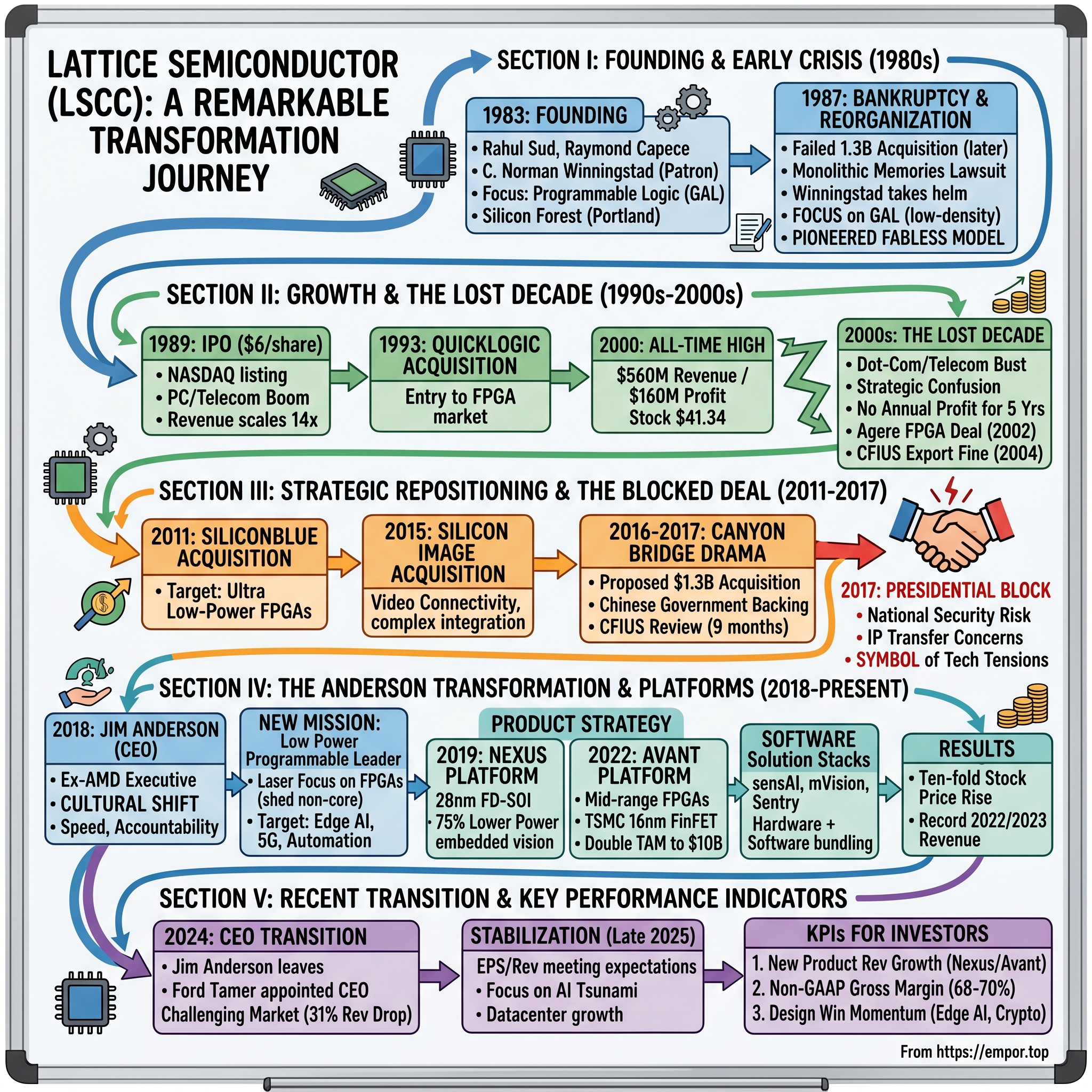

Lattice Semiconductor: The Low-Power FPGA Underdog's Remarkable Transformation

I. Introduction & Episode Roadmap

Picture this: It's September 2017, and the White House has just issued an executive order blocking a $1.3 billion acquisition of an Oregon-based semiconductor company. The buyer? A Chinese government-backed private equity fund. The target? A company most Americans had never heard of—one that had filed for bankruptcy thirty years earlier, struggled through the dot-com bust, and spent most of the 2000s flirting with irrelevance.

That company was Lattice Semiconductor.

Lattice Semiconductor Corporation is an American semiconductor company specializing in the design and manufacturing of low power field-programmable gate arrays (FPGAs). Headquartered in the Silicon Forest area of Hillsboro, Oregon, the company also has operations in San Jose, Calif., Shanghai, Manila, Penang, and Singapore.

Today, in late November 2025, Lattice stands at an inflection point unlike any in its four-decade history. After AMD completed the acquisition of Xilinx in February 2022, Lattice Semiconductor became the last fully independent major manufacturer of FPGAs. The competitive landscape has shifted dramatically once again: Intel Corporation announced in April 2025 that it has entered into a definitive agreement to sell 51% of its Altera business to Silver Lake, a global leader in technology investing. The transaction, which values Altera at $8.75 billion, establishes Altera's operational independence and makes it the largest pure-play FPGA semiconductor solutions company.

As of late October 2025, the stock price of Lattice Semiconductor is $73.64, with a current market capitalization of approximately $10.1 billion. This represents a company that has transformed itself from a near-bankrupt startup into a critical player in one of the most strategically important industries on the planet.

The story of Lattice Semiconductor is not simply about semiconductors—it's about survival through bankruptcy, reinvention through crisis, the power of strategic focus, and how one company became a bellwether for U.S.-China technology tensions. How did a company that nearly died in 1987 become the last independent FPGA maker standing? How did a blocked Chinese acquisition become the turning point that ultimately led to a remarkable turnaround? And what does Lattice's future look like in a world where edge AI, 5G infrastructure, and industrial automation are driving unprecedented demand for low-power programmable logic?

These are the questions we'll explore in this deep dive into one of the most resilient companies in semiconductor history.

II. Founding Context: The 1980s Semiconductor Gold Rush

The early 1980s were a time of unbridled optimism in the semiconductor industry. Silicon Valley was minting millionaires, venture capital was flowing freely, and every chip designer believed they could be the next Intel. It was in this environment that two management novices decided to take their shot.

Rahul Sud and Raymond Capece started Lattice in the early 1980s, when the market for semiconductors was red hot. Sud, a native of India, had worked as a chip designer at both Inmos and vaunted Intel. Capece had gained experience raising capital through his job with venture capitalist Ben Rosen. Although neither partner had experience managing a company, they believed that Sud's ideas and Capece's ability to raise investment capital were a winning combination.

The pair had technical ambition but lacked the credentials and connections that typically opened doors in Silicon Valley. They needed a patron—someone with credibility, capital, and connections. They found that patron in an unlikely place: Portland, Oregon.

The pair formed Lattice International Inc. in April of 1983 with the help of C. Norman Winningstad, the founder of the successful Floating Point Systems, a maker of computers and peripherals.

Winningstad was more than just an investor; he was a visionary who saw an opportunity to build something larger than a single company. Winningstad was integral to Lattice's startup because he and several of his friends in the Portland business community fronted much of the initial investment capital. They invested in the company partly because they believed that Lattice's success would help Portland become a U.S. tech hub—what would later become known as the "Silicon Forest."

C. Norman Winningstad was instrumental in securing initial funding, raising approximately $19 million. This was a substantial war chest for a startup at the time, reflecting the heady valuations of the semiconductor boom.

Lattice was founded on April 3, 1983, by C. Norman Winningstad, Rahul Sud, and Ray Capece, with investment from Winningstad, Harry Merlo, Tom Moyer, and John Piacentini. Lattice was incorporated in Oregon in 1983 and reincorporated in Delaware in 1985.

The company's early technical focus centered on programmable logic—a nascent but promising field. Their innovation in programmable logic began with the 1985 introduction of the GAL, the first Electrically Erasable Programmable Logic Device (PLD). This was genuinely innovative technology: chips that could be programmed, erased, and reprogrammed, offering flexibility that fixed-function semiconductors couldn't match.

But Sud had grander ambitions. He envisioned building a substantial manufacturing facility and competing head-to-head with established players. It was an audacious goal for a startup with no operating history and founders with no management experience. As events would soon demonstrate, ambition and capital were not enough.

What matters for investors: Lattice's founding story contains the seeds of both its greatest strengths and its most persistent vulnerabilities. The company was born from technical innovation in programmable logic—a niche that would define its identity for four decades. But it was also born from overconfidence and inexperience, setting the stage for the crisis that would nearly destroy it.

III. Early Crisis: Bankruptcy and Reinvention (1985-1991)

The company's first product, a high-speed memory chip, was launched in early 1985. However, this debut coincided with a downturn in the semiconductor market, compounded by internal design and production hurdles.

The timing could not have been worse. The semiconductor industry, which had seemed invincible just months earlier, was entering one of its periodic savage downturns. Orders dried up. Venture capitalists became cautious. The memory chip that was supposed to establish Lattice as a serious player instead became a millstone around the company's neck.

Lattice lost $7 million in 1986 from sales of the same amount. Despite that deficit, it looked as though the company's fortunes might be changing. Sales of a version of its programmable memory chip were surging and overall revenues were climbing.

For a brief moment, it seemed like Lattice might survive through sheer determination. But then came the lawsuit that nearly killed the company.

But that temporary boon was squelched when Monolithic Memories, a Silicon Valley chip maker, filed suit against Lattice claiming patent infringement. Sales of Lattice's promising chip quickly dried up and the company found itself back at square one. By 1987 Lattice was on the ropes.

Desperate, Sud scrambled to raise $10 million in venture capital to keep the enterprise afloat. Just one year earlier he had explained to The Oregonian that Lattice would succeed because there were no semiconductor-industry venture capitalists involved to "force-feed the company with their conventional wisdom." Not surprisingly, Sud was unable to secure financing.

The irony was bitter. Sud had proudly kept traditional semiconductor VCs at arm's length, and now, when he desperately needed their help, they wanted nothing to do with him. The company went through chapter 11 bankruptcy reorganization in July 1987.

This could have been the end of the story. Many startups that file for bankruptcy never emerge. But Lattice had one critical advantage: C. Norman Winningstad.

Having kept the company from going under, Winningstad now faced the formidable task of making Lattice into a profitable competitor in the semiconductor industry. Success hinged on the company's ability to parlay its technology into products that it could market. When Winningstad took the helm, Lattice was trying to support five product lines. He decided to dump all except the most promising one; General Array Logic (GAL) devices.

This was a pivotal decision. Rather than trying to be everything to everyone, Lattice would focus on doing one thing extremely well. Lattice's GAL devices were low-density chips used primarily to link other microprocessors in consumer electronics and computers. Lattice's GAL chips were low-tech in comparison to some of its other products. But insufficient capital would force Lattice to shelve work on more advanced technology, such as its electrically erasable memory chips and digital signal processing devices.

Co-founder Sud left as president in December 1986, and Winningstad left in 1991 as chairman of the board.

Perhaps the most consequential move during this period was not a product decision but a personnel decision. Winningstad's most pivotal move at Lattice came in 1989, when he convinced Cyrus Tsui to become president of the company. Cyrus Tsui became the company's chief executive officer in 1988.

Beyond the management changes, Lattice emerged from bankruptcy with an innovation in business model that would prove far more valuable than any chip design: Lattice Semiconductor pioneered the fabless semiconductor model, a strategy that involved forging manufacturing agreements in exchange for licenses to its CMOS EEPROM technology. This innovative approach has since been widely adopted across the industry, now contributing to annual sales exceeding $100 billion.

What matters for investors: The bankruptcy and subsequent reorganization established two patterns that would define Lattice for decades: the importance of strategic focus (concentrating on what you do best rather than chasing every opportunity), and the power of the fabless model (which remains central to Lattice's strategy today). Companies that survive near-death experiences often emerge with a clarity of purpose that more comfortable competitors lack.

IV. The IPO and Growth Era (1989-2000)

The Lattice that emerged from bankruptcy was leaner, more focused, and finally ready to grow. On November 9, 1989, Lattice became a publicly traded company when its shares were listed on the NASDAQ after an initial public offering. The initial share price was $6, and raised almost $14 million for the company.

The timing was fortuitous. The late 1980s and early 1990s saw an explosion in personal computing and consumer electronics—exactly the markets where Lattice's programmable logic devices found their sweet spot. In July 1990, a second stock offering of nearly 1.5 million new shares raised $22.6 million at $16.25 per share. The stock had nearly tripled in less than a year, a sign of investor confidence in the company's turnaround.

Following the IPO, the company experienced revenue growth driven by sales of low-density programmable logic devices, with annual revenues reaching $38.9 million in fiscal 1990 and increasing to $64.5 million in fiscal 1991.

But Lattice's ambitions were expanding beyond its original niche. In 1993, the company made a strategic acquisition that would reshape its identity. Bolstering the success of that new line in 1993 was Lattice's $19 million purchase of QuickLogic Corp., a Santa Clara, California, designer and marketer of field-programmable gate arrays (FPGAs). FPGAs were a rapidly growing segment of the semiconductor industry that complemented Lattice's drive into high-density programmable logic devices. FPGAs were more versatile and generally more powerful than high-density programmable logic devices and were typically used in the most demanding military, aerospace, and industrial applications.

The merger worked well because Tsui had worked with the founders of QuickLogic when he was with Monolithic Memories. The same company that had nearly destroyed Lattice with a patent lawsuit had, ironically, created the professional network that enabled this strategic acquisition.

Lattice managed to boost sales of both its high-density and low-density devices during the early 1990s. Importantly, it advanced in the high-density market rather quickly. That speedy progress was largely attributable to an important advantage; unlike its competitors' high-density programmable chips, Lattice's semiconductors could be reprogrammed.

Recognition followed performance. Forbes ranked the company as their 162nd best small company in the United States in 1996, and Lattice began to double the size of its Hillsboro headquarters.

The dot-com era proved to be a golden age for Lattice. As telecommunications infrastructure expanded rapidly and consumer electronics proliferated, demand for programmable logic surged. In 2000, annual revenues topped $560 million with profits of $160 million.

These were staggering numbers for a company that had been bankrupt just thirteen years earlier. A 28% profit margin would be exceptional in any industry; in semiconductors, it was remarkable. Its stock price reached an all-time high of $41.34, adjusted for splits.

This expansion peaked in the late 1990s amid demand for its chips in telecommunications and networking applications.

What matters for investors: The 1990s demonstrated Lattice's ability to execute when conditions were favorable. Revenue growth of more than 14x (from $38.9 million to $560 million) over a decade showed that the company could scale. But as the next chapter would demonstrate, Lattice had become dangerously dependent on the telecom boom—and dangerously unfocused in its product strategy.

V. The Lost Decade: Dot-Com Bust to Financial Crisis (2000-2010)

The collapse came swiftly and mercilessly. When the dot-com bubble burst and the telecom industry imploded, Lattice's customers—the same companies that had been buying chips as fast as Lattice could make them—suddenly stopped ordering.

Revenues plunged approximately 48% after the dot-com and telecom bust around 2000-2001, leading to net losses and inconsistent profitability.

For the next five years, however, the company recorded no annual profit. The company that had earned $160 million in 2000 couldn't turn a profit for half a decade.

Lattice purchased Agere Corporation's FPGA division in 2002. In 2004, the company settled charges with the United States government that it had illegally exported certain technologies to China, paying a fine of $560,000. The export control issue—though resolved—foreshadowed the geopolitical tensions that would later become central to Lattice's story.

In 2005, Tsui was replaced as CEO by Steve Skaggs and the company laid off employees for the first time. The long-serving CEO who had guided Lattice through its post-bankruptcy growth was gone, and the company faced the painful reality of downsizing.

The financial crisis era brought fresh challenges. In June 2008, Bruno Guilmart was named as chief executive officer of the company, replacing Steve Skaggs. For fiscal year 2008, Lattice had a loss of $32 million on annual revenues of $222.3 million.

Through July 2009, the company had lost money for ten straight quarters, and had its first profitable quarter in three years during the fourth quarter of 2009. Bruno Guilmart left the company in August 2010, and Darin Billerbeck, former Zilog CEO, who had just sold Zilog in the previous year, was named the new CEO in October of that year, starting in November.

This period was characterized by what industry observers called "strategic confusion." Lattice was spreading itself too thin, chasing opportunities in multiple directions without clear focus. The company had lost the discipline that had saved it after bankruptcy.

The company reported 2011 revenue of $318 million. Lattice started a stock buy-back program in 2010 that continued into 2012 that would total about $35 million if fully implemented. In 2011, the company was ranked third among the world's makers of field programmable gate array (FPGA) devices and second for CPLDs & SPLDs.

What matters for investors: The lost decade illustrates a crucial lesson: market leadership can be fragile. Lattice went from dominant performer to struggling also-ran in less than five years. The company survived, but barely. The seeds of the next chapter—strategic focus through targeted acquisitions—were planted during this period of struggle.

VI. Strategic Acquisitions and Repositioning (2011-2016)

The turning point came not from internal innovation but from strategic acquisition. On December 9, 2011, Lattice announced it was acquiring SiliconBlue for $63.2 million in cash. Lattice announced in July 2012 a foundry agreement with United Microelectronics Corporation. Lattice returned to profitability in 2013 with a profit of $22.3 million on $332.5 million in revenues.

The SiliconBlue acquisition was particularly significant. SiliconBlue specialized in ultra-low-power FPGAs—chips designed for mobile devices and other applications where battery life was paramount. This acquisition planted the seeds for Lattice's future identity as "the low-power programmable leader."

The company acquired Silicon Image Inc. for $606 million in March 2015 and moved company headquarters to Downtown Portland.

The Silicon Image acquisition was Lattice's largest ever, nearly ten times the size of the SiliconBlue deal. Silicon Image brought expertise in video connectivity—technologies used to transmit high-definition video signals between devices. The deal expanded Lattice's product portfolio but also created integration challenges and added complexity to the business.

Then came an unexpected development that would prove prophetic. In April 2016, Tsinghua Holdings said in a U.S. filing that it accumulated a roughly 6 percent stake in Lattice Semiconductor through shares purchased on the open market.

Tsinghua Holdings was no ordinary investor. It was connected to the Chinese government and had been on an aggressive acquisition spree in the semiconductor industry. Tsinghua Group acquired a 6% equity stake in Lattice in April 2016, 4% shy of the 10% threshold that requires a CFIUS review.

The stake was just below the threshold that would trigger automatic government scrutiny—a fact that would not go unnoticed by U.S. national security officials.

What matters for investors: The 2011-2016 period saw Lattice lay the groundwork for its future identity through acquisitions. SiliconBlue brought low-power expertise that would become central to the company's differentiation. But the period also saw the first signs of Chinese interest in the company—interest that would soon create one of the most dramatic episodes in modern semiconductor history.

VII. The Canyon Bridge Drama: A Presidential Block (2016-2017)

In late 2016, Lattice Semiconductor found itself at the center of a geopolitical drama that would reshape not only the company but the entire landscape of foreign investment in American technology.

The acquisition of Lattice by Canyon Bridge was announced in November 2016 for a total purchase price of $1.3 billion.

Lattice was the target of a proposed acquisition by Canyon Bridge, an investment fund organized in Delaware whose ultimate owner is China Venture Capital Fund Corporation Limited, a corporation organized under the laws of the People's Republic of China. According to press reports, Canyon Bridge's mandate is to make investments in US companies in the semiconductor industry.

For Lattice shareholders, the deal looked attractive: a significant premium to the trading price, and a path to growth through access to Chinese capital and markets. For the acquiring party, Lattice represented exactly what China's "Made in China 2025" industrial policy sought: advanced semiconductor technology that could help close the gap with American chip makers.

Notably, Canyon Bridge is also backed by a Beijing-based "private equity firm" that is vertically linked to the Chinese central government and adjacently linked to China's space program. Dr. David Wang, a Senior Advisor with Canyon Bridge, was also formerly a chief executive at China's state-owned Semiconductor Manufacturing Industry Corporation (SMIC). Canyon Bridge's obtuse links to the Chinese government raised significant red flags about the underlying purpose of its bid and the motives of its stakeholders.

What followed was a regulatory gauntlet unlike any the semiconductor industry had seen. The CFIUS review of the Lattice transaction lasted more than nine months, including an initial 30-day review and three consecutive 45-day investigations, during which CFIUS was unable to resolve various national security concerns with the deal.

The parties filed a joint voluntary draft notice with CFIUS in December 2016 and, after receiving comments, filed a voluntary final notice. The parties subsequently went through three rounds of CFIUS filings, i.e., the parties withdrew their filing and submitted a new filing (presumably with revised deal terms and/or assurances to address national security concerns) on March 24, 2017, and again on June 9, 2017, "to allow more time for review and discussion with CFIUS."

On September 1, 2017, Lattice disclosed in an SEC filing that CFIUS had informed the parties that it intended to recommend that the President block the transaction. In the same filing, Lattice indicated that the parties had proposed "comprehensive mitigation measures" and that it had taken the unconventional approach of appealing to the President for approval. In the vast majority of cases when CFIUS recommends blocking a deal, the parties voluntarily withdraw their notice and abandon the transaction to avoid a near-certain public order from the President blocking the deal. However, Lattice, like Aixtron before it, sent the case to the President for final disposition, believing that it had solid arguments that might persuade the President on a political level.

The gamble failed.

On September 13, 2017, President Trump issued an Executive Order blocking the $1.3 billion acquisition of a U.S. semiconductor manufacturer, Lattice Semiconductor Corporation, by a Chinese government-backed private equity fund, Canyon Bridge Capital Partners. The order followed a recommendation from the Committee on Foreign Investment in the United States ("CFIUS") that the transaction posed a risk to national security.

This marks only the fourth time that a U.S. President has ordered a transaction blocked or unwound due to national security concerns.

The statement further explained, "The national security risk posed by the transaction relates to, among other things, the potential transfer of intellectual property to the foreign acquirer, the Chinese government's role in supporting this transaction, the importance of semiconductor supply chain integrity to the US government, and the use of Lattice products by the US government."

Sales to the US military: Although Lattice's sales to the US military reportedly had diminished in recent years, the White House press release cited US government use of Lattice products as a reason for blocking the transaction. In addition to being concerned with potential disruption of the supply of items critical to the US government, CFIUS also is wary of foreign buyers gaining access to details regarding the operations and interests of the US military and other government agencies with national security responsibilities.

The implications extended far beyond Lattice. Integrity of the semiconductor industry: In recent years, the national security community has come to regard the semiconductor industry as particularly sensitive, in part due to concerns over the integrity of the domestic supply chain for computer chip technology. In addition to the Aixtron deal discussed above, other recent deals involving Chinese investment in semiconductor technology have been abandoned due to concerns raised during the CFIUS review process.

Chinese transactions receive extra scrutiny. All of the transactions that CFIUS has blocked have involved Chinese buyers. And quite a few other transactions were withdrawn or perhaps never even submitted to CFIUS because of concerns that a Chinese buyer would make the transaction too difficult to get approved. In fact, in January 2017 (soon after Lattice and Canyon Bridge submitted their draft filing in December 2016), the President's Council of Advisors on Science & Technology issued a report identifying Chinese acquisitions in the semiconductor space to be a national security concern.

What matters for investors: The blocked acquisition transformed Lattice from an obscure chipmaker into a symbol of U.S.-China technology competition. The episode foreshadowed the CHIPS Act, export controls, and the broader decoupling of American and Chinese semiconductor supply chains. It also left Lattice's management scrambling—they had spent over a year pursuing this deal, and now they needed a new strategy.

VIII. The Jim Anderson Transformation Era (2018-2024)

The failure of the Canyon Bridge deal left Lattice rudderless. The company needed new leadership—someone who could articulate a clear vision and execute it. They found that leader in an unexpected place: the executive suite of one of their largest competitors.

Lattice Semiconductor Corporation announced the appointment of Jim Anderson as the Company's President and Chief Executive Officer, and to the Company's Board of Directors, effective September 4, 2018. Mr. Anderson brings broad technology industry experience and a proven track record of leading and transforming businesses to drive sustained growth and profitability. Mr. Anderson joins Lattice from Advanced Micro Devices (AMD) where he served as the General Manager and Senior Vice President of the Computing and Graphics Business Group.

The choice was inspired. In his role leading AMD's Computing and Graphics business group since 2015, Anderson drove a strategic and operational transformation that brought disruptive new products to the market and delivered market-leading revenue growth and significant profitability expansion for AMD.

The transformation he drove of AMD's Computing and Graphics business over the past few years is just a recent example of his long track record of creating significant shareholder value.

Jim holds an MBA and Master of Science in electrical engineering and computer science from the Massachusetts Institute of Technology, a Master of Science in electrical engineering from Purdue University, and a Bachelor of Science in electrical engineering from the University of Minnesota. He holds four patents for innovations in computer architecture.

Anderson's background was ideal: technical depth combined with business acumen, and a proven track record of turning around struggling semiconductor businesses.

He joined Lattice in September 2018 and focused the company on its mission as the leader in low power programmable solutions. Since then, the company accelerated its cadence of innovative product introductions and achieved record profitability.

Over those three years at Lattice, Jim has initiated a cultural shift that is playing out in the company roadmaps – new products, a more agile approach, and a need to focus on enabling machine learning at every part of its product stack.

The transformation Anderson drove was multifaceted. First and most importantly, he brought focus. Whereas the company was previously spreading itself thin across multiple businesses—including USB-C and HDMI—under Anderson, Lattice became laser-focused on small, low-power FPGAs. This focus meant putting R&D and the full weight of the company toward growth areas like AI, 5G, edge computing, datacenter, and security.

The management transformation didn't stop there though—Anderson rebuilt Lattice Semiconductor's leadership team with other proven industry experts in the FPGA realm. I believe Anderson is also responsible for an overhaul of the company's culture, with a renewed focus on speed, accountability, and metric-driven performance. What I am hearing from Lattice Semiconductor customers is that he brought new operational discipline throughout the company, not only driving new products, but also delivering profitability and cash flow.

The results were dramatic. Lattice turnaround: Anderson is credited with achieving a turnaround in his time at Lattice Semiconductor, with the company's stock price rising in value ten-fold since his September 2018 appointment.

The company's Q2 2019 financials showed a record non-GAAP operating profit of 24%, and revenue grew 4.3% sequentially from the first quarter of the year.

Anderson also made investor and financial analyst engagement a priority, contributing to an impressive expansion in market capitalization. The stock price rose from $7.55 in August 2018 to $19 by August 2019—a more than doubling in just one year.

Silicon is now bundled with software, IP, reference designs, hardware, and design partners, an approach that I believe will allow its customers to better leverage its FPGAs in next-generation applications such as AI. Some chip companies fire chips over the wall and hope their ecosystem embraces. Lattice Semiconductor is removing this "hope and pray" strategy by creating a full solution with accompanying hardware and software. It takes more resources to create a solution, but if you realign your resources around fewer, more profitable lines, overall costs don't increase.

What matters for investors: The Anderson era demonstrated the power of focused leadership. A CEO with the right vision, technical credibility, and execution discipline can transform a struggling company. Anderson's tenure—from September 2018 to June 2024—represents the most successful period in Lattice's history.

IX. The Nexus and Avant Platforms: Product Strategy That Worked (2019-Present)

Anderson's strategic focus found its expression in two transformative product platforms: Nexus and Avant.

Lattice's original Nexus platform, introduced in 2019, was based on Samsung's 28nm FD-SOI process.

The Nexus platform represented a fundamental rethinking of FPGA architecture. The Nexus platform, launched in December 2019, establishes the foundation for Lattice's low-power FPGA lineup using 28 nm FD-SOI technology, which delivers up to 75% lower power consumption and 100x reduced soft error rates compared to traditional bulk CMOS processes.

This wasn't merely incremental improvement—it was a step-function advance that gave Lattice's customers capabilities they couldn't get anywhere else. The Nexus platform enabled the rapid development of multiple device families: CrossLink-NX for video applications, Certus-NX for general-purpose applications, Mach-NX for system management, and more.

Lattice Semiconductor has been building out its collection of low-power programmable Lattice Nexus FPGAs since Q4 of 2019, when the company released its first Nexus CrossLink-NX FPGAs for enhanced embedded vision uses. Since that time Lattice has released four more Nexus FPGA models through Q2 of 2022.

Then came Avant, an even more ambitious platform. Lattice Semiconductor is moving upscale with its new mid-range Avant FPGA platform. After spending the last several years taking low-end market share from its bigger FPGA competitors, essentially while they weren't looking, Lattice has decided that a similar opportunity awaits in mid-range programmable-logic parts.

Its higher-end Avant platform, announced in 2022, is also based on TSMC's 16nm FinFET process.

"With Lattice Avant, we extend our low power leadership position in the FPGA industry and are poised to continue our rapid pace of innovation, while also doubling the addressable market for our product portfolio," said Jim Anderson, President and CEO, Lattice Semiconductor.

Meanwhile, system designers can welcome a new player in the mid-range market, which Lattice is defining as FPGAs with as many as 100K to 500K logic elements. According to Lattice, programmable-logic devices based on the mid-range Avant FPGA platform will compete directly against Intel Arria and AMD/Xilinx Kintex mid-range FPGAs. Understand that Lattice plans to use its new Avant platform, which is based on TSMC's 16nm FinFET process technology, to generate several mid-range FPGA families.

Lattice Avant offers best-in-class power efficiency, advanced connectivity, and optimized compute for customer applications across the Communications, Computing, Industrial, and Automotive markets. Compared to competing platforms, Lattice Avant helps customers gain a performance edge in their designs with up to 2.5x lower power, 2x faster throughput with 25 Gbps SERDES, 6x smaller package size, hardened support for PCIe® Gen 4, and high-speed memory interface support including LPDDR4 and DDR5.

The Avant platform significantly expanded Lattice's total addressable market to $10 billion. While Lattice had historically focused on small-scale FPGAs, with Avant it could now target high-growth areas such as edge AI, robotics, data centers, and 5G infrastructure.

The financial results followed. The company reported record full year 2022 revenue with 28% growth, and continued strong performance through 2023. Lattice achieved record full year 2023 revenue of $737 million, up 12% year over year.

Sherri Luther, CFO, said, "Q1 2023 represented our twelfth consecutive quarter of sequential growth, with revenue increasing 5% compared to Q4 2022. We achieved record operating profit of 32% on a GAAP basis and 41% on a non-GAAP basis, and expanded gross margin by 290 basis points on a GAAP basis and 260 basis points on a non-GAAP basis compared to Q1 2022. We also completed the tenth consecutive quarter of our share repurchase program." Record Revenue: Revenue increased 22% in Q1 2023 compared to Q1 2022 and 5% compared to Q4 2022, which represented the twelfth consecutive quarter of sequential growth.

Beyond hardware platforms, Lattice invested heavily in software and solution stacks. This strategy is what led to the development of a robust portfolio of application-specific solution stacks, which today comprises of Lattice sensAI™, Lattice mVision™, Lattice Sentry™, Lattice ORAN™, and Lattice Automate™. Each of these solution stacks combines hardware, software, and IP tools tailored to the needs of specific applications, from Edge AI, embedded vision, security, factory automation, and communications infrastructure, respectively. With these complete solutions, Lattice enables its customers to more easily evaluate, develop, and deploy FPGA-based systems and applications so they can get to market more quickly.

The Lattice mVision™ solutions stack includes the modular hardware development boards, design software, embedded vision IP portfolio, and reference designs and demos needed to quickly and easily develop low power embedded vision systems. The complete solutions stack includes the modular hardware development boards, design software, embedded vision IP portfolio, and reference designs and demos needed to implement sensor bridging, sensor aggregation, and image processing applications. The Lattice mVision solutions stack accelerates and simplifies the implementation of embedded vision systems such as machine vision, ADAS, drones and AR/VR for the industrial, automotive, consumer, smart home, and medical markets.

Most recently, at Lattice Developers Conference 2024, Lattice Semiconductor expanded its edge to cloud FPGA innovation leadership with the launch of exciting new hardware and software solutions. The new Lattice Nexus™ 2 next-gen small FPGA platform and the first device family based on the platform, Lattice Certus™-N2 general purpose FPGAs, offer advanced connectivity, optimized power and performance, and class-leading security. Lattice also announced new mid-range FPGA device capacity options – Lattice Avant™ 30 and Avant™ 50 – and new versions of Lattice design software tools and application-specific solution stacks to help accelerate customer time-to-market.

Although the Nexus 2 platform employs a fairly advanced 16nm process node, FPGAs based on Lattice's Nexus 2 platform will have fewer than 200K logic cells, which is relatively small these days. Instead of going for all-out performance and large programmable logic fabrics, Lattice is using the benefits of TSMC's 16nm FinFET process node to emphasize specific capabilities such as faster boot time and lower operating power.

What matters for investors: The Nexus and Avant platforms demonstrate Lattice's ability to innovate within its focused strategy. Rather than trying to compete with AMD/Xilinx and Intel/Altera at the high end, Lattice has carved out leadership in low-power and mid-range FPGAs—a strategy that delivers superior margins and defensible market position.

X. CEO Transition and Current Challenges (2024-Present)

Just as Lattice seemed to have found its footing, a shock hit the company. At the same time programmable chip company announced the departure of Anderson and the appointment of Esam Elashmawi, chief marketing and strategy officer, as interim CEO effective immediately.

Lattice Semiconductor, a leading FPGA chip manufacturer, has announced the sudden departure of its CEO Jim Anderson, who has jumped ship to join rival chipmaker Coherent. Following the news, Lattice's stock price fell nearly 11%, while Coherent's share prices rose. According to an official statement released on June 3, Lattice Semiconductor unexpectedly announced the resignation of its CEO Anderson, who has served for six years, effective immediately. The statement cited Anderson's "pursuit of an opportunity at another company" as the reason for his departure. Chief Marketing and Strategy Officer Esam Elashmawi has been appointed as interim CEO, effective immediately.

Jim Anderson was appointed Chief Executive Officer of Coherent Corp. and a member of the Board of Directors on June 3, 2024. He brings over 25 years of experience in the technology and semiconductor industries, with a strong track record in innovation-driven businesses. Prior to joining Coherent, Mr. Anderson served as President and Chief Executive Officer of Lattice Semiconductor Corporation from September 2018 to 2024.

Shares of Lattice Semiconductor (LSCC) closed 15% lower on Monday after CEO James Anderson left to join Coherent (COHR), which saw its shares spike 22% on the news. KeyBanc equity research analyst John Vinh tells Yahoo Finance's Julie Hyman that Anderson gets much credit for helping turn Lattice around. Vinh says the departure makes him "a little bit concerned" given Lattice's "very bright prospects ahead of themselves."

The market's reaction—a 15% drop in Lattice stock and a 22% rise in Coherent stock—vividly illustrated how closely investors associated Anderson with Lattice's turnaround.

Following a comprehensive search, the board found a new leader. Lattice Semiconductor Corporation today announced the appointment of Dr. Ford Tamer as Chief Executive Officer and to the Company's Board of Directors, effective September 2024. Tamer brings to his role extensive industry experience and leadership spanning semiconductors, networking, and enterprise software. In his most recent operating role, Tamer served as President and CEO of Inphi for over nine years, where he led the company to become the market leader for electro-optics solutions for cloud and telecom operators. Prior to Inphi, he was CEO of Telegent Systems, Senior Vice President and General Manager of Broadcom's Infrastructure Networking Group, co-founder and CEO of Agere Inc., amongst other roles earlier in his career. Most recently, he served as a Senior Operating Partner of Francisco Partners.

Tamer holds an M.S. and Ph.D. in Engineering from MIT. He currently serves on the Board of Directors of Teradyne Inc. and Groq, Inc. and, until recently, served on the Board of Marvell Technologies, Inc.

The leadership transition coincided with challenging market conditions. Lattice Semiconductor Full Year 2024 Revenue: US$509.4m (down 31% from FY 2023).

This restructuring involved a 14% reduction in the workforce and a streamlined operating budget aimed at promoting annual earnings growth by 2025. Lattice is concentrating on aligning resources with current market conditions while maintaining its long-term product roadmap.

Despite the cyclical downturn, the new product platforms continued to gain traction. Double-Digit New Product Revenue Growth: Revenue of our new products, including Nexus and Avant, grew double-digits in 2024 compared to 2023, with a record total number of design wins.

Looking ahead, Lattice remains committed to its goal of achieving 15% to 20% annual revenue growth over the long term.

As of late 2025, the company shows signs of stabilization. Lattice Semiconductor met Q3 2025 expectations with EPS of $0.28 (up 17% YoY) and revenue of $133.3 million (up 4.9% YoY), with strong performance in AI and post-quantum cryptography applications. The company reported solid financial metrics including a 69.5% non-GAAP gross margin (up 50 basis points YoY), $47.1 million operating cash flow, and $34 million free cash flow. For Q4 2025, Lattice projects revenue between $138-148 million (22% YoY growth), with communications and compute sectors expected to grow 20-40%.

CEO Ford Tamer emphasized the company's focus on AI-driven growth, stating 'We are seeing the AI infrastructure tsunami' and projecting data center revenue to reach 60% of total revenue by 2026.

What matters for investors: The CEO transition represents a critical test of Lattice's institutional strength. Can the company sustain its transformation momentum without the architect of that transformation? Early signs are encouraging—the new product platforms continue to gain traction, and gross margins remain strong—but the next 12-24 months will be crucial.

XI. Playbook: Business & Investing Lessons

Lattice's four-decade journey offers several enduring lessons for business leaders and investors:

1. Focus Beats Diversification

The contrast between Lattice's "lost decade" (2000-2010), when the company chased multiple opportunities without clear focus, and the Anderson era (2018-2024), when it concentrated exclusively on low-power FPGAs, could not be starker. When Anderson arrived, he shed non-core businesses (including USB-C and HDMI products) and aligned all resources toward a single strategic objective. The result: record profitability and tenfold stock appreciation.

2. The Fabless Model as Competitive Advantage

Lattice Semiconductor operates through a fabless business model, focusing on design and marketing while outsourcing manufacturing to third-party foundries. This approach allows the company to maintain a lean operational structure and quickly adapt to changing market demands.

Lattice pioneered this approach out of necessity during its post-bankruptcy period. What began as a survival strategy became a structural advantage: lower fixed costs, faster adaptation to market changes, and access to leading-edge manufacturing capabilities without the capital requirements of operating fabs.

3. Surviving Bankruptcy to Billion-Dollar Valuation

Lattice's journey from Chapter 11 in 1987 to a $10 billion market cap today demonstrates the power of persistence and reinvention. The bankruptcy forced difficult decisions—cutting product lines, replacing founders, embracing a new business model—that ultimately strengthened the company.

4. Software + Hardware Integration

Lattice's solution stacks (sensAI, mVision, Automate, Sentry) represent a crucial evolution: from selling chips to selling complete solutions. This approach increases switching costs for customers, improves margins, and differentiates Lattice from competitors selling commoditized hardware.

5. Strategic Niche Selection

Rather than competing across all FPGA segments, Lattice chose to be the best at one thing: low-power programmable logic. This focus enabled the company to out-innovate larger competitors in its niche while avoiding head-to-head battles it couldn't win.

6. The Importance of Timing

Lattice's transformation coincided with the emergence of edge AI, 5G infrastructure, and industrial automation—all markets that demand exactly what Lattice does best: low-power, flexible, programmable silicon. Sometimes strategy is about positioning yourself where the market is going, not where it is today.

XII. Porter's Five Forces Analysis

1. Threat of New Entrants: LOW-MEDIUM

FPGAs require substantial R&D investment, specialized talent, and years of customer relationship development. The barriers to entry are formidable. However, Chinese national champions like GOWIN Semiconductor are investing heavily to develop domestic alternatives, particularly as export controls limit access to Western technology. Chinese suppliers such as GOWIN and Pango sought to close the gap, yet hurdles in design tools, IP, and advanced process access limited immediate substitution.

2. Bargaining Power of Suppliers: MEDIUM-HIGH

Lattice depends on foundry partners for manufacturing. The company partners with leading foundries to fabricate its semiconductor devices. The Nexus 2 and Avant platforms rely on TSMC's 16nm process, creating concentration risk. During semiconductor shortages, fabless companies faced significant capacity constraints.

3. Bargaining Power of Buyers: MEDIUM

Lattice serves diverse customers across communications, computing, industrial, automotive, and consumer markets. Large OEMs have negotiating leverage, but high switching costs (due to design-in cycles that can span years) protect established relationships. The majority of sales are derived from customers in Asia.

4. Threat of Substitutes: MEDIUM

ASICs offer higher performance for high-volume, fixed-function applications. GPUs dominate for certain AI workloads. MCUs compete at the low end. However, Advanced FPGA fabrication is clustered at TSMC and Samsung, and FPGAs' unique ability to be reprogrammed in the field makes them ideal for applications requiring flexibility, performance, and adaptability.

5. Competitive Rivalry: HIGH

The field programmable gate array market remained concentrated, with AMD-Xilinx and Intel-Altera still generating the majority of revenue in 2024.

International Data Corp. estimates that AMD has a 55% share of the FPGA market thanks to the Xilinx deal with Altera accounts for over 30% of sales.

Lattice Semiconductor gained traction with low-power Nexus and Avant platforms, securing record design wins in generative AI and robotics.

Lattice Semiconductor focuses on low-power, edge-optimized FPGAs targeting automotive, industrial, and security applications.

XIII. Hamilton's 7 Powers Analysis

1. Scale Economies: WEAK

Lattice is significantly smaller than AMD (Xilinx) and Intel (Altera). However, the fabless model reduces fixed cost disadvantages. Lattice doesn't need massive fabs to compete; it needs excellent designs and strong customer relationships.

2. Network Effects: WEAK

Limited network effects exist in semiconductor hardware. Some developer ecosystem effects emerge through software tools and solution stacks, but these don't create winner-take-all dynamics.

3. Counter-Positioning: STRONG ⭐

This is Lattice's key power source. The company has adopted a business model that competitors can't easily match. AMD and Intel, with their focus on high-end FPGAs, would cannibalize their existing businesses by aggressively pursuing the low-power segment. Lattice's laser focus on small, low-power FPGAs creates a positioning advantage that larger competitors can't easily replicate.

4. Switching Costs: MEDIUM-STRONG

Design-in cycles for FPGAs typically span 18-24 months, creating significant switching costs once a customer commits to Lattice's platform. Software tool familiarity and IP investment further increase lock-in.

5. Branding: WEAK-MEDIUM

Lattice has built strong brand recognition within its niche as "the low power programmable leader," but brand power is limited in B2B semiconductor markets compared to consumer markets.

6. Cornered Resource: WEAK

Lattice doesn't possess unique, non-replicable resources. Its advantages stem from strategy and execution rather than proprietary assets.

7. Process Power: MEDIUM

Lattice's development methodology for low-power FPGAs and its solution stack approach represent accumulated organizational knowledge that competitors would take years to replicate.

XIV. Key Performance Indicators for Investors

For investors tracking Lattice Semiconductor, three metrics matter most:

1. New Product Revenue Growth Rate

This KPI measures whether Lattice's strategic investments in new platforms (Nexus, Avant) are translating into customer adoption. Revenue of new products, including Nexus and Avant, grew double-digits in 2024 compared to 2023, with a record total number of design wins. Sustained double-digit growth in new product revenue signals that the product strategy is working and that future revenue growth is secured.

2. Non-GAAP Gross Margin

Gross margin is the clearest indicator of Lattice's pricing power and competitive position. Lattice's gross margins are among the highest in the semiconductor sector, surpassing competitors like Altera and Xilinx, and approaching those of industry leaders such as Nvidia and Analog Devices. Margins in the 68-70% range indicate healthy pricing power; significant compression would signal competitive pressure.

3. Design Win Momentum

Design wins are leading indicators of future revenue, given the 18-24 month design-in cycles. CEO Ford Tamer pointed to a record level of design wins, concentrated around generative AI, robotics, ADAS, post-quantum crypto, and far-edge AI. Strong design win activity suggests the revenue pipeline is healthy; weakness here would be a concerning signal.

XV. Bull and Bear Cases

The Bull Case

Lattice is uniquely positioned at the intersection of several mega-trends: edge AI, 5G infrastructure, industrial automation, and automotive electronics. The company's focus on low-power FPGAs aligns perfectly with markets demanding flexible, energy-efficient compute at the edge.

The competitive landscape has shifted favorably. Altera Corporation announced that Silver Lake has completed its acquisition of a 51% stake in the company from Intel Corporation. Completion of the transaction establishes Altera as the world's largest independent, pure-play FPGA solutions provider. This transition may create customer uncertainty and sales execution challenges for Altera, potentially benefiting Lattice.

The continued ramp-up of the Avant and Nexus platforms, along with the growing adoption of edge AI solutions, will be key drivers. The shift toward mid-range FPGAs and increasing attach rates for software solutions will also play a crucial role in boosting margins.

Industry analysts remain optimistic: Benchmark raised its price target on Lattice Semiconductor to $82.00 from $75.00, while maintaining a Buy rating on the semiconductor company. Currently trading at $67.03, LSCC shares have delivered impressive returns of 40.34% over the past six months and 28.54% year-to-date. Analysts remain bullish with a strong consensus recommendation of 1.38 and price targets ranging from $60 to $85. The research firm cited Lattice's "solid quarter of execution" with results and guidance largely meeting expectations. Benchmark expressed increasing confidence in the company's growth trajectory as design wins ramp up and momentum accelerates into 2026.

The Bear Case

Lattice remains a niche player in a market dominated by much larger competitors. AMD/Xilinx has more than 55% market share; if AMD decided to aggressively pursue the low-power segment, Lattice's margins and market position could erode quickly.

The company is exposed to cyclical semiconductor demand. Lattice faces challenges from its mid-tier scale and exposure to semiconductor cyclicality, exemplified by a 35% year-over-year revenue drop to $92.8 million in Q1 2024 amid customer inventory adjustments and broader industry softening. This vulnerability stems from limited diversification beyond programmable logic—comprising over 90% of revenue—and hampers bargaining power in pricing and supplier negotiations relative to larger integrated device manufacturers.

Geopolitical risks compound this, with heavy reliance on foundries in Asia (including China-dependent nodes), raising supply disruption probabilities amid U.S.-China trade frictions.

The CEO transition creates execution risk. Jim Anderson was synonymous with Lattice's turnaround; whether Ford Tamer can sustain the momentum remains to be proven.

Regulatory and Legal Considerations

Lattice's history with CFIUS review, the blocked Canyon Bridge acquisition, and its 2004 export control settlement highlight the company's exposure to geopolitical and regulatory risks. As U.S.-China technology tensions intensify, semiconductor companies face increasing compliance burdens and potential market access restrictions.

XVI. Conclusion: The Last Independent FPGA Standing

Lattice Semiconductor's four-decade journey reads like a business school case study: near-death experience, reinvention, strategic missteps, transformation, and now—renewed uncertainty as a new CEO takes the helm amid cyclical headwinds.

The company that Rahul Sud and Ray Capece founded in 1983 with dreams of Portland becoming a tech hub has survived bankruptcy, the dot-com bust, the financial crisis, a blocked Chinese acquisition, and the departure of its transformational CEO. Along the way, it pioneered the fabless semiconductor model, built leadership in low-power FPGAs, and became a symbol of the strategic importance of semiconductor supply chains.

After AMD completed the acquisition of Xilinx in February 2022, Lattice Semiconductor became the last fully independent major manufacturer of FPGAs. That distinction carries both opportunity and burden. Lattice can position itself as the independent alternative to vertically integrated giants; but it must also navigate an industry increasingly shaped by geopolitics, capital intensity, and winner-take-all dynamics.

The key questions facing Lattice today are execution questions: Can the Avant platform successfully capture mid-range market share from established competitors? Will the Nexus 2 platform maintain leadership in small FPGAs? Can Ford Tamer build on Jim Anderson's foundation while navigating near-term headwinds?

The company's gross margins remain exceptional. Its product roadmap is executing. Design wins are at record levels. If management can sustain this trajectory through the current cyclical trough, Lattice should emerge stronger—leaner, more focused, and positioned for the next wave of growth in edge AI, industrial automation, and beyond.

But semiconductors remain a brutally competitive industry where technology leadership is fleeting, customer loyalty is conditional, and a single product miss can undo years of progress. Lattice has proven it can survive almost anything. Whether it can thrive in the next chapter of semiconductor competition—that remains to be written.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube