Invitation Homes: The Institutionalization of American Single-Family Rentals

I. Introduction & Episode Roadmap

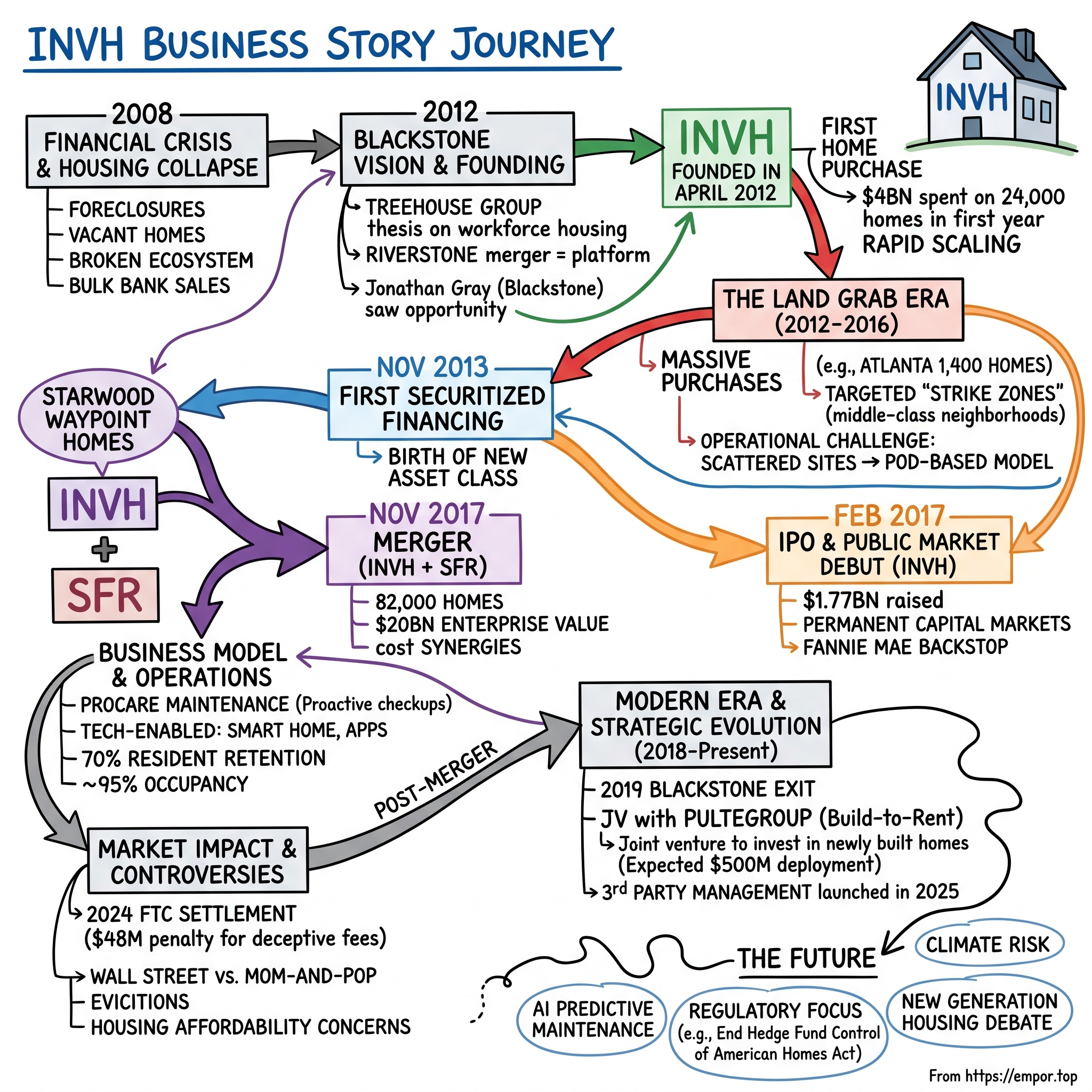

Picture this: April 2012, Phoenix, Arizona. The desert sun beats down on a modest three-bedroom house in a middle-class neighborhood—unremarkable except for one detail. This house, purchased for $130,000 cash, would become the first domino in what would transform into a $25 billion real estate empire. The buyer wasn't a family seeking shelter or a local investor chasing yield. It was Blackstone, the world's largest alternative asset manager, embarking on what would become the most audacious bet in American residential real estate history.

Today, Invitation Homes stands as a colossus—a $20+ billion market cap REIT generating $2.6 billion in annual revenue from 84,000 single-family rental homes scattered across 16 major U.S. markets. It's the nation's largest owner of single-family rental homes, a title that would have seemed absurd just fifteen years ago when this asset class was the exclusive domain of mom-and-pop landlords managing a handful of properties on weekends.

The central question isn't just how this happened—it's what it means. How did a post-financial crisis opportunistic bet morph into the permanent institutionalization of American single-family rentals? When private equity titans started buying foreclosed homes by the thousands, critics warned of Wall Street becoming America's landlord. Proponents countered that professional management would bring efficiency and quality to a fragmented market. A decade later, both were partially right.

This is a story about crisis-driven opportunities and the entrepreneurs who spot them. It's about scale economics in markets that resist scale. It's about technology transforming cottage industries into institutional asset classes. And perhaps most provocatively, it's about the American Dream itself—once defined by homeownership, now increasingly experienced through monthly rent payments to publicly-traded corporations.

The journey from that first Phoenix home to today's rental empire reveals fundamental truths about modern capitalism: how financial engineering can reshape entire markets, how technology enables previously impossible business models, and how the scars of economic crises create the foundations for new industries. What Blackstone and its competitors built wasn't just a portfolio of homes—they created an entirely new asset class, complete with its own securities markets, operational playbooks, and investment thesis.

As we unpack this transformation, we'll explore the characters who made the bold bets, the controversies that erupted along the way, and the lasting impact on American housing. Because whether you view Invitation Homes as a success story of American innovation or a cautionary tale about financialization, one thing is certain: the single-family rental market will never be the same.

II. The 2008 Financial Crisis & Housing Collapse

The implosion began quietly, almost imperceptibly. In early 2006, home prices in markets like Las Vegas and Phoenix started to plateau after years of meteoric rises. Real estate agents assured nervous sellers it was just a breather—a healthy pause before the next leg up. They were catastrophically wrong.

By December 2008, the Case-Shiller Home Price Index recorded its largest price drop in history. What started as a subprime mortgage problem had metastasized into a full-blown economic catastrophe. The statistics were staggering: 8.7 million jobs vaporized between 2007 and 2010. Unemployment rocketed from a comfortable 5% to a depression-era 10%. One in four American households watched 75% of their net worth evaporate. The American Dream wasn't just deferred—it was foreclosed upon.

The human toll was visceral. Drive through any subdivision in Phoenix, Las Vegas, or inland California, and you'd see the same haunting pattern: pristine homes with brown lawns, foreclosure notices taped to windows, swimming pools turning green with algae. Entire neighborhoods resembled modern ghost towns. In some Phoenix zip codes, over 70% of homes went into foreclosure. The sheer scale defied comprehension—millions of families displaced, their homes becoming distressed assets on bank balance sheets.

For traditional homebuyers, this was a nightmare. Banks weren't lending. Those with cash were terrified to catch a falling knife. The few local investors brave enough to buy were overwhelmed by the inventory. In Phoenix alone, over 50,000 homes sat vacant. Who could possibly absorb this tsunami of distressed properties?

The traditional real estate ecosystem had broken down completely. Banks, desperate to offload foreclosed homes, began selling in bulk—something previously unheard of in residential real estate. In 2011, the FDIC auctioned off a portfolio of 1,200 homes for $49 million. Bank of America was shopping packages of hundreds of properties. Fannie Mae and Freddie Mac, sitting on 250,000 foreclosed homes, launched pilot programs to sell properties to institutional investors who would rent them out.

This was the crucial pivot point—the moment when single-family homes stopped being just shelter and became distressed debt, an asset class that could be packaged, priced, and traded at institutional scale. The housing crisis had created something unprecedented in American history: the opportunity to buy thousands of homes at 30-50% discounts to peak prices, in concentrated geographic areas, with motivated sellers desperate for bulk buyers. The stage was set for one of the most audacious plays in real estate history. The crisis that destroyed millions of American dreams would become the foundation for Wall Street's entry into Main Street. What nobody could have predicted was how quickly, and how completely, the transformation would occur.

III. The Blackstone Vision & Founding Story (2012)

In 2005, when Phoenix real estate was still booming and everyone was a genius with a mortgage broker's license, a young entrepreneur named Dallas Tanner saw something different. While others chased quick flips and land development deals, Tanner and his partners formed Treehouse Group with a contrarian thesis: focus on workforce housing, the unsexy apartments and manufactured homes that provided steady, risk-adjusted returns. They called it "coupon-clipping real estate"—boring, predictable, profitable.

Between 2010 and 2011, Treehouse bought 1,000 distressed houses in Phoenix, Arizona, a city heavily impacted by foreclosures caused by the subprime mortgage crisis and one of the first areas where private equity investor purchases of homes for rent took place after the Great Recession. Phoenix had become ground zero for the housing collapse, with some neighborhoods seeing 70% foreclosure rates. While others saw disaster, Tanner saw opportunity at scale.

In 2011, Treehouse merged with the Dallas-based property management firm Riverstone Residential. This wasn't just a merger—it was the creation of a vertically integrated platform that could buy, renovate, and manage properties at institutional scale. They had cracked the code on something everyone said was impossible: running single-family rentals profitably at scale.

Enter Blackstone. Jonathan Gray, then head of real estate at the private equity giant, had been studying the housing wreckage with growing interest. The math was compelling: homes selling at 30-50% discounts to replacement cost, a growing pool of former homeowners who needed rental housing, and virtually no institutional competition. But Blackstone needed operators who understood the nuances of scattered-site property management.

"A startup company meets private equity … meets a moment in time in the marketplace," Tanner says of the coupling. "We had a perfect model in terms of one market [Phoenix], a high concentration of residential product, and a consistent operating history. Blackstone was intrigued. We knew if we could do a deal with Blackstone, we could do better scale, more markets, and we'd have the right kind of sponsor to expand."

The company was acquired by Blackstone Inc in the spring of 2012, forming Invitation Homes, with Blackstone giving Treehouse and Residential more capital to expand the business. Blackstone provided most of the capital, while Treehouse and Riverstone provided the know-how. It was a marriage of institutional capital and entrepreneurial expertise—Blackstone's billions meeting Tanner's boots-on-the-ground operational knowledge.

Invitation Homes' first home purchase was in April 2012, and within a year the company had spent $4 billion on 24,000 homes in the United States, becoming the largest buyer of homes for rent in the United States. The speed was breathtaking. In some weeks, Invitation Homes was buying 1,000 houses. They deployed teams to courthouse auctions with cashier's checks, competed with local flippers on foreclosure sites, and negotiated bulk deals with banks desperate to clear their books.

The thesis was elegant in its simplicity but revolutionary in its implications. For the first time in American history, single-family homes would be owned and operated like apartment buildings—with professional management, institutional capital, and economies of scale. The mom-and-pop landlords who had dominated the market for generations were about to face competition from one of the world's most sophisticated investment firms.

What Blackstone recognized—and what its competitors initially missed—was that technology had finally made this model possible. Property management software could handle maintenance requests across thousands of homes. Data analytics could optimize pricing and identify acquisition targets. Digital marketing could fill vacancies faster than yard signs. The same forces that had enabled Uber and Airbnb were about to transform residential real estate.

Critics immediately emerged. "Wall Street is becoming America's landlord," headlines screamed. Housing advocates warned that institutional ownership would drive up rents and lock out first-time buyers. But Blackstone pressed forward, convinced that professional management would actually improve the rental experience while generating attractive risk-adjusted returns.

Tanner was at the forefront of creating the single-family rental industry. He initially served as Executive Vice President and Chief Investment Officer from the company's founding in April 2012 until January 2019. His vision of transforming single-family rentals—making them institutional-quality assets—was becoming reality at a pace nobody had anticipated.

The transformation from that first Phoenix purchase to a multi-billion-dollar platform happened in mere months. By the end of 2012, Invitation Homes owned over 10,000 homes. The land grab was on.

IV. The Land Grab Era: Building Scale (2012-2016)

The summer of 2012 felt like the California Gold Rush, except the treasure wasn't buried in riverbeds—it was sitting vacant on suburban streets from Phoenix to Tampa. Invitation Homes wasn't just buying houses; they were vacuum-cleaning entire neighborhoods.

In April 2013, it made a $100-million-plus purchase of 1,400 Atlanta homes from Building and Land Technology. Think about that scale—1,400 homes in a single transaction. That's not real estate investing; that's industrial-scale acquisition. From August 2012 to June 2013, Invitation Homes purchased 1,650 homes in the Tampa Bay Area for over $250 million. The company was spending a million dollars a day, seven days a week, turning distressed assets into rental income streams.

At the time, corporate home owners like Invitation Homes were purchasing houses in "strike zones," neighborhoods located near several jobs, schools, and transportation systems that were also facing high amounts of foreclosures, and rented them to middle-aged parents raising children making around $100,000 a year or more. This wasn't random buying—it was surgical. They targeted the sweet spot of American suburbia: good schools, reasonable commutes, family-friendly neighborhoods that had been devastated by foreclosures but retained their fundamental appeal.

The operational challenge was staggering. How do you manage thousands of scattered properties across multiple states? Traditional property management broke down at this scale. You couldn't have a property manager driving between houses all day. Invitation Homes continues to build an efficient platform for single-family rentals, leveraging local experts and technology in its markets by rolling out a "pod-based" operations model with teams of 10- 15 local company associates who oversee all the needs of a defined set of homes in their market. Each pod functioned like a micro property management company, responsible for everything from leasing to maintenance for their assigned homes.

The competitive advantage wasn't just capital—it was speed. While a traditional buyer needed mortgage approval, inspections, and contingencies, Invitation Homes showed up with cashier's checks. In hot auctions, they could close in days, not weeks. Banks loved them because bulk sales meant clearing hundreds of distressed assets in one transaction rather than dealing with individual buyers for months.

By 2016, the transformation was complete. Between 2012 and 2016, Blackstone acquired almost 50,000 single family homes in thirteen markets including Southern California, Northern California, Seattle, Phoenix, Las Vegas, South Florida, Tampa, Orlando, Jacksonville, Atlanta, Charlotte, Chicago, and Minneapolis for purchase prices totaling $8.3 billion. The portfolio had reached critical mass—enough scale to justify custom technology platforms, negotiate volume discounts with contractors, and most importantly, access institutional capital markets.

The securitization breakthrough came in November 2013. Invitation Homes completes the first-ever securitized financing for residential rental homes, setting in motion a new form of investment in single-family rental homes. This wasn't just a financing mechanism—it was the birth of an entirely new asset class. Single-family rental bonds were now tradeable securities, bringing Wall Street capital markets to Main Street housing.

What Blackstone had proven was that single-family rentals weren't just viable at institutional scale—they were profitable. With 95% occupancy rates and rising rents in recovering markets, the returns were exceeding even the most optimistic projections. The "land grab" phase was ending not because opportunities dried up, but because the model had been validated. It was time to go public.

V. The IPO & Public Market Debut (2017)

February 1, 2017. The opening bell rings at the New York Stock Exchange, and a new ticker symbol lights up the boards: INVH. Five years after buying its first home in Phoenix, Invitation Homes was now a public company, and the transformation from opportunistic bet to permanent institution was complete.

Invitation Homes Inc. announced the pricing of an initial public offering of 77,000,000 shares of its common stock at $20.00 per share. The shares will be listed on the New York Stock Exchange and trade under the ticker symbol "INVH" beginning February 1, 2017. The demand was so strong that underwriters exercised their full option, bringing the total to 88.55 million shares and gross proceeds of $1,771.0 million.

In February, Invitation Homes became a public company via an initial public offering, the second-largest initial public offering of a real estate investment trust in the United States with $1.77 billion. Only Paramount Group's 2014 IPO had been larger in REIT history. This wasn't just a liquidity event—it was a validation of an entire asset class.

The timing was strategic brilliance. The housing market had recovered enough to demonstrate the model's durability, but institutional ownership of single-family rentals was still nascent enough to offer massive growth potential. With nearly 50,000 homes for lease in 13 markets across the country, Invitation Homes is meeting changing lifestyle demands by providing residents access to updated homes with features they value, such as close proximity to jobs and access to good schools.

Why go public? For Blackstone, it provided partial liquidity after five years of patient capital deployment. For Invitation Homes, it meant access to permanent capital markets—no longer dependent on private equity fund cycles. Public market investors could now participate in what had been an exclusively institutional play. The REIT structure also provided tax efficiency and required dividend distributions, appealing to income-focused investors.

The market reception spoke volumes. The shares priced at $20.00 per share, the higher end of the expected $18-$21 range. Institutional investors who had watched from the sidelines as Blackstone built the platform could finally buy in. The underwriter syndicate read like a who's who of Wall Street: Deutsche Bank, J.P. Morgan, Bank of America Merrill Lynch, Goldman Sachs, Wells Fargo, Credit Suisse, Morgan Stanley, and RBC Capital Markets.

What the IPO really represented was the institutionalization of an asset class. Single-family rentals were no longer a trade or a crisis-driven opportunity—they were a permanent feature of American housing. The public markets had blessed the model with liquidity, transparency, and most importantly, permanence.

Behind the financial engineering was a more profound shift. The Census Bureau announced that U.S. home ownership rates fell in the 2016 4Q to 63.7 percent from 63.8 percent a year earlier, continuing a trend of low home ownership. There are multiple reasons for the trend, ranging from a lack of millennial interest in owning a home to rising home prices driving down ownership. Invitation Homes wasn't just capitalizing on a temporary dislocation—it was positioned for a generational shift in how Americans approached housing.

Critics remained vocal. Just days before the IPO, Fannie Mae funded $1 billion of debt to Invitation Homes as back-up money, the first time in history it backstopped a single-family house landlord company. The decision received criticism from more than 25 affordable-housing advocate groups, who believed Fannie Mae wasn't following its principle of protecting home owners. The controversy highlighted the tension between efficient capital markets and housing affordability concerns.

But the market had spoken. Invitation Homes was now a public company, accountable to shareholders, regulated by the SEC, and subject to the quarterly scrutiny of public markets. The cowboys who had rushed into foreclosure auctions with cashier's checks were now executives of a NYSE-listed REIT. And they were just getting started—because six months later, they would engineer the biggest merger in single-family rental history.

VI. The Starwood Waypoint Merger: Creating a Behemoth (2017)

Six months after going public, Invitation Homes was ready for its boldest move yet. On August 10, 2017, the company announced a blockbuster deal that would reshape the single-family rental landscape forever.

Invitation Homes (NYSE: INVH) and Starwood Waypoint Homes (NYSE: SFR), two leading owners and operators of single-family rental homes in the United States, announced today the signing of a definitive agreement to combine in a 100 percent stock-for-stock merger-of-equals transaction. The language was careful—"merger of equals"—but the numbers told the real story: Based on the closing prices of Starwood Waypoint Homes common shares and Invitation Homes common stock on August 9, 2017, the equity market capitalization of the combined company would be approximately $11 billion and the total enterprise value (including debt) would be approximately $20 billion.

Under the terms of the agreement, each Starwood Waypoint Homes share will be converted into 1.614 Invitation Homes shares, based on a fixed exchange ratio. The math worked out to Invitation Homes stockholders will own approximately 59 percent of the combined company's stock, with current Starwood Waypoint Homes stockholders owning the remainder. For Blackstone, this meant dilution from 70% ownership to 41%—but in a company worth nearly twice as much.

The strategic logic was compelling. That means the combined company will own and operate approximately 82,000 single-family rental homes, with an average of 4,800 homes per market. This wasn't just about getting bigger—it was about achieving market density that would unlock operational efficiencies no competitor could match. In markets like Atlanta and Phoenix, the combined company would own thousands of homes, justifying dedicated maintenance crews, volume purchasing agreements, and sophisticated local management infrastructure.

"This merger creates the leading single-family rental company in the United States, which will be uniquely positioned to deliver exceptional service to residents, while also improving operating efficiency. That is a win-win for both residents and stockholders," said Fred Tuomi, Chief Executive Officer of Starwood Waypoint Homes. "We will have an irreplaceable portfolio of homes focused in select high-growth markets, offering unrivaled service and high-quality housing options for families choosing to rent. We have great admiration for Invitation Homes and its talented team, and look forward to embarking on an exciting new chapter together."

The synergies were real and quantifiable. Additionally, Invitation Homes expects annual run-rate cost synergies from the merger of between $45 million to $50 million. These would come from eliminating duplicate corporate functions, negotiating better vendor contracts at scale, and implementing best practices across the combined portfolio.

What made this merger particularly interesting was the complementary strengths each company brought. This strategic transaction combines two companies with highly complementary capabilities, including Invitation Homes industry-leading approach to customer service and asset-management expertise, and Starwood Waypoint Homes industry-leading technology. Starwood Waypoint had invested heavily in proprietary technology platforms for everything from maintenance dispatch to dynamic pricing. Invitation Homes had superior local market knowledge and operational density.

The choice of leadership was telling. Fred Tuomi, Starwood Waypoint's CEO, would lead the combined company. In addition, the current Starwood Waypoint Homes CEO Fred Tuomi, who will become CEO of the combined company, has experience successfully integrating mergers of large-scale, single-family rental companies. Tuomi had previously orchestrated the merger of Colony American Homes and Starwood Waypoint Residential Trust—he knew how to integrate large portfolios without disrupting operations.

Market reaction was enthusiastic. Shares of both companies reacted positively to the news. In mid-morning trading, Invitation Homes share prices were 4.9 percent higher from the previous day's closing price of $22.02. Starwood Waypoint share prices had gained 5.3 percent to $35.41. Wall Street recognized what this meant: the creation of a company with true competitive moats in an industry where scale was everything.

The merger also highlighted a crucial fact about the industry's evolution. While Invitation Homes is expected to be the largest single-family rental company in the United States upon the closing of the Merger, its portfolio will represent less than 0.1 percent of the more than 90 million single-family homes in the United States, and just 0.5 percent of the nearly 16 million single-family homes for rent in the United States. Despite the massive consolidation, the combined company would still own a tiny fraction of the total market—there was room to grow.

Invitation Homes Inc. (NYSE: INVH) today announced the completion of its previously announced merger with Starwood Waypoint Homes. Beginning today, the combined company will operate under the name "Invitation Homes" and continue trading on the New York Stock Exchange under the current ticker symbol for Invitation Homes (NYSE: INVH). The deal closed on November 16, 2017, creating an undisputed industry leader. The era of fragmented single-family rentals was officially over.

VII. Business Model & Operations Deep Dive

Behind the glossy IPO documents and merger announcements lies the operational reality of managing 84,000 homes scattered across America. This isn't traditional real estate—it's logistics, technology, and customer service at a scale never before attempted in residential housing.

The revenue model appears deceptively simple: The nation's premier home leasing company, provides professionally managed, updated homes for rent in desirable neighborhoods for a more inviting life. But the operational complexity behind that promise is staggering. Each home generates revenue through monthly rent, but also requires constant attention—maintenance, turnover management, capital improvements, and customer service.

The secret sauce is technology. We continue to innovate with Smart Home technology, an industry-leading maintenance app, and other forward-thinking programs that simplify your lifestyle. The Smart Home features aren't just amenities—they're operational tools. Lock and unlock your front door from your smart phone remotely or onsite. It's convenience and peace of mind all in one. When a resident moves out, property managers can remotely control access for cleaning crews, maintenance teams, and prospective tenants without ever visiting the property.

The maintenance model represents a fundamental reimagining of property management. ProCare is an innovative and proactive maintenance program designed to optimize each touchpoint with the resident and the home. The way it works is simple: we engage with the home and the resident at several points in the lifecycle of a lease, allowing us to make any tune-ups needed and to ensure the home meets our standards. This proactive approach reduces emergency calls, extends asset life, and improves resident satisfaction.

The technology stack is comprehensive. As the nation's premier home leasing company, Invitation Homes is enabling more than 80,000 people to live in a great house without the headache and long-term commitment of owning. Your dream home is just a lease away. It's easy, thanks to our app: • Search homes in 16 locations across the US. • Save and compare your favorite homes all in one place. • Book a self tour that works with your schedule. • Take a virtual 360° tour from wherever you are. • Use the "My Dashboard" tab to find quick links for payments, maintenance, and support. The entire resident journey—from initial search to move-out—happens digitally.

The operational model relies on local density. Invitation Homes continues to build an efficient platform for single-family rentals, leveraging local experts and technology in its markets by rolling out a "pod-based" operations model with teams of 10- 15 local company associates who oversee all the needs of a defined set of homes in their market. Each pod functions as a micro property management company, with dedicated maintenance technicians, leasing agents, and property managers responsible for approximately 500-750 homes in a concentrated geographic area.

Quality control happens through systematic inspections. Once you're settled in, we'll come by about 45 days later to make sure everything is working just as it should. To get a jump on maintenance needs for your home, we'll schedule a checkup every six months following your Post Move-In Visit. We'll focus on catching small issues early to prevent bigger problems later on. This scheduled maintenance reduces costly emergency repairs and extends the useful life of major systems.

The resident profile is carefully targeted. Tenants are typically in their late-30s with children and household income of approximately $100,000. These aren't residents who can't qualify for mortgages—they're families choosing flexibility over ownership, often relocating for work or preferring to avoid maintenance responsibilities.

Retention is the hidden metric that drives profitability. No wonder we have nearly 80% resident retention! With turnover costs averaging $3,000-$4,000 per home (cleaning, repairs, marketing, vacancy), keeping residents in place is crucial. The ProCare program, responsive maintenance, and quality homes all serve this retention goal.

Invitation Homes' occupancy stabilizes to 90% for total portfolio and 95% for Same Store portfolio. The company continues to grow its portfolio of homes to 50,000 across 13 markets and improves its services, launching ProCare proactive maintenance to better serve residents. These occupancy rates, combined with 3-5% annual rent increases, drive predictable revenue growth that REIT investors prize.

The institutional advantage becomes clear when compared to mom-and-pop landlords. Professional management, 24/7 maintenance response, standardized lease terms, and technology-enabled services create a differentiated product. Residents get consistency and professionalism; investors get predictable returns.

What Invitation Homes has built isn't just a real estate portfolio—it's an operating system for distributed residential assets. The same property that a local landlord might struggle to manage profitably becomes a cash-flowing asset in Invitation's system. Scale, technology, and operational excellence transform a fragmented cottage industry into an institutional asset class. The business model works not because Invitation Homes owns houses, but because they've industrialized the process of managing them.

VIII. Market Impact & Controversies

The gleaming corporate headquarters in Dallas tells one story. The tenant complaints flooding social media tell another. For every glossy investor presentation touting operational excellence, there's a Reddit thread documenting maintenance nightmares and surprise fees. The tension between Invitation Homes as financial innovation and Invitation Homes as America's controversial landlord reached a boiling point in 2024.

The Federal Trade Commission is taking action against Invitation Homes, the country's largest landlord of single-family homes, for an array of unlawful actions against consumers, including deceiving renters about lease costs, charging undisclosed junk fees, failing to inspect homes before residents moved in, and unfairly withholding tenants' security deposits when they moved out. Invitation Homes has agreed to a proposed settlement order that would require the company to turn over $48 million to be used to refund consumers harmed by its actions.

The FTC's investigation revealed practices that seemed designed to maximize revenue at every touchpoint. The complaint alleges that Invitation Homes advertised monthly rental rates that failed to include mandatory junk fees that could total more than $1,700 yearly. Consumers looking for rental houses paid nonrefundable fees—including application fees up to $55 and reservation fees up to $500—based on the deceptively advertised rates. Consumers learned that the price would be higher than advertised only when they received a copy of their lease, and sometimes not even until after they signed the lease.

The most damning evidence came from within. The complaint cites a 2019 email from Invitation Homes' CEO calling on the senior vice president responsible for overseeing the company's fee program to "juice this hog" by making the smart home fee mandatory for renters. This wasn't a rogue employee—it was corporate strategy from the top.

Since 2019, Invitation Homes has collected more than $18 million in application fees alone for deceptively priced houses. Between 2021 and June 2023, the complaint alleges, Invitation Homes charged consumers tens of millions of dollars in junk fees as part of their monthly rental payments.

The company's response was carefully calibrated. Invitation Homes Inc. (NYSE: INVH) ("Invitation Homes" or the "Company") has reached agreement with the Federal Trade Commission (the "FTC") resolving the FTC's civil investigation into certain company business practices. As part of the resolution, Invitation Homes will pay the FTC $48 million in monetary relief, with no civil penalties. The agreement contains no admission of wrongdoing by Invitation Homes. Invitation Homes believes that its disclosures and practices are industry leading, both among its professional peers as well as the millions of smaller owners of single-family homes for lease.

Beyond the FTC settlement, broader questions about institutional ownership's impact on housing affordability persist. A December 2016 Federal Reserve Bank of Atlanta study stated Wall Street rent corporations evicted tenants significantly more than regular mom-and-pop landlords; it reported Invitation Homes evicting 15% of its renters, and the entity it would later merge with, Starwood Waypoint, 30%, and stated being African-American also increased chances of being evicted if under a company like Invitation Homes. The data on market impact reveals a more nuanced reality than either critics or defenders acknowledge. Studies GAO reviewed found that institutional investors may have contributed to increasing home prices and rents and helped stabilize neighborhoods following the financial crisis. However, information on these investors' effects on homeownership opportunities and tenants (e.g., eviction rates) was unclear because data are limited and there is no consistent definition of institutional investor.

The concentration matters more than the aggregate. GAO estimates that institutional investors own 25% of Atlanta, GA's single-family rental housing market, 21% of Jacksonville, FL's, 18% of Charlotte, NC's, and 15% of Tampa, FL's single-family rental market. In these markets, the impact is undeniable. A landmark study from Georgia Tech found that the rise in investor activity caused a 1.4 percentage point drop in homeownership rates in metro Atlanta from 2007 to 2016. That translates to 16,500 fewer households owning homes than would be expected, were it not for the influx of Wall Street cash. African Americans like Lowman have been hit the hardest. Investor purchases explain a 4.2 percentage point drop in Black homeownership during that period, the research found.

Yet the national picture is different. According to John Burns Research & Consulting, only 0.4 percent of single-family homes in the United States are owned by institutional investors with over 1,000 homes in their portfolio. This share rises to 3.8 percent of single-family homes for institutional investors owning over 100 homes. The disconnect between local impact and national statistics explains much of the debate—both sides are right, depending on the geography.

The rental rate dynamics are particularly controversial. We also find that investors raise rents at 60 percent higher rates than the average increase when first acquiring the property, and higher investor share in a neighborhood is correlated with faster rent increases for non-investor landlords. This spillover effect suggests institutional ownership doesn't just affect their own tenants—it resets market expectations for entire neighborhoods.

Looking forward, the trajectory is concerning for affordability advocates. Per MetLife Investment Management, institutional investors may control 40 percent of U.S. single-family rental homes by 2030. If this projection materializes, the current debates about market impact will seem quaint in retrospect.

The political backlash has been swift. In December 2023, Senator Merkley (D-Oregon) introduced the End Hedge Fund Control of American Homes Act, which would force large corporate owners to divest from their current holdings of single-family homes over ten years. Entities that fail to divest homes they own in excess of a 50-home cap would be taxed $50,000 for each excess home.

For Invitation Homes, the controversies represent an existential challenge to their business model. The FTC settlement may be just the beginning of regulatory scrutiny. The company that pioneered institutional single-family rentals now finds itself at the center of a national debate about housing affordability, corporate power, and the American Dream.

The paradox is striking: Invitation Homes simultaneously represents the efficiency of modern capital markets and their potential for disruption. They've professionalized an industry that needed professionalization, yet in doing so, they've become a lightning rod for concerns about housing financialization. Whether they're viewed as innovative disruptors or predatory landlords depends entirely on where you sit—in the boardroom or the rental home.

IX. Modern Era & Strategic Evolution (2018-Present)

The post-merger era began with Blackstone's strategic exit. In May 2019, Blackstone started unwinding its position, selling $1 billion worth of shares. The private equity giant sold nearly 11 percent of Invitation Homes' shares for about $1.7 billion. In all, Blackstone made about $7 billion since the home rental business went public in 2017, according to the Wall Street Journal. By November 2019, the exit was complete. Upon consummation of this offering and Blackstone's related distribution of its remaining 300,452 shares in Invitation Homes to its partners, Blackstone will no longer beneficially own shares in Invitation Homes.

The timing was impeccable. Blackstone had ridden the recovery from crisis to prosperity, transforming a distressed asset play into an institutional asset class, then exiting at peak valuations. Jonathan Gray, Blackstone's president, who led its real estate division when it launched Invitation Homes, said the biggest challenge was building the business. Mission accomplished, with a sevenfold return to show for it.

For Invitation Homes, independence meant charting its own course without a controlling shareholder. The company pivoted from pure acquisition mode to optimization and strategic growth. In October 2020, Invitation Homes created a joint venture with Rockpoint Group to purchase $1 billion in single-family homes in Dallas, Seattle, South Florida and other U.S. markets. This wasn't the frenzied buying of the post-crisis era—it was selective, strategic expansion.

The most significant strategic shift came in 2021. In July 2021, the company launched a joint venture with Atlanta, Georgia-based home construction company PulteGroup, where Pulte was projected to design and build approximately 7,500 new homes over the next five years for sale to Invitation Homes for inclusion in their single-family rental leasing portfolio. This marked a fundamental evolution—from buying existing homes to creating purpose-built rentals. No more competing with first-time buyers at auctions; instead, adding net new supply to the rental market.

Then came COVID-19, transforming everything about how Americans viewed their homes. Suddenly, homes weren't just shelter—they were offices, schools, gyms, and sanctuaries. The single-family rental model, with its extra space and private yards, was perfectly positioned for the pandemic era. Occupancy rates remained robust even as urban apartments emptied. Rent collection stayed strong despite economic uncertainty, validating the resident profile Invitation Homes had cultivated—stable, higher-income families who prioritized space and quality.

The pandemic also accelerated technology adoption. Virtual tours, digital leasing, contactless maintenance—features that had been nice-to-haves became essential. Invitation Homes' prior investments in digital infrastructure paid dividends when in-person interactions became impossible. The company could show homes, sign leases, and handle maintenance requests without physical contact, maintaining operations while competitors scrambled to adapt.

Interest rates presented a new challenge and opportunity. As the Federal Reserve pushed rates to historic lows, home prices soared, pricing out even more potential buyers. As of December 2022, the company owned about 83,000 rental homes in 16 markets. The Wall Street Journal described Invitation Homes as competing "at the high end of the rental market". This wasn't bottom-fishing anymore—it was premium positioning in a structurally undersupplied market. The financial performance tells a story of operational maturity. During 2024, Invitation Homes delivered one of the strongest financial results among public residential REITs, with Same Store NOI growth of 4.6% and AFFO per share growth of 6.7% year over year. These achievements reflect the dedication of our associates, who are committed to providing a best-in-class resident experience and achieving high resident satisfaction, as most recently demonstrated by an average length of stay of nearly 38 months and a robust 80% renewal rate in Q4 2024.

The company's Q1 2025 results continued the momentum. Same Store NOI increased 3.7% year over year on 2.5% Same Store Core Revenues growth and no growth in Same Store Core Operating Expenses. Same Store Average Occupancy was 97.2%, a slightly higher result than expected, representing a reduction of 60 basis points year over year. The ability to grow revenues while keeping expenses flat demonstrates operational leverage at scale.

The strategic evolution is most evident in the company's capital deployment. As previously announced on November 18, 2024, the Company formed a joint venture to invest in newly built homes with an expected $500 million deployment. Invitation Homes will provide various management services and earn management fees in addition to the opportunity to earn a promoted interest subject to certain performance thresholds. This asset-light strategy leverages the company's operational expertise without requiring massive capital outlays.

The company is also expanding beyond ownership. The company launched this service in January for a portfolio of 14,000 single-family homes from an undisclosed owner, CEO Dallas Tanner said on the call. Third-party management represents a new revenue stream that capitalizes on Invitation Homes' operational infrastructure without capital investment. It's the natural evolution of a platform that has proven it can manage scattered-site assets at scale.

Market positioning has shifted toward quality over quantity. The trailing twelve month revenue for Invitation Homes is $2.68B. Invitation Homes owns a portfolio of over 85,000 single-family rental homes. The company focuses on owning homes in the starter and move-up segments of the housing market with an average sale price around $350,000 and generally less than 1,800 square feet. This targeted approach focuses on the sweet spot of American housing—homes that are aspirational for renters but not luxury products.

The modern era of Invitation Homes represents the maturation of an asset class. What began as an opportunistic bet on distressed assets has evolved into a sophisticated operating platform generating predictable, growing cash flows. The company has weathered regulatory scrutiny, navigated a pandemic, and emerged as a permanent fixture in American housing. Whether that permanence is beneficial or problematic depends on your perspective, but its reality is undeniable.

X. Playbook: Business & Investing Lessons

The Invitation Homes story isn't just about real estate—it's a masterclass in how institutional capital transforms fragmented industries. The playbook they wrote has implications far beyond housing.

Lesson 1: Crisis Creates Categories The 2008 financial crisis didn't just create distressed assets—it created an entirely new asset class. When traditional buyers disappeared and prices collapsed below replacement cost, Blackstone saw what others missed: the opportunity to institutionalize a massive but fragmented market. The lesson isn't to wait for crisis, but to recognize when structural dislocations create permanent shifts. The best opportunities often emerge when conventional wisdom says to run the other way.

Lesson 2: Technology Enables Scale in Unexpected Places Single-family rentals were considered uninvestable at scale because of operational complexity. Properties scattered across neighborhoods, each requiring individual attention, seemed antithetical to institutional ownership. But technology changed the equation. Property management software, dynamic pricing algorithms, Smart Home systems—these weren't just efficiency tools, they were the enablers that made the business model possible. The lesson: revisit "impossible" markets when technology shifts the operational dynamics.

Lesson 3: Operational Excellence Beats Asset Accumulation Invitation Homes didn't win by owning the most homes—they won by operating them better. The ProCare maintenance program, 97%+ occupancy rates, 80% renewal rates—these operational metrics drive returns more than property appreciation. In asset-heavy businesses, operational leverage often matters more than asset ownership. The company that runs assets best, not the one that owns the most, typically wins.

Lesson 4: Capital Structure Innovation Unlocks Value The creation of single-family rental securities wasn't just financial engineering—it was market creation. By securitizing rental income streams, Invitation Homes accessed cheaper capital and created liquidity for an illiquid asset class. When you can innovate on capital structure, you can often unlock value that operational improvements alone cannot achieve.

Lesson 5: Density Drives Economics The pod-based model with concentrated geographic focus wasn't accidental. Owning 5,000 homes in Atlanta is fundamentally different from owning 100 homes in 50 markets. Density enables operational efficiency, pricing power, and service quality that scattered ownership cannot match. In businesses with local service requirements, geographic concentration often trumps national footprint.

Lesson 6: Patient Capital Wins Long Games Blackstone held Invitation Homes for seven years, through the entire cycle from distress to prosperity. They didn't flip houses for quick profits; they built an institution. Patient capital that can weather cycles and invest in operational infrastructure often captures value that short-term players miss. The biggest returns often come from transforming industries, not just trading assets.

Lesson 7: Controversy Is a Moat The regulatory scrutiny and public criticism Invitation Homes faces actually protects their position. New entrants must consider not just economic returns but reputational risk and regulatory uncertainty. Controversial businesses that navigate initial criticism often enjoy less competition from traditional players. If you can handle the heat, controversial markets can offer sustainable advantages.

Lesson 8: The Platform Is Worth More Than the Assets Invitation Homes' move into third-party management reveals the ultimate lesson: the operational platform they built is more valuable than the homes they own. The ability to efficiently manage scattered-site residential assets at scale is the real competitive advantage. In the digital age, platforms that aggregate demand and supply often capture more value than asset owners.

Lesson 9: Institutionalization Is Irreversible Once an asset class becomes institutional, it rarely reverts to fragmented ownership. The operational infrastructure, capital markets access, and economies of scale create permanent advantages. Individual buyers can't compete with institutional cost of capital and operational efficiency. The lesson for investors: identify markets on the cusp of institutionalization and position accordingly.

Lesson 10: Social License Matters The FTC settlement and ongoing controversies highlight a crucial lesson: financial success without social license is unsustainable. Companies operating in essential services like housing must balance shareholder returns with stakeholder concerns. The most successful long-term investments align profit with purpose, or at least avoid egregious conflicts with social good.

The Meta-Lesson The Invitation Homes playbook ultimately demonstrates how modern capitalism works: identify inefficient markets, apply technology and capital at scale, create operational excellence, and capture value through financial engineering. Whether this creates value for society or merely extracts it remains hotly debated. But understanding the playbook is essential for anyone operating in modern markets, whether as investor, entrepreneur, or policymaker.

XI. Analysis & Bear vs. Bull Case

The investment case for Invitation Homes crystallizes around a fundamental question: Is institutionalized single-family rental a permanent fixture of American housing or a cyclical trade whose time has passed?

Bull Case: The Structural Tailwinds Are Generational

The demographics are destiny argument starts with sobering math. Millennials, despite being the largest generation in American history, have the lowest homeownership rates at comparable ages. Student debt, delayed family formation, and the flexibility demands of modern careers have fundamentally shifted housing preferences. The pandemic accelerated remote work, making location flexibility more valuable than ever. These aren't cyclical factors—they're structural shifts in how Americans approach housing.

Supply and demand dynamics overwhelmingly favor Invitation Homes. America is short approximately 4-7 million housing units, depending on the estimate. New construction focuses increasingly on build-to-rent rather than for-sale inventory. Zoning restrictions, NIMBY resistance, and construction costs make adding supply difficult. Invitation Homes isn't competing with new supply—they're benefiting from its absence. With Same Store renewal rent growth of 4.9% and near-97% occupancy, pricing power remains robust despite broader economic uncertainty.

The operational moat continues to widen. Managing 84,000 scattered-site properties efficiently requires technology infrastructure, operational expertise, and scale that new entrants cannot easily replicate. The Smart Home technology, ProCare maintenance program, and data analytics create switching costs and operational advantages that compound over time. Third-party management services demonstrate that the platform value extends beyond owned assets. This isn't just a real estate company—it's a technology-enabled operating platform with real estate assets attached.

Capital markets access provides sustainable advantages. Investment-grade credit ratings, diverse financing sources, and proven access to public markets mean Invitation Homes can weather downturns and capitalize on opportunities in ways smaller players cannot. The cost of capital advantage is permanent and widening. When the next crisis hits, Invitation Homes will be a buyer, not a seller.

Bear Case: The Political and Economic Risks Are Mounting

The regulatory backlash is just beginning. The FTC settlement represents the tip of the iceberg. Political pressure from both parties to address housing affordability makes institutional owners attractive targets. Rent control, eviction moratoriums, and ownership restrictions could fundamentally alter the business model. The End Hedge Fund Control of American Homes Act may not pass this session, but similar legislation will keep coming. Social license to operate is eroding, and political risk is rising.

Interest rate sensitivity could prove devastating. The business model was built in a zero-interest-rate world. As rates normalize, cap rates must expand, pressuring valuations. More importantly, higher mortgage rates should theoretically reduce home prices, making ownership more attractive relative to renting. The spread between owning and renting that drives Invitation Homes' business could compress or even invert. The company's leverage amplifies these risks.

Competition is intensifying from multiple directions. Build-to-rent communities offer purpose-built amenities that scattered site rentals cannot match. Traditional apartments are upgrading to compete for the same residents. Most concerning, if home prices moderate and mortgage rates stabilize, individual buyers return as competition. Invitation Homes thrived when traditional buyers were sidelined—what happens when they return?

The quality challenges are systemic, not fixable. Managing 84,000 individual properties across 16 markets is inherently more complex than managing apartment communities. Deferred maintenance, aging systems, and weather events create ongoing capital needs. The FTC settlement highlighted operational challenges that scale might exacerbate rather than solve. Resident satisfaction scores and online reviews suggest persistent quality issues that could erode pricing power over time.

Economic downturn vulnerability is underappreciated. Despite targeting affluent renters, Invitation Homes is still exposed to employment cycles. A recession that impacts professional employment would hit their resident base directly. Unlike apartments that can quickly adjust rents down, single-family rental leases are typically annual, creating rigidity during downturns. The company has never been tested by a serious recession as a public company.

The Verdict: A Mature Platform in a Growing but Challenging Market

The truth incorporates elements of both cases. Invitation Homes has successfully institutionalized an asset class and built a defensible platform. The demographic tailwinds are real, and the operational advantages are substantial. But the company also faces mounting political pressure, rising competition, and valuation questions after years of multiple expansion.

For investors, Invitation Homes represents a bet on American housing dysfunction continuing. If supply remains constrained, ownership remains unaffordable, and political responses remain ineffective, Invitation Homes will continue generating solid returns. But if any of these factors shift meaningfully—increased supply, improved affordability, or effective regulation—the investment thesis weakens considerably.

The stock trades at a premium to net asset value, suggesting markets believe the platform value exceeds the real estate value. This may be correct, but it also means investors are paying for growth and operational excellence that must be continually delivered. Any stumble in execution or shift in market dynamics could trigger multiple compression beyond what fundamental changes would suggest.

The most likely scenario is neither explosive growth nor dramatic collapse, but rather a steady evolution into a utility-like business—generating predictable but unspectacular returns, facing ongoing regulatory oversight, and serving a permanent but politically contentious role in American housing. For some investors, that stability is attractive. For others, the combination of political risk and premium valuation makes better opportunities available elsewhere.

XII. Epilogue & "What's Next"

As we stand in 2025, looking back at the thirteen-year journey from that first Phoenix purchase to today's $20+ billion real estate empire, the transformation feels both inevitable and improbable. Invitation Homes has succeeded in doing what seemed impossible: turning scattered suburban houses into an institutional asset class. But perhaps the more profound transformation isn't what happened to the houses—it's what happened to American housing itself.

The institutionalization of single-family rentals represents a fundamental shift in the American Dream. For generations, homeownership was the cornerstone of middle-class wealth building. Now, for millions of Americans, that dream is experienced through a lease agreement with a publicly-traded corporation. Whether this represents pragmatic adaptation to economic reality or troubling financialization of basic needs depends on your perspective. What's undeniable is that the shift is profound and likely permanent.

Looking forward, several trends will shape Invitation Homes' trajectory. Build-to-rent represents the next frontier. Instead of competing with individual buyers for existing homes, institutional capital is increasingly funding purpose-built rental communities. Invitation Homes' joint ventures with builders position them well for this shift, but it also means evolving from an acquisition-focused model to a development-oriented one. The skills required are different, the risks are different, and the returns profile may be different.

Technology will continue to reshape operations. Artificial intelligence for predictive maintenance, automated pricing optimization, virtual reality tours, blockchain-based lease agreements—the property management platform of 2030 will look radically different from today. Invitation Homes' scale provides the resources to invest in these technologies, but it also creates organizational inertia. Smaller, more nimble competitors might innovate faster.

The regulatory environment will only intensify. As institutional ownership grows, political pressure for intervention will mount. Rent control, tenant protections, ownership restrictions, and tax changes all remain possibilities. The industry will need to proactively address affordability concerns or face imposed solutions. Invitation Homes' response to these pressures—whether through affordable housing initiatives, resident ownership programs, or other innovations—will determine their social license to operate.

Climate change presents both risks and opportunities. The concentration in Sunbelt markets exposes the portfolio to extreme weather events, from hurricanes to droughts to extreme heat. But it also creates opportunities for retrofitting homes with sustainable technologies, potentially accessing green financing, and marketing climate-resilient housing. How Invitation Homes navigates physical climate risk and transition opportunities will impact long-term returns.

The generational wealth gap cannot be ignored. If an entire generation cannot build wealth through homeownership, the social and political implications are profound. Invitation Homes sits at the center of this tension—providing needed housing but also symbolizing the barriers to ownership. Creative solutions that align company interests with resident wealth-building could transform the narrative and the business model.

Competition will evolve in unexpected ways. The next disruption might not come from other institutional owners but from entirely new models. Blockchain-enabled fractional ownership, government-backed rent-to-own programs, cooperative housing models backed by technology platforms—the future competitors might not exist today. Invitation Homes' ability to adapt and evolve will determine whether they remain a leader or become disrupted themselves.

The human element remains paramount. Behind every lease agreement is a family making a home. Behind every maintenance request is someone's daily life. Behind every rent increase is a household budget. As Invitation Homes grows larger and more systematic, maintaining human connection becomes both harder and more important. Companies that forget the human element in pursuit of efficiency often find themselves facing backlash that no amount of operational excellence can overcome.

For investors, employees, residents, and policymakers watching this space, the Invitation Homes story offers crucial lessons about modern American capitalism. It shows how financial innovation can rapidly transform traditional industries. It demonstrates the power of operational excellence at scale. It highlights the tensions between efficiency and equity, between innovation and displacement, between private returns and public good.

The single-family rental industry that Invitation Homes pioneered is no longer an experiment—it's an established part of American housing infrastructure. The question isn't whether institutional ownership of single-family rentals will persist, but how it will evolve. Will it become a regulated utility, providing stable returns and stable housing? Will it fragment as new models emerge? Will it consolidate further into a handful of mega-platforms?

What's certain is that the story is far from over. The transformation of American housing continues, shaped by demographic shifts, technological change, and economic forces beyond any single company's control. Invitation Homes will remain a central player in this transformation, for better or worse. They've proven they can execute at scale, navigate controversy, and generate returns. Whether they can continue evolving to meet society's changing needs while satisfying shareholder demands remains the ultimate test.

The American Dream isn't dead—it's being redefined. And companies like Invitation Homes are writing that new definition, one lease at a time. Whether that new definition serves American families better than the old one remains an open question. But there's no going back to the pre-2008 world of fragmented ownership and mom-and-pop landlords. The institutionalization is complete. The implications are still unfolding.

As Dallas Tanner might say, they're "still in the earliest of innings in terms of where this industry is going to go." For a company that already owns 84,000 homes and generates $2.6 billion in revenue, that's either an exciting promise or an ominous warning, depending on where you sit. The next chapter of American housing is being written now. Invitation Homes will be one of the authors, but they won't be writing alone. The story belongs to all of us.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube