The Hershey Company: America's Sweetest Industrial Story

I. Introduction & Episode Setup

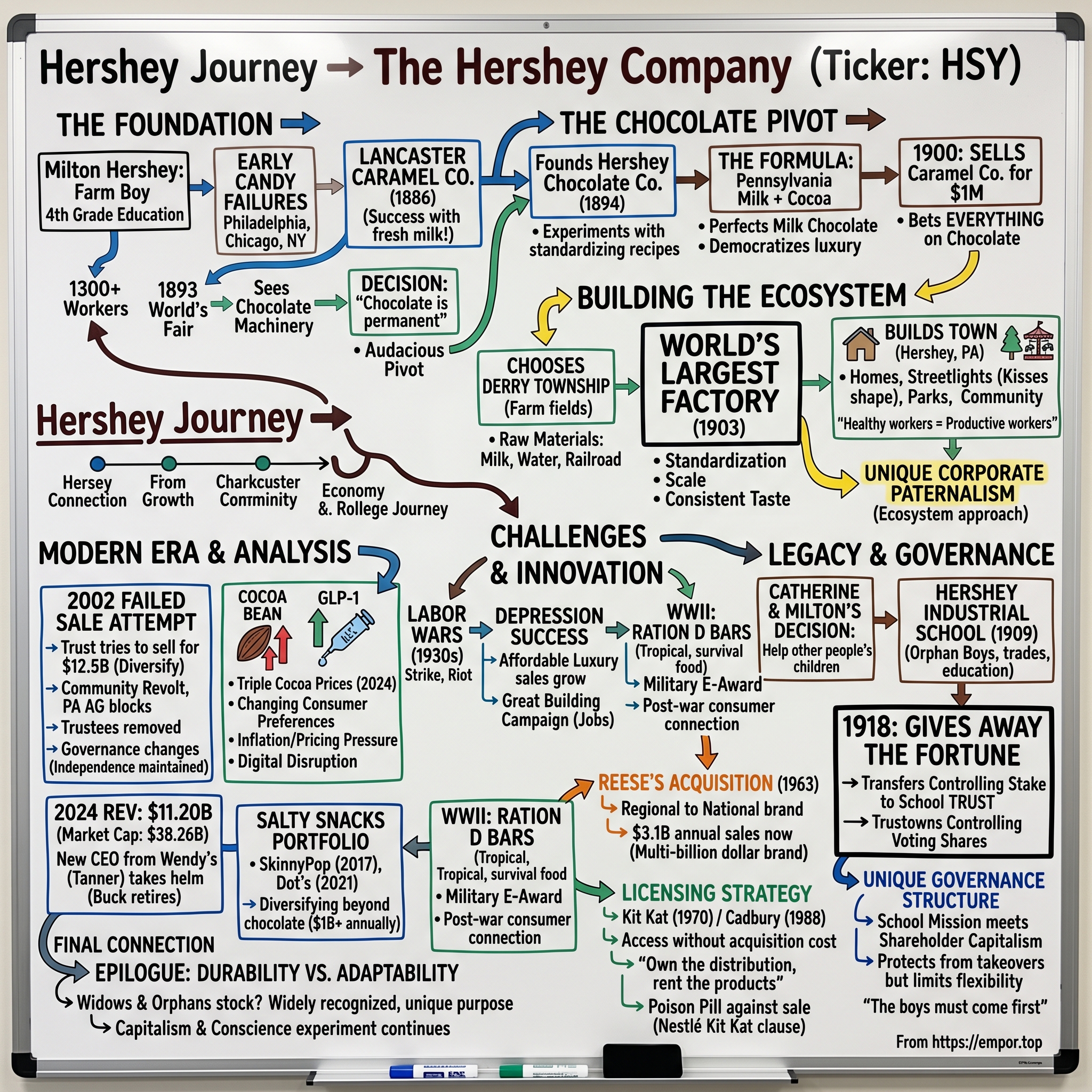

Picture this: A small Pennsylvania town where the air smells perpetually of chocolate, street lamps are shaped like Hershey's Kisses, and a Fortune 500 company exists primarily to fund a school for disadvantaged children. This isn't a utopian fantasy—it's Hershey, Pennsylvania, home to The Hershey Company, an $11.2 billion confectionery empire that defies every conventional business structure you've studied.

The question that should fascinate any student of business history: How did a man with a fourth-grade education who failed three times in the candy business before age 30 build America's most dominant chocolate company—and then give it all away in a structure so unusual that it's survived hostile takeovers, family feuds, and a century of capitalism's creative destruction?

This is the story of Milton Hershey, a Pennsylvania Dutch farm boy who saw chocolate-making machinery at the 1893 World's Fair and declared, "Caramels are a fad, but chocolate is permanent." It's about building not just a company but an entire ecosystem—factory, town, amusement park, school, and trust—that operates by its own rules. It's about Reese's Peanut Butter Cups becoming a multi-billion dollar brand through one of the shrewdest acquisitions in consumer goods history. And it's about a corporate governance structure so bizarre that in 2002, when trustees tried to sell the company for $12.5 billion, the Pennsylvania Attorney General literally removed them from their positions. The Hershey Company today trades at a market cap of $38.26 billion with 2024 revenue of $11.20 billion, making it one of America's largest confectionery companies. But here's what makes this story extraordinary: The controlling shareholder isn't a founding family or institutional investor—it's a trust that exists to fund a school for disadvantaged children. This governance structure has protected the company from hostile takeovers, constrained its strategic flexibility, and created one of the most unusual corporate control mechanisms in American capitalism.

We're about to explore how a fourth-grade dropout built a chocolate empire by democratizing what was once a luxury product, why he chose to give away his entire fortune in a way that still controls a Fortune 500 company 80 years after his death, and what happens when charitable mission meets shareholder capitalism. Along the way, we'll unpack the Reese's acquisition that created billions in value, the licensing deals that brought Kit Kat and Cadbury to American shelves without acquisition costs, and the modern challenges facing a company caught between cocoa price volatility and changing consumer preferences.

The themes we'll explore read like a business school curriculum: vertical integration before it was fashionable, the power of distribution as competitive advantage, brand building through consistency at scale, and the double-edged sword of paternalistic capitalism. This is also a story about industrial philanthropy on a scale rarely attempted—and even more rarely successful.

II. Milton Hershey's Early Failures & The Caramel Success

The autumn of 1857 in Derry Township, Pennsylvania, was unremarkable except for one thing: on September 13th, a boy was born to a Mennonite family who would revolutionize American confectionery. Milton Snavely Hershey entered the world speaking Pennsylvania Dutch, inheriting the Swiss-German immigrant values of thrift, diligence, and an almost religious devotion to hard work. His father, Henry, was a dreamer and serial failure at farming; his mother, Fanny, was the pragmatist who held the family together through constant relocations.

These moves disrupted Milton's education so thoroughly that he achieved only a fourth-grade level of formal schooling—a fact that would later make his business innovations even more remarkable. At age 14, his mother apprenticed him to Joseph Royer, a Lancaster confectioner, hoping to give her son a trade that his father's wanderlust couldn't destroy. For four years, Milton learned the art of candy-making: how to pull taffy, crystallize sugar, and most importantly, how fresh ingredients made the difference between mediocre and exceptional confections.

In 1876, at age 19, Milton borrowed $150 from his aunt and opened his first candy shop in Philadelphia, timing it to coincide with the Centennial Exposition. The location seemed perfect—thousands of visitors streaming through America's birthplace, eager to sample local treats. But Milton had learned how to make candy, not how to run a business. He worked eighteen-hour days, making candy at night and selling during the day, but couldn't manage cash flow, inventory, or the dozen other skills required for retail success. After six years of grinding poverty and mounting debts, the Philadelphia shop failed.

The pattern repeated in Chicago, where Milton thought proximity to the stockyards might provide cheaper ingredients. Wrong again. His father, ever the optimist, convinced him to try New York City in 1883. This third attempt was the most spectacular failure yet. Not only did the business collapse, but Milton returned to Lancaster literally penniless, his samples and equipment seized by creditors. At age 26, he was a three-time failure in the candy business.

But here's where the story turns. While working for a Denver confectioner between his failures, Milton had learned a secret: fresh milk added to caramel created a uniquely smooth, creamy texture that literally melted in your mouth. Nobody in Pennsylvania was making caramels this way. Despite having no money and a reputation as a serial failure, Milton convinced a local bank cashier, Harry Lebkicher, to loan him $700 to start the Lancaster Caramel Company in 1886.

This time was different. The milk caramels were an instant hit—not just locally, but with a British importer who placed a massive order after sampling them at a trade show. By 1893, just seven years after starting with borrowed money, the Lancaster Caramel Company employed over 1,300 workers across four plants in Lancaster, Mount Joy, Chicago, and Geneva, Illinois. Milton had built one of America's largest candy companies, with his "Crystal A" caramels becoming the premium brand nationwide.

The transformation was complete: the fourth-grade dropout who couldn't keep a single shop open was now, at age 36, a millionaire manufacturer shipping caramels across the Atlantic. But Milton wasn't satisfied. He sensed that caramels, despite their current popularity, were ultimately a fad. What he saw next at the 1893 World's Fair would change not just his business, but the entire American relationship with chocolate.

III. The Chocolate Pivot: Seeing the Future at the 1893 World's Fair

The World's Columbian Exposition of 1893 in Chicago was America's announcement to the world that it had arrived as an industrial power. Twenty-seven million visitors walked through the "White City," marveling at electric lights, the first Ferris wheel, and demonstrations of technology that would define the next century. Milton Hershey came to promote his caramels. He left with a vision that would transform American eating habits.

In the Machinery Hall, among the dynamos and engines, stood a Dresden company's exhibit demonstrating chocolate-making equipment from Germany. Milton watched, transfixed, as cocoa beans were roasted, ground, and transformed into smooth, dark chocolate. The machines were hypnotic—massive granite rollers crushing beans into liquor, conches kneading chocolate for hours until it achieved perfect texture, tempering equipment that gave the final product its distinctive snap and shine.

But what struck Milton wasn't just the machinery—it was the economics. In 1893, chocolate was a luxury product in America, imported from Europe and priced for the wealthy. A chocolate bar cost a day's wages for a typical worker. The market was tiny, exclusive, and in Milton's view, completely backwards. He turned to a companion and made a declaration that would sound insane to anyone who understood the chocolate business: "Caramels are a fad, but chocolate is permanent. I'm going to make chocolate."

The audacity of this statement can't be overstated. Milton was proposing to enter a market dominated by European craftsmen with centuries of expertise, using expensive equipment and rare ingredients, to make a product most Americans had never tasted. But Milton saw what others missed: chocolate didn't have to be a luxury. With the right manufacturing process, he could make it cheap enough for everyone.

In 1894, while still running his caramel empire, Milton founded the Hershey Chocolate Company as a subsidiary of Lancaster Caramel. He purchased the German equipment he'd seen at the fair and began experimenting. His early products were novelties—chocolate cigars, cigarettes, and bicycles sold alongside his caramels. But Milton was learning, iterating, searching for the formula that would crack the American market.

The breakthrough came from combining two insights. First, Americans preferred milk chocolate to the dark, bitter European varieties. Second, the Pennsylvania countryside was surrounded by dairy farms producing exceptional fresh milk. If he could figure out how to combine milk with chocolate in a shelf-stable form—a significant technical challenge given milk's tendency to spoil—he could create a uniquely American chocolate at a price point that would democratize the entire category.

By 1900, Milton had perfected his milk chocolate formula and produced the first Hershey's chocolate bars. The response was immediate and overwhelming. Orders poured in faster than his small chocolate operation could handle. Milton faced a choice: continue running his successful caramel company while chocolate remained a profitable sideline, or bet everything on his vision of mass-market chocolate.

In 1900, Milton Hershey sold the Lancaster Caramel Company for $1 million (approximately $35 million in today's dollars)—keeping only the chocolate manufacturing equipment and the rights to produce chocolate. His advisors thought he was insane. He was selling a proven, profitable business to focus on an unproven market. But Milton understood something fundamental: caramels were about craftsmanship, but chocolate could be about scale. And scale meant building not just a factory, but an entire ecosystem.

The sale provided capital, but Milton needed more than money. He needed abundant fresh milk, clean water for processing, reliable workers, and railroad access to ship products nationwide. He found all of this in an unlikely place: the cornfields of Derry Township, Pennsylvania, where he had been born 43 years earlier. The local farmers could provide milk, the Swatara Creek offered water, and the Pennsylvania Railroad ran through nearby. But there was nothing else—no houses for workers, no stores, no infrastructure.

Milton's solution was audacious: he wouldn't just build a factory. He would build an entire town.

IV. Building Hershey: The Factory, The Town, The Vision

In 1903, surveyors walking through the Derry Township cornfields must have thought Milton Hershey was delusional. He stood in the middle of nowhere, pointing at empty fields and describing streets, parks, and trolley lines. Where they saw corn and cows, Milton saw a model industrial community that would revolutionize both chocolate manufacturing and corporate paternalism. The scale of his ambition was breathtaking: build the world's largest chocolate factory in rural Pennsylvania, create an entire town around it, and use this ecosystem to produce chocolate so affordably that every American could enjoy it.

Construction began immediately on what would become a six-story factory covering more than 35 acres. Milton obsessed over every detail, from the placement of windows to maximize natural light to the flow of ingredients through the production process. The factory was designed for a single purpose: achieving unprecedented economies of scale in chocolate production. Raw cocoa beans would enter one end, and millions of identical chocolate bars would exit the other, with minimal human handling in between.

The factory opened in 1905, and its first product run demonstrated Milton's manufacturing genius. While European chocolatiers crafted small batches with careful attention to each piece, Hershey's factory produced 100,000 pounds of chocolate daily. The key innovation wasn't just scale—it was standardization. Every Hershey bar tasted exactly the same, whether purchased in Pennsylvania or California. This consistency, which some critics called bland, became the company's greatest asset. Americans learned to trust that distinctive Hershey's taste.

But Milton understood that a factory alone wasn't enough. Workers needed somewhere to live, and if he wanted the best workers, he needed to offer them something better than the grimy company towns that dotted Pennsylvania's industrial landscape. While other industrialists built cheap row houses and company stores designed to extract maximum profit from employees, Milton imagined something radically different: a real hometown.

The town plan, unveiled in 1905, was revolutionary for its time. Instead of cramped row houses, Milton commissioned diverse architectural styles—Colonial, Victorian, and Craftsman homes, each with its own yard and garden. Tree-lined streets with names like Chocolate Avenue and Cocoa Avenue (with street lamps shaped like Hershey's Kisses) gave the town a storybook quality. Every house had electricity, indoor plumbing, and central heating—luxuries many urban dwellers lacked.

The centerpiece of Milton's vision opened on May 30, 1906: a park designed for his employees and their families. What started as a simple picnic grove quickly expanded into something extraordinary. Milton added a carousel, a band shell for free concerts, a swimming pool, and eventually a roller coaster. The park wasn't just recreation—it was social engineering. Milton believed that healthy, happy workers were productive workers. Give them beauty, leisure, and dignity, and they would give you loyalty and quality work.

The Hershey Trust Company, established in 1905, served as the community's bank, but it was more than a financial institution. It provided low-interest loans for workers to buy homes, making them stakeholders in the community's success. The Hershey Department Store offered quality goods at fair prices—no company store markup. The Hershey Inn provided elegant accommodation for visitors. Each institution reinforced the same message: this wasn't exploitation disguised as paternalism. This was a genuine attempt to create a new model for industrial capitalism.

Milton's paternalism extended into every aspect of workers' lives. The company built churches (though Milton, raised Mennonite, belonged to none), schools, and a hospital. It sponsored baseball teams, bands, and social clubs. The Hershey Volunteer Fire Company protected the town; the Hershey Press published its news. By 1910, tourists were visiting just to see this chocolate-scented utopia—a publicity bonus Milton hadn't anticipated but certainly welcomed.

The economics were brilliant. By providing comprehensive services, Milton reduced worker turnover to near zero in an era when factory workers rarely lasted a year. The stable workforce became incredibly skilled at chocolate-making, further improving quality and efficiency. The town itself became a marketing tool—every visitor became a Hershey's evangelist, spreading stories of the magical place where chocolate was made.

Yet tensions simmered beneath the surface. Milton's control was absolute. He decided what businesses could operate, what entertainment was appropriate, even what architecture was acceptable. Workers joked that they needed Milton's permission to sneeze. The company's reach into personal lives felt suffocating to some. When Milton banned alcohol from the town, bootleggers did booming business just outside town limits. The paternalistic paradise had a authoritarian edge that would eventually explode into violence.

But in these early years, the model worked spectacularly. By 1915, Hershey's was the largest chocolate manufacturer in the world, producing 100 million pounds annually. The town's population had grown to 3,000, with hundreds more commuting from surrounding areas. The chocolate factory that experts said couldn't succeed in rural Pennsylvania had become the industry's dominant force. Milton had democratized chocolate, taking it from luxury to everyday treat. A Hershey bar cost a nickel—affordable for almost any American.

The success seemed to vindicate Milton's philosophy: treat workers well, and they'll build your empire. But Milton's greatest innovation was yet to come, born from personal tragedy and a desire to create a legacy that would outlast any factory or town.

V. The School, The Trust, and Giving It All Away

The mansion on the hill overlooking the chocolate factory was magnificent but empty. Milton and Catherine Hershey had everything money could buy except the one thing they wanted most: children. Years of trying, consulting specialists, and hoping had yielded only disappointment. By 1908, Catherine's health was deteriorating from a degenerative disease that would eventually claim her life. It was during one of their long evenings together, as Catherine grew weaker, that the couple made a decision that would define Milton's legacy more than any chocolate bar ever could.

"If we cannot have children of our own," Catherine said, "let us help those who have no one." On November 15, 1909, the Hershey Industrial School opened its doors to four orphaned boys. The initial vision was modest but radical for its time: provide not just basic care but a complete education, teaching both academics and practical trades to white orphan boys who would otherwise face lives of poverty and neglect.

Milton's approach to the school reflected his own abbreviated education and hard-won success. Boys would learn reading, writing, and arithmetic, but also farming, carpentry, and mechanical skills. They would live in homes with houseparents, not dormitories with wardens. They would work on the school's farms, learning self-sufficiency while providing food for their peers. This wasn't charity in the Victorian sense—it was investment in human potential.

Catherine died on March 25, 1915, leaving Milton devastated. For days, he couldn't enter the factory or speak to anyone. When he finally emerged from grief, he made a decision that stunned his advisors and family. In 1918, three years after Catherine's death, Milton transferred the bulk of his fortune—approximately $90 million (about $1.8 billion today)—to the Hershey Industrial School Trust. But he went further: he also transferred his controlling stake in the Hershey Chocolate Company.

The structure Milton created was unprecedented in American business. The Hershey Trust would own the majority of voting shares in the company, ensuring control in perpetuity. The company would exist primarily to fund the school. Profits that might have enriched shareholders would instead educate orphans. Milton had effectively turned a Fortune 500 company into a charitable endowment.

The legal documents creating this structure were masterfully crafted, anticipating challenges that wouldn't arise for decades. The trust was irrevocable—Milton couldn't change his mind. The trustees were bound by fiduciary duty to the school, not the company. They could sell the company only if it served the school's interests. The structure created an almost impregnable defense against hostile takeovers while ensuring the school's funding would continue forever.

Milton's gift transformed the school from a modest institution to one of the world's wealthiest educational charities. By 1935, enrollment had grown to 1,000 boys. The campus expanded to thousands of acres, with state-of-the-art facilities that put many colleges to shame. Each student received not just free education but clothing, healthcare, and spending money. Graduates left with both high school diplomas and practical skills, plus a network of alumni who helped each other succeed.

The school evolved with the times, though not without controversy. The original deed restricted admission to "white orphan boys," reflecting the prejudices of Milton's era. Legal challenges in the 1960s forced racial integration, and in 1977, the school began admitting girls. The name changed to Milton Hershey School in 1951, honoring its founder while modernizing its image. Today, the school serves nearly 2,200 low-income students from pre-K through 12th grade, providing everything from housing to college counseling at no cost to families.

The financial magnitude of Milton's philanthropy is staggering. The trust's assets, primarily its Hershey Company stake, are worth over $17 billion today. The school spends approximately $140,000 per student annually—more than most elite private schools charge in tuition. It provides every student with laptops, musical instruments, sports equipment, and even funding for senior trips. Graduates receive up to $95,000 for college expenses, making it one of the most generous educational institutions in the world.

But the structure creates unique tensions. The trustees must balance their duty to the school with the realities of running a public company. When cocoa prices spike or competitors gain market share, thousands of jobs and billions in shareholder value are at stake. Yet the trustees' legal obligation is to maximize value for the school, not other shareholders. This tension would explode into public view in 2002 when trustees attempted to sell the company, only to face a revolt that reached the Pennsylvania Attorney General's office.

Milton's personal involvement with the school continued until his death. He regularly ate meals with students, attended their sporting events, and knew hundreds by name. He lived modestly despite his wealth, wearing the same suits for years and driving an old Chrysler. When board members suggested he deserved a salary for running the school, he refused. When they proposed naming it after him, he resisted for years, finally relenting only when they argued it would help fundraising.

On October 13, 1945, Milton Hershey died at age 88 in the hospital he had built for his town. His funeral was simple, attended by workers, students, and townspeople who genuinely mourned the man who had shaped their lives. He was buried beside Catherine in the Hershey Cemetery, their graves marked by modest headstones that give no hint of their extraordinary legacy.

The school Milton created has now educated over 11,000 students, with alumni including executives, teachers, doctors, and at least one president of a South American country. The trust structure he designed has survived eight decades of legal challenges, economic upheavals, and social transformations. It remains one of the most successful examples of industrial philanthropy in American history, though its very success would soon create problems Milton never anticipated.

VI. Labor Wars, Depression Era, and World War II

By 1937, the chocolate-scented paradise of Hershey had developed a bitter aftertaste. The same paternalistic control that built the town now felt suffocating to a new generation of workers who had never known Milton's personal touch. The company still provided good wages and benefits, but workers resented being told where to shop, how to live, and what they could say. When organizers from the Congress of Industrial Organizations arrived promising dignity through collective bargaining, they found receptive audiences in the factory break rooms.

The tension exploded on April 2, 1937, when 600 workers staged a sit-down strike, occupying the factory floor and halting production. This wasn't just a labor dispute—it was a challenge to the entire Hershey model. Milton, now 79 and increasingly frail, watched in disbelief as workers he considered family barricaded themselves in his factory. The scenes that followed would shatter Hershey's utopian image forever.

On April 7, after five days of occupation, something snapped in the community. Over 1,000 loyal workers and dairy farmers whose livelihoods depended on the factory stormed the building. Armed with clubs, hammers, and baseball bats, they dragged strikers out, beating them in full view of newsreel cameras. The images—workers battling workers while chocolate machinery stood idle—became national news. The "Hershey Riot" destroyed the company's carefully cultivated image as a workers' paradise.

The violence shocked Milton more than any business failure ever had. He had built his entire philosophy on the belief that treating workers well would create loyalty. Now those workers were literally at each other's throats. The strike failed, but the damage was irreversible. The old paternalistic order was dying, and Milton knew it. When organizers returned in 1940, this time under American Federation of Labor leader John Shearer, Milton didn't resist. The workers voted to unionize, and collective bargaining replaced paternalistic benevolence.

But just as Hershey grappled with internal strife, external events offered redemption. The Great Depression, which had devastated American industry, barely dented Hershey's sales. Chocolate, it turned out, was an affordable luxury people wouldn't sacrifice even in hard times. A nickel candy bar provided comfort when little else could. Sales actually grew during the 1930s, making Hershey one of the Depression's few success stories.

Milton's response to the Depression showcased his philosophy at its best. While other companies laid off workers, he launched the "Great Building Campaign"—a massive construction program designed to provide jobs. Between 1933 and 1939, Hershey built the Hotel Hershey, a Mediterranean-style luxury resort; the Hershey Community Center, featuring theaters and sports facilities; the Hershey Sports Arena; and the Hershey Stadium. These weren't make-work projects but genuine investments in the community's future, all built with cash reserves while competitors struggled to survive.

The building campaign employed 600 men during the Depression's worst years, injecting money into the local economy when it was desperately needed. Milton insisted on using local materials and contractors whenever possible, spreading the wealth throughout central Pennsylvania. The Hotel Hershey alone, built for $2 million, became a symbol of optimism during America's darkest economic period. Critics called it "Milton's folly," but it would eventually become one of America's premier resorts.

Then came Pearl Harbor. Within days of the December 7, 1941 attack, the War Department contacted Hershey with an unusual request: create a chocolate bar that could survive tropical conditions, provide 600 calories, and taste bad enough that soldiers wouldn't eat it except in emergencies. The military wanted emergency rations, not treats that would disappear immediately.

The result was the Field Ration D, perhaps the most successful product nobody wanted to eat. Made with chocolate liquor, sugar, skim milk powder, cocoa butter, oat flour, and vanillin, it had the texture of a brick and tasted, according to soldiers, "like eating a chocolate-flavored vitamin." This was exactly what the military wanted. Between 1941 and 1945, Hershey produced over 3 billion ration bars, winning the Army-Navy "E" Production Award for excellence in wartime manufacturing.

The tropical chocolate bar followed, designed to withstand 120-degree heat without melting. Hershey's chemists achieved this by raising the melting point through precise manipulation of cocoa butter crystals—a technical achievement that would later influence commercial chocolate production. By 1945, Hershey was producing 24 million bars per week for the military, operating around the clock with workers pulling double shifts.

The wartime production transformed Hershey in unexpected ways. Women entered the workforce in unprecedented numbers, breaking the gender barriers Milton's generation had maintained. The company learned to operate with rationed sugar and cocoa, developing substitutes and efficiency measures that would benefit peacetime production. Most importantly, millions of American soldiers returned home with emotional connections to Hershey bars, having survived on them in foxholes from Normandy to Iwo Jima.

Milton lived just long enough to see the war end. In his final years, he still walked the factory floor, though workers noticed he moved slower and forgot names he'd known for decades. On October 13, 1945, just two months after Japan's surrender, Milton Hershey died at age 88. His last recorded words were reportedly about the school: "The boys must come first."

At his funeral, the Hershey Industrial School boys served as pallbearers, a fitting symbol for the man who had given them everything. The chocolate factory whistles blew for a full minute, and production stopped—the only time in company history. An era had ended, but the structures Milton created—the company, the trust, the school—would face their greatest tests in the decades ahead.

VII. The Reese's Acquisition & Building the Portfolio

Harry Burnett Reese started as just another Hershey employee in 1917, working on the dairy farms that supplied milk to the chocolate factory. But Reese had ambitions beyond milking cows. In his basement after work, he experimented with candy recipes, using excess Hershey chocolate he could buy at employee discounts. By 1923, Reese had saved enough to quit and start the H.B. Reese Candy Company, setting up shop just a few miles from his former employer. Milton Hershey, rather than seeing Reese as competition, became one of his biggest suppliers and supporters—a decision that would pay dividends neither man could have imagined.

Reese created dozens of products in those early years—the Johnny Bar, the Lizzie Bar, the Johnnie-and-Lizzie Bar—but nothing caught fire until he stumbled upon a simple idea in 1928: surround peanut butter with chocolate. The original Reese's Peanut Butter Cups were made by hand, with Reese's wife and children helping to wrap each one in yellow and brown paper. They sold for a penny each, marketed with the slogan "Made in Chocolate Town, So They Must Be Good."

The genius of Reese's creation wasn't just the combination of peanut butter and chocolate—others had tried that. It was the proportions, the texture, and most importantly, the use of Hershey's chocolate specifically. The slightly sour note in Hershey's milk chocolate perfectly complemented the salty-sweet peanut butter filling. Reese had created not just a candy but a flavor profile that would become one of the most beloved in American confectionery.

When H.B. Reese died suddenly in 1956, he left behind a thriving company and six sons determined to continue his legacy. But by the early 1960s, the brothers faced a dilemma. Competition was intensifying, with Mars and Nestlé growing through aggressive acquisitions. The Reeses needed either significant capital for expansion or a larger partner. They also worried about estate taxes that would eventually force a sale anyway. The obvious partner was right down the road.

On July 2, 1963, Hershey acquired H.B. Reese Candy Company in a tax-free stock-for-stock merger valued at $23.5 million. The Reese brothers received 666,316 shares of Hershey stock, making them significant shareholders while keeping the family connected to their father's creation. Analysts questioned the price—$23.5 million seemed steep for a regional candy company with one major product. Those analysts badly underestimated what Hershey could do with national distribution.

Within six years of the acquisition, Reese's Peanut Butter Cups had become Hershey's best-selling product, surpassing the original milk chocolate bar that built the company. By applying Hershey's manufacturing expertise and distribution network, production costs dropped while availability soared. Reese's went from a regional Pennsylvania treat to a national obsession. The orange packaging became as iconic as Hershey's brown wrapper. The numbers vindicate the acquisition brilliantly. Reese's are now a top-selling candy brand worldwide, with $3.1 billion in annual sales. By 1969, only six years after the Reese/Hershey merger, Reese's Peanut Butter Cups became the Hershey Company's top seller. As of September 20, 2012, Reese's was the best-selling candy brand in the United States, with sales of $2.603 billion.

But here's the truly remarkable part of the Reese's story: the value created for the original shareholders. Those 666,316 shares the Reese brothers received in 1963? Through stock splits and appreciation, they've multiplied into holdings worth over $4.4 billion today, generating approximately $87.6 million in annual dividends. The Reese family members who held onto their shares became some of Pennsylvania's wealthiest citizens, all from a basement candy operation that started with borrowed Hershey chocolate.

The success of Reese's taught Hershey's management a crucial lesson: sometimes it's better to partner than compete. This philosophy would drive the company's expansion strategy for the next half-century. Rather than developing all products internally or engaging in expensive bidding wars for companies, Hershey pioneered a hybrid approach—licensing deals that gave them access to world-class brands without the capital requirements of outright acquisition.

The model for this strategy emerged from Hershey's own experience. After seeing how Reese's flourished with access to Hershey's distribution and manufacturing expertise, executives realized they could apply the same formula to established international brands looking to crack the American market. The first major test of this theory would transform Kit Kat from a British curiosity into one of America's favorite candy bars.

VIII. The Licensing Deals: Kit Kat, Cadbury, and International Expansion

In 1969, Hershey executives faced a strategic puzzle. Rowntree's of York, the British confectionery giant, had created Kit Kat in 1935, and it had become the UK's best-selling chocolate bar. But Rowntree's American operations were failing. They lacked the distribution network, manufacturing scale, and marketing budget to compete with Hershey and Mars. Meanwhile, Hershey wanted to diversify its portfolio but faced internal resistance to developing copycat products. The solution they crafted would become a template for one of the cleverest expansion strategies in consumer goods history. The licensing agreement Hershey struck with Rowntree's in 1970 was straightforward but brilliant. Hershey would manufacture and distribute Kit Kat (and Rolo) in the United States, paying royalties to Rowntree's. The contract included a crucial poison pill: if Hershey was ever sold, the rights would revert to Rowntree's (later Nestlé). This clause would become incredibly valuable—not for what it gave Hershey, but for what it prevented others from taking.

When Nestlé acquired Rowntree's for £2.55 billion in 1988, they inherited not just Kit Kat but also the licensing agreement with Hershey. Nestlé, already a major player in the U.S. chocolate market, suddenly found their own brand licensed to their biggest American competitor. The irony was delicious: Nestlé owned Kit Kat globally but couldn't sell it in the world's largest chocolate market.

As Kit Kat is one of Hershey's top five brands in the US market, the Kit Kat licence was a key factor in Hershey's failed attempt to attract a serious buyer in 2002. When the Hershey Trust tried to sell the company that year, the Kit Kat license became a deal-breaker. Even Nestlé rejected Hershey's asking price. Any buyer would lose Kit Kat—one of Hershey's most profitable brands—the moment the deal closed. The license had transformed from a simple distribution agreement into a corporate defense mechanism.

The Kit Kat success inspired Hershey to pursue similar arrangements with Cadbury. In 1988, the same year Nestlé acquired Rowntree's, Hershey secured licenses to manufacture and distribute York Peppermint Patties, Almond Joy, and Mounds bars worldwide, plus Cadbury and Caramello products in the United States. Like the Kit Kat deal, these agreements were extendable at Hershey's option, subject to minimum sales requirements that Hershey consistently exceeded.

The economics of these licensing deals were extraordinary. Hershey gained access to proven brands without acquisition costs, integration risks, or brand development expenses. They paid royalties—typically 5-8% of sales—but kept the remaining margin. With Hershey's manufacturing efficiency and distribution dominance, these licensed brands often generated higher profits in the U.S. than in their home markets.

The strategy also solved a crucial problem: consumer variety without brand dilution. Rather than creating dozens of Hershey sub-brands that might cannibalize each other, the company could offer Kit Kat's crispy wafers, York's peppermint, and Cadbury's British-style chocolate, each with distinct brand identities. Retailers got variety, consumers got choice, and Hershey got margin without massive capital deployment.

The licensing model had another hidden benefit: competitive intelligence. Through these partnerships, Hershey gained insights into European confectionery trends, manufacturing techniques, and flavor profiles years before they reached American shores. This knowledge informed their own product development, keeping them ahead of purely domestic competitors.

By 2000, licensed brands represented nearly 20% of Hershey's confectionery sales but required virtually no capital investment beyond manufacturing equipment. The return on invested capital was astronomical—essentially infinite since Hershey invested almost nothing beyond royalty payments. Wall Street analysts called it "the best deal in consumer goods," though they underestimated just how valuable these licenses would become as consolidation swept the industry.

The model worked so well that competitors tried to copy it, but Hershey had locked up the best brands. Mars tried licensing European brands but found slim pickings. Nestlé, despite owning many premium brands, couldn't license them in the U.S. without helping competitors. Hershey had effectively used licensing to create a competitive moat as effective as any Warren Buffett had ever described.

Yet this brilliant strategy contained the seeds of its own limitation. The licenses that protected Hershey from takeover also made the company less attractive to potential acquirers. When the Trust decided to explore a sale in 2002, they would discover that their greatest strategic assets had become their biggest strategic constraints.

IX. The Trust Control & Failed Sale Attempts

The boardroom at the Milton Hershey School Trust was tense on a humid July evening in 2002. Seven trustees had just voted for something unthinkable: selling Milton Hershey's company. The offer on the table was staggering—$12.5 billion from Wrigley, backed by additional financing that might push it higher. At $89 per share, it represented a 40% premium over Hershey's stock price. For any normal company, this would be a straightforward fiduciary decision. But Hershey wasn't a normal company, and what followed would become one of the most dramatic corporate governance battles in American history.

The trustees' logic seemed unassailable. The trust's portfolio was dangerously concentrated—over 70% in Hershey stock. Any competent financial advisor would recommend diversification. The sale would generate enough cash to fund the school for centuries while eliminating market risk. The trustees had a fiduciary duty to maximize value for the school, and this deal would secure its future forever. They voted to explore the sale.

Within hours of the news leaking, Hershey, Pennsylvania, erupted. Workers marched on the factory with signs reading "Milton Hershey Must Be Rolling in His Grave." The town's residents, whose entire economy depended on the company, organized protests. Local politicians, sensing opportunity, denounced the "Wall Street betrayal" of Milton's legacy. The Pennsylvania Attorney General, Mike Fisher—conveniently running for governor—announced he would block any sale that harmed the community.

The legal battle was unprecedented. The Attorney General argued that the trust had obligations beyond maximizing financial returns—it had to consider the impact on the town Milton built. This was novel legal territory: could a charitable trust be forced to consider stakeholder interests beyond its beneficiaries? The Attorney General filed suit in Dauphin County Orphans' Court, seeking an injunction against the sale.

Former Pennsylvania Governor Dick Thornburgh, hired by the trust to negotiate with the state, found himself in an impossible position. The trust had clear legal authority to sell—Milton's deed gave trustees absolute discretion over assets. But political reality was different. The Attorney General threatened to investigate the trustees personally, question their expenses, and make their lives miserable. The community pressure was crushing; trustees received death threats and were shunned in local stores.

The business complications multiplied. When detailed negotiations began, potential buyers discovered the Kit Kat problem—the license would revert to Nestlé upon sale, removing one of Hershey's most profitable brands. The Milton Hershey School's unusual structure meant buyers would need to negotiate with both the trust and the school. Labor contracts included provisions that made post-merger restructuring expensive. The town's infrastructure was so intertwined with the company that separation costs would be enormous.

By September 2002, facing legal challenges, community opposition, and deal complexity, the trust capitulated. They withdrew the sale proposal. But the damage was done. Pennsylvania's legislature passed laws giving the Attorney General oversight of the trust's major decisions. Ten of seventeen trustees were forced to resign, replaced by members committed to keeping Hershey independent. Robert Vowler, the new chairman, declared, "The company is not for sale, period."

The failed sale revealed the fundamental tension in Hershey's structure. The trust's duty to the school suggested maximizing financial value through diversification. But the company's role in the community, the founder's vision, and political reality demanded continuity. This wasn't just about chocolate—it was about an entire ecosystem Milton had created where company, school, and town were inseparable.

The governance changes following 2002 were dramatic. New trustees were required to have ties to central Pennsylvania, ensuring community representation. The board adopted policies requiring consideration of "stakeholder interests" in major decisions. The trust committed to maintaining controlling interest in the company indefinitely. What had been implicit in Milton's vision became explicit in governance documents.

Yet the underlying tension remained. The trust still owned 80% voting control but only 30% economic interest in the company—a structure that aligned poorly with other shareholders' interests. Public shareholders owned 70% of the economic value but had minimal influence on strategic decisions. The trust's priority—stable funding for the school—sometimes conflicted with growth strategies that public market investors expected.

This manifested in conservative decision-making. While Mars aggressively acquired brands and Nestlé expanded globally, Hershey remained cautious. The trust preferred steady dividends over risky acquisitions. They valued employment stability over aggressive cost-cutting. They maintained manufacturing in high-cost Pennsylvania when competitors moved production offshore. These decisions made sense for the trust's mission but frustrated growth-oriented investors.

The 2002 crisis also revealed the license agreements' double-edged nature. While Kit Kat and other licenses provided excellent returns, they also made Hershey less attractive to acquirers. Any buyer would lose these profitable brands, reducing the company's value by billions. The licenses that protected Hershey's independence also constrained its strategic options. The company couldn't be sold without destroying significant value—exactly what Milton might have wanted.

The failed sale attempt had lasting implications. It demonstrated that Hershey existed in a unique space between public corporation and social enterprise. It showed that Milton's vision—a company serving a school and community—remained powerful enough to override pure market logic. And it proved that in Hershey, Pennsylvania, chocolate was never just about business.

X. Modern Era: Innovation, Competition, and Strategic Challenges

Michele Buck stood before investors in February 2024, delivering news that would have seemed impossible just years earlier: Hershey's prices would rise by double digits—again. In 2024 the company made a revenue of $11.20 Billion USD an increase over the revenue in the year 2023 that were of $11.16 Billion USD. But beneath the surface, the company faced the most challenging operating environment in its 130-year history. Cocoa prices had tripled, reaching $10,000 per metric ton. Consumer spending was weakening. Private label chocolates were gaining share. And a new CEO from Wendy's was about to take the helm, marking the end of Buck's transformative but turbulent tenure.

The modern Hershey operates in a radically different landscape than Milton could have imagined. The company has expanded far beyond chocolate, acquiring SkinnyPop popcorn for $1.6 billion in 2017, Pirate's Booty, and Dot's Homestyle Pretzels, building a salty snacks portfolio that now generates over $1 billion annually. The logic was sound—diversify beyond chocolate's volatility while leveraging Hershey's distribution dominance. But execution proved challenging, with the salty snacks division underperforming expectations and facing write-downs. The cocoa crisis represents an existential challenge. In early 2024, cocoa prices surged to over $11,000 per metric ton—a figure nearly three times higher than the average prices since the 1980s. For Hershey, which uses cocoa in virtually every product, this translates to hundreds of millions in additional costs. Management's response—double-digit price increases—risks breaking the social contract Milton established: chocolate as an affordable pleasure for everyone.

Innovation has become survival strategy. In 2023, the company entered the field of plant-based chocolate concocted with dairy alternatives. The 2018 $60 million expansion of the Kit Kat facility in Pennsylvania created 111 jobs but represents the challenge: massive capital investments for incremental growth in mature categories. Meanwhile, startups using fermentation and alternative proteins threaten to disrupt chocolate itself.

Digital transformation, long overdue, finally arrived with a new ERP system implementation in 2024 that caused temporary disruptions but promises long-term efficiency gains. The company is attempting to build direct-to-consumer capabilities, launching personalized products and limited editions exclusively online. But Hershey's digital presence remains weak compared to younger brands that grew up online.

The competitive landscape has intensified beyond anything Milton could have imagined. Mars, privately held and aggressive, can make long-term bets without quarterly earnings pressure. Ferrero has been acquiring aggressively, buying Ferrero Rocher, Butterfinger, and other brands. Mondelez offers global scale Hershey can't match. And premium chocolate makers like Lindt and Ghirardelli are capturing share at the high end while private label takes the low end. The leadership transition crystallizes the challenges. In July 2025, it was announced that Mark Tanner from Wendy's would replace Michelle Buck as CEO upon her retirement in August 2025. Tanner, a PepsiCo veteran who spent just 18 months at Wendy's, brings consumer packaged goods experience but inherits a company facing unprecedented headwinds. Buck, who led Hershey since 2017, had overseen the company's aggressive move into gummies and salty snacks and led some of the largest acquisitions in Hershey's history. Her departure marks the end of an era—and perhaps an acknowledgment that the company needs fresh thinking.

The sustainability challenge looms large. Hershey has committed to sourcing 100% certified sustainable cocoa by 2030, but with West African production devastated by climate change and disease, the entire chocolate industry faces an existential threat. Alternative proteins, lab-grown chocolate, and fermentation-based products aren't just novelties—they're potential industry disruptors that could make traditional chocolate as obsolete as film cameras.

Meanwhile, the trust structure that protected Hershey for decades increasingly looks like a constraint. While competitors can pivot quickly, acquire aggressively, or take risks, Hershey must consider the school, the town, and political stakeholders. The company can't easily move production offshore, can't be sold without destroying value, and can't prioritize growth over stability without risking trustee intervention.

Yet Hershey's modern challenges shouldn't obscure its remarkable resilience. The company has survived world wars, the Great Depression, family feuds, hostile takeovers, and now a cocoa crisis. Its brands remain powerful—Reese's alone generates more revenue than most entire companies. The distribution network Milton built, refined over a century, remains a formidable competitive advantage. And the trust structure, for all its constraints, ensures patient capital in an era of quarterly capitalism.

The question facing Tanner and future leaders is whether Milton's model—paternalistic capitalism, vertical integration, and charitable purpose—can survive in an era of global supply chains, activist investors, and disrupted consumer preferences. Can a company built to make chocolate affordable for everyone adapt when chocolate itself becomes a luxury? Can a trust structure designed for perpetual stability navigate markets that demand constant transformation?

XI. Playbook: Business & Investing Lessons

Milton Hershey never wrote a business book, but his century-old playbook reads like a masterclass in building enduring competitive advantages. The lessons from Hershey's history aren't just about chocolate—they're about how to construct moats so deep that even your mistakes become defensible positions. Let's decode what actually worked and why modern founders keep missing these insights.

The Ecosystem Play: When 1+1 = 10

Milton didn't just build a factory; he built an entire value chain that competitors couldn't replicate. The dairy farms provided milk, the town provided workers, the school provided purpose, and the trust provided patient capital. Each element reinforced the others. Workers stayed because their kids attended good schools. The school thrived because the company funded it. The company succeeded because workers were loyal. This is what venture capitalists now call "network effects," but Milton understood it intuitively: make every stakeholder's success dependent on your success.

Modern parallel: Amazon's AWS started as internal infrastructure, became a profit center, then became the platform everyone else built on. The lesson isn't to copy Milton's specific model—building company towns is neither practical nor desirable today. It's to think in systems. What infrastructure are you building for yourself that could become indispensable to others?

Vertical Integration: The Unfashionable Superpower

In an era when everyone outsources everything, Hershey's vertical integration looks antiquated. Yet it's precisely this "inefficiency" that saved them during cocoa crises, allowed them to maintain quality during wartime rationing, and created switching costs that keep retailers loyal. When you control the entire stack, from bean to bar to shelf, you control your destiny.

The modern mistake is confusing operational complexity with strategic vulnerability. Yes, it's easier to outsource production to contract manufacturers. But ease isn't advantage. Advantage is doing hard things that create compound benefits over time. Hershey's manufacturing expertise became a licensing advantage (Kit Kat), which became a defensive moat (unsaleable company), which became a negotiating lever (premium shelf space).

The Licensing Arbitrage: OPB (Other People's Brands)

Hershey's licensing strategy is perhaps the most underappreciated genius in consumer goods. By licensing Kit Kat, York, and Cadbury products, they captured value without capital, gained intelligence without espionage, and built variety without dilution. The return on invested capital is essentially infinite—you're investing nothing but distribution capacity you already have.

The deeper insight: Hershey recognized that distribution was their true competitive advantage, not product development. Once you have the pipes, you can flow anyone's water through them. This is why Spotify can challenge Apple, why Netflix could disrupt Hollywood, and why Shopify threatens Amazon. Own the distribution, rent the products.

The Taste Moat: When "Worse" is Better

Hershey's chocolate has a distinctive sour note from butyric acid, a result of Milton's unique milk processing. European chocolatiers mock it. Food scientists call it a defect. But to American palates, that taste IS chocolate. Hershey's didn't fix it because it had become their moat. Competitors could make "better" chocolate, but they couldn't make chocolate that tasted like childhood.

This is the same reason McDonald's fries, Coca-Cola's formula, and Kentucky Fried Chicken's recipe remain unchanged despite "improvements" being possible. Once you've trained a generation's taste buds, you own mental real estate that no amount of advertising can dislodge. The lesson: standardization at scale creates preference, even for objectively inferior products.

The Charitable Shield: Offense Through Defense

The trust structure everyone calls Hershey's weakness is actually its strength. Yes, it prevents sales, constrains strategy, and frustrates investors. But it also makes the company un-acquirable, which means management can think in decades, not quarters. While competitors wrestle with activist investors, Hershey can make patient bets on categories like salty snacks that take years to pay off.

More subtly, the charitable mission creates political protection. Try to hostile-takeover Hershey, and you're not fighting management—you're fighting the Pennsylvania congressional delegation. The school educates 2,200 disadvantaged kids; close factories, and you're on the evening news as the villain who stole Christmas. This "social license to operate" is worth billions in defensive value.

Commodity Hedging as Competitive Advantage

What most investors miss about Hershey is that it's really a commodity transformation business masquerading as a brand company. They take cocoa, sugar, and milk—all violently volatile commodities—and transform them into stable-priced consumer products. The company that hedges best wins, and Hershey has been hedging longer than anyone.

This manifests in subtle ways. Their recipes use cocoa more efficiently than competitors. Their contracts lock in prices further out. Their relationships with suppliers run deeper. When cocoa prices spike, Hershey hurts, but competitors break. It's not about avoiding commodity exposure—it's about surviving it better than others.

Distribution Density Economics

Hershey understood something about distribution that Amazon is only now learning with same-day delivery: density changes unit economics fundamentally. When you have a Hershey product in every store, vending machine, and checkout lane in a region, your cost per unit distributed plummets. This density also creates powerful psychological availability—the product is always within arm's reach when craving strikes.

This is why Hershey could profitably distribute nickel candy bars when competitors couldn't. It's why they can launch new products with guaranteed shelf space. And it's why e-commerce, despite all the hype, still struggles with impulse purchases. Physical density creates mental availability in ways digital shelves cannot replicate.

The Platform Power of Seasonal Moments

Hershey owns Halloween. Also Valentine's Day. And Easter. This isn't just about sales spikes—it's about owning cultural moments when purchase resistance disappears. During these windows, price sensitivity drops, new product trial increases, and brand impressions multiply. A Reese's Peanut Butter Cup Christmas Tree might seem silly, but it's actually brilliant platform leverage.

The strategic insight: find moments when your category becomes culturally mandatory, then dominate supply. This is why DeBeers tied diamonds to engagements, why Hallmark invented holidays, and why Apple owns back-to-school. The best businesses don't compete for market share—they compete for calendar share.

The Failure Museum as R&D Strategy

Hershey has launched thousands of failed products you've never heard of. Bar None, ReeseSticks, Kissables, Swoops—the graveyard is vast. But here's what's brilliant: each failure taught them something about consumer preference, manufacturing processes, or distribution dynamics that informed the next attempt. The failures were R&D disguised as products.

Compare this to startups that bet everything on one product, or conglomerates that acquire instead of innovate. Hershey's failure rate is high, but failure cost is low because they're using existing infrastructure. This portfolio approach to innovation—lots of small bets, few large ones—is why they could eventually succeed in salty snacks after decades of trying.

The Acquisition Integration Paradox

The Reese's acquisition worked because Hershey didn't integrate it—they just scaled it. The brand remained distinct, the recipe unchanged, even the packaging stayed orange. Hershey provided distribution and efficiency, not "synergies." This light-touch approach preserved what made Reese's special while amplifying what Hershey did well.

Most acquisitions fail because acquirers can't resist meddling. They harmonize products, integrate systems, optimize processes, and destroy value. Hershey's lesson: buy brands, not businesses. Keep what works, fix what's broken, and resist the urge to homogenize. The best acquisitions are multiplicative, not additive.

XII. Bear vs. Bull Case & Valuation Analysis

The investment case for Hershey presents one of the most fascinating dichotomies in the market: a company with unassailable brand strength facing potentially existential commodity challenges, wrapped in a governance structure that prevents both disaster and opportunity. Let's examine both sides with the clarity they deserve.

Bull Case: The Forever Company

Pricing Power in an Inflationary World Hershey has proven it can pass through double-digit price increases without breaking consumer demand. When cocoa costs triple, Hershey raises prices 15%, volumes decline 3%, and margins recover within quarters. This pricing power stems from habitual consumption, emotional attachment, and limited substitution. A Reese's fanatic won't switch to store brand when prices rise—they'll just buy fewer lattes. This inelastic demand in an inflationary environment makes Hershey a superior business to most consumer staples.

The Trust Discount is Actually a Premium The market consistently undervalues Hershey because of the trust structure, but patient investors should see this as opportunity. The trust prevents the company from being acquired, yes, but it also prevents stupid acquisitions, excessive leverage, and short-term thinking. While CPG peers destroy value chasing growth through M&A, Hershey compounds steadily. The "un-buyable" discount in the multiple is actually a quality premium in disguise.

Seasonal Dominance = Recurring Revenue Hershey's ownership of seasonal moments creates predictable revenue streams that the market underappreciates. Halloween, Valentine's, Easter—these aren't just sales spikes but cultural monopolies. Retailers can't not stock Reese's Pumpkins in October. This seasonal dominance provides pricing leverage, new product introduction windows, and marketing efficiency that appears nowhere on the balance sheet but everywhere in the returns.

International Expansion Finally Working After decades of false starts, Hershey's international business is gaining traction. India operations are approaching profitability. Mexico is growing double-digits. China distribution is expanding. The company generates only 15% of sales internationally versus 80%+ for competitors, suggesting massive runway. As emerging market consumers upgrade from local confections to branded chocolate, Hershey is positioned to capture disproportionate share.

Hidden Asset Value The Hershey Entertainment & Resorts properties—including Hersheypark, hotels, and real estate—aren't consolidated in company financials but are worth $2-3 billion conservatively. The brand licensing potential remains untapped. The distribution infrastructure could handle 2x current volume. These hidden assets provide downside protection and optionality that doesn't appear in traditional valuation metrics.

Bear Case: The Melting Point

Cocoa Reality Check The cocoa crisis isn't temporary—it's structural. Climate change is destroying West African production. Trees are aging. Diseases are spreading. Young farmers are abandoning cocoa for better-paying crops. Hershey's entire business model depends on affordable cocoa, and affordable cocoa may not exist in 10 years. Current prices of $8,000+ per ton versus historical $2,500 make the existing margin structure mathematically impossible without massive price increases that will destroy volume.

Health Conscious Apocalypse GLP-1 drugs like Ozempic are just the beginning. A generation raised on wellness influencers sees chocolate as poison, not pleasure. School nutrition standards are eliminating chocolate milk. Cities are taxing sugar. The cultural tide has turned against Hershey's core products in ways that no amount of marketing can reverse. Dark chocolate and sugar-free variants are band-aids on a bullet wound.

Distribution Disruption E-commerce penetration in confectionery remains low, but when it tips, Hershey's competitive advantage evaporates. Their power comes from controlling physical checkout lanes where impulse purchases happen. Online, infinite shelf space means infinite competition. Amazon can preference private label. Instagram can sell direct-to-consumer craft chocolate. The distribution moat that protected Hershey for a century becomes irrelevant in a digital world.

Innovation Failure Despite decades of trying, Hershey has failed to build meaningful positions outside chocolate. Salty snacks remain subscale. Protein bars flopped. Better-for-you initiatives died. The company is a one-trick pony in a world demanding portfolio diversity. Meanwhile, competitors like Mondelez have successfully pivoted to biscuits and snacks. Hershey's innovation muscle has atrophied from decades of milking legacy brands.

The Trust Trap The same structure that protects Hershey also imprisons it. The company can't be sold when industry consolidation demands scale. It can't move production to low-cost countries when competitors are. It can't take risks that might threaten school funding. It can't optimize for shareholders when the trust has different objectives. This structural disadvantage compounds over time as the industry evolves and Hershey cannot.

Valuation Reality Check

At current prices around $180/share, Hershey trades at approximately 20x forward P/E, in line with historical averages but expensive given the headwinds. The dividend yield of 3%+ provides support, but dividend growth is constrained by cocoa costs. The EV/EBITDA multiple of 14x suggests the market isn't pricing in either disaster or opportunity—it's pricing in muddle-through.

The key insight: Hershey's valuation makes sense only if you believe the cocoa crisis is temporary, pricing power remains intact, and the trust structure prevents value destruction. Break any of those assumptions, and the stock is either wildly overvalued (cocoa stays high forever) or significantly undervalued (cocoa normalizes, international works).

The Meta Question

The real question isn't whether Hershey is a good business—it clearly is. The question is whether it's a good investment at current prices given the structural challenges. The bull case requires faith that a 130-year-old company can navigate unprecedented commodity inflation, changing consumer preferences, and digital disruption while hamstrung by a governance structure designed for another era.

The bear case requires believing that everything that made Hershey great—vertical integration, distribution density, brand loyalty, seasonal dominance—becomes irrelevant in a world of expensive cocoa, healthy eating, and e-commerce.

The truth, as always, lies somewhere in between. Hershey will likely survive and even thrive, but at lower returns than history suggests. The company that made chocolate democratic may have to accept that chocolate becomes aristocratic again. The trust that protected Hershey from raiders may protect it from necessary evolution. The brands that defined American childhood may not define American adulthood.

For investors, Hershey represents a fascinating study in durability versus adaptability. It's a widows-and-orphans stock in a disruption economy. It's a value investment trading at growth multiples. It's a defensive play with offensive commodity exposure. These contradictions make Hershey impossible to categorize and therefore impossible to properly price—which might be the opportunity.

XIII. Epilogue: Legacy and Lessons

Standing in Hershey, Pennsylvania, today, you can still smell chocolate in the air when the wind blows east from the factory. The street lamps shaped like Kisses still line Chocolate Avenue. The school Milton built still educates disadvantaged children. The company he founded still makes the same chocolate bar he perfected in 1900. In an era of constant disruption, this continuity feels almost miraculous—or perhaps miraculous is exactly what it is.

Milton Hershey died believing he had failed. Despite building one of America's great companies, creating thousands of jobs, and educating tens of thousands of children, he supposedly told a nurse near the end, "I never accomplished what I set out to do." He wanted to make chocolate universal, affordable, democratic. By that measure, he succeeded beyond imagination. But he also wanted to prove that business could serve society, that capitalism could have conscience, that a company could last forever. On that score, the jury is still deliberating.

The Hershey story challenges every modern assumption about business. We're told companies must maximize shareholder value, but Hershey exists to fund a school. We're told growth requires global expansion, but Hershey stayed hyperlocal for decades. We're told innovation means disruption, but Hershey's biggest seller is a recipe unchanged since 1928. We're told founders should maintain control, but Milton gave everything away. Either Hershey is the exception that proves the rules, or the rules are wrong.

What modern founders can learn from Milton isn't his specific tactics—you can't build a company town, probably shouldn't create a controlling trust, and definitely can't replicate 1900s paternalistic capitalism. What you can learn is his systems thinking. Milton understood that businesses exist in ecosystems, that sustainable advantage comes from owning the full stack, that culture compounds faster than capital, and that purpose-driven organizations outlast profit-driven ones.

The tension between shareholder value and social mission that plagued Hershey's 2002 sale attempt isn't a bug—it's the feature. This tension forces long-term thinking, prevents reckless financialization, and ensures the company serves multiple stakeholders. In an era when private equity strips assets, activists demand buybacks, and CEOs optimize for option vesting, Hershey's structure looks less like a constraint and more like a protection.

Yet we cannot romanticize the model. The paternalistic capitalism Milton practiced was authoritarian, the racial exclusion of the school's early years was shameful, and the company's resistance to organized labor was sometimes violent. The same structure that enables long-term thinking also enables insular decision-making. The same trust that protects the company from raiders protects it from necessary change. The same culture that creates loyalty creates conformity.

The ultimate lesson from Hershey might be that there are no ultimate lessons—only tradeoffs. Every structural choice enables some strategies and prevents others. Every cultural decision attracts some people and repels others. Every business model works until it doesn't. The genius isn't in finding the perfect structure but in building something robust enough to evolve while maintaining its essence.

As Hershey faces its modern challenges—cocoa crises, changing preferences, digital disruption—the question isn't whether Milton's model will survive but whether it will adapt. Can a company built on abundance navigate scarcity? Can a brand built on indulgence embrace wellness? Can a structure built for stability enable transformation? These aren't just Hershey's questions; they're capitalism's questions.

Perhaps that's Milton's greatest legacy: building a company that forces us to confront what business is actually for. Is it to maximize returns, serve customers, support communities, or achieve some balance among all three? Hershey doesn't answer that question, but it makes avoiding it impossible. Every earnings call, every board meeting, every strategic decision requires wrestling with Milton's ghost, who asks not "what's the ROI?" but "what's the point?"

The chocolate bars rolling off the production lines in Hershey today are virtually identical to those from 1900. The recipe hasn't changed, the wrapper barely evolved, the taste exactly as Milton intended. But everything around them has transformed. The company trades on public markets Milton never imagined. The cocoa comes from supply chains he couldn't have mapped. The consumers live lives he wouldn't recognize. Yet somehow, impossibly, it still works.

This is the real Hershey miracle: not that a farm boy with a fourth-grade education built a billion-dollar company, but that he built it to last beyond any reasonable expectation. In a business world obsessed with disruption, Hershey represents duration. In an economy that celebrates exits, Hershey chose permanence. In a culture that worships founders, Hershey's founder gave it all away.

The story of Hershey isn't really about chocolate. It's about the audacious belief that business can be more than business, that companies can serve purposes beyond profit, that capitalism and conscience aren't incompatible. Milton Hershey proved these things possible, even if he never figured out how to make them easy. His company stands as a 130-year experiment in whether doing well and doing good can be the same thing.

That experiment continues today, with results still uncertain. But in a Pennsylvania town that smells like chocolate, where street lamps look like candy, where a school owns a company that makes children smile, Milton Hershey's impossible dream endures. And sometimes, perhaps, endurance is its own kind of success.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube