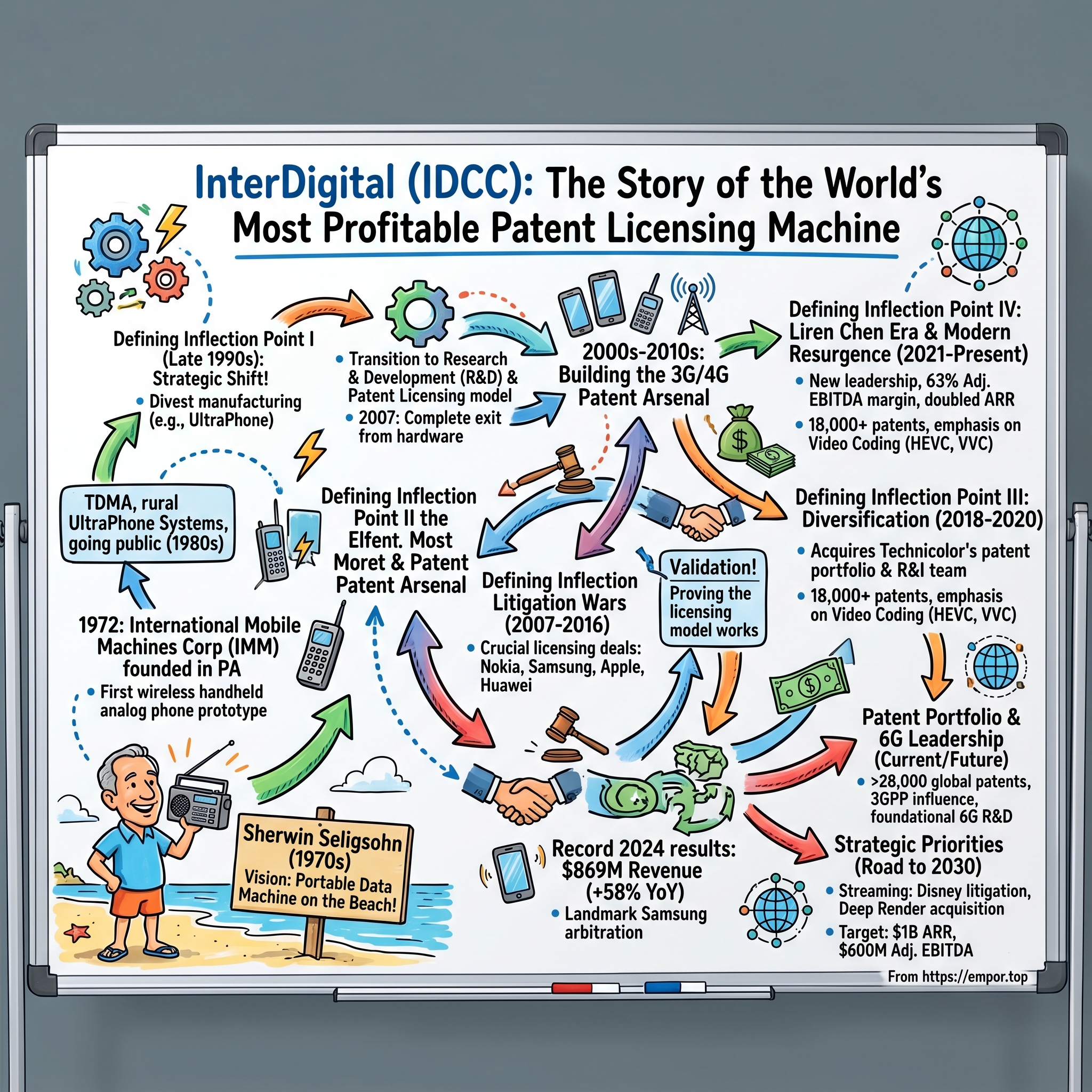

InterDigital: The Story of the World's Most Profitable Patent Licensing Machine

I. Introduction & Episode Roadmap

Picture this: you're holding a smartphone in your hand right now. Inside that slim rectangle of glass and silicon, unseen but indispensable, are thousands of patented innovations that make every call, text, and video stream possible. Somewhere in Wilmington, Delaware, a company you've probably never heard of collects a royalty every time you use that phone. Every iPhone, every Galaxy, every Xiaomi—they all pay tribute.

InterDigital, Inc. is an American technology research and development company that provides wireless and video technologies for mobile devices, networks, and services worldwide. Yet the company doesn't manufacture a single chip, produce a single handset, or run a single network. In 2024, the company achieved record revenue of $869 million, a 58% year-over-year increase, generating over $358.6 million in net income with a net margin that would make most tech CEOs weep with envy.

How did a company that doesn't make anything become one of the most profitable technology businesses on a per-employee basis? And why does every smartphone in your pocket use their inventions?

The answer lies in a fifty-three-year journey from analog radio dreams to 6G standardization leadership—a journey defined by a handful of pivotal decisions that transformed a struggling hardware company into what may be the purest intellectual property monetization machine in American business.

In 2024, InterDigital signed 14 new license agreements, with landmark deals including names like Google, Samsung, and OPPO. The company concluded its arbitration with Samsung, resulting in an 8-year license agreement worth over $1 billion—equating to $131 million per year, a 67% increase from the previous agreement. Annualized recurring revenue reached an all-time high of $588.0 million, up 49% year-over-year.

Yet InterDigital's story remains largely unknown outside the world of patent law and wireless engineering. Critics have long labeled companies like InterDigital as "patent trolls"—entities that exist solely to extract rents from productive companies through litigation. This framing fundamentally misunderstands the business. For 50 years, InterDigital has been inventing foundational wireless and video technologies that have become essential to daily life and enable the next generation of connected ecosystems.

What follows is the story of that transformation: from the beach-loving founder who dreamed of portable data machines, to the litigation wars that tested the business model, to the Technicolor acquisition that opened new frontiers, to the arrival of a new CEO who is betting the company's future on streaming video and artificial intelligence. Along the way, we'll examine what InterDigital's journey reveals about the economics of innovation, the power of standards-setting, and the art of capital allocation in knowledge-driven businesses.

II. Founding & Early Years: The Vision of Sherwin Seligsohn (1972–1980s)

Long before the first iPhone, before the Motorola flip phone became a status symbol, before anyone spoke of "mobile computing," a restless entrepreneur named Sherwin Seligsohn was lounging on the Jersey Shore, watching stock tickers scroll across a portable terminal, and asking himself: Why can't I make a phone call from here?

Born in 1935, Sherwin's immense drive for learning eclipsed conventional teaching methods, so he left high school and pursued his life's interests, including the stock market. Throughout his entire life, Sherwin loved the Jersey Shore and would regularly spend time on the beach with his young children. Sherwin's curiosity to track the financial markets and get real-time stock quotation updates, without having to leave the beach, sparked the idea of a portable data machine.

That curiosity would lead to something far more consequential than beach-side stock watching. He worked on the idea for three years and in 1971 presented a prototype of the world's first wireless handheld analog telephone. In 1972 he launched a company to exploit the idea, incorporating International Mobile Machines Corporation (IMM).

His pursuit and passion for wireless technology led Sherwin to form his first multi-billion dollar company in 1972, International Mobile Machines Corporation (IMM), now known as InterDigital, Inc. The company was headquartered in King of Prussia, Pennsylvania, a suburb of Philadelphia, in what was then the nascent heart of American telecommunications innovation.

The company's first public innovation was a portable analog radio system in the 450 MHz band, including a wireless handheld analog telephone capable of connecting to a public network. This was no minor achievement. In 1972, the idea of a truly portable telephone seemed like science fiction to most Americans. Mobile phones, to the extent they existed, were bulky affairs mounted in car trunks, not devices you could carry in your pocket.

The company staged a demonstration that consciously echoed telecommunications history. During the U.S. bicentennial celebrations in Philadelphia in 1976, IMM demonstrated its wireless telephone in Fairmount Park—the same place where Alexander Graham Bell had made his first demonstration of the telephone a century earlier. Seligsohn understood the power of symbolism. He was positioning his company as the inheritor of Bell's revolutionary vision, updated for the wireless age.

The company contributed foundational innovations to Time Division Multiple Access (TDMA) systems in the 1970s and 1980s, enabling the transition from analog to digital cellular networks for 2G deployments. As cellular technology emerged, IMM engineers turned to TDMA methods to create wireless cell phone systems that could carry more calls over the same spectrum—a crucial efficiency that would define the architecture of early mobile networks.

In 1981, IMM went public, making an initial offering of stock. Over the next five years the company made a total of three offerings, raising $32 million. For a company with revenues that remained modest, this was a significant capital base that would fund years of research.

But here is where Seligsohn made a decision that, in retrospect, defined the company's entire future trajectory. The company opted not to become a cell phone manufacturer. Rather, it would patent its cellular hardware and software technology and license those patents to other companies interested in making handsets. IMM began filing patents around the world, "in places that during the '80s, a rational person might not have filed." These efforts would pay off years later.

Consider what this meant. In 1981, cellular telephony was still a theoretical market. The first commercial cellular network in the United States wouldn't launch until 1983. No one knew which countries would adopt cellular technology, or which specific technical standards would prevail. Yet IMM was filing patents in jurisdictions across Europe and Asia—a forward-looking (some would say speculative) bet on the global adoption of mobile communications.

Despite all of IMM's promise, whether it be its cellular technology or the UltraPhone system, the company posted modest revenues and a string of losses throughout the 1980s. Although sales of the UltraPhone system grew steadily from 1987 to 1992, so too did IMM's losses. In 1991, for instance, IMM recorded revenues of $33.6 million and a loss of $7.7 million. A year later revenues improved to $39.7 million, yet the company lost nearly $23 million.

In 1990, Sherwin stepped down as Chairman of IMM and began to look for his next venture. He would go on to found Universal Display Corporation in 1994, becoming a pioneer in OLED technology—yet another instance of his prescient sense for transformative technologies. Sherwin Seligsohn passed away on December 3, 2022. The entire UDC community mourns the loss of Sherwin, an esteemed visionary, leader and friend. With an exceptional intellect and fervent curiosity, Sherwin leaves an indelible mark on the display and wireless industries.

But the company he founded was just getting started. The patent portfolio he had begun assembling was about to become extraordinarily valuable. The mobile revolution Seligsohn envisioned was arriving—and InterDigital owned pieces of its fundamental infrastructure.

III. The UltraPhone Era & Building the Patent Arsenal (1980s–1990s)

While IMM worked on cellular technology and filed patents through the 1980s, it continued pursuing Seligsohn's original rural radio-telephone concept, which had evolved into the digital UltraPhone system. The first UltraPhone System was installed in the mountainous area of Glendo, Wyoming, in 1986, purchased by Mountain Bell, a subsidiary of US West Inc. The system was set up to serve ten houses at a cost of $100,000. If copper wired had been used, the cost would have been an estimated $40,000 per house. By the end of 1988 the UltraPhone system was operating in ten communities in North America, including Kodiak, Alaska.

The economics told a compelling story: wireless technology could connect communities where wired infrastructure was prohibitively expensive. The remote mountain towns and Alaskan outposts served by UltraPhone were proof points for a broader thesis about wireless connectivity.

Yet the company struggled to scale. In 1981 the business was sold off when IMM decided to concentrate its efforts on the portable digital telephone. The tension between hardware operations and intellectual property development was already becoming apparent.

The mid-1990s brought new momentum through strategic partnerships. In 1994, InterDigital established a marketing and technology alliance with German electronics giant Siemens AG. In 1996, it entered into an alliance with Korea's Samsung Electronics Co. Ltd. Another technology partner was found in the French electronics firm Alcatel. These weren't casual relationships—they represented the major telecommunications equipment makers of the era, companies that were building the infrastructure for the mobile future.

InterDigital received both cash and engineering help from its partners, focusing on applying wideband CDMA technology to fixed wireless systems. During this period, from 1994 to 1999, the partners did not see much of a need, hence market, for mobile broadband technology. The internet was still a novelty for most consumers; the idea of streaming video on a phone seemed decades away.

The name change to InterDigital Communications Corp. came in this period, along with an alliance with Nokia—a company that would later become both a critical licensee and litigation adversary.

Founded in 1972, InterDigital is listed on the Nasdaq and is included in the S&P 600 index. The company began trading on the NASDAQ stock exchange under the ticker symbol IDCC on April 26, 2000—just weeks after the dot-com bubble began its spectacular collapse. For a company whose fortunes were tied to the growth of mobile communications, the timing was terrible for market sentiment, but the underlying business case was only getting stronger.

The patents filed in the 1980s, in those jurisdictions "a rational person might not have filed," were now maturing into a formidable portfolio. As 2G cellular networks rolled out across Europe and Asia, as handset manufacturers proliferated, as the mobile phone became a mass-market consumer product, InterDigital's intellectual property became increasingly valuable. The question was whether the company could monetize that value.

IV. The Great Pivot: From Hardware to Pure IP (Late 1990s–2007)

The First Defining Inflection Point

Every great business has moments when its leaders choose a path that fundamentally alters its trajectory. For InterDigital, that moment came in the late 1990s with a decision that remains controversial to this day: the complete exit from manufacturing.

The company underwent significant changes, moving from hardware to intellectual property. The most defining moment was the strategic decision in the late 1990s to divest manufacturing operations (like its UltraPhone product line) and concentrate solely on research, development, and the licensing of its patented technologies.

It wasn't always the R&D and licensing powerhouse we see today; its roots are in manufacturing. Understanding this transformation is essential to understanding InterDigital's current business model—and its vulnerabilities.

In the early 2000s, InterDigital transitioned from manufacturing chips and hardware to a pure research and development (R&D) and licensing model, beginning with the commercialization of its 3G technologies through patent licensing agreements. This strategic shift culminated in 2007 when the company fully exited hardware production, focusing instead on IP monetization.

A key technological milestone came in 2007 with the launch of the SlimChip, InterDigital's first High-Speed Packet Access (HSPA) chipset family, which delivered high-performance baseband processing and broadband modem capabilities for 3G mobile devices. But this was to be the company's last major hardware product. The SlimChip represented the culmination of InterDigital's chipset expertise—and the end of that chapter.

Why abandon hardware? The answer lies in the brutal economics of the semiconductor industry. Chipmaking requires massive capital investments, constant process node upgrades, and the ability to achieve enormous scale. By 2007, the mobile chipset market was dominated by Qualcomm, MediaTek, and a handful of other giants who could amortize billions in R&D across hundreds of millions of units. For InterDigital, competing in hardware meant fighting a war of attrition it could not win.

But patent licensing? That was a different game entirely. The marginal cost of licensing an existing patent is essentially zero. Once the R&D is done and the patents are granted, every new licensee drops almost entirely to the bottom line. For a company with decades of accumulated intellectual property in foundational wireless technologies, the economics were compelling.

Bill Merritt, who became CEO in 2005, navigated this transition. He served as President of InterDigital Technology Corporation from July 2001 to January 2008. He has led the building of InterDigital's successful licensing program and its strong intellectual property portfolio of important contributions to the wireless market. Mr. Merritt served as General Patent Counsel of InterDigital Inc., from July 2001 to May 2005 and also served as President of ITC since July 2001. Mr. Merritt served as an Executive Vice President of InterDigital Inc. from September 1999 to January 2004.

Merritt's background as a patent attorney was no coincidence. Leading a licensing company required deep expertise in intellectual property law, the ability to navigate complex multi-party negotiations, and the stomach for prolonged litigation when negotiations failed. InterDigital was becoming, in essence, a law firm with an engineering department attached.

The transition wasn't without risk. Critics—then and now—questioned whether a company without products could truly be considered an "innovator" at all. The term "patent troll" became common in the mid-2000s, typically applied to shell companies that acquired patents solely to extract licensing fees. InterDigital insisted it was different: it employed hundreds of engineers conducting original research that contributed to global standards. But the line between "legitimate IP licensor" and "troll" remained a matter of intense debate.

For investors, the pivot created a unique financial profile. Companies without significant device businesses, including Qualcomm and InterDigital, have no such overriding need to barter their intellectual property. Instead, they are focused on licensing cellular and smartphone patents for cash, upon which their technology developments crucially depend. SEP licensors do the costly technology developments that make new generations of standards including 3G, 4G and 5G openly available to all OEMs.

The asset-light, IP-heavy model was in place. Now it needed to be proven in the marketplace—and if necessary, in court.

V. The Litigation Wars & Licensing Breakthrough (2007–2016)

The Second Defining Inflection Point: Proving the Model Works

The patent licensing business has a fundamental challenge: convincing companies to pay for something intangible. A licensee must believe either that the patents are genuinely valuable to their products, or that the cost of refusing to license exceeds the cost of paying. InterDigital's business model depended on being able to credibly demonstrate both.

The Nokia wars illustrated the dynamic. Months earlier, InterDigital had filed a complaint with the ITC against Samsung Electronics Co., Ltd., and two of its affiliates, making similar allegations, also prompting an ITC investigation. In October 2007, in response to a motion by Nokia, the ITC consolidated its investigations involving Nokia and Samsung. In December 2007, Nokia moved to stay the consolidated investigation as to Nokia on the ground that, pursuant to a 1999 agreement between Nokia and InterDigital, the two entities were required to arbitrate the dispute. In January 2008, the ITC denied Nokia's motion for a stay.

The procedural maneuvering was complex, but the stakes were clear. Nokia was arguing that a 1999 agreement required arbitration rather than ITC litigation; InterDigital was pursuing every available legal venue to maximize pressure. InterDigital filed a complaint with the Commission in 2007 asserting that Nokia had violated section 337 of the Tariff Act of 1930, 19 U.S.C. § 1337, by importing Wideband CDMA handsets that infringed the '966 and '847 patents. The case was assigned to an administrative law judge who conducted an evidentiary hearing and ultimately ruled in Nokia's favor, finding that InterDigital had failed to prove infringement.

The initial ruling was a defeat, but InterDigital appealed. InterDigital Communications, LLC appeals from an order of the International Trade Commission finding that InterDigital's patents were not infringed by Nokia. We hold that the Commission erred in construing certain critical claim terms in both patents. We therefore reverse the Commission's order finding no infringement and remand this case to the Commission for further proceedings.

This whipsawing between victories and defeats characterized InterDigital's litigation strategy. Each case consumed years and tens of millions in legal fees, with uncertain outcomes. But the company was building a track record—and perhaps more importantly, signaling to the market that it would fight.

Samsung presented a different scenario. Another high-profile SEP case settled with InterDigital announcing that it reached a licensing deal with Samsung. Similar to InterDigital's recent settlement with Huawei, the Samsung settlement brings to a close ongoing litigation in Delaware's District Court and before the ITC involving InterDigital's assertion of 3G/4G cellular standard-essential patents. Having settled with Samsung and Huawei, InterDigital continues to litigate the FRAND issues raised by these patents with Nokia and ZTE. InterDigital initiated this round of SEP litigation against Samsung, Nokia, and ZTE in January 2013, first filing suit in the District of Delaware and then initiating a corresponding ITC action against the phone manufacturers in February 2013.

The accused Samsung devices included flagship products: the ATIV S, Galaxy Note, Galaxy Note II, Galaxy Note 10.1, Galaxy S III, and others. Samsung was not some marginal player—it was one of the largest smartphone manufacturers in the world. A successful licensing deal would validate InterDigital's entire business model.

In June 2014 Samsung and InterDigital entered into a patent license agreement that "resolves all pending litigation between the two companies." The agreement is cited at being worth just under $500 million.

This was the validation InterDigital needed. William J. Merritt, president and CEO of InterDigital said in a statement: "We are very happy to have resolved the licensing dispute with Samsung on mutually agreeable terms. This agreement with Samsung shows how our longstanding patent licensing framework and process can lead to effective, productive discussions and eventual resolution on fair and reasonable terms."

The Samsung deal demonstrated something crucial: even the largest device manufacturers would ultimately pay for InterDigital's patents. The company's persistence through years of litigation had established credibility. In 2013, Bloomberg recognized InterDigital as most profitable company in the US on a per worker basis, and named Bill Merritt among "Tech's Top Turnaround Artists."

The momentum continued. In September 2016, InterDigital signed a license agreement with Huawei, and the companies agreed to "a framework for discussions regarding joint research and development efforts." In December 2016, Apple and InterDigital entered into a multi-year license agreement.

With Apple, Samsung, and Huawei under license, InterDigital had established relationships with three of the world's largest smartphone manufacturers. The licensing model was working.

VI. The Technicolor Transformation & Video Expansion (2018–2020)

The Third Defining Inflection Point: Diversification Beyond Wireless

By 2018, InterDigital had proven it could extract value from its wireless patent portfolio. But the company faced a strategic challenge: how do you grow when your primary market—smartphone licensing—was dominated by a handful of manufacturers who were already paying? The answer came from an unexpected direction: vintage Hollywood.

William J. Merritt, President and CEO of InterDigital stated: "During the months that have followed the initial announcement, we've had the opportunity to meet and appreciate the tremendous capabilities of Technicolor's team and gain additional insight into the strength of the portfolio, which strengthens our licensing efforts in the mobile field while opening new markets for InterDigital. We've also been able to gauge the tremendous capabilities of Technicolor's Research & Innovation team, and the alignment between their research initiatives and our own in the video field." Under the terms of the agreement, InterDigital paid Technicolor $150 million in cash.

Irell & Manella LLP represented Technicolor in the July 2018 sale of its patent licensing business to InterDigital, Inc. for a total valuation of $475 million, including an upfront payment of $150 million.

The final transaction includes the acquisition by InterDigital of approximately 18,000 patents and applications, across a broad range of technologies, including approximately 3,000 worldwide video coding patents and applications.

The Technicolor acquisition wasn't just about adding more patents to the pile. The company didn't just stop at that and took another bite when they took hold of Technicolor's Research & Innovation department. Now they have more than 300 engineers and researchers of Technicolor's R&D departments who work for InterDigital. Also, with this acquisition InterDigital entered into consumer home electronics, display technology, and video technology segments.

Acquiring Technicolor's R&I arm in 2019 marked a significant expansion beyond core wireless into crucial adjacent areas like video coding, AI, and immersive technologies. This diversification aimed to broaden the scope of its licensable innovations, reflecting a forward-looking strategy aligned with evolving tech trends.

The strategic logic was compelling. As smartphones reached saturation in developed markets, growth would increasingly come from adjacent categories: smart TVs, gaming consoles, streaming devices, connected cars. All of these products consumed video content that required efficient compression—exactly what Technicolor's patents covered.

InterDigital holds a prominent position in video standards, with over 2,200 patents related to High Efficiency Video Coding (HEVC, also known as H.265) and more than 4,000 patents covering Versatile Video Coding (VVC, H.266), enabling efficient compression for high-resolution streaming and broadcasting.

The timing proved prescient. The streaming wars were about to explode. Netflix, Amazon Prime Video, Disney+, HBO Max, Apple TV+—billions of dollars were pouring into content production and distribution. All that content needed to be compressed for efficient delivery. InterDigital's expanded patent portfolio now covered foundational technologies for both transmission (wireless) and compression (video).

When the deal completed, InterDigital ended up acquiring more than 21,000 global patent assets from Technicolor, more than doubling InterDigital's current portfolio of 19,000 patent assets. This includes more than 2,500 Technicolor patents which cover video coding technologies.

The economics of the deal were also favorable. There is no revenue sharing associated with InterDigital's licensing of the new portfolio in the mobile industry, but Technicolor receives 42.5% of all future cash receipts (net of estimated operating expenses) from InterDigital's new licensing efforts in the consumer electronics field.

This structure allowed InterDigital to capture the full value of the mobile-related patents while sharing the upside in consumer electronics—a new market where its brand and relationships were less established. It was a bet that InterDigital could successfully extend its licensing model beyond smartphones.

VII. The Liren Chen Era & Modern Resurgence (2021–Present)

The Fourth Defining Inflection Point: New Leadership, New Vision

In April 2021, a new chapter began. Lawrence (Liren) Chen was appointed president and chief executive officer on April 5, 2021.

Chen's background made him uniquely suited for InterDigital's next phase. Liren Chen, 54, has served as InterDigital's President & CEO and as a director since April 5, 2021; he previously spent ~25 years at Qualcomm, most recently as SVP, Global Head of IP, and holds 28 U.S. patents and 120+ worldwide.

After earning his bachelor's degree in Automation from Tsinghua University in Beijing, where he also met his wife of 26 years, Liren came to the United States in 1994 to attend the University of Maine under full scholarship, where he earned his M.S.E.E. Liren joined Qualcomm after receiving his masters, and while working earned his J.D. degree from the University of San Diego, as well as an MBA from San Diego State University.

An engineer, a lawyer, and an MBA—Chen possessed exactly the hybrid skill set that IP licensing demands. His 25 years at Qualcomm, the industry's dominant patent licensor, provided deep experience in the strategic and tactical dimensions of SEP monetization.

With more than 25 years of experience in the technology industry, Mr. Chen has led technology, product management, IP strategy, and global ecosystem development for Qualcomm Technology Licensing. He also oversaw Qualcomm's worldwide IP portfolio.

Under Chen's leadership, InterDigital's financial performance accelerated dramatically. Business momentum accelerated through the fourth quarter of 2024 with revenue up 140% year-over-year to $253 million. 2024 was another outstanding year for the company with record revenue of $869 million, a 58% year-over-year increase, thanks to increased momentum across all of our licensing programs and new agreements with some of the world's largest device makers.

Under Chen, InterDigital delivered record 2024 results: revenue $869M (+58% YoY), Adjusted EBITDA margin 63%, GAAP EPS $12.07 and non-GAAP EPS $14.97; 2024 TSR was 81.1% and three-year annualized TSR 42.0%.

The Samsung smartphone arbitration represented a major milestone. An ICC tribunal ruled that U.S. tech developer InterDigital should receive US$1.05 billion in royalties from South Korea's Samsung Electronics. Late on Tuesday (July 29, 2025), InterDigital announced the conclusion of the arbitration proceedings. "The arbitration panel set the total royalties at $1.05 billion for the eight-year patent license, which commenced on January 1, 2023 and runs through December 31, 2030. Under this agreement, InterDigital will recognize approximately $131 million of recurring revenue per year, a 67% increase from the previous license agreement."

"Our agreement with Samsung is the largest license InterDigital has ever signed, worth more than $1 billion in total contract value over eight years. We have increased the mid-point of our annual revenue guidance by $110 million to $820 million and driven annualized recurring revenue to well over half a billion dollars," commented Liren Chen, President and CEO, InterDigital.

The company says roughly 85% of the smartphone market is under license and reaffirmed its target of $500 million in annualized recurring revenue from its smartphone program by 2027.

The dividend increase signaled confidence. The company announced that its Board of Directors has approved an increase in the company's quarterly cash dividend from $0.45 to $0.60 per share. The increase in the regular quarterly dividend will take effect beginning with the dividend paid in second quarter 2025.

InterDigital (Nasdaq: IDCC), a mobile, video, and AI technology R&D company, has set ambitious targets for 2030, aiming to achieve $1 billion in annual recurring revenue and $600 million in adjusted EBITDA. CEO Liren Chen highlighted the company's significant progress over the past four years, including nearly doubling revenue. Chen emphasized InterDigital's strong position for future growth, citing their world-class innovation in wireless, video, and AI, accelerating business momentum, and large addressable markets.

But the real strategic shift came in the video streaming space. The streaming industry is projected to be the same size as the smartphone industry by 2027, and we aim for $300 million in recurring revenue from streaming by 2030.

The Disney litigation crystallized this ambition. InterDigital, Inc. today announced that it has initiated litigation against The Walt Disney Company, including Disney+, Hulu and ESPN+, over their ongoing infringement of InterDigital's intellectual property. "Our video technologies enable Disney to efficiently stream content and enhance the user experience," said Josh Schmidt, Chief Legal Officer, InterDigital.

InterDigital's Chief Licensing Officer stated: "Disney's move into streaming has been one of the company's recent success stories, helping it to build a business of more than 250 million paying subscribers across brands like Disney Plus, ESPN Plus and Hulu. With the help of our innovation, Disney has created a profitable business spread across its multiple platforms and, in its most recent financial results, reported annual revenue of around $25 billion from its streaming businesses."

The German courts ruled in InterDigital's favor. InterDigital, Inc. today announced it has been awarded an injunction against Disney by a court in Germany. The Munich Regional Court ruled that InterDigital is entitled to an injunction over Disney's infringement of an InterDigital patent which enables a method for dynamically overlaying a first video stream with a second video stream comprising, for example, subtitles.

Then came a second injunction. InterDigital today announced it has been awarded another injunction against Disney by a court in Germany. The Munich Regional Court ruled that InterDigital is entitled to an injunction over Disney's infringement of an InterDigital patent related to the streaming of video content using high dynamic range (HDR) technology.

InterDigital announced on Nov 10, 2025 that it has initiated litigation against Amazon over alleged infringement of patents covering video compression and HDR picture-quality technologies. InterDigital says the asserted infringement involves Amazon devices and services including Fire TV, Kindle and Prime Video.

The acquisition strategy also evolved. InterDigital announced on Oct 30, 2025 that it has acquired AI startup Deep Render, adding the startup's team and its AI-based video coding patent portfolio to InterDigital's video assets. The deal transfers Deep Render's research and engineering talent into InterDigital's Video Lab, aims to accelerate AI-native video research.

The market has responded. InterDigital market cap as of October 2025 is $9.66B. The stock has more than quadrupled from its 2021 levels.

VIII. The Patent Portfolio & Standards-Essential Position

At the heart of InterDigital's business lies something remarkably abstract: a collection of legal rights to ideas. Understanding the nature and quality of this portfolio is essential to evaluating the company's competitive position.

InterDigital's portfolio of wireless patents and applications is among the largest in the world and its engineers have been closely involved in the development of each generation of cellular technology all the way through to current leadership in 5G.

According to the company, since 2012 it has been listed by third-party analysts within the top 3 patent holders for cellular wireless more often than any other company, with percentages ranging from 8–10% of patents deemed likely to be standards-essential.

In total, InterDigital owns more than 13,000 cellular patents and applications which relate to a 5G multi-mode device.

What makes these patents particularly valuable is their "standards-essential" status. When an industry consortium like 3GPP develops a cellular standard, it inevitably incorporates patented technologies from participating companies. These "standard-essential patents" (SEPs) cannot be designed around—any company manufacturing compliant devices must license them.

In 2022, 2023, 2024 and 2025 InterDigital has been included in the LexisNexis Innovation Momentum: The Global Top 100 report. The company's total patent count for 5G already exceeds our patent count for 4G and is expected to grow substantially with subsequent releases and continued research.

InterDigital's innovation is so fundamental that it enables multiple generations of cellular all the way through to 5G Advanced. Because many technologies are carried over from one generation to the next, our 5G inventions combine with earlier breakthroughs to give us a patent footprint on a device that builds as generations advance and devices maintain backward compatibility.

This is crucial: new devices still use older technology. A 5G phone still needs 4G fallback, which still needs 3G capabilities. InterDigital's patents from the 2000s remain relevant for devices manufactured today.

For 4G Long-Term Evolution (LTE), InterDigital's contributions included enhancements to Orthogonal Frequency-Division Multiplexing (OFDM) and Multiple-Input Multiple-Output (MIMO) techniques, optimizing spectrum use and enabling widespread high-speed internet access on mobile devices. These efforts extended into 5G, where InterDigital contributed to developments in 3GPP Releases 15 through 18.

InterDigital has deepened involvement in 5G-Advanced and 6G standardization through leadership roles in 3GPP, including contributions to Release 20, which bridges current 5G enhancements with future 6G specifications.

"We started the foundational development for 6G a few years ago," Chen explains. "Frankly, we do not know for sure. So we work on a lot of different technologies, but we're especially looking at ultra-high frequency flows called terahertz. We also look at more intelligent network architecture and the role AI might play there as well."

InterDigital's early-stage 6G patent portfolio (50+ filings) ranks among the top 10 global leaders, underscoring its technical leadership.

Beyond wireless, the video portfolio has become increasingly significant. The earlier video standards—HEVC and VVC—are essential for streaming. In video, InterDigital is one of the leading contributors to the latest video codecs, HEVC and VVC.

InterDigital's history of AI research stretches back more than 30 years including early work on the application of neural networks to image and signal processing. Today, AI expertise is based in the standalone AI Lab and also supports domain experts embedded throughout wireless and video research teams. Together they are exploring new ways to make wireless networks and advanced video technologies more efficient, reliable and sustainable. In total, the growing patent portfolio of AI-related innovations stretches to over 500 patent families.

The quality matters as much as quantity. According to analysis by LexisNexis, InterDigital's 5G portfolio ranks in the top seven of all major patent owners in the space when ranked on both quantity and quality.

IX. Business Model Deep Dive: The IP Licensing Playbook

InterDigital's business model is deceptively simple to describe and fiendishly complex to execute: invent foundational technologies, patent them, and license those patents to everyone who needs them. The devil lies in every detail.

InterDigital has been involved in mobile patent licensing for over two decades. During this period, InterDigital has negotiated hundreds of agreements involving its patents, with manufacturers of all sizes, without the need for litigation. The basis of the rates in these agreements was purely the value of the patent portfolio, not any additional products or technologies. In addition to licensing history, InterDigital has participated in arbitration and litigation proceedings that have also supported the fairness of our licensing program.

The key constraint is FRAND: Fair, Reasonable, and Non-Discriminatory. InterDigital believes that license rates for large SEP portfolios should be determined based upon the value of a portfolio as a whole, rather than looking at individual patents and assigning individual value. The entire purpose of cellular, Wi-Fi, and video coding standards is to provide manufacturers with easy access to technology that enables them to address a global market. A leading standards-based portfolio like ours includes thousands of patents and applications, and is implemented by companies that design, develop, manufacture, distribute and sell a range of products to markets around the world.

The financial dynamics are extraordinary. Once patents are granted, the marginal cost of licensing additional parties approaches zero. The company invests heavily upfront in R&D, then harvests returns over the patent life.

The majority of revenue is generated from fixed-fee patent license agreements, with a smaller portion coming from variable royalty agreements.

The "catch-up" revenue dynamic is particularly important for investors. When a company operates without a license for several years, then signs a deal, InterDigital recognizes all the accumulated royalties at once. Over the last 10 years, InterDigital has recognized approximately $1.5 billion of catch-up revenue. This has been tremendously valuable because the company used the majority of that money to fund share repurchases.

The operating expenses in Q1 2025 fell 51% to $78.7 million, while non-GAAP EBITDA surged 22% to $159.1 million, with a 76% margin.

The competitive landscape shapes this dynamic. Companies without significant device businesses, including Qualcomm and InterDigital, have no such overriding need to barter their intellectual property. Instead, they are focused on licensing cellular and smartphone patents for cash.

Major licensors Alcatel-Lucent, Ericsson, InterDigital, Nokia and Qualcomm accounted for most royalties paid, even with conservatively high estimates for other licensors.

In 2017, Ericsson said it would charge $2.50 to $5 per phone. Sisvel charges $0.50 per gadget for its 5G patent pool. Nokia wants $3.50. And Qualcomm believes it could get up to $16.25 in royalties for every 5G phone sold.

InterDigital occupies a distinctive niche: smaller than Qualcomm, but with a higher-quality patent portfolio than most pure-play licensors. The company has enough heft to be taken seriously, but not so much that it faces the antitrust scrutiny that has plagued Qualcomm.

X. Playbook: Business & Investing Lessons

Strategic Insights from InterDigital's Journey

1. The Power of Early Positioning in Standards

Seligsohn's decision to file patents globally in the 1980s—in places "a rational person might not have filed"—created decades of value. Standards-essential patents derive their power from the difficulty of designing around them. By participating in standard-setting from the earliest stages, InterDigital ensured its innovations would be baked into the technology roadmap.

2. Knowing When to Exit Hardware

The 2007 pivot from manufacturing to pure R&D/licensing transformed InterDigital's unit economics. Hardware businesses consume capital voraciously; IP licensing generates cash. The SlimChip was InterDigital's last chipset—and the decision to exit chipmaking remains the strategic move that enabled everything that followed.

3. Litigation as a Business Tool

InterDigital has demonstrated that strategic use of ITC complaints and district court actions accelerates licensing negotiations. The company's willingness to litigate—and its track record of winning key rulings—establishes credibility that makes settlement more attractive for potential licensees.

4. Diversification Timing

The Technicolor acquisition positioned InterDigital for video streaming growth before that market exploded. The $150 million upfront investment has generated access to a market that may eventually rival smartphones in licensing potential.

5. Capital Allocation Excellence

InterDigital has used catch-up revenue to fund aggressive share repurchases, reducing share count and concentrating ownership. Combined with consistent dividend growth, this creates a shareholder-friendly profile unusual among technology companies.

Competitive Analysis: Porter's Five Forces

Threat of New Entrants: LOW Building a standards-essential patent portfolio takes decades and hundreds of millions in R&D. New entrants cannot replicate InterDigital's position without similarly sustained investment.

Bargaining Power of Suppliers: LOW InterDigital's key inputs are engineering talent and legal expertise. Both are available in competitive markets.

Bargaining Power of Buyers: MODERATE Large smartphone manufacturers like Apple and Samsung have negotiating leverage, but ultimately cannot avoid licensing if they want to sell compliant devices. The rise of Chinese manufacturers (Xiaomi, OPPO) has actually expanded InterDigital's addressable market.

Threat of Substitutes: LOW Standards-essential patents cannot be designed around by definition. Alternative technologies would require rebuilding the entire global telecommunications infrastructure.

Competitive Rivalry: MODERATE Qualcomm, Ericsson, Nokia, and Huawei all compete for licensing revenue, but the market is more cooperative than zero-sum. Companies often cross-license, and patent pools like Avanci allow collective monetization.

Hamilton Helmer's 7 Powers Analysis

Process Power: InterDigital has developed deep institutional knowledge in patent prosecution, licensing negotiation, and standards-body politics—competencies that take decades to build.

Scale Economies: Not applicable in traditional sense, but portfolio scale matters. A larger, higher-quality portfolio commands better licensing terms.

Network Effects: Limited, though participation in standards bodies creates virtuous cycles of influence.

Counter-Positioning: InterDigital's pure-play IP model allows focus that vertically integrated competitors cannot match.

Switching Costs: Licensees cannot easily switch away from required SEPs.

Branding: Limited consumer relevance, but strong reputation among potential licensees and within standards bodies.

Cornered Resource: The patent portfolio itself represents an inimitable asset accumulated over 50 years.

Key Performance Indicators for Investors

1. Annualized Recurring Revenue (ARR) The single most important metric. ARR represents contracted, predictable licensing fees. Annualized recurring revenue reached an all-time high of $588.0 million, up 49% YoY. Watch for growth toward the 2030 target of $1 billion.

2. Share of Global Smartphone Shipments Under License The company says roughly 85% of the smartphone market is under license. Approaching 100% represents market saturation in the core smartphone segment.

3. Patent Grant Rate and Standards Participation Track new patent grants, especially in 5G, 5G-Advanced, and 6G. Leadership positions in 3GPP working groups signal future portfolio strength.

Material Risk Factors

Regulatory/Legal Overhangs

The DOJ's statement in the Disney antitrust case represents a favorable development. The DOJ's statement opined that patents, including standard essential patents (SEPs), do not necessarily confer market power to the patentee.

However, jurisdictional fragmentation creates ongoing uncertainty. While the Munich ruling reinforced InterDigital's FRAND compliance, it also highlights jurisdictional fragmentation: UK courts penalize holdouts, while German courts enforce injunctions. This duality creates operational and financial risks.

Revenue Concentration

Apple and Samsung represent a substantial portion of licensing revenue. While both relationships have been stable and recently renewed, any deterioration would significantly impact financial results.

Technology Transition Risk

Each generational transition (5G to 6G) creates risk that InterDigital's patent position may be stronger or weaker in the new standard. The company's 6G investments suggest awareness of this risk.

The Bull Case

InterDigital is a unique asset: a profitable, cash-generative technology company with recurring revenue, high barriers to entry, and multiple growth vectors. The smartphone licensing business is mature but still growing through emerging market manufacturers. The video streaming opportunity represents a potentially larger addressable market that is just beginning to be monetized. The 2030 targets of $1 billion ARR and $600 million adjusted EBITDA imply significant upside from current levels.

The Bear Case

Patent licensing is inherently adversarial. Relationships with licensees can deteriorate, leading to litigation that consumes management attention and creates earnings volatility. The FRAND framework constrains pricing power. Chinese manufacturers may prove more difficult to monetize than expected given geopolitical tensions. The streaming opportunity remains unproven—Disney has chosen to fight rather than settle, suggesting other streamers may take similar approaches.

Myth vs. Reality

Myth: InterDigital is a "patent troll." Reality: The company employs over 300 engineers, conducts original R&D, and has contributed foundational innovations to every generation of cellular technology from 2G through 5G-Advanced. This is fundamentally different from companies that simply acquire patents for litigation purposes.

Myth: Standards-essential patents provide unlimited pricing power. Reality: FRAND obligations and competitive pressure constrain licensing rates. The royalty yield was no more than around 5 percent in aggregate including all licensors. That percentage is the sum of the royalty yields for individual licensors.

Myth: The smartphone opportunity is exhausted. Reality: While developed markets are saturated, continued growth in emerging markets, combined with price increases in renewals, suggests runway remains.

Closing Perspective

Fifty-three years after Sherwin Seligsohn incorporated International Mobile Machines Corporation, the company he founded stands at a remarkable inflection point. The total contract value of licenses signed since 2021 now exceeds $4 billion, demonstrating strong momentum in InterDigital's IP-as-a-service business model.

The wireless technology that seemed like science fiction on the beaches of New Jersey in the 1970s has become as essential to modern life as electricity. And hidden in the protocols that make every phone call and video stream possible, InterDigital's intellectual property continues to generate returns for shareholders who have had the patience to hold.

One of the critical aspects of InterDigital's business is that it's innovating five to ten years before technologies will be implemented in consumer devices and services. For example, engineers were working on 5G almost a decade before the standard was finalized in 2018.

That same long-term mindset applies to the investment case. InterDigital is not a momentum stock or a quarterly earnings play. It is a bet on the continued importance of intellectual property in the global technology stack—and on the company's ability to maintain its position at the foundation of connected communications for decades to come.

XI. The Road to 2030: Strategic Priorities and Execution

InterDigital's management has articulated a clear vision for the remainder of the decade, anchored by three strategic pillars: maximizing the smartphone licensing opportunity, building a substantial video streaming business, and maintaining leadership in next-generation wireless standards. The path to reaching these goals comprises three distinct market segments. The growth is expected to come from three main segments: smartphones ($500+ million), CE/IoT/Auto ($200+ million), and streaming and cloud services ($300+ million).

The biggest greenfield opportunity is in streaming, where the company does not have any ARR today, but management believes they can achieve $300 million or more by 2030. That opportunity centers on getting new customers under license who are already using InterDigital's technology—essentially reaching agreements with companies that have been consuming the innovation without paying for it.

The smartphone segment remains the foundation. InterDigital is targeting $500 million ARR in smartphones by 2027. The company now licenses 8 of the top 10 smartphone vendors, representing approximately 85% of the market. New customer acquisitions include OPPO, with existing licenses to Vivo, Honor, Apple (until 2028), and Samsung (until 2030).

The consumer electronics, IoT, and automotive segments represent a substantial expansion opportunity. Management plans to double consumer electronics/IoT ARR to $200 million by 2030. The company projects a 10% or greater growth rate in connected cars. Recent licensing activity has demonstrated momentum in these adjacent categories. In October 2025, InterDigital renewed its patent license agreement with Sharp and signed a new agreement with an EV charger manufacturer. The company also renewed a multi-year, worldwide, non-exclusive, royalty-bearing license with Seiko Solutions Inc.

Based on the strength of its intellectual property and the huge markets built upon it, management believes the company is on track to grow ARR at a double-digit CAGR towards the 2030 target of $1 billion or more. Fourteen months after the September 2024 Investor Day announcement, CEO Liren Chen reported that the company has performed "really well" and is ahead of schedule.

Perhaps most notably, InterDigital has stated that no inorganic investments are needed to achieve the 2030 goals—the company believes organic growth from its existing portfolio and research capabilities can deliver the targets.

The Video Streaming Opportunity

The video streaming licensing program represents InterDigital's most ambitious expansion effort. The company's focus for the streaming programme will be the subscription video on demand and advertising video on demand sectors.

InterDigital argues that streaming services are leveraging technology that is vital for their operations without a proper licensing framework. CEO Liren Chen has emphasized: "With the consumption of video booming across smartphones, consumer electronics, and video services such as streaming, we believe that video innovation will become an even more significant driver of our growth strategy."

The Disney litigation illustrates both the opportunity and the challenges. The Walt Disney Company and InterDigital have failed to reach an amicable video streaming license agreement, resulting in claims or counterclaims against each other in California and Delaware federal courts plus other jurisdictions around the world. O'Melveny & Myers represent Disney and accuse InterDigital of antitrust violations in the global market for video compression and streaming technologies, while McKool Smith on behalf of InterDigital accuses Disney of patent infringement.

The intricacies of the case suggest that technology patents are becoming central to business strategies for companies operating in digital streaming. This case has drawn significant attention from legal experts and corporations alike, given its potential to set precedents in the streaming industry.

InterDigital continues to demonstrate its video innovation capabilities at industry events. At the International Broadcasting Convention (IBC) 2025 in Amsterdam, InterDigital demonstrated alongside MC-IF partners at the Ultra HD Forum booth, spotlighting the benefits of Versatile Video Coding (VVC) enhanced with Film Grain preservation to deliver premium, cinema-grade streaming experiences.

Government Contracts and Spectrum Research

Beyond commercial licensing, InterDigital has secured government research contracts that underscore its technical credibility. Shortly after Q3 2025, the company announced it had been awarded a contract by the National Spectrum Consortium in partnership with the U.S. Government to lead research and conduct demonstrations on how to better manage the use of spectrum in the United States by both civil and military applications.

This work aligns with InterDigital's long-term positioning in 6G development. The company maintains that its leadership positions in standards bodies mean it is "ideally positioned to lead the development of 6G ahead of the expected rollout of next-gen mobile network devices and services in 2030."

XII. Capital Allocation and Shareholder Returns

InterDigital's capital allocation philosophy reflects the unique characteristics of an IP licensing business: high cash generation, low capital requirements, and the imperative to balance investment in future innovation against returns to shareholders.

InterDigital's capital allocation priorities include maintaining a strong balance sheet, investing organically in research and IP portfolio development, pursuing strategic acquisitions, and returning excess cash to shareholders. Since 2011, the company has returned nearly $1.9 billion cumulatively to shareholders, including approximately $1.4 billion in share repurchases.

The share count has decreased by over 40% since 2011, with a 17% dividend increase implemented in September 2025. This aggressive share repurchase program has been funded substantially by catch-up revenue from newly signed licensing agreements.

Over the last 10 years, InterDigital has recognized $1.5 billion of catch-up revenue. This has been tremendously valuable because the company has used the majority of that money to fund share repurchases over that time period. Today, the company continues to have substantial catch-up opportunity remaining, which tends to be 100% gross margin.

In Q3 2025, the company generated free cash flow of $381 million, increased the quarterly dividend by 17% to $0.70 per share, and returned $53 million to shareholders, including $35 million in share repurchases.

Cash reserves amounted to approximately $1 billion as of late 2025, providing substantial flexibility for opportunistic acquisitions, accelerated shareholder returns, or weathering potential licensing disputes.

The balance sheet strength enables InterDigital to pursue litigation when necessary without existential risk. Management has emphasized that the subscription-based IP-as-a-service model offers a high level of visibility and provides a reliable source of cash flow even in the face of an uncertain economic environment, enabling continued investment in the innovation engine while driving future revenue growth.

XIII. Competitive Landscape and Industry Positioning

InterDigital operates in a distinctive competitive environment. Unlike most technology companies that compete for customers through product differentiation, InterDigital's "customers" are companies that must license its patents to legally sell compliant devices. The competitive dynamics involve both other patent licensors and the collective negotiating power of device manufacturers.

The major patent licensors in cellular technology include Qualcomm, Ericsson, Nokia, and Huawei. Each has different strategies and constraints. Qualcomm operates the largest licensing business but faces ongoing antitrust scrutiny. Ericsson and Nokia balance licensing revenue against network equipment sales relationships with the same companies they license patents to. Huawei's licensing program operates under geopolitical constraints that limit its market access.

InterDigital occupies a distinctive position: large enough to command respect, focused enough to avoid the conflicts that vertically integrated competitors face, and nimble enough to pursue opportunities in emerging segments like video streaming.

The video licensing landscape adds new competitive dynamics. Multiple patent pools exist for HEVC and VVC, including Via Licensing, MPEG LA, and Access Advance. InterDigital has chosen to license its video patents directly rather than through pools, preserving pricing flexibility while requiring greater enforcement capabilities.

Nokia recently hired a senior licensing director from InterDigital to lead its New Segments business, aiming to build on video streaming momentum and explore how the Finnish innovator can expand its licensing business in new and emerging technologies. This talent movement suggests that InterDigital's video licensing expertise is recognized as valuable across the industry.

XIV. Conclusion: The Next Fifty Years

Sherwin Seligsohn's beach-side vision in the 1970s has evolved into something he likely never imagined: a company that collects royalties from billions of devices worldwide without manufacturing a single one. InterDigital's fifty-three-year journey offers lessons about patience, pivots, and the enduring value of intellectual property in technology markets.

The company's defining strategic decisions—filing patents globally in the 1980s, exiting hardware manufacturing in 2007, acquiring Technicolor's IP and research capabilities in 2018-2019, and now pursuing video streaming licensing—each represented calculated bets on where value would accrue in the connected future. Not every bet worked immediately. The UltraPhone system never achieved commercial success. The SlimChip chipset represented an exit from hardware, not a triumph. The years of litigation against Nokia and Samsung consumed management attention and capital before ultimately validating the business model.

Yet the cumulative effect has been extraordinary. InterDigital has signed over $4 billion in contracts since 2021. The market capitalization has grown from less than $4 billion at the September 2024 Investor Day to nearly $10 billion today. The company generates margins that would be the envy of virtually any technology business.

The next chapter brings new challenges. The Disney litigation will test whether InterDigital can successfully extend its licensing model to video streaming—a market where the company has no existing relationships and faces determined opposition. The 6G transition will determine whether decades of investment in standards leadership can repeat in the next generation. The rise of AI in both wireless network optimization and video compression may reshape the innovation landscape in ways that favor or disadvantage InterDigital's research capabilities.

CEO Liren Chen summarized his outlook: "The future is bright. We have great technology. We have a very solid strategy. We have a fantastic team. We have built a track record of executing. Our technology has never been so valuable. It is being adopted even more broadly in different fields."

Whether that optimism proves warranted will depend on execution over the coming years. But InterDigital's history suggests that betting against a company that has survived and thrived through five decades of wireless evolution—from analog radio phones to 5G Advanced—requires substantial conviction.

The technology inside every smartphone, every streaming service, every connected car increasingly relies on innovations that trace their lineage to a laboratory in suburban Philadelphia. As long as the connected world keeps growing, InterDigital's invisible infrastructure will continue generating returns for those who understand what hides beneath the surface of the devices we can no longer live without.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube