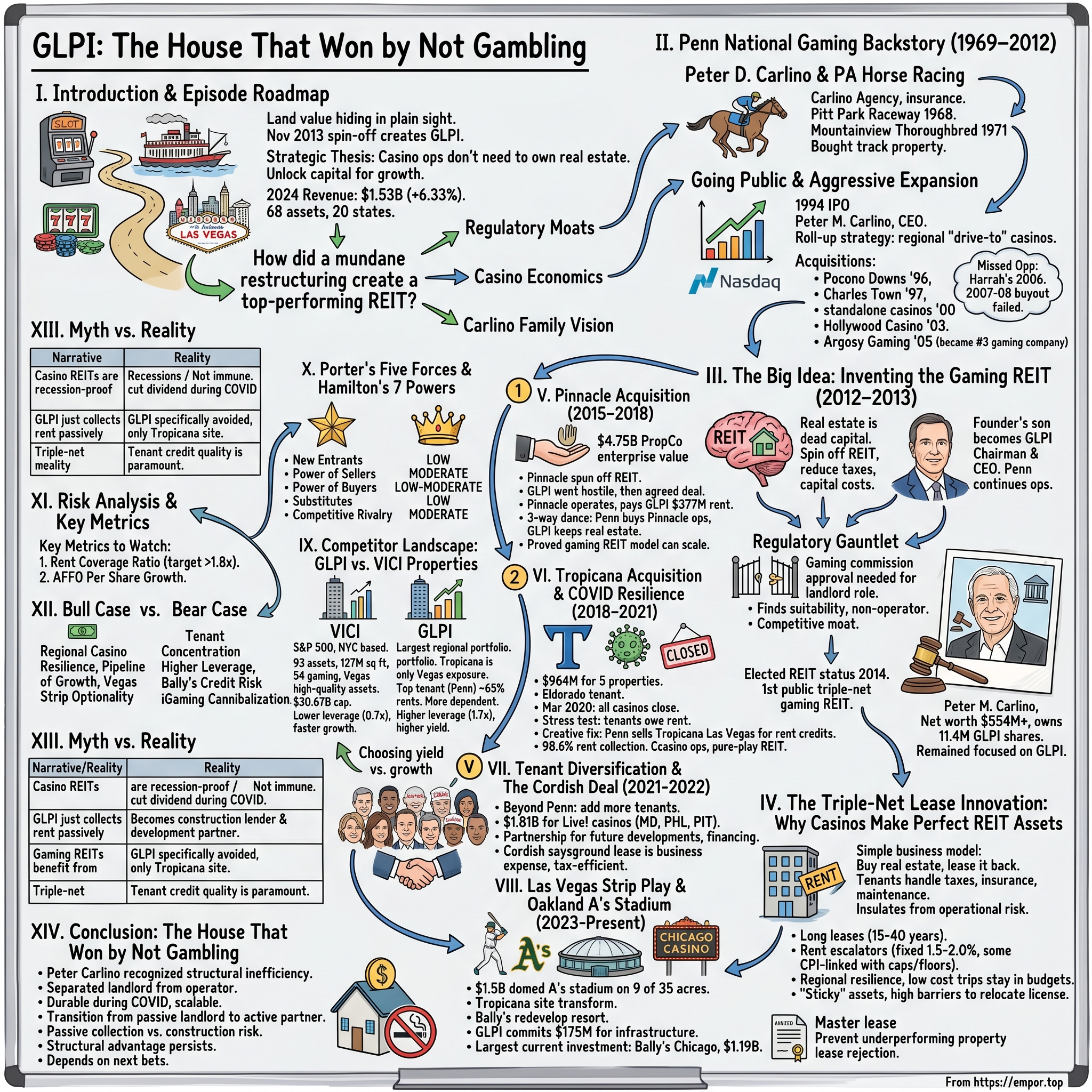

Gaming and Leisure Properties: The House That Won by Not Gambling

I. Introduction & Episode Roadmap

The most valuable insight in casino real estate was hiding in plain sight for decades. Underneath every slot machine whirring on a riverboat, beneath every blackjack table in a Las Vegas showroom, sat something far more valuable than the gambling floor above: the land itself.

In November 2013, a small-town Pennsylvania company did something that would reshape the entire gaming industry. Penn National Gaming, born from a horse track outside Harrisburg, spun off its real estate holdings into a separate entity called Gaming and Leisure Properties, Inc.—GLPI. The spin-off was completed on November 1, 2013, creating Gaming and Leisure Properties, Inc.

The strategic thesis was elegant in its simplicity: Why should a casino operator—a company Wall Street valued based on gaming revenues, slot hold percentages, and table game win rates—also own billions of dollars in real estate? Why should they tie up capital in land and buildings when that capital could fund acquisitions, marketing, or debt reduction?

In 2024, GLPI's revenue was $1.53 billion, an increase of 6.33% compared to the previous year's $1.44 billion. The company now sits atop 68 high-quality regional gaming assets spread across 20 states—a remarkable expansion from the 19 properties it began with just eleven years ago.

The question at the heart of this story is deceptively simple: How did a mundane accounting restructuring—separating real estate from operations—create one of the best-performing REITs of the past decade? The answer lies in understanding regulatory moats, the unique economics of casino properties, and the vision of a family that understood both horse racing and high finance.

This article traces GLPI's journey from a Pennsylvania racetrack to an institutional-grade landlord that has reshaped how the gaming industry thinks about capital allocation. Along the way, we'll examine the Pinnacle acquisition that proved the model could scale, the COVID stress test that vindicated the triple-net lease structure, the tenant diversification push that reduced concentration risk, and the audacious Las Vegas Strip play that could transform a 35-acre parcel into Major League Baseball's newest home.

II. The Penn National Gaming Backstory: From Horse Track to Casino Empire (1969–2012)

The Carlino Family and Pennsylvania Horse Racing

The story begins not with slot machines but with thoroughbreds and the Philadelphia suburb of Wyomissing—an improbable headquarters for what would become one of America's largest regional casino operators.

The youngest of nine in an Italian-American family from a modest rowhome neighborhood in working-class Philadelphia, the elder Carlino attended local parochial schools, including an all-male high school. Peter D. Carlino's path to gambling mogul passed through an unlikely sequence of jobs: florist, insurance salesman, title company executive. A workaholic, he also moonlighted selling fire and homeowners insurance door to door after finishing his day job, forming the Peter D. Carlino Agency as an agent for a fire insurance company linked back to Ben Franklin, Philly's original entrepreneur.

By the late 1960s, Pennsylvania had opened the door to thoroughbred racing with parimutuel wagering. Two companies that later formed part of Penn National Gaming were founded in 1968 by groups seeking one of the four available racing licenses: Pitt Park Raceway, Inc., formed by several Erie area businessmen, and the Pennsylvania National Turf Club, established by a group of Central Pennsylvania investors.

Pitt Park lost half a million dollars in its first meet, leading its owners to sell the company to a group of investors, including Philadelphia insurance businessman Peter D. Carlino. It was a classic case of following the money into a distressed asset—a pattern his son would replicate decades later on a much larger scale.

In 1971 Carlino formed Mountainview Thoroughbred Racing Association, which ran a thoroughbred racing meet at Penn National from its opening in 1972. A decade later, he acquired the racetrack property itself. From a florist shop to a racetrack—an only-in-America story of entrepreneurial ambition meeting regulatory opportunity.

Going Public and Aggressive Expansion

In May 1994, Penn National Gaming became a public company via an initial public offering on the Nasdaq, raising $18 million to pay down debt and fund construction of off-track betting parlors.

The younger Carlino—Peter M. Carlino, a Penn State graduate who had cut his teeth in real estate development—took the reins. In 1994 the track became the basis of Penn National Gaming when his family company went public. A son, Peter M. Carlino, oversaw the IPO, and he became CEO, a position he held until 2013, though he remained Penn's chairman for years.

What followed was a masterclass in roll-up strategy. Penn National didn't try to compete with the Vegas Strip titans. Instead, it pursued regional "drive-to" casinos—properties that served local markets rather than destination tourists.

The company acquires the Pocono Downs racetrack, near Wilkes-Barre, Pennsylvania in 1996. Penn National acquires 89 percent ownership of the Charles Town Race Track in West Virginia in 1997.

The pivot from racing to casino gaming accelerated at the turn of the millennium. The company acquired its first standalone casino properties in 2000, buying Casino Magic Bay St Louis and Boomtown Biloxi from Pinnacle Entertainment for $201 million.

Then came the deals that transformed the company. In 2003, Penn National bought Hollywood Casino Corp. for $328 million plus $360 million in assumed debt, gaining three casinos in Aurora, Illinois; Tunica, Mississippi; and Shreveport, Louisiana. The acquisition, which doubled Penn National's revenues, was part of a continuing strategy to shift away from the horse racing business and into the casino business.

In 2005, Penn National acquired Argosy Gaming Company for $1.4 billion plus $791 million in assumed debt, adding five casinos and one horse track to its portfolio. The purchase again doubled Penn National's size, making it, at the time, the third largest publicly held gaming company in the country.

The Regional Gaming Strategy

Penn's unique approach was geographic arbitrage. Vegas meant competition with MGM, Caesars, and the institutional capital flooding the Strip. Regional markets meant local monopolies, regulatory barriers to entry, and customers who would never book a flight to Nevada.

Penn's revenues grew from $40 million in 1994 to more than $1 billion by 2003. By 2001, Penn National Gaming had made Fortune magazine's 100 Fastest Growing Companies list at 58th. It jumped to 12th the following year.

The numbers tell the story of compound growth through disciplined acquisitions. But what made Penn special wasn't just deal-making—it was understanding that regional casinos were fundamentally different businesses than destination resorts. A riverboat in Baton Rouge or a racino in West Virginia served a local population that would return week after week, regardless of what happened in Vegas.

The Missed Opportunity: Harrah's Entertainment

Every great business story has a turning point that didn't happen. For Penn National, it was the failed bid to acquire Harrah's Entertainment in 2006.

Penn National Gaming failed in an attempt to acquire Harrah's Entertainment in 2006.

Imagine the alternative history: Penn National—a regional powerhouse from Pennsylvania—merging with Harrah's, the company that would become Caesars Entertainment. It would have created a gaming behemoth spanning Vegas and every regional market in America.

Instead, an attempt to take Penn private through a $6.1 billion buyout fell through in 2007-2008. The financial crisis had arrived, and with it came different opportunities—including the insight that would birth GLPI.

The failure to go private forced a rethink. If Penn couldn't take itself off the public markets, perhaps there was a different way to unlock value trapped in its balance sheet.

III. The Big Idea: Inventing the Gaming REIT (2012–2013)

The Strategic Insight

The real estate under casinos was dead capital. Penn National owned the land and buildings for dozens of properties, but Wall Street valued the company based on gaming metrics—revenue per available room, hold percentages, same-store gaming revenue growth. The real estate was just there, buried in the balance sheet, generating no explicit return.

Penn National Gaming created the gaming REIT when it spun GLPI off from Penn in 2013. Peter Carlino, who founded Penn National and served as its chairman for nearly 20 years, became chairman and CEO of the new REIT.

The innovation wasn't the REIT structure itself—real estate investment trusts had existed since the 1960s. The innovation was applying it to casinos, which had always been vertically integrated operations. Hotel companies had done it. Mall operators had done it. But gaming companies?

Penn National spun off a new real estate investment trust with ownership of most of its properties. The reorganization reduces taxes and capital costs and overcame license ownership restrictions for a time. A former rival called the move "brilliant" and said the innovation "redefined the future of the industry."

The arbitrage opportunity was structural. REITs trade at higher multiples than casino operators because they distribute most of their earnings as dividends, pay minimal corporate taxes, and own hard assets. By separating the real estate from the operations, Penn could surface the underlying value of its property portfolio—and give both entities more focused capital allocation strategies.

The Spin-Off Mechanics

On May 1, 2013, the planned REIT was officially named Gaming and Leisure Properties, reflecting its emphasis on gaming and leisure real estate holdings. The spin-off was approved by Penn National's board of directors on September 26, 2013, as part of a broader corporate breakup to distribute GLPI shares tax-free to Penn National shareholders.

Shareholders of record as of the close of business on October 16, 2013, received one share of GLPI common stock for every five shares of Penn National common stock held.

In November 2012, the company announced a plan to spin off a new real estate investment trust (REIT) with ownership of most of its properties, in an effort to reduce taxes and cost of capital, and overcome license ownership restrictions. The REIT owned the land and buildings for 21 of Penn National's 29 casinos and racetracks; Penn National continued to operate all but two of the properties under a lease agreement.

The Regulatory Gauntlet

Gaming isn't like other industries. Every property needs gaming commission approval. Every owner, every investor above a certain threshold, needs to be "found suitable"—a process involving background checks, financial disclosure, and ongoing regulatory oversight.

These regulations, aimed at safeguarding public interests, revenue generation, and operational integrity, mandate that GLPI obtain findings of suitability or approvals from gaming authorities for its landlord role in properties hosting casino operations. As a non-operator, GLPI avoids direct gaming licenses but must demonstrate that its ownership structure does not facilitate unsuitable influences, with charter provisions limiting individual share ownership to 7% to comply with both gaming suitability tests and REIT diversification rules under Internal Revenue Code Section 856.

This regulatory barrier would become one of GLPI's most important competitive moats. Any potential competitor would need to navigate gaming commission approvals across multiple states—a process that could take years and might fail entirely.

GLPI elected to be taxed as a real estate investment trust ("REIT") for United States federal income tax purposes commencing with the 2014 taxable year and is the first publicly traded triple-net lease REIT focused on gaming.

Peter Carlino: Running Both Companies

The founder's son now ran two public companies simultaneously.

Mr. Carlino has served as the Chairman of the Board of Directors and Chief Executive Officer of GLPI since its inception in February 2013. Mr. Carlino was the founder of PENN and served as our Chief Executive Officer of PENN from 1994 through October 2013. Mr. Carlino also served as the Chairman of the Board of Directors of PENN from 1994 through May 2019.

This dual role wouldn't last. Peter Carlino has stepped down from his position as chairman of Penn National Gaming, the company citing the federal Clayton Antitrust Act and the acquisition of Pinnacle Entertainment as requiring the move, which will leave him as chairman of the GLPI REIT. Company officials said the federal Clayton Antitrust Act requires the move, in the wake of Penn's acquisition last year of Pinnacle Entertainment. Carlino, who has been Penn's chairman since the company went public in 1994, will remain chairman and CEO of Gaming and Leisure Properties, the real estate investment trust spun off from Penn in 2013.

The estimated net worth of Peter M. Carlino is at least $554 Million dollars as of 2025-10-23. Peter M Carlino is the Chairman,CEO,President of Gaming and Leisure Properties Inc and owns about 11,466,890 shares of Gaming and Leisure Properties Inc (GLPI) stock worth over $516 Million.

Today, at 78 years old, Carlino remains firmly in control of GLPI, recently promoting Brandon Moore to President while maintaining his CEO title. "Brandon has been a key driver of the approach our excellent finance, accounting, development and legal teams take as they work closely with tenants and seek to identify and consummate new transactions for GLPI, while financing our growth with a prudent approach to capital allocation," Carlino said.

IV. The Triple-Net Lease Innovation: Why Casinos Make Perfect REIT Assets

The Business Model Deep Dive

GLPI's business model appears simple on the surface. Buy casino real estate. Lease it back to operators under triple-net leases. Collect rent. Repeat.

This model insulates GLPI from operational risks like patronage fluctuations, fulfilling REIT mandates such as 75% real estate asset allocation, 95% passive income sourcing, and 90% taxable income distribution, while enabling operators access to capital for expansions.

But the devil is in the details. "Triple-net" means the tenant is responsible for property taxes, insurance, and all maintenance. GLPI is engaged in the business of acquiring, financing, and owning real estate property to be leased to gaming operators in triple-net lease arrangements, pursuant to which the tenant is responsible for all facility maintenance, insurance required in connection with the leased properties and the business conducted on the leased properties, including coverage of the landlord's interests taxes levied on or with respect to the leased properties and all utilities and other services necessary or appropriate for the leased properties.

The lease structures are long—typically 15 to 40 years with multiple renewal options. GLPI has benefitted from the durability of its contractually guaranteed rental stream from regional casinos. GLPI has long (15-40 year leases) with strong casino operators including PENN Entertainment, Bally's, Ceasars and Boyd.

Rent escalators provide inflation protection. Most of GLPI's leases are subject to fixed escalators between 1.5-2.0%. While some of GLPI's leases are linked to CPI, all of these leases have narrow caps and floors which effectively fix rent growth in a narrow band of 0-2% annually.

Why Casinos Are Uniquely Suited

Critically, unlike their hotel REIT peers which have been among the worst-performing REIT sectors since the start of the pandemic, casino REITs' ultra long-term (15-50 year) triple-net master lease structure leaves most of the financial and operational risk - both on the upside and the downside - to their tenants. As a result, casino REITs have delivered some of the strongest 5-year returns in the REIT sector.

Consider the alternative. Hotel REITs typically use management agreements where the REIT bears operational risk. If occupancy falls, the REIT's income falls. Casino REITs like GLPI receive fixed rent regardless of how many tourists show up on any given weekend.

"What happens when it's time to upgrade these properties?" an industry analyst asked. "Under this triple net lease, the tenant is responsible for the maintenance of its properties, not the landlord. So what happens if their casino gets a little down in the dumps and it needs a billion-dollar makeover? They're going to have to pay for that."

Casinos are also "sticky" assets. The regulatory barriers to relocating a gaming license are enormous. A tenant can't simply move to a competing landlord's building—they'd need new gaming approvals, potentially in an entirely different jurisdiction. It is also worth noting that regional gaming properties (as opposed to properties on the Vegas strip) have shown to be more resilient during economic downturns. The reason for this is that relatively inexpensive local trips tend to remain in household budgets (while more expensive destination trips like Vegas may get cut).

Inflation Protection Built In

Market participants tend to treat triple-net REITs on par with longer-dated bonds, meaning these stocks can be vulnerable to rising interest rates. This year, however, investors are focusing more on the inflation-fighting advantages GLPI and VICI offer. "Despite their ultra-long term triple net lease structures, casino REITs are better protected from inflation than many initially presumed," added Hoya. "Inflation sensitivity is driven by several interacting factors, including external growth potential, lease structure and term, tenant credit quality, and the cyclicality of the underlying property type."

The master lease structure adds another layer of protection. The master lease structure requires that tenants make good on lease payments on all properties. From the landlord's perspective, the purpose of a master lease is effectively to prevent the tenant from getting the leases on underperforming properties rejected in bankruptcy court.

V. Key Inflection Point #1: The Pinnacle Acquisition (2015–2018)

The Hostile Approach

In 2014, Pinnacle Entertainment announced its own plan to spin off a REIT with its 15 casino properties. The announcement caught GLPI's attention immediately—here was a potential competitor emerging with a copycat strategy.

Rather than wait for Pinnacle to create a rival gaming REIT, GLPI went on offense. When Pinnacle didn't respond to private overtures, GLPI went public with its offer.

The Transformational Deal

Pinnacle Shareholders Will Receive 0.85 Shares of GLPI Per Pinnacle Share and One Share of OpCo. The agreed-upon exchange ratio gives PropCo an implied enterprise value of $4.75 billion, implying 12.6x initial year PropCo adjusted earnings before interest, taxes, depreciation and amortization (adjusted EBITDA).

GLPI and Pinnacle today announced that the companies have successfully completed the previously announced transactions pursuant to which GLPI has acquired substantially all of Pinnacle's real estate assets.

After the close of the transaction, Pinnacle will operate the leased gaming facilities under a triple-net 10-year Master Lease agreement with GLPI that will have five subsequent, five-year extension periods at Pinnacle's option. Pinnacle will initially pay GLPI $377 million in rent in the first year after close, which will result in a lease coverage ratio of 1.9x.

This was the deal that proved the gaming REIT model could scale beyond its Penn National origins. GLPI wasn't just Penn's captive landlord—it was a true third-party acquirer capable of executing complex transactions.

The Three-Way Penn-Pinnacle-GLPI Dance

The plot thickened in 2018. In December 2017, Pinnacle agreed to be acquired by Penn National Gaming for $2.8 billion in cash and stock.

Pinnacle Entertainment, Inc. was an American gambling and hospitality company. It was acquired by Penn National Gaming in 2018. At the time of acquisition, it operated sixteen casino properties, located in Colorado, Indiana, Iowa, Louisiana, Mississippi, Missouri, Nevada, Pennsylvania, and Ohio.

The result was a three-way dance that consolidated the industry while expanding GLPI's tenant relationships. Penn National acquired Pinnacle's operations, but GLPI kept the real estate—and now had a bigger, more diversified tenant in Penn National.

The capstone to Wilmott's career at Penn was the 2018 purchase of Pinnacle Entertainment for $2.8 billion. The buy solidified Penn as the leading regional casino company, and relegated Carlino to his current non-voting chairman emeritus status on Penn's board (due to antitrust regulations).

VI. Key Inflection Point #2: The Tropicana Acquisition & COVID Resilience (2018–2021)

The Tropicana Entertainment Deal

In 2018, another major gaming operator was ready to sell. Tropicana Entertainment, controlled by corporate raider Carl Icahn, operated seven casinos across six states.

GLPI announced that it has successfully completed the previously announced acquisition of the real estate assets of five casino properties from Tropicana Entertainment for $964 million. The assets to be acquired are Tropicana Atlantic City, Tropicana Evansville, Tropicana Laughlin, Trop Casino Greenville and The Belle of Baton Rouge.

Eldorado will pay GLPI approximately $110 million in rent and interest in the first year. The deal added another major tenant—Eldorado Resorts, which would later merge with Caesars Entertainment—further diversifying GLPI's tenant base.

COVID-19: The Stress Test

Then came March 2020. Every casino in America closed its doors.

For a triple-net lease REIT, this was the ultimate stress test. Tenants with zero revenue would still owe rent. Would they pay? Would they survive?

On April 16, 2020, the Company and certain of its subsidiaries acquired the real property associated with the Tropicana from Penn National Gaming, Inc. in exchange for rent credits of $307.5 million, which will be applied to rent due under the parties' existing leases for the months of May, June, July, August, October and a portion of November 2020.

The Tropicana Las Vegas transaction was creative problem-solving under duress. Penn National desperately needed liquidity. GLPI needed to ensure its rent stream wasn't interrupted. The solution: Penn sold the Tropicana Las Vegas—its one Strip property—to GLPI in exchange for rent credits that would cover several months of lease payments.

While all of GLPI's tenants' properties as well as the Company's two TRS properties were closed in mid-March as a result of COVID-19 related precautions, the Company collected 98.6% of contractual April rent.

"For GLPI, we are receiving attractive real estate value which represents a prudent and thoughtful approach toward ensuring that our shareholders are made economically whole while positioning Penn National with a healthier runway to navigate the impacts of COVID-19 over the long term. These strategic transactions strengthen the credit support behind GLPI's rent payments, allows GLPI to control a unique and iconic site on the Las Vegas Strip without carrying costs."

The Dividend Cut and Recovery

Not everything went smoothly. Both REITs have since increased dividends a few more times, but the dividend cut marred Gaming and Leisure Properties' share value versus VICI properties. Between March 1, 2020, and March 1, 2021, Gaming and Leisure's total return was only 0.26%, while VICI Properties' total return was 22.17%. But since March 2021, Gaming and Leisure have outperformed VICI Properties, with total returns of 29.24% and 20.26%, respectively.

The pandemic became a buying opportunity. While competitors were frozen, GLPI was structuring deals. The Tropicana Las Vegas acquisition gave GLPI a 35-acre footprint on the Las Vegas Strip—a site that would prove far more valuable than anyone imagined.

Pivoting to Pure Real Estate

The Company also completed on December 17, 2021, the previously announced sale of the operations of Hollywood Casino Baton Rouge to Casino Queen Holding Company for total cash consideration of $28.2 million.

By 2021, GLPI had sold the operations of its two owned-and-operated casinos, completing its transformation into a pure-play real estate owner.

VII. Key Inflection Point #3: Tenant Diversification & The Cordish Deal (2021–2022)

Beyond Penn National

GLPI's origin as a Penn National spin-off created an obvious concentration risk. If Penn National stumbled, GLPI would feel the pain. The solution: add more tenants.

GLPI did score a win in late 2021 with a major $1.8B acquisition of the Live! casinos in Maryland, Philadelphia, and Pittsburgh from Cordish Companies. Acquired at a 6.9% cap rate, the acquisition is GLIP's largest since 2016 and helps to diversify its tenant base further.

The initial transaction has an aggregate consideration of approximately $1.81 billion.

The master lease and single asset lease will have an initial term of 39 years, with a maximum term of 60 years inclusive of tenant renewal options. The initial annual cash rent for all three properties will be $125.0 million, with a 1.75% fixed yearly escalator on the entirety of the rent commencing upon the leases' second anniversary, representing an implied capitalization rate of 6.9%.

But the Cordish deal was more than a one-time acquisition. The transaction for the three properties includes not only the existing real estate assets, but also a binding partnership on future Cordish casino developments, as well as potential financing partnerships between GLPI and Cordish in other areas of Cordish's portfolio of real estate and operating businesses.

Cordish also noted the tax and balance sheet benefits of partnering with a REIT. "GLPI paid off 100 percent of the debt on all our casinos, so the three casinos we actively own and manage are debt-free," Cordish told GGB. "In lieu of debt, we have a ground lease—and a ground lease is a business expense, fully deductible. If you have debt service, principal is not a deduction when you pay it; the interest is deductible, but the principal is not. So, it's extremely tax-efficient."

VIII. Key Inflection Point #4: The Las Vegas Strip Play & Oakland A's Stadium (2023–Present)

The Tropicana Las Vegas Transformation

That 35-acre parcel GLPI acquired during COVID-19 for $307.5 million in rent credits? It became the centerpiece of one of the most ambitious development projects in Las Vegas history.

The A's say they will build their $1.5 billion domed stadium in Las Vegas on nine acres of the 35 acres owned by Gaming and Leisure Properties, Inc. (GLPI) at Tropicana Ave. and Las Vegas Blvd. Demolition of the Tropicana facilities will start in the fall, with a stadium groundbreaking in the first half of 2025.

The ballpark will occupy nine acres of the 35-acre Tropicana site. Bally's and GLPI are working on a master plan for a related resort development.

The A's Stadium Development

This 33,000-seat covered stadium occupies a nine-acre plot on Las Vegas Boulevard between Tropicana and Reno Avenues. Scheduled to open in spring 2028, the project marks a renewed collaboration between BIG and the Athletics, following an earlier ballpark design proposed for Oakland, California in 2018. The Oakland A's officially break ground on their Las Vegas ballpark, designed by Bjarke Ingels Group (BIG) and HNTB.

"From what we understand, they want to begin the 2028 season in that park and when you start working backwards from that, they don't have a lot of room for error," said Brandon Moore, chief operating officer, general counsel and secretary for GLPI.

Gaming industry analyst Joe Greff of New York-based J.P. Morgan said the letter of intent says that the A's will pay all the costs related to the design, development and construction of the stadium, and Bally's will pay all costs for the redevelopment of the casino and hotel resort. GLPI has committed $175 million to fund infrastructure that would benefit both the stadium and the resort.

Gaming and Leisure Properties (GLPI), which owns the 35-acre site, told analysts last week at the Global Gaming Expo there were funds left over from its $175 million commitment toward the Tropicana demolition that could be used to develop the site's non-stadium aspects. GLPI committed the funding to Bally's in May 2023 for the demolition.

The Bally's Chicago Partnership

While Las Vegas captures headlines, GLPI's largest current development investment is in Chicago.

The project will bring an iconic, world-class entertainment destination, featuring a 178,000 square-foot casino with over 3,300 slots and 170 table games, a 500-room luxury hotel, vibrant dining and nightlife, extensive event space, and a community-enhancing riverwalk and green space. GLPI's $1.19 billion investment, inclusive of the 2024 $250 million acquisition of the site, demonstrates its commitment to supporting its tenants' growth through innovative projects that are expected to deliver long-term value to GLPI's shareholders.

Reflecting these transactions, GLPI will provide in aggregate up to $2.07 billion of financing to Bally's, thereby further cementing the companies' long-term strategic alliance. GLPI has a strong history of successful development experience and construction oversight of casino resort projects, and Bally's looks forward to benefitting from their experience and expertise as a strategic stakeholder for the Project.

Bally's expects the property to open in the 4th quarter of 2026.

IX. Competitor Landscape: GLPI vs. VICI Properties

The Two Giants

One of several success stories of the "Modern REIT Era" alongside other outperforming entrants, including Single-Family Rentals, Cell Towers, and Data centers, Casino REITs have been the single-best-performing property sector since their emergence in the mid-2010s, honing the competitive advantages of the public REIT model with precision. Within the Hoya Capital Casino REIT Index, we track the two casino REITs: VICI Properties (VICI) - which owns a dominant share of the Las Vegas casino market, and Gaming and Leisure Properties (GLPI) - which owns the largest portfolio of regional casinos. These two casino REITs together account for $46B in market value and own 100 casinos and entertainment facilities across the United States.

VICI Properties is a New York City-based member of the S&P 500 that owns 93 assets totaling 127 million square feet, including 54 gaming properties and 39 other experiential properties across the U.S. and Canada. VICI has over 500 restaurants, bars, clubs and sportsbooks. It's much larger than Gaming and Leisure, with a $30.67 billion market cap.

Strategic Positioning Differences

An important difference between VICI and its casino net lease peer, Gaming and Leisure Properties (GLPI), is that VICI has much greater exposure to Las Vegas and its higher quality assets.

GLPI deliberately avoided the volatility of Strip real estate, instead focusing on regional casinos that serve local populations. For its part, GLPI largely eschews the volatility of Las Vegas Strip real estate, owning only the Tropicana there.

Gaming & Leisure's top tenant generates roughly 65% of rents. All of the rest of its tenants are less than 10%. While neither of these casino REITs stand out for customer diversification, Gaming & Leisure is much more dependent on just one operator.

The balance sheet comparison is also notable. Vici's debt-to-equity ratio, a measure of leverage, is 0.7 times. Gaming & Leisure's figure is more than twice that at almost 1.7 times. Leverage can increase returns, but it also reduces financial flexibility in times of adversity.

The Valuation Gap

From 2019 to 2024, GLPI grew AFFO per share at a 1.69% CAGR (compound annual growth rate). During the same period, Realty Income grew AFFO per share at a 4.66% CAGR. GLPI paid out a moderately larger dividend and had two small special dividends.

GLPI offers a higher yield but slower growth. VICI commands a premium valuation but delivers faster AFFO expansion. The choice between them depends on investor preference for income versus growth.

X. Porter's Five Forces & Hamilton's 7 Powers Analysis

Porter's Five Forces

Threat of New Entrants: LOW

Gaming REITs require regulatory approval across multiple jurisdictions. These regulations, aimed at safeguarding public interests, revenue generation, and operational integrity, mandate that GLPI obtain findings of suitability or approvals from gaming authorities for its landlord role in properties hosting casino operations.

Only two major pure-play casino REITs exist today. The barriers—regulatory complexity, capital requirements, and relationship-building with operators—keep potential entrants at bay.

Bargaining Power of Suppliers (Property Sellers): MODERATE

Casino operators have limited alternatives when seeking sale-leaseback capital. Only GLPI and VICI specialize in gaming properties. Traditional net lease REITs like Realty Income have shown interest but lack deep gaming expertise.

However, operators can choose to retain real estate or pursue alternative financing structures.

Bargaining Power of Buyers (Tenants): LOW-MODERATE

Of course casinos have a history of getting into trouble which is why GLPI makes use of master leases. The master lease structure requires that tenants make good on lease payments on all properties.

High switching costs due to regulatory requirements make tenants sticky. Once a casino is operating in a GLPI-owned building, relocating is enormously expensive and time-consuming.

Threat of Substitutes: LOW

No direct substitute exists for specialized gaming real estate financing. Banks are reluctant to lend heavily to gaming operators, and capital markets are more expensive and less patient than REIT financing.

iGaming and online gambling represent a potential long-term structural shift, but regional casinos have proven resilient despite online competition.

Competitive Rivalry: MODERATE

With only two major competitors, rivalry could be intense. However, GLPI and VICI have carved out distinct niches—VICI in Vegas and high-profile assets, GLPI in regional markets. Recent entrants like Realty Income (which acquired Encore Boston Harbor) suggest the competitive landscape may evolve.

Hamilton's 7 Powers Analysis

Scale Economies: MODERATE

Portfolio size provides negotiating leverage with tenants and reduces per-property overhead. Reflecting our disciplined operating strategy, a hallmark of the Company since our formation eleven years ago, and excluding the original transaction with PENN Entertainment, we have executed over $12 billion of gaming real estate related transactions, adding over $900 million of annual rent or financing revenue to our portfolio, at attractive and accretive average multiples.

However, each property is unique—there are no manufacturing-style efficiencies from owning more casinos.

Network Effects: WEAK

Not a traditional network business. Some benefit accrues from reputation—operators prefer dealing with experienced, regulatory-approved landlords.

Counter-Positioning: STRONG (Key Power)

GLPI's entire business model was counter-positioning against casino operators' traditional approach. Incumbents couldn't easily respond because separating real estate from operations would dilute their control and complicate corporate structures.

Switching Costs: STRONG

Once a casino is leased to GLPI, relocating is prohibitively expensive. Gaming licenses are location-specific, renovations are custom-built, and regulatory approval for any change takes years.

Branding: WEAK

Consumers don't choose casinos based on who owns the real estate. GLPI's brand matters only to operators and investors.

Cornered Resource: MODERATE

Gaming regulatory approvals across multiple states represent a form of cornered resource. New entrants cannot simply buy these approvals—they must earn them through years of regulatory navigation.

Process Power: MODERATE

"GLPI's first-hand experience as an operator in the gaming industry combined with our ability to deliver innovative financing solutions to current and prospective tenants are significant differentiators that drive our access to and ability to complete transactions."

GLPI's Penn National heritage gives it operational understanding that pure financial players lack. This institutional knowledge helps structure deals that work for both parties.

XI. Risk Analysis & Key Metrics

Tenant Concentration Risk

GLPI's largest tenant remains Penn Entertainment. While diversification has improved with Cordish, Bally's, Caesars, and Boyd, concentration risk persists.

Penn Entertainment, which accounted for approximately 59% of GLPI's rental income as of mid-2025, generate revenues primarily from discretionary consumer spending on casino gaming, lodging, and entertainment.

Any significant financial distress at Penn would immediately impact GLPI's cash flows—though the master lease structure provides some protection.

Interest Rate Sensitivity

In a recent note to clients, Truist Securities analyst Barry Jonas cited the familiar headwind of elevated interest rates as one of the primary drags on VICI's and GLPI's price action through the first half of 2024. Due to its capital-intensive nature, real estate is one of the sectors most negatively correlated to interest rates.

REITs generally struggle when interest rates rise, as their dividend yields become less attractive relative to risk-free alternatives. GLPI's heavy reliance on debt financing for acquisitions amplifies this sensitivity.

Development Execution Risk

The Bally's Chicago project represents GLPI's largest single investment. This investment, including the $250 million acquisition of the former Chicago Tribune site in 2024, represents approximately 10% of GLPI's total asset base, making it one of their most significant single-property commitments.

Construction delays, cost overruns, or Bally's financial difficulties could significantly impact returns on this capital commitment.

Key Metrics to Watch

1. Rent Coverage Ratio — The ratio of tenant EBITDAR to rent payments. GLPI targets coverage ratios above 1.8x, providing a cushion against tenant financial stress. Watch for any degradation in coverage, which could signal tenant distress.

2. AFFO Per Share Growth — Adjusted Funds From Operations is the key earnings metric for REITs. GLPI provided AFFO guidance for the full year 2025, estimating between $1.105 billion and $1.121 billion, or between $3.83 and $3.88 per diluted share. Track actual results against guidance and year-over-year growth rates.

XII. Bull Case vs. Bear Case

The Bull Case

Regional Casino Resilience: Regional gaming properties (as opposed to properties on the Vegas strip) have shown to be more resilient during economic downturns. The reason for this is that relatively inexpensive local trips tend to remain in household budgets (while more expensive destination trips like Vegas may get cut).

Pipeline of Growth: Notably, our work in 2024 also resulted a healthy pipeline of growth opportunities for 2025 and beyond based on our ability to serve as a growth financing source for current and potential new tenants.

Accretive Acquisition Capacity: Significant corporate developments include the amendment of GLPI's credit agreement, increasing the revolver capacity to $2.09 billion and extending its maturity to December 2028.

Vegas Strip Optionality: The Tropicana site development with the A's stadium could generate substantial value if executed successfully.

Dividend Sustainability: The company also set guidance for 2025 and declared a first-quarter dividend of $0.76 per share. Current payout ratios remain manageable.

The Bear Case

Tenant Concentration: Nearly 60% of rental income from a single tenant creates meaningful risk.

Higher Leverage: GLPI's debt-to-equity ratio significantly exceeds VICI's, reducing financial flexibility in downturns.

Bally's Credit Risk: GLPI's $2+ billion exposure to Bally's through the Chicago project creates substantial single-counterparty risk. Bally's has struggled operationally.

iGaming Cannibalization: Online gambling could eventually cannibalize regional casino revenues, impacting tenant performance and rent coverage.

Interest Rate Pressure: Higher-for-longer interest rates compress REIT valuations and increase borrowing costs for acquisitions.

XIII. Myth vs. Reality

| Common Narrative | Reality Check |

|---|---|

| "Casino REITs are recession-proof" | Regional casinos proved resilient in 2008 and COVID, but aren't immune to extended downturns. GLPI cut its dividend during COVID. |

| "GLPI just collects rent passively" | Increasingly, GLPI functions as a construction lender and development partner, taking on more project risk. |

| "Gaming REITs benefit from Vegas growth" | GLPI specifically avoided Vegas exposure, focusing on regional markets. Only the Tropicana site represents Strip exposure. |

| "Triple-net means zero risk" | Tenant credit quality is paramount. If tenants can't pay rent, the triple-net structure doesn't help. |

XIV. Conclusion: The House That Won by Not Gambling

Peter Carlino didn't discover a new industry or invent a new technology. He recognized a structural inefficiency hiding in plain sight: casino operators owned billions in real estate that Wall Street valued at a discount because it was bundled with volatile gaming operations.

By separating the landlord function from the operator function, GLPI unlocked value for Penn National shareholders, created a new category of institutional-grade real estate investment, and established barriers to entry that persist eleven years later.

Reflecting our disciplined operating strategy, a hallmark of the Company since our formation eleven years ago, and excluding the original transaction with PENN Entertainment, we have executed over $12 billion of gaming real estate related transactions, adding over $900 million of annual rent or financing revenue to our portfolio, at attractive and accretive average multiples.

The gaming REIT model proved its durability during COVID—collecting 98%+ of rents while every casino in America was shuttered. It demonstrated scalability through the Pinnacle acquisition. And it continues evolving as GLPI transitions from passive landlord to active development partner.

Today's GLPI is not your grandfather's triple-net REIT. The company is funding the construction of Chicago's first major casino, backing Major League Baseball's newest stadium on the Las Vegas Strip, and partnering with tribal gaming operations on reservation developments. Each project takes GLPI further from its origins as a simple real estate holding company.

The question for investors is whether this evolution creates value or introduces risk. Passive rent collection is predictable; construction lending is not. Regional casinos are stable; Las Vegas Strip development is volatile.

What remains constant is the fundamental insight that launched GLPI in 2013: casino operators don't need to own their real estate, and REITs are better suited to own these specialized assets than traditional real estate investors. As long as that structural advantage persists—and as long as gaming regulators maintain their exacting standards—GLPI's competitive position remains secure.

The house won by not gambling. Whether it keeps winning depends on how carefully it places its next bets.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube