MasTec: Building America's Infrastructure from Cuban Dreams to Clean Energy Empire

I. Introduction: The $50,000 Loan That Built an Empire

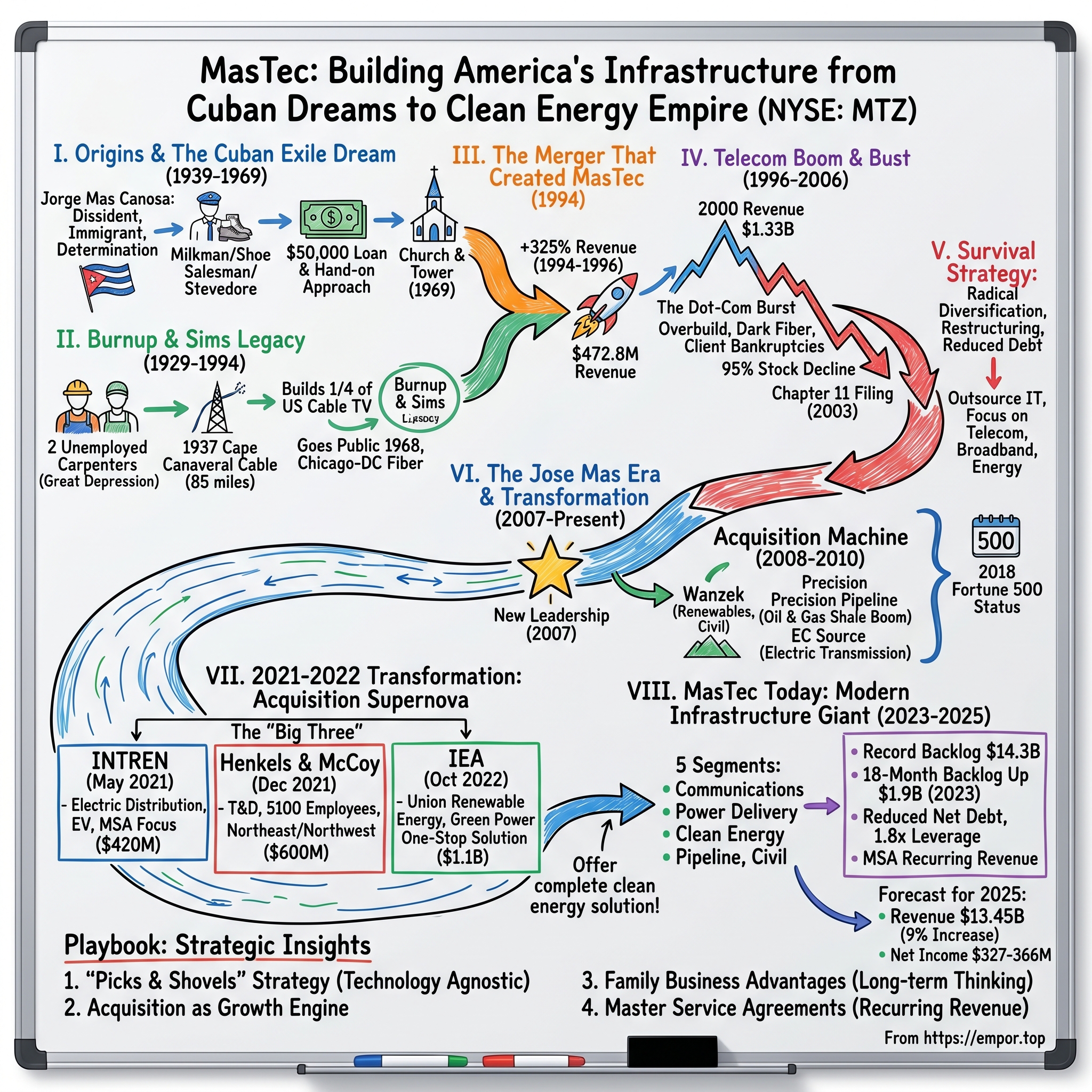

Picture this: Miami, 1969. A young Cuban exile—recently returned from a failed invasion at the Bay of Pigs, having worked as a milkman, stevedore, and shoe salesman—walks into a failing construction company with a borrowed $50,000 and a fierce determination to succeed. That man was Jorge Mas Canosa. The company he salvaged would eventually become MasTec, Inc., today one of America's largest infrastructure construction companies, with operations spanning from fiber optic networks to wind farms, from natural gas pipelines to solar installations.

In 2024, MasTec (NYSE: MTZ) reported record quarterly revenue of $3.4 billion and annual revenue of $12.3 billion. The company achieved a record 18-month backlog of $14.3 billion, representing a $1.9 billion increase over 2023. For 2025, the company projects revenue of $13.45 billion, a 9% increase over 2024, with GAAP net income between $327 million and $366 million.

The hook to this story is deceptively simple: How did a Cuban exile who worked as a milkman and shoe salesman build a $12+ billion infrastructure giant that's now building America's energy transition? The answer involves immigration dreams, family dynasties, near-death corporate experiences, and a prescient "picks and shovels" strategy that positioned MasTec to profit regardless of which energy technology ultimately wins.

MasTec, Inc. is the second largest Hispanic-owned company in the United States with over 20,000 employees in North America. The company's story encompasses nearly a century of American infrastructure development, from the Great Depression to the clean energy revolution. It demonstrates how family continuity, strategic acquisitions, and an ability to pivot through industry disruptions can create enduring business value.

The themes running through MasTec's history read like a masterclass in American entrepreneurship: an immigrant founder who turned personal struggle into business opportunity; a family dynasty that maintained control through three generations while navigating public markets; a near-death experience during the telecom bust that forced radical diversification; and finally, a transformational acquisition strategy that repositioned the company at the forefront of America's energy transition.

For long-term investors, MasTec represents a fascinating case study in what Hamilton Helmer might call "counter-positioning"—betting on infrastructure when others bet on technology companies themselves. As the old saying goes, during a gold rush, sell shovels. MasTec has been selling shovels across multiple infrastructure gold rushes for nearly a century.

II. Origins: The Cuban Exile & American Dream (1939-1969)

Jorge Mas Canosa's Backstory: From Santiago to Miami

In the sweltering heat of Santiago de Cuba on September 21, 1939, Jorge Lincoln Mas Canosa was born into a middle-class family that would shape his destiny as a dissident. Born into a religious, middle-class family in Santiago de Cuba, Cuba, since an early age he was outspoken about his opposition to dictatorships and was persecuted and imprisoned for his views by both the Fulgencio Batista and Fidel Castro regimes.

This dual opposition to authoritarian rule—first against Batista's right-wing dictatorship, then against Castro's communist revolution—would define Mas Canosa's character: a man who valued freedom above ideology and was willing to sacrifice everything for his beliefs. At the age of fifteen, Mas Canosa spoke out against Batista's dictatorship and was briefly imprisoned. Released into his father's custody, his family sent him to Presbyterian Junior College in Maxton, North Carolina.

The pivotal moment came in 1959 when Castro's forces overthrew Batista. Mas Canosa was sent by his father to the United States in the late 1950s to attend Presbyterian Junior College in Maxton, North Carolina, amid concerns over political unrest in Cuba. He returned to Cuba in January 1959, days after Fidel Castro's forces overthrew Fulgencio Batista on January 1, to enroll in law studies at the University of Oriente in Santiago de Cuba.

Following Castro's consolidation of power and evident shift toward Marxist policies, including nationalizations and suppression of dissent by mid-1959, Mas Canosa turned his opposition to the new regime, criticizing its dictatorial tendencies and alignment with Soviet influence. This stance led to his brief arrest by Cuban authorities for anti-government activities.

In 1960, he fled Cuba for the United States and settled in Miami, Florida, where he joined the Cuban exile force being trained by the Central Intelligence Agency to launch the April 1961 Bay of Pigs invasion. The young revolutionary was ready to fight to free his homeland. He did not participate in the fight, serving on a decoy ship instead. The excursion, later known as the Bay of Pigs, failed.

Following his return to the United States, Mas Canosa enlisted in the U.S. Army, eventually graduating from Officer Training School at Fort Benning, Georgia, as a second lieutenant. But military service was not to be his path. After his arrival in Miami, Mas Canosa worked a series of low-paying jobs: stevedore, shoe salesman, and milkman.

This period of struggle—working dawn milk routes, selling shoes, loading cargo at the docks—forged the work ethic and determination that would later transform a failing construction company into a telecommunications empire. Penniless and struggling to make ends meet—like most Cubans in the early days of exile—he worked at numerous jobs to feed his family, including working as a milkman and a stevedore.

Church & Tower: The Foundation

The moment that would change everything came in 1969. In 1969, Mas Canosa went into business with the owners of Iglesias y Torres, a floundering and overextended construction firm that constructed and serviced telephone networks in Puerto Rico. Renaming the company Church & Tower, Mas Canosa obtained a $50,000 loan and became a part owner.

What happened next reveals the essence of what made Mas Canosa successful. Rather than sitting in an office directing operations from above, eager to improve the business, Mas Canosa climbed down into ditches, manholes, and trenches to observe workers' construction methods. He listened to advice from telephone-companies and government inspectors; he studied books about the most efficient and newest construction methods.

This hands-on approach—learning the business from the ground up, literally getting his hands dirty—was classic immigrant entrepreneurship. Mas Canosa didn't just want to manage the company; he wanted to understand every aspect of the work. He studied construction techniques, talked to inspectors, and learned what customers actually needed.

BellSouth Telecommunications, Inc. awarded Church & Tower a long-term contract for projects in the greater Miami and Fort Lauderdale areas. By 1971, Mas Canosa had turned the failing company around; he then borrowed $50,000 and bought the remaining shares of the firm.

From $50,000 borrowed in 1969 to full ownership in 1971—that's the kind of turnaround that defines entrepreneurial legends. The company that telecommunications giant BellSouth had trusted with its Miami infrastructure was now entirely his. The company grew from South Miami to Ft. Lauderdale. By 1980, it had $40 million in yearly earnings.

In just over a decade, Mas Canosa had transformed a failing Puerto Rico-based operation into a $40 million South Florida powerhouse. The construction techniques he had learned by crawling into trenches, the relationships he had built with telephone companies, and the reputation for reliability he had established would prove to be the foundation for everything that followed.

For investors studying entrepreneurial success, the Church & Tower story offers a timeless lesson: sometimes the path to business success runs through ditches and manholes, not corner offices. Mas Canosa's willingness to learn the business from the bottom up created a competitive advantage that no amount of capital could have purchased.

III. The Burnup & Sims Legacy (1929-1994)

Two Unemployed Carpenters and the Birth of American Telecom Infrastructure

The MasTec story has a second origin—one that predates Jorge Mas Canosa by four decades and begins not with a Cuban exile but with two American carpenters facing the Great Depression.

In 1929, two unemployed carpenters – Russell Burnup and Riley Sims – envisioned creating a construction company that would serve the growing telecommunications and civil construction market in Florida and, eventually, the Southeast. With a handshake and their mutual trust, they formed their firm.

The timing couldn't have been worse—or better. From those humble beginnings in the depths of the Great Depression, Burnup & Sims grew into a construction powerhouse. While the economic collapse destroyed countless businesses, Burnup and Sims found that telecommunications infrastructure remained essential. People might lose their jobs, but they still needed telephones.

During the years of the Great Depression, the two established an office in West Palm Beach, Florida, and by 1936, had a small fleet of trucks and staff. The company's first telecommunications projects were undertaken the following year at Cape Canaveral, where it was responsible for burying 85 miles of cable.

This Cape Canaveral project in 1937 marked Burnup & Sims' transition from survival mode to growth mode. The same year that would later become famous for rocket launches saw the quiet burial of 85 miles of telecommunications cable—the kind of unglamorous but essential infrastructure work that would define both Burnup & Sims and eventually MasTec.

B&S contributed to national defense during World War II by building airfields and telephone systems. The war transformed Burnup & Sims from a regional contractor into a nationally significant player. Military communications required reliable infrastructure, and Burnup & Sims delivered.

After the war, the company became involved in the laying of underwater cable from Florida to Puerto Rico, and from there to Barbados, for such companies as AT&T and General Telephone. The company built telephone networks throughout the nation, as well as in the Middle East and the Pacific Islands, laid the first underwater telephone cable from Florida to Puerto Rico, and built nearly one-fourth of the country's cable television systems.

Think about that last statistic: Burnup & Sims built nearly one-fourth of America's cable television infrastructure. In an era before Netflix, before streaming, before the internet, cable TV was the future of entertainment—and Burnup & Sims was building it.

In 1968 Burnup & Sims went public, and the shares sold helped raised capital for new, more ambitious projects. The company is remembered for constructing the first fiber-optic link between Chicago and Washington, D.C. and, according to historian George P. Oslin in The History of Telecommunications, for doing "a large and very profitable business installing cables for Cable TV." In fact, by 1982, Burnup & Sims "had installed a fifth of the 500,000 miles of TV cables in use."

The first fiber-optic link between Chicago and Washington, D.C.—a technological milestone that would eventually enable the internet revolution—was built by these two former unemployed carpenters' company.

The Burnup & Sims Turmoil and Corporate Raiders

But success breeds challenges. The dispute that eventually spawned National Beverage had its roots in the late 1970s, when a Fort Lauderdale company named Burnup & Sims Inc. was thriving as an installer of cable television and telecommunications systems. Headed by a Pennsylvania coal miner's son named Nick Caporella, the company was performing phenomenally well, demonstrating a level of profitability that delighted Wall Street.

Posner watched Burnup & Sims's earnings nearly triple between 1978 and 1981 and decided to secure a piece of the rising profits. Victor Posner, a notorious corporate raider of the era, saw Burnup & Sims as prey. At first, as Posner's holding in Burnup & Sims gradually increased, it appeared Caporella was unwilling to fight. In 1982, when Posner's stake eclipsed 29 percent, Caporella quit in disgust, vacating his chief executive position at Burnup & Sims and taking 17 executives with him.

The corporate drama that followed would weaken Burnup & Sims throughout the 1980s. Posner, however, did not make his full retreat until 1988 when Cincinnati financier Carl Lindner purchased Posner's shares and transferred them to Burnup & Sims.

By the end of the decade, however, unsettled economic conditions, changes in utility spending, and aggressive competition for contracts brought tough years for Burnup & Sims. Moreover, budgetary constrictions led certain telecommunications companies to postpone payments and to cut expenditures for plant construction and maintenance. By the end of fiscal 1993 Burnup & Sims' losses amounted to $9.31 million, and senior management was seeking a buyer for the company.

The Merger That Created MasTec

The collision of these two trajectories—a struggling public company with a storied history and a thriving private company led by an ambitious immigrant family—created MasTec.

Church & Tower's leadership realized that to serve the national telecommunications giants that would emerge from the industry's deregulation, the company needed to grow. The Mas family saw South Florida-based Burnup & Sims as a major player in many markets, but also as a company struggling to define its culture and vision for the future. Under Jorge Mas' guidance, the two companies became one.

On March 11, 1994, Church & Tower Group acquired 65 percent of the outstanding common stock of publicly traded Burnup & Sims, Inc. It was a reverse acquisition—the smaller private company effectively taking over the larger public one. The name of Burnup & Sims was changed to MasTec, Inc., Jorge Mas Canosa became MasTec's chairman and his son, Jorge Mas, was named president and chief executive officer.

The name "MasTec" cleverly combined the family name with "technology"—signaling both continuity and transformation. From 1994 to 1996 MasTec revenues increased 325 percent, growing from $111.29 million to $472.8 million.

A 325% revenue increase in just two years demonstrated what family management combined with public company resources could achieve. The Mas family brought entrepreneurial energy and operational discipline; the Burnup & Sims infrastructure provided scale and customer relationships.

The company was listed on the New York Stock Exchange in 1998. Jorge Mas Canosa, the former milkman and shoe salesman, had built a company significant enough to trade on the most prestigious stock exchange in the world.

For investors, the Burnup & Sims merger illustrates a crucial principle: sometimes the best acquisitions aren't about buying growth—they're about acquiring established relationships and infrastructure that would take decades to build organically. Church & Tower's purchase of Burnup & Sims gave the Mas family instant credibility with national telecommunications giants.

IV. The Family Dynasty & Political Connections

Jorge Mas Canosa's Dual Legacy

Understanding MasTec requires understanding that Jorge Mas Canosa was never just a businessman. His life was divided between two consuming passions: building a telecommunications empire and working to free Cuba from Castro's rule.

In 1981, Mas Canosa and Raul Masvidal established the non-profit Cuban American National Foundation (CANF). Throughout his leadership of the organization, Canosa and CANF held immense influence over the U.S policy with Cuba.

The group was founded as part of a broader strategy to sideline more moderate perspectives within the Cuban-American community, and to convert anti-Castro activism from a more militant to a more political strategy. CANF was widely described during Mas Canosa's tenure as one of the most powerful ethnic lobbying organizations in the US, and used campaign contributions to advance its policy in Washington, DC.

Congressman Robert Torricelli credited Mas Canosa with aiding him in the design of the 1994 Cuban Democracy Act and the Helms-Burton Act. Mr. Mas Canosa was instrumental in the creation of Radio & TV Marti, U.S., government broadcasts of uncensored news and information to the Cuban people. Fashioned after Radio Free Europe and Radio Liberty, Radio & TV Marti have been highly successful in sending a message of hope to the Cuban people in their struggle for liberty. Mr. Mas Canosa was appointed by President Ronald Reagan as Chairman of the President's Advisory Board for Cuba Broadcasting and also served Presidents George Bush and Bill Clinton in that capacity.

More than any other individual, Mas Canosa was responsible for the U.S. government's hardline stance in its Cuban foreign policy, and he influenced the policies of presidents Ronald Reagan, George H. W. Bush, and Bill Clinton.

This political influence created both opportunities and challenges for MasTec. On one hand, Mas Canosa's Washington connections opened doors. On the other, his controversial activism attracted critics. "I am a misunderstood man," he said in a 1992 interview in Miami. "I have never assimilated. I never intended to. I am a Cuban first. I live here only as an extension of Cuba."

The organization would go on to become the foundation of a telecommunications empire and multinational corporation MasTec. Mr. Mas would become one of the wealthiest Hispanic businessmen in the United States, with a net worth of over $100 million at the time of his death.

The Succession: Father to Sons

Jorge Mas Canosa died on November 23, 1997, just one year after MasTec had completed its spectacular growth phase. When he passed away in 1997, thousands of Cubans and others inspired by his life's work gathered in Miami to attend his funeral, the largest ever held in this region.

But the patriarch had planned carefully. Back in Miami, he married Irma Santos with whom he shared a fruitful family life along with their three sons, Jorge Mas, Jr., Juan Carlos Mas, and Jose Ramon Mas, all of whom work for MasTec, Inc.

The transition to the next generation had already begun before Jorge Mas Canosa's death. When MasTec was formed in 1994, his son Jorge Mas was named president and chief executive officer. The founder took the chairman's role, allowing the next generation to gain operational experience while maintaining family oversight.

Jose Mas grew up in the business and has worked from the field to the boardroom at MasTec. Mr. Mas started with MasTec in 1992, and from 1999 until 2001 he was head of MasTec's Communications Group, responsible for approximately $350 million in annual revenue. Since August of 2001, he has served as Vice Chairman of the Board of Directors and Executive Vice President of Business Development, primarily responsible for the Company's customer marketing and acquisition activity.

In April 2007, Jose Mas became CEO of MasTec. The succession was complete: from Jorge Mas Canosa to Jorge Mas Jr. to Jose Mas—three generations of Mas family leadership.

Jose Mas grew up in the construction business and worked his way from field labor to the boardroom. He is a graduate of the University of Miami where he obtained a Bachelor of Business Administration and a Master of Business Administration.

This hands-on apprenticeship—starting in the field, just as his grandfather had climbed into ditches to learn the business—ensured that Jose Mas understood MasTec's operations intimately before taking the top job.

For family business investors, the Mas succession offers a textbook example of thoughtful transition planning. The founder gradually ceded operational control while maintaining strategic oversight. Multiple family members gained experience across different functions. And when the transition came, it was orderly rather than chaotic.

V. The Telecom Boom & Bust (1996-2006)

Riding the Dot-Com Wave

The 1996 Telecommunications Act promised to reshape American communications infrastructure. By removing barriers to competition, it unleashed a wave of investment that would benefit infrastructure contractors like MasTec—until it didn't.

1997: MasTec goes public; its stock is traded on the New York Stock Exchange. 2000: MasTec revenue peaks at $1.33 billion.

The late 1990s were intoxicating for telecommunications infrastructure companies. Every new fiber optic network, every wireless tower, every broadband buildout required construction services. MasTec was perfectly positioned to capitalize on the frenzy.

MasTec experienced significant revenue growth during the late 1990s telecommunications expansion, with annual revenues surpassing $2 billion by 2000 amid heavy investment in network buildouts.

But beneath the surface, warning signs were accumulating. Telecommunications companies were building infrastructure for demand that didn't exist. The famous "dark fiber" problem—miles of unused fiber optic cable buried beneath American cities—reflected an industry disconnected from economic reality.

The Near-Death Experience

2001: Economic downturn of telecom and cable markets heavily impacts MasTec and restructuring begins.

However, as Rolf Boone observed in a 2002 article in the Wenatchee Business Journal, "a funny thing happened on the way to ever-expanding growth and revenue—the telecommunications bubble burst." In its 2001 annual report, MasTec management noted that "certain segments of the telecom industry suffered a severe downturn that resulted in a number of our clients filing for bankruptcy protection, or experiencing financial difficulties." Even clients not in financial difficulty began limiting capital expenditures for infrastructure projects.

MasTec, heavily reliant on telecom construction, experienced a severe revenue contraction as carriers curtailed spending and many customers faced financial distress. Revenues peaked at $1.33 billion in 2000 before declining sharply, with the company reporting a net loss of $136 million on $838 million in revenue for 2002 amid client insolvencies and uncollectible receivables.

The numbers tell a brutal story: from $2 billion in revenue at the peak to $838 million in 2002—a decline of more than 60%. This overbuild created excess capacity that collapsed with the 2001 telecom bust, triggering client bankruptcies and forcing MasTec to write off massive uncollectible receivables, including $185.5 million in bad debt provisions for 2001 and $15.4 million for 2002.

From 2001 to 2004, for example, our common stock fluctuated from a high of $24.75 in the first quarter of 2001 to a low of $1.31 in the first quarter of 2004.

A 95% decline in stock price. Clients declaring bankruptcy. Massive write-offs. Financial results for 2002 were disappointing, with the company posting a net loss of $128.8 million on revenues of $838.1.

MasTec's Chapter 11 bankruptcy filing in early 2003 was precipitated by the telecommunications industry's severe contraction after years of speculative overinvestment in fiber-optic and broadband infrastructure during the late 1990s dot-com expansion.

The Survival Strategy

In response, MasTec implemented aggressive operational restructuring starting in 2001, including significant workforce reductions totaling approximately 1,025 employees by 2003 and charges for asset impairments and restructuring costs exceeding $8 million in 2002 alone.

We continuously review our operations in an effort to improve profitability. In 2002, we implemented a restructuring program under which we: eliminated services offerings that no longer fit into our current business strategy; reduced or eliminated services that did not produce adequate revenue or margin; reduced costs of businesses which provided adequate profit contributions but needed margin improvements. As a result of this program, we incurred a pre-tax charge of $3.7 million in 2002.

Facing a market that had dried up, Shanfelter and Weinstein remained cautiously optimistic, reminding the public that MasTec had predicted the downtown and was making adjustments accordingly. The company's Project 2100 was introduced to streamline, downsize, and realize economies through strategic partnerships. Another key to the plan was in outsourcing much of the company's information technology functions. As a result, MasTec was refocused on telecom, broadband, intelligent traffic systems, and energy.

During the proceedings, MasTec restructured its balance sheet by negotiating debt reductions and operational divestitures, emerging in early 2004 with lowered leverage and a sharpened focus on profitable operations. Emerging from restructuring later that year, the company pivoted toward diversification into power delivery, oil and natural gas infrastructure, and other utilities, reducing reliance on cyclical telecom projects.

The key insight from this period: under the stewardship of the Mas family, MasTec survived when many competitors did not. Unlike companies driven by short-term pressures to maximize quarterly earnings, the family-controlled structure allowed MasTec to make painful but necessary decisions for long-term survival.

For investors, the telecom bust years offer crucial lessons about concentration risk and the value of diversification. MasTec entered the crisis as essentially a telecommunications-focused contractor. It emerged committed to serving multiple infrastructure end markets—a strategy that would prove transformational.

VI. The José Mas Era & Transformation (2007-2021)

Key Inflection Point #1: New Leadership & Diversification Strategy

When Jose Mas took the CEO role in early 2007, MasTec was a company that had survived but not yet thrived. The telecom bust had exposed the dangers of concentration, and the company needed a new strategic direction.

Jose R. Mas is the Chief Executive Officer of MasTec, Inc., (NYSE: MTZ) one of the largest and most diversified infrastructure services providers in North America. During Mr. Mas' tenure as CEO, MasTec's revenue has grown from $930 million in 2007 to an expected $12.4 billion in 2024.

Since assuming the Chief Executive Officer position at MasTec, Mr. Mas transformed MasTec from a predominantly telecommunications contractor to one of the most diversified specialty infrastructure contractors in North America.

Shanfelter continued, "It has been a very difficult, but rewarding, five years in the CEO role and we have accomplished many things. The turnaround is complete, the Company is recapitalized, margins are improving and MasTec is now focused on core businesses that show much growth potential going forward."

Jose Mas inherited a stabilized company and set about transforming it. Discussing the industry, Jose Mas continued, "We are presented with exciting opportunities ahead in communications as fiber deployments, High-definition TV, satellite and other technologies ramp up, broadband over power lines begins to deploy and as the electrical grid starts its long overdue upgrades. Additionally, new technologies and innovations will continue to drive demand for power, fixed and mobile video programming, voice and data delivery."

Key Inflection Point #2: Strategic Acquisition Machine

Jose Mas's strategy was clear: use acquisitions to rapidly diversify beyond telecommunications into energy infrastructure. The timing proved prescient as the shale revolution, renewable energy build-out, and grid modernization created enormous demand for infrastructure construction.

The first major move came in 2008 with the acquisition of Wanzek Construction. Based in Fargo, North Dakota, Wanzek specialized in heavy civil construction, concrete projects, and increasingly, renewable energy installations. The acquisition gave MasTec immediate capabilities in wind farm construction and heavy civil work—markets where telecommunications expertise was irrelevant.

The acquisition strategy accelerated in 2009 with Precision Pipeline, which enhanced MasTec's oil and gas pipeline capabilities just as the shale boom was transforming American energy production. The company followed up in 2010 with EC Source, entering the electrical transmission construction market.

The results spoke for themselves. Revenue climbed from the post-crisis trough to $1.62 billion by 2009 and $2.14 billion in 2010. But more importantly, the revenue mix had fundamentally shifted. MasTec was no longer dependent on telecommunications spending—it had become a diversified infrastructure contractor serving communications, energy, and utilities customers.

As co-owner of Inter Miami CF, Mr. Mas is proud to have brought soccer, the world's biggest sport, to the city of Miami and is now focused on developing Miami Freedom Park, a $1 billion plus real estate development project that will include a soccer stadium, hotels, an office park, a retail and entertainment village and a 56-acre public park for all of the South Florida community to enjoy. Mr. Mas has been awarded the Ernst & Young National Entrepreneur of the year award, the South Florida Business Journal Ultimate CEO award and was also featured in the season finale of the CBS hit show Undercover Boss.

Jose Mas's visibility extended beyond the construction industry. His appearance on Undercover Boss, his ownership stake in Inter Miami CF (the soccer club that brought Lionel Messi to Miami), and his development of Miami Freedom Park demonstrated the broader ambitions of the Mas family in shaping South Florida.

In 2018 for the first time in the Company's history, MasTec was named as a Fortune 500 company, and is currently ranked no. 394.

Fortune 500 status represented a milestone that would have seemed impossible during the telecom bust years. The shoe salesman's grandson had built a company that ranked among America's 400 largest.

VII. The 2021-2022 Transformation: Acquisition Supernova

Key Inflection Point #3: The "Big Three" Acquisitions

The period from 2021 to 2022 represented the most aggressive acquisition phase in MasTec's history. Three transformational deals—INTREN, Henkels & McCoy, and IEA—fundamentally repositioned the company at the forefront of America's clean energy transition.

INTREN (May 2021):

In the transaction, MasTec acquired all the equity interests of INTREN for approximately $420 million in cash plus a contingent earnout through year end 2021. At closing, INTREN is expected to have approximately $100 million in tangible net worth.

Jose Mas, MasTec's President and CEO noted, "We are very excited to add INTREN to the MasTec family and substantially expand our reach in the electric utility distribution business. We believe that changes in electrical distribution needs, led by grid modernizations and hardening, coupled with the transition towards increased electric vehicle usage, will have an enormous impact on the last mile distribution of electricity. The acquisition of INTREN represents a major expansion of MasTec's operations at the forefront of that high-growth market."

INTREN was founded in 1988 by one woman, Loretta Rosenmayer, with a dream and a loan from a friend. Today, it employs more than 2,000 people and operates in 14 states.

The INTREN story had echoes of Jorge Mas Canosa's own journey—a founder with a dream and borrowed money building something substantial. As the largest woman owned utility specialty contractor in the country, I have always been impressed with the quality of INTREN's management and their entrepreneurial spirit.

Founded in 1988 by a sole female founder, INTREN has exhibited significant growth over the past ten years with a +23% compounded annual revenue growth rate. For the trailing twelve-month period ended March 2021, INTREN generated approximately $550 million of revenue, with over 90% generated from its multiple master service agreements, at a double-digit EBITDA margin.

The key statistic: 90% of revenue from master service agreements with double-digit margins. This was exactly the kind of recurring, stable revenue that MasTec sought to build.

Henkels & McCoy (December 2021):

MasTec closed its previously announced acquisition of Henkels & McCoy Group, Inc. ("Henkels"), the 5th largest U.S. utility contractor in the recent 2021 Engineering News-Record ranking, in a cash and stock transaction valued at approximately $600 million.

Florida-based specialty contractor giant MasTec Inc. has agreed to acquire electrical power transmission and distribution utility services firm Henkels & McCoy in a $600-million deal. During a conference call to investors, CEO Jose Mas said the acquisition is the largest in company history and comes at the "right time" to continue expanding its non-oil and gas pipeline services.

Founded in 1923, Henkels has been in operation for over 98 years, with approximately $1.5 billion in fiscal 2021 revenue primarily with long tenured relationships across a diverse blue chip customer base.

"This transaction will double our transmission and distribution resources, expanding our presence in the Northeast markets and the Northwest, where MasTec has traditionally been underrepresented," Mas said.

The Pennsylvania-based company has approximately 5,100 employees. In a labor-constrained industry, acquiring 5,100 trained workers was perhaps as valuable as acquiring customer relationships.

"We believe that the addition of Henkels, coupled with MasTec's existing operations, creates a market leading utility contractor with significant expertise, scale and capacity that can provide a complete and compelling suite of service offerings to our customers as they work to transition to renewable energy generation, modernize power grid systems and reduce carbon emissions."

Infrastructure & Energy Alternatives (IEA) (October 2022):

MasTec completed the previously announced acquisition of IEA, one of the largest utility-scale renewable energy infrastructure solutions providers in North America, following approval by the IEA stockholders at a special meeting held on October 7, 2022.

MasTec and IEA today announced that they have entered into a definitive agreement under which MasTec will acquire all of the outstanding shares of IEA in a cash-and-stock transaction valued at $14.00 per IEA share.

Based on estimated IEA net debt levels at closing, the total transaction consideration will be approximately $1.1 billion. MasTec expects to issue approximately 2.8 million MasTec shares in the transaction.

Founded in 2011 with roots dating to 1947, IEA is a premier services provider in renewable energy and infrastructure solutions, with extensive expertise and capabilities spanning engineering, procurement, construction and other related services.

"We are excited to announce the closing of the IEA transaction and look forward to expanding our green power construction and maintenance capacity in the country's push towards a carbon-neutral economy. Combining IEA's renewable energy business with MasTec's electric transmission and substation capabilities gives customers a one-stop solution in the expanding renewable energy markets."

The Results: A Transformed Company

MasTec's Chief Executive Officer, commented, "As we end 2022, it is important to note the significant end market transformation we have undertaken over the past two years to support the nation's energy transition to sustainable renewable energy sources. We believe that acquisition activity over the last two years has greatly enhanced our scale, expertise and market positioning to meet expected high customer demand growth for renewable power generation, power grid transmission and distribution and civil infrastructure over the next decade. We believe that this opportunity, coupled with continued expected growth in telecommunications infrastructure and expanding demand for traditional and new green pipeline services, positions us with multiple strong long term growth opportunities."

First, it continues to grow our presence in the energy market and enhances our ESG profile in what we believe is an ongoing early transformation related to both power generation and delivery as the country transitions to a carbon neutral economy. Second, IEA's roots are those of a union renewables contractor. This transaction expands our renewable business into union markets. MasTec has been an exclusively non-union renewables construction company. More importantly, it allows us to cross-sell complementary services to these same customers with the investments we made last year in growing our union transmission and distribution presence through the acquisitions of both INTREN and Henkels & McCoy.

The strategic logic was clear: by combining renewable energy construction (IEA) with electrical transmission and distribution (Henkels & McCoy and INTREN), MasTec could offer customers a complete solution for the clean energy transition—from building wind farms and solar installations to connecting them to the grid.

VIII. MasTec Today: The Modern Infrastructure Giant (2023-2025)

Current Business Model

MasTec has transformed into one of North America's most diversified infrastructure contractors. The company operates through five primary segments:

Communications: Serves both wireless and wireline/fiber infrastructure, including 5G network deployment, fiber optic installation, and broadband expansion. This segment represents MasTec's original business but is now just one part of a diversified portfolio.

Power Delivery: Serves utility customers in transmission and distribution markets. This segment expanded dramatically through the Henkels & McCoy and INTREN acquisitions.

Pipeline Infrastructure: Serves energy and other customers with installation and maintenance services primarily for natural gas pipeline and distribution infrastructure.

Clean Energy and Infrastructure: Provides renewable energy engineering and construction services, including wind farms, solar installations, and battery storage facilities. This segment grew substantially through the IEA acquisition.

The recurring revenue model has become central to MasTec's value proposition. With a substantial portion of revenue coming from Master Service Agreements (MSAs), the company has reduced the project-by-project volatility that once characterized the construction industry.

2024-2025 Performance and Outlook

For the full year 2024, MasTec Inc (NYSE:MTZ) achieved revenue of $12.3 billion, a 20% year-over-year increase in adjusted EBITDA, and reduced net debt by over $700 million.

Cash flow from operations surged 63% to $1.1 billion, enabling a Q4 net debt reduction of $318 million and improving the net debt leverage ratio to 1.8x.

MasTec's Executive Vice President, and Chief Financial Officer, noted, "We saw continued improvement in our balance sheet, driven by improvement in both earnings and our working capital, resulting in $1.1 billion of cash flow generated by operations for the year. With net debt leverage at a comfortable 1.8x adjusted EBITDA, we are positioned to shift back to a more balanced, return focused capital allocation framework."

The company expects significant growth in its non-pipeline businesses for 2025, with anticipated revenue growth of 14% and EBITDA growth of over 25%. MasTec Inc (NYSE:MTZ) has a record backlog of $14.3 billion, indicating strong demand across all segments, particularly in communications, power delivery, and clean energy.

For 2025, MasTec is issuing initial guidance including revenue of $13.45 billion, a 9% increase over 2024, GAAP net income of $327 million to $366 million, adjusted EBITDA of $1.10 billion to $1.15 billion, with diluted earnings per share of $3.75 to $4.24.

The pipeline segment experienced a decline in revenue for the fourth quarter and is expected to see reduced activity in 2025 due to the completion of the Mountain Valley Pipeline.

The Mountain Valley Pipeline completion illustrates both the opportunity and challenge of large project work: these projects provide substantial revenue during construction but create difficult year-over-year comparisons when completed.

The communications segment is expected to grow by 11% in 2025, with a focus on wireline due to fiber demand. Wireless growth is anticipated in future years, driven by increased investments from carriers like T-Mobile and Verizon.

Macro Tailwinds

MasTec is positioned at the intersection of several powerful secular trends:

Clean Energy Transition: The Inflation Reduction Act provides substantial incentives for renewable energy construction. Whether through wind farms, solar installations, or battery storage, MasTec's Clean Energy segment stands to benefit from unprecedented federal support.

Grid Modernization: America's electrical grid requires massive investment to accommodate renewable energy, support electric vehicle charging infrastructure, and improve resilience against extreme weather events. MasTec's Power Delivery segment serves exactly this need.

Broadband Expansion: Federal infrastructure programs include significant funding for rural broadband deployment. MasTec's Communications segment has decades of experience in fiber optic installation.

Natural Gas Infrastructure: Despite the focus on renewable energy, natural gas continues to play a significant role in the energy transition. MasTec's Pipeline segment serves this market, though the company has clearly been diversifying away from oil and gas concentration.

"We are ready to take on a second major project and are hopeful to be awarded another during 2025. We aim to work on two large projects simultaneously by 2026 and eventually expand to a third." (Jose Mas, CEO)

IX. Playbook: Business Lessons & Strategic Insights

The "Picks & Shovels" Strategy

The most elegant aspect of MasTec's business model is its indifference to technology outcomes. The company doesn't generate energy—it builds the infrastructure that enables energy generation and transmission. Whether solar wins, wind wins, natural gas persists, or some new technology emerges, MasTec profits from the construction.

This "picks and shovels" approach to infrastructure investing—named after the legendary wisdom that the real money during the Gold Rush went to those selling tools rather than mining for gold—provides natural diversification against technology risk. When telecommunications boomed, MasTec built fiber networks. When shale revolutionized energy, MasTec built pipelines. When renewables surged, MasTec built wind farms and solar installations.

Acquisition as Growth Engine

MasTec's transformation from a $930 million telecommunications contractor in 2007 to a $12+ billion diversified infrastructure company in 2024 occurred primarily through acquisitions. The company has demonstrated remarkable discipline in identifying targets that:

-

Fill geographic gaps: The Henkels & McCoy acquisition expanded MasTec's presence in the Northeast and Northwest.

-

Add capabilities: The IEA acquisition brought union-based renewable energy construction expertise.

-

Provide recurring revenue: INTREN's 90%+ MSA-based revenue model reduced project volatility.

-

Include skilled workers: In a labor-constrained industry, acquiring trained workforces is as valuable as acquiring customer contracts.

Family Business Advantages

Multi-generational family control enabled MasTec to survive the telecom bust when short-term pressures might have forced competitors into destructive decisions. The Mas family's willingness to think in decades rather than quarters provided strategic flexibility that publicly traded companies with dispersed ownership often lack.

The family structure also ensures cultural continuity. Jose Mas learned the business from his father and grandfather, who themselves learned by climbing into trenches. This hands-on operational understanding permeates the organization.

Master Service Agreements (MSAs)

The shift to recurring revenue through MSAs represents perhaps the most important business model evolution in MasTec's history. Rather than bidding for individual projects, MSAs establish ongoing relationships with customers for maintenance, upgrades, and construction services. This provides:

- Revenue visibility for planning purposes

- Reduced business development costs

- Deeper customer relationships

- More stable earnings patterns

The Immigrant Entrepreneur Playbook

From a $50,000 loan to a $12+ billion empire—the MasTec story represents a classic American bootstrap narrative. Jorge Mas Canosa arrived in Miami with nothing, worked menial jobs, learned a business from the ground up, and built something enduring.

The ingredients of his success—determination forged by adversity, willingness to do whatever work was necessary, relentless focus on customer needs, and long-term thinking—remain as relevant today as they were in 1969.

X. Porter's Five Forces & Hamilton's Seven Powers Analysis

Porter's Five Forces Assessment

Threat of New Entrants: LOW-MEDIUM

Infrastructure construction requires substantial capital for equipment, established relationships with major customers, trained workforces with specialized skills, and extensive regulatory compliance capabilities. These barriers protect established players like MasTec.

However, regional contractors can compete effectively in local markets, and private equity has shown interest in consolidating smaller players. The acquisition of Henkels & McCoy—a nearly century-old company—by MasTec demonstrates that even established players can become targets.

Bargaining Power of Suppliers: MEDIUM

Equipment and materials are relatively commoditized, limiting supplier power. However, skilled labor represents a critical input with significant bargaining power. The Pennsylvania-based company (Henkels & McCoy) has approximately 5,100 employees. Acquisitions partly serve to acquire trained workforces in a tight labor market.

Bargaining Power of Buyers: MEDIUM-HIGH

Major utilities and telecommunications companies represent concentrated buying power. Some of our larger clients include BellSouth Telecommunications, Inc., Comcast Cable Communications, Inc., DIRECTV, Progress Energy, Sprint Corporation and Verizon Communications, Inc. The contracts generally provide for extensions by mutual consent. Although these contracts may legally be terminated by our clients for any or no reason on little notice; they can continue in place for many years. As an example, we, and our predecessor, Church & Tower, have had a relationship with BellSouth for more than twenty years.

The multi-decade relationship with BellSouth illustrates how switching costs and relationship value can offset raw buyer power.

Threat of Substitutes: LOW

Physical infrastructure must be built—there is no substitute for laying fiber optic cable, constructing transmission lines, or building wind farms. While technology may change (5G versus fiber, solar versus wind), the need for physical construction services remains constant.

Competitive Rivalry: HIGH

Mastec competitors include MYR Group, Quanta Services, EMCOR Group, Crown Castle and Dycom Industries.

Quanta Services has 58,400 employees and revenue of $23.7 billion. Jacobs Solutions Inc has 45,000 employees and revenue of $11.5 billion.

Quanta Services, at nearly twice MasTec's revenue, represents the industry leader. EMCOR Group provides facilities construction services. Dycom focuses on specialty telecommunications contracting. Competition for major projects is intense, with pricing pressure a constant factor.

Hamilton's Seven Powers Analysis

Scale Economies: STRONG ✅

"We believe that the addition of Henkels, coupled with MasTec's existing operations, creates a market leading utility contractor with significant expertise, scale and capacity that can provide a complete and compelling suite of service offerings to our customers."

MasTec's scale enables: - Competitive bidding on large projects that smaller contractors cannot handle - Equipment utilization efficiency across multiple projects - Procurement leverage with suppliers - Ability to absorb project cost overruns without existential risk

Network Effects: LIMITED ❌

Infrastructure construction does not benefit significantly from network effects. Adding more customers or projects does not inherently make the service more valuable to other customers.

Counter-Positioning: MODERATE ✅

MasTec's diversification strategy represents counter-positioning against pure-play contractors. By serving communications, energy, and power delivery markets simultaneously, MasTec can reallocate resources as market conditions shift—something that specialized competitors cannot easily replicate without cannibalizing existing business.

Switching Costs: MODERATE ✅

Master Service Agreements create modest switching costs through: - Established operational procedures - Trained workers familiar with customer systems - Institutional knowledge of customer infrastructure - Relationship value accumulated over decades

The 20+ year BellSouth relationship demonstrates how these costs accumulate over time.

Branding: LIMITED ❌

Infrastructure construction is not a brand-driven business. Customers select contractors based on capabilities, pricing, and track record rather than brand equity.

Cornered Resource: MODERATE ✅

Skilled labor represents a partially cornered resource. In a tight labor market, MasTec's trained workforce provides competitive advantage. Today, MasTec has more than 35,000 team members serving multiple industries in more than 840 locations throughout the U.S., Mexico and Canada.

Process Power: STRONG ✅

Decades of experience in infrastructure construction have embedded operational efficiencies that new entrants cannot easily replicate. The knowledge Jorge Mas Canosa gained by climbing into trenches in 1969 has evolved into institutional process capabilities across the organization.

Competitive Positioning Summary

MasTec occupies a differentiated position as a diversified infrastructure contractor with meaningful scale, counter-positioning advantages, and process capabilities. The company lacks the dominant market position of Quanta Services but offers superior diversification across end markets.

The primary competitive risk is margin pressure from larger competitors like Quanta who can leverage greater scale, or from smaller specialized players who may accept lower margins on specific project types.

Key Performance Indicators (KPIs) for Ongoing Monitoring

For investors tracking MasTec's ongoing performance, three metrics deserve particular attention:

1. Backlog Growth and Composition

The company achieved a record 18-month backlog of $14.3 billion, representing a $1.9 billion increase over 2023.

Backlog represents contracted future revenue and provides visibility into near-term performance. More importantly, the composition of backlog indicates strategic direction. Investors should monitor: - Total backlog absolute levels - Segment mix (Communications vs. Power Delivery vs. Clean Energy vs. Pipeline) - MSA versus project-based work proportion - Geographic diversification

A declining backlog or shift toward lower-margin segments would signal concern.

2. EBITDA Margin Progression

The path to profitability improvement runs through margin expansion. MasTec has historically operated at margins below competitors like Quanta Services. The integration of INTREN, Henkels & McCoy, and IEA should produce margin improvement as synergies are realized.

Key margin targets: - Corporate adjusted EBITDA margin target of 8.5%+ (versus 8.0% achieved in Q4 2024) - Segment margin improvement, particularly in Clean Energy where IEA integration continues - Maintenance and improvement of Communications segment margins

3. Net Debt Leverage Ratio

Cash flow from operations surged 63% to $1.1 billion, enabling a Q4 net debt reduction of $318 million and improving the net debt leverage ratio to 1.8x.

The acquisition-heavy strategy of 2021-2022 elevated leverage. The company's ability to generate cash flow and reduce debt indicates both operational performance and balance sheet health. Target leverage below 2.0x provides flexibility for future acquisitions or shareholder returns.

Conclusion: The Infrastructure Play on America's Future

The MasTec story spans nearly a century of American infrastructure development—from two unemployed carpenters during the Great Depression to a Cuban exile rebuilding his life, from the telecommunications boom and bust to today's clean energy transition.

What distinguishes MasTec from typical infrastructure stories is the combination of family continuity and strategic evolution. The Mas family has maintained control through three generations while fundamentally transforming the business multiple times. From telephone networks to fiber optics, from pipelines to wind farms, MasTec has demonstrated an ability to adapt to technological change while maintaining operational excellence.

During Mr. Mas' tenure as CEO, MasTec's revenue has grown from $930 million in 2007 to an expected $12.4 billion in 2024.

A 13x revenue increase in seventeen years represents extraordinary growth for a mature infrastructure company. More importantly, that growth has come with diversification that reduces the concentration risk that nearly destroyed the company during the telecom bust.

For long-term investors, MasTec offers exposure to multiple secular tailwinds—renewable energy, grid modernization, broadband expansion—through a single diversified vehicle. The company's "picks and shovels" positioning means it can benefit regardless of which specific technologies or energy sources ultimately prevail.

The risks are equally clear: competition from larger players like Quanta Services, margin pressure in a labor-constrained environment, integration challenges from the rapid acquisition pace, and regulatory uncertainty around clean energy incentives. The pipeline segment faces particular uncertainty as natural gas infrastructure investment potentially moderates.

But perhaps the most compelling aspect of the MasTec story is what it says about American entrepreneurship. A Cuban exile who fled Castro's regime, who worked as a milkman and shoe salesman to support his family, who borrowed $50,000 to save a failing construction company—that man built something that endures across generations and now helps build America's energy future.

In Jorge Mas Canosa's own words: "I am a Cuban first. I live here only as an extension of Cuba." But the company he founded has become quintessentially American—a builder of the infrastructure that powers modern life, from the telephone networks of the past to the renewable energy installations of the future.

The trenches and manholes where Jorge Mas Canosa learned the construction business in 1969 may seem far removed from today's wind farms and solar installations. But the fundamental insight he discovered there—that success comes from understanding the work, serving customers, and building relationships that last—remains at the core of MasTec's competitive advantage.

For those investing in America's infrastructure future, MasTec represents both a legacy and a proposition: that family businesses can compete in public markets, that diversification can protect against industry disruption, and that building things that matter—the cables, towers, pipelines, and power lines that connect and power modern society—remains a viable path to creating enduring business value.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube