latest trends, Realty Income sticks to what works. While others make bold predictions, Realty Income under-promises and over-delivers. It's a culture that prizes reliability over brilliance, consistency over creativity.

Building trust with retail operators over decades has created a unique competitive advantage. When Roy visits a major retailer's headquarters, he's not starting from scratch. The relationship might go back 20, 30, even 40 years. Multiple generations of executives on both sides have worked together. This isn't just business—it's institutional memory, shared history, mutual success.

Consider the relationship with 7-Eleven. Realty Income has been their landlord for decades, through multiple ownership changes, strategic pivots, and economic cycles. When 7-Eleven needs to quickly monetize stores for an acquisition, they don't shop the deal—they call Sumit Roy directly. This relationship is worth billions in deal flow, and it can't be replicated with money alone. It requires time, trust, and a track record of fair dealing.

The monthly dividend as cultural commitment goes beyond financial policy—it's an organizing principle. Every employee understands that their ultimate job is to support that monthly payment. The acquisitions team doesn't celebrate closing deals; they celebrate deals that enhance dividend stability. The asset management team doesn't optimize for maximum rent; they optimize for sustainable rent. The entire organization aligns around a single, measurable objective: pay and grow the dividend.

This clarity creates remarkable cultural cohesion. There's no confusion about priorities, no competing objectives. When faced with a decision, employees ask: "Does this help or hurt the dividend?" It's a North Star that guides everything from multi-billion-dollar acquisitions to routine maintenance decisions.

Balance sheet conservatism as competitive advantage might seem paradoxical—how can being conservative create advantage? But in real estate, survival is the ultimate competitive advantage. Every crisis wipes out leveraged players, creating opportunities for the survivors. Realty Income's conservative culture ensures they're always among the survivors.

Roy has built on this foundation while adapting to modern realities. Data-Driven Strategy: Sumit Roy's vision for Realty Income puts technology at the forefront through predictive analytics and machine learning. The company uses data from external sources and its 15,600-property portfolio to project industry trends. This isn't abandoning the old culture but enhancing it with new capabilities.

The integration of VEREIT and Spirit revealed another cultural strength: the ability to absorb and transform other organizations. Rather than imposing Realty Income's culture through mandate, they lead by example. VEREIT employees saw how Realty Income operated—the analytical rigor, the long-term thinking, the tenant focus—and naturally adopted these practices. Culture spread through osmosis rather than edict.

Roy's leadership style reflects this cultural evolution. He's equally comfortable discussing cap rates with Wall Street analysts and touring properties with local managers. He maintains Bill Clark's open-door policy while bringing modern management practices. He respects the company's history while pushing toward its future. "Realty Income's ability to consistently deliver monthly dividends that increase over time is proof of the dynamic platform we have built," Roy emphasized, showing how tradition and innovation can coexist.

The power dynamics within Realty Income are surprisingly flat for a $50+ billion company. Yes, there's a hierarchy, but ideas can come from anywhere. A junior analyst who identifies a portfolio opportunity gets the same hearing as a senior executive. This meritocracy of ideas ensures the best thinking rises to the top, regardless of source.

External power dynamics are more complex. Realty Income's size gives them enormous leverage in negotiations, but they rarely use it aggressively. They understand that squeezing the last dollar from a deal might win the battle but lose the war. Better to leave something on the table and maintain the relationship for future deals. This restraint—this voluntary limitation of power—paradoxically increases their power by making them the preferred partner for large transactions.

The board composition reflects this balance of continuity and change. Long-serving directors who knew the Clarks serve alongside newcomers with expertise in technology, international markets, and modern governance. This mix ensures institutional memory while preventing staleness. The recent additions from the VEREIT and Spirit mergers brought fresh perspectives while respecting existing culture.

Perhaps most tellingly, Realty Income has avoided the cultural pitfalls that doom many successful companies. They haven't become arrogant despite their success. They haven't become complacent despite their market position. They haven't become rigid despite their size. The culture remains hungry, humble, and adaptable—a rare combination in a company with a 55-year history.

The ultimate test of culture is crisis, and Realty Income has passed every test. During COVID, when retail tenants were struggling, Realty Income worked with them rather than against them. They offered deferrals, modifications, and support. Not because they had to, but because it was the right thing to do. This approach—firm but fair, principled but practical—defines the Realty Income way.

As Roy looks toward the future, the cultural challenge is maintaining this balance as the company globalizes and diversifies. How do you preserve Midwestern values while operating in London and Madrid? How do you maintain simplicity while adding complexity? How do you stay humble while becoming dominant? These aren't easy questions, but Realty Income's track record suggests they'll find answers, just as they always have.

XII. Recent Developments & Future Outlook

Standing at the beginning of 2025, Realty Income isn't the same company that entered the decade. With current market position: 15,600+ properties across 50 states and Europe, they've transformed from a large U.S. retail REIT into a global net lease platform. The numbers tell part of the story—$63 billion enterprise value, presence in eight countries, expansion into gaming and data centers. But the real story is about capability, not just scale.

The integration of artificial intelligence and machine learning into property selection represents a quantum leap from the days of driving around Southern California looking for Taco Bells. Realty Income now processes millions of data points daily—foot traffic patterns, demographic shifts, competitive dynamics, lease comparables. Their models can predict with startling accuracy which properties will outperform, which tenants might struggle, which markets offer the best risk-adjusted returns.

But this isn't technology for technology's sake. Every algorithmic insight gets vetted by human judgment. The machine might identify an opportunity, but experienced real estate professionals make the final call. This hybrid approach—combining Silicon Valley capabilities with old-school real estate wisdom—gives Realty Income an edge that neither pure tech players nor traditional REITs can match.

Climate change and property resilience has moved from theoretical concern to operational reality. Realty Income now evaluates every acquisition for climate risk—flood zones, wildfire exposure, hurricane paths. They're retrofitting properties with resilient systems, negotiating green leases with sustainability requirements, and even investing in renewable energy projects at select properties. This isn't environmental activism; it's risk management. Properties that can't withstand climate impacts won't generate reliable cash flows for 20-year leases.

The future of retail: Experience, convenience, last-mile continues to evolve in ways that actually benefit Realty Income. The death of retail was greatly exaggerated. Instead, retail is bifurcating. Experiential retail—places you go for entertainment, dining, services—is thriving. Convenience retail—quick trips for immediate needs—remains essential. And last-mile logistics—the final step in e-commerce delivery—requires physical locations close to consumers.

Realty Income's portfolio aligns perfectly with these trends. Their properties aren't enclosed malls or department stores—the real casualties of e-commerce. They're convenience stores that serve as pickup points, pharmacies that provide healthcare services, dollar stores that offer value shopping experiences. Even their industrial properties often serve last-mile logistics functions. They're not fighting e-commerce; they're complementing it.

Potential new verticals: Healthcare, infrastructure, alternative assets represent the next frontier. Healthcare real estate—medical offices, urgent care centers, specialized treatment facilities—offers similar characteristics to Realty Income's existing portfolio: essential services, stable cash flows, long-term leases. The aging population ensures growing demand. Infrastructure—cell towers, renewable energy, transportation assets—provides inflation-protected returns with high barriers to entry.

The most intriguing possibility might be alternative assets that don't fit traditional categories. Realty Income's gaming investments proved they could evaluate any asset that generates predictable cash flows. Could they buy movie theaters with percentage rent components? Cannabis dispensaries as they become federally legal? Electric vehicle charging stations with utility-like returns? The platform they've built can evaluate and manage almost any income-producing asset.

Recent developments show this evolution in action. The partnership with Digital Realty for data centers. The acquisition of European logistics facilities. The exploration of sale-leaseback opportunities with technology companies needing to monetize real estate. Each move expands the aperture of what Realty Income can be while maintaining the discipline of what it must be—a reliable generator of monthly dividends.

The macroeconomic environment presents both challenges and opportunities. Higher interest rates increase Realty Income's cost of capital but also reduce competition from leveraged buyers. Inflation pushes up expenses but triggers rent escalators in many leases. Economic uncertainty might reduce acquisition volumes but creates opportunities to buy from distressed sellers.

Management's recent commentary suggests quiet confidence. They're not chasing growth at any price. They're not making bold predictions. They're doing what Realty Income always does—methodically executing, carefully acquiring, reliably paying dividends. The guidance for 2025 suggests mid-single-digit AFFO growth, consistent with long-term averages. No moonshots, no surprises, just steady execution.

The competitive landscape continues to evolve. New entrants, attracted by Realty Income's success, are raising capital for net lease strategies. Private equity firms are aggregating properties. International players are entering the U.S. market. But competition isn't necessarily bad for Realty Income. It validates the model, creates acquisition opportunities when competitors fail, and highlights Realty Income's advantages in scale, cost of capital, and execution.

The international expansion story is just beginning. Europe represents a multi-decade opportunity as sale-leaseback transactions become more common. Asia, still largely closed to foreign real estate investment, might eventually open. Even within existing markets, Realty Income has barely scratched the surface. They could deploy $100 billion internationally over the next decade without approaching market saturation.

Technology investments continue to compound. The systems built for the VEREIT integration now handle routine acquisitions. The analytics developed for U.S. properties are being applied internationally. The machine learning models get smarter with every transaction. This technological infrastructure represents a hidden asset not reflected on the balance sheet but crucial for future growth.

The most important recent development might be the least visible: the institutionalization of excellence. Realty Income no longer depends on any single person or small group. The systems, processes, and culture can perpetuate themselves. New employees are trained in the Realty Income way. Best practices are documented and refined. Institutional knowledge is preserved and transmitted. This organizational capability ensures Realty Income can thrive for another 55 years.