KKR & Co.: The Evolution of Private Equity

I. Introduction & Episode Roadmap

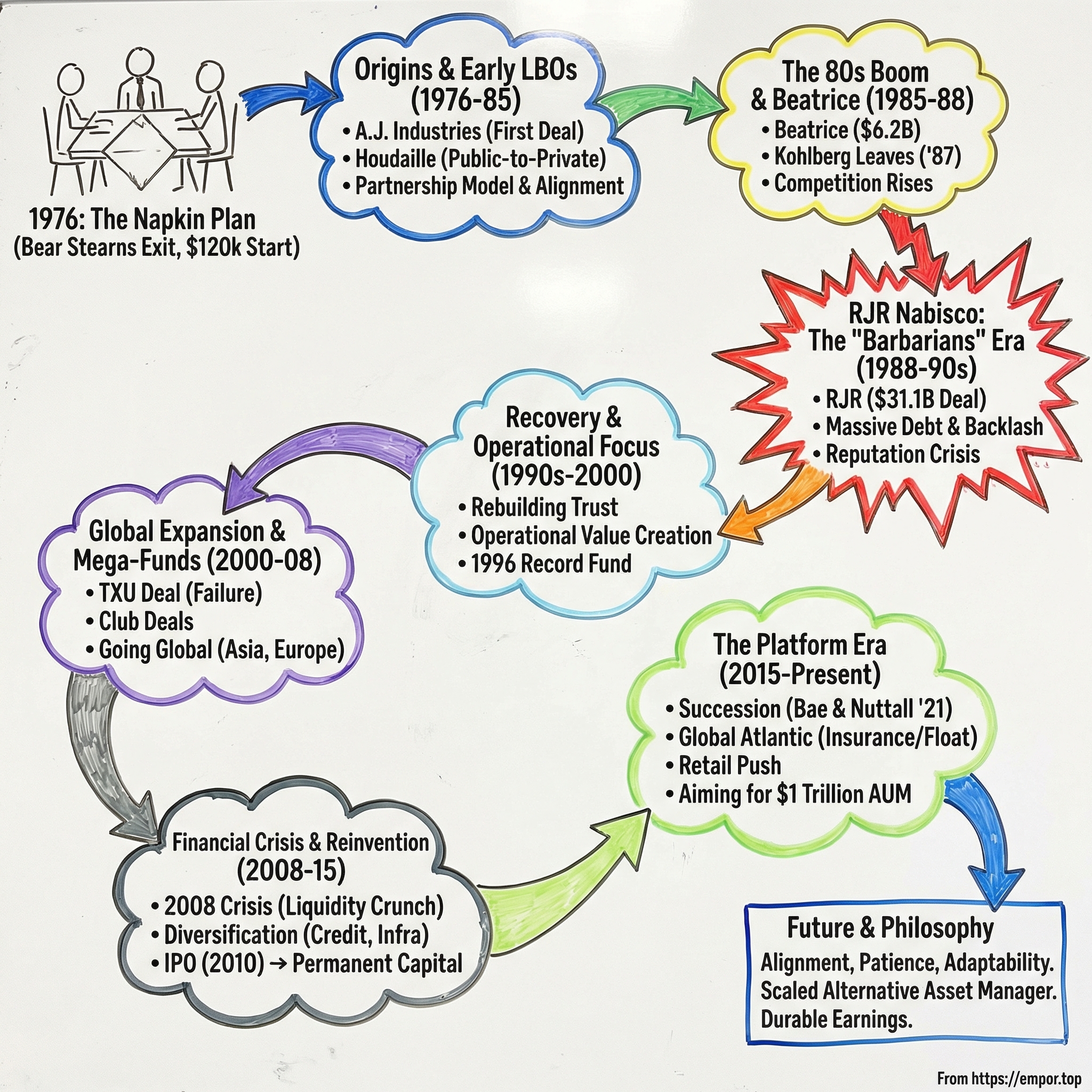

Picture this: It's May 1976, and three men sit in a Manhattan restaurant, sketching out ideas on a napkin that would fundamentally reshape global capitalism. They have no office, no fund, no investors—just $120,000 between them and an audacious vision for a new kind of financial firm. Fast forward to today, and that napkin sketch has become KKR & Co., managing $553 billion in assets and having completed 770 private equity investments worth approximately $790 billion in total enterprise value.

The question that drives this story isn't just how three guys from Bear Stearns built the firm that pioneered modern private equity—it's how they transformed from Wall Street's most feared "barbarians" into trusted partners of the world's largest corporations, pension funds, and governments. This is a tale of invention, reinvention, and the relentless evolution of an industry that didn't exist when Jerome Kohlberg, Henry Kravis, and George Roberts first shook hands on their partnership.

What you're about to discover goes beyond the headlines and Hollywood dramatizations. This is the story of how leveraged buyouts went from a niche financial technique to a dominant force in corporate America. It's about how a firm vilified for the excesses of the 1980s became a pioneer of stakeholder capitalism and operational excellence. And it's about the fundamental tension at the heart of private equity: the balance between financial engineering and genuine value creation.

The themes we'll explore resonate far beyond KKR's boardrooms. We'll examine how reputation crises can catalyze transformation, why institutional building matters more than individual deals, and how the best dealmakers think about time horizons that span decades, not quarters. Whether you're an investor trying to understand alternative assets, an operator curious about private equity's playbook, or simply someone fascinated by power and money, this journey through KKR's evolution offers lessons that transcend finance.

II. Origins: Bear Stearns and the Birth of an Idea (1960s–1976)

The fluorescent lights of Bear Stearns' trading floor hummed overhead as Jerome Kohlberg Jr. stared at another corporate loan document in 1964. At 39, Jerry—as everyone called him—had already built a respectable career in corporate finance. But something bothered him about the traditional investment banking model. Companies would come to Bear Stearns for advice, debt financing, maybe an IPO, but the relationship was transactional. What if, he wondered, an investment firm could actually own these companies, partner with management, and create value over years rather than quarters?

This wasn't how Wall Street worked in the 1960s. Investment banks advised and underwrote; they didn't buy and operate. But Jerry had noticed something interesting in his work with family-owned businesses. Many founders wanted liquidity but didn't trust public markets. They worried about quarterly earnings pressure, hostile takeovers, and losing control of their life's work. Meanwhile, corporate conglomerates were buying everything in sight, often destroying what made these businesses special in the first place.

Jerry's innovation was elegantly simple: use borrowed money to buy companies, partner with existing management, improve operations, and sell later at a profit. The leverage would amplify returns, management would have skin in the game through equity stakes, and patient capital could enable long-term value creation. He called these transactions "bootstrap acquisitions"—a term that would later evolve into "leveraged buyouts."

In 1965, Jerry recruited his first protégé: Henry Kravis, a 21-year-old from Tulsa with an economics degree from Claremont McKenna. Henry was everything Jerry wasn't—aggressive where Jerry was thoughtful, impatient where Jerry was methodical. But they shared a crucial trait: both believed the traditional Wall Street model was broken. Henry's cousin, George Roberts, joined the team in 1969, bringing a quieter intensity and an exceptional ability to build relationships with institutional investors.

The trio completed several small buyouts at Bear Stearns, but the firm's culture grated on them. Bear operated on an "eat what you kill" model—producers kept most of their fees, the firm took its cut, and there was little institutional support or long-term thinking. Partners fought over compensation, backstabbed for credit, and viewed clients as transactions rather than relationships. Jerry, Henry, and George had a different vision: a true partnership where economics were shared, decisions were collective, and relationships spanned decades.

By early 1976, the tension became unbearable. Bear Stearns' senior partners didn't understand why Jerry wanted to tie up capital in illiquid buyouts when the firm could earn quick fees from traditional banking. The final straw came when Bear's management committee rejected a buyout fund proposal, essentially telling the trio to stick to conventional deals or leave.

They chose to leave.

The now-famous napkin meeting happened at a coffee shop near Grand Central Station. Jerry sketched out the structure: they'd raise capital from institutions, buy companies with borrowed money, improve operations, and share profits with both investors and management teams. George and Henry each scraped together $10,000, while Jerry, nineteen years older and more financially established, contributed $100,000. They calculated they needed $500,000 annually to cover expenses for at least five years.

Their fundraising pitch was refreshingly honest. They approached eight individuals—mostly successful executives Jerry knew from his Bear Stearns days—asking for $50,000 each over five years. In return, these backers would see every deal and could invest on a deal-by-deal basis. No management fees, no guaranteed returns, just the opportunity to co-invest alongside three guys who believed they could revolutionize corporate finance.

On May 1, 1976, Kohlberg Kravis Roberts & Co. opened for business in a small office at 645 Madison Avenue. They had no secretary, no analyst, no track record as an independent firm. But they had something more valuable: a conviction that American business needed a new model of ownership, one that aligned the interests of investors, managers, and owners over the long term.

III. Early Years: Building the LBO Playbook (1976–1985)

The elevator at A.J. Industries' headquarters creaked as it climbed to the executive floor in January 1977. Henry Kravis adjusted his tie nervously—this was KKR's first real shot at a buyout, and everything hinged on convincing CEO John Jordan that three guys with no track record deserved to buy his company. A.J. Industries wasn't glamorous—it manufactured brake drums and industrial equipment—but it was profitable, underleveraged, and Jordan was ready to retire. Perfect.

The meeting that followed established what would become KKR's signature approach. Instead of the hostile, slash-and-burn tactics that corporate raiders employed, Henry and Jerry presented themselves as partners. They would keep existing management, invest in growth, and give executives equity stakes that could make them wealthy. Jordan was intrigued but skeptical: "How do I know you won't just load us with debt and strip our assets?"

Jerry's response became KKR gospel: "Because we're not financial engineers, we're business builders. We make money when companies grow, not when they shrink."

The A.J. Industries deal closed for $94 million in 1977, with KKR putting up just $1.7 million in equity. The rest came from bank loans and seller financing—a 55-to-1 leverage ratio that would make modern regulators faint. But it worked. Over the next six years, KKR improved operations, made strategic acquisitions, and eventually sold A.J. Industries for $447 million, generating a 45% annual return.

This success established the template, but KKR's real breakthrough came from an unexpected source: pension funds. In 1978, the Department of Labor clarified that pension funds could invest in alternative assets under the "prudent man rule." Suddenly, massive pools of capital seeking higher returns could flow into private equity. George Roberts, working from a small office in Menlo Park, California, became KKR's secret weapon in tapping this market.

While Henry worked Wall Street with characteristic aggression, George methodically built relationships with state pension funds, insurance companies, and endowments. His pitch was counterintuitive: "We're not asking you to take more risk. We're asking you to be more patient." He explained how ownership and operational improvement could generate superior returns with less volatility than public markets—if investors could handle illiquidity.

The Oregon State Treasury became KKR's first major institutional investor in 1981, committing $178 million to what would become known as the "Oregon Investment Pool." This wasn't just capital; it was validation. If conservative pension trustees believed in the model, others would follow. The deal that truly announced KKR's arrival as a major force was the 1979 public-to-private leveraged buyout of Houdaille Industries, valued at $380 million. This wasn't just big—it was the first time a leveraged buyout took a major public company private. The engineering was audacious: KKR kicked in a microscopic $1 million toward the buyout, while arranging $300 million in debt financing. Houdaille shareholders, who held $15 shares before the offer, walked away with $40 per share.

The Houdaille deal became Wall Street's Rosetta Stone for understanding leveraged buyouts. "The public documents on that deal were grabbed up by every firm on Wall Street," one buyout artist recalled. "We all said, 'Holy mackerel, look at this!'" Every investment banker in New York suddenly wanted to understand how three guys with minimal capital could buy a $380 million company.

But Houdaille also foreshadowed the challenges ahead. The company struggled with debt service during the 1981-82 recession and faced unexpected Japanese competition in machine tools. KKR de-emphasized the company's machine tool business, which was facing stiff competition from Japanese companies, and decided to expand the rubber gaskets business through acquisitions. They later sold Houdaille to Tube Investments in 1987, making a great return for investors.

This experience taught KKR a crucial lesson: leverage amplified both returns and risks. Future deals would require more careful attention to competitive dynamics and economic cycles. But the basic model had been proven. Between 1977 and 1985, KKR completed 24 buyouts, refining their approach with each transaction.

The firm's structure evolved alongside their deals. They pioneered the "2 and 20" fee model—2% annual management fees on committed capital, 20% of profits above a hurdle rate. Limited partners got 80% of gains, general partners got 20%, but crucially, KKR executives invested their own money in every deal. This wasn't just about alignment; it was about credibility. As they would tell skeptical CEOs: "We're betting our own fortunes on this working."

By 1985, KKR had raised multiple funds totaling over $1 billion and completed buyouts worth $7 billion. They had created an entirely new asset class, attracted institutional capital at scale, and proven that patient, aligned ownership could generate exceptional returns. The apprenticeship was over. The masters were ready for bigger game.

IV. The 1980s Buyout Boom: From Niche to Mainstream (1985–1988)

The Marriott ballroom in midtown Manhattan buzzed with anticipation in October 1985. KKR was hosting its annual investor meeting, but this year felt different. In the audience sat representatives from 47 pension funds, insurance companies, and endowments—a far cry from the eight individual backers who had launched the firm nine years earlier. Henry Kravis took the stage, his boyish face belying the audacity of his message: "The real opportunity in leveraged buyouts hasn't even started yet."

He was right. The economic stars had aligned perfectly for an LBO explosion. Interest rates had fallen from their 1981 peak of 20% to under 10%. The Reagan administration's tax cuts left corporations flush with cash. Hostile raiders like Carl Icahn and T. Boone Pickens terrorized boardrooms, making friendly buyouts look attractive by comparison. And most importantly, Michael Milken's junk bond machine at Drexel Burnham Lambert had created a seemingly bottomless pool of debt financing.

KKR's deals grew exponentially larger. In 1985, they acquired Storer Communications for $2.5 billion—at the time, the largest leveraged buyout ever. The following year came Beatrice Companies at $6.1 billion, then Safeway at $4.2 billion. Each deal pushed the boundaries of what markets thought possible, yet each generated stellar returns. Beatrice alone netted KKR and its investors over $2 billion in profits through asset sales and restructuring.

But something significant happened in 1987 that would reshape KKR's future: At age 61, Kohlberg resigned, with Henry Kravis succeeding him as senior partner. Jerry had grown increasingly uncomfortable with the mega-deals and aggressive tactics the firm was employing. He believed in building businesses, not financial engineering. The split was amicable but profound—the mentor who had invented the LBO was leaving just as his creation was conquering Wall Street.

Competition emerged from every corner. Forstmann Little, founded by former KKR target Ted Forstmann, positioned itself as the "white knight" alternative—no junk bonds, no asset stripping, just good old-fashioned equity and bank debt. Blackstone, launched in 1985 by Lehman Brothers veterans Stephen Schwarzman and Pete Peterson, brought establishment credibility to the buyout world. Thomas H. Lee, Clayton Dubilier & Rice, and dozens of other firms crowded into the space.

The competition bred innovation but also excess. Buyout firms began paying higher multiples, using more leverage, and making increasingly optimistic projections. The "auction" process became standard—investment banks would shop companies to multiple buyout firms, driving up prices. KKR's advantage shifted from being the only game in town to being the most sophisticated player in an increasingly complex game.

Wall Street itself transformed to serve this new ecosystem. Investment banks created dedicated financial sponsors groups. Law firms built practices around buyout documentation. Consulting firms like Bain & Company spawned their own buyout funds. An entire industry crystallized around what had been, just a decade earlier, a niche financial technique.

Michael Milken's junk bond empire deserves special attention in this story. By 1986, Drexel could raise billions in hours through its network of savings and loans, insurance companies, and mutual funds. Milken's "highly confident letter"—a promise that Drexel could raise financing for any deal—became Wall Street's most powerful weapon. KKR initially resisted using junk bonds, preferring traditional bank debt, but the competitive reality forced their hand. To win deals, you needed Drexel.

The cultural impact was equally profound. Gordon Gekko's "greed is good" speech in 1987's "Wall Street" captured the zeitgeist, though it conflated raiders with buyout firms. Business school graduates, who once aspired to run Fortune 500 companies, now dreamed of partnership at KKR or Blackstone. The leveraged buyout had gone from obscure financial technique to the dominant force in American capitalism.

By 1988, KKR had completed over 30 major buyouts with a combined value exceeding $40 billion. They had generated average annual returns above 30% for their investors. Henry Kravis graced magazine covers, attended state dinners, and served on museum boards. George Roberts, operating from California, had built relationships with every major institutional investor in America.

But success bred hubris. Deals got bigger, leverage got higher, and competition got fiercer. The stage was set for the deal of the century—a transaction that would define not just KKR, but an entire era of American business.

V. RJR Nabisco: The Deal That Changed Everything (1988–1989)

Ross Johnson's Gulfstream IV descended through the October clouds toward Atlanta's Hartsfield Airport, carrying the CEO of RJR Nabisco back from another round of golf with celebrities and politicians. At 57, the Canadian-born executive had perfected the art of corporate excess—a fleet of jets, lavish parties, million-dollar consulting contracts for friends. RJR Nabisco, the tobacco and food conglomerate behind Winston cigarettes and Oreo cookies, generated $15 billion in annual revenue, but its stock languished around $56 per share. Johnson saw an opportunity: take the company private, slash the perks (except his own), and make a fortune.

On October 19, 1988, Johnson shocked Wall Street by announcing a management buyout at $75 per share, partnering with Shearson Lehman Hutton. The bid valued RJR at $17 billion—already the largest LBO ever proposed. Johnson would personally make over $100 million. But he had made a fatal miscalculation: by going public with his intentions, he had started an auction.

Henry Kravis learned about the bid from the morning papers at his Park Avenue apartment. He was furious. KKR had actually approached Johnson months earlier about a buyout, only to be rebuffed. Now Johnson was trying to steal the company for himself at what Henry immediately recognized as a lowball price. Within hours, KKR's team was mobilizing for war.

The battle that followed resembled a Shakespearean drama more than a financial transaction. Ted Forstmann entered the fray, positioning his firm as the "moral alternative" to both Johnson's greed and KKR's junk bond tactics. First Boston assembled its own bid group. The auction drew in every major player on Wall Street—investment banks, law firms, commercial banks, junk bond dealers. Everyone wanted a piece of the biggest fee bonanza in history.

The negotiations took place in wood-paneled conference rooms and Park Avenue restaurants, but the real action happened in the media. Leaks flew fast and furious. Johnson's lavish spending became front-page news—the $51 million fleet of corporate jets, the $2.9 million in fees to celebrity golfers, the Atlanta mansion maintained for his dog. Public opinion turned decisively against the management team.

KKR played the game masterfully. They positioned themselves as responsible stewards who would preserve jobs and honor communities—a stark contrast to Johnson's crew of corporate raiders. George Roberts flew in from California to work his relationships with institutional investors. Jerry Kohlberg, despite having left the firm, even made appearances to lend gravitas.

The bidding war escalated beyond all reason. After multiple bidding rounds, KKR emerged with an offer of $109 a share, or $25 billion total. Including assumed debt, the transaction value reached $31.1 billion—by far the largest leveraged buyout in history. The numbers were staggering: $20 billion in debt, $5 billion in equity, annual interest payments exceeding $2 billion.

KKR collected a $75 million fee in the RJR takeover, but the real payday would come from their equity stake—if they could make the deal work. The financing alone required a symphony of sources: bank debt, junk bonds, bridge loans, preferred stock, convertible debentures. Drexel Burnham Lambert alone raised $5 billion in junk bonds in a matter of days.

Victory came at 1:00 AM on December 1, 1988, when RJR's board voted to accept KKR's bid. Ross Johnson, who had started the process expecting a coronation, left with a $53 million golden parachute—wealthy but humiliated. The photographs from that night show exhausted bankers and lawyers, their ties askew, surrounded by the detritus of a hundred takeout dinners.

But winning was just the beginning. KKR now owned a company with businesses ranging from Nabisco's cookies to Reynolds' cigarettes, saddled with crushing debt in an era of growing anti-smoking sentiment. They immediately began selling assets: the European food business went for $2.5 billion, Del Monte for $1.48 billion. They cut costs, eliminated corporate jets, and moved headquarters from Atlanta to New York.

The human cost was significant. Thousands of jobs disappeared. Factories closed. Communities that had depended on RJR for generations watched their economic anchor disappear. The efficiency that private equity promised came with a very real price in disrupted lives and broken social contracts.

For KKR, the financial engineering required to keep RJR afloat was extraordinarily complex. They refinanced debt multiple times, issued new securities, and constantly juggled cash flows to meet interest payments. The tobacco business, while generating enormous cash, faced mounting legal challenges. The food business, which they had hoped would drive growth, struggled against competitors.

The final accounting took years to calculate. KKR began reducing its ownership in 1991, fully exiting by 1995. Depending on how you counted—including fees, refinancings, and dividends—KKR either made a modest profit or took a small loss on its equity. For a deal that consumed billions in capital and thousands of hours of effort, the returns were shockingly pedestrian.

Yet the impact transcended financial returns. RJR Nabisco became a cultural watershed, the moment when private equity entered mainstream consciousness—and not in a flattering light.

VI. The "Barbarian" Years: Reputation Crisis and Recovery (1989–2000)

Bryan Burrough and John Helyar's manuscript landed on Henry Kravis's desk in late 1989 with the weight of a verdict. "Barbarians at the Gate: The Fall of RJR Nabisco" painted KKR as ruthless financial engineers who destroyed companies for profit. The book became an instant bestseller, spawning an HBO movie where James Garner portrayed a sympathetic Ross Johnson against faceless Wall Street villains. The unpleasant by-product of the RJR Nabisco deal was being labeled "barbarians", a reputation that would haunt KKR for years.

The label stung because it contradicted everything KKR believed about itself. In Henry's mind, they were builders, not destroyers. They partnered with management, improved operations, and created value. But public perception had crystallized: private equity meant job losses, asset stripping, and greed.

After that, every company visit required explaining they had ideas and resources to help achieve vision and potential, as reputation and trust are crucial in business. CEOs who might have welcomed KKR's capital now viewed them with suspicion. Politicians denounced leveraged buyouts as destroying American industry. Even their own investors grew nervous about the reputational risk.

The early 1990s delivered a harsh reality check beyond reputation. The recession that began in 1990 exposed the fragility of highly leveraged companies. Several KKR portfolio companies struggled to service debt. Hillsborough Holdings (the renamed Jim Walter Corporation) filed for bankruptcy in 1989. Seaman Furniture followed in 1992. The easy money era was definitively over.

KKR's response revealed the firm's resilience and adaptability. First, they addressed the RJR albatross directly. KKR spent the early 1990s repaying RJR debt through asset sales and restructuring, reducing ownership starting in 1994, and divesting its final stake by 1995. They turned a potential disaster into a controlled exit, preserving investor confidence even without generating significant returns.

Second, they transformed their approach to deals. Gone were the days of pure financial engineering. KKR built an operations team, hiring former executives who could actually run businesses. They created portfolio support groups for strategy, technology, and human resources. They started measuring success not just by IRR but by revenue growth, operational improvements, and job creation.

The firm also pioneered a new narrative around private equity's social value. They emphasized stories of saving failing companies, preserving jobs that would otherwise disappear, and providing growth capital to businesses neglected by public markets. When they bought Duracell from Kraft in 1988, they didn't slash costs—they invested in new products and international expansion, eventually selling to Gillette for three times their purchase price.

Geographic expansion offered another path forward. While the U.S. dealt with recession and reputation issues, Europe was embracing privatization and deregulation. KKR opened a London office in 1991, though initial progress was slow. European businesses remained skeptical of American financial engineering, and local competitors understood the market better.

The mid-1990s brought an unexpected tailwind: the technology boom. While KKR largely missed the internet bubble—Henry famously said they "didn't understand technology companies"—the rising tide lifted all boats. Credit markets reopened, multiples expanded, and exit opportunities multiplied. In 1996, KKR was able to complete fundraising for what was then a record $6 billion private equity fund, the KKR 1996 Fund.

This fund marked KKR's full recovery from the "barbarian" years. Institutional investors had returned, convinced that KKR had learned from its mistakes. The deals from this era—Amphenol, Spalding, Kindercare—were smaller and more operationally focused than the 1980s mega-buyouts, but they generated superior returns with less drama.

Perhaps the most important evolution was in KKR's culture and messaging. They stopped celebrating financial engineering and started emphasizing partnership. Henry Kravis became a major philanthropist, donating hundreds of millions to hospitals, museums, and universities. George Roberts maintained his low profile but built deep relationships with pension funds whose retirees depended on KKR's returns.

By 2000, KKR had largely shed the "barbarian" label among sophisticated investors, though it lingered in popular culture. They had proven that private equity could evolve, that financial buyers could add operational value, and that patient capital could generate returns without destroying companies.

The lessons from this era would prove invaluable. KKR learned that reputation was an asset as valuable as any portfolio company, that operational improvement mattered more than leverage, and that private equity needed a social license to operate. These insights would guide them through the next phase of explosive growth—and the inevitable crisis that would follow.

VII. The Second Wave: Mega-Funds and Global Expansion (2000–2008)

The champagne flutes clinked at KKR's London office in September 2005 as the team celebrated closing Legrand SA, a €3.6 billion French electrical equipment manufacturer. It was KKR's first major European buyout, thirteen years after opening their London office. George Roberts, visiting from California, raised his glass with characteristic understatement: "It only took us a decade to figure out Europe. Asia might be faster."

The early 2000s had started inauspiciously. The dot-com crash vaporized exit opportunities, credit markets seized up, and limited partners questioned private equity allocations. But KKR recognized opportunity in crisis. While others retreated, they methodically built capabilities that would power their next phase of growth.

The transformation began with operational expertise. KKR hired Dean Nelson from McKinsey to lead a new "Capstone" team—internal consultants who worked exclusively with portfolio companies. They recruited former CEOs as "Executive Advisors" who could step into leadership roles. They created industry teams with deep sector knowledge. This wasn't window dressing for LPs; it was a fundamental shift in how KKR created value.

Credit markets roared back to life by 2003, fueled by low interest rates and yield-hungry investors. But this time, the dynamics were different. Banks eager to win lucrative M&A mandates offered "covenant-lite" loans with fewer restrictions. Credit default swaps allowed risks to be sliced, diced, and distributed globally. The CLO (collateralized loan obligation) market exploded, creating seemingly infinite demand for leveraged loans.

KKR capitalized on these conditions with increasingly audacious deals. In 2005, they acquired Toys "R" Us for $6.6 billion alongside Bain Capital and Vornado. In 2006, they bought HCA, the hospital chain, for $33 billion with Bain and Merrill Lynch—surpassing even RJR Nabisco as the largest LBO ever. The speed and size were breathtaking: KKR was deploying more capital in months than they had in entire decades. But the crown jewel—or perhaps the crown of thorns—came in 2007. KKR and TPG, together with Goldman Sachs Capital Partners, announced the acquisition of Texas power company TXU for an astounding $44.3bn in Enterprise Value, the largest LBO in history at the time. That purchase was the largest leveraged buyout in history. The deal closed on October 10, 2007, with TXU shareholders entitled to $69.25 in cash for each share of TXU common stock held.

The TXU deal epitomized both the ambition and the hubris of the era. At the time, the bet seemed logical and the buyout, while expensive, seemed relatively safe. Natural gas prices were at their peak, giving TXU Corp. sizable margins on their coal and nuclear power. The key assumption being made at the time of the buyout was that natural gas prices would remain high. KKR and TPG had even succeeded with a similar play before—in 2004, they had bought Texas Genco for $3.7 billion and sold it two years later for $5.8 billion.

Geographic expansion accelerated alongside these mega-deals. After years of frustration, KKR's European operation finally gained traction. The Legrand acquisition opened doors across the continent. They completed buyouts in Germany, Italy, and the UK, adapting their model to local regulations and business cultures. Asia presented different challenges—relationship-based business cultures, skepticism of foreign capital, complex regulatory frameworks—but KKR persevered, opening offices in Hong Kong, Tokyo, and Mumbai.

The operational capabilities KKR built during this period were genuinely transformative. They didn't just cut costs; they invested in growth. When they bought Dollar General in 2007 for $7.3 billion, they didn't slash stores—they opened 2,000 new locations. When they acquired HCA, they improved quality metrics while expanding services. This wasn't the asset-stripping of the 1980s; it was strategic value creation.

Club deals became the norm for the largest transactions. KKR would partner with Blackstone, Carlyle, or TPG to spread risk and share expertise. These consortiums could marshal tens of billions in days, making any public company a potential target. The cooperation was remarkable given the fierce competition—firms that battled viciously in auctions would seamlessly collaborate when the deal required it.

But warning signs were emerging. Covenant-lite loans meant fewer protections when things went wrong. Payment-in-kind (PIK) toggles allowed companies to defer cash interest payments by issuing more debt. Dividend recapitalizations let sponsors extract profits without improving operations. The system was building leverage upon leverage, risk upon risk.

By late 2007, KKR had raised a record $15 billion fund and was deploying capital at unprecedented speed. They had offices on four continents, hundreds of investment professionals, and a portfolio generating hundreds of billions in revenue. From the outside, it looked like unstoppable success.

But George Roberts, ever the careful investor, was growing nervous. In a partners' meeting that December, he posed a simple question: "What happens to TXU if natural gas prices fall?" The models showed disaster, but everyone assured him that gas prices had nowhere to go but up. Within months, the financial crisis would prove them catastrophically wrong.

VIII. Financial Crisis and Reinvention (2008–2015)

The Lehman Brothers logo came down from the Times Square building on September 15, 2008, as employees streamed out carrying cardboard boxes. Henry Kravis watched from KKR's offices at 9 West 57th Street, his usual confidence shaken. Lehman wasn't just another bank—they were KKR's partner on multiple deals, including having become an equity investor in TXU at closing. If Lehman could fall, what else might collapse?

The answer came swiftly and brutally. Credit markets froze overnight. Pending deals evaporated—KKR's $1.8 billion acquisition of Primedia collapsed when financing disappeared. Portfolio companies that depended on refinancing found themselves facing bankruptcy. The advent of fracking led to lower energy prices in the unregulated Texas energy market, devastating TXU's business model. Despite keeping up with interest payments, the debt load was far too large for TXU to be able to repay the principle, leading to its bankruptcy in 2014.

The TXU catastrophe deserves special attention as the largest LBO failure in history. Thanks to new technological advances and the expanded extraction of natural gas from the Eagle Ford Shale Play, natural gas prices dropped dramatically, reducing the reliance on coal and nuclear energy sources. The company that KKR and partners had bought for $44 billion was suddenly worth a fraction of that. In just seven years what amounted to the largest buyout in history would become the largest nonfinancial bankruptcy in U.S. history.

But crisis breeds opportunity for those with capital and courage. While competitors retreated, KKR made a pivotal strategic decision: go public. On March 2010, KKR filed to list its shares on the New York Stock Exchange (NYSE), with trading commencing on July 15, 2010. The move was controversial—private equity firms were supposed to be private. But George and Henry recognized that permanent capital from public markets could provide stability and flexibility that limited partner funds couldn't match.

Going public forced transparency that the secretive world of private equity had always resisted. KKR now reported quarterly earnings, disclosed portfolio performance, and faced analyst scrutiny. But it also gave them currency for acquisitions, liquidity for employees, and credibility with regulators. The stock initially struggled, trading below its $10 IPO price for years, but the long-term benefits would prove transformative.

The crisis also accelerated KKR's evolution beyond traditional buyouts. They launched a credit business, recognizing that dislocated debt markets offered attractive risk-adjusted returns. Starting with distressed debt and special situations, they gradually built capabilities in direct lending, mezzanine finance, and structured credit. By 2015, KKR's credit business managed over $20 billion—a business that didn't exist five years earlier.

Infrastructure became another growth vector. Governments worldwide faced budget constraints and aging infrastructure, creating opportunities for private capital. KKR raised dedicated infrastructure funds, investing in airports, pipelines, renewable energy, and telecommunications networks. These assets offered stable, long-term cash flows—exactly what pension funds needed in a low-interest-rate environment.

Real estate, long ignored by KKR as too competitive, suddenly became attractive as commercial property values collapsed. They hired teams from failed investment banks and distressed real estate funds, building capabilities from scratch. Their contrarian bets on U.S. commercial real estate in 2009-2010 generated exceptional returns as markets recovered.

The operational focus that had begun in the 2000s became existential during the crisis. Financial engineering couldn't save overleveraged companies when revenues declined and credit markets closed. KKR doubled down on portfolio support, creating specialized teams for procurement, technology implementation, and revenue growth. They hired former CEOs as "Executive Advisors" who could step into portfolio companies during crises.

The shift from financial engineering to operational improvement was more than tactical—it was philosophical. In a 2012 investor presentation, Henry Kravis declared: "The days of buying cheap and selling dear are over. Value creation is the only path to superior returns." This wasn't just marketing; KKR's post-crisis deals showed meaningfully more revenue growth and margin expansion than their pre-crisis portfolio.

Public market strategies offered another avenue for growth. KKR had traditionally avoided minority stakes and public equity, but the crisis created opportunities. They launched a hedge fund partnership, took strategic stakes in public companies, and pioneered "PIPE" investments (private investment in public equity). These strategies leveraged KKR's analytical capabilities while providing more flexibility than traditional buyouts.

The talent model evolved as well. KKR had always hired from investment banks and consulting firms, but now they recruited operating executives, technologists, and sector specialists. The firm that had once prided itself on lean staffing—remember, they started with just three people—now employed over 1,000 professionals globally.

By 2015, KKR had not just survived the financial crisis—they had emerged stronger. Assets under management exceeded $100 billion across multiple strategies. They had proven that private equity could adapt, evolve, and thrive even in the worst conditions. The firm that had pioneered leveraged buyouts was now pioneering the transformation of alternative asset management.

But the most important change was generational. Henry and George, now in their 70s, began succession planning in earnest. They promoted Joe Bae and Scott Nuttall to co-presidents, signaling a transition that would take years to complete. The founders who had built KKR from a napkin sketch were preparing to hand over their life's work to a new generation.

IX. The Platform Era: Becoming an Alternative Asset Manager (2015–Present)

The mahogany conference table at 30 Hudson Yards gleamed under the morning light as Joe Bae and Scott Nuttall took their seats for their first board meeting as co-CEOs in October 2021. The moment marked more than a leadership transition—it symbolized KKR's transformation from a buyout shop into a global alternative asset powerhouse. As of December 31, 2024, the firm had completed 770 private-equity investments with approximately $790 billion of total enterprise value, with assets under management (AUM) and fee paying assets under management (FPAUM) of $553 billion and $446 billion, respectively.

The handover from Henry and George had been meticulously orchestrated over years. In 2021, George and Henry handed over their CEO roles, with the intention to share learnings accumulated over half a century including the importance of collaboration, entrepreneurial spirit, and belief that companies must evolve to survive. Unlike many founder transitions that end in acrimony, this was a masterclass in succession planning. The founders remained as executive chairmen, providing guidance without micromanaging.

Joe Bae, a Harvard Business School graduate who joined KKR in 1996, brought deep expertise in Asia and credit markets. Scott Nuttall, who started as an analyst in 1996, had architected much of KKR's expansion into new asset classes. Together, they represented both continuity and change—steeped in KKR's culture but unencumbered by its history.

Their vision was audacious yet methodical. KKR's assets under management reached $638 billion, up 15% from the previous year, while fee-paying AUM rose to $512 billion, also a 15% increase. KKR raised $114 billion in new capital throughout 2024 and deployed a record $84 billion in investments. But the real ambition went further: KKR laid out a plan to reach at least $1 trillion of assets under management in five years and seeks to generate annual adjusted net income of more than $15 a share within a decade. The most transformative move came in 2021 when KKR closed their acquisition of Global Atlantic Financial Group Limited, with the acquisition of the leading retirement and life insurance company expected to add approximately $90 billion to KKR's Assets Under Management. KKR acquired a majority of Global Atlantic in 2021, and since that time, KKR has served as Global Atlantic's asset manager, offering access to its global investment and origination capabilities for the benefit of Global Atlantic's policyholders. This wasn't just another acquisition—it was a strategic revolution. Insurance companies needed alternative assets to meet return targets in a low-rate world, while KKR needed permanent capital to deploy. The synergies were obvious once you saw them.

By 2024, Global Atlantic became a wholly-owned subsidiary of KKR, after KKR acquired the remaining 37% stake. Global Atlantic's assets under management have grown significantly, up from $72 billion in 2020 to $158 billion today. The insurance business provided KKR with something invaluable: patient, permanent capital that could be deployed across credit, real estate, and infrastructure without the J-curve pressures of traditional private equity funds.

The democratization of alternatives became another frontier. Historically, private equity was accessible only to institutions and ultra-high-net-worth individuals. But Bae and Nuttall recognized that mass affluent investors—those with $1-10 million in investable assets—represented a $70 trillion opportunity. KKR launched dedicated vehicles for wealth management platforms, created interval funds for smaller investors, and partnered with wirehouses to distribute alternative products.

Technology transformation accelerated under the new leadership. KKR built a data science team that used machine learning to identify acquisition targets, predict portfolio company performance, and optimize exit timing. They created digital platforms for investor reporting, automated much of the due diligence process, and even experimented with tokenizing fund interests. This wasn't Silicon Valley disruption—it was thoughtful application of technology to enhance traditional strengths.

The firm's investment philosophy evolved while maintaining core principles. KKR aims to generate attractive investment returns by following a patient and disciplined investment approach, employing world-class people, and supporting growth in its portfolio companies and communities. They still believed in aligned interests, operational improvement, and patient capital. But the toolkit expanded dramatically—from minority growth investments to continuation funds that could hold assets for decades. Perhaps most notably, KKR became a founding partner of Ownership Works, a nonprofit created to support companies in implementing ownership cultures. Pete Stavros, a KKR partner, pioneered an innovative employee engagement and ownership model that has been successfully implemented at more than 50 KKR companies and has positively impacted more than a hundred thousand employees. The goal of Ownership Works is to create more than $20 billion of wealth for working families over the next decade.

This wasn't just corporate social responsibility—it was smart business. Companies with broad-based ownership showed higher engagement, lower turnover, and better financial performance. It also helped rehabilitate private equity's image, demonstrating that financial returns and worker prosperity weren't mutually exclusive.

The geographic footprint continued expanding strategically. In June 2022, KKR rose to the top of Private Equity International's PEI 300 ranking for the first time, replacing Blackstone Inc. as the largest private equity firm in the world, slipping back to second place in 2023 and 2024, before regaining top spot in the 2025 list. They weren't just competing on size—they were building local expertise, relationships, and capabilities in markets from Mumbai to São Paulo.

The firm's culture evolved while maintaining core values. KKR personally invests in everything they do from the firm's balance sheet for alignment, wouldn't ask anyone to invest in something they didn't put their own money into, with almost everyone who works at KKR being a shareholder in the company. This alignment extended beyond economics—it was about shared purpose and long-term thinking.

By 2024, KKR's transformation was complete. Fee related-earnings, total operating earnings and adjusted net income all grew over 35% year-over-year as the operating backdrop continued to improve. They had reached a capital markets milestone by generating $1 billion in revenues for the first time. The firm that had started with three guys and a napkin now employed thousands globally, managed over half a trillion in assets, and influenced the allocation of capital across the world economy.

X. Investment Philosophy & Operational Playbook

The war room at KKR's headquarters hummed with activity as the deal team evaluated a potential $5 billion acquisition in 2023. But this wasn't the testosterone-fueled, all-nighter culture of the 1980s. The team included former CEOs, McKinsey partners, data scientists, and sustainability experts. They weren't asking "how much leverage can we apply?" but rather "how can we double this company's organic growth rate?"

This evolution from leverage to operational value creation represents the fundamental transformation of KKR's investment philosophy. In the early days, the math was simple: buy a company for 5x EBITDA using 80% debt, improve margins slightly, and sell for 6x EBITDA five years later. The leverage amplified returns magnificently. Today, with purchase multiples often exceeding 12x and leverage capped by cautious lenders, the old playbook is obsolete.

KKR's modern approach starts with sector specialization. They've built dedicated teams for healthcare, technology, consumer, industrials, infrastructure, and financial services. Each team includes former operators who've actually run businesses in their sectors. When KKR evaluated a medical device company, the deal team included physicians who understood clinical workflows, former hospital administrators who knew reimbursement dynamics, and FDA regulatory experts who could assess approval timelines.

The operational playbook has become remarkably sophisticated. KKR Capstone, their portfolio operations team, employs over 100 professionals globally. They don't parachute in as consultants; they embed with portfolio companies for months or years. A typical engagement might include implementing procurement best practices to reduce costs by 15%, upgrading IT systems to enable data-driven decision making, or redesigning salesforce compensation to accelerate growth.

Take their approach to digital transformation. Every portfolio company undergoes a "digital diagnostic" within 100 days of acquisition. KKR's technology team assesses everything from cybersecurity vulnerabilities to e-commerce capabilities. They've developed playbooks for common transformations—moving to the cloud, implementing CRM systems, building data analytics capabilities. But they customize each approach, recognizing that a consumer products company needs different digital capabilities than an industrial manufacturer.

The talent strategy has become equally systematic. KKR maintains a network of over 400 senior advisors and operating executives who can step into portfolio companies as CEOs, CFOs, or board members. They've learned that leadership changes must be handled delicately—founder-led businesses require different approaches than corporate carve-outs. The firm has developed assessment tools to evaluate management teams objectively, identifying gaps and development needs early.

ESG integration represents another evolution in KKR's philosophy. What began as risk management—avoiding investments with environmental liabilities or governance problems—has become a value creation strategy. They've found that companies with strong ESG practices trade at premium multiples, attract better talent, and grow faster. KKR now measures and reports on ESG metrics across their portfolio, from carbon emissions to workplace diversity.

The stakeholder capitalism approach extends beyond rhetoric. KKR believes in the power of capitalism bringing prosperity to companies and people, that business can be a force for good, and was the pioneer of the buyout fund industry, today often referred to as private equity. Their broad-based ownership programs have created meaningful wealth for hourly workers—machine operators, warehouse staff, customer service representatives. When KKR sold CHI Overhead Doors in 2022, the average employee received $175,000 from their equity stake.

Patient capital has become a competitive advantage. While the traditional private equity model assumes a 5-7 year hold period, KKR has developed structures that enable longer ownership. Their core private equity strategy can hold assets for 10+ years. Their continuation funds allow them to retain ownership of successful companies even after returning capital to original investors. This patience enables transformations that wouldn't be possible under shorter timelines.

The measurement of success has evolved accordingly. IRR (internal rate of return) remains important, but KKR now tracks multiple metrics: revenue growth rates, EBITDA margin expansion, employee engagement scores, customer satisfaction metrics, and ESG improvements. They've learned that sustainable value creation requires balanced scorecards, not single-point optimization.

Risk management has become more sophisticated as well. Every investment undergoes scenario planning—what happens if there's a recession, if interest rates spike, if key customers defect? KKR builds downside protection into deal structures through earnouts, warranties, and insurance products. They've learned from disasters like TXU that even the best analysis can't predict black swans, so resilience matters more than optimization.

The approach to exits has also evolved. The old model was simple: take a company public or sell to a strategic buyer. Today, KKR employs multiple exit strategies. They might sell to another private equity firm, to a continuation fund, through a SPAC, or via partial exits that maintain upside exposure. They've learned to be opportunistic, selling when markets are frothy even if the business plan isn't complete.

This operational excellence hasn't come cheap. KKR spends hundreds of millions annually on portfolio support, technology, and talent development. But the returns justify the investment. Their post-2010 funds have generated consistent outperformance not through financial engineering but through genuine business building.

XI. Competitive Analysis & Industry Position

The quarterly earnings calls of the "Big Four" alternative asset managers—KKR, Blackstone, Apollo, and Carlyle—have become required listening for anyone trying to understand global capital flows. Combined, these firms manage over $4 trillion, influencing everything from housing prices to healthcare delivery. But beneath the surface similarities, each has carved out distinct competitive positions.

In June 2022, KKR rose to the top of Private Equity International's PEI 300 ranking for the first time, replacing Blackstone Inc. as the largest private equity firm in the world. While KKR slipped back to second place in 2023 and 2024, before regaining top spot in the 2025 list, the jockeying for position reveals less about absolute dominance and more about strategic choices.

Blackstone, with over $1 trillion in AUM, has become the Walmart of alternative assets—massive scale, operational efficiency, and presence in every major market and asset class. Their real estate business alone is larger than most firms' total AUM. But size brings challenges: finding enough large deals to deploy capital, managing regulatory scrutiny, and maintaining culture across 4,000+ employees.

Apollo has differentiated through credit expertise and insurance synergies. Their acquisition of Athene gave them permanent capital similar to KKR's Global Atlantic deal, but Apollo has pushed further into yield-generating strategies. They've essentially become a alternative to traditional fixed income, attracting investors seeking returns in a low-rate environment.

Carlyle, despite being the smallest of the Big Four, maintains advantages in certain sectors and geographies. Their government connections—multiple former cabinet members and ambassadors—provide unique access in regulated industries and emerging markets. They've also been more willing to experiment with new structures and strategies.

KKR's competitive position rests on several pillars. First, their balance sheet strength—with over $20 billion in investments and cash—provides flexibility that pure fund managers lack. They can warehouse deals, seed new strategies, and co-invest alongside LPs at scale. This balance sheet also signals conviction; when KKR leads a deal, they're putting their own money at risk.

Second, geographic diversification gives KKR advantages in cross-border transactions. When a European company wants to expand in Asia, or an Asian company needs U.S. market access, KKR's global platform provides unique value. They've completed more true cross-border deals than any competitor, leveraging relationships and expertise across regions.

Third, the breadth of strategies creates synergies. A company might start as a private equity investment, transition to credit financing for growth, require infrastructure investment for expansion, and eventually need real estate capital for facilities. KKR can provide all of this internally, creating stickier relationships and better economics.

The private credit opportunity has become a key battleground. As banks retreat from leveraged lending due to regulatory constraints, private credit has exploded from $500 billion in 2015 to over $1.5 trillion today. KKR's credit business, while smaller than Apollo's or Ares', benefits from deal flow from their private equity platform. They see transactions earlier and can offer integrated solutions that pure credit funds cannot.

But KKR faces real challenges. Fee pressure continues across the industry as sophisticated LPs demand better terms. The traditional "2 and 20" model is becoming "1.5 and 15" or worse for large investors. KKR has responded by offering co-investment opportunities, separately managed accounts, and lower-fee vehicles, but margins are compressing.

Competition for deals has intensified beyond the Big Four. Middle-market firms like Thoma Bravo in software or Leonard Green in retail have developed sector expertise that rivals or exceeds the large firms. Sovereign wealth funds increasingly compete directly for assets rather than investing through funds. Strategic buyers have returned with strong balance sheets and synergy arguments.

The talent war represents another challenge. KKR competes not just with other PE firms but with hedge funds, tech companies, and startups for top talent. Compensation expectations have soared—talented VPs expect seven-figure packages, and the carry pool must be divided among more professionals. KKR has responded with phantom equity, long-term incentive plans, and cultural initiatives, but retention remains challenging.

Regulatory scrutiny continues to intensify globally. The SEC has increased enforcement actions around fee disclosure, valuation practices, and conflicts of interest. European regulators are examining leverage levels and market concentration. Asian governments are restricting foreign investment in sensitive sectors. KKR has built substantial compliance infrastructure, but regulatory risk remains material.

The generational transition at KKR—from Henry and George to Joe and Scott—has gone smoothly so far, but leadership changes create uncertainty. Blackstone's Stephen Schwarzman and Apollo's Marc Rowan remain actively involved, potentially providing continuity advantages. Whether KKR's collective leadership model proves superior to founder-led competitors remains to be seen.

Market cycles pose the ultimate test. KKR has navigated multiple downturns, but the next recession will challenge portfolios assembled at peak valuations. Their diversification across strategies and geographies provides some protection, but a synchronized global downturn would stress every business line simultaneously.

Despite these challenges, KKR's position remains formidable. They've proven the ability to adapt, evolve, and innovate across multiple decades. Their culture of partnership, operational excellence, and long-term thinking has survived generational transition. And their scale, while not the largest, is sufficient to compete for any deal while maintaining agility.

XII. Bear & Bull Cases for the Future

The bull case for KKR starts with the inexorable shift of global capital toward alternative investments. Institutional investors currently allocate about 15% to alternatives; many plan to reach 25-30% within the decade. With $150 trillion in global institutional assets, even small allocation increases mean trillions flowing to firms like KKR. The math is compelling: if KKR maintains just its current market share, AUM could double within five years.

The Global Atlantic acquisition provides a strategic moat that's difficult to replicate. Insurance float offers permanent capital at attractive costs, enabling KKR to be patient when others face redemption pressures. As interest rates normalize, insurance companies desperately need higher-yielding assets—exactly what KKR's credit and real estate platforms provide. This virtuous cycle could accelerate: more insurance assets enable more lending, which attracts more insurance partnerships.

Geographic diversification offers another growth vector. While developed markets are saturated, emerging markets remain underpenetrated. KKR's early investments in India, Southeast Asia, and Latin America position them to capture growth as these economies mature. Their local presence and relationships, built over decades, cannot be easily replicated by competitors arriving late.

The technology and healthcare megatrends play to KKR's strengths. Digital transformation, aging populations, and scientific breakthroughs create massive investment opportunities. KKR's sector expertise, operational capabilities, and patient capital model align perfectly with these long-term themes. They can fund biotech development, roll up fragmented healthcare services, or enable digital transformation across industries.

Operational excellence provides sustainable differentiation. While anyone can raise capital, few can consistently improve portfolio companies. KKR's track record of operational value creation—documented across hundreds of case studies—attracts the best companies and management teams. This becomes self-reinforcing: success attracts better deals, which generate better returns, which attracts more capital.

The democratization of alternatives opens massive new markets. If KKR can successfully distribute products through wealth management channels, they'll access the $100+ trillion in global individual wealth. Even capturing a tiny fraction would transform the business. Their brand, track record, and institutional credibility provide advantages over upstarts targeting the same opportunity.

But the bear case is equally compelling. The private markets saturation debate has merit—too much capital chasing too few deals inevitably compresses returns. With over $4 trillion in dry powder globally, competition for assets is fierce. KKR must deploy capital to earn fees, potentially leading to poor investment decisions. The TXU disaster reminds us that even sophisticated firms make catastrophic errors when pressured to invest.

Fee pressure threatens the economic model. Large investors increasingly demand lower fees, co-investment rights, and transparency that erodes margins. If management fees fall to 1% and carry to 15%, the business becomes far less attractive. KKR's public listing helps with permanent capital, but also subjects them to quarterly earnings pressure that may conflict with long-term investing.

The next recession will test portfolios assembled at peak valuations. Many recent buyouts used 7-8x leverage at 15x+ EBITDA multiples. Even modest EBITDA declines could trigger covenant breaches and restructurings. KKR's reputation for operational improvement won't matter if portfolio companies can't service debt. The firm survived 2008, but that portfolio was assembled at lower valuations with less leverage.

Regulatory risks are intensifying globally. Proposed legislation could limit leverage, tax carry as ordinary income, or restrict pension fund investments in alternatives. Antitrust authorities increasingly scrutinize private equity roll-ups. Any major regulatory change could fundamentally alter the business model. KKR has adapted to past regulations, but future changes might be more restrictive.

The talent model faces structural challenges. The best investors increasingly want to start their own funds rather than share economics with large platforms. Carry pool dilution—spreading profits among hundreds of professionals—reduces individual upside. KKR must compete with tech companies offering massive equity packages and hedge funds with higher cash compensation. The apprenticeship model that developed Henry and George may not work for Generation Z.

Technology disruption poses existential questions. Could AI replace much of what junior investment professionals do? Might blockchain enable direct investment without intermediaries? Will crowd-funding platforms democratize access to deals? KKR is investing in technology, but incumbents rarely survive platform shifts. The firm's human-capital-intensive model might prove obsolete.

Public market volatility affects KKR directly as a listed company. The stock often trades at discounts to book value, reflecting investor skepticism about fee streams and carried interest. Market downturns could trigger a negative spiral: falling stock price makes retention harder, talent departures reduce competitiveness, lower returns further pressure the stock.

China exposure creates geopolitical risk. KKR has invested billions in Chinese companies, but U.S.-China tensions threaten these investments. Forced divestments, sanctions, or investment restrictions could impair returns and damage relationships. The firm must navigate competing pressures from Washington and Beijing without clear precedents.

The founder transition, while smooth so far, remains incomplete. Henry and George's relationships, reputation, and judgment cannot be fully transferred. Joe and Scott are capable leaders, but they haven't been tested by a major crisis. Leadership transitions often reveal hidden weaknesses; KKR's collective model might prove less effective under stress.

Limited partner concentration is concerning. KKR's top 20 investors represent a significant portion of AUM. If major pensions or sovereigns reduce allocations—due to performance, regulation, or politics—the impact would be severe. The firm is diversifying its investor base, but institutional concentration remains a vulnerability.

XIII. Lessons & Legacy

KKR's journey from a three-person startup to a global financial powerhouse offers lessons that transcend private equity. The firm didn't just pioneer leveraged buyouts—it fundamentally changed how we think about corporate ownership, governance, and value creation.

The first lesson is about timing and patience. Jerry Kohlberg spent years developing the LBO concept at Bear Stearns before launching KKR. They waited until the regulatory environment, capital markets, and economic conditions aligned. This patience—rare on Wall Street—became embedded in KKR's DNA. They've consistently been early to new strategies but willing to wait years for them to mature.

The power of aligned interests runs through every chapter of KKR's story. From the beginning, they invested their own money alongside clients. This wasn't just about economics—it was about trust. When you're asking pension funds to entrust billions, saying "we're in this together" matters. The principle extends to portfolio companies, where management equity stakes align executives with value creation.

Reputation, KKR learned, is an asset as valuable as any portfolio company. The "Barbarians at the Gate" label took years to overcome, teaching them that financial success without social legitimacy is ultimately hollow. Their evolution toward stakeholder capitalism wasn't just political correctness—it was recognition that sustainable value creation requires buy-in from employees, communities, and society.

The importance of operational excellence over financial engineering represents perhaps the most important evolution. The easy money of the 1980s, when leverage alone could generate returns, is gone forever. KKR's build-out of operational capabilities—from procurement to digital transformation—shows that sustainable competitive advantages come from genuinely improving businesses, not just restructuring their capital.

Culture, often dismissed as soft in finance, proved crucial to KKR's longevity. The partnership ethos, where economics and decision-making are shared, created stability through multiple cycles. While competitors imploded from internal conflicts, KKR maintained cohesion. Their motto—"one firm, one team"—sounds clichéd but guided real decisions about compensation, governance, and strategy.

The value of diversification became clear through successive crises. Firms focused solely on buyouts struggled when credit markets closed. Those concentrated in one geography missed global opportunities. KKR's expansion into credit, infrastructure, real estate, and insurance provided ballast during storms and growth when traditional buyouts slowed.

Adaptation without abandoning core principles enabled survival across different eras. KKR evolved from bootstrap acquisitions to mega-buyouts to operational value creation to platform building. But throughout, certain principles remained constant: aligned interests, long-term thinking, and partnership. This balance between evolution and consistency is rare in finance.

The transformation of corporate finance and governance represents KKR's broadest impact. Before private equity, corporate ownership was binary: public companies with dispersed shareholders or private companies with concentrated ownership. Private equity created a hybrid—concentrated ownership with institutional governance. This model, pioneered by KKR, has become standard across industries.

The firm's influence on corporate management practices extends beyond their portfolio. The operational improvements KKR pioneered—zero-based budgeting, salesforce effectiveness, digital transformation—have been adopted by corporations globally. Management teams now think like private equity investors, focusing on cash flow, returns on capital, and exit multiples.

KKR believes in the power of capitalism bringing prosperity to companies and people, that business can be a force for good, and was the pioneer of the buyout fund industry, today often referred to as private equity. This belief, tested through multiple crises and controversies, drives their approach to investing. They've shown that financial returns and social value aren't mutually exclusive—properly structured, they can be mutually reinforcing.

For investors, KKR's story offers several takeaways. First, true value creation takes time—the best investments often require years of patient work. Second, operational improvements matter more than financial engineering in generating sustainable returns. Third, alignment of interests between investors and managers is crucial for long-term success.

For operators, the lessons are equally valuable. KKR has shown that professional management, combined with appropriate incentives and capital, can transform underperforming businesses. Their playbooks for operational improvement, while not revolutionary individually, prove powerful when systematically applied. The emphasis on measurement, accountability, and continuous improvement has raised performance standards across industries.

The ongoing evolution of alternative investments, which KKR helped catalyze, continues reshaping global finance. Private markets now rival public markets in importance. Patient capital competes with quarterly capitalism. Professional investors partner with management rather than passively holding shares. These trends, pioneered by KKR, will likely accelerate.

Looking forward, KKR's legacy depends on navigating new challenges while maintaining historical strengths. Can they democratize alternatives without compromising returns? Will operational excellence remain differentiating as competitors build similar capabilities? How will they balance stakeholder interests when they conflict? These questions will determine whether KKR's next chapter matches its remarkable history.

The firm that started with three men and a napkin has become a symbol of American financial innovation—for better and worse. Critics see financial engineering that destroys jobs and loads companies with debt. Supporters see value creation that improves businesses and generates returns for pensioners. The truth, as KKR's complex history shows, encompasses both perspectives.

What's undeniable is KKR's transformation of global capitalism. They didn't just create an industry; they changed how we think about ownership, governance, and value. Whether you view private equity as capitalism's pinnacle or its perversion, you're grappling with ideas that KKR helped introduce. That intellectual legacy, beyond any financial returns, may be their most lasting contribution.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube