W. P. Carey: The Pioneer of Net Lease REITs

I. Introduction & Episode Roadmap

In the glass-and-steel towers of Manhattan, where billion-dollar deals are forged and forgotten daily, one company has spent over half a century perfecting a remarkably simple concept: owning real estate that tenants never want to leave. W. P. Carey Inc. is a diversified net lease real estate investment trust (REIT) specializing in the acquisition, ownership, and management of single-tenant commercial properties leased to tenants under long-term triple-net (NNN) agreements, where tenants bear most operating expenses such as taxes, insurance, and maintenance.

As of December 31, 2024, W. P. Carey ranks among the largest net lease REITs with a well-diversified portfolio of high-quality, operationally critical commercial real estate, which includes 1,555 net lease properties covering approximately 176 million square feet and a portfolio of 78 self-storage operating properties.

The central question animating this deep dive is deceptively simple: How did a man who rented refrigerators to Princeton classmates build a $24 billion real estate empire? The answer involves pioneering financial innovations, a model that survived the IRS crackdown on tax shelters, and a dramatic 2023 decision to exit an entire property sector that redefined the company's future.

Throughout its history, the company has gone through different stages on its journey from a small, privately held investment management firm to a $24 billion publicly traded REIT. What makes W. P. Carey particularly fascinating is how its evolution mirrors the transformation of American finance itself—from private partnerships to publicly traded vehicles, from domestic to global, from asset management to pure-play real estate ownership.

Approximately 61% of the company's revenue is derived in the United States and 33% in Europe. The company was founded in 1973 by William P. Carey. Unlike its net lease peers who concentrate on retail (Realty Income) or U.S.-only retail (NNN REIT), W. P. Carey has built something different—a globally diversified platform that invests across industrial, warehouse, retail, and formerly office properties.

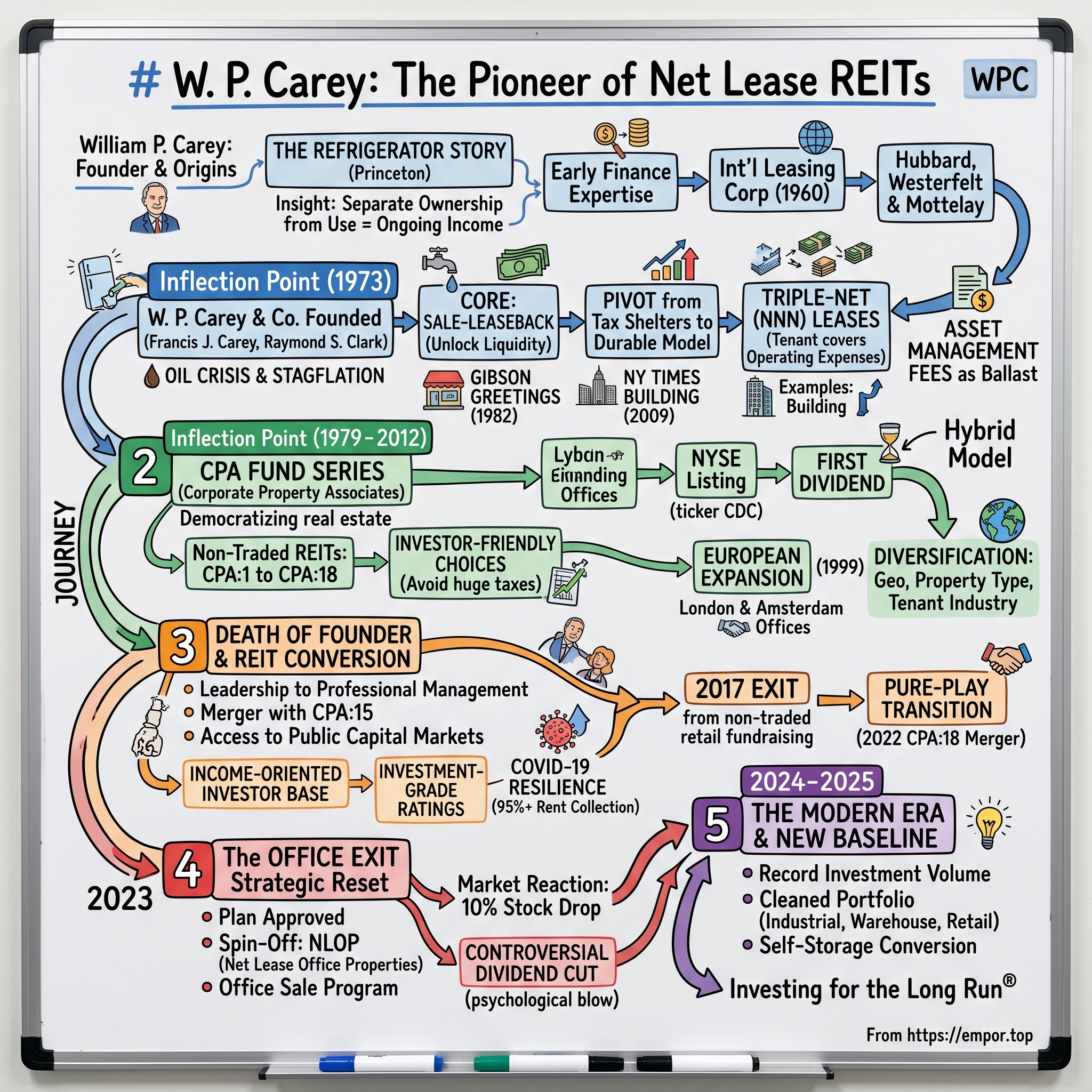

The story traces through five major inflection points: the founding vision of pooled net lease investing (1973), the creation of the CPA fund series that democratized institutional real estate for retail investors (1979-2012), the REIT conversion that marked a founder's death and a company's rebirth (2012), the completion of the pure-play transition through CPA mergers (2017-2022), and the controversial 2023 office exit that divided investors and reset the company's baseline. Each decision reveals something fundamental about how patient capital, creative structuring, and willingness to evolve can compound across decades.

II. The Founder: William Polk Carey & His Origins

William Polk Carey (May 11, 1930 – January 2, 2012) was an American philanthropist and businessman. To understand W. P. Carey the company, you must first understand Bill Carey the man—a child of the Depression who never forgot what scarcity felt like and built an empire predicated on the opposite principle: generating steady, reliable income for investors who couldn't afford to lose.

Carey's interest in business emerged early when, as a child of the Depression, he sold ink he made in the basement of his family's Baltimore home. This wasn't idle childhood play—it was practical economics. He attended top schools, including Gilman School, the first country day school in America, founded by Carey's grandmother in 1897, and Pomfret School, often mixing school activities with work. He recalled selling soda on the streets of Baltimore: "I tried to buy wholesale and sell retail, whenever possible," he said.

The Carey lineage reads like American aristocracy. Carey was a direct descendant of James F. Polk, the 11th President of the United States, and the great-great-great-grandson of Quaker abolitionist James Carey. His grandmother, Anne Galbraith Carey, founded the Gilman School. His grandfather, Francis King Carey, was a successful lawyer who sat on government committees arguing for compulsory health insurance. But growing up during the Depression meant that legacy alone wouldn't pay the bills.

The Refrigerator Story That Launched Everything

When he arrived at Princeton University to begin his freshman year, he soon discovered he owned something many of his schoolmates did not—a small dorm room refrigerator. Seeing an opportunity, he purchased as many refrigerators as he could afford and leased them to his schoolmates for a small fee. By the end of his sophomore year, he had made over $10,000.

Think about that number in context. In 1949 dollars, $10,000 represented roughly $125,000 in today's purchasing power—earned by a college sophomore leasing appliances. The genius wasn't the refrigerators themselves; it was recognizing that people would pay for ongoing access to an asset rather than tying up capital to own it outright. This insight—that separation of ownership from use could benefit both parties—would become the philosophical foundation of his entire career.

The venture was profitable, but left him with little time for chapel or classes. He withdrew from Princeton, then enrolled in the Wharton School of Business at the University of Pennsylvania, where he earned a bachelor's degree in economics in 1953. After serving two years in the U.S. Air Force, rising to the rank of lieutenant, he joined his stepfather's auto dealership in New Jersey, where he learned about lease financing.

Building Expertise Across Wall Street

Following graduation, he entered the U.S. Air Force for two years and by age 28, started International Leasing Corporation, which specialized in foreign cars. Soon he was also arranging private placements of corporate debt and leased vehicle fleets, aircraft and factories. A globalist from the start, Carey completed his first international transaction in 1960, with the first-ever foreign direct investment in Australia.

That 1960 Australian transaction is worth pausing on. At a time when most American businessmen viewed "international" as meaning Canada or perhaps Mexico, Carey was structuring deals on the other side of the world. This global perspective would later distinguish W. P. Carey from domestic-only competitors.

In 1964, International Leasing merged into Hubbard, Westerfelt & Mottelay (later Merrill Lynch), where he focused on the net leasing of corporate real estate. He went on to serve as Head of Real Estate and Equipment Financing at Loeb, Rhodes & Co. (later part of Lehman Brothers) and became Vice Chairman of the Investment Banking Board and Director of Corporate Finance at DuPont Glore Forgan. After nearly a decade of working for other firms, he decided the time was right to again become his own boss.

In 1973, he resigned and at the age of 43 faced a crossroads in his life. According to a speech he delivered to the Newcomen Society, "I was being wooed by Lazard Freres, among others. I was quite content to be part of a large organization—the opportunities real and challenging, the compensation appropriate and the atmosphere congenial. But I despised the office politics that big, competitive operations often breed, and I hadn't forgotten the pleasures of being the boss."

At 43, Carey chose entrepreneurship over prestige. He'd spend the next four decades proving that decision right.

III. The Founding Vision: W. P. Carey & Co. (1973)

In 1973, he formed the real estate investment firm W. P. Carey & Co., along with his brother, Francis J. Carey, and brother-in-law, Raymond S. Clark. The company was founded during one of the worst periods for the U.S. economy—the 1973 oil crisis, stagflation, and a stock market that would lose nearly half its value over the next two years. It was a terrible time to start a business, and perhaps the perfect time to start this business.

Founded in 1973 by William Polk Carey, the firm initially concentrated on delivering long-term capital to businesses through sale-leaseback transactions, allowing companies to unlock liquidity from their real estate assets without disrupting operations.

The Early Tax Shelter Era—and the Pivot That Saved the Company

During the first years of its existence, W.P. Carey focused on lease-back ventures which served more as tax shelters than revenue producers. Although many high-flying firms were engaged in the same activity, Carey quickly grew wary of these tax-advantaged transactions.

This wariness proved prescient. When the Tax Reform Act of 1986 eliminated most real estate tax shelters, it devastated firms that had built their entire business model around them. By then, W. P. Carey had already pivoted to something more durable.

The company turned to real estate limited partnerships (RELPs) in 1979, launching CPA:1, the first in a series of Corporate Property Associates investment funds. Only later, when the Tax Reform Act of 1986 made it more attractive, would W.P. Carey turn to real estate investment trust (REIT) funds.

The Survival Insight: Asset Management Fees as Ballast

Building a business that makes money only when deals close is a precarious existence. Carey recognized this early and built a structure that could survive dry periods. The asset management business—earning fees for managing the properties in CPA funds—provided steady income regardless of transaction volume. This "recurring revenue before it was cool" approach gave the firm runway when deals took time to materialize.

Self-Governance Against Self-Interest

Perhaps the most revealing insight into Carey's character came from how he structured governance. The company created an independent investment committee to approve all acquisitions. Carey's explanation was bracingly honest: "Basically, I set it up because I'm a deal man, and I wanted to protect myself against myself."

This admission—that a successful dealmaker recognized his own potential for overenthusiasm—demonstrated the kind of self-awareness that separates long-term survivors from flame-outs in the real estate industry. It also established a culture of institutional discipline that would outlast the founder.

The company started small, operating from 67 Wall Street in New York, with the primary business of structuring single-asset private placements. But Carey recognized that net lease investment partnerships could offer substantial benefits for income-oriented individual investors—people who wanted real estate exposure but couldn't buy warehouses themselves. This democratization of institutional real estate would become the company's defining contribution.

IV. The Net Lease Innovation: How the Business Model Works

To understand W. P. Carey's durability, you must understand triple-net leases—the contractual structure that makes the entire business model work.

Explaining Triple Net (NNN) Leases

The REITs focus on owning freestanding properties secured by long-term net leases. That lease structure requires tenants to cover all of a property's operating costs, including routine maintenance, real estate taxes, and building insurance.

In a traditional lease, the landlord worries about property taxes rising, the roof leaking, and insurance premiums increasing. In a triple-net lease, those are the tenant's problems. The landlord receives "net" rent—pure income without operating headaches. Because of that, the REITs generate very low volatility cash flow that tends to rise steadily each year as lease rates escalate.

Sale-Leaseback: The Core Transaction

In a sale-leaseback, a company sells its real estate to an investor like W. P. Carey for cash and simultaneously enters into a long-term lease. In doing so, the company extracts 100% of the property's value and converts an otherwise illiquid asset into working capital to reinvest in its business or pay down debt, while maintaining operational control.

Consider the economics from the tenant's perspective. A manufacturing company might have $50 million tied up in its factory—capital that earns nothing except appreciation (maybe) while the business could deploy it to build new products, enter new markets, or pay down debt. Through a sale-leaseback, the company gets $50 million in cash, continues operating in the same building, and converts an ownership cost into a predictable lease expense.

The Gibson Greetings Deal: Where LBOs Meet Real Estate

In the early 1980s, the company was innovative in the use of leaseback transactions to acquire properties. In 1982, the company acquired three Gibson manufacturing and warehouse buildings from Wesray Capital Corporation.

This transaction was historically significant. In January 1982, Simon, Chambers, and a group of other investors acquired Gibson Greetings, a producer of greeting cards. The purchase price for Gibson was $80 million, of which only $1 million was rumored to have been contributed by the investors. The Gibson Greetings LBO is often cited as one of the deals that launched the modern private equity industry. W. P. Carey's role—providing the sale-leaseback financing that helped make the deal possible—demonstrated how net lease capital could complement leveraged buyouts.

The New York Times Building: High-Profile Validation

By January 2009, the Times was negotiating to sell the nineteen stories that it occupied, the 2nd through 21st stories, to W. P. Carey for $225 million. In exchange, the Times would lease back its floors for $24 million a year for 10 years. The leaseback was finalized in March 2009.

When the deal was made, the Times was in the midst of extricating itself from $1 billion in debt, and W.P. Carey had characterized its purchase as a loan, rather than a real estate investment.

This framing—a loan rather than a real estate investment—reveals how sophisticated sale-leasebacks truly are. The Times needed liquidity during a moment of existential crisis for the newspaper industry. W. P. Carey provided it, secured by the company's headquarters in one of the most valuable real estate markets on Earth. The Times exercised its option on the leasehold in late 2019 for $245 million. W. P. Carey earned a spread on its capital for a decade while holding a trophy asset as collateral.

Major Corporate Clients

Major corporations engaged in such leasing arrangements with W.P. Carey include Federal Express, Wal-Mart, and PETsMART, Inc. In addition, W.P. Carey works closely with private equity firms seeking to optimize the capital structure of their portfolio companies through the sale-leaseback of owned real estate.

The private equity angle became increasingly important. As leveraged buyouts proliferated from the 1980s onward, PE sponsors discovered that sale-leasebacks could reduce equity requirements for acquisitions, improve returns on invested capital, and provide portfolio companies with operational flexibility. W. P. Carey became a preferred partner for this capital.

V. Building the CPA Empire: The Non-Traded REIT Era (1979–2012)

The Corporate Property Associates (CPA) fund series represents one of the most successful investor-friendly structures in real estate history. Starting with CPA:1 in 1979 and continuing through CPA:18, these funds provided individual investors access to institutional-quality real estate with professional management.

The Tax Shelter Exit and the Birth of CPA:1

The timing was perfect. As tax shelter deals became increasingly aggressive industry-wide, Carey saw the writing on the wall. The shift to real estate limited partnerships in 1979 positioned W. P. Carey to survive the 1986 Tax Reform Act that destroyed competitors. CPA:1, with approximately $20 million in capital, was designed to provide consistent returns for investors, with the only tax shelter component being depreciation.

Growth Through the Fund Series

W.P. Carey launched CPA:11 in 1991, later called Carey Institutional Properties (CIP), because of its attractiveness to institutional investors. By 1994, the firm topped the $1 billion mark in assets under its management. That amount would surpass $2 billion in 1997.

By 2010, assets under management had reached approximately $9.7 billion, reflecting the company's maturing platform and investor appeal.

The Investor-Friendly Dilemma

As the early CPA funds matured, Carey faced a decision that would define his relationship with investors. According to Carey, the firm faced a dilemma: "If we simply dissolved the funds and sold the assets, our investors—whose support and goodwill we had labored so tirelessly to earn and keep—would be saddled with huge, immediate taxes on $350 million in capital gains, just because we had been so successful. Many real estate operators were doing just that." He said: "It wasn't easy, but we found a way for our investors to have their cake and eat it, too. In January 1998, with the overwhelming consent of the investors, we consolidated the first nine funds in the series, CPAs 1 through 9, into Carey Diversified, a Limited Liability Company headed by Frank Carey, which we immediately listed on the New York Stock Exchange." Because investors could swap their partnership interest for shares in the new company they not only avoided capital gains taxes, they were now in a position to achieve instant liquidity and decide for themselves when they wanted to realize capital gains.

This decision—choosing a more complex but investor-friendly path over the simple but taxable approach—built tremendous goodwill. It also demonstrated that W. P. Carey viewed investors as long-term partners rather than sources of capital to be exploited.

The Non-Traded REIT Model

Non-traded REITs occupy a peculiar niche in the investment landscape. Unlike publicly traded REITs, their shares don't trade on exchanges, providing stability (no daily price fluctuations) at the cost of liquidity (you can't sell easily). For income-focused investors who didn't need immediate access to their capital, this tradeoff was attractive.

The most recent one was its official exit from the non-listed REIT space in 2022 when it completed a $2.2 billion merger with CPA®:18, one of numerous investment funds the company began issuing in 1979 for individual investors.

The CPA fund series created a virtuous cycle: successful track record attracted new investors, new capital allowed for more acquisitions, more acquisitions generated fees for the management company, and growing assets under management made the platform more attractive to institutional partners.

VI. Going Public: The 1998 NYSE Listing

On January 21, 1998, Carey Diversified LLC—the consolidation of Corporate Property Associates 1-9 which would later merge with W. P. Carey & Co to become W. P. Carey—began trading on the New York Stock Exchange under the ticker symbol "CDC" (now "WPC"). When the company started trading, it had a portfolio of 198 properties in 37 states. This milestone made W. P. Carey accessible to all investors and broadened the company's opportunities for future capital. It was also the year W. P. Carey issued its first dividend, laying the foundation for its reputation today as a reliable income-producing stock.

The Hybrid Model

The 1998 listing created a unique structure: a publicly traded entity that both owned real estate directly and managed non-traded REIT funds. This hybrid model provided multiple revenue streams—lease income from owned properties plus management fees from administered funds—while also creating potential conflicts of interest that would eventually need resolution.

The next step in the evolution of the firm came in June 2000 when its management company, W.P. Carey & Co., Inc., was merged with Carey Diversified LLC to form W.P. Carey & Co. LLC. The result was a fully integrated investment company—the nation's largest net lease firm and the world's largest publicly traded LLC, which was subsequently listed on the New York Stock Exchange and the Pacific Exchange. Not only did shareholders in the company enjoy the consistent returns of Carey Diversified's net lease operations, they also benefited from the asset management business, which included the newer CPA series of REITs.

Building the Dividend Reputation

The first dividend payment in 1998 began a streak that would become central to the company's identity. Income-oriented investors gravitated toward W. P. Carey precisely because of its consistent, growing distributions. This reputation took decades to build and would face its severest test in 2023.

VII. European Expansion & Diversification (1999–2012)

In 1999, W. P. Carey expanded into Europe with the opening of its London office. This launched a whole new avenue of investment opportunities and reinforced the company's commitment to diversification—now across geography, in addition to property type and tenant industry.

The European expansion wasn't just about finding new deals—it was about risk management through geographic diversification. Economic cycles don't perfectly correlate across continents. A recession in the United States might coincide with stability in Germany, and vice versa. By spreading investments across regions, W. P. Carey reduced its vulnerability to any single economy.

The European Net Lease Opportunity

While the sale-leaseback model is prevalent in the U.S., the trend is less pronounced in Europe. While acceptance has increased since W. P. Carey helped launch the sale-leaseback model there in 1998, Europe still has a much higher percentage of corporate or commercial real estate that's owned and occupied by the user.

This underpenetration represented opportunity. European corporations, like their American counterparts, could benefit from unlocking capital tied up in real estate. W. P. Carey became a leading educator and practitioner of sale-leasebacks in European markets.

LLC pursued aggressive growth, acquiring hundreds of properties worldwide and diversifying beyond office and warehouse assets into industrial and retail sectors to mitigate risk and broaden revenue streams. This expansion included significant sale-leaseback transactions with corporate tenants, growing the managed portfolio's scale and geographic footprint.

The Amsterdam office opening further deepened the European footprint, providing local presence in one of the continent's major logistics hubs and financial centers.

VIII. Inflection Point #1: Death of the Founder & REIT Conversion (2012)

Following the death of founder William P. Carey on January 2, 2012, W. P. Carey Inc. underwent a leadership transition to professional management, culminating in the appointment of Jason E. Fox as Chief Executive Officer effective January 1, 2018.

Bill Carey's death at 81 marked the end of an era, but the company he built was designed to outlast him. The governance structures, the investment discipline, the diversification philosophy—all were institutionalized in ways that didn't depend on one person's presence.

The REIT Conversion

On September 28, 2012, W. P. Carey converted to a Real Estate Investment Trust. Somewhat limited by its existing structure, the REIT conversion helped increase the company's visibility and expanded its access to institutional capital. As a result, W. P. Carey was able to significantly increase the size of its portfolio, grow dividends and diversify its shareholder base with both active and passive REIT investors. In 2014, the company completed its inaugural public equity and US bond offerings and received investment-grade ratings from Moody's and S&P.

A landmark consolidation in September 2012 involved the merger of W. P. Carey & Co. LLC with CPA:15, creating W. P. Carey Inc. as an internally managed real estate investment trust listed on the NYSE under the ticker WPC, which unified the remaining CPA programs and improved operational efficiency through centralized management and access to public capital markets.

Under the terms of the proposed merger, CPA®:15 stockholders received $1.25 in cash and 0.2326 of a share of W.P Carey common stock for each CPA®:15 share at closing. The transaction valued CPA®:15 at $2.6 billion, including the assumption of CPA®:15 debt of $1.2 billion.

The Strategic Rationale

Upon completion of the transactions, W. P. Carey Inc. will have a total market capitalization of approximately $5 billion and a portfolio of over 39 million square feet of corporate real estate leased to over 130 companies around the world.

The REIT conversion served multiple purposes: - REIT Index Inclusion: Automatic buying from passive funds tracking REIT indices - Analyst Coverage: More research coverage meant greater visibility to institutional investors - Tax Efficiency: REITs pass through income without corporate-level taxation - Comparability: Investors could now benchmark W. P. Carey against peers like Realty Income and NNN REIT

Leadership Transition

Following the death of founder William P. Carey on January 2, 2012, W. P. Carey Inc. underwent a leadership transition to professional management, culminating in the appointment of Jason E. Fox as Chief Executive Officer effective January 1, 2018. Fox, who had joined the company in 2002 and previously served as Global Head of Investments and President, led the firm through a period of strategic refinement in its net lease operations.

Fox's ascension represented continuity—he'd been with the company for 16 years before becoming CEO and understood its culture, relationships, and investment philosophy deeply. This wasn't an outsider brought in to "shake things up" but an insider positioned to preserve what worked while adapting to new realities.

IX. Inflection Point #2: Completing the Pure-Play Transition (2017–2022)

*In 2017, W. P. Carey exited all non-traded retail fundraising activity as part of its evolution to a pure-play net lease REIT.

This decision reflected a fundamental strategic reorientation. The non-traded REIT business had served W. P. Carey well for decades, but it also created complexity—potential conflicts between the public company and managed funds, earnings volatility from management fees, and investor confusion about what the company actually was.

Sequential CPA Mergers

Subsequent consolidations included the mergers of CPA:16 – Global in January 2014, CPA:17 – Global in October 2018, and the final CPA:18 – Global in August 2022, fully integrating all prior programs into W. P. Carey Inc.

On August 1, 2022, W. P. Carey announced the completion of its merger with its final Corporate Property Associates program, CPA®:18 – Global. This marked the exit of the company from the non-traded REIT business, effectively completing its transition to a pure-play net lease REIT.

COVID-19 Resilience: The Model Proves Itself

Even in the midst of the global COVID-19 pandemic, W. P. Carey managed to maintain industry-leading rent collection rates that never dropped below 95%, a low point reached in May 2020.

These consistently strong collections make it one of the top performers in the net lease peer group and among the best in the REIT sector in general. In April, it collected 97% of rent; in May, 96%; in June, 98%; and in July, 98% as well.

Compare this to peers: National Retail Properties (NYSE:NNN), a bellwether in the net-lease space, was only able to collect around 52% of its rents in April. In the second quarter, it only managed to collect 69% of its rents. That improved to 84% in July, but that still means the REIT hasn't been able to collect rent from 16% of its portfolio.

The main reason for this stellar performance and corona-resilient results is W. P. Carey's crucial diversification. If done right, diversification trumps even the most unprecedented crisis, provided you have the right tenants. The company's core focus on companies, industries and real estate that is able to withstand even the current dislocation and respond adequately to challenges is a strong testament of success.

Green Bond and Ratings Upgrade

W. P. Carey executes its inaugural green bond offering. In addition, the company receives ratings upgrade from Moody's, affirming it sustained positive trajectory since its initial investment grade rating from Moody's and Standard & Poor's in 2014.

The green bond offering signaled recognition of ESG considerations while the ratings upgrade reflected the balance sheet strength built through disciplined management.

X. Inflection Point #3: The 2023 Office Exit—A Pivotal Strategic Reset

In September 2023, W. P. Carey made one of the most controversial decisions in its 50-year history: a full exit from the office sector.

On September 21, 2023, W. P. Carey Inc. today announced that its Board of Directors has unanimously approved a plan to exit the office assets within its portfolio by (i) spinning-off 59 office properties into Net Lease Office Properties ("NLOP"), so that it will become a separate publicly-traded REIT (the "Spin-Off"), and (ii) implementing an asset sale program to dispose of 87 office properties retained by W. P. Carey (the "Office Sale Program"). The Spin-Off is expected to close on or around November 1, 2023, subject to the satisfaction of certain conditions, and all sales under the Office Sale Program are targeted to be completed by January 2024.

Deal Mechanics

Under the terms of the Spin-Off, W. P. Carey stockholders received one NLOP common share for every 15 shares of W. P. Carey common stock held as of the record date of October 19, 2023.

The assets being contributed to NLOP represent approximately 10% of W. P. Carey's annualized based rent (ABR) as of June 30, 2023. NLOP is expected to comprise a portfolio of 59 high-quality office properties, totaling approximately 9.2 million leasable square feet primarily leased to corporate tenants on a single-tenant net lease basis. The vast majority of the office properties that will be owned by NLOP are located in the U.S., with the balance in Europe. NLOP's portfolio will consist of 62 corporate tenants operating in a variety of industries, generating ABR of more than $141 million as of June 30, 2023.

The Strategic Rationale

The office exit reflected a fundamental reassessment of post-COVID work patterns. Remote and hybrid work had permanently altered demand for traditional office space, creating structural vacancies that wouldn't fill regardless of economic conditions. Rather than wait for these properties to become problematic, W. P. Carey chose proactive divestiture.

"We've made excellent progress in a short space of time thanks to the hard work and dedication of our employees, bringing our office exposure down to less than 3% of ABR."

Market Reaction and Criticism

W. P. Carey's spin-off of Net Lease Office Properties has destroyed shareholder value for WPC and left long-term investors scarred.

W. P. Carey's spinoff of its office assets resulted in a 10% drop in stock price over two days due to poor communication with investors. The spinoff is expected to have a minimal impact on cashflows and growth trajectory, and the discount in stock price is seen as an opportunity. The dividend cut tanked the stock, but is actually a strategic move to retain capital for future growth and maximize total returns.

Dividend Cut Implications

Dividends declared during 2024 totaled $3.490 per share, a decrease of 14.2% compared to total dividends declared during 2023 of $4.067 per share, reflecting the impact on dividends declared since the 2023 fourth quarter of both the Company's strategic exit from the office assets within its portfolio and a lower payout ratio.

For a company that had built its identity around consistent dividend growth—increasing payments annually for over two decades—this cut was psychologically devastating for income-focused investors. The company's messaging emphasized that the cut was strategic rather than a sign of weakness, but dividend investors don't easily forget reductions.

Post-Spin Portfolio

Celebrating its 50th anniversary, W. P. Carey ranks among the largest net lease REITs with a well-diversified portfolio of high-quality, operationally critical commercial real estate, which includes 1,416 net lease properties covering approximately 171 million square feet and a portfolio of 85 self-storage operating properties, pro forma for the spin-off of NLOP, as of June 30, 2023.

The remaining portfolio focused on industrial, warehouse, and retail properties—asset classes with stronger long-term demand characteristics than office.

XI. The Modern Era: 2024–2025 & The New Baseline

"The fourth quarter concluded a pivotal year for W. P. Carey during which we successfully exited the office sector, setting the foundation for future growth," said Jason Fox, Chief Executive Officer. "We finished strongly with record investment volume for the quarter, and we're well-positioned to capitalize on opportunities in 2025."

Record Investment Volume

W. P. Carey announced investment volume for the 2024 full year of approximately $1.6 billion at a weighted-average initial cap rate of approximately 7.5% and an average yield of approximately 9% (which reflects contractual rent escalations over the terms of the leases).

During 2024, the company remained primarily focused on acquiring high-quality, single-tenant warehouse and industrial properties, which comprised close to 60% of its full-year investment volume, with retail properties comprising approximately 30%. From a geographic perspective, approximately three-quarters of its 2024 investment volume was located in North America and one-quarter in Europe.

Financial Results

Revenues, including reimbursable costs, for the 2024 full year totaled $1.58 billion, down 9.2% from $1.74 billion for the 2023 full year.

AFFO for the 2024 full year was $4.70 per diluted share, down 9.3% from $5.18 per diluted share for the 2023 full year, primarily reflecting the impact of the NLOP Spin-Off and dispositions under the Office Sale Program.

Office Exit Completion

The Company has effectively completed the strategic plan it announced on September 21, 2023 to exit the office assets within its portfolio through (i) the spin-off of 59 office properties into Net Lease Office Properties, a separate publicly-traded REIT, which was completed on November 1, 2023 (the NLOP Spin-Off), and (ii) the disposition of 85 properties retained by W. P. Carey under a sale program (the Office Sale Program).

Self-Storage Conversion

On September 1, 2024, the Company entered into agreements with Extra Space Storage Inc. (Extra Space) to convert 16 self-storage operating properties to net leases, each with a term of 25 years and fixed annual rent escalations plus a variable component based on revenue growth. Twelve self-storage operating properties converted to net leases on September 1, 2024, with the remaining four properties expected to convert in 2025.

This transaction converted operating properties—where W. P. Carey bore operating risk—into net lease properties with more predictable cash flows, consistent with the pure-play net lease strategy.

2025 Outlook

2025 AFFO guidance range of between $4.82 and $4.92 per diluted share announced, based on anticipated full year investment volume of between $1.0 billion and $1.5 billion.

"Furthermore, 2024 has established a new baseline from which we will grow our AFFO and dividend."

"We can fund our investments this year without needing to access the equity market, achieved through accretive sales of non-core assets—including self-storage operating properties—which should generate a meaningful spread to our net lease investments. Given the uncertainty in the broader market, however, particularly over the direction of interest rates and other macroeconomic factors, our guidance reflects a measured approach, which we hope proves conservative as the year progresses."

XII. Competitive Positioning & Strategic Analysis

The Net Lease REIT Landscape

W. P. Carey operates in a competitive space that includes Realty Income (NYSE: O), NNN REIT (NYSE: NNN), Agree Realty (NYSE: ADC), and several other players. Each has a distinct approach:

Realty Income has a much larger and more diversified portfolio. It's the seventh biggest REIT in the world, with $58 billion in real estate in eight countries. It owns over 15,450 properties leased to more than 1,550 clients in 90 industries.

NNN REIT currently owns about 3,550 properties (worth $12.9 billion) across 49 states. It leases its properties to over 375 tenants in 37 lines of trade (all retail-related) with an average remaining term of 10 years.

It has increased its dividend annually for 29 consecutive years. That's impressive, but NNN REIT has hiked its dividend for an even longer 34 years.

Porter's Five Forces Analysis

Threat of New Entrants: LOW Net lease REITs require massive capital bases, established tenant relationships, and underwriting expertise developed over decades. W. P. Carey's 50-year history, investment-grade credit rating, and relationship network create high barriers to entry.

Bargaining Power of Suppliers (Property Sellers): MODERATE Corporations considering sale-leasebacks have multiple potential buyers, but established players like W. P. Carey offer certainty of close, execution speed, and relationship value that newer entrants cannot match.

Bargaining Power of Buyers (Tenants): MODERATE While tenants can shop lease terms, the mission-critical nature of properties limits their negotiating leverage. A warehouse integral to a company's supply chain isn't easily replaced.

Threat of Substitutes: MODERATE Traditional mortgage debt, corporate bonds, and equity issuance all compete with sale-leasebacks as capital sources. However, sale-leasebacks offer unique advantages (full value extraction, operational control retention) that other structures cannot replicate.

Competitive Rivalry: HIGH Net lease REITs compete intensely for deal flow, particularly for high-quality assets with investment-grade tenants. W. P. Carey's diversification strategy—property type, geography, tenant industry—differentiates it from more focused competitors.

Hamilton Helmer's 7 Powers Framework

Scale Economies: W. P. Carey's size provides lower cost of capital, broader geographic coverage, and ability to execute larger transactions. Significant but not overwhelming versus peers.

Network Effects: Limited. This is not a network-effects business.

Counter-Positioning: W. P. Carey's diversification represents counter-positioning against retail-focused competitors. The COVID-19 pandemic demonstrated the value of this approach when retail rent collections plummeted industry-wide while W. P. Carey maintained 96%+ collections.

Switching Costs: High for tenants. Long-term leases (10-25 years) with mission-critical properties create substantial switching costs. Moving a warehouse or manufacturing facility is enormously disruptive.

Branding: Bill Carey's reputation for investor-friendly practices and the company's 50-year track record create meaningful brand value among corporate treasurers and CFOs evaluating sale-leaseback partners.

Cornered Resource: Not applicable.

Process Power: W. P. Carey's underwriting expertise, developed over five decades, represents embedded organizational knowledge difficult to replicate. The company's ability to correctly assess tenant credit risk across diverse industries and geographies is a genuine capability moat.

XIII. The Myth vs. Reality Box

Myth #1: "The 2023 dividend cut signals fundamental weakness"

Reality: The cut reflected strategic portfolio repositioning, not deteriorating fundamentals. W. P. Carey's late 2023 dividend cut was misunderstood and does not reflect the permanent weakness of the business. Dividend growth has already resumed. The payout ratio moved to 70-75%, more sustainable than the prior level.

Myth #2: "European exposure creates unnecessary currency risk"

Reality: Geographic diversification proved its value during COVID-19 when different regions experienced pandemic impacts at different times. European net lease markets remain underpenetrated compared to the U.S., creating acquisition opportunities with less competition.

Myth #3: "The office exit was panic selling at the worst time"

Reality: Management recognized structural—not cyclical—changes in office demand. Post-COVID hybrid work isn't reverting; it's becoming permanent. Better to exit proactively than manage a portfolio of declining assets. The NLOP spin structure allowed shareholders to participate in any office recovery through their NLOP shares while WPC focuses on stronger asset classes.

Myth #4: "Non-investment-grade tenants mean higher risk"

Reality: W. P. Carey's 96%+ rent collections during COVID-19—when some peers saw 50%+ drops—demonstrates that tenant selection and diversification matter more than credit ratings. Large companies just below investment grade often provide better risk-adjusted returns through higher cap rates while remaining financially sound.

XIV. Bull Case vs. Bear Case

The Bull Case

-

New Baseline for Growth: With office exit complete, W. P. Carey has a cleaner portfolio concentrated in industrial, warehouse, and retail—asset classes with stronger fundamentals. AFFO growth should resume from the new baseline.

-

Advantaged Cost of Capital: Investment-grade ratings and established market presence provide capital access when competitors struggle. In volatile markets, W. P. Carey can deploy capital when others retreat.

-

Built-in Rent Growth: Over 99% of leases include annual rent escalations—roughly half tied to CPI, half fixed. This provides organic growth regardless of acquisition activity.

-

European Underpenetration: Sale-leasebacks remain less common in Europe than the U.S., creating acquisition opportunities with less competition and potentially higher returns.

-

Track Record Through Cycles: 50 years of operating through multiple recessions, rate cycles, and crises demonstrates organizational resilience.

The Bear Case

-

Interest Rate Sensitivity: Net lease REITs trade as quasi-bonds. Rising rates compress valuations and increase financing costs, squeezing spreads between acquisition cap rates and cost of capital.

-

Dividend Trust Damaged: The 2023 cut alienated income-focused investors who may not return regardless of future performance. Rebuilding the dividend growth track record will take years.

-

Retail Exposure Concerns: Approximately 30% of recent investment volume went to retail properties. E-commerce disruption continues, potentially threatening long-term rental streams from physical retail.

-

Geographic Complexity: European investments create currency exposure, regulatory complexity, and management attention drain. Some investors prefer U.S.-only competitors for simplicity.

-

Scale Disadvantages vs. Realty Income: At roughly one-third the enterprise value of Realty Income, W. P. Carey may face capital access and transaction size disadvantages in competitive situations.

XV. Key Metrics for Ongoing Monitoring

For investors tracking W. P. Carey's performance, three KPIs deserve particular attention:

1. Adjusted Funds From Operations (AFFO) Per Share

AFFO is the gold standard metric for REITs—it captures actual cash-generating ability after maintenance capital expenditures. Watch for: - Quarterly trajectory relative to guidance - Year-over-year comparisons after the office exit normalization period (2025+) - Spread between AFFO and dividends (payout ratio sustainability)

Current baseline: $4.70 per share (2024 full year) 2025 guidance: $4.82-$4.92 per share

2. Same-Store Rent Growth

This measures organic rent increases from the existing portfolio, driven by lease escalators and re-leasing spreads. It reveals whether the portfolio is generating real growth versus just acquisition-driven expansion.

56% of W. P. Carey's rents came from leases tied to CPI, and in combination with strong fixed rent escalations, the company generated record year-over-year contractual same store rent growth, which at 4.1% was among the best in the net lease sector.

Sustained 2-4% same-store rent growth indicates a healthy portfolio with embedded inflation protection.

3. Investment Volume & Cap Rate Spread

Track quarterly acquisition volume, weighted-average cap rates on new investments, and the spread between those cap rates and W. P. Carey's cost of capital (weighted-average cost of debt plus equity cost). Positive spreads indicate accretive growth; compressed spreads suggest discipline may be slipping.

2024 metrics: $1.6 billion investment volume at 7.5% weighted-average cap rate

XVI. Key Risks & Regulatory Considerations

Interest Rate Environment

Net lease REITs are highly sensitive to interest rates. Rising rates increase borrowing costs, compress property values (cap rate expansion), and make dividend yields less attractive relative to risk-free alternatives. The Fed's rate trajectory remains the single largest external factor affecting W. P. Carey's valuation.

Tenant Credit Deterioration

While the portfolio is diversified across 355 tenants, significant tenant bankruptcy could impact results. Monitor the company's largest tenant exposures and credit quality disclosures.

REIT Tax Status

REITs must distribute at least 90% of taxable income to shareholders and meet various other requirements. Failure to maintain REIT status would create substantial tax liabilities.

Currency Exposure

With approximately 33% of revenue from Europe, W. P. Carey faces euro, pound, and other currency fluctuations. Material dollar strengthening would reduce reported earnings from non-U.S. properties.

Accounting Judgment: Impairments

Property impairment recognition requires management judgment about fair values. During the office exit, impairment charges increased materially. Investors should monitor ongoing impairment trends across the remaining portfolio.

XVII. Conclusion: The Verdict After Fifty Years

William Polk Carey died in January 2012, just months before his company converted to a REIT. He never saw the transformation that would more than double assets under management, nor the 2023 decision to exit office properties entirely. But the company he built—with its emphasis on diversification, long-term relationships, and investor-friendly structures—proved resilient enough to navigate changes he couldn't have anticipated.

The refrigerator story from Princeton wasn't just a founding myth; it was a philosophical statement. People will pay for ongoing access to assets they need. Separate ownership from use, and you create value for both parties. Structure the economics properly, and you can do well while doing good.

We don't run our business with a focus on quarterly results. We make our decisions through a long-term lens, which has served us well over many market cycles. We pride ourselves on hiring the best and the brightest, and strive to build a community of people with diverse opinions and experiences.

The 2023 office exit tested that long-term philosophy. Rather than hold depreciating assets hoping for improvement, management chose to rip off the bandage—accepting short-term pain (dividend cut, stock decline, investor anger) for long-term positioning (cleaner portfolio, growth from a new baseline, focus on stronger asset classes).

Whether that decision was right will take years to fully evaluate. What's clear is that W. P. Carey, after 50 years, remains what its founder intended: a vehicle for delivering stable, growing income from well-managed commercial real estate. The structure has evolved—from private partnerships to public LLC to traded REIT—but the core proposition endures.

For investors seeking exposure to net lease real estate with genuine diversification (property type, geography, tenant industry), W. P. Carey offers something distinct from more concentrated peers. The dividend cut wounded its reputation among income investors, but the lower payout ratio provides more margin for safety and future growth.

Bill Carey's final insight might have been his most important: build structures that outlast you. Governance that protects against individual mistakes. Diversification that survives sector disruptions. Relationships that compound across decades. These aren't just business practices—they're the foundation for compounding over generations.

The company operates from offices in New York, London, Amsterdam, and Dallas—a global footprint that its Depression-era founder couldn't have imagined when he was selling homemade ink in his Baltimore basement. But the principle remains the same: buy wholesale, sell (or lease) retail, and never forget that today's investment is tomorrow's income stream.

Investing for the Long Run® isn't just a trademark—it's the philosophy that built a $24 billion real estate empire from a college kid's refrigerators.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube