Ternium: Latin America's Steel Empire Built from Post-War Vision

I. Introduction: The House That Agostino Built

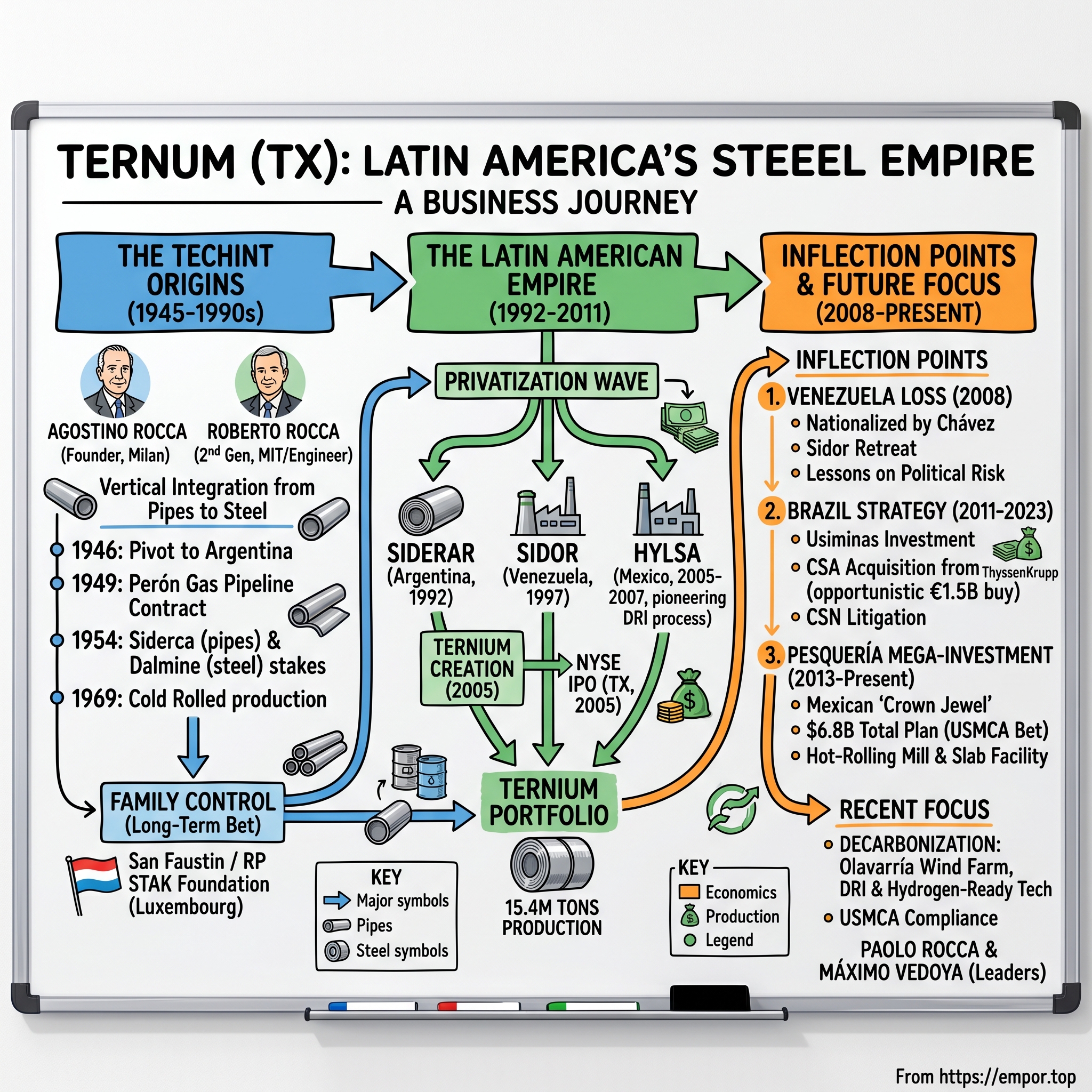

In the industrial heartlands of Nuevo León, Mexico, a sprawling steel complex rises from the desert floor near Monterrey. The Pesquería Industrial Center—with its state-of-the-art hot-rolling mills, cold-rolling facilities, and galvanizing lines—represents the crown jewel of a multi-billion-dollar bet on the future of North American manufacturing. But understanding Ternium requires looking far beyond these Mexican highlands, back across the Atlantic to post-World War II Milan, where an Italian industrialist named Agostino Rocca made a fateful decision that would reshape Latin American industry for the next eight decades.

Ternium is a leading steel producer in the Americas, providing advanced steel products to a wide range of manufacturing industries and the construction sector. The company has an annual production capacity of 15.4 million tons. With a market capitalization that fluctuates around $5-6 billion and trailing twelve-month revenue of approximately $16 billion, Ternium stands as a colossus in Latin American heavy industry—yet it remains relatively obscure to most American investors.

The central question animating this deep dive is both historical and forward-looking: How did an Italian immigrant fleeing post-Mussolini Italy build Latin America's dominant steel empire through privatization waves, geopolitical chaos, and industrial consolidation? And more pressingly, can this empire—built on decades of opportunistic acquisitions, family discipline, and a willingness to operate where others feared to tread—continue to thrive amid the tariff chaos and trade uncertainty reshaping global manufacturing?

In 2023, 55% of its sales were from Mexico; 21% of sales were from Argentina, Bolivia, Chile, Paraguay and Uruguay; 13% of sales were from Brazil; and 11% of sales were from the United States, Colombia and Central America. This geographic concentration tells a story of strategic bets and calculated retreats. The company's heavy Mexican weighting is no accident—it reflects both the USMCA's promise and the scars of a painful Venezuelan expropriation that taught the Rocca family hard lessons about political risk.

The company takes its name from the Latin words Ter (three) and Eternium (eternal) in reference to the integration of the three steel mills. Those three mills—Siderar of Argentina, Sidor of Venezuela (before its nationalization), and Hylsa of Mexico—represented the founding pillars of a pan-Latin American steel champion. Today, only two of those original three remain under Ternium's control, but the name persists as a reminder of both ambition and the volatility inherent in emerging market operations.

Approximately 21% of the company is publicly traded; the remainder is controlled by San Faustin S.A., which is in turn controlled by Rocca & Partners Stichting Administratiekantoor Aandelen San Faustin, a Stichting. This ownership structure—with the founding Rocca family maintaining overwhelming control through a Dutch foundation—is central to understanding Ternium's strategic patience and willingness to make long-term bets that public markets might punish in the short term.

II. Techint Origins: The Rocca Family & Post-War Industrial Vision (1945-1990s)

The Escape from Fascism

The story of Ternium begins not in a steel mill, but in the chaos of a collapsing European order. Born in Milan in 1895, grandfather Agostino Rocca fought in the Italian army in World War I. After the war, he enrolled at the Politecnico di Milano to study engineering, beginning a career that would intertwine with some of the twentieth century's most transformative—and destructive—political movements.

After working in steel and engineering firms, he joined Mussolini's government in the wake of the Great Depression to help oversee the reconstruction of Italy's industry. His role shoring up companies and rejiggering them as defense contractors during the 1930s earned him the title of "inventor of Italy's steel industry," according to Italian newspaper Corriere della Sera.

This description, while flattering, understates the moral complexity of Rocca's position. Supported by Mussolini, Rocca had been entrusted with the direction of the State iron and steel industries, the post of Secretary of the Metallurgical War Industries in 1933. He was, in essence, a key architect of Italy's war machine—building the industrial capacity that would enable Fascist military adventures across North Africa and Europe.

Yet Rocca was also a calculating survivor. The prospect of a German defeat brought him, like other Italian bourgeois, to distance himself from the regime of Mussolini from 1943. He broke with Mussolini before the end of World War II. He founded Techint in Milan in 1945 to bid for engineering contracts around the world.

The timing of Techint's founding—November 1945, mere months after the war's end—suggests a man who had carefully prepared his exit strategy. Initially named Compagnia Tecnica Internazionale, the company—soon abbreviated as Techint—was conceived as an international engineering consultancy amid the post-World War II reconstruction efforts in Europe.

The Argentine Pivot

But Europe, devastated by war and crawling with those who remembered Rocca's Fascist connections, offered limited opportunities. In 1946, Rocca relocated to Argentina, opening the company's first office in Buenos Aires and shifting its primary operations to South America, where opportunities in infrastructure were abundant and questions about one's wartime activities less pointed.

Argentina under Juan Perón proved remarkably hospitable. Awarded a contract to build a 1,600 km gas pipeline from Comodoro Rivadavia to Buenos Aires in 1949 by President Juan Perón, Techint became a leading government contractor during Perón's ambitious infrastructure program. This single contract—stretching over 1,000 miles across the Argentine pampas—transformed Techint from a consulting firm into a major construction enterprise.

Joined by his brother Enrico and a few minority partners, Agostino's focus soon turned to Latin America where he built pipelines and steel factories in Argentina and Mexico. The strategic vision was becoming clear: rather than compete in mature European markets, Techint would become the go-to contractor for developing nations building their industrial infrastructure.

Vertical Integration: From Pipes to Steel

The 1950s marked Techint's transformation from an engineering contractor into a vertically integrated industrial enterprise. Establishing subsidiaries in Brazil (1947), Chile (1951), and Mexico (1954), the company purchased a majority stake in Dalmine (Rocca's erstwhile employer), in 1954, and opened its first seamless steel tube plant in Campana, the same year.

This twin movement—geographic expansion and vertical integration—would become the defining pattern of Techint's growth strategy. By the late 1960s, the company had taken another crucial step. Techint's Ensenada plant, in 1969, became the only Argentine manufacturer of cold rolled steel.

The aging industrialist transferred management of the company to his elder son, Roberto Rocca, in 1975, and died in Buenos Aires on February 17, 1978, at age 83. Techint was, by then, a conglomerate with 15,000 employees, two steel manufacturing facilities in Argentina and with international engineering and construction interests.

Roberto Rocca: Engineering the Second Generation

Roberto Rocca was born in Milan, in 1922, as the eldest son of Maria Queirazza and Agostino Rocca. The elder Rocca was an engineering apprentice who would later become a member of the board of directors of the Istituto per la Ricostruzione Industriale (IRI), the centerpiece of the corporate state advanced by Fascist dictator Benito Mussolini.

Roberto's path reflected both family tradition and strategic positioning. During World War II, Roberto Rocca enlisted in the Italian Navy, serving from June 1942 until September 8, 1943, as a Second Lieutenant in naval engineering on board a submarine. He graduated as mechanical engineer at the Politecnico di Milano in July 1945, though seven months later, the family left Italy for Buenos Aires, Argentina.

His father's new establishment, Techint, prospered during the administration of populist President Juan Perón, and Rocca enrolled at MIT, earning a degree in science at the end of 1949. This combination—Italian industrial heritage, Argentine street smarts, and American technical education—would define Roberto's leadership approach.

He was named head of the technical department in 1959, and oversaw the company's expansion into the steel industry. He became General Manager of Techint at the end of 1969, and CEO upon his father's retirement in 1975.

The succession was methodical, reflecting the family's belief in long apprenticeships and earned authority rather than inherited title. This pattern would repeat with the third generation, though tragedy would force an unexpected acceleration.

For investors, the Rocca family's multi-generational approach represents both opportunity and complexity. The family's willingness to deploy capital across decade-long cycles, accepting near-term underperformance for long-term strategic advantage, differs fundamentally from publicly-traded competitors beholden to quarterly earnings expectations. Yet this same long-term orientation can mean shareholders are along for rides they didn't anticipate.

III. The Privatization Wave: Building the Latin American Steel Empire (1992-2005)

Argentina's Somisa: The First Major Acquisition

The early 1990s presented Techint with the opportunity it had been cultivating for decades. Latin America's embrace of market liberalization—manifested in waves of privatizations from Mexico to Argentina—created a once-in-a-generation chance to acquire industrial assets at distressed valuations.

Techint participated in the privatization drive adopted by President Carlos Menem in the early 1990s, purchasing a majority stake in Argentina's then-leading steel manufacturer, the state-owned Somisa, in 1992.

Somisa had been Argentina's flagship steel enterprise, but like many state-owned heavy industrial assets, years of underinvestment and political interference had left it bloated and inefficient. Rocca converted Somisa into Siderar, and integrated Techint's cold rolled steel operations (for which Somisa had long been a leading supplier, reportedly at a loss to the state concern) into Siderca.

The results of this integration were dramatic. Between 1992 and 1996 Siderar raised its share of domestic consumption of flat steel (used in major appliances and the auto industry, among others) from about 56 percent to about 79 percent. Rocca embarked on a five-year investment program for Siderar, modernizing operations and shedding unprofitable units. Productivity almost tripled during this period, and costs per ton fell by 28 percent.

This pattern—acquiring distressed state assets, investing heavily in modernization, eliminating waste, and capturing market share—would become Techint's playbook across Latin America.

Venezuela's Sidor: Expansion into the Orinoco

The late 1990s brought Venezuela into Techint's orbit. The Sidor company which had been created to provide the national oil industry with pipes, was privatized in 1997; it came under the control of Ternium-Techint, an Italo-Argentinian consortium which bought 60% of the stock.

Terms of the sale called for the Amazonia consortium – made up of Mexico's Hylsa and Tamsa, Argentina's Siderar, Venezuela's Sivensa, and Brazil's Usiminas de Brasil – to control a 70% stake in the company. This consortium structure reflected the scale of the acquisition and the desire to share both risks and capital requirements.

Sidor represented significant production capacity in a country blessed with abundant natural resources—cheap hydroelectric power from the Orinoco basin, iron ore deposits, and access to Atlantic shipping routes. Siderúrgica de Orinoco C.A. (Sidor) is Venezuela's largest steel maker. Before its nationalization in May 2008, it was the largest steel exporter in Andean South America and the fourth largest steel exporter in all of Latin America.

Mexico's Hylsa: The Innovation Engine

The Mexican acquisition proved even more strategically significant. Production rapidly increased and diversified throughout the 1940s, and by 1950 the plant was already supplying steel to 900 industrial clients in Mexico.

What made Hylsa truly special was its pioneering technological achievement. By the late 1950s, shortages of scrap metal prompted the company to develop a new gas-based method for producing direct reduced iron (DRI). Known as the Hyl process, Hylsa's pioneering DRI technology was patented in 1957, and San Nicolás de los Garza became the world's first steel plant to adopt it for large-scale commercial use.

This innovation—born of necessity during the Korean War scrap shortage—gave Hylsa a technological edge that would prove increasingly valuable as environmental concerns and energy efficiency became industry priorities. DRI technology uses natural gas rather than coal, producing significantly lower carbon emissions than traditional blast furnace operations.

Between the years 2005 & 2007 Ternium acquired the two biggest steel companies in Mexico (Hylsa & IMSA) both located in Monterrey, becoming the biggest steel producer in Latin America.

The strategic logic was compelling: Mexico's proximity to the United States, its NAFTA membership (later USMCA), its relatively stable regulatory environment, and its growing automotive and appliance industries made it the ideal anchor for a pan-American steel platform.

The Creation of Ternium

Ternium was formed in 2005 by the consolidation of three companies: Siderar of Argentina, Sidor of Venezuela and Hylsa of Mexico.

The Techint Group acquires Hylsa in Mexico, which -together with Siderar and Sidor- creates Ternium. Ternium begins trading on the New York Stock Exchange under the TX symbol.

The NYSE listing represented both a capital-raising exercise and a stamp of legitimacy—a family-controlled Latin American industrial conglomerate accessing the world's deepest capital markets. Ternium is consolidated in Mexico with the incorporation of Imsa.

The timing proved fortuitous. Global steel demand was surging, driven by Chinese infrastructure investment and global economic growth. Ternium entered public markets as a beneficiary of the commodity supercycle, its pan-Latin American footprint suddenly appearing visionary rather than merely opportunistic.

IV. Birth of Ternium & NYSE IPO (2005-2007)

The Luxembourg Domicile

Ternium's choice of Luxembourg as its domicile—rather than Argentina, Mexico, or the United States—revealed the sophisticated financial engineering underlying the family's corporate structure. Luxembourg offered favorable tax treatment, European legal protections, and distance from the political volatility that had periodically disrupted operations in Latin American host countries.

This arrangement created a multi-layered structure. The family controls Techint through Luxembourg-based holding company San Faustin. According to a 2023 filing with the US Securities and Exchange Commission, about 65% of San Faustin's voting shares and 42% of its total capital are controlled by RP STAK, a foundation incorporated in the Netherlands.

Though the filings say no individual or group controls RP STAK, a person with knowledge of the foundation told Bloomberg News in July 2012 that it's controlled by the Roccas. This opacity—legal and well-documented, but nonetheless complex—allows the family to maintain strategic control while offering minority shareholders exposure to the underlying businesses.

The Third Generation Takes Command

Just as Ternium was being formed, tragedy struck the Rocca family. The family was shaken by the April 28, 2001, aviation death of Agostino Rocca, president of Techint and Roberto Rocca's successor. Agostino's younger brother, Paolo Rocca, was appointed to the post.

Paolo Rocca was born in Milan, Italy, in 1952. He is the son of Roberto Rocca, who was Honorary Chairman of Techint, and grandson of Agostino Rocca, founder of this industrial group.

Unlike his grandfather (an engineer) or his father (also an engineer), Paolo came from a different educational tradition. Paolo Rocca earned a degree in political science from the Università degli Studi di Milano. In 1985 he attended the PMD at Harvard Business School.

After having been an assistant to the executive director of the World Bank, in 1985 Paolo Rocca began his career at Techint Group as assistant to the chairman of the board of directors. In 1990 he assumed as executive vice-president of Siderca. Since 2002, he is the CEO of Tenaris and Techint.

The transition from engineer-leaders to a more broadly-trained executive reflected the increasing complexity of managing a global industrial conglomerate. Rocca led Techint in a series of acquisitions in Latin America and the world, which led to the development of operations in more than 20 countries.

As of July 2024, Forbes estimated his net worth at US$5.0 billion. This wealth—derived primarily from Techint's two publicly-traded steel companies, Tenaris and Ternium—places Paolo Rocca among the wealthiest individuals in Latin America and globally significant in the steel industry.

V. INFLECTION POINT #1: The Venezuela Nationalization Crisis (2008)

Chávez Moves Against Ternium

The Venezuelan crisis unfolded with the suddenness that characterizes political risk in emerging markets. Early Wednesday morning, the Vice President of Venezuela, Ramón Carrizalez, announced the nationalization of Argentine-controlled Ternium Sidor, the largest steel company in the Andean region, concluding a 14-month collective contract dispute between the company and the United Steel Industry Workers Union (SUTISS).

The decision to nationalize was made by President Hugo Chávez and communicated by telephone at 1:30am to Carrizalez, who had been mediating negotiations since Monday in southeastern Bolívar state, where the company is based.

The immediate catalyst was a labor dispute, but underlying tensions had been building for years. The company had 8,000 subcontracted, precarious workers: Ternium had brought non-contract workers in while regular workers were being dismissed.

Critics accused Ternium of extracting value from Venezuela without adequate reinvestment. It obeyed the interests of markets in other countries in deciding how to place its production. Instead of producing laminated steel or transformed products for export or national consumption, thus adding value to our production, we produced slabs and billets. The export of these semi-finished products had clear advantages for the corporation, but it hurt Venezuela.

Paolo Rocca's Failed Intervention

Shortly after the nationalization was announced, Paolo Rocca, the president and top shareholder of Techint, an Argentine conglomerate which owns 60% of Sidor, sent a letter to Chávez requesting a "constructive solution" to avoid nationalization. In the missive, Rocca offered a pay raise nearly equal to the workers' demand and agreed to increase pensions to minimum wage, but did not alter its position on contract labor.

The letter came too late. Chávez had made his decision, and the nationalization became a fait accompli. Chavez nationalized Sidor, a steel making company, a Venezuelan government official told CNN. The Argentine company Ternium owns the majority of shares in Sidor, according to a report about Chavez's decision in the Venezuelan-based Bolivariana News Agency.

The Settlement

The following year, Ternium SA, Sidor's parent company, agreed to sell its 59.7 percent stake in the company to Venezuela for $1.97 billion, finalizing the government's takeover of Venezuela's largest steel mill.

CVG paid US$400 million in cash against the aggregate amount of US$1.97 billion that Ternium has agreed to receive an as compensation for its Sidor shares. The balance has been divided in two tranches, the first of which totals US$945 million and will be paid in six equal quarterly installments.

The compensation, while substantial, represented a significant haircut from the asset's replacement value. More importantly, it marked the end of Ternium's presence in Venezuela—a strategic retreat that would prove prescient as the country's economy subsequently collapsed.

The Aftermath: What Happened to Sidor

The Venezuelan government's stewardship of Sidor proved disastrous. The plant's production declined steadily over the ensuing decade. A former Sidor director said that Chávez had "received it as a productive and solvent company; but management coming from the military world, unaware of 'steel manufacturing' activity, together with the 'absence of strategic planning and investments, led to a sustained fall in production.'"

For Ternium, the Venezuela experience became a cautionary tale incorporated into all future strategic planning. The company would never again concentrate such significant assets in countries with comparable political risks—and the loss reinforced the importance of Mexico as the cornerstone of the company's future.

VI. The Brazil Play: Usiminas Investment (2011-2023)

Joining the Control Group

Brazil represented both enormous opportunity and significant complexity. Ternium and Tenaris join the control group of Brazil's steel giant Usiminas, together with Nippon Steel and Usiminas employees' pension fund.

Usiminas was not a distressed asset—it was Brazil's largest steel company, with premium positioning in the automotive and appliance markets. Acquiring control would be expensive and contested. The Techint group chose a different approach: joining a control consortium rather than attempting a full takeover.

In addition, Ternium participates in the control group of Usiminas, Brazil's largest steel company.

The CSN Litigation Saga

The Usiminas investment triggered a decade-long legal battle that continues to this day. LUXEMBOURG / ACCESSWIRE / June 18, 2024 / Ternium S.A. (NYSE:TX) announced today that the Brazilian Superior Court of Justice (SCJ) resolved that Ternium's subsidiaries Ternium Investments and Ternium Argentina, and Tenaris's subsidiary Confab, all of which compose the T/T Group under the Usiminas shareholders agreement, should pay Companhia Siderúrgica Nacional, or CSN, an indemnification in connection with the acquisition by the T/T Group of a participation in Usiminas in January 2012. CSN and various entities affiliated with CSN had filed a lawsuit in Brazil against the T/T Group, alleging that, under applicable Brazilian laws and rules, the acquirers were required to launch a tag-along tender offer to all non-controlling holders of Usiminas ordinary shares for a price per share equal to 80% of the price per share paid in such acquisition.

The legal theory was that Ternium's acquisition had triggered a change of control that entitled minority shareholders—including competitor CSN—to "tag-along" rights allowing them to sell their shares at the acquisition price. Ternium vigorously disputed this interpretation.

The SCJ modified the monetary adjustment mechanism and capped attorney's fees, reducing the potential payment. Ternium Investments could face approximately BRL1.9 billion ($307 million) in payments, while Ternium Argentina could owe BRL0.7 billion ($109 million).

Ternium maintains that CSN's claims are meritless and plans to pursue further appeals.

This litigation represents a material contingent liability that investors must monitor. The amounts, while substantial, are not existential for a company of Ternium's scale—but the uncertainty creates ongoing overhang.

The 2023 Consolidation Milestone

Despite the litigation, Ternium continued building its Brazilian position. On July 3, 2023, Ternium acquired an additional stake in Usiminas of 57.7 million ordinary shares, increasing its participation in the Usiminas control group to 51.5% and its economic participation to 23.3%. In addition, the Usiminas shareholders agreement was updated to reflect a new governance structure. Pursuant to the updated agreement, Ternium started to fully consolidate Usiminas balance sheet and results of operations.

This consolidation represented a major milestone—transforming Usiminas from an equity-method investment into a consolidated subsidiary, dramatically increasing Ternium's reported revenues and assets.

Ternium would pay $2.06 per ordinary share, which would result in an aggregate purchase price of approximately $315.2 million in cash for 153.1 million ordinary shares, increasing its participation in the Usiminas control group from 51.5% to 83.1%. This November 2025 announcement indicates continued commitment to Brazil despite the challenges.

VII. INFLECTION POINT #2: CSA Brazil Acquisition from ThyssenKrupp (2017)

ThyssenKrupp's Billion-Dollar Disaster

The CSA acquisition represents perhaps the clearest example of Ternium's willingness to buy quality assets from distressed sellers at attractive valuations.

With the sale of CSA, thyssenkrupp is bringing its loss-making chapter of Steel in the Americas to an end: In 2005 the Group decided to expand its steel business into the Americas. The original plan was to produce slabs at low cost in Brazil and process and sell them in the USA and Europe. The plan didn't work out. Following a significant increase in construction costs for the facilities in Brazil and Alabama in the USA as well as technical problems with the ramp-up of the plants and high start-up losses, thyssenkrupp placed the entire project under review immediately after Heinrich Hiesinger took over as CEO.

The scale of ThyssenKrupp's losses was staggering. To date Steel Americas has cost the Group over €12 billion in capital expenditures and start-up losses. Even after deducting the proceeds from the divestment of the plants in the USA and Brazil and Vale's share in the financing, a net loss of around €8 billion remains.

This €8 billion net loss—from a single strategic miscalculation—ranks among the most expensive blunders in modern industrial history.

Ternium's Opportunistic Acquisition

The purchase price is €1.5 billion.

CSA is a steel slab producer with a steelmaking facility located in the state of Rio de Janeiro, Brazil, and has an annual production capacity of 5 million tons of high-end steel slabs, a deep-water harbor and a 490 MW combined cycle power plant.

For €1.5 billion, Ternium acquired assets that had cost ThyssenKrupp over €5 billion to construct—not including the operating losses. With the purchase of CSA, Ternium will acquire additional production capacities of up to 5 million metric tons of slabs per year.

Ternium will integrate CSA into its industrial and supply-chain systems. As part of this process, CSA has changed its corporate name to Ternium Brasil.

The acquisition exemplified the Rocca family's patient approach to capital allocation. While ThyssenKrupp was under pressure to exit a troubled investment, Ternium had the balance sheet strength and strategic patience to acquire a world-class facility at a fraction of replacement cost.

VIII. INFLECTION POINT #3: The Pesquería Mega-Investment & USMCA Bet (2013-Present)

Building the Crown Jewel

This plant, located in an expanse of 437 hectares, began operations in 2013 after an investment of 1,120 million dollars for a cold rolling plant and a continuous galvanizing line.

The Pesquería Industrial Center near Monterrey, Mexico represents Ternium's largest and most ambitious investment—a multi-phase, multi-billion dollar bet on the future of North American manufacturing.

In 2017, an expansion to this complex was announced, which is contemplating a new galvanizing line and another painting one, as well as a new hot roller with a capacity of 4.4 million tons. By this stage, the company allocated 1,400 million dollars. More than 2,520 million dollars have been invested in both stages.

In June 2023, it was announced that Pesquería, in Mexico, would be the destination of the largest investment plan in the history of Ternium: 3.2 billion dollars to build the continent's most modern and sustainable steel mill. "Many people think of steel as an old, ancient material, but steel is the material of the future and we are convinced of that," explains Máximo Vedoya, CEO of Ternium.

Once the third part of the project is completed, the Pesqueria complex will add up to a total investment of $6.8 billion.

The Hot-Rolling Mill Milestone

Also, the new hot-rolling mill in Pesquería, Mexico, produced its first coils in May. It has an annual production capacity of 4.4 million tons.

The continued ramp-up of Ternium's Pesqueria industrial center also assisted in the record quarterly shipment level. The project's new 550,000-ton-per-year (tpy) pickling line and three of five finishing lines began operating in Q3'24.

Stage 3: The Steelmaking Facility

Ternium will begin making slabs in Mexico in mid-2026. Construction work continues on the 2.6-million-tpy slab facility in Pesqueria. Vedoya said that once completed, it will ensure a steady supply of slabs for downstream processing and reduce its dependency on external suppliers.

The Pesquería expansion project cost estimate increased to $4.0 billion, with operations expected to begin by Q4 2026.

USMCA Strategic Driver

The entire Pesquería investment thesis rests on the USMCA (United States-Mexico-Canada Agreement) and the regional content requirements it imposes on automotive and other manufacturers.

Beyond market analysis, Vedoya outlined the progress of Ternium's USD 4 billion investment in its Industrial Center in Pesquería, Nuevo León. The project, currently employing more than 8,000 workers, will result in the most modern and sustainable steel plant in the Americas.

The company sees "nearshoring", the trend of U.S. firms relocating production to Mexico, as a silver lining, potentially boosting demand for Ternium's USMCA-compliant steel even as tariffs squeeze margins.

IX. Decarbonization & Sustainability Strategy

The Olavarría Wind Farm

Ternium moves forward in its decarbonization strategy with the start-up of the Vientos Olavarría Wind Farm, its first great renewable energy project with an investment of over $220 million dollars.

With 72 megawatts of power, Ternium Argentina will be able to replace 65% of the electricity it currently purchases from external suppliers in the national grid. Senior Engineering Director Gastón Rodriguez Araya explains that, "The power produced by the wind farm will be directly fed into the national electricity network, allowing us to reduce the amount of electricity we purchase from the public grid, of which some 60% comes from hydrocarbons. This means that we will avoid emitting 93,000 tons of CO2 per year, enabling us to press ahead with our decarbonization plan."

Technology Pathway: DRI and Hydrogen-Ready

The main feature of the plant is also its charging flexibility: in fact, the EAF can also be fed with scrap in variable percentage, in addition to hot DRI. Additionally, the DR plant includes a carbon capture technology and is prepared for use of hydrogen, offering the most sustainable solution in steelmaking available on the market.

The new plant in Mexico will use low carbon technologies. This DRI-EAF steel mill contemplates the use of renewable energy, as well as CO₂ capture. In addition, it will have the possibility of transitioning from natural gas to green hydrogen in the DRI module when economically feasible.

The Hylsa DRI heritage—technology pioneered in Mexico in the 1950s—now positions Ternium advantageously for the decarbonization transition. DRI using natural gas produces significantly lower emissions than traditional blast furnace operations, and the pathway to hydrogen-based reduction offers a credible route to near-zero emissions steelmaking.

X. Current Operations & Financial Performance

2024 Full-Year Results

Ternium (NYSE:TX) reported its Q4 and full-year 2024 results, with Q4 net income of $333 million, including a $404 million provision reversal related to Usiminas litigation. The full-year net income was $174 million, with an adjusted net income of $584 million excluding litigation provisions.

The company faced market challenges in Q4 2024, with a downturn in the Mexican steel market due to seasonality and trade uncertainties. Despite this, Ternium maintained a strong financial position with a net cash position of $1.6 billion at year-end, supported by operating cash flow of $1.9 billion.

Q1 2025: Navigating Trade Uncertainty

Ternium reported its Q1 2025 financial results, showing mixed performance across regions. The company's Adjusted EBITDA increased sequentially due to improved margins and higher steel and iron ore shipments, despite lower revenue per ton.

The company reported Net Income of $142 million, with Adjusted Net Income at $188 million after excluding a $45 million provision charge. Ternium maintained a Net Cash position of $1.3 billion, down from $1.6 billion at end-2024.

Tariff Challenges

The current trade environment presents significant uncertainty. For context, on June 4, 2025, U.S. President Donald Trump doubled the tariffs on steel and aluminum imports to 50%. The move impacted Mexican steel exports unless they comply with USMCA's strict "rules of origin" requirements.

MEXICO CITY (Reuters) -Ternium, a steelmaker with a massive Mexico business, on Wednesday pushed for stronger terms of a regional trade agreement ahead of a pending review, despite current headwinds from steel tariffs imposed by the government of U.S. President Donald Trump. Shipments from Mexico to the U.S. under the U.S.-Mexico-Canada (USMCA) trade agreement are currently exempt from tariffs, though steel products face a whopping 50% tariff.

Ternium's sales volume in Mexico decreased both sequentially and year-over-year in the first quarter of 2025. Uncertainty surrounding evolving U.S. trade policies continued to weight on shipments in the first quarter, primarily in the commercial steel market. However, the company's sales to industrial customers remained relatively stable.

XI. Leadership: Paolo Rocca and Máximo Vedoya

Paolo Rocca: The Family Patriarch

Paolo Rocca, born on October 14, 1952, in Milan, Italy, is a prominent Argentine-Italian businessman. He serves as the Chairman and CEO of the Techint Group, a multinational conglomerate with significant operations in steel production, engineering, construction, and energy sectors. Under his leadership, Techint has expanded its global footprint, reinforcing its position as a leader in various industries.

Paolo Rocca's recognition within the industry reflects his standing. In 2004 within the "Argentina-México: Visión y Perspectivas" forum, he was awarded with the Orden Mexicana del Aguila Azteca. In 2008 he was recognized by Fundación Konex with the "2008 Platinum Konex Prize: Industry businessmen"; and in 2011 he was chosen "Steelmaker of the Year" by the Association of Iron and Steel Technology (AIST). In 2013 the Columbia Business School honored Paolo Rocca with the "Deming Cup" in recognition to the impact of his leadership on Tenaris's competitiveness.

Máximo Vedoya: The Operating CEO

Mr. Vedoya currently serves as our Chief Executive Officer. Prior to that, he served as President of Ternium Mexico. He has held several other executive positions since joining the Techint Group in 1992, such as chief executive officer of Ferrasa, director of Ternium Mexico's international

Born in Argentina in 1970, Vedoya holds a degree in Industrial Engineering from the Instituto Tecnológico de Buenos Aires (ITBA) and a Master of Science in Management from Stanford University.

Maximo Vedoya was appointed as Chief Executive Officer of the Company, effective March 1, 2018.

Since 1992, Vedoya's key positions have included Planning, Sales, Exports and Commercial Director in Ternium companies in Argentina and Venezuela.

Vedoya's career path—from entry-level roles through commercial and operational positions in multiple countries—reflects the Techint philosophy of developing leaders through extended operational apprenticeships rather than fast-tracking MBA graduates.

XII. Competitive Positioning & Strategic Analysis

Porter's Five Forces Analysis

Threat of New Entrants: LOW Steel production requires massive capital investment—Ternium's Pesquería facility alone represents over $6 billion in cumulative investment. Integrated steelmakers benefit from scale economies in procurement, logistics, and processing that newcomers cannot easily replicate. Regulatory requirements, particularly environmental permits, create additional barriers.

Supplier Power: MODERATE Iron ore and energy represent major input costs. Ternium's vertical integration—including mining operations in Mexico and ownership stake in Usiminas' iron ore assets in Brazil—mitigates some supplier power. However, the company remains exposed to global commodity prices and natural gas costs, particularly in Mexico.

Buyer Power: MODERATE TO HIGH Major customers—automotive OEMs, appliance manufacturers—are sophisticated purchasers with significant bargaining leverage. Ternium counters this through value-added services, technical support, and long-term supply relationships. The company's proximity to customers in Mexico and Brazil provides logistics advantages that partially offset price pressure.

Threat of Substitutes: LOW TO MODERATE Steel remains essential for construction, automotive, and industrial applications where substitutes (aluminum, plastics, composites) offer inferior performance-to-cost ratios for most applications. Electric vehicle production actually increases steel content in some applications due to battery casings and structural requirements.

Competitive Rivalry: HIGH Ternium competes with global giants (ArcelorMittal, Nippon Steel, POSCO) and regional players (CSN in Brazil, local minimills in Mexico). Chinese overcapacity creates persistent pressure on global prices, with imports threatening local market share. The company's strategy of focusing on value-added products and customer service attempts to differentiate from pure price competition.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Ternium benefits significantly from scale, particularly in procurement and logistics. The Pesquería investment specifically targets scale advantages in the USMCA automotive supply chain.

Network Effects: Limited in commodity steel production, though customer integration systems and technical support create some switching costs.

Counter-Positioning: Ternium's DRI-based production technology positions it advantageously for decarbonization versus blast furnace competitors, though this advantage is not yet fully monetized.

Switching Costs: Moderate—automotive OEMs develop technical specifications and testing protocols with suppliers that create friction, but commodity steel grades face minimal switching barriers.

Branding: Minimal brand power in a B2B commodity context.

Cornered Resource: The HYL DRI technology heritage and decades of operational expertise represent intellectual capital, though much of this knowledge has diffused across the industry.

Process Power: Ternium's operational excellence—demonstrated in the turnarounds at Somisa and CSA—represents genuine process power that competitors struggle to replicate.

XIII. Bull Case & Bear Case

The Bull Case

USMCA Fortress: The USMCA's rules of origin requirements mandate high levels of North American content in automobiles. Ternium's Mexican production—especially the Pesquería steelmaking facility scheduled for 2026—positions the company as an essential supplier for automotive OEMs seeking USMCA compliance. As nearshoring accelerates, Ternium captures volume that would otherwise go to Asian competitors.

Distressed Asset Expertise: The Rocca family has repeatedly demonstrated ability to acquire quality assets at distressed prices and turn them around. This optionality—the ability to capitalize on others' misfortunes—could deliver future value not reflected in current valuations.

Decarbonization Leadership: The DRI-EAF production route, with hydrogen-readiness, positions Ternium advantageously as carbon pricing and environmental regulations tighten globally. European carbon border adjustments could make Ternium's products more competitive versus blast furnace steel.

Strong Balance Sheet: A net cash position exceeding $1 billion provides resilience and acquisition optionality unusual for capital-intensive industrial companies.

Family Control Benefits: Long-term oriented ownership allows investments in projects (like Pesquería) that public market short-termism might otherwise preclude.

The Bear Case

Tariff Uncertainty: The 50% steel tariff on Mexican exports to the United States—even with USMCA carve-outs for qualifying products—creates significant uncertainty for Pesquería's economics. Should tariff regimes become more restrictive, billions in invested capital could be stranded.

Brazil Challenges: Ternium noted some challenges for the Brazilian market in its Q3 report, including high import levels, particularly from China. Chinese steel overcapacity represents a persistent threat to Brazilian market share and margins.

Litigation Overhang: The CSN litigation, while reduced in scope, creates ongoing uncertainty and potential cash obligations totaling approximately $400-500 million.

Emerging Market Exposure: Operations in Argentina, Brazil, and Mexico expose Ternium to currency volatility, political risk, and macroeconomic instability. The Venezuela experience demonstrated how quickly asset values can evaporate.

Commodity Cyclicality: Steel remains a deeply cyclical commodity. Global recessions compress margins dramatically, and Ternium's capital-intensive operations face high fixed costs that amplify earnings volatility.

Family Control Risks: Concentrated family control can lead to conflicts with minority shareholders, related-party transactions, and succession risks.

XIV. Key Performance Indicators for Investors

For long-term fundamental investors, the following KPIs merit closest attention:

1. EBITDA per Ton Shipped

This metric captures both pricing power and operational efficiency across regions. Given Ternium's multi-country exposure, tracking EBITDA per ton by segment (Mexico, Brazil/Usiminas, Southern Region) reveals relative competitive positioning and margin trends. Deterioration in this metric—absent equivalent price pressure on competitors—would signal competitive erosion.

2. Pesquería Ramp-Up Progress

With approximately $4 billion committed to the Pesquería expansion, successful execution on schedule and budget is critical. Key milestones include: cold mill startup (expected early 2026), galvanizing line startup (expected end 2025), and slab mill startup (expected Q4 2026). Delays or cost overruns would pressure returns on this transformational investment.

3. Mexican Steel Shipment Volumes

Mexico accounts for 55% of sales and represents Ternium's strategic priority. Tracking quarterly shipment volumes to Mexico—particularly to automotive and industrial customers—provides the most direct read on demand trends and competitive positioning in the company's core market. Sustained volume declines would raise questions about the USMCA thesis.

XV. Material Legal and Accounting Considerations

CSN Litigation

Assuming monetary adjustment through November 30, 2024, and BRL5 million in attorney's fees, in each case as determined pursuant to the SCJ decision published today, the revised aggregate amount potentially payable by Ternium Investments and Ternium Argentina would be of approximately BRL1.9 billion (approximately $307 million) and BRL0.7 billion (approximately $109 million), respectively. Ternium continues to believe that all of CSN's claims and allegations are unsupported and without merit, and that in connection with the Usiminas acquisition the T/T Group was not required either to launch a tender offer or to pay indemnification to CSN.

The company has recorded provisions and subsequently partially reversed them based on legal developments. Further appeals remain possible, creating ongoing uncertainty.

Related Party Transactions

Given the complex ownership structure through San Faustin and RP STAK, investors should carefully review related party transactions disclosed in annual reports (Form 20-F). Transactions with sister company Tenaris—which shares the same ultimate ownership—require particular scrutiny.

Currency Translation

With major operations in Argentina (peso), Brazil (real), and Mexico (peso), currency movements significantly impact reported results. The Argentine currency situation is particularly volatile, requiring attention to both transaction and translation effects.

XVI. Conclusion: Steel Eternal?

Ternium's story—from Agostino Rocca's post-Fascist flight to Paolo Rocca's stewardship of a multi-billion dollar empire, from Argentine privatization opportunism to the Mexican nearshoring bet—captures the romance and risk of emerging market industrial capitalism.

The company has survived and thrived through Venezuelan nationalizations, Brazilian legal battles, Argentine economic collapses, and global commodity cycles. This resilience reflects both the advantages of family control—patient capital, long-term thinking, operational discipline—and the hard lessons learned from exposure to political and economic volatility.

The current moment presents both maximum opportunity and maximum risk. The Pesquería investment, if successful, could cement Ternium's position as the indispensable steel supplier to North American manufacturing. The USMCA's regional content requirements, combined with the secular nearshoring trend, create a structural tailwind potentially lasting decades.

Yet the tariff uncertainty, the Chinese overcapacity threat, the Brazilian litigation, and the inherent volatility of steel markets demand caution. The name "Ternium"—evoking eternity through the integration of three mills—now seems almost ironic given that Venezuela's Sidor has been lost and Brazil's Usiminas has been a source of persistent litigation headaches.

For investors, Ternium offers something increasingly rare in modern markets: a family-controlled industrial enterprise with genuine competitive advantages, trading at modest valuations, controlled by operators with an 80-year track record of value creation. The risks are real but quantifiable; the opportunities are substantial but dependent on factors—trade policy, commodity prices, political stability—beyond any company's control.

The Rocca family has bet generations of wealth on Latin American industry. The current generation has bet billions on the USMCA thesis. Whether that eternal optimism proves justified remains to be written—but the story of Ternium, whatever its ultimate chapter, will remain one of the most compelling in global industrial history.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube