MP Materials: America's Rare Earth Renaissance

I. Introduction: The Hedge Fund Manager Who Bought America's Strategic Future

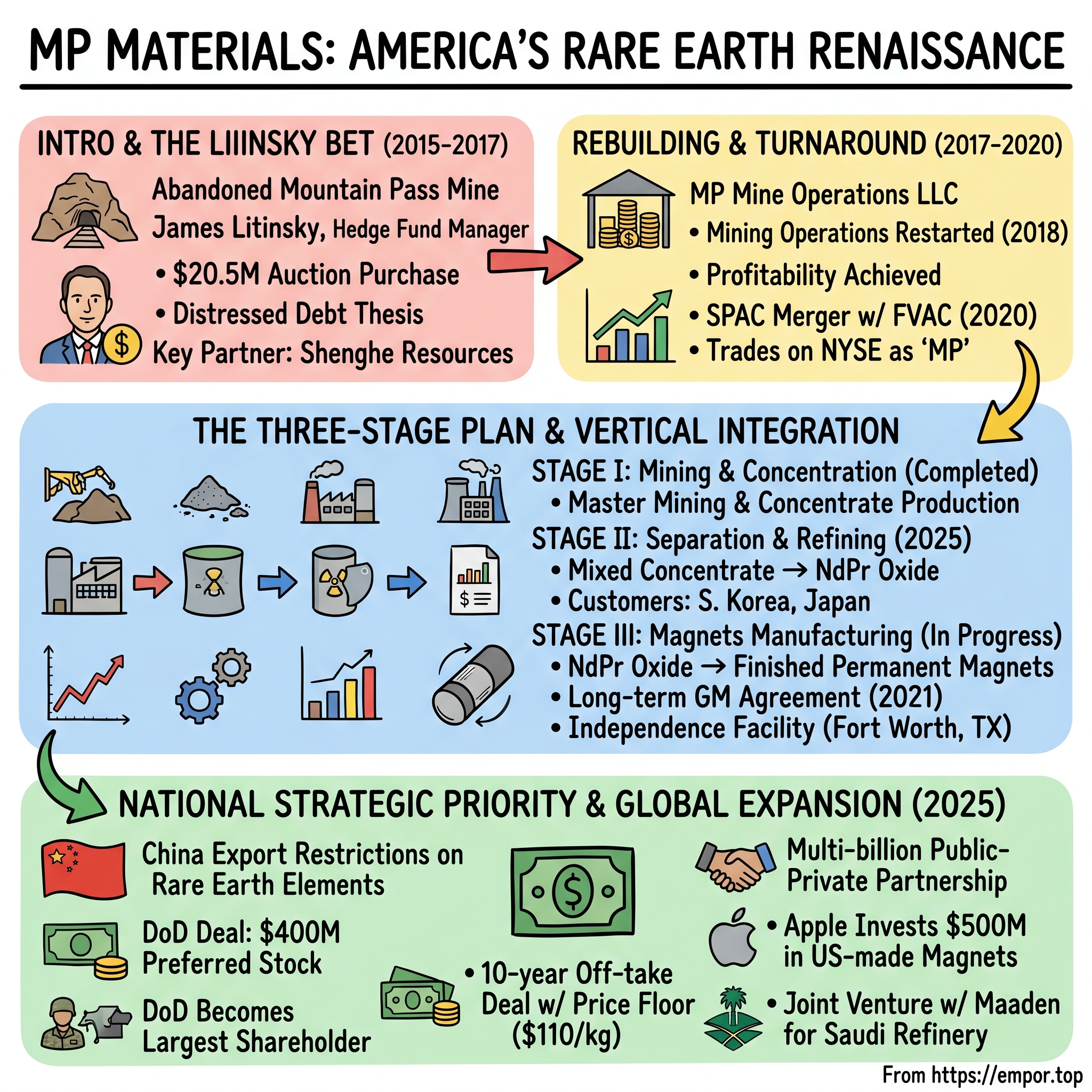

Picture the Mojave Desert in 2016—a blistering expanse of sand and sagebrush stretching toward the Clark Mountain Range. Hidden among those rust-colored peaks sits an abandoned industrial complex, its processing towers silent, its massive open pit still carved into ancient carbonatite. This is Mountain Pass, once the crown jewel of American rare earth production, now reduced to a skeleton crew of eight caretakers watching over $1.25 billion worth of mothballed equipment.

Into this desolation drives James Litinsky, a 40-year-old hedge fund manager from Chicago. He has never operated a mine. He has no background in metallurgy, chemistry, or minerals processing. What he does have is $300 million in Molycorp bonds—debt instruments from the bankrupt previous owner—and a growing conviction that something extraordinary lies beneath his feet.

The Mountain Pass mine was purchased at auction for $20.5 million by a new entity called MP Mine Operations LLC (MPMO). MPMO was a consortium formed principally by JHL Capital Group, a Chicago-based investment firm led by James Litinsky, along with QVT Financial LP and Shenghe Resources. That $20.5 million represented roughly 1.6% of the capital Molycorp had poured into the facility just years earlier. It was either the deal of the century or financial suicide.

Today, MP Materials stands at the center of one of the most consequential geopolitical struggles of the 21st century. The Defense Department will become the largest shareholder in rare earth miner MP Materials after agreeing to buy $400 million of its preferred stock. Shares of MP Materials have nearly quadrupled since the start of the year, pushing the miner's market capitalization to nearly $10 billion.

How did a distressed asset play become a national strategic priority? How did a bondholder become the steward of America's rare earth independence? And what does MP Materials reveal about the new era of great power competition—where supply chains are weapons and minerals are sovereignty?

This is the story of rare earth elements, the invisible foundation of the modern world, and one company's mission to restore American leadership in an industry abandoned decades ago.

II. Rare Earths 101: The Not-So-Rare Elements That Power Everything

The name is misleading. Rare earth elements are neither particularly rare nor, strictly speaking, earth. The seventeen chemically similar metallic elements—the fifteen lanthanides plus scandium and yttrium—are scattered throughout the planet's crust in concentrations that dwarf gold or platinum. Cerium, the most abundant, exists in quantities comparable to copper. Yet "rare earths" has stuck since 1788, when Swedish scientist Carl Axel Arrhenius discovered a peculiar black mineral near a village called Ytterby.

The reality is more nuanced. Rare-earth elements are a select group of 17 chemical elements that are widely dispersed throughout Earth's crust, but at low amounts. Compared to other mineral commodities, REEs are rarely found in concentrations abundant enough to be mined. The challenge has never been geological scarcity—it's economic extractability. These elements rarely concentrate into mineable deposits, and when they do, separating them from each other demands extraordinary chemical precision.

MP Materials focuses its production on Neodymium-Praseodymium (NdPr), a rare earth material used in high-strength permanent magnets that power the traction motors found in electric vehicles, robotics, wind turbines, drones and other advanced motion technologies. This compound represents the economic heart of the rare earth industry—the ingredient that makes possible the most powerful permanent magnets ever created.

Consider what happens inside your smartphone when it vibrates. A tiny neodymium magnet, smaller than a pea, oscillates with enough force to shake a device through clothing. The same physics, scaled up, drives the motors in a Tesla Model 3, where rare earth magnets generate sufficient torque to accelerate 4,000 pounds of metal from zero to sixty in under four seconds. Wind turbines stretching 500 feet into the air rely on permanent magnet generators that can weigh over 5,000 pounds—each containing hundreds of kilograms of NdFeB magnets.

NdFeB magnets are the dominant rare earth magnet technology, representing 96% of global demand in 2025. IDTechEx expects robotics demand for rare earth magnets to take-off in 2025, with humanoid robots a key growth segment. Over 95% of motors used in humanoid robots contain rare earth permanent magnets, where NdFeB magnets are critical for providing high torque density and energy efficiency. Moreover, humanoid robots contain an average of 40 motors per unit, further driving magnet volume demand.

The defense implications are equally stark. Every F-35 fighter jet contains approximately 920 pounds of rare earth materials. Tomahawk cruise missiles, Predator drones, satellite guidance systems, submarine propulsion—all depend on rare earth permanent magnets. A Virginia-class attack submarine requires roughly 9,200 pounds of rare earths.

Rare earth metals are indispensable for producing high-performance permanent magnets, key components in many clean energy technologies, such as wind turbines. However, the limited availability and environmental impact of rare earth mining, processing, and purification pose challenges for the green energy transition.

The supply chain that transforms rock into magnets spans at least six stages: mining the ore, concentrating it, chemically separating individual elements, refining those elements to high purity, converting oxides to metals, alloying the metals, and finally manufacturing finished magnets. Each step requires specialized expertise accumulated over decades. Each step presents an opportunity for chokepoint control.

III. Mountain Pass: America's Lost Crown Jewel (1949–2002)

The discovery happened by accident. In 1949, three prospectors sought uranium in the Clark Mountain Range in the midst of high demand for the element during the developing Cold War. However, instead of uranium, the prospectors struck bastnaesite, which contains rare-earth elements found in familiar gadgets we use today.

The Mountain Pass rare earth deposit was discovered on April 23, 1949, when prospectors Herbert S. Woodward, Clarence Watkins, and P.A. Simon, motivated by a lecture on uranium prospecting, used a Geiger counter to identify radioactive bastnasite. The Geiger counter readings were anomalous—high enough to suggest uranium, but the radiation came from thorium impurities in a different mineral entirely. When U.S. Geological Survey geologist D.F. Hewett analyzed samples that July, he recognized what the prospectors had found: one of the richest rare earth deposits on Earth.

By the early 1950s, the Molybdenum Corporation of America began extracting rare earth elements (REEs), making it one of the first large-scale REE operations outside Asia. The company, known informally as Molycorp, initially produced rare earths for modest applications—lighter flints, glass polishing compounds, petroleum refining catalysts. But the 1960s brought an application that would transform Mountain Pass into a global powerhouse.

Color television required europium. The red phosphors coating cathode ray tubes needed this specific rare earth element to produce vibrant reds, and Mountain Pass contained it in commercially viable concentrations. Throughout the 1960s and 70s, Mountain Pass emerged as the world's leading supplier of rare earths. The mine's primary products were cerium, lanthanum, neodymium, and praseodymium. These REEs became increasingly crucial for applications such as color televisions, military lasers, and early computing systems.

Discovered in 1949 and entering production in 1952 under the Molybdenum Corporation of America (Molycorp), the mine dominated global REE supply through the 1980s, accounting for over 70% of world production at its peak.

The geology at Mountain Pass defied expectations. The Mountain Pass deposit is in a 1.4 billion-year-old Precambrian carbonatite intruded into gneiss. It contains 8% to 12% rare-earth oxides, mostly contained in the mineral bastnäsite. Carbonatites—igneous rocks rich in carbonate minerals—rarely form, and even more rarely concentrate rare earths to ore grades. Mountain Pass represented a geological fluke: 1.4 billion years ago, unusual magmatic processes had deposited rare earths in concentrations ten to one hundred times typical crustal abundance.

Molybdenum Corporation of America changed its name to Molycorp in 1974. The corporation was acquired by Union Oil in 1977, which in turn became part of Chevron Corporation in 2005.

But environmental liability was accumulating. The mine piped wastewater to evaporation ponds near Ivanpah Dry Lake, and pipeline leaks contaminated soil and groundwater. The mine closed in 2002 after a toxic waste spill, and then wasn't reopened due to competition from Chinese suppliers, though processing of previously mined ore continued.

By the time Mountain Pass fell silent, a new force had emerged to dominate global rare earth production—one that had spent two decades preparing precisely for this moment.

IV. Inflection Point #1: Deng Xiaoping's Strategic Vision (1980s–2000s)

In 1992, while visiting Baotou, Inner Mongolia, one of China's biggest rare earth mines, Chinese leader Deng Xiaoping famously said, "The Middle East has oil, China has rare earths." But unlike the Middle Eastern oil producing countries who primarily drill and export crude, China built an entire ecosystem around the rare earths.

That single sentence—seven words in Mandarin, twelve in English—encapsulated one of the most prescient resource strategies of the late 20th century. Deng Xiaoping captured PRC's strategic view of rare earths in 1992, saying, "There is oil in the Middle East, there is rare earth in China." This began the CCP's efforts to control global supply chains, weaponize them, and then deploy them against the United States and its allies.

While Western economies chased the dot-com boom and celebrated the "end of history," Beijing executed a decades-long industrial policy with systematic precision. During the 1980s and 1990s, while Western nations were preoccupied with information technology and financial deregulation, China quietly built an industrial base rooted in resource control. Aggressive state incentives, cheap credit, and permissive environmental policies allowed China to rapidly scale extraction and refining. This flood of low-cost supply depressed global prices and forced competitors in the United States and Australia out of the market.

The strategy worked through what economists call environmental arbitrage. Rare earth separation and refining are complex, chemically intensive processes that generate large volumes of toxic waste. Western producers faced strict environmental standards and high cleanup costs; China tolerated the pollution as the price of industrial ascendancy.

A critical turning point came in 1995, when General Motors sold its subsidiary Magnequench—a company that had pioneered rare earth permanent magnet manufacturing and supplied magnets for precision-guided munitions. In the early 1990s, a General Motors subsidiary called Magnaquench was producing 85 percent of the magnets used in precision-guided missiles and other defense systems. When GM sold the company in 1995 to a consortium that included two Chinese entities, the consequences were immediate.

The sale transferred not just manufacturing capability but irreplaceable know-how. Within years, Magnequench's U.S. facilities closed, and production shifted to China. The United States had effectively handed over strategic intellectual property for short-term shareholder returns.

China has maintained leadership at every step up the ladder. Though its global production share dipped from a staggering 97% in 2011 to around 70% in 2022, it still controls over 85% of processing capacity. China has an effective monopoly over processing major heavy rare earths.

The numbers today tell the story of total supply chain dominance. Three decades later, China commands an overwhelming monopoly over the rare earth ecosystem controlling 70 percent of global mining, 90 percent of refining, and over 93 percent of permanent magnet production.

This wasn't luck or geological accident. China holds perhaps 36% of known rare earth reserves—significant but far from monopolistic. Its dominance stems from deliberate policy: subsidized production, tolerated environmental damage, strategic acquisitions, and accumulated processing expertise that took decades to develop.

V. Inflection Point #2: Molycorp's Rise and Spectacular Fall (2008–2015)

In September 2008, Chevron Mining sold Mountain Pass to a newly formed entity called Molycorp Minerals LLC. In 2008, Chevron sold the mine to privately held Molycorp Minerals LLC, a company formed to revive the Mountain Pass mine. Molycorp announced plans to spend $500 million to reopen and expand the mine, and on July 29, 2010, it raised about $400 million through an initial public offering, selling 28,125,000 shares at $14 under the ticker symbol MCP on the New York Stock Exchange.

The timing seemed impeccable. In September 2010, a Chinese fishing trawler collided with Japanese Coast Guard vessels near the disputed Senkaku Islands. China was accused of unofficially banning of rare earths exports to Japan during a diplomatic standoff between the two countries after the 2010 Senkaku boat collision incident, though China denies such reports.

The market response was immediate and violent. The incident caused prices to surge by up to 500% in 2011 and 2012, driven by speculation, and this impelled heightened awareness in the West about Chinese dominance.

Molycorp's stock price exploded. From an IPO price of $14 in July 2010, shares rocketed to $79.16 by May 2011—a 465% gain in less than a year. Wall Street analysts proclaimed a new commodity super-cycle. Molycorp management embarked on an ambitious expansion dubbed "Project Phoenix," targeting $1.25 billion in capital spending to create a state-of-the-art, vertically integrated rare earth production facility.

At first the situation looked promising. Chinese companies restricted rare earth exports to Japan over a diplomatic dispute in 2010, leading prices to spike. Molycorp's stock would later soar. The cash-rich company announced several acquisitions—processing plants in Arizona and Estonia as well as a Canadian rare earth technology group named Neo Materials that had extensive operations in China. But in actuality, Molycorp was struggling to stay solvent.

The problem was classic commodity hubris. Molycorp had bet everything on permanently elevated prices, but China still controlled the global market's pricing mechanism. When Beijing relaxed export restrictions following a 2014 WTO ruling, rare earth prices collapsed. When China subsequently relaxed export rules, however, prices fell, leaving Molycorp to pay the bill for a $1.25 billion state-of-the-art processing facility.

The processing plant was in full production on June 25, 2015, when Molycorp filed for Chapter 11 bankruptcy with outstanding bonds in the amount of $1.4 billion. The company's shares were removed from the NYSE.

The stock that had traded at $79 went to zero. Molycorp ended its corporate life at a price of 35 cents per share, less than one two-hundredth of what it went for at its all-time high: $79.16, on May 3, 2011.

America's brief rare earth renaissance had ended in financial catastrophe. Mountain Pass was the only rare earths mine operating in the United States, before it went bankrupt in 2015—a victim of low rare earth oxide prices. At the time Molycorp listed $1.7 billion in debt.

VI. Inflection Point #3: The Litinsky Bet—From Bondholder to Mine Owner (2015–2017)

James Litinsky's path to Mountain Pass ran through distressed debt markets. Prior to establishing MP Materials, James founded JHL Capital Group in 2006, a multibillion-dollar alternative investment firm, where he served as CEO and CIO. His education—a B.A. in Economics, cum laude from Yale University, followed by a J.D. and M.B.A. from Northwestern University School of Law and the Kellogg School of Management—reflected the hybrid financial-legal mindset that excels in bankruptcy investing.

Earlier in his career, James worked at Fortress Investment Group, served as Director of Finance at Omnicom Group, and was a merchant banker at Allen & Company. His time at Fortress, in particular, had exposed him to distressed situations—companies whose operational fundamentals exceeded their capital structure's capacity to survive.

JHL Capital had purchased Molycorp bonds during the bankruptcy proceedings. The thesis was straightforward distressed investing: acquire senior secured debt at a discount, receive recovery value through restructuring. But something changed when Litinsky visited Mountain Pass.

What he found contradicted every expectation. Molycorp's failure hadn't been operational—it had been financial and timing-related. The processing facility was genuinely state-of-the-art. The geology remained world-class. The infrastructure—tailings systems, water treatment, crushing and flotation circuits—represented over a billion dollars of invested capital sitting idle in the desert sun.

At the time, Mountain Pass was in a state of "care and maintenance" and had only eight employees according to Litinsky.

The bankruptcy auction attracted minimal competition. The eventual sale price was significantly higher than ERP's original "stalking horse" offer of $1.2 million back in April. MP Mine Operations (MPMO) put in a winning bid of $20.5 million.

In June 2017, the Mountain Pass mine was purchased at auction for $20.5 million by a new entity called MP Mine Operations LLC (MPMO). MPMO was a consortium formed principally by JHL Capital Group, a Chicago-based investment firm led by James Litinsky, along with QVT Financial LP and Shenghe Resources. Shenghe Resources held a minority, non-voting interest.

The Shenghe partnership proved essential but controversial. Shenghe Resources, a Chinese rare earth trading company partly owned by China's Ministry of Natural Resources, provided something no American or European partner could: guaranteed offtake for the concentrate and processing expertise. In 2017, there was literally no other option for monetizing Mountain Pass production—the entire downstream supply chain existed in China.

The strategic calculation was uncomfortable but pragmatic: use Chinese capital and market access to rebuild American production capacity, then gradually reduce dependence as domestic capabilities matured.

VII. The Turnaround: Rebuilding Mountain Pass (2017–2020)

MP's co-founders, together with an original team of eight, restart mining operations at Mountain Pass and embark on a mission to restore the full rare earth supply chain in the United States.

The turnaround proceeded faster than almost anyone expected. MP Materials resumed mining and refining operations in January 2018. By the end of that first full year, Mountain Pass had produced 14,000 metric tons of rare earth oxides in concentrate. The following year, output doubled to 28,000 tons.

MP stabilizes production at a run-rate exceeding 30,000 MT of contained TREO, or ~15% of global production.

The economics surprised industry observers. Molycorp had struggled with crushing operating costs; MP Materials achieved profitability almost immediately. The difference lay in operational discipline and realistic expectations. Where Molycorp had attempted to become a fully vertically integrated producer overnight, MP Materials followed a staged approach: master mining and concentration first, then tackle separation, then downstream processing.

Up until 2022, MP earned 95+% of its revenues by selling the vast majority of its rare-earth concentrate to the trading affiliate of Shenghe Resources (Shenghe), a Chinese rare-earth company, which then sold it to Chinese refiners for processing.

This dependency represented MP's original sin and its survival strategy simultaneously. Critics pointed out that American rare earths were simply being shipped to China for processing—hardly independence. Defenders noted that without the Shenghe relationship, the mine would have remained closed and the deposits unmined.

The SPAC merger in 2020 represented a strategic inflection point. MP Materials, the largest rare earth materials producer in the Western Hemisphere, today announced the completion of its business combination with Fortress Value Acquisition Corp. (NYSE: FVAC), a special purpose acquisition company sponsored by an affiliate of Fortress Investment Group LLC. The combined company, MP Materials Corp., will begin trading on the New York Stock Exchange (NYSE) tomorrow, November 18th, under the ticker symbol "MP".

MP Materials is expected to deliver over $100 million in estimated revenue and nearly $30 million in estimated Adjusted EBITDA in 2020. The net proceeds raised from the transaction will be used to fund MP Materials' strategic plan to retrofit and fully recommission its existing on-site refining facilities.

The transaction valued the combined company at approximately $1.5 billion and provided capital for what management called a "three-stage plan" to restore the full rare earth supply chain domestically.

VIII. Inflection Point #4: The Three-Stage Plan & Vertical Integration (2020–Present)

MP Materials' strategy acknowledged a fundamental truth: owning a mine isn't the same as owning a supply chain. The company articulated three stages of vertical integration:

Stage I: Mining and Concentration (Completed) Mountain Pass already excelled at extracting bastnäsite ore and processing it into mixed rare earth concentrate. This established the foundation—consistent, high-quality feedstock from the world's second-richest rare earth deposit.

Stage II: Separation and Refining The critical middle step: transforming mixed concentrate into individual purified rare earth oxides, particularly the prized NdPr. By the first quarter of 2025, 40% of MP's revenues were from oxide sales. The company has sold oxide primarily to customers in South Korea and to Sumitomo Corporation via a distributorship agreement for sales to customers in Japan.

Stage III: Magnets Manufacturing The highest-value portion of the supply chain: converting rare earth metals into finished permanent magnets for automotive, defense, and industrial applications.

In December 2021, MP Materials signed a long-term agreement with General Motors to provide neodymium-iron-boron magnets for use in GM's electric vehicle motors. As part of the contract, MP Materials also agreed to provide alloy and finished magnets to GM for its electric vehicles and to open a new factory located in Fort Worth, Texas to produce the magnets.

Under the long-term agreement, MP Materials will supply U.S.-sourced and manufactured rare earth materials, alloy and finished magnets for the electric motors used in the GMC HUMMER EV, Cadillac LYRIQ, Chevrolet Silverado EV and more than a dozen models using GM's Ultium Platform.

The Independence facility in Fort Worth, Texas, broke ground in April 2022. MP's initial magnetics facility will have the capacity to produce approximately 1,000 tonnes of finished NdFeB magnets per year with the potential to power approximately 500,000 EV motors annually.

Production records continued to accumulate. MP Materials achieved record production of 45,455 metric tons of REO in concentrate in 2024 and produced record 1,294 metric tons of NdPr oxide in 2024.

MP Materials increased revenues 48% year over year to $61.0 million in Q4 2024. "MP had a terrific year of execution across our materials and magnetics divisions," said MP Materials Chairman and CEO, James Litinsky. "Notably, we achieved record upstream and midstream production at Mountain Pass and, in the fourth quarter, commenced commercial production of NdPr metal and trial production of automotive-grade magnets at Independence."

IX. Inflection Point #5: The DoD Deal & Apple Investment (2025)

The escalation arrived in April 2025. On April 4, 2025, the Ministry of Commerce introduced export restrictions on seven rare earth elements in retaliation for President Trump's new tariffs on Chinese goods.

In April 2025, first-of-their-kind export restrictions were imposed by China on NdFeB and SmCo magnet materials, stalling critical material supply to original equipment manufacturers across the world.

Export data from May 2025 shows that China's total exports of rare earth magnets fell by 74% year-over-year to 1.2 million kilograms, the lowest level since February 2020 during the COVID-19 pandemic. The US-specific decline was even higher, with shipments of rare earth magnets to the US plummeting by 93.3% year-on-year in May.

The Pentagon's response came in July. MP Materials has entered a multi-billion-dollar public-private partnership with the US Department of Defense (DoD) to build a domestic supply chain for rare earth magnets, reducing America's reliance on foreign sources. The deal will make the DoD the largest shareholder in MP Materials, after acquiring $400 million worth of preferred stock.

As a result of the strategic investment, DoD is positioned to become the Company's largest shareholder. On an as-converted and as-exercised basis, the convertible preferred stock and the warrant represent, in the aggregate, 15% of the Company's issued and outstanding shares of common stock.

The deal structure reflects lessons learned from Molycorp's failure. The DoD has signed a 10-year off-take deal that establishes a price floor of $110 per kilogram for neodymium-praseodymium (NdPr) materials. "The price floor not only guarantees stable revenue for MP but also sends a strong price signal across the sector."

Companies such as MP have been struggling to compete in the current rare-earth price environment—to wit the NdPr decade-long price guarantee of $110/kg in the deal is over twice MP's realized prices of $51/kg in 2024.

"I want to be very clear, this is not a nationalization," Litinsky told CNBC. "We remain a thriving public company. We now have a great new partner in our economically largest shareholder, DoD, but we still control our company. We control our destiny. We're shareholder driven."

MP Materials will build its second magnet manufacturing facility in the U.S. to serve defense and commercial customers with support from the Pentagon. The facility, whose location wasn't disclosed, is expected to start commissioning in 2028.

Days later, Apple announced its own strategic bet. Apple announced a new commitment of $500 million with MP Materials, the only fully integrated rare earth producer in the United States. With this multiyear deal, Apple is committed to buying American-made rare earth magnets developed at MP Materials' flagship Independence facility in Fort Worth, Texas.

The two companies will also work together to establish a cutting-edge rare earth recycling line in Mountain Pass, California, and develop novel magnet materials and innovative processing technologies to enhance magnet performance.

MP Materials plans to start shipping magnets in 2027.

The most recent development came in November 2025. MP Materials partnered with the U.S. Department of War to establish a strategic joint venture with the Saudi Arabian Mining Company (Maaden) to develop a rare earth refinery in the Kingdom. The formation of a joint venture to build a rare earth refinery in Saudi Arabia is a pivotal step toward rebalancing the global rare earth supply chain.

The company's stock rose 8.61% to close at $63.55, bringing its year-to-date gain to nearly 290%.

X. The Market Opportunity: EVs, Wind, Robotics, and Beyond

The secular trends driving rare earth demand are structural, not cyclical. IDTechEx forecasts that the rare earth magnet market will grow to US$9.19B in annual revenue by 2036, driven by growing demand in e-mobility, wind energy and robotics applications.

The Rare Earth Magnets Market is projected to be USD 21.98 billion in 2025 and reach USD 30.01 billion by 2030, at a CAGR of 6.4%.

Electric vehicles represent the largest demand driver. Each EV motor typically requires 1-3 kilograms of NdFeB magnets, with some high-performance applications demanding more. As global EV production scales from tens of millions to hundreds of millions of units annually, rare earth magnet demand will grow proportionally.

Upwards trends in magnet demand for wind turbine applications are compounded by the increasing adoption of direct drive permanent magnet synchronous generators, which typically require more NdFeB than geared systems.

IDTechEx forecasts that rare earth magnet weight demand in robotics will increase seven times by 2036, as major adopters such as BYD and Tesla employ humanoid robots in automotive assembly applications.

The emerging "physical AI" applications—humanoid robots, autonomous systems, advanced manufacturing—represent blue-sky demand that didn't exist a decade ago.

CEO Jim Litinsky highlighted the strategic importance of self-sufficiency, stating, "We are now locked in a new kind of Cold War, a race of mutually assured economic destruction, fought not with weapons but with supply chains."

XI. Playbook: Business & Investing Lessons

Distressed Asset Investing Done Right

Litinsky's journey from bondholder to mine owner illustrates a classic distressed investing playbook executed with unusual discipline. Most distressed investors seek recovery value; Litinsky recognized operational potential that the market had mispriced due to Molycorp's financial trauma. The lesson: separate operational fundamentals from capital structure problems.

The Shenghe Paradox

MP Materials' Chinese partnership exemplifies the uncomfortable compromises required to build competitive positions in concentrated industries. Without Shenghe, the mine might have remained closed for years; with Shenghe, critics questioned whether American rare earths shipped to China represented genuine progress. The resolution came through staged independence: use the partnership to establish viability, then systematically reduce dependence as domestic capabilities mature.

Government as Strategic Partner

The DoD deal represents a new model for public-private cooperation in strategic industries. The price floor mechanism—guaranteeing $110/kg when market prices were $51/kg—acknowledges that private capital alone cannot build supply chains to compete with state-subsidized Chinese production. This isn't subsidy in the traditional sense; it's risk-sharing that aligns corporate incentives with national security objectives.

Vertical Integration as Moat

MP Materials' three-stage strategy reflects a fundamental truth about commodities: mining captures value, but processing captures more, and finished products capture most. By integrating from mine to magnet, MP positioned itself to capture value at every step while reducing vulnerability to any single market disruption.

XII. Bull Case vs. Bear Case: Analytical Framework

The Bull Case

Strategic Asset Premium: MP Materials operates the only rare earth mine in the United States—a position that cannot be replicated without decades of permitting, construction, and environmental remediation. Scarcity confers pricing power.

Government Backstop: The DoD price floor eliminates downside risk from Chinese price manipulation—the mechanism that destroyed Molycorp. For ten years, MP has guaranteed economics regardless of global pricing dynamics.

Multiple Customer Moats: Long-term agreements with the Department of Defense, General Motors, and Apple provide revenue visibility rare in commodity businesses. Customer prepayments totaling $150 million from GM demonstrate commitment.

Secular Demand Growth: Every major secular trend—electrification, automation, defense modernization, data center expansion—increases rare earth demand. MP sits at the intersection of multiple growth vectors.

The Bear Case

Execution Risk: Transitioning from mining to integrated magnet manufacturing requires mastering capabilities that took China decades to develop. The Independence facility must achieve cost parity with Chinese competitors operating at massive scale.

Price Floor Dependency: The $110/kg guarantee lasts ten years—then what? If MP cannot achieve competitive economics by 2035, the company faces renewed exposure to Chinese price manipulation.

Customer Concentration: Dependence on a handful of large customers creates revenue concentration risk. GM's EV program rollout has faced challenges; Apple's magnet requirements represent a relatively small portion of global demand.

China Response: Beijing retains multiple tools to pressure Western rare earth initiatives. Export restrictions in 2025 demonstrated willingness to weaponize supply chains; future escalation could disrupt MP's customer base or supply chain partners.

Porter's Five Forces Analysis

Supplier Power (Low): MP controls its own mining operation—no upstream supplier dependency.

Buyer Power (Moderate): Large customers like GM and Apple can negotiate favorable terms, but strategic necessity limits their alternatives.

Threat of New Entrants (Low-to-Moderate): Permitting timelines, environmental regulations, and capital requirements create substantial barriers; however, government subsidies may attract new projects.

Threat of Substitutes (Low): No commercially viable alternatives to NdFeB magnets exist for high-performance applications. Research continues on rare-earth-free motors, but permanent magnet motors maintain fundamental efficiency advantages.

Competitive Rivalry (Low in U.S., High Globally): MP has no domestic competitors of comparable scale; globally, Chinese producers dominate with massive cost advantages.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Mountain Pass benefits from fixed-cost spreading across increasing production volumes. The 45,000+ MT annual output represents scale advantage versus potential entrants.

Network Effects: Not directly applicable to commodity production.

Cornered Resource: MP controls the only operational U.S. rare earth mine—a genuine cornered resource that cannot be replicated without decades of development.

Counter-Positioning: Government partnerships and defense applications create positioning that Chinese competitors cannot easily match due to regulatory and security barriers.

Switching Costs: Customer integration (particularly in automotive qualification) creates modest switching costs, though not as pronounced as in software or technology businesses.

Branding: Limited applicability in B2B commodity context.

Process Power: Accumulated expertise in domestic rare earth processing—expertise that took years to develop and cannot be easily transferred.

XIII. Key Performance Indicators for Investors

For investors tracking MP Materials' ongoing execution, three metrics deserve primary focus:

1. NdPr Production Volume (metric tons/quarter)

This measures MP's progress on Stage II—the critical transition from concentrate exporter to separated products producer. Q3 2025 achieved record NdPr oxide production of 721 metric tons, more than double year-ago levels. Watch for continued volume growth as separation capacity ramps.

2. Realized NdPr Price vs. Benchmark

The spread between MP's realized pricing and the DoD price floor ($110/kg) indicates how much government support is actually required. In 2024, realized prices averaged approximately $51/kg—less than half the guaranteed floor. Narrowing this gap would demonstrate improving market fundamentals.

3. Magnetics Segment Revenue and Adjusted EBITDA

Revenues in the Magnetics segment were $21.9 million for the three months ended September 30, 2025, as the initial magnetic precursor product deliveries began during the first quarter of 2025. This segment represents MP's future—tracking its path to profitability signals progress on Stage III vertical integration.

XIV. Risks, Regulatory Overhangs, and Accounting Considerations

Material Risks: - China retaliation: Beijing has repeatedly demonstrated willingness to weaponize rare earth supply. Future export restrictions could disrupt MP's customer base or force production cutbacks. - Commodity price volatility: Despite the DoD price floor, prices below floor levels require government payments that could face political scrutiny. - Execution risk: Manufacturing sintered NdFeB magnets at commercial scale and competitive cost has never been achieved in the United States. Technical challenges could delay timelines.

Regulatory Considerations: - Environmental permits: Rare earth processing generates radioactive thorium waste. Any environmental incidents could trigger regulatory review and operational disruption. - CFIUS scrutiny: The Shenghe relationship remains subject to regulatory oversight. Any future national security concerns could complicate the partnership.

Accounting Judgment Areas: - Customer prepayments: MP has received $150 million in prepayments from GM for magnetic precursor products. Revenue recognition timing affects reported results. - Capitalized development costs: Stage II and Stage III investments are capitalized; accelerated depreciation could materially impact reported earnings as facilities enter service. - Government grants and credits: The $58.5 million Section 48C tax credit and various DoD awards involve complex accounting treatment affecting cash flow presentation.

XV. Conclusion: The New Great Game

In 1949, three prospectors hunting uranium stumbled upon a geological anomaly in the California desert. Seventy-six years later, that discovery has become a linchpin of American industrial strategy—a strategic asset at the center of great power competition between the world's two largest economies.

MP Materials' journey from abandoned mine to national champion reflects broader truths about 21st-century geopolitics. Supply chains are not neutral infrastructure; they are vectors of power. Minerals are not just commodities; they are strategic assets that determine which nations can build advanced technologies. The company that controls the rare earths controls the magnets; the nation that controls the magnets shapes the future of transportation, defense, and energy.

The administration has made sure that we have a successful national champion in MP. We've got to execute.

James Litinsky, the hedge fund manager who never intended to run a mine, now leads an enterprise central to American technological sovereignty. The bondholder became the steward; the distressed investment became a national priority.

Whether MP Materials can execute its vision—building an integrated mine-to-magnet supply chain competitive with Chinese incumbents who have three decades of accumulated advantage—remains uncertain. What seems clear is that the attempt will be made, backed by billions in government capital and strategic partnerships with America's most important defense and technology companies.

The Middle East has oil. China has rare earths. America, for the first time in a generation, is fighting back.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube