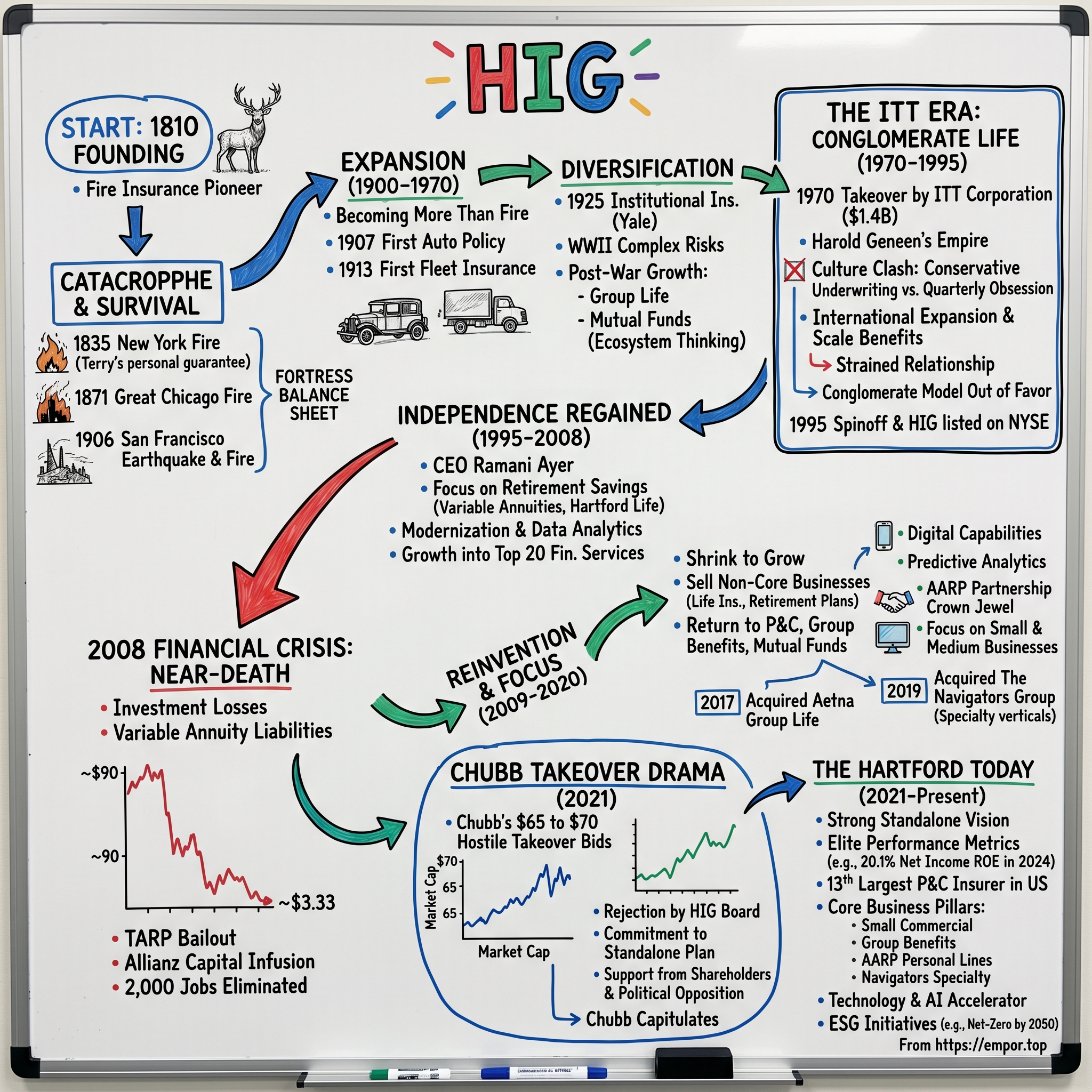

The Hartford: From 1810 Fire Insurance to Modern Financial Services Giant

I. Introduction & Episode Roadmap

Picture this: December 1835, New York City's financial district engulfed in flames, temperatures so cold that water from fire hoses freezes on contact. Insurance companies across the nation face ruin as claims pour in. In Hartford, Connecticut, a 60-year-old company president named Eliphalet Terry watches his firm's reserves evaporate. What he does next—pledging his personal fortune to honor every single claim—becomes the stuff of corporate legend and sets the DNA for a company that would survive 214 years, outlast conglomerate ownership, and reject a $25 billion hostile takeover. Today, The Hartford (NYSE: HIG) stands as a Fortune 500 company headquartered in its namesake city, with trailing twelve-month revenue of $27.25 billion and 2024 net income of $3.1 billion. But these numbers only tell part of the story. How did a fire insurance company founded by merchants with $15,000 in working capital survive 214 years, outlast ITT ownership, and reject a $25 billion takeover bid to become one of America's most resilient financial institutions?

This is a story of survival through catastrophe, strategic reinvention, and the delicate dance between independence and scale. It's about a company that learned to say no to empire builders—twice—and emerged stronger each time. Along the way, we'll uncover the business lessons hidden in two centuries of insurance underwriting, explore what it means to build a financial services fortress in the digital age, and ask the question every long-term investor needs answered: Is The Hartford's greatest chapter behind it, or still being written?

We'll journey from Hartford's founding tavern meeting in 1810 through the Great Chicago Fire, examine life inside Harold Geneen's ITT conglomerate, dissect the near-death experience of 2008, and analyze the boardroom drama when Chubb came calling with $70 per share. Buckle up—this is insurance, but it's anything but boring.

II. Founding & Early History: The Fire Insurance Pioneer (1810–1900)

The summer of 1810 was unseasonably hot in Hartford, Connecticut. Inside Sanford's Tavern, the air thick with pipe smoke and possibility, a group of local merchants gathered around rough-hewn tables. They weren't revolutionaries or inventors—just practical businessmen who understood a fundamental truth: in a nation built of wood, fire was the universal enemy, and protection from it could be worth a fortune.

With $15,000 in working capital—roughly $400,000 in today's money—they incorporated the Hartford Fire Insurance Company. The timing was prescient. America was expanding westward, cities were growing vertically with wooden structures, and the industrial revolution was about to transform everything from textile mills to shipping warehouses into tinderboxes of commercial activity. Insurance wasn't just a business; it was the lubricant that would allow American capitalism to take risks.

The company's first test of character came not in Hartford but in New York City. On December 16, 1835, temperatures plunged to negative 17 degrees Fahrenheit. A fire started in a five-story warehouse on Merchant Street, and before it was contained, it had consumed 17 blocks of Manhattan's financial district. The inferno was so intense that merchant marines dynamited buildings to create firebreaks. Insurance companies across the young nation faced immediate insolvency.

Eliphalet Terry, Hartford Fire's president, received the devastating news by horseback messenger. The claims would wipe out the company's reserves entirely. What happened next would define The Hartford's culture for the next two centuries. Terry, then 60 years old and one of Hartford's wealthiest citizens, stood before his board and made an extraordinary declaration: he would pledge his personal fortune to ensure every legitimate claim was paid in full. While competitors declared bankruptcy or negotiated partial settlements, Hartford Fire paid 100 cents on the dollar.

Word spread through the merchant networks of Boston, Philadelphia, and beyond. Here was an insurance company that would honor its obligations even if it meant the founder's personal ruin. New business flooded in. By 1840, Hartford Fire's premiums had tripled. Terry's gamble had paid off, but more importantly, it had established a reputational moat that money couldn't buy: absolute trust.

The company's next defining moment came with the Chicago Fire of October 1871. The disaster started in a barn (though probably not Mrs. O'Leary's) and burned for three days, destroying over 17,000 structures and leaving 100,000 people homeless. The Hartford faced $1.8 million in claims—an astronomical sum that would bankrupt most insurers. Once again, while competitors failed or fled, The Hartford paid every claim. The company's agents worked through the night processing paperwork by candlelight, some literally handing out cash from wagons to desperate policyholders.

But it was the 1906 San Francisco earthquake and subsequent fire that truly tested The Hartford's resilience. The earthquake struck at 5:12 AM on April 18, but it was the fires—burning for three days unchecked due to ruptured water mains—that caused 90% of the damage. The Hartford faced its largest disaster yet: $11 million in claims, equivalent to over $300 million today. Company President Richard Bissell took a train to San Francisco personally, set up a claims office in a tent, and began the methodical process of rebuilding both the city and The Hartford's West Coast presence.

Through these catastrophes, The Hartford developed what would become its competitive advantage: superior risk assessment combined with conservative reserves and an ironclad commitment to claims payment. While flashier competitors chased growth, The Hartford built a fortress balance sheet. They pioneered new underwriting techniques, sending inspectors to examine not just individual buildings but entire city blocks, mapping fire risk with scientific precision.

The company's iconic logo emerged during this period, first appearing on an 1861 policy issued to Abraham Lincoln himself for his Springfield, Illinois home—a $8,000 policy that still exists in the company archives. The logo depicts a hart (a male deer) fording a stream, a visual pun on "Hartford" but also a metaphor for navigating treacherous waters—something the company had proven repeatedly it could do.

By 1900, The Hartford had transformed from a local mutual insurance company into a national powerhouse. They had learned that in insurance, reputation is everything, that catastrophes create opportunities for those with the capital and courage to pay claims, and that conservative underwriting paired with aggressive claims payment was a paradox that actually worked. These lessons, forged in literal fire, would guide the company through its next chapter of explosive growth.

III. Expansion & Diversification: Building an Insurance Empire (1900–1970)

The twentieth century dawned with The Hartford in an enviable position: trusted, well-capitalized, and ready to ride the greatest economic expansion in human history. But President Richard Bissell, still bearing scars from San Francisco, understood that survival required evolution. "We must become more than a fire company," he told his board in 1907, "or we will become history."

The transformation began with a radical idea: automobile insurance. In 1907, when there were only 140,000 cars in all of America, The Hartford wrote its first auto liability policy. The policyholder was a Buffalo, New York manufacturer named Clarence E. Fay, and the premium was $771.75 for a year of coverage. Most insurers thought cars were a fad. The Hartford's actuaries, led by a young mathematician named Harry Williams, saw different patterns in their data. They noticed that wealthy car owners—their target market—were generally cautious, employed chauffeurs, and maintained their vehicles meticulously. This wasn't reckless speculation; it was calculated risk-taking based on superior data analysis.

By 1913, The Hartford had another breakthrough: they created the first automobile insurance policy specifically designed for commercial fleets. The Borden Milk Company needed coverage for their growing delivery truck operations, and The Hartford's underwriters crafted a novel solution—fleet pricing based on aggregate risk rather than individual vehicle assessment. This innovation opened an entirely new market segment that competitors wouldn't recognize for another decade.

The 1920s brought jazz, prosperity, and The Hartford's next strategic leap. In 1925, the company wrote the first insurance policy for an institution of higher education when Yale University—just 40 miles north—sought comprehensive coverage for its growing campus. The policy was revolutionary in scope, covering not just fire but liability, theft, and even reputational damage from student misconduct. This wasn't just a single policy; it was the birth of institutional insurance, a market The Hartford would dominate for the next century.

During the Great Depression, while competitors retrenched, The Hartford's CEO, Louis Butler, made a contrarian bet. "When everyone is selling, that's when you buy," he told shareholders in 1932. The company acquired three failing regional insurers for pennies on the dollar, instantly expanding their agent network by 400 offices. They also pioneered payment plans, allowing cash-strapped customers to pay premiums monthly rather than annually—a simple innovation that retained thousands of policies that would have otherwise lapsed.

World War II transformed The Hartford again. The company insured defense contractors, Liberty ships, and even the Manhattan Project facilities (though they didn't know what they were insuring at the time). More importantly, they developed expertise in complex industrial risks that would prove invaluable in the post-war boom. By 1945, The Hartford had 3,000 employees and operated in every state.

The post-war era saw The Hartford's most ambitious diversification yet. In 1954, they entered the group life and health insurance market, targeting the growing universe of corporate employee benefits. Their timing was perfect—unions were negotiating health benefits into contracts, corporations were using benefits to attract talent, and the tax code made employer-provided insurance attractive. Within five years, The Hartford was insuring 500,000 employees across 200 major corporations.

But the real masterstroke came in 1959 when The Hartford created the first mutual fund designed specifically for pension plans. The Hartford Growth Fund gave small and medium businesses access to professional investment management previously available only to the largest corporations. This wasn't just product innovation; it was ecosystem thinking. The Hartford was becoming a full-service financial partner, not just an insurance company.

The 1960s brought both opportunity and challenge. The company expanded internationally, opening offices in London, Toronto, and Tokyo. They pioneered computer-based underwriting, installing an IBM System/360 mainframe in 1964 that could process in hours what previously took weeks. But they also faced new competition from aggressive conglomerates and foreign insurers entering the U.S. market.

By 1969, The Hartford had grown to $1.2 billion in annual premiums, employed 8,000 people, and operated one of the most sophisticated insurance operations in the world. They had successfully transformed from a regional fire insurer into a diversified financial services company. But this success had attracted attention from an unexpected source: Harold Geneen, the legendary CEO of ITT Corporation, who saw in The Hartford exactly what he needed for his grand conglomerate vision.

The company that had survived fires, depressions, and wars was about to face its most unusual chapter yet—life inside one of history's most ambitious corporate empires.

IV. The ITT Era: Conglomerate Life (1970–1995)

Harold Geneen didn't do small deals. The legendary CEO of International Telephone & Telegraph Corporation, who had already assembled a bewildering empire spanning Sheraton Hotels to Wonder Bread, set his sights on The Hartford in 1969. His pitch to The Hartford's board was seductive: "Together, we'll create the world's first truly integrated financial services conglomerate. Your expertise, our capital and global reach—it's the future of American business. "The deal closed in 1970 for $1.4 billion, at the time the largest corporate takeover in American history. The Hartford and the International Telephone & Telegraph Corp. completed what at the time was the largest corporate merger in U.S. history, overcoming a lengthy antitrust challenge sparked by consumer advocate Ralph Nader. The new entity was renamed ITT-Hartford Group, Inc., and suddenly, the conservative insurance company from Connecticut found itself part of a sprawling empire that included Wonder Bread, Sheraton Hotels, Avis Rent-A-Car, and dozens of other unrelated businesses across 80 countries.

Life inside ITT was surreal. The Hartford's executives, accustomed to measuring risk in actuarial tables and thinking in decades, now reported to Geneen, who demanded 58 quarterly meetings a year and managed through a system of relentless interrogation he called "unshakeable facts." Every month, Hartford's leadership would fly to New York for marathon sessions where Geneen and his staff would grill them on everything from expense ratios to paper clip procurement. One former Hartford executive recalled: "We'd present our insurance results, then sit through four hours of discussion about Brazilian telecommunications or frozen food margins. It was like being at a business school case competition that never ended."

Yet there were unexpected benefits. ITT's massive capital base allowed The Hartford to pursue opportunities that would have been impossible as an independent company. They expanded aggressively into Europe and Asia, leveraging ITT's existing international infrastructure. The company developed sophisticated computer modeling for risk assessment years ahead of competitors, funded by ITT's deep pockets and technological expertise from its telecommunications divisions. Hartford's premiums grew from $1.2 billion in 1970 to over $4 billion by 1980.

But the cultural tension was palpable. Hartford's insurance professionals, who prided themselves on conservative underwriting and long-term relationship building, clashed with ITT's quarterly earnings obsession. Geneen pushed The Hartford to write more aggressive policies, expand into riskier lines, and juice returns through financial engineering. The Hartford's management pushed back, arguing that insurance was fundamentally different from manufacturing telephones or running hotels—that reputation and capital preservation mattered more than quarterly earnings growth.

The relationship grew more strained in the late 1970s when Geneen retired and was replaced by Rand Araskog. Where Geneen had been a micromanager who at least understood financial services, Araskog was focused on simplifying ITT's unwieldy structure. The Hartford became increasingly isolated within the conglomerate, neither fully independent nor fully integrated. Investment decisions required approval from ITT headquarters, but ITT executives didn't understand insurance economics. The Hartford couldn't pursue acquisitions without lengthy corporate reviews, losing deals to nimbler competitors.

By the 1980s, the conglomerate model was falling out of favor on Wall Street. Investors wanted "pure plays" they could understand and value properly. The Hartford's earnings were buried in ITT's consolidated statements, making it impossible for insurance investors to properly assess the company. Meanwhile, ITT's stock price was being dragged down by its struggling manufacturing and defense businesses, even as The Hartford posted record profits.

The breaking point came in the early 1990s. Araskog, under pressure from activist investors and facing a hostile takeover threat from Hilton Hotels, realized that ITT's sum-of-the-parts value far exceeded its market capitalization. The Hartford alone was likely worth more than half of ITT's entire market value. In 1992, ITT confirms it may consider splitting off its financial services and hotel operations, but insists The Hartford is not for sale.

But the pressure was relentless. Corporate raiders circled, sensing opportunity. The insurance industry was consolidating rapidly, and The Hartford needed the flexibility to participate or risk being left behind. After 25 years of conglomerate life, The Hartford had learned valuable lessons about scale, technology, and international expansion. But it had also learned that insurance was too specialized, too long-term oriented, and too dependent on reputation to thrive inside a conglomerate focused on quarterly earnings. The stage was set for one of the most significant corporate spinoffs of the 1990s.

V. Independence Regained: The 1995 Spinoff & Public Company Transformation

The boardroom at ITT's Manhattan headquarters was unusually quiet on the morning of June 13, 1995. Rand Araskog, ITT's CEO, stood before a small group of executives and investment bankers from Morgan Stanley. After months of secret negotiations and pressure from the board, he was about to announce the unthinkable: the complete breakup of Harold Geneen's empire. ITT announces plans in 1995 to spin off to its shareholders The Hartford, along with its industrial products and hospitality, entertainment and information services businesses

The announcement sent shockwaves through Wall Street. The Hartford, valued at approximately $11 billion, would be spun off to ITT shareholders as an independent company. After 25 years, Hartford would trade on its own, free to chart its destiny without seeking approval from a conglomerate parent more interested in hotels and defense contracts than insurance underwriting.

The mechanics of the spinoff were complex but elegantly executed. ITT shareholders would receive one share of The Hartford for every share of ITT they owned. The Hartford regained its independence on December 20, 1995, and began trading on the NYSE under the "HIG" symbol. The opening bell that morning wasn't just ceremonial—it was a declaration of strategic freedom. The stock opened at $24.88 per share (adjusted for subsequent splits), valuing the company at roughly $11 billion.

Ramani Ayer, who had risen through The Hartford's ranks during the ITT years, was named CEO of the newly independent company. His first town hall with employees in Hartford set the tone: "We're not just free from ITT—we're free to become what we were always meant to be: a premier financial services company that happens to be rooted in insurance excellence." The strategy was ambitious but clear: leverage the company's insurance expertise to become a diversified financial services powerhouse.

The transformation began immediately. Within six months, The Hartford acquired Columbian Mutual Life Insurance Company for $1.1 billion, instantly adding 500,000 life insurance policies and critical mass in the individual life market. They followed this with the purchase of London Life's U.S. operations, adding sophisticated variable annuity capabilities that would become crucial to the company's growth strategy.

But Ayer's boldest move came in 1997 with the creation of Hartford Life, a dedicated platform for retirement savings and investment products. This wasn't just adding products—it was recognizing a fundamental shift in American retirement planning. With defined benefit pensions disappearing and 401(k) plans proliferating, millions of Americans needed help managing retirement savings. The Hartford positioned itself at the intersection of insurance and investment management, offering variable annuities that provided both growth potential and downside protection.

The strategy worked brilliantly. By 1998, The Hartford's stock had split and was trading above $85, more than tripling from its spinoff price. Over the last 10 years since independence, The Hartford, which now has a workforce of approximately 30,000 employees worldwide, has produced consistent growth across its businesses, delivering a 16 percent annualized total return to shareholders. Revenue grew from $9 billion in 1995 to over $18 billion by 2000. The company was firing on all cylinders: property and casualty premiums were growing at 8% annually, life insurance sales were booming, and the investment products division was capturing billions in new assets each quarter.

The company also modernized aggressively. They launched one of the industry's first comprehensive online platforms for agents and brokers in 1999, allowing real-time quoting and policy issuance. They pioneered data analytics for risk assessment, using credit scores and behavioral data to price auto insurance more accurately than competitors still relying on traditional factors. The Hartford wasn't just competing; it was leading.

Wall Street took notice. Analysts praised The Hartford's "best-in-class" expense ratios and innovative product development. The company was included in the S&P 500 index in 1999, a validation of its transformation from conglomerate subsidiary to standalone financial services leader. By 2000, The Hartford had grown to become the nation's largest writer of auto and homeowners insurance through employers and affinity groups, building on its pioneering 1984 exclusive partnership with AARP for home and auto insurance.

Yet beneath this success, seeds of future trouble were being planted. The variable annuity business that drove so much growth was inherently risky, with The Hartford guaranteeing minimum returns even if markets declined. The company was essentially writing put options on the equity markets, collecting premiums in good times but potentially facing massive liabilities in a market downturn. Risk models suggested these scenarios were remote, perhaps once-in-a-generation events.

As the dot-com bubble burst in 2001, The Hartford weathered the storm relatively well, its diversified business model providing stability. The company even saw opportunity in the chaos, acquiring Fortis Financial Group's U.S. operations in 2001 for $1.15 billion, adding scale in group benefits and retirement plans. By 2007, The Hartford had grown to over $25 billion in revenue and was ranked among the 20 largest financial services companies in America.

CEO Ayer, preparing to retire after a spectacular run, told investors at the company's 2007 investor day: "The Hartford has never been stronger. Our capital position is fortress-like, our products are industry-leading, and our risk management is state-of-the-art." Within 18 months, each of these claims would be severely tested.

VI. The 2008 Financial Crisis: Near-Death Experience

In January 2008, The Hartford's new CEO Ramani Ayer handed the reins to his successor, having built the company into a $26 billion revenue giant. The transition seemed seamless. The company's investment portfolio was rated AA, its variable annuity business was printing money, and its stock was trading near all-time highs around $90 per share. Nine months later, that same stock would trade below $5, and The Hartford would be fighting for its very survival.

The unraveling began slowly, then suddenly. Hartford, like several other insurers, has suffered massive losses in its investment portfolio during the past few months due to bets on financial firms such as Fannie Mae, Freddie Mac, Lehman Brothers, American International Group and Washington Mutual. What seemed like conservative investments in blue-chip financial institutions turned into toxic waste almost overnight. The company's $2 billion in preferred stock of Fannie Mae and Freddie Mac was essentially worthless after the government takeover. Lehman Brothers bonds, once considered gold-standard corporate debt, became wallpaper.

But the real catastrophe was hiding in the variable annuity book. During the bull market years, The Hartford had aggressively sold annuities with guaranteed minimum withdrawal benefits, essentially promising retirees they could withdraw 5-7% of their investment annually for life, regardless of market performance. With the S&P 500 down 37% in 2008, these guarantees transformed from profitable products into existential liabilities. The company faced potential payouts of $30 billion or more if markets didn't recover.

October 10, 2008, marked the nadir. The Hartford's stock plunged 47% in a single day, closing at $12.75. Credit default swaps on The Hartford's debt—essentially the cost to insure against the company's bankruptcy—spiked to levels suggesting a 40% probability of default within five years. Rating agencies placed the company on negative watch, threatening downgrades that would trigger massive collateral calls and potentially fatal capital requirements.

On Wednesday's conference call that October, Hartford Chief Financial Officer Lizabeth Zlatkus said the company would consider an investment as part of TARP if it was offered. The admission was both pragmatic and humiliating. The Hartford, which had survived the Great Depression without government help, was now essentially asking for a federal bailout. But the TARP program was designed for banks, not insurers, creating a Kafkaesque situation where The Hartford needed to become something it wasn't to access lifesaving capital.

The solution came from an unexpected source. Earlier that month, Hartford turned to German insurer Allianz for a $2.5 billion capital infusion. The deal was expensive—Allianz received preferred shares paying 10% interest plus warrants for 69 million common shares—but it provided crucial breathing room. The capital injection, combined with the Federal Reserve's subsequent decision to allow The Hartford to acquire a small savings and loan (making it technically a bank holding company eligible for TARP), stabilized the immediate crisis.

By June 2009, The Hartford had received $3.4 billion in TARP funds, drawn down Allianz's investment, and raised another $2.5 billion through dilutive common stock offerings. The company that entered 2008 with 311 million shares outstanding now had over 425 million, representing massive dilution for existing shareholders. The stock price, which had peaked above $90 in 2007, bottomed at $3.33 in March 2009.

The human toll was equally severe. The Hartford eliminated 2,000 jobs, froze pension plans, and slashed dividends. CEO Liam McGee, brought in from Bank of America to navigate the crisis, implemented draconian cost cuts while simultaneously trying to maintain agent and customer relationships. "We're not just fighting for profitability," he told employees in a company-wide meeting, "we're fighting for relevance."

The crisis revealed fundamental flaws in The Hartford's pre-2008 strategy. The company had chased growth through increasingly complex products without fully understanding tail risks. Risk models that showed variable annuity disasters as "25-sigma events" (essentially impossible) proved worthless when the impossible happened. The pursuit of becoming a diversified financial services company had led The Hartford away from its core competency: carefully underwriting predictable risks.

Yet The Hartford survived where others didn't. Unlike AIG, which required over $180 billion in government support, The Hartford's core insurance operations remained profitable throughout the crisis. The company's property and casualty business, built over two centuries, provided stable cash flow even as the investment products division hemorrhaged money. By March 2010, The Hartford had repaid its TARP obligations in full, ahead of most recipients.

The near-death experience of 2008-2009 forced a fundamental reckoning. The Hartford had survived, but barely. The question now was whether it could transform itself once more, shedding the failed diversification strategy and returning to its insurance roots. The answer would require the kind of dramatic restructuring not seen since the ITT spinoff.

VII. Reinvention & Focus: The Post-Crisis Transformation (2009–2020)

Liam McGee stood before The Hartford's board in early 2012 with a radical proposal that would have been unthinkable just five years earlier. "We need to shrink to grow," he said, outlining a plan to essentially split the company in half. The board's response was unanimous: do it.

In 2012, The Hartford announced it would focus on property and casualty insurance, group benefits and mutual funds, and would sell its wealth management businesses. This wasn't optimization; it was amputation. The variable annuity business that had nearly killed the company would be systematically unwound. The individual life insurance business, built through billions in acquisitions, would be sold. The Hartford would return to what it knew best: commercial insurance, group benefits, and its cornerstone AARP personal lines partnership.

The execution was swift and decisive. In 2013, The Hartford sold its life insurance business to Prudential for $615 million, its retirement plans business to MassMutual for $400 million, and its broker-dealer to AIG for $110 million. Combined with the runoff of the variable annuity book, The Hartford shed over $100 billion in liabilities. The company that had aspired to be a financial supermarket was deliberately choosing to become a focused specialty retailer. Christopher Swift took over as CEO in July 2014, joining from AIG where he had served as CFO. Named CEO in 2014, he expanded the company's capabilities and geographic reach through organic growth and strategic investments, continuing a strategy that included streamlining and focusing more heavily on property/casualty, group benefits and mutual funds. Unlike his predecessors who chased growth, Swift was a numbers man who understood that sometimes the best strategy was saying no.

The transformation under Swift accelerated. The company invested heavily in digital capabilities, launching predictive analytics platforms that could price commercial insurance in real-time based on thousands of data points. They modernized their legacy IT systems, moving from 1980s-era mainframes to cloud-based architecture that could scale elastically. The Hartford wasn't trying to be a Silicon Valley disruptor; it was using technology to do what it had always done—underwrite risk—but do it better and faster than competitors.

The AARP partnership, which began in 1984 when The Hartford became the exclusive provider of Home and Auto insurance for AARP members, became the crown jewel of the personal lines business. By 2015, The Hartford was insuring over 1 million AARP members, generating stable, profitable premiums from a demographic that was inherently lower-risk—older, wealthier, and more cautious drivers. Competitors coveted this relationship, but The Hartford's decades of trust-building proved unassailable.

In commercial lines, The Hartford pursued a "small is beautiful" strategy. While competitors chased Fortune 500 accounts, The Hartford focused on small and medium businesses—contractors, restaurants, retailers—that needed comprehensive coverage but weren't large enough to self-insure. They developed industry-specific products, understanding that a plumbing contractor had fundamentally different risks than a software developer. By 2016, The Hartford was insuring over 1 million small businesses, with renewal rates exceeding 85%.

The biggest strategic move came in 2017 when The Hartford acquired Aetna's U.S. group life and disability business in 2017 for $1.45 billion. This wasn't just an acquisition; it was a doubling down on group benefits at a time when the gig economy and changing workforce dynamics were making employer-provided benefits more valuable, not less. The deal added 7 million covered lives and made The Hartford a top-five player in group disability insurance.

But Swift's masterstroke came in 2019 with the acquisition of The Navigators Group, Inc., a specialty lines property and casualty business, in 2019 for $2.1 billion. Navigators brought expertise in ocean marine, energy, and professional liability—complex risks that commanded premium pricing and required deep technical expertise. The acquisition added 22 specialty verticals and gave The Hartford a presence in Lloyd's of London, the world's most prestigious insurance marketplace.

By 2020, The Hartford had been completely transformed. The company completed its exit from the run-off life and annuity business, providing greater financial flexibility and improving The Hartford's return on equity and earnings growth profile. Revenue had stabilized around $20 billion, but more importantly, return on equity had improved from single digits during the crisis to consistently above 12%. The stock, which had bottomed at $3.33 in 2009, was trading above $50.

The company that had nearly died from financial engineering had been reborn as a focused, technology-enabled, specialty insurer. It was smaller than its pre-crisis peak but far more profitable, more resilient, and strategically positioned for the future. The Hartford had learned that in insurance, as in life, sometimes you have to lose yourself to find yourself.

VIII. The Chubb Takeover Drama: Independence Defended (2021)

The email landed in Christopher Swift's inbox at 7:47 AM on March 11, 2021. The sender: Evan Greenberg, CEO of Chubb, the Swiss-based insurance giant. The subject line was innocuous—"Strategic Opportunity"—but the content was explosive. Chubb was offering $65 per share in cash and stock to acquire The Hartford, valuing the company at approximately $23.2 billion. After 25 years of independence, The Hartford was once again in play.

The timing seemed calculated to maximize pressure. The Hartford's stock had been trading around $48, making the 35% premium difficult to dismiss. Chubb, with its $75 billion market cap and global reach, argued the combination would create the world's premier property and casualty insurer. Greenberg's letter, which quickly leaked to the press, painted a compelling picture: "Together, we would be a $74 billion revenue company with unmatched distribution, product breadth, and financial strength."

Swift's first call was to his lead independent director. His second was to Goldman Sachs. By noon, The Hartford's board was assembled via emergency video conference, directors joining from homes and offices across the country. The atmosphere was tense. Several directors noted that rejecting a 35% premium without consideration could trigger shareholder lawsuits. Others worried about losing independence after working so hard to regain it.

The Hartford's response on March 23 was carefully worded but unambiguous: the offer "significantly undervalues" the company and was "not in the best interests of The Hartford's shareholders." Privately, Swift and the board saw fundamental issues beyond price. Chubb operated a centralized, command-and-control culture that clashed with The Hartford's decentralized, relationship-driven approach. Integration would likely mean massive layoffs in Hartford, Connecticut—a betrayal of the company's 210-year commitment to its hometown.

Greenberg didn't give up. On March 30, 2021, Chubb raised its offer to "in excess of $67 per share," with more favorable terms including regulatory breakup protections. When this too was rejected, Greenberg played his final card, announcing publicly that Chubb was "willing to increase its offer to $70 per Hartford share, the top end of our range," payable approximately 60% in cash and 40% in Chubb stock.

The pressure was immense. Activist investors began circling, with some calling for The Hartford's board to at least engage in negotiations. Proxy advisors started preparing reports questioning whether the board was properly fulfilling its fiduciary duties. Financial media ran daily speculation about whether The Hartford could remain independent.

Swift's response was bold and risky. Instead of negotiating, The Hartford announced a strategic plan that would return $18 billion to shareholders over the next three years through dividends and buybacks—essentially promising to deliver the takeover premium to shareholders without the takeover. The company raised its ROE target to 13.5% and announced $500 million in additional cost savings.

The decisiveness had an unexpected effect. Major shareholders, including Wellington Management and BlackRock, publicly backed management. They saw in The Hartford's plan something more valuable than Chubb's premium: a focused, high-performing specialty insurer with room to grow. As one portfolio manager told the Financial Times: "Merging with Chubb didn't make sense for shareholders in the long term. The Hartford has a unique market position that would be diluted, not enhanced, in a combination."

The Connecticut political establishment also mobilized. Governor Ned Lamont privately called Greenberg, making clear that a hostile takeover destroying thousands of Connecticut jobs would face significant political opposition. The state's congressional delegation wrote public letters questioning the antitrust implications of combining two of America's largest commercial insurers.

By April 15, 2021, Greenberg capitulated. In a terse statement, Chubb announced it was "withdrawing its proposal to acquire The Hartford" after the company's "repeated refusal to engage in discussions." The Hartford's stock, rather than plummeting as many predicted, actually rose 2% on the news. The market was betting that independence, combined with aggressive capital returns, was worth more than becoming a division of Chubb.

The successful defense had broader implications. It proved that in an era of relentless consolidation, a well-managed, focused company could still choose independence if it had a compelling alternative strategy. It also demonstrated that The Hartford's board and management had learned from history—sometimes the best deal is the one you don't make.

Swift's internal message to employees the day after Chubb withdrew was telling: "We didn't survive 211 years to become someone else's subsidiary. We survived to thrive on our own terms." The Hartford had once again chosen the harder path of independence, betting that its best days were still ahead.

IX. Modern Era: The Hartford Today (2021–Present)

The Hartford that emerged from the Chubb takeover battle was a company transformed not just strategically but psychologically. The successful defense had galvanized employees, energized management, and most importantly, forced the company to articulate and execute on a compelling standalone vision. As Swift told investors in the Q2 2021 earnings call: "We didn't just reject $70 per share—we committed to delivering more than that in value over time."

The post-Chubb strategy centered on three pillars: expanding margins through technology and automation, growing in attractive specialty niches, and returning massive amounts of capital to shareholders. The execution has been remarkably consistent. The Hartford is now the 13th-largest property and casualty insurance company in the United States, but its influence extends far beyond its ranking.

In commercial P&C, The Hartford has become the preferred insurer for specific verticals where deep expertise matters more than scale. The company insures 40% of America's tow truck operators, 30% of rental property managers, and 25% of small construction contractors. These aren't glamorous markets, but they're sticky, profitable, and defensible. Competitors could theoretically enter these niches, but replicating decades of claims data, underwriting expertise, and broker relationships would take years and billions in investment.

The personal lines business, anchored by the AARP partnership, continues to be a cash generation machine. The Hartford now insures 1.1 million AARP members, with average tenure exceeding 12 years. The relationship, renewed through 2032, provides predictable, profitable premiums from customers who rarely switch insurers and file fewer claims than the general population. It's a moat that money can't buy—built on trust earned over four decades.

Group benefits has emerged as an unexpected growth engine. The pandemic fundamentally changed how employers think about employee wellbeing, and The Hartford's integrated approach—combining disability, life, accident, and critical illness coverage with return-to-work programs—resonated with HR departments struggling to retain talent. The company now covers 13 million employees across 280,000 employers, from Fortune 500 companies to 10-person startups.

Technology investment has accelerated dramatically. The Hartford spends over $600 million annually on technology, focusing on three areas: automation to reduce expense ratios, analytics to improve underwriting precision, and digital interfaces to enhance customer experience. The company's new small commercial platform can quote, underwrite, and issue policies in under 10 minutes—a process that used to take days. Claims can be filed, processed, and paid entirely through mobile apps, with AI handling routine cases and flagging complex ones for human review. The financial results speak for themselves. For the full year 2024, The Hartford posted net income available to common stockholders of $3.1 billion, or $10.35 per diluted share, reflecting a 24% increase from $2.5 billion, or $7.97 per diluted share, in 2023. The company reported a net income return on equity (ROE) of 19.9% and a core earnings ROE of 16.7% for the year. These aren't just good numbers—they're elite performance metrics that validate the strategic transformation.

ESG initiatives have become central to The Hartford's corporate identity. The company ranks highest among insurance companies on the 2024 JUST 100 list by JUST Capital and CNBC, marking the sixth consecutive year of recognition. This isn't greenwashing—The Hartford has committed to net-zero emissions by 2050, increased board diversity to 40%, and invested $2.3 billion in affordable housing and renewable energy projects.

The company's approach to climate change is particularly sophisticated. Rather than simply excluding high-risk properties, The Hartford has developed proprietary models that price climate risk with unprecedented precision. They're working with municipalities on resilience planning, offering discounts for properties with flood defenses or fire-resistant construction. It's turning an existential threat into a competitive advantage.

Yet challenges remain. The Hartford's $90 billion investment portfolio faces headwinds from volatile interest rates. Personal auto insurance, despite the AARP partnership, struggles with inflation in repair costs and increasing accident frequency as Americans return to pre-pandemic driving patterns. Cyber insurance, a growth market The Hartford entered aggressively, faces massive loss potential from state-sponsored attacks and ransomware.

Competition has intensified from both traditional insurers and InsurTech startups. Companies like Lemonade and Root promise to revolutionize insurance through AI and behavioral economics. While these startups have yet to prove profitable, they're forcing incumbents like The Hartford to accelerate digital transformation. The company has responded by launching its own innovation lab, partnering with startups, and even making strategic investments in InsurTech ventures.

The most intriguing development is The Hartford's quiet expansion into embedded insurance—coverage integrated directly into the purchase of products or services. When you buy a high-end bicycle, expensive electronics, or book a vacation rental, The Hartford's white-label insurance products increasingly power the protection offered at checkout. It's invisible to consumers but generates billions in premiums with minimal acquisition costs.

As 2024 ends, The Hartford stands at an inflection point. The company has successfully defended its independence, delivered on its promises to shareholders, and positioned itself for the future. But the insurance industry faces fundamental disruption from climate change, technology, and changing consumer expectations. The question isn't whether The Hartford can survive—214 years of history suggests it can—but whether it can thrive in a world that's changing faster than ever.

X. Playbook: Business & Investing Lessons

After 214 years of corporate evolution, The Hartford's journey offers a masterclass in strategic decision-making, capital allocation, and organizational resilience. These aren't abstract business school concepts but hard-won lessons paid for in market crashes, near-bankruptcy, and hostile takeover attempts.

The Power of Focus vs. Diversification Debates

The Hartford's history reads like a controlled experiment in corporate strategy. The company has twice pursued aggressive diversification—first under ITT's conglomerate umbrella, then through its pre-2008 transformation into a financial supermarket—and twice retreated to its core insurance competency. The lesson isn't that diversification is always wrong, but that successful diversification requires genuine synergies, not just financial engineering.

When The Hartford expanded into variable annuities, it seemed logical: leverage insurance distribution to sell investment products. But variable annuities aren't insurance—they're derivatives on equity markets requiring completely different risk management, capital allocation, and expertise. The Hartford learned that related diversification can be more dangerous than unrelated diversification because it creates an illusion of competence.

Contrast this with successful adjacencies: expanding from fire insurance to auto insurance leveraged the same actuarial capabilities and distribution channels. Moving into group benefits built on existing corporate relationships. The difference? These expansions enhanced rather than diluted core capabilities.

Surviving Existential Crises

The Hartford has faced existential threats roughly every 50 years: the 1835 New York fire, the 1906 San Francisco earthquake, the 2008 financial crisis. Each time, survival came down to three factors: conservative balance sheet management before the crisis, decisive leadership during it, and aggressive repositioning after it.

Eliphalet Terry's personal guarantee in 1835 wasn't just heroic—it was strategically brilliant. By paying claims when competitors couldn't, The Hartford captured market share that lasted decades. Similarly, accepting TARP funds in 2009 was humiliating but necessary. Pride is a luxury companies can't afford during existential crises.

The pattern is consistent: companies that survive existential crises emerge stronger not despite the crisis but because of it. Crises force strategic clarity, eliminate weak competitors, and create opportunities for prepared companies to gain permanent advantages.

When to Sell vs. Stay Independent

The Hartford has faced three major ownership inflection points: the 1970 ITT acquisition, the 1995 spinoff, and the 2021 Chubb approach. Each decision hinged on whether independence or combination would better serve long-term value creation.

The ITT sale made sense in 1970—The Hartford needed capital for expansion and technology that it couldn't access independently. The spinoff made sense in 1995—conglomerate structures were destroying value and preventing strategic focus. Rejecting Chubb made sense in 2021—The Hartford had a credible standalone plan worth more than the takeover premium.

The key insight: ownership structure should follow strategy, not vice versa. When The Hartford needed resources, it sold. When it needed focus, it separated. When it had both, it stayed independent. Too many companies make ownership decisions based on investment banking fees or executive egos rather than strategic logic.

Building Distribution Moats Through Partnerships

The Hartford's AARP partnership, now four decades old, generates over $3 billion in annual premiums with minimal marketing costs and industry-leading retention rates. This wasn't luck—it was patient relationship building combined with consistent execution.

The partnership works because of aligned incentives. AARP wants quality coverage for members at competitive prices. The Hartford wants access to low-risk customers with high retention. Both parties benefit from the relationship's longevity—AARP doesn't have to repeatedly vet insurers, and The Hartford can invest in AARP-specific products and services.

Modern companies obsess over customer acquisition costs and lifetime value, but The Hartford understood these concepts centuries before they had names. Distribution moats aren't built through technology or marketing spend but through trust, consistency, and mutual benefit sustained over decades.

Capital Allocation Through Cycles

Insurance is inherently cyclical—hard markets with high prices and strict underwriting followed by soft markets with price competition and loosened standards. Most insurers follow the cycle, growing aggressively in soft markets and retrenching in hard ones. The Hartford has learned to do the opposite.

During the 1930s Depression, The Hartford acquired failed competitors. After 2008, while others were in survival mode, The Hartford invested in technology and talent. When commercial insurance markets hardened in 2019-2020, The Hartford had the systems and expertise to capture profitable growth while competitors scrambled to add capacity.

This countercyclical approach requires two things most companies lack: patient capital and institutional memory. The Hartford's board includes insurance veterans who've seen multiple cycles. Management compensation emphasizes long-term returns over quarterly earnings. The result is capital allocation that looks contrarian in the moment but obvious in hindsight.

The Importance of Management Credibility

When Christopher Swift promised to return $18 billion to shareholders while rejecting Chubb's $70 per share offer, markets could have punished the stock. Instead, it rose. Why? Because Swift had credibility earned through years of delivering on promises.

Management credibility is like brand equity—invisible on balance sheets but invaluable during crises. It's built through hundreds of small promises kept: earnings guidance achieved, strategic initiatives completed, timelines met. It's destroyed instantly through one big promise broken.

The Hartford's management learned this lesson the hard way during the financial crisis when rosy pre-crisis assurances about risk management proved hollow. Rebuilding credibility took years of under-promising and over-delivering. Now, when management makes bold claims, markets listen.

Timing Market Cycles in Insurance

Insurance profitability depends on two variables: underwriting margins and investment returns. When both align positively, returns are spectacular. When both turn negative, insurers fail. The Hartford has survived by never betting on both simultaneously.

During the 1990s bull market, The Hartford loosened underwriting standards, essentially using investment returns to subsidize competitive pricing. When markets crashed in 2008, this strategy nearly proved fatal. Post-crisis, The Hartford maintains strict underwriting discipline regardless of investment markets.

The lesson extends beyond insurance: companies should have one primary profit driver with others as supplements, not substitutes. When multiple profit sources are equally important, companies lose focus and accountability. The Hartford now treats investment income as a bonus, not a baseline.

XI. Analysis & Bear vs. Bull Case

Standing at the end of 2024, The Hartford presents one of the most fascinating investment debates in financial services. Bulls see an elite operator trading at a discount to intrinsic value with multiple expansion catalysts. Bears see a melting ice cube facing structural headwinds in a disrupting industry. Both sides have compelling arguments.

Bull Case: The Compound Opportunity

The bullish thesis starts with valuation. The Hartford trades at roughly 1.3x book value and 9x forward earnings—a meaningful discount to peers like Chubb (1.8x book, 12x earnings) and Travelers (1.6x book, 11x earnings). This discount persists despite The Hartford's superior ROE, better expense ratios, and higher-quality business mix. Bulls argue this is a classic case of market inefficiency—investors still associate The Hartford with its 2008 near-death experience rather than its current excellence.

The commercial insurance market offers enormous growth potential. Small and medium businesses remain significantly underinsured, with coverage gaps in cyber, employment practices, and climate-related risks. The Hartford's focus on these segments positions it perfectly to capture profitable growth as awareness increases and regulations potentially mandate coverage.

Technology investments are hitting inflection points. The Hartford's new AI-powered underwriting platform can price complex commercial risks in minutes rather than days, enabling the company to win business that previously went to larger competitors with more resources. Digital distribution reduces acquisition costs by 60%, flowing directly to bottom-line margins.

Capital allocation optionality provides multiple paths to value creation. The Hartford generates over $2 billion in free cash flow annually. Management could accelerate buybacks (reducing share count by 8-10% annually), pursue strategic acquisitions (specialty MGAs or InsurTech platforms), or surprise with special dividends. Each dollar of capital returned at current valuations is highly accretive.

Climate change, counterintuitively, could be a massive opportunity. As extreme weather increases, insurance becomes more valuable, not less. The Hartford's sophisticated catastrophe modeling and conservative exposure management position it to raise prices faster than losses increase. Companies that can successfully price climate risk will earn oligopoly profits.

The AARP partnership becomes more valuable every year. America is aging rapidly—10,000 people turn 65 daily. These new retirees need auto, home, and umbrella insurance. They're wealthier, more risk-averse, and more loyal than younger customers. The Hartford's exclusive access to this demographic through 2032 is essentially a license to print money.

Finally, bulls point to management quality. Christopher Swift has delivered on every major promise since becoming CEO. The team has shown discipline in rejecting bad deals (Chubb), courage in making good ones (Navigators), and wisdom in knowing the difference. In an industry where management matters enormously, The Hartford has one of the best teams in the business.

Bear Case: The Disruption Scenario

The bearish thesis acknowledges The Hartford's current strength but questions its durability. Insurance is being disrupted by forces that favor scale (which The Hartford lacks) or innovation (where incumbents struggle). Being a well-run subscale incumbent might be the worst position in a disrupting industry.

Scale disadvantages compound over time. Larger insurers spread technology costs across bigger premium bases, negotiate better reinsurance rates, and attract superior talent with resources The Hartford can't match. As insurance becomes increasingly data-driven and technology-dependent, scale advantages grow exponentially, not linearly.

InsurTech disruption is accelerating. While startups like Lemonade and Root haven't yet proven profitable, they're backed by billions in venture capital and can operate at losses for years. They're unbundling insurance, offering single products through digital channels at prices The Hartford can't match while maintaining its expense structure. Death by a thousand cuts is still death.

Climate change could break the insurance model. The Hartford assumes climate risks are priceable and insurable. But what if they're not? What if extreme weather becomes so frequent and severe that insurance becomes either unaffordable for customers or unprofitable for insurers? The Hartford's conservative approach might simply mean it's the last company to fail, not that it won't fail.

The investment portfolio faces structural headwinds. The Hartford has $50 billion invested primarily in fixed income securities. If interest rates fall, reinvestment yields decline, pressuring returns. If rates rise, bond values fall, hurting book value. If credit spreads widen, defaults increase. There's no scenario where the investment portfolio becomes a meaningful growth driver.

Distribution disruption threatens core franchises. The AARP partnership has been golden, but AARP itself faces disruption. Younger retirees don't identify with AARP like previous generations. Digital-native seniors might prefer buying insurance directly through apps rather than affinity groups. The partnership that's been The Hartford's greatest asset could become its biggest liability if customer behavior shifts.

Regulatory and political risks are rising. Insurance is becoming politicized, with states mandating coverage in unprofitable areas (California wildfire zones, Florida hurricanes) while restricting pricing flexibility. The Hartford's geographic concentration in regulated states makes it vulnerable to political interference that destroys profitability under the guise of consumer protection.

Bears also worry about capital allocation. Returning $18 billion to shareholders sounds impressive, but it represents financial engineering, not business building. Great companies reinvest capital at high returns. The Hartford's massive buybacks suggest management sees no compelling growth opportunities—hardly a bullish signal.

The Verdict: Asymmetric Opportunity

Weighing both cases, The Hartford appears to offer asymmetric upside with limited downside. The bear case relies primarily on long-term structural concerns that will take years to materialize. The bull case rests on near-term catalysts that could drive rerating within quarters. At current valuations, the market is pricing in the bear case while ignoring the bull case—creating opportunity for contrarian investors.

XII. Epilogue & "If We Were CEO"

If we were sitting in Christopher Swift's corner office, looking out at Hartford's skyline from the company's iconic tower, what strategic moves would we make? The Hartford has successfully navigated its transformation from near-death to prosperity, but the next chapter requires different skills—not recovery but renaissance.

Strategic Options: Organic Growth vs. M&A

First, we'd pursue a barbell M&A strategy: acquire small InsurTech companies for technology and talent while simultaneously buying established specialty MGAs for immediate profitable growth. The Hartford should spend $500 million annually on 5-10 acquisitions of $50-100 million each. These wouldn't move the needle individually but would collectively transform capabilities over five years.

The ideal targets would be companies like Coalition (cyber insurance), Hippo (home insurance technology), or Next Insurance (small business digital distribution). Not to compete with them but to absorb their technology and talent. Every acquisition would include earnout provisions keeping founders invested in long-term success.

The Next Transformation Opportunity

We'd create "Hartford Ventures," a $1 billion fund investing in early-stage InsurTech companies globally. This wouldn't be corporate venture capital seeking financial returns but strategic investment securing technological capabilities. The Hartford would offer startups what they desperately need—access to regulated insurance capacity, claims data, and distribution networks—in exchange for technology transfer and strategic partnerships.

Simultaneously, we'd establish "Hartford Re," a Bermuda-based reinsurance subsidiary. This would serve three purposes: provide internal reinsurance capacity reducing dependence on third parties, generate fee income by reinsuring other carriers' risks, and create a more tax-efficient structure for international expansion. Lloyd's of London syndicates, accessed through the Navigators acquisition, would provide the initial pipeline.

Technology and AI in Insurance

The Hartford should become the "AI-first" insurer. Not through press releases or marketing but through fundamental reimagination of core processes. Every underwriter would have an AI assistant providing real-time risk scoring. Every claims adjuster would use computer vision for damage assessment. Every customer service representative would have predictive analytics anticipating customer needs.

We'd partner with Google or Microsoft, providing them insurance data to train models in exchange for preferential access to AI capabilities. The Hartford's 214 years of claims data is invaluable for training AI—a moat that startups can't replicate. This data advantage, properly leveraged, could sustain competitive advantages for decades.

Climate Adaptation Strategies

Climate change requires radical rethinking, not incremental adjustment. We'd create "Hartford Resilience Services," a consulting subsidiary helping businesses and municipalities adapt to climate risks. This wouldn't be charity but a profit center—companies pay for risk assessment, adaptation planning, and implementation oversight. The Hartford would then insure adapted properties at preferential rates, creating a virtuous cycle of risk reduction and profitable growth.

We'd also launch "parametric insurance" products that pay automatically when specific conditions occur (wind speed exceeding thresholds, rainfall below certain levels). These products eliminate claims adjustment costs and provide immediate liquidity to customers during disasters. The Hartford's data capabilities position it perfectly for parametric leadership.

Final Reflections on 214 Years of Survival and Reinvention

The Hartford's story is ultimately about institutional resilience—the ability to survive and thrive through radically different eras, technologies, and challenges. From insuring wooden buildings against fire to protecting digital assets against cyber attacks, The Hartford has continuously evolved while maintaining core principles: conservative underwriting, faithful claims payment, and long-term thinking.

The company that started with $15,000 in a Hartford tavern now manages $50 billion in investments and generates $3 billion in annual profits. It has survived fires, earthquakes, depressions, world wars, conglomerate ownership, and financial crises. Each challenge made it stronger, more focused, and more valuable.

Looking forward, The Hartford faces its next evolution. The insurance industry is being transformed by technology, climate change, and shifting demographics. Success requires balancing tradition with innovation, stability with agility, independence with partnership. The Hartford has proven it can adapt—the question is whether it can lead.

If history is any guide, The Hartford will still be here in another 214 years, probably insuring risks we can't imagine with technologies that don't exist, serving customers not yet born. The hart will still be fording the stream, steady and sure, navigating waters that are always changing but never defeating this remarkable company.

The ultimate lesson from The Hartford's journey isn't about insurance or finance but about institutional purpose. Companies that survive centuries don't do so through strategic brilliance alone but through understanding their fundamental role in society. The Hartford exists to help individuals and businesses manage risk, enabling them to pursue opportunities they otherwise couldn't. As long as humans take risks—and they always will—The Hartford will have purpose.

That purpose, more than any strategy or technology, explains why The Hartford has survived 214 years and why it will likely survive 214 more. In an era of quarterly capitalism and instant gratification, The Hartford stands as a monument to patient capital, conservative management, and the radical idea that companies exist to serve customers across generations, not just shareholders across quarters.

XIII. Recent News**

Q3 2024 Earnings Excellence**

The Hartford (NYSE: HIG) announced financial results for the third quarter ended Sept. 30, 2024, with Chairman and CEO Christopher Swift noting the company "delivered an excellent quarter with a trailing 12-month core earnings ROE of 17.4 percent." The Hartford reports robust Q3 earnings: 18% profit surge to $761M, 10% premium growth, and increased dividends.

Core Earnings reached $752 million, or $2.53 per diluted share, with the company achieving strong top-line growth in commercial lines of 9% with double-digit new business growth. The company achieved a very strong underlying combined ratio of 88.6 in commercial lines, marking the 14th consecutive quarter below 90%.

Personal lines saw a 12% top-line growth with significant improvements in the auto underlying combined ratio. The Hartford announced an 11% increase in its common quarterly dividend, reflecting strong earnings power and capital generation. Group Benefits reported a core earnings margin of 8.7%, driven by strong group life results and long-term disability execution.Management Changes and Board Updates

The Hartford announced the promotion of Prateek Chhabra to chief risk officer, effective September 1, 2025, succeeding Robert Paiano, who will retire at the end of the year after 29 years with the company. Chhabra, who has served as senior vice president and chief insurance risk officer since 2018, will report directly to Chairman and CEO Christopher Swift. Before joining The Hartford, Chhabra was chief risk officer for domestic businesses at The Hanover Insurance Group and held risk and strategy consulting positions at firms including McKinsey and Company, Aon and Verisk.

Swift commented on the appointment: "Prateek is an accomplished risk manager with deep knowledge of the insurance industry." The leadership transition represents continuity in The Hartford's risk management approach, with Paiano, who has been with The Hartford since 1996 and has served as chief risk officer since 2017, transitioning to an advisory role on September 1 to ensure a smooth leadership change, capping a 40-year financial services career.

Market Conditions and Industry Trends

The insurance industry continues to navigate a complex environment of elevated catastrophe losses, persistent inflation in repair costs, and evolving regulatory landscapes. The Hartford's strategic focus on commercial lines, which generated strong top-line growth at highly profitable margins, positions the company well amid these challenges. The company's investment in technology and AI capabilities demonstrates its commitment to maintaining competitive advantages in underwriting precision and operational efficiency.

Climate-related events remain a significant factor, with Hurricane Helene contributing to elevated catastrophe losses in Q3 2024. However, The Hartford's sophisticated catastrophe modeling and conservative exposure management have enabled the company to maintain profitability despite these challenges.

Regulatory Developments

The insurance regulatory environment continues to evolve, with states implementing new requirements around climate risk disclosure, cybersecurity standards, and rate filing processes. The Hartford's proactive approach to regulatory compliance and its strong relationships with state insurance departments position it well to navigate these changes while maintaining pricing flexibility and market access.

XIV. Links & Resources

Annual Reports and Investor Presentations - The Hartford Investor Relations: https://ir.thehartford.com - Annual Reports Archive: https://ir.thehartford.com/financials/annual-reports/ - Quarterly Earnings Materials: https://ir.thehartford.com/financials/quarterly-results/ - SEC Filings: https://www.sec.gov/edgar/browse/?CIK=874766

Industry Research and Analysis - A.M. Best Company (Insurance Ratings) - Insurance Information Institute - National Association of Insurance Commissioners (NAIC) - S&P Global Market Intelligence Insurance Portal

Historical Documents and Archives - The Hartford Heritage Project - Connecticut Historical Society - Insurance Company Archives at Baker Library, Harvard Business School - Lloyd's of London Historical Collection

Books on Insurance History and The Hartford - "Hartford: An Illustrated History" by Glenn Weaver - "The Hartford of Hartford: An Insurance Company's Part in a Century and a Half of American History" by Hawthorne Daniel - "Risk and Reward: The Science of Casino Blackjack" (includes insurance probability theory)

Regulatory Filings and Governance Documents - The Hartford Proxy Statements - Corporate Governance Guidelines - Board Committee Charters - Code of Ethics and Business Conduct

Podcasts and Interviews with Management - Insurance Speak Podcast - The Insurance Guys Podcast - Carrier Management Executive Interviews - CNBC and Bloomberg TV interviews with Christopher Swift

Academic Papers on Insurance Economics - "The Economics of Insurance" - Journal of Economic Perspectives - "Insurance Market Dynamics" - NBER Working Papers - "Climate Change and Insurance Markets" - Risk Management and Insurance Review

Trade Publications and Industry Reports - Business Insurance Magazine - Insurance Journal - Carrier Management - PropertyCasualty360 - Best's Review

Historical Society Resources - Connecticut State Library Insurance Collection - Hartford History Center - New England Insurance History Project

Documentary Materials on ITT Era - "The Sovereign State of ITT" by Anthony Sampson - ITT Annual Reports 1970-1995 (SEC Archives) - Harvard Business School Case Studies on ITT-Hartford - Wall Street Journal Coverage of 1995 Spinoff

This comprehensive resource list provides multiple entry points for deeper research into The Hartford's history, current operations, and the broader insurance industry context. From primary source documents to contemporary analysis, these materials offer the foundation for understanding one of America's most enduring financial institutions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube