Lincoln Electric Holdings: The $200 Spark That Forged America's Manufacturing Spirit

I. Introduction & Episode Roadmap

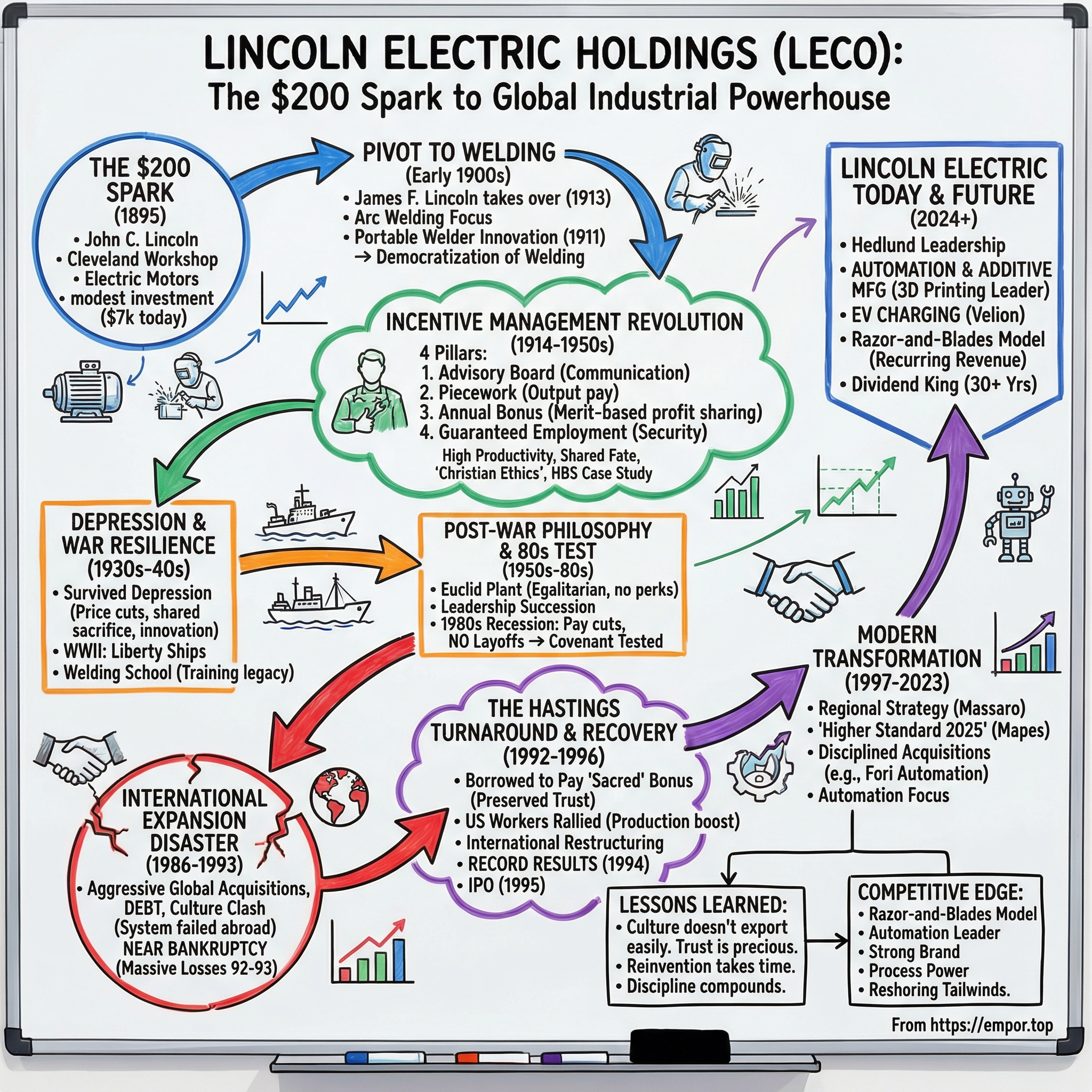

On a December day in 1895, in a modest Cleveland workshop, a young inventor named John C. Lincoln scraped together $200—equivalent to perhaps $7,000 today—and incorporated a company to manufacture electric motors of his own design. He could not have imagined that this modest sum would become the seed capital for one of the most extraordinary 130-year runs in American industrial history.

Lincoln Electric Holdings, Inc. is an American multinational and global manufacturer of welding products, arc welding equipment, welding accessories, plasma and oxy-fuel cutting equipment and robotic welding systems headquartered in Euclid, Ohio. Today, it has a network of distributors and sales offices covering more than 160 countries and 42 manufacturing locations in North America, Europe, the Middle East, Asia and Latin America.

The numbers are impressive: the company's revenue in the last twelve months reached $4.18 billion, up 3.24% year-over-year, following annual revenue of $4.01 billion in 2024. Its current market cap hovers around $13 billion with 55 million shares outstanding. The company employs approximately 12,000 people globally, and its products touch virtually every corner of modern manufacturing—from the pipelines carrying natural gas to your home, to the ships crossing the Pacific, to the automotive factories reshaping mobility in the electric age.

But the numbers only scratch the surface of what makes Lincoln Electric truly remarkable. This is a company that invented one of the most studied management systems in business school history—the Lincoln Incentive Management System—and nearly destroyed itself trying to export it overseas. It's a company that survived the Great Depression by dramatically cutting prices while doubling worker pay. It's a company that borrowed money to pay employee bonuses during a near-bankruptcy crisis in 1992, a decision that would either save the company or seal its fate.

The central question for this deep dive: How did a $200 startup survive 130 years, create the most famous employee incentive system in American business history, nearly go bankrupt in the 1990s, and reinvent itself as an automation and 3D printing leader?

The themes that emerge are universal to any student of business history: culture as competitive advantage, the limits of system transplantation across borders and cultures, disciplined capital allocation through economic cycles, and the perpetual challenge of industrial reinvention. Along the way, we'll examine whether Lincoln Electric's legendary management approach still gives it an edge—and what its transformation into automation and additive manufacturing tells us about the future of American industry.

II. The Lincoln Brothers & Founding Vision (1895–1914)

John C. Lincoln: The Inventor-Founder

The story begins with John Cromwell Lincoln, born in 1866 in Painesville, Ohio, to a minister who would later name another son James Finney Lincoln—the "Finney" a tribute to Charles Grandison Finney, a famous nineteenth-century revivalist and president of Oberlin College. This religious heritage would prove more consequential than anyone could have predicted, embedding itself into the philosophical DNA of a company that would become one of America's most unusual industrial experiments.

John C. Lincoln was an engineer by training and an inventor by temperament. By the 1890s, electricity was still a novelty rapidly becoming a necessity, and the young Lincoln saw opportunity in the nascent market for electric motors. The company was founded in 1895 by John C. Lincoln with an investment of $200 to make electric motors he had designed.

That initial $200 purchased basic equipment and materials for a one-man operation. Lincoln Electric was, at its founding, nothing more than a small workshop producing direct current motors for industrial applications. The business grew slowly but steadily. John C. Lincoln remained active in the company as its president until 1928 and as chairman of the board through the following years. But even as he led the company through its first three decades, John's attention was increasingly drawn elsewhere—to real estate, philanthropy, and the economic theories of Henry George.

John C. Lincoln's intellectual passions would leave their own mark on American life. The Lincoln Institute of Land Policy was established by Lincoln Electric's founder, John C. Lincoln, in 1946, based on his admiration for the work of Henry George. Today, that institute remains one of the world's leading research centers on land use and taxation policy. But back in the early 1900s, John's divided attention meant the company needed operational leadership—and that need would be filled by his younger brother James.

The Pivot to Welding: A Technology Bet

The transformation from a small motor manufacturer to a welding powerhouse began with a technological insight. Arc welding—using electricity to generate heat intense enough to fuse metals together—was emerging as a revolutionary technique that would eventually displace riveting and other mechanical joining methods in countless applications.

The Lincoln brothers recognized the opportunity early. In 1909, they began experimenting with welding equipment. By 1911, they had achieved a breakthrough that would define the company's future: they introduced the world's first variable voltage, single-operator portable arc welder. This innovation enabled more stable and controllable welding arcs compared to the constant-current machines of the era.

The significance of this innovation cannot be overstated. Prior arc welding equipment required multiple operators and produced inconsistent results. Lincoln's variable voltage design meant a single skilled worker could produce high-quality welds reliably and repeatedly. It was a democratization of welding technology—and it established the template for Lincoln Electric's approach for the next century: engineer solutions that increase worker productivity.

James F. Lincoln Takes the Reins

In 1913, a pivotal transition occurred: John C. Lincoln turned over management of the company to his brother James F. Lincoln. The change would prove transformative in ways that extended far beyond simple succession planning.

Under James Lincoln, the company shifted its focus to standardized, rather than custom designed products and focused on innovation in arc welding. Where John had been the inventor-entrepreneur, James was the philosopher-manager. His educational background provided an unusual foundation for industrial leadership. He traced his elder brother's footsteps to Ohio State University to study electrical engineering and became one of the school's outstanding fullbacks, leading the football team to an undefeated season in 1906. In 1907, however, typhoid fever so debilitated him that he was compelled to drop out of school without completing his degree. Rather than finish later, he elected to go to work for his older brother.

This early adversity—the derailed education, the physical recovery—seemed to shape James Lincoln's worldview. He became intensely focused on questions of human motivation, productivity, and fairness. He brought to the company not just operational expertise but a philosophical framework that would evolve into one of the most distinctive management systems in American business history.

The brothers' different strengths proved complementary. John continued to provide technical guidance and served as chairman, while James ran day-to-day operations and began the experiments in labor relations that would make Lincoln Electric famous. Together, they had created something unusual: a company built on technological innovation that would soon become equally known for its innovations in human organization.

As World War I approached, Lincoln Electric was positioned at the intersection of two powerful trends: the rising importance of welding technology in modern manufacturing and the emerging questions about how to organize industrial labor in an age of mass production. James Lincoln would spend the next five decades answering those questions in ways that continue to fascinate management scholars today.

III. The Lincoln Incentive Management System: A Management Revolution (1914–1950s)

James Lincoln's Management Philosophy

To understand Lincoln Electric, you must understand James F. Lincoln—a man who defies easy categorization. Although Lincoln Electric Co. was founded by John C. Lincoln in 1895, it is his younger brother, James, who is most identified with the firm and its unique management system.

James Lincoln was a rock-ribbed conservative and a vocal advocate of free markets who nonetheless attempted to create a classless society within his company. He believed that the primary task of business leaders was to create conditions under which people's talents could be developed—and that the success with which leaders used that talent would determine the progress of industry and society. This was not empty corporate rhetoric. Lincoln published extensively on management philosophy and became a sought-after speaker on industrial relations.

Lincoln Electric is perhaps best known for its unique strategy for handling employee relations, known as the Lincoln Incentive Management System. This program evolved during the first half of the twentieth century, and has remained virtually intact during the second half of the century. It focuses on six themes that are interwoven throughout the company's history: people as assets, Christian ethics, principles, simplicity, competition, and customer satisfaction.

Lincoln's middle name—Finney—referenced Charles Grandison Finney, the famous revivalist. This Congregationalist upbringing undoubtedly contributed one of the fundamental tenets of the Incentive Management System: Christian ethics. But James Lincoln was no naïve idealist. His system was designed to align worker interests with company interests through mechanisms that were simultaneously principled and practical.

The Four Pillars of Incentive Management

1. The Advisory Board (Communication & Participation)

The first pillar was established early in James Lincoln's tenure. He instituted an employee advisory board that helped manage relations between workers and management, and a piecework pay scale that enabled workers to earn higher wages based on performance. The advisory board was comprised of elected representatives from each department and met for bi-weekly meetings. It is a practice the company continues to this day.

The Advisory Board was—and remains—a remarkable institution. It is empowered to make suggestions, lodge complaints, criticize management, propose new ways to improve productivity and product quality, and raise any other concerns on workers' minds. The board meets with the company's top management every two weeks, and they jointly make almost every major decision.

This is not a suggestion box or a grievance committee in disguise. Lincoln's domestic U.S. workers have agreed, through the Advisory Board process, to create new jobs abroad instead of at home, reasoning that foreign expansion was necessary for the long-term viability of their enterprise. That unprecedented decision represents a degree of employee cooperation with management found in virtually no other U.S. enterprise.

2. Piecework Compensation

The second pillar struck at the heart of industrial wage systems. Rather than paying hourly rates or salaries, Lincoln developed an elaborate piecework system tied to individual output. About a third of Lincoln Electric's employees are factory workers. They earn a base wage comparable to that of unionized workers in their region, but with no upper limit on additional pay, which is based on the number of "pieces" they complete.

This system gives employees an incentive to work themselves out of their jobs by finding ways to automate their tasks. When they do so, they are rewarded and promoted to jobs requiring higher human skills—rather than laid off. The psychological dynamic is powerful: every process improvement benefits the worker who discovers it.

3. The Merit-Based Annual Bonus

James Lincoln was also influential in developing a worker incentive plan in which the company offered its employees free life insurance and paid vacations; however, the plan's major element was an incentive bonus instituted in 1934.

The bonus became the system's centerpiece. Each year, after dividends are paid to shareholders, a substantial portion of profits is distributed to employees based on their individual merit ratings. The dollar amounts distributed as bonuses have varied each year since 1934, but since 1955, the rate has averaged approximately 77% of base pay.

To put that in perspective: Lincoln's U.S. workers have consistently earned two to three times the average income of people in the U.S., in good times and bad. Hard workers who don't mind overtime have been known in good years to gross more than $80,000—in wages that were exceptional decades ago and remain impressive today.

4. Guaranteed Employment

The final pillar addressed the fear that undermines virtually every productivity improvement system: the worry that working harder or smarter will simply eliminate your own job.

Lincoln's solution was radical: guaranteed employment. The economic crisis of the early 1980s put the manufacturer's no-layoff policy to the test. About 15 percent of Lincoln's employees were reassigned; production workers did plant maintenance, took clerical assignments, and even went on the road as salesmen. Average pay was halved, from $44,000 to $22,000. But no one was laid off.

Lest employees worry about working themselves right out of a job, the company has maintained this long-standing policy. For more than 50 years, the combination of pay by output, bonus, and job security worked like a charm.

Progressive Policies Ahead of Their Time

The meetings of the Advisory Board yielded progressive workplace policies decades before they became standard practice: group life insurance (1915), paid vacations (1923), employee stock ownership (1925), annual cash bonuses (1934), annuities for retired employees (1936), and guaranteed employment formalized in 1958.

Lincoln's incentive management system became so distinctive that several business cases were written about it by Harvard Business School, making it one of the most studied management innovations in American industrial history.

The System's Productivity Results

The results were extraordinary. Lincoln's employees produce an average of two to three times what their counterparts produce at competitive plants, including those in Japan. While the average Lincoln Electric worker's pay more than doubled during the decade of the Great Depression, electrodes that sold for $0.16 per pound in 1929 were selling for less than $0.06 per pound by 1942.

Unlike many companies in other manufacturing sectors, Lincoln staved off foreign competitors by maintaining high productivity and quality while offering goods at low prices. Although material costs multiplied in the postwar era, James Lincoln set a goal of reducing costs by ten percent annually. With money-saving ideas from the employee suggestion plan, the company was able to hold prices at 1933 levels until runaway inflation in the 1970s compelled price hikes.

Lincoln is a low-cost provider, focusing intensely on manufacturing excellence. This dedication minimizes production costs. The strategic outcome was continuous price reduction, which allowed Lincoln to expand its market share (over 40% of the U.S. market) and forced major competitors like General Electric to exit the core welding products business.

The Myth vs. Reality

Myth: Lincoln Electric's system is about being nice to workers. Reality: The system is intensely demanding. Performance expectations are high, peer pressure is significant, and the merit-based bonus creates genuine competition among workers. The system works because it aligns incentives, not because it softens them.

Myth: The system could work anywhere with proper implementation. Reality: As Lincoln would learn painfully in the 1990s, the system depends on cultural factors—trust, individualism, performance orientation—that don't translate easily across borders.

Myth: The system eliminates labor-management conflict. Reality: The Advisory Board process can be contentious. Workers advocate forcefully for their interests. The difference is that conflict is channeled into productive dialogue rather than strikes or work-to-rule tactics.

For investors evaluating Lincoln Electric today, the relevant question is whether this cultural inheritance still provides competitive advantage. The answer appears to be yes—but with important caveats about geographic limitations that would become brutally apparent decades later.

IV. Depression, War & Post-War Dominance (1930s–1980s)

Surviving the Great Depression

When the Great Depression struck, most American manufacturers scrambled to cut costs, lay off workers, and survive. Lincoln Electric did something different.

During the Depression, Lincoln Electric unveiled a new coated electrode—still manufactured today as the Fleetweld 5P—that ensured the company's fiscal continuity during the economic downturn. Product innovation during the worst economic crisis in American history might seem counterintuitive, but it exemplified Lincoln's approach: use difficult times to strengthen competitive position rather than merely survive them.

The unique incentive system also allowed the company to stay competitive and stable during the Depression and after World War II. Workers accepted reduced hours rather than layoffs. The profit-sharing bonus adjusted automatically to economic conditions. And because workers had skin in the game, they contributed cost-saving ideas that helped the company maintain profitability even as revenue declined.

The contrast with other industrial companies was stark. While competitors struggled with labor unrest, Lincoln's workforce remained engaged and productive. The social compact between management and workers—built over two decades—proved remarkably resilient under economic stress.

World War II and Building America

World War II transformed American manufacturing, and Lincoln Electric was at the center of that transformation. The Lincoln Electric Welding School was set up in 1917 and has since instructed over 150,000 men and women in the various methods and techniques of safety and arc welding processes.

The company created new welding techniques that helped build 2,700 Liberty ships for the war effort. These mass-produced cargo ships were essential to supplying Allied forces across two oceans, and welding technology made their rapid construction possible. The traditional riveting methods were too slow for wartime demands; welded construction could be completed far more quickly.

The Welding School, which the U.S. Army had requested Lincoln establish in 1917 to train troops heading into World War I, expanded dramatically during World War II. Today, it remains the longest continuously operating welding school in the world—a direct link between Lincoln's founding era and its current efforts to address the skilled welder shortage that plagues modern manufacturing.

The Euclid Era: A Factory Built on Philosophy

The company expanded the factory in Euclid in 1968 and opened another in Mentor, Ohio in 1977. But the philosophical underpinning of Lincoln's facilities dated to 1951, when James Lincoln was able to incorporate his management theories into the design and construction of a new 30-acre plant in Euclid.

The building embodied Lincoln's beliefs about simplicity and egalitarianism. It did not include windows, carpeting, or elaborate executive quarters. All aspects of the company fostered a sense of belonging and unity, including the physical layout of the plant, which had an open floor plan where all materials needed were positioned at workstations, plus an employee cafeteria where executives ate lunch alongside factory workers. Executives didn't have elaborate offices—in fact, the office didn't even have carpet.

This was not mere symbolism. Lincoln believed that physical barriers between management and workers reinforced psychological barriers. By eliminating executive perks and status symbols, he reinforced the message that everyone's contribution mattered—and that everyone's rewards would be tied to collective success.

Leadership Succession: Irrgang to Willis

Upon James Lincoln's death in 1965, William Irrgang, who had started at the company on the assembly line, assumed the position of CEO and chairman. Like Lincoln, Irrgang believed in keeping the product line small and simplified.

Irrgang represented continuity with the founder's vision. He had risen through the ranks at Lincoln Electric, absorbing its culture and philosophy through decades of experience. Irrgang saw Lincoln Electric through a recession in the early 1980s during which the company guaranteed continuous employment for its workers, though they worked fewer hours and operations were reduced. Operations returned to normal in the mid-1980s and George Willis succeeded Irrgang as CEO and Chairman in 1986.

The 1980s Recession: Testing the No-Layoff Promise

The early 1980s recession provided the most severe test yet for Lincoln's management system. Lincoln Electric's revenues dropped 40 percent, from $450 million in 1981 to $220 million in 1982, as all of the company's traditional markets declined.

The company's response demonstrated the flexibility embedded in its system. No workers were laid off, but the pain was shared across the organization. George Willis' pay dropped 20 percent, and Donald Hastings' compensation was cut by over 11 percent. The fact that executive pay was cut alongside worker pay reinforced the social compact that made the system function.

The experience validated the no-layoff guarantee. Workers had taken the company's promises seriously, and management had honored them—not out of charity, but because the long-term value of a committed, highly skilled workforce exceeded the short-term savings from layoffs. When demand recovered, Lincoln Electric had its experienced workforce intact and ready to ramp up production.

Willis' innovation to Lincoln Electric was to ensure another recession would not severely damage the company by expanding globally. The company expanded to 22 plants in 15 countries, which increased sales dramatically.

This decision—to diversify geographically to reduce dependence on the cyclical U.S. market—seemed eminently sensible. But it would lead Lincoln Electric into the greatest crisis in its history.

V. The International Expansion Disaster (1986–1993): Lincoln's Near-Death Experience

The Ambition: Going Global

Lincoln was primarily a U.S. company until the mid-1980s, but recession at home and competition from abroad led executives to dream that the company could become a global power. Between 1986 and 1991, Lincoln took on unprecedented debt in order to finance foreign acquisitions, mostly in Europe.

The expansion was ambitious in scope. A total of 19 acquisitions from 1986 to 1991 helped boost annual sales by 87.3 percent, from $445.31 million to $833.89 million. In 1986, Lincoln acquired Cleveland's Airco Electrode plant from BOC Group. In 1987, Lincoln purchased an Australian electrode plant from France's Air Liquide. A 1988 joint venture with Norweld Holding A.A., a Norwegian company with $100 million in annual sales, quadrupled Lincoln's business in Northern Europe to $135 million annually. That same year saw the acquisition of two welding factories in Mexico and two more in Brazil.

Upon his 1992 retirement, Willis was praised for doubling Lincoln Electric's sales, expanding its international presence from four to 15 countries, and securing a spot for the company on the "Forbes 500."

The Fatal Assumption

The expansion rested on a crucial assumption: that Lincoln's legendary productivity and culture would transfer seamlessly to acquired operations abroad. Management believed that by implementing the incentive system, they could transform underperforming foreign plants into Lincoln-quality operations.

A number of factors doomed the venture: recession in Europe, unfamiliarity with Europe's labor culture, lack of international expertise at the top. But the root cause, Hastings admits, was overconfidence on the part of Lincoln's leaders in the company's manufacturing abilities and systems.

It rapidly acquired 17 plants across 15 countries but lacked international experience and did not successfully implement its proven compensation model abroad. The piecework system that motivated American workers proved incompatible with European labor laws and cultural expectations. In Germany, works councils and labor regulations made the Lincoln system essentially impossible to implement. In other countries, workers simply didn't respond to the incentive structure in the same way American workers did.

The Crisis Unfolds

The fast-paced expansion had increased long-term debt from $17.5 million in 1988 to $221.5 million in 1993. Unanticipated difficulties in transplanting the incentive system to operations in such countries as Brazil, Mexico, and Germany, coupled with a 40 percent drop in the European market, contributed to a $46 million loss in 1992.

Although orders in the United States were so high that Lincoln stayed open through its usual summer shutdown in 1993, the company still suffered its worst quarter ever. The company saw an overall loss of $38 million in 1993.

The situation was worse than the numbers suggested. The European welding market was severely oversupplied, and the companies Lincoln acquired were competing against each other. Germany's reunification and the Persian Gulf War created additional economic disruption. What had been planned as a gradual, profitable internationalization became a cascading crisis.

The Bonus Crisis: Threatening the Sacred Covenant

Less than half an hour after Donald Hastings became chairman and CEO of the Lincoln Electric Company in July 1992, he got the shocking news: losses from the company's European operations were so steep that Lincoln was at risk of defaulting on its loans and being unable to pay its employees their year-end bonus. Since the bonus was the foundation of the company's unusually successful manufacturing operations, Hastings knew that failure to pay it could lead to the company's unraveling.

At 5:01 p.m. on the last Friday of July 1992, I took over as chairman and CEO of the Lincoln Electric Company. I had worked at Lincoln for 38 years and had reached the pinnacle of my career. But Hastings' exhilaration lasted exactly 24 minutes—until he learned the full extent of the crisis.

This was an existential threat. The bonus wasn't just money; it was the embodiment of the social compact that had made Lincoln Electric exceptional for six decades. If the company failed to pay it, workers would reasonably conclude that management's promises were worthless. The trust that made the incentive system function would be destroyed—possibly permanently.

The Hastings Turnaround

Hasting knew Lincoln Electric's Incentive Management only worked because workers trusted the management team to do the right things. The company's difficulties were caused by management's strategic errors, while workers continued to work hard as before. Therefore, it would be unfair to punish the workers. Workers reciprocated this gesture by going the extra mile. Hastings' turnaround plan called upon the company's US colleagues to increase production so that higher sales and profits in the US could offset the losses in Europe.

The plan required US factories to operate beyond 100% capacity utilization, increase daily sales targets from $1.8 million to $2.1 million, and increase overall pre-tax profit from $39 million to $52 million. By the end of 1993, daily sales in the US reached $3.1 million—50% above target. Some 450 people in key bottleneck areas gave up 614 weeks of vacations, with some people working seven-day weeks for months on end.

In 1992, Lincoln Electric paid $52 million in bonuses to its US workers and, in 1993, $55 million. Both times, the bonuses were paid out of borrowed money.

Borrowing money to pay bonuses when the company was losing tens of millions of dollars might seem insane. But Hastings understood that breaking the covenant would cost far more in the long run than the interest on the loans. The workers reciprocated by delivering the productivity gains that pulled the company back from the brink.

In 1992, Donald Hastings, who by then had spent four decades at Lincoln Electric, replaced Willis as the CEO. Immediately, he went about fixing the company's international operations. Hastings hired seasoned executives with international experience, including Anthony Massaro, who would later succeed Hastings as the CEO. He also arranged a $230 million loan facility to shore up the balance sheet. In 1993, Hastings relocated to Europe, where Lincoln Electric's problem was the gravest.

The Decisive Actions

Early in 1994, the company closed factories in Europe, Latin America, and South America, thereby eliminating 770 jobs. In the United States, however, where demand continued to run high, the company added 600 jobs. The company's decision to shed itself of those international operations resulted in a complete turnaround: 1994 sales and earnings reached record levels of $907 million and $48 million, respectively.

After suffering back-to-back net losses in 1992 and 1993, the company scored record sales and earnings in 1994.

The firm commemorated its 1995 centenary with a $100-million public stock offering, the first such stock offering in the company's history. It was a remarkable recovery from what had been a near-death experience.

Lessons Learned

The international expansion disaster taught Lincoln Electric several painful lessons that continue to shape its strategy today:

-

Culture doesn't export automatically. The incentive system that worked brilliantly in the U.S. required cultural assumptions—individualism, performance orientation, trust in management—that weren't universal.

-

International expertise matters. The company had expanded aggressively without adding leaders who understood international operations. When problems emerged, there was no one equipped to address them.

-

Debt is dangerous when combined with cyclical businesses. The combination of high leverage and economic downturn in Europe nearly destroyed the company.

-

The social compact is fragile and precious. Preserving trust with workers was worth borrowing money during a crisis—but only because that trust had been built over decades.

The experience left Lincoln Electric more cautious about international expansion but also more sophisticated in its approach. The company that emerged from the crisis was still committed to global growth, but with a very different strategy for achieving it.

VI. Modern Transformation: From Recovery to Reinvention (1997–2020)

The Massaro Era: Regionalized Global Strategy

Anthony Massaro was named President and the chief operating officer in 1996. Massaro restructured the incentive system so that it would function better in an international company.

The new CEO organized the company into five regional hubs. While he encouraged each region to align themselves to Lincoln Electric's US culture, he also gave each region leader a high degree of autonomy so they could adapt to local culture and customer demand. Having learned the lessons from earlier international expansion, Lincoln continued to cautiously expand abroad—but with a fundamentally different approach.

Rather than trying to transplant the American incentive system wholesale, Massaro allowed each region to develop compensation and management practices appropriate to local conditions. The U.S. operations continued to use the full Lincoln system; international operations adopted elements that worked locally while maintaining Lincoln's commitment to quality and customer service.

John M. Stropki succeeded Massaro as CEO and chairman in 2004 and remained in that position until Charles L. Mapes succeeded him in 2012.

The Mapes Era and Higher Standard 2025 Strategy

Under Christopher Mapes, who led the company from 2012 to 2023, Lincoln Electric executed a transformation that positioned it for the next phase of growth. Mapes was chair of the board since 2013, and president and CEO from 2012 to 2023.

Under the leadership of Chris Mapes, CEO since 2012, Lincoln has increased its global reach and product offerings, prioritized training welders as well as making welding equipment and innovating around the manufacture of electric-vehicle chargers.

The centerpiece of this era was the "Higher Standard 2025 Strategy," which focused on accelerating sales growth, profitability, and earnings performance during the 2020-2025 period. In the 2025 higher standard strategy, the objective is to achieve high single-digit, low double-digit type growth. Fundamental drivers are leading with technology, innovation.

Disciplined Acquisition Strategy

Lincoln Electric pursued a series of strategic acquisitions that expanded its capabilities while maintaining financial discipline. The company acquired J.W. Harris Co., a global leader in brazing and soldering alloys, to broaden its solutions capabilities and complement its core product lines.

The biggest deal came in 2022. Lincoln Electric's largest acquisition to date was in 2022, when it acquired Fori Automation for $427M.

Fori Automation, a privately held automation engineering firm founded in 1984, is a leading designer and manufacturer of complex, multi-armed automated welding systems with an extensive range of automated assembly systems, automated material handling solutions, automated large-scale, industrial guidance vehicles (AGVs), and end of line testing systems. Fori Automation primarily serves automotive and aerospace OEMs and is headquartered in Shelby Township, Michigan, with additional operations in six international facilities across Europe, Latin America and Asia.

The acquisition increases our annualized automation portfolio revenue to over $850 million as we advance towards our Higher Standard 2025 Strategy $1 billion target.

The Fori acquisition exemplified Lincoln's evolved M&A approach. Rather than acquiring troubled foreign operations hoping to fix them, Lincoln targeted well-run companies with complementary capabilities and strong cultural fit. When the Koerner family decided it was the right time to sell, one of the most important considerations, aside from valuation and deal terms, was to find a buyer that appreciated and committed to maintaining Fori's culture. It was also important to Fori's executive team and ownership that the buyer be based in the U.S., have a Midwest culture and be well-capitalized to make future investments needed to properly grow in the electrified space. Ultimately, Cleveland, Ohio-based Lincoln Electric was a great strategic fit and still maintained a family culture despite being a public company.

Since 2014, the company has executed 18 acquisitions with a cumulative investment of $1.1 billion.

Automation and Additive Manufacturing: The Future

Lincoln Electric's pivot toward automation represents both a strategic response to industry trends and a natural extension of its core capabilities.

In just three years, Lincoln Electric Co. has built in Euclid what may be the largest 3D printing factory of its kind anywhere. The operation, Lincoln Electric Additive Solutions (LAS), mates Lincoln's core arc welding capability with robotics to give the 125-year-old company entry into additive manufacturing, a rapidly growing sector of the manufacturing industry.

LAS's operation uses a kind of 3D printing called wire-arc additive manufacturing, or WAAM, that involves a process Lincoln has been working with for decades, arc welding. A robot-guided electric welder melts wire that is deposited layer upon layer in a process that uses multi-axis turntables to create a piece that may take days to build.

A key piece that helped kick off its additive manufacturing venture was added in 2015 when it purchased Wolf Robotics, a Fort Collins, Colorado, firm that developed robotic welding and cutting systems. After acquiring Wolf, Lincoln spent the next few years integrating Wolf's robots with its own welding systems before opening LAS in 2019. After starting with three robots, LAS has grown to 30 employees operating 18 robots.

"I would feel pretty confident with the assertion that it is the biggest facility there is," said one industry analyst. "When it comes to the ability to use robots to melt wire and build big, big things like big tools or big casting replacements, Lincoln Electric is not unique, but no one would dispute that they're a leader in this area."

Lincoln Electric's large-scale metal 3D printing solution has been selected by Bechtel Plant Machinery, Inc (BPMI) to provide mission critical applications to the US Navy.

VII. Lincoln Electric Today: Leadership, Strategy & Position (2024–2025)

The Hedlund Era

Steven Hedlund was appointed Chair of the Board of Directors in January 2025, and as President and Chief Executive Officer in January 2024 after serving as Chief Operating Officer since 2022.

Prior to joining Lincoln Electric, Mr. Hedlund held various leadership roles at Fortune Brands, Inc. and served as principal at Booz Allen & Hamilton. He earned a bachelor's degree and an MBA from Dartmouth College.

Hedlund joined Lincoln Electric in 2008 as Vice President, Strategy and Business Development and a member of the executive leadership team, where he led an accelerated acquisition strategy.

Hedlund brings a different background than many of his predecessors—strategy consulting rather than rising through manufacturing ranks. His tenure has emphasized continued execution of the automation strategy while navigating challenging macroeconomic conditions.

Current Financial Performance

Lincoln Electric generated net sales of $4 billion for the full year 2024, with automation portfolio sales of $911 million on track for the $1 billion target in 2025. The adjusted operating income margin reached 17.6% for the full year.

Record profitability was achieved with a 17.6% adjusted operating income margin, reflecting strong execution of strategic initiatives and diligent cost management. The company maintained strong cash flow generation with over 90% cash conversion, contributing to a 23% increase in returns to shareholders through dividends and share repurchases.

Lincoln Electric demonstrated robust performance in Q3 2025, with an 8% increase in sales and an 11% rise in gross profit. The gross profit margin expanded by 90 basis points to 36.7%.

The EV Charging Initiative: Velion

In a striking example of leveraging core competencies into adjacent markets, Lincoln Electric has entered the electric vehicle charging infrastructure business.

The Velion™ is the industry's first American-designed and American-made electric vehicle DC fast charger backed by over 125 years of manufacturing industrial-grade, high power electronic equipment built for high-duty cycles and 24/7 use in mission-critical industrial applications.

"Our DCFC charger is also the first and only American-designed and American-made EV charger to not only meet, but exceed, the requirements of the federal government's National Electric Vehicle Infrastructure Formula Program (NEVI)." The inaugural 150kW Velion™ DC fast charger exceeds 75% domestic content and is engineered to exceed 97% uptime.

This initiative represents the kind of adjacency expansion that plays to Lincoln's strengths: power electronics expertise, manufacturing excellence, and the ability to produce rugged industrial equipment designed for harsh operating conditions.

Dividend Excellence

Lincoln Electric Holdings, Inc. (LECO) has increased its dividends for 30 consecutive years. This is a positive sign of the company's financial stability and its ability to pay consistent dividends in the future.

"I am pleased to announce our 30th consecutive annual dividend increase," stated Steven B. Hedlund, chairman, president and chief executive officer.

Lincoln Electric Holdings, Inc.'s (LECO) dividend yield is 1.38%, with a payout ratio of 31.76% which means that 31.76% of the company's earnings are paid out as dividends.

The low payout ratio indicates significant capacity to maintain dividend growth even if earnings face cyclical pressure—a reassuring signal for income-focused investors.

VIII. Competitive Landscape and Industry Position

The Welding Industry Structure

The global welding equipment market represents a substantial industrial segment. The Welding Equipment market was valued at USD 14.17 Billion in 2024 and is projected to reach USD 23.1 Billion by 2031, growing at a CAGR of 6.30% during the forecast period 2024-2031.

Lincoln Electric has established one of the most trusted brands in welding and enjoys leading market share.

Key Competitors

Illinois Tool Works (ITW) / Miller Electric

ITW comprises a number of subsidiaries. Notable brands include Hobart, Miller Electric, Paslode, Foster Refrigerator, Brooks Instrument, and Permatex adhesives. As of 2024, ITW employed 44,000 employees in 51 countries and held 20,900 granted and pending patent applications worldwide. The company is based in Glenview, Illinois, a suburb of Chicago.

Illinois Tool Works, as the parent company of Miller Electric, competes indirectly with Lincoln Electric through its diversified portfolio in industrial products, including welding equipment. ITW's strategy focuses on innovation, with a strong commitment to research and development across various product lines. The company's extensive experience and resource availability provide it with a competitive advantage in terms of market reach and scalability.

ESAB Corporation

ESAB, Elektriska Svetsnings-Aktiebolaget (English: Electric Welding Limited company), is an American-Swedish industrial company. The ultimate parent company of ESAB is ESAB Corporation, a New York Stock Exchange listed company with its principal executive office in North Bethesda, Maryland, U.S. The company was founded in 1904 by Swedish businessman Oscar Kjellberg in Gothenburg, Sweden.

In a market that includes major competitors such as Lincoln Electric and Miller, ESAB distinguishes itself through its sustained focus on innovation and engineering excellence.

Key players like Lincoln Electric and Miller Electric dominate the landscape, supported by a strong distribution network. The competitive environment is characterized by innovation in electrode technology and a focus on sustainability.

The Razor-and-Blades Business Model

LECO is a high-quality, global leader in welding, with a sticky "razor-and-blades" business model driving recurring revenue. Capital allocation is disciplined, focusing on shareholder yield.

Lincoln strategically dominates both the capital equipment (welding machines) and the consumable products (electrodes). Machines last over 30 years, creating a need for a steady, recurring purchase of high-margin consumables, which provides stable, secure revenue for decades.

This business model creates significant switching costs and recurring revenue—classic characteristics of durable competitive advantage. Once a customer has standardized on Lincoln equipment and trained workers on Lincoln products, the incentive to switch is minimal while the consumables revenue flows reliably.

Porter's Five Forces Analysis

Threat of New Entrants: LOW - High capital requirements for manufacturing facilities - Established brands with decades of reputation - Extensive distribution networks difficult to replicate - Technical expertise and patent portfolios create barriers - Customer relationships built over decades

Bargaining Power of Suppliers: LOW to MODERATE - Lincoln Electric has significant scale in purchasing - Steel and raw materials are commodity inputs - Vertical integration in key components

Bargaining Power of Buyers: MODERATE - Large industrial customers have negotiating leverage - But switching costs are meaningful due to training and standardization - Distribution channel provides buffer with smaller customers - Consumables create recurring relationship

Threat of Substitutes: LOW to MODERATE - Welding remains essential for metal fabrication - Alternative joining methods (adhesives, mechanical fasteners) have limited applicability - Automation complements rather than replaces welding - Additive manufacturing is additive to, not substitutive for, welding capabilities

Competitive Rivalry: MODERATE - Concentrated industry with few major players - Competition primarily on innovation and service rather than price - Regional market share varies; Lincoln stronger in Americas - Automation growth attracts new competition

Hamilton Helmer's 7 Powers Framework

1. Scale Economies: PRESENT Lincoln Electric's manufacturing scale allows it to spread fixed costs across high volumes, enabling competitive pricing while maintaining margins.

2. Network Effects: LIMITED Unlike software platforms, welding equipment doesn't benefit from network effects.

3. Counter-Positioning: PRESENT HISTORICALLY Lincoln's incentive management system represented counter-positioning—competitors couldn't adopt it without disrupting their existing labor models. This advantage has diminished as the system hasn't translated internationally.

4. Switching Costs: STRONG Training investment, standardization on equipment and consumables, and relationship-specific knowledge create meaningful switching costs.

5. Branding: STRONG Lincoln Electric has established one of the most trusted brands in welding and enjoys leading market share. The "Welding Experts" positioning carries genuine credibility built over 130 years.

6. Cornered Resource: MODERATE The workforce culture developed over decades represents a resource competitors cannot easily replicate. The Welding School provides ongoing talent development.

7. Process Power: STRONG Lincoln's manufacturing excellence, embedded in both its incentive system and continuous improvement culture, represents process power that enables superior cost position.

IX. Bull Case & Bear Case for Investors

The Bull Case

1. Structural Growth in Automation Manufacturing automation is a multi-decade trend driven by labor shortages, rising wages, and the need for precision. Automation portfolio sales reached $911 million in 2024 and are on track for the $1 billion target in 2025. The Fori acquisition positioned Lincoln as a leader in this space.

2. Infrastructure Renaissance U.S. infrastructure spending under recent legislation creates substantial demand for welding equipment and consumables. Construction, transportation, and energy projects all require metal fabrication.

3. Reshoring and Nearshoring Trends The company expressed cautious optimism about potential for growth driven by reshoring and nearshoring trends. Manufacturing returning to North America benefits Lincoln's strongest geographic segment.

4. Razor-and-Blades Recurring Revenue The installed base of Lincoln equipment creates ongoing consumables demand. This provides revenue stability through economic cycles.

5. Capital Allocation Excellence Lincoln Electric Holdings, Inc. (LECO) stands out as a rare blend of operational resilience, disciplined capital allocation, and a 30-year dividend growth legacy. With a history of navigating economic cycles while maintaining robust cash flow generation, the company has cemented its reputation as a "buy-and-hold" stalwart in the industrial sector.

6. EV Charging Optionality The Velion DC fast charger represents a call option on EV infrastructure growth, leveraging existing manufacturing capabilities.

The Bear Case

1. Cyclical Exposure Welding demand correlates with industrial production, construction, and automotive investment. Economic downturns directly impact equipment sales.

2. International Weakness Lincoln Electric's international welding business is not as strong as domestic welding, with operating margins lagging the Americas welding segment by roughly 900 basis points.

3. Automotive Transition Uncertainty Electric vehicles require less welding than internal combustion vehicles. While Lincoln is positioning for EV-related opportunities, the transition creates uncertainty for traditional automotive welding demand.

4. Tariff and Trade Policy Risk Potential impacts from pending tariffs and trade policies present uncertainties that could affect the company's operations and financial performance.

5. Valuation Lincoln Electric Holdings remains a "Hold," as shares are pricey despite its leading position in the global arc welding market.

6. Culture Transferability Limits The incentive system that drives U.S. productivity hasn't transferred to international operations, limiting the company's ability to replicate its domestic model globally.

Key Metrics to Track

For investors monitoring Lincoln Electric's ongoing performance, the most critical KPIs are:

1. Automation Portfolio Revenue Growth This segment represents Lincoln's strategic future. Tracking progress toward and beyond the $1 billion target indicates success in the transformation strategy. Watch for organic growth rates separate from acquisition contributions.

2. Americas Welding Segment EBIT Margin This is Lincoln's core profit engine. Americas Welding adjusted EBIT margin was 19.1% in the fourth quarter of 2024. Sustained margins above 18% indicate pricing power and operational excellence are intact. Margin compression would signal competitive or cost pressures.

X. Looking Forward: Challenges and Opportunities

The Skilled Welder Shortage

One of Lincoln Electric's most important advantages may be one of its oldest initiatives: the Welding School. The skilled welder shortage that plagues modern manufacturing creates both challenges and opportunities.

The challenge is clear: customers can't utilize welding equipment if they lack trained operators. But the opportunity is equally clear: Lincoln's training infrastructure positions it as a solution provider, not just an equipment vendor. Companies increasingly value suppliers who can help address their workforce challenges.

Additive Manufacturing Scale

Lincoln Electric Additive Solutions represents a strategic bet on the future of manufacturing. Douglass said Lincoln envisions building regional printing centers around the United States and the world. "Look at the supply chain issues," he said. "Do we want to be printing up a part in Cleveland that (gets sent) to Singapore? No. We'll digitally send the (computer design) file to Singapore and you can print the same part there, because they'll have the same equipment, same wire."

This vision—global manufacturing capacity that can produce locally using digital designs—represents a fundamental shift in how industrial parts might be sourced and manufactured.

Digital Solutions and Software

The company is increasingly emphasizing software and digital solutions. The company offers a range of software and digital solutions to help its customers increase their productivity, remotely monitor their welding operations, and digitize their documentation.

This mirrors broader industrial trends toward connected equipment and data-driven operations.

Electric Vehicle Infrastructure

The Velion initiative may represent a significant growth avenue if EV adoption accelerates as projected. Lincoln's positioning as "American-designed and American-made" aligns with federal infrastructure preferences.

XI. Conclusion: What 130 Years Teaches Us

Lincoln Electric's story offers several lessons for students of business history and long-term investors:

Culture matters—but doesn't travel easily. The Lincoln Incentive Management System created extraordinary productivity and loyalty in the U.S. workforce. But the attempt to export it globally nearly destroyed the company. Culture is context-dependent, and competitive advantages rooted in culture may have natural geographic limits.

Trust, once built, is worth preserving—almost at any cost. When Donald Hastings borrowed money to pay employee bonuses during a crisis caused by management's strategic errors, he preserved the social compact that made Lincoln's system function. The short-term cost was enormous; the long-term value was incalculable.

Industrial businesses can reinvent themselves—but not overnight. Lincoln's transformation from a pure welding company to an automation and additive manufacturing leader has taken decades and continues today. Reinvention requires patience, discipline, and willingness to make acquisitions that add capabilities rather than just scale.

The razor-and-blades model creates durable competitive advantage. Lincoln's combination of long-lived equipment and high-margin consumables creates recurring revenue and switching costs that sustain profitability through cycles.

Capital allocation discipline compounds over time. Thirty consecutive years of dividend increases don't happen by accident. They reflect a management culture that balances reinvestment with returns to shareholders.

For Lincoln Electric, the $200 that John C. Lincoln invested in 1895 has compounded into a $13 billion enterprise that remains essential to modern manufacturing. The next 130 years will bring challenges that are impossible to predict—but the company's history suggests it has the cultural and operational foundations to adapt.

Whether that makes it an attractive investment at current prices depends on individual circumstances and views on valuation, cyclicality, and the trajectory of industrial automation. But as a case study in building and sustaining industrial competitive advantage, Lincoln Electric has few peers.

The journey from that December day in 1895 to the present offers one final reflection worth considering: the tension between continuity and adaptation that defines all enduring enterprises.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube