Meta Platforms: The Social Empire That Ate The Internet

I. Introduction & Episode Roadmap

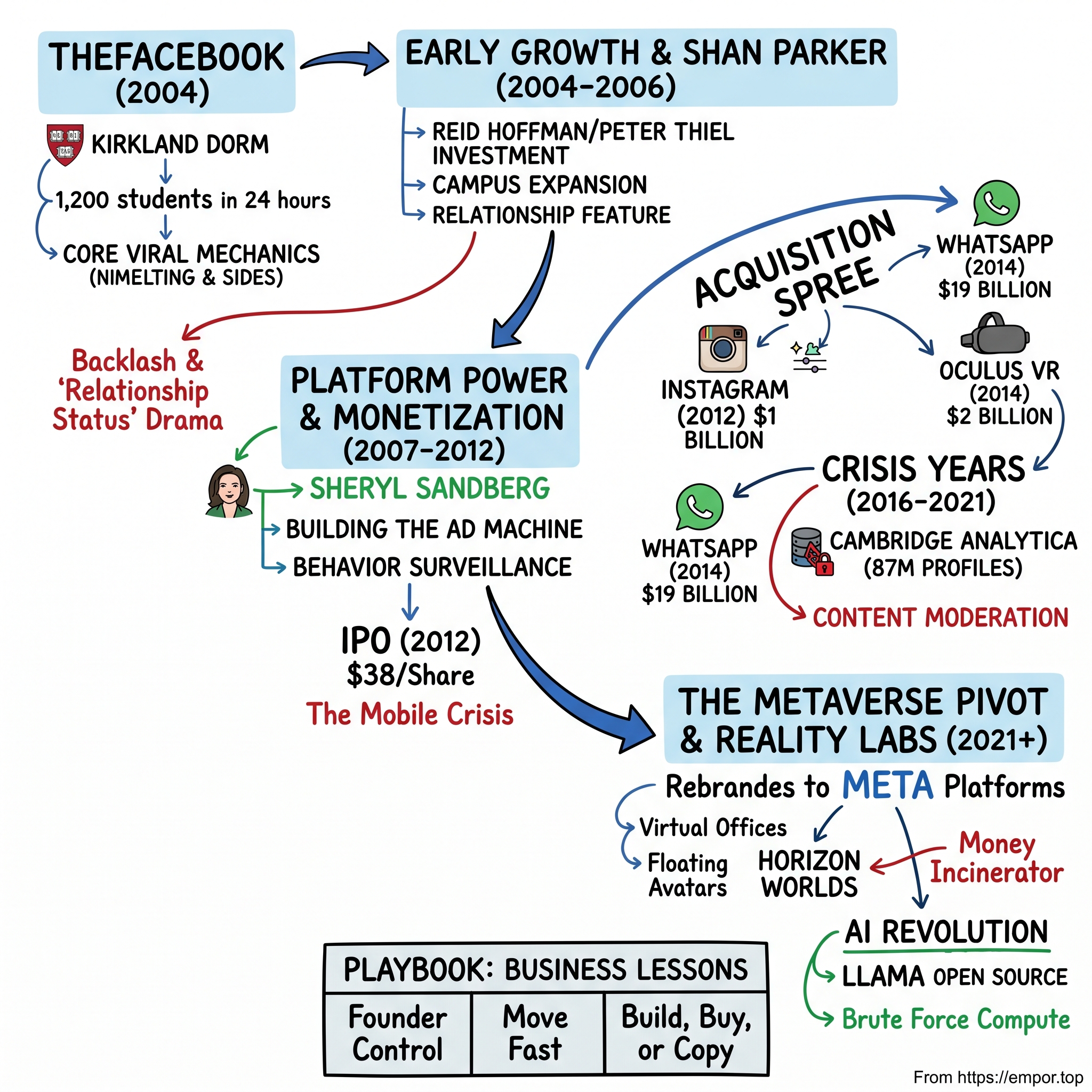

Picture this: February 4, 2004. Snow blankets Harvard Yard as a nineteen-year-old computer science student hits enter on his laptop, launching a website from his Kirkland House dorm room. The site's header reads "TheFacebook" in light blue Klavika font against a darker blue banner. Within twenty-four hours, 1,200 Harvard students have signed up. Within a month, half the undergraduate population has profiles. Mark Zuckerberg has just unleashed something that will fundamentally rewire how humanity connects, communicates, and—some would argue—thinks.

Fast forward two decades. That dorm room project, renamed Facebook in 2005 and rebranded as Meta in 2021, commands a market capitalization of $1.49 trillion as of October 2024, making it the world's seventh most valuable company. Its platforms reach over 3 billion humans monthly—nearly 40% of Earth's population. In 2024 alone, it generated $164.5 billion in revenue, more than the GDP of most countries.

How did a Harvard hot-or-not clone become the digital infrastructure for human connection at planetary scale? How did a college kid who couldn't maintain eye contact in meetings become one of the most powerful executives in history, controlling the primary communication channels for billions? And why, after conquering social networking so thoroughly that "Facebook" became a verb, did Zuckerberg bet the company's future—and tens of billions of dollars—on virtual worlds that most people don't want?

This is a story about network effects so powerful they create gravitational fields that bend entire industries. It's about a founder who maintained iron-fisted control through dual-class shares and strategic maneuvering that would make Machiavelli blush. It's about platform dominance so complete that governments worldwide are scrambling to contain it. And ultimately, it's about a company at an inflection point, pivoting from social media monopolist to metaverse pioneer—a transition that could either cement its dominance for another generation or mark the beginning of its decline.

The themes we'll explore read like a Silicon Valley playbook: the power of timing and execution over originality, the compounding nature of network effects, the strategic value of copying competitors, the perils of platform power, and the existential question facing every tech giant: what comes after you've won everything?

Meta's journey from TheFacebook to the metaverse isn't just a business story—it's the defining narrative of the internet age, a cautionary tale about power and responsibility, and possibly a preview of humanity's digital future. Whether that future is utopian or dystopian depends largely on decisions being made right now in Menlo Park, where a hoodie-wearing CEO continues to move fast and break things, even if those things increasingly include societal norms, democratic institutions, and our shared sense of reality.

II. The Harvard Origins & Founding Drama

The mythology begins with a breakup. October 28, 2003: Mark Zuckerberg, a Harvard sophomore from Dobbs Ferry, New York, sits in his Kirkland House dorm room, beer in hand, blogging about his ex-girlfriend. "Jessica Alona is a bitch," he types, before channeling his romantic frustration into code. Within hours, he's hacked into Harvard's house databases, downloading student ID photos. By 4 a.m., Facemash is live—a site where students can vote on who's hotter between two randomly paired classmates.

The site explodes across campus. Within four hours, 450 visitors cast 22,000 votes. Harvard's network nearly crashes. The Administrative Board hauls Zuckerberg in for violations including "breaching security, violating copyrights and violating individual privacy." He narrowly avoids expulsion. But here's what everyone missed while focusing on the controversy: Zuckerberg had just proven something profound about human psychology and digital networks. Given the right interface and social context, people would compulsively engage with each other's photos online.

Born May 14, 1984, to a dentist father and psychiatrist mother, Zuckerberg was coding before he could drive. At Phillips Exeter Academy, he built "ZuckNet," a primitive instant messenger for his father's dental practice. He created Synapse, a music player that learned your preferences—Microsoft and AOL tried to buy it for millions, but the teenager turned them down. By the time he arrived at Harvard in 2002, studying computer science and psychology, he wasn't seeking education so much as a launching pad.

Enter the Winklevoss twins—Cameron and Tyler—6'5" Olympic rowers with jaw lines that could cut glass and an idea for "Harvard Connection," a dating site for the Harvard community. In November 2003, they approach Zuckerberg to code their vision. He agrees, then proceeds to systematically ghost them while secretly building his own social network. Their emails, later revealed in litigation, show increasing desperation: "We're very deep into the semester, and we're all scrambling to define our futures before we graduate," Tyler writes. Zuckerberg responds with vague promises while racing to launch first.

January 11, 2004: Zuckerberg registers the domain "thefacebook.com" for $35. He recruits roommate Dustin Moskovitz for coding help, Andrew McCollum to design the iconic original logo, and Eduardo Saverin—a junior from a wealthy Brazilian family—as business manager and CFO, fronting $1,000 in initial capital for servers. Chris Hughes joins to handle communications. The founding equity split: Zuckerberg 65%, Saverin 30%, Moskovitz 5%.February 4, 2004, 9:47 p.m.: Zuckerberg sends an email to his roommates. "Check it out." He includes a link: thefacebook.com. The site's tagline reads "An online directory that connects people through social networks at colleges." The home page features Al Pacino's face from a scene in "The Devils Advocate"—a choice that, in retrospect, seems almost prophetic. TheFacebook goes live on a Wednesday, and overnight, the site takes off.

Within twenty-four hours, 1,200-1,500 students have registered. Within two weeks, 4,300 had created accounts. Within the first month, more than half the undergraduate population at Harvard was registered on the service. The viral mechanics are perfect: exclusivity (Harvard email required), social proof (see who else joined), and network effects (more valuable with each user). Students refresh obsessively to see who added them as friends. The poke feature—whose purpose Zuckerberg deliberately kept ambiguous—becomes a campus flirtation tool.

But drama erupts immediately. Just six days after the launch, three Harvard seniors, Cameron Winklevoss, Tyler Winklevoss, and Divya Narendra, accused Zuckerberg of intentionally misleading them into believing he would help them build a social network called HarvardConnection.com. The twins claim Zuckerberg stalled them while secretly building his competing site. Their evidence: emails where Zuckerberg strings them along ("I'm still a little skeptical that we have enough functionality") while furiously coding TheFacebook.

The Eduardo Saverin saga proves equally explosive. Initially the company's CFO and business manager, owning 30% equity, Saverin begins clashing with Zuckerberg over strategy. While Zuckerberg wants to move fast and expand, Saverin focuses on monetization through advertising, alienating users with intrusive ads. The relationship deteriorates when Zuckerberg moves to Palo Alto for the summer of 2004, while Saverin takes an internship in New York.

What happens next becomes Silicon Valley legend and cautionary tale. Zuckerberg reincorporates Facebook in Delaware, issues new shares to himself and others, and systematically dilutes Saverin's stake from 30% to under 10%, then eventually to less than 5%. Saverin's reaction when he discovers the dilution: "Mark, you're scaring me. Please don't do anything without telling me. It's starting to feel like you're trying to cut me out of something." He was right. The lawsuit settles for undisclosed terms, with Saverin keeping around 5% (worth over $10 billion today) and a co-founder title, but his name scrubbed from Facebook's official history for years.

In June 2004, Facebook moved its base of operations to Palo Alto, California. Zuckerberg and Moskovitz drop out of Harvard—though Zuckerberg maintains for years he's just "taking time off." The move to Silicon Valley isn't just geographic; it's cultural. They shed their East Coast collegiate identity for West Coast disruption ethos. The company that began as an elite Harvard directory was about to become something far more ambitious—and far more dangerous.

III. The Sean Parker Era & Early Growth

Sean Parker stumbles into the Palo Alto house Facebook is renting in late summer 2004, brought by his girlfriend who knows someone living there. The Napster co-founder, then 24, finds Zuckerberg and Moskovitz coding in their pajamas, empty Red Bull cans everywhere, whiteboards covered in growth charts. Parker sees something others miss: not just another social network, but a data goldmine with perfect viral mechanics. Within weeks, he's sleeping on their couch. Within months, he's president.

Parker's first masterstroke: approaching Reid Hoffman, the CEO of LinkedIn, for funding. Hoffman liked Facebook but declined to be the lead investor because of potential conflict of interest with his duties as LinkedIn CEO. He redirected Parker to Peter Thiel, whom he knew from their PayPal days.

The Thiel meeting at Il Fornaio restaurant in Palo Alto becomes the stuff of startup folklore. Peter Thiel made a $500,001 angel investment in Facebook for 10.2% of the company and joined Facebook's board. This was the first outside investment in Facebook. The extra dollar? Pure Thiel—making the valuation $4.9 million instead of an even $5 million, a psychological trick suggesting precision in what was really a gut bet. Thiel's investment thesis: Facebook had already won the elite college market, and history shows the masses follow elite adoption patterns.

Parker orchestrates Facebook's campus-by-campus expansion with military precision. Rather than opening everywhere at once like failed competitor Friendster, Facebook maintains artificial scarcity. In March 2004, Facebook expanded to Stanford, Columbia, and Yale. This expansion continued when it opened to all Ivy League and Boston-area schools. Each new school launch creates local press, FOMO at nearby colleges, and desperate emails from students begging for access. The waiting list becomes a marketing tool.

The strategy is brilliant psychological manipulation. By keeping Facebook exclusive to college students with .edu email addresses, they create a "safe space" where students share freely, knowing parents and employers can't see. The real names policy—controversial even then—creates accountability that MySpace's anonymous profiles lack. Every feature reinforces authentic identity: one profile per person, real photo required, college email verification.

Competition with MySpace seems laughable now, but in 2005, MySpace has 20 million users to Facebook's 5 million. MySpace is where bands promote music and teenagers customize HTML profiles with glitter graphics. Facebook is clean, uniform, austere—almost anti-fun. But that's the point. As Parker explains to investors: "MySpace is a nightclub. Facebook is your living room."

The relationship feature—"single," "in a relationship," "it's complicated"—becomes Facebook's killer app for college students. Entire relationships play out in status updates. The term "Facebook official" enters the lexicon. Students check their ex's profile obsessively. The "relationship status change" becomes the most watched notification.

Facebook introduced the News Feed in September 2006, and the backlash is immediate and fierce. Hundreds of thousands join protest groups like "Students Against Facebook News Feed." Students organize rallies outside Facebook's office. The feature seems like a privacy violation—suddenly everyone can see everything you do. Zuckerberg issues one of his first public apologies: "We really messed this one up."

But they don't remove News Feed. Within weeks, the protests die down as users realize they're addicted to the constant stream of updates. News Feed engagement is 10x higher than the previous homepage. It transforms Facebook from a static directory you check occasionally into a living, breathing organism you monitor constantly. Parker later calls it "the most important innovation in social media history."

By 2006, Facebook expanded to everyone with a valid email address along with an age requirement of being 13 or older. The decision to open beyond colleges is controversial internally. Early employees worry about losing the magic. But growth has plateaued at 12 million users. MySpace has 100 million. The choice is expand or die.

By 2007, Facebook surpassed MySpace in global traffic and became the world's most popular social media platform. The victory comes not from being cooler or more feature-rich, but from superior execution and growth hacking. While MySpace dealt with spam, fake profiles, and server crashes, Facebook maintained quality through careful expansion and engineering excellence.

Parker's tenure ends abruptly in 2005 when police find cocaine at a party he's attending. Though charges are dropped, Thiel and Accel Partners force him out, fearing the reputational risk. Parker maintains his equity but loses operational control. His parting advice to Zuckerberg: "Just don't fuck it up." The transformation from college project to global platform is complete. What comes next will require a different kind of leadership.

IV. Platform Power: Building the Advertising Machine

The first time Mark Zuckerberg calls Sheryl Sandberg is 4:30 p.m. on a Friday afternoon in 2007. She's sitting in her Google office, contemplating the weekend, when this twenty-three-year-old CEO asks if she wants to discuss joining Facebook. She almost says no—she's built Google's advertising business from a startup operation to a multi-billion dollar machine. Why would she leave for a company with no clear revenue model?

But they meet at a Christmas party hosted by Dan Rosensweig, and something clicks. In late 2007, Zuckerberg met Sandberg at the party, and though he had no formal search for a chief operating officer, he thought of Sandberg as "a perfect fit" for this role. Over the next two months, they have marathon conversations—sometimes six hours straight—about Facebook's future. Sandberg grills him: "What's your real mission?" Zuckerberg's answer surprises her: "I don't want to own a business. I want to change the world."

In March 2008, Facebook announced the hiring of Sandberg for the role of COO and her leaving Google. Sandberg joins Facebook after six years at Google, where she served as Vice President of Global Online Sales & Operations, building and managing Google's online sales channels for both AdWords and AdSense. The hire sends shockwaves through Silicon Valley. Google loses one of its most valuable executives; Facebook gains instant credibility with advertisers and investors.

After joining the company, Sandberg quickly began trying to figure out how to make Facebook profitable. Before she joined, the company was "primarily interested in building a really cool site; profits, they assumed, would follow." By late spring, Facebook's leadership had agreed to rely on advertising, "with the ads discreetly presented"; by 2010, Facebook became profitable.

The cultural clash is immediate. Facebook's office looks like a frat house—programmers coding in their underwear, Nerf gun battles, Red Bull pyramids. Sandberg arrives in designer suits, leaves at 5:30 p.m. to have dinner with her kids, and sends emails with proper punctuation. Early employees mockingly call her "Mom." But she doesn't try to change Facebook's culture; she builds a parallel one alongside it—professional, metrics-driven, revenue-focused.

Her first major victory comes in October 2007, before she even officially joins. Microsoft announced that it would take a $240 million equity stake in Facebook's next round of financing at a $15 billion valuation. The investment represents just 1.6% of the company, but the psychological impact is enormous. Facebook is suddenly worth more than many public companies. Google had competed for the deal but lost—a rare defeat that signals Facebook's growing power.

The advertising model Sandberg builds is revolutionary in its sophistication and creepiness. Every like, comment, photo tag, and status update becomes a data point. Facebook doesn't just know your demographics; it knows your relationships, interests, political views, shopping habits, and emotional states. Advertisers can target "recently engaged women aged 25-30 who live in San Francisco and like yoga"—a level of precision that makes Google's keyword targeting look primitive.

Facebook Platform launches in May 2007, allowing developers to build applications within Facebook. Within months, apps like FarmVille and Mafia Wars turn Facebook into not just a social network but a gaming platform, keeping users engaged for hours. Each app collects more data, creates more engagement, and generates more ad inventory.

The Open Graph, introduced in 2010, extends Facebook's reach across the entire internet. Any website can add Facebook's "Like" button, turning the web into Facebook's data collection network. When you click "Like" on a news article, Facebook knows. When you browse a shopping site, Facebook knows. The social network becomes a surveillance network, tracking users even when they're not on Facebook.

But the real transformation—the one that saves Facebook from irrelevance—is mobile. In 2012, Facebook has almost no mobile revenue despite half its users accessing it primarily through phones. Wall Street panics. The stock price craters. Sandberg and Zuckerberg make the boldest decision of their partnership: completely rebuild Facebook as a mobile-first company.

They acquire Instagram for $1 billion just before going public—a deal Sandberg helps negotiate despite board skepticism. They rebuild their entire advertising platform for mobile. They create new ad formats optimized for small screens and short attention spans. By 2013, mobile ads represent 41% of revenue. By 2016, it's 84%. The company that almost died because of mobile becomes the mobile advertising king.

As of 2023, advertising accounted for 97.8 percent of total revenue. Facebook hasn't just built an advertising business; it's built the most sophisticated behavior modification engine in human history. Every click is tracked, every scroll measured, every pause analyzed. The algorithm doesn't just show you ads; it shapes what you see, what you think, what you want. As one former executive puts it: "The thought process was: they trust us with their data, and we make money off it. And we do it so well that they don't even realize what's happening."

The transformation from dorm room project to advertising colossus is complete, but at what cost?

V. The IPO & Public Company Era

May 18, 2012, 6:30 a.m. Pacific Time: Mark Zuckerberg wakes up in his Palo Alto home wearing his signature gray t-shirt—the same one he'll wear to ring the opening bell, virtually, from Facebook's Menlo Park headquarters. By market close, he'll have lost $3 billion in personal wealth. Facebook's IPO, the most anticipated public offering since Google, is about to become one of the most catastrophic debuts in market history.

Facebook's initial public offering came on May 17, 2012, at a share price of US$38. The company was valued at $104 billion, the largest valuation to that date. The IPO raised $16 billion, the third-largest in U.S. history, after Visa Inc. in 2008 and AT&T Wireless in 2000.

The warning signs appear in the amendment filed just days before. Buried in the legalese: Facebook admits it has no idea how to make money from mobile, where half its users already access the platform. "We do not currently directly generate any meaningful revenue from mobile," the filing states—a confession that should have triggered alarm bells. Instead, institutional demand exceeds available shares by five times.

The underwriters—Morgan Stanley, Goldman Sachs, and JPMorgan—make a fateful decision. During the roadshow, nine days before the IPO, the underwriters selectively verbally disclosed to some institutional investors that Facebook may not meet its projected revenue and earnings estimates. Morgan Stanley, Goldman Sachs and J.P. Morgan collectively agreed to increase the offering range to $34–$38 per share with 421 million shares offered, a 25% increase in the number of shares. Overall, 74% of the IPO shares were placed with institutional investors and 26% went to retail investors.

This selective disclosure—telling big clients that revenue projections were weak while keeping retail investors in the dark—will later trigger lawsuits and regulatory investigations. But on IPO eve, the hype machine runs at full throttle. CNBC runs Facebook coverage nonstop. Retail investors mortgage houses to buy shares. The cultural phenomenon overshadows business fundamentals.

Trading was to begin at 11:00am Eastern Time on Friday, May 18, 2012. However, trading was delayed until 11:30am Eastern Time due to technical problems with the NASDAQ exchange. Those early jitters would foretell ongoing problems; the first day of trading was marred by numerous technical glitches that prevented orders from going through, or even confused investors as to whether or not their orders were successful.

The technical disaster compounds. The systems problems encountered during the Facebook IPO on May 18, 2012, caused the cross to fall 19 minutes behind the orders received by NASDAQ, whose IPO cross application calculated the price and volume of the cross based on the orders and cancellations received up until 11:11 a.m. Nasdaq's matching engine enters an infinite loop, unable to process cancellations properly. Some investors can't sell as the price falls; others receive shares at prices they never agreed to pay.

The stock opens at $42, briefly touches $45, then begins its descent. Morgan Stanley deploys what traders call the "green shoe"—buying shares to support the price at $38. They burn through hundreds of millions trying to prevent a first-day collapse. Initial trading saw the stock shoot up to as much as $45. This was seen as one of the biggest IPOs in technology and Internet history, with a peak market capitalization of over $104 billion. However, the stock fell as soon as it opened, and the share prices crashed more than 50% over the next couple of months.

Zuckerberg announced at the start of October 2012 that Facebook had one billion monthly active users, including 600 million mobile users, 219 billion photo uploads and 140 billion friend connections. But the market doesn't care about users who don't generate revenue. By September 2012, Facebook trades below $18—less than half its IPO price. Employees with stock options worth millions watch them become worthless. The financial press declares the IPO a "fiasco."

The stock stayed below the $38 mark for months and finally bottomed out in September 2012 below $18. The shares did not get back to the initial $38 again until August the following year, a full 16 months later.

The mobile crisis nearly kills Facebook. In Q2 2012, mobile represents zero revenue but over half of usage. Every user who shifts from desktop to mobile becomes less valuable. Wall Street realizes Facebook might be the next MySpace—a desktop relic in a mobile world. One analyst sets a price target of $5.

But Zuckerberg, humbled by the market's judgment, makes the decision that saves Facebook: burn everything down and rebuild for mobile. They rewrite the entire app in native code. They retrain every engineer to think mobile-first. They invent new ad formats—not banner ads shrunk for phones, but native ads that look like regular posts. They put ads directly in the News Feed, despite user backlash.

The transformation is brutal but effective. Mobile ad revenue grows from nothing to 14% of total revenue by Q3 2012, then 23% by year-end. The stock finally recovers to $38 in August 2013. By 2014, mobile represents the majority of ad revenue. The company that almost died because it missed mobile becomes the mobile advertising leader, second only to Google.

The Securities and Exchange Commission today charged NASDAQ with securities laws violations resulting from its poor systems and decision-making during the initial public offering (IPO) and secondary market trading of Facebook shares. NASDAQ has agreed to settle the SEC's charges by paying a $10 million penalty – the largest ever against an exchange.

Looking back, the IPO debacle seems almost quaint. The technical glitches, the trading delays, the lawsuits—all forgotten as Facebook's market cap soared past a trillion dollars. But the mobile crisis revealed something fundamental: Facebook survives not through innovation but through paranoid adaptation. When threatened, it doesn't create; it copies, acquires, or destroys. That playbook, forged in the crucible of 2012, would define its next decade.

VI. The Acquisition Spree: Instagram & WhatsApp

April 9, 2012, 11:45 a.m.: Zuckerberg sits in a conference room at Facebook headquarters, about to make the company's second most expensive acquisition ever. Across from him: Kevin Systrom, 28, Stanford graduate, former Googler, wearing his signature plaid shirt. Instagram launched just 18 months earlier on October 6, 2010, and already has 30 million users. The acquisition price: $1 billion in cash and stock—a figure that seems insane for a company with zero revenue and 13 employees.

The backstory makes the deal even more remarkable. At Stanford, Systrom turned down a recruitment offer from Mark Zuckerberg. Years later, when Systrom was building his first app, a location-based check-in service called Burbn, he founded Instagram in a San Francisco co-working space on October 6, 2010, after working on Burbn a year earlier. When that failed to catch fire, he and his partner peered deeply into the data.

In 2010, Kevin Systrom co-founded the photo-sharing and, later, video-sharing social networking service Instagram with Mike Krieger in San Francisco, California. The duo discovered users were ignoring Burbn's check-in features but obsessively sharing photos. They made a radical decision: strip everything except photos, add filters inspired by Systrom's love of analog photography, and rebuild from scratch. They renamed it Instagram, a portmanteau of instant camera and telegram.

The launch metrics were staggering. Instagram was released to the public in Apple's App Store on October 6, 2010, and reached 25,000 users on its first day. A month after launching, Instagram had grown to 1 million users. A year later, Instagram hit more than 10 million users. No app had ever grown this fast.

What made Instagram special wasn't just filters—it was timing. The iPhone 4 had just launched with a dramatically improved camera. Suddenly everyone had a high-quality camera in their pocket but no good way to share photos. Instagram solved this with elegant simplicity: take photo, add filter, share instantly. The square format, inspired by Polaroid and Kodak Instamatic, made every photo feel artistic.

Zuckerberg watches Instagram's rise with increasing alarm. Facebook's own photo-sharing features feel clunky by comparison. Worse, teenagers are flocking to Instagram, seeing Facebook as the platform where their parents lurk. He tries to build competing features—Camera, Poke—but they fail miserably. The only option left: buy or be disrupted.

The courtship begins subtly. Zuckerberg starts using Instagram, liking Systrom's photos, leaving comments. They meet for coffee, then dinner. Zuckerberg makes his intentions clear: join Facebook, keep your independence, build your vision with unlimited resources. Systrom hesitates. Twitter is also circling with a $500 million offer. Sequoia Capital values Instagram at $500 million in a recent funding round.

But Zuckerberg goes nuclear. Over a weekend in April 2012, he calls Systrom repeatedly, increasing the offer each time. The final number—$1 billion—is so high that Systrom can't refuse. The kicker: Zuckerberg promises Instagram will remain independent, keeping its brand, its culture, its team. Meta Platforms (then Facebook, Inc.) bought Instagram for $1 billion in 2012, a large sum at that time for a company that had 13 employees.

The deal closes just before Facebook's IPO, adding another headache to that disaster. Critics call Zuckerberg crazy for paying $33 per user for a company with no revenue. But Zuckerberg sees what others miss: Instagram isn't just an app; it's a generational shift in how humans communicate—from text to images. Instagram today has over one billion users and contributes over $20 billion to Meta Platforms's annual revenue.

On September 24, 2018, it was announced that Kevin Systrom resigned from Instagram and would be leaving in few weeks, along with co-founder Mike Krieger. The founders grew frustrated as Facebook gradually broke its independence promise, forcing Instagram to share data, integrate systems, and prioritize Facebook's advertising goals over product innovation. The acquisition that saved Facebook from irrelevance also revealed its pathological need for control.

February 19, 2014: Another massive acquisition, this time even more expensive and controversial. Jan Koum chose the name WhatsApp because it sounded like "what's up", and on his birthday, February 24, 2009, he incorporated WhatsApp Inc. in California. In 2014, Koum and Acton sold WhatsApp to Facebook for approximately US$19 billion in cash and stock.

The WhatsApp story begins with rejection and friendship. Jan Koum was hired as an infrastructure engineer at Yahoo shortly after he met Brian Acton while working at Ernst & Young as a security tester. Over the next nine years, the two worked together at Yahoo. In September 2007, Koum and Acton left Yahoo and took a year off, traveling around South America. They both tried to get jobs at Facebook, but weren't hired.

The irony is delicious—Facebook rejects two engineers who will later force Zuckerberg to pay $19 billion for their creation.

In January 2009, Koum bought an iPhone and believed the App Store was about to spawn a whole new industry of apps. He talked to his friend, Alex Fishman, about developing an app. Koum chose the name WhatsApp because it sounded like "what's up", and a week later on his birthday, February 24, 2009, he incorporated WhatsApp Inc. in California.

WhatsApp's genius was its simplicity and philosophy. No ads. No gimmicks. Just messaging that works everywhere, costs $0.99 per year, and respects privacy. Koum, who grew up in Soviet Ukraine where the government monitored all communications, was obsessed with user privacy. This wasn't just a business principle—it was personal.

The app struggled initially until Apple launched push notifications in June 2009. In September 2009, Koum released a new version with a messaging component. It was an instant hit with users, and within a few months, the user base increased from just a handful to 250,000. By 2014, WhatsApp had 450 million users, adding a million new users daily.

Zuckerberg's pursuit of WhatsApp was even more aggressive than Instagram. He emails Koum directly: subject line "Get together?" When Koum hesitates, Zuckerberg persists. They meet at Zuckerberg's home on February 9, 2014. The initial offer: $14 billion. Koum says no. Zuckerberg increases it to $16 billion. Still no. Finally, $19 billion—the largest acquisition of a venture-backed company ever.

Why pay such an astronomical sum? WhatsApp owned international messaging, especially in markets where Facebook was weak: India, Brazil, Africa. More importantly, WhatsApp was replacing SMS globally. Facebook couldn't build this—it had to buy it or watch another platform become the default communication layer for billions.

But the cultural clash was immediate and irreconcilable. Koum and Acton, former co-workers at Yahoo, founded WhatsApp in 2009. It promised private communications for 99 cents a year. Facebook wanted to monetize through ads and weaken encryption for business features. Koum and Acton refused. Acton left the company in November. He has joined a chorus of former executives critical of Facebook. Acton recently endorsed a #DeleteFacebook social media campaign.

In April 2018, Koum announced that he was leaving WhatsApp and stepping down from Facebook's board of directors due to disputes with Facebook. He left nearly $1 billion in unvested stock on the table—a billion-dollar middle finger to Zuckerberg's surveillance capitalism.

The failed attempts reveal Facebook's desperation. Snapchat spurned a $3 billion offer in 2013, with founder Evan Spiegel reportedly saying he'd rather build his own empire than be Zuckerberg's employee. Facebook tried to buy Musical.ly, which became TikTok, but lost to Chinese company ByteDance. Each rejection forced Facebook to copy features instead—Stories from Snapchat, Reels from TikTok—turning Facebook into a Frankenstein of borrowed innovations.

The $2 billion Oculus VR acquisition in 2014 was different—a bet on the future rather than buying competition. Palmer Luckey's virtual reality headsets represented Zuckerberg's first attempt to own the next computing platform. It would later become the cornerstone of the metaverse pivot, burning billions in pursuit of a future that might never arrive.

The acquisition spree reveals Facebook's fundamental weakness: it can't innovate, only imitate or acquire. Every major growth driver—Instagram, WhatsApp, Oculus—was built outside Facebook's walls. The company that promised to connect the world became a digital colonizer, buying potential competitors and crushing those who wouldn't sell. The price tag for this empire? Over $22 billion. The cost to society? That calculation is still being tallied.

VII. Crisis Years: Cambridge Analytica to Capitol Hill

March 17, 2018: The Guardian's office in London buzzes with nervous energy. Carole Cadwalladr and her team are about to publish the story that will trigger Facebook's worst crisis. Christopher Wylie, pink-haired and chain-smoking, has just blown the whistle on how Cambridge Analytica harvested data from up to 87 million Facebook profiles to build psychological warfare tools for elections. The revelation will wipe $134 billion off Facebook's market value in nine days.

The scandal's roots trace back to 2013, when University of Cambridge researcher Aleksandr Kogan creates an innocuous-looking app called "This Is Your Digital Life." The app consisted of a series of questions to build psychological profiles on users, and collected the personal data of the users' Facebook friends via Facebook's Open Graph platform. Only 270,000 people download the app, but Facebook's API allows it to harvest data from all their friends—a feature Facebook deliberately built to maximize data collection.

The app harvested the data of up to 87 million Facebook profiles. Cambridge Analytica used the data to analytically assist the 2016 presidential campaigns of Ted Cruz and Donald Trump. The stolen data includes not just names and birthdays but intimate details: private messages, likes, religious views, relationship status. Cambridge Analytica uses this to build "psychographic" profiles—algorithmic models that claim to predict and manipulate voter behavior better than voters know themselves.

The whistleblower, Christopher Wylie, describes it chillingly: "We exploited Facebook to harvest millions of people's profiles. And built models to exploit what we knew about them and target their inner demons. That was the basis the entire company was built on."

Facebook knew. In late 2015, The Guardian first reports Cambridge Analytica's activities. Facebook's response? Send a letter asking them to delete the data. No verification. No disclosure to affected users. No regulatory notification. For two years, Facebook sits on this knowledge while Cambridge Analytica uses the stolen data to influence Brexit and the U.S. presidential election.

When the story breaks, Facebook's initial response makes everything worse. They insist it's not a "data breach" because the data was accessed through their API as designed. Technically true but morally bankrupt—like saying it's not theft if you leave your door unlocked. Paul Grewal, Facebook's deputy general counsel, posts a defensive blog claiming users consented by not changing their privacy settings—settings buried so deep most users don't know they exist.

On March 26, 2018, a little after a week after the story was initially published, Facebook stock fell by about 24%, equivalent to $134 billion. The market finally understands what technologists have known for years: Facebook's business model depends on surveillance. Every feature, every design choice, every acquisition serves one purpose: harvesting human behavior for advertisers.

April 10-11, 2018: Zuckerberg sits before Congress for ten hours of testimony across two days. He wears a suit instead of his gray t-shirt, coached to appear contrite. Senators struggle with basic internet concepts—one asks how Facebook makes money if it's free (Zuckerberg's smirk: "Senator, we run ads"). But between the grandstanding and tech illiteracy, real damage emerges.

Senator Dick Durbin asks Zuckerberg if he'd be comfortable sharing what hotel he stayed in last night. Zuckerberg declines. "I think that might be what this is all about," Durbin says. "Your right to privacy, the limits of your right to privacy, and how much you give away in modern America in the name of, quote, 'connecting people around the world.'"

The prepared testimony reads like hostage statements: "It was my mistake, and I'm sorry." But when pressed on specifics—will you stop tracking non-Facebook users across the web? Will you support privacy legislation? Will you change your business model?—Zuckerberg deflects with practiced non-answers. His team will "follow up."

In July 2019, the Federal Trade Commission (FTC) voted 3-2 to approve fining Facebook $5 billion to finally settle the investigation into the data breach. The record-breaking settlement was one of the largest penalties ever assessed by the U.S. government for any violation. In the ruling, the FTC cited Facebook's continued violations of FTC privacy orders from 2012.

Five billion dollars sounds massive until you realize Facebook made $15 billion in profit that quarter. The stock price actually rises on the news—investors relieved the punishment isn't worse. It's the cost of doing business, like a restaurant paying health violations while continuing to serve contaminated food.

The deeper scandal isn't Cambridge Analytica—it's Facebook's entire model. The platform that promised to connect humanity has become history's most sophisticated surveillance apparatus. Every photo tagged, every message sent, every article read feeds algorithms designed to maximize engagement, which means maximizing outrage, division, and addiction.

The 2016 U.S. election reveals another crisis layer. Russian operatives create thousands of fake accounts, buying $100,000 in ads but generating billions of organic impressions. They organize both Black Lives Matter protests and Blue Lives Matter counter-protests, sometimes at the same location. Facebook's algorithms, optimized for engagement, amplify the most divisive content. The platform designed to bring people together tears democracy apart.

Content moderation becomes an impossible task. Facebook employs 15,000 moderators—many outsourced to countries like the Philippines, paid $2 per hour to watch beheadings, child abuse, and suicide videos. They develop PTSD at epidemic rates. Meanwhile, the AI systems Facebook promises will solve everything can't distinguish between historical war photos and violence, between art and pornography, between legitimate political speech and hate.

The political pressure intensifies from all sides. Conservatives claim bias when Alex Jones gets banned for harassment. Liberals demand more action against misinformation. Foreign governments threaten to ban Facebook unless it censors dissidents. Every decision becomes political. The platform that claimed to be neutral infrastructure reveals itself as the world's most powerful media company, making editorial decisions that affect billions.

In December 2020, FTC launched antitrust lawsuit concerning Instagram and WhatsApp acquisitions. Forty-six states join, seeking to break up the company. Internal documents, leaked by whistleblower Frances Haugen in 2021, reveal Facebook knowingly amplified hate speech for profit and knew Instagram was toxic for teenage girls' mental health but buried the research.

Yet nothing fundamental changes. The apologies follow a script. The fines get paid from petty cash. The congressional hearings produce viral moments but no legislation. The business model—surveillance capitalism—remains intact. As long as humans crave connection and validation, Facebook will monetize that need, no matter the cost to democracy, mental health, or social cohesion.

The Cambridge Analytica scandal wasn't a bug in Facebook's system—it was the system working exactly as designed. The real tragedy? We all know this now, and we keep scrolling anyway.

VIII. The Metaverse Pivot & Reality Labs

October 28, 2021, 10:00 a.m. Pacific: The Facebook logo disappears from the giant thumb sign outside headquarters. Workers scramble to replace it with "Meta"—a four-letter word that will cost shareholders hundreds of billions. Inside the company's virtual Connect conference, Zuckerberg appears as a cartoonish avatar, floating in digital space, demonstrating a future where we all live as legless torsos in pixelated wonderlands.

"From now on, we're going to be metaverse-first, not Facebook-first," Zuckerberg declares. The rebrand comes at a convenient time—just as Frances Haugen's whistleblower documents dominate headlines, revealing Facebook knowingly amplified hate for profit. Critics call it the most expensive distraction in corporate history.

The vision Zuckerberg pitches sounds like science fiction written by someone who's never experienced human joy. Virtual offices where avatars high-five. Digital concerts where you can't feel the bass. Shopping malls in cyberspace, because apparently what humanity needs is more consumption, now without physical constraints. He promises this will be more "embodied" than current internet, yet every demo shows floating torsos without legs—a technical limitation that becomes an unintentional metaphor.

Reality Labs, the division tasked with building this future, becomes a money incinerator of historic proportions. The losses are staggering: $6.6 billion in 2020, $10.2 billion in 2021, $13.7 billion in 2022, $16 billion in 2023. By Q4 2024, Reality Labs has tallied an operating loss of more than $60 billion since 2020. To put this in perspective, that's enough money to buy Twitter twice, or fund NASA's entire budget for three years.

The Quest headset evolution tells the story of a product nobody asked for, solving problems nobody has. Quest 2 launches at $299, selling reasonably well during pandemic lockdowns when people are desperate for escape. But retention is abysmal—most headsets gather dust after a few weeks. The dirty secret: VR makes people nauseous, sweaty, and isolated. The very thing Facebook claims to solve—human connection—becomes harder when you're wearing a face computer.

Quest Pro launches in October 2022 at $1,499, targeting professionals who might want to attend meetings as cartoon avatars. It flops spectacularly. The technology is impressive—eye tracking, face tracking, mixed reality—but nobody can explain why you'd want it. Reviews are brutal. The battery lasts two hours. The avatars still have no legs. Zuckerberg himself admits he uses it mainly for exercise—a $1,500 fitness device in a world where running is free.

Inside Reality Labs, former employees describe chaos. "A software company is trying to get into hardware and doesn't know how to manage it," says a former manager in engineering. "They're getting ahead of themselves with product launches and work teams when they don't even know what the technology is yet."

The cultural disconnect is profound. Facebook's motto "Move fast and break things" doesn't work for hardware. You can't push a buggy update to fix a physical device. The company goes through constant reorganizations—teams build projects for years only to have them cancelled when leadership changes. Executives with no VR experience are parachuted in to run divisions. Engineers joke they're building the Metaverse for an audience of one: Mark Zuckerberg.

Horizon Worlds, Meta's flagship metaverse app, becomes a punchline. Screenshots of Zuckerberg's avatar in front of the Eiffel Tower go viral for looking worse than 2006's Nintendo Wii graphics. Monthly users peak at 300,000—in a world of 3 billion Facebook users. Even Meta employees don't use it. Internal memos leak showing executives begging staff to spend time in Horizon Worlds, instituting mandatory "quality lockdowns" where employees must report bugs. The forced enthusiasm feels Soviet.

Then Apple enters the arena. The Vision Pro announcement in June 2023 is everything Meta's presentations aren't: polished, purposeful, premium. At $3,499, it's absurdly expensive, but it makes Meta's offerings look like toys. The interface is intuitive. The passthrough is crisp. Most importantly, Apple positions it as a productivity device, not an escape from reality. Meta scrambles to respond, rushing out Quest 3 announcements, but the damage is done. The company that was supposed to own the future of computing is suddenly playing catch-up.

February 2023 pivot to focus on generative AI while metaverse deemed for smaller audience marks an awkward admission. After burning $45 billion and restructuring the entire company, Zuckerberg quietly acknowledges what everyone else knew: the metaverse isn't happening, at least not now. AI becomes the new obsession, but Reality Labs continues hemorrhaging money, too big to kill, too failed to succeed.

The Ray-Ban Meta smart glasses, launched in 2023, offer a glimpse of what Reality Labs should have built from the start. They look like normal sunglasses. They don't make you nauseous. People actually wear them. The AI assistant is genuinely useful. They sell well. But they're a $299 accessory, not a computing platform. The metaverse vision that justified $60 billion in losses remains science fiction.

The tragedy of Reality Labs isn't just the money—it's the opportunity cost. While Meta burned billions on cartoon avatars, TikTok ate their lunch in social media. While they built virtual offices nobody wanted, OpenAI created ChatGPT. While they tried to escape reality, reality moved on without them.

Zuckerberg remains defiant, insisting history will vindicate him. He points to mobile phones, reminding skeptics that people mocked early smartphones too. But there's a crucial difference: phones solved obvious problems. They made communication easier. They put the internet in your pocket. The metaverse makes everything harder—socializing requires hardware, shopping requires headsets, working requires wearing a computer on your face.

The numbers tell the story. Reality Labs generates less than 2% of Meta's revenue while accounting for 20% of expenses. It's a vanity project funded by Instagram's profits, a billionaire's hobby subsidized by billions of users who never asked for it. Every quarter, analysts ask when the losses will stop. Every quarter, Zuckerberg promises the future is just around the corner.

The metaverse might eventually happen. Technology does tend toward more immersive experiences. But Meta's approach—building expensive hardware for nonexistent use cases while hemorrhaging billions—feels like trying to invent the airplane by throwing money off a cliff and hoping it flies. The pivot that was supposed to save Facebook from its reputation crisis has become a different kind of crisis: a CEO so powerful nobody can stop him from burning the company's future on his personal obsession with becoming the hero of Ready Player One.

IX. The AI Revolution & Current Strategy

The pivot happens quietly, without fanfare or apology. One day Meta is burning billions on legless avatars in the metaverse; the next, Zuckerberg is evangelizing about artificial general intelligence like he's always been an AI believer. The February 2023 announcement that metaverse investments would focus on a "smaller audience" while the company pursues generative AI marks one of the most expensive about-faces in corporate history.

But here's the twist: Meta was always an AI company. The News Feed algorithm that determines what 3 billion people see every day? That's AI. The system that recognizes faces in photos, translates languages instantly, and serves ads with creepy precision? All AI. Meta just never called it that because "algorithm" sounded less threatening than "artificial intelligence."

The LLaMA (Large Language Model Meta AI) project begins as a defensive move. OpenAI's ChatGPT explodes in November 2022, becoming the fastest-growing consumer application in history. Google has Bard. Anthropic has Claude. Amazon partners with everyone. Meta has... nothing public. Behind the scenes, they've been training massive models for years, but kept them internal, using them to moderate content and improve recommendations.

In February 2023, Meta releases LLaMA to researchers—not a product launch but a leak waiting to happen. Within weeks, the weights spread across 4chan and torrents. Instead of panicking, Meta leans in. If you can't control distribution, make openness your strategy.

Today, we're introducing Meta Llama 3, the next generation of our state-of-the-art open source large language model. This release features pretrained and instruction-fine-tuned language models with 8B and 70B parameters that can support a broad range of use cases.

The open-source strategy is genius wrapped in principle. By giving away what OpenAI charges for, Meta undermines competitors' business models while ensuring their AI runs everywhere. Every startup using LLaMA instead of GPT-4 weakens OpenAI. Every researcher improving LLaMA benefits Meta. We believe these are the best open source models of their class, period. In support of our longstanding open approach, we're putting Llama 3 in the hands of the community.

Bringing open intelligence to all, our latest models expand context length to 128K, add support across eight languages, and include Llama 3.1 405B—the first frontier-level open source AI model. Llama 3.1 405B is in a class of its own, with unmatched flexibility, control, and state-of-the-art capabilities that rival the best closed source models. The 405 billion parameter model represents Meta's Manhattan Project—thousands of GPUs running for months, burning enough electricity to power a small city.

The infrastructure investment is staggering. Meta announces they'll spend $60-65 billion on AI infrastructure in 2025 alone. They're building data centers the size of cities, installing hundreds of thousands of NVIDIA H100 GPUs at $30,000 each. The capital expenditure makes Reality Labs' losses look like pocket change. But unlike VR headsets, AI infrastructure has immediate returns: better ads, better engagement, better everything.

Meta AI, integrated across WhatsApp, Instagram, and Facebook, reaches billions overnight—a distribution advantage no competitor can match. While OpenAI struggles to scale ChatGPT to millions of users, Meta deploys to billions with a software update. The assistant is genuinely useful: answering questions, generating images, helping with tasks. But it's also training on every interaction, learning what billions of humans want, think, fear.

The Ray-Ban Meta smart glasses featuring Meta AI conversational assistant represent the convergence of Meta's hardware and AI ambitions. Unlike Quest headsets, they're subtle, practical, useful. You can ask them to identify objects, translate signs, remember where you parked. They're surveillance devices, yes, but ones people actually want to wear. The AI makes them magical; the form factor makes them acceptable.

Content recommendation algorithms powered by AI become Meta's secret weapon against TikTok. Reels, initially a desperate TikTok clone, transforms into something more sophisticated. The algorithm doesn't just show you what you've liked before; it predicts what you'll like next, keeping you scrolling longer than TikTok's famously addictive feed. Time spent on Reels increases 40% year-over-year.

The creator economy integration is masterful. Meta provides AI tools that help creators generate content, optimize posting times, even create AI versions of themselves to interact with fans. Every creator using Meta's AI tools becomes dependent on Meta's platform. The lock-in is complete: leave Meta, lose your AI-powered audience.

But the real game is bigger than products. Meta Founder & CEO Mark Zuckerberg shared, Llama has quickly become the most adopted model, with more than 650 million downloads of Llama and its derivatives, twice as many downloads as we had three months ago. Putting that in perspective, Llama models have now been downloaded an average of one million times a day since our first release in February 2023.

Zuckerberg's vision extends beyond current AI to artificial general intelligence (AGI)—machines that match or exceed human intelligence. He claims Meta will achieve this first, not through breakthrough research but through brute force: more compute, more data, more scale. The same strategy that built Facebook: not innovation but execution at planetary scale.

The contradictions are glaring. Meta claims to democratize AI while building massive moats. They champion open source while keeping their best models internal. They promise AI safety while racing to build AGI as fast as possible. The company that couldn't be trusted with social media data now wants to build superintelligence.

The deeper concern: Meta's AI knows too much. It's trained on decades of Facebook posts, Instagram photos, WhatsApp messages (despite encryption promises). It knows your relationships, preferences, weaknesses. Every baby photo, every drunk text, every political rant—all training data for machines that grow more powerful daily.

The AI strategy is working. Revenue grows. Engagement increases. Stock price soars. But the fundamental question remains: Should the company that amplified genocide in Myanmar, enabled election manipulation, and caused teen mental health crises be racing to build AGI?

Meta's AI revolution isn't just about competing with OpenAI or Google. It's about survival. If AI makes search obsolete, Google dies. If AI makes mobile apps unnecessary, Apple loses control. But social networks? They become more valuable with AI, not less. Every interaction generates data. Every data point improves the AI. Every improvement increases engagement. It's a flywheel that only accelerates.

The transformation from Facebook to Meta to AI company happens so fast it gives whiplash. But maybe that's the point. Keep moving fast enough and nobody can pin down what you actually are. Social network? Metaverse company? AI leader? The answer is whatever keeps the stock price rising and regulators confused.

As Zuckerberg races toward AGI, one thing becomes clear: Meta isn't pivoting to AI. AI has always been the core product. Those 3 billion users? They're not customers—they're training data. The largest behavioral dataset ever assembled, now feeding machines that grow smarter every day. The question isn't whether Meta will achieve AGI, but what it will do with that power when Facebook's algorithms already broke democracy with far less intelligence.

X. Financial Analysis & Business Model

The numbers tell a story of obscene profitability built on surveillance capitalism. Meta reported full year 2024 revenue of $164.501 billion, up 22% from $134.902 billion in 2023. The company that started in a dorm room now generates more revenue than the GDP of Ukraine. Advertising accounted for 98.3% of Meta's total revenue in the third quarter—confirming what everyone knows: Meta is an advertising company wearing a social network costume.

The profit margins are pornographic. Operating margin hit 43% in Q3 2024, marking the company's highest profitability in years. To put this in perspective, luxury brands like Louis Vuitton manage 20% margins. Meta prints money more efficiently than actual mints. Every dollar of revenue costs 57 cents to generate, leaving 43 cents of pure profit. In Q3 alone, net income grew 35% to $15.7 billion from $11.6 billion a year earlier.

The business model remains elegantly simple and morally bankrupt: harvest attention, package it as data, sell it to advertisers. The sophistication lies in the execution. Meta doesn't just know you clicked on a shoe ad; it knows you paused for 1.3 seconds, your pupil dilated (if using VR), you showed it to your spouse, discussed it in WhatsApp, and will be most susceptible to purchasing at 9:17 p.m. on Thursday after your third glass of wine.

The dual-segment reporting reveals the schizophrenia. Family of Apps (Facebook, Instagram, WhatsApp, Messenger) generates astronomical profits—operating income of $21.7 billion in Q3 2024 alone. Meanwhile, Reality Labs hemorrhages money like a severed artery, losing $4.4 billion in the same quarter. It's essentially two companies: one of history's most profitable businesses funding one of history's most expensive hobbies.

User metrics remain robust despite perpetual predictions of Facebook's death. Facebook's daily active users averaged 2.09 billion in September 2023, up 5% from a year earlier. Almost 3.07 billion monthly active users as of December 2023 across all platforms. That's 40% of humanity checking Meta properties monthly. The company has achieved something unprecedented: digital colonization of Earth.

But the real story is ARPU—Average Revenue Per User—the metric that reveals Meta's genius and evil. In the U.S. and Canada, ARPU exceeds $60 per quarter. Meta makes $240 annually from each American user—more than most streaming services charge. Except users aren't paying; they're being sold. Facebook International's significantly lower ARPU level vs. U.S. ARPU presents an opportunity for further monetization. Translation: Meta hasn't finished extracting value from the developing world.

The geographic revenue breakdown exposes digital imperialism. North America, with 10% of users, generates 45% of revenue. Asia-Pacific, with 45% of users, contributes just 20%. Meta extracts maximum value from wealthy democracies while using developing nations as data farms for AI training. Indians and Indonesians provide behavioral data that makes the algorithm smarter, which Meta then monetizes by selling ads to Americans.

Capital allocation tells its own story. Full-year 2024 capital expenditures will come in at $38 billion to $40 billion, mostly for AI infrastructure. Meta is building data centers like Egypt built pyramids—massive monuments to algorithmic power. The $60-65 billion planned for 2025 infrastructure spending exceeds the entire market cap of most Fortune 500 companies.

The buyback machine runs constantly. Meta announced a $50 billion share repurchase program in 2024, on top of the $40 billion announced in 2023. They're buying back stock faster than a guilty conscience, using profits from selling user data to increase the wealth of shareholders who don't care where the money comes from. It's wealth transfer from the surveilled to the investors, laundered through advertising.

Debt? Essentially zero. Cash and equivalents? Over $70 billion. Meta could stop generating revenue for two years and still pay every bill. This financial fortress makes them essentially regulation-proof. Fines become operating expenses. Lawsuits settle from petty cash. When the EU fines them $1.3 billion for privacy violations, the stock rises because investors expected worse.

The efficiency metrics are terrifying. Revenue per employee approaches $2 million—among the highest in corporate history. Meta generates more revenue per worker than oil companies extract per barrel. The "Year of Efficiency" in 2023, which saw 21,000 layoffs, proved you can fire 25% of your workforce and revenues still grow 20%. Those weren't jobs; they were inefficiencies in the money-printing machine.

Meta said it expects total expenses for fiscal 2024 to be in the range of between $96 billion and $98 billion. Nearly $100 billion in annual expenses sounds massive until you realize it generates $164 billion in revenue. The company spends money like a drunken sailor—if that sailor owned a casino where the house edge is 40%.

The real concern isn't profitability but concentration. Three companies—Meta, Google, and Amazon—control 70% of digital advertising globally. Meta alone controls 20%. When one company can influence what 3 billion people see, think, and buy, it's not just a business—it's a government without elections, a religion without salvation, a drug without rehabilitation.

Wall Street loves it. Meta said it is expecting fourth-quarter revenue to be between $45 billion and $48 billion, and investors rejoice. The stock trades at a P/E of 27—reasonable for a company growing 20% annually. But should any company with this much power over human behavior be valued like a normal business?

The financial success masks societal failure. Every earnings beat represents millions more addicted to scrolling. Every margin expansion means more effective manipulation. Every revenue surprise indicates the algorithm got better at hijacking human psychology. Meta's financial statements are humanity's psychological autopsy, documenting our descent into digital dependency with quarterly precision.

The paradox of Meta's business model: it's simultaneously too profitable and not profitable enough. Too profitable because 40% margins from selling human attention is obscene. Not profitable enough because those margins must fund the metaverse losses, the AI arms race, the regulatory settlements, and Zuckerberg's imperial ambitions. The machine must grow or die, extract more or collapse.

Looking forward, the business model faces existential questions. What happens when users age out? When regulators finally act? When Apple's privacy changes cut deeper? When AI makes advertising irrelevant? Meta's financials look invincible today, but so did Yahoo's, MySpace's, and every other digital empire before their fall.

For now, the numbers keep climbing, the profits keep flowing, and the machine keeps grinding human attention into shareholder value with unprecedented efficiency. Meta has perfected the alchemy of surveillance capitalism: turning privacy into profit, connection into cash, and human behavior into the most valuable commodity on Earth. The quarterly earnings calls celebrate new records while democracy burns and children develop anxiety disorders. But the stock is up, so nobody asks questions.

The ultimate metric isn't revenue or margins—it's power. And by that measure, Meta is priceless.

XI. Playbook: Business & Investing Lessons

The Meta playbook reads like a war criminal's memoir—effective tactics you hope nobody else copies. But for investors and entrepreneurs seeking lessons from Facebook's conquest of humanity, the strategies are as powerful as they are troubling.

Network Effects at Planetary Scale

The first lesson: network effects aren't linear, they're exponential with tipping points. Facebook didn't grow steadily—it exploded campus by campus, country by country. Each market had a critical mass moment where not being on Facebook became social suicide. The genius was maintaining scarcity during expansion. By keeping Facebook exclusive to college students until 2006, they created desire in the broader market. When they finally opened the gates, the masses flooded in.

The network effect compounds across products. Instagram makes Facebook stickier. WhatsApp keeps users in the ecosystem. Messenger becomes the default communication layer. Each product reinforces the others, creating a gravitational pull no single app can match. Leaving Facebook means leaving your entire social graph—a cost too high for most humans to bear.

The Power of Founder Control and Dual-Class Shares

Zuckerberg's iron grip on Facebook through supervoting shares—he controls 57% of voting power with 13% economic interest—enables long-term thinking impossible at normal public companies. He survived Cambridge Analytica, Congressional hearings, advertiser boycotts, and employee revolts because nobody can fire him. The board is decorative. Shareholders are passengers.

This structure enabled the Instagram and WhatsApp acquisitions when the board was skeptical, the pivot to mobile when desktop was still profitable, the metaverse bet when everyone thought it insane, and the AI transformation when investors wanted efficiency. A normal CEO would have been ousted five times over. Zuckerberg remains because he structured power before he needed it.

"Move Fast and Break Things" to "Move Fast with Stable Infrastructure"

The evolution of Facebook's motto reveals strategic maturation. Early Facebook really did break things—the site crashed constantly, features shipped half-built, privacy settings changed without warning. This was acceptable when fighting for survival. But you can't run critical infrastructure for 3 billion people like a startup.

The new approach maintains speed but adds sophistication. Facebook still ships faster than any company its size—thousands of code changes daily, constant experimentation, features tested on millions before global rollout. But now it's controlled chaos. The infrastructure is bulletproof even as the surface constantly evolves. They learned to move fast without breaking the money machine.

Platform Strategy: Build, Buy, or Copy

Facebook's three-pronged approach to competition is brutally effective:

- Build: Create your own version if you have unique insight (News Feed, Groups)

- Buy: Acquire threats before they scale (Instagram, WhatsApp, Oculus)

- Copy: Shameless clone features that work (Stories from Snapchat, Reels from TikTok)

The key insight: originality is overrated. Execution matters more than innovation. Facebook didn't invent social networking, photo sharing, messaging, or stories. They just did them better, at scale, with superior infrastructure. When Snapchat invented Stories, Facebook copied it across all properties within months. Snapchat had the idea; Facebook had 3 billion users.

The Importance of Transitions

Every platform shift could have killed Facebook: - Desktop to mobile (2012): Stock crashed 50% on mobile monetization fears - Feed to Stories (2017): Cannibalized their own product before competitors could - Social to messaging (2014): Bought WhatsApp for $19 billion when messaging threatened social - Mobile to AR/VR (2021): Betting $60+ billion that spatial computing is next

The lesson: cannibalize yourself before competitors do. Facebook killed its own desktop experience to win mobile. They undermined their feed to push Stories. They're burning billions on VR while mobile still prints money. The transitions are painful, expensive, and often wrong—but missing one is fatal.

Regulatory Arbitrage and the Cost of Being Too Big

Facebook mastered regulatory arbitrage—operating between jurisdictions, exploiting gaps in outdated laws, moving faster than regulators can respond. Data protection in Europe? Route through Ireland. Content moderation in Myanmar? Claim you're a platform, not a publisher. Tax optimization? Double Irish with a Dutch sandwich.

But size becomes its own prison. When you're too big, every move draws scrutiny. Every acquisition faces antitrust review. Every feature change triggers Congressional hearings. The FTC lawsuit seeking to break up Instagram and WhatsApp proves that success at Facebook's scale becomes self-limiting. The lesson: there's an optimal size for dodging regulation—big enough to matter, small enough to maneuver.

When to Pivot Hard vs. Incremental Evolution

The Meta rebrand was a masterclass in misdirection. Facing the worst crisis in company history (whistleblowers, teen mental health, democracy concerns), Zuckerberg changed the conversation entirely. Instead of defending Facebook, he announced a new future. The media spent months debating the metaverse instead of discussing genocide in Myanmar.

But most changes are incremental. The News Feed evolved through thousands of tiny adjustments. The ad platform improved through millions of experiments. The lesson: save dramatic pivots for existential moments. Everything else should be constant, data-driven iteration.

Data as Defensive Moat

Facebook's true moat isn't users or features—it's data. Twenty years of behavioral data, social graphs, preference histories, and interaction patterns. A competitor can copy Facebook's features in a weekend. They can't copy two decades of data accumulation. Every day users spend on Facebook widens this moat.

The playbook: make data accumulation feel like value creation. Users think they're building profiles, sharing memories, connecting with friends. Really, they're training algorithms that become impossible to replicate. The switching cost isn't leaving the app—it's losing the algorithm that knows you better than you know yourself.

The Platform Paradox

Facebook wants to be seen as a neutral platform (to avoid liability) while acting as a publisher (to maximize engagement). They want the benefits of being infrastructure (regulatory protection) with the profits of being media (advertising dollars). This deliberate ambiguity—are we tech or media? platform or publisher?—lets them claim whatever identity serves the moment.

Talent and Culture

Facebook's culture is unique: paranoid, aggressive, cult-like. The interview process selects for true believers. The compensation creates golden handcuffs. The peer pressure enforces conformity. Employees work crushing hours not because they have to, but because everyone else does. The mission—"connecting people"—justifies any sacrifice.

The recruiting playbook: hire the best engineers at any cost, acqui-hire entire teams for talent, create internal competition between teams, and fire the bottom 15% annually. It's social Darwinism with stock options. Brutal but effective.

The Innovator's Dilemma Solution

Facebook solved the innovator's dilemma by becoming multiple companies. When Instagram threatened Facebook, they bought it but kept it separate. When WhatsApp emerged, same playbook. Now TikTok threatens Instagram, so they build Reels. Each product cannibalizes the others, but Meta owns them all. It's controlled cannibalization—they eat themselves before competitors can.

Capital as a Weapon

Facebook weaponizes capital. They don't just outspend competitors; they make competition economically irrational. Paying $1 billion for Instagram wasn't about Instagram's value—it was about denying it to others. Spending $60 billion on the metaverse isn't about VR—it's about preventing anyone else from owning the next platform.

The Ultimate Lesson

Facebook's playbook proves an uncomfortable truth: in technology, dominance compounds. The big get bigger. The rich get richer. The powerful get more powerful. Network effects, data accumulation, capital advantages, and talent concentration create insurmountable moats. Facebook didn't win by being better—they won by being bigger, faster, and more ruthless than everyone else.

For investors, the lesson is clear: bet on network effects, dual-class shares, and founders with dictatorial control. For entrepreneurs: move fast, copy what works, and sell to Facebook before they copy you. For society: maybe some things shouldn't be optimized for engagement. Maybe some powers shouldn't be concentrated. Maybe some playbooks shouldn't be followed.

But the market doesn't care about maybe. It cares about returns. And by that measure, Facebook's playbook is perfect.

XII. Bear vs. Bull Case

Bear Case: The Empire's End

The bear case for Meta isn't about quarterly earnings misses or user growth deceleration—it's about existential threats converging simultaneously. Start with regulation: In July 2019, the Federal Trade Commission (FTC) voted 3-2 to approve fining Facebook $5 billion to finally settle the investigation into the data breach. The record-breaking settlement was one of the largest penalties ever assessed by the U.S. government for any violation. But that was just the beginning. The FTC's antitrust lawsuit seeking forced divestiture of Instagram and WhatsApp could shatter Meta's empire into competing pieces.

Youth exodus presents an demographic death spiral. TikTok doesn't just compete for attention—it's rewiring how generations consume content. Facebook is now "for old people," Instagram increasingly abandoned by Gen Z, and WhatsApp irrelevant in markets where WeChat or Telegram dominate. Meta's response—copying TikTok with Reels—feels desperate, like a middle-aged dad learning to skateboard.

Reality Labs is the money pit that could sink the ship. The numbers only became worse for Meta over the ensuing years: a $10 billion loss in 2021, $13 billion in 2022, and $16 billion in 2023. Over $60 billion incinerated chasing a vision nobody wants. The metaverse pivot increasingly looks like Zuckerberg's Howard Hughes moment—a billionaire's descent into expensive obsession while the core business rots.

Apple's App Tracking Transparency (ATT) was just the opening salvo. As Apple controls iOS and Google controls Android, they can slowly strangle Meta's data collection. Every privacy feature Apple announces shaves billions off Meta's market cap. The platform dependency is fatal—Meta doesn't control its distribution, making it vulnerable to operating system changes that could cripple ad targeting overnight.

The reputational damage may be irreversible. On March 26, 2018, a little after a week after the story was initially published, Facebook stock fell by about 24%, equivalent to $134 billion. Trust, once broken, rarely returns. Parents actively warn children about Facebook. Governments treat Meta as a hostile foreign power. Employees leak constantly. The brand is toxic, association radioactive.

Competitive threats multiply faster than Meta can copy. TikTok proved someone could build a billion-user platform despite Facebook's dominance. BeReal captured authenticity. Discord owns gaming communities. Telegram has secure messaging. LinkedIn has professionals. The unbundling of Facebook's bundle accelerates—each vertical picked off by a specialized competitor.

The advertising model faces structural challenges. Privacy regulations like GDPR make targeting harder. Cookie deprecation eliminates tracking. Consumers install ad blockers. Brands shift to influencer marketing, bypassing Meta's ad platform. The precision targeting that justifies premium prices erodes daily.

AI disruption could obsolete social networks entirely. Why scroll Facebook when ChatGPT can summarize what your friends are doing? Why post to Instagram when AI can generate better content? Why use WhatsApp when AI assistants handle communication? Meta's pivot to AI might be too late—OpenAI, Google, and Anthropic have insurmountable leads.

The China risk looms large. Revenue from Meta's Asia-Pacific region grew 15%, representing the company's slowest-growing region. That was down from growth of 28% in the second quarter, attributed to the deceleration to lapping demand from China advertisers. If China-linked advertisers like Temu and Shein pull spending, or if geopolitical tensions escalate, billions in revenue evaporate.

Finally, the key person risk: everything depends on Zuckerberg. His control is absolute, his vision unquestioned, his mistakes uncorrectable. One health issue, one scandal, one board revolt (if they could manage it), and Meta becomes a rudderless ship. The company is structured as an extension of one man's will—a single point of failure for a three-trillion-dollar enterprise.

Bull Case: The Unstoppable Machine

The bull case starts with math: 3 billion users growing 5% annually, multiplied by rising ARPU, equals inevitable growth. Meta has achieved something unprecedented—default communication infrastructure for humanity. Leaving isn't just hard; for billions, it's impossible. Where else do you find your high school friends, your family photos, your business contacts? The switching costs approach infinity.

The advertising duopoly with Google remains unbreakable. Advertising accounted for 98.3% of Meta's total revenue, and that revenue grew 19% year-over-year despite every headwind. Small businesses have no alternative for targeted advertising at scale. Meta's self-serve ad platform is crack cocaine for entrepreneurs—instant customers for minimal spend. Until someone builds better targeting with equal reach, advertisers are prisoners.

AI leadership is understated but real. Llama has quickly become the most adopted model, with more than 650 million downloads of Llama and its derivatives. Llama models have now been downloaded an average of one million times a day since our first release in February 2023. Meta's open-source strategy is brilliant—let others improve your models for free while maintaining control of deployment at scale.

Reels successfully defended against TikTok. Time spent increased 40% year-over-year. The algorithm improved. Creator tools evolved. Meta proved they can copy and crush any social innovation. They don't need to invent—just fast-follow with superior infrastructure and existing users.

WhatsApp monetization remains nascent. With 2 billion users generating minimal revenue, it's a sleeping giant. Business messaging, payments, commerce—each worth tens of billions in untapped potential. WhatsApp could become WeChat for the rest of the world, a super-app generating $100+ billion annually.