Halliburton: From Oil Well Cementing to Global Energy Services Giant

I. Introduction & Episode Roadmap

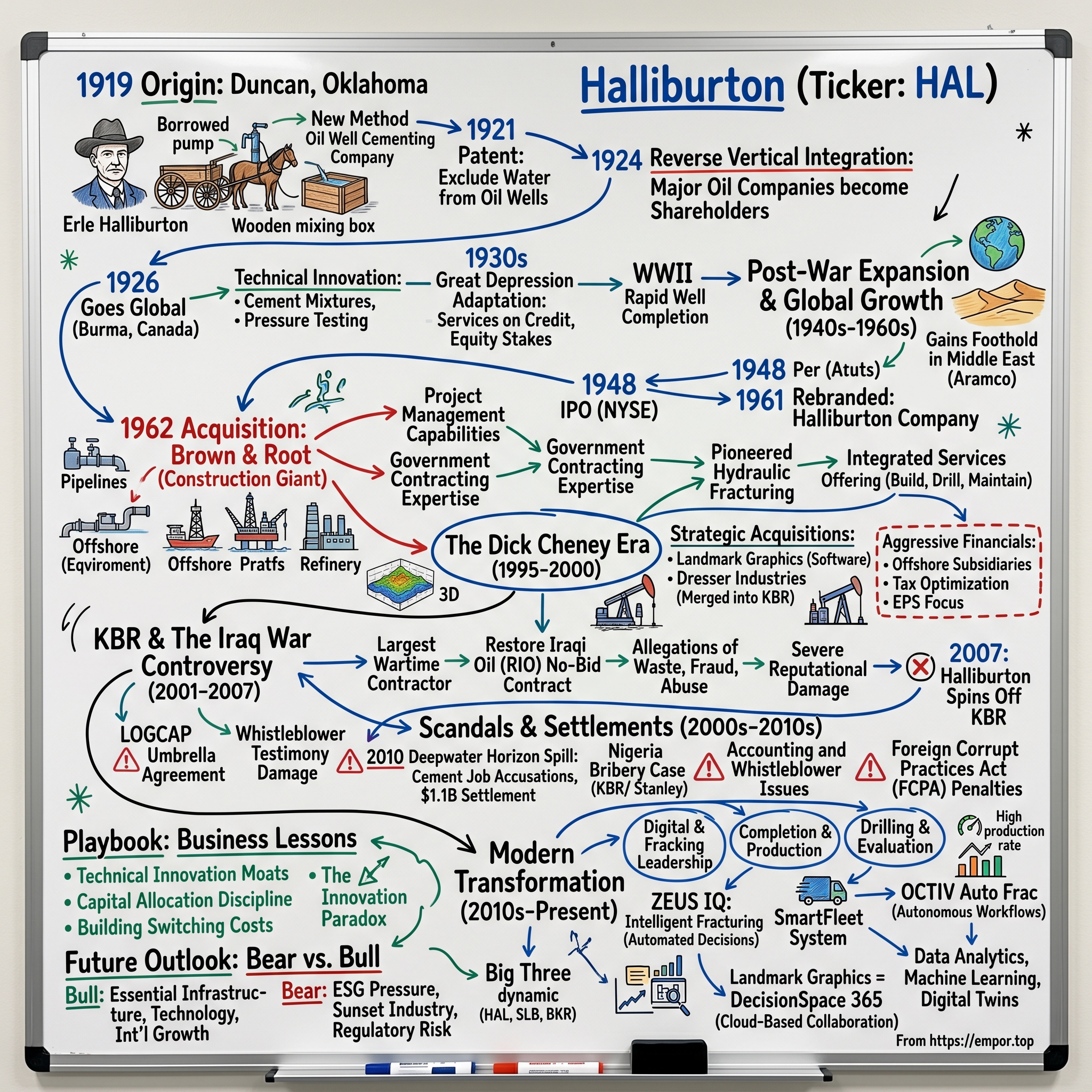

Picture this: It's 1919 in Duncan, Oklahoma. A Navy veteran named Erle Halliburton is mixing cement in a wooden box, using a borrowed pump and a horse-drawn wagon to service oil wells that nobody else wants to touch. Fast forward a century, and that humble operation has morphed into a $23 billion revenue colossus, employing 55,000 people across 70 countries, responsible for the majority of the world's hydraulic fracturing operations.

Halliburton today stands as the world's second-largest oilfield services company, a technological powerhouse that has literally shaped how humanity extracts energy from the earth. But between that borrowed pump and today's AI-powered fracturing systems lies a story of relentless innovation, controversial government contracts, geopolitical intrigue, and a former CEO who became Vice President of the United States.

How did a guy with a wagon and a wild idea about cementing oil wells build the foundation for one of the most controversial yet essential companies in modern energy? How did a technical services company become so intertwined with American foreign policy that its name became synonymous with the Iraq War? And how has it managed to reinvent itself as a digital technology leader while carrying decades of reputational baggage?

This is the story of three transformations: from mechanical to digital, from domestic to global, and from pure technical excellence to the messy intersection of business and geopolitics. It's a tale that teaches us about the power of patents, the perils of government contracting, and what happens when engineering brilliance meets political ambition.

We'll trace Halliburton's journey from those Oklahoma oil fields through the boom-bust cycles of the energy industry, into the corridors of power in Washington, through the sandstorms of Iraq, and into today's digital oilfield revolution. Along the way, we'll unpack the strategic playbook that allowed this company to survive and thrive through multiple existential crises while maintaining its position at the technological frontier of energy extraction.

II. The Erle Halliburton Origin Story (1919–1940s)

The year is 1918, and Erle P. Halliburton has just been discharged from the Navy. The Tennessee native, born in 1892, finds himself in California working for the Perkins Oil Well Cementing Company. But Erle isn't your typical employee—he's obsessed, constantly suggesting improvements to the cementing process. So obsessed, in fact, that his bosses find him obnoxious and fire him. Years later, Halliburton would say that getting hired and fired by Perkins were the two best things that ever happened to him.

Think about that for a moment. Here's a guy who gets canned for being too innovative, too pushy about making things better. In most stories, that's where the protagonist gives up. But Erle saw opportunity where others saw rejection. He'd learned enough about oil well cementing to know that the industry was doing it wrong—and more importantly, he knew how to do it right.

With a borrowed pump, a wagon and team of horses, and a wooden mixing box, Erle launched what he called the New Method Oil Well Cementing Company. The name wasn't fancy, but it was accurate. His method was genuinely new: a way to pump cement down oil wells to seal them properly, preventing water infiltration that plagued early oil extraction. In an era when most oil wells quickly became contaminated and useless, Halliburton's technique could extend their productive life dramatically.

On March 1, 1921, the U.S. Patent Office granted Halliburton a patent for his "method and means of excluding water from oil wells." This wasn't just a piece of paper—it was a monopoly on the best cementing technique in the industry. By late summer 1922, riding the wave of the Mexia, Texas oil boom, the renamed Halliburton Oil Well Cementing Company (HOWCO) had cemented its 500th well. The company was employing 56 people and growing fast.

Here's where Erle made a brilliant strategic move that would define Halliburton's DNA forever: in 1924, when he incorporated in Delaware, he didn't just take venture capital or bank loans. He sold equity stakes to seven major oil companies—Magnolia, Texas, Gulf, Humble, Sun, Pure, and Atlantic. His customers became his shareholders. Think about the elegance of this structure: your biggest clients now have a vested interest in your success, and you have guaranteed access to their wells. It's vertical integration in reverse—instead of the oil companies buying their supplier, the supplier made the oil companies buy into him.

The company's slogan captured Erle's relentless spirit: "We will get there, somehow." Not "we might get there" or "we'll try"—but a definitive statement of inevitable success coupled with an acknowledgment that the path might be unclear. This wasn't corporate puffery; it was a mission statement that employees lived. When a well needed cementing in the middle of nowhere, Halliburton crews would find a way to reach it, whether by truck, mule, or on foot.

By 1926, Halliburton was already thinking globally. The company sold five cementing units to an English company operating in Burma, marking the beginning of its Eastern Hemisphere operations. Erle's brothers expanded the business into Alberta, Canada, following the oil boom north. This wasn't opportunistic expansion—it was systematic. Wherever oil was being extracted inefficiently, Halliburton could add value.

The technical innovations kept coming. Halliburton wasn't content with just cementing wells; the company pioneered new tools and techniques that became industry standards. They developed specialized cement mixtures for different geological conditions, created pressure-testing equipment to ensure well integrity, and built custom trucks that could mix and pump cement on-site. Each innovation was patented, creating a thicket of intellectual property that competitors couldn't easily navigate around.

By the 1930s, as America plunged into the Great Depression, Halliburton faced its first existential crisis. Oil prices collapsed, drilling slowed, and customers couldn't pay their bills. Lesser companies folded, but Halliburton adapted. They offered services on credit, took equity stakes in struggling oil fields, and even bartered services for crude oil that they could sell later. Erle understood something fundamental: in a cyclical industry, survival during downturns determines who dominates during upturns.

The company also began diversifying beyond cementing. They moved into well logging, formation testing, and perforating—all services that helped oil companies understand what was happening thousands of feet below ground. Each new service created more customer touchpoints, more revenue streams, and more technical moats. By 1940, Halliburton wasn't just a cementing company; it was becoming an integrated oilfield services provider.

As World War II began, Halliburton found itself in a unique position. The war effort needed oil, lots of it, and quickly. The company's expertise in rapid well completion became a strategic asset. They worked around the clock to cement wells that would fuel Allied planes, tanks, and ships. The war years taught Halliburton how to operate at unprecedented scale and speed—lessons that would prove invaluable in the post-war boom that was about to begin.

III. Post-War Expansion & Global Growth (1940s–1960s)

The year 1946 marked a pivotal moment. With Europe rebuilding and global energy demand exploding, Halliburton made a bet that would define its next half-century: the company went truly global. Teams landed in Colombia, Ecuador, and Peru, following American oil companies developing South American fields. But the real prize was the Middle East. Halliburton began servicing the Arabian-American Oil Company—the forerunner of Saudi Aramco—gaining a foothold in what would become the world's most important oil region.

Consider the audacity of this move. Here's an Oklahoma company, barely 25 years old, sending roughnecks and engineers to the Arabian desert where temperatures hit 120 degrees, where sandstorms could destroy equipment in minutes, where the cultural and linguistic barriers seemed insurmountable. But Halliburton crews adapted, developing specialized equipment for desert conditions, learning Arabic, building relationships with local rulers. They weren't just exporting services; they were exporting expertise and adapting it to local conditions.

In 1948, Halliburton went public on the New York Stock Exchange. The IPO wasn't just about raising capital—it was about institutionalizing the company beyond the Halliburton family. Public markets meant quarterly earnings, professional management, and the discipline of external scrutiny. For a company built on one man's vision, this was a critical transition toward becoming a true institution.

By 1951, just three years after going public, Halliburton had expanded to 190 locations in 20 countries. The speed of this expansion was breathtaking. They weren't just following oil companies anymore; they were often arriving first, helping discover and develop new fields. The company had become essential infrastructure for the global energy industry.

Then, in 1957, Erle P. Halliburton died in Los Angeles. The founder's death could have been catastrophic—many companies built around charismatic founders struggle to survive the transition. But Erle had built something bigger than himself. The patents, the processes, the culture of technical excellence—these survived. The company had been institutionalized.

The post-Erle era began with a symbolic change: in 1961, the company dropped "Oil Well Cementing" from its name, becoming simply Halliburton Company. This wasn't just rebranding; it reflected a fundamental strategic shift. Cementing was now just one service among many. The company offered everything from drilling fluids to well testing, from pipeline construction to offshore platforms.

But the real transformation came in 1962 with the acquisition of Brown and Root, a Houston-based construction giant. This wasn't an obvious move—what did construction have to do with oil wells? Everything, as it turned out. Brown and Root brought massive project management capabilities, government contracting expertise, and a whole new revenue stream building infrastructure for the energy industry. Refineries, pipelines, offshore platforms—suddenly Halliburton could build the entire energy infrastructure, not just service the wells.

The Brown and Root acquisition also brought something else: deep government connections. The company had built military bases during World War II, worked on NASA facilities, and had relationships throughout Washington. These connections would prove both valuable and problematic in decades to come, but in the 1960s, they opened doors to massive federal contracts.

By the late 1960s, Halliburton was riding high. The company had pioneered hydraulic fracturing—using high-pressure fluids to crack rock formations and release trapped oil and gas. This technology would later become controversial, but in the 1960s, it was revolutionary, unlocking reserves that were previously uneconomical to extract. Halliburton held key patents and had more experience than anyone in making fracking work.

The global footprint kept expanding. Halliburton crews were working in the North Sea as offshore drilling took off, in Indonesia as that nation developed its resources, in Nigeria as African oil emerged. Each new geography brought challenges—different geology, different regulations, different politics—but also opportunities to develop new technical solutions that could be exported elsewhere.

The integration of Brown and Root created unexpected synergies. When an oil company needed to develop an offshore field, Halliburton could design and build the platform (Brown and Root), drill and complete the wells (Halliburton Services), and maintain the entire operation. This full-service capability was unique in the industry. Competitors could match Halliburton on individual services, but nobody could match the integrated offering.

By 1970, Halliburton had grown into something Erle probably never imagined: a multinational conglomerate with tens of thousands of employees, billions in revenue, and operations on every continent except Antarctica. The company that started with a borrowed pump was now essential to global energy supply. But this success brought new challenges—size brought bureaucracy, global operations brought political risk, and the energy industry itself was about to enter a period of unprecedented volatility.

The early 1970s energy crisis would test everything Halliburton had built. Oil prices quadrupled almost overnight, creating both massive opportunity and dangerous instability. The company would need new leadership, new strategies, and new capabilities to navigate what was coming. Before the energy industry's decline beginning in 1982, Halliburton operations reached a peak with revenues at $8.5 billion and a workforce of 115,000—massive scale that would soon become a liability as the industry contracted.

IV. The Dick Cheney Era & Strategic Acquisitions (1995–2000)

In August 1995, Halliburton's board made a shocking decision. They hired Dick Cheney—former Secretary of Defense under George H.W. Bush, architect of the Gulf War, consummate Washington insider—as CEO and Chairman. Cheney had zero experience running a public company, had never worked in the energy industry, and his main qualification seemed to be his Rolodex. The stock market was skeptical; analysts questioned whether a politician could run a complex technical services company.

But the board saw something others missed. The post-Cold War world was reshaping global energy markets. Countries that had been off-limits were opening up. Massive infrastructure projects were being planned from the Caspian to the South China Sea. Halliburton didn't need another engineer as CEO; it needed someone who could navigate the intersection of geopolitics and business. Cheney was uniquely positioned to do exactly that.

Cheney inherited a company that Thomas H. Cruikshank had already streamlined. Cruikshank, who served from 1989 to 1995, had executed a painful but necessary restructuring, cutting costs and focusing on core competencies. Net income had risen to $178 million in 1994—respectable but not spectacular for a company of Halliburton's size. Cheney's mandate was growth, and he immediately launched one of the most ambitious acquisition sprees in company history.

His first major move came in October 1996: acquiring Landmark Graphics Corp for $550 million in stock. Landmark was a software company specializing in 3D seismic visualization and reservoir modeling. This wasn't just buying technology; it was buying the future. Landmark's software could help oil companies "see" underground formations before drilling, dramatically improving success rates. For Halliburton, this meant moving up the value chain from executing drilling programs to actually designing them.

But the real bombshell came in 1998 when Halliburton merged with Dresser Industries in a $7.7 billion deal. Dresser brought a massive portfolio of drilling equipment, pump manufacturing, and measurement tools. More importantly, it brought Kellogg, a major engineering and construction firm that, when combined with Brown and Root, created Kellogg Brown & Root (KBR)—instantly one of the world's largest engineering and construction companies.

The Dresser merger was classic Cheney—bold, complex, and controversial. Critics argued Halliburton was paying too much for a company with significant asbestos liabilities. But Cheney saw synergies others didn't. Dresser's equipment manufacturing combined with Halliburton's services created a vertically integrated offering. When Halliburton designed a fracturing program, it could now manufacture the pumps, provide the crews, and analyze the data—capturing value at every step.

Under Cheney's leadership, Halliburton's government services business exploded. The company won contracts to support U.S. military operations in the Balkans, built facilities at Guantanamo Bay, and expanded its logistics support for the Army. Cheney's Pentagon connections obviously helped, but he was careful to maintain plausible distance from direct contract negotiations. The revolving door between government and industry was nothing new, but Cheney elevated it to an art form.

Here's where things get murky. According to later Washington Post reporting, Halliburton held stakes in two firms that signed contracts worth $73 million to sell oil production equipment to Iraq while Cheney was CEO—despite U.S. sanctions. Cheney claimed he wasn't aware of these dealings, conducted through foreign subsidiaries. Whether true or not, it established a pattern of aggressive interpretation of sanctions that would follow Halliburton for decades.

The financial engineering under Cheney was equally aggressive. The number of Halliburton subsidiaries in offshore tax havens increased from 9 to 44 during his tenure. The company's tax bill dropped dramatically—from paying $302 million in taxes in 1998 to receiving an $85 million refund in 1999. This wasn't illegal, but it raised eyebrows about a company led by a former Defense Secretary using every loophole to avoid paying U.S. taxes.

Cheney also transformed Halliburton's culture. The company had always been engineering-focused, priding itself on technical excellence. Cheney brought a more financial, deal-making mentality. Performance metrics shifted from operational efficiency to earnings per share. Stock options became a major component of executive compensation. The company started thinking more like an investment bank that happened to drill oil wells.

By 2000, when Cheney left to join George W. Bush's presidential ticket, Halliburton looked radically different than when he arrived. Revenue had doubled to $15 billion. The company had leading positions in virtually every segment of oilfield services. The stock price had risen from $20 to over $50. On paper, the Cheney era was a spectacular success.

But Cheney left behind time bombs. The Dresser acquisition brought massive asbestos liabilities that would plague Halliburton for years. The aggressive tax strategies attracted IRS scrutiny. The government contracts, especially a mysterious umbrella contract called LOGCAP (Logistics Civil Augmentation Program), would soon thrust Halliburton into the center of American foreign policy in ways nobody could have predicted.

Cheney's departure package was as controversial as his tenure. He received $36 million in severance, plus deferred compensation that would continue paying out while he served as Vice President—creating an unprecedented situation where the sitting VP was receiving payments from a company bidding on massive government contracts. Cheney claimed he had no influence over Halliburton after leaving, but the optics were terrible and would haunt both him and the company through the Iraq War.

V. KBR, Iraq War & The Controversy Years (2001–2007)

March 2003. American forces are racing toward Baghdad. Behind them comes an army of contractors, and at the forefront is KBR, Halliburton's engineering and construction subsidiary. Within days of the invasion, KBR crews are extinguishing oil well fires, rebuilding infrastructure, and operating military bases. By the time the dust settles, KBR will have received over $39 billion in Iraq-related contracts—the largest wartime contractor in American history.

To understand how Halliburton became synonymous with the Iraq War, we need to revisit KBR's origins. Brown & Root, acquired back in 1962, had been building military infrastructure since World War II. The company constructed bases in Vietnam, supported operations in Somalia, and maintained facilities in the Balkans. When combined with Kellogg after the Dresser merger, KBR became a unique entity—a private company capable of deploying thousands of workers into war zones to build and operate entire military installations.

The key to KBR's Iraq dominance was LOGCAP—the Logistics Civil Augmentation Program. This wasn't a specific contract but rather an umbrella agreement that allowed the military to quickly assign tasks without competitive bidding. KBR had won the LOGCAP contract in 2001, before 9/11, through a competitive process. But when Iraq operations began, the Army used LOGCAP to assign KBR massive no-bid contracts, arguing that speed was essential and KBR was the only company with the necessary capabilities.

The most controversial was the Restore Iraqi Oil (RIO) contract. In March 2003, the Army Corps of Engineers awarded KBR a no-bid contract to extinguish oil well fires and restore Iraq's oil infrastructure. The contract was "cost-plus"—meaning KBR would be reimbursed for all costs plus a guaranteed profit percentage. It had no ceiling, no time limit, and minimal oversight. KBR would essentially have a blank check to rebuild Iraq's oil industry.

Bunnatine Greenhouse, the Army Corps' top contracting official, objected strenuously. She argued the contract should be competed, limited in duration, and have spending caps. Her objections were overruled. When she continued to protest, she was demoted. She later testified to Congress that the RIO contract was "the most blatant and improper contract abuse I have witnessed during the course of my professional career."

As KBR's operations in Iraq expanded, so did the allegations of waste and fraud. Whistleblowers reported KBR was serving troops spoiled food, providing contaminated water, and billing for services never performed. A draft Pentagon audit found KBR had overcharged $61 million for fuel alone—buying gas from Kuwait at inflated prices when cheaper sources were available. KBR charged $45 per case of soda, $100 per bag of laundry. The company billed for 42,000 meals per day when only 14,000 soldiers were being fed.

The human cost was even more troubling. KBR subcontracted security to companies that employed poorly trained guards, leading to incidents where contractors opened fire on civilians. KBR truck drivers, many recruited from the American South with promises of high pay, found themselves driving through combat zones without adequate protection. When convoys were attacked, the military often couldn't or wouldn't provide support, arguing that protecting contractors wasn't their primary mission.

Former KBR employees began coming forward with damaging testimonies. Marie deYoung, a former KBR logistics specialist, testified that her supervisors ordered her to approve invoices without documentation. "I was instructed to pay vouchers regardless of whether they were correct," she told Congress. Another whistleblower revealed KBR was billing the government for brand-new trucks that were abandoned after minor problems like flat tires—it was more profitable to buy new trucks than fix old ones under the cost-plus structure.

The political fallout was devastating. Democrats hammered the Bush administration over the Halliburton connection. Dick Cheney's continuing deferred compensation payments from Halliburton—$398,548 received while serving as Vice President—created the appearance of conflict of interest, even though Cheney claimed he had no role in contract awards. Every KBR scandal became a Cheney scandal, every wasted dollar was attributed to cronyism.

Halliburton's management tried to distance themselves from the controversy. CEO Dave Lesar repeatedly testified that the company was performing essential services in dangerous conditions, that any waste was minimal compared to the scope of operations, and that KBR employees were patriots supporting American troops. But the damage to Halliburton's reputation was severe and lasting.

By 2006, the situation had become untenable. KBR's government business was generating massive revenues but also massive headaches. The legal costs were mounting—defending against fraud allegations, filing claims against the government for disputed payments, managing congressional investigations. The reputational damage was affecting Halliburton's core energy services business, with some oil companies reluctant to be associated with the "Iraq War contractor."

On April 5, 2007, Halliburton announced it was spinning off KBR as an independent company. The separation was complex—KBR took the government contracts but also the associated liabilities. Halliburton received $2.5 billion in cash and eliminated a massive distraction. CEO Dave Lesar called it "the right decision for our shareholders, customers, and employees."

The KBR spinoff marked the end of an era. Halliburton would return to its roots as an energy services company, leaving the military contracting business behind. But the scars remained. Years later, Halliburton would still be fighting lawsuits related to Iraq, still be defending its reputation, still be explaining how a company founded to cement oil wells ended up at the center of America's most controversial war.

VI. Scandals, Settlements & Reputation Management (2000s–2010s)

April 20, 2010. The Deepwater Horizon drilling rig explodes in the Gulf of Mexico, killing 11 workers and triggering the worst oil spill in U.S. history. As investigations unfold, a critical fact emerges: Halliburton had performed the cement job on the well just 20 hours before the blowout. The company that built its reputation on cementing excellence now faced accusations that its faulty cement contributed to an environmental catastrophe.

The Deepwater Horizon disaster was particularly devastating for Halliburton because it struck at the company's core competency. Internal documents revealed that Halliburton knew its cement slurry was unstable but proceeded anyway. Tests showing the cement mixture was likely to fail were never shared with BP. The presidential commission investigating the disaster concluded that Halliburton bears significant responsibility for the blowout.

Halliburton fought the allegations vigorously, arguing that BP's well design was fundamentally flawed and that BP ignored Halliburton's recommendations for additional safety measures. But the damage was done. In September 2014, Halliburton agreed to pay $1.1 billion to settle the majority of claims against it—a massive sum, though far less than BP's $20 billion liability.

But Deepwater Horizon was just one scandal among many. The Nigeria bribery case, inherited from the Cheney era, finally came to a head. Between 1994 and 2004, KBR had participated in a scheme to pay $180 million in bribes to Nigerian officials to secure $6 billion in liquefied natural gas contracts. The bribes were funneled through a British lawyer and Japanese trading companies to create distance from KBR, but investigators unraveled the scheme.

In 2009, Halliburton and KBR agreed to pay $579 million to settle criminal and civil charges—at the time, the largest Foreign Corrupt Practices Act penalty in history. Albert "Jack" Stanley, KBR's former CEO, was sentenced to 30 months in prison. The case revealed a culture where bribery was seen as a necessary cost of doing business in certain countries—a culture that Halliburton claimed to have reformed but that continued to damage its reputation.

The whistleblower retaliation cases were equally damaging. Anthony Menendez, a Halliburton accounting director, discovered that the company was systematically understating costs on long-term projects to boost quarterly earnings. When he raised concerns internally, he was marginalized and eventually forced out. He filed a complaint with the SEC, triggering an investigation that revealed Halliburton had concealed billions in cost overruns.

In 2015, a jury found Halliburton guilty of illegal retaliation against Menendez, awarding him $30 million in damages. The verdict was particularly embarrassing because it came just as Halliburton was trying to rebuild its reputation as an ethical company. The jury found that Halliburton had violated the Sarbanes-Oxley Act's whistleblower protections—provisions enacted specifically to prevent the kind of accounting fraud Menendez had uncovered.

The company also faced scrutiny over its tax strategies. A 2010 investigation revealed that Halliburton had avoided billions in U.S. taxes by routing profits through Dubai and other tax havens. While legal, the strategies were politically toxic—a company that had profited enormously from U.S. government contracts was doing everything possible to avoid paying U.S. taxes. Senator Carl Levin called Halliburton's tax avoidance "particularly offensive" given its role as a major defense contractor.

Throughout this period, Halliburton employed an army of lawyers, lobbyists, and public relations specialists to manage the fallout. The company spent millions on lobbying Congress, hired former government officials to navigate regulatory agencies, and launched advertising campaigns emphasizing its role in American energy independence. But every settlement, every scandal, added to a narrative that Halliburton was a company that put profits above ethics.

The financial impact was substantial but manageable. Between 2007 and 2015, Halliburton paid over $3 billion in settlements, fines, and legal costs related to various scandals. But with annual revenues exceeding $20 billion, the company could absorb these costs. The reputational damage was harder to quantify but arguably more lasting. Halliburton became a symbol of corporate malfeasance, referenced in movies, documentaries, and political speeches as shorthand for corruption.

Internally, the scandals forced real changes. Halliburton implemented new compliance programs, hired chief ethics officers, and created anonymous hotlines for reporting misconduct. The company required extensive anti-bribery training and instituted rigorous review processes for high-risk contracts. Whether these changes reflected genuine reform or merely better scandal management remained debatable.

By 2015, CEO Dave Lesar was attempting to turn the page. "We've learned from our mistakes," he told investors. "Today's Halliburton is focused on technical excellence, ethical behavior, and creating value for all stakeholders." But the settlements kept coming. In 2017, Halliburton paid $29.2 million to settle SEC charges that it had inadequate internal controls. In 2018, the company settled a lawsuit alleging it had destroyed evidence related to Deepwater Horizon.

The cumulative effect of these scandals fundamentally changed how Halliburton operated. The company became more risk-averse, more bureaucratic, more focused on compliance than innovation. Some argued this was necessary maturation; others saw it as a loss of entrepreneurial spirit. Either way, the swashbuckling company that would "get there, somehow" had evolved into something more careful, more corporate, and perhaps less dynamic.

VII. Modern Transformation: Digital & Fracking Leadership (2010s–Present)

Inside Halliburton's Real Time Operations Center in Houston, 2019. Wall-sized screens display live data from fracturing operations in the Permian Basin. An engineer in Houston adjusts pump pressure on a well in West Texas with a click. Another monitors sand concentration through sensors that relay information every second. This isn't your grandfather's oil field—it's the digital transformation of energy extraction, and Halliburton is leading the charge.

The company that Erle Halliburton founded with mechanical pumps and horse-drawn wagons has evolved into a technology powerhouse. Today's Halliburton operates in two main segments: Completion and Production (responsible for fracturing, intervention, and artificial lift) and Drilling and Evaluation (covering drilling services, wireline, and project management). But what distinguishes modern Halliburton isn't just what it does—it's how it does it.

The crown jewel of Halliburton's digital transformation is ZEUS IQ, an intelligent fracturing platform that represents the industry's most ambitious attempt to automate hydraulic fracturing. Launched in 2018, ZEUS doesn't just collect data—it makes decisions. The platform can automatically adjust pump rates, sand concentrations, and chemical mixtures based on real-time downhole conditions. It's machine learning applied to rock fracturing, and it's revolutionary.

Consider what this means: traditionally, fracturing operations required dozens of workers on site, making manual adjustments based on experience and intuition. ZEUS reduces that to a handful of operators monitoring screens, while algorithms optimize every aspect of the operation. The system can detect problems before they occur—a slight pressure anomaly that suggests an impending screen-out, a temperature variation indicating formation changes. It's preventive medicine for oil wells.

The Octiv Auto Frac service, introduced in 2020, takes automation even further. This is the industry's first truly autonomous fracturing service—customers can literally push a button and execute their fracturing design without human intervention. The system manages multiple pumps, adjusts to changing conditions, and optimizes performance in real-time. It's the oil field equivalent of a self-driving car, except it's navigating through rock formations thousands of feet underground.

The SmartFleet system, also launched in 2020, represents another leap forward. This intelligent automated fracturing system doesn't just operate pumps—it orchestrates entire fleets of equipment. SmartFleet can coordinate dozens of pumps, blenders, and sand conveyers, optimizing their interaction to maximize efficiency while minimizing wear. The system predicts maintenance needs, automatically schedules equipment rotations, and can even adjust operations to minimize emissions.

Halliburton's partnership with Chevron demonstrates how this technology translates to real-world results. Together, they developed autonomous workflows that adjust completion behavior based on subsurface feedback. The Sensori monitoring system provides continuous downhole intelligence, while OCTIV makes real-time adjustments. It's a closed-loop system where the well essentially tells the equipment how to optimize production.

The results are staggering. Wells completed with ZEUS show 15-20% higher production rates compared to conventional methods. Equipment uptime has increased by 25%. Most importantly, safety incidents have plummeted—with fewer workers on site and more operations controlled remotely, the dangerous work of fracturing has become significantly safer.

But Halliburton's digital transformation extends beyond fracturing. The company's Landmark subsidiary, acquired during the Cheney era, has evolved into a comprehensive digital ecosystem. DecisionSpace 365 provides cloud-based collaboration tools that allow geologists, engineers, and managers to work on the same data simultaneously from anywhere in the world. The platform integrates seismic data, well logs, production history, and economic models into a single environment.

The data analytics capabilities are particularly impressive. Halliburton processes petabytes of information daily—sensor readings, seismic surveys, production metrics. Machine learning algorithms identify patterns humans would never notice: subtle correlations between pump pressure and production decline, relationships between geological features and fracturing success. This isn't just big data; it's intelligence extraction from noise.

The company has also embraced digital twins—virtual replicas of physical assets that allow operators to test scenarios without real-world risk. Before fracturing an actual well, engineers can simulate thousands of variations in the digital twin, optimizing the design before committing resources. It's like having a practice field for million-dollar operations.

The competitive implications are profound. Schlumberger, Halliburton's primary rival, has its own digital initiatives, but Halliburton's focus on automation gives it an edge in North American unconventional plays where rapid, efficient fracturing is essential. Baker Hughes has partnered with tech companies like Microsoft, but Halliburton has chosen to develop most capabilities in-house, maintaining tighter integration and control.

The transformation hasn't been without challenges. Older field workers, some with decades of experience, have struggled to adapt to digital tools. The company has invested heavily in training programs, creating "digital academies" where roughnecks learn to code and engineers become data scientists. It's a cultural transformation as much as a technological one.

Cybersecurity has emerged as a critical concern. These digital systems, if compromised, could shut down oil production across entire regions. Halliburton has had to become as sophisticated about firewalls and encryption as it is about formation pressure and proppant selection. The company now employs hundreds of cybersecurity specialists—a job category that didn't exist in the oil field a decade ago.

Looking ahead, Halliburton is pushing into even more futuristic territory. The company is experimenting with autonomous drilling rigs that can operate with minimal human supervision. It's developing AI systems that can design entire well programs, from initial drilling to final completion. There's even research into using quantum computing to solve complex reservoir modeling problems that current computers can't handle.

The irony isn't lost on industry observers: Halliburton, a company synonymous with old-school oil extraction, has become one of the energy industry's most innovative technology companies. The company that started with mechanical cementing has evolved into something that looks more like a Silicon Valley tech firm that happens to work in oil fields. It's a transformation that would have seemed impossible even a decade ago, but it's essential for survival in an industry facing existential questions about its future.

VIII. Playbook: Business & Strategic Lessons

When studying Halliburton's century-long playbook, several strategic patterns emerge that explain both its survival through multiple industry cycles and its ability to maintain technological leadership despite reputational challenges. These lessons offer insights not just for energy companies but for any business navigating the intersection of technical excellence, government relationships, and cyclical markets.

First-Mover Advantages in Technical Innovation

Erle Halliburton's original patent for cementing oil wells wasn't just a technical breakthrough—it was a blueprint for how the company would compete for the next century. That 1921 patent created a temporary monopoly that generated cash flow, established customer relationships, and funded further innovation. This pattern repeated with hydraulic fracturing in the 1960s, horizontal drilling in the 1990s, and now with digital automation.

The key insight: being first matters less than being first with patents. Halliburton has consistently translated technical innovations into intellectual property moats. The company's current focus on "drilling technology, unconventionals, well intervention, and artificial lift" represents the latest iteration of this strategy—identifying technical bottlenecks and creating proprietary solutions before competitors recognize the opportunity.

The Power and Peril of Government Relationships

No aspect of Halliburton's playbook is more double-edged than its relationship with government. The Brown & Root acquisition brought capabilities to execute massive government projects, from Vietnam to Iraq. These contracts generated billions in revenue and provided stability during energy downturns. But they also created reputational damage that persists decades later.

The lesson here is nuanced: government relationships can provide countercyclical revenue streams, but they require different risk management than commercial contracts. The cost-plus structure that made KBR so profitable in Iraq also created perverse incentives for waste. The political connections that won contracts also attracted scrutiny when those contracts went wrong.

Vertical Integration Through Strategic Acquisitions

Halliburton's acquisition strategy reveals a pattern of buying capabilities rather than just assets. Brown & Root brought project management. Dresser brought manufacturing. Landmark brought software. Each acquisition expanded what Halliburton could offer customers, creating a one-stop shop for energy services.

But integration matters more than acquisition. The KBR spinoff demonstrated that not all capabilities belong under one roof. When synergies don't materialize or when one business damages another's reputation, divestiture becomes the right strategic move. Today's Halliburton, with 2024 revenue of $22.9 billion and operating income of $3.8 billion, is more focused than the conglomerate of the early 2000s—and more profitable as a result.

Managing Reputational Risk While Maintaining Market Position

Perhaps no company has maintained market leadership despite worse reputational damage than Halliburton. The Iraq War, Deepwater Horizon, bribery scandals—any one of these might have destroyed a lesser company. Yet Halliburton remains the world's second-largest oilfield services company.

How? Technical excellence provides resilience against reputational damage. When you're the only company that can efficiently fracture certain formations or cement deep-water wells, customers need you regardless of headlines. But this doesn't mean reputation doesn't matter—it just means technical moats can buy time for reputation repair.

The Transition from Service Provider to Technology Platform

Halliburton's digital transformation represents a fundamental shift in business model. Traditional oilfield services sold labor and equipment by the hour. Digital platforms sell outcomes and efficiency. The ZEUS platform doesn't just pump fracturing fluid; it optimizes entire well programs using machine learning.

This transition required massive cultural change. Training roughnecks to operate tablets instead of wrenches. Hiring data scientists alongside petroleum engineers. Building cybersecurity capabilities from scratch. The payoff has been substantial: the company generated over $2.6 billion in free cash flow in 2024, demonstrating that technology leadership translates to financial performance.

Capital Allocation During Commodity Cycles

Energy is cyclical, and Halliburton has survived by accepting rather than fighting this reality. During booms, the company invests in technology and acquisitions. During busts, it cuts costs and consolidates market share as weaker competitors fail. The key is maintaining financial flexibility to act countercyclically.

In Q4 2024, Halliburton generated $1.5 billion in cash from operations and returned 60% of free cash flow to shareholders through $1 billion in share repurchases. This capital allocation discipline—investing in technology while returning cash to shareholders—reflects lessons learned from previous cycles where overexpansion during booms led to painful restructuring during busts.

The Offshore Tax Haven Strategy and Financial Engineering

Cheney's expansion of Halliburton's offshore subsidiaries from 9 to 44 exemplified aggressive but legal tax optimization. While politically controversial, this strategy freed up billions for investment and acquisitions. The lesson: in commodity businesses with thin margins, every basis point of tax efficiency matters.

But there's a counter-lesson: tax optimization that appears unseemly can damage relationships with other stakeholders. Halliburton's tax strategies became ammunition for critics and complicated its government contracting business. Financial engineering must be balanced against reputational considerations.

Building Switching Costs Through Integrated Solutions

Halliburton doesn't just provide services; it embeds itself in customers' operations. When Chevron uses ZEUS for fracturing, they're not just buying pumping services—they're integrating Halliburton's technology into their completion workflows. Switching providers would require redesigning entire operational processes.

This strategy of building switching costs through integration rather than contracts provides more durable competitive advantages. Customers stay not because they're locked in legally but because the cost and risk of switching exceed any potential savings.

The Innovation Paradox

Here's the ultimate paradox in Halliburton's playbook: the company must constantly innovate to make its own services obsolete. The digital automation that makes fracturing more efficient also reduces the number of workers and equipment needed. The AI that optimizes drilling programs could eventually eliminate the need for human designers.

Yet Halliburton has embraced this self-disruption. Why? Because if they don't obsolete their own services, competitors will. Better to cannibalize your own revenue with superior technology than lose it entirely to disruption. This requires a culture that celebrates innovation even when it threatens existing business lines—a difficult balance that few century-old companies achieve.

IX. Bear vs. Bull Case & Industry Analysis

The Bull Case: Essential Infrastructure for the Energy Transition

Halliburton bulls see a company perfectly positioned for the next decade of energy development. Yes, the world is transitioning to renewable energy, but that transition will take decades, not years. As CEO Jeff Miller noted, he's "excited about the long term outlook" with plans to "drive value through our growth engines: drilling technology, unconventionals, well intervention, and artificial lift".

The math supports this optimism. Global oil demand continues growing, albeit at a slower pace. Natural gas, positioned as a "transition fuel," requires the same services Halliburton provides for oil. Even renewable energy requires hydrocarbons for manufacturing, transportation, and backup power. The energy transition isn't replacing oil and gas—it's adding renewables on top of growing fossil fuel consumption.

Halliburton's technological leadership in hydraulic fracturing gives it an almost unassailable position in North American shale. No other company can match its combination of equipment scale, operational expertise, and digital capabilities. The ZEUS platform and autonomous fracturing systems create switching costs that lock in customers for multi-year programs.

The international opportunity is even more compelling. National oil companies from Saudi Aramco to Petrobras need Halliburton's expertise to maximize recovery from mature fields and develop challenging new resources. These multi-decade relationships provide steady, high-margin revenue streams insulated from North American drilling volatility.

Financially, the bull case is straightforward. With 2024 revenue of $22.9 billion and adjusted operating income of $3.9 billion, Halliburton generates substantial cash flow even in a moderate commodity price environment. The company has cleaned up its balance sheet, divested non-core assets, and focused on returning cash to shareholders.

The digital transformation creates new revenue opportunities beyond traditional services. Software licenses, data analytics, and automation systems carry higher margins than pumping services. As Halliburton transitions from selling iron to selling intelligence, margins should expand even if revenue growth slows.

The Bear Case: Structural Decline in a Sunset Industry

Bears see Halliburton as a melting ice cube—profitable today but facing inevitable decline as the world abandons fossil fuels. Every Tesla sold, every wind turbine installed, every solar panel deployed reduces long-term demand for Halliburton's services. The company may be optimizing buggy whips just as automobiles arrive.

ESG concerns pose existential threats. Major investors are divesting fossil fuel investments. Banks are restricting lending to oil and gas projects. Insurance companies are refusing to cover certain operations. Halliburton may find itself unable to access capital markets or attract talent as sustainability concerns intensify.

The regulatory environment is turning hostile. Carbon taxes, drilling restrictions, and environmental regulations are increasing costs and limiting opportunities. The Biden administration's pause on LNG export permits shows how quickly policy can shift. A future administration could ban fracking entirely, destroying Halliburton's core business overnight.

Competition is intensifying from multiple directions. Schlumberger remains larger and more diversified. Baker Hughes is pivoting toward energy transition technologies. New entrants from tech companies to Chinese nationals are competing for contracts. Halliburton's technological moat may prove less durable than expected.

Management acknowledges headwinds, expecting "2025 to be sequentially softer in North America". This could be the beginning of a longer decline as shale drilling matures and international markets become more competitive. The easy money from the shale boom is over; future growth requires competing in more challenging, lower-margin markets.

The reputational overhang from past scandals continues to create problems. Government contracts remain politically sensitive. Environmental lawsuits pose ongoing liability. The company spends millions on lobbying and legal defense that could otherwise fund innovation or shareholder returns.

Competitive Positioning: The Big Three Dynamic

The oilfield services industry is dominated by three giants: Schlumberger, Halliburton, and Baker Hughes. Each has distinct strategies and positioning that illuminate Halliburton's competitive situation.

Schlumberger, with roughly $33 billion in revenue, remains the industry leader. It's more internationally focused than Halliburton, with particular strength in offshore and conventional fields. Schlumberger's digital initiatives are impressive, but its size makes rapid pivoting difficult. The company is essentially betting on international and offshore growth offsetting North American decline.

Baker Hughes, the smallest of the three at roughly $23 billion in revenue, has made the boldest strategic pivot. The company is investing heavily in energy transition technologies—carbon capture, hydrogen, geothermal. It's partnering with tech companies like Microsoft for digital capabilities. Baker Hughes is hedging its bets, maintaining oil and gas services while building new energy capabilities.

Halliburton has chosen a different path: doubling down on oil and gas excellence. While competitors diversify, Halliburton is perfecting its core services. This focused strategy could prove brilliant if oil and gas demand remains robust longer than expected. But it could leave the company stranded if the energy transition accelerates.

National oil companies increasingly compete with the Big Three by developing internal capabilities. Saudi Aramco, Petrobras, and others are building their own service arms, reducing dependence on foreign providers. This "insourcing" trend could limit international growth opportunities for all three major service companies.

Chinese competition is emerging as a significant threat. Companies like CNPC and Sinopec offer services at lower prices, particularly in Africa and Latin America. While they lack Halliburton's technical sophistication, they're improving rapidly and have government backing that Western companies can't match.

The Future of Oilfield Services

The industry faces a fundamental question: what happens to oilfield services in a net-zero world? The optimistic scenario sees continued demand for decades as developing nations industrialize and energy consumption grows. The pessimistic scenario sees rapid decline as alternatives become cheaper and climate policies tighten.

Reality will likely fall between these extremes. Oil and gas won't disappear overnight, but growth will slow and eventually reverse. The winners will be companies that can maintain profitability in a declining market while developing new capabilities for the energy transition.

Halliburton's strategy implicitly bets on a longer, slower transition. By focusing on efficiency and automation, the company can maintain margins even as activity declines. If oil prices stay elevated due to underinvestment in new production, Halliburton's services become even more valuable for maximizing output from existing fields.

The key variable is timing. If the energy transition takes 30-40 years, Halliburton has time to adapt. If it accelerates to 15-20 years, the company faces serious challenges. Management seems to be betting on the former, but preparing for the latter through cost reduction and capital discipline.

X. Epilogue & Reflections

Standing in Halliburton's Houston headquarters, you can feel the weight of history. Photos of Erle P. Halliburton line the halls—the Tennessee farm boy who started with a borrowed pump and built an empire. Display cases hold ancient drilling bits and early patents. But walk into the Real Time Operations Center, and you're transported into the future: wall-sized screens, real-time data streams, engineers controlling operations thousands of miles away.

This juxtaposition captures Halliburton's essential paradox. It's simultaneously one of America's oldest energy companies and one of its most technologically advanced. It carries the baggage of a controversial past while pioneering the digital future of resource extraction. It's reviled by environmentalists yet essential for the energy that powers modern civilization.

What would Erle Halliburton think of the company today? He'd likely be amazed by the technology—imagine explaining machine learning and autonomous fracturing to someone who mixed cement by hand. But he'd recognize the fundamental business: solving technical problems that others can't or won't solve, then scaling those solutions globally.

He might be troubled by the controversies. Erle built his company on technical excellence and customer service, not political connections and government contracts. The idea that Halliburton would become synonymous with war profiteering would likely appall him. Yet he was also a pragmatist who understood that business operates in the real world, not an ideal one.

The company's transformation from mechanical to digital would surely impress him. Erle was an innovator who constantly sought better methods. The ZEUS platform and autonomous systems represent exactly the kind of technical advancement he championed. That Halliburton leads in these technologies rather than being disrupted by them would validate his emphasis on innovation.

The Paradox of Being Essential Yet Controversial

Halliburton embodies a unique position in American capitalism: a company that's simultaneously essential and controversial, innovative and notorious, technically brilliant and ethically challenged. This paradox isn't easily resolved because both aspects are true.

The company is essential. Without Halliburton and its competitors, global oil and gas production would be significantly lower and more expensive. This would mean higher energy prices, reduced economic growth, and lower living standards. Like it or not, modern civilization depends on the hydrocarbons that Halliburton helps extract.

But the controversies are real too. The Iraq War profiteering, the Deepwater Horizon disaster, the bribery scandals—these aren't fabricated attacks but documented failures. The company's aggressive tax avoidance and political connections raise legitimate questions about corporate responsibility and the revolving door between business and government.

This duality makes Halliburton a Rorschach test for views on American capitalism. Supporters see a company that provides essential services, creates jobs, and drives innovation. Critics see a symbol of corporate excess, environmental destruction, and political corruption. Both views contain truth.

Lessons for Founders on Scaling, Succession, and Legacy

Halliburton's century-long journey offers valuable lessons for founders building enduring companies. First, technical excellence provides the most durable competitive advantage. Erle's original patents created a foundation that survived his death and continues generating value today. Building deep technical moats matters more than rapid scaling.

Second, succession planning is critical. Erle institutionalized his company before his death, ensuring continuity beyond the founder. The company's ability to attract leaders like Dick Cheney—whatever one thinks of his tenure—demonstrates the importance of building an institution that outlasts its creator.

Third, diversification must be strategic, not opportunistic. The Brown & Root acquisition made sense because construction and oil services had genuine synergies. But the company learned from KBR that not all diversification creates value. Focus matters as much as growth.

Fourth, reputation is easier to destroy than rebuild. Halliburton's technical excellence has allowed it to survive reputational crises that would destroy other companies. But the cost has been enormous—in legal fees, lost opportunities, and difficulty attracting talent. Better to avoid scandals than prove you can survive them.

Finally, adaptation is essential for longevity. The company Erle founded bears little resemblance to today's Halliburton beyond the name and culture of innovation. Successful succession means allowing the company to evolve beyond the founder's original vision while maintaining core values.

The Role of Energy Services in Geopolitics

Halliburton's history illuminates the inseparable relationship between energy and geopolitics. The company's expansion followed American foreign policy—into the Middle East after World War II, into Latin America during the Cold War, into Iraq during the War on Terror. Energy services aren't just businesses; they're instruments of national power.

This relationship creates opportunities and obligations. Halliburton has benefited enormously from American military and diplomatic support for its operations worldwide. But this also made the company a target for anti-American sentiment and created expectations of patriotic behavior that pure commercial entities don't face.

The future will likely see this relationship evolve rather than disappear. As great power competition intensifies, energy security becomes even more critical. Halliburton and its peers may find themselves caught between competing powers, forced to choose sides in ways that purely commercial logic wouldn't dictate.

Final Thoughts on Innovation, Ethics, and Corporate Power

Halliburton's story ultimately raises fundamental questions about corporate power in modern society. How much power should corporations wield? What obligations do they have beyond generating profits? How do we balance innovation with responsibility, efficiency with ethics?

The company's technical innovations have undeniably benefited society by making energy more abundant and affordable. The hydraulic fracturing technologies Halliburton pioneered transformed America from an energy importer to an exporter, with profound economic and geopolitical benefits. The digital technologies being developed today will make resource extraction more efficient and less environmentally damaging.

But innovation without ethics leads to disasters like Deepwater Horizon. Efficiency without responsibility leads to the waste and fraud seen in Iraq. Corporate power without accountability leads to tax avoidance and regulatory capture that undermine democratic governance.

The challenge for Halliburton—and for society—is finding the right balance. We need companies capable of solving complex technical challenges and operating at global scale. But we also need mechanisms to ensure these companies serve broader interests than just their shareholders.

Halliburton's next century will be shaped by how well it navigates these tensions. Can it maintain technical leadership while addressing environmental concerns? Can it operate globally while avoiding political entanglements? Can it generate profits while earning social legitimacy?

The answers will determine not just Halliburton's future, but the future of the energy industry and perhaps industrial capitalism itself. Because if a company with Halliburton's capabilities, resources, and importance can't solve these challenges, what company can?

As we reflect on Halliburton's journey from a borrowed pump to a digital powerhouse, one thing becomes clear: the next chapter of this story is still being written. The company that Erle P. Halliburton founded with mechanical cementing will help determine how humanity powers its future—whether through continued fossil fuel extraction, carbon capture and storage, or technologies we haven't yet imagined.

The only certainty is that the world will need energy, and companies with the technical capabilities to provide it will remain essential. Whether Halliburton can maintain its position while addressing its contradictions will determine if it thrives for another century or becomes a cautionary tale of corporate hubris.

For investors, policymakers, and citizens, Halliburton represents both the promise and peril of industrial capitalism—a company capable of remarkable innovation and troubling excess, essential services and ethical failures, technical brilliance and political corruption. Understanding this duality isn't just important for evaluating one company; it's essential for grappling with the role of corporate power in the 21st century.

The story that began with Erle P. Halliburton and his wooden mixing box continues today in digital control rooms and automated fracturing sites. Where it goes next depends on decisions being made right now—in boardrooms and trading floors, in regulatory agencies and legislative chambers, in engineering labs and on drilling platforms around the world.

Halliburton's future, like its past, will be written by those willing to get there, somehow.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube